?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the impact of monetary policy instruments such as discount rate, reserve requirement and liquidity requirement on bank credit to the private sector in the Kingdom of Eswatini. Monthly data sourced from the Central Bank of Eswatini and Eswatini Central Statistics Office is used for the period January 2000 to December 2017. Using the Johansen cointegration test and Vector Error Correction Model, our results show that: there is one cointegration in the model and the current levels of the discount rate, reserve requirement and liquidity requirement bear a negative and significant effect to bank credit to the private sector. This indicates that the three instruments are not supportive to economic growth and they are not optimal to stimulate credit. Applying the Quadratic approach, findings of this study reveal that the optimal monetary policy mix (thresholds) to stimulate bank credit to the private sector while maintaining inflation within reasonable levels is 5.42% for the discount rate, 4.03% for the reserve requirement, 12.48% for the liquidity requirement. The study recommends that the Central Bank of Eswatini should always take into account the existence of trade-off in monetary policy instruments results in order to stimulate bank lending to the private sector.

Public Interest Statement

This paper analyses the effects of the discount rate, reserve requirement and liquidity requirement on bank credit to the private sector in the Kingdom of Eswatini. The research also determines the thresholds of the three monetary policy instruments, with an aim of strengthening regulation of the Central Bank of Eswatini. Monthly data for the period 2000 to 2017 from the Central Bank of Eswatini is used. The findings of this study indicate that the current levels of the discount rate, reserve requirement and liquidity requirement have a negative effect on bank credit to the private sector. Findings of this study show that the three instruments had not been at their optimal to positive influence bank lending to the private sector. The Central Bank of Eswatini should take into account the existence of trade-off in policy results when stimulating credit and controlling inflation.

1. Introduction

Central bank regulation is important to ensure stability and efficiency, to improve the competitiveness of the banking system, to mitigate the occurrence of superfluous financial distortions that emanate from bank panics and crises, and to moderate depositors’ risk exposure during financial distress (Poole & Wheelock, Citation2008). While the mandate of the central bank is to ensure stability and foster economic growth, it is of paramount importance to understand that monetary policy regulation may not be costless to the economy and its effect may be more pronounced via the lending system to the private sector.

In 2012 in the Kingdom of Eswatini, the Central Bank Lending system policy mix became a cause for concern amid a decline in credit to the private sector and economic growth despite adjustments made by the monetary policy authorities on the bank rate, cash reserve requirement and liquidity requirement. The slowdown in bank credit was experienced after major fiscus challenge in 2010 and 2011 which resulted to significant government’s financing shortfalls. In 2015, the country experienced a major shock on credit to the private sector (corporate lending turned negative), which reduced the average to 7.5% in 2016 from 15.4% in 2015 (Central Bank of Eswatini, Citation2015). The shock was a result of a decline of seinorage from Southern Africa Customs Union. This episode was accompanied by deterioration in banks’ asset quality, with Non-Performing Loans (NPL) escalating to more than 10% of total loans in March 2017 (International Monetary Fund, Citation2017). The prevailing situation in terms of credit seems to signal monetary policy instruments imbalances, with a resulting need to first determine the impact of these instruments and establish the optimal thresholds for the Central Bank of Eswatini to aim at, when setting its monetary policy stance. Therefore, this study seeks to examine the current monetary policy mix of the Central Bank of Eswatini to determine if does have an influence on bank credit to the private sector in the Kingdom of Eswatini. This research also seeks to examine the current levels of monetary policy instruments and recommend optimal thresholds for bank credit to the private sector if there is misalignment. No study with a similar approach has been undertaken for the Kingdom of Eswatini.

Previous studies such as Amidu (Citation2006), Gambacorta and Rossi (Citation2007), Hofmann (Citation2001), Ajayi and Atanda (Citation2012), Olweny and Chiluwe (Citation2012), and Sharma and Gounder (Citation2012), and Assefa (2014) explored the determinants of bank credit using different regression models. Younus and Akhteruzzaman (Citation2012), Tule et al. (Citation2015), and Olade (Citation2015) applied the quadratic function to determine thresholds for monetary policy indicators. While the contribution of the above-stated research studies is appreciated, their assessment is limited only investigate the determinants of bank credit to the private sector, ignoring an important aspect of guiding Central Banks in terms of the thresholds of monetary policy instruments to aim at in order to stimulate bank credit to the private sector credit which is essential for investment and economic growth.

This research is envisaged to make several contributions in the body of literature, as the researcher has underscored and bridged the gaps present in the past research, such as the lack of empirical evidence of the impacts of monetary policy instruments on bank lending to the private sector and thresholds for monetary policy instruments in the Kingdom of Eswatini. There were almost no empirical references and proofs to explain the relationship between monetary policy instruments and the lacklustre bank lending performance. Further, this provides an empirical guide in terms of thresholds for the Central Bank of Eswatini to aim at when setting its monetary policy instruments. Therefore, the major contribution for this research is that, it has determined the thresholds for the discount rate (DR), reserve requirement (CRR) and liquidity requirement (LQR) and further provided policy recommendation for the Kingdom of Eswatini, which when adopted may significantly bring a turnaround not only for bank credit but also for economic growth which has been subdued in the past decade.

2. Trends analyses of the discount rate, reserve requirement and liquidity requirements

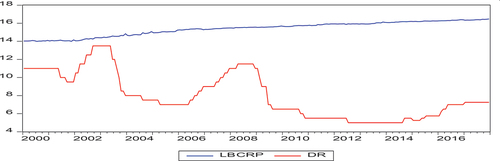

Since 2001, the discount rate was set at par with the South African repo rate until June 2008. From 2008, the Central Bank of Eswatini sometimes deviated from parity by 50 basis points either below or above the SA repo rate but in March 2010 decided to restore parity of the bank rate with the South African Reserve Bank (SARB) repo rate. Further deviations from the parity were noted from 2015 but were not more than 100 basis point. Since the local economy is dominated by South African firms, a surge in the discount rate triggered need to source credit across the border, in the form of reinvested earnings. Therefore, an increase in discount rate reduce the firms’ appetite to source credit in the local banking industry (Dlamini & Skosana, Citation2017). below shows the trend of bank credit and discount rate from year 2000 to 2017.

