?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Understanding the monetary policy transmission mechanism is pivotal for the design of an effective monetary policy. In this regard, the coexistence of interest rate and cost channel of monetary policy has raised important implications for the conduct of monetary policy. This article estimates a New Keynesian model to quantify the strength of interest rate and cost channel by estimating retail rate stickiness and share of firms considering interest rate in their marginal cost function. It examines the extent of interest rate pass-through and cost channel for exogenous monetary policy shock and endogenous movement in official rate arising due to other financial, nominal, and real shocks in the economy. The trade-off between the degree of pass-through and cost channel of monetary policy has also been examined. The minimum distance estimation of the Dynamic Stochastic General Equilibrium (DSGE) model has confirmed that the degree and nature of interest rate pass-through depend on the nature of shock hitting the economy and the cost channel exists only for monetary and financial shocks. A weak trade-off also exists between the degree of pass-through and cost channel of monetary policy. The study recommends that coordination between central banks and financial and non-financial firms is essential for effective stabilization through monetary policy.

1. Introduction

The strength and the speed of the monetary policy transmission mechanism (MTM) determine the effectiveness of monetary policy that allows the central bank to steer the economy in the desired direction. The mechanism is complicated, and it affects the real economy through a variety of channels, depending on the macroeconomic and financial structure of the country (Gigineishvili, Citation2011). In contemporary discussions, two practices are increasingly adhered to in the operation of monetary policy: the adoption of policy rules and the inflation targeting framework. Both of these practices have led to the intense scrutiny of the traditional interest rate channel of MTM. The strength of the interest rate channel determines the extent of monetary control over the future paths of inflation and output gap which in turn is determined by the degree of pass-through of official rates to retail rates (Hofmann & Mizen, Citation2004).

In a perfectly competitive environment, the official rates completely pass-through to retail rates over a reasonably short horizon (Aziakpono & Wilson, Citation2010). However, due to the presence of liquidity smoothing motive, monopolistic competition in the banking industry, and costly financial intermediation, the retail rates adjust sluggishly in response to the official rate. Incomplete pass-through undermines the supremacy of inflation targeting framework of monetary policy. It is further worsened in an environment where the Taylor principle is not strictly observed in monetary policy rule (Kwapil & Scharler, Citation2006) and the cost channel of MTM is fairly active. It may be added that the cost channel of the monetary policy works on the premise that firms relate their production plans and price-setting behavior to credit conditions as their production costs are directly affected by interest rate (Barth & Ramey, Citation2000; Hulsewig et al., Citation2009; Kaufmann & Scharler, Citation2007).

The coexistence of incomplete pass-through and cost channels presents a trade-off for monetary authority. The scope of macroeconomic stabilization is limited in the presence of incomplete pass-through; nonetheless, its prevalence mitigates the procyclicality of prices to monetary contraction, thus moderating the cost channel of MTM. This trade-off generates complex choices for the monetary authority. For example, in face of exogenous shock, any effort by the monetary authority to increase its effectiveness for demand management by improving the pass-through may exacerbate the adverse implications for the supply side of the economy originating from the cost channel of MTM.

The present article belongs to the strand of literature that includes both interest rate and cost channel in the analysis of MTM. The article employs the New Keynesian DSGE model to achieve two objectives. First, we intend to estimate the retail rate stickiness and how it reacts to different nominal and real shocks in the economy. We are particularly concerned about the length of time it takes for interest rate pass-through to occur, as well as the speed of pass-through to different impulses. Second, we examine the relationship between retail loan stickiness and the evolution of prices in face of different shocks. In this regard, following Barth and Ramey (Citation2000), we assume that the presence of the price puzzle represents the existence of the cost channel of MTM. In this regard, we are particularly involved in investigating the interaction among central banks and financial and non-financial firms and how different impulses are transmitted to the economy given this interaction. Even though the research on the quantification of retail rate sluggishness has grown rather well over time, its implications for the real effects of monetary policy have only recently attracted attention. Our motivation derives from a dearth of research on this topic in general, and specifically in the context of emerging economies, despite its current relevance.

Pakistan, in this regard, is an important case study due to a long history of financial repression, widespread prevalence of financial frictions, and a continuous rise in inflation despite monetary contractions. Both interest rate pass-through and cost channel of monetary policy have been studied independently like Qayyum et al. (Citation2005), Khawaja and Khan (Citation2008), Hanif (Citation2012), Mahmood (Citation2018), and Batool et al. (Citation2021) investigating the incomplete interest rate pass-through using traditional econometric techniques while studies like Javid and Munir (Citation2010) and Chaudhry et al. (Citation2015) provide evidence on cost channel. However, the assessment of MTM given the coexistence of interest rate pass-through and cost channel of monetary policy in a general equilibrium framework is rarely attempted for Pakistan.

The theoretical framework of the research is based on Hulsewig et al. (Citation2009), but we extend the model to incorporate nominal, financial, and real shocks, as well as monetary shocks, to investigate the degree of pass-through and its consequences for the cost channel. It is also worth noting that the general equilibrium framework, particularly DSGE models, allows researchers to incorporate the structural and behavioral characteristics of a specific sector of the economy, as well as its interactions with the rest of the economy. In this regard, we aim to investigate the dynamic interaction between the central bank, financial institutions (banks), and non-financial institutions (firms) to comprehend the transmission mechanism of monetary policy given a number of impulses by estimating a DSGE model using data on Pakistan economy.

This study contributes to the literature in two ways. First, it allows us to dismantle the strength of pass-through and cost channel of monetary policy, especially the response of retail loan to endogenous changes in the official rate and second to understand the response of financial and non-financial firms to financial, nominal, and real shocks. It would be interesting to know how the response of financial firms to an exogenous shock to changes in official rates differs from a situation when these firms are faced with endogenous changes in official rates arising out of other nominal and real shocks in the economy. This will enable us to discern that for which shocks financial firms are more likely to pass-through interest rate changes to retail rates. It will also reveal the firms’ information regarding the difference in the endogenous and exogenous changes in official rates. Second, along with predicting the behavior of financial firms, extending the model for other shocks is expected to reveal the price-setting behavior of non-financial firms in response to endogenous and exogenous changes to official rates. Both of this information are essentially important to understand the MTM.

The rest of the study is organized as follows. Section 2 presents the methodology. In Section 3 results and discussion are presented. Section 4 concludes the study.

2. Literature review

Until recently, the literature on interest rate pass-through and cost channel assumed independent pathways. As far as the study of pass-through is concerned, the existing literature lacks consensus regarding the responses of retail loans to monetary stimulus, hence providing diverse cross-country experiences. Empirical evidence attributes the observed cross-country heterogeneity to several factors including but not limiting to the bank or market dominated nature of financial systems (Ehrmann et al., Citation2001; Kaufmann & Scharler, Citation2007), banking concentration or competition (Güntner, Citation2011), the stage of financial development, degree of financial openness, and macroeconomic environment (Gigineishvili, Citation2011; Sander & Kleimeier, Citation2004). Along with financial and structural factors, policy factors such as monetary policy regime (Egert et al., Citation2007) and policy transparency are also held responsible for the cross-country differences in pass-through (Gambacorta, Citation2008; Liu et al., Citation2008). In a recent meta-analysis of pass-through literature, Gregor et al. (Citation2021) underscored several factors responsible for the strength of pass-through. For instance, they highlighted the importance of a country’s macro-financial situation particularly the depth of stock markets has a substantial impact on interest rate pass-through. They also demonstrated that the pass-through deteriorated during the global financial crisis, owing to increased trade openness and supply chain finance, greater volatility, stock market turnovers, and weakening central bank independence. If inflation targeting frameworks were in place, they helped mitigate the weakening of the pass-through.

