?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Despite the long history of testing agency theory, it is yet standing undefeated. This study examines the relationship between capital structure and firm performance in an emerging economy, Iraq. Moreover, it seeks to find an answer for the question “does agency cost moderates the relationship between capital structure and financial performance?” in the case of a developing industrial sector. Data was collected from published financial statements from the Iraqi Stock Exchange. The study sample consists of several companies from industrial sector listed on ISX over the period 2004–2020. Firm performance is measured using both accounting data and market indicator. Agency cost is measured through operating expense ratio and asset utilization ratio. Testing for short-term and long-term parameters between groups, pooled mean group estimation method is used for data analysis. The results manifest evidence to support agency theory in explaining the relationship between capital structure and financial performance. Moreover, strong interactions are found indicating that agency cost has a considerable impact on the capital structure and firm performance association, that is, agency cost moderates the relationship between capital structure and firm performance. These results are robust checking various methods and diagnostics checks. These results are key evidence from an emerging country, Iraq to support the agency theory arguments. The results provide significant insights for managers of the sector particularly for the current rapid development in the sector.

1. Introduction

The conflict of interest among different stakeholders, particularly between principal and agent, creates cost for enterprises. Such cost is commonly known in business and is theoretically explained through agency cost theory. There are reasons for the separation of ownership and management in industrial companies. Most enterprises require large sums of capital to achieve economies of scale. Professional managers may be more qualified to run the business because of their technical expertise, experience, and personality traits. The separation of ownership and management allows for unlimited change in ownership through share transfers without disrupting the firm’s operations. However, managers may attempt to reach a specific degree of acceptable performance in terms of shareholder welfare. These factors cause the arise of conflict of interest between shareholders and managers. This study aims to examine the moderating effect of agency cost on the relationship between capital structure and financial performance.

The agency theory explains the notion of separation of ownership and control in firms, and it emphasizes ownership structure and firm performance. Understanding the agency theory application in financial management is important because it gives greater insight for investors, stockholders, and those concerned about this issue, which create so-called “agency costs.” The agency cost is the cost incurred in scrutinizing and controlling the managers and trying to eliminate their exploitation. One way to reduce the agency problem is to use debt in financing policy. The agent usually wants to maximize his own benefit by increasing his personal wealth and job security, while the principal wants to maximize his own wealth (Abdulah & Tursoy, Citation2022; Kalash, Citation2019). Agency costs of equity arise when the interests of the shareholders differ from those of the managers. These costs may be reduced by good planning. The most famous and widely used theoretical framework for examining the conflict of interest during the operation of a firm and its management decision process is the agency theory. The current research is mostly concerned with agency theory. According to the primary assumption of this theory, agency theory has a positive impact on financial performance (Berger & Di Patti, Citation2006; Dawar, Citation2014; Tarazi, Citation2019).

The capital structure of a company, which is a combination of debt and equity, can be found on the balance sheet. Company assets, also listed on the balance sheet, are purchased with debt or equity. Capital structure can be a mixture of a company’s long-term debt, short-term debt, common stock, and preferred stock (Abdullah, Citation2021). A company’s proportion of short-term debt versus long-term debt is considered when analyzing its capital structure. Managers decision regarding financing policy could create agency cost (Dawar, Citation2014). Thus, there is evidence that capital structure influences firm financial performance (Abdullah & Tursoy, Citation2021b; Liao et al., Citation2022). The results from literature are mix and studies yet recommend more investigations need to be conducted from developing countries (Kontuš, Citation2021).

Proposals on capital structure began in the late 1950s, when the first theory attempting to explain this issue appeared. The irrelevance theory of Modigliani and Miller (Citation1958), the MM theory of capital structure, was developed as a theoretical foundation for the capital structure issue. According to theory, there is no optimal capital structure for firms. Moreover, Modigliani and Miller (Citation1963) revised their previous work and liberated the MM theory assumptions from taxation. They also mentioned that the market value of a firm with a proportion of debt on its balance sheet outperforms that of a firm that relies solely on equity financing. The key assumptions of the MM theory are based on the conditions of a perfect capital market. Previous empirical research has given some support or assumptions to this theory (Abdullah & Tursoy, Citation2021a; Le & Phan, Citation2017) for the relationship between capital structure and financial performance in both developed and emerging economies. In addition, some of the studies have different results in determining the relationship between capital structure and firm performance by controlling different variables (Abdullah, Citation2020; Imelda & Dewi, Citation2019; Jouida, Citation2018).

The objectives of this study are several. It aims to investigate the nature of relationship between capital structure and financial performance of industrial firms from an emerging market. Agency theory is mainly used to build the theoretical relationship. Moreover, it examines the impact of agency cost on firm financial performance and seeks to answer the question whether agency cost has any moderating effect on the relationship between capital structure and financial performance. Investigating such issues from an emerging economy, namely Iraq, can provide significant insights and highly contribute to the current literature. The industrial sector of Iraq is the largest after oil and gas. The sector is going through a rapid development with the support of government’s strategy to develop the private non-oil sectors in the country. The country has been attempting to diversify its sources of government revenue and the industrial sector is considered as on of the stable sources of economic growth. A good health of this sector’s financial performance can highly contribute to the growth and assist the country achieve the aim.

