?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Using panel data from 2004 to 2012, we employ a two-step system GMM estimation technique, with robust standard errors, collapsed instruments and illus-trate marginal effects of central bank independence on financial development in Africa. We also examine the moderating roles of human capital, proxied by literacy rates on the CBI-financial development nexus. We find that, in countries with higher literacy rates/human capital, the positive impact of dejure CBI on financial development is enhanced. Higher literacy rates however, worsen the negative impact of de facto CBO on financial devel-opment. Independent central banks can be made more effective in achieving financial development through governments improving literacy rates. The study is the first to empirically examine the impact of central bank independence on financial development using both dejure and de facto CBI measures and literacy rates in explaining this relationship

1. Introduction

Issues pertaining to central bank independence are not a new phenomenon in academic literature, with respect to empirical studies that have well established a coherent argument include but not limited (De Haan & Kooi, Citation2000; Tayssir & Feryel, Citation2017). Late in the 1970s, economic institutions such as the central bank in Africa begun gaining recognition as having a key attribute towards the growth of their economies through economic theories such as the New Classical Revolution theory (Piazzesi & Schneider, Citation2009).

Prior to the global financial crisis, an agreement was reached on the model of a perfect central bank system, i.e., being independent of government with the aim of managing macroeconomic fluctuations (Masciandaro et al., Citation2008). This agreement has been backed by empirical evidence that depicts that central bank independence is important in managing macroeconomic fluctuations without any negative impact on growth (Kang & Pflueger Citation2015a; Cukierman, Citation2008).

The independent nature of central banks is crucial in the development of the financial sector (Tayssir & Feryel, Citation2017). However, according to Debelle and Fischer (Citation1994), the nature of central banks’ independence is seen in two aspects. These are “goal independence” and “instrument independence.” The “goal independence” deals with the implementation of monetary policies that are aimed at the growing of an economy without the direct influence of the fiscal authority and such policies include reduction in inflation, stabilization of currency (Richard & Gertler, Citation1997) as Governments control on central banks reduces the efficiency of monetary policy measures (Bernanke, Citation2004).

A major contribution of central banks towards the development of their financial sector has to do with the regulatory and supervisory role they play (Gnan et al., (Citation2007)) as this helps to have a conducive financial system. A wide range of literature exists on financial sector development globally; especially in developing economies in Africa (Baltagi et al., Citation2009; M. Chinn & Ito, Citation2011).

The financial system in Africa is considered to be bank-based with relatively low capital market activities, low access to finance and as such the impact of central banks as a regulatory institution on the financial sector development in Africa could be challenged (Table ). The financial sector is poorly developed as a result of institutional factors (see, Tayssir & Feryel, Citation2017) and are characterized by high transaction and information costs (Ayadi et al., Citation2015).

Table 1. Financial Development in Africa, Developing and Developed Countries

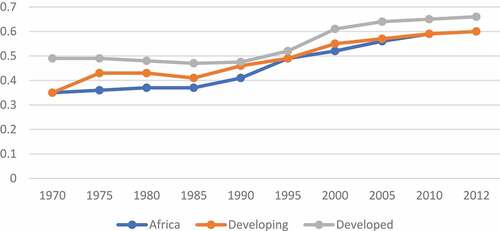

There exist empirical evidence that suggests that monetary institutions such as the central bank positively affect the financial development of a country by influencing the level of inflation as well as the inflation target to be achieved that will be conducive for development in the financial sector (Piazzesi & Schneider, Citation2009; Raza et al., Citation2014; Boyd, Levine & Smith, 2001). In the quest of improving the independence of central banks globally, many developing countries especially those in Africa have drafted laws that grants “more freedom” to the central banks in implementing their policies that helps in developing the financial sector (Doumpos et al., Citation2016; Masciandaro et al., Citation2008) even though cost of credits is high in these financial markets (Bascom, 2016). This notwithstanding, Agoba et al. (Citation2019) in their study, posit that having an independent central bank does not guarantee an improvement in the banking sector thus financial sector development. But central banks globally, strive in developing the financial sector when there is a strict legal regime supporting their policy implementations. This is on the backdrop of similarities in legal independence of central banks in Africa, other developing and developed countries (Figure ).

Figure 1. Trend in Central Bank Independence: 1970-2012

The role of human capital in financial development has not been studied much in academic literature (Bernanke, 2006; Welch & Braunstein, Citation2002), even though its impacts on financial development could be enormous. While high literacy rates or human capital leads to high productivity, high incomes and high savings, it also enhances digital and financial literacy which are essential for taking advantage of the stable macro-and regulatory environment created by the independent central bank. Thus, high literacy rates should enhance the impact of CBI on financial development. Given economic and regulatory stability, when individuals cultivate the habit of savings, it makes more resources available to financial institutions for loan activities as these are done through their innovative products channeled out (Deutsche Bundesbank Report, 2006). It is further argued that high literacy rates enhance the adoption of digital financial products and services which arise out of innovation.

Ideally, central banks particularly in Africa and other developing countries have interest in financial literacy rates in their jurisdictions. According to Gnan Citation2007 some of the reasons why central banks have interest in finance education include its contribution to enhancing effective monetary policy, smooth functioning of the financial markets, supporting of economic policies among others. This is because, literacy makes consumers to understand the working; as such literacy rates are complementary to the efforts of central banks to promote financial development in enhancing the effectiveness of their policies. A cursory look at Table shows that other developing countries have much higher literacy levels than Africa. This could have implications for the effectiveness of CBI on financial development.

