?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the potential relationship between inflation and remittance outflows in Saudi Arabia over the period 1971–2019 by applying the autoregressive distributed lag (ARDL) model. As a pioneering study in Saudi Arabia, the paper addresses an important literature gap. The statistical tests reveal the model’s reliability and the existence of a long-run equilibrium among the variables. Moreover, the empirical results show a significant negative impact of inflation has on remittance outflows, and the short-run and long elasticities of remittance with respect to inflation are 0.26% and 0.32% respectively. These results suggest that despite the weak elasticity of remittance outflows to the inflation rate, an increase in general prices would reduce remittance outflows in Saudi Arabia. Moreover, we find that the capital investment indicator has a more significant effect on the volume of remittance outflows. Therefore, policymakers in Saudi Arabia should apply appropriate actions to reduce the outflows of foreign workers by urging private companies to hire more Saudi workers, increasing capital investment and encouraging foreign workers, especially those with high incomes, to invest in Saudi Arabia by facilitating their ownership of financial market shares and real estate units.

1. Introduction

It is well documented in the economic literature that international migration plays a considerable role in both labor-sending and labor-receiving countries (Javid & Hasanov, Citation2022). Regarding sending countries, labor migration is due to wage differentials, unemployment, and poverty, among other factors. Hence, labor migration helps to mitigate unemployment and improve the balance of payments. The Saudi Arabian economy depends heavily on oil. In addition, it is amongst the largest oil producers and exporters in the world, with a daily average of 9.3 million barrels of total world exports (World Energy Outlook, Citation2019). For decades, Saudi Arabia has been one of the most attractive host countries for labor migration, due both to its high oil revenues and its chronic shortage of skilled and unskilled domestic labor. The surge in oil revenues stimulated the Saudi government’s ambitions to boost various targeted development plans by increasing government spending. As a result, various economic activities have experienced growth, such as the industrial, education, and transportation sectors.

The booming Saudi economy has attracted a large flow of international workers since the 1970s. Migrant workers represent, on average, about 30% of KSA’s total population (see, Table in Section 4). This proportion increased from 4% in the early 1970s to 38% in 2018, and migrants’ labor market share increased to reach about 76% in 2019 (GAS, Citation2019). The increase of migrant workers is associated with a considerable volume of remittance outflows from sending economies, since they remit a large portion of their income to their home country. Saudi Arabia is among the highest remittance-sending countries, ranking third in the world after the United States of America and the United Arab Emirates (World Migration report, Citation2020, page 37). In 2018, KSA remittance outflows reached 33.9 billion USD, representing 4.31% of (GDP), compared with a maximum of 38.787 billion USD in Citation2015 (see, Table in Section 4).

Table 1. Dependent and Independent Variables

Table 2. Migrants and remittance outflows in the KSA

In oil-exporting countries, oil prices play a major role at the macroeconomic level. Hence, higher oil prices may cause a short and long run surge in inflation rates. Moreover, increases in global oil prices are expected to generate fiscal surpluses, which would encourage the Saudi government to significantly increase its public spending, stimulating domestic aggregate demand and raising the level of general prices. According to our analysis, this may lead to a decline in remittance outflows, since, foreign expatriates increase their spending on goods and services to maintain the same level of living in host countries.

While remitting countries have received little attention due to their small relative contribution to GDP, a considerable number of applied studies on remittance flows have heavily focused on the flows’ impact on labor-sending countries (Balderas & Nath, Citation2008; Cazachevici et al., Citation2020; Kadozi, Citation2019; Khan & Islam, Citation2013; Lastovetska, Citation2017; Meyer & Shera, Citation2017; Narayan et al., Citation2011; Opperman & Adjasi, Citation2019; Rao & Hassan, Citation2011). Naufal and Genc (Citation2018) noted that recent research on remittance outflows has focused on examining their macroeconomic impact on remittance-sending countries (Al-Kaabi, Citation2016; Alkhathlan, Citation2013; Edrees, Citation2016; Haddad & Choukir, Citation2017; Rahmouni & Debbiche, Citation2017; Salameh & Aldaarmi, Citation2019; Termos et al., Citation2013).

Regarding the Gulf Cooperation Council (GCC) countries, very little applied research has examined the association between remittance outflows- oil price fluctuations nexus in the GCC region. For example, for the GCC countries, Termos et al. (Citation2013), found a negative association between remittance outflows and inflation rate; Naufal and Termos (Citation2009) found a weak elasticity (0.4) of remittance outflows to oil prices; Ratha et al. (Citation2015) found a statistically small positive effect (0.1) on remittance outflows; and, more recently, De et al. (Citation2019) found that a sharp decline in oil prices was associated with a modest decline in remittance outflows in GCC countries in 2016 and 2017. Moreover, Taghavi (Citation2012) reported a unidirectional causality running from remittances to inflation. In contrast, Al-Kaabi (Citation2016) found that inflation was irresponsive to the growth of remittance outflows and was negative only for Bahrain. Although migrant remittances do not have adverse effects in the GCC countries, as they do not account for a significant share of GDP, Termos et al. (Citation2013) stated, “The staggering amount of remittances fleeing the GCC region during economic upturns seems to play a stabilizing role as a tacit monetary policy tool reducing inflationary pressure in these economies.” For Saudi Arabia, Haddad and Choukir (Citation2017) confirmed the main finding of Termos et al. (Citation2013).

However, as oil prices start to fall and reach their lowest levels, the high share of remittances could negatively influence the balance of payments and, thus, aggregate demand, posing a serious problem for policymakers. Therefore, reducing remittance outflows in GCC countries is of great importance. This can be achieved by studying the determinants of remittance outflows (e.g., inflation rate) in remitting countries. A high general price level in remitting countries could increase expenditures and thus reduce remittance outflows.

This paper is motivated by the concern of policymakers in KSA, a remitting country, regarding the volume of remittance outflows, which constitute a considerable share of GDP. In addition, remittance outflows are considered a drain on foreign reserves. For KSA, the trend of the percentage of remittance outflows is increasing despite fluctuations in certain years, and their volume reached about 33.5 billion USD in 2019. Moreover, applied research on remittance outflows in Saudi Arabia provides evidence on their negative impacts on financial development (Al-Abdulrazag & Abdel-Rahman, Citation2016) and economic growth (Alkhathlan, Citation2013) among others. These negative impacts are expected to slow investment activities in Saudi Arabia. This behavior of remittance outflows has raised concerns among policymakers in KSA about the potential negative impacts on Saudi economy.

The main finding of this paper is that the inflation rate has significant long-run and short-run negative impacts on remittance outflows. Regarding control variables, we find that economic growth has a significant positive effect, whereas capital investment and trade openness exert negative effects on remittance outflows. The estimation results show that, after a sudden shock, about a year and a quarter is required for the model to restore its long-run equilibrium (as indicated by the ECM term).

The present study contributes to the existing applied literature in several ways. First, the existing literature focuses heavily on the determinants and effects of remittance flows in the context of receiving countries rather than sending countries. Consequently, the factors affecting the volume of sending countries’ remittance outflows have received less attention from both policymakers and researchers. For example, Al-Abdulrazag and Abdel-Rahman (Citation2016) and Alkhathlan (Citation2013) examined their adverse impacts on selected macroeconomic factors in Saudi Arabia, such as economic growth, monetary policy, and inflation. It is clear that very few researchers have studied the inflation—remittance outflows nexus in Saudi Arabia. Thus, this study represents a pioneering effort to fill this gap in the existing literature. It examines the long-run and short-run impacts of inflation on remittance outflows by applying the ARDL estimation method and the H. Y. Toda and Yamamoto (Citation1995) approach to annual data. In addition, it suggests some policy implications that would be useful to KSA policymakers to reduce the volume of remittance outflows and their adverse impacts on the Saudi economy.