The current study varies from previous studies in that it explores how agency cost affects financial performance through its relationship with the capital structure in Iraqi industrial firms using a large body of data. This study includes a considerably large number of observations, 187 firm-year, over a long period of time, 2004–2020 from an emerging country. Therefore, the sample consists of 11 firms from 17 years, that is, balanced panel data is sample traits. This study examines the relationship between capital structure and financial performance, considering the moderating effect of agency theory on this relationship. Previous research provides some support for the relationship between capital structure and financial performance in both developed and developing nations. Nonetheless, no research, to our knowledge, has studied the moderating effect of agency cost on that association. This study could contribute to the existing literature and provide empirical evidence around the relationships among capital structure, agency cost and financial performance from an emerging market.

The development of our paper proceeds as follows: literature review and hypotheses development, methodology, data analysis, discussion of the results, and conclusions.

2. Literature review

Financial performance is defined as a reflection of the ability of the firm to achieve its objectives (Abdullah & Tursoy, Citation2021a). According to Ali (Citation2018), financial performance is referred to as a measure of the efficiency and effectiveness of an organization’s internal as well as external actions and operations. Moreover, it is frequently used in literature to determine a company’s success, conditions, and compliance. Mansyur et al. (Citation2020) explain financial performance as a result of managers’ efforts in carrying out tasks related to financial management. From these definitions of, we observe the common understanding about financial performance as a mirror that reflects the accomplishments of a company’s goals, while others believe it is the effective use of the resources available to the company. Consequently, it can be claimed that financial performance measures the financial health of firms. This is demonstrated by using several indicators to identify how successful and efficient a company is in managing its resources for operations, financing, and investment activities. Many factors can have an impact on financial performance (Liu et al., Citation2022), and capital structure is one of the key variables to have potential influencing firm financial performance.

Financing decision considers the way that assets are accumulated in a firm through the methods of debt or equity financing. The mixture of debt and equity of financing policy is referred to as capital structure. The way that the assets are financed has potential to influence firm financial performance. Several theories were developed in literature to explain this relationship such as MM theory, trade-off theory, pecking order theory, and the most importantly agency theory (Abdullah & Tursoy, Citation2021b).

The irrelevance theory of Modigliani and Miller (Citation1958) is the first theory attempting to explain capital structure issue. Accordingly, there is no optimal capital structure for firms to consider. The theory is based on a set of assumptions about a perfectly efficient market with no taxes, no risk of bankruptcy, and no information asymmetry. Moreover, Modigliani and Miller (Citation1963) revised their previous work and liberated it from no taxation assumption. They also mentioned that performance of a firm with a portion of debt on its balance sheet outperforms that of a firm that relies solely on equity financing (Ankamah-Yeboah et al., Citation2021). The reason is firms take advantage of the tax shield of debt. This is the proposition of trade-off theory (Abdullah, Citation2020), arguing that firms prefer debt to equity when benefit of debt through interest expense deduction before income tax calculation is larger than the cost of debt, the interest expense itself. The relationship between capital structure and financial performance may differ depending on the context. According to the existing research, a variety of situations, such as the country’s development level and firm size, tend to impact the nature of the relationship between capital structure and financial performance (Abdullah & Tursoy, Citation2021a; Li et al., Citation2018; Mansyur et al., Citation2020).

The agency theory, initially developed by Berle and Means (Citation1932), posits that managers pursue their own interests instead of maximizing returns to shareholders. Agency theory terms include the owners, who are principals, and the managers, who are agents, and there is an agency cost, which is the extent to which returns to the residual claimants, the owners, fall below what they would be if the principals, the owners, exercised direct control of the corporation (Jensen & Meckling, Citation1976). It is claimed that with high debt, managers are under pressure to invest in profitable projects to create cash flow to pay off the debt (Jensen, Citation1986). The key element of the agency theory is the conflict of interest (Shrestha, Citation2019). The theory is concerned with resolving problems that arise as a result of a conflict of interest between the principal and agent (Nidumolu, Citation2018). As a result, firm performance maximization could be achieved (Abdullah et al., Citation2021). The lower the agency cost the higher the financial performance is expected. Additionally, Tuan et al. (Citation2019) confirm that debt can be a useful tool for reducing the negative impact of agency costs on financial performance because of the pressure on managers to pay back the debts. Thus, managers are less able to concentrate on their own interest and thus the conflict of interest is reduced.

Despite the massive examination of the agency theory over the last several decades since its appearance, it is still standing against the hypotheses. Miller (Citation1977) measured the association between capital structure and firm value by using agency cost theory and some other theories; namely, MM theory, pecking order theory, and trade-off theory. Using opposing techniques, the study found a positive relation between capital structure and financial performance. Additionally, the study found evidence to support agency theory. Other studies found that capital structure has a positive effect on financial performance (Abdullah, Citation2020; Jouida, Citation2018) under different context. Moreover, several studies looked at whether the association between a firm’s capital structure and performance is significantly negative (Al-Imam & Hassan, Citation2019; Al-Qudah, Citation2017; Li et al., Citation2018). Some other studies use different data or measurements to defend both negative and positive statistical findings among them (Abdullah & Tursoy, Citation2021a; Ngatno et al., Citation2021; Sultan & Adam, Citation2015; Tretiakova et al., Citation2021). Other studies found no effect of capital structure on firm performance (Al-Taani, Citation2013; Berger & Di Patti, Citation2006).

