Abstract

This study aimed to determine the effect of Islamic financial literacy, spiritual intelligence, public perception, and behaviour on public interest in Islamic banking services. This research is classified as quantitative research. Islamic financial literacy, spiritual intelligence, and public perception are independent variables. Public behaviour as a mediating variable. The population in this study is the entire community in Padang city who are already customers of Islamic banks. The sample is determined by the Hair method, five times the number of indicators, where the number of indicators is 46 items. The number of respondents in this study was 230 people. Data analysis using structural equation model by using Smart-PLS. The results show Islamic financial literacy and public perception have no significant effect on public interest in Islamic banking services. However, spiritual intelligence has a positive and significant effect on public interest in Islamic banking services. Public behaviour fully mediates the relationship between public perception and public interest in Islamic banking services. Islamic banking is expected to be able to educate prospective customers through increasing spiritual intelligence. Public behaviour can be improved with the religiosity community, thereby increasing interest in saving in Islamic banks.

PUBLIC INTEREST STATEMENT

Padang city is one of the big cities in Indonesia with a majority Muslim population located on the island of Sumatra. The high population is not in line with the increasing number of customers in using Islamic banking products. This article presents empirical evidence of the factors that cause public interest in using Islamic banking services. This article contributes to the public to understand the difference between conventional banks and Islamic banks. For academics, this article contributes to obesrves at the relationship between related variables. For Islamic banks, this article can be a recommendation to increase the public interest in Islamic banking product through Islamic financial literacy, spiritual intelligence, public perception and behaviour.

1. Introduction

Islamic banking in Indonesia was started in 1992 through Law no. 7/1992, which allows banks to run their business operations with a murabahah or profit-sharing system. So that in the same year, the first Islamic bank in Indonesia was established, namely Bank Muamalat Indonesia. The development of Islamic banks is likely to run well if it can refer to public demand for Islamic bank products and services. With the capital of the Act and the moral and spiritual values of the community, the behaviour patterns of the increasingly religious people, Islamic banking must be able to prove that its existence in the banking world will be able to serve the needs of the community, both in terms of surplus pending units and deficit spending units. Although the intensive development of Islamic banks is still relatively new, it should be remembered that its development is not based on the infant industries argument, which is based on protection and privileges alone. Islamic banks comb through the emotional aspects of the religiosity of the Indonesian people, who are predominantly Muslim.

As part of the national banking system, Islamic banking has an essential role in the economy. The role of Islamic banking in Indonesia’s economic activity is not much different from conventional banking. The primary difference between the two is the principles in financial/operational transactions. One of the principles in sharia banking operations is the application of profit and loss sharing. This principle does not apply in conventional banking that applies the interest system. However, the three main banking activities, namely funding, landing, and service, are also carried out by Islamic banking as a whole, as is the case with conventional banks.

In its development, Islamic banking faces many challenges and problems. Problems that arise include the low level of public knowledge of Islamic banking, mainly due to the dominance of conventional banking (Nouman et al., Citation2018). Several obstacles arise in connection with the development of Islamic banking, which include: inadequate public understanding of the operational activities of Islamic banks (Alam et al., Citation2019), the prevailing banking regulations have not fully accommodated the operations of Islamic banks (Suzuki et al., Citation2019), (3) Sharia bank office network which is not yet extensive (Hosen et al., Citation2019), and (4) human resources who have expertise in Islamic banking are still few (Py Lai & Samers, Citation2017).

Various public perceptions and paradigms emerged after the existence of Islamic banks. Among them is that the “profit-sharing” system only changes its name to “interest,” even though it is the same without any difference, even its implementation is considered more burdensome than existing conventional banks. This opinion is formed from their experiences and information circulating in the community. Another thing is the spiritual intelligence of the people. The higher the religious spirit of the community, the higher their tendency to leave things that are considered usury. So with this trend, we are also interested in knowing how this spiritual intelligence can encourage their behaviour patterns to use Islamic bank products in this banking need.

