?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

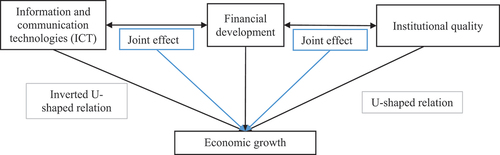

This research aims to consider determinants of economic growth, such as financial development, institutional quality, and information and communication technology (ICT) penetration, which have been explored separately in previous studies and have produced mixed findings in different regions. Using the two-step system generalized method of moments (GMM) estimator for a dynamic panel dataset of 35 selected emerging countries, several research findings could be drawn as the following. First, both ICT penetration and institutional quality have significantly positive effects on economic growth. On the contrary, economic development could be hampered by financial development. Second, there are the U-shape and inverted U-shape relations for the cases of institutional quality and ICT penetration on economic growth, respectively. Third, the interaction effect of ICT penetration and financial development could enhance economic growth while the negative impact of financial development on economic development is amplified by the high level of institutional quality. These findings are robust to the global financial crisis control and the use of an alternative ICT proxy when setting up the approach of principal component analysis. Given these findings from emerging countries, some policy challenges that policy-makers should address by simultaneously considering each growth driver, such as financial development, ICT evolution, and institutional quality and interactions between them, as well as the non-monotonic effect of ICT penetration and institutional quality to facilitate economic growth.

PUBLIC INTEREST STATEMENT

This research aims to test the growth determinants and the joint effect of financial development and ICT penetration, as well as that of financial development and institutional quality on economic growth. Moreover, the non-linear linkage of ICT diffusion-growth and institutional quality-growth is also investigated. We provide several findings, which give a more intensive understanding of the factors driving the growth. While financial development has a detrimental effect on growth, ICT diffusion and institutional quality can stimulate economic growth. However, these effects are evidently non-monotonic in which inverted U-shaped and U-shaped patterns for the growth effect of ICT penetration and institutional quality are found respectively. The interaction effect of increased ICT penetration and financial development may boost economic growth. Nevertheless, the high degree of institutional quality may amplify the adverse effects of increased financial development on economic development. Understanding these effects may facilitate determining the appropriate policy towards sustainable economic growth.

1. Introduction

Since economic growth (hereafter, EG) has been of great interest to academicians and practitioners across the globe, it does not come as a surprise that a great deal of attention has been focused on the diverse determinants of growth. Despite the endeavor to determine the factors influencing economic growth, the existing driving forces of growth are inconclusive and the other factors such as ICT diffusion and institutional quality are under-researched. This is due to the varying features of the country, the use of disparate techniques, the fluctuation of data periods, and a failure to determine the appropriate variables (Rahman & Alam, Citation2021).

When it comes to sources driving economic growth, there are conflicting debates considering the benefits and drawbacks of financial development, ICT diffusion, and institutional quality. Accordingly, financial development, institutional quality, and ICT diffusion have a positive or negative impact on EG, which has been highlighted in previous research. With respect to the determining role of financial development, the economic system could work effectively (Cheng et al., Citation2021), leading to enhanced economic activities. More precisely, increased resource efficiency, rapid technological upgrades, and material and human capital accumulation characterized by financial development could spur growth (Levine, Citation2005). However, financial development is usually detrimental to economic growth, but the negative impact could be amplified in high-income nations (Cheng et al., Citation2021).

In terms of ICT evolution, the development of technology could have a significant impact on both high-income and low and middle-income countries in such a manner that economic growth could be enhanced thanks to the ICT expansion (Appiah-Otoo & Song, Citation2021). Moreover, one could observe that the rapid enhancement of ICT diffusion could be associated with considerable development in the banking and financial sectors (Del Gaudio et al., Citation2021). ICT has significantly decreased transaction costs in financial services (Hasbi & Dubus, Citation2020). On the contrary, Beck et al. (Citation2016) illustrate that financial innovation has a negative impact on the banking business in terms of both performance and risk, resulting in the decreased growth of the economy.

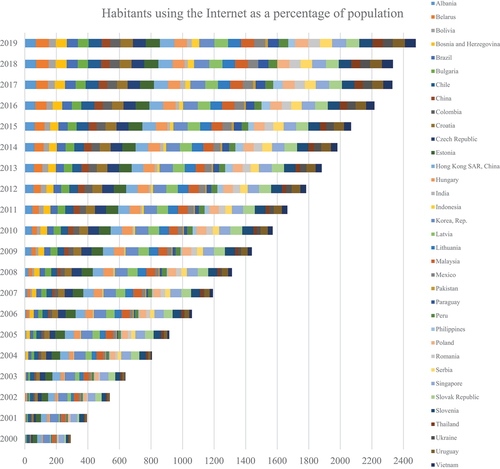

With the Internet at its heart, the penetration of ICT has triggered a fundamental change of the globe into an information society (Vu, Citation2011). In general, there is a growing trend in the development of ICT in terms of the internet for emerging economies in the study sample (see Figure ), which highlights the evolution of ICT in the era of innovation and breakthroughs. Taking Vietnam—a typical emerging country, for example, there has been an exponential increase pattern covering two decades, from 0.254 in 2000 to 68.7 in 2019, in terms of the number of individuals using the Internet as a share of the population. Therefore, technological progress has experienced considerable growth over the last decades (Stanley et al., Citation2018).

Figure 1. Evolution of individuals using the Internet as a proportion of population.

Regarding institutional quality, Rodrik (Citation2000) argues that institutions not only have a direct impact on economic growth but they also have an impact on other drivers of growth such as physical and human capital, investment, and technological advances, all of which contribute to an increase in an economy’s growth. Two of the most significant institutional qualities of countries—the rule of law and the practice of democracy—affect economic growth differently, particularly in developing countries (Butkiewicz & Yanikkaya, Citation2006). It appears to agree that maintaining the rule of law is crucial for economic growth (Knack & Keefer, Citation1995), but democracy has no significant influence on growth after adjusting for other relevant growth drivers (Dollar & Kraay, Citation2000).

The motivations driving us to do this current research are as follows: First, ICT penetration has picked up speed in recent years, and numerous studies have looked into how it affects economic growth. ICT-achieved information can be communicated via electronic coding and virtual movement, which affects the technological advancement of various industries and, as a result, navigates economic operations. ICT plays a crucial role in global change and has a direct impact on every sector of the economy. None of these ICT products and services are exclusive to developing or emerging economies. However, ICT frequently makes services available in these economies that were previously unavailable in either the digital or non-digital sectors (Niebel, Citation2018). The important role played by ICT should be revisited in emerging countries, which can benefit the most. Second, previous empirical research has not adequately investigated the driving effect of institutional quality on economic growth. When researching the influence of ICT on emerging countries, not only economic but also political factors should be considered. Third, previous studies have shown that financial development, ICT penetration, and institutional quality can have a positive or negative impact on economic growth separately. This study brings all these factors together into the same model to more fully consider the dynamics of economic growth. Finally, previous studies have mainly addressed the linear influence of ICT penetration and institutional quality on growth. The author expects that positive and negative effects can occur when considering the role of non-linear models, so this study attempts to test whether nonlinearity exists in the impact of ICT penetration and institutional quality on economic growth.

The main added value of this study to the prevailing literature is as follows: First, this research is among the first attempts to detect the impact of ICT diffusion and institutional quality and their interactions with financial development in driving economic growth in the case of emerging countries. Despite the fact that development of ICT in emerging countries might share some similarities with the ICT progress encountered in India, South Asia, Latin America, Eastern Europe, and Sub-Saharan Africa, there is an urgent need to examine whether ICT penetration in emerging economies has begun to produce stronger growth. In addition, institutional backgrounds do not have the same influence on economic growth across countries. Accordingly, institutions with comparable qualities can yield different outcomes among groups, regions, and economies (Nawaz et al., Citation2014). Therefore, this research might provide a comprehensive background of 35 emerging countries covering the period of 2000–2019, which highlights the focus on emerging economies with a more recent database.

