Abstract

As part of Governments of Ghana efforts to deal with misappropriation of public sector resources, the Internal Audit Agency Act, 2003 (Act 658) was established to ensure probity, accountability, and transparency in the management of public sector resources, yet there is a high Corruption Perception Index in Ghana as asserted by the Transparent International 2021 release. To address this concern, our paper is aimed to develop a new model to explain the extent to which internal audit effectiveness (IAE) could be used to build strong organizational resilience as a mechanism through which efficiency in public procurement could be achieved while reducing public sector corruption incidence. Data have been collected from a cross-section of public sector workers. The structural equation modeling approach has been used to analyze the survey data. Our results have shown that cultural, and strategic resilience dimensions of organizational resilience significantly mediate the relationship between IAE and procurement performance. These results have implications for re-enforcement of audit regulations to ensure transparency in managing public sector resources with a focus on reducing negative public sector corruption perception.

PUBLIC INTEREST STATEMENT

This paper argues that in the midst of other priorities the Governments of Ghana have upscaled measures to deal with misappropriation of public sector resources. The Internal Audit Agency Act, 2003 (Act 658) was established to ensure probity, accountability, and transparency in the management of public sector resources, yet there is a high Corruption Perception Index in Ghana as asserted by the Transparent International 2021 release. This paper investigates the extent to which IAE could be used to build strong organizational resilience as a mechanism through which efficiency in public procurement could be achieved. The study has discovered that contextual variables such as internal audit independence, internal audit staff competency, and top management support for internal audit functions are significant contributors towards internal audit effectiveness. Again, these variables work together to ensure organizational resilience which drive procurement best practices and enhance overall public procurement performance. Moreover, the study re-enforces internal audit regulations (Act, 2003, (Act 658) to eenhance transparency, accountability and probity in managing public sector resources.

1. Introduction

The United Nations (UN) 2030 Agenda for Sustainable Development has necessitated urgent need to reenforce strong institutions, Peace, and Justice as established in the SDG 16 as part of the global wider efforts to deal with corruption incidence which is consistent with the Governments of Ghana efforts to deal with misappropriation of public sector resources. The Internal Audit Agency Act, 2003 (Act 658) in Ghana for instance, was established to ensure probity, accountability, and transparency in the management of public sector resources, yet there is a high Corruption Perception Index in Ghana as asserted by the Transparent International 2021 release (Appiah et al., Citation2022). Apparently, the rate of corruption among Public Officials in Africa partly accounts for the weak and slow economic, social, and political development in the continent. It has detrimental effects on good governance, economic growth and ultimately basic freedoms which include but not limited to citizens right to hold governments accountable or freedom of speech. The central proposition of this paper is that there is a symbiotic relationship between internal audit, organizational resilience and public procurement performance which has not been adequately explored in the wave of high corruption perception (Appiah et al., Citation2022; Changalima et al., Citation2022; Hazaea et al., Citation2021; Huy et al., Citation2020).

Our paper is interested to establish the roles of internal audit effectiveness (IAE), and organizational resilience on public procurement efficiency in order to reduce the menace of financial profligacy and opulence among public officials (Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022; Kannan, Citation2021). Thus, effective procurement combines planned and actual procurement resources to achieve planned goals and objectives (Barbanti et al., Citation2022; Chesseto et al., Citation2019; Kiage, Citation2013). According to the Institute of Internal Auditors (IIA) internal audit is an independent and objective audit and advisory service designed to add value to an organization’s operations, management, risk management and internal control (Institute of Internal Auditors, Citation2016). Internal audit controls work by analyzing and evaluating the scope and capability of other controls to reach its conclusion. Internal audit equips organizations with investigations, proposals, data, and reconciliations related to the audited activity (Lenz et al., Citation2014; Roussy et al., Citation2020). Generically, the audit regulation is aimed to ensure that auditors comply with good practice standards and that they are competent and independent when conducting audits. All of these elements are considered important to auditors’ ability to detect and report material misstatements in financial information (Kannan, Citation2021; Roussy et al., Citation2020). Relatedly, Quaye (Citation2019) averred that for internal audit to be effective, it must clearly define its objectives and achieve them. Accordingly, Tackie et al. (Citation2016) argued that IAE is usually measured by the end result or output of the internal audit. Audit measures are the first reinforcement of the basic pillars of accountability, as they enable the monitoring and control of public institutions. Thus, audits reinforce confidence in the democratic system, prevent corruption and abuse of power, improve the functioning, efficiency, responsiveness and learning capacity of organizations and, ultimately, increase the legitimacy of boards of directors (Dzikrullah et al., Citation2020; Harris, Citation2014; Josh & Karyawati, Citation2022).

This paper aims to develop a new model to explain the extent to which IAE could be used to build strong organizational resilience as a mechanism through which efficiency in public procurement could be achieved while reducing public sector corruption incidence. Evidence from extant literature suggests that public institutions are often subject to control systems designed to ensure accountability and limit the power of boards of directors. These systems include controls that can be performed by individuals inside or outside the controlled entities (Fonseca et al., Citation2020; Khalid & Sarea, Citation2020). The role of internal audit has been linked to efficiency in public procurement. In his seminal work Kheir (Citation2018) evaluated the contribution of internal audit to the procurement of goods and services in public organizations, and reported that internal audit gives an average score of 56 percent for policies and procedures that provide clear guidance to the procurement department. Besides, IAE is vital in assessing and managing risks in the purchasing department. Moreover, Thumbi and Mutiso (Citation2018) found that in most cases, procurement process reviews include both compliance and performance reviews. The compliance criteria against which the procedure is assessed are based on the applicable legal framework in the specific context of the Public Procurement Act. The procurement process must be designed to maximize competition in public procurement and ensure value for money.

