?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article investigates the impact of the audit committee attributes in determining the financial performance of Saudi non-financial firms. The research sampled the data of 100 companies spanning from 2010 to 2019 obtained from the firms’ financial statements. The data generated were analysed using different panel data techniques (pooled OLS, fixed and random effects). This study emphasises that audit committee size and meetings negatively influence firms’ performance. However, audit committee independence and financial expertise indicate a strong and positive relationship with financial performance. Therefore, this study provides valuable insights into how audit committee attributes affect profitability. Furthermore, this research may guide companies’ top management on restructuring the audit committee to improve corporate governance practices. Also, the results suggest that Saudi regulatory agencies should ensure that listed firms set up audit committees with more independent directors and financial experts. This requirement may help the firms mitigate information disparity between management and shareholders, thus, reducing agency conflicts and boosting firm performance. Consequently, this paper sheds light on the Saudi corporate environment, so investors may find this research helpful in making their investment decisions.

1. Introduction

Sequel to the collapse of many companies across the globe, the board of directors’ role became the central issue and has been given more attention by regulatory authorities and researchers (Romano, Citation2005). As a result, several countries strengthened the corporate boards’ functions to improve investors’ confidence. For instance, the USA enacted the Sarbanes-Oxley Act. Similarly, Australia enacted the Audit Reform and Corporate Disclosure Act 2004. Furthermore, the 1997 Asian financial crisis led to a series of regulatory reforms highlighting the relevance of the audit committee in ensuring sound corporate governance practices (Min, Citation2018; Min & Chizema, Citation2015). Thus, the audit committee’s primary duty is to oversee accounting, auditing, and financial reporting processes, thereby strengthening firms’ internal control mechanisms (Anderson et al., Citation2004; Buallay & Al-Ajmi, Citation2019).

Given the vital role the audit committee plays in promoting best corporate governance practices, many studies were undertaken to unveil its effect on firm performance. Accordingly, a considerable body of empirical evidence shows that the audit committee composition with a higher proportion of independent directors mitigates information asymmetry and agency costs, which improves firms’ performance (Beasley, Citation1996; Kallamu & Saat, Citation2015). Also, evidence suggests that an audit committee with a smaller meetings frequency and size is more capable of monitoring top management, thereby providing shareholders with timely financial reports (Ben Barka & Legendre, Citation2017; Karamanou & Vafeas, Citation2005). More importantly, the literature emphasises that firms should set up their audit committees with a substantial number of financial experts. In this context, it is reported that when an audit committee is composed of finance and accounting experts, companies’ financial reporting quality enhances (Chaudhry et al., Citation2020; Nelson & Devi, Citation2013). In this way, accounting and finance specialists have incentives to strengthen the audit committee function.

Although this study is not entirely new, most past studies on this subject matter mainly focus on other Asian countries (Al-ahdal & Hashim, Citation2022; Alqatamin, Citation2018; Chaudhry et al., Citation2020; Fariha et al., Citation2021; Kallamu & Saat, Citation2015; Musallam, Citation2020). Accordingly, prior studies in Saudi mainly focus on board structure and thus pay less attention to audit committee attributes linkage with firm performance (see, Al-Matari, Citation2022; Altuwaijri & Kalyanaraman, Citation2016; Boshnak, Citation2021; Gerged & Agwili, Citation2020). This gap motivates the conduct of this research, given the role of audit committee composition in determining sound corporate governance. Therefore, this paper seeks to contribute to the literature by focusing on the effect of different audit committee attributes in influencing corporate performance in the Saudi context. More importantly, the study utilised other panel data techniques to provide more consistent and reliable empirical evidence on the subject matter.

The present research focuses on the Saudi corporate environment of its unique institutional structure. Firstly, Saudi firms’ market capitalisation constitutes about half of the Arab capital market. In addition, the country is a giant crude oil producer with a contribution of about 25% of the world’s oil reserve (Al-Bassam et al., Citation2018). Furthermore, the Saudi corporate ownership structure is widely dispersed among families, thereby paving managerial discretion on firm policies. More specifically, the country’s corporate governance regulation suggests firms should compose their audit committees with finance experts and independent directors to promote disclosure (Alzeban, Citation2020). Given this background, it is desirable to assess how audit committee mechanisms influence firms in Saudi.

Consequently, evidence from the present study shows that audit committee attributes substantially impact the firms’ financial performance. This article continues in the following manner: section two reviews the literature, whereas part three contains the research methodology. Sections four and five present discussions and conclusions, respectively.

