?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Corporate governance reports (CGR) and annual reports are two fundamental corporate documents disseminated to shareholders about the companies’ financial condition and operation. While the annual reports could be seen as outside appearance, the CGR reflects internal processes that an entity monitors the actions, policies, practices and decisions (Muttanachai and Thanyaorn, 2022; Ho and Taylor, 2014). Vietnam’s publicly traded companies are compulsory required to provide annual reports and CGR to shareholders. The purpose of this research is to investigate the link between the level of corporate governance disclosure (CGD) and the quality of annual reports in the context of Vietnam—an emerging and dynamic country in South East Asia. The existing literature review is developed by using a bibliometric analysis (via VOSviewer software) with Scopus database from 2002 to 2022 provides comprehensive evidence for mixed effects of the level of CGD on quality of annual reports, therefore, the paper attempts to contribute to the ongoing debate by examining whether the association between CGD and the quality of annual reports is nonlinear. Furthermore, the quality of annual reports and level of CGD are measured basing on scorecard of Vietnam Listed Company Awards (VLCA) reflect the typical research issues in the context of Vietnam. A panel smooth transition regression (PSTR) model is applied in order to test the relationship and calculate the value transition threshold of 356 Vietnamese listed companies from 2017 to 2022. Empirical findings indicate that there has been a nonlinear relationship between two tested variables. In addition, the quality of annual reports positively increases when the level of CGD exceeds the value transition threshold. Hence, the listed companies with high level of CGD (exceeds threshold value) have an incentive of preparing high quality annual reports.

1. Introduction

Annual reports quality (ARQ) including financial statements, management discussion and analysis, notes to the financial statements and auditor’s report play a crucial role in maintaining the efficiency of financial market especially for investors, creditors and regulators to rely on financial reporting information to make decision. However, in the case of Vietnam, an emerging country where information disclosures lacks accountability and transparency, the economy have witnessed devastating stock market manipulation scandals of FLC group, Tan Hoang Minh group in the 2nd quarter of 2022. The manipulated information on annual reports has caused serious damage to financial market participants and affected operations of Vietnam’s stock exchange. Therefore, the current situations in emerging economies, typically in Vietnam, indicate the need for annual report quality.

On the other hand, corporate governance report is a form of nonfinancial information disclosure. Corporate governance including issues of disclosure and transparency are important instruments to protect investors’ interest and performance of the capital market (Cadbury Committee, Citation1992; COSO, Citation2013; OECD, Citation2004). The corporate governance illustrates a critical role in the adoption of not only economic but also environmental and social performance of financial reporting system in the organization (Hahn & Kuhnen, Citation2013; Shamil et al., Citation2014). Several studies state that effective corporate governance mechanism enhances transparency and accountability and consequently leads to better reporting practices (Crifo et al., Citation2019; Rao et al., Citation2012; Said et al., Citation2009). The corporate governance reports are mandatory for Vietnam listed companies and often published on an annual basis as a separate, standalone report containing nonfinancial information about a firm’s policies and practices.

Within this context, Vietnamese regulatory agencies acknowledge the importance of financial and non-financial information on annual reports and corporate governance reports (CGR) so they deploy several actions to improve the quality of annual reports and disclosure level of corporate governance reports (CGR). The Vietnam Listed Company Awards (VLCA) is annually co-organized by the Ho Chi Minh City Stock Exchange (HSX), the Hanoi Stock Exchange (HNX) and Vietnam Investment Review under the sponsorship of Dragon Capital Group to promote the healthy development of the local stock market. VLCA focuses on three categories of Annual Reports, Corporate Governance Reports and Sustainable Development Reports. Among these categories, there are organizations that are awarded to have the best annual reports as well as the best corporate governance reports in 2021, such as Vietnam Dairy Products Joint Stock Company (VNM) on HOSE, the PAN Group Joint Stock Company (PAN) on HOSE, DHG Pharmaceutical Joint Stock Company (DHG) on HOSE. Current practice in Vietnam have addressed the connection and linkage between the quality of annual reports and level of disclosure on corporate governance reports.

The literature review illustrates that, although the extant literature mainly examined the association between corporate governance and reporting in the context of developed countries (Elshabasy, Citation2018; Jizi et al., Citation2014; Kumar et al., Citation2022; Kumari & Vincent, Citation2022), the studies exploring the same issues on emerging countries are limited (Mahmood & Orazalin, Citation2017). For instance, Ikram et al. (Citation2019) conducted a longitudinal survey examining the influence of CGD on firms’ information reporting in small and medium sized companies in Pakistan. The findings show that CGD are positively correlated with the quality of annual reports and, in particular, corporate reputation and employee commitment. Likewise, within a developed countries context, a number of studies have reported that a positive relationship exists between CGD and annual reports (Kim et al., Citation2018; Broadstock et al., Citation2020), whereas other research signified either a negative (Lin et al. Citation2019) or a neutral relationship (Surroca et al., Citation2009). Especially in the case of Vietnam there is no study providing evidence on the relationship between corporate governance disclosure and the quality of annual reports, to the best of authors’ research.

From current situation and academic perspectives, the paper aims to provide empirical evidence to fill the “research gap” with respect to the linkage between level of CGD and the quality of annual reports in an unstainable country—level governance setting. Additionally, this research is distinguished and rationale by the number of research condition. Firstly, we use the CGD and annual reports index measurement basing on the Annual Vietnam Listed Company Awards (VLCA) scorecards. The advantage of these scorecards is that it provides objectively and regulated benchmark to evaluate the level of disclosure and the score of annual reports. By using R software to apply Exploratory Factor Analysis (EFA) we aim to test whether the underlying structures of VLCA scorecard is consistent with collected observations. Secondly, a comprehensive literature review of prior research has been developed by a modern bibliometric analysis to depict a complete and meaningful overall research picture. This literature review methodology is distinguished with prior research by emerging new technologies and inventing bibliometric software packages resulted in bibliometric visualization of journals, including among others mapping their co-authorship, co-citation, keywords co-occurrence and bibliographic coupling patterns and networks.

In order to achieve the above objectives, the study makes several significant contributions to the current literature. The study further examines the reliability and structural equivalence of VLCA scorecard. The scorecard incorporates environmental, social and governance transition dimensions along with promoter and government ownership. The tests on VLCA questionnaires would be helpful to policy makers, the government, specialist in Vietnam to have an insight overview in corporate governance control mechanism as well as score range of the annual reports quality. In addition, the governing agencies may wish to improve their guidance concerning CGD, CGR and annual reports. It is also helpful for international researchers and regulators in other emerging countries to acknowledge about corporate governance scorecard to apply in another context.

To present these issues, the paper is structured as follows. Section 2 reviews comprehensively the literature on the quality of annual reports and CGD by highlighting theoretical and empirical studies. The following section 3 is methodology section to describe data collection, variable measurement and empirical test model. Section 4 includes the empirical result and some discussion on findings whereas section 5 describes further robustness tests. Conclusion is the last section to summarize the overall content, the limits of the study and some future research directions.

2. Literature review

2.1. Corporate governance disclosure and annual reports quality background in Vietnam

The set of annual reports is mandatory for Vietnam listed companies and often published on an annual basis including financial statements, management discussion and analysis and auditor’s report. These reports aim to provide an overview of financial situation and performance of a business for one year to the public, potential investors, media, shareholders and government regulatory agencies. In almost all emerging countries, including Vietnam, the economy background has experienced poor implementation or enforcement of laws and regulations as the bane of a sound system of corporate governance, non—financial disclosure. Hence, the annual reports maintain several limitations such as many items of financial value are omitted or income numbers are affected by the accounting judgments and estimates etc …

In early of the second and the third quarter of 2022, Vietnam stock market has experienced the vast and considerably effect of stock prices manipulation of FLC group and Tan Hoang Minh group. In turn, government aims to improve annual reports quality as an essential role to promote stronger, cleaner and fairer economics growth. It fosters an environment of market confidence and business integrity that supports capital market development. Moreover, Vietnamese firms rely heavily on external sources of finance outside the stock market, the improvement of annual reports quality have been promoting foreigner capital sources apart from the traditional capital provision (Abaidoo & Agyapong, Citation2022; Gerayli et al., Citation2021).

