?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Taxes have extraordinary roles in any country’s economic development and policymaking. This study extends prior studies by investigating the impact of direct and indirect taxes on the economic development of 47 developed and 90 developing countries. All data about the variables involved in the study are accessed from the World Bank, covering from 2000 to 2020. Three equation models are developed to examine the impacts of tax structures on economic growth, which are gross domestic product per capita (GDPPC), foreign direct investment (FDI), and unemployment (UE). The study employed fixed effects (FE) and random effects (RE) of Generalized Least Square regression in testing the relationship between taxes structure (direct and indirect) and economic development (GDPPC, FDI, and UE). In addition, the cross-sectional dependence (CD) test is used to identify the presence of spatial dependence for FE and RE estimators. Overall, direct and indirect taxes have a significant negative relationship with economic development based on the GDPPC of developing countries. These results indicated that the tax structure in developing countries does not enhance the countries’ economic growth. By contrast, for developed countries, a significant positive relationship exists between direct taxes and economic development. Economics and Development; Economics; Public Finance

PUBLIC INTEREST STATEMENT

Taxes generate public revenues to finance investments in human capital and infrastructure and provide services for citizens and businesses. This study investigates the impact of taxes on economic development, covering the gross domestic product per capita (GDPPC), foreign direct investment (FDI), and unemployment (UE). The findings provide evidence that direct tax positively affects the economic development of developed countries but negatively affects the economic development of developing countries. Hence, the policymakers of developing countries are recommended to revisit the tax structures if they want to enhance the positive impact of taxes on their countries’ economic development. In doing so, the policymakers would be able to identify the best type of taxes that will be able to generate high revenues for the country to provide the best infrastructure and services to the citizens and businesses.

1. Introduction

The endorsement of the Sustainable Development Goals (SDG) by worldwide partnerships has sparked a slew of economic development studies. Eradicating poverty requires efforts to enhance health and education, reduce inequality, and spur economic growth, while also combating climate change and protecting seas and forests. Thus, the United Nations has identified 17 development objectives that must be met by 2030. The eighth goal is to ensure long-term, inclusive, and sustainable economic growth, including full and productive employment for all people. Sustainable economic growth and full employment are essential to achieve the aim. In the least developed countries, at least 7% gross domestic product (GDP) growth per year, including full and productive employment, can be realized by 2030. However, in 2020, COVID-19 has caused a global recession and a dramatic increase in unemployment contributing to a global drop in SDG performance, including Organisation for Economic Co-operation and Development (OECD) countries (Sachs et al., Citation2021).

Economic development can be broadly defined as the structural transformation of an economy through the introduction of more mechanized and updated technology to enhance labor productivity, employment, income, and the population’s standard of living. Various measurements of economic development have emerged as a result of the ambiguity of specific definitions of economic development, such as structural changes in GDP, per capita income, full employment, normative values, improvement in human status, physical quality of life index, human development index, poverty index, and sustainable development (Panth, Citation2020).

As measured by increases in GDP, economic growth is an enabler of economic development, according to the concept and measurements of economic development. GDP is comprised of various components, such as consumption, investment, government spending, and net export. Furthermore, increased investment adds to the advancement of technology and employment rate. The performance of developed and developing countries in terms of economic development demonstrates considerable variances throughout time. According to the World Bank (data.worldbank.org), low and middle-income countries performed better than high-income countries in terms of GDP per capita growth between 1991 and 2020, despite economic downturns, such as the financial crisis in 2009 and the COVID-19 pandemic in 2020. Hence, developing countries have higher economic development in comparison to developed countries.

Studies concerning the elements that drive economic development are popular among scholars. Taxes are among the most studied variables because they drive a country’s economic policy (Shahmoradi et al., Citation2019). Taxes are commonly categorized into two main types: direct and indirect. Direct taxes are taxes levied on income and activities done by taxpayers and paid directly to the government. The direct tax burden cannot be passed to another party. From another aspect, indirect taxes are levied on products and services, and the tax burden can be shifted to another party. A prior study showed that taxes on international trade (TRADET) account for a larger share of revenue than direct taxes in developing countries (Thaçi & Gerxhaliu, Citation2018). Therefore, developing countries face significant challenges in developing their tax systems and mobilizing domestic resources than to developed countries. In contrast, direct tax such as consumption, social insurance, and income taxes bring greater revenue for industrialized countries.

The past literature documented conflicting findings on the impact of taxes on economic growth. Taxes on domestic goods and services, including tariffs, have boost GDP growth in developed and developing countries (Maganya, Citation2020; Mdanat et al., Citation2018; Vintilă et al., Citation2021). However, according to Thaçi and Gerxhaliu (Citation2018), taxes and economic growth in developing nations have a negative relationship. In addition, tax on income is significantly and inversely related to GDP in developed countries but insignificant in developing countries (Shahmoradi et al., Citation2019). These conflicting results require further investigation to understand the impact of taxes on economic development in developed and developing countries.

In terms of tax category, research showed that direct taxes have a favorable impact on economic growth, but conclusions on the impact of indirect taxes are contradictory (Hakim, Citation2020; Korkmaz et al., Citation2019). Indirect taxes have a favorable impact on economic growth, according to a study conducted in developing countries. From another aspect, direct taxation has an intangible effect (Nguyen, Citation2019). Bringing two different taxes structures: direct and indirect taxes, in one study, would provide additional evidence to support or reject the contradiction finding of prior studies.

Other indicators of economic development include investment and employment. For investment, the literature documented inconsistent findings about how taxes affect investment. Several studies found that taxes have an impact on investment in developed and developing countries (Abdioglu et al., Citation2016; Ajetunmobi et al., Citation2019; Mohs et al., Citation2018; Shafiq et al., Citation2021). However, other research found mixed results for distinct groupings of countries (Goodspeed et al., Citation2011; Mercer-Blackman & Camingue-Romance, Citation2020). Furthermore, the types of taxes can also influence their impact on investment (Appiah-Kubi et al., Citation2021).

In addition, the literature has shown that taxes considerably impact the unemployment rate, even though research on this topic is somewhat limited (Disney, Citation2000; Nikolka, Citation2016; Seward, Citation2008). Using single-country data, Tagkalakis (Citation2013) found a positive and strong association between taxes and employment in Greece. Thus, investment and employment can also be good indicators of whether the tax structures introduced in a particular country can initiate positive economic development. Including these two economic indicators in the study would add knowledge to the existing literature.

This study differs from past research in terms of two aspects. First, the study investigates the impact of direct and indirect taxes on economic development in developed and developing countries using recent 2000–2020 data. Data on the year 2020 may produce interesting results to see the impact of the Covid-19 pandemic on economic development. Second, in addition, to GDP per capita growth, the study also includes foreign direct investment (FDI) and unemployment (UE) to measure economic development. In addition, the study employed fixed effect (FE) and random effect (RE) of Generalized Least Square regression in testing between tax structures and economic development.

The rest of this paper is organized as follows. Sections 2 and 3 present the literature review and the research method, respectively. Then, Section 4 provides the analysis of the key results, discussion, and robustness checks in detail. Finally, Section 5 provides some limitations and concludes the study.

2. Literature review and theory

2.1. Theory related to taxes and economic growth

Economic growth is linked to taxation through economic agents’ decision, which is influenced by the changes in tax (Myles, Citation2009). Taxation generates revenue for the government, controls economic activity, and promotes economic growth. (Minh Ha et al., Citation2022). However, the higher tax will limit individual taxpayers’ contribution to economic growth. The same applies to corporate taxpayers, as higher taxes might restrict their ability to produce more products in the market. From the government’s perspective, the higher tax will allow them to invest in education, health, basic info structure, or even infrastructural improvements. These investments will increase the economy’s productivity in the future.