We used the ARDL model to test the hypothesised long-run negative relationship between inflation rate (INF) and remittance outflows in KSA over the period 1971–2019. The research’s importance relies on the fact that it takes place in the midst of the Saudi government’s new policy—Vision 2030—to cut down the number of foreign workers and increase the dependence on local labor, which suffers from unemployment, and hence, reduce remittance outflows.

The structure of the study is as follows. Section 2 surveys the most relevant empirical literature. Section 3 describes the data and methodology. Section 4 contains estimation results, followed by the discussion section. Finally, conclusions and policy recommendations are presented in Section 6.

2. Key findings of previous empirical literature

The increasingly important economic role of remittances has attracted the attention of applied researchers, who have studied their impacts on various economic activities. A review of applied empirical studies of remittance flows clearly shows that most applied work has focused on the flows’ adverse impact on key macroeconomic and microeconomic variables in receiving countries rather than sending countries. Moreover, extensive empirical work has applied modern estimation techniques using time-series and panel data. For example, such studies have examined economic growth (Al-Kaabi, Citation2016; Alkhathlan, Citation2013; Edrees, Citation2016; Kadozi, Citation2019, Citation2019; Makhlouf & Kasmaoui, Citation2017; Meyer & Shera, Citation2017; Rahmouni & Debbiche, Citation2017; Salameh & Aldaarmi, Citation2019). Others have investigated inflation, (Haddad & Choukir, Citation2017; Iqbal et al., Citation2013; Khan & Islam, Citation2013; Narayan et al., Citation2011; Termos et al., Citation2013); trade openness (Ebeke, Citation2011; R. R. Kumar, Citation2012); financial development (Aslam & Selliah, Citation2020;; ; Al-Abdulrazag & Abdel-Rahman, Citation2016); and imports (Al-Abdulrazag, Citation2018); among others.

Generally, the applied work is in two strands. The first strand focuses heavily on the labor-sending (remittance-receiving) countries. The second strand, which receives less attention, focuses on the labor-receiving (remittance-sending) countries. Termos et al. (Citation2013) suggested that the reason for the gap between the two strands is the relatively insignificant contribution of emittance outflows to the GDP of most remitting countries. Nevertheless, Saudi Arabia emerges as a remarkable exception, with remittances making up a large share of GDP.

The applied work mostly covers several dimensions including economic growth, inflation, financial development, trade openness, and imports. Regarding the relationship between remittance flows and economic growth, the results were mixed. However, they tended toward positive association, as Cazachevici et al. (Citation2020) pointed out in a meta-analysis: approximately 40% of these studies reported a positive effect, approximately 20% reported a negative effect, and approximately 40% reported no significant impact.

The relationship between remittance outflows, inflows, and economic growth has been the subject of a vast body of empirical work. By ignoring endogeneity issues, time-series studies reported systematically larger effects of remittances on growth, and the results were mixed. Whereas, some researchers, including Rapoport and Docquier (Citation2005), De et al. (Citation2019), Ratha et al. (Citation2015), and B. Kumar (Citation2021), report a positive and significant impact. However, Salameh and Aldaarmi (Citation2019), Al-Kaabi (Citation2016), Alkhathlan (Citation2013), and Abdel‐Rahman (Citation2006) found a negative relationship in Saudi Arabia. In contrast, Rahmouni and Debbiche (Citation2017) revealed an insignificant impact in Saudi Arabia.

As for other countries, Kadozi (Citation2019) found an insignificant impact of remittances on GDP in the region of Sub Saharan Africa, except in Rwanda concerning the period 1980–2014. Bouoiyour et al. (Citation2019) showed that the effect of remittances on GDP in Tunisia varies with time. Meyer and Shera (Citation2017) showed a positive relationship in Albania, Bulgaria, Macedonia, Moldova, Romania and Bosnia Herzegovina during the period 1999–2013. While Lueth and Ruiz-Arranz (Citation2006), Bettin et al. (Citation2017), and Lianos (Citation1997) found that remittance inflows to the recipient countries respond positively to the GDP of the host country, Sayan (Citation2004) and Panda and Trivedi (Citation2015) indicated that remittance inflows in Turkey respond negatively to German GDP. However, Ahmed and Inmaculada (Citation2014) found that the GDP of the host country has an insignificant effect on remittances. In a more general result, Panda and Trivedi (Citation2015) revealed that global GDP exerts a positive impact on remittance inflows.

Another stream of research focused on the remittances–trade openness nexus. Ebeke (Citation2011) found a significant negative impact of trade openness on the cyclicality of remittances; remittances are countercyclical, and this effect increases as trade openness increases. Vanuatu and R. R. Kumar (Citation2012) found that greater openness could boost remittances.

Focusing on the literature related to the remittance outflows–inflation nexus for labor-receiving countries, the results are mixed. Makhlouf and Kasmaoui (Citation2017), Narayan et al. (Citation2011), Panda and Trivedi (Citation2015), Lueth and Ruiz-Arranz (Citation2006), Lianos (Citation1997), Iqbal et al. (Citation2013), Khan and Islam (Citation2013), and Taghavi (Citation2012) found that, in Saudi Arabia, inflation is positively influenced by remittance outflows. In addition, a negative relationship was reported by Barua et al. (Citation2007), Termos et al. (Citation2013), and Haddad and Choukir (Citation2017).

Regarding financial development, Gupta et al. (Citation2009) and Aggarwal et al. (Citation2011) found that remittance inflows promote the financial development of recipient countries by raising the level of deposits and credit intermediated by the local banking sector. On the one hand, Ezeoha (Citation2013) identified a positive impact of financial development on remittances, especially in developing economies. While, Al-Abdulrazag and Abdel-Rahman (Citation2016) found a negative effect of financial development on remittance outflows from Saudi Arabia.

To this end, the abovementioned literature on the remittance outflows-major macroeconomic variables nexus has produced mixed results spanning from positive to insignificant impacts. These different results are due to differences in country-specific or cross-country factors, research estimation techniques, data types, or the time span of the data. For Saudi Arabia, the remittance outflows–inflation nexus has received little attention. Instead, the literature has focused on the impact of variables other than remittance outflows, such as oil prices and inflation, in remittance-receiving countries. Hence, this paper contributes to examining the remittance outflows-inflation nexus in the context of Saudi Arabia, thus bridging this empirical gap.

3. Conceptual framework, econometric model and methodology

The relationship between the inflation rate and remittance flows has been conceptualized theoretically in the economic literature in various approaches. For example, Javid and Hasanov (Citation2022) tackle this relationship through labor demand and labor supply functions. They show through a demand function that marginal productivity equals the wage rate in profit maximization. In addition, through the utility function of labor supply, remittance outflows depend on price level along with other factors, such as GDP in the host country. They argue that price increases lead to extra expenditure on consumption, hence forcing foreign workers to reduce their remittances.

The Saudi Arabian economy is an open economy. The total production at the equilibrium point:

Where:

C: Consumption,

I: Investment,

G: Government public expenditure

X-M: Net exportation

Consumption and government expenditures are the two main components of the demand side through which remittances are affected. As it has been mentioned before, millions of foreigners work and live in Saudi Arabia. They represent, on average, about 30% of KSA’s total population (See, Table in Section 4). Hence, foreigners represent a significant share of households in KSA. The total annual amount of their remittances is determined directly by the net income after subtracting all their internal consumption bills, fees, and taxes.