Although the assessment of the monetary policy shock as the supply-side shock has been undertaken both implicitly (Gertler & Gilchrist, Citation1994; Kashyap et al., Citation1994) and explicitly (L. J. Christiano et al., Citation1998), it gained prominence after the seminal work of Barth and Ramey (Citation2000) who argued that the amplification of shocks and price puzzle is the result of cost channel of monetary policy. The existence of the cost channel of monetary policy presents mixed results. Ravenna and Walsh (Citation2006), Chowdhury et al. (Citation2006), Tillmann (Citation2008), and L. Christiano et al. (Citation2005) validated the importance of cost channel, whereas Rabanal (Citation2007) and Gabriel and Martins (Citation2010) concluded that cost channel is active neither in the US nor in Europe. In a comparative study of the closed and open economy of Taiwan, Chang et al. (Citation2014) showed that supply-side pass-through of interest rate is substantial in a closed economy however is largely mitigated in an open economy owing to the sluggish exchange rate pass-through. Similarly, Baqaee et al. (Citation2021) showed that monetary easing has a favorable impact on productivity, demonstrating yet another avenue to capture monetary policy’s supply-side effect. In a recent study, Qureshi and Ahmad (Citation2021) used a general equilibrium analysis to show that the cost channel is more visible when inflation is low but weakens when inflation rises.

The empirical exercises encompassing both cost and interest channel started to appear in general equilibrium literature are scant. Rabanal (Citation2003) and L. Christiano et al. (Citation2005) are early contributions in this regard where both showed cost channel ineffective for monetary policy for the UK and the US. Hulsewig et al. (Citation2006) not only examined the coexistence of interest rate and cost channel but also examined the role of interest rate pass-through for the strength of cost channel of monetary policy. They showed that incomplete pass-through significantly mitigates the cost channel of monetary policy.

According to the brief review of literature, examining the cohabitation of traditional interest rates and novel cost channels, as well as their consequences for the conduct of monetary policy, is a rarely attempted research endeavor. The collective assessment of interest rate pass-through and supply-side impact of monetary transmission is expected to provide very useful insights not only for gauging the relative strength of each channel of MTM but also for the effective conduct of monetary policy in countries like Pakistan, where interest rates are regulated, financial frictions are widespread, and price puzzles are evident. This study is an attempt to achieve this objective.

3. Methodology

To examine the strength of interest rate pass-through and its implications for the cost channel of monetary policy, we use the DSGE model that includes the pass-through equation in the base model of Hulsewig et al. (Citation2009) and hosts six shocks. The model economy has four types of agents: households, non-financial firms, financial firms, and monetary authority. The model incorporates a variety of nominal and real rigidities, such as accumulation of habit stock by households, investment adjustment costs, variable capital utilization, and staggered price and wage rigidities in Calvo-style, along with incomplete indexation. The model has state-of-the-art features; hence, we refrain from a detailed account of first principles and present the log-linearized version of the model.

3.1. The model

The expected lifetime utility of representative households is maximized given a Constant Relative Risk Aversion (CRRA) utility function with separable preferences for consumption , working hours

, and money.Footnote1 An intertemporal substitution in consumption and an intratemporal trade-off between consumption and working hours give rise to aggregate consumption that evolves around past

and future consumption

and real interest rate

. Intertemporal elasticity of substitution

and habit persistence

determines the extent to which consumption responds to the interest rate.Footnote2 The Euler equation for consumption is given as follows.

Household consumption behavior is also subject to a preference shock , where

, and

is coefficient of auto-covariance in exogenous AR(1) process defining the shock.

Households supply differentiated labor to intermediate good producers and set wages under staggered contracts with constant (Calvo) probability of renegotiation in each period. A fraction of household that optimize, set wages as a mark-up

over the marginal rate of substitution between leisure and consumption

. Symbolically,

The wages for the remaining households are incompletely indexed with inflation parameterized through . The combination of non-reoptimized wages and partial indexation results in the following wage equation.

Equation (3) shows that real wage is a weighted average of past and expected future wages and past, current, and expected inflation rates along with wage mark-up. The indexation of non-reoptimized wages determines the strength of the relationship between current wages and current and past inflation, whereas

is the deviation of actual wages from wages that would have prevailed given the fully flexible labor market.Footnote3

The evolution of optimal investment trajectory specified in a dynamic Euler equation for investment is derived under the assumption that capital producers produce new capital stock in the competitive market and rent it out to entrepreneurs/intermediate goods producers at a given rental rate of

. Supply of capital rental services

is determined as a result of the maximization problem of a capital producer either by investing in additional capital

or by changing the utilization rate

of already installed capital. Capital goods producers incur quadratic capital adjustment cost

for both of their actions. Investment responds sluggishly to different shocks due to costs for adjusting capital and directly affects the price of capital. Capital price is a unit without capital adjustment costs. Therefore, capital adjustment costs permit the capital price to fluctuate, which contributes to the impulsiveness of the net worth of entrepreneurs.

The investment equation is given as follows.

Similar to consumption, current investment is the weighted average of past

and expected future investment

, and the value of installed capital

. Investment is also subject to shock

which is innovation to efficiency with which consumer goods are converted into capital goods.

where

and

as a coefficient of auto-covariance in exogenous AR(1) process.

The evolution of capital stock is depicted by the standard capital accumulation equation as follows.

where is depreciation cost and Equation (6) determines the aggregate supply of capital in the economy.

The real rate of capital and capital utilization is as follows:

where , it is assumed that the utilization rate is equal to one in a steady state.

Entrepreneurs are monopolistically competitive and produce intermediate goods, which are converted into homogeneous final goods by perfectly competitive final goods producers. Aggregate supply yields from a typical Cobb-Douglas technology augmented with a fixed cost

, variable capital utilization rate and technology

shock which is faced uniformly by all entrepreneurs.

Similar to wages, price setting by monopolistically competitive firms also takes the form of staggered contracts. A fraction of firms find the opportunity to revise prices with constant Calvo probability and sets prices a mark-up

over wages. Those prices which are not reoptimized are indexed

to past inflation partially. Consequently, inflation

dynamics assume the following process.

Equation (9) is a hybrid NK price Philips curve, where forward-looking behavior is depicted by expected future inflation term and backward-looking part succeeds from partial indexation. A price mark-up shock

also determines the evolution of the current inflation process.

The dynamics of the gross loan rate (LR) is given by:

The value of is associated with the LR stickiness. When the fraction of banks, which are not changing their LR in response to policy change,

goes to zero, then

and interest rate pass-through will be complete. This condition is as per the approach applied by Ravenna and Walsh (Citation2006) who considered that banks operate under perfect competition. If

takes a positive fraction, the LRs will be sticky in response to the policy rate, leading to incomplete pass-through in the short run.

Finally, we close the model by indicating the reaction function of the central bank for Pakistan, which is designated by the following log-linearized interest rate rule:

where the extent of interest rate smoothing is captured by and the coefficient of the central bank’s reaction function concerning the expected inflation rate and the output gap are

and

, and

implies monetary policy shock.

The resource constraint decomposes aggregate output in consumption, investment good, government expenditure, and resource lost owing to variable capital utilization. The resource constraint is given in the following manner:

where is steady-state household consumption.

