?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study primarily investigates the effect of financial sustainability on capital leverage in microfinance setting. In doing this, this study looks at operating performance of 45 commercial microfinance institutions under current dual pressure of downturn and deleveraging in China. Empirically, this study employs the system GMM to observe a robustly small and negative impact of financial sustainability on capital leverage. Furthermore, this study presents a conclusion with evidence by mediation analysis that profitability exhibits a suppressing effect on the relationship between financial sustainability and capital leverage. Theoretically, this study verifies that the impact of financial sustainability on capital structure obeys the pecking order theory.

1. Introduction

After more than 40 years of theoretical deepening and practical accumulation, the establishment of microfinance institutions (MFIs) with complete functions and systems is widely regarded as a panacea to eliminate financial constraints on poor and vulnerable groups excluded from services of conventional banking (Lopatta et al., Citation2017). This is a vital initiative to promote financial inclusion. In China, MFIs, as a crucial part of the construction of inclusive-financial service system, are of great significance for consolidating and expanding the effective connection between poverty alleviation and rural revitalization. In 2008, the China Banking Regulatory Commission issued The Opinions on Adjusting and Relaxing the Access Policies of Banking Financial Institutions in Rural Areas to Better Support the Construction of New Socialist Countryside and The Guiding Opinions on The Pilot Project of Small Loan Companies (hereinafter referred to as the Opinions). According to the requirements of the Opinions, pilot projects of rural banks, rural mutual funds and other types of small loan companies have been actively carried out nationwide, marking the formal beginning of the development of MFIs in China. Among these new forces, commercial MFIs represented by small loan companies, including microcredit companies and microfinancing guarantee companies,Footnote1 have risen rapidly during the pilot promotion period, and gradually become the main forces to specialize in financial inclusion. In a nutshell, with multi-level, broad coverage and moderate competition, the reform and development of commercial MFIs is conducive to the mechanism of financial inclusion for long-tailed market.Footnote2 Whether from the perspective of Hayek’s theory of partial knowledge or incomplete market theory, MFIs can help break the financial constraints of majority of small and medium-sized enterprises (SME) and ordinary self-employed household (Besley & Coate, Citation1995; Hayek, Citation2020; Stiglitz, Citation1989), thereby stimulating the endogenous development of the poor and establishing a long-term mechanism to solve relative poverty.

The relevant research shows that the core of microfinance commercialization development is to achieve commercial sustainability. However, microfinance of full welfare nature is highly dependent on external characteristics, so it cannot provide all-round and long-term financial support to poor and vulnerable groups (Lustig & Tommasi, Citation2020). Due to their historical background of serving the underprivileged, MFIs are largely reliant on donor funds. However, these funds are highly volatile and inadequate leading to financial unsustainability, which is likely to erode the quality of their future services. Thus, MFIs must strive for financial sustainability to meet their goals (Ghosh & Van Tassel, Citation2013). Financial sustainability regarded as an approach of securing future capital flow can be achieved via commercialization and competition of micro-lending services, especially for current shortage in procurement of subsidies and donations (Abate et al., Citation2013; Chakravarty & Pylypiv, Citation2015). It can be seen that in the context of commercialization, in order to continue sustainable development, MFIs should strengthen their capital structure management.

Modigliani and Miller firstly introduce the content of capital structure on a firm’s value. They suggest the levered firm has a higher value than unlevered within tax consideration (Modigliani & Miller, Citation1963). This content is important for financial institutions as well followed by Berger et al. (Citation1995). With the research progressed, capital structure has evolved into several theories. Among them, trade-off theory predicts firm to determine leverage by trading-off between the tax shield of debt financing and cost of financial distress, including debt cost (Myers, Citation1984). On the other side, pecking order theory emerged that explains that the more sustainable firm relies less on debt owing to higher capacity of internal financing. The more reliance on external financing by less fortunate firm will lay an underlying danger of future debt crisis (Vasiliou et al., Citation2009). Apparently, there is a great debate among scholars on whether to leverage or not.

As Pettis (Citation2013) had ever described that, “Investments were misallocated on a tremendous scale in China”, a storm of negatives which were companied with the extensive economy had been intentionally or unintentionally ignored. To handle this misallocation, since 2014, the process of economic transition along with economic downturn primarily conducted pressure of deleveraging on financial sector. Deleveraging is an important measure to seek economic transformation in the context of economic downturn. By balance sheet reduction of financial institutions, it guides financial institutions to diversify their lending orientation away from over-indebted sectors towards less indebted ones. It aims to solve misallocation and drive emerging industries becoming a new force for the economy (K. Chen et al., Citation2022). However, commercial MFIs, which can operate credit-only businesses, are seen as low-credit and high-risk institutions, since their borrowers are more vulnerable in the current economic downturn. Therefore, it is extremely difficult for MFIs to obtain external financing (Wang & Ran, Citation2019). In order to have sufficient capital flow, microfinance institutions can only adopt defensive business strategies, that is, to reduce loan issuance and to focus on collection of outstanding loans. According to statistics disclosed by the Central Bank, the loan balance of small loan companies has decreased year by year from the peak of 942 billion yuan in 2014 to 888.8 billion yuan in 2020. The data seem to indicate a weakening of the MFIs’ role in financial inclusion. Paradoxically, lightly indebted microloan borrowers, who are supposed to be the beneficiaries of economic transition, are trapped by deleveraging policies. However, this problem has not been taken seriously. This problem leads to a deeper consideration that the sustainable development and capital structure of microfinance institutions matter for their ability to practice financial inclusion.