The neoclassical growth theory stipulates that capital accumulation and labor are the main drivers of growth in the long run. According to Solow Growth Model (Solow, Citation1956), economic growth is influenced by the changes in the population growth rate, the savings rate, and the rate of technological progress. In addition, long-term growth is driven by exogenous factors, whereas government policy can have only a transitory effect on growth. The economic model is extended to accommodate the influence of personal income tax on saving rate, where the tax effect depends on whether the tax proceeds are directly consumed or involve investment. Hence, if all revenues are used to create new capital, the saving-investment identity is portrayed as follows:

where is capital stock, Y is the production, s is the saving rate and t is the tax rate.

The researched model was widened and enhanced by Barro (Citation1991) and Jones et al. (Citation1993) into endogenous growth models, which examined the economic effects of tax composition. For example, the endogenous growth model of Mendoza et al. (Citation1997) considers the effect of the economic growth of the marginal tax rate on human and physical capital and consumption. The model predicted that consumption taxes affect the “net after-tax return on physical capital” (Mendoza et al., Citation1997, p. 104) only indirectly via the labor–leisure choice. This case, in turn, impacts the capital-to-labor ratio employed in production. In addition, Arnold et al. (Citation2011) noted that value-added tax (VAT) also affects the labor–leisure choice as consumer goods become more expensive. This event can impact the labor supply as the reward for working is lower. The economic theory suggests that all taxes influence the economic growth rate. However, personal and corporate income taxes would do more than consumption taxes.

2.2. Empirical studies on taxes and economic development in developing and developed countries

Fiscal policies can affect economic growth and economic development. Policies such as increasing public spending on healthcare and education or reducing tax rates can positively influence the stock of human capital and support economic growth in the short term and economic development in the long term. Many scholars and researchers are interested in analyzing the relationship between fiscal policy and economic growth in developing and developed countries. The interest sparked because of the necessity to stimulate the rate of economic growth and to reduce the budget deficits because of inefficient government spending. Arnold et al. (Citation2011) argued that fiscal policy needs to be adjusted to reduce poverty and inequalities for the welfare of society.

Taxation, the main element of fiscal policy, undoubtedly affects household income and economic output. When the level of taxation is high, the taxpayer’s ability to work decreases considerably. In addition, people may become uncertain about working more because, by increasing taxation, their income would be significantly reduced. From another aspect, an increased level of taxation negatively affects income distribution and indirectly alters the productive capacity. In certain circumstances, taxation may affect the allocation of production and the population’s income. Eventually, this case leads to significant consequences on social welfare. Thus, governments should consider the economic and social impact of taxation, particularly when increasing taxation will cause taxpayers to work harder to maintain a balanced of their income levels. Instead of increasing their income, this event will worsen their financial situation.

Past literature has documented conflicting findings on the impact of taxation towards economic development in developed and developing countries. Research about taxes and economic growth in developing countries is enormous but concentrated to Africa and Middle East. In South Africa, Ocran (Citation2011) examined the effect of fiscal policy variables, including government gross fixed capital formation (GFCF), tax and government consumption expenditure, and budget deficit on economic growth from 1990 to 2004. He used quarterly data in the estimation with the aid of the vector regressive modeling technique and impulse response functions. The findings indicated that government consumption expenditure, GFCF from the government, and tax receipts positively affect output growth. Similarly, Eugene and Abigail (Citation2016) studied the impact of taxation policies on the overall economic growth from 1994 to 2013 using the OLS method. The results confirmed the positive impact of a tax on Nigerian economic growth. Babatunde et al. (Citation2017) investigated the impact of taxation on economic growth from 2004 to 2013 in 16 African states using the panel data. They found a significant and positive relationship between tax revenues and GDP, which suggests that tax revenues accelerate the economic growth of African states.

In Nigeria, Ojong et al. (Citation2016) examined the impact of tax revenue on the Nigerian economy from 1986 to 2010. They examined the impact of company income tax and the effectiveness of non-oil revenue on the Nigerian economy. Ordinary least square (OLS) of multiple regression models were used to test the relationship between dependent and independent variables. Their finding reveals a significant relationship between petroleum profit tax and the growth of the Nigerian economy. However, no significant relationship is found between company income tax and the growth of the Nigerian economy.

A number of studies in developing countries have found, however, that taxes do not significantly affect economic growth. In Zimbabwe, Canicio and Zachary (Citation2014) investigated the effects of government tax revenue growth on economic growth from 1980 to 2012. They found an independent relationship between economic growth and total government tax revenue with a 30% speed of adjustment in the short run toward the equilibrium level in the long run. This finding implies that fiscal independence exists between tax revenue and growth.

Meanwhile, in Pakistan, Ahmad and Sial (Citation2016) examined the relationship between total tax revenues and economic growth using annual time series data from 1974 to 2010. The autoregressive distributed lag (ARDL) bounds testing approach for co-integration was applied to estimate the long-run and short-run relationship among the variables. The results show that total tax revenues have a negative and significant effect on economic growth in the long run. The finding suggests that a 1% upsurge in total taxes would reduce the economic growth by 1.25%. In their research on developing countries, (Thaçi & Gerxhaliu, Citation2018) provided evidence in favour of the adverse association between taxes and economic growth. Similarly, (Shahmoradi et al., Citation2019) concluded that there is a significant and negative relationship between the ratio of tax revenues and Gross Domestic Product in developed countries.

In Romania and Turkey, Göndör and Özpençe (Citation2014) conducted an empirical study on fiscal policy during the crises time. Providing some empirical basis for the argument, they revealed that the pro-cyclical fiscal policy does not assist in dampening the GDP shocks. The finding must be interpreted carefully because the study focuses on the cyclical dynamics of macroeconomic aggregates. Thus, the result only offers conjectures as to the reasons behind the behavior of fiscal policy and its influence on macroeconomic output. Korkmaz et al. (Citation2019), observed similar findings in their research of the Turkish economy where taxes are significantly and negatively associated with economic growth.

Widmalm (Citation2001) found a negative relationship between direct income taxes and economic growth. However, the adverse effects of indirect taxes on economic growth are not confirmed. The finding is later supported by the latest study in Tanzania (Maganya, Citation2020) and Jordan (Mdanat et al., Citation2018). Mdanat et al. (Citation2018) analyzed the Jordan tax structure and its implications on economic growth between 1980 and 2015 by using error correction techniques. Their study provided empirical evidence, which entails that direct and indirect tax structure is insufficient to help improve the economic growth of Jordan, particularly when the country faces poor fiscal performance. In addition, Jordan has an inefficient fiscal structure that should determine politicians within their politics to focus more on increasing the GDP per capita by addressing the importance of consumption taxes and customs duties. They believed that sustainable economic growth could only be achieved if poverty and inequalities are to be reduced and living conditions are to be improved.

For evidence from the selective Islamic countries, Asghari and Mohseni Zenouzi (Citation2013) investigated the effect of taxes and government consumption expenditure on the economic growth of the Middle East and North Africa regions from 1995 to 2011, using the panel smooth transition regression model. The results indicate that taxes and government consumption expenditure negatively affect economic growth; as the threshold of GDP for government consumption expenditure and taxes increases, the positive effects of investment and export revenues on economic growth decrease.

