?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

A stable economic condition is crucial for an organization’s success. Any fluctuation in economic policy directly influences corporate-level decisions. However, exercising better governance can mitigate the adverse effect of such unstable economic conditions. Owing to this, the current research tends to disclose the impact of economic policy uncertainty (EPU) on corporate investment decisions and how this impact varies across countries having better governance quality. To achieve the underlying objective, we use the data for the years 2010–2019 of publicly listed enterprises from 6 Asian economies. The empirical analysis was performed by employing the generalized least square (GLS) and GMM techniques. The statistical analysis reveals an inverse relationship between EPU and corporate investment while a direct relationship between governance quality and corporate investment. In addition to individual impact, better governance quality can mitigate the magnitude of the adverse impact of EPU on corporate investment. Better governance can diversify the negative impacts of EPU by protecting investor rights, eliminating information asymmetric, and enhancing policy stability. Based on empirical analysis, the policy officials are directed to exert efforts for exercising better governance. Similarly, corporate managers are advised to consider the current economic situation while formulating any strategy relating to physical investment. This study is innovative as it reinforces the significance of better governance in disentangling the adverse impacts of EPU on corporate investment.

Public Interest Statement

This study highlights the significance of governance quality in mitigating the adverse impact of economic policy uncertainty (EPU) on corporate investment decisions. EPU has an adverse impact while governance quality shows a positive relationship with corporate investment. In addition to individual analysis, the better governance quality shows a moderating role in deferring the adverse impact of EPU on investment. The findings recommend an open policy to corporate managers regarding the management of investment as they should invest more during better governance quality. In addition, they should equally consider the economic sensitivity of investment and should develop some corporate-level policies, e.g., holding more cash, etc., to enhance the immunity of firms against adverse impacts of EPU.

1. Introduction

The industrial community (including all firms from different industrial sectors) is a key member of an economic environment and is open to being affected by any change in existing economic policy. Generally, the industrial sector adjusts its financial and investing decisions according to the policy movements of the federal government. Economic policy shocks can mitigate the organizational efficiency related to such decisions because such shocks reduce the profit, sale volume, and even the return on investment. In this regard, the study arranged by Chen et al. (Citation2019) has documented the adverse impact of economic policy uncertainty (EPU hereafter) on corporate investment decisions. Not surprisingly, there exist several studies that explicitly illustrated the negative influence of EPU on corporate investment decisions (Akron et al., Citation2020; Wang et al., Citation2014; Xie et al., Citation2019). Most studies have explored the potential impact of EPU on corporate investment decisions, but limited literature offers a solution to how can we overcome such adverse impacts of EPU. Thus, this study offers new insights regarding the governance effectiveness in mitigating the adverse effects of EPU on corporate investment. Mainly, this study explores the moderating role of governance in the nexus of EPU-corporate investment.

In literature, an extensive debate has been on the possible consequences of EPU for various business decisions. In this regard, Demir and Ersan (Citation2017), and Feng et al. (Citation2019) have documented the effect of EPU on cash holdings, Cui et al. (Citation2021a) have asserted the relationship between EPU and earnings management, Lee et al. (Citation2021) have argued the impact of EPU on financing decisions, and Iqbal et al. (Citation2020) have highlighted the possible consequences of EPU for the financial performance of industrial sectors. Given such adverse impacts of EPU on various business decisions, it is crucial to disseminate such policies that can ensure policy stability and can impede the adverse impacts of EPU on business decisions. Among the other factors, exercising better governance can decouple the adverse impacts of EPU (Omoteso & Mobolaji, Citation2014). Furthermore, a better institutional quality that reflects the good governance situation can ensure the protection of investors’ rights in a country (Driss et al., Citation2021) which eventually leads to boost in the investment behavior of corporate managers. Leaning on such arguments, it can be suggested that a better governance system can moderate the adverse impacts of EPU on corporate investment decisions.

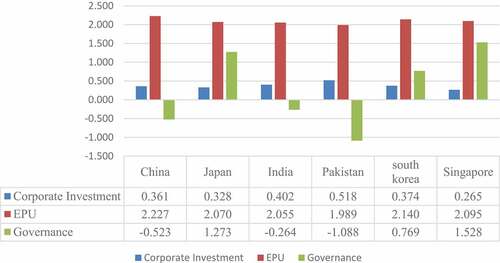

Economic policy uncertainty is an emanating challenge for policy analysts as it can hamper the growth of almost all economic sectors of an economy (Istiak & Serletis, Citation2018). This effect is stronger in emerging economies that are already sufferings from other economic complexities including energy crisis, unskilled labor, and lack of subsidies, etc. Thus, it is necessary to develop a strategic solution to overcome the adverse impacts of EPU on industrial decisions specifically in such economies. Supporting this, the study of Doan et al. (Citation2020) has observed the co-movements among country-level governance, stock price synchronicity for banks, and economic policy uncertainty. They have explicitly documented that country-level governance can help to reduce the synchronicity in stock prices of commercial banks in emerging economies. They have also found robust evidence that EPU changes the direction of liaison between governance and stock price synchronicity. Following this, it can be comprehended that EPU, and governance have conjunction impacts on other financial decisions of the industrial sector, e.g., investment decisions. Owing to this, the current study is intended to find out the empirical impacts of EPU, and governance on investment decisions and how this relationship changes across the countries having better governance scores. As governance has strong strategical linkages with both EPU and investment, therefore it is obvious to consider its role as a moderating variable in the relationship between EPU and corporate investment. The quality of governance helps to manage the spurious economic situation caused by EPU in a country. It can further mitigate the negative spillover impacts of EPU on the efficiency of other economic sectors (Essen et al., Citation2013). Figure explains the relative trend between three main variables of the study, i.e., corporate investment, EPU, and governance. According to Figure , the highest EPU is suffered by China (2.227), followed by South Korea (2.140), Singapore (2.095), Japan (2.070), India (2.055), and Pakistan (1.989). Due to low uncertainty, Pakistani enterprises have a high investment ratio of 0.518, corroborating the inverse relationship between EPU and corporate investment.

Figure 1. Trend across the countries.