This study also measured the effect of agency theory on financial performance. Based on the assumptions by Jensen and Meckling (Citation1976), agency cost is associated with firm performance. Empirically, Kontuš (Citation2021) found evidence to propose that variations in agency costs have little or no impact on the firm performance in Croatia. Tuan et al. (Citation2019) found evidence for the existence of a negative association between agency cost and financial performance in the case of Vietnam. Similar results found for Chinese listed firms by Khan et al. (Citation2020). However, some studies determine positive relationship between agency cost and financial performance; Pandey and Sahu (Citation2019) in the case of India and Wellalage and Locke (Citation2013) in Sri Lanka.

Agency cost, measured through the expense ratio, could have moderate effect on the relationship between capital structure and firm performance. The higher the expense ratio, the lower the retained earnings would be. Thus, firms would rely on external source of funding, equity or debt. Muneer et al. (Citation2013) review the literature around the moderating role of agency theory. Corresponding to the objective of the study, we develop the following three null hypotheses:

H1: capital structure is negatively related to financial performance

H2: agency cost is inversely related to financial performance

H3: agency cost moderates the capital structure and financial performance relation.

3. Methodology

3.1. Sample and data

Initially, the data sample consists all listed firms on Iraq Stock exchange working in the industrial sector. This sector in Iraq has gone through several phases in recent history. The initiation of some industries is seen as milestones for the sector, that is, opening the first industries such as grain mills, cotton gin, small craft making, and hand weaving workshops. Recently, the government set laws and regulations for the sector such as the Investment Law (2006), the Ministry of Industry and Minerals Law (2011), the Industrial Cities Law (2018), and the industrial national development plan of 2018–2022. There are 25 industrial firms listed on the market as per 2022 data, producing food, beverages, medicine, furniture, packaging, construction materials. Firms with their data available over 2004–2020 period are included in the sample and the others are excluded. Considering a balanced panel data, the final sample consists of 187 firm-year observations, 11 firms over 17 years period. Data is collected from the Iraq Stock Exchange (Citation2021) website. Table shows the sample firms with their stock price and book value per share in Iraqi Dinar as at the end of quarter 2/ 2022.

Table 1. Study sample firms

3.2. The variables

3.2.1. Financial performance

Financial performance is the dependent variable. Theoretically, it is predicted that it will be influenced by internal factors such as capital structure. There are different measures of financial performance used in the literature. Scholars use accounting data to create measures based on ratios from balance sheets and income statements. The accounting measures of profitability ratios include return on assets, return on equity and profit margin (Abdullah, Citation2021; Ankamah-Yeboah et al., Citation2021; Li et al., Citation2018). Others use market performance indicators such as market to book value, share price volatility and Tobin’s Q (Abdulah & Tursoy, Citation2022; Para et al., Citation2022; Rasul, Citation2018; Tretiakova et al., Citation2021). Therefore, the current study uses return on asset and market-to-book value ratio (see, Table ).

Table 2. Definition of variables

3.2.2. Capital structure

The capital structure is an independent variable and one of the significant variables that describe the findings of this study, which are predicted to have an impact on financial performance according to the theories. The capital structure is a combination of debt and equity in the firm’s form of financing (Kontuš, Citation2021). The capital structure is measured in the literature by different ratios of financial leverage, such as long-term debt ratio, short-term debt ratio, debt to equity ratio, equity multiplier, and total debt to total assets (Al-Qudah, Citation2017; Ibhagui & Olokoyo, Citation2018; Li et al., Citation2018; Sultan & Adam, Citation2015; Tripathi, Citation2019). In this study, we measured the capital structure using both debt ratios and equity ratios (see, Table ).

3.2.3. Agency theory

According to the agency’s theory, the conflict of interest among stakeholders create agency cost. Agency cost is an independent variable in this study. It also plays a moderating role on the relation between capital structure and firm performance. Agency cost is measured in the literature as asset utilization ratio and operating expense ratio (Muneer et al., Citation2013; Tuan et al., Citation2019). The asset utilization ratio is used as an agent for the cost of equity agency. This ratio measures how successfully management uses the firm’s assets. In another word, it assesses management’s capacity to make optimal use of assets (Ang et al., Citation2000; Kontuš, Citation2021; Mcknight & Weir, Citation2009). Additionally, operating expense ratio is also used, as in our study too, to determine the agency cost through operating expense over total sales (Imelda & Dewi, Citation2019; Singh & Davidson, Citation2003). Operating expenses ratio is believed to show management’s judgment in allocating firm resources.

3.2.4. Control variables

This study investigates the effects of capital structure on financial performance as well as the agency theory on financial performance as a moderator. Consistent with the literature and aiming to control for firm-specific factor, (Abdullah & Tursoy, Citation2021a; Li et al., Citation2018), this study controls for firm size. According to Ibhagui and Olokoyo (Citation2018), firm size could have a significant effect on the relationship between capital structure and firm performance. Larger firms have higher investment opportunities due to their wider financing sources (Saed et al., Citation2021). Moreover, larger companies find it simpler to create funds internally and to obtain it from external sources as well (Ghafar et al., Citation2021). Firm size is measured through the natural logarithm of total assets (Abdullah & Tursoy, Citation2021b; Ardalan, Citation2017).