3.2. Empirical methodology

We estimate the log-linearized version of the DSGE model described in the preceding section by applying the minimum distance estimation technique following L. Christiano et al. (Citation2005), Henzel et al. (Citation2009), Hulsewig et al. (Citation2009), and Silva et al. (Citation2016).

The minimum distance approach comprises two steps. First, a Dynamic Stochastic General Equilibrium- Structural Vector Autoregression DSGE-SVAR (Citation2012) model is specified to generate empirical impulse response functions (IRFs) for different shocks based on the theoretical model specified in the above section. Second, parameters of the DSGE model are estimated by the minimization of the distance between the empirical and theoretical impulse response function where empirical IRFs are obtained from DSGE-SVAR and theoretical is obtained from the calibrated model.

The VAR model for Pakistan’s economy is represented by the structural equation given below:

As denotes the vector of endogenous variable, the parameter matrix is denoted by

, the vector of constant terms is defined as

, and

is the error term vector which is assumed to be white noise. In the first step, reduced form, the VAR model is estimated and then VAR with identifying restrictions is applied.

The reduced form VAR model is defined as:

The error term of reduced-form VAR and structural shocks are associated as:

The B matrix relates the VAR residuals () with the structural shocks

. However, B is a non-singular

matrix. Multiply both sides of Equation (14) with the

returns:

As,

Now, adding to both sides of Equation (16) yields

However, is an (

) identity matrix. For shock identification in SVAR, recursive Cholesky ordering has been applied followed by Blanchard and Perotti (Citation2002) where B matrix is an upper triangular matrix with the following representation of

for Pakistan.

where denotes the real output and expressed in percentage terms,

is the inflation rate,

is the central bank’s money market rate, and the LR is denoted by

. Consumption is denoted by

and investment is expressed as

.

Imposed restrictions are based on theoretical relationships given in the theoretical model. To check the validity of identifying restrictions, LR test results are analyzed, which shows that identification restrictions are valid. It tells

In the second step, the minimum distance approach is applied. The model has the following matrix representation:

where defined as the state vector, while the vector of shocks is denoted by

, and

denotes the expectational error vector, it satisfies the condition

. Structural parameters of the model are presented in

, and

(Sims, Citation2001).

The starting point to generate impulse response is defined as:

We estimate the following set of parameters for matching the impulse responses:

The other parameters are calibrated in which some of the parameters are based on empirical evidence from economic data while some others are based on the literature (Del Negro et al. (Citation2005); Smets & Wouters, Citation2003).

Following distance function suggested by L. Christiano et al. (Citation2005) estimator has been minimized:

where empirical impulse responses are denoted by ,

is the impulse response of a theoretical model, and the weighting matrix is described as

. The weighting matrix is drawn from the diagonal of sample variances of

. The purpose of the weighting matrix is to assure that priority will be given to point estimates with the smaller standard deviation (Henzel et al., Citation2009).Footnote4 The standard errors for estimated parameters are computed using the formula suggested by Hall et al. (Citation2012), and the formula for the variance of estimates is taken from Canova (Citation2005).Footnote5

where and

is the covariance matrix of

.

3.3. Data and calibration

The data for DSGE-SVAR covers the time period from 1980 Q-I to 2018 Q-IV for six observables: GDP, inflation, retail and policy interest rate, investment, and consumption. The details about the data are provided in Table .

Table 1. Variables, transformation, and sources

For matching impulse responses, a set of parameters are calibrated and given in 2.

The value of discount factor is calculated to be 0.99 by taking the inverse of the average long-term real interest rate. The discount factor is calculated using annual data on interest rates from 1970 to 2018. The formula used to calculate the discount factor is

and

is the discount rate following Tufail and Ahmed (Citation2017). All economic agents are assumed to have a similar discount factor in DSGE models. Ahmed et al. (Citation2012) also estimated

to be 0.99.

The depreciation rate is set to be 0.025 quarterly, which is in line with the literature to produce an annual depreciation rate of 10 percent. This value is also consistent with the non-financial firms reports of the Karachi stock exchange from 2001 to 2015.

The risk aversion parameter is estimated to be 1.01, the parameter is estimated through the GMM estimation procedure following Ahmed et al. (Citation2012). For the estimation procedure, annual data on consumption and interest rate from 1970 to 2018 has been used. The lag values of both variables have been used as an instrument in the estimation. The estimated value of risk aversion is consistent with the value set by Choudhri and Malik (Citation2012). The value is also consistent with the number of DSGE models for emerging economies.

The share of capital in production takes a value of 0.4, which is reasonably adjacent to the average of capital shares of other developing countries. The value is also close to the value of Tufail and Ahmed (Citation2017) and Ahmed et al. (Citation2012). The parameter of the firm’s monopoly power

is set to be 9 by following Amato and Laubach (Citation2003).

The labor supply elasticity is set to be 1.5 following Gabriel and Reiff (Citation2010) and Ahmed et al. (Citation2012). Similarly, the proportion of sticky prices

=0.08 has been taken from Ahmed et al. (Citation2012) and Tufail and Ahmed (Citation2017). For the simple Taylor rule, we follow Ahmed and Pasha (Citation2015), and Aleem and Lahiani’s (Citation2011) response of interest rate to inflation is set to be 0.16. The interest rate smoothing parameter and response to different output remained at 0.80 and 0.10 in the monetary policy rule.

4. Results

The section presents and discusses in three sections. To start with, the estimated coefficients obtained from the minimum distance approach are reported in Table and discussed. The impulse responses against different shocks are extracted from VAR estimation (estimated response) and the minimum distance approach and matching IRFs are presented afterward. Besides examining the behavior of macroeconomic aggregates, the focus of the discussion is to examine the strength of interest rate pass-through and the existence of the cost channel of monetary policy against different shocks. In the final section, the results of the tradeoff between the strength of pass-through and cost channel are presented by performing counterfactual analyses for different levels of pass-through and varying degrees of cost channel.

Table 2. Calibrated parameters

4.1. Estimated parameters

The results obtained from minimum distance estimation reported in Table show that the estimated value of habit persistence is 0.879. The Euler equation indicates the humped-shaped response of the output gap because monetary shock is driven by a higher habit persistence value. The estimated value is close to the value obtained by Tufail and Ahmed (Citation2019) for Pakistan in the context of the DSGE model estimated through the Bayesian estimation technique. Interestingly, the value obtained by them through GMM estimation using quarterly data also lies in the close vicinity. This implies the parameter of habit persistence is robust across different estimation techniques. This is also calculated by other studies conducted for other countries, for instance,Vereda and Cavalcanti (Citation2010) have also found a value closer to our estimated value. On the other hand, while Carvalho and Valli (Citation2011) found the habit persistence value to be 0.6, Silva et al. (Citation2016) reported a high value of 0.99.

Table 3. Estimated parameters

The significant value of the degree of loan rate stickiness specifies the role of the banking sector in the propagation of monetary shock. The estimated value of

is 0.79 for Pakistan, which indicates that loan rates are fixed for almost three quarters on average. This also depicts the gestation lag involved in materializing the effect of monetary policy for Pakistan. The estimated loan rate stickiness is 0.36 by Hulsewig et al. (Citation2009) and Silva et al. (Citation2016). Another Study by Henzel et al. (Citation2009) reported the estimated loan rate stickiness to be 0.41. Contrary to the studies of L. Christiano et al. (Citation2005) and Ravenna and Walsh (Citation2006), who consider the banking sector with

. The higher value for loan rate stickiness in Pakistan depicts the more concentrated banking industry of Pakistan as compared to developed countries. It also depicts the high level of disparity in the central bank’s goal of economic stabilization and intermediaries’ profit-making objectives in Pakistan.