Table 2. Adult literacy age 15 years and above

There are quite a number of studies on financial development (see, Laeven & Levine, Citation2009; Alagidede et al., Citation2018: Sare, Aboagye, Mensah & Bokpin, 2018; King & Levine, Citation1993) in addition to the impact of central bank independence on the development of the financial sector (see, Ayadi et al., Citation2015; Baltagi et al., Citation2009; Battiston et al., Citation2016). In a study by Agoba et al. (2020) examining the impact of central bank independence (CBI) on financial sector development, they found that while CBI had a significant impact on financial sector development in other developing countries, it had no significant impact in African countries. In examining what might have accounted for this, we consider the argument for reform complementarities, which posit that the success of reforms could be determined by conditions that accompany these reforms (Agoba et al., Citation2019). One key issue in this regard will be the level of literacy rates or human capital.

The motivation underlining this study is to add up to the existing literature on the conditions for effective central bank independence in developing countries; where literacy rate plays a moderating role in the impact of central bank independence on financial sector development particularly in Africa and other developing countries where financial development is low, central bank independence reforms have been numerous and where access to education is improving. This was done by examining whether central bank independence enhances financial development the more given higher levels of literacy rates or human capital. The study is the first to empirically examine the impact of central bank independence on financial development using both dejure and de facto CBI measures and literacy rates in enhancing this relationship

The rest of the paper is organised as follows: We review literature in section 2 and outline the methodology for the study in section 3. Section 4 presents an analysis and discussion of results obtained. In section 5, we conclude the study.

2. Literature review

The institutional framework of CBI has gained traction and the relationship between the policymaker–who designs the overall economic policy–and the central bank–who is in charge of monetary policy–has become critical in preventing inflation bias (Masciandaro et al., Citation2008). Taylor (Citation2013) considered changes in monetary policy to be a major reason for improved economic performance (measured by output and inflation variability) in the United States during part of the Great Moderation between 1984 and 2003.

According to Blancheton (Citation2016), the economic paradigm shifted towards the end of the 1970s following Friedman’s work on currency and Kydland & Prescott’s work on economic policy rules. Liberal economists‘ support for advanced international financial integration and sustainable deflationary policies was to fuel long-term growth. To expand growth in economic activity, price stability was needed to generate the best environment for long-term expansion of economic activity. To keep inflation under control, having an independent central bank was an important institutional guarantee.

CBI has significant economic benefits by lowering inflationary expectations and making the central bank responsible for its decisions (Eijffinger & van der Cruijsen, Citation2007; Papadamou et al., Citation2017; Stiglitz, Citation1998). Papadamou et al. (Citation2014) argue that a higher level of legitimacy in monetary policy contributes to lower interest rates, higher effective exchange rates and a positive impact on economic activity. Nevertheless, Agoba et al. (Citation2017) find no effect on inflation in Africa and other developing countries from central bank independence.

Independent regulators practice integrity and transparency in monitoring the banks ‘ financial condition, according to Barth et al. (Citation2003). In addition, bank regulatory and supervisory independence is important in maintaining financial stability for reasons similar to why CBI is critical for monetary stability (Quintyn & Taylor, Citation2002). Quintyn and Taylor (Citation2002) suggest that CBI is, among other things, a tool for reducing the economic costs associated with time-inconsistency issues. Similarly, a higher level of central bank independence from external pressures allows less politically controlled central banks to act to prevent financial distress (Cihák, Citation2010). This is because a more reliant central bank may be affected by political interests linked to poor and less compliant financial institutions, resulting in a weaker exercise of central bank control in exercising its powers to regulate these finite institutions. This may have consequences for financial stability and financial system trust. This is further emphasized by Hutchison and McDill (1999) who argue that a dependent central bank with close association with government may have more propensity to provide monetary finance to distressed financial institutions, thus providing an additional channel for the problem of moral hazard.

The role of the central bank in maintaining price stability cannot be over-emphasized in modern literature. To financial market participants, especially bond holders, price stability can have two positive impacts. First, lower inflation means lower short-term interest rates to raise demand for credit. The lower short-term policy rates often tend to decline intermediate and longer-term rates. Because bond prices and yields move in opposite directions, lower yields mean rising prices—and a higher principal value for fixed-income investors; thus, boosting the growth of the bond market (Kang and Pflueger Citation2015). The second impact has to do with real bond returns. For price stability, real bond yields are high compared to periods of high inflation where actual or inflation-adjusted rates are much smaller than nominal yields. This can go a long way in affecting the bond market’s growth. A clear example is Africa, where, among other things, domestic bond markets are underdeveloped with high inflation rates. Price stability ensuring that viable business ventures proposed to financial institutions are properly evaluated (Huang et al., Citation2015). CBI could have a direct impact on bank functioning in situations where the central bank is active in prudential supervision. Doumpos et al. (Citation2016) examined the effect of central bank independence on bank soundness and found that higher central bank independence enhances bank soundness, especially in the case of smaller banks, which is enhanced during the crisis.

3. CBI, literacy rate and financial development

Though there have been a number of literature examining the political economy of reforms (Drazen, 2000; Rogoff, Citation1985), a large part of these studies has paid attention to explaining why socially beneficial reforms do not happen and why if they do happen, they are often delayed (Fernández & Rodrik, 1991; Alesina & Drazen, 1991). Many empirical papers have shown that the success or otherwise of policies or shocks is dependent on the institutional environment (Bekaert, Harvey, & Lundblad, 2005; Mehlum, Moene, & Torvik, 2006). Extant literature has argued that the adoption of Bretton Woods institutions’ reforms in Africa such as the Structural Adjustment Program among others were done in the presence of populist policies as politics as usual (Roberts 1995; Gibson, 1997; Levitsky, 2003).

Critics assert that the benefits of policy reforms such as CBI have not been demonstrated in developing countries, mainly because countries have lagged behind in terms of reform complementarities (Rodrik & Subramanian, 2009). Most developing countries have imported policy reforms from developed countries, without considering the political, social and economic environments within which these reforms were made.

The study argues that literacy levels are social and economic conditions which can determine the success of independent central bank reforms in promoting the development of the financial sector.