Figure 1. Trends of bank credit and discount rate.

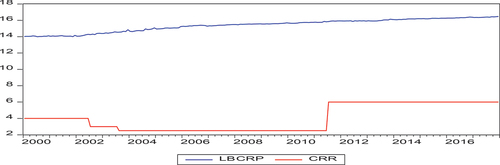

In the period 2000 to 2017, the Central Bank of Eswatini effected three changes on the reserve requirement. The first was to introduce a separate call account for banks in 2003, which earns interest. The reserve requirement was further revised in 2011 from 2.6 percent to 6 percent. The 6 percent is meant to facilitate the clearing and settlement of interbank transactions such as transactions between the commercial banks and central bank and to safeguard liquidity and the safety of banks. Over the period under review, commercial banks had been compliant to maintain levels of reserves at 6 percent as required by the Central Bank of Eswatini. The reserve requirement is one of the monetary policy instrument and increasing/decreasing affects banking liquidity and credit extension (Dlamini and Skosana, 2016). presents the relationship between bank credit and reserve requirement.

Figure 2. Trends of Bank Credit and Cash Reserve Requirement.

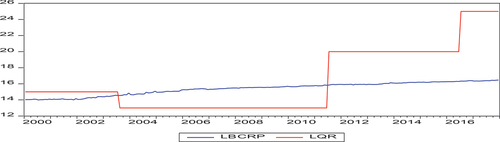

The liquidity requirement before year 2000 was fixed at 15 percent. The Central Bank reduced the liquidity requirement from to 13 percent in August 2003. The aim was to lessen the negative tax effect that it was exerting on banks’ intermediation. In July 2011, liquidity requirement was revised upwards to 20 percent in an effort to protect the industry from spillover effects of the fiscal crisis. A further increase was effected in July 2016, from 20 percent to 25 percent. The liquidity ratio in most cases was above the statutory requirement set by the Central Bank of Eswatini, as such foreign banks have increased their investments in South African markets due to lack of investment avenues in the domestic markets. According to Dlamini and Skosana (2016) an increase in liquidity requirement affects negatively affect commercial banks, which in turn slows down lending. The trend between bank credit and liqiuidity requirement is shown in below.

Figure 3. Trends Bank Credit and Liquidity Requirement.

3. Theory and literature review

3.1. Theoretical review

This study appreciates and acknowledges the contribution of the Classical theory, Keynesian theory and Monetarist theory regarding monetary policy transmission to the economy (Bernanke & Gertler, Citation1995; Mishkin, Citation2001).

Theoretically, this study is premised on the bank lending channel of monetary transmission which emphasizes on behaviour of commercial banks following changes of Central Bank monetary policy instruments. Specifically, the bank lending channel focuses on the potential intensification effects that banks may generate as a result of the impact of monetary policy on credit supply (Kashyap & Stein, Citation1995; Walsh, Citation2003). The bank lending channel theory was introduced by Bernanke and Gertler (Citation1995) and provides that there are two components of the credit channel, namely the bank lending channel and the balance sheet channel. Bernanke and Blinder’s (Citation1995) seminal work on bank lending channel demonstrates that the imperfect substitutability between bonds and loans increases monetary policy shocks compared to the interest rate channel. Bernanke and Blinder (1988) further argue that that soothing the hypothesis of perfect substitutability of loans and other debt instruments provides a distinct macroeconomic role of credit in an otherwise IS-LM model. Conversely, Hurlin and Kierzenkowski (Citation2002) assert that the bank lending channel cause monetary policy to be restrictive (or expansionary) compared to a standard IS-LM model due to the independent effect emanating from the asset side of the banking industry, which may lead to decreases (increases) of loan supply to borrowers.

Bernanke and Gertler (Citation1995) contributed to Bernanke and Blinder (1988)’s concept, by arguing that the credit channel should be considered a mechanism that reinforces the traditional money channel. Their emphasized on the importance of the institutional framework governing the financial system and economic agents’ financial position in assessing the bank lending behaviour. the institutional framework governing the financial system includes the extent to which the banking system secures liabilities that are not subject to reserve requirements and non-bank intermediaries as key determinants of the credit channel.

The strength of the bank lending channel is its ability to differentiate the “lending view” and the “credit rationing”. The lending view shed light on the relative degree of changes in the demand for and supply of credit following monetary policy tightening (Kashyap & Stein, Citation1995). According to the lending channel theory, a contractionary monetary policy will lead to a decline in the amount of new credit supplied, reflecting the proportional increase of market rates. Contrary, the credit rationing supports are of the view that while the volume of new loans would decline in following policy tightening, bank loan rates would proportionally rise but relatively lower than the market rates.

The bank lending channel largely emphasise that monetary policy has a direct impact on deposits which is core for the supply of loanable funds hence influencing the lending behaviour of banks. Therefore, contractionary monetary policy depletes deposits at the disposal of commercial banks. On the flipside, Disyatat (Citation2010) argues that policy-induced variation in deposits is misplaced in the bank lending theory, emphasising that commercial banks can issue credit up to a certain multiple of its own capital, set either by regulation or market discipline. Consequently, an increase in bank credit supply is largely driven by the demand for and supply of loans by banks.

M (Contractionary monetary policy) ↓ ⇒ (Bank Deposits) ↓ ⇒ (Bank Loans) ↓ ⇒ I (Investment) ↓ ⇒ C (Consumption) ↓⇒ Y (output) ↓ … … … … … … … … … … … … … … … … … … … … … … … … … . … … . … [Schematic 1]

3.2. Empirical literature

Owing to the understanding that the mandate of the Central bank is to control inflation, few researchers have conducted research studies on the effect of monetary policy instruments on bank credit to the private sector with a view to determine the optimal thresholds. Hence, the available information in body of literature is scant in most countries. This compromises the credibility of central banks in setting its instruments and existing empirical studies. Further, available empirical literature on the central bank lending system provides different conclusions on the impact of the discount rate, reserve requirement and liquidity requirement on bank credit to the private sector. These may be a result of the variables used, methodology, and scope of their studies.

