?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Using unit-level data on the entire population of registered manufacturing SMEs in 2007 for India, we explore the impact of religiosity on their access to finance. The findings indicate that certain categories of religion, such as Hindus and Sikhs, are less likely to have access to institutional credit, after accounting for other relevant factors. The disaggregated analysis suggests that these results differ across key characteristics such as SME ownership and gender and caste. In addition, the results also show SMEs for the aforesaid religious categories are less likely to use institutional credit. Therefore, our findings underscore the role and relevance of religion in influencing SMEs access to credit for a large emerging economy whose religious demography differs significantly from Western democracies.

Keywords:

1. Introduction

Small and Medium Enterprises (SMEs) have played a significant role worldwide in fostering the economic development of countries. It is often considered the nursery of entrepreneurship, driven by creativity and innovation, with a significant contribution to the country’s GDP, manufacturing output, exports and employment (Ayyagari et al., Citation2007; Gherghina et al., Citation2020; Madison et al., Citation2022). During 2007–12, SMEs accounted for 98% of all enterprises and 66% of the national labor force in Asia on average and 50% of these economies’ GDP (Yoshino & Taghizadeh-Hesary, Citation2018). Evidence in advanced economies such as the UK and US also suggests that small businesses contribute well over 40% of the GDP in these economies.

In accordance with these trends, the growth of the SME sector in India has been quite phenomenal. In 2008, the sector contributed a third of the country’s GDP, rising to nearly 40% in 2013. As per the Fourth Census of SMEs conducted by the Indian government for 2006–07, the sector accounted for about 45% of the value of manufacturing output and around 40% of the country’s exports. Furthermore, it employed over 110 million people in 2014 spread across 50 million enterprises as compared with 84 million employment in 38 million enterprises in 2008 (Government of India, Citation2016).

Researchers have often cited a key challenge for SMEs is their access to credit. Indeed, the literature is near-consensual on the view that finance is a key constraint for SME (Carpenter & Petersen, Citation2002; Cowling, Citation2010; De la Torre et al., Citation2010). In leading advanced economies, loans to SMEs have been witnessing a secular decline. In emerging economies, the twin challenges of “too-big-for-microfinance” and “too-risky-for banks” have meant that a whole host of SMEs—the “missing middle”—has been severely constrained for credit.

A growing body of evidence has examined various facets of SME behaviour, such as their capital structure (Huang et al., Citation2016), operational challenges (Ayyagari et al., Citation2008) or for that matter, R&D investment (Brancati, Citation2014). In the Indian context, studies have analysed determinants of SME start-up size (Audretsch & Tamvada, Citation2008), caste and gender disparities (Athaide & Pradhan, Citation2020; Chaudhuri et al., Citation2020; Deshpande & Sharma, Citation2013; Rajesh & Sasidharan, Citation2018) and investment decisions (Rajesh & Sen, Citation2015).

Notwithstanding these advancements, one aspect that has largely bypassed researchers’ attention is the impact of religion on access to credit for SMEs. Thus, if lenders—especially banks—become reluctant to finance small firms which are owned by members of a particular religion, it appears likely that credit constraints for such SMEs could become acute. The fact that non-financial factors could be at play is evidenced in recent research. For instance, Duarte et al. (Citation2012) find that borrowers who appear more trustworthy have a higher probability of obtaining loans. In a similar vein, greater disclosure of information on a voluntary basis as part of borrowing requests also improves the probability of access to credit (Michels, Citation2012). Similar evidence is manifest in case of religion as well. Rietveld and van Burg (Citation2014) and Audretsch et al. (Citation2013) document that religiosity plays a key role in driving employment behavior. Matto and Niskanen (Citation2019) observe that the variation in the share of trade credit across European economies can partly be explained by religion. Even with regard to gender, a whole host of studies have documented that women experience discrimination when accessing credit, both regarding credit approval and loan terms (Carbo-Valverde et al., Citation2008; Alesina et al., Citation2013; De Andres et al., Citation2021; Beck et al., Citation2018; Delis et al., Citation2022).

To contribute to this debate, we assess the importance of religion in impacting access to credit for SMEs, using India as a case study. In this regard, using cross-sectional data at the state-industry level for 2007, we address several interrelated issues: first, does religion influence SMEs access to credit? Second, does the amount of credit off-take get impacted by religion? Finally, do state characteristics make a difference in this regard?

In addition to these questions, we examine several associated aspects. First, how does gender interact with religion to influence access to credit? Second, we also address a derivative of Audretsch et al. (Citation2013) finding that certain religious categories are less inclined to engage in self-employment. We augment this line of thinking by exploring whether access to credit has an impact in this regard. Finally, we examine the interaction between caste and religion and its implications for credit access.

Our data consist of close to a million manufacturing SMEs for close to 60 industries at the 3-digit level across 70 districts in 20 states. We measure access to credit for these firms depending on whether they have an institutional loan outstanding and examine its independent effects with the religion of the SME owner. The analysis shows that religion exerts a dampening impact on SMEs credit and this impact differs across religious groups, after controlling for other confounding factors. We disaggregate these findings by size classes, age and gender and find evidence favouring an impact of religion on SME credit.

A comprehensive analysis of this issue in the Indian context is useful for several important reasons. First and more generally, the country is the world’s largest religiously pluralistic and multi-ethnic democracy. Freedom of religion is a fundamental right enshrined under the Indian constitution. Second, there are admittedly few studies focusing on religion in the Indian context (Ghosh, Citation2020; Reserve Bank of India, Citation2015) and very few in the context of emerging markets (Audretsch et al., Citation2013; Kumar et al., Citation2011) and virtually none of them focus on SMEs. Third, the country’s population includes the majority of the world’s Hindus and in addition, also the second largest group of Muslims within a single country, next only to Indonesia (Pew Research Center, Citation2018). The latest decadal Census of religious demography in 2011 released in 2015 shows that although Hinduism dominates, the share of other religions is equally relevant (Government of India, Citation2015). Importantly, the religious demography varies markedly across states. This rich variability in the data within a single country enables us to overcome the differences in institutional, social and economic outcomes that permeate cross-country studies. Finally, previous studies focus on a single (developed) country (Adhikari & Agrawal, Citation2016; Hilary & Hu, Citation2009). In contrast, our analysis focuses on a non-Western setting and, as a result, is able to overcome the culture-specific association between risk and religion that is pertinent for such economies.

The analysis connects several literatures. First, it assesses the interaction between culture and financial outcomes by analysing the impact of religiosity on SMEs. Academic evidence has highlighted the importance of religion for economic performance (Barro & McCleary, Citation2003; Guiso et al., Citation2006; Zingales, Citation2015). More recent evidence has examined the impact of religion on financial (Adhikari & Agrawal, Citation2016; Ghosh, Citation2022a) and non-financial (Hilary & Hu, Citation2009; Huoy & Ali, Citation2017) firms, but does not consider the impact on SMEs. Compared to this, cross-country studies that include religiosity as an independent variable are a country-level measure, limiting its empirical appeal (Kanagaretnam et al., Citation2015). Using cross-country data, Zelekha et al. (Citation2014) also affirm that religious institutions play a key role in driving entrepreneurship behavior of individuals, over and above the impact of national culture (North, Citation1991; Parboteeah et al., Citation2015). Other studies document higher stock market returns in Muslim-dominated Asian economies, coinciding with certain Muslim holy days (Ali et al., Citation2017). Using Indian survey data, Audretsch et al. (Citation2013) report that certain types of religious beliefs promote entrepreneurship. In the case of the USA, Deller et al. (Citation2018) find that small business activity is higher in communities with greater concentration of religious congregation. Umar et al. (Citation2020) affirm that religion is not a binding constraint in the quest towards 80% financial inclusion ambitioned by Nigeria, although certain modifications are needed in the banking system (e.g., introduction of Islamic windows) in order to achieve this goal. Alharbi et al. (Citation2021) highlight that customers who are more knowledgeable about Islamic financial literacy are more likely to achieve business success. Our data have the advantage in the sense that there is a specific question where SME owners have to specify their religion. This enables us to exploit this information without resorting to any inference or interpolation, as is the case with other such studies (Adhikari & Agrawal, Citation2016; Hilary & Hu, Citation2009).