The study makes the following arguments flowing from the existing literature. Firstly, a highly proportional educated populace creates the needed environment useful for taking advantage of the stable economic environment created by the independent central bank to participate in the financial markets. Given price stability for instance, a country with a largely educated population can have highly skilled and employable populace, who can earn high incomes and save with financial institutions (Cinnirella & Streb, Citation2017).

Secondly, these educated workforce stand in a stronger position, to access credit facilities at attractive rates as they can pay off these loans form their higher incomes. This results in more credit to the private sector (Mori et al., Citation2017). Thirdly, given independent supervision of financial markets, an educated populace knowing the impact of this on financial markets stability, will be able to take decisions in investing in financial instruments without fear of losing their investments. This should promote higher levels of financial development in such countries than in countries with a less educated populace, who are not able to process the impact of stable economic and regulatory environment, on their financial decisions (Yoshino & Morgan, Citation2016).

Finally, given higher central bank governor turnover rates, we argue that higher literacy rates would worsen the impact of low independence on financial development as the informed populace would be discouraged from participating in the financial markets. This is because of their knowledge of the implications of low independence on the macroeconomic environment and on effective supervision of the financial institutions they have invested or would want to invest in. With the knowledge of the negative impact of inflation on deposits and interests earned, as well as on interest on loans, a literate population would be more discouraged from participating in the financial markets when the independence of the central bank is threatened (Sehrawat & Giri, Citation2016).

4. Methodology

4.1. Data and sample

Due to date availability limitations, the study spans the years 1980–2014, on 138 developing countries, 48 of which are African countries. Our measures of central bank independence include the Garriga (Citation2016)’s CBI index computed from the central bank charter of various central banks, and the annualised central bank governor turnover rate which measures the rate at which central bank governors leave office within a period of time. This was obtained from Garriga (Citation2016). Literacy rates data is from the World Bank. Other control variables come from the models of Tayssir and Feryel (Citation2017) and M. D. Chinn and Ito (Citation2006). These include an indicator of trade openness, log of GDP per capita, the real GDP annual growth rate, public debt, and inflation targeting dummy and the exchange rate regime dummies. These were sourced from the World Development Indicators database.

4.2. Model and estimation technique

4.2.1. Model

We follow the models of Tayssir and Feryel (Citation2017), Bodea et al. (Citation2017), Lucotte (2009), Acemoglu et al. (Citation2008) and Romer (Citation1993) and summarise our model as follows:

To capture possible unobserved heterogeneity, and to analyse the impact of literacy rate on the CBI-financial development nexus, we specify the following interaction model:

where:

i denotes the country and t denotes the time,

is the error term

is the financial development indicator

is central bank independence measured by the CWN index

is the measure of literacy rate

and

is a set of control variables namely:

is the real GDP annual growth rate

is political institutional quality measured by the rescaled civil liberties index

is log of real GDP per capita,

is debt-to-GDP ratio,

lending-deposit spread measured as the difference between lending rate and deposit rate,

is the ratio of central bank assets to GDP

is trade openness measured as the sum of exports and imports as a percentage of GDP and

is financial openness measured as the Chinn-Ito Index.

4.2.2. Definition of variables

4.3. Dependent variable

The dependent variable is financial development (, measured as private credit to GDP ratio ((

which measures the extent of financial intermediation in a country and a gauge of the extent to which the banking sector is developed. Private credit is the value of all credit issued by financial intermediaries to the private sector as a share of GDP. It however does not include credit given to public corporations and other agencies of government which may not be allocated based on expected return. Having higher levels of private credit indicates “higher levels of financial services and therefore greater financial intermediary development” (Laeven and Levine (Citation2009).

We also use stock market capitalisation ( which is the ratio of the value of all stock on the domestic markets to GDP and is an indicator of the size of the economy’s stock market. The stock market provides alternative sources of finance and thus acts as a substitute of or complement to bank credit (Yao et al. 2014; Buttner and Hayo 2011).

4.4. Explanatory variables

Central bank independence is the annual central bank independence measure of country in period

. It represents first, the degree of CBI measured by the de jure indicator. This CBI index is given by Garriga (Citation2016), who computes an updated Cukierman, Webb and Neyapti (CWN) index for a large set of countries using the International Monetary Fund’s Central Bank Law Database. The index varies between 0 and 1, with larger values indicating independence. A central bank is legally more independent when the governor’s term in office is longer; the appointment and dismissal procedures are more insulated from the government; the mandate is more focused on price stability; the formulation of monetary policy lies squarely with the central bank; and the provisions on direct central bank lending are restrictive. The second measure is the central bank governor turnover rate which measures the frequency with which governors of central banks leave office within a period. It is also sourced from Garriga (Citation2016). With this measure, the higher the frequency, the less independent the central bank is.

The possibility of the CBI index being an endogenous variable is addressed by the choice of estimation technique. Also, financial development may have an impact on the level of independence granted to central banks. This raises potential endogeneity effects for which reason we adopt a System Generalised Methods of Moments (SGMM) estimation technique.

We include our variable of interest which is literacy rate. We utilise general measures of literacy which signify the proportion of the population who have passed through primary education system and have acquired basic literacy and numeracy skills. High literacy levels have been found by various studies to be significant determinants of financial literacy levels. Also, financial literacy will require basic reading and numeracy skills which should enable people make informed and effective decisions about and with their financial resources. Our measure of literacy rate is first the adult literacy rate which measures literacy among persons aged 15 years and older who can read and write with understanding, a short simple statement about their everyday life. The second is adult literacy rate which measures literacy among persons aged 15 − 24 years. These are sourced from the World Bank.

We measure political/legal institutional quality (), using the civil liberties score variable obtained from Freedom House database. The score for the variable ranges from 7 to 1, with 7 representing the least rating and 1 the highest. Following Bodea et al. (Citation2017), we rescale the original score to range from 0 to 6, so that lower scores now correspond to lower civil liberties rating and higher scores correspond to higher civil liberties rating. In order to do this, we use the formular −1*(CLS-7), where CLS is the civil liberties score as given by Freedom House. We expect the coefficient of political/legal institutional quality to be positive.