Second, although several studies have documented that economic growth is determined by ICT penetration or institutional quality, the non-linear relationship for ICT diffusion—growth and institutional—growth nexuses still remain scarce in previous studies. To this end, we address the U-shaped curve relationship using squared terms of ICT penetration and institutional quality measures in order to capture the existence of a threshold at which ICT diffusion and institutional quality could have differential impacts on growth. In addition, for the case of ICT proxies, we employ both measures, such as ICT individual variables reflecting the changes in the Internet, mobile, telephone and ICT import and ICT index using principal component analysis. This approach could offer a way to avoid the problem of multicollinearity among measures defining the main construct, which is used for robustness tests in our study.

Third, some research has discussed the impact of interaction terms among ICT diffusion and financial development on EG. However, the joint effect of institutional quality and financial development on EG has been under-explored in literature. To have a deeper understanding, we provide evidence for the moderating effect of institutional quality and ICT penetration on the growth-financial development nexus for the case of emerging markets. Empirical findings show that the increase in ICT diffusion could spur the positive impact of financial development on growth while being cautious of the amplifying effect of institutional quality on growth-decreasing financial development.

Addressing these contributions in an economic growth model, we apply a two-step system GMM for a sample of 35 emerging countries to capture the dynamic nature of economic growth and avoid the potential issue of endogeneity. Several findings could be provided as follows. First, a high level of ICT diffusion and institutional quality stimulate economic growth, while there is an unfavorable impact of financial development on growth. Second, ICT penetration and institutional quality have a U-shape relationship with economic growth by using the approach of quadratic terms, suggesting that there is a threshold at which the impact of ICT diffusion and institutional quality could change the direction of impact on economic growth. More specifically, inverted U-shape and U-shaped forms are evidence of the impact of ICT diffusion and institutional quality, respectively. Third, the union effect captured by the interaction terms of ICT diffusion-financial development and institutional quality-financial development on growth is statistically significant.

The rest of the paper is formatted as follows: The review of the literature is presented in Section 2. Section 3 describes the data and methods. Section 4 discusses the empirical results and shows the robustness test with an alternative proxy for ICT diffusion, while Section 5 presents the conclusion and policy implications.

2. Literature review and hypotheses development

2.1. Theoretical framework

From economic theory, such as that of Cobb and Douglas (Citation1928), the total production function captures the production function elements, such as labor, capital, and technology, as well as the effect of these indicators on economic growth. Similarly, the Solow-Swan neoclassical growth model highlights three factors that drive an economy’s output: technological advancement, labor, and capital (Solow, Citation1956; Swan, Citation1956). Among these variables, financial development might be regarded as an indicator of capital, while ICT indicates technological advancement. The theoretical foundation of this literature can be traced back to the works of Schumpeter (Citation1981) and Gurley and Shaw (Citation1960), who argued that the development of financial intermediaries, such as banks, can increase the efficiency of resource distribution and promote technological innovation in production, thereby fostering further economic growth. In addition, the financial sector may collect savings, allocate resources to the most profitable investments, reduce information and transaction costs, and facilitate inter-industry trade. This results in increased resource allocation efficiency, rapid technological upgrades, and the buildup of material and human capital (Bencivenga & Smith, Citation1991; Greenwood & Jovanovic, Citation1990).

However, country-specific growth varies due to diverse effective structures, such as organizations that oversee the implementation of policies and programs. Numerous modifications have been made to this growth hypothesis, and D. North (Citation1990) was the first to examine institutions as a driver of economic growth; since then, an abundance of data has demonstrated their effectiveness. Furthermore, despite the fact that the theoretical literature emphasizes the favorable benefits of financial development and ICT proliferation on economic growth, empirical research on this topic remains insufficient (Sassi & Goaied, Citation2013). Based on the theoretical perspective of concepts relating to institutional quality, financial development, and ICT diffusion, we present empirical evidence to give more understanding of the nexus among them.

2.2. The impact of financial development on growth

The nexus between financial development and EG has received great attention in prior studies. The literature’s theoretical foundation may be traced back to the work of Schumpeter (Citation1981), who demonstrated that the establishment of financial intermediaries (i.e., banks) may improve resource allocation efficiency and enhance technical innovation in manufacturing, thereby boosting EG. Many empirical studies have found a favorable impact of financial development on economic growth (Hassan et al., Citation2011; Uddin et al., Citation2013). For more details, Levine and Zervos (Citation1998) examined 48 countries covering the period of 1976–1993, finding a substantial and statistically significant link between stock market development and subsequent economic growth. Hondroyiannis et al. (Citation2005) used the VAR model to analyze the influence of the stock market and discovered that financial development contributed to long-term economic growth in Greece and Belgium, respectively.

However, there is the negative impact of financial development on EG. This is due to a surge in financial crises, the existence of non-linear correlations or because a stock market does not have enough listings to encourage economic development (Rousseau & Wachtel, Citation2000; Samargandi et al., Citation2015). Samargandi et al. (Citation2015) use a threshold model to examine the non-linear impact in middle-income countries for 1980–2008, suggesting that excessive finance has a negative impact on economic growth in the long run due to the existence of an inverted U-shaped relationship between finance and growth. Based on a data sample of 26 EU countries covering the period of 1990–2016, Asteriou and Spanos (Citation2019) use exponential dummies to examine how the 2008 global financial crisis affected the influence of financial development on economic growth. Their findings reveal that the effect was favorable prior to the financial crisis but negative afterward.

2.3. Growth effect of ICT diffusion and institutional quality

There are three channels through which ICT penetration might impact EG (Vu, Citation2011), such as promoting technological diffusion and innovation, improving the quality of business and household decision-making; and raising demand and lowering production costs, which together enhance the output level. Similarly, Pradhan et al. (Citation2014) also demonstrate the channels through which ICT diffusion could drive economic growth, such as (i) an increase in the quality of life; (ii) an improvement in the competitiveness of conducting business; (iii) economic diversification; and (iv) business retention. Following Abdelbary and Benhin (Citation2019), the fast expansion of ICT has resulted in the creation of new employment, the promotion of e-commerce, the development of human capital, the dissemination of knowledge, and network externalities.

Scholars have also extensively debated the impact of ICT diffusion on economic development in recent years, as ICT is one of the primary prerequisites for rapid economic expansion. Despite the prediction of favorable relationships between ICT spread and economic growth from the theoretical literature, there are mixed results offered from empirical perspectives. On the one hand, a large number of empirical studies show the beneficial effect of ICT diffusion on growth. Using a sample of 36 countries from 1985 to 1993, Dewan and Kraemer (Citation2000) discovered evidence of a favorable link between ICT and growth only in developed countries. Based on a yearly data set of 39 economies from 1980 to 1995, Pohjola (Citation2000) shows a relevant and positive influence of ICT on growth only for a smaller sample of 23 OECD countries. Vu (Citation2011) investigates the impact of ICT penetration on economic development using a panel set of 102 nations from 1996 to 2005 with the approach of the System Generalized Method of Moment (GMM). The results show that ICT plays a significant role as a source of growth and that internet penetration has a greater marginal effect than other mobile phones and personal computers.

On the other hand, some new empirical literature suggests that ICT penetration has an unclear influence on economic development. According to Steinmueller (Citation1996), ICT penetration might have a detrimental influence on employment and the labor market in developing countries. According to the research, the rapid accumulation of ICT would eliminate unskilled employees and poor people since they are not adequately equipped and qualified, thus increasing poverty and economic inequality. Furthermore, ICT will offer industrialized nations with additional advantages in competing emerging countries in their own markets. Using the autoregressive distributed lag boundary test, Ishida (Citation2015) discovers that ICT investment does not boost GDP in Japan.

