?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this study is to evaluate the influence of economic policy uncertainty in determining the FDI inflow for 19 economies with higher incomes between 2000 and 2021. Using the panel Ardl approach, the data were examined. The dynamic fixed effect approach was selected for assessing the necessary set of hypotheses based on the significance of the Hausman test. Increasing levels of economic policy uncertainty, exchange rate, and inflation rate discourage foreign investors from investing in the host country, whereas trade openness and real growth rate increase investors’ confidence in increasing FDI inflow in the host country. The economic implications of the study include the political stability of the host country and the uniformity of government policies, particularly in favor of international investors. This study contributes to the existing body of knowledge on FDI by examining the long-term and short-term effects of uncertainty for the high-income group. The findings of the study apply to higher-income economies. In the future, comparative time-series analysis may be used to assess studies on an individual or regional basis for other groups as well.

1. Introduction and background

Foreign direct investment (FDI) is a sort of international business in which an investor from one nation has long-term ownership in and substantial control over a company from another one (Blonigen, Citation2005). The significance of economic policy uncertainty grew with the occurrence of multiple economic and financial crises, which led to a decline in FDI inflows for host nations (Albulescu & Ionescu, Citation2018). The intensity of global uncertainty as a factor of FDI is greater for developing economies than for affluent ones for gross investment flow (Hlaing & Kakinaka, Citation2019). Economic policy uncertainty is distinct from global uncertainty in terms of its impact on FDI inflow. Investment flow for developed and developing nations exhibits varied characteristics for global uncertainty, and economic policy uncertainty (Suh & Yang, Citation2021). It is still a puzzle how economic policy uncertainty impacts the FDI inflow in the long run and short run for developed nations. Therefore, additional research is required to determine the effect of economic policy uncertainty on FDI inflow to high-income economies. The global financial crises and other economic crises in the past have highlighted the significance of economic policy uncertainty influencing future investment inflow decisions (Chen et al., Citation2019). The FDI flow is regarded as the most consistent type of capital movement. However, certain types of uncertainty, such as economic policy uncertainty, may be detrimental due to the fixed costs associated with FDI (Choi et al., Citation2021). Similarly, the ambiguity surrounding national and international economic policies has the potential to limit the flow of international investment, goods, and services (Sinha & Ghosh, Citation2021).

The increase in FDI inflow is a significant factor in the development of high-income, middle-income, and low-income nations. A deficiency of incoming capital may retard the development of any nation (Ogbonna et al., Citation2022). Similarly, uncertainty may occur in financial and non-financial markets, along with general economies, due to changes in international ties, limits or prohibitions on imports, tariffs, laws, etc. (Zhang et al., Citation2022). Sometimes, limits on economic policies may have a negative impact on FDI inflows in the near term, but they may yield long-term benefits (Williams et al., Citation2022). Some trade or economic barriers may be loosened to increase foreign direct investment (Bao et al., Citation2022). Recent years have witnessed the emergence of economic policy uncertainty as one of the most influential determinants of FDI inflows in developed economies. Whether the FDI inflow will materialize in an uncertain climate characterized by economic policy is the central issue of contention. The study’s novelty and originality consist of its examination of the influence of EPU on FDI inflow in high-income economies. Previous research studies have examined several sources of uncertainty for FDI inflow, such as global uncertainty, exchange rate uncertainty, pandemic uncertainty, geopolitical uncertainty, and political uncertainty. However, the present study adds new evidence to the previous literature about the effect of economic policy uncertainty on FDI inflow for a sample of high-income economies.

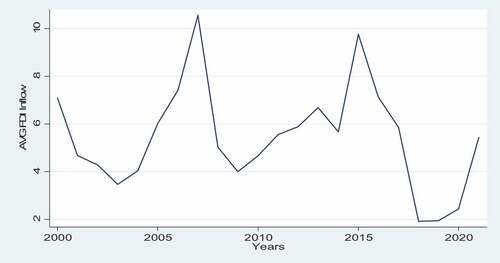

Figure indicates the average trend line for all 19 higher-income countries’ FDI inflow during 2000–2019. The graph depicts a random pattern exhibiting a rise and drop following a certain time. For instance, the FDI inflow reveals a falling tendency from 2000 to 2003, a rising trend from 2004 to 2007, followed by a decline, and so on. The final decline in FDI inflow for the target population was recorded between 2015 and 2019, following which it began to rise again. The appearance of COVID-19 around the end of 2019 has had a detrimental effect on the amount of FDI that is being brought in on a global scale (Khan et al., Citation2021).

Figure 1. Trend of FDI inflow in high income nations (yearly).

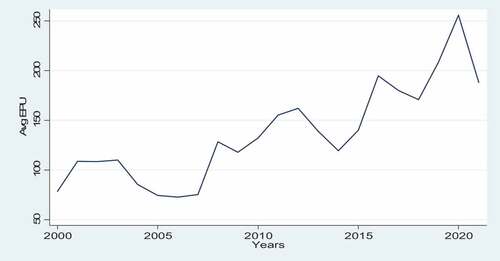

Figure depicts the average annual economic policy uncertainty in 19 countries with higher incomes from 2000 to 2021. Over the past 22 years, the figure indicates a rising tendency of uncertainty. It implies that emerging nations with greater incomes have been confronted with a persistently increasing amount of economic policy uncertainty over several years. Toward the global level, the spread of the Covid-19 pandemic at the end of 2019 has contributed to a rise in the overall level of uncertainty (Khan et al., Citation2021).

Figure 2. Trend of uncertainty in high income nations (yearly).

The rapid development of research on FDI attests to the fact’s growing significance as both a corporate reality and an academic research issue. To attract more FDI, these nations utilize more capital and encourage more investment in financial institutions and financial markets. The high-income economies must maintain their rising income levels, which must attract more foreign capital (mostly FDI). To attract FDI, these nations open up to it more and enact laws that encourage it.

The purpose of this study is to examine the influence of economic policy uncertainty on FDI inflows in 19 high-income economies from 2000 to 2021. In addition, the study investigates the influence of exchange rate, inflation, trade openness, and growth rate on FDI influx for the target population. FDI inflows are foreign investments made in the host nation. FDI inflow is essential for developing nations to increase their savings, achieve economic growth, and preserve their standard of life and national income. The host nation must be politically and legally stable to attract substantial FDI inflows. The uncertainty of future economic policies may discourage foreign investors from investing in the host nation or from withdrawing their investments. The outcome may also show that future consideration of uncertainty is an essential component for gaining a clearer knowledge of how to attract FDI inflows in economies with higher incomes.