A high degree of price rigidity has been reported in the results. The parameter of price stickiness is estimated to be 0.73. This shows that firms resist a price change for up to three quarters. This price stickiness is the depiction of coordination failure among the monetary policy agents and price setters. While adoption of price indexation

by the number of firms is estimated to be 0.51, the results are in line with Altig et al., Citation2004). Leith and Malley (Citation2005) estimated the price stickiness to be 0.29. Hulsewig et al. (Citation2009) reported a relatively high value of 0.56 for the share of firms following the indexation rule.

Wage rigidity is quite high like price rigidity. Parameter of wage stickiness is estimated to be 0.79 with the average duration of wage 3 quarters. The value is quite similar as reported by Ahmed et al. (Citation2012). The results are also similar to the Cavalcanti and Vereda (Citation2011), whereas a lower value is reported by Rabanal and Rubio-Ramirez (Citation2007), which has a lower average duration of 1.2 quarters. However, the estimate of the indexation rule

is 34 percent, whereas 36 percent of firms that follow the indexation rule are reported by Ahmed et al. (Citation2012) for annual data. Leith and Malley (Citation2005) applied a complete indexation rule in their study and report the share of indexation rule to be 17 percent, whereas the partial indexation rule is adopted by Smets and Wouters (Citation2003) who reported the estimated degree of wage indexation to be 0.66. A comparatively lowered value of 0.34 is reported by Rabanal and Rubio-Ramirez (Citation2007).

The parameter depicting cost channel of monetary policy is investigated through . The estimated value for

is 0.18. It implies that 18 percent of firms contemplated that short-term financial cost plays an important role in price-setting behavior. An increase in interest rates leads to a rise in the financial cost of firms. Hulsewig et al. (Citation2009) and Silva et al. (Citation2016) reported the estimated value to be 1 for the US and the UK. It denotes that 100 percent of firms consider financial cost role in price-setting.

The parameter for adjustment costs of investment is estimated to be 1.98. The value is quite close to the estimated value of 2.35 of Carvalho and Valli (Citation2011) and Silva et al. (Citation2016) estimate the value as 2.44. In the case of Pakistan, Tufail and Ahmed (Citation2019) reported the value of adjustment cost for investment to be 4. However, Henzel et al. (Citation2009) estimated the adjustment cost of investment to be 3.18.

The lagged policy coefficient in monetary policy rule reveals a degree of interest rate smoothing 0.81. The sluggish nature of the adjustment process by the central bank partly explains the high rigidity of prices. The reaction coefficients on inflation and output gap are 0.21 and 0.17, respectively. There is no general agreement in Pakistan for estimates of reaction coefficients in the monetary policy rule. For instance, Malik & Ahmed, Citation2007) argued that monetary policy in Pakistan is highly accommodative as weights on inflation (0.32) and output (0.19) in monetary policy rule diverge considerably from what has been proposed by Taylor. Nevertheless, Haider and Khan (Citation2008) in the context of DSGE model showed that estimated coefficients (1.17 and 0.72) are closer to what is conjectured by the Taylor rule. The estimated coefficients in the DSGE model by Tufail and Ahmed (Citation2019) are 0.92 and 0.44, respectively.

4.2. Shocks, interest rate pass-through, and cost channel of monetary policy

Three types of shocks are specified in the theoretical model. The matching impulse responses to these shocks are indicated in Figures , coupled with the error bands of 95 percent. Results showed that most of the theoretical impulse responses are closely matched with the empirical impulse responses, and they also lie in the confidence interval .

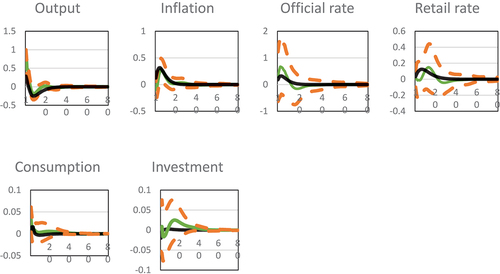

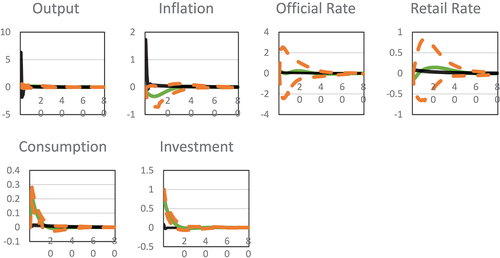

Figure 1. Matched impulse responses of monetary policy shock

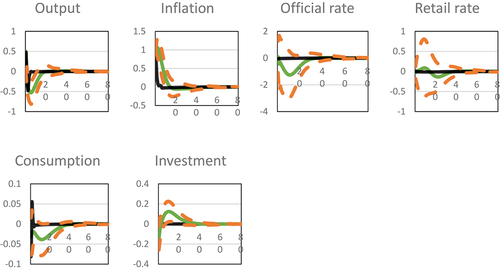

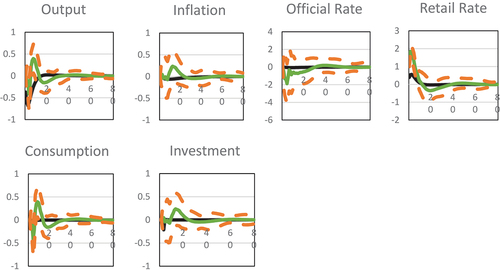

Figure 2. Matched impulse responses of price mark-up shock

4.3. Monetary policy shock

Figure shows the impulse responses of monetary policy shock from VAR and minimum distance approach. Several findings are noticeable. First, the humped-shaped estimated response reasonably replicates the matched output and inflation responses. For other variables, the difference is significant for retail loan rate and negligible for consumption. Moreover, theoretical responses of output, inflation, and interest rates are slightly more immediate in response to monetary shock.

Second, it can be observed that loan rate response is delayed after monetary shock, leading to incomplete interest rate pass-through. The loan rate stickiness highlights the sluggish response of banks in changing the loan rate in response to monetary policy shock. Generally, banks have a long-term customer relationship with firms, and they are providing loans to them at previous rates. However, holding on loan rate at the previous level is temporary. So, the time lag is involved in changing the loan rate, leading toward incomplete interest rate pass-through.

Third, inflation responds immediately with the increase in official rate showing the presence of price puzzle. The existence of price puzzle depicts the cost channel of monetary policy shock. As interest rate enters in the cost-function of firms, it affects the price-setting behavior of firms, leading to price puzzle.

Estimated and simulated responses of all variables are theoretically consistent (L. Christiano et al., Citation2005), whereas estimated model appears to be capable of replicating the data because the theoretical impulse responses functions are well inside empirical confidence intervals. The impulse responses of estimated model are quite similar to the calibrated impulse responses of Tufail and Ahmed (Citation2017; Tufail & Ahmed, Citation2019) for Pakistan. It is also worthwhile to indicate that the dynamics of macroeconomics variables after the matching technique are quite similar to the results of Hulsewig et al. (Citation2009) and Silva et al. (Citation2016).

4.4. Price-markup shock

Figure illustrates the response of macroeconomic variables in face of price markup shock. A positive price mark-up shock is the nominal shock and is contractionary for aggregate macroeconomic variables as depicted in both estimated and simulated responses of output, consumption, and investment. For these variables, simulated responses are not only immediate as compared to estimated responses but also short-lived while estimated responses are delayed and showed persistence .