Inspired by the research of D. C. North (Citation1991), the growth effect of institutions has remained a debated topic of study and rather limited. It is of paramount importance to integrate political variables in order to assess the economic process and determine the amount and direction to which a government’s political determinants impact the economic performance (Radu, Citation2015). In this regard, Abdelbary and Benhin (Citation2019) examine the influence of governance on economic growth and human capital using data from Arab nations from 1995 to 2014. According to their findings, governance has a favorable impact on human capital and economic growth. C. P. Nguyen et al. (Citation2018) employ the data of 29 emerging economies for the period of 2002–2015 and the S-GMM technique to show the favorable influence of institutional quality on EG. In addition, on the basis of the theoretical framework and empirical evidence in a sample of developed and developing Asian countries, Nawaz et al. (Citation2014) posit that institutions do have a role in determining long-term economic progress.

Helgason (Citation2010) uses a pooled regression model and a fixed-effects model to examine the impact of institutional quality on economic growth in developed and developing economies. According to the findings, institutional quality has a strong and positive association with growth in both types of countries. Glawe and Wagner (Citation2019) investigate the impact of institutional quality and human capital on economic growth in 35 European economies covering the period of 1996–2014. The results of system GMM estimation indicate that institutional quality has a stimulating effect on the growth of per capita income in Europe. The study also considers a disaggregated analysis of the effects of the institutional quality indices, showing that political stability, rule of law, regulatory quality, and corruption control can appear to be especially important, whereas voice and accountability, as well as government effectiveness, show less importance. Hayat (Citation2016) examines the influence of institutional quality on economic growth using 104 economies and the GMM estimators. According to the study, both FDI inflows and institutional quality are positively associated with economic growth.

However, institutions are primarily concerned with redistribution rather than production, with monopolies rather than competitive conditions, and with restricting rather than developing opportunities, rarely resulting in investments that boost productivity (Yıldırım & Gökalp, Citation2016). Employing annual time series data from 2001 to 2019, Utile et al. (Citation2021) investigate the impact of institutional quality on the development of the Nigerian economy. The Auto-Regressive Distributed Lag (ARDL) estimation reveals that institutional quality has a considerable negative influence on economic growth.

2.4. Non-linear U-shaped link for ICT penetration—growth and institutional quality—growth

Several studies have offered a profound understanding of the non-monotonic nexus between ICT diffusion and economic growth. For example, according to Grace et al. (Citation2004), the value of a telephone line increases exponentially with the number of people connected to the system. Furthermore, since a certain number of users is achieved, an exponential increase is observed. This explains why it was assumed that only rich economies could gain benefits from ICT development. Sassi and Goaied (Citation2013) use quadratic terms to capture the potential non-monotonic link between ICT and growth and find the existence of U-shaped forms for the ICT diffusion-growth nexus.

Similar to the ICT penetration-growth nexus, it is unrealistic to demonstrate that the impact of institutional quality and economic growth remain unchanged. We assume that when the quality of institutions is low, the government can not accelerate the economic incentives for economic agents in the economy. On the other hand, the high level of institutional quality could create a favorable environment in which economic agents could perform effectively, driving economic growth to a greater extent. These arguments are motivated by the work of Acheampong et al. (Citation2021) who suggest that globalization’s economic, social, and political dimensions follow an inverted U-shaped relationship with economic growth when employing a dataset of 23 emerging economies from 1970 to 2015. In addition, Law et al. (Citation2013) may be relevant to our research topic, showing the impact of financial development on EG conditional on the level of institutional quality. Accordingly, financial development has a beneficial and meaningful influence on growth only once a certain degree of institutional development has been reached. To the best of our understanding, we are among the first to address the U-shaped relationship between institutional quality and economic growth with the approach of quadratic term inclusion.

2.5. Joint effects of ICT diffusion—financial development and institutional quality—financial development on growth

The relationship between financial development and economic growth could be driven by the impact of ICT penetration and institutional quality, which have been ignored in previous research. There is also a body of empirical research relating to the important joint impact of ICT diffusion and financial development. Shamim (Citation2007) is among the first to present empirical evidence that a component of the financial sector generated through improved communications infrastructure is favorably related to long-run economic growth. The Generalized Method of Moment (GMM) was used to perform empirical research on dynamic panel data from 61 economies covering the period of 1990–2002. The finding shows that a rise in mobile phone subscribers and internet users has a favorable impact on financial depth, which is the backbone of any country’s ability to expand. Sassi and Goaied (Citation2013) incorporate the union impacts of ICT diffusion and financial development into the economic growth model and discover the positive joint effect of ICT diffusion and financial development on growth in a sample of 17 MENA countries using the GMM method. By constructing an economic growth framework and using the GMM technique, Das et al. (Citation2018) found that the interaction impact of ICT and financial development can boost economic growth in low-income nations but not in lower-middle-income countries from 2000 to 2014. Since ICT penetration can fuel the rise of financial technology, which is changing the current structure of the financial system and increasing competitors, ICT developments can hamper the development of traditional financial institutions. These new FinTech companies offer the same services as banks, possibly more efficiently due to technological advances, but in a different and unbundled manner. As a result, ICT applications in financial markets have increased rapidly, yet the impact of ICT diffusion on financial development is still unclear (Navaretti et al., Citation2018). Furthermore, ICT diffusion could cause different effects on financial development in lower and higher stages of ICT diffusion (Asongu & Acha-Anyi, Citation2017; Asongu & Odhiambo, Citation2019). This may pose an ambiguous union effect of ICT penetration and financial development on economic growth, which needs to be clarified.

In terms of the joint effect of institutional quality and financial development on EG, empirical evidence still remains scarce. When the financial sector is entrenched inside a solid institutional framework, it has a greater impact on economic growth (Demetriades & Hook Law, Citation2006). Law et al. (Citation2013) argue that due to the unfavorable practices of the banking sector or political intervention that may redirect credit to inefficient or even useless enterprises, a gain in financial development as measured by traditional financial development indicators might not result in higher growth. The influence of institutions on economic growth varies among Asian countries and is dependent on the development level of the economy (Nawaz et al., Citation2014). Dluhopolskyi et al. (Citation2019) assert that the country’s government could organize suitable drivers to improve environmental performance, leading to economic growth. Moreover, an effective business environment is aided by institutional quality, which could lower transaction costs and ensure stability and clarity via the protection of property rights and the rule of law (Abubakar, Citation2020), which is highly favorable for economic growth.

Law et al. (Citation2018) demonstrate that institutions moderate the favorable relationship between financial development and economic growth. Using data from 87 countries from 1984 to 2014 and the dynamic panel GMM estimators, findings show that when institutions are weak, the finance measured by private sector credit, liquid liabilities, and domestic credit reduces overall growth. Thus, institutions play a vital role in the relationship between financial development and economic growth, with economies whose institutions are of higher quality benefiting greatly from banking sector expansion. Fernández and Tamayo (Citation2017) highlight two primary areas in which institutions play a crucial role in encouraging financial development: the definition and enforcement of property rights in financial contracts and the formulation and execution of macroeconomic and financial policy. Then, financial development boosts economic growth primarily through reducing financial limitations, enhancing risk-sharing, and ensuring enough liquidity, thereby allowing for greater rates of capital accumulation and more effective resource allocation. Institutional quality and financial development are critical cornerstones of long-term economic success. However, their interaction remains scarce in prior studies. Therefore, we expect the moderating effect of institutional quality on the financial development—growth nexus.