2. Literature review

2.1. Theoretical framework

Most corporate governance studies exploited the agency and resource dependency frameworks as the theoretical base to view the nexus between audit committee attributes and firm performance. In particular, the agency theory focused on the board of directors’ monitoring capacity to reduce the possible conflicts of interests between shareholders and managers (Jensen & Meckling, Citation1976). According to this perspective, managers who are the custodians of firm resources are incentivised to pursue their personal goals at the expense of maximising the shareholders’ wealth. In this way, corporate boards are set up to monitor managers’ self-interest behaviour (Fama & Jensen, Citation1983). Within the agency theory framework, several studies pointed out the audit committee’s role in protecting shareholders’ goals. The audit committee is primarily constituted to strengthen firms’ financial reporting system, thereby monitoring the actions of top managers (Abbott et al., Citation2004; Klein, Citation2002). Also, it is established that an audit committee with a substantial number of independent directors and a higher proportion of financial experts enhances financial performance (Beasley, Citation1996; Buallay & Al-Ajmi, Citation2019). In sum, the agency theory served as a framework to unveil the board of directors’ role in minimising agency conflicts between managers and shareholders.

On the other hand, this research also employed resource dependency theory to understand how audit committee influences organisational outcomes. This theory discussed the board of directors’ capacity to draw valuable resources to organisations from the external environment (Pfeffer, Citation1973). In addition, this framework argued that corporate board composition is associated with diverse resources that companies can utilise to raise their performance (Hillman & Dalziel, Citation2003; Zahra & Pearce, Citation1989). In this context, several studies showed that audit committee attributes are pivotal resources that attract several benefits to firms. Accordingly, it is reported that a larger audit committee size with a higher percentage of financial expertise assists firms in attracting finances to improve their performance level (Chaudhry et al., Citation2020; Nelson & Devi, Citation2013). Consequently, the resource dependency theory considers audit committee attributes a pivotal network that firms should utilise to obtain diverse resources.

2.2. Empirical literature

2.2.1. Audit committee size (ACS)

Saudi corporate governance requires firms to have an audit committee with a minimum of three and a maximum of five members. Accordingly, the existing literature suggests that audit committee size indicates corporate governance quality (Buallay & Al-Ajmi, Citation2019). However, empirical findings documented diverse opinions regarding the effect of audit committee size in influencing the performance of firms. In this context, the resource dependency theory argued that as the audit committee size increases, the committee becomes more effective because more diverse knowledge and expertise are brought to the meetings (Buallay & Al-Ajmi, Citation2019; Karamanou & Vafeas, Citation2005). In addition, it is stated that a larger audit committee is more likely to scrutinise firms’ financial reporting process, thus having higher chances of mitigating financial fraud (Al-ahdal & Hashim, Citation2022; Detthamrong et al., Citation2017). In contrast, there is an ongoing argument in the literature that a larger audit committee is counterproductive to firms’ performance. In the same vein, agency theorists suggested that larger groups are associated with high conflicts and lesser cohesion, resulting in weak corporate governance (Dang et al., Citation2022; Haji, Citation2015; Jensen, Citation1993). Also, it is argued that a smaller audit committee size tends to be more effective in monitoring companies’ financial reporting (Fariha et al., Citation2021; Klein, Citation2002). Some empirical studies found a negative link between audit committee size and financial performance (Fariha et al., Citation2021; Musallam, Citation2020). Hence, given these arguments, the following hypothesis is derived:

H1: There is a negative and significant relationship between audit committee size and the financial performance of the companies.

2.2.2. Audit committee meetings (ACM)

Meeting frequency signifies the level of audit committee activities and is assumed to be a significant attribute for effective monitoring (Vafeas, Citation1999). In this regard, studies showed divergent views on how audit committee meeting frequency impacts organisational outcomes. In particular, it has been explained that regular meeting avails the audit committee members to thoroughly examine firms’ financial reports (Fariha et al., Citation2021; E. M. Al-Matari, Citation2019). Moreover, a considerable body of the literature reported that firms with higher audit committee meetings have fewer reports of financial fraud (Abbott et al., Citation2004; Haji, Citation2015). Similarly, Klein (Citation2002) emphasised that frequent meetings help provide timely financial information to investors, thereby reducing agency conflicts between shareholders and management. Accordingly, prior studies indicated a positive relationship between audit committee meetings and firm performance (Alzeban, Citation2020; Musallam, Citation2020). On the contrary, Ben Barka and Legendre (Citation2017) and Hasan et al. (Citation2022) found a negative relationship between audit committee meetings and financial performance. This finding implies that regular meetings may not necessarily improve firms’ performance. Thus, this research states the following hypothesis:

H2: There is a positive and significant association between audit committee meetings and the financial performance of the firms.