Second, the analysis speaks to the literature that examines the relevance of gender for economic outcomes. One strand of this literature highlights the usefulness of women political empowerment and its implications for financial and non-financial outcomes (Chattopadhyay & Duflo, Citation2004; Clots-Figueras, 2011; Bhalotra et al., Citation2018; Ghosh, Citation2022b Iyer et al., Citation2012). Another line of thinking focuses squarely on the differential impact of finance across gender (Delechat et al., Citation2018; Demirgüç-Kunt et al., Citation2018; Osei-Tutu & Weill, Citation2021; Reddy & Jadhav, Citation2019). In the Indian case, Chaudhuri et al. (Citation2020) focus on the differential response of SMEs across women-owned and women-managed firms and find that the latter exhibit much inferior performance and productivity as compared with the former. Our analysis differs from these studies in the sense that although we focus on similar firm categories as Chaudhuri et al. (Citation2020), our focus is whether the religion of the women-focused (i.e., women-owned or women-managed) SMEs impacts their credit response.

Third, the analysis sheds light on the influence of caste in driving access to finance and, more importantly, its interface with religion. Prior studies in this respect have highlighted the relevance of caste in driving lending behaviour (Banerjee & Munshi, Citation2004) and the challenges they encounter in accessing credit (Rajesh & Sasidharan, Citation2018). Exploiting information from multiple waves of the census of entrepreneurial units, Iyer et al. (Citation2013) report that scheduled castes and tribes owned less than 10% of the 42 million enterprises, well below their share of nearly 17% in the total population. Rani and Elliott (Citation2014) assess the disparities in earnings and education in India and find that backward castes and those belonging to religious minorities have lower returns to education. An aspect that does not appear to have been adequately factored into prior research is how caste interacts with religion, which the analysis seeks to address.

Finally, the analysis resonates with the broader literature that examines the impact of discrimination in credit markets, based on non-economic factors (Bertrand & Mullainathan, Citation2004). For instance, there is evidence in support of employment discrimination against blacks (Bertrand & Mullainathan, Citation2004), obese persons (King et al., Citation2006) and ex-convicts (Pager & Quillian, Citation2005). Drydakis (Citation2010) shows that religious minorities are less likely to be considered for higher-status jobs using data from the Greek labour market. Using survey data, Du and Zeng (Citation2019) report that religious entrepreneurs are able to obtain greater quantum of bank loans as compared to their counterparts and additionally, gender plays an important role in this regard. In the Indian case, studies have highlighted the importance of caste-based discrimination for employment and financing prospects of SMEs (Deshpande & Sharma, Citation2016; Iyer et al., Citation2013; Rajesh & Sasidharan, Citation2018; Thorat, Citation2005). These studies do not examine the association between religion and SME access to finance, which is central to the empirical enquiry of the analysis.

The rest of the analysis continues as follows. In Section II, we provide the theoretical background and derive testable hypotheses. Section III introduces the data and variables, followed by the empirical strategy and results. The final section concludes.

2. Literature and hypothesis

Several theories have been advanced as to how religion can influence entrepreneurship.

The sociological theory proposes that the ultimate goal of any religion is for mankind to strive to become better human beings. As a result, religious adherents are expected to behave in an ethical manner, especially when it comes to undertaking entrepreneurial activities (Baydoun et al., Citation1999). This theory thereby focuses on the social forms of the beliefs but does not adequately address why a particular religious group could be more (or, less) inclined to access credit.

The second view is based on the substantive theory, which suggests that religion is a personal decision and therefore should be segregated from their business interactions (Lewis, Citation2002). A corollary of this view is that religion should be excluded from business affairs.

The third view is based on the social capital theory. According to this theory, social capital—access through social connections—facilitates access to resources and opportunities via social networks and enhances entrepreneurial opportunities (Granovetter, Citation1973). There are two ways in which social capital can promote entrepreneurship. First, through bonding wherein members within a particular network (e.g., family members, close friends) who by virtue of their background and interests help promote business activity. Al-Maliki et al. (Citation2022), for instance, document that both family and non-family SMEs were equally impacted by the Covid-19. Alternately, social capital can develop through bridging (e.g., chamber of commerce, religious beliefs), wherein networking among members can help promote business interests. As a result, this theory does not inform which religious group would be inclined to access finance but emphasises the importance of networking to drive entrepreneurship.

Perhaps the most influential of these is Weber’s (Citation1930) religious theory of entrepreneurship. According to his argument, religious beliefs are a key determinant of entrepreneurial development. In particular, the theory contends that religions such as Hinduism focus more on the present and do not promote materialism. As a result, it is less conducive towards fostering entrepreneurship. Likewise in Islam, the rewards of the afterlife are quite overwhelming, dissuading them from material accumulation and pursuit of entrepreneurial goals. As a result, access to finance might not be a compelling concern for these two religious categories.

This leads us to our first hypothesis:

Hypothesis 1 (H1A): Under the social capital theory, SMEs owned by members of any particular religious group are likely to be inclined towards entrepreneurship and thereby inclined to access finance

H1B: Under the religious theory, SMEs owned by Hindus and Muslims are less likely to be inclined to access finance

Compared to this, Protestant work ethic views entrepreneurship as a moral activity and as a corollary, the pursuit of small business reflecting such behavior (Drakopoulou & Seaman, Citation1998). Using data for Christian countries, Galbraith and Galbraith (Citation2007) find that religiosity positively impacts entrepreneurial activity. Nunziata and Rocco (Citation2014) also affirm a positive impact of religion on entrepreneurship in the European Union. Henley (Citation2017) utilises cross-national data comprising both advanced and emerging economies and uncovers a positive impact of religion on entrepreneurship. Akin to Protestants, Sikhism encourages enterprise and earning an honest living when it comes to self-employment. Over and above, the philosophy of Sikhism does not dissuade the acquisition of property or wealth, but eschews mental attachment to such accumulation. Thus, Sikhism promotes the principles of ethical entrepreneurship. Therefore, access to finance will be an important consideration for these two religious groups. Based on the above discussion, we postulate our second hypothesis:

Hypothesis 2 (H2): Under the religious theory, SMEs owned by Christians and Sikhs are more likely to access finance

An additional complication in the Indian context is the relevance of caste. Unlike other religious groups, the caste system is a strong form of social stratification manifested primarily under Hinduism. Under this system, Hindus are divided into four major hierarchical groups based on their karma (i.e., work) and dharma (i.e., religion). At the top of the hierarchy are the Brahmins mainly involved in intellectual pursuits. This is followed by the Kshatriyas, or the warriors and rulers. Then comes the Vaishyas who are engaged in trade-related activities. The Sudras are at the bottom of the strata and undertake menial jobs. Cotterill et al. (Citation2014) have argued that the caste system is legitimised through the twin actions of karma and dharma, enabling the higher castes to exercise social dominance (Pratto et al., Citation2000; Sidanius & Pratto, Citation1999). Although much less discussed, caste discrimination is also manifest for the other religious categories (Ahmed, Citation1979; Catholic Bishops’ Conference of India, Citation2016; McLeod, Citation1975). Contextually, it may be mentioned that similar (racial) discrimination has also been reported in the US labor market, where resumes with white names received 50% more interview calls than resumes with black names (Bertrand & Mullainathan, Citation2004).