The study has strong and more relevant contributions to the literature as follows:

It contributes to the existing body of knowledge that how economic policy uncertainty as the major source of uncertainty in high-income economies helps to determine their FDI inflow.

It also contributes to how the exchange rate, inflation rate, trade openness, and growth rate determine the FDI inflow for high-income economies.

Furthermore, the study also contributes in terms of methodology for using the panel ARDL as the method of estimation for explaining the long-term and short-term impacts of uncertainty on FDI inflow in high-income economies.

The remaining part of this research includes a literature review in the second chapter, data and methodology in the third chapter, and empirical analysis in the fourth chapter. Finally, the conclusions are discussed in chapter 5, and the policy implications and future suggestions are discussed in chapter 6.

2. Literature review

Economic policy uncertainty is a type of risk in which future government policies are uncertain, delaying an individual’s investment or spending decision (Ogbonna et al., Citation2022). There is a possibility that a decline in the amount of foreign direct investment will occur if the level of economic policy uncertainty continues to rise (Smith, Citation2021). This uncertainty may be reduced by stable government policies, laws, etc., which may also lead to an increase in the flow of FDI (Yusuf et al., Citation2020).

2.1. Theoretical underpinning

This study derives its theoretical underpinnings from the eclectic theory in its various versions as formulated and evolved by Dunning (Citation1977), Dunning (Citation1980), and Dunning (Citation1988). The theory asserted that when ownership, localization, and internationalization benefits make foreign manufacturing more cost-effective, domestic firms become global and invest in FDI. This suggests that the primary motivators for international investments are anticipated investment income, investment safety, and the opportunity to withdraw funds when necessary. These elements are highly influenced by the political and economic atmospheres, as well as the larger economic governance systems of the host nation. How overseas investors feel about FDI is determined by the host nation’s socioeconomic circumstances and government laws, as well as the level of ambiguity around such projects.

2.2. Uncertainty and FDI inflow

One of the earliest studies to explain the connection between economic policy uncertainty and FDI was discovered by Ramasamy (Citation2003) for the Malaysian economy. The study underscored the significance of economic uncertainty in attracting international investors. In times of uncertainty, reversibility and delay ability were found to have a significant impact on FDI inflow into the host economy. Uncertainty delays foreign investment or, in severe situations, causes withdrawals. Albulescu and Ionescu (Citation2018) found that stable economic and financial conditions in a host country result in increasing the FDI inflow. They urged decision-makers to stabilize economic policies to reduce policy uncertainty and encourage foreign investment in the host nation.

Eregha (Citation2019) concluded that an economy needs stable economic policies such as currency rate stability, investment risk reduction, export product diversification, etc. to attract foreign capital. Hlaing and Kakinaka (Citation2019) underlined the importance of global uncertainty in determining the foreign capital flows of any economy. However, they discovered that the strength of this relationship differed significantly between developed economies and those that were still in the process of developing. Additionally, Chen et al. (Citation2019) found a significant drop in the level of FDI, while the economic policy uncertainty increases. If there is political stability, including democracy, uncertainty will be reduced, increasing FDI. Furthermore, Zhu et al. (Citation2019) found that politically unstable countries have substantial economic policy uncertainty, which causes capital flight, FDI outflow, and FDI inflow declines. They advised implementing a more democratic and stable political structure to reduce the uncertainty of economic policies, which could attract FDI. Choi et al. (Citation2021) found a negative impact of local uncertainty policy on FDI inflows in the host country. They concluded that the negative impact of this uncertainty may be greater in some economies with high incomes. This means that the negative effect of economic policy uncertainty on FDI inflow in the host economy seems to be softened in countries with developed financial markets.

Sinha and Ghosh (Citation2021) showed a stronger long-term impact of economic policy uncertainty on FDI inflow in India as compared to the short run. They advised establishing economic policies that are predictable to achieve the level of foreign direct investment (FDI) that was required. Ogbonna et al. (Citation2022) found an inverse and highly significant impact of global economic policy uncertainty on FDI inflow for the African region. They proposed authorities implement consistent economic policies to reduce uncertainty and boost FDI in this region. In contrast, it could not be demonstrated that economic policy uncertainty was a significant factor in deciding China’s FDI inflow (Zhang et al., Citation2022). The Chinese economy has moved from FDI inflow to FDI outflow; thus, the same is a big negative influence on FDI outflow. Furthermore, Williams et al. (Citation2022) observed that economic policy uncertainty has a negative and substantial short-run influence on FDI influx in Southern Africa, but a positive and weakly significant long-run impact. Additionally, Bao et al. (Citation2022) discovered that a reduction in the uncertainty of economic and trade policies has the potential to increase the inflow of FDI into China. Regarding the economic climate, regulations, norms, technical development, and financial situation, there is a significant disparity between the countries in the high-income category. Nonetheless, regardless of geography or income level, the uncertainty of any type, has a negative effect on even high-income countries. Historical evidence reveals an inverse association between economic policy uncertainty and FDI inflow for the majority of high-income nations; thus, the following 1st hypothesis is anticipated.

: There is a significantly negative impact of economic policy uncertainty on FDI inflow.

2.3. Exchange rate and FDI Inflow

FDI inflow for high-income host economies boosts demand for their currencies, such as the euro in Europe, the pound in the UK, and the dollar in the USA. The demand for these currencies raises the exchange rate, discouraging foreign investors from investing in high-income economies. A higher exchange rate reduces FDI inflow into these economies. Numerous historical studies have demonstrated a relationship between exchange rates and FDI primarily from wealthy nations. Foreign direct investment is sometimes discouraged in developed nations due to factors including the exchange rate depreciation caused by imperfect capital markets (Froot & Stein, Citation1991). In this situation, a negative relationship between the exchange rate (home per host currency) and FDI is expected. In the instance of the United States, the substantial negative impact of the devaluation of the host currency’s exchange rate was also reported (Barrel & Pain, Citation1998; Blonigen & Feenstra, Citation1997).

The degree of the conversion requirement affects foreign direct investment (FDI) in a few different ways (Hadj Fraj et al., Citation2018). In contrast, the currency rate can occasionally influence FDI inflows to the advantage of one nation and the disadvantage of all others (Lin et al., Citation2020). It has led to low foreign currency, and the economic success of developing nations, like other rising regions, is dependent on foreign investment inflow (Maryam & Mittal, Citation2020). Theoretically and in the literature, the influence of the exchange rate on FDI is ambiguous (Gautam et al., Citation2020). There is no logical explanation for why the exchange rate affects FDI (Babubudjnauth & Seetanah, Citation2020). However, the majority of recent research indicates that exchange rate has a negative effect on FDI inflow in various world economies (e.g. Alshubiri, Citation2022; Eregha, Citation2020; Korsah et al., Citation2022; Moraghen et al., Citation2021, Citation2020; Nwosa, Citation2021; Tan et al., Citation2021). Increasing the exchange rate discourages foreign investors from investing in the host economy, resulting in a decline in foreign direct investment (FDI). The following 2nd hypothesis is formulated based on the bulk of findings in the historical literature and the theoretical perspective of the exchange rate impact on FDI inflow.