In China, microfinance sector, as the vital channel to implement financial inclusion, is mainly in the form of commercialization (for-profit). However, compared with traditional banking, MFIs have defects in external debt financing (Visconti, Citation2016). The context of deleveraging policy and economic downturn further widens the financing gap of MFIs. In response to this dilemma, it is in urgent need of MFIs to improve sustainability within economic uncertainties while sustainability appears to initiate self-support financing. Thus, the growing concern about profitability obviously becomes the overwhelming choice of MFIs to maintain “self-loop” capital, though this would defeat the original intention of poverty alleviation to some extent. Aimed at this, little is known about the extent to which whether to weaken rely on capital leverage should be necessary for MFIs in pursuit of sustainability, as well the role that profitability plays therein. This study probes into the evidence on what impact of MFIs’ financial sustainability on their leverage strategy and what role the profitability plays in the relationship between financial sustainability and capital leverage.

2. 2. Literature review and hypothesis development

2.1. Theoretical review

This section in order for underpinning the present study to construct a logical theoretical framework of capital structure via discussing and integrating two theories: pecking order theory, trade-off theory. An understanding of the theoretical explanation is deemed vital as it makes apparent the related parties’ involvement within implications on capital leverage. The following paragraphs will discuss these theories in more detail.

The pecking order theory suggests that firms have a particular preference order for capital used to finance their businesses (Myers & Majluf, Citation1984). Owing to the theory of information asymmetry and considering the existence of transaction costs, managers have more inside information than investors and act in favor of old shareholders. When firms are financing for new projects, they will give priority to using internal earnings, then use debt financing, and finally consider equity financing (Gaud et al., Citation2005; Mazur, Citation2007). Thus, holding other factors constant, firms that generate more earnings should use less debt in their capital structure.

Trade-off theory deems that the firm determines the ratio of debt financing to equity financing by weighing the advantages and disadvantages of debt. The benefits of debt include tax savings, namely tax shield. The cost of debt refers to the cost of financial distress (Myers, Citation1984). Consequently, the lower costs (including bankruptcy costs and tax shield) are needed to burden, the more debt in capital structure should be expected, and vice versa (Matemilola et al., Citation2019). Trade-off theory suggests firm should weigh the benefits and costs of debt, so as to choose the appropriate leverage.

In sum, trade-off theory supports that lower cost of debt stimulates the use of leverage, while pecking order theory endorses an aversion to leverage based on consideration of information asymmetry. Although these theories clarify the determinants of capital leverage from different perspectives, the impact of financial sustainability on capital leverage is still blank. However, from the perspective of survival, financial sustainability undoubtedly has a crucial impact on use of capital leverage. This study combining with reality advocates capital leverage as the least preferred way of funding and expects less use of debt in line with sustainability, because the downward economy should boost self-financing by MFIs in priority to keep free capital flow and avoid stepping into financial distress rather than access to extreme leverage.

2.2. Empirical review

2.2.1. Financial sustainability and profitability

The concept of sustainability originates from natural science where it refers to the ability of a society ecosystem or any such ongoing system to continue functioning into the indefinite future without being forced into decline through exhaustion of its key resources (Cook & Robèrt, Citation1990). Sustainability in MFIs refers to the ability of institutions to cover their operating costs using operating revenue generated from their core activities (Ledgerwood, Citation1999; Woller et al., Citation1999). In this respect, the strong sustainability with fair profitability can be achieved when the institutions are able to reduce their transaction costs, offer better products and services that meet clients need, generate enough revenues as well innovate more financing ways for the unbaked poor households (CGAP, Citation2004). Ayayi and Sene (Citation2010) propose operational sustainability (OSS) for microfinance sustainability that MFIs cover the operating costs including financing costs. At present, MFIs can receive very low subsidies compared to their funding demands on background of commercialization. Thus, a simple truth must be aware of the significance of sustainability and profitability.

Much of time, however, sustainability and profitability mutually check and balance each other. To what extent should MFIs focus on sustainability versus profitability is a challenge on leverage adjustment. By investigation on 52 MFIs in Ghana from 1995 to 2004, Kyereboah‐Coleman (Citation2007) discovers that highly leveraged MFIs are easy access into profitability and outreach to breadth, and inversely harmful to sustainability and outreach to depth. They claim that chasing financial performance by reaching out to more clients takes leverage in account for guaranteeing enough funds. Simultaneously, financial burden and bankruptcy risk are unintentionally aggravated owing to incessant leveraging. Ibrahim et al. (Citation2018) also give an explanation in the view of mission on financial inclusion via a sample of 57 MIFs from the member countries of the Organization of Islamic Cooperation. Despite the fact of financial sustainability, they suggest MFIs should be in line with ethical operations. The unethical hunger of profit growth by charging high interest rates may result in mission drift, because MFIs expect to rapidly transfer their financing costs and eliminate the risks of leverage. However, cost efficiency cannot determine profitability and sustainability, due to no intrinsically better microfinance approach between for-profit and not-for-profit MFIs (Leite & Civitarese, Citation2019). In a consideration of MFIs’ social mission on financial inclusion, MFIs ought to maintain fair profit for sustainability, rather than endlessly chasing profitability (Hudon et al., Citation2020).