2.2.3. Audit committee Independence (ACI)

Studies pointed out the relevance of independent directors in monitoring top-level management. These directors are not under top managers’ control, and they are expected to enrich board decisions. Thus, independent directors have the incentives to scrutinise managers’ proposals and monitor the implementation of such proposals effectively (Beasley, Citation1996; Fama & Jensen, Citation1983). The audit committee’s oversight function includes safeguarding and strengthening companies’ internal control mechanisms. It is reported that the audit committee appears to be more effective when it is set up with a substantial number of outside directors due to the monitoring capacity of these directors (Buallay & Al-Ajmi, Citation2019; Musallam, Citation2020). In the same vein, it is argued that a higher proportion of independent directors in the audit committee is associated with lower information asymmetry and agency costs (Detthamrong et al., Citation2017). Accordingly, Kallamu and Saat (Citation2015) and Dang et al. (Citation2022) argued that audit committee independence mitigates agency conflicts, thereby lowering the chance of poor firms’ performance. Given the preceding discussion, this research stated the following hypothesis:

H3: There is a positive and significant relationship between audit committee independence and the financial performance of the companies.

2.2.4. Audit committee financial expertise (ACFE)

Another audit committee attribute that may influence firms’ performance is the presence of a financial expert in its composition. The Saudi corporate governance code requires that firms operating in the country should have at least one specialist in accounting and finance in their audit committees. The audit committee’s primary duty is to oversee firms’ accounting, auditing, and financial reporting processes (Anderson et al., Citation2004; Musallam, Citation2020). The existing literature suggests that financial expertise comprises acquiring education or experience in accounting and finance-related jobs (Buallay & Al-Ajmi, Citation2019; Davidson et al., Citation2004). Given the financial experts’ sophisticated knowledge and training, they have the incentives to monitor companies’ financial progress. Also, it is reported that when an audit committee is composed of finance and accounting experts, companies’ financial reporting quality enhances (Abernathy et al., Citation2013; Alzeban, Citation2020; Dhaliwal et al., Citation2010). In the same vein, Nelson and Devi (Citation2013) and Lee and Park (Citation2018) argued that audit committee financial expertise enhances earnings quality and lowers agency costs. In this way, some empirical studies found that a higher proportion of financial experts in the audit committee positively impact firms’ financial performance (Chaudhry et al., Citation2020; Kallamu & Saat, Citation2015). Given this review, the following hypothesis is formulated:

H4: There is a positive and significant relationship between audit committee financial expertise and the financial performance of the firms.

3. Methodology

3.1. Data source and sampling

This study used a secondary source of data collection by utilising the sampled firms’ annual reports and accounts covering the period from 2010 to 2019. The research developed some filters to generate the requisite data for analysis. First, the study excluded financial companies due to their unique reporting system and financial regulations (Rajan & Zingales, Citation1995). Accordingly, the research generated the corporate governance-related data from the sampled firms’ annual reports downloaded from the Saudi stock exchange market. Likewise, the firm-level data were obtained from the Thomas Reuters website. In addition, companies with substantial missing data were also ignored. Following the preceding criterion, the study’s final sample comprises a balanced panel data set of 100 Saudi non-financial listed companies.

3.2. Estimation model

Given the data structure, the panel data approach is the most suitable analytical framework that this research should employ to accomplish its objective. The panel data approach minimises estimation bias; it allows for more data points and enhances the efficiency of the econometric estimates (Baltagi, Citation2005; Gujarati, Citation2003). This research used the panel data analysis method, including the Pooled OLS, fixed effects, and random effects. The baseline models for these estimation methods are shown below:

Pooled OLS

Fixed Effects

Random Effects

The subscripts i and t capture the cross-sectional and time-series dimensions, respectively. The variable represents the dependent variable in the model,

is the intercept of the regression function,

is the vector of independent variables in the model,

in the fixed effect framework captures the firm-fixed effect, the

in Equationequation (3)

(3)

(3) is the composite error term, which covers cross-sectional and time-series error components

and the individual-specific error term

). Lastly,

is the regression error term applicable to Pooled OLS and fixed effects techniques.

3.3. Study variables

The research variables are classified into dependent, independent, and control variables. In particular, financial performance represents the dependent variable and is proxied by return on assets (ROA) and return on equity (ROE). ROA was measured as the operating profit ratio over total assets (Darmadi, Citation2013). However, the paper utilised ROE for robustness check, calculated as the net income ratio over common stock (Buertey & Pae, Citation2020; Short & Keasey, Citation1999). These performance measures were chosen because they signify managers’ efficiency in enhancing firms’ value (Kilic & Kuzey, Citation2016; Ujunwa, Citation2012). Moreover, the primary explanatory variables are: Firstly, audit committee size (ACS) is determined as the number of audit committee members (Haji, Citation2015; Klein, Citation2002). Secondly, audit committee meetings (ACM) are measured as the number of annual audit committee meetings (Al-Matari, Citation2019). Thirdly, audit committee independence (ACI) was quantified as the number of independent board members over audit committee size (Detthamrong et al., Citation2017; Kallamu & Saat, Citation2015). Finally, audit committee financial expertise (ACFE) was calculated as the number of audit committee members with accounting and finance qualifications over audit committee size (Buallay & Al-Ajmi, Citation2019; Davidson et al., Citation2004).