When it comes to CGD, corporate governance reports (CGR) is a form of nonfinancial disclosure. Several researchers suggest that when the financial reporting does not provide relevant information, stakeholders should rely on nonfinancial disclosure (Allegrini & Greco, Citation2013; Boateng et al., Citation2022). Corporate governance mechanism monitors managers’ performance and encourages them to provide full information disclosure (Shamil et al, 2004). According to agency theory and legitimacy theory perspective, managers improve the quality of sustainability disclosure to mitigate agency cost and information asymmetries. The legitimacy theory also advocates that level of corporate governance disclosure could influence the stakeholders’ view about the firm and demonstrate their commitment to public, social and environmental issues (Vogt et al., Citation2017). While annual reports are compulsory required for Vietnam listed companies, CGR is voluntarily disclosure.

In the context of Vietnam, the Vietnam Listed Company Awards (VLCA) is annually organized with the effort to enhance the transaparency of information disclosure, improving corporate governance and sustainable development toward integration into regional and international capital market. In order to improve the quality of annual reports, VLCA creates set of criteria focusing on two main areas: Content of annual reports, which accounts for 75% of total mark of 100 and Format of annual reports, which is 25% of total mark of 100. The highest mark for annual reports quality is 102 including rewarded marks on evaluation of greenhouse gas emissions (2 marks). The evaluation of the content of annual reports focuses on:

General Information (including an overall summary of the company, objectives and development strategy, information on governance structure, business organization and management mechanism, risks affect intended objectives)

Assessment on the company’s performance (including business situation, investment and project implementation, financial position)

Reports and assessment of Board of Directors, Board of Management on the company performance (including evaluation of achievements, organizational structure improvement, management policy, performance planning, future orientation)

Information on corporate governance (including information on board of directors, audit committee, board of management, related parties’ transactions, insider stock trading, assessment on implementation of corporate governance regulation)

Additionally, in 2022, Vietnam have provided more requirements to encourage enterprises to supplement information on enterprise risk management activities, compare operations with companies in the same industry, present and evaluate the implementation of corporate governance according to national standards such as Vietnam Corporate Governance Code, regional standards such as Asean Corporate Governance Code.

The VLCA also released corporate governance scorecard to evaluate level disclosure of corporate governance reports include four main areas: Rights and fair treatment among shareholders, Role of stakeholders, Disclosure and transparency, Responsibilities of Board of Directors. Some examples of content that might be in a CGR are: the reliance on corporate code of conducts, information of shareholder’s structure, remuneration of board of directors and audit committee, disclosure of risk control mechanism, independent members of board of directors, the number of accounting and finance expertise in board of directors. The criteria for evaluating the level of corporate governance disclosure by a company based on two main features:

Compliance with current Vietnamese laws on corporate governance for listed companies.

Good corporate governance practice based on the OECD/ G20 Corporate Governance Principles issued in 2015.

The VLCA set of scoring criteria includes 81 questions in four main parts:

Rights and Fair treatment of shareholders and basic ownership functions

The role of stakeholders

Disclosure and transparency

Responsibilities of the Board of Directors and Supervisory Board

According to VLCA (2021) the average score on CGR increased to 52.59 in comparison to the score of 49.67 in 2020. In detail, group of large companies illustrates higher score (64.89) on CGR than other groups of medium (57.30) and small companies (48.62).

The result of VLCA (2021) indicates a connection between the score of annual reports quality and level of corporate governance disclosure. In which, a company which is evaluated as good quality of annual reports, also achieves high score of corporate governance disclosure. In the scope of the research, the authors deploy the scorecards of VLCA to evaluate the level of disclosure of CGR and the quality of annual reports.

2.2. Corporate governance disclosure and annual reports quality

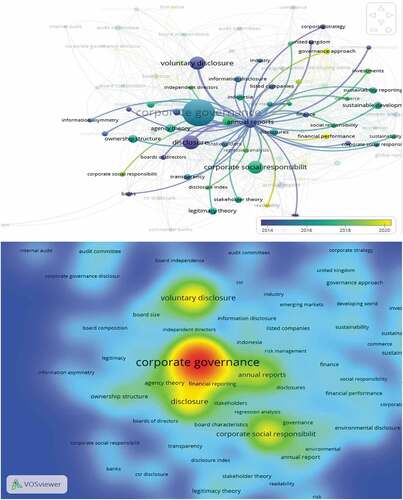

In order to present a comprehensive understanding of the existing literature review on corporate governance disclosure and quality of annual reports, the research utilizes the recently popularized methods of systematic literature review and bibliometric analysis. From the data of 529 publications sourced from the Scopus database from 2004 to 2022, the bibliometric mapping and citation analyses are graphically performed by VOSviewer.

The paper analyzed the number of research and authors with the minimum record of 5 papers (as a threshold). The results indicate that 11 authors have published more than 5 papers related to research issues. The Table exhibits the list of 11 authors and the top authors have the highest citations ranking are Husseny (published 16 papers), Ghazali (published 5 papers), Tower (published 5 papers), Soobaroyen (5 papers).

Table 1. Top authors that published papers related to corporate governance disclosure and quality of annual reports from 2004 to 2022

In the scope of this research, we focus on papers that received the highest citation as following illustration in Table . The result notices that the highest cited paper in this research area logically depended on its publication year. For example, a study by Haniffa and Cooke “The impact of culture and governance on corporate social reporting” was published in 2005 on Journal of Accounting and Public Policy has been cited by 938 times, and study by Barako et al., has been cited by 453 times was published in 2006. It should be interpreted that the research trend on this issue is focused on typical years of 2005–2006, 2008–2009 and 2013–2014.

Table 2. Top authors have the highest citations and research

When it comes to research issues, bibliometric analysis provides evidence that there has been a strong connection between corporate governance and annual reports as well as corporate governance disclosure and annual reports (Illustrated in chart 1). The findings are illustrated by applying VOSviewer as following table and charts. Table presents the list of most frequent keywords used by the authors in their publication’s documents and other related disclosure documents. It could be observed from Table that the most frequent keywords are “annual reports”, “corporate governance disclosure” and “corporate social responsibility”. In addition, chart 2 presents the connection between CGD and annual reports as assigned items to cluster. The cluster density visualization has a color that indicates the density of cluster at that point. By default, the colors range from blue to green to yellow to red. The larger the number of items in the neighborhood of a point and the higher the weights of neighboring items, the closer the color of the point is to yellow or to red. As can be seen in chart 2, the items of corporate governance, disclosure, annual reports, disclosures, agency theory, financial reporting have red color illustrating the strong connection between items.

Chart 1. The link strength between corporate governance disclosure and annual reports.

Table 3. Statistic of occurrences and total link strength of keywords

In summary, the literature review on corporate governance disclosure and annual reports quality illustrates a strong relationship between two variables. Basing on several bibliometric indicators and data of publications from Scopus, the literature highlights the top cited articles for further analysis. This research is also developed on the agency and legitimacy theory that identified from existing literature by bibliometric analysis.

2.2.1. Positive effects of corporate governance disclosure on the quality of annual reports

The OECD (Citation2004) lists timeliness as a principle of good corporate governance. There is some evidence to suggest that it takes more time to report bad news than good news (Van der Zahn, Citation2004) both because companies hesitate to report bad news and they take more time to message the numbers or resort to creative accounting techniques when they have to report bad news (Al. N et al., Citation2007). However, a study by Maingot and Zeghal (Citation2008) found that companies tend to disclose bad information quicker than the good ones, presumably because of conservatism. Collett and Hrasky (Citation2005) discuss this point in their research and state that firms with more conservative accounting systems are less likely to make timely voluntary disclosures than firms with less conservative accounting system. In other words, there has been a positive association of the nature of the information being reported and the readiness of level of disclosure. Merlin and Visser (Citation2002) provided more evidence to state that a company have a higher level of information disclosure could maintain a good financial reporting process in terms of conservatism, accrual basis and consistency. McGee and Tarangelo (Citation2009) found this relationship to hold true for municipalities. Several researchers namely Saad et al. (Citation2009) and Ghazali, Citation2009) found it to be the case for Chinese and Malaysian companies.