This paper contributes immensely to exiting knowledge stocks different ways. The first contribution of this paper is that it is among the very few (Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022; Kannan, Citation2021) to develop a new research model to explain how IAE is linked through organizational reliance mechanisms in order to attain efficiency in public procurement practices. The new model has disintegrated organizational resilience into cultural, strategic and relationship. We have separately tested how each of these sub-dimensions of organizational resilience is able to mediate the relationship between IAE and procurement performance. Secondly, our paper contributes to contextual variables development and their effects on procurement performance. For instance, the extent to which contextual factors such as IAE, cultural resilience, strategic resilience and relationship resilience directly affect public procurement performance. As evident in extant literature (Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022; Kannan, Citation2021; Khalid & Sarea, Citation2020; Al Nuaimi et al., Citation2020), the focus has always been on determinants of IAE. Our paper extends beyond IAE with new evidence from developing economy context. Thirdly, our paper presents immense theoretical contribution. Our new model has been developed by integrating agency theory and institutional theory for form new synergy which offer robust predictability in predicting public procurement performance using a structural equation modeling (SEM) approach with consistent and high reliability. The following specific objectives have been formulated to guide the study:

To examine the extent to which each dimension of organizational resilience (cultural resilience, strategic resilience, relationship resilience) mediates the relationship between IAE and public procurement performance.

To examine the direct relationships between organizational resilience (cultural resilience, strategic resilience, relationship resilience) and public procurement performance.

To examine the relationships between IAE and public procurement performance.

The rest of our paper is divided into the following sections: The section 2, presents review of literature, the section 3 presents research methodology, the section 4, presents results and discussions, the final section presents conclusions and implications of the study.

2. Literature review

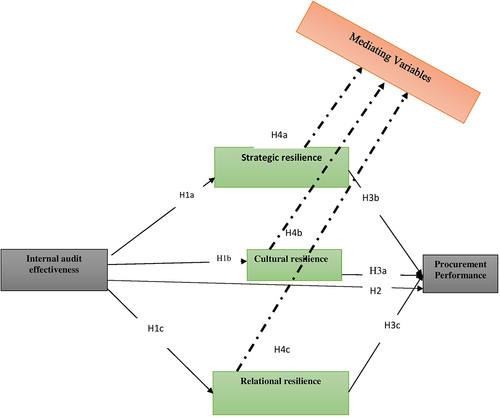

The underpinning theories for the current study comprise Agency theory and institution theory. Agency theory has been widely used to explain and predict the performance of internal auditors in most accounting literature. This theory stipulates that there is a relationship between agents and principals in ensuring public procurement effectiveness and efficiency. The agent are the technocrats (internal auditors) while government of Ghana and the procurement regulators serve as principal. The principals set the rules and then agent enforces these rules. In nut shell, for public procurement to be effective, there is the need for both the agent and principal to work on equal harmony (Mitnick, Citation2013). Relatedly, DiMaggio and Powell(Citation1983) have argued that institutional theory explains and predict observable behaviors of organization conforming to ever-increasing pressures. This theory fundamentally argues that there are support and regulations that work together to enhance public sector performance. For instance, the Public Procurement Act as well as the Internal Audit Act are parts of the Ghana’s public sector regulations to ensure accountability, probity and transparent in the use of public sector resources. Previous studies (Appiah et al., Citation2022; Kabuye et al., Citation2019; Rahayu & Rahayu, Citation2020; Sofyani et al., Citation2020; Tran et al., Citation2020; Tumwebaze et al., Citation2018) have argued that internal audit and procurement performance are linked. For instance, Jembe and Wandera (Citation2019) found that accountability in procurement has a significant impact on procurement performance, especially in procurement, with the right skills to address all critical and emerging procurement issues in terms of proper procurement plans and working in accordance with the law as a guide for all procurement activities. Moreover, David (Citation2019) revealed that that internal audit skills, procedures and independence have a positive impact on the contribution of internal audit to the performance of procurement functions in local government. Again, this paper argues from the perspectives of agency theory, and institutional theory frameworks. While the agency management theory is applied in the context that the agent or manager, i.e., the internal auditor, must be reliable and competent to protect the client’s resources, the institutional theory postulates the needs to comply with standards of audit regulations while controlling financial behavior of public officers relating to procurement of goods, services and public works, whether in parts or full. We argue that the synergy of these theories could better explain the relationships between IAE, organizational resilience and procurement as indicated in Figure . IAE is used in this paper refers to the extent to which public organizations are able to work independently through objective assurance and consulting in order to add value and enhance public sector operational effectiveness. Organizational resilience refers to the ability of public organization to proactively and reactively address uncertainties affecting its operations whiles procurement performance as used in this paper refers to the ability of the public organizations to effectively and efficiently procure goods, services and works without violating value for money requirements (Appiah et al., Citation2022; Kabuye et al., Citation2019; Sofyani et al., Citation2020).

Figure 1. Research framework.

2.0.1. Relationships between IAE, organizational resilience and public procurement performance

The first assumption of the paper is that IAE relates to organizational reliance in the context of public sector. The second assumption of the paper is that IAE relates to public procurement performance. Internal auditing is considered an important tool for controlling an organization’s management and performance (IIA, Citation2010). Initially, internal audit focused on compliance, financial management and asset protection (Dellai et al., Citation2016). In recent years, the areas in which internal audit is applied have expanded and increased in value. The IIA has asserted that internal audit is an independent and objective assurance and advisory activity designed to add value and improve the performance of an organization. It helps organizations achieve their objectives by providing a systematic and disciplined approach to assessing and improving the effectiveness of risk management, control and governance processes (IIA, Citation2017). According to Mihret (), the IAE consists of several elements, including ensuring that management procedures are adequate to identify and monitor observable risks and that the internal control systems in place are operating effectively. It also includes a robust process for communicating risks and assurances to management and an objective assurance that management receives sufficient quality assurance and reliable information from the board (Badara & Saidin, Citation2013; Dittenhofer, Citation2011; Maribe, Citation2010). Besides, Ljubisavljević and Jovanovi (Citation2011) conclude that internal audit is successful when it adds value to the organization’s internal control and risk management processes. The effectiveness of internal audit goes a long way to develop resilience against risk, uncertainty, mismanagement and embezzlement of public funds whiles improving organizational efficiency and effectiveness. In the light of the discussions herein, the paper hypothesizes as follow:

H1a-c: IAE has positive and significant effect on organizational resilience dimensions.