Research in developed countries also produces mixed findings. Poulson and Kaplan (Citation2008) explored the impact of tax policy on economic growth in the US within the framework of an endogenous growth model. They conducted the regression analysis to estimate the impact of taxes on economic growth from 1964 to 2004. The analysis showed a significant negative impact of higher marginal tax rates on economic growth. This evidence suggests that taxes can significantly impact economic growth. The government has a choice of directFootnote1 and indirectFootnote2 taxes to determine the efficiency of the allocation of resources, either through tax revenue or improvement of economic growth.

Numerous factors can also have an impact on economic growth. From the European Union countries, Armeanu et al. (Citation2018) conducted an empirical study on the sustainability factors of economic growth rate in the EU-28 member countries by using data panel regression models and by applying fixed and RE and the generalized method of moments. They include sustainability factors, such as the high level of education, the economic and business environment of a country, technology, infrastructure, communications, people’s lifestyle, media, and demographic changes in measuring the real growth rate of the GDP. They highlighted a positive connection between the economic growth and the level of the expenses for the education of the students between the ages of 18 and 26 years and the expenses for the research and development and the degree of employment of the fresh graduates. They also found that the indicator regarding the perception of corruption is negatively associated with economic development.

Research that makes a comparison between developed and developing countries using panel data also found conflicting results. In 2005, Lee and Gordon (Citation2005) found a significant negative relationship between statutory corporate tax rates and economic growth. Arnold (Citation2008) and Vartia (Citation2008) supported this finding—the negative effect of corporate taxes on growth. Their studies indicated a negative relationship between corporate taxes and the productivity of companies, which can be related to the economic growth across OECD countries. Additionally, Indirect taxes have a positive link with economic growth in selected developed and developing countries, according to Hakim (Citation2020). Similar to this, studies conducted in developing economies have shown that indirect taxes have a favorable impact on economic growth (Korkmaz et al., Citation2019; Nguyen, Citation2019). Tariffs and domestic goods and services taxes are two additional tax forms that have a direct impact on the economic growth of countries (Maganya, Citation2020; Mdanat et al., Citation2018).

It is undeniable how taxes affect other aspects of the economy, like investment and unemployment. Numerous research has produced contradictory results regarding how taxes affect investment. Taxes have a significant impact on investment, according to studies by Abdioglu et al. (Citation2016), Ajetunmobi et al. (Citation2019), Mohs et al. (Citation2018), Shafiq et al. (Citation2021), and Goodspeed et al. (Citation2011) proved that FDI in developed nations is responsive to host country taxation, but not in developing countries. The conflicting findings are backed by Mercer-Blackman and Camingue-Romance (Citation2020) study. Although research on the impact of taxes on unemployment is somehow limited, the existing literature revealed that taxes significantly impact the unemployment rate. In developed nations, the unemployment rate rises when the tax rate on labour is high, according to studies by Disney (Citation2000) and Seward (Citation2008). Similarly, Nikolka’s (Citation2016) report on taxes and the female labor force supports the claim.

The discussion in the above literature review identifies several gaps. There seem to be inconclusive results of the impact of taxes on economic growth, either in developed or developing countries. Next, this study does not only examine the impact of direct and indirect taxes on GDP but also on other indicators of economic development, namely unemployment and investment, which limited study has done so. This study covers more countries and more recent data years than to previous studies. It also includes the year 2020 data, the year Covid-19 pandemic. Including the year 2020 data may produce interesting results compared to prior studies.

3. Empirical model, methodology, and the data

3.1. Empirical model

The empirical model of this study is based on previous studies conducted by Mdanat et al. (Citation2018), Gashi et al. (Citation2018), and Nguyen (Citation2019). These studies examined the impact of tax structure on economic growth. The basic linear panel data growth equation is shown as follows:

where is dependent variable (GDP per capita growth),

is the intercept,

and IDT consist of direct and indirect taxes as the explanatory variables, respectively,

is the error term,

represents the country (

= 1, 2, 3, …, N), and

represents time (

= 1, 2, 3, …, T).

This study aims to investigate the impacts of direct and indirect taxes on economic growth, including other important economic indicators, namely, FDI and UE in developing and developed countries. Thus, the empirical model, as stated in EquationEq. (2(2)

(2) ), can be specified as follows:

Taxes on income, profits, and capital gains (INCOMET), labor tax (LABORT), and other taxes (OTHERT) are included as direct taxes (DT), while indirect taxes (IDT) include taxes on goods and services (GST) and taxes on international trade (TRADET). The control variables are included in each model regression, which is related to the dependent variables and tax structure as similar works by Mdanat et al. (Citation2018) and Mcnabb (Citation2018).

Based on the above equations, including direct and indirect taxes in each model regression can lead to a collinearity problem among explanatory variables. To avoid the collinearity problem in our model, we estimate the relationship between tax structure and economic development by disaggregating direct and indirect taxes. Moreover, the Variance Inflation Factor (VIF) test is applied to confirm that all explanatory variables are free from the multicollinearity problem (Daoud, Citation2017; Shrestha, Citation2020).

3.2. Methodology

Static Panel Fixed Effects (within) and RE GLS Regressions with Driscoll and Kraay Standard Errors

An econometrics study conducted by Hoechle (Citation2007) mentioned the standard errors produced by the OLS, White and Rogers, or clustered standard errors are assumed to be biased and invalid for the presence of heteroscedasticity, autocorrelation, and cross-sectional dependence (CD), which usually occurs in many panel datasets when the subjects are randomly selected. Hence, this study employs both the fixed effects (FE) (within) and RE generalized least square (GLS) regressions with Driscoll and Kraay’s (Citation1998) standard errors to produce a nonparametric covariance matrix estimator. The estimator is believed to generate heteroscedasticity and autocorrelation-consistent standard errors for the presence of CD.

The Hausman test is applied to choose between the FE or RE regressions for each empirical model as suggested by Wooldridge (Citation2002). Following DeHoyos and Sarafidis (Citation2006), a test for CD by Pesaran’s (Citation2004) CD test is adopted to identify the presence of spatial dependence for the FE and RE estimator. Rejecting the null hypothesis of this test indicates that CD is present in the estimation.

3.3. Data

The study sample covers 90 developing and 47 developed countries. We collect data on taxes and economic factors from 2000 to 2020, which is accessible in the World Bank (Databank, World Development Indicators, WDI). The selection of countries (developing and developed) and periods are based on the availability of the data provided by WDI. The list of countries is presented in Appendix Table . The dependent variables consist of three important economic indicators, namely, the annual growth rates of GDP per capita (GDPPC), FDI ratio to GDP (FDI), and unemployment (UE) rates. The economic development is measured by GDPPC, which widely used in most of the panel data tax-growth studies (see, Macek, Citation2015; Mcnabb, Citation2018; Minh Ha et al., Citation2022; Neog & Gaur, Citation2020).

Several macroeconomic variables, namely, gross fixed capital formation (GFCF), trade openness (TRADE), gross national expenditure (EXP), consumption expenditure (CONS), total tax revenue (TAXES), and population growth (POP), are included as the control variables for each of model regression. All these variables are treated as the ratio to GDP except for population growth.

Table shows the summary statistics for the variables used in the analysis. This table is quite revealing in several ways, whereby almost all the standard deviations categorized by developing and developed countries are quite dispersed around the means. These results are quite resilient throughout the cross-sectional data. The mean value of the total tax revenue to GDP ratio for developing countries is reported to be lower (14.69%) than that of developed countries (20.41%). For the case of direct and indirect taxes, developing countries recorded an average value of 39.74% from all three direct taxes (i.e., INCOMET, LABORT, and OTHERT) but a higher percentage for indirect taxes (GST and TRADET), which reported 42.55% of revenue. Despite that, the opposite results are found for developed countries, where the average value of all direct taxes is greater than that of indirect taxes, which recorded 49.09% and 32.78%, respectively.