2.2.2. Profitability and capital leverage

The sustainable view of capital structure asserts that financial institutions hold a level of capital adequacy for risk buffer. This requires minimization of the equity costs that arise from information asymmetries (Myers, Citation1984; Myers & Majluf, Citation1984). MFIs which maintain a high level of buffer capital are less levered. According to the pecking order theory, Degryse et al. (Citation2012) deploy the evidence of Dutch small and medium-sized enterprises (SMEs) from 2003 to 2005, to prove that sustainable MFIs confront with lower cost in rising their equity when access more SMEs, as well high profits further stay away from necessity to raise leverage. Whilst Towo et al. (Citation2019) emphasize the importance of debt financing for MFIs operation, they are adamant that financial leverage aggravates financial burden of MFIs, further leading to liquidation or takeover, as MFIs are compelled to spend or suspend fragile future cash flows to meet debt obligations. Siddik et al. (Citation2017) employ panel data of 22 banks in Bangladesh from 2005 to 2014 to conclude that excessive debt worsens capital structure. They recommend banking to optimize capital structure by reducing reliance on debt. Adusei and Obeng (Citation2019) carry out a dataset of MFIs from a global perspective to investigate the nexus between capital structure and performance. Their findings stand on the position of pecking order theory with some credence as well as indicate that profitability is negatively associated with leverage level.

The findings debated by existing literatures are largely mixed. Some scholars stand against the views above. Adusei and Sarpong-Danquah (Citation2021) come to a contrary view on sustainable development. They utilize trade-off theory to explain that if in a good institutional quality, due to more tax savings, the better opportunity for MFIs to profit accelerates more use of debts, vice versa. Bitok et al. (Citation2021) examine the impact of agency cost and capital structure on MFIs in Kenya with panel data model regression on a sample drawn from 30 MFIs during the period 2010–2018. They suggest prudent raise in capital leverage in virtue of that profitable MFIs boost investor confidence through strategic decision-making. These findings are similar to the study by Kar (Citation2012) that a positive nexus between profit-efficiency and capital leverage is confirmed with evidence of 92 cross-country MFIs.

From the existing literature, many studies on microfinance contribute their demonstrations that profitability has an important impact on capital leverage, and there is a close relationship between financial sustainability and profitability, but what is the impact of financial sustainability on capital leverage? As far as we know, the elaborations on this question are rare. In addition, profitability seems to play a conductive role in the relationship between sustainability and capital leverage. Little know how profitability plays therein. In doing these, we propose the hypotheses are:

: There is no significant effect of financial sustainability on MFIs’ leverage decision in China.

: Profitability does not mediate the relationship between financial sustainability and capital leverage.

3. Sample and data source

The commercial MFIs in China are classified into small loan companies, including microcredit companies and microfinancing guarantee companies. Although the number of population is huge, many of them limit in disclosure and financial records. In an effort to obtain as valid and complete data as possible, in addition to collecting from Wind Database which is the widely acceptable financial database, we also combine public financial reports to fill in missing value. Besides, this study applies macro data from the National Bureau of Statistics as well. To this end, the data set for this study originates from panel data of 45 commercial MFIs, including 35 microcredit companies and 10 microfinancing guarantee companies in the mature period of 2012–2020, and their local economic conditions of provinces or municipalities. Although the sample size is small compared to the population, these 45 MFIs can represent the mature group with consideration of late start of most of commercial MFIs. And these samples are geographically dispersed. Therefore, the sample is adequate for refracting the whole.

4. Methodology

The literature commonly mentions that financial sustainability is significant for the decision on capital structure, but cannot yet form a unanimous conclusion about its impact. To achieve the objectives of this study, this section examines the research hypotheses proposed in previous section by modelling.

4.1. Model specification

In analysis of MFIs, the heterogeneity caused by the difference in earnings management between for-profit and non-for-profit MFIs must be concerned (Pignatel & Tchuigoua, Citation2020; de Oliveira Leite et al., Citation2020). It is worth noting that commercial MFIs operate in profit orientation. Therefore, this study screens commercial MFIs as samples which naturally eliminate the problem of heterogeneity. Furthermore, it can be found from both practical and academic studies that the change in sustainability will cause dynamic adjustment of leverage. This requires analysis not only to consider the influence of current factors, but also to account for the influence of past factors. Hence, it is necessary to add the lag term of the explained variable to the explanatory variable. As for possibility of endogeneity, we use the generalized method of moment (GMM) estimation in the dynamic panel model for empirical analysis (Pacifico, Citation2020). GMM can not only overcome obstacles of weak instrumental variables and endogeneity, but also improve the efficiency of estimation.

In addition, credited to Arellano and Bover (Citation1995), the system GMM estimator uses moment conditions (instruments) that do not correlate with the regressors in the estimated model. We use a collapse technique to avoid the proliferation of instruments. We rely on two statistics to test the reliability of results obtained from this estimator: Arellano-Bond autocorrelation test and Hansen statistic. The former is used to test for serial correlation of the error term and the latter checks the validity of the instruments used.

4.1.1. Regression of main effect

This section implements the three-step approach to set a test for mediating effects. To empirically test hypothesis : the impact of financial sustainability on leverage, we include a baseline regression to construct Path A in Equation 4–1.

Where, is introduced as dependent variables that measures the capital structure (regarding as capital leverage expressed by debt-to-equity ratio) for one particular MFI during a specific year.

On the other side, is the first-order lag of explained variable;

,

and

are coefficients of independent variables to be estimated;

is the coefficient of vector formed by control variables; and

is the error term. This model launches the accounting measurement of core explanatory variable: operational self-sufficiency (OSS) that reflects the ability to compensate operating costs by operating incomes (Ayayi & Sene, Citation2010). The main problem affecting financial sustainability is the efficiency of the use of funds rather than the source of funds (Okumu, Citation2007). This study following Okumu’s conclusion concentrates uniquely on financial sustainability as OSS because the objective is to examine capital structure in the sense of efficiency of funds use. A better sustainability excercises less expenditures on financing and loads on less pressures on investment decisions (Pratomo & Ismail, Citation2006). The great sustainability is expected to decrease leverage.

