Abstract

Since its outbreak, Covid-19 has led to upsurge in economic inactivity, leaving many households and firms without access to and use of basic services including financial services. Specifically, with the lockdown and curfew, most traditional bank branches remained closed, leaving households without access to quality, affordable, convenient, and safe financial services. This study aims to establish whether contactless digital financial innovation like mobile money can promote access to and use of financial services in the presence of pandemic positive emotions in low-income countries. SmartPLS 3.0 was used to construct the structural equation mediation model with bootstrap based on 2,737 valid responses. It was found that contactless digital financial innovation such as mobile money significantly promotes access to and use of financial services in low-income countries under pandemic situation. Additionally, the findings showed that the use of contactless digital financial innovation promotes Covid-19 standard operating procedures in low-income countries. Cognizant to the role of human behaviour in technology adoption and usage, the structural equation model with bootstrapping revealed a 4 percentage points improvement in Covid-19 standard operating procedures due to the use of contactless mobile money channel. Accordingly, the findings could be useful in the following ways: governments in low-income countries may use it to promote public health concern under pandemic situations. Mobile money can allow individuals to store, send, and receive money during situation of limited or no movements caused by pandemic health restrictions. Besides, the use of contactless digital financial innovation may promote digital commerce in low-income countries under the pandemic situation. Similarly, mobile money can be used to promote government-to-person, person-to-person, person-to-business, and business-to-person payments under emergency situations. The findings may also help governments in low-income countries to rethink about taxes levied on mobile money.

PUBLIC INTEREST STATEMENT

While globalization comes with several positive benefits, especially to developing economies, it may present itself with negative effects such as the spread of infectious diseases. The recent outbreak of Covid-19 corroborates with past evidence, which indicates that the increased spread of infectious diseases from South to North to East and to West and from West to East to North and to South is due to globalization. Accordingly, international health institutions including governments in the world have appropriately implemented standard operating procedures (SOPs) to curb erratic spread of contagious diseases. Linking this to contactless digital financial innovation, use of mobile money combined with broaden-and-build theory that drive human thoughts and actions can limit sporadic spread of contagious diseases. This can reduce fatalities caused by these diseases contracted mostly through human-to-human physical contacts. Mobile money can help individuals to buy goods and services remotely under situation of limited movements caused by contagious and virulent diseases.

1. Introduction

Currently, the world economies are experiencing unprecedented challenges caused by the novel coronavirus (Covid-19) pandemic. This has greatly disrupted human lives and economic activities in different countries. Globally, the current infection rate from the virus stands at 760,360,950 people with 6,873,477 recorded deaths (World Health Organization, Citation2023). Contextually, Uganda has recorded about 170,409 cases and 3,630 confirmed deaths from the virus as of 1 March 2023 (Worldometer, Citation2023; Ministry of Health in Uganda, Citation2023).

Thus, in an attempt to contain the further spread and deaths from the virus, countries have imposed pandemic mitigation measures recommended by the World Health Organization in a bid to “flatten the curve” (see, e.g., World Health Organization, Citation2020). Specifically, mitigation measures such as lockdown, physical social distancing, travel ban, closures of public spaces and transport, mandatory quarantine, curfew, maintaining hand hygiene, wearing of face mask, and working remotely at home have been implemented by most governments to contain the spread of the virus. Succinctly, these measures have resulted in spurts of economic inactivity with most individuals without access to and use of basic goods and services including financial services (see, e.g., World Bank, Citation2020).

Consequently, the Global System for Mobile Communications-GSMA (Citation2020) suggests that the use of seamless, remote, and easy-to-use digital financial channel like mobile money has the potential to foster resilience by facilitating safe, efficient, and convenient money transfer and payment services among users under the Covid-19 pandemic situation. The United Nation Capital Development Fund (UNCDF, Citation2020) also contends that the use of digital payments through mobile money can enable key financial flows to quickly meet the financial needs of the underbanked population during emergency situation caused by the Covid-19 pandemic.

Scholars like Okello Candiya Bongomin et al. (Citation2021a); Okello Candiya Bongomin and Ntayi (Citation2020); and Arner et al. (Citation2020) argue that digital financial innovation like mobile money, which enables remote transactions, can effectively facilitate and provide feasible access to financial services such as payments, savings, credit, and insurance during the Covid-19 situation since it reduces human-to-human contact.

Auer et al. (Citation2020) further state that contactless digital payments through mobile money can promote merchant payments and support the social distancing measures since it limits physical cash transaction and in-person interaction along the supply chain. Moreover, mobile money can help individuals to smooth consumption and manage risk under the situation of lockdown caused by the Covid-19 pandemic.

In addition, Bangura (Citation2016) and Dumas et al. (Citation2017) also indicate that contactless digital payments through mobile money can be used for social safety net cash transfers, local and international remittances, emergency fund transfers, and payment of salaries and fees to essential workers during the pandemic crisis. Mobile money can allow payments and transfers to be effected remotely to offer financial support to reach those in need when other forms of disbursements become cumbersome due to restricted movements under strict health guidelines (see, e.g., Demirguc-Kunt et al., Citation2020). Thus, the adoption and use of innovative digital solution and technology tool like mobile money can boost resilience and slow the spread of the Covid-19 (Nalletamby, Citation2020).

In light of the above, while the mobile money technology seems helpful under the pandemic situation, the seminal work by Straub (Citation2009) points to the fact that successfully facilitating technology adoption and use is determined by its perceived usefulness and perceived ease of use grounded in cognitive, emotional, and contextual concerns of the individual users. Furthermore, Lerner, Small, and Loewenstein (Citation2004) also argue that positive emotions among individuals guide specific judgments and choices to adopt and use technology to respond to a significant crisis in the environment. This is based on emotional carryovers and experiences among individuals under such situation of crisis in the environment (see, e.g., Barrett & Campos, Citation1987; Schwarz, Citation1990), which fuel their judgments and decisions to adopt and use new technology such as mobile money under such situation (see, e.g., Lerner & Keltner, Citation2000).

Accordingly, the adoption and use of mobile money technology by individuals under a situation of crisis such as the Covid-19 pandemic are determined by its perceived usefulness and perceived ease of use driven by cognition, emotions, and context. The emotional carryovers and experience among the individuals determine their judgments and decisions to adopt and use mobile money technology for payments and transfers to respond to the Covid-19 crisis.

Whilst studies such as Okello Candiya Bongomin et al. (Citation2021a), Okello Candiya Bongomin et al. (Citation2021b), Ozili (Citation2018), World Bank (Citation2020), Baganzi and Lau (Citation2017), Suri and Jack (Citation2016), Nampewo et al. (Citation2016), Demirguc-Kunt et al. (Citation2018), Dupas and Robinson (Citation2013), Muralidharan et al. (Citation2016), and Economides and Jeziorski (Citation2017) among others have linked mobile money adoption and usage to access to and use of financial services, they make no reference to its adoption and usage under the global pandemic situation. Besides, although the unified theory of acceptance and use of technology (UTAUT2) and technology adoption model (TAM) have been used to explain technology adoption and usage, limited evidence exist, which combines UTAUT2 and TAM with Appraisal Tendency Framework (ATF) to articulate mobile money adoption and usage under the pandemic situation. Therefore, this study intends to establish whether contactless digital financial innovation like mobile money can significantly promote Covid-19 pandemic mitigation measures mediated by pandemic-positive emotions in low-income countries with evidence from Uganda.

2. Sociological and psychological theoretical underpinnings

2.1. Unified Theory of Acceptance and Use of Technology (UTAUT2) and Technology

Acceptance Model (TAM)

The UTAUT developed by Venkatesh et al. (Citation2012) conceives that behavioral intention to use a technology is determined by originally four constructs of performance expectancy, effort expectancy, social influence, and facilitating conditions. However, as a result of theory growth, hedonic motivation, price value, and habit moderated by age, gender, and experience in the consumer context were added to UTAUT to form UTAUT2. The new UTAUT2 assumes that performance expectancy, effort expectancy, and social influence are theorized to influence behavioral intention to use a technology. While behavioral intention and facilitating conditions determine technology use combined with hedonic motivation, price value, and habit moderated by age, gender, and experience in the consumer context. Relatedly, the technology acceptance model (TAM) rooted in the theory of reasoned action by Ajzen and Fishbein (Citation1980) posits that perceived ease of use, perceived usefulness, attitude regarding use, and behavioral intention predict actual usage of technology by individuals. Therefore, the adoption and use of mobile money technology to promote pandemic mitigation measures are determined by performance expectancy, effort expectancy, social influence, and facilitating conditions combined with hedonic motivation, price value, and habit moderated by age, gender, and experience together with perceived ease-of-use, perceived usefulness, and attitude of individuals stipulated under the UTAUT2 and TAM.