3.3. Method and model

This study uses a quantitative approach for secondary data disclosed by listed firms on Iraq Stock Exchange. An explanatory research design is used to investigate the proposed relationships. Regarding the data analysis method, the pooled mean group (PMG) estimator is performed. It is suitable for dynamic heterogeneous panels (Zaman et al., Citation2020). This method constrains long-run coefficients to be homogeneous but permits short-run coefficients and residual variances to vary across groups (Pesaran et al., Citation1999). The selection of the model is also based on the unit root and cointegration tests. The selected variables are I (0) and cointegrated over long-run. The equation for panel ARDL is given below:

Where, the dependent variable if financial performance (FFP) and the lagged value is used as independent; while X are other independent variables including capital structure measures, agency cost and control variable.

Based on the lag length, we select our model. The lag length is determined according to minimum value of Akaike Information Criterion (AIC). For observing short-run and long-run effects, pooled mean group estimator provides the results separately. The value of error correction term is given to show the convergence of the variables in the long-run. The specific model for PMG is given below:

Where

presents the differencing of the variables due to having unit root at level. EC shows the error correction term which elaborates the convergence or divergence, depending on the numerical value sign, of the model in the long-run. θ is adjustment coefficient while β illustrates long-run coefficient.

4. Data analysis

4.1. Descriptive statistics

Table summarize the descriptive statistics of the variables employed in the study, for the sample industrial companies over the years 2004–2020. ROA mean value is −0.016 with SD = 0.35, where MBV has the greater mean value and a higher standard deviation (M = 3.07; SD = 3.39). Mean value of agency cost measures are; EXR (M = 0.36; SD = 0.44), AUR (M = 1.2; SD = 0.292). Arithmetic mean for the measures of capital structure are DR (M = 0.29; SD = 0.34), ER (M = 1.23; SD = 6.45). Skewness and kurtosis should be “zero” and “three,” respectively, for an observed series to be normal or symmetric. Skewness and kurtosis data in Table suggest that none of the data sets are normally distributed. Variables (ROA and SIZE) are negative-skewed, while others (positive-skewed) tend to favor for the right or left of the distribution’s center, as seen by values for this parameter’s skewness. For most of the distributions studied, this means that most observations are positive. All variable distributions are also leptokurtic, according to the kurtosis results (values of kurtosis greater than 3). We know the series is not normally distributed since none of the kurtosis and skewness values for the variables meet the normalcy criteria. Because of this, we can confidently reject the null hypothesis that all observed series follow a normal distribution using the Jarque-Bera test for normality.

Table 3. Summary statistics of variables

4.2. Homogeneity and cross-sectional Independence tests

The results of the homogeneity test are summarized in Table . We can clearly reject the null hypothesis of the slope coefficients being homogeneous at a 1% level of significance using the estimated values of delta tilde (∆) and modified delta tilde (∆). Because of the variety in the different corporate groups, it is necessary to use heterogeneous panel methods, in which parameters vary across individual cross-sections of the panels.

Table 4. Pesaran-Yamagata’s homogeneity test

While the homogeneity test may be found in Table , the CD test can be found in Table . There is a 1% possibility that all variables in each panel’s CD test values are significant at a 1% level, which means that the null hypothesis of cross-sectional independence can be rejected by using CD test values and their related probability values. Cross-sectional dependency between variables across all companies in different panels is consequently implied. For the sake of domestic policy, it is critical to take this heterogeneity and cross-sectional correlation into consideration when making decisions at the federal level. There is strong evidence of cross-sectional dependence and variability among groups for several variables, necessitating the use of a second-generation panel unit root test. Given the cross-sectional correlations and heterogeneity among firm groups in a panel data, estimation results’ efficiency may be significantly reduced, as many researchers usually do. As a result, the CIPS and CADF tests from the Pesaran’s second generation panel unit are used in this research. For dependable and accurate results, panel data approaches have considered the challenges of heterogeneity and cross-sectional dependence due to the observation of both.

Table 5. Cross-section Independence test

4.3. Panel unit root tests

As shown in Table , panel unit root tests that are robust to heterogeneity as well as cross-sectional dependence may be found in the Pesaran CADF and CIPS. The estimation with a constant plus trend is considered in this study in order to take advantage of any hidden features that may exist. When the variables are in their first difference, the null hypothesis of non-stationarity of the variables at levels for all panels of firm groups cannot be ruled out. This shows that the variables have a unit root at the levels, but not at the first difference. A panel cointegration test was used to assess the long-term connection between the variables after confirming that the variables had unit roots at their respective levels but were stationary at their first difference.