Amidu (Citation2006) examined the effect of monetary policy instruments on bank lending in Ghana using cross-sectional panel data for the period 1998 to 2004. The explanatory variables employed were money supply and prime lending rate as proxy for monetary policy instruments. The results show that expansionary monetary policy had a positive effect on bank credit to the private sector, but prime lending rate negatively affected bank lending behaviour during this period.

Younus and Akhteruzzaman (Citation2012), assessed the effect of the cash reserve requirement and other monetary policy instruments on bank credit in Bangladesh. They adopted a descriptive approach-trend analysis and summary statistics. The results show that a reduction in cash reserve requirement yields a positive effect on bank credit and investment. Younus and Akhteruzzaman (Citation2012) concluded that the cash reserve requirement was an important instrument in influencing bank lending to the private sector, especially to small and medium businesses. The gap in Younus and Akhteruzzaman (Citation2012) study is that a descriptive approach does not provide enough evidence to allow a researcher to conclude with confidence. Therefore, there is a need to empirically test and validate the results. Also, there were no efforts to dictate the optimal range for the cash reserve requirement to guide the central bank.

Ajayi and Atanda (Citation2012) investigated the effect of monetary policy instruments using time-series data for the period 1980 to 2008. The bank total loan was estimated as a function of minimum policy rate, liquidity ratio, cash reserve ratio, inflation and exchange rate. The study utilised the Engle-Granger two-step cointegration approach. Based on findings, interest rate, inflation rate and exchange rate had a positive effect on bank loans. The liquidity ratio and cash reserve ratio had a negative effect on bank credit to the private sector. The study concludes that the liquidity ratio and cash reserve ratio do not stimulate bank lending in Nigeria.

Olweny and Chiluwe (Citation2012) investigated the impact of monetary policy on private sector investment in Kenya. These authors traced the effects of monetary policy through the transmission mechanism to establish the changes that emanated from alterations of monetary policy. The study utilised quarterly data for the period 1996 to 2009. A cointegration methodology was used to detect both the short- and long-run dynamics in response to an exogenous shock. The results show an inverse relationship between government domestic debt and the Treasury bill rate to private sector investment. The findings also reveal that money supply and domestic savings have a positive relationship with private sector investment, which is in line with the IS-LM model. Olweny and Chiluwe (Citation2012) conclude that a 1% tightening of monetary policy has the potential to reduce private sector investment by 2.63%.

Sharma and Gounder (Citation2012) investigated the determinants of bank credit extension to the private sector in six economies in the South Pacific for the period 1982 to 2009. The explanatory variables included the rate of inflation, the ratio of deposits to GDP, average interest rate on the loans, the size of the banks’ assets of output, a dummy variable reflecting the existence of a financial market, and GDP. The results depict that the higher interest rates on credit and the higher inflation rate tend to have a negative effect on the rate of growth in credit. They further conclude that the size of the deposits and assets had a positive effect on the growth of credit. The results also provide evidence that strong economic growth tends to stimulate credit to the private sector. However, the gap in Sharma and Gounder’s study is that they ignored other critical factors such as the cash reserve requirement and exchange rate. Olorunmade et al. (Citation2019) assessed the determinant of private sector credit and its implication on economic growth in Nigeria. The study finds a positive significant relationship between private sector credit and economic growth in Nigeria.

Gambacorta and Rossi (Citation2007) investigate the non-linearities monetary policy shocks on bank lending in the euro area for the period 1985–2005 using the Johansen cointegration test and Vector Error Correction Model (VECM). The paper uncovers negative effect of monetary policy tightening on bank lending. Other studies that adopted a similar approach include Hofmann (Citation2001), and Dlamini (Citation2008), Aziakpono (Citation2006), and Dlamini (Citation2008) assert that the Johansen cointegration procedure performs better than the other methods even when the errors are not normally distributed, or the dynamics of the VECM are unknown, and additional lags are included in the VECM.

A major shift in studies related to monetary policy instruments was observed after the seminal work of Tong in the early 1980s, who brought to the fore the need to ascertain thresholds. Khan and Senhadji (2001) and Mehrara and Karsalari (Citation2011) used the non-linear approach to assess thresholds of interest on private investment in developing economies. This study is motivated by Hofmann (Citation2001), Younus and Akhteruzzaman (Citation2012), Vargas and Cardozo (Citation2012), Tule et al. (Citation2015), and Olade (Citation2015), who used the quadratic function. The quadratic function is used as an extension to the Vector Error Correction model to determine the optimal thresholds for discount rate/bank rate, reserve requirement, and liquidity requirement.

Most of the studies have only assessed the determinants of inflation for the Kingdom of Eswatini, none has explored the effects of the monetary policy tools on bank credit to the private sector. Almost none of the past studies has determined the thresholds of the monetary policy instruments to enhance the Central Bank of Eswatini’s policy mix. The researcher has strived to bridge this existing gap by going beyond just establishing the relationship but also by determining the optimal threshold that the Central Bank of Eswatini can aim at to strike balance between containing inflation within reasonable levels while stimulating private sector credit.

4. Methodology

4.1. Econometric procedure and hypothesis

4.1.1. Cointegration test

The Johansen (1995) cointegration is used to test for cointegration and Vector Error Correction models are applied to estimate the long-run and short run relationship amongst the variables. Gujarati (2003) suggest that cointegration of two or more time-series reflects the presence of a long-run or equilibrium relationship. In principle, if the trace statistic ( trace) and maximum eigenvalues (

max) are less than their critical values at the 5% level, it suggests the presence of cointegrating vectors, and the opposite holds (Chakraborty and Basu, 2002). If the null hypothesis of no cointegration is rejected, it shows that the linear combination of the variables is cointegrated, hence a non-spurious long-run relationship exists between the variables. A summarized version of the trace and the maximum eigenvalues of the Johansen cointegration technique is presented as follows:

and

where r represents the number of cointegrating vectors under the null hypothesis, T shows the number of observations used in the selected period and denotes the estimated value for the ith ordered eigenvalue from the Π matrix. The

max is based on the greatest eigenvalue and it computes a separate test on the eigenvalue.