That being the case, the lower caste is often constrained for credit (Thorat & Neuman, Citation2012, Citation2012) from both the demand (e.g., intrinsic reluctance towards entrepreneurship, cautious attitude towards risk) and supply (e.g., treating a loan application from a lower caste as less creditworthy, potential lack of business acumen of applicants to productively utilise the loan) sides, the latter being consistent with the theory of “taste-based discrimination” (Becker, Citation1971). Following from this discussion, we postulate our third hypothesis.

2.1. Hypothesis 3 (H3): Individuals belonging to lower social classes are less likely to be able to access finance This should be in SAME FONT and STYLE as Hypothesis 2 above. Also,REMOVE 2.1

In recognition of these challenges, the government introduced a policy wherein these castes were categorised under three heads: the lower castes (termed, Scheduled Caste or SC), the backward tribes (termed, Scheduled Tribes or ST) and the disadvantaged castes (termed, Other Backward Castes or OBC). The government provided these categories job opportunities through affirmative action (Gupta, Citation2005).

3. Data and variables

We utilise three main data sources for the study: (a) data on SMEs and (b) data on state-level economic and financial variables obtained from the website of the Indian central bank and (c) data on state-wise religious demography of the population for 2011 published by the Indian government in 2015.

SME data: The Office of Development Commissioner of Micro, Small and Medium Enterprises (SME) is entrusted with collecting data pertaining to the SME sector. Till 2020, it has undertaken four censuses of the registered sector. The first three censuses were conducted at various time points during 1973–2001.

Our focus is the Fourth Census conducted in 2008–09 for the reference year 2006–07 on 7.5-lakh registered manufacturing SMEs. Under the Micro, Small and Medium Enterprises Development (MSMED) Act 2006, the manufacturing units are categorised under three size classes: Micro (with investment in plant and machinery up to Rs.2.5 million), Small (with investment in plant and machinery above 2.5 million and up to INR 50 million) and Medium (with investment in plant and machinery in excess of INR 50 million and up to 100 million).Footnote2 The database has been widely employed in prior research, to analyse issues relating to social class (Audretsch et al., Citation2013), gender (Deshpande & Sharma, Citation2013) and caste issues (Rajesh & Sasidharan, Citation2018).

We focus on registered SMEs, which were sampled on a complete enumeration basis and were working at the time of the survey. This provided a total of 978,480 SMEs across 20 states and 70 districts and 58 industries at the 3-digit level. Of the total, 94% are micro-SMEs, 5.6% are small SMEs and the remaining are medium SMEs, an aspect highlighted in previous research (Mazumdar & Sarkar, Citation2008).

The data provide us with a rich cross-section of firm characteristics ranging from size, age, location (i.e., rural versus urban), export status, ownership categorisation by gender and social strata, employment, gross output, use of raw materials and labor as well as whether the SME belongs to a cluster or otherwise. Importantly, the data contain a question regarding the religion of the SME owner and a codification of the possible responses as to whether the owner is a Hindu, Muslim, Sikh, Christian, Jain, Buddhist and others. We club these religious categories under five heads: Hindu, Muslim, Sikh, Christian and Others (comprising Jain, Buddhist and Others) and treat this “Others” as the control category.Footnote3

The key outcome variable of interest is a dummy which equals one if the SME has taken a loan from an institutional source, else zero.

We include several firm-specific controls, including its ownership status, location, whether the unit is women-focused, whether the enterprise belongs to a cluster to account for within-cluster externalities, quality certification and technical know-how, and energy dependence.

We winsorize all firm-specific continuous variables at 1% at both ends to moderate the influence of outliers.

State-specific data: At the state-level, we use three variables. First, we use the natural logarithm of state per capita income to control the level of economic development and the year-on-year change in state income to control the business cycle. We also control for the credit penetration in the state by incorporating the ratio of credit to state income. Information on these variables is obtained from the website of the Indian central bank, as reported in their various annual publications such as Handbook of Statistics on Indian States (Reserve Bank of India, Citation2018) and the Basic Statistical Returns of Banks (Reserve Bank of India, Citation2009).

Finally, since the religious composition varies widely across states, we utilise the 2011 decadal Census of religious demography and construct an index of religious diversity (DIV), akin to Alesina et al. (Citation2003). According to the reported information, roughly 80% of the country’s population were Hindus, followed by Muslims (14.2%), Christians (2.3%), Sikhs (1.7%) and the remaining belonging to other religions such as Buddhists, Jains and Zoroastrians (Government of India, Citation2015).

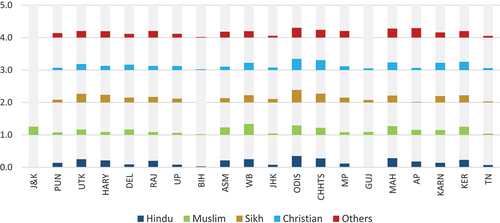

Table shows the variable definitions and summary statistics. On average, 13% of SMEs have taken loans from an institutional source. This figure, however, varies widely across states and by religion. We plot this information in Figure and, relatedly, show the “distance-to-frontier” by subtracting this value from 1 for each state-religion combination.Footnote4 In effect, the taller the length of the bar for each state-religion combination, the greater the likelihood that a particular religious group within a state has availed institutional loan. Viewed from this standpoint, the chart shows that access to finance is the lowest in Bihar and Gujarat and on the higher side in Odisha, Maharashtra and West Bengal. Categorised by religion, access to finance is the highest for Christians with an average of 20% reporting an institutional loan outstanding and the lowest for Sikh with an average of less than 10% reporting an outstanding institutional loan.

Figure 1. Proportion of SMEs with access to finance, by state-religion.

Table 1. Variable definition and summary statistics

In terms of religious ownership, we find that an overwhelming proportion of over 80% of SMEs are owned by Hindus, followed by Muslims (close to 9%) and other religious categories.

The natural logarithm of fixed asset equals 11.9, which is a control for size of the firm. The natural logarithm of age is over 2, so that firms have been in operative for quite some time, on average. Among others, over 40% of firms are located in rural areas, close to 2% have an export orientation and over 80% use traditional sources of power. Of the other two key variables, over 40% of firms are owned by disadvantageous social groups (SC, ST and OBC) and close to 10% (resp., 6%) are women-owned (resp., women-managed).

Table enlists the correlation matrix among the key variables. In our case, the relevant ones of focus are of loan with the religious categories and relatedly, with gender and caste variables. We find that all of these correlations are statistically significant at the 1% level, with the magnitude ranging from 1 to 7%. More specifically, loan displays a negative correlation with Hindu and Sikh and positive correlation with the remaining other religious categories. In other words, Hindus and Sikhs are less likely to obtain loans from institutional sources, whereas Muslims and Christians are more likely to do so. These raw correlations do not consider firm- and state-specific factors. We, therefore, resort to an econometric framework to examine this aspect in detail.

Table 2. Correlation matrix of key variables

4. Empirical methodology

To assess the impact of religion on access to finance for SMEs, while controlling for other relevant factors, for firm i in industry j in district d in state s, we estimate regressions of the following form:

In (1), Loan is a dummy measure if a SME has taken loan from an institutional source, else zero; Z and F are a vector of firm- and state-specific controls as mentioned earlier, λ and µ are industry- and district-fixed effects and ε is idiosyncratic error.