The third term in the model represents the sets of variables as control variables. Firstly, this model introduces real GDP growth rate (RGDP) and inflation rate (INF) as the essential macro variables for MFIs’ performance. Both two macro variables commonly indicate regional economic conditions of provinces or municipalities where MFIs are located.

The market structure is also involved in control variables. Wherein, geographic branch penetration (GBP) measured by regional branches of MFIs per 10 and demographic branch penetration (DBP) measured by regional branches of MFIs per 10 thousand capita, both are computed as nature logarithm to imply microcredit service coverage and competition status (Beck et al., Citation2007; Cull et al., Citation2009; Vanroose & D’Espallier, Citation2013). The higher value of these indicators, the more competition of there is in market. Besides this, in line with McKinsey Matrix, society’s leverage (SLEV) computed by the ratio of total credit issued by financial institutions for other sectors of society to regional GDP, reflect the size of credit gap and the extent of credit saturation (Yao & Liu, Citation2018). More competition and deeper saturation in credit market, the less space there is for microfinance.

Next, some specific variables work for the control vector. Size of assets (SIZE), measured as the nature logarithm of total assets, indicates MFI’s strength in favor of long-term operation (Al-Kayed et al., Citation2014). Subsequently, net loans ratio (NLR) ratio represents the ability of generate revenues (Alshatti, Citation2015), and non-earning assets ratio (NEAR) indicates that how much of assets is used for commitment of assets security rather than investments or other purposes (Akuetteh, Citation2019). Apart from these variables, some scholars generally believe that gender is an important factor affecting the asset quality of microfinance institutions (Afrifa et al., Citation2019; Fayyaz & Khan, Citation2021; Gyapong et al., Citation2021), as there is evidence that lending to female borrowers is associated with better loan performance than it is the case with male borrowers, but it seems to be an illusion that gender heterogeneity can determine the bias of MFIs’ capital-loan portfolio (X. Chen et al., Citation2020; Leite & Civitarese, Citation2019). Therefore, this study excludes gender as a specific variable.

Followed by the control vector, the fourth term represents a dummy variable (MCC) is used to distinguish the types of MFIs, where MCC takes the value 1 or 0 to manifest microcredit companies or microfinancing guarantee companies respectively. All these variables used in regression are summarized in Appendix Table .

4.1.2. Regressions of mediating effect

To test the mediating effect of profitability on sustainability and leverage, based on Path A above, we look at coefficient without adding mediator firstly to test if MFIs lessen the use of leverage in accordance with achieving sustainability. Then, through Path B, we inspect the estimated coefficient

of sustainability on the mediator. Finally, the Path C with adding mediator offers the observation of the effects of sustainability and mediator commonly on leverage, i.e. estimated coefficients

and

. The mediating regressions for Path B and Path C are formulated in Equation 4–2 and Equation 4–3 respectively.

Where the mediators indicate the profitability including return on assets (ROA) and return on equity (ROE) in modelling. ROA and ROE are regarded as the ability to generate revenue through utilizations of assets and capitals respectively (Al-Kayed et al., Citation2014; Dawar, Citation2014).

Given the regression results of Equation 4–2 and 4–3, when the coefficient in Path A, coefficient

in Path B and coefficient

in Path C are significant, and

is not significant, the mediator contributes a complete mediating effect. If the coefficient

in Path C is significantly smaller than

in Path A, there exists the partial mediating effects. Synchronously, the Bootstrap test can assist us to check whether mediating effect (

) and direct effect (

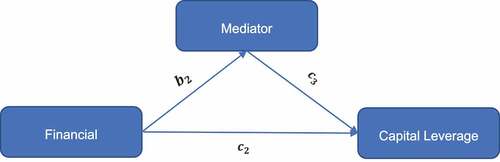

) are significant, as well estimate whether their confidence interval contains 0 (Fritz & MacKinnon, Citation2007; MacKinnon et al., Citation2004; Tofighi & MacKinnon, Citation2011). The structure of mediating effect in our model is exhibited in Figure . All these models introduced in this section are implemented within realistic data set through software Stata V.16.0.

Figure 1. Mediation model (Note: total effect is , direct effect is

and mediating effect is

).

5. Empirical results and discussion

5.1. Data description

To answer questions of this study, the statistics for formed sample are presented in Table firstly in the light of variables of interest we constructed. There is not any variable with high standard deviation reported that indicates the values of data set in all indicators are close to means. It is more likely to obey normal distribution on the whole.

Table 1. Descriptive statistics

Then, this study continues to check if multicollinearity is possible for variables within the sample period. Table demonstrates the correlation of independent variables included in the model introduced above. In Table , a great correlation between ROA and ROE at 0.982 and significant at 1% predict a suspected multicollinearity. To further confirm for possible multicollinearity, we apply the Variance Inflation Factor (VIF) test. The VIF values of ROA and ROE at 34.62 and 34.93, respectively, are both greater than the benchmark of 10 that a strong multicollinearity detected is convincing to be the truth.