Table 1. Descriptive statistics in developing vs. developed countries

Table presents the correlation matrix for developing and developed countries. Both groups of countries depicted criteria that are positive and negative correlations (<0.50). The developing countries depict the result of tax revenue as a percentage of GDP (TAXES) has a negative relationship with GDPPC. Meanwhile, TAXES is reported to stimulate GDPPC by approximately 0.05 percentage points in developed countries. INCOMET, LABORT, and GST have a positive relationship with GDPPC in both developing and developed countries. Nonetheless, TRADET are negatively correlated with GDPPC, with correlations of −0.13 and −0.08, respectively. The correlations of all variables of less than 0.80 indicate that the multicollinearity problem is not an issue in this analysis (Field, Citation2005).

Table 2. Correlation matrix for developing countries

3.3.1. Tax and growth trends

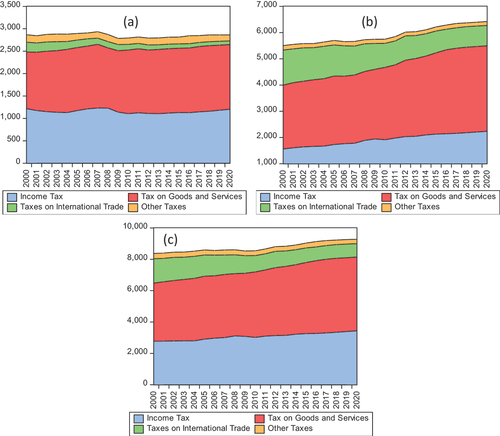

Figure depicts the average tax structure and ratio against income level for developed and developing countries. The tax structure comprises the income tax (including INCOMET), tax on goods and services (including all domestic consumption taxes, such as VAT), TRADET, and OTHERT. Compared with the four income structures, Figure ), representing developed countries, shows that the majority are contributed by the tax on goods and services and income tax, 49.3% and 40.6%, respectively.

Figure 1. Tax structures and ratio by income level; (a) developed; (b) developing; (c) developed and developing countries.

A similar case for developing countries (refer to )) reveals that the tax on goods and services contributes the highest, stated at 47.8%, while 32.5% from income tax. The trend revealed that developed and developing countries heavily rely on the goods and services tax, and income tax. On the one hand, developing countries depict more TRADET, 16.9% of its tax structures, compared to only 4.8% of its tax structures for developed countries. The high amount of TRADET indicates that developing countries initially rely on this type of tax structure (Karia, Citation2021; Mcnabb, Citation2018).

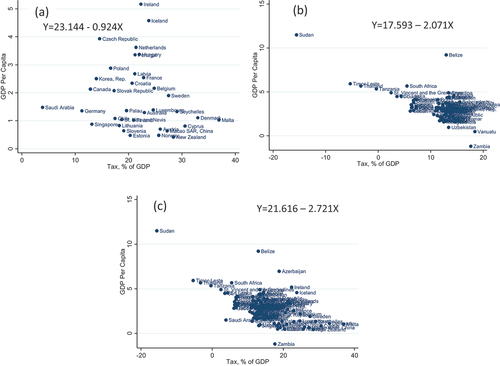

Figure depicts the scatter plots of the average tax as a percentage of GDP against average GDP per capita from 2000 to 2020. This figure is quite revealing in several ways, as developed and developing countries depict the negative relationship between tax and GDP per capita, with some outliers. Developed countries’ average tax ratio of GDP is 21.4%, with the maximum amount from Malta (36.9%) and the minimum amount from Saudi Arabia (3.9%). On the contrary, developing countries’ average tax ratio of GDP is 14.1%, followed by maximum and minimum, 18.4% and 12.9%, respectively. Among all countries, only Sudan, Timor-Leste, Thailand, and Tanzania recorded a negative average tax as a percentage of GDP. Sudan also depicted that its economy has a very low average tax ratio but comes out with a high average GDP per capita of more than 11%. Meanwhile, Malta, Denmark, Cyprus, Seychelles, and New Zealand are among the developed countries with a very high average tax ratio but low average GDP per capita of less than 1.3%. The scatter plots from Figure ) and (b) underline that most developed and developing countries that implement tax ratios at average groups values (21.4% and 14.1%, respectively) will yield higher GDP per capita.

Figure 2. Plots of the average tax as a percentage of GDP against average GDP per capita over 2000–2020, (a) developed; (b) developing; (c) developed and developing countries.

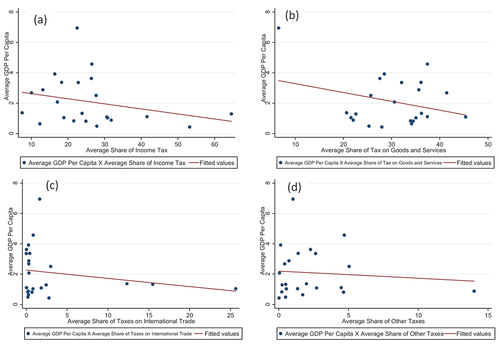

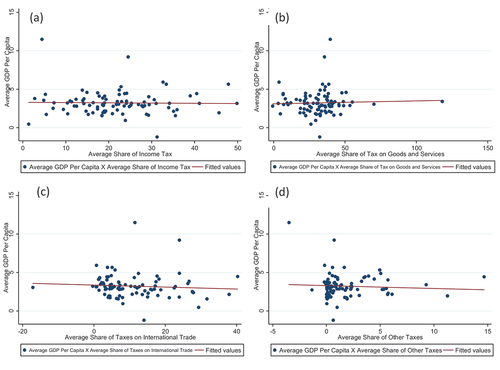

Turning to the GDP per capita and tax structures for developed and developing countries, Figures represent the average share of income tax against the average share of income tax and tax on goods and services, and average share TRADET and OTHERT, respectively. The solid line best fits GDP per capita and selected four tax structures. The average GDP per capita has a modest positive relationship with the selected four tax structures.

Figure 3. Plots of the average GDP per capita against (a) average share of income tax; (b) average share of tax on goods and services; (c) average share of taxes on international trade; (d) average share of other taxes for developed countries.

Figure 4. Plots of the average GDP per capita against (a) average share of income tax; (b) average share of tax on goods and services; (c) average share of taxes on international trade; (d) average share of other taxes, developing country.

4. Results and discussion

Tables present the empirical results of the linear models (EquationEq. (2)(2)

(2) , (Equation3

(3)

(3) ), and (Equation4

(4)

(4) )) using static panel data FE and RE regressions with Driscoll and Kraay (Citation1998) standard errors. The Pesaran CD test indicates that rejecting the null hypothesis of CD is not present in all model regressions. Thus, employing the Driscoll and Kraay (Citation1998) standard errors in all the models proves that the results reported are considered unbiased and suitable for the presence of CD as mentioned by Hoechle (Citation2007). Breusch and Pagan’s LM test shows that all models for developing and developed countries can be pooled by using RE and FE estimations. The results of the Hausman test show that the null hypothesis of RE is the best estimation and is rejected in all model regressions, as reported in Tables . Hence, the FE regression is selected to estimate the models. Meanwhile, as reported in Table , the null hypothesis of the Hausman test is failed to be rejected for the case of Model 2 (developed countries), Model 3 (developing and developed countries), Model 4 (developing and developed countries), and Model 6 (developing countries). This finding provides evidence that the RE regression is the best estimation for these models. The multicollinearity test (VIF) results show a value of less than 5. It indicates that no multicollinearity problem occurs among explanatory variables for all models (Daoud, Citation2017; Shrestha, Citation2020).