The key independent variable is Religion, which are dummies depending on the religion (i.e., Hindu, Muslim, Sikh and Christian with Others being the control category) of the SME owner. Provided a particular religious category of SME is not inclined to avail loan from an institutional source, β would be negative. Throughout, standard errors are clustered by state. Since the dependent variable is a dummy, we employ a logit model for purposes of estimation.

The empirics proceed as follows. We first estimate the baseline specification, sequentially incorporating the firm-level variables, while ensuring district and industry (3-digit) fixed effects as well as state controls in all regressions. Next, we exploit the cross-sectional variation by state. Subsequently, we explore the relevance of gender and caste.

Finally, we focus on the use of loans. In this case, we employ a Heckman model to address the selection aspect that the use of loan is conditional upon its access. Accordingly, we estimate a two-equation setup comprising the selection equation (first stage) and the outcome equation (second stage). Using same subscripts as EquationEquation (1)(1)

(1) , the two-equation specification takes the following form:

EquationEquation (2A)(2A)

(2A) is a probit model where the dependent variable is a dummy which equals one if the SME is not capital constrained, else zero; the remaining variables are as earlier. In Equationequation (2B)

(2B)

(2B) , the dependent variable is the natural logarithm of the amount of institutional loan outstanding; the remaining variables are defined previously. Both εFootnote1 and ε2 follow standard normal distribution.

The primary coefficient of interest is β2: it identifies whether the use of finance responds to religion. Provided the coefficient is positive and statistically significant, this would suggest that the use of the institutional loan is higher for SMEs owned by a particular religious category.

To identify the two equations, we include an additional variable, the year-on-year growth in output in the outcome equation (i.e., in Z2), which is not present in the selection equation (i.e., in Z1). This exclusion restriction is based on the rationale that greater output would necessitate increased demand for credit, although it does not affect the firm’s access to credit (Rajesh & Sasidharan, Citation2018). In the sample, 99% of SMEs did not report any constraint.

5. Empirical findings

5.1. Religiosity and SMEs access to finance

Table presents the baseline results. Across all columns, we control for state characteristics as well as industry- and district-fixed effects.

Table 3. Baseline regressions ;For the TABLE, the numbers within brackets should come below the coefficient

Column (1) shows that the coefficient on the religion variable is negative and statistically significant in all cases. By way of example, the coefficient on Hindu equals −0.32, so Hindus are 27% less likely to access an institutional loan.Footnote5 Likewise, Muslims are 28% less likely to access an institutional loan. These findings do not support H1A but are aligned with H1B.

Similarly, we find that Christians are 24% less likely to obtain an institutional loan. Perhaps the biggest difference is for Sikhs. The evidence suggests that they are over 50% less likely to access an institutional loan. These findings run contrary to H2.

Across columns, we gradually include the firm-specific controls and continue to find evidence in favor of H1B, although the evidence regarding H2 becomes less compelling.

Our preferred specification is column (12), which controls for the entire set of factors at the firm-level, in addition to state-level controls and fixed effects. Based on the estimates, we compute the Average Marginal Effects (AMEs) for the firm-level coefficients and report them in column (13). The AMEs provide a summary statistic that reflects the full distribution of independent variables. In addition, AMEs have the advantage in that they respect the distribution of the original data and better capture the variability of each covariate on the outcome (Cameron & Trivedi, Citation2010; Williams, Citation2021).

Based on the AMEs, we find that on average, the probability of Hindus accessing institutional loan is 2.5 percentage points lower and likewise, the probability of Sikhs accessing institutional loan is 5.4 percentage points lower.

We briefly discuss the control variables. The coefficient on size is positive and statistically significant, indicating that large firms are 2 percentage points less likely to encounter financing constraints (Beck & Demirgüç-Kunt, Citation2006, Citation2006; Kuntchev et al., Citation2013).

The point estimates on age are negative and suggest that young firms are 3.4 percentage points more likely to access loans from institutional sources. SMEs’ use of external loans in the initial phase of their life cycle concurs with evidence that supports heavy dependence on debt finance for such firms (Robb & Robinson, Citation2012).

In terms of legal form, partnership and private firms are less likely to obtain institutional finance. The negative coefficient on private is consistent with information asymmetry argument, wherein paucity of information on such borrowers impedes banks from providing credit. In the case of Vietnam, for instance, Nguyen et al. (Citation2006) show that the high degree of uncertainty impels banks to adopt a conservative strategy in lending to private SMEs.

Women-owned and women-managed firms have higher access to credit: the probability being double for the former compared with the latter. This contrasts with several studies which highlight the difficulty in obtaining credit for women-owned enterprises (Berger & Udell, Citation2006; Muravyev et al., Citation2009; Presbitero et al., Citation2014) but is consistent with evidence obtaining elsewhere that supports the lack of any gender-based discrimination in credit access (Aterido et al., Citation2013; Wellalage & Locke, Citation2017).

Firms with export orientation have established business models and likely to be certified by an external auditor. As a result, they are better equipped to convey quality and overcome the information asymmetries surrounding their activities. This is reflected in their AME, which shows that their probability of obtaining institutional loans is 4.6 percentage points higher than those without such orientation. Therefore, firms with export orientation are less likely to be constrained in obtaining institutional credit. Using data on West African countries, Quartey et al. (Citation2017) show that exporting SMEs have better access to bank loans.

As expected, higher growth foments greater demand for credit at the state level. In addition, greater religious diversity is also observed to positively impact institutional finance, consistent with evidence proffered by Nikolova and Simroth (Citation2015) who report that greater religious diversity correlates positively with entrepreneurship and credit access.

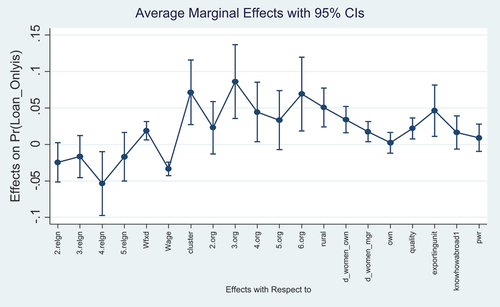

In Figure , we box-plot the AMEs for the firm-specific variables. The dot in the figure represents the magnitude of the marginal effect, whereas the vertical, capped lines represent the upper and the lower bound of a 95% confidence interval.

Figure 2. Average marginal effects.

Collectively, the findings suggest that religion plays an important role in influencing SMEs access to finance, after accounting for other relevant factors.

6. Robustness

6.1. Gender and religion

The interaction of gender and religion is a relatively unaddressed aspect in the literature. Recognising the dual roles that women can play as owner and as manager, akin to Chaudhuri et al. (Citation2020), we undertake the analysis separately for women as owner, as manager and when women perform both roles. The results are presented in Table .

Table 4. Robustness checks—Impact of gender

Across all columns, we find that only the coefficient on Sikh is statistically significant, suggesting that such SMEs are less likely to access institutional finance. The point estimates show that Sikh women are anywhere between 40 and 50% less likely to access institutional credit. These results can partially be explained by the low literacy levels of Sikh women, which compounds the complexities of documentation: field studies report their literacy levels as 38% compared with 50% for the Hindi-speaking states (Planning Commission, Citation2005).

6.2. Ownership and religion

Next, we assess the impact of ownership and caste on access to credit, by religion. In Table , the first five columns focus on SME ownership, whereas the remaining two columns highlight the interaction of caste and religion in influencing SMEs access to credit.

Table 5. Robustness checks—Impact of organization & caste The Figure within brackets in Table should come BELOW the coefficient)

The findings across columns (1)–(5) are fairly unequivocal: Sikhs are less likely to access finance, irrespective of ownership. Among others, under proprietorship, Hindus are less likely to access finance. In our sample, 88% of proprietorship firms are Hindus. Such an arrangement entails lower operating costs and necessitates less complicated governance arrangements. Although this promotes less risky behaviour, it also has the downside that owners have to bear the entire risk in a business failure. As a result, banks could be less inclined to extend loans. The point estimates in column (1) suggest that Hindu proprietorship firms are 25% less likely to access institutional loans.