The log of GDP per capita () captures the level of economic development. We expect that there will be more developed financial systems in more developed economies. This is as a result of the availability of higher incomes for investments, technological advancements and highly advanced developed systems that address issues of information asymmetry. The expected sign is therefore positive.

Another control variable is the real annual GDP growth rate (). Greenwood and Smith (1997) examined the impact of economic growth on financial market development. There are varied perspectives on the theoretical link between financial development and economic growth. While Schumpeter (1911) argues that the services provided by financial intermediaries are essential drivers for innovation and growth, Robinson (1952) argues that finance does not exert a causal impact on economic growth. He explains that financial development is a consequent of economic growth, because of higher demand for financial services. We also include real annual GDP growth rate () in the regression to proxy for economic activity as a result of the fact that demand for and supply of credit is sensitive to fluctuations in the economy.

We measure inflation targeting regime () as a dummy variable; with a value of 1 for inflation targeting countries and periods and 0 otherwise. Empirical work posits that most IT regimes have been successful at achieving price stability, which promotes financial sector development, minimize credit market frictions and ultimately, make financial institutions efficient in the allocation of resources for economic growth (Boyd & Nicolo, 2005; Stone, 2003; Agbeja, 2008). We therefore expect a positive sign.

Another dummy is the exchange rate variable (), which is captured as 1 for fixed exchange rate regimes and 0 otherwise. This is based on the de facto exchange rate regime classification by Reinhart & Rogoff (2004, 2009). This data is sourced from the International Monetary Fund. This dichotomous variable equals 1 when there is no separate legal tender, when there is a pre-announced peg or currency board arrangement, when there is a pre-announced horizontal band that is narrower than or equal to ±2%, or when there is a de facto peg, and 0 otherwise. It is argued that fixed exchange rate regimes minimise foreign exchange rate risks, which culminate in macro-economic stability, favourable to the growth of the banking sector and capital markets (Calvo & Reinhart, 2002 and Tayssir & Feryel, Citation2017).

We include a variable for public debt ), measured as the ratio of public debt to GDP. This is calculated as the sum of the accumulated debt-to-GDP ratio for the previous year, discounting it by the interest rate and the ratio of budget deficit to GDP for the current year. Though high public debt it is argued, leads to a crowding out effect, this negative impact is empirically ambiguous (Ismihan & Ozkan, 2012; Kutivadze, 2011).

Trade openness (), is determined as the ratio of the sum of exports and imports of goods and services to GDP. This variable is included to assess the degree of integration of a country in global trade. Higher levels of Trade Openness provide huge markets for domestic producers, which enables them, on one hand, to operate at minimum required scale and on the other hand, to reap benefits from increasing returns to scale. This increase in economic activity, leads to higher demand for financial services.

We also include the Central Bank assets variable (), which is measured as the ratio of central bank total assets held to GDP of a country. Central bank assets represent claims on domestic real nonfinancial sector by the central bank. Therefore, the more assets a central bank holds, the more finance it can provide to support the financial system when it needs funds.

The lending to deposit spread ) variable measures the efficiency of the financial system. It is calculated as lending rate minus deposit rate. Lending rate is the rate charged by banks on loans to the private sector and deposit interest rate is the rate offered by commercial banks on three-month deposits. More efficient financial systems are able to provide credit at lower rates which increases access to credit and expansion of the financial system (Odhiambo, 2005).

Our model includes time period and country dummies that capture year and country specific effects correlated with the variables of analysis in particular political stability that may affect all economies in a particular region or economic group.

4.4.1. Estimation Technique

Following earlier studies in literature, past values of financial development impact its current values. This means that, there is a need to include the lag of financial development as an explanatory variable. Not doing this will lead to low precision of point estimates as a result of the variance being higher when the lag is omitted—due to a specification error (Mizon 1995). To avoid Nickell bias, this study uses the two-step System Generalised Methods of Moments (SGMM) estimator developed by Arellano and Bond (1991), Arellano and Bover (1995) and Blundell and Bond (1998), with Windmeijer (2005) corrected standard errors since this is asymptotically more efficient than the one step-estimator. This estimator was designed for situations with 1) “small T, large N” panels, meaning few time periods and many individuals; 2) a linear functional relationship; 3) one left-hand-side variable that is dynamic, depending on its own past realizations; 4) independent variables that are not strictly exogenous, meaning they are correlated with past and possibly current realizations of the error; 5) fixed individual effects; and 6) heteroskedasticity and autocorrelation within individuals but not across them. The advantage of using the GMM estimator is that it allows possible correlation between regressors and the error components (inefficiency and noise), as well as heteroskedasticity and autocorrelation of unknown forms. In addition, estimating the model in first differences allows for consistent estimates of the frontier in the presence of heterogeneity in the intercept. This helps address issues of joint endogeneity of all explanatory variables in a dynamic formulation, and mitigates potential biases induced by fixed effects. The GMM estimator is consistent, meaning that under appropriate conditions, it converges in probability to β as sample size goes to infinity (Hansen 1982). But like two Stage Least Squares, it is, in general, biased, because in finite samples the instruments are almost always at least slightly correlated with the endogenous components of the instrumented regressors. Correlation coefficients between finite samples of uncorrelated variables are usually not exactly 0. Blundell and Bond (1998)have shown that the system GMM estimator is more powerful when only weak correlation exists between the current and lagged values of model variables. The system GMM also has been shown to be more powerful than the standard first-differenced GMM estimator when estimating a production function for a moderately short panel of data. The weakness of this technique, however, is the possibility of over-fitting of endogenous variables, as a result of instrument proliferation (Roodman 2006). When this happens, there is the likelihood of failing to expunge their endogenous components and biasing coefficient estimates.