H2: IAE has positive and significant effect on public procurement performance.

2.0.2. Organizational resilience and public procurement performance

The third assumption of the paper stems from the argument that a resilience organization can readily become effective and efficient. The concept of resilience has emerged in various contexts and emphasizes the need to improve a system’s ability to continue functioning in the face of disruptive events, such as internal and external fluctuations, changes, disruptions, and surprises (Hollnagel et al., Citation2007; Lay et al., Citation2015; Lee et al., Citation2013). Organizational resilience entails a dynamic structure of an organization, encompassing both typological and quantitative aspects and including processes such as reintegration, identity management, communication networks, emotional labor, and adaptation through improvisation (Ishak & Williams, Citation2018). Again, Kendra and Wachtendorf (Citation2003) argued that organizations become resilient through preparedness, suggesting that preparedness is not related to specific events but develops the skills and activities needed to cope with a range of unexpected events. More recently, Somers (Citation2009) has argued that “resilience is not just about survival, but about identifying potential risks and taking precautions so that organisations can thrive even in the face of failure”. The term “resilience” refers to the ability of a system, such as an ecosystem, economy, society or organisation, to return to its normal state after a disruptive event that changes its state (Annarelli & Nonino, Citation2016; Olsson et al., Citation2015; Pal et al., Citation2014). In addition, some researchers (Linnenluecke, Citation2017; McManus et al., Citation2008; Mumby & Bozec, Citation2014; Somers, Citation2009) have argued that organizational resilience include anticipating and avoiding potential threats before they occur, which is contrary to the definition of resilience as “the ability to learn to manage and recover from unexpected threats. It is very clear from the ongoing presentation that public organizations with strong institutional resilience are most likely to performance better in terms of managing procurement activities. The study therefore hypothesizes as follows:

H3a-c: Organizational resilience dimensions have significant and positive effect on procurement performance

H4a-c: Organizational resilience dimensions have significant mediating effects on the relationship between IEA and procurement performance

3. Research methodology

3.1. Setting of the study

This paper is limited to public sector of Ghana which comprises government-controlled enterprises of all levels, e.g., districts, regions. This sector excludes voluntary organizations and private corporations. The sector is the main provider of main social and other amenities in the country such as educational facilities, health facilities, road systems, sport facilities among others. Specifically, this paper centered on public agencies in Kumasi and Accra Metropolitan areas. These two Metropolitan Areas are the largest in Ghana interns of population, public administration, and commerce activities. Prior researchers have argued that over seventy percent of total Government budget is spent on procurement of goods, services and public works. As a result, public procurement and IAE are very much intense in these metropolitan areas. For these reasons it has been appropriate to investigate the relationship between IAE, organizational resilience and public procurement performance within the aforementioned settings.

3.2. Research design

This study is anchored on the objectivist research paradigm, the positivist ontology, and quantitative research methodology. Quantitative research approach has been employed to examine the relationship between IAE, organizational resilience and public procurement performance, because it is based on mathematical, statistical or computer methods to examine measurable or quantifiable data. Besides, quantitative research has been used to generalize the phenomenon or opinion being studied. Besides, survey strategy has been used, which involve collection of opinions and perceptions from representatives of the target population after which inferences could be made to the large population where the samples were drawn. Survey design was used due to its cost effective, large sample size, and generality of findings.

3.3. Population and sampling procedures

The main population of the study comprises government-controlled enterprises of all levels e.g., districts, regionals, and national levels within the Kumasi and Accra Metropolitan Areas. The target population of the study comprises public procurement officers, inventory managers, public accountants, public finance officers, designated internal and external auditors. The sample size for the study has been chosen following rule of ten principles. This rule postulates that the number of paths which have been directed towards a latent variable in SEM is multiple by ten (10) to determine the minimum sample requirements. As should in Figure the total number of paths directed towards a latent variable is 10. Therefore, (10*10 = 100). Given the minimum required sample size as 100, the paper sampled 200 participants and obtained 67.5 response rate. The participants in this paper have been selected by probability sampling. Using probability sampling, each person has the same chance of being selected from a population. The aim is to find samples that broadly represent the characteristics of the population. Random sampling procedure has followed to select the participants because it’s very effective when it comes to reducing sampling error and ensuring representativeness.

3.4. Constructs measurement and data collection instrument

All the measurement scales for the study have been adopted from previous studies. For instance, organizational resilience scale was adopted from Chowdhury and Quaddus (Citation2017), procurement performance scale was adopted from Nyamai and Ismail (Citation2018), finally IAE scale was adopted from Mihret (). Survey questionnaire has been the main data collection instrument used in this study. The survey data are data collected from a sample of respondents from a large population. The effectiveness of the survey design has been determined by factors related to the data collection in the survey, such as the method of contact between the interviewer and the respondent (offline), the way the information has been communicated to the respondents, etc. A face-to-face survey has been used in this study. Collecting information from respondents in face-to-face meetings is much more effective than other means of communication, as respondents tend to trust the interviewers and tend to give honest and clear answers about the topic. The survey has been conducted in among public officials. The participants responses have been rated on a five-point scale (strongly disagree = 1 and strongly agree = 5). Previous researchers have argued that the 5-point Likert type scale is very effective. The participants were requested to select from the scales the relevant statements related to IAE, organizational resilience and public procurement performance.