This study explores the moderating role of governance quality in the nexus between EPU and corporate investment decisions. For empirical analysis, we collect the 10-years (2010–2019) financial information of non-financial publicly listed firms from 6 Asian economies. The calculation of EPU is based upon the established indices of Baker et al. (Citation2016) while corporate investment decision is quantified as total expenditure incurred on PPE acquisition in fractioned with total assets. Similarly, the mathematical measurement of country-level governance was extracted from World Governance Indicator, The World Bank. The statistics of panel GLS and two-step system GMM techniques imply that EPU has an adverse impact on investment decisions. However, such a declining trend in investment due to high EPU responds differently when country-level governance was considered as a moderating variable in a formal relationship. A better quality of governance can deter the adverse impact of EPU on investment decisions. Briefly, the analysis provides explicit evidence on moderating effect of country-level governance between the relationship of EPU and investment decisions. In addition, the empirical analysis portrays the dynamic impact of other control variables considered at the firm level and country level on corporate investment.

This study contributes in the following ways: it provides robustness to empirical studies arranged on the liaison between EPU and corporate investment decisions in alternative data specification. However, most studies were limited to formal analysis and were unable to explore the possible solution to how we can mitigate the unfavorable impacts of EPU on investment decisions. Thus, current research has novel outcomes as it provides the clear significance of country-level governance to curtail the adverse impacts of EPU on industrial decisions, specifically investment decisions. This research also contributes novel ideas regarding the potential impact of accumulative governance and also the dynamic role of other indices of governance in determining the physical investment decisions of corporate firms. Limited studies found which have such arrangements of empirical analysis. Additionally, the current analysis provides meaningful policy insights to both economic policy officials and corporate managers regarding EPU and governance effects on corporate investment. Following the statistical outputs, this study suggests to policy officials that they should focus on policy stability and the exaggeration of better governance quality. Likewise, corporate managers should composite such investment strategies that can bear the volatility of policy uncertainty. They should attentively consider the current economic conditions while making investment strategies. In addition, this study asserts that corporate managers should enhance their investment during better governance because it has a positive effect on corporate investment. During better governance, there is a low probability of information asymmetric, and corporate firms may enjoy an early payout period due to transparency in business proceedings. Thus, it is recommended to enhance the investment during better governance. Additionally, the current analysis argues to international investors to invest in countries having good governance situations.

The residual paper carries the following sections: Section 2 explains the empirical findings of related literature and builds the hypotheses. Section 3 interprets the material and methods and section 4 offers the statistical results. Similarly, section 5 consists of the discussion on empirical results, and section 6 belong to the conclusion and policy implications.

2. Review of literature

The liaison between EPU and corporate investment decisions has been well-established in the literature. There exists an array of studies that attempt to explore the dynamic connection between EPU and firm-specific decisions (Akron et al., Citation2020; Chen et al., Citation2019; Wang et al., Citation2014). However, the findings of these studies are still inconclusive and limited to a formal relationship. The theoretical notion of the classical theory (Knight, Citation1921) asserted that corporate firms having the ability to evaluate investment options even in uncertain economic situations can earn profit through the integration of resources. The theorization of this theory can be used to build the link between the variables of the study. Better governance enhances the ability to evaluate the investment as it reduces the information asymmetric and protects the investor rights. Therefore, corporate managers can make more appropriate decisions regarding investment management even in the high EPU era. Similarly, another economic approach introduced by Hartman (Citation1972) and Abel (Citation1983) described the liaison between uncertainty and return on investment under the assumptions of perfect competition, and symmetrical adjustment of cost. Such theoretical statements were later advocated by Abel and Blanchard (Citation1986). Contrary to these, Caballero (Citation1991) documented that uncertainty hampers the investment of the industrial sector if we forgo the assumptions of Hartman’s (Citation1972) and Abel’s (Citation1983) models. The theoretical views of these theories provide underpinnings, i.e., EPU discourages the investment behavior of corporate managers. Nonetheless, such questionable contentions regarding the literature urge to expand more empirical studies on how EPU influences the industrial sector investment decisions.

2.1. Economic policy uncertainty (EPU) and investment

EPU can affect corporate capital investment decisions through various channels. The uncertain economic condition makes the investment spending irreversible and enhances the sunk cost by leveraging the information asymmetric problem (J. Wu et al., Citation2020). This factor allows the firms to make the weight between current and future investment options. For instance, Adjei and Adjei (Citation2017) vowed that economic uncertainty delayed the return on investment which eventually discouraged the firms from investing during such economic conditions. Additionally, policy uncertainty can raise the expected cost of investment projects due to fluctuations in economic conditions (Wang et al., Citation2014), and hence reduced the return on such investments. This effect is rigorous in developing economies where entrepreneurs typically follow the policy changes and limit their investment preferences until policy reforms have been executed. At the macro level, Zhang (Citation2019) asserted that an uncertain economic environment mitigates the legal protection of investors’ rights, thus leading to harm the investor’s confidence to make any investment.

Empirically, a study organized by Xie et al. (Citation2019) has indicated the inverse liaison between EPU and corporate investment decisions. He et al. (Citation2020) have also illustrated the inverse liaison between policy uncertainty and the investment decisions of enterprises. Cui et al. (Citation2021) conducted a study by examining the EPU impact on corporate innovation investment. Xu (Citation2020) discloses that the EPU upsurges cost regarding capital, and due to this the government does not prefer to further invest in innovation. Similarly, the work of Zhang (Citation2019) asserted that the existence of EPU in the host country discourages firms from overseas investment. They further illustrated that firms face uncertainty during high EPU and thus are unable to make strong decisions. Ilyas et al. (Citation2021) have expressed that the EPU limits a firm’s investment, reflecting the inverse relationship between EPU and investment. This negative liaison between EPU and investment was observed across various sub-samples. Moreover, this liaison is more pronounced in oil-producing economies than in oil-consumption economies. Liu and Zhang (Citation2020) noted that the upward movement of EPU impedes investment. They further vowed that banks and other financial institutions feel hesitation while granting debt during high EPU. Darsono et al. (Citation2022) also found a negative link between EPU and sustainable investment. Jackson and Orr (Citation2019) have identified the negative influence of EPU on managerial confidence regarding any venture investment. Recently, Chu and Fang (Citation2021) have observed decreasing trend in investment volume during the high EPU era in China. Leaning on the empirical findings of previous studies, it can be argued that

H1: Economic policy uncertainty has a negative relationship with corporate investment.