Prior to determining the thresholds diagnostic test, the impulse response and variance decomposition and diagnostic test are conducted. These include testing for autocorrelation, heteroscedasticity and Bera-Jarque normality test. The causality test is also applied to establish the existence and direction of causality similar to Chaudhry et al. (2015). The Granger causality approach provides that variable Y is Granger caused by X, if Y can be estimated better from past values of Y and X than from past values of Y alone, and vice versa. The results can be unidirectional causality from X to Y, unidirectional causality from Y to X, feedback or bi-directional causality, and no causality.

4.1.2. Determination of threshold

In line with Younus and Akhteruzzaman (Citation2012) for Bangladesh, Tule et al. (Citation2015) and Olade (Citation2015) for Nigeria, the Quadratic approach is applied in this study to determine the optimal thresholds for the Central Bank of Eswatini to aim at when setting these monetary policy instruments.

4.2. The quadratic model specification

Where: and

2 denotes the linear and non-linear terms of the threshold series. EquationEquation 4.3

(4.3)

(4.3) represents the relationship between

and

is non-linear of an upturned U-shape. Our positive coefficient of

is expected and a negative figure is expected for the squared variable. Therefore, differencing equation 4.4 when it is equated to zero it produces:

The optimal threshold level is obtained by solving equation 4.4 for * as shown below:

Empirical studies differ on the selection of economic fundamentals that influence bank credit in the short and long-run. For the purpose of achieving the objectives of this study, the variables were selected based on economic theory, the empirical literature and data availability. Further, the economic and banking industry history of Kingdom of Eswatini influenced the selection of variables.

From the foregoing, the following hypotheses which are in line with the two objectives of this study were tested:

H1: There is no effect of monetary policy instruments on bank credit to the private sector in the Kingdom of Eswatini.

H2: There are no optimal monetary policy instruments to stimulate bank lending directed to the private sector in the Kingdom of Eswatini.

4.3. Data description and variable signs

4.3.1. Bank credit to the private sector (±)

This is the logarithm of bank credit to the private sector (a proxy for bank lending in the Kingdom of Eswatini). TheoryFootnote1 suggests that this variable is largely influenced by monetary policy instruments such as the discount rate, reserve requirement, liquidity requirement and treasury bills. This variable can either be positive or negative.

4.3.2. Discount rate/bank rate (-)

This is the central bank rate used by central bank to maintain price stability which also influences bank lending either positive or negative depending on the monetary policy stance pursued. If the central bank pursues an expansionary monetary policy, the discount rate is reduced and the reverse is true. Ajayi and Atanda (Citation2012) suggest that the discount rate does not affect bank lending, while Karim et al. (Citation2011) advocate that the bank rate is an important instrument to influence credit to the private sector. A negative relationship between the central bank rate and bank credit to the private sector is expected.

4.3.3. Reserve requirement (-)

Central banks utilize the reserve requirement mainly to control money supply in the economy. Changes of reserve requirement first affects banks´ interest rates by influencing the banking optimal behaviour in maximising profits. Malede (Citation2014) show that there is a significant relationship between commercial bank lending and cash reserve requirement. Usually, an increase in the reserve requirement is followed by a decline in credit since it withdraws money from circulation. A negative sign is expected for this variable. Olokoyo (Citation2011) and Mwafag (Citation2015), who investigated factors affecting bank credit in Jordan and found that the cash reserve requirement was not statistically significant.

4.3.4. Liquidity requirement (-)

The central banks require banks to hold a sufficient level of liquid assets against short-term expected net liquid outflows, to ensure resilience of the banking industry. The higher the liquidity ratio, the lower loans offered by the commercial banks. This variable is expected to have a negative effect of this variable on the proportion of credit facilities (Alfon et al., Citation2004; Karim et al., Citation2011).

4.3.5. Treasury bills (±)

Treasury bills are issued by governments using their central banks to deal with temporarily insufficient budget. The 91-day treasury bill is utilized as a benchmark rate for government securities determined using auction as a measure of interest rates. Through treasury bills, central banks are able to raise short-term fund for governments and absorb surplus liquidity from financial markets concurrently. Eita (Citation2012) provides evidence that the 91-day Treasury bills have a significant effect on bank lending to the private sector.

4.3.6. Inflation (-)

Inflation defines the rise in the prices of most goods and services used such as food, clothing, housing, recreation, transport, consumer staples, etc. It measures the average price change in a basket of commodities and services over time. Inflation is suggestive of the decrease in the purchasing power of a unit of a country’s currency. Studies such as Imran and Nishatm (Citation2013), and Sharma and Gounder (Citation2012) show that the inflation rate had a negative impact on the rate of growth in credit. It is expected that this variable should exert a negative effect on the proportion of the credit facilities granted by banks.

4.3.7. Real GDP (+)

Real GDP depicts a country’s gross domestic product which has been adjusted for inflation. Studies such as Hofmann (Citation2001) and Calza et al. (Citation2001a) modelled the determinants of loans to the private sector and found that there is a positive relationship between bank credit to the private sector and real GDP. A positive relationship between bank lending and real GDP is expected in this study.

4.3.8. Lilangeni/dollar exchange rate (±)

The exchange rate is the rate at which the local/domestic currency can be changed into a foreign currency. Empirical findings by Manyok (Citation2016) provide that there is a negative association between exchange rates fluctuations and bank performance, including bank credit. Katusiime (Citation2018) who argues that there is a positive relationship between the exchange rate and credit to the private sector.

Explicitly, the equation is presented as:

where: L denotes the logarithm, LBCRP is bank credit to the private sector, DR is Central Bank rate/discount rate, CRR is the cash reserve requirement, LQR is the liquidity ratio/requirement, TRB Treasury bills rate, LINFL is inflation, LRGDP is real gross domestic product and LEDOLLAR is Lilangeni/Dollar exchange rate.