Table 6. CADF and CIPS panel unit root test

4.4. Panel cointegration test

Following the panel cointegration test’s conclusions, the findings are summarized in Table . According to the results using ROA (model 1 and 3) and MBV (model 2 and 4) as a response variable, each of the variables’ probability values, due to statistical evidence rejecting the null hypothesis of no cointegration, series for various panels of business groupings, has been found to be cointegrated. Using p-values, the same null hypothesis is rejected for all variables at a 5 percent significance level. The p-value results provide more convincing evidence of cointegration between the studied variables. We can conclude that the factors under investigation have a long-term relationship.

Table 7. Bootstrap panel cointegration tests

4.5. Pooled mean group estimation

Using the PMG estimator in conjunction with the ARDL model, it is possible to determine the long- and short-term estimates and evaluate the causal links when it has been proven that the variables are cointegrated across all groups of companies. Table sums up the findings of the PMG estimation approach in a concise manner. Panel vector error correction technique (PVECM) and Granger causality tests were used to assess the robustness of the PMG estimator in the four assessed models (M1 to M4). We perform more in-depth examination, representing two-way, one-way and no causal relationship. Despite the discrepancies in parameter estimates, the estimated results in relation to the causalities between financial performance, with the output of the PMG estimator utilizing the ARDL model, are similar. As a result, the PMG estimator’s findings about the relationships between the variables are considered reliable and accurate. However, the results show that there is no significant effect for all variables in the tested short-term equations, for the four models.

Table 8. PMG long-run estimation results

Capital structure, as assessed by ER and DR, has a large and negative impact on ROA but positively on MBV. According to the PMG results in Model 1, a 1% rise in total ER and DR would have a marginal impact on ROA of roughly 3.68 and 2.32 percent, and on MBV of 0.46 and 0.99 in ascending order. Moreover, Dr and ER tend to have significant negative effect of ROA, in Model 3, by 2.87 and 1.26, respectively. However, these impacts statistically seem to be insignificant on MBV in Model 4.

The results show that agency cost measures, EXR and AUR, have negative impact on ROA by 5.23 and 2.79, respectively. Every 1% increase in operating expense ratio and asset utilization ratio separately decreases ROA by 5.53 and 2.79 percentage. The coefficients of the variables are significant at 0.01 level. Nevertheless, EXR has positive effect on MBV by 1.021, but AUR has no significant impact. 1% increase in EXR will result in increase in MBV by 1.021 percent.

Regarding the results of the moderating effect of agency cost, the results of PMG long-run estimation show that the moderating effects of DR*EXR and ER*EXR are significant and positive on ROA by 4.76 and 2.29 percentages, in Model 1. DR*AUR also positively affects ROA by 1.546 percent in Model 3. The effect of ER*AUR on ROA in model 3 is not statistically significant. However, the results of PMG long-run estimation show that the moderating effects of DR*EXR and ER*EXR are significant and negative on MBV by 0.28 and 0.88 percentages, respectively, in Model 2. Moreover, ER*AUR negatively effects MBV by 0.81 percent. Firm size ted to positively effect return on assets but negatively effect market to book value ratio.

Over the panel of all companies, Table shows the PMG estimation findings based on the elasticity of ROA and MBV with respect to the investigated variables in the production function for the long and short term. Maximum dependent lag is found to be 1, based on automatic lag selection (see, Table ). AIC is the criterion method information for the model selection. ROA and MBV were shown to be strongly influenced by all variables in the four performed models. Because their long-term elasticity coefficients perform better than their short-term counterparts, these variables are particularly important for understanding dynamic behavior. Variables are highly significant according to PMG estimation results; this suggests that each variable responds quickly to changes over the long term.

Table 9. Model selection and evaluation

The PMG model adjusted for the interaction between DR and ER with EXR in order to capture the moderating influence of EXR on the link between capital structure and firm performance as measured by ROA and MBV. There are strong interactions in the model, which indicates that EXR has a considerable impact on the capital structure. The capital structure has a beneficial impact on ROA, while EXR’s role in DR and ER adoption has a positive impact on the link between the capital structure and ROA but has a negative impact on the link between the capital structure and MBV. On the other hand, firm size as a control variable has a positive impact on ROA but a negative effect on MBV.

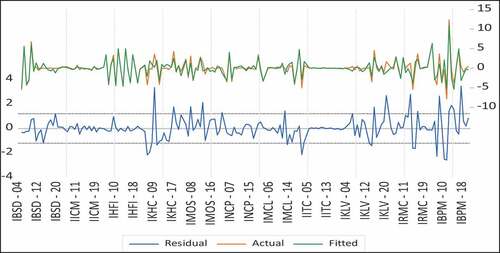

As shown in Figure , panel ARDL model 1 depend on ROA fitted and residual values for the entire time period are depicted graphically.

Figure 1. Panel ARDL model graph for model 1.

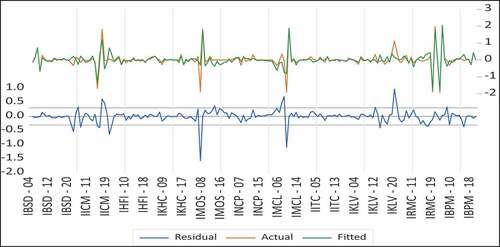

As shown in Figure , panel ARDL model 2 depend on MBV, fitted and residual values for the entire time period are depicted graphically.

Figure 2. Panel ARDL model graph for model 2.