3. Data and methodology

3.1. Data

Our data covers a sample of 35 selected emerging countries and the period of 2000–2019. The emerging countries included in the sample are listed in Appendix A, with data extending to 2019. The dataset for all variables is retrieved from the World Development Indicators of the World Bank, except for institutional quality, which is collected from Worldwide Governance Indicators. Given the availability of data, we collected 35 emerging countries based on the dataset of World Indicator Development. Several reasons for using this sample are as follows. First, emerging markets are undergoing fast expansion and modernization (Herrera-Echeverri et al., Citation2014), which gives a fertile context for a favorable environment to investigate ICT developments. Second, the impact of ICT penetration and institutional quality on financial growth is not always the same for all national groups (Sassi & Goaied, Citation2013). Hence, to avoid heterogeneity between countries, we only limit our analysis to the case of emerging countries. Third, Steinmueller (Citation2001) notes that ICT penetration has the potential to support the development strategy of “leapfrogging”; that is, possible skip some of the processes of accumulation of human capabilities and fixed investment in order to close the gap between industrialized and developing countries in terms of productivity and output. The success of this approach is contingent upon the absorptive capacity (the competence and considerable efforts of employees and management to employ new technologies) of emerging economies (Keller, Citation1996). The existence of the “leapfrogging” phenomenon drives us to test the role of ICT diffusion, which may be the most beneficial for emerging countries. Fourth, institutional quality plays a critical role in a certain economy (Khan et al., Citation2020). However, only a few studies have explored this in emerging economies. This gives rise to testing the effect of institutional quality on growth in both aspects of the non-linear and linear nexus to provide a more intensive understanding of the salience of institutional quality. For these reasons, we strongly believe that a sample of emerging countries is a favorable laboratory to test the concept of ICT penetration, institutional quality, and relationships among them.

3.2. Model

On the basic of the model of Sassi and Goaied (Citation2013) and Cheng et al. (Citation2021), we develop the empirical model with slight modifications in which institutional quality is included in order to account for the impact of institutional quality on economic growth. The baseline model adopts the following forms:

Greater capital expenditures are connected with more robust economic development, but higher current expenditures are associated with less favorable economic performance, according to one theory concerning the importance of government spending (Gupta et al., Citation2005). Another viewpoint holds that a higher government size is detrimental to economic progress and efficiency (Ram, Citation1986). Despite different opinions regarding the relationship between government expenditures and economic development, the current analysis anticipates a positive relationship between government consumption expenditures and economic growth.

The variables trade openess and inflation are employed on the basis of the work of Cheng et al. (Citation2021), who capture these variables as controlling other drivers of economic growth. The results statistically show that trade openess has a positive effect on economic growth, implying that greater competitiveness in trade can enhance economic growth. For instance, trade openness has been highlighted as a factor that influences economic growth. Malefane and Odhiambo (Citation2021) state that there is a robust positive relationship between trade openness and economic growth. Exposure to international trade can serve as a growth engine that might have a positive impact on an economy if greater trade openness is achieved.

The inclusion of the inflation rate in this study is due to the fact that a high inflation rate is indicative of macroeconomic instabilities that are likely to result in a fall in economic growth (Eriṣ & Ulaṣan, Citation2013). In both fast- and slow-developing of Sub-Saharan African economies, high inflation rates have a detrimental impact on economic growth (Bittencourt et al., Citation2015). Inflation is anticipated to have a negative relationship with economic growth in this aspect.

All variables are reported in Table . In addition, Table of Appendix B reports the summary statistics, showing clearly that there is no concern of multicollinearity among independent variables for our data, which is evidenced by the value of correlations less than the threshold of 0.8. For the pairs of dependent variables with correlation values greater than 0.8, we do not enter into the same specification to avoid the spurious regression.

Table 1. Variable definitions and descriptive statistics

To capture the threshold at which the impact of institutional quality and ICT diffusion on economic growth could change, we integrate the squared terms of independent variables, denoted by ICT2it and IQ2it, in order to test whether the U-shaped forms are present for both main independent variables of interest. The following specifications with quadratic terms are as follows:

Specification (2) and (3) use the same variables to specification (1), which is described in details of Table .

To test whether the union effect of financial development-ICT diffusion and financial development-institutional quality on economic growth, we include the interaction term for both cases, denoted by and

respectively. The regression function with interactive terms is as follows:

3.3. Econometric estimation method

For our study, we used the two-step system generalized method of moments (S-GMM) model, which is widely employed by previous studies (Cheng et al., Citation2021; Das et al., Citation2018; H. H. Nguyen et al., Citation2022a; Nguyen & Dinh, Citation2022; T. P. Nguyen et al., Citation2022b; Sassi & Goaied, Citation2013). When analyzing changes in financial variables, the GMM technique outperforms the standard OLS method (Huan, Citation2021). This model solves the issues of endogeneity, omitted variables, and heteroscedasticity. To obtain valid instruments, lagged endogenous variables and weakly exogenous variables must be free of autocorrelation in the fundamental model (Blundell & Bond, Citation1998). This means that disturbances in the difference model have considerable first-order correlation but minimal second-order autocorrelation. The Arellano-Bond tests for first- and second-order serial correlation in first-differenced residuals are employed for this purpose (Arellano & Bond, Citation1991). Furthermore, we employed the lagged values (two and above) of the regressors in the GMM dynamic technique as the estimated instrument to eliminate any bias owing to reverse causality.

4. Results

For econometric evaluations before discussing the empirical findings, at the bottom of each table for regression results, we observe that there is the existence of first-order and no second-order correlation with the error terms, which is evidenced by the significant value of AR(1) and insignificant value of AR(2), respectively. Furthermore, the Hansen test shows no significance, indicating the validity of instruments employed in the S-GMM estimator. In addition, the dynamic characteristics of economic growth is evidenced by the significantly positive values of the lagged GDP per capita. Taken together, the correctness of our estimating model is confirmed, showing the appropriate inference from these regression results.

4.1. The determinants of economic growth

Table reports the findings of specification (1) for the annual data of 35 emerging countries covering the period 2000–2019. In all regression models of Table , the coefficient on financial development (CPS) is significantly negative at least 10% significance level, suggesting that financial development could hamper economic growth. This is in line with Ram (Citation1999), Sassi and Goaied (Citation2013), and Cheng et al. (Citation2021) who show the unfavorable effect of financial development on growth. This could be explained by several points. According to Yong et al. (Citation2009), increased usage of interest-rate derivative financial instruments results in higher long-term risks. Banking hazards, according to Nijskens and Wagner (Citation2011), could result in increased long-term risks due to excessive bank lending and reduced capital reserves. Furthermore, due to excessive liquidity in the stock market, investors seek an extraordinary return for short-term investments, ignoring to monitor a company’s business performance and hampering economic growth.

Table 2. Growth effects of financial development, ICT penetration, and institutional quality

The findings also support that ICT diffusion, defined through the internet, mobile, telephone, and ICT imports, stimulate growth, which is evidenced by the significant value of coefficients on ICT proxies. This is consistent with Hassan (Citation2005) indicating that ICT is critical to growth since it is required to expand a country’s productive capacity in all areas of the economy, connects a country to the global economy, and assures competitiveness. Through electronic coding and virtual motion transmission, ICT may strengthen a country’s connection to the global economic system and stimulate more active economic activity (Cheng et al., Citation2021). It is worth noting that the coefficients of the internet are significantly greater than those of other measures for ICT diffusion, such as mobile, telephone, and ICT goods imports. This implies that the internet speeds up the transmission of information and improves the efficiency of information distribution, resulting in increased economic growth in the study of emerging markets. The finding also indicates the positive effect institutional quality could have on growth, suggesting that institution quality is critical in creating an enabling environment for economic development. This is in line with previous research (Iheonu et al., Citation2017; Parks et al., Citation2017).

In terms of other controlling variables, trade openness, inflation, and government consumption all have a considerable and predictable influence on growth. High government consumption and macroeconomic variations, as measured by high levels of inflation, depress economic growth in emerging countries, but trade openness has a positive influence on growth, demonstrating that lowering trade barriers promotes growth. The negative impact of GC on growth might be attributed to its preference for non-tradable commodities. Furthermore, there is evidence of growth convergence, implying that economies with greater initial income are being surpassed by those that are rising at a quicker pace. The global financial crisis in Models (2), (4), (6), and (8) in Table has a negative impact on growth, supporting the unfavorable effect of the 2008–2009 financial crisis on economic growth.