From legitimacy theory perspective, corporations may enhance their financial performance by catering to stakeholders’ requirements. For instance, focusing on the needs of employees results in enhancing their productivity and improving reputation of the company and the public’s confidence will improve competitive advantage of the firm resulting in good financial performance. Cerbioni and Parbonetti (Citation2007) examined 356 European biotechnology companies and found that companies have a strong shareholders orientation tend to disclose more corporate governance information than companies offer little incentive to do so. Following this, the different CGR areas and philanthropic practices that corporations engage in reflecting their values and internal corporate mechanism among the stakeholders (Said et al., Citation2009). It is not merely basing on legal obligations, however, CGR aims to establish solid relations between coporations and their stakeholders through investing in public, social, environmental activities and enhancing the transparency of financial reporting process. According to Nobanee and Ellili (Citation2022), whenever a company tends to focus of CGD, the company has an incentive to well—prepare financial information to attract its interested users.

Most cited documents such as Kent and Zunker (Citation2013), Khan et al. (Citation2013), and Jizi et al. (Citation2014) illustrated the link and positive interaction between the level of CGD and the quality of annual reports. Khan et al. (Citation2013) conducted research on Malaysian listed companies and found out that level of corporate governance disclosure, which were measured by board composition, multiple directorship and type of shareholders, positively associated with annual reports quality, which were measured by index score. This study based on the view of legitimacy theory, however, the attributes of CGD and annual reports need to be adjusted in the context of typical economy.

To elaborate, one stream of literature argues that engaging in corporate philanthropy impacts financial and nonfinancial reporting process positively (Mahdi et al, Citation2014; Ha & Finch, Citation2022; Mukhibad & Setiawan, Citation2020; Lauwo et al., Citation2016; Ridho, Citation2016). Further, firms engaging in CGD by increasing their transparency and stakeholder engagement have been evaluated high quality of annual reports. In 2017, the Malaysian Securities Commission has released new Malaysian Code of Corporate Governance (MCCG Citation2017) to replace the old one (MCCG 2012) with several changes and recommendations to enhance corporate governance’s accountability, transparency and sustainability. Within the context in Malaysia, Sadou et al. (Citation2017) access the likelihood of financial reporting fraudulent using PN17 companies as a proxy. The study provides initial evidence that the more adoption of MCCG Citation2017, the less possibility of the likelihood of financial reporting fraudulent.

In the context of an emerging country, Ha (Citation2022) investigated Vietnamese listed companies and revealed that the audit committee characteristics namely audit committee independence and size of audit committee are significantly associated with level of corporate governance disclosure. The empirical evidence of this study stated that the firm size is statistically linked to corporate governance disclosure indicating the capital demand of large companies.

Another strand of the literature emerged following the outbreak of COVID-19, which focused on examining the impact of the pandemic on the CGD and annual reports quality relationship. In a recent research study, Hsu and Yang (Citation2022) conducted an analysis of 3122 UK listed firms from 2018 to 2022 from FAME database. By examining the real earnings management behavior of companies, they found that the financial reporting information on annual reports is lower during the pandemic. The research results conclude that firms strongly engaged in CGD before the pandemic had superior stock performance and high quality of annual reports after the pandemic’s outbreak, thereby suggesting that CGD improve loyalty, stakeholders’ relations and the transparency of financial reporting process. Furthermore, Kumar et al. (Citation2022) found that firms with CGD’s information of the board size and board independence had higher quality of annual reports and were less impacted by the pandemic outbreak compared to the non CGD-firms in India. Another research of Abdelhak et al (Citation2022) focuses on governance mechanism (board diversity, audit committee independence) audit type and audit opinion affect the level of COVID-19 disclosure. It is confirmed as the first paper in Egypt that provides evidence on the impact of internal governance and audit quality on COVID-19 disclosure.

Consequently, following the above studies, the level of CGD is proved to have a positive correlation with quality of annual reports.

2.2.2. Negative effects of corporate governance disclosure on the quality of annual reports

Part of empirical studies have provided evidence on negative results as they emphasize that investments in CGR incur additional underestimated costs and expenses, which in turn indicates negatively on firms’ financial ratio (Lazarides, Citation2010). Under this circumstance, the firms are not willing to report unexpected financial and nonfinancial situations on CGR. Further, Othman and Zeghal (Citation2010) investigated firm-level moderators such as firm size and age to facilitate understanding level of disclosure of CGR and the annual reports quality correlation in MENA emerging markets. The modern analysis showed that CGD and ARQ were negatively correlated in small and/ or young firms. This could be due to limited experience and resources and lack of reputation in these firms. Therefore, a high level of CGD does not represent a good structure of financial reporting process and high quality of annual reports as an economic entity considers a balance of cost-benefit when obtaining CGR, especially in cases of small sized companies where focused orientation is financial information.

In contrast to the social and stakeholder impact of agency and legitimacy theory, the shift of focus hypothesis builds on the notion that engaging in CGD practices directs a firm towards financial reporting information or society welfare and results in shifting the focus towards practices that do not enhance shareholder value but increase the costs. Subsequently, CGD negatively impacts firms’ performance and the competitive advantages (Galant and Cadez, Citation2017; Kim et al, 2015). In turn, although firms have a good structure of financial reporting process they do not have an incentive for non-financial information disclosure on CGR. Further, other researchers such as Darus et al (2013 claim that managers engage in CGD to shift the focus from the firm’s shortcomings. They applied the Granger causality test and linear regression analysis engaging in CGD does not mean good financial performance and that the level of CGD negatively affects financial performance. Therefore, the shift of focus hypothesis indicates that the demands of different stakeholders on CGD also reflect negatively on quality of annual reports.

In addition, advocates for the traditionalist perspective or the trade-off hypothesis argue that there is negative relationship between CGD and ARQ due to the high costs incurred from social and environmental activities, which weaken the competitive advantage and profitability. Moreover, CGR can be considered as a component of a corporate strategy for social legitimacy and control (Li et al, 2008; Abaidoo & Agyapong, Citation2022; Aras et al., Citation2010; Nguyen & Huong, Citation2021; Said et al., Citation2009).

Therefore, the previous empirical research results are in accordance with the trade-off hypothesis that indicates a negative impact of CGD on ARQ.

2.2.3. Neutral effects of corporate governance disclosure on the quality of annual reports

Bhasin and Shaikh (Citation2016) performed an examination to discover a link between CGR and annual reports of 50 corporations during the period between 2003 and 2005. They selected 40 items from CGR and annual reports and found that there are no significant differences among the disclosure score of CGR and quality of annual reports across the research sample. Additionally, analyzing data from 549 companies in Nigeria for a period of 1986–2016, Ajide and Olayiwola (2020) reported that no direct correlation was found between ARQ and CGD. There is only one attribute “consistency and transparency” of CGD was affected by ARQ.

During COVID-19, Soepriyanto et al. (Citation2021) examined 1278 the United States firms and found little support that highly rated of CGR on environmental, social and governance corporation issues have enhanced the quality of annual reports. In addition, according to Sharma et al. (Citation2020), even when a company achieves good score of CGD, there is no proof that ARQ is affected. By applying the Granger causality approach, they also found that CGD is only associated with a firm’s performance in the stock market which is proxied by the market returns.

2.2.4. Research gap

In summary, literature review of empirical studies has shown a mixed result of positive, negative and neutral impact on the relationship between CGD elements/ dimensions and ARQ. These results could be interpreted that the link between CGD and ARQ is not a linear relationship by which it is either a positive, negative or neutral relationship. As the above literature review highlights the inconclusive result of research issues in typical context, the research gap is identified. First, although several approaches are used to explain the research issues such as agency or legitimacy theory, the authors highlight an absence of tailored approaches to understand corporate governance of emerging countries. Corporate governance has been mostly seen as unified and standards, however, the literature review does not mention how corporate governance practice could be manifested in multiple ways depending on the endogenous characteristics of the institutional framework where companies operate. We, therefore, consider the control variables to represent the dynamic dimensions of corporate governance and its effect to change and evolve over time when developing research hypotheses.