It is also notable that public firms owned by Muslims are more likely to have access to finance and in a similar vein, Muslim-owned cooperative SMEs are less likely to do so. Public SMEs are better known to external finance providers, who are able to elicit “soft information” on these firms, lowering the need for “hard information” (De la Torre et al., Citation2010). This overwhelms their religious affiliation so much that they can access institutional finance. In addition, cooperative SMEs are less likely to access finance, irrespective of religion. This evidence concurs with the European evidence which suggests that unique structural features of such SMEs combined with strict governance rules make them less attractive to external financiers and, as a result, result in difficulties in accessing capital (Cooperatives Europe, Citation2020).

6.3. Caste and religion

In the Indian context, Audretsch et al. (Citation2013) analyse the interaction between religion and caste for the Hindu sub-sample since the caste system is closely associated with this category. Their findings show that the lower castes are less likely to choose self-employment and more likely to work as casual labour.

Although the caste system has traditionally been part of Hinduism, it is also present in other religions. As early as the 1970s, Mines (Citation1972) observed that the caste organisation in the Muslim community is less rigid than Hindu and more amenable to individual and familial social mobility. Subsequently, Ahmed (Citation1979) provided a clear documentation of this phenomenon. Similar hierarchy has been documented in Sikhism. For instance, Puri (Citation2003) remarks that among the Sikhs, jats who had graduated to the position of the ruling class under Maharaja Ranjit Singh (the first king of the Sikh Empire) remained at the top of the hierarchy, followed by other castes (e.g., khatris, aroras) and then the artisans (e.g., Ahluwalia) and finally, the menial class, akin to the Hindus. The presence of caste-based discrimination among the Catholics in the Indian context has also been highlighted in recent research (Catholic Bishops’ Conference of India, Citation2016). The moot point of making these observations is that any analysis of caste system in India needs to undertake a holistic assessment and not just a particular religious community.

We conduct our analysis for the lower caste across all religious groups and report the findings in Table (columns 6–7). Two prominent findings emanate from these columns. First, whenever significant, the sign of the relevant coefficient across religion is negative, affirming that the lower castes are less likely to access institutional loan. This evidence is consistent with H3. In addition, we find that other (i.e., forward) castes are also less likely to have access to finance. Second, the coefficient on the lower caste is significantly higher (in absolute terms) as compared to that for the other caste, reiterating H3.

We find that the most significant impact is on Sikhs across the caste categories in terms of magnitude. In particular, Sikhs belonging to lower castes are 63% less likely to have access to institutional finance and likewise, those in forward caste are 42% less likely—a difference of 20 percentage points. Thus, while both categories are constrained in terms of access to institutional credit, the impact is much larger in case of lower castes. Thus, lack of access to credit could be one factor that could explain the likelihood of lower social classes to engage in casual labor and less towards self-employment (see, for example, Audretsch et al., Citation2013).

6.4. Amount of loans

Table sets out the results of the Heckman model (columns 1–2). It also reports the AMEs for the estimates relating to the amount of bank loans.

Table 6. Robustness check—Access to and use of loans

The AMEs suggest that all religious categories are less likely to use institutional loans, ranging from 8 to 67 percentage points. For example, the coefficient on Hindu is −0.20, so Hindus are 20 percentage points less likely to use bank loans. As in the case of access to institutional finance, the most significant impact is on Sikhs. Combined with our previous findings, the results indicate that both the access to and use of finance vary widely across religion.

6.5. Impact of state characteristics

Thus far, we have accounted for relevant state characteristics by including them as control variables in the regression. To explore this in detail, we re-estimate the baseline findings while categorising states based on the identified characteristics. Thus, states with per income higher than the in-sample median are classified as high-income states, else it is categorised as being a low-income state. The classification of states in terms of religious diversity and credit penetration is also done similarly. The estimation results are presented in Table .

Table 7. Robustness checks—Relevance of state characteristics The figure in bracket in Table should come BELOW the coefficient

In column (1), the results for high-income states show that Sikhs are more likely to access finance and likewise, the results for low-income states show the findings to be exactly the opposite. Therefore, our hypothesis H2 is relevant only in case of high-income states.

When we look at religious diversity as a state characteristic, column (3) results indicate that Hindus are 15% more likely to access finance in states with high religious diversity and relatedly 25% less likely to access finance in states with low religious diversity. As well, Muslims are 35% less likely and Christians are 58% less likely to access finance in states with low religious diversity.

Finally, in terms of credit penetration, the results show that Sikhs are 43% less likely to access finance, contrary to hypothesis H2.

To sum up, the findings in this section show that it is only in high-income states that Sikhs are likely to access finance, and in most other cases, they are less likely to access finance.

7. Concluding remarks

The importance of religion as a non-economic factor that can drive economic outcomes has been highlighted in recent times. Most of the related evidence is at the country level or large firms, with limited evidence being available with regard to SMEs. Given that SMEs are an important fulcrum of economic growth in several emerging and advanced economies and credit constraints are one of their foremost challenges, it remains a moot issue as to whether religion plays any role in this regard.

To inform this under-addressed line of thinking, we exploit unit-level data on the entire universe of manufacturing SMEs for India to assess the impact of religion on access to credit and relatedly its use. Our key finding is that after controlling for other factors, Hindus and Sikhs are less likely to have access to institutional loans, with the magnitude of the impact being much higher in the case of the latter than the former. These findings differ across key characteristics such as gender, caste and ownership when we categorise states based on several observable features.

The aforesaid analysis provides useful pointers towards avenues for future research. First, as more granular data become available, it would be useful to exploit the longitudinal nature of the data to ascertain how this behavior evolves over time. Second, it would also be useful to exploit changes in the definition of SMEs over time and understand how it influences the interplay of religion and caste. Third, besides the state characteristics already accounted for in the analysis, other state-specific features both economic and non-economic such as their business-friendliness and political orientation are also likely to have a bearing on this issue. Addressing these issues would be valuable additions towards future research.

To conclude, religiosity appears to be an important missing link that exerts a discernible impact on access to finance for SMEs. A US think tank has recently devised a Religious Equity, Diversity and Inclusion (REDI) Index to assess the commitment of Fortune 200 firms (Religious Freedom and Business Foundation, Citation2021). It would perhaps be sooner rather than later that other leading global companies begin integrating this aspect in their corporate culture. From this standpoint, our findings indicate that it is perhaps time that policymakers in India suitably incorporate this aspect in their decision-making process. This can lead to much greater appreciation of the importance of religion, which can help facilitate the flow of institutional loans to SMEs.

Data availability

The data are available in public domain and on the Indian Ministry of Micro, Small and Medium Enterprises website.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Saibal Ghosh

Dr. Saibal Ghosh worked at the Reserve Bank of India, moving up the ranks as Director in the Economic Analysis and Policy Research Department. In his final stint, he was Deputy Research Adviser at the Centre for Advanced Financial Research and Learning, an advanced research institute established by the Reserve Bank of India (RBI). He has over 20 years of experience in banking and financial stability and monetary policy issues. His research has been published in leading international and national journals. He is presently working with the Qatar Central Bank in Doha, Qatar.

Notes

1. Qatar Central Bank, ABJ Street, Doha, Qatar. Mail: [emailsaibal @gmail.com]. The work belongs to a large research project undertaken when the author was working with the Centre for Advanced Financial Research and Learning, Mumbai, India. The views expressed and the approach pursued in the paper reflects the personal opinion of the author.