Table 3. Results of fixed effects (within) estimations dependent variable: GDP per capita growth (N = 90 developing and 47 developed countries; T = 21; sample period = 2000–2020)

Table 4. Results of fixed effects (within) estimations dependent variable: FDI (net inflows) (N = 90 developing and 47 developed countries; T = 21; sample period = 2000–2020)

Table 5. Results of fixed effects (within) estimations dependent variable: Unemployment (N = 90 developing and 47 developed countries; T = 21; sample period = 2000–2020)

The results generated in this study show that the macroeconomic (control) variables are statistically significant in affecting economic growth, FDI, and UE in developing and developed countries. Trade openness and government expenditure to GDP ratio are positive and highly significant on GDP per capita growth and inflow of FDI, particularly in developing countries. Specifically, the coefficient estimate suggests that for a percentage point increase in both variables, the GDP per capita growth rate and inflow of FDI rise from 0.01 to 0.14 and 0.02 to 1.30 percentage points, respectively. The encouragement of the exchange of ideas and technologies through trade openness makes developing countries able to access superior technologies and enhance economic growth (Murphy et al., Citation1991). Waweru (Citation2021) expressed that productive government expenditure may lead to an input of the private production function in a country. Surprisingly, final consumption expenditure reported strong significance but in the opposite direction for both macroeconomic variables in developing and developed countries. Our results follow Barro (Citation1991) and Mose (Citation2021), who regarded the classical theories that consider consumption expenditure as ineffective because it has brought the crowding-out effect on investment and output growth. Thus, an increase in consumption expenditure will stimulate aggregate demand and higher interest rates in the market, thereby discouraging private investments (crowding-out effect). Another economic variable, namely population growth, shows a negative influence not only on economic growth but also on investment and unemployment.

From the descriptive statistics, Table shows that the mean value of population growth in developing countries is higher (1.46%) than that in developed countries (0.76%). The findings of the current study are consistent with Peterson’s (Citation2017) study about population growth and economic growth. That is, low population and limited migration in high-income countries seem to promote more social and economic problems, whereas higher population growth may slow down the development in low-income countries.

The main interest of this study is to examine the impact of tax structure on economic growth in developing and developed countries. The results presented in Table reveal that the total tax revenue and taxes on income, profit and capital gains have negatively impacted economic growth in developing countries (refer to panel 1- Model 1 & 2 of Table ). This result is not a surprising finding because it is consistent with most of the tax studies on growth who found the exact relationship between taxation and economic growth (Acosta-Ormaechea & Yoo, Citation2012; Mcnabb, Citation2018; Neog & Gaur, Citation2020; Petru-Ovidiu, Citation2015; Schwellnus & Arnold, Citation2008; Widmalm, Citation2001). However, we found a contradicting finding in the case of developed countries, whereby tax revenue and taxes on income, profits, and capital gains show a positive and statistically significant impact on economic growth (refer to Model 1 & 2 of Table ). This result implies that a percentage point increase in these taxes leads to a rise in GDP per capita growth by 0.12 and 0.16 percentage points, respectively. The positive relationship between taxation and economic growth supports several studies conducted in developed and high-income countries (Aghion et al., Citation2016; Mcnabb, Citation2018; Stoilova, Citation2017). Aghion et al. (Citation2016) studied the relationship between taxes and economic growth by including corruption as the main indicator in the United States. They reported a positive and significant impact between taxation and growth in a state with low levels of corruption.

Meanwhile, Stoilova (Citation2017) concluded that the positive and significant impact of tax structure on economic growth was associated with the general directions of development of the fiscal policy, government expenditure, balanced budget, and tax structure, which is believed to be conducive to growth in 28 European nations. Considering the results from the different groups of countries, Mcnabb (Citation2018) pointed out that the tax revenue to GDP ratio has contributed to growth in high-income and upper-middle income countries but has a negative effect on growth in lower-middle-income and low-income countries. Furthermore, labor tax positively influences economic growth in developing and developed countries (refer to Model 3 of Table ). Taxes on labor refer to the amount of taxes and mandatory contributions on labor paid by the business. Therefore, an increase in labor tax is not supposed to discourage the motivation of employees to provide more labor supplies in the market. Rather, it indicates a rise in hiring labors by the business, which leads to promoting higher growth in a country. In general, the effects of labor tax are associated with a 0.09 to 0.10 percentage points increase in per capita growth. From another aspect, this study found a positive and significant relationship between other taxes (including property tax) and per capita growth in developing countries and a negative but insignificant relationship among the variables in developed countries.

GST are negatively correlated to the GDP per capita growth in developing and developed countries. A percentage point increase in goods and services tax reduces growth rates by 0.01 to 0.02 percentage points in developing and developed countries. The results generated are in line with the findings of Ojede and Yamarik (Citation2012), Das (Citation2017), and Neog and Gaur (Citation2020). GST or VAT are part of indirect taxes where most of the countries own tax revenue mostly from this type of taxes. Despite that, GST is influenced positively by the inflationary pressure in the economy and brings a regressive impact on the society’s disposable income. Therefore, we can conclude that society seems to not gain economic benefits by implementing GST or VAT, particularly in developing countries. When excluding direct taxes and GST from the model estimation, we found that taxes on international trade (tariff) have a weak negative effect on economic growth in developing countries. Specifically, the coefficient estimates only a 0.01 percentage points decrease in GDP per capita growth following a percentage point increase in taxes on international trade. Flaaen et al. (Citation2020), who mentioned that tariff had increased the price of products in the markets, which negatively affects purchasing power. By contrast, Handley et al. (Citation2020) revealed that a rise in import tariffs leads to a decrease in export growth through the lens of supply chain linkages, which negatively affects the economic growth.

Apart from investigating tax structures and economic growth, this study also focuses on revealing the effects of taxation on the inflow of FDI and UE in developing and developed countries. Table reports the results of tax structure on the inflow of FDI in developing and developed countries. The regressions results show a strong significant positive relationship between tax revenue to GDP ratio and inflow of FDI in both groups of countries. This finding implies that a percentage point increase in tax revenue raises FDI by 0.03 and 1.37 percentage points, respectively. We found a similar finding in the case of taxes on income, profits, and capital gains in developing countries. The results reveal a strong positive relationship between these taxes and FDI (refer to Model 2 of Table ). Nevertheless, the coefficient estimates a negative but significant relationship among variables in developed countries. This effect signifies that a percentage point increase in taxes on income, profits, and capital gains is expected to reduce FDI by 0.41 percentage points. This finding can be related to Vartia (Citation2008), Assidi et al. (Citation2016), and Belotti et al. (Citation2016), who concluded that corporate and income taxes are negatively correlated with the firm’s investment activities to reduce productivity and the performance of the businesses. Similarly, our model estimates the significant and negative effect of labor tax on FDI in developed countries. The result suggests that a percentage point increase in labor tax is expected to decrease FDI by 0.727 (see Model 3 of Table ). Therefore, labor tax and taxes on income, profits, and capital gains negatively affect the inflow of FDI in developed countries.

Taxes on goods and services also demonstrate a highly significant and negative influence on FDI in developing countries. In this case, the literature did not clearly define the impact of GST on FDI. However, the relationship between GST and FDI could be related to one important determinant, which is the return on investment. We further examine the impact of taxation on unemployment. Table reveals the results of taxation and unemployment in both groups of countries. Mixed results are obtained regarding the impact of tax revenue to GDP ratio on unemployment. As shown in Model 1, the results indicate a highly significant and positive relationship between these two variables in developing countries. By contrast, in the case of developed countries, TAXES has a negative and statistically significant at the 10% level of unemployment. The same findings are generated for the case of taxes on income, profits, and capital gains, which show a positive and significant impact on unemployment in developing countries but a negative but insignificant in developed countries (see Model 2 of Table ).