The system GMM estimators described in the next section can generate moment conditions prolifically, with the instrument count quadratic in the time dimension of the panel, T. This can cause several problems in finite samples. First, because the number of elements in the estimated variance matrix of the moments is quadratic in the instrument count, it is quartic in T. A finite sample may lack adequate information to estimate such a large matrix well. It is not uncommon for the matrix to become singular, forcing the use of a generalized inverse. This does not compromise consistency (again, any choice of A will give a consistent estimator) but does dramatize the distance of Fixed Effects GMM from the asymptotic ideal. And it can weaken the Hansen test to the point where it generates implausibly good p-values of 1.000 (Bowsher 2002). Indeed, Sargan (1958) determined without the aid of modern computers that the error in his test is “proportional to the number of instrumental variables, so that, if the asymptotic approximations are to be used, this number must be small. We address the issue of instrument proliferation, by collapsing the instrument matrix as suggested by Rodman (2009) and Bontempi and Mammi (2015). This gives us higher point estimates and lower number of instruments. In addition, it leads to a more reliable Hansen test, consistently characterized by a lower p-value. Though the sign and significance of some of the control variables change (compared to earlier estimations where collapse of instruments matrix was not applied), the sign and significance of the main variables of interest (CBI, LitRate; and their interactions) do not. According to Bontempi and Mammi (2015), this shift in the sign of some of the control variables, is not directly driven by the reduction in the number of instruments rather, it is due to the restrictions imposed on the instrument matrix. The autocorrelation test and the robust estimates of the coefficient standard errors assumes no correlation across individuals in the idiosyncratic disturbances.

We report two standard specification tests: The Hansen test of over-identifying restrictions, which tests the overall validity of the instruments and failure to reject the null hypothesis gives support for the model, including our choice of endogenous variables. Second is the Arellano–Bond test for AR (2) in first differences, which also tests whether the residuals from the regression in differences is second order serially correlated. Failure to reject the null hypothesis supports the model specification. The study also reports the number of instruments as suggested by Bazzi and Clemens (2013). Multicollinearity is a problem because it undermines the statistical significance of an independent variable. Other things being equal, the larger the standard error of a regression coefficient, the less likely it is that this coefficient will be statistically significant. We test for multicollinearity using the Variance Inflation Factor (VIF); which is a measure of collinearity among predictor variables within a multiple regression. It is calculated by taking an independent variable and regressing it against every other predictor in the model. Including highly correlated variables in your model can lead to overfitting. If we are overfit, then the model doesn’t generalize well when we try to use it on new data. Only variables with a VIF less than 5 are included in the model. The results of our test indicate that there is low correlation among our regressors.

5. Analysis and discussion of findings

5.1. Main results

We present separate results for Equationequations (1)(1)

(1) and (Equation2

(2)

(2) ) for each group of countries (Africa and other developing countries). In estimating the regressions separately for Africa and other developing countries, there is no selection bias as a check of the variables indicate that, there exist significant variations in the variables except for institutional quality measure in which the variations are not wide. This is a result of the fact it is a score from 0–6 and most African countries have scores around the average. The results of the test of autocorrelation of errors (significant AR (1) and insignificant AR (2)) mean we accept the null hypothesis indicating that there is no correlation between the errors in the second order.

5.1.1. CBI, literacy rate and financial development

In Table , we see the results of regressions for the African sample and other developing countries sample; seeking to examine the impact of dejure CBI and literacy rate measured as the percentage of adults ages 15 and above on financial development. In Table , we measure central bank independence as central bank governor turnover rates and literacy rates as percentage of adults between 15 and 24 years. The tables also present results on the impact of literacy rate on effectiveness of CBI on financial development in Africa and other developing countries.

Table 3. Effect of CBI and Literacy Rate on Financial Development

In examining the impact of the CBI legal index on the banking sector and stock markets in Africa, we see in models (1) and (2), that though the coefficient is positive, it is not significant. This means that, in Africa, having an independent central bank () does not have any significant impact on banking sector development, measured as the ratio of private credit to GDP (

), neither does it have any impact of stock market development measured as the ratio of stock market capitalisation to GDP (

). This is seen in models 1 and 2, and 3 and 4 respectively. However, in other developing countries central bank independence (

) significantly improves banking sector and capital market development. This is indicated by the significantly positive coefficient of the

variable. The insignificant relationship between

and financial development indicators in Africa could be explained by the lack of a significant impact of legal CBI on inflation in Africa as detailed in Agoba et al. (Citation2017). This is because of the broad disregard for CBI legislations. Given an insignificant impact of CBI on inflation the probability of having a significant impact on financial sector development, is low. This is because, price stability is an important channel through which CBI impacts financial development. In other developing countries, having relatively higher legal CBI values, could explain the significant impact of CBI on financial sector development. However, in Table , when we measure CBI with the de facto variable, central bank governor turnover rate (

), we see a significantly negative impact on private credit to GDP in Africa(models 1 and 2) and on both private credit to GDP and stock market capitalisation in other developing countries (models 5–8). Thus, higher rates of central bank turnover imply low independence of central banks which has implications for inflation and fiscal deficits as political authorities influence central banks in accessing funds from the central bank to finance their projects. The increase in money supply generates inflation which is not conducive for lower interest rates and lending to the private sector.