2.2. Country-level governance and investment

The better governance situation enhances institutional transparency within the country. It matters both at the micro-level and macro-level. Each state defined its own specific rules and regulations to regularize the overall operations within the state. The transparency in the execution of such rules and regulations reflects the governance quality and it further has a close link to the decisional efficiency of other state stakeholders, e.g., industrial sectors. The governance system has a major chunk in determining overall economic progress, and due to this the industrial sectors consider the sensitivity of country governance. During a better governance system, corporate managers are more optimistic about future economic and industrial growth and thus are more likely to enhance their investment both in physical projects and security markets (Caixe, Citation2022). In this essence, many scholarly articles have emerged in the recent decade exploring the connection between corporate governance and corporate investment. The study of Azhar et al. (Citation2019) has described the positive impact of governance on investment. Another work by Iheonu et al. (Citation2019) worked to find the connection between governance and domestic investment by using Driscoll and Kray’s fixed effect technique. Their findings disclose that governance has a positive link with domestic investment which further unveil that when adequate governance exists, the volume of investment will upsurge. Other recent studies resulted in similar empirical outcomes regarding the connection between governance and investment (Bah & Kpognon, Citation2021; Cohen et al., Citation2017; Ogbonna et al., Citation2022). Irrespective of abundant literature, no analysis was found exploring the relevant impact of governance on corporate investment. However, leaning on empirical suggestions of existing literature, it can be declared that

H2: There is a positive link between governance and investment.

2.3. Policy uncertainty, governance, and investment decisions

Irrespective of the negative influence of EPU on corporate investment decisions, some studies have argued the influential behavior of some firm-specific factors on the liaison between EPU and investment decisions. These factors include firm size and financial constraints (Duchin et al., Citation2010; Xie, Citation2009). Likewise, another study arranged by Wang et al. (Citation2014) indicated that firms having high returns on investment are less affected by EPU. Guariglia et al. (Citation2011) posit that usage of internal finance for investment purposes can eliminate the adverse impacts of EPU on investment decisions. The empirical findings of these studies explained the role of firm-specific factors in deterring EPU influence on corporate investment decisions. At the macro level, there exist some factors that can impede the EPU’s influence on corporate investment decisions. The intervention of official authorities in the financial market can eliminate the EPU’s impact on industrial investment decisions. Huang et al. (Citation2011) have reported that state-owned enterprises have more certain information about policy movements and thus are willing to invest more in capital projects. Another study conducted by Passos and Modenesi (Citation2021) has highlighted the comparative advantage of state-owned banks over non-state-owned banks regarding monetary policy transmission. They stated that state-owned banks have more monetary policy execution power. These studies guide the transformation of country-level factors into the liaison between EPU and investment. However, no research was found that argued the dynamical role of governance (another macroeconomic factor) in determining the influence of EPU on corporate investment decisions.

Recent research organized by Lee et al. (Citation2020) has explicitly vowed that governance plays a particular role in mitigating corruption, which further led to more innovation investment. A high level of corruption restraints managers’ investment in innovation due to the non-protection of copyrights. However, the likelihood of a firm’s innovation can be increased by ensuring the governance implications. Doan et al. (Citation2020) have also found the co-movement of governance, bank price synchronicity, and political uncertainty. Omri (Citation2020) indicated the significance of governance in the regularization of entrepreneurship activities. They have suggested that governance has a positive influence on formal entrepreneurship activities and a negative impact on information activities. The negative influence on informal activities advocates that a good governance situation protects the investor rights which eventually led to more investment. In the line with these views, it can be stated that

H3: Governance quality has a moderating impact on the nexus between EPU and investment decisions.

3. Data and methodology

3.1. Data description

The current analysis is based on a sample of 10 years of data, spanning from 2010 to 2019. We use this span due to exclusion of two extraordinary events incurred in 2008 (2007–2008 financial depression across the world) and 2020 (spread of COVID). During the occurrence of both events, the corporate firms may follow dynamic strategies regarding investment and therefore show abnormal performance towards investing. Moreover, countries may experience different EPU scores and governance during both events. Thus, we limit our sample between these two spans (2010–2019) to get an unbiased analysis. We collect the data from non-financial sector firms from six Asian economies (China, India, Japan, Pakistan, Singapore, and South Korea). The selection of underlying Asian economies is subject to the availability of data and prevailing governance and EPU issues in these economies. In this study, we pursue the deductive technique of research and utilize secondary data for empirical analysis. Table gives information about data sources and the data availability statement comprises of.Footnote1

Table 1. Data source

An analysis based upon non-financial sector firms; we arrange our sample by ignoring the firms of the financial sector having SIC codes 6000 to 6999. Such type of firms was excluded due to irrelevancy with any physical investment. Financial sector firms do not indulge in any type of physical investment projects but invest in securities. Moreover, we exclude the financial firms as such firms do not involve in any production activities and thus are less concerned to change in the economic policy of a country. The financial firms have more financial assets and have a high immunity against any volatility in economic policies and therefore show different responses towards change in economic policies and governance. Moreover, financial institutions have professional management of assets as they have more professional managerial bodies and therefore are less likely to be affected by any change in the economic situation. Second, the financial institutions invest the money of their account holders and other stockholders and therefore they are more sensitive to managing the investment, and therefore their financial assets are less affected by economic uncertainty. The magnitude of harmful effects of economic uncertainty on the financial sector and the non-financial sector is always different, therefore we exclude the financial sector enterprises from the sample to make the analysis more results-oriented (Agomor et al., Citation2022). Owing to these, we limit our sample to non-financial sector enterprises. To forget the problem of an outlier, we set the limits from both ends and deleted the values by winsorizing at a 5% level. For a company to be in our sample, it should have financial information for five subsequent years for any respective variable. Corporate firms that do not meet such criteria were excluded from the final sample.