4.4. Data and sources

Monthly data from 2000 to 2017 is utilized with a total of 216 observations and 215 after adjustment. Except for DR, CRR, LQR and TBR, all the variables utilized for the model were transformed into natural logarithms. The data were obtained from the Central Bank of Eswatini statistics, quarterly reports, annual reports and Eswatini Central Statistics Office. Table presents a summary of the variable definitions and source.

Table 1. Definition of variables and sources of data

5. Empirical results and discussions

5.1. Descriptive statistics

Preceding to model estimation and in line with the methodology for dealing with time series data, we start by providing the descriptive statistics, which entail the mean, standard deviation, minimum and maximum values. The results are provided in Table . As can be observed from Table , the total bank lending to the private sector for all the banks in the Kingdom of Eswatini for the sample period ranged between a minimum of 13.99 percent to a maximum of 16.47 percent and had an average of 15.40 percent. The average discount rate of the Central Bank of Eswatini during the period 2000 to 2017 was recorded with a mean of 7.95 percent with a minimum discount rate of 5 percent and a maximum discount rate of 13.50 percent. The reserve requirement fluctuated from a minimum of 2 percent to a maximum of 6 percent with an average of 4 percent. The liquidity ratio recorded a minimum value of 13 percent and a maximum value of 25 percent, with a mean of 16.34 percent. The Treasury bill rate had a minimum of 5.62 percent and a maximum 13.04 percent, with a mean of 7.63 percent. Changes in inflation were ranging from a minimum value of 0.955 percent to a maximum value of 2.69 percent, with a mean of 1.88 percent. Oscillations of real gross domestic product ranged from a minimum of 10.11 percent to a maximum of 10.69 percent and had a mean of 10.41 percent. The exchange rate recorded an average of 8.96 percent and with a minimum value of 5.73 percent rising to a maximum of 10.11 percent. The standard deviations for all the variables show that the data were broadly spread around their corresponding means. The p-values of the Jarque-Bera are above 5% for all variables. Therefore, normality does not seem to be a problem in this case.

Table 2. Descriptive Statistics

5.2. Unit root results

We test selected series for unit roots tests to avoid spurious results, not to use series that are stationary at second difference I(2) to better understand the behavior, nature and order of integration of all the variables. The Augmented Dickey–Fuller (ADF) and Phillips-Perron (PP) tests were used to test for stationarity of the series Bondzie, Fosu & Asare (2014). The ADF and PP test the null hypothesis that the variables have a unit root. If the null hypothesis of the first two tests (ADF and PP) is rejected, that would suggest that the selected variables do not have a unit root. The automatic lag selection (max 1 lag) was used for all variables as provided by the Schwarz Information Criterion (SIC). The results are presented in Table .

Table 3. Unit root test

5.3. Johansen cointegration results

The results show that the trace test statistic to the null hypothesis of no cointegration (H0: r = 0) is 47.964 which is above the critical value of 41.7082 at the 5% significance level; thus, it rejects the null hypothesis of no cointegration (r = 0) in favour of the general alternative r ≥ 1. The null hypothesis of r ≤ 1 that the system has at most one, two and three (r ≤ 1) cointegrating vector cannot be rejected at the 5% significance level since the reported trace statistics are less than the critical values at the 5% significance level. Based on trace test concludes that there is one cointegrating vector in the model. Similarly, the max eigenvalue test results show that, for none the critical value is 48.8620 which is above the critical value of 41.7883 at the 5% significance level, therefore the null hypothesis of no cointegration is rejected for none. Beyond none, the null hypothesis cannot be rejected at the 5% significance level since the reported trace statistics are less than the critical values at the 5% significance level. Thus, the max eigenvalue test also confirms that there is one cointegrating vector in the model. Based on the results, we conclude that there is a long-run relationship among macroeconomic variables and bank credit to the private sector in the Kingdom of Eswatini. By normalizing based on the coefficient of LBCRP, we arrive at the following cointegrating vector: = [1.00, 0.6909, 0.4122, 0.7341, −0.3328, −0.0023, −0.8443, +0.021]. Thus, the cointegrating relationship is presented as follows:

The reported results provide evidence that the discount rate (DR), reserve requirement (CRR) and liquidity requirement (LQR) bear a significant negative relationship with bank credit to the private sector in the Kingdom of Eswatini. The results also show that there is a significant positive influence of an increase in real GDP (LRGDP) on bank credit to the private sector. Further, the reported results show that treasury bills (TBR) and inflation (LINFL) had positive signs but not significant. The exchange rate (LEDOLLAR) is also not significant. Worth noting is that DR is significant at 1%, CRR at (10%), LQR at 5% and LRGDP at 1%. This implies that the four variables contribute significantly to the cointegrating relationship.

The discount rate entered the long-run with a correct negative sign as expected. This implies that upward adjustment of the discount rate to control inflation has negative effects on lending to the private sector in the Kingdom of Eswatini. This finding is consistent with the bank lending theory of Olokoyo (Citation2011) and Yakubu et al. (Citation2018). The reserve requirement is significant and negative. This implies that an increase in the reserve requirement reduces the loanable funds for commercial banks to extend loans. This result is consistent with the findings of Meltzer (2003), and Ajayi and Atanda (Citation2012) who also provide evidence that an increased rise in the reserve requirement would negatively impact on bank lending and the ability to create loans. However, our findings in terms of the reserve requirement are contrary to those of Olusanya et al. (Citation2012) who found a positive relationship between bank credit and the reserve requirement. Further, the negative significant effect of liquidity requirement in this study suggests that the high liquidity requirement erodes the appetite lend more since banks are sceptical that borrowers may default leading to an increase in non-performing. Our finding in this study is consistent with those of Mwafag (Citation2015) and provide evidence that a high liquidity ratio negatively affects bank lending, by reducing the proportion of the credit facilities granted by the commercial banks. The real GDP, which is utilised as a proxy for the effect of economic conditions on bank credit to the private sector, is positive and statistically significant at 1%. Therefore, a billion increase in real GDP led to an increase in bank credit to private sector in the period 2000 to 2017. This is consistent with Olorunmade et al. (Citation2019) demonstrating a significant positive relationship between private sector credit and economic growth. The results are consistent with studies by Malede (Citation2014), who found a positive relationship between bank credit and real GDP. The error term indicates that deviations from the long-run equilibrium are corrected for with a speed of 34.2% in the current month. This also confirms that bank credit values are determined inside the model.