3.5. Data analysis and scale validations

Smart Partial Least Square version 3.3.1 has been used to analyze the data. Specifically, variance- based SEM strategy has been used. The PLS-SEM describes a flow chart for evaluating the measurement model (external model). It includes the evaluation of structural (internal) models such as convergent validity test, discriminant validity test (cross validity), average variance extracted (AVE) validity test, composite reliability test, R-square (value) test, cross validity test and hypotheses test. The conceptual model describes the relationship between the predictor variables. Mediation occurs when there is a third mediating factor between two other related constructs. In other words, changes in the exogenous construct leads to changes in the mediating variable, which in turn leads to changes in the endogenous construct. The mediating factor thus determines the nature of the relationship between the two components (i.e., the underlying mechanism or process). The causal mechanism between exogenous and endogenous constructs can be explained by analyzing the strength of the relationship between the mediating variable and other constructs. In Smart-PLS, the results of the PLS-SEM algorithm and bootstrap procedure include the direct effect, total indirect effect, specific indirect effects, and total effect. These results, which are available in the Smart-PLS results summaries, allow for mediator analysis (e.g., as suggested in Hair et al., Citation2017). It should be noted that Smart-PLS results allow for the analysis of models with single or multiple mediators (i.e., parallel or sequential mediation). In this paper multiple mediation analyses have been conducted. The mediating effect is based on the following three conditions:

(a) full mediation (indirect effect only);

(b) partial mediation (both direct and indirect effects);

(c) no intermediation (no indirect effect).

3.6. Ethical considerations

Since the paper requires participation of human subjects, some ethical considerations were made. Before the start of the survey each participant was given the consent letter. All those who accepted to participate in the study were guaranteed the following: Voluntary participation, protection from harm, respect for human right, anonymity and confidentiality of participants. These considerations have been made throughout study.

4. Results and discussions

4.1. Descriptive statistics—composite means and composite standard deviation and normality test

The composite means, composite standard deviations, and normality test using skewness and Kurtosis have been presented in the Table . The results have shown that cultural resilience as a sub-dimension of organizational resilience had the highest composite mean score of 4.175 with a corresponding composite standard deviation score of 0.837, procurement performance had the second highest composite mean score of 4.056 with a corresponding composite standard deviation score of 0.832. IAE had the third highest composite mean score of 3.939 with a corresponding composite standard deviation of 0.935. strategic resilience had least composite mean score of 3.63 with a corresponding standard deviation score of 1.080. These results imply that there is an inverse relationship between the composite mean values and the composite standard deviations values. As seen in the Table , the composite mean scores decrease with an increasing composite standard deviation score. To assess the normality of the data distribution the values of skewness and kurtosis were assessed. According to Hair et al. (Citation2017) and Bryne (Citation2010), a set of data is considered as normal distributed if the value of skewness is between −2 to 2 and kurtosis is between −7 to 7. Skewness and kurtosis, respectively, measure symmetry and peakedness of a distribution. The results from the study have showed that both skewness and kurtosis scores are within the accepted normal distribution range. Therefore, the data are normally distributed.

Table 1. Descriptive statistics—composite means and composite standard deviation

4.2. Scale validation—convergent validity and discriminant validity

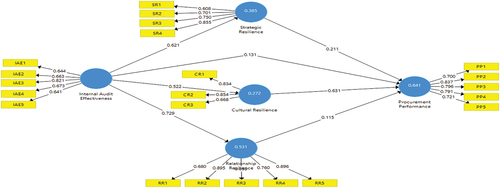

Table , presents results on scale validations focusing on discriminant validity and convergent validity. To assess the extent to which discriminant validity has been met in the model, 2 techniques have been utilized. As showed in Table , the square root of the values of AVE as showed in the diagonal have been compared with the inter-construct correlations values and the results have shown that the square root of AVEs far exceeded the correlated values (Fornell and Larcker, Citation1981). That implies that the constructs are unrelated suggesting that discriminant validity has been established. For robustness, a second assessment has been conducted as showed in the Table , using called Heterotrait-Monotrait Ratio (HTMT). This test required that for discriminant validity to be established the HTMT ratios should not exceed 0.90 (Henseler et al., 2015). The results have showed that HTMT ratio from the model ranged from 0.56 to 0.808 which is less than 0.90. Therefore, discriminant validity has been attained in the model. Besides, as showed in the Table , and Figures , the cross-loading results have shown that the factors load higher into their respective constructs as compared to other constructs further suggesting that discriminant validity has been achieved in the structural model. Conversely, convergent validity has been assessed in the model using composite reliability (CR) and Cronbach alpha (CA) values and AVE. The model to pass convergent validity test CR scores should be 0.70 or better, CA scores should be 0.70 or better, and AVE scores should be 0.50 or better. As showed in the Table , the results have showed that AVE scores ranged from 0.521 to 0.676 which suggests that the model has exceeded the minimum requirement for AVE test. Again, CA scored ranged from 0.726 to 0.828 which suggest that the model has exceeded the minimum requirement for CA test. Finally, CR scores ranged from 0.820 to 0.912 which suggest that the model has exceeded the minimum requirement for CR test. Clearly from the above, the model has far exceeded the requirement to pass convergence validity test as detailed in Table . Figure respectively show the factor loadins and path coefficients.

Figure 2. A map showing the locations of Kumasi and Accra.

Figure 3. Cross loadings and path coefficient.

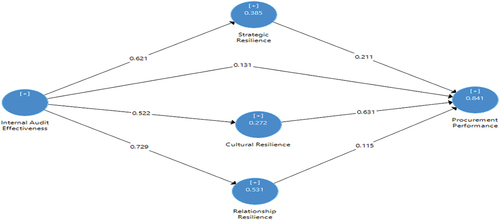

Figure 4. Structural model and hypothesized paths.