We also see that higher literacy levels improve banking sector and stock market development in Africa (model 1 and 4) and in other developing countries (model 5, 6, 7, and 8) respectively. This is true in the cases where financial literacy is measured by the proportion of the population aged 15 years and above in Table and proportion of the population aged 15–24 years in Table . This is explained by the significant and positive coefficient of the literacy rate measured as the percentage of adults aged 15 and above who can read and write. This means that, given a higher proportion of the adult population who are educated, financial literacy rates are likely to be high and therefore they can be aware of the existence of various financial products and services and make useful investment decisions. Secondly, a well-educated population can acquire employable skills which enables them to earn incomes part of which can be saved. They can also leverage on these incomes to access loans from the financial markets. When we examine the impact of literacy rate (measured as aged 15 years and above) on the effectiveness of in improving financial sector development, we consider the impact of the interactive term

. We realise it, this is significantly positive in Africa and other developing countries as indicated in models 2, 4, 6, and 8. The understanding we get from this result is that, given an educated adult population, the conditions created by independent central bank can be better taken advantage of, in terms of savings and access to loans from the financial markets, This is because, firstly, a well-educated population can serve as a pressure group on government to stick to the provisions of the central bank charter, that make the central bank independent. Such a knowledgeable populace can punish government for disrespecting central bank independence provisions as doing so hurts their welfare. This can be done either through demonstrations, elections or freedom of speech enabled through the media. Secondly, a well-educated adult population, realising there is price stability, can make savings on spending from their incomes, and place with financial institutions.

They can also better patronise loans at affordable interest rates, given their income levels and knowledge of the alternative financial products and services available. So, a country with a higher proportion of educated adults, will better translate the favourable macro-economic conditions created by an independent central bank as a result of higher proportions of financially literate and skilled workforce whose incomes could be invested in financial instruments and also serve as collateral for credit in various forms.

When we also consider the impact of financial literacy (measured as aged 15–24 years), on the impact of central bank governor turnover rate (CBGTOit) on financial development, we find that the negative impact of higher central bank governor turnover rate, (which signifies low independence of the central bank) on financial development, is worsened in the presence of higher levels of literacy for both Africa (models 10 and 12) and other developing countries (models 16 and 18) in Table . This is because, the increasing knowledge of the impact of low central bank independence on economic outcomes, makes the literate populace more reluctant in investing in the financial markets. Secondly, the literate populace being skilled and knowledgeable, can direct their incomes and /investments in the financial sector, into other productive areas of the economy such as the real estates. Knowledge of such alternative investment options makes their reactions to threat to central bank independence very pronounced as they quickly and accurately process this information and feed them into their investment decisions. This goes to further confirm the argument that, there are conditions that enhance the effectiveness of central bank reforms in terms of their impact of economic outcomes such as financial sector development.

Table 4. Effect of CBI and Financial Literacy on Financial Development

The results for a global sample (Appendix III) of all developing countries confirms the findings in Tables and IV. Here estimations were done using a Two stage Least Square technique with 3 year moving average data.

6. Conclusion

The paper sought to examine the behaviour of central bank independence in the midst of a literate society, on financial development in Africa and other developing countries. We argue that the impact of central bank independence on financial development will be enhanced in a literate society as their knowledge of the magnitude and direction of their investment decisions. We find that given more independence, a literate populace that is skilled can engage in employment to earn incomes with which they can invest in the financial instruments give the favourable economic conditions, this leads to higher levels of financial development.

However, given low independence, such as higher central bank governor turnover rates, the increasing knowledge of the impact of low central bank independence on economic outcomes makes the literate populace more reluctant in investing in the financial markets. Secondly, the literate populace being skilled and knowledgeable can direct their incomes and /investments in the financial sector, into other productive areas of the economy such as the real estates. Knowledge of such alterative investment options makes their reactions to threat to central bank independence very pronounced as they quickly and accurately process these information and feed them into their investment decisions The policy implications are that while central bank independence laws in Africa should be implemented together with other institutional reforms that strengthen the central bank’s ability to be independent of political authorities, the capacity of the investing public should be developed through investments in education, which will equip many to participate in the financial markets given the favourable economic conditions that come with having an independent central bank.

Disclosure statement

The authors do not have any known competing interests.

Data Availability Statement

The data that support the findings of this study are openly available in:

1. World Bank (2017). The World Development Indicators, at https://datacatalog.worldbank.org/dataset/world-development-indicators 2. Freedom House (2017). Freedom in the World, at https://freedomhouse.org/report-types/freedom-world 3. Garriga (2016). CBI Data, https://sites.google.com/site/carogarriga/cbi-data-

Additional information

Funding

References

- Acemoglu, D., Johnson, S., Querubin, P., & Robinson, J. A. (2008). When does policy reform work? The case of central bank Independence (No. w14033). National Bureau of Economic Research.

- Agoba, A. M., Abor, J. & Osei, K. A., (2019). Do independent central banks exhibit varied behaviour in election and non-election years: The case of fiscal policy in Africa. Journal of African Business, 21(1), 105–23. https://doi.org/10.1080/15228916.2019.1584263

- Agoba, A. M., Abor, J., Osei, K. A., & Sa-Aadu, J. (2017). Central bank Independence and inflation in Africa: The role of financial systems and institutional quality. Central Bank Review, 17(4), 131–146. https://doi.org/10.1016/j.cbrev.2017.11.001

- Alagidede, P., Mensah, J. O., & Ibrahim, M. (2018). Optimal Deficit Financing in a Constrained Fiscal Space in Ghana, African Development Review, https://doi.org/10.1111/1467-8268.12337

- Arora, R. U. (2012). Financial inclusion and human capital in developing Asia: The Australian connection. Third World Quarterly, 33(11), 177–197. https://doi.org/10.1080/01436597.2012.627256

- Ayadi, R., Arbak, E., Naceur, S. B., & De Groen, W. P. (2015). Financial development, bank efficiency, and economic growth across the Mediterranean. In Economic and social development of the Southern and Eastern Mediterranean countries. Springer.

- Ayadi, R., Naceur, S. M., & De Groen, W. (2014). Determinants of Financial Development Across the Mediterranean, Economic and Social Development of the Southern and Eastern Mediterranean Countries.