Table 2. Correlation matrix

Some studies propose the use of principal component analysis (PCA) as a statistical technique for quantifying and adjusting multicollinearity in a data base (Adnan et al., Citation2006; Perez, Citation2017; Sulaiman et al., Citation2021). PCA by simplifying data set is a dimensionality reduction process that converts multiple indicators into a few comprehensive indicators with a linear change. In our study, ROA and ROE are the main indicators for profitability of MFIs. Hence, the multicollinearity can be solved by reducing the dimension of these two indicators into a comprehensive indicator (PROFIT) that results of adjusted correlation is shown in Table . After VIF test with adjusted variables again, there is no longer existing evidence of multicollinearity among adjusted variables.

Table 3. Adjusted correlation matrix

5.2. Baseline regression results

The baseline regression in this study uses the system GMM estimation method, and selects the first-order lag of the explained variable as the exogenous variable. In order to ensure the reliability of the GMM estimation results, this study also tries the static panel fixed effect (FE) model for estimation. Table shows the baseline regression estimation results where the explained variable is the leverage ratio and the core explanatory variable is financial sustainability.

Table 4. Results of baseline regression

As shown in Table , the Hausman test (p = 0.0002) mentions that there is a significant difference in coefficient estimation between fixed and random effects. The fixed effect better matches modelling. The first column is the estimation result of the panel fixed effect model. The result implies that financial sustainability opposes MFIs to raise the extent of debt financing, and it is significant at the 1% level. While considering the endogeneity, the estimation results of the GMM are shown in the second column. Sustainability still has a suppressive effect on the behaver to leverage of MFIs with a significance level at 1%, and the influence coefficient is larger, which becomes −0.055, indicating that no matter whether static panel estimation or dynamic panel estimation is used, sustainability has a significant negative effect on leverage. Both obey the pecking order theory looking upon debt financing as the least preference order. However, the endogenous term will underestimate the inhibiting effect of sustainability on the leverage. Therefore, the system GMM estimation method should be better for estimating the relation between sustainability and leverage within Equation 4–1. Even so, financial sustainability has the least impact on capital leverage compared to other independent variables.

In the system GMM estimation, the P value of Arellano-Bond test for AR (1) in first differences is less than 1 %, and the P value of AR (2) test is more than 10 %; that is, the regression does not exist second-order sequence autocorrelation, indicating that the model effectively overcomes the endogeneity problem. The Hansen test reports that the instrumental variables selection of the model is reasonable, and the results of regression appear to be unbiased while GMM is applied to estimate the effects. Following the second column of Table , the impact of the first-order lag of the leverage on current leverage is significant at 0.548, indicating that the leverage in previous period of MFI has a significantly promoting effect on the current leverage. By implication, along with improvement of financial sustainability, MFIs are able to get rid of reliance on debt, as well as curtail the burden of financing cost and facilitate quality of capital structure. This goes against the trade-off theory of insisting that lower cost in debt financing.

As for the effects of control variables, local inflation index significantly scales up the debt burden of MFIs, while GDP growth ease the MFIs’ debt positions without a significant effect. This agrees with the conclusion of Adusei and Sarpong-Danquah (Citation2021), that the quality of external conditions slows down capital structure of MFIs in line with the pecking order theory. From the perspective of market structure, the scale of aggregate social indebtedness and geographic distribution density of financial institutions jointly report the market competition pressure against expansion of leveraging for business within a saturated condition. Unexpectedly, the demographic coverage density of financial institutions promotes the leverage of MFIs. The likely reason is that the lower costs of information and transaction in a buoyant lending environment trigger more aggressive leverage strategy acted by MFIs, despite intensifying competition.

In respect of specific characteristics, with the increase in assets scale, the ability of MFIs to leverage also raises. It is worth noting that the proportion of outstanding loans negatively affects the use of debts by MFIs. Along with business scale growth, the aversion to debt deepens, that contradicts agency theory. From a security standpoint, the priority shifts over time to holding non-earning assets as business growth. Priority of recoverable non-earning assets further dispels desires of MFIs to capital leverage. This supports the preference of self-sufficiency by the pecking order theory. In addition, the dummy variable (MCC), which indicates different types of MFIs, is positive to leverage. This reflects that microcredit companies are more leveraged accept than microfinancing guarantee companies.

5.3. Robust test

This study covers commercial MFIs as the sampling range, including microcredit companies and microfinancing guarantee companies. Among them, microcredit companies are regarded as the main sampling objects. Although we have control over type variable (MCC), it is suspected whether the regression model for synthetic types is still valid for the primary observations. Towards this end, we run the baseline regression only with observations of microcredit companies. The estimated results report an impact of financial sustainability on capital leverage up to −0.0199, strongly significant at 1%, and this regression test can success in Arellano-Bond test and Hansen test. This demonstrates that the baseline model is still robust in a single type of sample.

Moreover, this study introduces regional conditions as MFIs’ external control variables. Considering that the municipality-level data is far greater than the province-level data in terms of economic prosperity and competition intensity, we exclude the influence of the MFIs located in the municipality on the model to test if robust. The test likewise indicates that the baseline model is robust with the influence coefficient of core explanatory variable (OSS) at −0.0218 and significant at 5%.

Similarly, this study varies control variables in three levels (macro variables, market structure variables and institution-specific variables) that the results may exist instability. It’s necessary to test if robust excluding the influence of macro variables. The coefficient of OSS is −0.0223 and significant at 1% without macro variables. It declares that the model running variables in different level is still robust.