: There is a significantly negative impact of the exchange rate on FDI inflow.

2.4. Inflation rate and FDI Inflow

A study conducted in several European nations demonstrated a potentially detrimental effect of inflation on FDI inflow determination (Özkan-Günay, Citation2011). The majority of studies provide evidence in support of the negative and statistically significant impact of inflation rate on FDI inflow in different economies. However, a study conducted in the Indian region indicated that the inflation rate has a negative but statistically insignificant effect on FDI inflow (Singhania & Gupta, Citation2011). Therefore, the divergent evidence still supported the negative impact of the inflation rate on FDI inflow. For example, a study conducted on the Indian nation indicated that inflation has a negative but significant effect on FDI inflow (Kaur & Sharma, Citation2013). In addition, a study conducted in the ASEAN region supported the detrimental impact of inflation on FDI inflow (Xaypanya et al., Citation2015). Similarly, research of BRICS nations utilizing the panel data analysis technique indicated a negative relationship between inflation rate and FDI inflow (Gupta & Singh, Citation2016). Furthermore, a study conducted on emerging nations found a negative and highly significant influence of the inflation rate on FDI inflow (Kumari & Sharma, Citation2017). In addition, a study conducted in Vietnam found that the inflation rate had a negative and significant effect on the FDI inflow (Vi Dũng et al., Citation2018). A similar negative relationship between the inflation rate and foreign direct investment (FDI) inflow was found by some studies (Agudze & Ibhagui, Citation2021; Asiamah et al., Citation2019; Gnangnon, Citation2021; Jaiblai & Shenai, Citation2019; Khudari et al., Citation2023; Morshed & Hossain, Citation2022; Sabir et al., Citation2019; Tahir & Alam, Citation2022; Tien et al., Citation2022). High-income economies like Europe and the UK and the USA have varied macroeconomic, financial, and technical development compared to developing nations like India, Pakistan, etc. Therefore, the majority of research has shown discrepancies in the relevance of influence for the majority of macroeconomic indicators, such as inflation, in various locations. High-income, middle-income, and low-income economies all need domestic and foreign capitals for sustainable growth. The main distinction between the first two hypotheses is the level of relevance of the negative impact of inflation on FDI inflow, which provides the basis for the 3rd hypothesis.

: There is a significantly negative impact of the inflation rate on FDI inflow.

2.5. Trade OPENNESS and FDI inflow

A time-series analysis undertaken in Mauritius revealed a statistically significant and positive relationship between trade openness and FDI inflow (Seetanah & Rojid, Citation2011; Yuxiang & Chen, Citation2011). Furthermore, Jiang et al. (Citation2013) revealed a positive and statistically significant role of trade openness in determining the FDI inflow for China. Similarly, a study conducted in India revealed a statistically significant and positive relationship between trade openness and FDI influx (Kaur & Sharma, Citation2013). Additionally, market openness has a substantial effect on regional trade agreements (Sahoo et al., Citation2014). The same applies to host country financial experts; attractive investment climate and arrangements increase competition inside the country of origin and should fuel FDI surges to confront competitors in business sectors (Kishor & Singh, Citation2015). Similarly, some studies have revealed a positive and significant impact of the inflation rate on FDI inflow in various global locations (Dimitrova et al., Citation2020; Gupta & Singh, Citation2016; Jaiblai & Shenai, Citation2019; Korsah et al., Citation2022; Kumari & Sharma, Citation2017; Maryam & Mittal, Citation2020; Mousavian et al., Citation2021; Saini & Singhania, Citation2018; Smith, Citation2021). Regardless of their differences in the financial environment, income level, and technical development, all the studies under consideration demonstrate the favorable effects of trade openness. The main variation is the level of significance for the beneficial impact of trade openness on FDI inflow, which provides the basis for constructing the 4th hypothesis for high-income economies.

: There is a significantly positive impact of trade openness on FDI inflow.

2.6. Real growth and FDI inflow

A rising real growth rate suggests that an economy is growing and sustaining itself, which encourages foreign investors to invest with confidence in the host economy. As a result, the FDI intake into these economies increases significantly. Research on Mexico and Brazil uncovered a possible positive effect of growth rate on FDI inflow (Castro et al., Citation2013). Additionally, Sahoo et al. (Citation2014) also reported a positive and strong impact of growth rate on FDI inflow in South Asia. Furthermore, Kishor and Singh (Citation2015) observed that an economy with a positive growth rate is more likely to attract foreign capital than one experiencing a recession. Similarly, Aziz and Mishra (Citation2016) also reported a positive link between growth rate and FDI inflow in Arab nations. Developing nations must attract more FDI to increase their development rate (Kumari & Sharma, Citation2017). Numerous recent studies have demonstrated a positive relationship between real growth rate and FDI inflow (Azam & Haseeb, Citation2021; Camarero et al., Citation2020; Gopalan et al., Citation2019; Gupta, Citation2018; Korsah et al., Citation2022; Yimer, Citation2017). Historical literature shows a positive and large impact of real growth rates on FDI inflow, especially for most high-income nations, which forms the basis for the formation of the following 5th hypothesis.

: There is a significantly positive impact of the real growth rate on FDI inflow.

3. Data and methodology

3.1. Data

The analysis comprises 22 years of data at an annual frequency, from 2000 to 2021, for 19 high-income economies. World development indicators (WDI) and economic policy uncertainty websites are utilized as data sources. FDI inflow, exchange rate, inflation rate, trade openness, and real growth rate are among the variables included in the statistics acquired from the WDI website. Additionally, the data obtained from the EPU website include the economic policy uncertainty index. This study requires investigating the impact of uncertainty on FDI inflow in higher-income nations. The EPU website gives economic policy uncertainty index data for higher-income economies only, thus researchers collected data from 2000 to 2021 for 19 nations (high-income group). The EPU data for other groups, such as middle- and low-income economies, were unavailable. As a result, this study focused on high-income economies. To ensure consistency in data collection procedures, the study additionally gathered data for the following variables using the same data availability range.