Second, further exploration is called for deeper analyses of agency issues such ARQ as result of annual reporting process of directors and executives (the agency) while CGD as control mechanism setting for shareholders (the principal). Similarly, it is observed a research gap in the literature regarding low level setting of corporate governance mechanism in emerging countries.

Third, previous studies in corporate governance suggest that there are several limitations such as a single-period study, only focus on financial or non-financial firms, limited data or not specifically measuring the impact of corporate governance mechanism on annual reports quality.

In consequence, the paper aims to provide more contribution to the ongoing debate. From the authors’ point of research view, we propose the following hypotheses:

H1: The relationship between level of corporate governance disclosure and annual reports quality

2.3. Is nonlinear

H2: Level of corporate governance disclosure has a positive effect on annual reports quality when annual reports quality is below a certain threshold.

H3: Level of corporate governance disclosure has a negative effect on annual reports quality when annual reports quality is below a certain threshold.

H4: Firm size has a positive effect on annual reports quality.

H5: Firm leverage has a positive effect on annual reports quality.

H6: Firm sales growth has a positive effect on annual reports quality.

3. Research methodology

3.1. Sample selection and data source

A criterion sampling technique is adopted for the study. According to Green (Citation1991), in order to evaluate the factor analysis of each independent variable such as t-test, regression coefficient, the minimum sample size should be 104 + m (m is the number of independent variables). According to Tauchen (Citation1986) condition for estimation of reliability for performing regression analysis is n > 200. Combined of two principles, the sample size chosen of 356 observations by authors is reasonable. The 356 observations are non-financial companies listed on the two Vietnam Stock Exchange that are the Ho Chi Minh City Stock Exchange (HOSE) and the Hanoi Stock Exchange (HNX) in 2022. The sample also includes 15 companies of each category were awarded as the best corporate governance reports and the best annual reports in 2022. Awarded companies illustrating high score of CGR and annual reports that could demonstrate full and diversity characteristics of corporate governance as well as the structure of annual reports. The representativeness of the awarded companies suggests the inclusion of selecting these typical economic entities in the sample to check the consistency and reliability of VLCA questionnaires. Other control variables were taken from annual reports of listed companies. Businesses with specific reporting standards, along with firms with missing data, were omitted in this research.

We did not consider financial, banking and insurance companies because of their specific disclosure requirements and accounting regulations. The companies in initial sample are also in the VNX Allshare general index. VN Allshare is the Vietnamese third exchange index and issued after VN index at HOSE and HNX index at HNX, which cover nearly 90 percent of the combined market capitalization. The companies in the VNX Allshare need to meet three requirements namely: first, the company’s stocks must have been listed for at least six months without violating market rules; second, the company must have a stock return of at least 0.02 percent to ensure the company is eligible for business and finally, the minimum free-float rate must be no less than five percent.

The VLCA organizing committee develops a set of marking criteria based on the principles of Organization for Economic Cooperation and Development (OECD) and Vietnam regulation on annual reports. The set of marking criteria has been adjusted to be consistent with current regulations on corporate governance and in the context of Vietnamese enterprises. Therefore, before examining the relationship between the corporate governance disclosure and quality of annual reports, the study needs to confirm the reliability of marking criteria as well as internal consistency of the set of marking criteria in a group. We use Cronbach Alpha test to measure reliability or the consistency of VLCA scoring criteria.

3.2. Dependent, independent and control variables’ measurements

3.2.1. The dependent variable

Annual reports quality is the dependent variable and the construct of ARQ is very complex, as illustrated by the numerous definitions found in the existing literature therefore, it is not surprising that many different proxies have been employed to measure ARQ. However, in the scope of this study, we use scoring index based on the VLCA set of marking criteria to measure the quality of annual reports by companies (see appendix for VLCA ARQ scorecard). The set of marking ARQ is developed by VLCA organizing committee basing on Vietnamese Circular 155/2015/TT-BTC on guidelines for information disclosure on securities market (The Ministry of Finance, Citation2015). The set of criteria has 102 questions indicating the highest mark for annual reports quality could be 102 including rewarded marks on evaluation of greenhouse gas emissions (2 marks).

Consistently with prior studies on ARQ measurement, we used the Cronbach’s coefficient alpha (Cronbach, 1951) to assess the internal consistency of VLCA scoring index. Internal consistency refers to the degree to which the items in a test measure the same construct. Ho (Citation2006) stated that Cronbach’s alpha is a single correlation coefficient that is an estimate of the average of all the correlation coefficient of the items within a test. If alpha is higher than 0.6 then this suggests that all of the items are reliable and the entire test in internally consistent.

3.2.2. Independent variables

Similar with annual reports, the VLCA organizing committee develops a set of corporate governance marking criteria based on the principles of Organization for Economic Cooperation and Development (OECD). The set of marking criteria has been adjusted to be consistent with current regulations on corporate governance and in the context of Vietnamese enterprises. The criteria for evaluating the level of corporate governance disclosure by a company based on two main features:

Compliance with current Vietnamese laws on corporate governance for listed companies.

Good corporate governance practice based on the OECD/ G20 Corporate Governance Principles issued in 2015.

VLCA’s corporate government scorecard includes a wide range of inputs, namely function and responsibility of Board of Directors, audit committee activity, organization structure, relationship with stakeholders, business political participation, the reliance on corporate code of conducts, information of shareholder’s structure, remuneration of board of directors and audit committee, disclosure of risk control mechanism etc …

Basing on VLCA’s criteria, this study used four independent variables that are Rights and fair treatment among shareholders (RIGHTS), Role of stakeholders (ROLE), Disclosure and transparency (DISCLOSURE), Responsibilities of Board of Directors (BOD). The index measures the level of corporate governance disclosure including 81 questions in four above main parts. Each question in four categories is assigned a score 0 for No and 1 for Yes. A company which is evaluated as good corporate governance disclosure, achieves high score of CGR. According to VLCA survey, the average score on CGR increased to 52.59 in comparison to the score of 49.67 in 2020. In detail, group of large companies illustrates higher score (64.89) on CGR than other groups of medium (57.30) and small companies (48.62).

Before examining the relationship between the annual reports quality and the level of corporate governance disclosure, the study needs to confirm the reliability of marking criteria as well as internal consistency of the set of marking criteria in a group. We use Cronbach Alpha test to measure reliability or the consistency of VLCA scoring criteria on CGD.

3.2.3. Control variables

Control variables are identified on the basis of previous studies. Ahmed and Courtis (Citation1999), Allegrini and Greco (Citation2011), Madi et al. (Citation2014), and Boateng (Citation2021) confirm the effect of firm size (SIZE), which is calculated as the natural logarithm of total assets at year end. The authors states that large sized companies tend to disclose more information than smaller companies. It could be explained that agency costs are associated with the separation of management from ownership which is likely to be greater in larger companies.

In accordance with Camfferman and Cooke (Citation2002), Allegrini and Greco (Citation2011), Madi et al. (Citation2014), firm leverage (LEVERAGE) also has been illustrated to be a significant control variable, which is calculated as the ratio of total debts to total assets. Alsaeed (Citation2006), Allegrini and Greco (Citation2011) and Alzeban (Citation2020) acknowledged that highly leveraged firms may deal with higher agency costs. Companies with a high level of debt try to reduce agency costs by disclosing more information and have a good quality of annual reports in order to more attract potential users.

In addition, sales growth (S-GROWTH) is also identified by previous studies illustrating that it is a considerable control indicator to reflect relationship between ARQ and level of CGD (Khan et al., Citation2013; Mousa et al., Citation2018; Owusu—Ansha & Ganguli, Citation2010). This control variable is measured as current year sales minus previous sales divided by current year sales.