The growth of the Islamic banking industry in Indonesia shows a trend that continues to increase rapidly after experiencing a slowdown in growth due to the 2008/2009 United States crisis. At the end of September 2011, asset growth reached 47.8% or Rp. 123.4 trillion, the highest since 2005. The growth of depositor funds and financing provided at the same time was even more rapid, reaching 53% or Rp. 97.8 trillion and 52.3% or Rp. 92.8 trillion, with an FDR (financing to deposits ratio) of 95.7%. In comparison, the growth of conventional banking assets at the same time reached 22.2% or Rp. 3371.5 trillion, with a DR (loan to deposits ratio) of 81.4%. Padang City, West Sumatra, is one of the provinces with a Muslim population of almost 97.6%. Padang City, West Sumatra, is one of the provinces with a Muslim population of almost 97.6%. However, the increase in Islamic bank assets in Padang is still below the expected target of 15% in 2021.

This research is different from previous research by Abdullah and Anderson (Citation2015), specializing in Islamic financial literacy as a predictor. This research adds spiritual intelligence and public behaviour as predictors. In addition, there are differences in population and research samples. Previous research by Ali and Raza (Citation2017) used service quality perception as a predictor. However, this research used public perception. Selvanathan et al. (Citation2018) used bank reputation, convenience, religious value, and cost-benefit as preditors. Several previous studies have focused on the facilities and brands or the convenience offered by Islamic banks. However, this study focuses more on how the knowledge of customers can influence their behaviour in choosing an Islamic bank.

2. Literature review

Financial Services Authority Regulation in Indonesia, Number 76/POJK.07/2016 states that Financial Literacy is knowledge, skills, and beliefs, which influence attitudes and behaviour to improve the quality of decision-making and financial management to achieve prosperity. Objectives of Financial Literacy, (a) improving the quality of individual financial decision making; and (b) changes in individual attitudes and behaviour in financial management for the better, so that they can determine and utilize financial institutions, products, and services that are by the needs and abilities of consumers or society in order to achieve prosperity. Meanwhile, the scope of efforts to increase financial literacy to improve Financial Literacy is the planning and implementation of (a) Financial Education; and (b) the development of infrastructure that supports Financial Literacy for Consumers or the public. The objective of the Islamic financial literacy development program is to expand and improve knowledge, understanding, and community participation in the use of Islamic financial products and services (Abdullah & Anderson, Citation2015: Er & Mutlu, Citation2017: Nawi et al., Citation2018). The higher the community’s financial literacy, it will reduce the hedonistic lifestyle and create a habit of saving. Financial literacy will affect people’s saving behaviour (Lusardi, Citation2019).

Spiritual intelligence focuses on the teachings of God. Those who are spiritually intelligent are the type of calm soul. Thus, they always display a self-image full of morals, love, and affection, loves and wants to be loved by God, so that wherever man is, he always feels watched by his God (Dhiman, Citation2019). Spiritual intelligence is the intelligence of the soul that can help a person build himself as a whole and have a clear meaning and purpose for himself. Spiritual intelligence does not depend on the value that other people place on themselves. However, spiritual intelligence creates the possibility to have its values for others (Hanefar et al., Citation2016; Vasconcelos, Citation2020). Spiritual intelligence is a human ability that makes humans realize and determine the meaning, values, morals, and love for greater power and fellow living beings because awareness is born as part of the whole. So that people can put themselves and live more positively with complete wisdom. Spiritual intelligence embodied in religiosity can improve financial management (Agarwala et al., Citation2019: Nugroho et al., Citation2017).The term perception is usually used to express the experience of an object or an event that is experienced (Hassenzahl et al., Citation2015). Perception is the starting point for the birth of what kind of behaviour humans will do (Mha, Citation2015). In other words, perception is a potential that is ready to be actualized at any time in the form of attitudes and behaviour. Departs from the conclusion that perception is one of the cognitive abilities that play a critical role concerning other human activities, which are more complex. Perceptions of Islamic banks are divided into three parts, namely perceptions of bank interest, profit sharing, and Islamic bank products (Wulandari & Subagio, Citation2015). The better the public’s perception of this will affect people’s behaviour in saving in Islamic banks (Musa et al., Citation2020: Rahmi et al., Citation2020).