Furthermore, this research employed leverage, firm size, board size, board independence, and family ownership as control variables. First, leverage (LEV) was considered and computed as the total debt ratio over total assets. A segment of the literature revealed that profitable firms have less preference for debt financing because of the costs attached to the external borrowings (Sheikh & Wang, Citation2013; Shyam-Sunder & Myers, Citation1999). So, this paper assumed a negative association between leverage and performance. Furthermore, firm size (FS) was determined as the logarithms of the sampled companies’ total assets (Sani, Citation2021; Shan, Citation2019). It is suggested that firm size is strategic in enhancing performance because larger companies may derive economies of scale and lower production costs (Altaf & Shah, Citation2018; Muniandy & Hillier, Citation2015). Thus, this paper expects a positive link between firm size and performance. In addition, board size (BS) was also employed and measured as the total number of board members (Abor, Citation2007; Ezeani et al., Citation2021). The agency theory argues that a smaller board is more efficient due to its robust monitoring ability (Yermack, Citation1996). Therefore, companies with many directors may be associated with high agency costs, thereby eroding their performance (Pillai & Al-Malkawi, Citation2018; Sani, Citation2020; Yermack, Citation1996). Therefore, this research anticipates a negative link between board size and financial performance.

Also, the model specification controls for board independence (BI), determined as the number of independent directors over board size (Frye & Pham, Citation2018). It is reported that board independence may enhance board of directors’ monitoring ability and resource provisions to firms because of outside directors’ expertise and network influence (Fama & Jensen, Citation1983; He & Kyaw, Citation2018). Hence, it is expected that BI impacts financial performance positively. Lastly, family ownership (FO) represents the number of family shares over total common stock (Al-Najjar & Kilincarslan, Citation2016; Ngo et al., Citation2020).

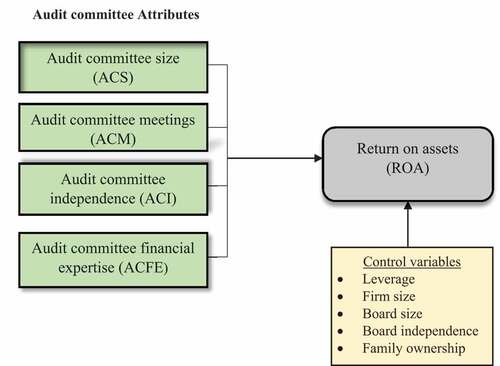

Consequently, given the review of literature and model specification, this paper designed the following conceptual framework, as shown in Figure .

Figure 1. Research framework.

4. Empirical results and discussion

This segment demonstrates the empirical results. The presentation is classified into description analysis, followed by a correlation matrix of the study variables in Table . Finally, Table presents the regression results using the Pooled OLS, fixed and random effects techniques. Some diagnostic tests were performed before running the regression analysis to specify a less biased model. First of all, the multicollinearity test using the variance inflation factor (VIF) was conducted. A VIF value of 10 indicates the existence of multicollinearity (Field, Citation2009). Accordingly, the study variables’ VIF ranged from 1.08 to 1.34, indicating the non-appearance of multicollinearity in the model specification. Also, the Breusch-Pagan/Cook-Weisberg and Wooldridge tests were carried out to determine heteroscedasticity and serial correlation problems. The results appeared significant (Prob > F = 0.000), thus suggesting heteroscedasticity and serial correlation. In this case, a robust regression option was used to obtain a more consistent and efficient result (Hoechle, Citation2007).

Table 1. Descriptive statistics

Table 2. Correlation matrix

Table shows the descriptive statistics of the study variables. The return on assets (ROA) indicates a mean of 0.0547 with a maximum of 0.3550. This evidence suggests that, on average, the sampled firms recorded a profit on assets employed of 5.47% within the period under review. Return on shareholders’ equity (ROE) signifies 7.21% of the firms’ net income. The audit committee size (ACS) shows an average of 4 members approximately. Audit committee meetings (ACM) exhibit a wide deviation among the firms, with an average of 6 meetings approximately. The variable audit committee independence (ACI) suggests that 45.62% of audit committee members are independent directors. Audit committee financial expertise (ACFE) exhibits 54.6%, on average. Leverage (LEV) demonstrates that debt capital constitutes about 22.35% of the firms’ capital employed within the period under review. The firm size measured as the logarithms of total assets indicates an average value of 9.3401 and a maximum of 14.0400. The number of board members (BS) ranged from 3 to 13, and the ratio of independent directors (BI) denotes about 21.21% of the board size. Finally, the family ownership (FO) mean ratio stands at 12.38% of the firms’ common stock.