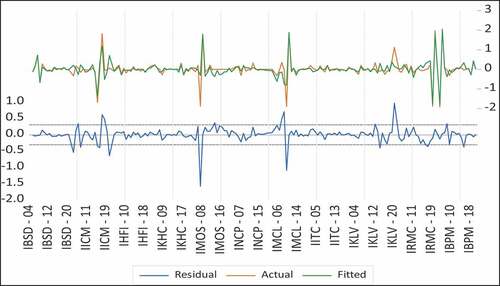

Figure shows that panel ARDL model 3 depend on ROA fitted and residual values for the entire time period are depicted graphically.

Figure 3. Panel ARDL model graph for model 3.

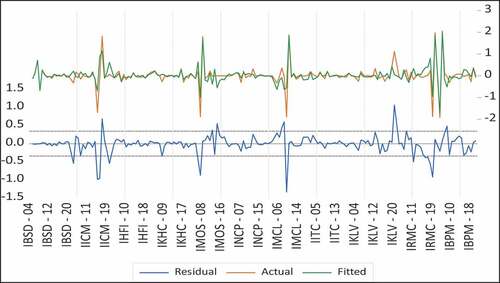

Figure shows that panel ARDL model 4 depend on MBV fitted and residual values for the entire time period are depicted graphically.

Figure 4. Panel ARDL model graph for model 4.

5. Discussion and conclusion

The purpose of this study is to provide empirical evidence for the relations between financial performance and capital structure for the industrial sector in Iraq Stock Exchange. Moreover, the study contributes to the literature through investigating the moderating effect of agency cost on the proposed relationship. Data were collected from the published financial statements of several industrial firms listed on ISX over 2004–2020. Panel Mean Group estimation method is used for data analysis purposes. Various models and estimations are used for robustness check in the results.

The results of the study confirm that capital structure, as assessed by ER and DR, has a large and negative impact on ROA but positively on MBV. There is strong evidence in the results, which indicates that agency cost has a considerable impact on the financial performance measures. Firm size also effects firm financial performance measures differently in which it is controlled for the ARDL estimation models. Moreover, the PMG model adjusted for the interaction between DR and ER with agency cost measures in order to capture the moderating influence of EXR and AUR on the association between capital structure and firm performance measured by ROA and MBV. The results of PMG long-run estimation show that the moderating effects of DR*EXR and ER*EXR are significant and positive on ROA. DR*AUR also positively affects ROA. However, the results of PMG long-run estimation show that the moderating effects of DR*EXR and ER*EXR are significant and negative on MBV. Moreover, ER*AUR negatively effects MBV with lower impact.

The results confirm the hypotheses of the study. We anticipated the existence of a significant and negative relationship between capital structure and financial performance. Agency cost negatively effects firm financial performance. We propose the existence of a significant moderate impact of agency cost on the relationship between capital structure and firm performance. These results support agency theory, more debt discourages managers from making decisions unconsciously. Managers are obliged to follow the performance more carefully in order to not default their obligations. This way, the expected agency cost is reduced, and performance of the firm is served. The results are consistent with the work of Abdullah and Tursoy (Citation2021a) in the cases of Frankfurt stock exchange in Germany; Al-Qudah (Citation2017) in the cases of Abu Dhabi; Sultan and Adam (Citation2015) in the cases of Iraq. The moderating effect of agency cost could support the literature as similar results found by, Tarazi (Citation2019) in Palestine; Berger and Di Patti (Citation2006) in the cases of US banking industry.

The results of this study can be a valuable addition to the literature around capital structure, financial performance under agency cost theory from a developing country like Iraq. Practically, the results provide significant insight to the financial authority in the country in which they could more support the industrial sector through facilitating regulations and rules of borrowing. Moreover, these results an provide managers with valuable insight that debt and agency cost reduction have potential to improve firms’ financial performance. This could aid the managers to enhance the level of competitive advantage particularly for the current rapid development in the sector. Finally, future studies may control for breaks in such a long series due to potential political, economic and financial instabilities in the emerging countries.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abdulah, H., & Tursoy, T. (2022). The effect of corporate governance on financial performance: Evidence from a shareholder-oriented system. Iranian Journal of Management Studies. https://doi.org/10.22059/IJMS.2022.321510.674798

- Abdullah. (2020). Capital structure, corporate governance and firm performance under IFRS implementation in Germany. [ PhD Thesis], Near East University.

- Abdullah, H. (2021). Profitability and leverage as determinants of dividend policy: Evidence of Turkish financial firms. Eurasian Journal of Management and Social Science, 2(3), 15–16. https://doi.org/10.23918/ICABEP2021p32

- Abdullah, H. A., Awrahman, H. G., & Omer, H. A. (2021). Effect of working capital management on the financial performance of banks: An empirical analysis for banks listed on the Iraq stock exchange. Qalaai Zanist Journal, 6(1), 429–456. https://doi.org/10.25212/lfu.qzj.6.1.17

- Abdullah, H., & Tursoy, T. (2021a). Capital structure and firm performance: Evidence of Germany under IFRS adoption. Review of Managerial Science, 15(2), 379–398. https://doi.org/10.1007/s11846-019-00344-5