Acceptance of the existence of Islamic banks will affect people’s behaviour in saving (Raza et al., Citation2019; Selvanathan et al., Citation2018). Some groups assume that conventional banks are no different from conventional banks (Zarrouk et al., Citation2016). However, the behaviour of people who accept the existence of Islamic banks and understand the differences with conventional banks will affect behaviour in using products from Islamic banks (Ltifi et al., Citation2016). Community religiosity encourages people’s behaviour to use Islamic products, including banking services (Sarofim et al., Citation2020)

Based on literature review and previous studies, the hypotheses of this research are as follows:

H1: Islamic financial literacy has a positive and significant effect on public interest in Islamic banking services

H2: Spiritual intelligence has a positive and significant effect on public interest in Islamic banking services

H3: public perception has a positive and significant effect on public interest in Islamic banking services

H4: public behaviour mediates Islamic financial literacy and public interest in Islamic banking services

H5: public behaviour mediates spiritual intelligence and public interest in Islamic banking services

H6: public behaviour mediates public perception and public interest in Islamic banking services

3. Methods

This research uses a quantitative approach. A quantitative approach explains phenomena by collecting numerical data that are analyzed using mathematically based methods (Apuke, Citation2017). The population in this study is the entire community in Padang city who are already customers of Islamic banks or not with 950,000 people. The sample was determined by the calculation method of Hair et al. (Citation2021). The minimum number of samples is five times the indicator. The number of indicators in this study was 46, so the number of samples was 230 respondents. The instrument for collecting data in this study was a questionnaire compiled using a Likert scale. Likert Scale consisting of 1) strongly disagree 2) disagree 3) neutral 4) agree 5) strongly agree, were used in the answer section.

The independent variables used in this study are Islamic financial literacy (X1), spiritual intelligence (X2), and public perception (X3). Public behaviour (Y) as a mediating variable. The independent variable is the public interest in Islamic banking services (Z).

The Islamic financial literacy (X1) variable consists of five dimensions: (1) knowledge of Islamic finance; (2) Islamic financial communication skills; (3) the ability to use knowledge of Islamic finance for decision making; (4) actual use of Islamic financial instruments; (5) financial trust (Ahmad et al., Citation2020; Dinc et al., Citation2021; Setiawati et al., Citation2018). Spiritual intelligence (X2) consists of nine dimensions: (1) ability to be flexible; (2) ability to adapt and take advantage of suffering; (3) ability to adapt and utilize suffering; (4) ability to face and overcome pain; (5) quality of life inspired by vision and mission; (6) reluctance to cause harm unnecessarily; (7) holistic view; (8) significant tendency to ask why or how to seek basic answers; (9) dedicated and responsible leader (Mahasneh et al., Citation2015; Sirine & Kurniawati, Citation2018; Vasconcelos, Citation2020). Public perception (X3) consists of three dimensions: (1) perception about interest; (2) perception of profit-sharing; (3) perception of Islamic bank products (Ali & Raza, Citation2017; Chaouch, Citation2017; Kashif et al., Citation2016). Public behaviour (Y) consists of four dimensions (1) Attitude to accept Islamic banks; (2) control of perceptions of Islamic banks; (3) subjective norms towards saving intentions (4) community religiosity (Kaakeh et al., Citation2018; Mahadin & Akroush, Citation2019; Nugroho et al., Citation2017). Public interest in Islamic banking services (Z) consists of five dimensions (1) bank performance (2) managed by trusted professionals (3) able to provide competitive profit sharing, and attractive prizes (4) able to provide products according to community needs (5) have an extensive branch network and good infrastructure (Ezeh & Nkamnebe, Citation2019; Pitchay et al., Citation2019; Usman et al., Citation2017; Wulandari & Subagio, Citation2015). The operational definition and measurement of variables is presented in Table .