Table 3. Regression results

Table exhibits how the study variables are correlated with each other. The correlation coefficient across the explanatory variable is not high based on the results. The highest association that the correlation matrix contained is between firm size (FS) and leverage (LEV), with a coefficient of 38.8%, which is far less than the 80% threshold that Baltagi (Citation2005) suggested. Hence, this evidence indicates that the multicollinearity problem does not exist in the research model specification.

Table exhibits the regression results on the relationship between audit committee attributes and financial performance using the Pooled OLS, fixed, and random-effects techniques. The estimates in all the models indicate that audit committee size (ACS) negatively impacts return on assets (ROA), therefore going in line with H1. This result demonstrates that the audit committee’s efficiency tends to be lesser when it is composed of larger members (Al-ahdal & Hashim, Citation2022; Haji, Citation2015; Klein, Citation2002). Also, the result supports the argument that a smaller audit committee size tends to be more effective in monitoring companies’ financial reporting (Fariha et al., Citation2021; Klein, Citation2002). However, the audit committee meetings (ACM) coefficient appears negative and statistically insignificant in predicting financial profitability. This evidence marginally implies that Saudi non-financial listed firms with a higher number of ACM may likely record lower performance measured by ROA.

Moreover, in both the estimation methods, audit committee independence (ACI) is positively related to ROA at the 1% significance level, therefore agreeing with H3. The result supports the conjecture that a higher proportion of independent directors in the audit committee enhances disclosure and minimises agency costs, thus, raising firms’ (Buallay & Al-Ajmi, Citation2019; Detthamrong et al., Citation2017; Musallam, Citation2020). Additionally, audit committee financial expertise (ACFE) shows a strong positive coefficient in all the models this paper specified. This empirical finding reinforces the conjecture that accounting and finance experts have the incentives to monitor firms’ financial reporting process due to their sophisticated expertise and training (Abernathy et al., Citation2013; Alzeban, Citation2020; Chaudhry et al., Citation2020; Kallamu & Saat, Citation2015). In this way, this paper fails to reject H4. Thus, it suggests that Saudi non-financial firms with a considerable number of financial experts in their audit committee may register a high performance.

Furthermore, regarding the control variables, total debt (TD) is negatively associated with ROA. Thus, it supports the ongoing argument that profitable firms pursue lower debt policy presumably due to the cost associated with raising external funding (Sheikh & Wang, Citation2013; Shyam-Sunder & Myers, Citation1999). Profitable firms may likely use internally generated funds to minimise costs and raise their performance because internal funds are relatively cheaper. Firm size (FS) is positively related to ROA at the 1% significance level. This finding aligns with the conclusion that bigger companies are relatively more profitable because they benefit from economies of scale (Altaf & Shah, Citation2018; Muniandy & Hillier, Citation2015). Therefore, this lower operating cost may enhance the profitability level of larger companies, resulting in a positive relation between FS and ROA.

However, board size (BS) registers a negative and significant coefficient. This negative outcome implies that Saudi firms with a higher number of directors may be associated with lower profitability. The finding predicts that a larger board size deteriorates corporate governance and fuels agency costs, negatively affecting financial performance (Pillai & Al-Malkawi, Citation2018; Sani, Citation2020; Yermack, Citation1996). The results suggest a positive and significant association between board independence (BI) and financial performance measured by ROA. The empirical evidence means that as the ratio of independent directors on board rises, Saudi firms’ financial performance may also enhance. This finding aligns with the conjecture that monitoring by independent directors may pressure managers to formulate policies that can improve performance (Fama & Jensen, Citation1983; He & Kyaw, Citation2018). Lastly, family ownership (FO) shows a positive coefficient, indicating that family shareholdings may improve financial performance because of their activism (Al-Najjar & Kilincarslan, Citation2016).

5. Robustness check

Table contains further evidence using a return on equity (ROE) as a different proxy for measuring financial performance to validate the results in Table . Again, these results appear consistent with the earlier outcome in Table . According to the estimates, audit committee size (ACS) and audit committee meetings (ACM) are still negatively related to the ROE. Like the earlier findings, audit committee independence (ACI) and audit committee financial expertise (ACFE) maintain their positive effect on the financial performance measured by ROE. In sum, the study findings appear robust using both ROA and ROE measures of financial performance.

Table 4. Regression results

6. Conclusion

This study investigated the impact of audit committee attributes on financial performance. The research analysed the balanced panel data of 100 Saudi non-financial listed firms spanning from 2010 to 2019 using different panel data techniques. The analysis in this article strongly emphasised that audit committee size and meetings negatively influence the firms’ performance. Thus, supporting the agency theory perspective. Moreover, audit committee independence and financial expertise indicated a strong and positive relationship with financial performance. In particular, this positive effect seems to signify that firms with a higher ratio of independent and financial expert directors in their audit committees may have superior performance.