2.2. Appraisal Tendency Framework (ATF)

The ATF linked to cognitive appraisal and functional theories of emotions postulate that specific emotions give rise to specific cognitive and motivational processes. The ATF suggests that emotion carries with it motivational properties, cognitive appraisals, and themes. These derive the content and depth of thoughts, which fuel judgments and decisions by individuals under a situation of crisis (Lerner & Keltner, Citation2000). Lazarus (Citation1991a) and Raghunathan and Pham (Citation1999) observe that emotions characterized by appraisal themes of uncertain existential threats help anxious people to choose an option that reduces risk under the situation of crisis. Bodenhausen, Kramer, & Siisser (Citation1994), Forgas and Bower (Citation1987), and Schwarz and Clore (Citation1983) further contend that positive emotions produced by experiencing a crisis or relieving stressful events have an influence on consumer judgment and decision-making. This is achieved through recall of past emotional experiences and events (Smith & Ellsworth, Citation1985). Additionally, positive emotional valence derived from a situation of crisis may influence individuals to make judgments and decisions for precautionary measures associated with fear about the uncertainty of novel situations such as the Covid-19 crisis. Consequently, positive emotions combined with emotional valence and past experiences of a situation of crisis like a pandemic outbreak characterized by appraisal themes of uncertain existential threats may help individuals to make sound judgments and decisions to adopt and use mobile money technology under the novel Covid-19 situation.

3. Literature and hypothesis development

3.1. Contactless digital financial innovation and pandemic mitigation measures

Presently, with the ever up-surging trends in global infection rates and deaths resulting from the Covid-19 pandemic, most countries have continued to impose mitigating measures among its population to contain the spread of the virus. Thus, with the lockdown and closure of most traditional bank branches, most individuals have remained unbanked and underbanked with limited or no access to financial services (World Bank, Citation2020).

The Consultative Group to Assist the Poor-CGAP (Citation2020) suggests that the use of digital financial technology through digitization of financial services such as payments, savings, insurance, and remittances over the mobile money platform can make significant progress towards financial inclusion of the unbanked and underbanked population under the Covid-19 pandemic. Demirguc-Kunt et al. (Citation2020) also state that mobile money has the potential to bring the unbanked population into the financial system by increasing access to and use of financial services remotely during a pandemic crisis. Mobile money can help users of mobile phones to deposit, transfer, pay, and withdraw money remotely without having a bank account (Global System for Mobile Communications-GSMA, Citation2020; Okello Candiya Bongomin et al. Citation2021a, Okello Candiya Bongomin et al. Citation2021b; Suri, Citation2017).

Besides, Pazarbasioglu et al. (Citation2020) observe that mobile money can facilitate the government to transfer money and other public services to individuals under a crisis such as Covid-19 situation. Indeed, mobile money can conveniently and affordably facilitate none peer-to-peer transactions and allow government to reach households and firms with emergency grants and support through G2P and G2B in a timely fashion during a pandemic crisis. The use of contactless digital payments through mobile money for G2P and G2B transfers can help to maintain social distancing and reduce the potential spread of Covid-19.

Furthermore, Agur et al. (Citation2020) also contend that the use of digital financial innovation like mobile money can permit remote payments and transactions. This promotes social distancing recommended in reducing contagion during the Covid-19 pandemic. Through digital payments over mobile money, consumers can transfer funds, pay bills, and pay for goods and services from home, or in a market or store setting, with limited or no physical contact.

A study by Bangura (Citation2016) and Dumas et al. (Citation2017) revealed that mobile money transfer significantly facilitated payments to frontline workers during the Ebola outbreak in Sierra Leone. Huang et al. (Citation2020) also found that reliance on fintech-based credit provision through mobile money improved SMEs’ shock resilience before and during the current Covid-19 pandemic in China. Certainly, the use of mobile money bridges the gap between cash and digital economies. This enable individuals to load cash in a mobile wallet and transact digitally and remotely using money transfers, deposits, withdrawals, and payments with no physical contact. Therefore, here we hypothesize that:

H1: Adoption and use of contactless digital financial innovation significantly promotes Covid-19 pandemic mitigation measures in low-income countries.

3.2. Pandemic positive emotions and contactless digital financial innovation

Bagozzi et al. (Citation1999) and Phillips and Baumgartner (Citation2002) state that anticipated emotions can be both positive and negative. Therefore, individuals may exhibit adaptive bias to approach and explore novel objects, people, or situations within their environments differently. The more intense are the positive anticipated emotions and the negative anticipated emotions, the more consumers are motivated to adopt behaviors needed to achieve the positive outcome or to avoid the negative consequence of their actions (Perugini & Bagozzi Citation2001). Particularly, positive anticipated emotions represent the positive feelings arising from the possibility to achieve a goal defined by stimuli or events in the environment.

Kahneman (Citation1999) and Diener (Citation2000) show that positive emotions signal health and well-being in the environment. This is supported by the broaden-and-build theory, which posits that positive emotions produce health and well-being (Fredrickson, Citation2001). As a result, positive emotions broaden peoples’ momentary thought–action repertoires that widen the array of thoughts and actions that come to mind. This creates the urge among individuals to explore, take in new information, and experiences, which expands their minds to deal with events such as Covid-19 crisis. Accordingly, they adopt and use contactless digital financial innovation like mobile money to avoid catching the virus.

Similarly, Frijda (Citation1986), Levenson (Citation1994), and Oatley and Johnson-Laird (Citation1996) argue that positive functional emotions, which serve an impressive coordination role, may trigger a set of responses (behavior, experience, and communication) that enable individuals to adopt and use mobile money to deal quickly with the health and well-being problem caused by the Covid-19 pandemic to avoid catching the virus.

Besides, Forgas (Citation1995) observes that emotions arising from fear based on incidental affect linked to affect-related cognitive processes can influence subsequent judgments and choices among individuals to adopt and use mobile money technology under a situation of Covid-19 crisis to avoid catching the virus.

Furthermore, Bower (Citation1981, Citation1991) and Isen, Shalker, Clark, and Karp (Citation1978) also show that people may selectively retrieve mood-congruent information from memory and then use it in judgments to make decisions to prevent risk. Consequently, people in good moods may make optimistic judgments and decisions to adopt and use mobile money technology to remotely perform transactions under the Covid-19 crisis (see, e.g., Kavanagh & Bower, Citation1985; Wright & Bower, Citation1992). Without a doubt, positive emotion-related cognition directs attention, memory, and judgment of individuals to adopt and use mobile money technology to address emotion-eliciting events such as contracting Covid-19 (see e.g., Johnson-Laird & Oatley, Citation1992; Lazarus, Citation1991a; Schwarz, Citation1990; Simon, Citation1967; Tooby & Cosmides, Citation1990).

Maria, Lorena, and Natalia (Citation2020) found that positive emotions and feelings of responsibility to adopt different ways including technology due to uncertainty, fear, and anguish greatly contributed towards adherence to Covid-19 mitigation measures in Argentina. Hence, here we hypothesize that:

H2: Pandemic positive emotions significantly promotes the adoption and use of contactless digital financial innovation under Covid-19 in low-income countries.

3.3. Contactless digital financial innovation and pandemic mitigation measures: role of pandemic positive emotions as mediator

According to Mulligan and Scherer (Citation2012), emotion is an intense feeling and a complex and usually a strong subjective response that is typically accompanied by physiological and behavioral changes in the body caused by stimuli. Thus, emotion is defined by a tendency to perceive new events and objects in ways that are consistent with the original cognitive-appraisal dimensions of the emotion.

Fredrickson (Citation2000) argues that emotions might improve the psychological well-being and physical health of individuals by cultivating experiences of positive emotions at opportune moments to cope with negative emotions. Correspondingly, Lazarus et al. (Citation1980), Folkman (Citation1997), and Folkman and Moskowitz (Citation2000) observe that experiences of positive affect during chronic stress may help people to cope. Aspinwall (Citation2001) also contends that positive affect and positive beliefs serve as resources for people coping with adversities such as the Covid-19 pandemic.