5.4. Mediation results

In this study, profitability (PROFIT) is applied as mediating variable to test the mediating effect. Following the results of Table , in the Path A, we can extract the total effect that is significant effect of financial sustainability on leverage, , at −0.055 in line with baseline regression in Equation 4–1. By regression of Equation 4–2, Path B obtains a significantly positive effect of financial sustainability on profitability,

, at 0.190. With insight of Path C in the light of Equation 4–3, the results reveal that both sustainability and profitability have significant impacts on leverage, where the direct effect

is −0.090 and the influence coefficient

is 0.064. In light of Bootstrap test, the indirect effect (mediating effect) is significant at 95% confidence interval between 0.00274 and 0.0105, without involvement of 0. Followed by computing, The indirect effect is

. As indirect effect has a different sign as direct effect, i.e. indirect effect is positive and direct effect is negative, a suppressing effect can be ascertained in the model and its proportion equals to

. All results of mediation are exhibited in Table .

Table 5. Results of mediation model

Financial sustainability has a small and positive effect on profitability can be examined by Path B. This reflects that financial sustainability can allow MFIs to create fair profit by consistent commercial activities. In addition, the ability of leveraging is stronger as along with as along with profit growth that can be proved by the positive influence coefficient of PROFIT in Path C. As the coefficient of OSS in Path A is greater than it in Path C, at the same level of sustainability, the leverage without considering the impact of profitability is higher than that with considering the impact of profitability. This verifies profitability conduct a suppressing impact on the nexus between sustainability and leverage. It can be concluded that some reliance on external debt financing can be further offset by earnings generated by profit growth. This, likewise, proves that the impact of financial sustainability on capital structure follows the pecking order theory on the priority of internal earnings.

6. Conclusion and implication

This study investigates the impact of financial sustainability on MFIs’ capital structure based on the balanced panel data set during period of 2012–2020 of commercial MFIs in China by using the system GMM method. It gives a particular focus to the mediating role of profitability on the relationship between financial sustainability and capital leverage. This study provides a new perspective for deeply excavating the theoretical basis for MFIs’ capital structure. The findings are presented as follows: First, financial sustainability significantly weakens the reliance on capital leverage. Second, financial sustainability significantly enhances the fair profit of MFIs. Third, profitability can suppress the effect of financial sustainability on capital leverage so that sustainable MFIs deepen aversion to leverage along with profit growth. Fourth, financial sustainability determines the capital structure in light of the pecking theory.

Therefore, based on the findings above, this study proposes the following recommendations. First of all, MFIs should scientifically rule the external debt scale and strengthen the sustainable and healthy development. To do this, MFIs should sound their internal management and operation mechanisms. While accelerating loan turnover and arranging loan maturities reasonably, it also innovates asset diversification, improves liquidity and revitalizes outstanding loans and reduces non-performing loans. By practicing “small and decentralized” lending, MFIs can operate efficient microloans for more micro borrowers and consolidate self-financing ability, so that their headwinds of debt will fade. Secondly, the profitable MFIs should benefit their micro borrowers by reducing interest charge on the premise of ensuring fair profits. In the way of surrendering profits, MFIs can improve their repayment rate and establish creditworthiness so as to lessen transaction costs of external financing. Thirdly, policymakers should moderately release deleveraging stress in terms of the operating status of MFIs. Policymakers can screen some creditable MFIs as a plot to broaden them financing channels such as bill market and inter-banking market, as well as encourage consistently profitable MFIs to list on National Equities Exchange and Quotations. Fourth, policymakers should allow the MFIs which operate in good conditions to cross-regional operation. With preferential policies and relevant subsidies, policymakers can not only guide MFIs to access into underdeveloped region, but also ease regional competition of financial saturation.

Does financial sustainability decelerate raise in leverage of MFIs because it improves operating efficiency in such a way that MFIs become more self-sufficient away to offset the gap in external financing? And does the similar circumstance occur in deposit-taking MFIs with deposit liabilities as their main funding sources? These matters are not mentioned herein. Further research is needed in this direction to answer these questions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Microcredit companies piloted in 2008 by Guiding Opinions on the Pilot Operation of Microcredit Companies No. 23 [2008] of China Banking Regulatory; and financing guarantee companies launched since 2010 by Interim Measures for the Administration of Financing Guarantee Companies NO. 3 [2010] of the China Banking Regulatory. Both of them cannot absorb deposits and specialize in microcredit services for small and medium customer groups.

2. Long-tailed market regarded as a whole, in which amounts of scattered financing demands are excluded by conventional banking, can match the main financial market.

References

- Abate, G. T., Borzaga, C., & Getnet, K. (2013). Financial sustainability and outreach of microfinance institutions in Ethiopia: Does organizational form matter? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2288627

- Adnan, N., Ahmad, M. H., & Adnan, R. (2006). A comparative study on some methods for handling multicollinearity problems. Matematika, 22(2), 109–17. https://doi.org/10.11113/matematika.v22.n.179

- Adusei, M., & Obeng, E. Y. T. (2019). Board gender diversity and the capital structure of microfinance institutions: A global analysis. The Quarterly Review of Economics and Finance, 71, 258–269. https://doi.org/10.1016/j.qref.2018.09.006

- Adusei, M., & Sarpong-Danquah, B. (2021). Institutional quality and the capital structure of microfinance institutions: The moderating role of board gender diversity. Journal of Institutional Economics, 17(4), 641–661. https://doi.org/10.1017/S1744137421000023

- Afrifa, G. A., Gyapong, E., & Zalata, A. M. (2019). Buffer capital, loan portfolio quality and the performance of microfinance institutions: A global analysis. Journal of Financial Stability, 44, 100691. https://doi.org/10.1016/j.jfs.2019.100691

- Akuetteh, J. O. S. H. U. A. (2019). Understanding the Sustainability of Credit Unions Using the Pearls Model: Credit Unions in the Volta Region of Ghana in Perspective [ Doctoral dissertation], University of Ghana.