This study provides valuable insights into how audit committee attributes influence financial performance. Consequently, findings from this research may guide Saudi companies’ top management on restructuring the audit committee to improve corporate governance practices. Likewise, this paper sheds light on the Saudi corporate environment, so investors may find this research helpful in making their investment decisions. Accordingly, this study may equip Saudi regulatory authorities and policymakers to understand better how audit committee attributes affect firms’ performance. Therefore, it may be helpful to these authorities in formulating new policies that may strengthen audit committee functions. Furthermore, the formulation of new policies may help protect shareholders’ investment and attract foreign direct investment into the Saudi corporate environment. Although this paper offers valuable insights on financial performance determinants, further research can be undertaken to validate the predictions of this investigation. Also, since this article considers accounting-based performance measures, future studies should employ other dimensions of measuring firm performance to provide further empirical evidence.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abbott, L. J., Parker, S., & Peters, G. F. (2004). Audit committee characteristics and restatements. Auditing: A Journal of Practice and Theory, 23(1), 69–13. https://doi.org/10.2308/aud.2004.23.1.69

- Abernathy, J. L., Herrmann, D., Kang, T., & Krishnan, G. V. (2013). Audit committee financial expertise and properties of analyst earnings forecasts. Advances in Accounting, Incorporating Advances in International Accounting, 29(1), 1–11. https://doi.org/10.1016/j.adiac.2012.12.001

- Abor, J. (2007). Corporate governance and financing decisions of Ghanaian listed firms. Corporate Governance: The International Journal of Business in Society, 7(1), 83–92. https://doi.org/10.1108/14720700710727131

- Al-ahdal, W. M., & Hashim, H. A. (2022). Impact of audit committee characteristics and external audit quality on firm performance: Evidence from India. Corporate Governance (Bingley), 22(2), 424–445. https://doi.org/10.1108/CG-09-2020-0420

- Al-Bassam, W. M., Ntim, C. G., Opong, K. K., & Downs, Y. (2018). Corporate boards and ownership structure as antecedents of corporate governance disclosure in Saudi Arabian publicly listed corporations. Business and Society, 57(2), 335–377. https://doi.org/10.1177/0007650315610611

- Al-Matari, E. M. (2019). Do characteristics of the board of directors and top executives have an effect on corporate performance among the financial sector? Evidence using stock. Corporate Governance (Bingley), 20(1), 16–43. https://doi.org/10.1108/CG-11-2018-0358

- Al-Matari, Y. A. (2022). Do the characteristics of the board chairman have an effect on corporate performance? Empirical evidence from Saudi Arabia. Heliyon, 8(4), e09286. https://doi.org/10.1016/j.heliyon.2022.e09286

- Al-Najjar, B., & Kilincarslan, E. (2016). The effect of ownership structure on dividend policy: Evidence from Turkey. Corporate Governance (Bingley), 16(1), 135–161. https://doi.org/10.1108/CG-09-2015-0129

- Alqatamin, R. M. (2018). Audit committee effectiveness and company performance: Evidence from Jordan. Accounting and Finance Research, 7(2), 48. https://doi.org/10.5430/afr.v7n2p48

- Altaf, N., & Shah, F. A. (2018). Ownership concentration and firm performance in Indian firms: Does investor protection quality matter? Journal of Indian Business Research, 10(1), 33–52. https://doi.org/10.1108/JIBR-01-2017-0009

- Altuwaijri, B., & Kalyanaraman, L. (2016). Is ‘excess’ board Independence good for firm performance ? An empirical investigation of Non-financial listed firms in Saudi Arabia. International Journal of Finance Research, 7(2), 84–92. http://dx.doi.org/10.2139/ssrn.2747474

- Alzeban, A. (2020). The relationship between the audit committee, internal audit and firm performance. Journal of Applied Accounting Research, 21(3), 437–454. https://doi.org/10.1108/JAAR-03-2019-0054

- Anderson, R. C., Mansi, S. A., & Reeb, D. M. (2004). Board characteristics, accounting report integrity, and the cost of debt. Journal of Accounting and Economics, 37(3), 315–342. https://doi.org/10.1016/j.jacceco.2004.01.004

- Baltagi, B. H. (2005). Econometric analysis of panel data (third edit). John Wiley & Sons, Ltd. West Sussex.

- Beasley, M. S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review, 71(4), 443–465. https://www.jstor.org/stable/248566

- Ben Barka, H., & Legendre, F. (2017). Effect of the board of directors and the audit committee on firm performance: A panel data analysis. Journal of Management and Governance, 21(3), 737–755. https://doi.org/10.1007/s10997-016-9356-2

- Boshnak, H. A. (2021). The impact of board composition and ownership structure on dividend payout policy: Evidence from Saudi Arabia. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-05-2021-0791

- Buallay, A., & Al-Ajmi, J. (2019). The role of audit committee attributes in corporate sustainability reporting: Evidence from banks in the gulf cooperation council. Journal of Applied Accounting Research, 21(2), 249–264. https://doi.org/10.1108/JAAR-06-2018-0085