Where:

REMT: the total annual volume of remittances sent by foreign workers to their countries.

GI: gross annual Income earned by foreign workers in the host country (Saudi Arabia).

CB: annual Consumption Bills of foreign workers in the host country (Saudi Arabia).

CB are the sum of all goods and services consumed by foreigners in the host country (Saudi Arabia). It constitutes the largest proportion of their total expenditures. The general commodity prices in the host country are considered the most important determining factor of the s of foreigners’ annual consumption bills. In short, the increase in general prices will increase the expenses of foreign workers in the host country, which will reduce the volume of their remittances abroad.

DT: direct Taxes on incomes generated by foreign workers.

It is to be mentioned that the Saudi government doesn’t impose any direct taxes on the revenues earned by foreigners. Therefore, this variable has no effect on the remittance outflows.

RGSF: residence and government service fees paid by foreigners.

Here we mention that the VAT application of 15% and the gradual increase in the price of fuel by the Saudi government led to a rise in the prices of goods, services, and real estate, which constituted a burden on the budget of foreigners, leading to an increase in their consumption bills. In addition, imposing fees for accompanying family members led to a continuous decline in the volume of their remittances since 2016 (See, Table in Section 4).

In oil-exporting countries, oil prices play a major role at the macroeconomic level. Hence, higher oil prices in these countries may lead to an increase in inflation rates in both the short and long run. The increase in global oil prices is expected to generate fiscal surpluses in the Saudi budget, which would encourage the Saudi government to significantly increase its public spending G, thereby stimulating domestic aggregate demand and raising general prices consequently. According to our analysis, the rise in global oil prices is associated with a rise in inflation and a decline in remittance outflows. As a result, foreign expatriates increase their spending on goods and services to maintain the same standard of living in their host countries. Therefore, relying on theory and previous applied research, the econometric model is expressed as follows:

where is the remittance outflows;

is the inflation rate;

is a set of control variables thought to affect

; and

is the normally distributed error term. All the variables except inflation rate are expressed in logarithmic form, which transforms the estimated parameters into elasticities. The expected negative sign of inflation parameter

indicates that remittance outflows decrease as inflation rate increases. Please refer to Table for the parameters and expected signs.

In investigating the outflows of the remittances–inflation nexus in the KSA, the present paper uses the autoregressive lag (ARDL) model approach to cointegration introduced by Pesaran et al. (Citation2001). This approach is documented in the applied literature (Janesh, Citation2013; Javid & Hasanov, Citation2022; Nkoro & Uko, Citation2016), and it has several advantages over other estimation approaches (Engle & Granger, Citation1987; Johansen & Juselius, Citation1990). The conventional cointegration approaches of Granger (Citation1981) and Engle and Granger (Citation1987) require that all variables be integrated of the same orders—that is, either the I(1) or I(0) orders (Nkoro & Uko, Citation2016). Moreover, EG suffers from the problem of variable order, which becomes far more serious in the case of more than two variables. In addition, it does not provide the number of cointegrating vectors (Asteriou & Hall, Citation2007). In our case, using the EG approach is ruled out for the abovementioned reasons, whereas the Johansen and ARDL cointegration procedures are applicable. However, the application of ARDL requires that only one cointegrating vector exists. In contrast, when there are multiple cointegrating vectors, the Johansen and Juselius (Citation1990) approach is the alternative. The application of Johansen cointegration approach requires that all variables are integrated of the same order (Asteriou & Hall, Citation2007).

The autoregressive lag (ARDL) model can be applied to small samples regardless of whether the variables are I(0) or I(1), but it cannot be applied to I(2) variables (Pesaran et al., Citation2001). That is, the ARDL cointegration technique does not require pretests for unit roots, unlike other techniques (Nkoro & Uko, Citation2016). Furthermore, it captures both short-run and long-run effects, and it addresses the potential problem of endogeneity. In addition, ARDL explicitly tests for the existence of a unique cointegration vector (Javid & Hasanov, Citation2022; Nkoro & Uko, Citation2016). This approach’s main advantage is that it can identify cointegrating vectors when there are multiple cointegrating vectors (Nkoro & Uko, Citation2016). It also provides different optimal lag orders for each model’s variables.

3.1. Measuring variables

Table summarizes the variables expected to affect migrant remittance outflows, including inflation rates, real economic activity, investment levels, and trade openness. According to El-Sakka and Mcnabb (Citation1999), “A high rate of domestic inflation may thus act as a proxy for uncertainty and risk and, therefore, discourage the flow of remittance earnings.” Moreover, Termos et al. (Citation2013) reported that remittance outflows in sending countries negatively affect inflation. Accordingly, the authors suppose similarly that inflation in sending countries may also reduce remittance outflows by increasing the consumption expenditures of migrant workers; therefore, the inflation coefficient is expected to be negative.

According to Swamy (Citation1981), the economic activity of remitting countries determines the volume of remittance outflows. Desai et al. (Citation2009) showed that migrants’ remittance outflows are affected by pro-cyclical activities, which increase their income and strengthen their ability to transfer money.

We assume that a higher level of investment (the Log of gross fixed capital formation in the remitting countries) improves efficiency by replacing expatriate workers, decreasing their demand, and reducing their wages and employment, hence lessening their ability to transfer money abroad. Therefore, LGF is expected to have a negative impact on remittance outflows via the marginal rate of technical substitution.

Finally, LOPEN is the trade openness (measured as the ratio of total trade to GDP). On the one hand, Allen and n.d.ikumana (Citation2000) reported a positive correlation between LOPEN and economic growth, which increases workers’ income and, consequently, their remittances. We believe that imports, especially capital goods, can have a negative impact on remittance outflows. Imports may have a detrimental impact on growth by increasing the prices of intermediate goods and hence the production cost of final goods. Indeed, the increase in prices reduces the competitive power of final local goods, decreasing profits and potentially eliminating local industries. As a result, local production decreases, which may lead to the layoff of a considerable reduction in the number of foreign workers or a reduction in their wages; this implies that trade openness can negatively affect remittance outflows.

3.2. The ARDL model

The unrestricted ARDL specification of the long-run relationship between and

in the KSA is as follows:

The specification outlined in EquationEq. (2)(2)

(2) allows for the short- and long-run effects of exogenous variables. By estimating the parameter of the first-difference of the variable, we show the short-run effect of an exogenous variable, whereas, the long-run effects are captured by the estimates of λ2–λ3 normalized by λ1.While Narayan (Citation2005) offers critical values for small samples, Pesaran et al. (Citation2001) recommend F-test to establish a joint significance of the linear combination of lagged variables as an evidence supporting the cointegration, and offered a new set of tabulated critical values applicable to large sample sizes.

EquationEq. (2)(2)

(2) can also be considered as an ARDL of order (p, q, s) for outflows. The Akaike Minimum Information Criteria (AIC) are used to define the appropriate lag length structure. The long-term equilibrium can be determined by the computed F-statistic using Wald test, which is sensitive to the lag length (Shahbaz et al., Citation2012). The null hypothesis of no long-run equilibrium relationship is

:

0 versus the alternative hypothesis

:

≠ 0. Accepting or rejecting

is based on the calculated F-statistic compared with the critical values. Accordingly, if the F-statistic is greater than the upper limit I(1), the null hypothesis is rejected; whereas, if the F-statistic is less than the lower bound I(0),

is accepted. However, if the F-statistic is between the two limits, the outcome is inconclusive (Mahmoudinia et al., Citation2013).