Since the reported results show that all three monetary policy instruments (discount rate, reserve requirement and liquidity requirement) have a negative effect on bank lending to the private sector, we proceed to determine their optimal thresholds. The purpose is not to guide monetary authorities on the range to aim at when setting credit regulation instruments in order to stimulate economic growth and encourage investment in the Kingdom of Eswatini. Before determining the thresholds for the three variable of concerns, a residual test was conducted.

5.4. Diagnostic Checks analysis

In line with Hasan and Nasir (Citation2008), residual tests were conducted to ascertain the risk of serial correlation, heteroskedasticity and non-normality distribution. The most important aspect in these cases is that residual diagnostics should be free from heteroskedasticity and serial correlation. The results rfor the trace test are provided in . provides a summary of the normalized long run VECM estimates and the Error Correction Terms.

Table 4. Unrestricted Cointegration Rank Test (Trace)

Table 5. Normalized long—run VECM estimates and the Error Correction Terms

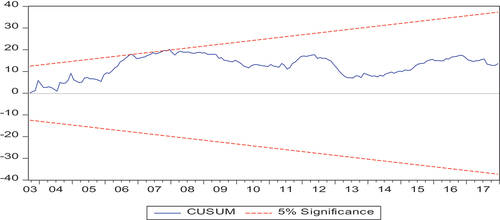

It is obvious from Table that the resultant p-value for the serial correlation test is 8%, which is greater than 5% significance level. This indicates that the model is free from serial correlation. Likewise, the corresponding Chi-square p-value for the Breusch-Godfrey heteroskedasticity test is 51%, (above 5%) which indicates that there is no risk of heteroscedasticity. The Jarque-Bera test for autocorrelation shows that the p-value is 62% while the Kurtosis is 2.28. Both values indicate that the data is normally distributed. Further, our residual stability tests below confirm residuals stability overtime in Figure , since the residual lines largely fall within the CUSUM bounds at the 5% significance level.

Figure 4. Cumulative sum of recursive residuals (CUSUM).

Table 6. Residual tests result

5.5. Threshold Determination

The determination of optimal monetary mix for the three variables of concern is based on the hypothesis that the current levels of the monetary policy instruments are not optimal to influence bank lending to the private sector which is key for investment and economic growth, against an alternative hypothesis that they are optimal to positively influence bank lending to the private sector in the Kingdom of Eswatini. Holding all other factors constant, a shock was applied on each variables of concern, respectively, to obtain the optimal thresholds, based on:

to attain

.

Table show the optimal threshold results of the variables of concern:

Table 7. Threshold Results Dependent variable: LBCRP

The null hypothesis cannot be rejected that the monetary policy instruments are not optimal. The optimal thresholds/Central Bank Eswatini lending system policy mix for bank credit to private sector are: 5.42% for the discount rate, 4.03% for the reserve requirement and 12.48% for the liquidity requirement. Any increase above these thresholds would negatively affect bank lending to the private sector in the Kingdom of Eswatini.

6. Conclusions, policy implications, and recommendations

The findings of this study indicate that only the discount rate among the variables of concern is significant. The Johansen cointegration approach, Vector Error Correction Model and the Quadratic model were used to analyse monthly data from 2000 to 2017. The results provide evidence that the discount rate, reserve requirement and liquidity requirement bear a significant negative relationship with bank credit to the private sector in the Kingdom of Eswatini. The results also show that there is a significant positive influence of an increase in real GDP (LRGDP) on bank credit to the private sector. This finding is consistent with Meltzer (2003), Olokoyo (Citation2011), Yakubu et al. (Citation2018), Ajayi and Atanda (Citation2012), Malede (Citation2014), Malede (Citation2014), and Mwafag (Citation2015) and Dlamini and Skosana (2016). However, our findings in terms of the reserve requirement are contrary to those of Olusanya et al. (Citation2012) who found a positive relationship between bank credit and the reserve requirement. The error term indicates that deviations from the long-run equilibrium are corrected for with a speed of 34.2% in the current month. This also confirms that bank credit values are determined inside the model.

Using the Quadratic model, this study also uncovered that the current thresholds of the variables of concern are not optimal. The optimal thresholds for the Central Bank lending system (policy mix) are: 5.42% for the discount rate, 4.03% for the reserve requirement, 12.48% for the liquidity requirement. Any point above these thresholds will have a negative effect on bank lending to the private sector. Overall, these findings confirm with the bank lending of monetary policy transmission. According to Mishkin (Citation1996) to be successful in influencing the economy through monetary policy, the Central Bank should understand the mechanism and extent through which monetary policy affects the economy.

The first policy implication of the Johansen cointegration and VECM reported result is that, since the discount rate, reserve requirement and liquidity requirement coefficients are statistically significant and negative, the Central Bank of Eswatini should strike a balance between inflation controls and strategies to stimulate bank credit to the private sector which is essential to encourage investment and to foster economic growth. Specifically, the Central Bank of Eswatini should take into account the existence of trade-off in policy results when controlling inflation. Second, since the current levels of three variables of concern (discount rate, reserve requirement and liquidity requirement) are not optimal to positively influence bank credit to the private sector, there is a need to consider the optimal thresholds for the three instruments. This study recommends that an optimal monetary policy stance for the discount rate, cash reserve requirement, and liquidity requirement should be premised on forward-looking guidance anchored on economic growth and inflation expectations. Therefore, in setting the discount rate, cash reserve requirement, and liquidity requirement the Central Bank of Eswatini should take into account the existence of trade-off in policy results. This study recommends that the Central Bank of Eswatini should consider a policy mix of 5.42% for the discount rate, 4.03% for the reserve requirement, 12.48% for the liquidity requirement to stimulate bank credit to the private sector. These thresholds will allow Central Bank of Eswatini to maintain inflation within reasonable levels, encourage investment and stimulate economic growth.