Table 2. Scale validation – discriminant validity and convergence validity

Table 3. Heterotrait-Monotrait ratio

4.3. Evaluation of the structural model

As suggested by Hair et al. (2014), there are steps to evaluate the structural model. Namely, hypotheses testing, path coefficients, coefficient of determination (R-squared), effect size (f-squared) and predictive relevance (Q-squared) and blindfolding. The steps have been described in detail below. First, the collinearity potential has been assessed for each item. As shown in Table , the values of the variance inflation factor (VIF) for all items in the structural model ranged from 1.169 to 3.499, which is below the recommended minimum threshold of 5.0 (Hair et al., 2014). Therefore, serious collinearity problem has not been demonstrated in this study.

4.4. Structural model—hypothesized paths, paths coefficients, and hypotheses testing

As showed in Table and Figure , the structural model has been assessed. Using R-squared, and T-statistics to the predictive power of the model as well as hypothesis testing have been respectively carried. The result shows that cultural resilience has significant and positive effect (Beta = 0.631, T-value = 12.226, P-value = 0.000) on procurement performance. Again, the results show that IAE has significant and positive effect (Beta = 0.522, T-value = 8.846, P-value = 0.000) on cultural resilience. Also, the result shows that IAE has significant and positive effect (Beta = 0.675, T-value = 14.431, P-value = 0.000) on procurement performance. The result similarly shows that IAE has significant and positive effect (Beta = 0.729, T-value = 22.887, P-value = 0.000) on relationship resilience. In addition, the result shows that IAE has significant and positive effect (Beta = 0.621, T-value = 15.619, P-value = 0.000) on strategic resilience. The result likewise shows that strategic resilience has significant and positive effect (Beta = 0.211, T-value = 3.015, P-value = 0.003) on procurement performance. On the contrary, the result show that relationship resilience has insignificant but positive effect (Beta = 0.115, T-value = 1.437, P-value = 0.151) on procurement performance. These results imply that IAE has significant effect on procurement performance and with the exception of relationship resilience which has insignificant effect on procurement performance, all the dimensions of organizational resilience have significant effect on procurement performance. In other words, internal audit staff competency, internal audit independence, as well as top management support for internal audit functions work together to develop fierce resilience culture. Therefore, we maintain that IEA is a driver of public firm resilience.

Table 4. Structural model

The result shows that cultural resilience significantly mediates (Beta = 0.329, T-value = 8.010, P-value = 0.000) the relationship between IAE and procurement performance. Also, the result shows that strategic resilience significantly mediates (Beta = 0.130, T-value = 2.973, P-value = 0.003), the relationship between IAE and procurement performance. Conversely, the result shows that relationship resilience insignificantly mediates (Beta = 0.084, T-value = 1.421, P-value = 0.156) the relationship between IAE and procurement performance. These results imply that although in rare cases effective internal audit practices could positively affect procurement performance. Meanwhile, our results have revealed that internal audit functions require a mechanism through which to effectiveness predict procurement performance. The study has specifically revealed that cultural resilience and strategic resilience significantly mediate the relationship between IAE and procurement performance.

4.5. Predictive relevance (Q2)

Q-squared is a measure of the predictive ability of the model. It focuses on the value of the endogenous variables of the model. The predictability of a structural model can be assessed using the Stone-Gaisser criterion. The test stipulates that as a rule of thumb the value of the endogenous variables should not be zero. That is any test score greater than zero suggests that the models have predictive relevance. As shown in Table , the predictive adequacy of the model is assessed by estimating the redundancy score, which is cross-validated using the blind folding PLS-SEM method. For Model 1, the cross-validated redundancy score for the endogenous variable (CR) is greater than zero, indicating that the model is adequate for prediction. For model 2, the cross-validated index for the endogenous variable (PP) is greater than zero, indicating that the path model has predictive validity. In the Model 3, the cross-validated index for the endogenous variable (RR) is greater than zero, indicating that the path model has predictive validity. Finally, the cross-correlation coefficient for the endogenous variable (SR) in model 4 is greater than zero, indicating that the path model has predictive validity.

Table 5. Construct cross validated redundancy

4.6. Discussion

This study was conducted to examine the extent to which each dimension of organizational resilience (cultural resilience, strategic resilience, relationship resilience) mediates the relationship between IAE and public procurement performance; examine the direct relationships between organizational resilience (cultural resilience, strategic resilience, relationship resilience) and public procurement performance, and examine the relationships between IAE and public procurement performance. The study has revealed that cultural resilience has significant and positive effect on procurement performance. Again, the results show that IAE has significant and positive effect on cultural resilience. Also, the result shows that IAE has significant and positive effect on procurement performance. The result similarly shows that IAE has significant and positive effect on relationship resilience. Previous studies (Appiah et al., Citation2022; Kabuye et al., Citation2019; Rahayu & Rahayu, Citation2020; Sofyani et al., Citation2020; Tran et al., Citation2020; Tumwebaze et al., Citation2018) have argued that internal audit and procurement performance are linked. For instance, Jembe and Wandera (Citation2019) found that accountability in procurement has a significant impact on procurement performance, especially in procurement, with the right skills to address all critical and emerging procurement issues in terms of proper procurement plans and working in accordance with the law as a guide for all procurement activities. Moreover, David (Citation2019) revealed that that internal audit skills, procedures and independence have a positive impact on the contribution of internal audit to the performance of procurement functions in local government.

In addition, the result shows that IAE has significant and positive effect on strategic resilience. The result likewise shows that strategic resilience has significant and positive effect on procurement performance. On the contrary, the result show that relationship resilience has insignificant but positive effect on procurement performance. These results imply that IAE has significant effect on procurement performance and with the exception of relationship resilience which has insignificant effect on procurement performance, all the dimensions of organizational resilience have significant effect on procurement performance. Prior studies (Barbanti et al., Citation2022; Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022; Kannan, Citation2021) have argued that IAE exerts influence on organizational resilience which could eventually lead to effective procurement practices in the context of Ghanaian public sector. In other words, internal audit staff competency, internal audit independence, as well as top management support for internal audit functions work together to develop fierce resilience culture. Therefore, we maintain that IEA is a driver of public firm resilience.