3.3. Johansen cointegration approach

The study applies the cointegration method developed by Johansen (Citation1988, Citation1991) and Johansen and Juselius (Citation1990) to determine the rank of cointegration. The Johansen method is preferred over the two-step Engle-Granger method because it can test for multiple cointegrating vectors and directly obtains the maximum likelihood estimates of the cointegrating vectors and fitting parameters. The system of cointegrating vectors can be described as a set of vector autoregressions (VAR) of nonstationary time series as follows (Boon, Citation2000):

The matrix coefficient is the long run impact matrix that contains information about the stationarity of the variables and the long-run relationship between them. The rank of the matrix determines the number of cointegration vectors. If the coefficient matrix is full rank,

, then all variables are stationary with no trend or long-term relationship between them. However, if the rank of the matrix is zero,

, then there is no cointegration and the variables are not stationary. The last possible case is where the rank lies between zero and p

. In this case, there are r linear combinations of variables in Xt that are stationary, and the variables are cointegrated with r vectors in the long-run. Johansen and Juselius (Citation1990) and Johansen (Citation1988) derived two likelihood ratio tests for the hypothesis of (

) cointegrating vectors; the trace test and the Maximum Eigenvalues test. The trace test tests whether the number of distinct cointegrated vectors is less than or equal to

against the alternative of more than

cointegrating vectors. The trace test is computed as follows:

Where T is the sample size, are

smallest estimated Eigenvalues and ln is the natural log. The null of the second (max) test is the number of cointegrating vectors r against the alternative of r + 1 cointegrating vectors. The Maximal Eigen value test is given by the statistic:

Where, equals the estimated Eigenvalue of the characteristic roots, r = 0,1, 2,., T = number of observations. The critical values of these tests are produced by the Monte Carlo simulation and tabulated by Johansen (Citation1988) and Osterwald-Lenum (Citation1992). In the case of conflicting cointegration rank results provided by λ_trace and λ_max, the λ_trace statistic is preferable to the λ_max statistic (Enders, Citation2003).

3.4. Toda and yamamoto causality test

The Granger causality test assumes the stability of the time series. However, it performs poorly if the time series are not integrated from the same order. In other word, the integration process must be clear. Instead, the approach of H. Y. Toda and Yamamoto (Citation1995) applies a VAR model to determine the existence of a long-run equilibrium relationship among variables. Toda and Yamamoto’s method has the advantage of not requiring integration and cointegration of variables; for further information see, Moftah and Dilek (Citation2021), Fawad (Citation2013), H. Toda and Phillips (Citation1993), and Zapata and Rambaldi (Citation1997).

To determine the causality direction between inflation rates and remittance outflows in Saudi Arabia, the causality test of H. Y. Toda and Yamamoto (Citation1995) estimates the VAR (k+ dmax) model as following:

Where: k is the optimal lag-length of the level VAR, dmax is the maximum order of integration.

The following four steps are required for carrying out Toda-Yamamoto causality test:

1) To improve the estimated model’s explanatory power, we determine the appropriate optimal lag order in the estimated VAR model (k), based on either the lowest Akaike Information Criterion or the lowest Schwartz Information Criterion. See, Umoru and Tizhe (Citation2014).

2) The second step is applying unit root tests to determine the maximum order of integration (dmax) for all series.

3) The estimation of the VAR in level form with the modified order of VAR (k+dmax).

4) At final step, the Wald test for Granger causality well be conducted.

4. Estimation results

This section presents the estimation results of EquationEq. (2(2)

(2) ), including the ADF unit root test, bounds test to cointegration, ARDL estimation results, diagnostic residuals tests, stability test, and Grange causality test based on the Toda–Yamamoto method.

4.1. Descriptive analysis

Table presents the development of remittance outflows over the period 1980–2019. It shows that the number of migrants in KSA has steadily increased over time, representing about 30% of the total population on average. Consequently, remittance outflows rose continually. Table shows that the total amount of remittances doubled between 2005 and 2010 and then increased by $11 billion between 2010 and 2015. This growth was due to the significant increase in oil prices between 2005 and 2015. Thereafter, remittances began to decline, coinciding with the decline in oil prices. Although the value of foreign remittances increased to record levels between 2005 and 2015, their share of GDP declined from the maximum of 11.65% in 1995 to 5.93% in 2015. This is because GDP (the denominator) rose very sharply during this period due to the surge in oil prices, which superpass the increase in remittances.

Table shows that remittance outflows represent 5.77% of the GDP on average over the period 1971–2109, which is similar to the percentage calculated by Alkhathlan (Citation2013) for the period 1970–2010 (5.61%). This percentage puts KSA in the top 10 remitting countries in the world. Moreover, the mean inflation rate is 3.7%, which is within the acceptable standard inflation rates. The inflation rate ranges from a minimum of −3.20% to a maximum of 34.57%, indicating the absence of hyperinflation episodes in Saudi Arabia. The Jarque–Bera test statistics is insignificant for all variables except for the inflation rate at the 1% level. This implies that these variables are normally distributed.

Table 3. Descriptive statistics during the period from 1971 to 2019

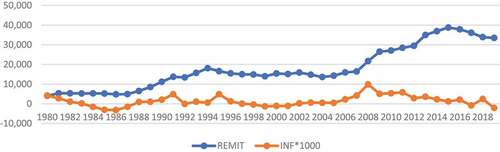

Figure depicts the development of migrant remittance outflows (REMIT) and inflation rates (INF) over time, highlighting their similar trends. Both variables witnessed fluctuations due to the state of the Saudi economy. Furthermore, they are moving in opposite directions, indicating the inverse relationship.

Figure 1. Evolution of outflows remittance and inflation rates in the KSA from 1980 to 2019.

This figure is elaborated by the authors based on World Bank dataset.

To make the comparison possible, the inflation rates were multiplied by 1000.

4.2. Unit root test

Nkoro and Uko (Citation2016) indicated that the ARDL approach can not be applied to I(2) variables. Table indicate that all series are composed of either I(0) or I(1) variables. Three other stationarity tests (not reported) were performed, and they suggested similar results.

Table 4. Break Point Unit Root Tests (Model with Constant and Linear Trend)

4.3. Analysis of cointegration results

To begin, the application of Johansen cointegration analysis requires estimating a VAR model to determine the lag number. The endogenous variables (LREMIT, LGDPC, LOPEN, LGF and INF) are included in the VAR model. We also include a dummy variable for the year 2015 (Dum = 1), when remittance outflows increased dramatically. This increase was triggered by the increase in oil revenues and fiscal reforms. Table . reports the lag selection results. Following the SC criterion, we estimate the VAR with one lag.

Table 5. Optimal Lag selection creterion

Table . Reports the optimal lag length selection; however, there are different lags, and most of the criteria indicated four lags. To be more specific, a VAR(1) with one lag is estimated and tested for autocorrelation, and the LM test rejects the null hypothesis of no autocorrelation. However, the VAR(4) accepts the null hypothesis. Hence, we use VAR(4) with four optimal lags.

The VAR estimation passes all the statistical diagnostic tests for the residuals, including the serial correlation LM test, normality tests, stability test and the heteroscedasticity test, as reported in Table .