Additional Information. AQ1 and AQ2: Graduate School of Business and Leadership, College of Law and Management Studies, University of KwaZulu-Natal, Westville Campus, Durban, South Africa

Additional References:

Assefa, M. (2014). Determinants of growth in bank credit to the private sector in Ethiopia: A supply side approach, Research Journal of Finance and Accounting, 5(17), 90 - 102.

Bernanke, B. S., & Gertler, M. (1995). Inside the Black Box: The Credit Channel of Monetary Policy Transmission. Journal of Economic Perspectives 9(4):1-38.

Bondzie, E. A., Fosu, G. O., & Asare, O. G. (2014). Does Foreign Direct Investment really affect Ghana’s Economic Growth? International Journal of Academic Research in Economics and Management Sciences, 3(1), 148-158

Chakraborty, C., & Basu, P. (2002). Foreign direct investment and growth in India: a cointegration approach, Applied Economics, 2002, 34(9), 1061-1073. DOI: 10.1080/00036840110074079

Chaudhry, I.S., Farooq R., & Murtaza, G. (2015). Monetary policy and its inflationary pressure in Pakistan. Pakistan Economic and Social Review, 53(2), 251-268.

Gujarati, D. N. (2003). Basic Econometrics, Gary Burke, New York.

Khan, M.S, & Senhadji, A.S. (2001). Threshold Effects in the Relationship Between Inflation and Growth, International Monetary Fund Staff Papers Series No. 00/110, International Monetary Fund, 48(110), 1-1.

Malede, M. (2014). Determinants of Commercial Banks’ Lending: Evidence from Ethiopian Commercial Banks. European Journal of Business and Management, 6(20).

MacKinnon, J.G., Haug, A.A., & Michelis, L. (1999). Numerical Distribution Functions of Likelihood Ratio Tests for Cointegration. Journal of Applied Econometrics, 14, 563-577. http://dx.doi.org/10.1002/(SICI)1099-1255(199909/10)14:5<563::AID-JAE530>3.0.CO;2-R

Meltzer, A. H. (2003). A History of the Federal Reserve, ''Bank Financial History Review, 13(1), 123– 134. Chicago.

Vargas, H., & Cardozo, P. (2012). The Use of Reserve Requirements in an Optimal Monetary Policy Framework, BancoDe La Republica Colombia Working Paper No. 7161/2012. Banco de la Republica de Colombia.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Samuel Nkosinathi Dlamini

Samuel Nkosinathi Dlamini is a Senior Macroeconomic Convergence Officer at SADC Head Quarters. Before joining the SADC, he was a Chief Economist at Eswatini Competition Commission and had worked at the Central Bank of Eswatini. He holds a Masters’ Degree in Financial Markets from Rhodes University, South Africa. Currently he is doing a PhD. in Business Administration at the Graduate School of Business and Leadership, University of KwaZulu-Natal, South Africa.

Dr Pfano Mashau

Dr Pfano Mashau is a Senior Lecturer at the University of KwaZulu-Natal, Graduate School ofBusiness and Leadership. He holds a PhD in Management. He lectures postgraduate classes. His research focus is on Small Business Development, Innovation, Business Management, Entrepreneurship and Agglomeration Economies. Prior to working as an academic, he worked for JET Education Services, and Bio Regional businesses. Dr Mashau has published over 20 research articles and supervised research studies at Honours, Masters and Doctoral level.

Notes

1. Keynes theory.

References

- Ajayi, F. O., & Atanda, A. A. (2012). Monetary policy and bank performance in Nigeria: A two-step co-integration approach. African Journal of Scientific Research, 9(1), 462–20. https://fliphtml5.com/ygov/nces/basic/

- Alfon, I., Argimon, I., & Bascunana-Ambros, P. (2004). What determines how much capital is held by UK banks and building societies. FSA Occasional Papers, (22). https://www.researchgate.net/publication/248419253_What_determines_how_much_capital_is_held_by_UK_banks_and_building_societies/link/53f1ac250cf26b9b7dd0e154/download

- Amidu, M. (2006). The link between monetary policy and banks’ lending behavior: The Ghanaian case. Banks and Bank Systems, 1(4), 38–47. https://www.businessperspectives.org/images/pdf/applications/publishing/templates/article/assets/1593/BBS_en_2006_04_Amidu.pdf

- Aziakpono, M. J. (2006). Financial integration amongst the SACU countries: Evidence from interest rate pass-through analysis. https://doi.org/10.1080/10800379.2006.12106405

- Bernanke, B. S., & Gertler, M. (1995). Inside the black box: The credit channel of monetary policy transmission. Journal of Economic Perspectives, 9(4), 1–38. https://doi.org/10.1257/jep.9.4.27

- Calza, A., Gartner, C., & Sousa, J. (2001a). Modelling the demand for loans to private sector in euro area. Journal of Applied Economics, 35(1), 107–117. https://doi.org/10.1080/00036840210161837

- Central Bank of Eswatini. (2015). Central Bank of Eswatini annual report. Central Bank of Eswatini, 1(1), 1–36.

- Disyatat, P. (2010). Inflation targeting, asset prices, and financial imbalances: Contextualizing the debate. Journal of Financial Stability (Forthcoming), 6(3), 145–155. https://doi.org/10.1016/j.jfs.2009.05.003

- Dlamini, S. N. (2008). Bank credit extension to the private sector and Inflation in South Africa. Masters Thesis. Rhodes University.

- Dlamini, B., & Skosana, S. (2017). Relationship and causality between interest rates and macroeconomic variables in Swaziland. Central Bank of Eswatini Research Bulletin, 1.

- Eita, J. H. (2012). Explaining Interest Rate Spread in Namibia. International Business & Economics Research Journal, 11(10), 1123–1132. https://doi.org/10.19030/jabr.v28i5.7230

- Gambacorta, L., & Rossi. (2007). Modelling bank lending in the Euro area: A non-linear approach. https://doi.org/10.1080/09603101003781430

- Hasan, A., & Nasir, Z. M. (2008). Macroeconomic factors and equity prices: An empirical investigation by using ARDL approach. Pakistan development review, 47(4), 501–513. https://www.researchgate.net/publication/46532471_Macroeconomic_Factors_and_Equity_Prices_An_Empirical_Investigation_by_Using_ARDL_Approach

- Hofmann, B. (2001). The determinants of private sector credit in industrialised countries: Do property prices matter? Bank for International Settlements, No. 108.