3.3. The proposed research model of corporate governance disclosure and the quality of annual reports

We deployed a panel smooth transition regression (PSTR) model to examine the potential nonlinearity relationship between ARQ and CGD of listed companies basing on the agency and legitimacy theory . The model was developed by Fok et al. (Citation2005) and Gonzalez et al. (Citation2018) and has been confirmed by extant literature that it is suitable for the needs of various perspectives of analysis. In the scope of this study, this model illustrates several research advantages. Firstly, the model allows researchers to observe the panel’s items to be classified into a few homogenous groups. Secondly, the model allows for the computation of various elasticities. Finally, the PSTR model was chosen because it indicates smooth transitions rather than sharp ones, especially when authors do not know which type of transition exists in the model.

Basing on the above reason, the research model to investigate the relationship between ARQ and CGD has been proposed as following:

Where:

ARQit is the annual report quality of the company i at time t

CGDit is the vector of the various CGD measures of the company i at time t

αi illustrates an individual fixed affect

Zit is a k-dimensional vector for control variables

In accordance with Gonzalez et al. (Citation2018), the transition function in the logistic form g(qit; γ; c) is a continuous function of the transition variable qit, bounded between 0 and 1 and defined as:

with γ > 0 and c1 ≤ c2 ≤ … ≤ cm

γ is the slope of the transition function

c equals (c1, … ., cm) which is an m-dimensional vector of threshold. For m = 1 and m = 2, there are one or two levels of CGD around which the association between ARQ and CGD is nonlinear. Gonzalez et al. (Citation2018) and Fok et al. (Citation2005) confirmed that m = 1 or 2 is sufficient because these values allow for frequency type of variables in the parameters.

EquationEquation (1)(1)

(1) aims to test whether nonlinearity is related to various level of CGD which is influenced by ARQ. The Equationequation (1)

(1)

(1) also illustrates the elasticities in the PSTR model vary across firms and over time depending on the value of the transition function.

Before applying the PSTR model to determine a selection between using a linear of a non-linear model to estimate Equationequation (1)(1)

(1) , a homogeneity test need to be conducted. In turn, the next section includes the following tests: firstly, Homogeneity test; secondly, Cronbach alpha test in addition to descriptive analysis and correlation matrix; thirdly, estimation test of PSTR model to consider Equationequation (1)

(1)

(1) and fourthly, robustness tests.

4. Empirical analysis and results

4.1. Analysis on the homogeneity test

Table indicates the results of the homogeneity tests. The p-value of the Lagrange multiplier and Fisher-type tests for the null hypothesis of linearity versus the alternative of nonlinearity specifications.

The result illustrates the null hypothesis of homogeneity is rejected at the 1% significance level. At value m = 1 the result also indicates that the rejection of linearity is significant and there should be a single threshold of ARQ beyond which the effect of ARQ on level of CGD would become nonlinear. We follow with an assumption that there has been one threshold (m = 1) of ARQ. Therefore, the findings reveal that the impact of ARQ on level of CGD depends on the value/ score (illustrating by a threshold) of ARQ. As a result, we continue our analysis by using PSTR model.

4.2. Cronbach alpha test

Table shows the alpha coefficient for the items on VLCA’s scorecard of ARQ and CGD. Number of items in the second row are 102 which equivalents to 102 questions and the number of items in the third row are 81 which equivalents to 81 questions. (See more in appendix)

Table 4. Summary and analysis of literature review on corporate governance

The analysis result shows the coefficient of ARQ and CGD scorecard is 0.73 and 0.852 respectively suggesting that the items have relatively high internal consistency with chosen sample (Henseler et al., Citation2010). Moreover, the Cronbach Alpha values above 0.6 and 0.7 are considered fitting in exploratory studies (Hair et al., Citation2014). Therefore, we keep the set of questionnaires for further analysis.

4.3. Descriptive statistics

Table represents the descriptive statistics of variables that used in the research. Regarding the statistics of ARQ, the mean score for overall sample is 73.8, with a range from a minimum of 54 to a maximum of 91 points. The result indicates that the ARQ of listed companies in the research sample is relatively high with a small fluctuation of standard deviation.

Table 5. Top 25 companies’ annual reports were awarded in term of size in 2021

When it comes to CGD’s indicators, the result show that the average CGD value fluctuates differently in terms of Rights and fair treatment among shareholders (20.5 out of a possible of 30), Role of stakeholders (15.6 out of a possible of 20), Disclosure and transparency (12.7 out of a possible of 20) and Responsibilities of Board of Directors (7.03 out of a possible of 12). The statistics reflect a fluctuated pattern or nonlinearity correlation of each variables CGD-RIGHTS, CGD-ROLE, CGD-DISCLOSURE and CGD-BOD.

4.4. Analysis on correlation

Table shows the result on correlation test of dependent variable (ARQ) and independent variables (CGD’s indicators) and the control variables. The table generally illustrates low correlation among independent variables. When it comes to the relationship between dependent and independent variables, it reports that there is considerable connection between Rights and fair treatment among shareholders (CGD-RIGHTS), Role of stakeholders (CGD-ROLE), Disclosure and transparency (CGD-DISCLOSURE) and Responsibilities of Board of Directors (CGD-BOD) and ARQ. In addition, only LEVERAGE has the expected sign and is statistically connected to the ARQ. Other control variables: firm size (SIZE) and sales growth (S-GROWTH) have no statistically connection with the dependent variable. In summary, it is evidence to state that there is no indication of material multicollinearity in the proposed model.

Table 6. Top 15 companies’ CGR were awarded in term of size in 2021

4.5. Analysis on the PSTR model

Table represents the estimation result applying the PSTR model. The multiple CGD dimensions, which are (CGD-RIGHTS), (CGD-ROLE), (CGD- DISCLOSURE), (CGD- BOD), are reported in the first column. The finding indicates that the direct impact of each CGD attribute on ARQ, as measured by β0, is significantly positive through all the regressions. This result is consistent with some empirical evidence, which implies that CGD indicators have a detrimental influence on ARQ (Dao Thi & Ta Dieu, Citation2020; Owusu—Ansha & Ganguli, Citation2010)

Table 7. LM and F tests of homogeneity

Table 8. Reliability statistic

represents the descriptive statistics of annual reports quality for the research sample. The mean ARQ score for overall sample is 73.8, with a range from a minimum of 54.00 to a maximum of 91.00. The evaluated result shows that the ARQ of companies in research sample is relatively high with a small fluctuation of standard deviation. A clear indication that the research categories achieves average ARQ score includes compliance and current practices.

Table 9. Descriptive statistics for dependent, independent and control variables (n = 356)

illustrates the Pearson correlation between each variable. The result shows that there is a positive relationship between the dependent variable (ARQ) and each independent variable. The result also confirms that there is no association among four independent variables.

Table 10. Pearson correlation matrix

The second line under each variable of confirms the homogeneity test results: the impact of CGD on ARQ appear to be highly nonlinear. Additionally, the coefficient β1, which is associated with the model’s nonlinear component, is always positive and significant at the 1% level. As assumed in the hypotheses, the effect of CGD on ARQ is conditional on the level of CGD. When the CGD level moves from low to high values indicating that the firms more invest in CGR, the coefficient vary from β0 to β1. The transition between these values occurs around the endogenous location parameter c1,1. The findings are consistent with previous research that have depicted a nonlinear relationship between CGD and ARQ (Kim et al., Citation2018; Broadstock et al., Citation2020; Ting et al., Citation2019; Lin et al., Citation2019). This empirical result shows that when the level of CGD surpassed the transition point, the ARQ of a company will positively improve. Particularly, it is also corroborating with research methodology of, Chen and Lee (Citation2017) that applied the PSTR model to assess whether the CGD level reflects a nonlinear two regime relationship between CGD and ARQ.