Studies like Komiak and Benbasat (Citation2006), Wood and Moreau (Citation2006), Zeeleberg, Nelisse, Breugelmans, and Pieters (Citation2008), and Anderson and Agarwal (Citation2011) show that decision-making itself is often an emotional process, which involves affective processes because it elicits forward-looking anticipated emotions (see, also, Bagozzi & Baumgartner, Citation2000; Perugini & Bagozzi, Citation2001). Therefore, anticipated positive emotions become relevant in influencing adoption and use decisions of products like mobile money because it affects behavior due to ease of use (see, e.g., Davis, Citation1989, Davis et al. Citation1989). The behavior to adopt and use mobile money product is motivated by the anticipated positive emotions that may occur such as fear to catch Covid-19 through human-to-human physical contact (see, e.g., Frijda, Citation1986).

Additionally, Lazarus (Citation1991a) argues that positive emotions characterized by appraisal themes of uncertain existential threats can help anxious people to choose an option, which reduces the individual’s risk. This provides a basis for predicting the influence of specific emotions on consumer decision-making. Therefore, fear caused by positive emotions defined by appraisals of uncertainty may help individuals to make wise judgments and decisions to adopt and use mobile money to maintain hand hygiene and keep physical social distancing to avoid catching Covid-19.

Agarwal and Prasad (Citation1998) and Wood and wait (Citation2002) also observe that when individuals are faced with a situation of crisis in a certain context, they tend to quickly adopt innovation such as mobile money technology supported by the surrounding environment. The World Bank (Citation2020) contends that due to fear of getting infected with Covid-19, individuals have adopted and switched to a cashless society through mobile wallets to enable peer-to-business payments to maintain hand hygiene.

Lerner, Gonzalez, Small, and Fischhoff (Citation2003) in a national field experiment conducted in the US in the aftermath of 11 September 2001 confirmed that fear resulting from positive emotions increased the perceived risk of terrorism and plans for precautionary measures. This finding was held across non-terror-related risks like getting flu. Thus, here we hypothesize that:

H3: Pandemic positive emotions significantly mediates the relationship between the adoption and use of contactless digital financial innovation and Covid-19 pandemic mitigation measures in low-income countries.

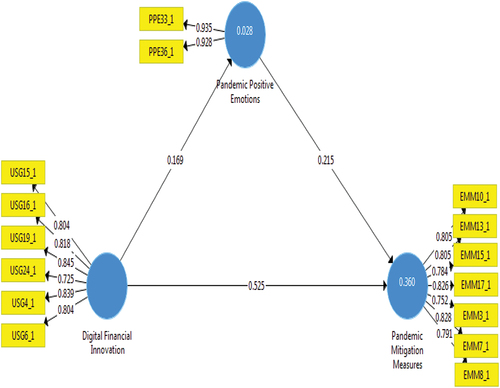

This study is guided by the proposed conceptual model in Figure .

Figure 1. Proposed conceptual model.

4. Methodology and approach

4.1. Research design

This study adopted a cross-sectional research design combined with both descriptive and analytical approaches. The data were collected at a specific point in time to test the hypotheses derived under this study. This design was adopted because of its ability to collect a large amount of data over a shorter period of time, especially in this time of the Covid-19 pandemic. In addition, this method was also used because it does not suffer from unavailability of samples common in longitudinal study since it looks at the population at one point in time. Besides, this design was adopted because it does not suffer from inherent mistakes in data collection instrument rampant while using longitudinal study.

4.2. Study area

The data for this study were collected from the four regions of central, northern, eastern, and western Uganda based on the Uganda Bureau of Statistics (UBOS) National Population and Housing census mapping (UBOS, Citation2014). The data were collected concurrently by 20 research assistants and 4 field supervisors located in the four regions.

4.3. Participants and samples

The participants for this study were selected from registered mobile money users and authorized mobile money agents residing in the four regions in Uganda. Overall, a total sample of 2,737 respondents participated in this study.

4.4. Sampling method and procedures

The sampling for this study was performed in two stages: First, purposive sampling was used to identify registered mobile money users and authorized mobile money agents. Second, simple probability sampling was used to select respondents from registered mobile money users and authorized mobile money agents to participate in this study. This was done to give all the participants equal chances to participate in the study. Additionally, in order to avoid collecting responses from the same samples, unique numbers were assigned to all respondents who were selected to provide responses in this study. Therefore, data were collected from a total of 2,386 registered mobile money users and 351 authorized mobile money agents.

4.5. Questionnaire and data collection

The data for this study were collected using a semi-structured questionnaire, which had items anchored on a 5-point Likert scale (from 1 = strongly disagree to 5 = strongly agree). This scale was used because of its versatility, clarity, simplicity, and wide applicability in social science research (see, e.g., Likert, Citation1932; John, Citation2010; DeVellis, Citation2003). The questionnaire was designed in line with guidelines recommended by Churchill and Iacobucci (Citation2004). The data for this study were collected by 20 research assistants using Kobocollect platform installed on Ipads/smart phones on which the questionnaire was uploaded. The research assistants were trained on the use of Kobocollect platform before the main data collection. Prior to start of the data collection exercise, the research assistants obtained the consent of all respondents before participating in the study. The research team also ensured that the recommended SOPs on Covid-19 issued by the World Health Organization and Ministry of Health in Uganda were observed throughout the data collection exercise, which lasted for a period of 60 days from 15 July to 15 September 2020.

4.6. Data analysis and management

The quantitative data for this study were analyzed using statistical packages for social sciences (SPSS) and SmartPLS 3.0 professional version. Preliminary analyses were performed on the data to check whether errors arising from incorrect data entry, missing values, and outliers existed in the data files (Field, Citation2005). Frequencies for all the items in the questionnaire were generated using SPSS to establish whether missing values were present in the data. The results indicated that missing values existed in the data and were missing at completely random (MCAR) at less than 3%. Thus, linear interpolation was used to replace the missing data as recommended by Field (Citation2005). Besides, box plots were used to test for the existence of outliers in the data. The results revealed that outliers were not a problem in our data and the results were tenable and good enough for further statistical analyses using SmartPLS 3.0.

4.7. Measures of research variables

The measures for the research variables used in this study were developed from previous studies referenced in internationally recognized journals. The measures for contactless digital financial innovation through mobile money were adopted from Okello Candiya Bongomin et al. (Citation2020), Alliance for Finance Inclusion (Citation2011); Aker et al. (Citation2016), and Suri and Jack (Citation2016), and the measurement items for pandemic mitigation measures were developed from SOPs recommended by the World Health Organization (Citation2020). Besides, the measures for pandemic positive emotions were developed from scholars such as Bagozzi et al. (Citation1999), Phillips and Baumgartner (Citation2002), and Lerner and Keltner (Citation2000). All the measurement items in the questionnaire were put on a 5-point Likert scale ranging from 1 = strongly disagree to 5 = strongly agree as indicated in appendix 1 and 2.

4.8. Common-method bias

The tests to establish whether common-method bias existed in this study were performed as stipulated by Bagozzi and Yi (Citation1988), Nunnally (Citation1978), and Spector (Citation2006). Two steps were adopted to test for common-method bias in this study. Statistically, exploratory factor analysis was performed on the variable of digital financial innovation through mobile money. The results revealed that none of the constructs emerged dominant. This confirmed that common-method bias was not a problem in this study as recommended by Podsakoff et al. (Citation2003). Furthermore, procedural remedy was also used to test for the presence of common-method bias in this study. This was performed on the measurement items by removing vague concepts, keeping questions simple, specific, and concise, avoiding double-barreled questions, and decomposing and making the questions easier and more focused to the variables under study (Tourangeau et al., Citation2000). Thus, a more refined questionnaire was developed and used in this study with no evidence of common-method bias.

4.9. Assumptions of parametric test

Statistical tests were performed to establish whether the data satisfied the assumption of parametric test. The tests for normality and homogeneity of variances were conducted on the data. Notably, two assumptions of interval data and independence of observation were left out since they are ascertained by common sense (Field, Citation2009). The assumption of normality was tested using the histogram, normal probability plots, and scatter plots. While homogeneity of variances was tested using the Levene’s test statistics. The results from the normality test revealed that the histogram was bell-shaped, and the normal probability plots had all the values falling along the straight line. Additionally, the results of the scatter plots showed that all the values were clustered together, thus, showing evidence of association. Besides, the Levene’s test statistics, results indicated that all the variables had variances that were stable at all levels and non-significant at p-value >0.05. This implied that the assumptions of normality and homogeneity of variances were met and tenable in this study (Hair et al., Citation2016).