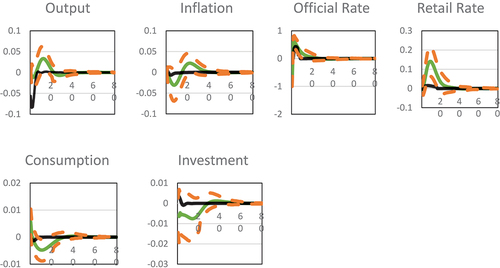

Figure 3. Matched impulse responses of preference shock

Figure 4. Matched impulse responses of investment adjustment shock

Price markup shock also induces endogenous changes in the official rate. Official rate reduces, however, this reduction is not passed-on to retail rate rather retail rate that showed an increase for the first 16 quarters. This shows that price mark-up shock is treated differently by the central bank and banking intermediaries as price mark-up shock calls for economic stabilization by the central bank. However, banks consider this shock as an opportunity to earn higher profits by charging a higher interest rate. This finding is very important from a monetary policy perspective as in the case of exogenous price mark-up shock a contradiction in central bank objective and intermediaries profit motive may limit the efficacy of monetary policy. For price mark-up shock, the existence of a cost channel cannot be isolated as an increase in inflation is exogenous in case of mark-up shock.

4.5. Preference shock

The IRF-matching results for preference shock are reported in Figure . In response to preference shock, both estimated and simulated responses show that individuals are more induced to discount future depicted in a reduced level of current consumption. However, responses from both models are not similar, depicting that theoretical model is not fully representing the data. In response to an economic downturn, official interest rate reduces but retail loan shows an increase showing that pass-through is asymmetrical in face of preference shock. Moreover, inflation also reduces showing in case of preference shock, higher interest costs are not passed on to consumers primarily to encourage consumers to consume more.

4.6. Investment adjustment shock

Figure reports the results of investment adjustment cost in the IRF-matching technique. The estimated responses are quite immediate and substantial to adjustment cost shock as compared to simulated responses. A negative investment shock that materializes through an increase in the adjustment cost of investment decreases the marginal efficiency with which the consumer goods are converted into investment goods. The output and investment decrease in both estimated and simulated responses. This contraction leads to a reduction in the official rate which is followed almost completely by retail rate leading to a complete pass-through. The reduction in retail rate is well depicted in the price-setting behavior of firms showing a price decline. For investment adjustment cost, monetary policy objectives and bank behavior are highly consistent. Response of inflation does not depict the price puzzle indicating that investment adjustment cost is not transferred to prices. In face of investment adjustment cost, the trade-off between interest rate channel and cost channel of monetary policy is not present.

Figure 5. Matched impulse responses of retail rate shock

4.7. Retail rate shock

Figure shows the IRF-matching results for shock to retail rate. The retail rate shock is a financial shock that induces more substantial and immediate responses to macroeconomic variables. The retail rate shock creates more unstable responses as compared to other shocks in the economy. The retail rate shock is contractionary as it prompts the output to drop, driven by decrease in investment and consumption. For retail rate shock, the pass-through behavior cannot be ascertained as the shock has induced exogenous changes in retail rate. The higher interest cost faced by non-financial firms is depicted in higher prices. Born and Pfeifer (Citation2011) reported that the retail rate shock reduces the output, which is driven by collapse in investment which occurs due to sluggish behavior of consumption owing to habit persistence.

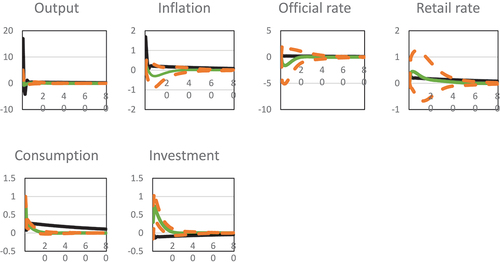

4.8. Productivity shock

Figure reports the matching IRFs of macroeconomic variables in response to productivity shock. The estimated IRFs of macroeconomic variables are matched as the IRFs of simulations. For estimated model, the responses are more substantial than theoretical model. Generally, the responses of key macroeconomic variables are concomitant with existing literature. For output and investment, a humped-shaped response is observed As our model economy is characterized by financial frictions, so productivity shock slowed down output and investment for a few quarters. With the increase in output, monetary policy becomes stringent. It is followed by a higher retail rate leading to interest rate pass-through which is timely but less than proportional. A productivity shock induces firms to reduce the inflation showing the benefits obtained from positive productive shock exceed the marginal cost due to increased interest rate. However, with the persistent increase in retail rate, inflation finally increases.

Figure 6. Matched impulse responses of productivity shock

4.9. Trade-off between pass-through and cost channel

In DSGE framework, the extent to which fluctuations in the official rate are passed to the retail rate depends on the Calvo parameter which shows a fraction of banks in each period that retains their retail rates unchanged. The immediate interest rate pass-through is not complete which is confirmed by our estimated value of

. Note that when

, system enters in regime of complete interest rate pass-through (Ravenna & Walsh, Citation2006) where for complete interest rate pass-through

at each point in time

. A Calvo–style financial system reduces the effect of alterations in the money market rate not just during the period in which monetary policy shock occurs, but also in the subsequent periods. So, in case of varying policy rates, firms got shelter from banks in the bank-based financial system.

Similarly, the strength of cost channel of monetary policy depends on the fraction of firms dependent on credit to finance the production. In our estimation results, this fraction is estimated to be 15 percent. For

, the cost channel does not operate. Here, we have assumed different degrees of interest rate stickiness and different fractions of finance-dependent firms to examine the extent of trade-off between interest rate pass-through and cost channel of monetary policy for monetary and retail rate shock. These shocks are considered for this analysis on the basis that cost channel is active only for these two shocks. The results are shown in Figures .

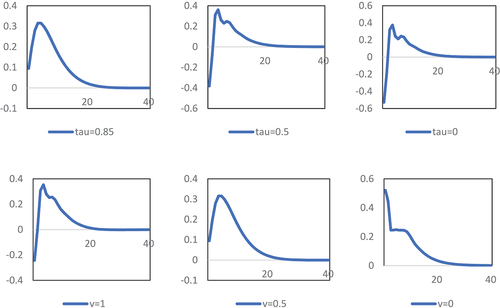

Figure 7. Counter factual analysis: response of inflation to monetary policy shock

Figure 8. Counter factual analysis: response of inflation to retail rate shock

The results indicate that as the degree of retail rate stickiness reduces, the on-impact monetary policy becomes effective for controlling inflation. However, apart from a first few quarters, a sharp increase in inflation is observed peaking high for low retail rate stickiness confirming the existence of trade-off between cost channel and interest rate pass-through but to a smaller extent. This becomes more obvious when the responses of inflation are drawn for varying values of . A continuous decrease in inflation for

depicts that the interest rate does not matter for marginal cost of the firm. For highest degree of loan rate stickiness, the peak inflation response occurs at low level as compared to the cases where interest rate stickiness is low.

For retail rate shock, the decrease in retail rate stickiness not only moderates the on-impact response of inflation but also reduces the peak intensity of responses. This shows that inflation is more stable in case of complete pass-through. Similarly, when a fraction of finance-dependent firms reduces to zero, marginal cost does not depict the cost of finance, hence inflation reduces. The tradeoff between retail rate stickiness and cost channel is only evident for on-impact responses of inflation. For instance, for more rigid retail rates, on-impact reduction in inflation is most substantial. For later quarters, this trade-off is not significant.