The result shows that cultural resilience significantly mediates the relationship between IAE and procurement performance. Also, the result shows that strategic resilience significantly mediates the relationship between IAE and procurement performance. Conversely, the result shows that relationship resilience insignificantly mediates the relationship between IAE and procurement performance. These results imply that although in rare cases effective internal audit practices could positively affect procurement performance. Meanwhile, our results have revealed that internal audit functions require a mechanism through which to effectiveness predict procurement performance. The study has specifically revealed that cultural resilience and strategic resilience significantly mediate the relationship between IAE and procurement performance which is consistent with prior studies (Barbanti et al., Citation2022; Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022: Kannan, Citation2021).

5. Conclusions and implications

The main purpose of this study was to develop a new model to explain the extent to which IAE could be used to build strong organizational resilience as a mechanism through which efficiency in public procurement could be achieved. The study has revealed that IAE has positive effect on organizational resilience and procurement performance. Besides, organizational resilience has positive effect on procurement performance. Also, cultural and strategic resilience dimensions of organizational resilience significantly mediate the relationship between IAE and PPP. The results expand prior works (Gaosong & Leping, Citation2021; Josh & Karyawati, Citation2022; Kannan, Citation2021) on IAE by linking it to organizational resilience, and public procurement performance in Ghana where paucity of studies has been conducted. Besides, the results tease out need to re-enforce audit regulations to ensure transparency in managing public sector resources.

Theoretically, our paper has implications on expansion of existing theories. For instance, agency theory and institutional theory have been merged to create a new research model to explain how IAE is linked through organizational reliance mechanisms in order to attain efficiency in public procurement practices to solve corruption related issues in the procurement of public related goods, and services. The new model has disintegrated organizational resilience into cultural, strategic and relationship using a SEM approach with is consistent, and has high reliability. We have separately tested how each of these sub-dimensions of organizational resilience is able to mediate the relationship between IAE and procurement performance. We have established in this paper that cultural resilience and strategic resilience are the strongest mechanisms through which IAE can be felt on public procurement best practices such as compliance with the required regulations (Appiah et al., Citation2022; Jembe & Wandera, Citation2019; Kabuye et al., Citation2019; Rahayu & Rahayu, Citation2020; Sofyani et al., Citation2020; Tran et al., Citation2020; Tumwebaze et al., Citation2018) have argued that internal audit and procurement performance are linked.

In practical and policy terms, this paper has implications on internal auditing and public procurement practices. The study has discovered that contextual variables such as internal audit independence, internal audit staff competency, and top management support for internal audit functions are significant contributors towards IAE. Again, these variables work together to ensure organizational resilience which drive procurement best practices and enhance overall public procurement performance. Moreover, our paper extends beyond IAE with new evidence from developing economy context. Besides, the results have implications on the need to re-enforce audit regulations (Act, 2003, (Act 658) to ensure transparency in managing public sector resources. This paper has a limitation which could be resolved by future studies. Future considerations should be given to internal audit role, value for money and sustainable procurement practices (Appiah et al., Citation2022; Kabuye et al., Citation2019; Tran et al., Citation2020) Moreover, the relationship between internal audit and financial sustainability reporting should also been considered in the context of developing countries. Again, comparative studies involving two or more specific sectors should be considered in the future with respect to IAE, organizational resilience and procurement performance.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Michael Karikari Appiah

Michael Karikari Appiah is a Research Consultant and Lecturer at the School of Sustainable Development, University of Environment and Sustainable Development in Ghana. Michael does research in sustainable development, energy economics, environmental economics and policy, renewable energy resources and technologies, development economics, entrepreneurship, Financial Sustainability, Management and Sociology. His current project is “Modelling SMEs Investment Strategies to Enhance Indigenous Participation in Renewable Energy Transition Industry”. Michael conceptualized the idea, developed the theoretical framework, contributions of the study, designed the data collection instruments, analyzed the data. All the contributors proofread and approved the final draft.

References

- Al Nuaimi, B. K., Khan, M., & Ajmal, M. (2020). Implementing sustainable procurement in the United Arab Emirates public sector. Journal of Public Procurement, 20(2), 97–19. https://doi.org/10.1108/JOPP-07-2019-0044

- Amaratunga, D., & Baldry, D. (2002). Moving from performance measurement to performance management. Facilities, 20(5/6), 217–223. https://doi.org/10.1108/02632770210426701

- Annarelli, A., & Nonino, F. (2016). Strategic and operational management of organizational resilience: Current state of research and future directions. Omega (United Kingdom);, 62, 1–18. https://doi.org/10.1016/j.omega.2015.08.004

- Appiah, K. M. T., Ware, N., & Kwarteng, C. (2022). Modelling the implications of internal audit effectiveness on value for money and sustainable procurement performance: An application of structural equation modeling. Cogent Business & Management, 9(1), 1–26. https://doi.org/10.1080/23311975.2022.2102127

- Badara, M. S., & Saidin, S. Z. (2013). The relationship between audit experience and internal audit effectiveness in the public sector organisations. International Journal of Academic in Accounting, Finance and Management Science, 3(3), 329–339.

- Barbanti, A. M., Anholon, R., Rampasso, I. S., Martins, V. W. B., Quelhas, O. L. G., & Leal Filho, W. (2022). Sustainable procurement practices in the supplier selection process: An exploratory study in the context of Brazilian manufacturing companies. Corporate Governance, 22(1), 114–127.

- Byrne, B. M. (2010). Structural Equation Modeling with AMOS: Basic Concepts, Applications, and Programming (2nd ed.). Routledge.