Conversely, in the case of developing countries, the results reveal that labor tax and other taxes have a statistically significant negative impact on unemployment (see Model 3 & 4 of Table ). The regression outputs indicate a consistent finding between GST and unemployment concerning the impact of indirect taxes on unemployment in both countries. The results in regression Model 5 disclose a significantly negative relationship between GST and unemployment at 10% and 1% levels, respectively. Nevertheless, international trade tax has a positive relationship with unemployment in developing countries and is statistically significant at the 1% level, suggesting that a percentage point increase in international trade leads to a rise the unemployment by 0.11 percentage points.

5. Conclusion

This study used panel data from 47 developed and 90 developing countries from the year 2000 to 2020 to investigate the impact of direct and indirect taxes on the economic development of the developed and developing countries. Direct taxes include taxes on income, profits, and capital gain, labor tax, and other taxes. Indirect taxes are taxes on goods and services and taxes on international trade. Three equation models were developed to examine the impacts of tax structures on economic growth: GDPPC, FDI, and UE. The study employed FE and RE of Generalized Least Square regression in testing the relationship between taxes structure (direct and indirect) and economic development (GDPPC, FDI, and UE).

This study concludes that the influences of indirect and direct taxes on economic development are different for developed and developing countries. The findings show that direct and indirect taxes have a significant negative relationship with economic development based on the GDPPC of developing countries. However, a significant positive relationship exists between direct taxes and economic development for developed countries. The results show that indirect taxes have a negative relationship with economic development measured by GDPPC. These results indicate that the tax structure in developing countries does not enhance the countries’ economic growth. Interestingly, GST are negatively correlated to the GDP per capita growth in developing and developed countries. Although GST is part of indirect taxes where most of the countries own tax revenue mostly from this type of taxes, this study concludes that the society seems to not gain economic benefits from the GST implementation, particularly in developing countries.

Furthermore, direct taxes of developing countries are positively related to FDI, which indicates that taxes encourage the inflow of FDI into the countries. However, indirect taxes seem negatively related to FDI, suggesting that investors are hesitant to invest in countries that impose GST and trade international tax. For developed countries, direct and indirect taxes are negatively related to FDI. This result suggests that for developed countries with a mature market and strong economic status, FDI may not be critical. Finally, direct and indirect taxes can help reduce the unemployment rate in developed and developing countries.

The findings provide evidence that direct tax positively affects the economic development of developed countries but negatively affects the economic development of developing countries. This finding provides additional support and confirmation to the existing research on which different tax structures may impact the economic growth of a particular country differently. Many other factors can influence the economic growth of a country other than taxes structures, for example, socio-political factors and technology. Hence, the policymakers are recommended to revisit the tax structures of their country if they want to enhance the positive impact of taxes on their countries’ economic development, explicitly securing more investment and reducing the unemployment rate.

This study is not without limitations. Firstly, although the study has included all variables after reviewing past literature, other factors, such as socio-political and technological advancement, might have been considered. Secondly, the data collected, including the year 2020, may not be adequate since the CV-19 pandemic lasted more than two years, but the study only obtained up to 2020 data. As such, the results may not be robust enough to conclude that the CV-19 pandemic significantly impacts the economic development of developing and developed countries. Future studies may need to look into these limitations to produce more robust and reliable results.

Acknowledgements

This work was supported by the Accounting Research Institute (ARI), HICoE, Universiti Teknologi (UiTM), Shah Alam, Malaysia under the Grant:600-RMC/ARI 5/3(012/2021).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Taufik Abd Hakim

Taufik Abd Hakim is a senior lecturer at Universiti Teknologi MARA (UiTM), Faculty of Business and Management. He holds a Doctor of Philosophy (PhD) in Business Management (Economics) from UiTM. His research interests include taxation, macroeconomics and panel data econometrics.

Abdul Aziz Karia

Abdul Aziz Karia is an Associate Fellow at Accounting Research Institute, HICoE, Universiti Teknologi MARA. He received his PhD in Economic Forecast from the Universiti Teknologi MARA. He actively participates in the policy paper and decision-making at the state level.

Jasmine David

Jasmine David began her career at Universiti Teknologi MARA in July 2005. She has a Ph.D. in accounting from the Victoria University of Wellington. She is actively engaged in research collaboration and networking with local, as well as international, universities and organizations.

Rainah Ginsad

Rainah Ginsad is a fellow at Accounting Research Institute, HICoE, Universiti Teknologi MARA. She holds a Doctor of Business Administration from Universiti Teknologi MARA (UiTM).

Norziana Lokman

Norziana Lokman is an Associate Professor and a Fellow at Accounting Research Institute, HICoE, Universiti Teknologi MARA. She has received her PhD in the field of Corporate Administration/Corporate Governance from the University of Southern Queensland. She has presented papers at various conferences and published articles in reputable scholarly journals.

Salwa Zolkafli

Salwa Zolkafli is a fellow at Accounting Research Institute, HICoE, Universiti Teknologi MARA. She holds a Doctor of Philosophy (Accounting) degree from Universiti Teknologi MARA (UiTM), with the title Factors and Challenges Influencing Money Laundering Investigation Outcome among the Law Enforcement Agencies in Malaysia.

Notes

1. Direct taxation refers as taxation imposed to an individual who is intended to be the final bearer of the tax payment.

2. Indirect taxation refers to taxation imposed to others than the individual who is intended to bear the final payment.

References

- Abdioglu, N., Binis, M., & Arslan, M. (2016). The effect of corporate tax rate on foreign direct investment: A panel study for OECD countries. EGE Academic Review, 16(4), 599–30. https://dergipark.org.tr/en/download/article-file/561136

- Acosta-Ormaechea, S., & Yoo, Y. (2012). Tax composition and growth: A broad cross-country perspective. IMF Working Paper, 12(257), 1. https://doi.org/10.5089/9781616355678.001

- Aghion, P., Akcigit, U., Cagé, J., & Kerr, W. (2016). Taxation, corruption and growth. National Bureau of Economic Research (NBER) Working Paper Series, WP 21928. http://dx.doi.org/10.3386/w21928.

- Ahmad, S., & Sial, M. (2016). Taxes and economic growth: An empirical analysis of Pakistan. European Law Review, 8(6), 01. https://doi.org/10.21859/eulawrev-08062

- Ajetunmobi, O., Uwuigbe, U., Uwuigbe, O. R., Lanre, N., & Omoyiola, A. (2019). Taxation, exchange rate and foreign direct investment in Nigeria. Banks and Bank Systems, 14(3), 76–85. https://doi.org/10.21511/bbs.14(3)

- Appiah-Kubi, S. N. K., Malec, K., Phiri, J., Maitah, M., Gebeltová, Z., Smutka, L., Blazek, V., Maitah, K., & Sirohi, J. (2021). Impact of tax incentives on foreign direct investment: Evidence from Africa. Sustainability (Switzerland), 13(15). https://doi.org/10.3390/su13158661

- Armeanu, D. S., Vintila, G., & Gherghina, S. C. (2018). Empirical study towards the drivers of sustainable economic growth in EU-28 countries. Sustainability, 10. https://doi.org/10.3390/su10010004