3.2. Econometric models and variables specification

The general form of the equation for the GMM model is as

The general form of the equation for the EGLS model is as

In equations (1a) and (1b), Yijt is a vector of the dependent variable, Xijt is a vector of the independent variable, Zijt is a vector of firm-specific control variables and Wijt is a vector of country-specific control variables. The relationship between variables can be expressed in the form of the following econometric equations:

The above econometric equation 1 portrays the liaison between INV (industrial investment) and EPU and INV was calculated by dividing the expenditure regarding fixed assets by total assets by perusing the study of Farooq et al. (Citation2021). The EPU was built by pursuing the indices that were developed by (Baker et al., Citation2016). They have specified the policy uncertainty based upon three factors, i.e., newspaper-based uncertainty, expiration of tax reserves against federal tax in the coming year, and deviation of economic forecasts. They give monthly index measurements while in this study we consider the annual EPU index, aggregating the monthly index over 12 months. We get the average index of 12 months. As the other data are in annual form, therefore, we get the average by adding the 12-month values and dividing it by 12. A short description of these variables and other control variables has also been provided in Table . In equation (1), is a vector of firm-specific control variables including ROA, LVG, and FS, while

is a vector of country-specific control variables (IFR, IR, GDP). Similarly, equation (2) presents the econometric relationship between CGI (aggregate country governance index) and INV. It also consists of other indices of governance including VA (voice and accountability), GE (governance effectiveness), PS (political stability), RQ (regulatory quality), RL (rule of law), and CC (corruption control). The performance score of a specific country on these variables was collected from the website of the World Governance Indicators project by Kaufmann et al. (Citation2011).

Table 2. Definition of variables

Equation (3) exemplifies the moderating effect of CGI (aggregate governance quality) on the relationship between EPU and INV. This equation deems to identify whether governance can moderate the impact of EPU on investment decisions. Table provides a brief description of these variables. A collection of studies have considered these variables as potential determinants of corporate investment decisions (Adelino et al., Citation2017; Du et al., Citation2018; Farooq et al., Citation2021). In these equations, subscript i is for a firm, j is for the country, and t is for the time where vector μ_i and δ_t exemplify the time and cross-section fixed effect. The symbol of ε_ijt displays the error term.

3.3. Discussion of methodology

This research unveils the role of country-level governance in moderating the liaison between EPU and corporate investment decisions. To test this relation, we gradually follow the different econometric techniques. We start our statistical analysis with a fundamental panel data estimation technique named the panel fixed effect model. However, statistical outputs (shown in Table ) of some diagnostic techniques including the heteroscedasticity test and cross-section dependency test suggest the inconsistency of the panel fixed-effect model. The significant p-value of the likelihood ratio suggesting the rejection of the null hypothesis, i.e., a variance of residuals is homoscedastic. We have also run the Breusch-Pagan LM test (Breusch & Pagan, Citation1980), and Pesaran LM test (Pesaran, Citation2004) to check the cross-section dependency (CD). The significant p-values of the CD test confirm the existence of CD issue which motive to employ the EGLS model. Thus, to account for the problem of heteroscedasticity, we employ the Panel EGLS (estimated generalized least square) test for regression analysis. The EGLS model can eradicate the problem of CD and heteroscedasticity. Furthermore, as the econometric equations carry a set of macroeconomic variables, the probability of a stationarity problem is high. Therefore, we execute unit testing to diagnose the possible problem of stationarity. The probability value of the ADF-test assumes the acceptance of the alternative hypothesis, i.e., data are stationary at normal (Im et al., Citation2003).

Table 3. Detail of diagnostic tests

Extending our analysis, we have employed another diagnostic test named the Wald test to detect the problem of endogeneity. It can be argued that the possible problem of endogeneity exists as econometric equations carry both firm-specific and macroeconomic variables (Killins, Citation2020). In such a type of analysis, the error term is typically endogenous with explanatory variables and thus causes the problem of endogeneity. As expected, the significant p-value of restriction terms in the Wald test specified the acceptance of the alternative hypothesis, i.e., the error term is correlated with explanatory variables. The statistical summary of all these diagnostic tests has been presented in Table .

To alleviate the concerned problems, we employ EGLS (to treat the heteroscedasticity issue) and two-step system GMM models (primary estimation technique for endogeneity) for robustness. The GMM approach was first introduced by Arellano and Bond (Citation1991) and later developed by Arellano and Bover (Citation1995). By using the lag of explanatory variables as instruments, the GMM model eliminates the chances of correlation between residual terms and explanatory variables and thus eradicates the endogeneity issue. This technique is practiced by Chen et al. (Citation2019), Doan et al. (Citation2020) and Farooq et al. (Citation2021).

4. Results

Table elucidates that the average investment rate in under analysis countries is 0.356. Corporate firms invest 35.6% of their total assets in acquiring PPE. The average EPU index is 129.31 which shows the level of uncertainty in these countries. Table also exemplifies the average scores of governance indices and mean trends of several firm-specific and macroeconomic control variables.

Table 4. Descriptive statistics

In Table , we have presented the current research correlation analysis. The respective correlation coefficients indicate the degree of association between two variables. As column 2 of Table specifies, EPU and governance have negative correlation trends toward investment decisions of corporate firms. The negative correlation trend of governance is consistent across all the proxies of governance. Similarly, ROA and FS have a negative while LVG has a positive association with INV. At the macro level, all control variables including IFR, IR, and GDP carry positive correlation coefficients. However, the high correlation coefficients among proxies of governance are restricted to the addition of all the proxies in the main regression analysis as shown in . The inclusion of all proxies of governance may give spurious regression estimation; therefore, we only consider CGI (aggregate governance index) in interaction with EPU to check the moderating impact of these variables on INV.

Table 5. Correlation analysis

To test the first hypothesis (H1), we estimate the effect of EPU on investment by controlling both firm-specific and macroeconomic control. For regression analysis, we first apply the panel EGLS and check the robustness by employing the two-step system GMM models. Table shows the statistical outcomes of these models. As the results show, EPU has an inverse and significant coefficient value of −0.056 which implies the significant but adverse impact of EPU on investment. This negative effect is consistent and becomes stronger after incorporating the endogeneity error (the coefficient value in model 2 is −0.151 which is greater than in model 1). At the firm level, ROA has a negative while LVG and FS have positive and significant coefficient values. Their coefficient values are −0.017, 0.382, and 0.010 relatively. All the values are significant at the 1% level. Meanwhile, the implication of the GMM model results in stronger coefficient values for ROA and LVG while an insignificant coefficient value of FS. At the macro level, IFR and IR have negative while GDP has a positive and significant coefficient value. In addition to the main regression results, it can be seen at bottom of Table that the value of the adjusted R-square improves after addressing the endogeneity issue. The insignificant value of J-statics illustrates the acceptance of the null hypothesis, i.e., instruments are valid.