Table 6. VAR residual diagnostics test results

As a results, the Johansen cointegration test can be applied. The results of the trace and the maximum eigenvalue are reported in Table . It recommended dropping models 1 and 5 to avoid any linear trend in the long-run part of the VECM (Javid & Hasanov, Citation2022). The trace and maximum eigenvalue statistics both reject the null hypotheses of no cointegration for the five models (r = 0). Table . clearly shows that both tests indicate only one cointegration equation.

Table 7. Johansen cointegration test summary

Table 8. Johansen cointegration test results for type (model2)

The critical values for the cointegration test are taken from MacKinnon

Based on these results, we can consider employing single-equation-based or residual-based cointegration methods and long-run estimators. Therefore, we can employ the bounds-testing approach proposed by Pesaran et al. (Citation2001), which is superior to other long-run estimators for small sample sizes.

4.4. ARDL estimation results

The ARDL technique is applied to estimate the long-run and short-run relationships between remittance outflows and inflation.

4.4.1. Optimal model lags

The automatic AIC optimal lag selection criterion was used over 768 evaluated models’ adjusted and F-statistic values. We opted for automatic selection by choosing the maximum lag length at three lags. Table shows the relative goodness adjusted

as 0.99, indicating that the model explains approximately 99% of the variation in the remittance outflows. Moreover, the F-statistic is significant at the 1% level, indicating that the model is not spurious.

Table 9. ARDL Optimal Model Lags (1971–2019)

4.4.2. ARDL bound-test result

The bounds-test result is reported in Table . As the F-statistic (6.486) is greater than the upper limit (5.06), a long-run relationship is detected between the model variables.

Table 10. Bounds-Test of Cointegration

4.4.3. ARDL model diagnostic tests

To provide evidence supporting our model validity, statistical diagnostic tests are reported in Table .

The Breusch–Pagan–Godfrey test indicates the acceptance of the null hypothesis of homoscedasticity. This implies that the t-statistics, and consequently the p-values, are asymptotically normally distributed.

The Breusch–Godfrey Lagrange multiplier test indicates that the residuals are not serially correlated.

The Jarque–Bera statistic shows the normal distribution of residuals.

The Ramsey RESET test indicates that the model is correctly specified.

Table 11. Residuals and Stability Tests

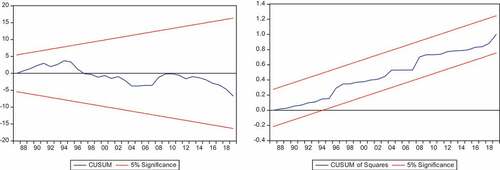

Figure shows that both the cumulative sum (CUSUM) and the cumulative sum squared CUSUMSQ of recursive residuals indicate model stability. This confirms that the OLS regression parameters do not suffer from structural changes.

Figure 2. Plot of cumulative sum and cumulative sum of squared recursive residuals.

4.4.4. Short-run estimation results

The high significance of the error correction coefficient , which equals −0.829 (with a t-statistic of −12.784), is another indication that the model variables are cointegrated, as shown in Table . As

represents the speed of adjustment, this indicates that our variables quickly return to equilibrium; 83% of any short-run shock is corrected within one period. Moreover, we observe a significant negative effect of inflation on remittance outflows (−0.268), suggesting that a 1% increase in inflation rate leads to a 0.26% decrease in outflows. Thus, inflation reduces remittances in the short run.

Table 12. Short-Run ARDL (1, 0, 1, 2, 3)

4.4.5. Long-run estimation results

The long-run estimation results reported in Table show the significantly negative coefficient of inflation implies that increasing inflation by 1% decreases remittance outflows by 0.32%. As expected, the real level of economic activity (represented by LGDPC) positively affects remittance outflows, since a higher level of economic activity in the sending country increases workers’ income, which strengthens the ability of migrant workers to transfer money abroad. The empirical results reveal a negative impact of trade openness on remittance outflows. Finally, the negative coefficient of LGF indicates the efficiency of capital formation in reducing remittance outflows by replacing foreign workers with capital machines.

Table 13. Long-Run Estimation Results of ARDL model

4.4.6. Toda–Yamamoto test: Non-Granger causality test

The long-run causal relationship between inflation and remittance outflows confirmed by the ARDL estimation results was examined by Granger causality based on the H. Y. Toda and Yamamoto (Citation1995) method. Table reports the Toda–Yamamoto (TY) results. The table shows that there is a significant unidirectional causal relationship running from inflation rate to remittance outflows but not vice versa. This result confirms the ARDL result, implying that inflation is a significant determinant of remittance outflows. However, one must bear in mind that the TY result provides the causal direction but not the sign or magnitude of the effect, which can be deduced by estimating the ARDL model.

Table 14. Toda-Yamamoto VAR Granger Causality/Block Exogeneity Wald Tests

variables are available upon the request from the authors.

5. Discussion of the empirical estimation results

The current study is a pioneer in investigating the remittance outflows- inflation nexus in Saudi Arabia. Table shows the ADF test results, which indicate that all variables are either I(1) or I(01). This means that their means, variances and covariances are not constant over time. Therefore, any sudden shock to these variables—including policy shocks—would result in a permanent change. However, these variables turn out to be stationary after differencing. Moreover, the cointegration results shown in Table indicate that the variables have a long-run equilibrium relationship. The estimation results are expected to improve our understanding of the long-run behavior of remittance outflows in Saudi Arabia, thus providing useful information to policymakers when formulating relevant measures.

The empirical results reveal a long-run inverse relationship between the inflation rate and remittance outflows, and the price negatively affects remittance outflows from Saudi Arabia. A 1% increase in the inflation rate reduces remittance outflows by 0.32%. Since the inflation rate reflects the cost of living, higher rates discourage migrants from sending more money to their homelands. While our empirical results suggest that higher general prices reduce remittance outflows in Saudi Arabia, Termos et al. (Citation2013) found that an increase in remittance outflows in the GCC region reduced inflation rates. For Saudi Arabia, Taghavi (Citation2012) showed a unidirectional causality, suggesting that higher outflows could lead to changes in the inflation rate.

These results indicate that inflation rates and remittance outflows interact. The finding that remittance outflows exhibit weak elasticity to inflation rates could be explained by this interaction, as each of the two variables weakens the influence of the other. The mechanism of this feedback effect runs through oil prices, as Saudi Arabia is highly dependent on oil. Indeed, higher oil prices could lead to higher inflation rates in both the short and long run. Finally, the presence of a statistically weak negative impact of inflation on remittance outflows in Saudi Arabia is consistent with De et al. (Citation2019), Ratha et al. (Citation2015) and Naufal and Termos (Citation2009).

Additionally, one of the main empirical findings of our study is that although the increase in inflation reduces the ability of foreigners in Saudi Arabia to transfer money abroad, its effect is clearly limited compared to the capital investment indicator, which is associated with higher elasticity. This result is in line with the recommendation of Alkhathlan (Citation2013): “Saudi Arabia must find appropriate new channels to convince foreign workers to consume and invest their money in the country.”

The estimation results shown in Table also reveal that all the explanatory variables have the theoretical expected long-run impacts. The elasticity of Saudi GDP is positive and statistically significant, and a 1% increase in Saudi Arabia’s GDP increases remittance outflows by 1.38% in the long run. There are two possible justifications for this positive relationship. First, the increase in Saudi Arabia’s GDP increases the level of economic activity, which, in turn, increases the demand for domestic labor and foreign workers (AlKhathlan, Citation2013; Javid & Hasanov, Citation2022). This can be seen from the fivefold increase in the level of GDP during the study period (1971–2019), which is associated with a 22-fold increase in the number of expatriates during the same period, which would lead to an increase in remittance outflows. Second, the increase in the level of economic activity—and hence labor demand—would increase the average wage, thereby increasing remittance outflows.