4.2. The U-shaped relation for ICT diffusion-EG and institutional quality-EG

Inspired by the arguments that the ICT diffusion—growth and institutional quality—growth linkages could follow the U-shaped forms, empirical results to confirm these U-shaped relations are reported in Table and Table . The coefficient on the quadratic term, ICT2, is negative and significant in almost all models, except model (5) and (6) for the internet indicator. This finding reveals that the relationship between ICT penetration and growth follows an inverted U-shaped form, suggesting the existence of a threshold at which the impact of ICT diffusion on economic growth could vary. If the ICT value is below this threshold, economic growth is positively affected by ICT development. However, the negative impact of ICT diffusion on growth could be evidenced if the value of ICT is above this threshold. This finding is contrary to the work of Sassi and Goaied (Citation2013) who find the U-shaped relation for ICT penetration-growth in the MENA region. Observing the case of the coefficient on IQ2, the significantly positive signs show the U-shaped forms for the impact of institutional quality on economic growth, with no exception for any case of ICT diffusion. The quality of the institutional environment could positively affect growth when the values of institutional quality are greater than a given threshold. This means that in the case of the value of institutional quality being less than this threshold, the nexus between institutional quality and growth turns negative.

Table 3. U-shaped relationship between ICT penetration and economic growth

Table 4. U-shaped relationship between institutional quality and economic growth

In addition to the stimulating effect of institutional quality on economic growth, we also provide a more intensive understanding than prior studies have; that is, we shed further light on the U-shaped impact of institutional quality on economic growth. There is a certain threshold at which this nexus changes from a positive to a negative pattern. Relevant research shows that political dimensions follow an inverted U-shaped relationship with economic growth (Acheampong et al., Citation2021). However, this research shows the impact of political globalization on economic growth displays an inverted U-shaped pattern. One should note that political globalization in this research is primarily based on the definition that this term is the diffusion of government policies and includes international non-government organizations, embassies, and United Nations peacekeeping missions (Gygli et al., Citation2019). This definition is not our focus in the current research and hence, we are the first to explore the U-shaped pattern for institutional quality-growth nexus for a case of emerging countries.

4.3. The joint effects of financial development—ICT diffusion and financial development—institutional quality on EG

Regression results in Table are employed to capture the related hypothesis of whether the impact of financial development is necessary to promote growth through the driving role of institutional quality and ICT diffusion. The coefficient on the interaction term, CPS*ICT, is positive and significant at 5% level, suggesting that although financial development has a negative influence on growth, ICT penetration could exert a positive impact on financial development, and the interaction effect could boost economic growth even more. In reality, the usage of telecommunications services has increased at an unexpected rate during the last two decades. The expansion of wireless technologies and telecommunications industries is primarily driving this nexus. According to King (Citation2012), mobile financial services enable firms to recognize a wide access rights, including telecommunications, retail, and e-commerce, in order to provide bill payment and other financial services. This tendency will continue, fundamentally altering the rules of the game for conventional banks.

Table 5. Interaction terms for ICT penetration—financial development and institutional quality—financial development in driving the economic growth

Regarding the impact of ICT investments on the economic progress of emerging economies, empirical data has been very limited and equivocal. The paucity of high-quality micro- and macro-level data sets on ICT for developing countries may be primarily responsible for the lack of strong empirical evidence on the effects of ICT in these economies (Niebel, Citation2018). Given our empirical evidence, we show the positive impact of ICT diffusion on growth. Moreover, we provide an empirical result of the combined effect of financial development and ICT penetration on economic growth, showing the stimulating role of ICT diffusion in changing the negative effect of financial development on growth. These results confirm the work of Sassi and Goaied (Citation2013) and Das et al. (Citation2018) who show the favorable impact of ICT on the financial development-growth nexus. This may imply that without a critical enhancement in ICT penetration, financial development will not be likely to gain the benefits of the interaction effect and promote economic growth (Das et al., Citation2018).

On the contrary, the interaction term, CPS*IQ, has a negative sign of its coefficients at a 1% significance level, indicating that the negative impact of financial development on growth could be amplified by the high level of institutional quality. This finding could be explained by the fact that the emerging countries have not yet attained a high level of economic development (Daniela-Neonila & Roxana-Manuela, Citation2014) and the institutional quality measured by voice of accountability negatively affects financial development (Khan et al., Citation2020). Both aspects could imply the negative impact of financial development on EG is pronounced in emerging countries despite having a high level of institutional quality.

With respect to the joint effect of institutional quality and financial development on economic growth, Effiong (Citation2015) indicates that there are positive but insignificant coefficients on the interaction impact of both financial development and institutions on growth. This research suggests that the existence of institutions has not improved the link between finance and growth in Sub-Saharan Africa. Sohag et al. (Citation2019) evaluate the importance of institutional quality in the finance-growth nexus in Indonesia and Malaysia from 1984 to 2017. In Malaysia, a positive improvement in institutional quality was shown to have a significantly bigger effect on growth than serving as a mediator. More interestingly, institutional quality was shown to hamper economic growth in Indonesia, but to have a positive and important mediating effect on the link between finance and growth. Given these conflicting findings in previous studies, we hold the view that, in the case of 35 emerging countries, the negative effect of institutional quality on growth is exacerbated under a high level of institutional quality.

4.4. Robustness test

To address the problem of multicollinearity in the dataset and reflect the generalized impact of ICT penetration development, we use principal component analysis (PCA) to build an ICT index using the comprehensive data of mobile, internet, telephone, and ICT goods imports. This approach is widely used by Gries et al. (Citation2009) and Cheng et al. (Citation2021). Specifically, to avoid a narrow sense of each indicator of ICT diffusion, we apply principal component analysis (PCA) to establish a combined index of ICT penetration, including fixed telephone lines (per 100 people), mobile cellular subscriptions (per 100 people), individuals using the Internet as a share of the total population (% of the total population), and ICT goods imports as a share of total goods imports (% of total goods imports), so as to capture a more comprehensive picture of ICT diffusion; hence, this approach can provide a generalized impact, not a narrow impact, of ICT on growth. In addition, PCA is a statistical approach used to create fewer variables or an index that describes the majority of the original variables’ variability (Achia et al., Citation2010; Olofin, Citation2012). Accordingly, this approach could combine sub-items of ICT indicators to establish a single index, providing the generalized impact of ICT diffusion. We use this combined approach of ICT diffusion to revisit the linkages among financial development, ICT diffusion, institutional quality, and economic growth.

One should note that PCA is an analytical process whose primary objective is to reduce the size of a data set containing a large number of linked variables by reducing the original set of variables into smaller sets consisting of linearly uncorrelated variables, known as principle components (Owoeye et al., Citation2022). Main result from PCA approach is a composite index which shows the most explanatory feature of original data variations. To test the suitability of the PCA index, a scoring coefficient is normally employed in which it is satisfactory if the composite index is greater than the threshold figure of 0.3 (Appiah-Otoo & Song, Citation2021). The component with a high percentage and an eigenvalue larger than one is the most appropriate to obtain, which resonably represents one single composite index for regression treatment (Phan et al., Citation2021).

Table displays a summary of the research methods employed in previous studies to calculate aggregate CPA from sub-items of ICT diffusion or one-by-one ICT proxy. Based on the widely used PCA in prior research, we apply this method to compute a composite index for ICT penetration.