Table 6. EPU and corporate investment decisions

Table mainly explains the regression analysis for country governance and corporate investment decisions. As the coefficient values show, CGI (aggregate governance index) positively and significantly impinges upon corporate investment decisions. However, some indices (VA, GE, RQ, and RL have negative coefficient values) of country governance influence the investment decisions negatively and significantly, while the others (PS and CC carry significant and positive coefficient values) show positive cohesiveness with INV. The influence of control variables on corporate investment decisions is similar as mentioned in Table .

Table 7. Governance and corporate investment decisions

Table reports the main regression results, i.e., how governance affects the effect of EPU on corporate investment decisions. First, the statistical outcomes of EGLS regarding the interaction term (EPU*CGI) suggest a significant but negative association with INV. However, after curbing the error of endogeneity via the implication of the two-step system GMM model, this negative effect converts into a positive impact. The positive coefficient value of EPU*CGI further suggests the acceptance of the second alternative hypothesis (H2) and implies that we can mitigate the adverse effects of EPU by focusing on governance quality.

5. Results’ discussion

This research aims to identify the moderating intervention of country-level governance between EPU and decisions regarding investment. To pursue the core aim of current research, we employ EGLS and two-step system GMM approaches to estimate the coefficients. The empirical analysis is segregated into three parts: EPU impact on INV (corporate investment decisions), governance impact on INV, and combine the impact of EPU and CGI on INV. According to Table statistics, EPU has an adverse impact on corporate investment decisions. During high EPU, the cost of capital investment increases due to greater information asymmetric problems. EPU further diminishes the returns from capital investment due to lower sale volume which further leads to low capital reserve and hence fewer funds for any future investment (Chen et al., Citation2019). EPU leads an uncertain economic environment that limits managerial courageous behavior while making any type of physical investment. This negative impact of EPU on decisions regarding corporate investment is like the findings of extant literature (Jackson & Orr, Citation2019; Wang et al., Citation2014; J. Wu et al., Citation2020).

Secondly, CGI influences corporate investment decisions positively. A country having better governance conditions can facilitate its industrial sector through vast opportunities for new investments. A better governance situation has positive spillover impacts on investment and is an indication of government efficiency regarding overall governance matters which led to boosting the industrial confidence for new investments (Ernstberger & Grüning, Citation2013). No specific study was found that directly disclosed such a relationship. However, an empirical analysis arranged by Lee et al. (Citation2020) suggested the positive association of governance situations with innovation activities. In addition to aggregate governance, we can also see the dynamic impact of other governance indices on INV in Table . Referring to empirical results, it can see that some indices of governance, i.e., VA (voice and accountability), GE (governance effectiveness), RQ (regulatory quality), and RL (rule of law) adversely impact corporate investment. Contrary to expectations, the negative influence of such indices can be understood through the assumption of the negative influence of government rigidness regarding law implication on industrial investment (Zhang et al., Citation2017). Such behavior of the government can hamper the growth of the industrial sector as it limits the freedom to some extent. Industrial sectors need some relaxation regarding rules implications in the pre-maturation period.

However, PS (political stability) and CC (corruption control) positively influence investment in the industrial sector. A fresh work arranged by Dai and Zhang (Citation2019) indicated that corporate firms hold the most cash during unstable political conditions due to precautionary motives. Holding more cash alternatively reduces the investment as more funds are limited to hand (Shiau et al., Citation2018). Another empirical analysis conducted by Thakur and Kannadhasan (Citation2019) concluded the positive influence of corruption on cash holdings which led to the effect.

Table gives the knowledge when we check the moderating impact of country-level governance on the relation between EPU and corporate investment decisions. According to Table statistics, the interaction term (EPU*CGI) has a significant but negative coefficient sign (in the model 1 case). However, this negative sign is not consistent and converts to a positive coefficient sign when we address the problem of endogeneity through the implication of model 2. The significant and positive coefficient sign implies that corporate firms located in a country having good governance situations are less affected by EPU (Escribá & Murgui, Citation2009). It appears from the analysis that country-level governance impedes the adverse impacts of EPU by ensuring institutional efficiency and confronting the manipulation practices of investor’s rights (Du et al., Citation2018). Better governance quality and law implication have positive spillover impacts on ensuring policy stability (Doan et al., Citation2020) which further encourages corporate managers for investing. More specifically, the impact of governance on EPU can be segregated across news-based uncertainty, provisional variation in federal tax collection, and mismatching of economic forecasts from actually happening. Focusing on exercising better governance situations can overcome the multiple uncertainties regarding economic situations which further achieve positive investment growth. A better country governance situation defers the negative impact of economic uncertainty by mitigating the information asymmetric issues, ensuring investors’ rights, and making business operations more transparent. Therefore, the firms are less affected by economic volatility in the presence of good governance (Chen et al., Citation2019).

Table 8. Economic policy uncertainty, corporate investment, and governance quality

Prolonging the debate on the dynamic impacts of control variables and following the statistics of model 2, ROA (profitability) has a negative while FS (firm size) and LVG (leverage) have positive and significant effects on investment. Farooq et al. (Citation2021) argued that highly profitable corporations are less interested to invest in such projects having a long payback period. However, larger firms disseminate more funds in capital projects due to voluminous demand for their products which further require more PPE proliferation. Similarly, the availability of bank loans or leverage provides a flexible financial environment to the industrial sector for investment in new ventures, and such statements are advocated by Nguyen and Dong (Citation2013) and Akron et al. (Citation2020). At the macroeconomic level, the negative influence of IFR (inflation rate) and IR interest (rate) can be comprehended through the conjecture of value depreciation and opportunity cost relatively. During IFR, the current value of any future investment, particularly fixed assets continues to be depreciated (AChu & Lai, Citation2013). Correspondingly, high IR creates an opportunity cost and corporate managers make a trade-off between investment in government securities giving high return and physical investment. Thus, they are more likely to invest in securities instead of physical projects (Vithessonthi et al., Citation2017). The positive association between GDP growth rate and investment may be disclosed through a prosperous economic situation, causing high demand for industrial products and thus more investment in PPE (Xie et al., Citation2019).