- Buertey, S., & Pae, H. (2020). Corporate governance and forward-looking information disclosure: Evidence from a developing country. Journal of African Business, 21(4), 1–16. https://doi.org/10.1080/15228916.2020.1752597

- Chaudhry, N. I., Roomi, M. A., & Aftab, I. (2020). Impact of expertise of audit committee chair and nomination committee chair on financial performance of firm. Corporate Governance, 20(4), 621–638. https://doi.org/10.1108/CG-01-2020-0017

- Dang, V. C., Nguyen, Q. K., & McMillan, D. (2022). Audit committee characteristics and tax avoidance : Evidence from an emerging economy. Cogent Economics & Finance, 10(1), 2023263. https://doi.org/10.1080/23322039.2021.2023263

- Darmadi, S. (2013). Board members’ education and firm performance: Evidence from a developing economy. International Journal of Commerce and Management, 23(2), 113–135. https://doi.org/10.1108/10569211311324911

- Davidson, W. N., Xie, B., & Xu, W. (2004). Market reaction to voluntary announcements of audit committee appointments: The effect of financial expertise. Journal of Accounting and Public Policy, 23(4), 279–293. https://doi.org/10.1016/j.jaccpubpol.2004.06.001

- Detthamrong, U., Chancharat, N., & Vithessonthi, C. (2017). Corporate governance, capital structure and firm performance: Evidence from Thailand. Research in International Business and Finance, 42, 689–709. https://doi.org/10.1016/j.ribaf.2017.07.011

- Dhaliwal, D., Naiker, V., & Navissi, F. (2010). The association between accruals quality and the characteristics of accounting experts and mix of expertise on audit committees. Contemporary Accounting Research, 27(3), 787–827. https://doi.org/10.1111/j.1911-3846.2010.01027.x

- Ezeani, E., Salem, R., Kwabi, F., Boutaine, K., Bilal, & Komal, B. (2021). Board monitoring and capital structure dynamics: Evidence from bank-based economies. Review of Quantitative Finance and Accounting, 58, 473–498. https://doi.org/10.1007/s11156-021-01000-4

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Fariha, R., Hossain, M. M., & Ghosh, R. (2021). Board characteristics, audit committee attributes and firm performance: Empirical evidence from emerging economy. Asian Journal of Accounting Research, 7(1), 84–96. https://doi.org/10.1108/AJAR-11-2020-0115

- Field, A. (2009). Discovering Statistics Using SPSS (Third Edit). SAGE Publications LTD.

- Frye, M. B., & Pham, D. T. (2018). CEO gender and corporate board structures. Quarterly Review of Economics and Finance, 69, 110–124. https://doi.org/10.1016/j.qref.2017.12.002

- Gerged, A. M., & Agwili, A. (2020). How corporate governance affect firm value and profitability ? Evidence from Saudi financial and non-financial listed firms. International Journal of Business Governance and Ethics, 14(2), 144–165. https://doi.org/10.1504/IJBGE.2020.106338

- Gujarati, D. N. (2003). Basic Econometrics (Fourth Edi). McGraw-Hill Higher Education.

- Haji, A. A. (2015). The role of audit committee attributes in intellectual capital disclosures: Evidence from Malaysia. Managerial Auditing Journal, 30(9), 756–784. https://doi.org/10.1108/MAJ-07-2015-1221

- Hasan, A., Aly, D., & Hussainey, K. (2022). Corporate governance and financial reporting quality : A comparative study. Corporate Governance, 5(3), 114–121. https://doi.org/10.1108/CG-08-2021-0298

- He, W., & Kyaw, N. A. (2018). Capital structure adjustment behaviors of Chinese listed companies: Evidence from the split share structure reform in China. Global Finance Journal, 36, 14–22. https://doi.org/10.1016/j.gfj.2018.02.006

- Hillman, A. J., & Dalziel, T. (2003). Boards of directors and firm performance: Integrating agency and resource dependence perspectives. The Academy of Management Review, 28(3), 383–396. https://doi.org/10.2307/30040728

- Hoechle, D. (2007). Robust standard errors for panel regressions with cross-sectional dependence. Stata Journal, 7(3), 281–312. https://doi.org/10.1177/1536867X0700700301

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Kallamu, B. S., & Saat, N. A. M. (2015). Audit committee attributes and firm performance: Evidence from Malaysian finance companies. Asian Review of Accounting, 23(3), 206–231. https://doi.org/10.1108/ARA-11-2013-0076

- Karamanou, I., & Vafeas, N. (2005). The association between corporate boards, audit committees, and management earnings forecasts: An empirical analysis. Journal of Accounting Research, 43(3), 453–486. https://doi.org/10.1111/j.1475-679X.2005.00177.x