- Baltagi, B. H., Demetriades, P., & Law, S. H. (2009). Financial Development and Openness: Evidence from Panel Data. Journal of Development Economics, 89(22), 285–296. https://doi.org/10.1016/j.jdeveco.2008.06.006

- Barth, J. R., Nolle, D. E., Phumiwasana, T., & Yago, G. (2003). A cross-country analysis of the bank supervisory framework and bank performance. Financial Markets, Institutions & Instruments, 12(22), 67–120. https://doi.org/10.1111/1468-0416.t01-2-00001

- Battiston, S., Farmer, J. D., Flache, A., Garlaschelli, D., Haldane, A. G., Heesterbeek, H., Scheffer, M., JaegerJaeger, C.C., MayMay, R.R., & SchefferScheffer, M. (2016). Complexity theory and financial regulation. Science, 351(6275), 818–819. https://doi.org/10.1126/science.aad0299

- Becker, G. S. (2009). Human capital: A theoretical and empirical analysis, with special reference to education. University of Chicago press.

- Bernanke, B. S. (2004). Remarks by Governor At the meetings of the Eastern Economic Association, “The Great Moderation”.

- Bhushan, P., & Medury, Y. (2013). Financial literacy and its determinants.

- Blancheton, B. (2016). Central bank Independence in a historical perspective. Myth, lessons and a new model. Economic Modelling, 52, 101–107. https://doi.org/10.1016/j.econmod.2015.02.027

- Bodea, C., Garriga, A. C., & Higashijima, M. (2017). Monetary Constraints, Spending, and the Autocratic Survival in Dominant Party Regimes. Paper presented at the 2016 Annual Meeting of the American Political Science Association.

- Chinn, M. D., & Ito, H. (2006). What matters for financial development? Capital controls, institutions, and interactions. Journal of Development Economics, 81(1), 163–192. https://doi.org/10.1016/j.jdeveco.2005.05.010

- Chinn, M., & Ito, H. (2011). Financial Globalization and China. In forthcoming in the Encyclopedia of Financial Globalization, edited by Gerard Caprio, et al. (Elsevier).

- Cihák, M. (2010). Price stability, financial stability, and central bank Independence. In: 38th Conference of the Oesterreichische National bank. http://www.oenb.at/en/Publications/Economics/Economics-Conference/2010/.

- Cinnirella, F., & Streb, J. (2017). The role of human capital and innovation in economic development: Evidence from post-Malthusian Prussia. Journal of Economic Growth, 22(2), 193–227. https://doi.org/10.1007/s10887-017-9141-3

- Coulombe, S., & Tremblay, J. F. (2006). Le capital humain et les niveaux de vie dans les provinces canadiennes. Statistique Canada.

- Coulombe, S., Tremblay, J. F., & Marchand, S. (2004). Literacy scores, human capital and growth across fourteen OECD countries. Statistics Canada.

- Cukierman, A. (2008). Central Bank Independence and Monetary Policymaking Institutions–Past, Present and Future. European Journal of Political Economy, 24(4), 722–736. https://doi.org/10.1016/j.ejpoleco.2008.07.007

- Cukierman, A., Webb, S. B., & Neyapti, B. (1992). Measuring the independence of central banks and its effect on policy outcomes. The World Bank Economic Review, 6(3), 353–398. https://doi.org/10.1093/wber/6.3.353

- Debelle, G., & Fischer, S. (1994). How independent should a central bank be? (pdf) proceedings of a conference sponsored by the federal reserve bank of Boston. Mass.

- De Haan, J., & Kooi, W. J. (2000). Does central bank Independence really matter? New evidence for developing countries using a new indicator. Journal of Banking and Finance, 24(4), 643–664. https://doi.org/10.1016/S0378-4266(99)00084-9

- Doumpos, M., Gaganis, C., & Pasiouras, F. (2015). Central bank Independence, financial supervision structure and bank soundness: An empirical analysis around the crisis. Journal of Banking & Finance, 611 , S69–S83. https://doi.org/10.1016/j.jbankfin.2015.04.017

- Doumpos, M., Gaganis, C., & Pasiouras, F. (2016). Bank Diversification and Overall Financial Strength: International Evidence (August 2016). Financial Markets, Institutions & Instruments, 25(3), 169–213. https://doi.org/10.1111/fmii.12069

- Eijffinger, S. C. W., & van der Cruijsen, C. A. B. (2007). The economic impact of central bank transparency: A survey. CEPR.

- Garriga, A. C. (2016). Central bank Independence in the world: A new data set. International Interactions, 42(5), 849–868. https://doi.org/10.1080/03050629.2016.1188813

- Gazdar, K. (2011). Institutions, développement financier et croissance économique dans la région MENA (Doctoral dissertation, Reims).

- Gnan, E., Silgoner, M., & Weber, B. ((2007)). Economic and financial education: concepts, goals and measurement. Monetary Policy & the Economy, 3, 28–49 https://doi.org/10.1113/1.4127 .

- Group, W. B. (2017). WORLD DEVELOPMENT INDICATORS 2017. WORLD BANK.

- Hielscher, K., & Markwardt, G. (2012). The role of political institutions for the effectiveness of central bank Independence. European Journal of Political Economy, 28(3), 286–301. https://doi.org/10.1016/j.ejpoleco.2011.08.004

- Huang, T., Wu, F., Yu, J., & Zhang, B. (2015). International Political Risk and government bond pricing. Journal of Banking & Finance, 55(1) , 393–405 https://doi.org/10.1016/j.jbankfin.2014.08.003.

- Infe, O. (2011). Measuring financial literacy: Core questionnaire in measuring financial literacy: Questionnaire and guidance notes for conducting an internationally comparable survey of financial literacy. In Pariz: OECD.

- Kang, J., & Pflueger, C. (2015). Inflation risk in corporate bonds. Journal of Finance, 70(1), 115–162 https://doi.org/10.1111/jofi.12195.