3.2. Variables

FDI inflow as a percentage of GDP is the study’s output variable. The economic policy uncertainty index measures uncertainty as the independent variable. The remaining factors, exchange rate, inflation, trade openness, and real growth rate, are control variables. The control variables were chosen based on the most common FDI inflow factors identified in several significant international studies. This study necessitates the inclusion of a control variable based on the most significant factors of FDI inflow, which are primarily derived from historical research. Table provides a summary of the study’s measurements of all variables, including their data sources and references.

Table 1. Variable measurement

3.3. Method of estimations

The study compiles data for 19 high-income economies on an annual basis between 2000 and 2021. To increase the number of observations, efficiency, and reliability, the data were processed into a panel format. The panel data is advantageous to other data forms, such as cross-sectional or time series (Mousavian et al., Citation2021). The panel data improve normality and mitigate the multicollinearity problem that typically affects other types of data (Nasir et al., Citation2017). The panel data of this study include N = 19, and T = 22. The panel data are considered as long-form panel data where T > N. Therefore, the data for the present study are long-form panel data. This involves descriptive statistics, a correlation matrix, a cross-sectional dependence test, panel unit root, and panel regression estimates. This study requires estimation approaches such as panel autoregressive distributive lag (ARDL); mean group (MG), pooled mean group (PMG), and dynamic fixed effect (DFE) as per the guidelines of similar research studies (Gupta & Singh, Citation2016). The selection of a suitable estimating method involves the satisfaction of specific criteria; the Hausman test is one of them (Sahin & Ege, Citation2015).

3.4. Modeling

This study must determine the effect of economic policy uncertainty on the FDI inflow of emerging high-income nations from 2000 to 2021. To achieve this purpose, the following economic model, EquationEq. 1(1)

(1) , is constructed.

To evaluate the hypothesis using econometric estimations, the study requires the following basic model, which contains FDI inflow, uncertainty, and control variables: exchange rate, inflation rate, trade openness, and real growth as EquationEq. 2(2)

(2) .

To achieve uniformity in the measured values of all the variables of the study, and to control for basic violations of regression assumptions; multicollinearity, heteroscedasticity, etc., a natural log for each variable was taken, and the following equation 3 is formed.

Based on the data formation as a panel, the study requires applying the relevant techniques for the estimation of data and the testing of the hypothesis. The following 4th equation as the panel regression equation is formed.

Finally, the study also requires estimating the data and testing the hypothesis using the panel ARDL model as per the guidelines of previous research studies (Ganda, Citation2019). The following equation 5th is formed for this purpose.

4. Empirical analysis

The study estimates the impact of economic policy uncertainty on FDI inflow for the target population along with the exchange rate, inflation rate, trade openness, and economic growth rate. For this, the data were assembled into a panel, and estimation procedures such as descriptive statistics, correlation matrix, unit root, cross-sectional dependence, panel co-integration, optimal lag, and panel ARDL were used. Each one’s description and interpretation are provided below.

Table presents the summary statistics and raw data for the variables of the study. During the 22 years (2000–2021), FDI inflows averaged 5.43% of GDP in 19 countries with high incomes. Likewise, the annual average for economic policy uncertainty is 137. In addition, the average exchange rate for the target group over the study period is around $231. In addition, the inflation rate over this time for the target population is 2.42%. Trade openness as a proportion of GDP is reported to be roughly 82% on average. In the last 22 years, the higher-income economies have experienced an average growth rate of 2.62% (2000–2021).

Table 2. Descriptive statistics

Table reports the correlation matrix for the variables of the study. The correlation matrix is used to quantify the relationship between research variables and to test for perfect and significant multicollinearity. The table shows that independent and control variables are not perfectly multicollinear. The table shows a statistically significant negative connection between uncertainty, exchange rate, and FDI inflow. Finally, there is a positive and statistically significant correlation between trade openness, growth rate, and FDI inflow.

Table 3. Correlation matrix

According to Bai et al. (Citation2016), macro-panel data with a series of a long time; T > 20–30, may have the issue of cross-sectional dependence. Furthermore, De Hoyos and Sarafidis (Citation2006) stated that long-form panel data assumes an absence of cross-sectional dependence when choosing between the generation of unit-root testing approaches. The absence of cross-sectional dependence validates the first-generation stationarity testing using LLU, IPS, and Harris & Tzavalis (Sarafidis & Wansbeek, Citation2012). The long-form Panel data where T > N require Breusch-Pagan LM, and Pesaran’s test for testing cross-sectional dependence (Pesaran, Citation2021). Table reports the test statistics and p-values of the required set of these tests. The results confirm the absence of cross-sectional dependence and validate the first-generation unit root.

Table 4. Testing Cross-sectional dependence

Table indicates the stationarity testing using the panel unit root of the first generation. The analysis includes Levin-Lin-Chu, Harris & Tzavalis, and Im-Pesaran-Shin. The null hypothesis assumes a unit root, while the alternative hypothesis assumes stationarity. The table reports that all the variables have stationarity at the level, as well as at the first difference except for the exchange rate, which is stationary at the first difference only. This confirms that a mixed order of stationarity; I(0), I(1) exists in the data, which confirms the test of this hypothesis using Panel ARDL.

Table 5. Panel unit root

The estimation of panel ARDL requires estimating the optimal lag level. The present study considered 19 high-income countries as per the availability of EPU data. The optimal lag for each of these countries is indicated in Table . The AIC criterion was used to select the most optimal lag length for each country (pqqqqqq). “p” stands for the required number of optimal lags for the dependent variable, while “q” refers to the required number of optimal lags for independent variables, respectively. The most common optimal lags for FDI inflow, uncertainty, exchange rate, inflation, trade openness, and economic growth are 1,1,1,0, 1, and

Table 6. Countrywide optimal lag (111,011)

The study requires evaluating panel co-integration as a prerequisite for the estimation of panel ARDL after determining the ideal lag duration. A co-integration test is required to determine whether the estimation includes spurious regression. The existence of co-integration validates the stability of the panel ARDL regression estimate. Using Pedroni and Westerlund’s tests, the existence of co-integration must be determined for a long form of panel data. The null hypothesis of both tests assumes that the variables of the investigation are not co-integrated. Table displays the results of both tests, rejects the null hypothesis, and concludes that the variables in the study are co-integrated.

Table 7. Panel co-integration

To evaluate the required set of hypotheses, the study must estimate the panel ARDL model after validating the long-run co-integration. As estimation approaches, the panel Ardl model utilized pooled mean group (PMG), mean group (MG), and dynamic fixed effect (DFE). The ultimate selection of suitable procedures is determined using the Hausman test. The significance of the Hausman test validated the DFE method for evaluating the final panel ARDL model’s null hypothesis. The panel ARDL DFE model estimates are presented in Table , together with the results of the Hausman test.