Finally, we acknowledge that this study has one limitation: it does not include the number of foreign workers due to a lack of data. Previous studies have revealed this variable’s positive effect on remittances (Chami et al., Citation2005; El-Sakka & Mcnabb, Citation1999; Swamy, Citation1981).

6. Conclusions and policy recommendations

Numerous empirical studies have focused on the impact of remittance inflows on economic performance in receiving developing countries. However, most of the research on remitting countries has focused on the role of remittance outflows in determining selected macroeconomic variables. In contrast, factors like the impact of inflation on remittance outflows have not attracted much attention due to the relatively small share of remittance outflows of GDP, especially in GCC countries. Recently, Saudi Arabia has begun to focus on the high level of migrant remittances. This study is an attempt to determine whether high inflation in KSA reduces remittance outflows. Thus, this research stems from the hypothesis that there is an inverse relationship between inflation and remittance outflows in Saudi Arabia. To examine this relationship in the long and short term with the presence of different degrees of integration -I(0) or I(1)- among variables, the ARDL model is employed regardless of the degree of integration (Pesaran et al., Citation2001).

To find out the direction of causality between the two main variables, we used the Granger causality test based on the H. Y. Toda and Yamamoto (Citation1995) method, since it has the advantage of not requiring integration and cointegration of variables. The causality test result shows a unidirectional causality running from inflation rate to remittance outflows, which implies that price indicator causes remittance outflows.

We examined the potential long-run and short-run impacts of inflation, along with selected control variables, on the outflow of remittances from Saudi Arabia over the period 1971–2019 by applying the ARDL bounds test to cointegration. The empirical estimation results revealed a long-run equilibrium relationship between the selected variables in this study. The empirical results show an inverse relationship between migrant remittance outflows and inflation in Saudi Arabia. The inflation rate coefficient implies that a 10% increase in inflation reduces remittance outflows by 3.2%; a reduction in remittance outflows by a small percentage of 3.2% requires a significant (threefold) increase in the inflation rate. Thus, foreign remittance outflows are weakly responsive to changes in inflation. Since the elasticity of remittance outflows to the inflation rate is low, migrant workers will likely remit a significant amount of their money abroad no matter how high inflation is in Saudi Arabia. This empirical result also suggests that migrant workers in KSA will be able to adjust their consumption patterns to rising prices over time in order to maintain their remittance levels. The weak elasticity in Saudi Arabia can be attributed to the acceptable inflation rates, the absence of hyperinflation, and the pegged Saudi Riyal exchange rates against the US dollar over the past five decades. Hence, policymakers should consider that opting to raise inflation as a consequence of any economic policy would not have a considerable effect on remittance outflows.

Our empirical findings reveal that remittance outflows in Saudi Arabia are strongly influenced by factors such as capital investment rather than general prices.

It is well documented in the literature that the number of expatriates has a significant impact on the volume of remittances (Chami et al., Citation2005; El-Sakka & Mcnabb, Citation1999; Swamy, Citation1981). However, this variable is not considered in the present study, as there is no data available for the study period. In addition to the number of migrant workers, other macroeconomic variables affect remittance outflows. Although our results suggest that inflation reduces remittance outflows in the KSA, this study does not explain the nature of this relationship. Therefore, it would be interesting to investigate whether there is an asymmetric relationship between inflation and remittance outflows in the KSA, i.e., whether a positive shock to the inflation rate has a different effect than a negative shock to inflation. Thus, the present study leaves the door open for future research using more variables and other estimation methodologies.

These findings may be useful to policymakers, as remittance outflows have adverse impacts on the development of the Saudi economy. Indeed, remittances are considered the main channel for the leakage of Saudi Arabia’s foreign reserves. A large volume of applied research has found that the outflow of remittances has a negative impact on essential economic activities such as economic growth, consumption and investment. Moreover, these results may prove important and useful for policymakers because KSA has expressed a desire for changes in its labor market policies to facilitate economic participation among Saudis.

The Saudi authorities should continue to encourage and urge private companies to hire more Saudi workers, with a commitment to train and qualify them to meet the demands of the labor market. In order to reduce the volume of remittance outflows from Saudi Arabia, the Saudi policy makers are invited to encourage foreign workers, especially those with high incomes, to invest in Saudi Arabia by facilitating their ownership of financial market shares and real estate units.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

The authors express their gratitude to all of the individuals mentioned in the references who contributed to/for the purpose of this study.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Bashier Al-Abdulrazag

Bashier Al-Abdulrazag is a Professor of economics at King Saud University (KSA) and Mu’tah University (Jordan). Holding PhD in economics Graduated from Texas Tech. University USA in 1991. His research interests focus on Labor Economics, Applied Econometrics (TSA), Economic Theory, and International Trade. He published in various Journals: The Journal of Energy and Development, European Scientific Journal, Journal of Empirical Economics., The Jordan Journal for Agricultural Science. Moreover, participating in refereeing for many journals, supervising many graduate theses.

Musa Foudeh

Musa Foudeh is an Associate Professor of Economics at Imam Mohammad Ibn Saud Islamic University, College of Economics and Administrative Sciences and holds a PhD. in Economics from University of Limoges, France. He is a university lecturer in economics with strong academic and teaching background, possessing 12 years of academic experience and six years of banking experience. Foudeh research interests are in the areas of Privatization, Energy Economics, Economic Development and Applied Economics.

References

- Abdel‐Rahman, A.-M.-M. (2006). The determinants of foreign worker remittances in the Kingdom of Saudi Arabia. Journal of King Saud University, 18(2), 93–23. https://cba.ksu.edu.sa/sites/cba.ksu.edu.sa/files/imce_images/lbhth_lthlth_mn_mjld_18dd2.pdf

- Aggarwal, R., Demirgüç-Kunt, A., & Peria, M. S. M. (2011). Do remittances promote financial development? Journal of Development Ecomomics, 96(2), 255–264. http://www.sciencedirect.com/science/article/pii/S0304387810001161

- Ahmed, J., & Inmaculada, M.-Z. (2014). What drives bilateral remittances to Pakistan? A gravity model approach. Centre for European Governance and Economic Development. ECONSTOR. https://www.econstor.eu/bitstream/10419/97486/1/786982659.pdf

- Al-Abdulrazag, B. (2018). The impact of remittances on the import demand function in Jordan: An ARDL bounds testing approach. European Scientific Journal, ESJ, 14(10), 304. https://doi.org/10.19044/esj.2018.v14n10p304

- Al-Abdulrazag, B., & Abdel-Rahman, A.-M.-M. (2016). Remittances and financial development in a Host Economy: The case of the Kingdom of Saudi Arabia. International Review of Management and Business Research, 5(3), 1134–1150. https://www.irmbrjournal.com/papers/1475479828.pdf

- Al-Kaabi, F. (2016). The nexus between remittance outflows and GCC growth and inflation. Journal of International Business and Economics, 4(1), 76–85. https://doi.org/10.15640/jibe.v4n1a7

- Alkhathlan, K. A. (2013). The nexus between remittance outflows and growth: A study of Saudi Arabia. Economic Modelling, 33, 695–700. https://doi.org/10.1016/j.econmod.2013.05.010

- Allen, D. S., & Ndikumana, L. (2000). Financial intermediation and economic growth in Southern Africa. Journal of African Economies, 9(2), 132–160. https://doi.org/10.1093/jae/9.2.132

- Aslam, A. L. M., & Selliah, S. (2020). Empirical relationship between workers' remittances and financial development (an ARDL cointegration approach for Sri Lanka). International Journal of Social Economics, Emerald Group Publishing, 47(11), 1381–1402. https://doi.org/10.1108/IJSE-03-2020-0157

- Asteriou, D., & Hall, S. G. (2007). Applied econometrics: A modern approach. PALGRAVE MACMILLAN.