4.10. Mediation test in Smart PLS

This study intends to establish whether contactless digital financial innovation like mobile money can significantly promote Covid-19 pandemic mitigation measures mediated by pandemic positive emotions in low-income countries with evidence from Uganda. The research model in Figure was tested using structural equation (SEM) modeling in SmartPLS bootstrap, which allow researchers to perform path analytic modeling with latent variables (Bollen, Citation1989). This study used a two-step modeling process proposed by Anderson and Gerbing (Citation1988) to establish the mediating effect. First, a measurement model was constructed; second, the structural model was constructed in SmartPLS 3.0 as recommended by Hair et al. (Citation2016).

4.11. Constructing measurement model

The measurement model was constructed to test for composite reliability and convergent and discriminant validity between the manifest and latent variables under this study taking into consideration the outer loadings in the model. The composite reliability was measured using Cronbach’s alpha (α) coefficient. The rule of thumb is that the composite reliability should have values greater 0.70 as recommended by Nunnally (Citation1978), Bagozzi and Yi (Citation1988), and Cronbach (Citation1971). Similarly, Fornell and Larcker (Citation1981) criterion was used to test for discriminant validity under this study. The rule of thumb requires that the diagonal correlation figures should be higher than the inter-construct correlations. More so, the average variance extracted (AVE) was also generated to test for the convergent validity of the manifest constructs. All the results were significant and tenable as recommended by Hair et al., (Citation2014).

4.12. Constructing structural model

The structural equation model was constructed to show the interrelationships between the manifest and latent constructs of the key variables in one complex model. While constructing the structural model, Hair et al. (Citation2016) suggest that the predictive relevance and effect size of the model should be established to determine the explanatory and effect of the predictor and mediator variables on the outcome variable. Consequently, a structural model combining all the variables under this study was constructed in SmartPLS through bootstrap with 5,000 samples to establish whether contactless digital financial innovation through mobile money can significantly promote Covid-19 pandemic mitigation measures mediated by pandemic positive emotions in low-income countries with evidence from Uganda. The findings are indicated in the preceding section.

5. Findings

5.1. Sample characteristics

The findings from this study indicated that most respondents were male (65%) as compared to female who comprised of 35%. The findings also showed that majority (39%) of the respondents were in the 26–33 age bracket, while those in the 34–41, 18–25, 42–49, and 50+ age bracket constituted 36%, 14%, 9%, and 2%, respectively. Besides, the findings indicated that 35% of the respondents reported having attained a secondary level of education followed by diploma (30%), bachelor degree (26%), postgraduate (4%), primary (3%), and no school (2%). Furthermore, the findings also showed that most (69%) respondents were married followed by those who were single (29%), separated (1%), and divorced (0.4%). Similarly, the findings revealed that most (92%) respondents who used mobile money lived in urban areas as compared to peri-urban (6%) and rural areas (2%). More so, the findings also indicated that most respondents (53%) had used mobile money services for 6–10 years while those who had used it for 11–15 years and 5 or less years were 25% and 22%, respectively. Additionally, the findings showed that most (36%) respondents used mobile money for withdrawals as compared to savings (34%), payments (27%), remittances (2%), and borrowings (1%). The findings further showed that almost all (99%) mobile money agents reported providing mobile money services to increasing number of users with high cash float needs during this time of Covid-19. Finally, the findings revealed that Mobile Telephone Network (MTN) had over 91% of mobile money subscribers followed by Airtel, Lycamobile, Africell, Uganda Telecom-UTL, and K2 Telecom, respectively. The sample characteristics are indicated in Table .

Table 1. Sample characteristics

5.2. Mediation test in Smart PLS

5.2.1. Measurement model

The measurement model results revealed that all the variables under this study had Cronbach’s alpha (α) coefficients above the threshold of 0.70 as recommended by Nunnally (Citation1978), Bagozzi and Yi (Citation1988), and Cronbach (Citation1971). The reliability results for the variables of contactless digital financial innovation through mobile money, pandemic mitigation measures, and pandemic positive emotions were 0.892, 0.906, and 0.848, respectively. The composite reliability (CR) for the variables of contactless digital financial innovation through mobile money, pandemic mitigation measures, and pandemic positive emotions were 0.918, 0.925, and 0.929, respectively. In addition, the results also indicated that the variables of contactless digital financial innovation through mobile money, pandemic mitigation measures, and pandemic positive emotions achieved convergent validity with AVE figures of 0.651, 0.639, and 0.868, respectively. Furthermore, the discriminant validity test results based on Fornell and Larcker (Citation1981) criterion also revealed that the diagonal correlation figures between the variables were higher than the inter-constructs correlations. The correlation figures for contactless digital financial innovation through mobile money, pandemic mitigation measures, and pandemic positive emotions were 0.807, 0.799, and 0.932, respectively. The results of the reliability, composite reliability, convergent and discriminant validity tests, and cross loadings are shown in Tables . Furthermore, the variance inflation factors (VIF) for the different manifest variables under this study were also assessed, and the results are indicated in Table .

Table 2. Construct reliability and validity for the key variables

Table 3. Discriminant validity for the key constructs

Table 4. Factor loadings and cross loadings for the key constructs

Table 5. Factor loadings significant for the key constructs

5.2.2. Structural model

The results of the path coefficients together with the t-values and p-values in the structural model revealed that pandemic positive emotions significantly mediates the relationship between contactless digital financial innovation through mobile money and Covid-19 pandemic mitigation measures in low-income countries (β = 0.036; t = 5.658; p < 0.0001). This finding supports hypothesis (H3) derived under this study. The inclusion of pandemic positive emotions into the structural model increases the predictive power of contactless digital financial innovation through mobile money by 4% to promote pandemic mitigation measures in low-income countries.

Furthermore, the results also indicated that the adoption and use of contactless digital financial innovation like mobile money significantly promotes Covid-19 pandemic mitigation measures in low-income countries (β = 0.561; t = 19.059; p < 0.0001). This finding supports hypothesis (H1) generated under this study.

Finally, the results showed that pandemic positive emotions significantly promotes the adoption and use of contactless digital financial innovation through mobile money in low-income countries (β = 0.169; t = 6.551; p < 0.0001). This finding supports hypothesis (H2) derived under this study. The results of the hypotheses testing are shown in Table .

Table 6. Results of hypotheses testing

5.3. Predictive relevancy of the model

Field and Hole (Citation2003) and Field (Citation2005) suggest that the predictive relevancy of a model can be determined by the coefficient of determination denoted by (R). This shows by how much the predictor variable explains the predicted value of the outcome variable. This depends on the sample size used in the study. Therefore, for larger samples, the adjusted coefficient of determination denoted by R2 is used to explain the predicted value of the outcome variable. However, for smaller samples, the coefficient of determination denoted by R is used to explain the predicted value of the outcome variable. Thus, the b-value should be significantly different from zero based on t-test statistic when variables referred to as predictor variables exert significant effects on outcome variable. The results from this study showed that the direct and indirect effects of contactless digital financial innovation through mobile money technology and pandemic positive emotions explain 36% of the variation in pandemic mitigation measures as indicated in Figure . Accordingly, based on Cohen (Citation1988) who recommends that R2 above 0.26 is considered substantial in explaining the effect of the predictor variable on the outcome variable, it can be concluded that the model is relevant to predict pandemic mitigation measures in low-income countries like Uganda.

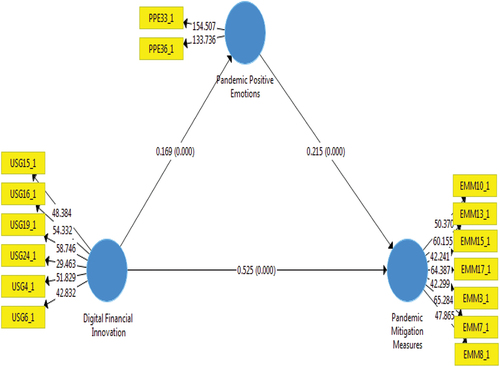

Figure 2. PLS SEM algorithms with both direct and indirect effects.

Figure 3. PLS SEM algorithms with t-values and p-values.