5. Discussion

The results from preceding sections confirm that as far as the estimated values of parameters are concerned, several differences and similarities have been observed (See Table ) from the existing DSGE literature for advanced economies and Pakistan. One such striking feature is that financial, wage and prices rigidities are strong in Pakistan as compared to developed world.

Table 4. Discussion of results

There are two opinions regarding the difference of extent in nominal price and wage rigidities in advanced and emerging economies. According to Klenow and Kryvtsov (Citation2008), Dhyne et al. (Citation2006), advanced economies have large services sectors where frequency of price change is very low, hence, developing economies have more flexible prices. Contrarily, Bils and Klenow (Citation2004) pointed out that price rigidity also depends on market structure as models of price adjustment predict a greater frequency of price changes in markets with more competition. In this regard, given that market failure is more prevalent in developing economies and the nonmarket institutions that ameliorate its consequences are not very successful in doing so (Stiglitz, Citation1989), frequency of prices changes in that respect may be higher in developed countries and less in developing countries. The issue of price and wage rigidity is of particular importance to gauge the effectiveness of monetary policy as the strength of both interest rate and cost channel of monetary policy rest on the extent prices and wages are rigid.

Along with nominal rigidities, real wage and price rigidities determined by the extent of indexation are also substantial in Pakistan. It shows the prevalence of suboptimal behavior among the price and wage setters and can also be attributed to information barriers faced by economic agents. Interestingly, this behavior is also observed for advanced economies.

The high level of financial rigidity depicted in retail loan stickiness is also pivotal in monetary transmission mechanism. Resistance of banks to change retail rate in tandem to policy rate highlights the role of banks in transmitting monetary policy actions. However, the findings of second exercise showed that bank behavior is not unanimous to exogenous and endogenous changes to policy rate. For instance, pass-through is complete in case of investment adjustment cost which implies that for the real shock originated from production sector the central bank and banking intermediaries are well aligned as far as the objectives of monetary policy are concerned. However, for nominal shock originating from production sector interest rate pass-through is reversed showing the opposite response in retail rate. For the real shock originating from household sector, the results are similar to price markup shock.

For cost channel of monetary policy, only 18 percent of firms are estimated to consider interest rate in their marginal cost function still the evidence of cost channel is present particularly of monetary policy and retail rate shock. For rest of nominal and real shocks evidence of cost channel of monetary policy is not found. A look at the following table will make the findings of the research clearer.

A clear difference is also found regarding the coefficients of monetary policy rule where for many advanced and emerging economies, the response of policy rate to inflation and output gap is quite strong while for Pakistan it is quite moderate.

6. Conclusion and Recommendations

In this article, we have quantified the strength of interest rate pass-through, the presence of cost channel and trade-off between retail rate stickiness and strength of cost channel in transmission mechanism of monetary policy for Pakistan. We estimated a New Keynesian DSGE model featuring the pass-through of official rate to retail rate and fractions of firms with an interest rate as cost of production. The model also hosts six different shocks including nominal, real and financial shocks. Model is estimated using minimum distance estimation approach that comprises of estimation of SVAR and impulse response matching. Counterfactual analysis is also conducted to examine the trade-off between degree of pass-through and cost channel of monetary policy.

Our main conclusion was that neither banks nor firms behave similarly in face of all kinds of shocks hitting the economy. Banks not only shelter firms by smoothing retail rates in face of monetary policy shock but also seize opportunities to earn higher profit in face of shocks that improve the net worth of the firm. For such shocks, a clear contradiction arises in the economic stabilization goal of monetary policy and profit earning motive of banks. Non-financial firms only transfer financial costs to prices in face of monetary policy and retail rate shock. For other shocks in the economy the impact on inflation dynamics arising through changes in interest rates is quantitatively unimportant. Moreover, it has been confirmed that degree of interest rate pass-through has important implications for stabilization inflation but is less important for cost channel of monetary policy.

It is therefore recommended that designing monetary policy given these implications requires information about the nature of shock, monopoly power of banks, type of coordination between financial and non-financial firms, and coordination between financial institutions and the central bank and the factors that determine the nominal and real rigidities in the economy. In this regard it would also be very interesting to examine the interest rate pass-through and its implications for cost channel for strong endogenous response of official rate in monetary policy feedback rule.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. In log-linearized form of model, these variables will appear in small letters.

2. Habit persistence determines the degree of consumption persistence and preference shock is a shock to discount factor that effects intertemporal substitution decisions.

3. The parameter determines the degree of wage rigidity in labor market. Higher the value of parameter lower is the difference.

4. As weighting matrix is the requirement of estimator. However, According to Giannoni and Woodford (Citation2002a), the convergence of optimization can be hindered by the weighting matrix.

5. For above formula, Dynare code and script min_impunk.m and fun_impunk.m have been used, which can be downloaded from the Fabio Canova website.

References

- Ahmed, S., Ahmed, W., Khan, S., Pasha, F., & Rehman, M. (2012). Pakistan economy DSGE model with informality. State Bank of Pakistan Paper No. 53135. Research Department.

- Ahmed, S., & Pasha, F. (2015). A pragmatic model for monetary policy analysis I: The case of Pakistan. SBP Research Bulletin, 11(1), 1–26. http://www.sbp.org.pk/research/bulletin/2015/Vol-11-1/A%Pragmatic%20mode

- Aleem, A., & Lahiani, A. (2011). Monetary policy rules for a developing country: Evidence from Pakistan. Journal of Asian Economics, 22(6), 483–494. https://doi.org/10.1016/j.asieco.2011.07.001

- Altig, D., Christiano, L., Eichenbaum, M., & Jesper, L. (2004). Firm-specific capital, nominal rigidities and the business cycle. Mimeo, Northwestern University.

- Amato, J. D., & Laubach, T. (2003). Rule-of-thumb behavior and monetary policy. European Economic Review, 47(5), 791–831. https://doi.org/10.1016/S0014-2921(02)00270-2

- Aziakpono, M. J., & Wilson, M. K. (2010, March 21 & 23). Interest rate pass-through and monetary policy regimes in South Africa. Paper for Presentation at the CSAE Conference UK: Oxford University.

- Baqaee, D., Farhi, E., & Sangani, K. (2021). The supply-side effects of monetary policy (No. w28345). National Bureau of Economic Research.

- Barth, M. J., & Ramey, V. A. (2000). The cost channel of monetary transmission. NBER Working Paper 7675. National Bureau of Economic Research.

- Batool, S., Asghar, N., & Rasul, F. (2021). Analyzing the maturity wise interest rate pass through in Pakistan. Review of Applied Management and Social Sciences, 4(1), 93–104. https://doi.org/10.47067/ramss.v4i1.103

- Bils M and Klenow P. (2004). Some Evidence on the Importance of Sticky Prices. Journal of Political Economy, 112(5), 947–985. 10.1086/422559

- Blanchard, O., & Perotti, R. (2002). An empirical characterization of the dynamic effects of changes in government spending and taxes on output. The Quarterly Journal of Economics, 117(4), 1329–1368. https://doi.org/10.1162/003355302320935043

- Born, B., & Pfeifer. (2011). Policy risk and the business cycle. Bonn Econ Discussion Pa- pers bgse 062011.

- Canova, F., & Sala, L. (2005). Learning about the parameters and the dynamics of DSGE models. Model Evaluation Conference.

- Carvalho, F. A., & Valli, M. (2011). Fiscal policy in Brazil through the lens of an estimated DSGE model. Working Paper Series (240), Central Bank of Brazil, Research Department.