Table 8. Panel ARDL (DFE)

The table depicts a negative and statistically significant long-term impact of uncertainty on FDI inflow for selected economies with high incomes. The coefficient value for this negative link indicates that a 1% increase in uncertainty will decrease the FDI inflow by 0.3886%. The negative relationship between uncertainty and FDI inflow accepts the 1st hypothesis. However, in the short run, the same is positive and statistically insignificant. The negative and very significant long-term impact of uncertainty on FDI inflows is consistent with previous unfavorable findings in some influential research (Nguyen & Lee, Citation2021; Ogbonna et al., Citation2022; Sinha & Ghosh, Citation2021; Smith, Citation2021; Williams et al., Citation2022; Zhang et al., Citation2022). According to prior studies, increased uncertainty may cause foreign investors to delay or withdraw from their investments in the host nation. In addition, the table revealed a negative and statistically significant long-term impact of the exchange rate on FDI inflow for the target population during the study period. The coefficient value for this negative impact is 0.0268. It indicates that the FDI inflow declined by 0.0268% by increasing 1% in the exchange rate. This negative link accepts the 2nd hypothesis. Short-run estimations reveal a positive and highly significant influence of exchange rates on high-income FDI inflow. Some important studies show a long-run negative link between the exchange rate and FDI inflow for the target population and period (Alshubiri, Citation2022; Gautam et al., Citation2020; Tan et al., Citation2021). According to previous studies, a rising exchange rate makes foreign currency costlier for foreign investors, discouraging them from investing or motivating them to withdraw from the host country.

The table indicates a negative and statistically significant long-term impact of the inflation rate on FDI inflow for the population under study over the study period. The coefficient value for this negative relationship is 0.0907. It is inferred that a 1% increase in the rate of inflation decreases the FDI inflow by 0.0907%. The negative relationship between the rate of inflation and FDI inflow accepts the 3rd hypothesis. However, the short-term estimates imply that inflation has a positive and statistically significant effect on FDI inflows in high-income economies. The detrimental impact of inflation on FDI inflows over the long run is likewise consistent with prior research findings (Alshubiri, Citation2022; Nguyen & Lee, Citation2021; Smith, Citation2021). Increasing inflation makes it too expensive for foreign investors to invest, which discourages them and reduces FDI inflow. In addition, the table indicates that trade openness is the positive factor influencing FDI inflows for the target population during the study period. The coefficient value for this positive link is 0.5687. It means that a 1% increase in the level of trade openness strongly enhances the FDI inflow by 0.5687%. This positive relationship accepts the 4th hypothesis. However, short-term estimates imply that trade openness has a favorable but small effect on FDI inflows to high-income economies. The positive relationship between trade openness and FDI inflow for the target population throughout the study period is consistent with the findings from other studies (Alshubiri, Citation2022; Nguyen & Lee, Citation2021; Smith, Citation2021). This strong relation may be seen as the relaxation of trade restrictions and promotion of trade openness boosting the trust of foreign investors in the host nation, hence increasing the FDI inflow. Finally, the table reveals a positive and statistically significant long-term effect of the real growth rate on the FDI inflow for higher-income economies during the study period. The coefficient value for this positive link is 0.1181. It is inferred that increasing 1% in the real growth rate enhances the FDI inflow by 0.1181% for the higher-income economies. The positive impact of the real growth rate of FDI inflow accepts the 5th hypothesis. However, short-term estimates imply a negative impact that is statistically insignificant on the growth rate of FDI inflows into high-income economies. This conclusion is consistent with comparable findings from several earlier studies (Korsah et al., Citation2022; Osei & Kim, Citation2020; Shahbaz et al., Citation2021). In keeping with prior research, one possible interpretation for this positive link between real growth rate and FDI influx is that it encourages foreign investors in the host country to increase the inflow of funds, which boosts the FDI inflow.

5. Conclusion

The purpose of this study was to examine the influence of economic policy uncertainty on FDI inflows for 19 economies with higher incomes throughout the period 2000–2021. The dependent variable was foreign direct investment (FDI) inflow, whereas the independent variable was economic policy uncertainty. The exchange rate, inflation rate, trade openness, and real growth rate were the control variables. The data were examined using the panel Ardl method. Based on the relevance of the Hausman test, the DFE method for testing hypotheses with the panel Ardl was finalized. Uncertainty, exchange rate, and inflation have a statistically significant negative influence on FDI inflow for higher-income economies over the study period. Trade openness and real growth rate have a statistically significant positive impact. Growing economic policy uncertainty, exchange rate, and inflation rate deter foreign investors from investing in the host country, but trade openness and real growth rate boost investor confidence in increasing FDI inflow.

6. Policy implications, limitations, and suggestions for future research

The stability of the host country’s political environment and consistency in government regulations favoring foreign investors are economic consequences of the study. Therefore, the policymakers in high-income economies should recommend that governments and relevant authorities stabilize their laws and political environment and make a favorable economic environment for international investors that encourage them to enhance their investment in host economies. Strict laws and a difficult political and economic environment may discourage foreign investors, which ultimately decline their investment in host economies of high-income groups. The implications also include stabilizing the exchange rate, and inflation rate to attract more FDI inflow. In addition, governments must encourage trade openness and real growth in the world’s higher-income economies to increase FDI inflows.

The study’s outcomes apply to higher-income economies but not lower-income/middle-income nations since the level and source of uncertainty for these groups may be different from high-income economies. Future research may include a comparative analysis of economies with higher, middle, and lower incomes.

Acronyms list

FDI – Foreign Direct Investment

EPU – Economic Policy Uncertainty

MG – Mean Group

PMG – Pooled Mean Group

DFE – Dynamic Fixed Effect

ARDL – Autoregressive distributed Lag

EXR – Exchange Rate

INFR – Inflation Rate

TOP – Trade Openness

RGR – Real Growth Rate

WDI – World Development Indicators

GDP – Gross Domestic Product

Availability of data and material

The datasets used and/or analyzed during the current study have been taken from the world development index (WDI) and economic policy uncertainty (EPU) websites and made available from the corresponding author on reasonable request.

Authors contributions

MAH: Conceptualization, Writing the original draft, Data collection, Data analysis, and Designing the methodology, ZB: Supervision and Conceptualization, MUA: Data analysis, Editing, and Revision, NY: Methodology, Revision, and Proofreading.

Ethics statement

This material is the authors’ original work, which has not been previously published elsewhere. The paper is not currently being considered for publication elsewhere.