2. Based on average exchange rates during that year, the equivalent amounts were up to US $55,000 for Micro enterprises, up to US $1.1 million for small enterprises and up to US $2.2 million for medium enterprises.

3. Sadeghloo et al. (Citation2018) report that local entrepreneurs in Iran typically prefer to do business in urban (as opposed to rural) areas in order to ensure higher returns on their investment.

4. The state notations are as follows: Jammu & Kashmir (J&K), Punjab (PUN), Uttarakhand (UTK), Haryana (HARY), Delhi (DEL), Rajasthan (RAJ), Uttar Pradesh (UP), Bihar (BIH), Assam (ASM), West Bengal (WB), Jharkhand (JHK), Odisha (ODIS), Chhattisgarh (CHHTS), Madhya Pradesh (MP), Gujarat (GUJ), Maharashtra (MAH), Andhra Pradesh (AP), Karnataka (KARN), Kerala (KER) and Tamil Nadu (TN).

5. This is calculated as (exp(−0.32)-1)*100. The other calculations are done in a similar manner.

References

- Adhikari, B. K., & Agrawal, A. (2016). Does local religiosity matter for bank risk-taking? Journal of Corporate Finance, 38, 272–23. https://doi.org/10.1016/j.jcorpfin.2016.01.009

- Ahmed, I. (1979). Caste and Social Stratification among Muslims in India (IInd Ed.). Manohar Book Service.

- Alesina, A., Devleeschauwer, A., Easterly, W., Kurlat, S., & Wacziarg, R. (2003). Fractionalisation. Journal of Economic Growth, 8(2), 155–194. https://doi.org/10.1023/A:1024471506938

- Alesina, A., Lotti, F., & Mistrulli, P. (2013). Do women pay more for credit? Evidence from Italy. Journal of the European Economic Association, 11, 45–66. https://doi.org/10.1111/j.1542-4774.2012.01100.x

- Alharbi, R. K., Yahya, S. B., & Kassim, S. (2021). Impact of religiosity and branding on SME performance: Does financial literacy play a role? Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-08-2019-0162

- Ali, I., Akhter, W., Ashraf, N., & Elgammal, M. M. (2017). Impact of Muslim holy days on Asian stock markets: An empirical evidence. Cogent Economics and Finance, 5(1311096), 1311096. https://doi.org/10.1080/23322039.2017.1311096

- Al-Maliki, H. S., Salehi, M., & Kardan, B. (2022). The effect of Covid-19 on risk-taking of small and medium-sized family and non-family firms. Journal of Facilities Management. https://doi.org/10.1108/JFM-09-2021-0105

- Aterido, R., Beck, T., & Iacovone, L. (2013). Access to finance in sub-Saharan Africa: Is there a gender gap? World Development, 47, 102–120. https://doi.org/10.1016/j.worlddev.2013.02.013

- Athaide, M., & Pradhan, H. K. (2020). A model of credit constraints for SMEs in India. Small Business Economics, 55(4), 1159–1177. https://doi.org/10.1007/s11187-019-00167-4

- Audretsch, D. B., Boente, W., & Tamvada, J. P. (2013). Religion, social class, and entrepreneurial choice. Journal of Business Venturing, 28(6), 774–789. https://doi.org/10.1016/j.jbusvent.2013.06.002

- Audretsch, D. B., & Tamvada, J. P. (2008). The distribution of firm startup size across geographic space. CEPR Discussion Paper No. 6846. CEPR: London.

- Ayyagari, M., Beck, T., & Demirgüç-Kunt, A. (2007). Small and medium enterprises across the globe. Small Business Economics, 29(4), 415–434. https://doi.org/10.1007/s11187-006-9002-5

- Ayyagari, M., Demirguc-Kunt, A., & Maksimovic, V. (2008). How important are financing constraints? The role of finance in the business environment. World Bank Economic Review, 22(3), 483–516. https://doi.org/10.1093/wber/lhn018

- Banerjee, A., & Munshi, K. (2004). How efficiently is capital allocated? Evidence from the knitted garment industry in Tirupur. Review of Economic Studies, 71(1), 19–42. https://doi.org/10.1111/0034-6527.00274

- Barro, R., & McCleary, R. (2003). Religion and economic growth. NBER Working Paper No. 9682. Cambridge: MA.

- Baydoun, N., Mamman, A., & Mohmand, A. (1999). The religious context of management practices: The case of Islamic religion, accounting, commerce and finance. Islamic Perspective Journal, 3, 59–79. https://researchers.cdu.edu.au/en/publications/the-religious-context-of-management-practices-the-case-of-the-isl

- Beck, T., Behr, P., & Madestam, A. (2018). Sex and credit: Do gender interactions matter for credit market outcomes? Journal of Banking and Finance, 87, 380–396. https://doi.org/10.1016/j.jbankfin.2017.10.018

- Beck, T., & Demirgüç-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. Journal of Banking and Finance, 30(11), 2931–2943. https://doi.org/10.1016/j.jbankfin.2006.05.009

- Becker, G. (1971). The economics of discrimination. University of Chicago Press.

- Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking and Finance, 30(11), 2945–2966. https://doi.org/10.1016/j.jbankfin.2006.05.008

- Bertrand, M., & Mullainathan, S. (2004). Are Emily and Greg more employable than Lakisha and Jamal: A field experiment on labor market discrimination. American Economic Review, 94(4), 991–1013. https://doi.org/10.1257/0002828042002561

- Bhalotra, S., Irma Clots-Figueras, I., & Iyer, L. (2018). Pathbreakers? Women’s electoral success and future political participation. Economic Journal, 128(613), 1844–1878. https://doi.org/10.1111/ecoj.12492

- Brancati, W. (2014). Innovative financing and the role of relationship lending for SMEs. Small Business Economics, 44, 449–473.

- Cameron, A. C., & Trivedi, P. K. (2010). Microeconometrics Using Stata (Rev.) ed.). Stata Press.

- Carbo-Valverde, S., Rodriguez-Fernandez, F., & Udell, G. F. (2008). Bank lending, financing constraints and SME investment Working Paper No. 4. Federal Reserve Bank of Chicago, ChicagoIL.

- Carpenter, R. E., & Petersen, B. C. (2002). Is the growth of small firms constrained by internal finance? Review of Economics and Statistics, 84(2), 298–309. https://doi.org/10.1162/003465302317411541

- Catholic Bishops’ Conference of India. (2016). Policy of Dalit Empowerment in the Catholic Church in India: An Ethical Imperative to Build Inclusive Communities. http://www.cbci.in/DownloadMat/dalit-policy.pdf

- Chattopadhyay, R., & Duflo, E. (2004). Women as policy makers: Evidence from a randomised policy experiment in India. Econometrica, 72(5), 1409–1443. https://doi.org/10.1111/j.1468-0262.2004.00539.x

- Chaudhuri, K., Sasidharan, S., Seethamma, R., & Rajesh, S. R. (2020). Gender, small firm ownership and credit access; Some insights from India. Small Business Economics, 54(4), 1165–1181. https://doi.org/10.1007/s11187-018-0124-3

- Cooperatives Europe. (2020). A new SME strategy: For an inclusive SME strategy at EU level. Brussels (March 11). https://coopseurope.coop/sites/default/files/SME%20strategy_Position%20paper%20extended.pdf

- Cotterill, S., Sidanius, J., Bhardwaj, A., & Kumar, V. (2014). Ideological support for the Indian caste system: Social dominance orientation, right-wing authoritarianism and karma. Journal of Social and Political Psychology, 2(1), 98–116. https://doi.org/10.5964/jspp.v2i1.171

- Cowling, M. (2010). The role of loan guarantee schemes in alleviating credit rationing in the UK. Journal of Financial Stability, 6(1), 36–44. https://doi.org/10.1016/j.jfs.2009.05.007

- De Andres, P., Gimeno, R., & de Cabo, R. M. (2021). The gender gap in bank credit access. Journal of Corporate Finance, 71, 101782. https://doi.org/10.1016/j.jcorpfin.2020.101782

- de la Torre, A., Martínez Pería, M. S., & Schmukler, S. (2010). Bank involvement with SMEs: Beyond relationship lending. Journal of Banking and Finance, 34, 2280–2293. https://doi.org/10.1016/j.jbankfin.2010.02.014

- Delechat, C., Newiak, M., Xu, R., Yang, F., & Aslan, G. (2018). What is driving women’s financial inclusion across countries? IMF Working Paper No. 38. IMF: Washington DC.