- Cavalcanti, M. A. F. H., & Vereda, L. (2011). Dynamic properties of a DSGE model with alternative parameterizations for Brazil. IPEA Discussion Text (1588), Institute of Applied Economic Research, Brasilia.

- Chang, J. C. D., Huang, C. J., & Chien, I. C. (2014). Cost channel of monetary policy: Financial frictions and external shocks. Emerging Markets Finance and Trade, 50(2), 138–152. https://doi.org/10.2753/REE1540-496X500208

- Chaudhry, I. S., Ismail, R., Farooq, F., & Murtaza, G. (2015). Monetary policy and its inflationary pressure in Pakistan. Pakistan Economic and Social Review, 53(2), 251–268. http://pesr.econpu.edu.pk/website/journal/article/607690951631b/page

- Choudhri, E. U., & Malik, H. (2012). Monetary policy in Pakistan: A dynamic stochastic general equilibrium analysis. International Growth Centre.

- Chowdhury, I., Hoffmann, M., & Schabert, A. (2006). Inflation dynamics and the cost channel of monetary transmission. European Economic Review, 50(4), 995–1016. https://doi.org/10.1016/j.euroecorev.2005.01.007

- Christiano, L. J., Eichenbaum, M., & Evans, C. L. (1998). Monetary policy shocks: What have we learned and to what end? NBER working papers 6400. National Bureau of Economic Research, Inc.

- Christiano, L., Eichenbaum, M., & Evans, C. (2005). Nominal rigidities and the dynamic effects of a shock to monetary policy. Journal of Political Economy, 113(1), 1–45. https://doi.org/10.1086/426038

- Del Negro, M., Schorfheide, F., Smets, F., & Wouters, R. (2005). On the fit and forecasting performance of new keynesian models. CEPR Discussion Paper 4848. Centre for Economic Policy Research.

- Dhyne E, Álvarez L J, Bihan H Le, Veronese G, Dias D, Hoffmann J, Jonker N, Lünnemann P, Rumler F and Vilmunen J. (2006). Price Changes in the Euro Area and the United States: Some Facts from Individual Consumer Price Data. Journal of Economic Perspectives, 20(2), 171–192. 10.1257/jep.20.2.171

- Egert, B., Crespo-Cuaresma, J., & Reininger, T. (2007). Interest rate pass-through in central and Eastern Europe: Reborn from ashes merely to pass away? Journal of Policy Modeling,Vol, 29(2), 209–225. https://doi.org/10.1016/j.jpolmod.2007.01.005

- Ehrmann, M., Leonardo, G., & Martinez, J. (2001, December). Financial systems and the role of monetary policy transmission in the Euro area. Working Paper Series No. 105. European Central Bank.

- Gabriel, V. J., & Martins, L. F. (2010). The cost channel reconsidered: A comment using an identification-robust approach. Journal of Money, Credit and Banking, 42(8), 1703–1712. https://doi.org/10.1111/j.1538-4616.2010.00361.x

- Gábriel P and Reiff Á. (2010). Price setting in Hungary-a store-level analysis. Manage. Decis. Econ., 31(2–3), 161–176. 10.1002/mde.1479

- Gambacorta, L. (2008). How do banks set interest rates? European Economic Review, 52(5), 792–819. https://doi.org/10.1016/j.euroecorev.2007.06.022

- Gertler, M., & Gilchrist, S. (1994). Monetary policy, business cycles and the behavior of small manufacturing firms. Quarterly Journal of Economics, 109(2), 309–340. https://doi.org/10.2307/2118465

- Giannoni, M. P., & Woodford, M. (2002a). Optimal interest-rate rules: I. General theory. NBER Working Paper no. 9419. Cambridge, Mass: National Bureau of Economic Research.

- Gigineishvili, N. (2011). Determinants of interest rate pass-through: Do macroeconomic conditions and financial market structure matter? Monetary Economics eJournal, 11, 176. http://imf.org/en/Publications/WP/Issues/2016/12/31/Determinants-of-interest-rate-pass-through-Do-macroecnomic-conditions-and-financial-market-25096

- Gregor, J., Melecký, A., & Melecký, M. (2021). Interest rate pass‐through: A meta‐analysis of the literature. Journal of Economic Surveys, 35(1), 141–191. https://doi.org/10.1111/joes.12393

- Güntner, J. H. F. (2011). Competition among banks and the pass-through of monetary policy. Economic Modelling, 28(4), 1891–1901. https://doi.org/10.1016/j.econmod.2011.03.015

- Haider, A., & Khan, S. U. (2008). A small open economy DSGE model for Pakistan. The Pakistan Development Review.

- Hall, A. R., Inoue, A., Nason, J. M., & Rossi, B. (2012). Information criteria for impulse response function matching estimation of DSGE models. Journal of Econometrics, 170(2), 499–518. https://doi.org/10.1016/j.jeconom.2012.05.019

- Hanif, M. N. (2012). Pass-through of SBP policy rate to market interest rates: An empirical investigation. JISR Managment and social sciences and Economics.

- Hanif, N., Iqbal, J., & Malik, J. (2013). Quarterisation of national income accounts of Pakistan. SBP Working Paper Series.

- Henzel, S., Hulsewig, O., Mayer, E., & Wollmershaeuser, T. (2009). The price puzzle revisited: Can the cost channel explain a rise in inflation after a monetary policy shock? Journal of Macroeconomics, 31(2), 268–289. https://doi.org/10.1016/j.jmacro.2008.10.001

- Hofmann, B., & Mizen, P. (2004). Interest rate pass-through and monetary transmission: Evidence from individual financial institutions’ retail rates. Economica, 71(281), 99–123. https://doi.org/10.1111/j.0013-0427.2004.00359.x

- Hulsewig, O., Mayer, E., & Wollmershauser, T. 2006. Bank behavior and the cost channel of monetary transmission. Working Paper 1813. CESifo.

- Hulsewig, O., Mayer, E., & Wollmershauser, T. (2009). Bank behavior, incomplete interest rate pass-through, and the cost channel of monetary policy transmission. Economic Modelling, 26(6), 1310–1327. https://doi.org/10.1016/j.econmod.2009.06.007

- Javid, M., & Munir, K. (2010). The price puzzle and monetary policy transmission mechanism in Pakistan: Structural vector autoregressive approach. The Pakistan Development Review, 49(4II), 449–460. https://doi.org/10.30541/v49i4IIpp.449-460

- Kashyap, A. K., Lamont, O., & Stein, J. C. (1994). Credit conditions and the cyclical behavior of inventories. Quarterly Journal of Economics, 109(3), 565–592. https://doi.org/10.2307/2118414

- Kaufmann, S., & Scharler, J. (2007). Financial systems and the cost channel transmission of monetary policy shocks. Economic Modelling, 26(1), 40–46. https://doi.org/10.1016/j.econmod.2008.05.002

- Khawaja, M. I., & Khan, S. (2008). Pass-through of change in policy interest rate to market rates. The Pakistan Development Review, 47(4II), 661–674. https://doi.org/10.30541/v47i4IIpp.661-674

- Klenow, P. J., & Kryvtsov, O. (2008). State-Dependent or Time-Dependent Pricing: Does It Matter for Recent U.S. Inflation? The Quarterly Journal of Economics, 123(3), 863–904. https://doi.org/10.1162/qjec.2008.123.3.863

- Kwapil, C., & Scharler, S. (2006). Limited pass-through from policy to retail interest rates: Empirical eviidence and macroeconomic implications. Monetary policy and the economy Q4, 26–36.