More so, Hair et al. (Citation2016) also argue that the quality of the structural model should be determined to ensure its robustness. They recommend that the quality of the model can be examined through cross-validated redundancy. This is done through the blind-folding technique in SmartPLS sub-menu. The rule of thumb is that some data values should be removed, which would be estimated as missing values. The omission distance under cross-validated redundancy ranges between 5 and 12, and the recommended omission distance is 7 although other ranges of omission distance may also be applicable (see Hair et al. Citation2016). Hence, under this study, an omission distance of 5 was used because of the large sample size. This was done to determine certain values that would be generated and a comparison made in order to test how close the real result is from the assumed results. Hair et al. (Citation2016) suggest that the value of the predictive relevance of the model must be above zero, which is applicable to this study. Indeed, the results of the cross-validated redundancy for all the variables were above zero as indicated in Table .

Table 7. Predictive relevance of the model for mediation

5.4. Effect size of the model

According to Field (Citation2005), the effect size is an objective and standardized measure of the magnitude of the observed effect. The effect size of a model should be determined because it gives an objective measure of the importance of an effect since R2 value of the dependent variable shows the strength of the model. Therefore, a change in R2 by omitting one dependent variable in the model can also be used to assess the contribution of the omitted variable on the endogenous constructs (Hair et al. Citation2014). The effect size is computed by excluding an exogenous variable from the model and including the exogenous construct in the model to compare the change in R2 to determine the effect size. Field (Citation2005) contends that the effect size can be categorized to include: small effect = 0.10; medium effect = 0.30; and large effect = 0.50. Conclusively, the results from this study indicated that contactless digital financial innovation through mobile money and pandemic positive emotions exert 36% effect on pandemic mitigation measures as indicated in . Explicitly, including pandemic positive emotions into the structural model increases the effect size of contactless digital financial innovation through mobile money on pandemic mitigation measures by 4% as shown in Table .

Table 8. Effect size of exogenous variables on Pandemic mitigation measures

6. Discussion

This study intends to establish whether contactless digital financial innovation like mobile money can significantly promote Covid-19 pandemic mitigation measures mediated by pandemic positive emotions in low-income countries with evidence from Uganda. Three hypotheses were derived under this study, and the findings are discussed below.

The findings from this study revealed that pandemic positive emotions significantly mediates the relationship between the adoption and use of contactless digital financial innovation like mobile money and Covid-19 pandemic mitigation measures. Lazarus et al. (Citation1980), Folkman (Citation1997), and Folkman and Moskowitz (Citation2000) state that experiences of positive affect grounded in emotions during chronic stress may help people to cope. Aspinwall (Citation2001) further contends that positive affect and positive beliefs derived from emotions serve as resources for people to cope with adversities such as the Covid-19 pandemic. Komiak and Benbasat (Citation2006), Wood and Moreau (Citation2006), Zeeleberg et al. (2008), and Anderson and Agarwal (Citation2011) also argue that decision-making itself is often an emotional process, which involves affective processes because it elicits forward-looking anticipated emotions during crisis like Covid-19 situation (Bagozzi & Baumgartner, Citation2000; Perugini & Bagozzi, Citation2001). This finding is in line with Lerner et al. (Citation2003) who discovered that fear resulting from positive emotions increased the perceived risk of terrorism and plans for precautionary measures in a national field experiment conducted in the US in the aftermath of 11 September 2001. This finding was held across non-terror-related risks like getting flu. It is worthwhile noting that anticipated positive emotions become relevant in influencing adoption and use decisions of products like mobile money because it affects behavior due to ease of use (see, e.g., Davis, Citation1989). The behavior to adopt and use mobile money product is motivated by the anticipated positive emotions that may occur such as fear to catch Covid-19 through human-to-human physical contact (see, e.g., Frijda, Citation1986). This finding supports hypothesis (H3) derived under this study.

Additionally, the findings from this study indicated that the adoption and use of contactless digital financial innovation like mobile money significantly promotes Covid-19 pandemic mitigation measures. Demirguc-Kunt et al. (Citation2020) argue that mobile money has the potential to bring the unbanked population into the financial system by increasing access to and use of financial services remotely during pandemic crisis. Similarly, the GSMA (2020) observes that mobile money can help users of mobile phones to deposit, transfer, pay, and withdraw money remotely without having a bank account. Furthermore, Agur, Martinez, and Rochon (2020) also contend that mobile money can permit remote payments and transactions. This may promote social distancing recommended in reducing contagion during the Covid-19 pandemic. Besides, through digital payments over mobile money, consumers can transfer funds, pay bills, and pay for goods and services with limited or no physical contact. This may help to promote social distancing by enabling transactions remotely under Covid-19 measures that restrict movements. Correspondingly, Bangura (Citation2016) and Dumas et al. (Citation2017) found that mobile money transfer significantly supported payments to frontline workers during the Ebola outbreak in Sierra Leone. Digital financial innovation like mobile money can help individuals to limit movements and human-to-human contacts under situation of contagious pandemic outbreak to curb the spread and death. This finding supports hypothesis (H1) derived under this study.

Finally, the findings from this study showed that pandemic positive emotions significantly promotes the adoption and use of contactless digital financial innovation like mobile money. Kahneman (Citation1999) and Diener (Citation2000) state that positive emotions signal health and well-being in the environment. This is supported by the broaden-and-build theory, which posits that positive emotions produce health and well-being (Fredrickson Citation2001). As a result, positive emotions broaden peoples’ momentary thought–action repertoires that widen the array of thoughts and actions that come to mind. This creates the urge among individuals to explore, take in new information, and experiences, to expand their minds in dealing with events such as Covid-19 crisis to adopt and use contactless digital financial innovation like mobile money to avoid catching the virus. In addition, Frijda (Citation1986), Levenson (Citation1994), and Oatley and Johnson-Laird (1996) also observe that positive functional emotions, which serve an impressive coordination role, may trigger a set of responses (behavior, experience, and communication) that enable individuals to adopt and use mobile money to deal quickly with the health and well-being problem caused by the Covid-19 pandemic to avoid getting infected by the virus. In the same vein, Forgas (Citation1995) also argues that emotions arising from fear based on incidental affect linked to affect-related cognitive processes can influence subsequent judgments and choices among individuals to adopt and use mobile money technology under the situation of Covid-19 crisis to avoid catching the virus. This finding corroborates with Maria et al. (2020) who found that positive emotions and feelings of responsibility to adopt different ways including technology due to uncertainty of fear and anguish greatly contributed towards adherence to Covid-19 mitigation measures in Argentina. The fear and intense feelings to avoid contracting a contagious disease like Covid-19 drive individuals to adopt and use contactless means like mobile money channel to remotely perform daily financial activities in life. This is grounded on broaden-and-build theory, which drives human thoughts and actions. This finding supports hypothesis (H2) derived under this study.

7. Conclusion

This study intends to establish whether contactless digital financial innovation like mobile money can significantly promote Covid-19 pandemic mitigation measures mediated by pandemic positive emotions in low-income countries with evidence from Uganda.

The findings from this study indicated that pandemic positive emotions significantly mediates the relationship between the adoption and use of contactless digital financial innovation like mobile money and Covid-19 pandemic mitigation measures. Indeed, individuals have switched to a cashless society through mobile wallets to enable peer-to-business payments to maintain physical social distancing and hand hygiene due to fear of getting infected with Covid-19. This confirms hypothesis (H3) of this study.

The findings from this study also revealed that the adoption and use of contactless digital financial innovation like mobile money significantly promotes Covid-19 pandemic mitigation measures. Mobile money can conveniently and affordably facilitate none peer-to-peer transactions and allow governments to reach households and firms with emergency grants and support through G2P and G2B in a timely fashion during a pandemic crisis. The use of contactless digital payments through mobile money for G2P and G2B transfers may help to maintain social distancing and reduce the potential spread of Covid-19. This confirms hypothesis (H1) of this study.

Lastly, the findings from this study showed that pandemic positive emotions significantly promotes the adoption and use of contactless digital financial innovation like mobile money. Indeed, positive emotion-related cognition directs attention, memory, and judgment of individuals to adopt and use mobile money technology to address emotion-eliciting events such as contracting Covid-19. This confirms hypothesis (H2) of this study.

8. Policy implications

The findings from this study can help the unbanked individuals to access and use basic financial services without operational bank accounts under Covid-19 pandemic. Mobile money can help the unbanked individuals to make payments, savings, withdrawals, and remittances remotely at cheaper cost with convenience and privacy during lock down caused by Covid-19 health restrictions. Through mobile money, individuals can receive money and buy goods and services under lockdown.