Summarizing the above discussion, it can be interpreted that EPU dampens corporate investment decisions, but it can be amplified by focusing on governance conditions. The analysis shows the declining trend in the magnitude of EPU’s adverse impact when a country focuses on governance quality. This change also implies that governance is an important channel through which a country can impede the adverse impacts of EPU on industrial sector investment.

6. Conclusion

The policy uncertainty has an apparent influence on corporate-level decisions as this sector is a key stakeholder in any fluctuation in economic policies. The prevailing uncertain economic situation discourages the investment behavior of entrepreneurs due to the high risk of investment failure. In contrast, a better governance situation of a country can defer the adverse impacts of EPU as it ensures investor rights and reduces the issue of information asymmetric. Owing to this, the current study prescribes the role of country-level governance in mitigating the adverse impacts of economic policy uncertainty (EPU) on decisions regarding corporate investment. We employ GLS and a two-step system GMM approach to run the regression due to endogeneity. The statistics suggest that EPU has an inverse impact on decisions regarding industrial investment. But such an inverse impact between EPU and investment is moderated by governance. For corporate investment decisions, the adverse impacts of EPU can be minimalized by employing better governance situations. This moderating effect of country-level governance was found to be reliable even after curbing the error of endogeneity. A country suffering from negative industrial investment can uplift its industrial sector by focusing on governance situations. Better governance can reduce the problem of information asymmetric, ensure the protection of investor rights, and legitimize the economic certainty that further achieve positive investment growth. The empirical analysis further advocates the dynamic role of other control variables in corporate investment decisions. All alternative hypotheses were accepted, and the objective of the study was fulfilled by playing the dynamic role of EPU in investment decisions. However, the relevance of the findings to corporate investors enables them to make informed decisions before investing in a new country since they cannot individually (whether individual or firm) improve the quality of institutions in a country. This is a limitation of the study. Future studies may find solutions over which the corporate investor has control over.

The current empirical analysis provides the following policy implications. Policymakers should maintain the transparency, stability, and continuity of economic policies because an uncertain economic situation hampers the investment of the industrial sector which is a key sector of an economy. As the statistics imply, the creation of a better governance situation can achieve the declining trends in adverse impacts of EPU. Thus, policy officials should maximize the governance quality to defer the negative impacts of uncertain economic conditions on the industrial sector. Corporate managers should composite such policies that can enhance the immunization of enterprises against EPU.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Umar Farooq

Umar Farooq is a PhD (applied economics) scholar at the school of Economics and Finance, Xian Jiaotong University, China. He has a strong research interest in the areas of corporate finance and investment, green finance, sustainable development, and macroeconomic theory and practice. He has recently published papers in peer-reviewed journals including the Borsa Istanbul Review, Research in International Business and Finance, Journal of Cleaner Production, International Journal of Finance and Economics, Energy Policy, Energy, Bulletin of Economic Research, International Review of Administrative Sciences, Environmental Science and Pollution Research, Global Business Review, and Cogent Business and Management. He has also won the title of “distinguished researcher” for the year 2020–2021 as his research appeared in 10 SSCI, and Scopus indexed journals. He is also working as an active reviewer in several peer-reviewed journals including Energy Policy, Energy Economics, International Journal of Finance and Economics, and Environment, Development, and Sustainability.

E-mail: [email protected]

Google Scholar: https://scholar.google.com/citations?user=fe3IZCIAAAAJ&hl=en&oi=ao

ORCID: https://orcid.org/0000-0002-5772-5243

Scopus Author ID: 57,195,806,567

Notes

1. Data that support the findings of current study are available at WDI, The World Bank, WGI, and Thomson Reuters Data Stream. These sites are publicly accessible on monetary subscription.

References

- Abel, A. B. (1983). Optimal investment under uncertainty. The American Economic Review, 73(1), 228–20. https://www.jstor.org/stable/1803942

- Abel, A. B., & Blanchard, O. J., 1986. Investment and sales: Some empirical evidence. NBER Working Paper 2050. University of Pennsylvania.

- Adelino, M., Ma, S., & Robinson, D. (2017). Firm age, investment opportunities, and job creation. The Journal of Finance, 72(3), 999–1038. https://doi.org/10.1111/jofi.12495

- Adjei, F. A., & Adjei, M. (2017). Economic policy uncertainty, market returns, and expected return predictability. Journal of Financial Economic Policy, 9(3), 242–259. https://doi.org/10.1108/JFEP-11-2016-0074

- Agomor, P. E., Onumah, J. M., & Duho, K. C. T. (2022). Intellectual capital, profitability, and market value of financial and non-financial services firms listed in Ghana. International Journal of Learning and Intellectual Capital, 19(4), 312–335. https://doi.org/10.1504/IJLIC.2022.123841

- Akron, S., Demir, E., Díez-Esteban, J. E. M., & García-Gomez, C. D. (2020). Economic policy uncertainty and corporate investment: evidence from the U.S. Hospitality industry. Tourism Management, 77(April), 1–10. https://doi.org/10.1016/j.tourman.2019.104019

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Azhar, A. B., Abbas, N., Waheed, A., & Malik, Q. A. (2019). The impact of ownership structure and corporate governance on investment efficiency: An empirical study from Pakistan Stock Exchange (PSX). Pakistan Administrative Review, 3(2), 84–98. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-63378-8

- Bah, M., & Kpognon, K. (2021). Public investment and economic growth in ECOWAS countries: Does governance matter? African Journal of Science, Technology, Innovation and Development, 13(6), 713–726. https://doi.org/10.1080/20421338.2020.1796051

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

- Breusch, T., & Pagan, A. (1980). The LaGrange multiplier test and its applications to model specification in econometrics. The Review of Economic Studies, 47(1), 239–253. https://doi.org/10.2307/2297111