- Kilic, M., & Kuzey, C. (2016). The Effect of board gender diversity on firm performance: Evidence from Turkey. Gender in Management, 31(7), 434–455. https://doi.org/10.1108/GM-10-2015-0088

- Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375–400. https://doi.org/10.1016/S0165-4101(02)00059-9

- Lee, J., & Park, J. (2018). The impact of audit committee financial expertise on management discussion and analysis (MD&A). European Accounting Review, 11(2), 1–22. https://doi.org/10.1080/09638180.2018.1447387

- Min, B. S. (2018). Determinants of board size in an emerging market. Journal of International Financial Management and Accounting, 29(1), 5–29. https://doi.org/10.1111/jifm.12066

- Min, B. S., & Chizema, A. (2015). Board meeting attendance by outside directors. Journal of Business Ethics, 147(4), 901–917. https://doi.org/10.1007/s10551-015-2990-9

- Muniandy, B., & Hillier, J. (2015). Board Independence, investment opportunity set and performance of South African firms. Pacific-Basin Finance Journal, 35, 108–124. https://doi.org/10.1016/j.pacfin.2014.11.003

- Musallam, S. R. M. (2020). Effects of board characteristics, audit committee and risk management on corporate performance: Evidence from Palestinian listed companies. International Journal of Islamic and Middle Eastern Finance and Management, 13(4), 691–706. https://doi.org/10.1108/IMEFM-12-2017-0347

- Nelson, S. P., & Devi, S. (2013). Audit committee and earnings quality. Corporate Governance, 13(4), 335–351. https://doi.org/10.1108/CG-02-2011-0009

- Ngo, A., Duong, H., Nguyen, T., & Nguyen, L. (2020). The effects of ownership structure on dividend policy: Evidence from seasoned equity offerings (SEOs). Global Finance Journal, 44, 100440. https://doi.org/10.1016/j.gfj.2018.06.002

- Pfeffer, J. (1973). Size, composition, and function of hospital boards of directors : A study of organization- environment linkage. Administrative Science Quarterly, 18(3), 349–364. https://doi.org/10.2307/2391668

- Pillai, R., & Al-Malkawi, H. A. N. (2018). On the relationship between corporate governance and firm performance: Evidence from GCC countries. Research in International Business and Finance, 44, 394–410. https://doi.org/10.1016/j.ribaf.2017.07.110

- Rajan, R. G., & Zingales, L. (1995). What do we know about capital structure? some evidence from international data. The Journal of Finance, 50(5), 1421–1460. https://doi.org/10.1111/j.1540-6261.1995.tb05184.x

- Romano, R. (2005). The Sarbanes-Oxley act and the making of quack corporate governance. The Yale Law Journal, 114(7), 1521–1611.

- Sani, A. (2020). Managerial ownership and financial performance of the Nigerian listed firms : The moderating role of board Independence. International Journal of Academic Research in Accounting, Finance and Management Sciences, 10(3), 64–73. https://doi.org/10.6007/IJARAFMS/v10-i3/7821

- Sani, A. (2021). Board diversity and financial performance of the Nigerian listed firms : A dynamic panel analysis. Journal of Accounting and Business Education, 6(1), 1–13. https://doi.org/10.26675/jabe.v6i1.18817

- Shan, Y. G. (2019). Managerial ownership, board Independence and firm performance. Accounting Research Journal, 32(2), 203–220. https://doi.org/10.1108/ARJ-09-2017-0149

- Sheikh, N. A., & Wang, Z. (2013). The impact of capital structure on performance: An empirical study of non-financial listed firms in Pakistan. International Journal of Commerce and Management, 23(4), 354–368. https://doi.org/10.1108/IJCoMA-11-2011-0034

- Short, H., & Keasey, K. (1999). Managerial ownership and the performance of firms: Evidence from the UK. Journal of Corporate Finance, 5(1), 79–101. https://doi.org/10.1016/S0929-1199(98)00016-9

- Shyam-Sunder, L., & Myers, S. C. (1999). Testing static tradeoff against pecking order models of capital structure. Journal of Financial Economics, 51(2), 219–244. https://doi.org/10.1016/S0304-405X(98)00051-8

- Ujunwa, A. (2012). Board characteristics and the financial performance of Nigerian quoted firms. Corporate Governance (Bingley), 12(5), 656–674. https://doi.org/10.1108/14720701211275587

- Vafeas, N. (1999). Board meeting frequency and firm performance. Journal of Financial Economics, 53(1), 113–142. https://doi.org/10.1016/S0304-405X(99)00018-5

- Yermack, D. (1996). Higher market valuation for firms with a small board of directors. Journal of Financial Economics, 40(2), 185–211. https://doi.org/10.1016/0304-405X(95)00844-5

- Zahra, S. A., & Pearce, J. A. (1989). Boards of directors and corporate financial performance: A review and integrative model. Journal of Management, 15(2), 291–334. https://doi.org/10.1177/014920638901500208