Table 6. ICT index from previous studies

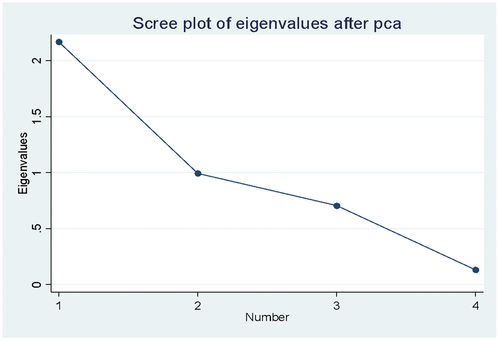

In Table , among components of ICT diffusion, we observe that the eigenvalue of component 1 is greater than 1. This could be illustrated by the scree plot chart in Figure , showing that component 1 has an eigenvalue over the balance line (eigenvalue = 1). Phan et al. (Citation2021) propose that since it includes enough information from the original data, the component with a large percentage and an eigenvalue greater than one should be chosen. Furthermore, component 1 could more appropriately explain the overall variance of the sample than the other components. The result is that the ICT diffusion index proxy may be expressed by the preference of the first component over the three remaining proxies.

Figure 2. Scree plot eigenvalues after running principal component analysis.

Table 7. Each component is capturing four proxies for ICT diffusion with eigenvalue and proportion

The Hansen test and the values of AR(1) and AR(2) at the bottom of each table support the correctness of the dynamic model using the approach of S-GMM, which could enable us to make inference from these regression results. Tables show the re-estimation of the specifications (1)-(4) to provide the consistent and robust results aforementioned in which the ICT sub-items are replaced with a single index of ICT diffusion from the PCA technique and other variables remain.

Table 8. Determinants of growth with an alternative proxy for ICT diffusion

Table 9. U-shaped form for the ICT diffusion—and institutional quality—EG relations

Table 10. The impact of ICT diffusion and institutional quality on financial development—growth nexus

Table displays the regression results for the determinants of economic growth with the alternative proxy for ICT diffusion, which is combined from four sub-items via the approach of principal component analysis. The findings for the main variables of interest and control variables are similar to those reported in Table , highlighting the stimulating role of ICT penetration and institutional quality on growth. These results are robust when accounting for the influence of the global financial crisis. Table shows the empirical U-shaped forms for the impact of ICT diffusion and institutional quality on growth, respectively. The findings are qualitatively consistent with those revealed in the previous section, indicating the quadratic linkages between ICT penetration—growth and institutional quality—growth. Table reports the joint effect of ICT diffusion—and institutional quality—financial development on economic growth. The positive coefficient on the union effect of ICT diffusion and financial development suggests the fact that because of the expansion of the financial sector, the influence of ICT penetration development on economic growth in emerging countries is positively found. On the contrary, institutional quality could amplify the negative impact of financial development on economic growth for the case study of emerging markets. These results again consistently confirm those reported previously.

5. Conclusion

It is widely discussed that financial development, ICT diffusion, and institutional quality could play a critical role in shaping economic activities (Cheng et al., Citation2021; Khan et al., Citation2020; Sassi & Goaied, Citation2013). For each of above determinants, the findings provide a mixed conclusion in previous studies. In addition, the U-shaped non-linear relationship and the interaction terms for ICT penetration—and institutional quality—growth linkage have been under-explored, especially in emerging economies. To bridge these research gaps, we not only investigate jointly the impact of financial development—institutional quality and financial development—ICT diffusion on economic growth, but also conduct an experiment with quadratic terms to capture the non-linear U-shaped forms for the impact of institutional quality and ICT diffusion on growth, employing the case study of 35 emerging countries from 2000 to 2019.

The results provided from the approach of a two-step system generalized method of moment (S-GMM) estimator could suggest the following: (i) Regardless of which ICT proxies are included, the impact of ICT diffusion on growth is statistically positive, while financial development negatively affects economic growth. In addition, institutional quality could create a favorable environment to spur economic growth; (ii) There are threshold values of institutional quality and ICT diffusion at which the impact of these variables on growth could change. This implies the U-shaped relation for the nexus between the economic growth and institutional quality and the inverted U-shaped form of ICT diffusion—growth relation; and (iii) The negative impacts of financial development on economic growth could be mitigated by ICT penetration while the negative relation between financial development and economic growth could be amplified under a high level of institutional quality. These results are qualitatively consistent when using a composite index of ICT diffusion through the approach of principal component analysis and remain robust to the inclusion of a time event such as the global financial crisis.

Our research cannot avoid limitations. First, one might argue that the effect of ICT penetration on economic growth in emerging and developing economies may be greater than that of developed economies. Accordingly, ICT could facilitate a “leapfrog” process in emerging countries where conventional approaches to raising production are dominant. However, the emerging markets are our main focus and, therefore, we do not make the comparison between a group of countries with different national incomes. Second, the current research poses an emphasis on the use of squared terms to test the non-linear institutional quality-growth and ICT diffusion-growth relationships. In econometric models, there are other non-linear testing approaches such as panel smooth transition regression (PSTR), which may be used to test the robustness of the results in this study.

This research may identify several further opportunities for future research. First, it is possible that emerging economies have limited absorptive capabilities, such as an adequate amount of human capital or other complementary variables such as R&D expenditures. These factors could be significant drivers of growth, which is excluded in this research due to the issue of an unavailable dataset. Future research can integrate these potential factors to capture a more comprehensive picture of economic growth. Second, based on the theoretical model of economic growth, Pradhan et al. (Citation2016) investigate the causal relationships between ICT infrastructure, FD, and economic growth in Asian countries. The existence of causal links between ICT and FD is not a focus of this research. From this idea, future research could consider this causality to give more understanding relating to determinants of growth and causality among them. Third, the scope of current research is limited to three proxies of ICT diffusion and a composite ICT index from the PCA approach. Due to data availability, we could not use other ICT indicators such as cloud computing, Internet of Things (IoT), fintech, artificial intelligence (AI), social media, 5G, and e-commerce suggested by the work of Vu et al. (Citation2020). This may be a good point to start the next research in the near future.

In terms of policy recommendations, in addition to the emphasis on financial development, which has a negative impact on growth, the findings suggest that authorities in emerging countries should increase investments in ICT infrastructure in order to benefit from the joint effect of financial development and ICT diffusion on stimulating economic growth. Hence, strengthening and enhancing ICT applications in the financial sector can help reduce the negative effects of financial development on an economy, which is particularly beneficial for emerging economies. However, there is a weak point that needs to be addressed by policy-makers: there is hardly a favorable effect of ICT penetration on growth because of a certain threshold at which over-developed ICT diffusion may exert a negative influence on growth. In addition, the direct influence of institutional quality on growth indicates that emerging countries must strengthen their institutions. However, the indirect influence of institutional quality on growth through the interaction with financial development is significantly negative, necessitating a cautious growth strategy that accounts for the interaction between financial development and institutional quality. This might be because, under a certain threshold level of institutional quality, economic growth is hampered and the negative effect of financial development may be amplified due to this level of institutional quality. This study might be crucial to the government’s formulation of its financial sector, with a greater emphasis on ICT penetration and institutional quality to support its economic growth objective.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

This research is funded by the University of Economics Ho Chi Minh City (UEH). The first author is grateful for financial support from Van Lang University (VLU). We also appreciate valuable comments and suggestions from anonymous reviewers of the journal to greatly improve our research We are responsible for any remaining errors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abdelbary, I., & Benhin, J. (2019). Governance, capital and economic growth in the Arab Region. The Quarterly Review of Economics and Finance, 73, 184–33. https://doi.org/10.1016/j.qref.2018.04.007

- Abubakar, S. (2020). Institutional quality and economic growth: Evidence from Nigeria. African Journal of Economic Review, 8(1), 48–64.

- Acheampong, A. O., Boateng, E., Amponsah, M., & Dzator, J. (2021). Revisiting the economic growth–energy consumption nexus: Does globalization matter? Energy Economics, 102, 105472.