Table 11. The effect of CGD’s dimensions and ARQ

Furthermore, results from transition parameters identify that the predicted threshold of CGD level is approximately 51 (out of total score of 81). As explained, once the CGD score is less than 51, the association between CGD and ARQ is unpredicted. Under these circumstances, the effect of CGD and ARQ could be positive, negative or neutral which explain the heterogeneous phenomenon in the literature review as Haniffa (2015), Khan et al. (Citation2013), Jizi et al. (Citation2014), Nguyen and Huong (Citation2021), Zin et al., (2020), Mukhibad and Setiawan (Citation2020), , Lauwo et al. (Citation2016), Ridho (Citation2016). It also means that if a company achieves a low CGD score (less than 51), the more investment in CGR does not equivalent to the more quality of annual reports. Our findings could be interpreted as number of reasons: firstly, initial investment on corporate governance may incur high marginal cost, moreover, companies with little expertise and a poor reputation in CGD may find that the marginal cost exceeds the marginal benefit. As a result, they do not have incentives to more invest into annual reports which has to raise the operational expenses and risk losing its viability. Some companies also consider the investment in CGD is sufficient, lowering the firm performance. Secondly, when the marginal benefit exceeds the cost (as illustrated in Equationequation (1)(1)

(1) , CGD > c) CGD is a positive indicator to corporate performance as well as financial result. As a result, a company could earn more capital investment, reduce agency cost, improve operational efficiency, corporate reputation, corporate performance and corporate value by issuing good quality of annual reports. On the other hands, the firms below the threshold number are those which do not invest enough in annual reports.

The result from Table also indicate the slope of the transition function (γ) which illustrates the transition speed. The greater the (γ) value, the sharper the transition between two scenarios. If a firm with a CGD level that is below the threshold of 51, the relationship between level of CGD and ARQ is unpredicted. However, we would like to confirm that our threshold is only related to developing economies where companies focus on CGD in order to earn more financial benefit.

When it comes to the effect of each attribute of CGD, the coefficient of CGD-RIGHTS, CGD-ROLE, CGD-DISCLOSURE, CGD-BOD (β0) are positive and significant across all regressions. Each dimension of CGD also appear to have a nonlinear impact on ARQ. However, the result shows that the threshold value varies between four independent variables. In detail, the cutoff values of CGD-RIGHTS, CGD-ROLE, CGD-DISCLOSURE and CGD-BOD are 25, 18, 15 and 10 respectively. As above explanation, the ARQ is improved only when the score of the component Rights and fair treatment among shareholders of CGD exceeds the score 25, whereas the score of component Role of stakeholders, Disclosure and transparency and Responsibilities of board of directors exceed 18, 15 and 10 respectively. Interestingly, the variable CGD-ROLE associated with the highest cutoff value (18 points out of total 20). This finding suggests that a company, which has more information disclosure on role of stakeholders of corporate governance reports, will also more invest on annual reports.

Finally, empirical results show that the majority of the control variables do not have the anticipated sign. Only LEVERAGE has positive and significant coefficients, two other control variables that are SIZE and S-GROWTH have no statistical effect on ARQ. Although the findings are not aligned with the previous studies of Kend (Citation2015), Khan et al. (Citation2013), who investigated that strong sales growth and firm size have substantial positive coefficient. They explained that huge firms in terms of size and sales figures are better able to invest in annual reports and corporate governance disclosure. In addition, debt ratio (LEVERAGE) is found to be negative and significant in literature.

4.6. Robustness Tests

After conducting the OLS regression, we applied the fixed effects model (FEM) to provide more evidence of the robustness of these result. Particularly we applied Wald test to examine the heteroskedasticity phenomenon. The following hypothesis is given for the Wald test:

H0: data is homoscedastic

H1: data is heteroscedastic

Table 12. Wald test result in fixed effect regression model

5. Conclusion

The objective of this research is to investigate the association between the level of CGD and ARQ in the context of Vietnam. Most prior research in literature review argued that CGD and ARQ have a mixed effect of positive, negative or neutral linear connection. Additionally, the empirical literature highlights inclusive results that addressed the research issues in different contexts. Starting with the controversial theoretical background, the paper strove to contribute to the ongoing debate by investigating the potential nonlinearity of the relationship between CGD and ARQ. Moreover, the methodology also aims to examine the effect of each CGD’s attributes, including Rights and fair treatment among shareholders (CGD-RIGHTS), Role of stakeholders (CGD-ROLE), Disclosure and transparency (CGD-DISCLOSURE) and Responsibilities of Board of Directors (CGD-BOD) and ARQ.

In order to achieve the above objectives, the authors firstly, employ bibliometric analysis to develop a comprehensive existing literature review and secondly, apply the PSTR model to test the whether the relationship between the level of CGD and ARQ and the relationship between CGD’s dimensions and ARQ is nonlinear. The sets of VLCA scorecard are used to measure CGD and ARQ of 356 listed companies in Vietnam from 2017 to 2022.

The research results illustrate the following findings: First, each set of VLCA’s questionnaires is internal consistent. In other words, the test items are considered to be valid and reliable for exploratory studies. Second, the relationship between CGD and ARQ is nonlinear. In detail, findings suggest that in the first regime, when the score of CGD (equivalents to the level of CGD) exceeds the threshold of 51, the higher level of CGD the more quality of annual reports. However, when the CGD level is less than 51, the more investment in CGD does not promote a good quality of annual reports. These findings depict a current practice in emerging economies, particularly in Vietnam, that almost all companies with limited competence or weak reputation in corporate governance may find that the marginal benefit is initially minimal in comparison to the marginal cost they need to invest. However, when their corporate governance investment expands to reach above the 51-point value transition barrier and attracts more public attention and increase capital investments from investors, CGD becomes a positive factor to ARQ.

Specifically, the research result also indicates that a nonlinear relationship exists between each CGD’s dimension. It is important to note that the highest threshold level is associated with the role of stakeholders (CGD-ROLE) attribute. This finding could be interpreted that Vietnamese listed companies tend to focus on ARQ under the impact of stakeholders such as potential investors, the Government, creditors, financial institutions, etc. Moreover, when the role of stakeholders reaches a particular threshold, the public starts to be interested in firms’ information and CGD positively connects with ARQ.

Basing on this finding, the Vietnamese Government and regulators should improve the quality of annual reports by require listed companies to achieve a minimum score (threshold level) of CGD. As a result, Governments of developing countries should emphasize on the mechanism of CGD and corporate governance framework in order to improve the ARQ and in turn to strengthen the securities exchange market. The research result also states that stakeholders are placing a higher impact on ARQ than other dimensions of corporate governance, suggesting that Vietnamese firms should maintain strong relationship in the community in order to avoid friction with key stakeholders. Managers of companies might benefit from this study’s implications as they can have a better understanding on the link between corporate governance mechanism and annual reports. They also increase the quality of annual reports by more investing into corporate governance especially on commitment with related stakeholders.

In conclusion, despite of contributions on academic and current practice perspectives, the authors acknowledge that the findings might be different in the context of different countries which are affected by different macroeconomics pattern. Therefore, the future research would like to investigate the relationship between CGD and ARQ in emerging countries by applying data from other countries.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Manh Dung Tran

Manh Dung Tran Assoc. Prof. Dr. Manh Dung Tran is an associate editor of Journal Economics and Development of National Economics University, Vietnam. His major research focuses on economics, accounting, auditing and finance. He has published a number of research papers on these areas in national and international journals.

Author’s ORCID identifier is 0000-0002-9864-9304

Hong Hanh Ha

Hong Hanh Ha Dr Hong Hanh Ha is a senior lecturer of Accounting and Auditing School, National Economics University (NEU), Hanoi, Vietnam. She has been teaching as a full-time lecturer at National Economics University for 12 years. Her major research focuses on accounting, auditing, accounting information system and internal control. She has published several research papers in these areas in national and international journals.

References

- Abaidoo, R., & Agyapong, K. E. (2022). Financial development and instituational quality among emerging economies. Journal of Development, 24(3), 198–32. https://doi.org/10.1108/JED-08-2021-0135

- Abdelhak, E., Hussainey, K., & Albitar, K. (2022). Covid-19 disclosure: Do internal corporate governance and audit quality matter? International Journal of Accounting and Information Management. https://doi.org/10.1108/IJAIM-05-2022-0108

- Ahmed, K., & Courtis, K. J. (1999). Associations between corporate characteristics and disclosure levels in annual reports: A meta-analysis. The British Accounting Review, 31 (1), 35–61.