Governments in low-income countries may use the findings to promote public health concern on the spread of the Covid-19 pandemic. The use of contactless digital financial innovation like mobile money technology may be helpful for sending and receiving money other than physical cash and automated teller machines (ATMs), which are found to be laden with life-threatening bacteria including the novel Covid-19. The use of contactless digital platform like mobile money can prevent individuals from touching dirt surfaces in order to maintain hand hygiene and human-to-human physical distance to avoid catching the contagious Covid-19. This may be achieved through creating public health awareness among the population to adopt and use contactless digital innovations like mobile money.

Besides, governments in low-income countries may use mobile money to send emergency payments, salaries, stipends, pensions, aid, and grants under pandemic situation. This may promote G2P (government to person), P2P (Person-to-Person), P2B (Person-to-Business), and B2P (Business-to-Person) payments through remote transaction between governments, businesses, and citizens under Covid-19 pandemic situation. The governments may achieve this through digitizing its payment system and encouraging digital commerce among its citizens with strong regulations and laws put in place to protect the users.

Furthermore, the findings from this study may also help governments in low-income countries to digitize health service provision, especially among individuals with chronic illness residing in hard-to-reach areas during a pandemic situation. Indeed, governments and other donors may use mobile money to remit money directly to health service providers located in rural areas to offer treatment and medicine to the terminally ill individuals during situation of limited movements and lockdown caused by the Covid-19 pandemic.

Similarly, the findings from this study may help governments in low-income countries to rethink and revise taxes levied on mobile money transactions to promote mobile money use. This could be achieved by adopting international best practices on taxation within the digital financial ecosystem. The taxes could be levied on other telecommunication devices and gadgets that may not hamper the growth of the infant FinTech sector, especially under pandemic situation.

More so, the findings from this study may also help governments in low-income countries to enact laws that protect mobile money stakeholders. The Unstructured Supplementary Service Data (USSD), Short Messaging Service (SMS), and Sim Tool Kit (STK) have long been known as susceptible to cyber attack and frauds. Therefore, governments should set up stringent laws to punish fraudsters over the mobile money platform. This may be achieved by creating laws that protect users of digital financial technology like mobile money.

Finally, the findings may also help mobile money inventors in low-income countries to design customized financial products to suit the needs of different consumers under a pandemic situation. Cheap, reliable, and suitable mobile money products that attract users of different economic status should be developed to promote digital financial inclusion under pandemic situation such as Covid-19. The mobile money service providers should loosen the requirements for mobile money registration in order to on-board more users under pandemic situation. This may be achieved through the use of biometrics to solve the problem of lack of identification among prospective customers.

9. Research limitations and future studies

While this study examined the role of contactless digital financial innovation under the Covid-19 pandemic, it focused mainly on mobile money innovation. Thus, future studies may investigate the role of other digital financial innovations like mobile banking, internet banking, and other online banking platforms under pandemic situation. Similarly, the current study was conducted in low-income countries with data collected from only Uganda. Therefore, future studies may collect data from other middle and high-income countries to establish cross-country analyses. Besides, this study collected data through cross-sectional research approach. Future studies could use longitudinal design to collect data over a long time span. Finally, data collection exercise in this study was limited by Covid-19 lockdown. However, Kobocollect data collection tool was used to remotely elicit responses from individuals at lockdown.

Acknowledgements

This work was funded by the Government of Uganda through Makerere University Research and Innovations Fund (grant number MAK-RIF/COVID/032).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

George Okello Candiya Bongomin

George Okello Candiya Bongomin holds a PhD in Finance, MSc (Accounting & Finance) and Bachelor’s degree in Commerce Accounting from Makerere University, Kampala, Uganda. He is a Research Fellow at the Faculty of Graduate Studies and Research, Makerere University Business School, Kampala, Uganda, and an international financial inclusion scholar. Currently, he is a Visiting Professor and Scholar at Laboratory for Financial Engineering at Laval University, State University of New York, and a member of Centre for Global Finance at SOAS University of London. He is a Principal Investigator on MUBS and Bank of Uganda Joint Research Collaboration on Digital Financial Services and Financial Inclusion in Uganda. His research interests are in financial inclusion, artificial intelligence/machine learning and financial services, digital financial services, microfinance, behavioural finance, banking and finance practice, institutional economics, financial consumer protection, and business psychology. George Okello Candiya Bongomin is the corresponding author and can be contacted at [email protected].

References

- Agarwal, R., & Prasad, J. (1998). A conceptual and operational definition of personal innovativeness in the domain of information technology. Information Systems Research, 9(2), 204–41.

- Agur, I., Peria, S. M., & Rochon, C. (2020 Digital financial services and the pandemic: Opportunities and risks for emerging and developing economies). and : and and . International Monetary Fund Special Series on COVID-19, Transactions, Vol. 1, pp. 2–1. IMF Publications, Washington DC. Retrieved from https://www.imf.org/en/Publications/SPROLLs/covid19-special-notes.

- Alliance for Financial Inclusion. (2011). “Measuring financial inclusion: a core set of indicators”. AFI Financial Inclusion Data Working Group Paper, available at: http://www.afiglobal.org.

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior. Englewood Cliffs, NJ: Prentice-Hall.

- Aker, J.C., Boumnijel, R., McClelland, A. and Tierney, N. (2016). “Payment Mechanisms and Anti-Poverty Programs: Evidence from a Mobile Money Cash Transfer Experiment in Niger”, Tufts University working paper, Fletcher School and Department of Economics, Tufts University, Medford, MA

- Anderson, C. L., & Agarwal, R. (2011). The digitization of healthcare: Boundary risks, emotion, and consumer willingness to disclose personal health information. Information Systems Research, 22(3), 469–490.

- Alliance for Financial Inclusion. (2011). “Measuring financial inclusion: a core set of indicators”. AFI Financial Inclusion Data Working Group Paper, available at: http://www.afiglobal.org.

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychol. Bull, 103(3), 411–423. https://doi.org/10.1037/0033-2909.103.3.411

- Arner, D. W., J. N. Barberis, J. Walker, R. P. Buckley, A. M. Dahdal, D. and A. Zetzsche. (2020). “Digital Finance & the COVID-19 Crisis.” University of Hong Kong Faculty of Law Research Paper No. 2020/017. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3558889

- Aspinwall, L. G. (2001). Dealing with adversity: self-regulation, coping, adaptation, and health. In A. Tesser & N. Schwarz (Eds.), The Blackwell handbook of social psychology (Vol. 1, pp. 591–614). Malden, MA: Blackwell. Intraindividual processes

- Auer, R., Comelli, G., & Frost, J. (2020). COVID-19, Cash, and the Future of Payments. In BIS Bulletin, No. (3). BIS Publications: Basel, Switzerland. https://www.bis.org/publ/bisbull03.pdf

- Baganzi, R., & Lau, A. K. W. (2017). Examining trust and risk in mobile money acceptance in Uganda. Sustainability, 9(12), 1–22.

- Bagozzi, R., & Baumgartner, H. (2000). The role of emotions in goal-directed behavior. The Why of Consumption: Contemporary Perspectives on Consumer Motives, Goals, and Desires, 36–58.

- Bagozzi, R. P., Gopinath, M., & Nyer, P. U. (1999). “The role of emotions in marketing. Journal of the Academy of Marketing Science, 27(2), 184–206. https://doi.org/10.1177/0092070399272005

- Bagozzi, R., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1),74–94. https://doi.org/10.1007/BF02723327.

- Bangura, J. A. (2016). “Saving money, saving lives: A case study on the benefits of digitizing payments to Ebola response workers in sierra Leone.” https://www.betterthancash.org/tools-research/case-studies/saving-money-saving-lives-a-case-study-on-the-benefits-of-digitizing-payments-to-ebola-response-workers-in-sierra-leone

- Barrett, K., & Campos, J. (1987). Perspectives on emotional development: II. A functionalist approach to emotions. In J. Osofsky (Ed.), Handbook of infant development (2nd ed., pp. 555–578). New York: Wiley.

- Bodenhausen, G. V., Kramer, G. P., & Süsser, K. (1994). Happiness and stereotypic thinking in social judgment. Journal of Personality & Social Psychology, 66, 621–632.

- Bollen, K. A. (1989). Structural equations with latent variables. John Wiley & Sons.

- Bower, G. H. (1981). Mood and memory. The American Psychologist, 36, 129–148.

- Bower, G. H. (1991). Mood congruity of social judgment. In J. Forgas (Ed.), Emotion and social judgment (pp. 31–54). Oxford, UK: Pergamon.

- Chin, W. W. (1998). The partial least squares approach for structural equation modeling: Methodology for business and management. Erlbaum

- Chin, W. W., & Newsted, P. R. (1999). Structural equation modeling analysis with small samples using partial least squares. In R. H. Hoyle (Ed.), Statistical strategies for small sample research (pp. 307–341). Sage Publications, Inc.: Thousand Oaks.