- Achia, T. N., Wangombe, A., & Khadioli, N. (2010). A logistic regression model to identify key determinants of poverty using demographic and health survey data.

- Alimi, A. S., & Adediran, I. A. (2020). ICT diffusion and the finance–growth nexus: A panel analysis on ECOWAS countries. Future Business Journal, 6(1), 1–10.

- Appiah-Otoo, I., & Song, N. (2021). The impact of ICT on economic growth-Comparing rich and poor countries. Telecommunications Policy, 45(2), 102082.

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

- Asongu, S. A., & Acha-Anyi, P. N. (2017). ICT, conflicts in financial intermediation and financial access: Evidence of synergy and threshold effects. NETNOMICS: Economic Research and Electronic Networking, 18(2), 131–168.

- Asongu, S. A., & Odhiambo, N. M. (2019). Mobile banking usage, quality of growth, inequality and poverty in developing countries. Information Development, 35(2), 303–318.

- Asteriou, D., & Spanos, K. (2019). The relationship between financial development and economic growth during the recent crisis: Evidence from the EU. Finance Research Letters, 28, 238–245.

- Barro, R. J. (1996). “Determinants of economic growth: A cross-country empirical study”. National Bureau of Economic Research Cambridge.

- Beck, T., Chen, T., Lin, C., & Song, F. M. (2016). Financial innovation: The bright and the dark sides. Journal of Banking & Finance, 72, 28–51.

- Bencivenga, V. R., & Smith, B. D. (1991). Financial intermediation and endogenous growth. The Review of Economic Studies, 58(2), 195–209.

- Bittencourt, M., Van Eyden, R., & Seleteng, M. (2015). Inflation and Economic Growth: Evidence from the S outhern A frican D evelopment C ommunity. South African Journal of Economics, 83(3), 411–424.

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

- Butkiewicz, J. L., & Yanikkaya, H. (2006). Institutional quality and economic growth: Maintenance of the rule of law or democratic institutions, or both? Economic Modelling, 23(4), 648–661.

- Cheng, C.-Y., Chien, M.-S., & Lee, -C.-C. (2021). ICT diffusion, financial development, and economic growth: An international cross-country analysis. Economic Modelling, 94, 662–671.

- Chien, M.-S., Cheng, C.-Y., & Kurniawati, M. A. (2020). The non-linear relationship between ICT diffusion and financial development. Telecommunications Policy, 44(9), 102023.

- Cobb, C. W., & Douglas, P. H. (1928). A theory of production.

- Daniela-Neonila, M., & Roxana-Manuela, D. (2014). The emerging economies classification in terms of their defining, grouping criteria and acronyms used for this purpose. Management Strategies Journal, 26(4), 311–319.

- Das, A., Chowdhury, M., & Seaborn, S. (2018). ICT diffusion, financial development and economic growth: New evidence from low and lower middle-income countries. Journal of the Knowledge Economy, 9(3), 928–947.

- Del Gaudio, B. L., Porzio, C., Sampagnaro, G., & Verdoliva, V. (2021). How do mobile, internet and ICT diffusion affect the banking industry? An empirical analysis. European Management Journal, 39(3), 327–332.

- Demetriades, P., & Hook Law, S. (2006). Finance, institutions and economic development. International Journal of Finance & Economics, 11(3), 245–260.

- Dewan, S., & Kraemer, K. L. (2000). Information technology and productivity: Evidence from country-level data. Management Science, 46(4), 548–562.

- Dluhopolskyi, O., Koziuk, V., Ivashuk, Y., & Klapkiv, Y. (2019). Environmental welfare: Quality of policy vs. society’s values. Problemy Ekorozwoju, 14(1).

- Dollar, D., & Kraay, A. (2000), “Property rights, political rights, and the development of poor countries in the post-colonial period”, World Bank Working Papers.

- Effiong, E. (2015). Financial development, institutions and economic growth: Evidence from Sub-Saharan Africa.

- Eriṣ, M. N., & Ulaṣan, B. (2013). Trade openness and economic growth: Bayesian model averaging estimate of cross-country growth regressions. Economic Modelling, 33, 867–883.

- Fernández, A., & Tamayo, C. E. (2017). From institutions to financial development and growth: What are the links? Journal of Economic Surveys, 31(1), 17–57.

- Glawe, L., & Wagner, H. (2019), “The role of institutional quality for economic growth in Europe”, Available at SSRN 3375215.

- Grace, J., Kenny, C., & Qiang, C. Z.-W. (2004). Information and communication technologies and broad-based development: Partial review of the evidence.

- Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of Political Economy, 98(5, Part 1), 1076–1107.

- Gries, T., Kraft, M., & Meierrieks, D. (2009). Linkages between financial deepening, trade openness, and economic development: Causality evidence from Sub-Saharan Africa. World Development, 37(12), 1849–1860.

- Gupta, S., Clements, B., Baldacci, E., & Mulas-Granados, C. (2005). Fiscal policy, expenditure composition, and growth in low-income countries. Journal of International Money and Finance, 24(3), 441–463.

- Gurley, J. G., & Shaw, E. S. (1960). Money in a theory of finance.

- Gygli, S., Haelg, F., Potrafke, N., & Sturm, J.-E. (2019). The KOF globalisation index–revisited. The Review of International Organizations, 14(3), 543–574.

- Hasbi, M., & Dubus, A. (2020). Determinants of mobile broadband use in developing economies: Evidence from Sub-Saharan Africa. Telecommunications Policy, 44(5), 101944.

- Hassan, M. (2005), “FDI, information technology and economic growth in the Mena region. 10th ERF paper”, in Economic Research Forum.

- Hassan, M. K., Sanchez, B., & Yu, J.-S. (2011). Financial development and economic growth: New evidence from panel data. The Quarterly Review of Economics and Finance, 51(1), 88–104.

- Hayat, A. (2016). Foreign direct investment, institutional framework and economic growth.

- Helgason, M. (2010). Institutional quality and economic growth-A comparison across development stages.

- Herrera-Echeverri, H., Haar, J., & Estévez-Bretón, J. B. (2014). Foreign direct investment, institutional quality, economic freedom and entrepreneurship in emerging markets. Journal of Business Research, 67(9), 1921–1932.

- Hondroyiannis, G., Lolos, S., & Papapetrou, E. (2005). Financial markets and economic growth in Greece, 1986–1999. Journal of International Financial Markets, Institutions and Money, 15(2), 173–188.

- Huan, N. H. (2021). Market structure, state ownership and monetary policy transmission through bank lending channel: Evidence from Vietnamese commercial banks. 739898418.

- Iheonu, C., Ihedimma, G., & Onwuanaku, C. (2017). Institutional quality and economic performance in West Africa.

- Ishida, H. (2015). The effect of ICT development on economic growth and energy consumption in Japan. Telematics and Informatics, 32(1), 79–88.

- Jahanger, A., Usman, M., & Ahmad, P. (2022). A step towards sustainable path: The effect of globalization on China’s carbon productivity from panel threshold approach. Environmental Science and Pollution Research, 29(6), 8353–8368.

- Keller, W. (1996). Absorptive capacity: On the creation and acquisition of technology in development. Journal of Development Economics, 49(1), 199–227.

- Khan, H., Khan, S., & Zuojun, F. (2020). Institutional quality and financial development: Evidence from developing and emerging economies. Global Business Review. 0972150919892366

- King, B. (2012). Bank 3.0: Why banking is no longer somewhere you go but something you do. John Wiley & Sons.

- Knack, S., & Keefer, P. (1995). Institutions and economic performance: Cross‐country tests using alternative institutional measures. Economics & Politics, 7(3), 207–227.

- Law, S. H., Azman-Saini, W. N. W., & Ibrahim, M. H. (2013). Institutional quality thresholds and the finance – Growth nexus. Journal of Banking & Finance, 37(12), 5373–5381.