- Allegrini, M., & Greco, G. (2011). ‘Corporate boards, audit committees and voluntary disclosure: Evidence from Italian Listed Companies’. Journal of Management & Governance, 15(3), 1–30.

- Allegrini, M., & Greco, G. (2013). Corporate boards, audit committees and voluntary disclosure: Evidence from Italian listed companies. Journal of Management Government, 17, 187–216. https://doi.org/10.1007/s10997-011-9168-3

- Al. N, N., Adiloglu, B., & Taylan, A. A. (2007). Evolution of reporting on corporate social responsibility by the companies in ISE national-30 Index in Turkey. Social Responsibility Journal, 3(3), 19–25. https://doi.org/10.1108/17471110710835545

- Alsaeed, K. (2006). The association between firm specific characteristics and disclosure: The case of Saudi Arabia. Managerial Auditing Journal, 21(5), 476–479. https://doi.org/10.1108/02686900610667256

- Alzeban, A. (2020). The relationship between the audit committee, internal audit and firm performance. Journal of Applied Accounting Research.

- Aras, G., Aybars, A., & Furtuna, K. O. (2010). Managing corporate performance: Investigating the relationship between corporate social responsibility and financial performance in emerging markets. International Journal of Productivity and Performance Management, 59(3), 229–254. https://doi.org/10.1108/17410401011023573

- Bhasin, M., & Shaikh, M. J. (2016). Economic value added and shareholders' wealth creation: The portrait of a developing Asian country. International Journal of Managerial and Financial Accounting, 5(2), 107–137.

- Boateng, R. N., Tawiah, V., & Tackie, G. (2022). Corporate governance and voluntary disclosures in annual reports: A post international financial reporting standard adoption evidence from an emerging capital market. International Journal of Accounting and Information Management, 30(2), 252–276. https://doi.org/10.1108/IJAIM-10-2021-0220

- Broadstock, D. C., Chan, K., Cheng, L. T., & Wang, X. (2020). The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Responsibility Letter, 38. https://doi.org/10.1016/j.frl.2020.101716

- Cadbury Committee. (1992), Report of the committee on the financial aspects of orporate governance, Vol.1, GEE

- Camfferman, K., & Cooke, T. E. (2002). An Analysis of Disclosure in the Annual Reports of UK and Dutch Companies. Journal of International Accounting Research, 1, 3–30.

- Cerbioni and Parbonetti. (2007). Exploring the effects of corporate governance on intellectual capital disclosure: An analysis of european biotechnology companies. European Accounting Review, 1–52.

- Chen, R. C. Y., & Lee, C. (2017). The influence of CSR on firm value : An application of panel smooth transition regression on Taiwan. Applied Economics, 49(34), 3422–3434.

- Collett, P., & Hrasky, S. (2005). Voluntary disclosure of corporate governance practices by listed Australian companies. Corporate Governance: An International Review, 13(2), 188–196. https://doi.org/10.1111/j.1467-8683.2005.00417.x

- COSO. (2013). Internal Control – Integrated Framework. John Wiley & Sons, Inc., Hoboken, New Jersey. 978-1-118-62641-2.

- Crifo, P., Escrig-Olmedo, E., & Mottis, N. (2019). “orporate governance as a key driver of corporate sustainability in France. the Role of Board Members and Investor Relations, Journal of Business Ethics, 159, 1127–1146. https://doi.org/10.1111/joes.12055

- Dao Thi, T. B., & Ta Dieu, N. T. (2020). A meta-analysis: Capital structure and firm performance. Journal of Economics and Development, 22(1), 111–129. https://doi.org/10.1108/JED-12-2019-0072

- Elshabasy, Y. N. (2018). The impact of corporate characteristics on environmental information disclosure: An empirical study on the listed firms in Egypt. Journal of Business and Retail Management Research, (2), 232–241. https://doi.org/10.24052/JBRMR/V12IS02/TIOCCOEIDAESOTLFIE

- Fok, D., Van Dijk, D., & Franses, P. (2005). A multi-level panel STAR model for US manufacturing sectors. Journal of Applied Econometrics, 20(6), 811–827. https://doi.org/10.1002/jae.822

- Galant, A., & Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research, 30(1), 676–693.

- Gerayli, S. M., Pitenoei, R. Y., & Ahmad, A. (2021). Do audit committee characteristics improve financial reporting quality in emerging markets? Evidence from Iran. Asian Review of Accounting, 29(2), 251–267. https://doi.org/10.1108/ARA-10-2020-0155

- Ghazali, N. A. M. (2009). Voluntary disclosure in Malaysian corporate annual reports: Views of stakeholders. Social Responsibility Journal. Issue, 4(4), 504–516. https://doi.org/10.1108/17471110810909902

- Gonzalez, A., Teräsvirta, T., & Van Dijk, D. (2018). Panel smooth transition regression models. Working paper series in economics and finance, No. 60 Uppsala University: Uppsala. Sweden, 2018.

- Green, B. S. (1991). How many subjects does it take to do a regression analysis. Mathematics and Statistics Journals, 26(3). https://dx.doi.org/10.1207/s15327906mbr2603_7

- Ha, H. H. (2022). Audit committee characteristics and corporate governance disclosure: Evidence from Vietnam listed companies. Cogent Business and Management, 9(1), https://doi.org/10.1080/23311975.2022.2119827

- Ha, L. T., & Finch, N. (2022). Effects of trend inflation on monetary policy and fiscal policy shocks in Vietnam. Journal of Economics and Development, 24(2), 158–175. https://doi.org/10.1108/JED-04-2021-0052

- Hahn, R., & Kuhnen, M. (2013). Determinants of sustainability reporting: A review of results. Trends, Theory, and Opportunities in an Expanding Field of Research, Journal of Cleaner Production, 59, 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS -SEM). In European Journal of Tourism Research. Sage Publication.

- Henseler, Henseler, J., & Chin, W. W. (2010). A comparison of approaches for the analysis of interaction effects between latent variables using partial least squares path modeling. Structural Equation Modeling: A Multidisciplinary Journal, 17(1), 82–109. https://doi.org/10.1080/10705510903439003

- Ho, R. (2006). Handbook of unvariate and multivariate data analysis and interpretation with SPSS 1st edition. Chapman and Hall Publishing.

- Hsu, Y., & Yang, Y. (2022). Corporate governance and financial reporting quality during COVID-19 pandemic. Finance Research Letters, (47), 1–13. https://doi.org/10.1016/j.frl.2022.102778

- Hussain, A. I., Chatha, S. A. S., Anwar, F., Latif, S., Sherazi, S. T. H., Ahmad, A., & Sarker, S. D. (2013). Chemical composition and bioactivity studies of the essential oils from two Thymus species from the Pakistani flora. LWT – Food Sciences and Technology, 50, 185–192.