- Delis, M., Hasan, I., Iosifidi, M., & Ongena, S. (2022). Gender, credit and firm outcomes. Journal of Financial and Quantitative Analysis, 57(1), 359–389. https://doi.org/10.1017/S0022109020000897

- Deller, S. C., Conroy, T., & Markeson, B. (2018). Social capital, religion and small business activity. Journal of Economic Behavior and Organization, 155, 365–381. https://doi.org/10.1016/j.jebo.2018.09.006

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring financial Inclusion and the Fintech Revolution. The World Bank.

- Deshpande, A., & Sharma, S. (2013). Entrepreneurship or survival? Caste and gender of small business in India. Economic and Political Weekly, 48, 38–49.

- Deshpande, A., & Sharma, S. (2016). Disadvantage and discrimination in self-employment: Caste gaps in earnings in Indian small business. Small Business Economics, 46(2), 325–346. https://doi.org/10.1007/s11187-015-9687-4

- Drakopoulou, D. S., & Seaman, P. T. (1998). Religion and enterprise: An introductory exploration. Entrepreneurship: Theory and Practice, 23, 71–86. https://doi.org/10.1177/104225879802300104

- Drydakis, N. (2010). Religious affiliation and employment bias in the labor market. Journal for the Scientific Study of Religion, 49(3), 477–493. https://doi.org/10.1111/j.1468-5906.2010.01523.x

- Duarte, J., Siegel, S., & Young, L. (2012). Trust and credit: The role of appearance in peer-to-peer lending. Review of Financial Studies, 25(8), 2455–2484. https://doi.org/10.1093/rfs/hhs071

- Du, X., & Zeng, Q. (2019). Bringing religion back in: Religious entrepreneurs, entrepreneurial gender and bank loans in Chinese family firms. Asian Review of Accounting, 27(4), 508–545. https://doi.org/10.1108/ARA-04-2018-0097

- Galbraith, C., & Galbraith, D. (2007). An empirical note on entrepreneurial activity, intrinsic religiosity and economic growth. Journal of Enterprising Communities: People and Places in the Global Economy, 1, 188–201.

- Gherghina, S. C., Botezatu, M. A., Hosszu, A., & Simionescu, L. N. (2020). Small and medium-sized enterprises (SMEs): The engine of economic growth through investments and innovation. Sustainability, 12(347), 347. https://doi.org/10.3390/su12010347

- Ghosh, S. (2020). Access to and use of finance: Does religion matter? Indian Economic Review, 55(1), 67–92. https://doi.org/10.1007/s41775-020-00082-6

- Ghosh, S. (2022a). Religiosity and bank performance: How strong is the link? Journal of Behavioral and Experimental Finance, 33(100600). https://doi.org/10.1016/j.jbef.2021.100600

- Ghosh, S. (2022b). Political empowerment of women and financial inclusion: Is there a link? Social Science and Humanities Open, 5(100267). https://doi.org/10.1016/j.ssaho.2022.100267

- Government of India. (2015). Religion Census 2011.

- Government of India. (2016). Annual Report 2015-16. Ministry of Micro, Small and Medium Enterprises. :.

- Granovetter, M. S. (1973). The strength of weak ties. American Journal of Sociology, 78(6), 1360–1380. https://doi.org/10.1086/225469

- Guiso, L., Sapienza, P., & Zingales, L. (2006). Does culture affect economic outcomes? Journal of Economic Perspectives, 20(2), 23–48. https://doi.org/10.1257/jep.20.2.23

- Gupta, D. (2005). Caste and politics: Identity over system. Annual Review of Anthropology, 34(1), 409–427. https://doi.org/10.1146/annurev.anthro.34.081804.120649

- Henley, A. (2017). Does religion influence entrepreneurial behavior ? International Small Business Journal, 35(5), 1–21. https://doi.org/10.1177/0266242616656748

- Hilary, G., & Hu, J. K. (2009). Does religion matter in corporate decision making in America? Journal of Financial Economics, 93(3), 455–473. https://doi.org/10.1016/j.jfineco.2008.10.001

- Huang, W., Boateng, A., & Newman, A. (2016). Capital structure of Chinese listed SMEs: An agency theory perspective. Small Business Economics, 47(2), 535–550. https://doi.org/10.1007/s11187-016-9729-6

- Huoy, C.-W., & Ali, R. (2017). Does a Muslim CEO matter in Shariah-compliant companies? Evidence from Malaysia. Pacific Basin Finance Journal, 42, 126–141. https://doi.org/10.1016/j.pacfin.2016.08.010

- Iyer, L., Khanna, T., & Varshney, A. (2013). Caste and entrepreneurship in India. Economic and Political Weekly, 47(February), 52–60.

- Iyer, L., Mani, A., Mishra, P., & Topalova, P. (2012). The power of political voice: Women’s political representation and crime in India. American Economic Journal: Applied Economics, 4, 165–193. https://doi.org/10.1257/app.4.4.165

- Kanagaretnam, K., Lobo, G. J., & Wang, C. (2015). Religiosity and earnings management: International evidence from the banking industry. Journal of Business Ethics, 132(2), 277–296. https://doi.org/10.1007/s10551-014-2310-9

- King, E. B., Shapiro, J., Hebl, M., Singletary, S., & Turner, S. (2006). The stigma of obesity in customer service: A mechanism for remediation and bottom-line consequences of interpersonal discrimination. Journal of Applied Psychology, 91(3), 579–593. https://doi.org/10.1037/0021-9010.91.3.579

- Kumar, S. M. (2013). Does access to formal agricultural credit depend on caste? World Development, 43, 315–328. https://doi.org/10.1016/j.worlddev.2012.11.001

- Kumar, A., Page, J. K., & Spalt, O. G. (2011). Religious beliefs, gambling attitudes, and financial market outcomes. Journal of Financial Economics, 102(3), 671–708. https://doi.org/10.1016/j.jfineco.2011.07.001

- Kuntchev, V., Ramalho, R., Rodriguez-Meza, J., & Yang, J. S. (2013), What have we learned from the Enterprise Surveys regarding access to finance by SMEs? Policy Research Working Paper No. 6670. The World Bank: Washington DC.

- Lewis, B. (2002). What went wrong? The clash between Islam and modernity in the Middle East. HarperCollins.

- Madison, K., Moore, C. B., Daspit, J. J., & Nabisaalu, J. K. (2022). The influence of women on SME innovation in emerging markets. Strategic Entrepreneurship Journal, 16(2), 281–313. https://doi.org/10.1002/sej.1422

- Matto, M., & Niskanen, M. (2019). Religion, national culture and cross-country differences in the use of trade credit: Evidence from European SMEs. International Journal of Managerial Finance, 15(3), 350–370. https://doi.org/10.1108/IJMF-06-2018-0172

- Mazumdar, D., & Sarkar, S. (2008). Globalisation, Labor Markets and Inequality in India. Routledge.