- Leith, C., & Malley, J. (2005). Estimated general equilibrium models for the evaluation of monetary policy in the US and Europe. European Economic Review, 49(8), 2137–2159. https://doi.org/10.1016/j.euroecorev.2004.09.010

- Liu, M. H., Margaritis, D., & Tourani-Rad, A. (2008). Monetary policy transparency and pass-throughpass- through of retail interest rates. Journal of Banking and Finance, 32(4), 501–511. https://doi.org/10.1016/j.jbankfin.2007.06.012

- Mahmood, F. (2018). Interest rate pass-through in Pakistan: Evidence from the asymmetric co-integration approach. NUST Journal of Social Sciences and Humanities, 4(2), 168–183. http://njssh.nust.edu.pk/index.php/njssh/article/view/32

- Malik, W. S., & Ahmed, A. M. (2007). The Taylor rule and the macroeconomic performance in Pakistan. Pakistan Institute of Development Economics Working Papers, No. 34.

- Pfeifer, J. (2018). A guide to specifying observation equations for the estimation of DSGE models. Research Series, 1–150. http://randomwalk.top/wp-content/uploads/2020/04/Pfeifer-2013-Observatio-Equations.pdf

- Qayyum, A., Khan, S., Khawaja, I., & Khalid, A. M. (2005). Interest rate pass-through in Pakistan: Evidence from transfer function approach. The Pakistan Development Review, 44(4II), 975–1001. https://doi.org/10.30541/v44i4IIpp.975-1001

- Qureshi, I. A., & Ahmad, G. (2021). The cost-channel of monetary transmission under positive trend inflation. Economics Letters, 2011, 109802. https://doi.org/10.1016/j.econlet.2021.109802

- Rabanal, P. (2003). The cost channel of monetary policy: Further evidence for the United States and the Euro area. Working Paper 149. International Monetary Fund.

- Rabanal, P. (2007). Does inflation increase after a monetary policy tightening? Journal of Economic Dynamics and Control, 31(3), 906–937. https://doi.org/10.1016/j.jedc.2006.01.008

- Rabanal, P., & Rubio-Ramirez, J. F. (2007). Comparing new Keynesian models in the Euro area: A bayesian approach. Spanish Economic Review, 10(1), 23–40. https://doi.org/10.1007/s10108-007-9031-5

- Ravenna, F., & Walsh, C. E. (2006). Optimal monetary policy with the cost channel. Journal of Monetary Economics, 53(2), 199–216. https://doi.org/10.1016/j.jmoneco.2005.01.004

- Sander, H., & Kleimeier, S. (2004). Convergence in Euro-zone retail banking? What interest rate pass-through tells us about monetary policy transmission, competition and integration. Journal of International Money and Finance, 23(3), 461–492. https://doi.org/10.1016/j.jimonfin.2004.02.001

- Silva, I. E. M., Nelson, L. P., & Bezerra, J. F. (2016). EvidenceEvidences of incomplete interest rate pass-through, directed credit and cost channel of monetary policy in Brazil. Proceedings of the 43rd Brazilian Economics Meeting.

- Sims, C. A. (2001). Solving Linear Rational Expectations Models. Computational Economics, 20(1/2), 1–20. https://doi.org/10.1023/A:1020517101123

- Smets, F., & Wouters, R. (2003). An estimated stochastic dynamic general equilibrium model of the Euro area. Journal of the European Economic Association, 1(5), 1123–1175. https://doi.org/10.1162/154247603770383415

- Stiglitz, J. E. (1989). Market, Market Failures and Development. The American Economic Review, 79(2), 197–203.

- Tillmann, P. (2008). Do interest rates drive inflation dynamics? An analysis of the cost channel of monetary transmission. Journal of Economic Dynamics & Control, 32(9), 2723–2744. https://doi.org/10.1016/j.jedc.2007.10.005

- Tufail, S., & Ahmed, M. A. (2017). Financial frictions and optimal policy response. PIDE Conference Proceedings.

- Tufail, S., & Ahmed, M. A. (2019). Finance-growth nexus and relative efficacy of alternative policy regimes: An investigation for Pakistan. Forman Journal of Economic Studies, 15(January–December), 23–67. https://doi.org/10.32368/FJES.20191502

- Vereda, L. & Cavalcanti, M. A. (2010).Dynamic Stochastic General Equilibrium Model (DSGE) for Brazilian Economy: Version 1). Text for Discussion

- Welz, P. (2006). Assessing Predetermined Expectations in the Standard Sticky-Price Model: A Bayesian Approach.ECB Working Paper No. 621.https://doi.org/10.2139/ssrn.870547

Appendix

Robustness of Estimates

When calibrating a subset of model parameters, an important matter is whether model parameter estimates are robust to changes in the calibrated parameters. Usually, the calibrated parameters and

has uncertainty regarding their values in the literature. For example,

calibrated, and the estimated value is always close to 0.99. However, Leith and Malley (Citation2005) estimate the degree of risk aversion relative to 2 for the Euro area. Yet, the degree of monopoly power for firm

is set by Leith and Malley (Citation2005) and Welz (Citation2006). Whereas some of the authors set high markup for monopoly power, for instance, Amato and Laubach (Citation2003) calibrate the value of

to be 7.9 and 15 percent markup, and Del Negro et al. (Citation2005) sets a relatively higher value of 23 percent markup and

. The calibrated values of elasticity of marginal disutility and labor share in production are 1.5 and 0.68 by Leith and Malley (Citation2005). However, Del Negro et al. (Citation2005) estimate these values as 2.3 for the elasticity of marginal disutility and 0.85 for a share of labor in production.

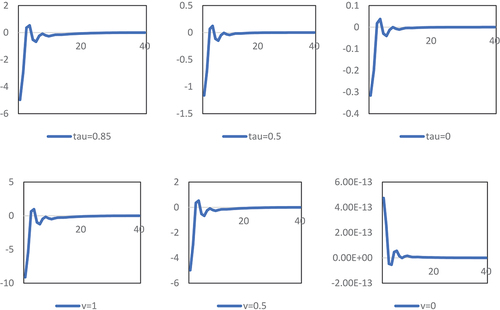

The most important parameter of interest is the degree of retail rate stickiness . The value of

is robust by changing the calibrated parameters. Despite changing calibrated parameter values, the estimated value of

is lying in the close vicinity of our estimated value of 0.79 (as reported in Figures A1 to 11A).

Figure A1. Robustness of the estimated parameters against variations in

Figure A2. Robustness of the estimated parameters against variations in

Figure A3. Robustness of the estimated parameters against variations in

Figure A4. Robustness of the estimated parameters against variations in

Identification of the Parameters

Identification is critical for providing reliable estimates and statistical inferences for every analytical methodology. For example, if the objective function has a unique minimum, the parameters can be identified and defined ample curvature related to all dimensions. We have used the Canova, and Sala (Citation2005) proposed diagnostics tools for parameter identification in moments estimates for the distance minimization function between empirical and theoretical models. To identify the process, the shape of the objective function is plotted in the optimum neighborhood (see, ). The graph’s horizontal axis shows the difference of the objective function value defined as a function of estimated parameters specified on the top of the graph, conditional with other calibrated parameters and unique baseline value of the objective function (

). The graph shows that the curvature of the objective function can identify the sufficient minimum for structural parameters. So, we can conclude that monetary policy shocks can provide useful information regarding structural parameters’ responses.

Figure A5. Shape of the objective function