- Cronbach, L. J. (1971). “Test Validation.” In Educational Measurement, edited by R. L. Thorndike, 443–507. Washington, DC: IGI Publishing, American Council on Education.

- Consultative Group to Assist the Poor-CGAP. (2020). COVID-19 (coronavirus) – Insights for inclusive finance. CGAP Publications, Washington, DC.

- Churchill, G.A., & Iacobucci, D. (2004). Marketing research: Methodological foundations, 9th ed, Thomson South-Western, Ohio.

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Lawrence Erlbaum.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

- Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/10.1287/mnsc.35.8.982

- DeVellis, R. F. (2003). Scale development: Theory and applications (2nd ed.). Sage.

- Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2020). The Global Findex Database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review, The World Bank.

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring financial inclusion and the fintech revolution. World Bank. https://globalfindex.worldbank.org/sites/globalfindex/files/2018-04/2017%20

- Diener, E. (2000). Subjective well-being: The science of happiness and a proposal for a national index. The American Psychologist, 55(1), 34–43. https://doi.org/10.1037/0003-066X.55.1.34

- Dumas, T., Frisetti, A., & Radice, H. W. (2017). Harnessing digital technology for cash transfer programming in the Ebola response: Lessons learned from USAID/Office of Food for Peace Partners’ West Africa Ebola Responses (2015–2016).Washington D.C. https://www.alnap.org/help-library/harnessing-digital-technology-for-cash-transfer-programming-in-the-ebola-response

- Dupas, P., & Robinson, J. (2013). Savings Constraints and Microenterprise Development: Evidence from a Field Experiment in Kenya. American Economic Journal. Applied Economics, 5(1), 163–192.

- Economides, N., & Jeziorski, P. (2017). Mobile Money in Tanzania. Marketing Science, 36(6), 813–1017.

- Field, A. P., & Hole, G. (2003). How to Design and Report Experiment. London: Sage Publishing.

- Field, A.P. (2005). Discovering statistics using SPSS, Sage.

- Field, A.P. (2009). Discovering Statistics using SPSS, Sage, London.

- Folkman, S. (1997). Positive psychological states and coping with severe stress. Social science & medicine, 45, 1207–1221.

- Folkman, S., & Moskowitz, J. T. (2000). Positive affect and the other side of coping. The American Psychologist, 55, 647–654.

- Forgas, J. P. (1995). Mood and judgment: The affect infusion model (AIM). Psychological Bulletin, 117, 39–66.

- Forgas, J. P., & Bower, G. H. (1987). Mood effects on person-perception judgments. Journal of Personality and Social Psychology, 53(1), 53–60.

- Fredrickson, B. L. (2000). Cultivating positive emotions to optimize health and well-being. Prevention and Treatment, 3, 1–25.

- Fredrickson, B. L. (2001). The role of positive emotions in positive psychology: The broaden and build theory of positive emotions. American Psychology, 56(3), 218–226. https://doi.org/10.1037//0003-066x.56.3.218

- Frijda, N. H. (1986). The emotions. Cambridge University Press.

- Global System for Mobile Communications-GSMA., (2020), “Mobile money recommendations to central banks in response to COVID-19.” https://www.gsma.com/mobilefordevelopment/resources/mobile-money-recommendations-to-central-banks-in-response-to-covid-19

- Hair, J. F. J., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Sage.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2016). A Primer on Partial. Least Squares Structural Equation Modeling (PLS-SEM) (2nd ed.). Sage.

- Huang, Y., Lin, C., Wang, P., & Wu, Z. (2020). Saving China from the Coronavirus and Economic Meltdown: Experiences and Lessons. In R. Baldwin (Ed.), Mitigating the COVID Economic Crisis: Act Fast and Do Whatever It TakesMitigating the COVID Economic Crisis: Act Fast and Do Whatever It Takes online book

- Isen, A. M., Shalker, T. E., Clark, M., & Karp, L. (1978). Affect, accessibility of material in memory, and behavior: A cognitive loop?. Journal of Personality and Social Psychology, 36(1), 1–12.

- Johns, R (2010). Likert items and scales. Retrieved from Survey Question Bank website: http://www.surveynet.ac.uk/sqb/datacollection/likertfactsheet.pdf.

- Johnson Laird, P. N., & Oatley, K. (1992). Basic emotions, rationality, and folk theory. Cognition & emotion, 6, 201–223.

- Kahneman, D. (1999). Objective happiness. In D. Kahneman, E. Diener, & N. Schwarz (Eds.), Well-being: Foundations of hedonic psychology (pp. 3±25). New York: Russell-Sage.

- Kavanagh, D. J., & Bower, G. H. (1985). Mood and self-efficacy: Impact of joy and sadness on perceived capabilities. Cognitive Therapy and Research, 9, 507–525.

- Komiak, S. Y. X., & Benbasat, I. (2006). The effects of personalization and familiarity on trust and adoption of recommendation agents. MIS Quarterly, 30(4), 941–960.

- Lazarus, R. S. (1991a). Cognition and motivation in emotion. American Psychology, 46:352–67

- Lazarus, R. S. (1991b). Progress on a cognitive-motivational-relational theory of emotion. The American Psychologist, 46(8), 819–834.

- Lazarus, R. S., Kanner, A. D., & Folkman, S. (1980). Emotions: A cognitrve-phenomenological analysis. In R. Plutchik & H. Kellerman (Eds.), Theories of emotion (pp. 189–217). New York: Academic Press.

- Lerner, J. S., Gonzalez, R. M., Small, D. A., & Fischhoff, B. (2003). Effects of fear and anger on perceived risks of terrorism: A national field experiment. Psychological Science, 14, 144–150.

- Lerner, J. S., & Keltner, D. (2000). Beyond valence: Toward a model of emotion-specific influences on judgement and choice. Cognition & Emotion, 14(No4), 473–493. https://doi.org/10.1080/026999300402763

- Lerner, J. S., Small, D. A., & Loewenstein, G. (2004). Heart strings and purse strings: Carryover effects of emotions on economic decisions. Psychological Science, 15(5), 337–340.

- Levenson, R. W. (1994). Human emotion: A functional view. In P. Ekman & R. J. Davidson (Eds.), The nature of emotion: Fundamental questions (pp. 123–126). New York: Oxford University Press.

- Likert, R (1932). A technique for the measurement of attitudes, Archives ofPsychology, 140(1), 44–53.

- María, J. C., Lorena, S., & Natalia, T. (2020). Emotions, concerns and reflections regarding the COVID-19 pandemic in Argentina. Ciênc. saúde coletiva, 25(1), 2447–2456. https://doi.org/10.1590/1413-81232020256.1.10472020

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1),39–50. https://doi.org/10.1177/002224378101800104

- Ministry of Health in Uganda, (2023), Cumulative Number of Covid-19 cases; Cumulative Number of Covid-19 DEATHS: Cumulative Number of Covid-19 RECOVERIES. https://covid19.gou.go.ug/statistics.html

- Mulligan, K., & Scherer, K. R. (2012). Toward a working definition of emotion. Emotion Review, 4(4), 345–357. https://doi.org/10.1177/1754073912445818

- Muralidharan, K., Niehaus, P., & Sukhtankar, S. (2016). Building State Capacity: Evidence from Biometric Smartcards in India. The American Economic Review, 106(10), 2895–2929.

- Nalletamby, S. (2020). COVID-19 pandemic bolsters case for technology-based economic resilience. African Development Bank Bulletin, 16. https://www.afdb.org/en/news-and-events/covid-19-pandemic-bolsters-case-technology-basedeconomic-resilience-35255on13/07/2021

- Nampewo, D., Tinyinondi, G. A., Kawooya, D. R., & Ssonko, G. W. (2016). Determinants of private sector credit in Uganda: The role of mobile money. Financial Innovation, 2(13), 1–16.

- Nunnally, J. C. (1978). Psychometric theory. McGraw–Hill.

- Oatley, K., & Johnson Laird, P. N. (1996). The communicative theory of emotions: Empirical tests, mental models, and implications for social interaction. (L. L. Martin & A. Tesser, Eds.). Erlbaum.