Sincerely,

Acknowledgements

We thank all editorial board members and anonymous reviewers for reviewing and improving the paper through their valuable suggestions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Agudze, K., & Ibhagui, O. (2021). Inflation and FDI in industrialized and developing economies. International Review of Applied Economics, 35(5), 749–18. https://doi.org/10.1080/02692171.2020.1853683

- Albulescu, C. T., & Ionescu, A. M. (2018). The long-run impact of monetary policy uncertainty and banking stability on inward FDI in EU countries. Research in International Business and Finance, 45, 72–81. https://doi.org/10.1016/j.ribaf.2017.07.133

- Alshubiri, F. (2022). The impact of the real interest rate, the exchange rate and political stability on foreign direct investment inflows: A comparative analysis of G7 and GCC Countries. Asia-Pacific Financial Markets, 29(3), 569–603. https://doi.org/10.1007/s10690-022-09360-0

- Asiamah, M., Ofori, D., & Afful, J. (2019). Analysis of the determinants of foreign direct investment in Ghana. Journal of Asian Business and Economic Studies, 26(1), 56–75. https://doi.org/10.1108/JABES-08-2018-0057

- Azam, M., & Haseeb, M. (2021). Determinants of foreign direct investment in BRICS- does renewable and non-renewable energy matter? Energy Strategy Reviews, 35, 100638. https://doi.org/10.1016/j.esr.2021.100638

- Aziz, O. G., & Mishra, A. V. (2016). Determinants of FDI inflows to Arab economies. The Journal of International Trade & Economic Development, 25(3), 325–356. https://doi.org/10.1080/09638199.2015.1057610

- Babubudjnauth, A., & Seetanah, B. (2020). An empirical investigation of the relationship between the real exchange rate and net FDI inflows in Mauritius. African Journal of Economic and Management Studies, 11(1), 63–74. https://doi.org/10.1108/AJEMS-02-2019-0081

- Bai, J., Baltagi, B., Pesaran, H., Bai, J., Baltagi, B., & Pesaran, H. (2016). Cross-Sectional dependence in panel data models, a special issue. Journal of Applied Econometrics, 31(1), 1–3. https://doi.org/10.1002/jae.2507

- Bao, X., Deng, J., Sun, H., & Sun, J. (2022). Trade policy uncertainty and foreign direct investment: Evidence from China’s WTO accession. Journal of International Money and Finance, 125, 102642. https://doi.org/10.1016/j.jimonfin.2022.102642

- Barrel, R., & Pain, N. (1998). Real exchange rates. agglomeration, and.

- Blonigen, B. A. (2005). A review of the empirical literature on FDI determinants. Atlantic Economic Journal, 33(4), 383–403. https://doi.org/10.1007/s11293-005-2868-9

- Blonigen, B., & Feenstra, R. (1997). Protectionist threats and FDI. In Robert, C. F. (Ed.) effects of US trade protection and promotion policies (pp.55-80). University of Chicago Press for NBER.

- Camarero, M., Montolio, L., & Tamarit, C. (2020). Determinants of FDI for Spanish regions: Evidence using stock data. Empirical Economics, 59(6), 2779–2820. https://doi.org/10.1007/s00181-019-01748-8

- Canh, N. P., Binh, N. T., Thanh, S. D., & Schinckus, C. (2020). Determinants of foreign direct investment inflows: The role of economic policy uncertainty. International Economics, 161, 159–172. https://doi.org/10.1016/j.inteco.2019.11.012

- Castro, P. G. D., Fernandes, E. A., & Campos, A. C. (2013). The determinants of foreign direct investment in Brazil and Mexico: An Empirical Analysis. Procedia Economics and Finance, 5, 231–240. https://doi.org/10.1016/S2212-5671(13)00029-4

- Chen, K., Nie, H., & Ge, Z. (2019). Policy uncertainty and FDI: Evidence from national elections. The Journal of International Trade & Economic Development, 28(4), 419–428. https://doi.org/10.1080/09638199.2018.1545860

- Choi, S., Furceri, D., & Yoon, C. (2021). Policy uncertainty and foreign direct investment [https://doi.org/https://doi.org/10.1111/roie.12495]. Review of International Economics, 29(2), 195–227. https://doi.org/10.1111/roie.12495

- De Hoyos, R. E., & Sarafidis, V. (2006). Testing for cross-sectional dependence in panel-data models. The Stata Journal, 6(4), 482–496. https://doi.org/10.1177/1536867X0600600403

- Dimitrova, A., Rogmans, T., & Triki, D. (2020). Country-specific determinants of FDI inflows to the MENA region. Multinational Business Review, 28(1), 1–38. https://doi.org/10.1108/MBR-01-2019-0003

- Dunning, J. H. (1977). Trade, location of economic activity and the MNE: A search for an eclectic approach. In B. Ohlin, P.-O. Hesselborn, & P. M. Wijkman (Eds.), The International Allocation of Economic Activity: Proceedings of a Nobel Symposium held at Stockholm (pp. 395–418). Palgrave Macmillan UK. https://doi.org/10.1007/978-1-349-03196-2_38

- Dunning, J. H. (1980). toward an eclectic theory of international production: Some empirical tests. Journal of International Business Studies, 11(1), 9–31. https://doi.org/10.1057/palgrave.jibs.8490593

- Dunning, J. H. (1988). The theory of international production. The International Trade Journal, 3(1), 21–66. https://doi.org/10.1080/08853908808523656

- Eregha, P. B. (2019). Exchange rate, uncertainty and foreign direct investment inflow in west African Monetary Zone. Global Business Review, 20(1), 1–12. https://doi.org/10.1177/0972150918803835

- Eregha, P. B. (2020). Exchange rate regimes and foreign direct investment flow in west African Monetary Zone (WAMZ). International Economic Journal, 34(1), 85–99. https://doi.org/10.1080/10168737.2019.1669689

- Froot, K. A., & Stein, J. C. (1991). Exchange rates and foreign direct investment: An imperfect capital markets approach. The Quarterly Journal of Economics, 106(4), 1191–1217. https://doi.org/10.2307/2937961

- Ganda, F. (2019). The environmental impacts of financial development in OECD countries: A panel GMM approach. Environmental Science and Pollution Research, 26(7), 6758–6772. https://doi.org/10.1007/s11356-019-04143-z

- Gautam, S., Chadha, V., & Malik, R. K. (2020). Inter-linkages between real exchange rate and capital flows in BRICS economies. Transnational Corporations Review, 12(3), 219–236. https://doi.org/10.1080/19186444.2020.1779525

- Gnangnon, S. K. (2021). Aid for trade and inflation: Exploring the trade openness, export product diversification and foreign direct investment channels [https://doi.org/https://doi.org/10.1111/1467-8454.12219]. Australian Economic Papers, 60(4), 563–593. https://doi.org/10.1111/1467-8454.12219

- Gopalan, S., Rajan, R. S., & Duong, L. N. T. (2019). Roads to Prosperity? Determinants of FDI in China and ASEAN. The Chinese Economy, 52(4), 318–341. https://doi.org/10.1080/10971475.2018.1559092

- Gupta, J. (2018). Trends and Macro-economic determinants of FDI Inflows to India. In Mayank S. (Ed.) Advances in Computing and Data Sciences (Vol. 96). Singapore: Springer.