- Changalima, A. I. M., Ismail, J. I., & Ismail, I. J. (2022). Supplier development and public procurement performance: Does contract management difficulty matter? Cogent Business & Management, 9(1), 2108224. https://doi.org/10.1080/23311975.2022.2108224

- Chesseto, C. S., Gudda, P., & Mbuchi, M. (2019). Transparency and procurement performance of public universities in Kenya: The case of Moi University. International Journal of Academic Research in Business and Social Science, 9(9), 437–447.

- Chowdhury, M., & Quaddus, M. (2017). Supply chain resilience: Conceptualization and scale development using dynamic capability theory. International Journal of Production Economics, 188, 185–204. https://doi.org/10.1016/j.ijpe.2017.03.020

- David, J. I. (2019). The contribution of internal audits on the effective procurement assignments in selected local government authorities in Tanzania. Doctorate Thesis, University of Tanzania.

- Dellai, H., Ali, M., & Omri, B. (2016). Factors affecting the internal audit effectiveness in tunisian organizations. Research Journal of Finance and Accounting, 7(16), 2222–2847.

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Dittenhofer, M. (2011). Internal auditing effectiveness: An expansion of present methods. Managerial Auditing Journal, 16(8), 443–450. https://doi.org/10.1108/EUM0000000006064

- Douza, S., & Jain, K. A. (2021). Impact of internal audit quality on financial stability. Journal of Commerce and Accounting Research, 10(4), 19–30.

- Dzikrullah, D. A., Harymawan, I., Ratri, C. M., & Ntim, C. G. (2020). Internal audit functions and audit outcomes: Evidence from Indonesia. Cogent Business & Management, 7(1), 1750331. https://doi.org/10.1080/23311975.2020.1750331

- El Gharbaoui, B., & Chraibi, A. (2021). Internal audit quality and financial performance: A systematic literature review pointing to new research opportunities. Revue Inter Nationale Des Sciences de Gestion, 4(2), 794–820.

- Fonseca, A. R., Jorge, S., & Nascimento, C. (2020). The role of internal auditing in promoting accountability in higher education institutions. Journal of Public Administration, 54(2), 243–265.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.2307/3151312

- Gaosong, Q., & Leping, Y. (2021). Measurement of internal audit effectiveness: Construction of index system and Empirical analysis. Microprocessors and Microsystems, 104046. https://doi.org/10.1016/j.micpro.2021.104046

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM) (2nd) ed.). Sage Publications Inc.

- Harris, S. B. (2014). The importance of auditing and audit regulation to the capital markets PCAOB

- Hazaea, S. A., Zhu, J., Al-Matari, E. M., Senan, N. A. M., Khatib, S. F. A., & Ullah, S. (2021). Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Business & Management, 8(1), 1938351. https://doi.org/10.1080/23311975.2021.1938351

- Hollnagel, E., Woods, D. D., & Leveson, N. (2007). Resilience engineering: Concepts and precepts. Ashgate publishing, Ltd.

- Huy, Q. P., Phuc, K. V., & Ntim, C. G. (2020). The impact of public sector scorecard adoption on the effectiveness of accounting information systems towards the sustainable performance in public sector. Cogent Business & Management, 7(1), 1717718. https://doi.org/10.1080/23311975.2020.1717718

- IIA. (2010). Measuring internal audit effectiveness and efficiency.

- IIA. (2017). International standards for the professional practice of internal auditing.

- Institute of Internal Auditors. (2016). International standards for the professional practice of internal auditors.

- Ishak, A. W., & Williams, E. A. (2018). A dynamic model of organizational resilience: Adaptive and anchored approaches. Editor. Advis. Board, 23, 180–196.

- Jembe, B. K., & Wandera, J. (2019). Effect of procurement audit on the procurement performance of non-governmental organizations in Kenya. (A case study of compassion Kenya, Mombasa). The Strategic Journal of Business & Change Management, 6(2), 1207–1224.

- Josh, L. P., & Karyawati, P. G. (2022). The institutional theory on the internal audit effectiveness: The case of India.

- Kabuye, F., Bugambiro, N. A., Akugizibwe, I., Nuwasiima, S., & Naigaga, S. (2019). The influence of tone at the top management level and internal audit quality on the effectiveness of risk management practices in the financial services sector. Cogent Business & Management, 6(1), 1704609. https://doi.org/10.1080/23311975.2019.1704609

- Kannan, D. (2021). Sustainable procurement drivers for extended multi-tier context: A multi-theoretical perspective in the Danish supply chain. Transportation Research Part E: Logistics and Transportation Review, 15(1), 35–48. Elsevier, vol. 146(C). Iranian Journal of Management Studies

- Kendra, J. M., & Wachtendorf, T. (2003). Elements of resilience after the world trade center disaster: Reconstituting New York City’s emergency operations centre. Disasters, 27(1), 37–53. https://doi.org/10.1111/1467-7717.00218

- Khalid, A. A., & Sarea, A. M. (2020). Independence and effectiveness in internal Shariah audit with insights drawn from Islamic agency theory. International Journal of Law and Management, ahead-of-print(ahead-of-print). https://doi.org/10.1108/IJLMA-02-2020-0056

- Kheir, A. (2018). Contribution of Internal Audit in Procurement of Goods and Services at the President’s Office (PO), Constitution, Legal Affairs, Public Service and Good Governance-Zanzibar. Master’s Thesis, Mzumbe University.

- Kiage, J. O. (2013). Factors affecting procurement performance: A case of ministry of energy. International Journal of Business and Commerce, 3(1), 54–70.