- Arnold, J. (2008), “Do tax structures affect aggregate economic growth?: Empirical evidence from a panel of OECD countries”, OECD Economics Department Working Papers No. 643, OECD Publishing, Paris, available at: https://doi.org/10.1787/236001777843

- Arnold, J. M., Brys, B., Heady, C., Johansson, A., Schwellnus, C., & Vartia, L. (2011). Tax policy for economic recovery and growth. Economic Journal, 121(550), 59–80. https://doi.org/10.1111/j.1468-0297.2010.02415.x

- Asghari, R., Heidari, H., & Mohseni Zonouzi, S. J. (2014). An investigation of the impact of government size on economic growth: New evidence from selected MENA countries. Iranian Journal of Economic Studies, 3(2), 63–80. https://ijes.shirazu.ac.ir/article_3670.html

- Assidi, S., Aliani, K., & Omri, M. A. (2016). Tax optimization and the firm’s value: Evidence from the Tunisian context. Borsa Istanbul Review, 16(3), 177–184. https://doi.org/10.1016/j.bir.2016.04.002

- Babatunde, A., Ibukun, O., & Oyeyemi, G. (2017). Taxation revenue and economic growth in Africa. Journal of Accounting and Taxation, 9(2), 11–22. https://doi.org/10.5897/JAT2016.0236

- Barro, R. J. (1991). Economic growth in a cross section of countries. Quarterly Journal of Economics, 106(2), 407–444. https://doi.org/10.2307/2937943

- Belotti, F., Porto, E. D., & Santoni, G. (2016). The effect of local taxes on firm performance: Evidence from geo referenced data. CEPII Working Paper, 1–36. Centre d'Études Prospectives et d'Informations Internationales (CEPII). http://dx.doi.org/10.2139/ssrn.2764349

- Canicio, D., & Zachary, T. (2014). Causal relationship between government tax revenue growth and economic growth: A case of Zimbabwe. Journal of Economics and Sustainable Development, 5(17), 9–22. https://d1wqtxts1xzle7.cloudfront.net/69619293/Causal_Relationship_between_Government_T20210914-10168-l9nwr1.pdf?1631614274=&response-content-disposition=inline%3B+filename%3DCausal_Relationship_between_Government_T.pdf&Expires=1667787406&Signature=fDbf98tmmfRsobhVYXev53V6jqPcOkysHEhlSeybjWr~BEgGgzuWz3cDj8ujZ7GFz-qnxJpH~XJF27Ed5aGE4tris1ConrbeGbA3JDsHEhi7tRLUUP4~bZVAxZ4IoiCtjradHAKJ2k4oeniRVZjb-5DLjjmjTRlnmYFJVUXfPTsucfgqW-bXDXfkn~eEitaf4NVjMb1nucGqpgf6~Fe2q3FI2V95cBagQvFb9UnBqY~5ouH6qCOpStQWtov1A-QyzawcBTDknSWzNyVWeDFeO~dmuzWjs6Fod-S~tVjveCrj3LcEOXPz7Nxc~tp1LztQ0117o5giv8-sabh~etIyHg__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA

- Daoud, J. I. (2017). Multicollinearity and regression analysis. Journal of Physics: Conf. Series, 949, 012009. https://doi.org/10.1088/1742-6596/949/1/012009

- Das, S. (2017). Some concerns regarding the goods and services tax. Economic and Political Weekly, 52(9). https://www.hansrajcollege.ac.in/hCPanel/uploads/elearning/elearning_document/G_E__Public_Finance,_B__Com_(H)_4th_Sem-Part-B-UNit-2-Some_Concerns_Regarding_the_Goods_and_Services_Tax_Notes.pdf

- DeHoyos, R. E., & Sarafidis, V. (2006). Testing for cross-sectional dependence in panel data models. Stata Journal, 6(4), 482–496. https://doi.org/10.1177/1536867X0600600403

- Disney, R. (2000). The impact of tax and welfare policies on employment and unemployment in OECD countries. https://www.imf.org/en/Publications/WP/Issues/2016/12/30/The-Impact-of-Tax-and-Welfare-Policieson-Employment-and-Unemployment-in-OECD-Countries-3827

- Driscoll, J., & Kraay, A. C. (1998). Consistent covariance matrix estimation with spatially dependent data. Review of Economics & Statistics, 80(4), 549–560. https://doi.org/10.1162/003465398557825

- Eugene, N., & Abigail, E. C. (2016). Effect of tax policy on economic growth in Nigria (1994-2013). International Journal of Business Administration, 7(1), 50–58. https://doi.org/10.5430/ijba.v7n1p50

- Field, A. (2005). Discovering statistics using SPSS. Sage Publication Ltd.

- Flaaen, A., Hortacsu, A., & Tintlenot, F. (2020). The production relocation and price effects of U.S. Trade policy: The case of washing machines. American Economic Review, 110(7), 2103–2127. https://doi.org/10.1257/aer.20190611

- Gashi, B., Asllani, G., & Boqolli, L. (2018). The effect of tax structure in economic growth. International Journal of Economics and Business Administration, 6(2), 56–67. https://doi.org/10.35808/ijeba/157

- Göndör, M., & Özpençe, Ö. (2014). An empirical study on fiscal policy in crises time: Evidence from Romania and Turkey. Procedia Economics and Finance, 15, 975–984. https://doi.org/10.1016/S2212-5671(14)00657-1

- Goodspeed, T., Martinez-Vazquez, J., & Zhang, L. (2011). Public policies and FDI location: Differences between developing and developed countries. Public Finance Analysis, 67(2), 171–191. https://doi.org/10.2307/41303586

- Hakim, T. A. (2020). Direct versus indirect taxes: Impact on economic growth and total tax revenue. International Journal of Financial Research, 11(2), 146–153. https://doi.org/10.5430/ijfr.v11n2p146

- Handley, K., Kamal, F., & Monarch, R. (2020). Rising imports tariffs, falling export growth: When modern supply chains meet old-style protectionism. International Finance Discussion Papers (IFDP), Board of Governors of the Federal Reserve System, United States, 1270. https://doi.org/10.17016/IFDP.2020.1270

- Hoechle, D. (2007). Robust standard errors for panel regression with cross-sectional dependence. The Stata Journal, 7(3), 281–312. https://doi.org/10.1177/1536867X0700700301

- Jones, L. E., Manuelli, R. E., & Rossi, P. E. (1993). Optimal taxation in models of endogenous growth. Journal of Political Economy, 101(3), 485–517. https://doi.org/10.1086/261884

- Karia, A. A. (2021). Are there any turning points for external debt in Malaysia? Case of adaptive neuro-fuzzy inference systems model. Journal of Economic Structures, 10(1), 1–16. https://doi.org/10.1186/s40008‑021‑00236‑6

- Korkmaz, S., Yilgor, M., & Aksoy, F. (2019). The impact of direct and indirect taxes on the growth of the Turkish economy. Public Sector Economics, 43(3), 311–323. https://doi.org/10.3326/pse.43.3.5

- Lee, Y., & Gordon, R. H. (2005). Tax structure and economic growth. Journal of Public Economics, 89(5–6), 1027–1043. https://doi.org/10.1016/j.jpubeco.2004.07.002

- Macek, R. (2015). The impact of taxation on economic growth: Case study of OECD countries. Review of Economic Perspectives, 14(4), 309–328. https://doi.org/10.1515/revecp-2015-0002

- Maganya, M. H. (2020). Tax revenue and economic growth in developing country: An autoregressive distribution lags approach. Central European Economic Journal, 7(54), 205–217. https://doi.org/10.2478/ceej-2020-0018