- Balderas, J. U., & Nath, H. K. (2008). Inflation and relative price variability in Mexico: The role of remittances. Applied Economics Letters, 15(3), 181–185. https://doi.org/10.1080/13504850600722070

- Barua, S., Majumdar, M. D., & Akhtaruzzaman, M. (2007). Determinants of workers’ remittances in Bangladesh: An empirical study. Bangladesh Bank Working Paper WP 0713. Munich Personal RePEc Archive Available Online at: https://mpra.ub.uni-muenchen.de/15080/

- Bettin, G., Presbitero, A. F., & Spatafora, N. (2017). Remittances and vulnerability in developing countries. IMF Working Paper WP/14/13. World Bank Economic Review Available online at : https://doi.org/10.1093/wber/lhv053

- Boon, T. H. (2000). Saving, investment and capital flows: An empirical study on the ASEAN economies. In Chapter 3 in ASEAN in an interdependent world (1st) ed.) (pp.13). Routledge.

- Bouoiyour, J., Selmi, R., & Miftah, A. (2019). The relationship between remittances and macroeconomic variables in times of political and social upheaval: Evidence from Tunisia’s Arab spring. Economics of Transition and Institutional Change, 27(2), 355–394. https://doi.org/10.1111/ecot.12199

- Cazachevici, A., Havranek, T., & Horvath, R. (2020) Remittance and economic growth: A meta-analysis. World Development, 134 Article 105021, 105021. https://doi.org/10.1016/j.worlddev.2020.105021

- Chami, R., Fullenkamp, C., & Jahjah, S. (2005). Are immigrant remittance flows a source of capital for development? IMF Staff Papers, 52(1), 55–81. https://doi.org/10.5089/9781451859638.001

- De, S., Quayyum, S., Schuettler, K., & Yousefi, S. R. (2019). Oil prices, growth, and remittance outflows from the Gulf Cooperation Council. Economic Notes, 48(3), e12144. https://doi.org/10.1111/ecno.12144

- Desai, M. A., Kapur, D., McHale, J., & Rogers, K. (2009). The fiscal impact of high-skilled emigration: Flows of Indians to the U.S. Journal of Development Economics, 88(1), 32–44. https://doi.org/10.1016/j.jdeveco.2008.01.008

- Ebeke, C. (2011). Remittances, countercyclicality, openness and government size. Recherches Économiques De Louvain/Louvain Economic Review, 77(4), 89–114. https://doi.org/10.3917/rel.774.0089

- Edrees, A. (2016). The impact of foreign workers, outflow remittances on economic growth in selected GCC countries: ARDL approach. Arabian Journal of Business and Management Review, 6(5), 1–4. https://doi.org/10.4172/2223-5833.1000250

- El-Sakka, M. I. T., & Mcnabb, R. (1999). The macroeconomic determinants of emigrant remittances. World Development, 27(8), 1493–1502. https://doi.org/10.1016/S0305-750X(99)00067-4

- Enders, C. K. (2003). Performing Multivariate Group Comparisons Following a Statistically Significant MANOVA. (Methods, Plainly Speaking). Measurement and Evaluation in Counseling and Development, 36, 40–56. https://doi.org/10.1080/07481756.2003.12069079

- Engle, R. F., & Granger, C. W. J. (1987). Cointegration and error correction representation: Estimation and testing. Econometrica, 55(2), 251–276. https://doi.org/10.2307/1913236

- Ezeoha, A. E. (2013). Financial determinants of international remittance flows to the Sub-Saharan African region. International Migration, 51, e84–e97 . https://doi.org/10.1111/imig.12061

- Fawad, A. (2013). The effect of oil prices on unemployment: Evidence from Pakistan. Business and Economics Research Journal, 4(1), 43–57. http://www.berjournal.com/

- General Authority for Statistics (GaStat). 2019. “The Statistical Yearbook, 2019 A.D (1440/1441 A.H).” https://www.stats.gov.sa/en/25

- Granger, C. W. J. (1981). Some properties of time series data and their use in econometric model specification. Journal of Econometrics, 16, 121–130. https://doi.org/10.1016/0304-4076(81)90079-8

- Gupta, S., Pattillo, C. A., & Wagh, S. (2009). Effect of remittances on poverty and financial development in Sub-SaharanAfrica. World Development, 37(1), 104–115. https://doi.org/10.1016/j.worlddev.2008.05.007

- Haddad, H. B., & Choukir, J. (2017). Short- and long-run effects of remittance outflow shocks on the Saudi Arabian economy. International Journal of Economics and Business Research, 14(2), 194–213. https://doi.org/10.1504/ijebr.2017.10007794

- Iqbal, J., Nosheen, M., & Javed, A. (2013). The nexus between foreign remittances and inflation: Evidence from Pakistan. Pakistan Journal of Social Sciences, 33(2), 331–342. https://www.researchgate.net/publication/284351087_The_Nexus_between_Foreign_Remittances_and_Inflation_Evidence_from_Pakistan

- Janesh, S. (2013). Remittances, banking sector development and economic growth in Fiji. International Journal of Economics and Financial Issues, 3(2), 503–511. https://www.econjournals.com/index.php/ijefi/article/view/275

- Javid, M., & Hasanov, F. J. (2022). Determinants of remittance outflows: The case of Saudi Arabia. The King Abdullah Petroleum Studies and Research Center (KAPSARC). IDEAS. https://ideas.repec.org/p/prc/dpaper/ks–2022-dp05.html

- Johansen, S. (1988). Statistical Analysis of Cointegration Vectors. Journal of Economic Dynamics and Control, 12(2–3), 231–254. https://doi.org/10.1016/0165-1889(88)90041-3

- Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica, 59(6), 1551–1580. https://doi.org/10.2307/2938278

- Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration with applications to the demand for money. Oxford Bulletin of Economics and Statistics, 52(2), 169–210. https://doi.org/10.1111/j.1468-0084.1990.mp52002003.x

- Kadozi, E. (2019) Remittance inflows and economic growth in Rwanda. Research in Globalization, 1 Article 100005, 100005. https://doi.org/10.1016/j.resglo.2019.100005

- Khan, Z. S., & Islam, S. (2013). The effects of remittances on inflation: Evidence from Bangladesh. Journal of Economics and Business Research, 19(2), 198–208. https://www.econbiz.de/Record/the-effects-of-remittances-on-inflation-evidence-from-bangladesh-khan-zakir-saadullah/10009756209

- Kumar, R. R. (2012). Role of trade openness, remittances, capital inflows, and financial development in Vanuatu: Migration and remittances during the global financial crisis and Beyond (pp. 325–333). World Bank.

- Kumar, B. (2021). Construction of household welfare index and welfare impact of international remittances in Rural Bangladesh. Preprints 2021, 20210505512021050551. Preprints. https://doi.org/10.20944/preprints202105.