- Hurlin, C., & Kierzenkowski, R. (2002). A theoretical and empirical assessment of the bank lending channel and loan market disequilibrium in Poland. Working Paper 22, May 2002, National Bank of Poland, Research Department.

- Imran, K., & Nishatm, M. (2013). Determinants of Bank Credit in Pakistan: A Supply Side Approach. Economic Modelling, 35, 384–390. http://dx.doi.org/10.1016/j.econmod.2013.07.022

- International Monetary Fund. (2017). Kingdom of Swaziland 2017 article IV report. Kingdom of Swaziland. https://www.imf.org/en/Publications/CR/Issues/2017/09/11/Kingdom-of-Swaziland-2017-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-45240

- Karim, Z. A., Azman-Saini, W. N. W., & Karim, B. A. (2011). Bank lending channel of monetary policy: Dynamic panel data study of Malaysia. Journal of Asia-Pacific Business, 12(3), 225–243. https://doi.org/10.1080/10599231.2011.570618

- Kashyap, A., & Stein, J. (1995). The impact of monetary policy on bank balance sheets. Carnegie Rochester Conference Series on Public Policy 42:151–195.

- Katusiime, L. (2018). Private Sector Credit and Inflation Volatility. Economies, 6(2), 28. https://doi.org/10.3390/economies6020028

- Malede, M. (2014). Determinants of commercial banks’ lending: Evidence from Ethiopian commercial banks. European Journal of Business and Management, 2222–1905.

- Manyok, A. J. (2016). Effects of exchange rate fluctuations on financial performance of commercial banks in South Sudan. Masters Thesis University of Nairobi.

- Mehrara, M., & Karsalari, A. R. (2011). The nonlinear relationship between private investment and real interest rates based on dynamic threshold panel: The case of developing countries. Journal of Money, Investment and Banking, 1(21), 32–42.

- Mishkin, F. (1996). The channels of monetary transmission: Lessons for monetary policy. Banque de FranceUniversite Conference. National Bureau of Economic Research.

- Mishkin, F. (2001). The transmission mechanism and the role of asset prices in monetary policy. NBER Working Paper, 2001(8617). http://www.nber.org/papers/w8617

- Mwafag, R. (2015). Factors Affecting the Bank Credit: An empirical study on the Jordanian commercial banks. International Journal of Economics and Finance, 7(5), 166–178. https://doi.org/10.5539/ijef.v7n5p166

- Olade, S. O. (2015 January). Determination of an optimal threshold for the Central Bank of Nigeria’s monetary policy rate. In Central bank of Nigeria working paper series (pp. 1-27). Monetary Department, Central Bank of Nigeria.

- Olokoyo, F. O. (2011). Determinants of commercial banks’ lending behavior in Nigeria. International Journal of Financial Research, 2(2), 61–62. https://doi.org/10.5430/ijfr.v2n2p61

- Olorunmade, G., Samuel, O. J., & Adewole, J. A. (2019) Determinant of private sector credit and its implication on economic growth in Nigeria: 2000-2017. American Economic and Social Review, 5. https://doi.org/10.46281/aesr.v5i1.242

- Olusanya, S., Oyebo, A., & Ohadebere, E. (2012). Determinants of lending behaviour of commercial banks: Evidence from Nigeria, A Co-integration analysis (1975 to 2010). Journal of Humanities and Social Science, 5(5), 71–80. https://doi.org/10.9790/0837-0557180

- Olweny, T., & Chiluwe, M. (2012). The effect of monetary policy on private sector investment in Kenya. Journal of Applied Finance and Banking, 2(2), 239–287. https://www.scienpress.com/journal_focus.asp?Main_Id=56

- Poole, W., & Wheelock, D. C. (2008). Stable prices, stable economy: Keeping inflation in check must be No. 1 goal of monetary policymakers. Federal Reserve Bank of St. Louis. https://www.stlouisfed.org/publications/regional-economist/january-2008/stable-prices-stable-economy-keeping-inflation-in-check-must-be-no-1-goal-of-monetary-policymakers

- Sharma, P., & Gounder, N. (2012). Determinants of bank credit in small open economies: The case of six Pacific Island Countries. Discussion Paper Finance, Griffith Business School, Griffith University, No. 2012-13. https://pdfs.semanticscholar.org/8ab5/aaab02b3b2ff43f67ea15864dad913cdd01c.pdf .

- Tule, M. K. 1., Audu, I., Oji, O. K., Oboh, V. U., Imam, S. Z., & Ajay, K. J. (2015). Determination of an optimal threshold for the central bank of Nigeria’s monetary policy rate. Central Bank of Nigeria. https://www.cbn.gov.ng/out/2015/ccd/strategies%20for%20lowering%20banks%20cost%20of%20funds%20in%20nigeria%202%20do.pdf

- Vargas, H., & Cardozo, P. (2012). The Use of Reserve Requirements in an Optimal Monetary Policy Framework, BancoDe La Republica Colombia Working Paper, No. 7161-2012.

- Walsh, C. E. (2003). Monetary theory and monetary policy (Second) ed.). MIT Press.

- Yakubu, J., Omosola, A. A., & Obiezue, T. O. (2018). Determinants of Bank lending Behaviour in Nigeria. An Empirical Investigation Economic and Financial Review, 56(4) Central Bank of Nigeria. Accessed, 15 December 2018 https://www.cbn.gov.ng/Out/2019/RSD/EFR%20Volume%2056%20No%204%20December%202018%20-%20Upload.pdf

- Younus, S., & Akhteruzzaman, M. (2012). ‘Estimating growth-inflation trade-off threshold in Bangladesh, thoughts on banking and finance. Bangladesh Bank Training Academy, 1(1).