- Law, S. H., Kutan, A. M., & Naseem, N. (2018). The role of institutions in finance curse: Evidence from international data. Journal of Comparative Economics, 46(1), 174–191.

- Levine, R. (2005). Chapter 12 Finance and growth: Theory and evidence. Handbook of Economic Growth, 1(Part A), 865–934.

- Levine, R., & Zervos, S. (1998). Stock markets, banks, and economic growth. American economic review. 537–558

- Malefane, M. R., & Odhiambo, N. M. (2021). Trade openness and economic growth: Empirical evidence from Lesotho. Global Business Review, 22(5), 1103–1119.

- Navaretti, G. B., Calzolari, G., Mansilla-Fernandez, J. M., & Pozzolo, A. F. (2018), “Fintech and banking. Friends or foes?”, Friends or Foes.

- Nawaz, S., Iqbal, N., & Khan, M. A. (2014). The impact of institutional quality on economic growth: Panel evidence. The Pakistan Development Review. 15–31

- Nguyen, C. P., Su, T. D., & Nguyen, T. V. H. (2018). Institutional quality and economic growth: The case of emerging economies. Theoretical Economics Letters, 8(11).

- Nguyen, H. H., Nguyen, T. P., & Tram Tran, A. N. (2022a). Impacts of monetary policy transmission on bank performance and risk in the Vietnamese market: Does the Covid-19 pandemic matter? Cogent Business & Management, 9(1), 2094591.

- Nguyen, T. P., & Dinh, T. T. H. (2022). The role of bank capital on the bank lending channel of monetary policy transmission: An application of marginal analysis approach. Cogent Economics & Finance, 10(1), 2035044.

- Nguyen, T. P., Dinh, T. T. H., Tran Ngoc, T., & Duong Thi Thuy, T. (2022b). Impact of ICT diffusion on the interaction of growth and its volatility: Evidence from cross-country analysis. Cogent Business & Management, 9(1), 2054530.

- Niebel, T. (2018). ICT and economic growth–Comparing developing, emerging and developed countries. World Development, 104, 197–211.

- Nijskens, R., & Wagner, W. (2011). Credit risk transfer activities and systemic risk: How banks became less risky individually but posed greater risks to the financial system at the same time. Journal of Banking & Finance, 35(6), 1391–1398.

- North, D. (1990). “Institutions institutional change and economic performance. UK.

- North, D. C. (1991). Institutions. Journal of Economic Perspectives, 5(1), 97–112.

- Ofori, I. K., & Asongu, S. A. (2021). ICT diffusion, foreign direct investment and inclusive growth in Sub-Saharan Africa. Telematics and Informatics, 65, 101718.

- Olofin, O. P. (2012). Defense spending and poverty reduction in Nigeria. American Journal of Economics, 2(6), 122–127.

- Owoeye, T., Idowu, O. O., & Ogunsola, A. J. (2022). Does ICT diffusion drive the finance-growth nexus? evidence from sub-saharan Africa. In Corporate finance and financial development (pp. 37–53). Springer.

- Parks, B., Buntaine, M., & Buch, B. (2017). Why developing countries get stuck with weak institutions and how foreign actors can help. In The.

- Phan, T. N. T., Bertrand, P., Phan, H. H., & Vo, X. V. (2021). The role of investor behavior in emerging stock markets: Evidence from Vietnam. The Quarterly Review of Economics and Finance.

- Pohjola, M. (2000). Information technology and economic growth: A cross-country analysis.

- Pradhan, R. P., Arvin, M. B., & Hall, J. H. (2016). Economic growth, development of telecommunications infrastructure, and financial development in Asia, 1991–2012. The Quarterly Review of Economics and Finance, 59, 25–38.

- Pradhan, R. P., Arvin, M. B., Hall, J. H., & Bahmani, S. (2014). Causal nexus between economic growth, banking sector development, stock market development, and other macroeconomic variables: The case of ASEAN countries. Review of Financial Economics, 23(4), 155–173.

- Radu, M. (2015). The impact of political determinants on economic growth in CEE countries. Procedia-Social and Behavioral Sciences, 197, 1990–1996.

- Rahman, M. M., & Alam, K. (2021). Exploring the driving factors of economic growth in the world’s largest economies. Heliyon, 7(5), e07109.

- Ram, R. (1986). Government size and economic growth: A new framework and some evidence from cross-section and time-series data. The American Economic Review, 76(1), 191–203.

- Ram, R. (1999). Financial development and economic growth: additional evidence.

- Rodrik, D. (2000). Institutions for high-quality growth: What they are and how to acquire them. Studies in Comparative International Development, 35(3), 3–31.

- Rousseau, P. L., & Wachtel, P. (2000). Equity markets and growth: Cross-country evidence on timing and outcomes, 1980–1995. Journal of Banking & Finance, 24(12), 1933–1957.

- Samargandi, N., Fidrmuc, J., & Ghosh, S. (2015). Is the relationship between financial development and economic growth monotonic? Evidence from a sample of middle-income countries. World Development, 68, 66–81.

- Sassi, S., & Goaied, M. (2013). Financial development, ICT diffusion and economic growth: Lessons from MENA region. Telecommunications Policy, 37(4–5), 252–261.

- Schumpeter, J. (1981). “Theory of Economic Development (Social Science Classics Series)”. Transaction Publishers.

- Shamim, F. (2007). The ICT environment, financial sector and economic growth: A cross‐country analysis. Journal of Economic Studies.

- Sohag, K., Shams, S. R., Omar, N., & Chandrarin, G. (2019). Comparative study on finance‐growth nexus in Malaysia and Indonesia: role of institutional quality. Strategic Change, 28(5), 387–398.

- Solow, R. M. (1956). A contribution to the theory of economic growth. The Quarterly Journal of Economics, 70(1), 65–94.

- Stanley, T. D., Doucouliagos, H., & Steel, P. (2018). Does ICT generate economic growth? A meta‐regression analysis. Journal of Economic Surveys, 32(3), 705–726.

- Steinmueller, W. E. (1996). Work for all or mass unemployment? Computerised technical change into the twenty-first century. Journal of Economic Literature, 34(1), 137.

- Steinmueller, W. E. (2001). ICTs and the possibilities for leapfrogging by developing countries. Int’l Lab. Rev, 140, 193.

- Swan, T. W. (1956). Economic growth and capital accumulation. Economic Record, 32(2), 334–361.

- Uddin, G. S., Sjö, B., & Shahbaz, M. (2013). The causal nexus between financial development and economic growth in Kenya. Economic Modelling, 35, 701–707.

- Utile, T. I., Ijirshar, V. U., & Adoo, S. (2021). Impact of Institutional Quality on Economic Growth in Nigeria. Gusau International Journal of Management and Social Sciences, 4(3), 21–28.

- Vu, K., Hanafizadeh, P., & Bohlin, E. (2020). ICT as a driver of economic growth: A survey of the literature and directions for future research. Telecommunications Policy, 44(2), 101922.

- Vu, K. M. (2011). ICT as a source of economic growth in the information age: Empirical evidence from the 1996–2005 period. Telecommunications Policy, 35(4), 357–372.

- Wahidin, D., Akimov, A., & Roca, E. (2021). The impact of bond market development on economic growth before and after the global financial crisis: Evidence from developed and developing countries. International Review of Financial Analysis, 101865.

- Yıldırım, A., & Gökalp, M. F. (2016). Institutions and economic performance: A review on the developing countries. Procedia Economics and Finance, 38, 347–359.

- Yong, H. H. A., Faff, R., & Chalmers, K. (2009). Derivative activities and Asia-Pacific banks’ interest rate and exchange rate exposures. Journal of International Financial Markets, Institutions and Money, 19(1), 16–32.

Appendix A:

Countries list.

Table A1. List of 35 emerging countries

Appendix B:

Correlation matrix.

Table B1. Correlation matrix among variables