- Caballero, R. J. (1991). On the Sign of the investment—uncertainty relationship. American Economic Review, 81(1), 279–288. https://www.jstor.org/stable/2006800

- Caixe, D. F. (2022). Corporate governance and investment sensitivity to policy uncertainty in Brazil. Emerging Markets Review, 51, 100883. https://doi.org/10.1016/j.ememar.2021.100883

- Chen, P. F., Lee, C. C., & Zeng, J. H. (2019). Economic policy uncertainty and firm investment: Evidence from the U.S. Market. Journal of Applied Economics, 51(31), 3423–3435. https://doi.org/10.1080/00036846.2019.1581909

- Chu, J., & Fang, J. (2021). Economic policy uncertainty and firms’ labor investment decision. China Finance Review International, 11(1), 73–91. https://doi.org/10.1108/CFRI-02-2020-0013

- Chu, A. C., & Lai, C. C. (2013). Money and the welfare cost of inflation in an R&D growth model. Journal of Money, Credit and Banking, 45(1), 233–249. https://doi.org/10.1111/j.1538-4616.2012.00568.x

- Cohen, J., Webb, L. H., & Khalil, S. (2017). A further examination of the impact of corporate social responsibility and governance on investment decisions. Journal of Business Ethics, 146(1), 203–218. https://doi.org/10.1007/s10551-015-2933-5

- Cui, X., Wang, C., Liao, J., Fang, Z., & Cheng, F. (2021). Economic policy uncertainty exposure and corporate innovation investment: Evidence from China. Pacific-Basin Finance Journal, 67, 101533. https://doi.org/10.1016/j.pacfin.2021.101533

- Cui, X., Yao, S., Fang, Z., & Wang, H. (2021a). Economic policy uncertainty exposure and earnings management: Evidence from China. Accounting and Finance, 61(3), 3937–3976. https://doi.org/10.1111/acfi.12722

- Dai, L., & Zhang, B. (2019). Political uncertainty and finance: A survey. Asia-Pacific Journal of Financial Studies, 48(3), 307–333. https://doi.org/10.1111/ajfs.12257

- Darsono, S. N. A. C., Wong, W.-K., Nguyen, T. T. H., & Wardani, D. T. K. (2022). The economic policy uncertainty and its effect on sustainable investment: A panel ARDL approach. Journal of Risk and Financial Management, 15(6), 254. https://doi.org/10.3390/jrfm15060254

- Demir, E., & Ersan, O. (2017). Economic policy uncertainty and cash holdings: Evidence from BRIC countries. Emerging Markets Review, 33(December), 189–200. https://doi.org/10.1016/j.ememar.2017.08.001

- Doan, A. T., Phan, T., & Lin, K. L. (2020). Governance quality, bank price synchronicity, and political uncertainty. International Review of Economics and Finance, 69(September), 231–262. https://doi.org/10.1016/j.iref.2020.05.002

- Driss, H., Drobetz, W., Ghoul, S. E., & Guedhami, O. (2021). Institutional investment horizons, corporate governance, and credit ratings: International evidence. Journal of Corporate Finance, 67(April), 101874. https://doi.org/10.1016/j.jcorpfin.2020.101874

- Duchin, R., Ozbas, O., & Sensoy, B. A. (2010). Costly external finance, corporate investment, and the subprime mortgage credit crisis. Journal of Financial Economics, 97(3), 418–435. https://doi.org/10.1016/j.jfineco.2009.12.008

- Du, J., Li, W., Lin, B., & Wang, Y. (2018). Government integrity and corporate investment efficiency. China Journal of Accounting Research, 11(3), 213–232. https://doi.org/10.1016/j.cjar.2017.03.002

- Ernstberger, J., & Grüning, M. (2013). How do firm- and country-level governance mechanisms affect firms’ disclosure? Journal of Accounting and Public Policy, 32(3), 50–67. https://doi.org/10.1016/j.jaccpubpol.2013.02.003

- Escribá, F. J., & Murgui, M. J. (2009). Government policy and industrial investment determinants in Spanish regions. Regional Science and Urban Economics, 39(4), 479–488. https://doi.org/10.1016/j.regsciurbeco.2009.02.005

- Essen, M. V., Engelen, P. J., & Carney, M. (2013). Does “good” corporate governance help in a crisis? The impact of country- and firm-level governance mechanisms in the European financial crisis. Corporate Governance: An International Review, 21(3), 201–224. https://doi.org/10.1111/corg.12010

- Farooq, U., Ahmed, J., & Khan, S. (2021). Do the macroeconomic factors influence the firm’s investment decisions? A generalized method of moments (GMM) approach. International Journal of Finance and Economics, 26(1), 790–801. https://doi.org/10.1002/ijfe.1820

- Feng, X., Lo, Y. L., & Chan, K. C. (2019). Impact of economic policy uncertainty on cash holdings: Firm-level evidence from an emerging market. Asia-Pacific Journal of Accounting & Economics, 1–23. https://doi.org/10.1080/16081625.2019.1694954

- Guariglia, A., Liu, X., & Song, L. (2011). Internal finance and growth: Microeconometric evidence on Chinese firms. Journal of Development Economics, 96(1), 79–94. https://doi.org/10.1016/j.jdeveco.2010.07.003

- Hartman, R. (1972). Effects of price and cost uncertainty on investment. Journal of Economic Theory, 5(2), 258–266. https://doi.org/10.1016/0022-0531(72)90105-6

- He, F., Ma, Y., & Zhang, X. (2020). How does economic policy uncertainty affect corporate innovation?–Evidence from China-listed companies. International Review of Economics & Finance, 67(May), 225–239. https://doi.org/10.1016/j.iref.2020.01.006

- Huang, W., Jiang, F., Liu, Z., & Zhang, M. (2011). Agency cost, top executives’ overconfidence, and investment-cash flow sensitivity: Evidence from listed companies in China. Pacific-Basin Finance Journal, 19(3), 261–277. https://doi.org/10.1016/j.pacfin.2010.12.001

- Iheonu, Iheonu, C. O., & Okechukwu, C. (2019). Governance and Domestic Investment in Africa. Journal of Government and Economics, 8(1), 63–80. https://doi.org/10.17979/ejge.2019.8.1.4565