- Abdullah, H., & Tursoy, T. (2021b). Capital structure and firm performance: A panel causality test. Munich Personal RePEc Archive (MPRA). https://mpra.ub.uni-muenchen.de/105871/

- Ali, M. (2018). Impact of corporate governance on firm’s financial performance (A comparative study of developed and non-developed markets). Economic Research, 2(1), 15–30. https://doi.org/10.29226/TR1001.2018.7

- Al-Imam, S., & Hassan, M. (2019). The effect of capital structure on financial performance. Journal of AL-Turath University College, 27, 189–212. https://www.iasj.net/iasj/article/201851

- Al-Qudah, A. (2017). The relationship between capital structure and financial performance in the companies listed in ABU DHabi securities exchange: Evidences from United Arab Emirates. Review of European Studies, 9(2), 1. https://doi.org/10.5539/res.v9n2p1

- Al-Taani, K. (2013). The relationship between capital structure and firm performance: Evidence from Jordan. Journal of Finance and Accounting, 1(3), 41–45. https://doi.org/10.11648/j.jfa.20130103.11

- Ang, J. S., Cole, R., & Lin, J. W. (2000). Agency costs and ownership structure. The Journal of Finance, 55(1), 81–106. https://doi.org/10.1111/0022-1082.00201

- Ankamah-Yeboah, I., Nielsen, R., & Llorente, I. (2021). Capital structure and firm performance: Agency theory application to Mediterranean aquaculture firms. Aquaculture Economics & Management, 1–21. https://doi.org/10.1080/13657305.2021.1976884

- Ardalan, K. (2017). Capital structure theory: Reconsidered. Research in International Business and Finance, 39, 696–710. https://doi.org/10.1016/j.ribaf.2015.11.010

- Berger, A. N., & Di Patti, E. B. (2006). Capital structure and firm performance: A new approach to testing agency theory and an application to the banking industry. Journal of Banking & Finance, 30(4), 1065–1102. https://doi.org/10.1016/j.jbankfin.2005.05.015

- Berle, A. A., & Means, G. C. (1932). The modern corporation and private property. Commerce Clearing House, New York: The Mcmillan Company. social sciences

- Dawar, V. (2014). Agency theory, capital structure and firm performance: Some Indian evidence. Managerial Finance, 40(12), 1190–1206. https://doi.org/10.1108/MF-10-2013-0275

- Ghafar, S., Abdullah, H., & Van Rasul, H. (2021). Bank profitability measurements and its determinants: An empirical study of commercial banks in Iraq. Journal of Zankoy Sulaimani, 4(22), 607–627. https://ideas.repec.org/p/pra/mprapa/114697.html

- Ibhagui, O. W., & Olokoyo, F. O. (2018). Leverage and firm performance:0 New evidence on the role of firm size. The North American Journal of Economics and Finance, 45, 57–82. https://doi.org/10.1016/j.najef.2018.02.002

- Imelda, E., & Dewi, A. P. (2019). Capital structure, corporate governance and agency costs. In Proceedings of the 7th International Conference on Entrepreneurship and Business Management (pp. 203–207). https://doi.org/10.5220/0008490602030207

- Iraq Stock Exchange. (2021). Companies guide. http://www.isx-iq.net/isxportal/portal/companyGuideList.html?currLanguage=en, retrieved 15 December 2021

- Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329. https://www.jstor.org/stable/1818789

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jouida, S. (2018). Diversification, capital structure and profitability: A panel VAR approach. Research in International Business and Finance, 45, 243–256. https://doi.org/10.1016/j.ribaf.2017.07.155

- Kalash, İ. (2019). Firm leverage, agency costs and firm performance: An empirical research on service firms in Turkey. İnsan ve Toplum Bilimleri Araştırmaları Dergisi, 8(1), 624–636. https://doi.org/10.15869/itobiad.513268

- Khan, R., Khidmat, W. B., Hares, O. A., Muhammad, N., & Saleem, K. (2020). Corporate governance quality, ownership structure, agency costs and firm performance. Evidence from an emerging economy. Journal of Risk and Financial Management, 13(7), 154. https://doi.org/10.3390/jrfm13070154

- Kontuš, E. (2021). Agency costs, capital structure and corporate performance: A survey of Croatian, Slovenian and Czech listed companies. Ekonomski Vjesnik, 34(1), 73–85. https://doi.org/10.51680/ev.34.1.6

- Le, T. P. V., & Phan, T. B. N. (2017). Capital structure and firm performance: Empirical evidence from a small transition country. Research in International Business and Finance, 42, 710–726. https://doi.org/10.1016/j.ribaf.2017.07.012

- Liao, Y., Huang, P., & Ni, Y. (2022). Convertible bond issuance volume, capital structure, and firm value. The North American Journal of Economics and Finance, 60, 101673. https://doi.org/10.1016/j.najef.2022.101673

- Li, K., Niskanen, J., & Niskanen, M. (2018). Capital structure and firm performance in European SMEs: Does credit risk make a difference? Managerial Finance. https://doi.org/10.1108/MF-01-2017-0018

- Liu, X., Tang, Z., & Zhao, Y. (2022). Determinants of financial performance: An evidence from Internet finance sector. Managerial and Decision Economics. https://doi.org/10.1002/mde.3451