- Gupta, P., & Singh, A. (2016). Determinants of foreign direct investment inflows in BRICS Nations: A Panel Data Analysis. Emerging Economy Studies, 2(2), 181–198. https://doi.org/10.1177/2394901516661095

- Hadj Fraj, S., Hamdaoui, M., & Maktouf, S. (2018). Governance and economic growth: The role of the exchange rate regime. International Economics, 156, 326–364. https://doi.org/10.1016/j.inteco.2018.05.003

- Hlaing, S. W., & Kakinaka, M. (2019). Global uncertainty and capital flows: Any difference between foreign direct investment and portfolio investment? Applied Economics Letters, 26(3), 202–209. https://doi.org/10.1080/13504851.2018.1458182

- Jaiblai, P., & Shenai, V. (2019). The Determinants of FDI in Sub-Saharan Economies: A Study of Data from 1990–2017. International Journal of Financial Studies, 7(3), 43. https://doi.org/10.3390/ijfs7030043

- Jiang, N., Liping, W., & Sharma, K. (2013). Trends, Patterns and Determinants of Foreign Direct Investment in China. Global Business Review, 14(2), 201–210. https://doi.org/10.1177/0972150913477307

- Kaur, M., & Sharma, R. (2013). Determinants of foreign direct investment in India: An empirical analysis. DECISION, 40(1), 57–67. https://doi.org/10.1007/s40622-013-0010-4

- Khan, A., Khan, N., & Shafiq, M. (2021). The economic impact of COVID-19 from a global perspective [Report]. Contemporary Economics, 15(1), 64+. https://doi.org/10.5709/ce.1897-9254.436

- Khudari, M., Sapuan, N. M., & Fadhil, M. A. (2023). The impact of political stability and macroeconomic variables on foreign direct investment in Turkey. Innovation of Businesses, and Digitalization during Covid-19 Pandemic, Cham. https://doi.org/10.1007/978-3-031-08090-6_31

- Kishor, N., & Singh, R. P. (2015). Determinants of FDI and its Impact on BRICS Countries: A panel data approach. Transnational Corporations Review, 7(3), 269–278. https://doi.org/10.5148/tncr.2015.7302

- Korsah, E., Amanamah, R. B., & Gyimah, P. (2022). Drivers of foreign direct investment: New evidence from West African regions. Journal of Business and Socio-economic Development, https://doi.org/10.1108/JBSED-12-2021-0173

- Kumari, R., & Sharma, A. K. (2017). Determinants of foreign direct investment in developing countries: A panel data study. International Journal of Emerging Markets, 12(4), 658–682. https://doi.org/10.1108/IJoEM-10-2014-0169

- Lin, Z., Ouyang, R., & Zhang, X. (2020). The effects of macro news on exchange rates volatilities: Evidence from BRICS Countries. Emerging Markets Finance and Trade, 56(8), 1817–1842. https://doi.org/10.1080/1540496X.2019.1680540

- Maryam, J., & Mittal, A. (2020). Foreign direct investment into BRICS: An empirical analysis. Transnational Corporations Review, 12(1), 1–9. https://doi.org/10.1080/19186444.2019.1709400

- Moraghen, W., Seetanah, B., & Sookia, N. U. H. (2020) The impact of exchange rate and exchange rate volatility on Mauritius foreign direct investment: A sector-wise analysis [https://doi.org/https://doi.org/10.1002/ijfe.2416]. International Journal of Finance & Economics. n/a(n/a. https://doi.org/10.1002/ijfe.2416.

- Moraghen, W., Seetanah, B., & Sookia, N. (2021). Impact of exchange rate and exchange rate volatility on foreign direct investment inflow for Mauritius: A dynamic time series approach [https://doi.org/https://doi.org/10.1111/1467-8268.12596]. African Development Review, 33(4), 581–591. https://doi.org/10.1111/1467-8268.12596

- Morshed, N., & Hossain, M. R. (2022). Causality analysis of the determinants of FDI in Bangladesh: Fresh evidence from VAR, VECM and Granger causality approach. SN Business & Economics, 2(7), 64. https://doi.org/10.1007/s43546-022-00247-w

- Mousavian, S. R. Z., Mirdamadi, S. M., Farajallah Hosseini, S. J., & Omidi Najafabadi, M. (2021). Determinants of foreign direct investment inflow to the agricultural sector: A panel-data analysis. Journal of Economic and Administrative Sciences, https://doi.org/10.1108/JEAS-11-2020-0196

- Nasir, M. A., Ahmad, F., & Ahmad, M. (2017). Foreign direct investment, aggregate demand conditions and exchange rate Nexus: A panel data analysis of BRICS Economies. Global Economy Journal, 17(1. https://doi.org/10.1515/gej-2016-0012

- Nguyen, C. P., & Lee, G. S. (2021). Uncertainty, financial development, and FDI inflows: Global evidence. Economic Modelling, 99, 105473. https://doi.org/10.1016/j.econmod.2021.02.014

- Nwosa, P. I. (2021). Oil price, exchange rate and stock market performance during the COVID-19 pandemic: Implications for TNCs and FDI inflow in Nigeria. Transnational Corporations Review, 13(1), 125–137. https://doi.org/10.1080/19186444.2020.1855957

- Ogbonna, O. E., Ogbuabor, J. E., Manasseh, C. O., & Ekeocha, D. O. (2022). Global uncertainty, economic governance institutions and foreign direct investment inflow in Africa. Economic Change and Restructuring, 55(4), 2111–2136. https://doi.org/10.1007/s10644-021-09378-w

- Osei, M. J., & Kim, J. (2020). Foreign direct investment and economic growth: Is more financial development better? Economic Modelling, 93, 154–161. https://doi.org/10.1016/j.econmod.2020.07.009

- Özkan-Günay, E. N. (2011). Determinants of FDI inflows and policy implications: A comparative study for the enlarged eu and candidate countries. Emerging Markets Finance and Trade, 47(sup4), 71–85. https://doi.org/10.2753/REE1540-496X4705S405