- Al-Kayed, L. T., Zain, S. R. S. M., & Duasa, J. (2014). The relationship between capital structure and performance of Islamic banks. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-04-2012-0024

- Alshatti, A. S. (2015). The effect of the liquidity management on profitability in the Jordanian commercial banks. International Journal of Business and Management, 10(1), 62. https://dx.doi.org/10.5539/ijbm.v10n1p62

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Ayayi, A. G., & Sene, M. (2010). What drives microfinance institution’s financial sustainability. The Journal of Developing Areas, 44(1), 303–324. https://doi.org/10.1353/jda.0.0093

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27–49. https://doi.org/10.1007/s10887-007-9010-6

- Berger, A. N., Herring, R. J., & Szegö, G. P. (1995). The role of capital in financial institutions. Journal of Banking & Finance, 19(3–4), 393–430. https://doi.org/10.1016/0378-4266(95)00002-X

- Besley, T., & Coate, S. (1995). Group lending, repayment incentives and social collateral. Journal of Development Economics, 46(1), 1–18. https://doi.org/10.1016/0304-3878(94)00045-E

- Bitok, S. K., Cheboi, J., & Kemboi, A. (2021). Influence of financial leverage on financial sustainability: a case of microfinance institutions in Kenya. Journal of Finance and Accounting Research, 3(1), 1–17. https://doi.org/10.32350/jfar.0301.01

- BRIEF, D. (2004). The impact of interest rate ceilings on microfinance. CGAP. CGAP

- Chakravarty, S., & Pylypiv, M. I. (2015). The role of subsidization and organizational status on microfinance borrower repayment rates. World Development, 66, 737–748. https://doi.org/10.1016/j.worlddev.2014.09.007

- Chen, K., Guo, W., Kang, Y., & Wang, J. (2022). Does the deleveraging policy increase the risk of corporate debt default: Evidence from China. Emerging Markets Finance and Trade, 58(3), 601–613. https://doi.org/10.1080/1540496X.2020.1809376

- Chen, X., Huang, B., & Ye, D. (2020). Gender gap in peer-to-peer lending: Evidence from China. Journal of Banking & Finance, 112, 105633. https://doi.org/10.1016/j.jbankfin.2019.105633

- Cook, D., & Robèrt, K. H. (1990). Natural Step: A Framework for Sustainability. UIT Cambridge Limited.

- Cull, R., Demirgüç-Kunt, A., & Morduch, J. (2009). Microfinance meets the market. Journal of Economic Perspectives, 23(1), 167–192. https://doi.org/10.1257/jep.23.1.167

- Dawar, V. (2014). Agency theory, capital structure and firm performance: Some Indian evidence. Managerial Finance, 40(12), 1190–1206. https://doi.org/10.1108/MF-10-2013-0275

- Degryse, H., de Goeij, P., & Kappert, P. (2012). The impact of firm and industry characteristics on small firms’ capital structure. Small Business Economics, 38(4), 431–447. https://doi.org/10.1007/s11187-010-9281-8

- de Oliveira Leite, R., dos Santos Mendes, L., & de Lacerda Moreira, R. (2020). Profit status of microfinance institutions and incentives for earnings management. Research in International Business and Finance, 54, 101255. https://doi.org/10.1016/j.ribaf.2020.101255

- Fayyaz, S., & Khan, A. (2021). Impact of microfinance on quality of life, personal empowerment and familial harmony of female borrowers in Pakistan. Journal of Public Affairs, 21(3), e2614. https://doi.org/10.1002/pa.2614

- Fritz, M. S., & MacKinnon, D. P. (2007). Required sample size to detect the mediated effect. Psychological Science, 18(3), 233–239. https://doi.org/10.1111/j.1467-9280.2007.01882.x

- Gaud, P., Jani, E., Hoesli, M., & Bender, A. (2005). The capital structure of Swiss companies: An empirical analysis using dynamic panel data. European Financial Management, 11(1), 51–69. https://doi.org/10.1111/j.1354-7798.2005.00275.x

- Ghosh, S., & Van Tassel, E. (2013). Funding microfinance under asymmetric information. Journal of Development Economics, 101, 8–15. https://doi.org/10.1016/j.jdeveco.2012.09.005

- Gyapong, E., Gyimah, D., & Ahmed, A. (2021). Religiosity, borrower gender and loan losses in microfinance institutions: A global evidence. Review of Quantitative Finance and Accounting, 57(2), 657–692. https://doi.org/10.1007/s11156-021-00958-5

- Hayek, F. A. (2020). The constitution of liberty: The definitive edition. Routledge.

- Hudon, M., Labie, M., & Reichert, P. (2020). What is a fair level of profit for social enterprise? Insights from microfinance. Journal of Business Ethics, 162(3), 627–644. https://doi.org/10.1007/s10551-018-3986-z

- Ibrahim, Y., Ahmed, I., & Minai, M. S. (2018). The influence of institutional characteristics on financial performance of microfinance institutions in the OIC countries. Economics and Sociology, 11(2), 19–35. https://doi.org/10.14254/2071-789X.2018/11-2/2

- Kar, A. K. (2012). Does capital and financing structure have any relevance to the performance of microfinance institutions? International Review of Applied Economics, 26(3), 329–348. https://doi.org/10.1080/02692171.2011.580267

- Kyereboah‐Coleman, A. (2007). The impact of capital structure on the performance of microfinance institutions. The Journal of Risk Finance, 8(1), 56–71. https://doi.org/10.1108/15265940710721082

- Ledgerwood, J. (1999). Sustainable banking with the poor microfinance handbook.