- Ilyas, M., Khan, A., Nadeem, M., & Suleman, M. T. (2021). Economic policy uncertainty, oil price shocks, and corporate investment: Evidence from the oil industry. Energy Economics, 97, 105193. https://doi.org/10.1016/j.eneco.2021.105193

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Iqbal, U., Gan, C., & Nadeem, M. (2020). Economic policy uncertainty and firm performance. Applied Economics Letters, 27(10), 765–770. https://doi.org/10.1080/13504851.2019.1645272

- Istiak, K., & Serletis, A. (2018). Economic policy uncertainty and real output: Evidence from the G7 countries. Applied Economics, 50(39), 4222–4233. https://doi.org/10.1080/00036846.2018.1441520

- Jackson, C., & Orr, A. (2019). Investment decision-making under economic policy uncertainty. Journal of Property Research, 36(2), 153–185. https://doi.org/10.1080/09599916.2019.1590454

- Kaufmann, D., Kraay, A., & Mastruzzi, M. (2011). The worldwide governance indicators: Methodology and analytical issues. Hague Journal on the Rule of Law, 3(2), 220–246. https://doi.org/10.1017/S1876404511200046

- Killins, R. N. (2020). Firm-specific, industry-specific and macroeconomic factors of life insurers’ profitability: Evidence from Canada. The North American Journal of Economics and Finance, 51, 1–16. https://doi.org/10.1016/j.najef.2019.101068

- Knight, F. H. (1921). Risk, Uncertainty, and Profit. Houghton Mifflin Company.

- Lee, C. C., Lee, C. C., & Xiao, S. (2021). Policy-related risk and corporate financing behavior: Evidence from China’s listed companies. Economic Modelling, 94(January), 539–547. https://doi.org/10.1016/j.econmod.2020.01.022

- Lee, C. C., Wang, C. W., & Ho, S. J. (2020). Country governance, corruption, and the likelihood of firms’ innovation. Economic Modelling, 92(November), 326–338. https://doi.org/10.1016/j.econmod.2020.01.013

- Liu, G., & Zhang, C. (2020). Economic policy uncertainty and firms’ investment and financing decisions in China. China Economic Review, 63, 101279. https://doi.org/10.1016/j.chieco.2019.02.007

- Nguyen, P. D., & Dong, P. T. A. (2013). Determinants of corporate investment decisions: The case of Vietnam. Journal of Economics and Development, 15(1), 32–48. https://doi.org/10.33301/2013.15.01.02

- Ogbonna, O. E., Ogbuabor, J. E., Manasseh, C. O., & Ekeocha, D. O. (2022). Global uncertainty, economic governance institutions, and foreign direct investment inflow in Africa. Economic Change and Restructuring, 55(4), 2111–2136. https://doi.org/10.1007/s10644-021-09378-w

- Omoteso, K., & Mobolaji, H. I. (2014). Corruption, governance and economic growth in Sub-Saharan Africa: A need for the prioritisation of reform policies. Social Responsibility Journal, 10(2), 316–330. https://doi.org/10.1108/SRJ-06-2012-0067

- Omri, A. (2020). Formal versus informal entrepreneurship in emerging economies: The roles of governance and the financial sector. Journal of Business Research, 108(January), 277–290. https://doi.org/10.1016/j.jbusres.2019.11.027

- Passos, N., & Modenesi, A. D. M. (2021). Do public banks reduce monetary policy power? Evidence from Brazil based on state dependent local projections (2000–2018). International Review of Applied Economics, 35(3–4), 502–519. https://doi.org/10.1080/02692171.2020.1837745

- Pesaran, M. H., 2004. General diagnostic tests for cross section dependence in panels. CESifo working paper series 1229. Munich.

- Shiau, H. L., Chang, Y. H., & Yang, Y. J. (2018). The cash holdings and corporate investment surrounding financial crisis: The cases of China and Taiwan. The Chinese Economy, 51(2), 175–207. https://doi.org/10.1080/10971475.2018.1447833

- Thakur, B. P. S., & Kannadhasan, M. (2019). Corruption and cash holdings: Evidence from emerging market economies. Emerging Markets Review, 38, 1–17. https://doi.org/10.1016/j.ememar.2018.11.008

- Vithessonthi, C., Schwaninger, M., & Müller, M. O. (2017). Monetary policy, bank lending, and corporate investment. International Review of Financial Analysis, 50, 129–142. https://doi.org/10.1016/j.irfa.2017.02.007

- Wang, Y., Chen, C. R., & Huang, Y. S. (2014). Economic policy uncertainty and corporate investment: evidence from China. Pacific-Basin Finance Journal, 26(January), 227–243. https://doi.org/10.1016/j.pacfin.2013.12.008

- Wu, J., Zhang, J., Zhang, S., & Zou, L. (2020). The economic policy uncertainty and firm investment in Australia. Applied Economics, 52(31), 3354–3378. https://doi.org/10.1080/00036846.2019.1710454

- Xie, F. (2009). Managerial flexibility, uncertainty, and corporate investment: The real options effect. International Review of Economics & Finance, 18(4), 643–655. https://doi.org/10.1016/j.iref.2008.11.001

- Xie, G., Chen, J., Hao, Y., & Lu, J. (2019). Economic policy uncertainty and corporate investment behavior: Evidence from China’s five-year plan cycles. Emerging Markets Finance and Trade, 1–18. https://doi.org/10.1080/1540496X.2019.1673160

- Xu, Z. (2020). Economic policy uncertainty, cost of capital, and corporate innovation. Journal of Banking & Finance, 111, 105698. https://doi.org/10.1016/j.jbankfin.2019.105698

- Zhang, B. (2019). Economic policy uncertainty and investor sentiment: Linear and nonlinear causality analysis. Applied Economics Letters, 26(15), 1264–1268. https://doi.org/10.1080/13504851.2018.1545073

- Zhang, Y., Zhang, M., Liu, Y., & Nie, R. (2017). Enterprise investment, local government intervention, and coal overcapacity: The case of China. Energy Policy, 101, 162–169. https://doi.org/10.1016/j.enpol.2016.11.036