- Mcnabb, K. (2018). Tax structures and economic growth: New evidence from the government revenue dataset. Journal of International Development, 30(2), 173–205. https://doi.org/10.1002/jid.3345

- Mdanat, M. F., Shotar, M., Samawi, G., Mulot, J., Arabiyat, T. S., & Alzyadat, M. A. (2018). Tax structure and economic growth in Jordan, 1980-2015. EuroMed Journal of Business, 13(1), 102–127. https://doi.org/10.1108/EMJB-11-2016-0030

- Mendoza, E., Milesi-Ferretti, G., & Asea, P. (1997). On the ineffectiveness of tax policy in altering long-run growth: Harberger’s superneutrality conjecture. Journal of Public Economics, 66(1), 99–126. https://doi.org/10.1016/S0047-2727(97)00011-X

- Mercer-Blackman, V., & Camingue-Romance, S. (2020). The impact of United States tax policies on sectoral foreign direct investment to Asia. Asian Development Bank (ADB), Economic Working Paper Series, 628. https://doi.org/10.22617/WPS200388-2

- Minh Ha, N., Minh, P. T., Binh, Q. M. Q., & Ercolano, S. (2022). The determinants of tax revenue: A study of Southeast Asia. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2026660

- Mohs, J. N., Wnek, R., & Galloway, A. (2018). The impact of taxes on foreign direct investments. International Journal of Accounting and Taxation, 6(2), 54–63. https://doi.org/10.15640/ijat.v6n2a6

- Mose, N. (2021). Impact of public consumption on economic growth. African Journal of Economics and Sustainable Development, 4(3), 61–71. https://doi.org/10.52589/ajesd_tyrz1j6s

- Murphy, K., Shleifer, A., & Vishny, R. (1991). The allocation of talent: Implications for growth. Quarterly Journal of Economics, 106(2), 503. https://doi.org/10.2307/2937945

- Myles, G. D. (2009). Economic growth and the role of taxation-theory. https://doi.org/10.1787/222800633678

- Neog, Y., & Gaur, A. K. (2020). Tax structure and economic growth: A study of selected Indian states. Economic Structures, 9(38), 1–12. https://doi.org/10.1186/s40008-020-00215-3

- Nguyen, H. H. (2019). Impact of direct tax and indirect tax on economic growth in Vietnam. Journal of Asian Finance, Economics and Business, 6(4), 129–137. https://doi.org/10.13106/jafeb.2019.vol6.no4.129

- Nikolka, T. (2016). Taxation and female labor supply in OECD countries. https://www.econstor.eu/bitstream/10419/167264/1/ifo-dice-report-v14-y2016-i2-p55-58.pdf

- Ocran, M. (2011). Fiscal policy and economic growth in South Africa fiscal policy and economic growth in South Africa. Journal of Economic Studies. https://doi.org/10.1108/01443581111161841

- Ojede, A., & Yamarik, S. (2012). Tax policy and state economic growth: The long-run and short-run of it. Economics Letters, 116(2), 161–165. https://doi.org/10.1016/j.econlet.2012.02.023

- Ojong, M., Anthony, O., & Arikpo, F. (2016). The impact of tax revenue on economic growth: Evidence from Nigeria. IOSR Journal of Economics and Finance, 7(1), 32–38. https://doi.org/10.9790/5933-07113238

- Panth, P. (2020). Economic development: Definition, scope, and measurement (pp. 1–13). Springer Nature Switzerland. https://doi.org/10.1007/978-3-319-69625–6_38-1

- Pesaran, M. H. (2004). General diagnostic tests for cross section dependence in panels. University of Cambridge, Faculty of Economics, Cambridge Working Papers in Economics No. 0435.

- Peterson, E. W. F. (2017). The role of population in economic growth. SAGE Open, 1–15. https://doi.org/10.1177/2158244017736094

- Petru-Ovidiu, M. (2015). Tax composition and economic growth: A panel-model approach for Eastern Europe. Annals of the Constantin Brancusi University of Targu Jiu, Economy Series, 1(2), 89–101. https://www.utgjiu.ro/revista/ec/pdf/2015-01.Volumul%202/14_Mura.pdf

- Poulson, W., & Kaplan, G. (2008). State income taxes and economic growth. Cato Journal, 28(1), 53–71. https://heinonline.org/HOL/LandingPage?handle=hein.journals/catoj28&div=7&id=&page=

- Sachs, J., Schmidt-Traub, G., Kroll, C., Lafortune, G., & Fuller, G. (2021). Sustainable development report 2020. In sustainable development report 2020. Cambridge University Press. https://doi.org/10.1017/9781108992411

- Schwellnus, C., & Arnold, J. (2008). Do corporate taxes reduce productivity and investment at the firm level? cross-country evidence from the amadeus dataset. OECD Economics Department Working Papers, 641. https://doi.org/10.1787/236246774048

- Seward, T. (2008). The impact of taxes on employment and economic growth in industrialized countries. https://core.ac.uk/download/pdf/6538568.pdf

- Shafiq, M. N., Hua, L., Bhatti, M. A., & Gillani, S. (2021). Impact of taxation on foreign direct investment: empirical evidence from Pakistan. Pakistan Journal of Humanities and Social Sciences, 9(1), 10–18. https://doi.org/10.52131/pjhss.2021.0901.0108

- Shahmoradi, M., Mohamadi Molqarani, A., & Moayri, F. (2019). Tax policy and economic growth in the developing and developed nations. International Journal of Finance and Managerial Accounting, 4(14), 15–25. https://www.researchgate.net/publication/352787977

- Shrestha, N. (2020). Detecting multicollinearity in regression analysis. American Journal of Applied Mathematics and Statistics 8(2), 39–42. https://doi.org/10.12691/ajams-8-2-1

- Solow, R. M. (1956). A contribution to the theory of economic growth. The Quarterly Journal of Economics, 70(1), 65–94. https://doi.org/10.2307/1884513

- Stoilova, D. (2017). Tax structure and economic growth: Evidence from the European Union. Contaduría y Administración, 62(3), 1041–1057. https://doi.org/10.1016/j.cya.2017.04.006

- Tagkalakis, A. O. (2013). The unemployment effects of fiscal policy: Recent evidence from Greece. IZA Journal of European Labor Studies, 2(1), 1–32. https://doi.org/10.1186/2193-9012-2-11

- Thaçi, L., & Gerxhaliu, A. (2018). Tax structure and developing countries. European Journal of Economics and Business Studies, 4(1), 213–220. https://doi.org/10.26417/ejes.v10i1.p220-227

- Vartia, L. (2008). How do taxes affect investment and productivity? An industry-level analysis of OECD countries. OECD Economics Department Working Papers, (656). https://doi.org/10.1787/230022721067

- Vintilă, G., Gherghina, Ş. C., & Chiricu, C. Ş. (2021). Does fiscal policy influence the economic growth? Evidence from OECD countries. Economic Computation and Economic Cybernetics Studies and Research, 55(2), 229–246. https://doi.org/10.24818/18423264/55.2.21.14

- Waweru, D. (2021). Government capital expenditure and economic growth: An empirical investigation. Asian Journal of Economics, Business and Accounting, 21(8), 29–36. https://doi.org/10.9734/ajeba/2021/v21i830409

- Widmalm, F. (2001). Tax structure and growth: Are some taxes better than others? Public Choice, 107(3/4), 199–219. http://dx.doi.org/10.1023/A:1010340017288

- Wooldridge, J. M. (2002). Econometric analysis of cross section and panel data. MIT Press.

APPENDIX

Appendix 1: List of countries

Table A1. Developing countries

Table A2. Developed countries