- Pesaran, M. H. (2021). General diagnostic tests for cross-sectional dependence in panels. Empirical Economics, 60(1), 13–50. https://doi.org/10.1007/s00181-020-01875-7

- Ramasamy, B. (2003). FDI and uncertainty: The Malaysian case. Journal of the Asia Pacific Economy, 8(1), 85–101. https://doi.org/10.1080/1354786032000045255

- Sabir, S., Rafique, A., & Abbas, K. (2019). Institutions and FDI: Evidence from developed and developing countries. Financial Innovation, 5(1), 8. https://doi.org/10.1186/s40854-019-0123-7

- Sahin, S., & Ege, I. (2015). Financial Development and FDI in Greece and Neighbouring Countries: A Panel Data Analysis. Procedia Economics and Finance, 24, 583–588. https://doi.org/10.1016/S2212-5671(15)00640-1

- Sahoo, P., Nataraj, G., & Dash, R. K. (2014). Determinants of FDI in South Asia. In P. Sahoo, G. Nataraj, & R. K. Dash (Eds.), Foreign Direct Investment in South Asia: Policy, Impact, Determinants and Challenges (pp. 163–199). Springer India. https://doi.org/10.1007/978-81-322-1536-3_6

- Saini, N., & Singhania, M. (2018). Determinants of FDI in developed and developing countries: A quantitative analysis using GMM. Journal of Economic Studies, 45(2), 348–382. https://doi.org/10.1108/JES-07-2016-0138

- Sarafidis, V., & Wansbeek, T. (2012). Cross-sectional dependence in panel data analysis. Econometric Reviews, 31(5), 483–531. https://doi.org/10.1080/07474938.2011.611458

- Seetanah, B., & Rojid, S. (2011). The determinants of FDI in Mauritius: A dynamic time series investigation. African Journal of Economic and Management Studies, 2(1), 24–41. https://doi.org/10.1108/20400701111110759

- Shahbaz, M., Mateev, M., Abosedra, S., Nasir, M. A., & Jiao, Z. (2021). Determinants of FDI in France: Role of transport infrastructure, education, financial development and energy consumption [https://doi.org/10.1002/ijfe.1853]. International Journal of Finance & Economics, 26(1), 1351–1374. https://doi.org/10.1002/ijfe.1853

- Singhania, M., & Gupta, A. (2011). Determinants of foreign direct investment in India. Journal of International Trade Law and Policy, 10(1), 64–82. https://doi.org/10.1108/14770021111116142

- Sinha, A., & Ghosh, T. (2021). Impact of Economic Policy Uncertainty on FDI Inflows: Evidence from India. W. A. Barnett & B. S. Sergi(Eds.), Recent Developments in Asian Economics International Symposia in Economic Theory and Econometrics. (Vol. Vol. 28, pp. 157–167). Emerald Publishing Limited. https://doi.org/10.1108/S1571-038620210000028009

- Smith, F. (2021). Uncertainty, Financial Development and FDI Inflows: France Evidence. Asian Business Research Journal, 6, 7–13. https://doi.org/10.20448/journal.518.2021.6.7.13

- Suh, H., & Yang, J. Y. (2021). Global uncertainty and Global Economic Policy Uncertainty: Different implications for firm investment. Economics Letters, 200, 109767. https://doi.org/10.1016/j.econlet.2021.109767

- Tahir, M., & Alam, M. B. (2022). Does well banking performance attract FDI? Empirical evidence from the SAARC economies. International Journal of Emerging Markets, 17(2), 413–432. https://doi.org/10.1108/IJOEM-04-2020-0441

- Tan, L., Xu, Y., Gashaw, A., & Gil-Lafuente, A. M. (2021). Influence of Exchange Rate on Foreign Direct Investment Inflows: An Empirical Analysis Based on Co-Integration and Granger Causality Test. Mathematical Problems in Engineering, 2021, 7280879. https://doi.org/10.1155/2021/7280879

- Tien, L. T., Duc, N. C., & Kieu, V. T. T. (2022). The Effect of Exchange Rate Volatility on FDI Inflows: A Bayesian Random-Effect Panel Data Model. In Financial Econometrics: Bayesian Analysis, Quantum Uncertainty, and Related Topics. ECONVN 2022. Studies in Systems, Decision and Control, vol 427. Springer, Cham. https://doi.org/10.1007/978-3-030-98689-6_32

- Vi Dũng, N., Bíchthủy, Đ. T., & Ngọcthắng, N. (2018). Economic and non-economic determinants of FDI inflows in Vietnam: A sub-national analysisPost-Communist Economies. Post-Communist Economies, 30(5), 693–712. https://doi.org/10.1080/14631377.2018.1458458

- Williams, M., Alrub, A. A., & Aga, M. (2022). Ecological Footprint, Economic Uncertainty and Foreign Direct Investment in South Africa: Evidence From Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Approach. SAGE Open, 12(2), 21582440221094607. https://doi.org/10.1177/21582440221094607

- Xaypanya, P., Rangkakulnuwat, P., & Paweenawat, S. W. (2015). The determinants of foreign direct investment in ASEAN. International Journal of Social Economics, 42(3), 239–250. https://doi.org/10.1108/IJSE-10-2013-0238

- Yimer, A. (2017). Macroeconomic, Political, and Institutional Determinants of FDI Inflows to Ethiopia: An ARDL Approach. In A. Heshmati (Ed.), Studies on Economic Development and Growth in Selected African Countries (pp. 123–151). Springer Singapore. https://doi.org/10.1007/978-981-10-4451-9_7

- Yusuf, H. A., Shittu, W. O., Akanbi, S. B., Umar, H. M., & Abdulrahman, I. A. (2020). The role of foreign direct investment, financial development, democracy and political (in)stability on economic growth in West Africa. International Trade, Politics and Development, 4(1), 27–46. https://doi.org/10.1108/ITPD-01-2020-0002

- Yuxiang, K., & Chen, Z. (2011). Resource abundance and financial development: Evidence from China. Resources Policy, 36(1), 72–79. https://doi.org/10.1016/j.resourpol.2010.05.002

- Zhang, L., Colak, G., & Zi, S. (2022). Foreign direct investment and economic policy uncertainty in China. Economic and Political Studies, 1–11. https://doi.org/10.1080/20954816.2022.2090096

- Zhu, J., Jia, F., & Wu, H. (2019). Bankruptcy costs, economic policy uncertainty, and FDI entry and exit. Review of International Economics, 27(4), 1063–1080. https://doi.org/10.1111/roie.12412