- Mansyur, A., Mus, A. R., Rahman, Z., & Suriyanti, S. (2020). Financial performance as mediator on the impact of capital structure, wealth structure, financial structure on stock price: The Case of the Indonesian banking sector. European Journal of Business and Management Research, 5(5). https://doi.org/10.24018/ejbmr.2020.5.5.526

- Mcknight, P. J., & Weir, C. (2009). Agency costs, corporate governance mechanisms and ownership structure in large UK publicly quoted companies: A panel data analysis. The Quarterly Review of Economics and Finance, 49(2), 139–158. https://doi.org/10.1016/j.qref.2007.09.008

- Miller, M. H. (1977). Debt and taxes. Journal of Finance, 32(2), 261–275. https://doi.org/10.2307/2326758

- Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. Am` Econ Rev, 48(3), 261–297. https://www.jstor.org/stable/1809766

- Modigliani, F., & Miller, M. H. (1963). Corporate income taxes and the cost of capital: A correction. Am Econ Rev, 53(3), 433–443. https://www.jstor.org/stable/1809167

- Muneer, S., Bajuri, N. H., & Saif-ur-Rehman, S. U. R. (2013). Moderating effect of agency cost on the relationship between capital structure, dividend policy and organization performance: A brief literature review. Actual Problems of Economics, 11, 434–442.

- Ngatno, Apriatni, E. P., & Youlianto, A. (2021). Moderating effects of corporate governance mechanism on the relation between capital structure and firm performance. Cogent Business & Management, 8(1), 1866822. https://doi.org/10.1080/23311975.2020.1866822

- Nidumolu, R. (2018). Exploring the effects of agency theory on ownership structures and firm performance. Working paper. https://ssrn.com/abstract=3809607

- Pandey, K. D., & Sahu, T. N. (2019). Debt financing, agency cost and firm performance: Evidence from India. Vision, 23(3), 267–274. https://doi.org/10.1177/0972262919859203

- Para, I., Bala, H., Khatoon, G., Karaye, A., & Abdullah, H. (2022). IFRS adoption and value relevance of accounting information of listed industrial goods firms in Nigeria. Humanities Journal of University of Zakho, 10(2), 564–571. https://doi.org/10.26436/hjuoz.2022.10.2.776

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. https://doi.org/10.1080/01621459.1999.10474156

- Rasul, R. (2018). The Relationship Between Dividend Policy and Firm Value in the IFRS Adoption Era: A Case of Borsa Istanbul, [ Master thesis], Near East University.

- Saed, Y., Ahmed, R., & Abdullah, H. (2021). Consideration of environmental cost disclosure in the oil sector of Kurdistan Region. AL-Anbar University Journal of Economic and Administration Sciences, 13(2), 151–170. https://aujeas.uoanbar.edu.iq/article_171345.html

- Shrestha, A. (2019). Analysis of Capital Structure in Power Companies in Asian Economies. [ Doctoral dissertation], Asian Institute of Technology.

- Singh, M., & Davidson, W. N., III. (2003). Agency costs, ownership structure and corporate governance mechanisms. Journal of Banking & Finance, 27(5), 793–816. https://doi.org/10.1016/S0378-4266(01)00260-6

- Sultan, A., & Adam, M. (2015). The effect of capital structure on profitability: An empirical analysis of listed firms in Iraq. European Journal of Accounting, Auditing and Finance Research, 3(2), 61–78. https://www.eajournals.org/

- Tarazi, D. D. (2019 ()). Agency Theory and the Company’s Financial Performance: An Empirical Study with Evidence from Companies Listed in Palestine Exchange (PEX) (2012-2016) [ Doctoral dissertation. Al-Azhar University. Gaza]. http://dspace.alazhar.edu.ps/xmlui/handle/123456789/1277

- Tretiakova, V. V., Shalneva, M. S., & Lvov, A. S. (2021). The relationship between capital structure and financial performance of the company. In SHS Web of Conferences (Vol. 91). EDP Sciences. https://doi.org/10.1051/shsconf/20219101002

- Tripathi, V. (2019). Agency theory, ownership structure and capital structure: An empirical investigation in the Indian automobile industry. Asia-Pacific Management Accounting Journal, 14(2), 1–22. https://dx.doi.org/10.24191/apmaj.v14i2.766

- Tuan, T. M., Nha, P. V. T., & Phuong, T. T. (2019). Impact of agency costs on firm performance: Evidence from Vietnam. Organizations and Markets in Emerging Economies, 10(2), 294–309. https://doi.org/10.15388/omee.2019.10.15

- Wellalage, N. H., & Locke, S. (2013). Women on board, firm financial performance and agency costs. Asian Journal of Business Ethics, 2(2), 113–127. https://doi.org/10.1007/s13520-012-0020-x

- Zaman, K., Al-Ghazali, B. M., Khan, A., Rosman, A. S. B., Sriyanto, S., Hishan, S. S., & Bakar, Z. A. (2020). Pooled mean group estimation for growth, inequality, and poverty triangle: Evidence from 124 countries. Journal of Poverty, 24(3), 222–240. https://doi.org/10.1080/10875549.2019.1678553