- Ikram, M., Sroufe, R., Mohsin, M., Solangi, Y. A., Shah, S. Z. A., & Shahzad, F. (2019). Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. Journal of Global Responsibility, (11)(1), 27–53. https://doi.org/10.1108/JGR-12-2018-0088

- Jizi, M. I., Salama, A., Dixon, R., & Stratling, R. (2014). Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of Business Ethics, 125(4), 601–615. https://doi.org/10.1007/s10551-013-1929-2

- Kend, M. (2015). Governance, firm-level characteristics and their impact on the client’s voluntary sustainability disclosures and assurance decisions. Sustainability Accounting, Management and Policy Journal, 6(1), 54–78. https://doi.org/10.1108/SAMPJ-12-2013-0061

- Kent, P., & Zunker, T. (2013). Attaining legitimacy by employee information in annual reports. Accounting, Auditing and Accountability Journal, 26(7), 1072–1106. https://doi.org/10.1108/AAAJ-03-2013-1261

- Khan, A., Muttakin, M. B., & Siddiqui, J. (2013). Corporate governanceand corporate social responsibility disclosures: Evidence from anemerging economy. Journal of Business Ethics, 114(2), 207–223. https://doi.org/10.1007/s10551-012-1336-0

- Kim, K. H., Kim, M., & Qian, C. (2018). Effects of corporate social responsibility on corporate financial performance: A competitiveaction perspective. Journal of Managment, 44, (1097–1118). https://doi.org/10.1177/0149206315602530

- Kumari, T., & Vincent, T. N. (2022). Capturing non-financial information in integrated reporting. International Journal of Business Information Systems, (40)(1), 98–116. https://doi.org/10.1504/IJBIS.2022.122879

- Kumar, K., Kumari, R., Nandy, M., Sarim, M., & Kumar, R. (2022). Do ownership structures and governance attributes matter for corporate sustainability reporting? An examination in the Indian context. Management of Environmental Quality: An International Journal, 33(5), 1077–1096. https://doi.org/10.1108/MEQ-08-2021-0196

- Lauwo, S. G., Otusanya, O. J., & Bakre, O. (2016). Corporate social responsibility reporting in the mining sector of Tanzania: (Lack of) government regulatory controls and NGO activism. Accounting, Auditing and Accountability Journal, 29(6), 1038–1074. https://doi.org/10.1108/AAAJ-06-2013-1380

- Lazarides, T. (2010). Corporate governance law effect in Greece. Journal of Financial Regulation and Compliance, 18(4), 370–385.

- Lin, W. L., Law, S. H., Ho, J. A., & Sambasivan, M. (2019). The causality direction of the corporate social responsibility – Corporate financial performance Nexus: Application of Panel Vector Autoregression approach. Journal of Economics and Finance, 48, (401–418 doi:10.1016/j.najef.2019.03.004).

- Madi, K. H., Ishak, Z., & Manaf, A. A. N. (2014). The impact of audit committee characteristics on corporate voluntary disclosure. International Conference on Accounting Studies, ICAS 2014, 19

- Mahdi, R. O., Mohd, G. B. S. E., & Almsafir, K. M. (2014) ‘Empirical Study on the Impact of Leadership Behavior on Organizational Commitment in Plantation Companies in Malaysia ‘ 2nd World Conference On Business, Economics And Management - WCBEM 2013

- Mahmood, M., & Orazalin, N. (2017). Green governance and sustainability reporting in Kazakhstan’s oilgas, and mining sector: Evidence from a former USSR emerging economy. Journal of Cleaner Production, 64, 389–397. https://doi.org/10.1016/j.jclepro.2017.06.203

- Maingot, M., & Zeghal, D. (2008). An analysis of corporate governance information disclosure by Canadian banks. Corporate Ownership and Control, (5)(2), 225–234. https://doi.org/10.22495/cocv5i2c1p7

- MCCG. (2017). Malaysian Code on Corporate Governance. Securities Commission Malaysia.

- McGee, R. W., & Tarangelo, T. (2009). The timeliness of financial reporting and the Russian banking system: An empirical study. Accounting Reform in Transition and Developing Economies, 467–487. https://doi.org/10.1007/978-0-387-25708-2_34

- Merlin, A., & Visser, W. T. (2002). Culture, corporate governance and disclosure in Malaysian corporations. Corporate Environmental Strategy Issue, 9, 79–85. https://doi.org/10.1111/1467-6281.00112

- Ministry of Finance. (2015). Circular 155/2015/TT – BTC. Ministry of Finance.

- Mousa, G. A., Desoky, A. M., & Khan, G. U. (2018). The association between corporate governance and corporate social responsibility disclosure – Evidence from Gulf cooperation council countries. Academy of Accounting and Financial Studies Journal, 22(4), 581–593.

- Mukhibad, H., & Setiawan, D. (2020). Could risk, corporate governance, and corporate ethics enhance social performance? Evidence from Islamic Banks in Indonesia. Indian Journal of Finance. Issue, 14(4), 24–38. https://doi.org/10.17010/ijf/2020/v14i4/151706

- Nguyen, T., & Huong, T. (2021). Measuring financial inclusion: A composite FI index for the developing countries. Journal of Economics and Development, 23(1), 77–99. https://doi.org/10.1108/JED-03-2020-0027

- Nobanee and Ellili. (2022). Impact of economic, environmental and corporate responsibility reporting on financial performance of UAE banks. Environment, Development and Sustainability. https://doi.org/10.1007/s10668-022-02225-6.

- OECD. (2004). OECD principles of corporate governance. Retrieved March 10, from https://www.oecd.org/daf/ca/corporategovernanceprinciples/31557724.pdf

- Othman, B. H., & Zeghal, D. (2010). Investigating transparency and disclosure determinants at firm-level in MENA emerging markets. International Journal of Accounting Auditing and Performance Evaluation, 6(4), 368–396.

- Owusu – Ansha, S., & Ganguli, G. (2010). Voluntary reporting on internal control systems and governance characteristics: An analysis of large U.S companies. Journal of Managerial Issues, 22(3), 383–408. https://doi.org/10.2307/20798918

- Rao, K. K., Tilt, C. A., & Lester, L. H. (2012). Corporate governance and environmental reporting: An Australian study. Corporate Governance, 12(2), 143–163. https://doi.org/10.1108/14720701211214052

- Ridho, K. T. (2016). The influence of csr on performance and its determinants in listed companies in indonesia. National Academy of Management.

- Saad, S. M., Ahmad, S. N. S., Jusoff, K., Daud, M. M., & Rahim, M. A. (2009). Income statements transparency and firms’ characteristics of companies listed on the Bursa Malaysia. American Journal of Applied Sciences, 6(9), 1718–1724. https://doi.org/10.3844/ajassp.2009.1718.1724

- Sadou, A., Alom, F., & Laluddin, H. (2017). Corporate social responsibility disclosures in Malaysia: Evidence from large companies. Social Responsibility Journal, 13(1), 177–202. https://doi.org/10.1108/SRJ-06-2016-0104

- Said, R., Zainuddin, Y., & Haron, H. (2009). The relationship betweencorporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal, 5(2), 212–226. https://doi.org/10.1108/17471110910964496

- Shamil, M., Shaikh, J., Ho, P.-L., & Krishnan, A. (2014). The influence of board characteristics on sustainability reporting: Empirical evidence from Sri Lanka firms. Asian Review of Accounting, 22(2), 78–97. https://doi.org/10.1108/ARA-09-2013-0060

- Sharma, P., Panday, P., & Dangwal, R. C. (2020). Determinants of environmental, social and corporate governance (ESG) disclosure: A study of Indian companies. International Journal of Disclosure and Governance, 17(4), 208–217. https://doi.org/10.1057/s41310-020-00085-y

- Soepriyanto, G., Meiryani, M., & Modjo, I. M. (2021) Theory and factors influencing fraud in financial statements: A systematic literature review. The 6th International Conference on E-business and Mobile Commerce

- Surroca, J., Tribó, J. A., & Waddock, S. (2009). Corporate responsibility and financial performance: The role of intangible resources. Strategic Management Journal, (31), 463–490. https://doi.org/10.1002/smj.820

- Tauchen, G. (1986). Finite state markov – Chain approximations to univariate and vector autoregressions. Economics Letters, 20(2), 177–181. https://doi.org/10.1016/0165-1765(86)90168-0

- Ting, I. W. K., Azizan, N. A., Bhaskaran, R. K., & Sukumaran, S. K. (2019). Corporate social performance and firm performance: Comparative study among developed and emerging market firms. Sustainability, 12(1), 26. https://doi.org/10.3390/su12010026

- Van der Zahn, J. (2004). Association between board of director characteristics and the amount of voluntary audit committee disclosures. International Journal of Business Governance and Ethics, 1(2/3), 210–232. https://doi.org/10.1504/IJBGE.2004.005256

- Vogt, M., Hein, N., Da Rosa, F. S., & Degenhart, L. (2017). Relationship between determinant factors of disclosure of information on environmental impacts of Brazilian companies. Estudios Gerenciales. Issue, 142(142), 24–38. https://doi.org/10.1016/j.estger.2016.10.007

Appendix 1:

VLCA 2022 Vietnam Corporate Governance Disclosure Scorecard