- Lay, E., Branlat, M., & Woods, Z. (2015). A practitioner’s experiences operationalizing resilience engineering. Reliability Engineering & System Safety, 141, 63–73. https://doi.org/10.1016/j.ress.2015.03.015

- Lee, A. V., Vargo, J., & Seville, E. (2013). Developing a tool to measure and compare organizations’ resilience. Natural Hazards Review, 14(1), 29–41. https://doi.org/10.1061/(ASCE)NH.1527-6996.0000075

- Lenz, R., Sarens, G., & Silva, D. (2014). Probing the discriminatory power of characteristics ofinternal audit function: Sorting the wheat from the chaff. “International Journal of Auditing, 18(2), 126–138. https://doi.org/10.1111/ijau.12017

- Linnenluecke, M. K. (2017). Resilience in business and management research: A review of influential publications and a research Agenda. International Journal of Management Reviews, 19(1), 4–30. https://doi.org/10.1111/ijmr.12076

- Ljubisavljević, S., & Jovanovi, D. (2011). Empirical research on the internal audit position of companies in Serbia. Economic Annals, LVI(191), 123–141. https://doi.org/10.2298/EKA1191123L

- Mahyoro, A. K., & Kasoga, P. S. (2021). Attributes of the internal audit function and effectiveness of internal audit services: Evidence from local government authorities in Tanzania. Managerial Auditing Journal, 36(7), 999–1023. https://doi.org/10.1108/MAJ-12-2020-2929

- Maribe, G. (2010). Is blood thick than water? A study of stewardship perceptions in family busines. Paulines Publications.

- McManus, S., Seville, E., Vargo, J., & Brunsdon, D. (2008). Facilitated Process for Improving Organizational Resilience. Natural Hazards Review, 9(2), 81–90. https://doi.org/10.1061/(ASCE)1527-6988(2008)9:2(81)

- Mitnick, B. M. (2013). Origin of the Theory of Agency: An Account by One of the Theory's Originators SSRN. Electronic Journal. https://doi.org/10.2139/ssrn.1020378

- Mumby, P. J. C., & Bozec, I. (2014). Ecological resilience, robustness and vulnerability: How do these concepts benefit ecosystem management? CurrOpin Environ Sustain, 7, 22–27. https://doi.org/10.1016/j.cosust.2013.11.021

- Nalukenge, I., Kaawaase, T. K., Bananuka, J., & Ogwal, P. F. (2021). Internal audit quality, punitive measures and accountability in Ugandan statutory corporations. Journal of Economic and Administrative Sciences, ahead-of-print No. ahead-of-print. https://doi.org/10.1108/JEAS-05-2020-0084

- Nonnenmacher, J., & Gomez, M. J. (2021). Unsupervised anomaly detection for internal auditing: Literature review and research agenda. The International Journal of Digital Accounting Research, 21, 1–22. https://doi.org/10.4192/1577-8517-v21_1

- Nyamai, J. K., & Ismail, N. (2018). Role of Strategic Procurement Practices on Procurement Performance in State Corporations in Kenya. American Based Research Journal, 7(05). https://ssrn.com/abstract=3578330

- Oladejo, A., & Nwachukwu, C. (2021). Assessing internal audit function and public sector performance in Nigeria. International Journal of Economics and Accounting, 10(1), 97–110. https://doi.org/10.1504/IJEA.2021.112784

- Olsson, L., Jerneck, A., Thoren, H., Persson, J., & O’Byrne, D. (2015). Why resilience is unappealing to social science: Theoretical and empirical investigations of the scientific use of resilience. Science Advances, 1(4), 1–12. https://doi.org/10.1126/sciadv.1400217

- Pal, R., Torstensson, H., & Mattila, H. (2014). Antecedents of organizational resilience in economic crises—An empirical study of Swedish textile and clothing SMEs. International Journal of Production Economics, 147(PART B), 410–428.

- Quaye, B. L. (2019). Internal audit effectiveness within the Public Tertiary Institutions of Ghana: the influence of audit and organizational characteristics. master’s thesis, University of Ghana.

- Rahayu, S. Y., & Rahayu. (2020). Internal auditors role indicators and their support of good governance. Cogent Business & Management, 7(1), 1–14 1751020. https://doi.org/10.1080/23311975.2020.1751020

- Roussy, M., Barbe, O., & Raimbault, S. (2020). Internal audit: From effectiveness to organisational significance. Managerial Auditing Journal, 35(2), 322–342. https://doi.org/10.1108/MAJ-01-2019-2162

- Sofyani, H., Riyadh, A. H., Fahlevi, H., & Ardito, L. (2020). Improving service quality, accountability and transparency of local government: The intervening role of information technology governance. Cogent Business & Management, 7(1), 1735690. https://doi.org/10.1080/23311975.2020.1735690

- Somers, S. (2009). Measuring resilience potential: An adaptive strategy for organizational crisis planning. Journal of Contingencies and Crisis Management, 17(1), 12–23. https://doi.org/10.1111/j.1468-5973.2009.00558.x

- Tackie, G., Marfo-Yiadom, E., & Achina, S. O. (2016). Determinants of internal audit effectiveness in decentralized local government administrative systems. International Journal of Business and Management, 11(11), 184–195. https://doi.org/10.5539/ijbm.v11n11p184

- Thumbi, I. N., & Mutiso, J. M. (2018). Influence of procurement process audit on procurementperformance in public health facilities in Kiambu County, Kenya. International Journal of Social Science and Information Technology, 4(10).

- Tran, T. Y., Nguyen, P. N., & Bisogno, M. (2020). The impact of the performance measurement system on the organizational performance of the public sector in a transition economy: Is public accountability a missing link? Cogent Business & Management, 7(1), 1792669. https://doi.org/10.1080/23311975.2020.1792669

- Tumwebaze, Z., Mukyala, V. S., Tirisa, B., & Tumwebonire, A. (2018). Corporate governance, internal audit function and accountability in statutory corporations. Cogent Business & Management, 5(1), 1–13 1527054. https://doi.org/10.1080/23311975.2018.1527054

Appendix A.

Cross loadings

Table A1. Cross loadings

Appendix B.

Variance inflation factor

Table A2. Output of variance inflation factor (VIF) test