- McLeod, W. H. (1975). The Evolution of Sikh Community: Five Essays. Oxford University Press.

- Michels, J. (2012). Do unverifiable disclosures matter? Evidence from peer-to-peer lending. Accounting Review, 87(4), 1385–1413. https://doi.org/10.2308/accr-50159

- Mines, M. (1972). Muslim social stratification in India: The basis for variation. SouthWestern Journal of Anthropology, 28(4), 333–349. https://doi.org/10.1086/soutjanth.28.4.3629316

- Muravyev, A., Talavera, O., & Schäfer, D. (2009). Entrepreneurs’ gender and financial constraints: Evidence from international data. Journal of Comparative Economics, 37(2), 270–286. https://doi.org/10.1016/j.jce.2008.12.001

- Nguyen, T. V., Le, N. T. B., & Freeman, N. (2006). Trust and uncertainty: A study of bank lending to private SMEs in Vietnam. Asia Pacific Business Review, 12(4), 547–568. https://doi.org/10.1080/13602380600571260

- Nikolova, E., & Simroth, D. (2015). Religious diversity and entrepreneurship in transition: Lessons for policymakers. IZA Journal of European Labor Studies, 4(1), 1–21. https://doi.org/10.1186/s40174-014-0028-4

- North, D. C. (1991). Institutions. Journal of Economic Perspectives, 5(1), 97–112. https://doi.org/10.1257/jep.5.1.97

- Nunziata, L., & Rocco, L. (2014). A tale of minorities: Evidence on religious ethics and entrepreneurship. Journal of Economic Growth, 21, 189–224.

- Osei-Tutu, F., & Weill, L. (2021). Sex, language and financial inclusion. Economics of Transition and Institutional Change, 29(3), 369–403. https://doi.org/10.1111/ecot.12262

- Pager, D., & Quillian, L. (2005). Walking the talk: What employers say versus what they do. American Sociological Review, 70(3), 355–380. https://doi.org/10.1177/000312240507000301

- Parboteeah, K. P., Walter, S. G., & Block, J. H. (2015). When does Christian religion matter for entrepreneurial activity? The contingent effect of a country’s investments into knowledge. Journal of Business Ethics, 130(2), 447–465. https://doi.org/10.1007/s10551-014-2239-z

- Pew Research Center. (2018). 5 facts about religion in India (June 29). Pew Research Centre.

- Planning Commission. (2005). Micro finance and empowerment of scheduled caste women. In An Impact Study of SHGs in Uttar Pradesh and Uttaranchal. Government of India. New Delhi: Government of India.

- Pratto, F., Liu, J. H., Levin, S., Sidanius, J., Shih, M., Bachrach, H., & Hegarty, P. (2000). Social dominance orientation and the legitimisation of inequality across cultures. Journal of Cross-Cultural Psychology, 31(3), 369–409. https://doi.org/10.1177/0022022100031003005

- Presbitero, A. F., Rabellotti, R., & Piras, C. (2014). Barking up the wrong tree? Measuring gender gaps in firm’s access to finance. Journal of Development Studies, 50(10), 1430–1444. https://doi.org/10.1080/00220388.2014.940914

- Puri, H. K. (2003). Scheduled castes in Sikh community: A historical perspective. Economic and Political Weekly, 38(June), 2693–2701.

- Quartey, P., Turkson, E., Abor, J. Y., & Iddrisu, A. M. (2017). Financing the growth of SMEs in Africa: What are the constraints to SME financing within ECOWAS? Review of Development Finance, 7(1), 18–28. https://doi.org/10.1016/j.rdf.2017.03.001

- Rajesh, S. N., & Sasidharan, S. (2018). Does the caste of the firm owner play a role in access to finance for small enterprises? Evidence from India. Developing Economies, 56(4), 267–296. https://doi.org/10.1111/deve.12183

- Rajesh, R., & Sen, K. (2015). Finance constraints and firm transition in the informal sector: Evidence from Indian manufacturing. Oxford Development Studies, 43(1), 123–143. https://doi.org/10.1080/13600818.2014.972352

- Rani, G. P., & Elliott, C. (2014). Disparities in earnings and education in India. Cogent Economics and Finance, 2(1), 941510. https://doi.org/10.1080/23322039.2014.941510

- Reddy, S., & Jadhav, A. M. (2019). Gender diversity in boardrooms – A literature review. Cogent Economics and Finance, 7(1644703). https://doi.org/10.1080/23322039.2019.1644703

- Religious Freedom and Business Foundation. (2021). Corporate Religious Equity, Diversity and Inclusion Index. USA.

- Reserve Bank of India. (2009). Basic Statistical Returns of Banks 2008. RBI.

- Reserve Bank of India. (2015). Report of the Committee on Medium-term Path on Financial Inclusion. Mumbai.

- Reserve Bank of India. (2018). Handbook of Statistics on Indian States 2017-18. RBI.

- Rietveld, C. A., & van Burg, E. (2014). Religious beliefs and entrepreneurship among Dutch Protestants. International Journal of Entrepreneurship and Small Business, 23(3), 279–295. https://doi.org/10.1504/IJESB.2014.065515

- Robb, A. M., & Robinson, D. T. (2012). The capital structure decisions of new firms. Review of Financial Studies, 1, 1–27. https://doi.org/10.1093/rfs/hhs072

- Sadeghloo, T., Qeidari, H. S., Salehi, M., & Jalali, A. F. (2018). Analysis of risk and return on investment of local entrepreneurs in Iran. Journal of Rural Development, 37(3), 539–564. https://doi.org/10.25175/jrd/2018/v37/i3/139523

- Sidanius, J., & Pratto, F. (1999). Social Dominance: An Intergroup Theory of Social Hierarchy and Oppression. Cambridge University Press.

- Thorat, S. (2005). Caste, social exclusion and poverty linkages: Concept, measurement and empirical evidence. In Concept Paper for PACS.

- Thorat, S., & Neuman, K. S. (2012). Economic Discrimination Concept, Consequences and Remedies. In S. Thorat and K.S. Krieger (eds.) Blocked by caste: Economic discrimination in modern India (pp. 3-15). Oxford University Press.

- Umar, U. H., Ado, M. B., & Ayuba, H. (2020). Is religion (interest) an impediment to Nigeria’s financial inclusion targets by the year 2020? A qualitative inquiry. Qualitative Research in Financial Markets, 12(3), 283–300. https://doi.org/10.1108/QRFM-01-2019-0010

- Weber, M. (1930). The Protestant Ethic and the Spirit of Capitalism. Routledge.

- Wellalage, N., & Locke, S. (2017). Access to credit in South Asia: Do women entrepreneurs face discrimination? Research in International Business and Finance, 41, 336–346. https://doi.org/10.1016/j.ribaf.2017.04.053

- Williams, R. (2021). Adjusted predictions and marginal effects for multiple outcome models and commands. University of Notre Dame. Accessed at [https://www3.nd.edu/~rwilliam/stats3/Margins05.pdf]

- Yoshino, N., & Taghizadeh-Hesary, F. (2018). The role of SMEs in Asia and their difficulties in accessing finance. ADBI Working Paper 911. Asian Development Bank Institute: Tokyo.

- Zelekha, Y., Avnimelech, G., & Sharabi, E. (2014). Religious institutions and entrepreneurship. Small Business Economics, 42(4), 747–767. https://doi.org/10.1007/s11187-013-9496-6

- Zingales, L. (2015). The cultural revolution in finance. Journal of Financial Economics, 117(1), 1–4. https://doi.org/10.1016/j.jfineco.2015.05.006