- Leite, R. D. O., & Civitarese, J. (2019). Microfinance for women: Are there economic reasons? Evidence from Latin America. Economics Bulletin, 39(1), 571–580.

- Lopatta, K., Jaeschke, R., Tchikov, M., & Lodhia, S. (2017). Corruption, corporate social responsibility and financial constraints: International firm‐level evidence. European Management Review, 14(1), 47–65. https://doi.org/10.1111/emre.12098

- Lustig, N., & Tommasi, M. (2020). Covid-19 and social protection of poor and vulnerable groups in Latin America: A conceptual framework. CEPAL Review-Special Issue. https://hdl.handle.net/11362/46939

- MacKinnon, D. P., Lockwood, C. M., & Williams, J. (2004). Confidence limits for the indirect effect: Distribution of the product and resampling methods. Multivariate Behavioral Research, 39(1), 99–128. https://doi.org/10.1207/s15327906mbr3901_4

- Matemilola, B. T., Bany-Ariffin, A. N., Azman-Saini, W. N. W., & Nassir, A. M. (2019). Impact of institutional quality on the capital structure of firms in developing countries. Emerging Markets Review, 39, 175–209. https://doi.org/10.1016/j.ememar.2019.04.003

- Mazur, K. (2007). The determinants of capital structure choice: Evidence from Polish companies. International Advances in Economic Research, 13(4), 495–514. https://doi.org/10.1007/s11294-007-9114-y

- Modigliani, F., & Miller, M. H. (1963). Corporate income taxes and the cost of capital: A correction. The American Economic Review, 53(3), 433–443. https://www.jstor.org/stable/1809167

- Myers, S. C. (1984). Finance theory and financial strategy. Interfaces, 14(1), 126–137. https://doi.org/10.1287/inte.14.1.126

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/10.1016/0304-405X(84)90023-0

- Okumu, L. J. (2007). The microfinance industry in Uganda: sustainability, outreach and regulation [ Doctoral dissertation] University of Stellenbosch.

- Pacifico, A. (2020). A two-step system for hierarchical bayesian dynamic panel data to deal with endogeneity issues, structural model uncertainty, and causal relationship.

- Perez, L. V. (2017). Principal component analysis to address multicollinearity. Whitman College.

- Pettis, M. (2013). Avoiding the fall: China’s economic restructuring. Brookings Institution Press.

- Pignatel, I., & Tchuigoua, H. T. (2020). Microfinance institutions and International Financial Reporting Standards: An exploratory analysis. Research in International Business and Finance, 54, 101309. https://doi.org/10.1016/j.ribaf.2020.101309

- Pratomo, W. A., & Ismail, A. G. (2006). Islamic bank performance and capital structure.

- Siddik, M., Alam, N., Kabiraj, S., & Joghee, S. (2017). Impacts of capital structure on performance of banks in a developing economy: Evidence from Bangladesh. International Journal of Financial Studies, 5(2), 13. https://doi.org/10.3390/ijfs5020013

- Stiglitz, J. E. (1989). Financial markets and development. Oxford Review of Economic Policy, 5(4), 55–68. https://doi.org/10.1093/oxrep/5.4.55

- Sulaiman, M. S., Abood, M. M., Sinnakaudan, S. K., Shukor, M. R., You, G. Q., & Chung, X. Z. (2021). Assessing and solving multicollinearity in sediment transport prediction models using principal component analysis. ISH Journal of Hydraulic Engineering, 27(sup1), 343–353. https://doi.org/10.1080/09715010.2019.1653799

- Tofighi, D., & MacKinnon, D. P. (2011). RMediation: An R package for mediation analysis confidence intervals. Behavior Research Methods, 43(3), 692–700. https://doi.org/10.3758/s13428-011-0076-x

- Towo, N., Mori, N., & Ishengoma, E. (2019). Financial leverage and labor productivity in microfinance co-operatives in Tanzania. Cogent Business & Management, 6(1), 1635334. https://doi.org/10.1080/23311975.2019.1635334

- Vanroose, A., & D’Espallier, B. (2013). Do microfinance institutions accomplish their mission? Evidence from the relationship between traditional financial sector development and microfinance institutions’ outreach and performance. Applied Economics, 45(15), 1965–1982. https://doi.org/10.1080/00036846.2011.641932

- Vasiliou, D., Eriotis, N., & Daskalakis, N. (2009). Testing the pecking order theory: The importance of methodology. Qualitative Research in Financial Markets, 1(2), 85–96. https://doi.org/10.1108/17554170910975900

- Visconti, R. M. (2016). Microfinance vs. traditional banking in developing countries. International Journal of Financial Innovation in Banking, 1(1–2), 43–61. https://doi.org/10.1504/IJFIB.2016.076613

- Wang, J., & Ran, B. (2019). Balancing paradoxical missions: How does microfinance rebuild a sustainable path in poverty alleviation? SAGE Open, 9(2), 2158244019857838. https://doi.org/10.1177/2158244019857838

- Woller, G. M., Dunford, C., & Woodworth, W. (1999). Where to microfinance. International Journal of Economic Development, 1(1), 29–64.

- Yao, Y., & Liu, Q. (2018). Research on China’s macro-leverage ratio and risk prevention. In 2018 International Conference on Management, Economics, Education and Social Sciences (MEESS 2018), (pp. 470–477). Atlantis Press.