- Okello Candiya Bongomin, G., & Ntayi, J. M. (2020). Mobile money adoption and usage and financial inclusion: Mediating effect of digital consumer protection. Digital Policy, Regulation and Governance, 22(3), 157–176. https://doi.org/10.1108/DPRG-01-2019-0005

- Okello Candiya Bongomin, G., Yosa, G., & Ntayi, J. M. (2021a). Reimaging the mobile money ecosystem and financial inclusion of MSMEs in Uganda: Hedonic motivation as mediator. International Journal of Social Economics, 48(11), 1608–1628. https://doi.org/10.1108/IJSE-09-2019-0555

- Okello Candiya Bongomin, G., Yourougou, G., Yosa, P., Amani, F., & Ntayi, J. M. (2021b). Psychoanalysis of the mobile money ecosystem in the digital age: Generational cohort and technology generation theoretical approach. Development in Practice. https://doi.org/10.1080/09614524.2021.1937539

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329–340. https://doi.org/10.1016/j.bir.2017.12.003

- Pazarbasioglu, C., Mora, A. G., Uttamchandani, M., Natarajan, H., Feyen, E., & Saal, M. (2020). Digital financial services.: World Bank Group. http://pubdocs.worldbank.org/en/230281588169110691/Digital-Financial-Services.pdf

- Perugini, M., & Bagozzi, R. (2001). The role of desires and anticipated emotions in goal‐directed behaviours: Broadening and deepening the theory of planned behaviour. British Journal of Social Psychology, 40(1), 79–98.

- Phillips, D., & Baumgartner, H. (2002). The role of consumption emotions in the satisfaction response. Journal of Consumer Psychology, 12(3), 243–252.

- Podsakoff, P.M., MacKenzie, S.B., Lee, J.Y. & Podsakoff, N.P (2003). “Common method biases in behavioural research: a critical review of the literature and recommended remedies”, Journal of Applied Psychology, 88(5), 879–903.

- Raghunathan, R., & Pham, M.T. (1999). “All Negative Moods Are Not Equal: Motivational Influences of Anxiety and Sadness on Decision Making,” Organizational Behavior and Human Decision Processes, 79 (1), 56–77.

- Schwarz, N. (1990). Feelings as information: Informational and motivational functions of affective states. In ET Higgins (Ed.), Handbook of Motivation and Cognition (Vol. 2, pp. 527–561). New York: RM Sorrentino.

- Schwarz, N., & Clore, G. L. (1983). Mood, misattribution and judgments of well-being: Informative and directive functions of affective states. Journal of Personality and Social Psychology, 45(3), 513–523.

- Simon, H. A. (1967). Motivational and emotional controls of cognition. Psychological Review, 74, 29–39.

- Smith, C. A., & Ellsworth, P. C. (1985). Patterns of cognitive appraisal in emotion. Journal of Personality & Social Psychology, 48(4), 813–838.

- Spector, P.E. (2006). “Method variance in organizational research: truth or urban legend?”, Organizational Research Methods, Vol. 9 No. 2, pp. 221–232.

- Straub, E. T. (2009). Understanding technology adoption: Theory and future directions for informal learning. Review of Educational Research, 79(2), 625–649. https://doi.org/10.3102/0034654308325896

- Suri, T. (2017). Mobile money. Annual Review of Economics, 9(1), 497–520. https://doi.org/10.1146/annurev-economics-063016-103638

- Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288–1292. https://doi.org/10.1126/science.aah5309

- Tooby, J., & Cosmides, L. (1990). The past explains the present: Emotional adaptations and the structure of ancestral environments. Ethology and Sociobiology, 11, 375–424.

- Tourangeau, R., Rips, L.J. and Rasinski, K. (2000). The Psychology of Survey Response, Cambridge University Press, Cambridge.

- Venkatesh, V., Thong, J. Y. L., & Xu, X. (2012). Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly, 36(1), 157–178. https://doi.org/10.2307/41410412

- Wood, S., & Moreau, C. (2006). From fear to loathing?: How emotions influence the evaluation and early use of innovation. Journal of Marketing, 70, 44–57.

- Wood, S. L., & Swait, J. (2002). Psychological indicators of innovation adoption: Cross-classification based on need for cognition and need for change. Journal of Consumer Psychology, 12, 1–13.

- World Bank, (2020), Covid-19 and Digital Financial Inclusion in Africa: How to leverage digital technologies during the pandemic. Africa Knowledge in Time Policy Brief October, Issue 1, NO. 4, The World Bank Washington D.C

- World Health Organization. (2020). Coronavirus disease (Covid-19) pandemic Dashboard. Daily and weekly update. 13th December, 2020. https://www.who.int/emergencies/diseases/novel-coronavirus-2019?adgroupsurvey={adgroupsurvey}&gclid=Cj0KCQjwwtWgBhDhARIsAEMcxeBbGvwCcoY-X4MX3g58eaJgpYIhx7ZgNkq5txprZzKPkOx1Mt7D3YoaAuXZEALw_wcB

- World Health Organization. (2023). Coronavirus disease (Covid-19) pandemic Dashboard. Daily and weekly update. 16th March, 2023. https://www.who.int/emergencies/diseases/novel-coronavirus-2019?adgroupsurvey={adgroupsurvey}&gclid=Cj0KCQjwwtWgBhDhARIsAEMcxeBbGvwCcoY-X4MX3g58eaJgpYIhx7ZgNkq5txprZzKPkOx1Mt7D3YoaAuXZEALw_wcB

- Worldometer. (2023). COVID-19 Coronavirus Statistics: Daily and weekly update. https://www.worldometers.info › coronavirus

- Uganda Bureau of Statistics. (2014). The National Population and Housing Census 2014 – Main Report, Kampala, Uganda.

- United Nations Capital Development Fund. (2020). Digitizing Payments in the Time of COVID-19 and Beyond. News Letter, April 29, 2020 Brussels, Belgium. https://www.uncdf.org/article/5574/digitizing-payments-in-the-time-of-covid19-and-beyond

- United Nations Capital Development Fund. (2020). Digitizing Payments in the Time of COVID-19 and Beyond. News Letter, April 29 2020, Brussels, Belgium. https://www.uncdf.org/article/5574/digitizing-payments-in-the-time-of-covid19-and-beyond

- Wright, W. F., & Bower, G. H. (1992). Mood effects on subjective probability assessment. Organizational Behavior and Human Decision Processes, 52, 276–291.

- Zeelenberg, M., Nelissen, R. M. A., Breugelmans, S. M., & Pieters, R. (2008). On emotion specificity in decision-making: Why feeling is for doing. Judgment and Decision Making, 3, 18–27.

Appendix 1

COVID-19 SURVEY IN UGANDA 2020—MOBILE MONEY AGENTS QUESTIONNAIRE

Section 1: Background information

Please kindly tick appropriately:

1. Gender

1) Male_____ 2) Female _____

2. Age group

1) 18–25 ___ 2) 26–33 ___ 3) 34–41 __ 4) 42–49 ____ 5) 50+ ____

3. Education level

1) Primary school certificate ___ 2) Secondary school certificate ____

3) Diploma ____ 4) Bachelor Degree ____ 5) Postgraduate degree ____

6) Others (please specify) ____

4. Marital status

1) Single ___ 2) Married ____3) Separated ___ 4) Divorced ____

5) Others (please specify) ____

5. Profession _____________

6. Region

1) North ____ 2) Central ____ 3) East ____ 4) Western ____

7. Language _____________

8. Location

1) Urban ____ 2) Peri-urban____ 3) Rural ____

9. Number of people in your household

1) 5 or less ____ 2) 6–10 ____ 3) More than 10 ____

10. Are you a registered mobile money Agent?

1) Yes ____ 2) No ____

11. For how long have you been a mobile money agent?

1) 5 years or less ____ 2) 6–10 years ___ 3) 11–15 years ____

12. In the last 3 months have you provided mobile money services?

1) Yes ____ 2) No ____

13. What type of mobile money transaction do you provide most?

1) Savings ____ 2) Payments _____ 3) Loans ______ 4) Deposits _____

5) Remittances _____ 6) Withdrawals _____ 7) others (please specify) ____

14. Which mobile network operator(s) do you represent? ______

1) MTN _____ 2) Airtel _____ 3) Africell 4) Lycamobile ______

5) K2 Telecom ____ 6) UTL ____ 7) Smile Telecom ____ 8) Vodafone Uganda _____

15. Which network operator has many users? _______________

Why? __________________

16. What is the level of your capital at this particular time?

1) 1,000,000Ugx or less ____ 2) 1,000,000–2,000,000Ugx_____ 3) 2,000,000–3,000,000Ugx____