- King, R. G., & Levine, R. (1993). Finance and growth: schumpeter might be right. The Quarterly Journal of Economics, 108(3), 717–737. https://doi.org/10.2307/2118406

- Kodongo, O. (2018). Financial regulations, financial literacy, and financial inclusion: Insights from Kenya. Emerging Markets Finance and Trade, 54(12), 2851–2873. https://doi.org/10.1080/1540496X.2017.1418318

- Laeven, L., & Levine, R. (2009). Bank Governance, Regulation and Risk Taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and retirement planning in the United States. Journal of Pension Economics & Finance, 10(4), 509–525. https://doi.org/10.1017/S147474721100045X

- Masciandaro, D. (2015). Current account and real exchange rate changes: The impact of trade openness, with Cristina Terra and Enrico Vasconcelos. European Economic Review, 105(1) , 135–158.

- Masciandaro, D., Quintyn, M., & Taylor, M. (2008). Financial Supervisory Independence and Accountability—Exploring the Determinants. International Monetary Fund working paper https://ssrn.com/abstract=1154324.

- McCracken, M., & Murray, T. S. (2009). The economic benefits of literacy: Evidence and implications for public policy. In London. Canadian Language and Literacy Research Network.

- Mori, N., Nyantori, T., & Olomi, D. (2017). Effects Of Clients’ literacy on Default and Delinquency of Savings and Credit Co-Operative Societies in Tanzania. Business Management Review, 19(2), 1–12 http://hdl.handle.net/11159/3224.

- Murray, T. S., McCraken, M. W., Jones, D., Shillington, S., & Stucker, J. (2009). Addressing Canada’s Literacy Challenge: A Cost. In Benefit Analysis, Data Angel.

- Nantembelele, F. A., & Gopal, S. (2018). Assessing the challenges to e‐commerce adoption in Tanzania. Global Business and Organizational Excellence, 37(3), 43–50. https://doi.org/10.1002/joe.21851

- Nath, R., & Murthy, V. N. (2019). What accounts for the differences in internet diffusion rates around the world? in advanced methodologies and technologies in network architecture, mobile computing, and data analytics. IGI Global.

- Papadamou, S., Sidiropoulos, M., & Spyromitros, E. (2014). Determinants of Central Bank Credibility and Macroeconomic Performance. Eastern European Economics, 52(4), 5–31.

- Papadamou, S., Spyromitros, E., & Tsintzos, P. (2017). Public investment, inflation persistence and central bank Independence. Journal of Economic Studies, 44(6), 976–986. https://doi.org/10.1108/JES-10-2016-0214

- Piazzesi, M., & Schneider, M. (2009). Momentum Traders in the Housing Market: Survey Evidence and a Search Model. American Economic Review, 99(2), 406–411. https://doi.org/10.1257/aer.99.2.406

- Quintyn, M., & Taylor, M. W. (2002). Regulatory and supervisory Independence and financial stability. IMF Working Paper 02/46. International Monetary Fund.

- Ramakrishnan, R. (2012). Financial Literacy and Financial Inclusion. 13th Thinkers and Writers Forum.

- Raza, S. H., Shahzadi, H., & Akram, M. (2014). Exploring the determinants of financial development, using panel data on developed and developing countries. Journal of Finance and Economics, 2(5), 166–172. https://doi.org/10.12691/jfe-2-5-6

- Richard, C. A., & Gertler, M. (1997). How the Bundesbank Conducts Monetary Policy,”. In C. D. Romer & D. H. Romer (Eds.), Reducing Inflation: Motivation and Strategy (pp. 363–412). University of Chicago Press.

- Rogoff, K. (1985). Can international monetary policy cooperation be counterproductive? Journal of International Economics, 18(3–4), 199–217. https://doi.org/10.1016/0022-1996(85)90052-2

- Romer, P. (1993). Idea gaps and object gaps in economic development. Journal of Monetary Economics, 32(3), 543–573. https://doi.org/10.1016/0304-3932(93)90029-F

- Sare, Y. A., Aboagy, A. Q. Q., Mensah, L., & Bokpin, G. A. (2018). Effect of financial development on international trade in Africa: Does measure of finance matter? Journal of International Trade and Economic Development, 27(1), 1–20 https://doi.org/10.1080/09638199.2018.1474246.

- Sehrawat, M., & Giri, A. K. (2016). Impact of Inflation on Financial Development: Evidence from India. Journal of Economic Policy and Research, 11(2), 56 https://www.proquest.com/openview/43b13d298f4ba66e1a7c1ef77206c922/1?pq-origsite=gscholar&cbl=2030550.

- Stiglitz, J. (1998). Central banking in a democratic society. De Economist, 146(2), 199–226. https://doi.org/10.1023/A:1003272907007

- Taylor, J. (2013). The Effectiveness of Central Bank Independence Versus Policy Rules. American Economic association Annual Meeting. San Diego American Economic Association Annual Meeting.

- Tayssir, O., & Feryel, O. (2017). Does central banking promote financial development? Borsa Istanbul Review, 24(1), 52–75 https://doi.org/10.1016/j.bir.2017.09.001.

- Van Rooij, M. C. J., Lusardi, A., & Alessie, R. J. M. (2012). Financial literacy, retirement planning and household wealth. The Economic Journal, 122(560), 449–478. https://doi.org/10.1111/j.1468-0297.2012.02501.x

- Welch, C., & Braunstein, S. F. (2002). Financial literacy: An overview of practice, research, and policy, Federal Reserve Bulletin, Board of Governors of the Federal Reserve System (U.S.) https://heinonline.org/HOL/LandingPage?handle=hein.journals/fedred88&div=158&id=&page=.

- Yoshino, N., & Morgan, P. (2016). Overview of financial inclusion. regulation, and education.

- Yu, T. K., Lin, M. L., & Liao, Y. K. (2017). Understanding factors influencing information communication technology adoption behavior: The moderators of information literacy and digital skills. Computers in Human Behavior, 71(1) , 196–208. https://doi.org/10.1016/j.chb.2017.02.005

Appendices

Appendix I: Descriptive Statistics

Appendix II: Correlation Matrix

Appendix III: Developing Countries Sample