- Lastovetska, R. (2017). Mechanisms of remittances influence on the economy of Ukraine. Handel Wewnetrzny, 366(1), 30–40. https://www.ceeol.com/search/article-detail?id=543968

- Lianos, T. P. (1997). Factors determining migrant remittances: The case of Greece. International Migration Review, 31(1), 72–87. https://doi.org/10.1177/019791839703100104

- Lueth, E., & Ruiz-Arranz, M. (2006). A gravity model of workers’ remittances. IMF Working Paper WP/06/290. International Monetary Fund. https://www.imf.org/external/pubs/ft/wp/2006/wp06290.pdf

- Mahmoudinia, D., Amroabadi, B. S., Pourshahabi, F., & Jafari, S. (2013). Oil products consumption, electricity consumption-economic growth nexus in the economy of Iran: A bounds testing cointegration approach. International Journal of Academic Research in Business and Social Sciences, 3(1), 353. https://hrmars.com/index.php/IJARBSS/article/view/9433/Oil-products-Consumption-Electricity-Consumption-Economic-growth-Nexus-in-the-Economy-of-Iran-A-Bounds-Testing-Co-integration-Approach

- Makhlouf, F., & Kasmaoui, K. (2017). The impact of oil price on remittances: The case of Morocco. The Journal of Energy and Development, 43(1/2), 239–310. https://www.researchgate.net/publication/329738944_The_impact_of_oil_price_on_remittances_The_case_of_Morocco

- Meyer, D., & Shera, A. (2017). The impact on economic growth: An econometric model. Economia, 18(2), 147–155. https://doi.org/10.1016/j.econ.2016.06.001

- Moftah, N. A., & Dilek, S. (2021). Toda-Yamamotto causality test between energy consumption and economic growth: Evidence from a panel of Middle Eastern Countries. Journal of Empirical Economics and Social Sciences, 3(1), 56–78. http://dx.doi.org/10.46959/jeess.651976

- Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. https://doi.org/10.1080/00036840500278103

- Narayan, P. K., Narayan, S., & Mishra, S. (2011). Do remittances induce inflation? Fresh evidence from developing countries. Southern Economic Journal, 77(4), 914–933. https://doi.org/10.4284/0038-4038-77.4.914

- Naufal, G., & Genc, I. (2018). Impact of remittance outflows on sending economies: The case of the Russian Federation. Asia-Pacific Population Journal, 32(2), 61–85. https://doi.org/10.18356/f61bc783-en

- Naufal, G., & Termos, A. (2009). The responsiveness of remittances to price of oil: The case of the GCC. OPEC Energy Review, 33(3–4), 184–197. https://doi.org/10.1111/j.1753-0237.2009.00166.x

- Nkoro, E., & Uko, A. K. (2016). Autoregressive Distributed Lags (ARDL) cointegration technique: Application and interpretation. Journal of Statistical and Econometric Methods, 5(4), 63–91. http://www.scienpress.com/Upload/JSEM%2fVol%205_4_3.pdf

- Opperman, P., & Adjasi, C. K. D. (2019). Remittance volatility and financial sector development in sub-Saharan African countries. Journal of Policy Modeling, 41(2), 336–351. https://doi.org/10.1016/j.jpolmod.2018.11.001

- Osterwald Lenum, M. (1992). A Note with Quantiles of the Asymptotic Distribution of the Maximum Likelihood Cointegration Rank Test Statistics1. Oxford Bulletin of Economics and Statistics, 54, 461–472. https://doi.org/10.1111/j.1468-0084.1992.tb00013.x

- Panda, D. P., & Trivedi, P. (2015). Macroeconomic determinants of remittances. Journal of International Economics, 6(2), 83–100. https://www.proquest.com/docview/1790896535?parentSessionId=w8OsOfuKieGED3IXDdKkMEo0dSwl6AVkvjUZbAysKxA%3D

- Pesaran, M. H., Shin, Y., & Smith, R. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Rahmouni, O., & Debbiche, I. (2017). The effects of remittances outflow on economic growth in Saudi Arabia: Empirical evidence. Journal of Economics and International Finance, 9(5), 36–43. https://doi.org/10.5897/JEIF2017.0828

- Rao, B. B., & Hassan, G. M. (2011). A panel data analysis of the growth effects of remittances. Economic Modelling, 28(1–2), 701–709. https://doi.org/10.1016/j.econmod.2010.05.011

- Rapoport, H., & Docquier, F. (2005). The Economics of Migrants’ Remittances. IZA DP No. 1531. http://dx.doi.org/10.2139/ssrn.690144

- Ratha, D., Scheuttler, K., & Yousefi, S. R. (2015). Will falling oil prices lead to a decline in outward remittances from GCC countries. In L. Mottaghi & S. Devarajan (Eds.), Annex 1 in Plunging oil prices. MENA Quarterly Economic Brief (pp. 26–28). Washington, DC: World Bank. https://blogs.worldbank.org/peoplemove/will-falling-oil-prices-lead-decline-outward-remittances-gcc-countries

- Salameh, H., & Aldaarmi, A. (2019). Is outflow of workers’ remittances affecting the Kingdom of Saudi Arabia’s economy in the long run? Journal of Economic Issues, 13(2), 5–13. https://www.researchgate.net/publication/340580301_

- Sayan, S. (2004). Guest workers’ remittances and output fluctuations in Host and Home Countries: The case of remittances from Turkish workers. Emerging Markets Finance and Trade, 40(6), 70–84. https://doi.org/10.1080/1540496X.2004.11052590

- Shahbaz, M., Zeshan, M., & Afza, T. (2012). Is energy consumption effective to spur economic growth in Pakistan? New evidence from bounds test to level relationships and Granger causality tests. Economic Modelling, 29(6), 2310–2319. https://doi.org/10.1016/j.econmod.2012.06.027

- Swamy, G. (1981). International migrant workers’ remittances: Issues and prospects. The World Bank Staff Working Paper. https://www.oecd.org/els/mig/38840502.pdf

- Taghavi, M. (2012) The impact of workers’ remittances on macro indicators: The case of the gulf cooperation council. Topics in Middle Eastern and North African economies. Electronic Journal. 14 Middle East Economic Association and Loyola University Chicago. http://www.luc.edu/orgs/meea/

- Termos, A., Naufal, G., & Genc, I. (2013). Remittance outflows and inflation: The case of the GCC countries. Economics Letters, 120(1), 5–47. https://doi.org/10.1016/j.econlet.2013.03.037

- Toda, H., & Phillips, P. (1993). Vector Autoregressions and causality. Econometrica, 61(6), 1367–1393. https://doi.org/10.2307/2951647

- Toda, H. Y., & Yamamoto, T. (1995). Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics, 66(1–2), 225–250. https://doi.org/10.1016/0304-4076(94)01616-8

- Umoru, D., & Tizhe, N. A. (2014). Causality dynamics between money supply and inflation in Nigeria: A Toda-Yamamoto test and error correction analysis. Journal of Empirical Economics, 3(2)63–75. https://ideas.repec.org/a/rss/jnljee/v3i2p2.html

- World Energy Outlook. (2019). Data and Statistics: https://webstore.iea.org/world-energy-outlook-2019

- World Migration report., 2020: https://publications.iom.int/system/files/pdf/wmr_2020.pdf

- Zapata, H. O., & Rambaldi, A. N. (1997). Monte Carlo evidence on cointegration and causation. Oxford Bulletin of Economics and Statistics, 59(2), 285–298. https://econpapers.repec.org/article/blaobuest/v_3a59_3ay_3a1997_3ai_3a2_3ap_3a285-98.htm