Table 1. Operational definitions and measurement

The analysis used in this study consists of convergent validity test, discriminant validity test, reliability test, composite reliability test, multicollinearity test, the goodness of fit test, coefficient determination test, direct effect, and an indirect effect by using Smart-PLS.

4. Result and discussion

4.1. Result

Respondents of this research have quite different characteristics. The respondent profile of the study is presented in Table below. In this Table, 55.6% of the respondents were male and 44.4% were female. The majority of the respondents were married, 58%, whereas 42% participated in our study as single. During the data collection time, most of the respondents were between 41 and 45 years of age (22.6%), followed by 46 ≤ 50 (20%), > 55 (11.4%), 51 ≤ 55 (10.9%) and < 25 (9%).

Table 2. Respondent profile

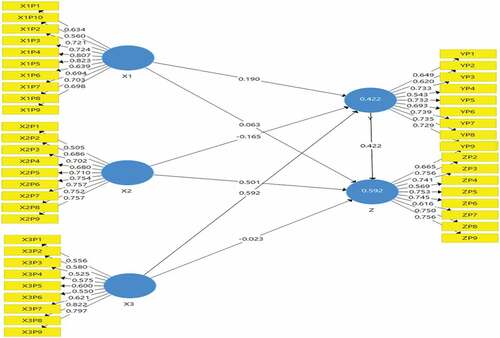

The results of data processing with Smart-PLS are presented in Figure below.

Figure 1. Smart-PLS analysis result.

The results of the convergent validity test contained in Table indicate that the indicators used in this study are classified as valid. It can be seen from the factor loading value in each variable > 0.5.

Table 3. Convergent validity test result

The result of discriminant validity test results are shown in Table below:

Table 4. Discriminant validity test result

Based on Table above, it can be seen that the data is classified as valid because the average variance is > the correlation of the latent variables. The reliability test and composite reliability test results are shown in Table .

Table 5. Reliability test and composite reliability test result

Based on Table above, it can be concluded that the variables are classified as reliable because the Cronbach’s value and composite reliability value > 0.7. The result of the multicollinearity test is shown in Table .

Table 6. Multicollinearity test result

Based on the calculations in the Table, the data is free from multicollinearity symptoms because the value of each VIF indicator is < 10. The results of the goodness of fit test from the proposed model are in Table below:

Table 7. The goodness of fit test result

Based on Table above, it can be concluded that the model is feasible because the value of Standardized Root Mean Square Residual (SRMR) < 0.1. Furthermore, the Normed Fit Index (NFI) value is in the range of 0 and 1. The result of the coefficient determination test are shown in Table below:

Table 8. Coefficient determination test

Table and presented Direct, Indirect and total Effect of the model

Table 9. Direct effect calculation

Table 10. Indirect effect calculation

Table 11. Total Effect Calculation Results

5. Discussion

Based on the results of the calculations in Table , it can be seen that the effect of Islamic financial literacy (X1), spiritual intelligence (X2), public perception (X3) on public behaviour (Y) simultaneously is 0.422 or 42.2%, other variables outside the model influence the rest. From Table , it can also be seen that the effect of Islamic financial literacy (X1), spiritual intelligence (X2), public perception (X3), public behaviour (Y) on public interest to Islamic banking services (Z) simultaneously is 0.592 or 59.2%, other variables outside the model influence the rest.

Direct effect calculations are presented in Table . Based on the calculation, the effect of Islamic financial literacy (X1) on public behaviour (Y) is 0.190, with aprobability of 0.215. Islamic financial literacy (X1) on public interest to Islamic banking services (Z) is 0.063 with a probability of 0.552. The effect of spiritual intelligence (X2) on public behaviour (Y) is −0.165, with a probability of 0.358. The effect of spiritual intelligence (X2) on public interest in Islamic banking services (Z) is 0.501 with probability. 0.000. The effect of public perception (X3) on public behaviour (Y) is 0.592 with a probability of 0.000. The effect of public perception (X3) on public interest in Islamic banking services (Z) is −0.023 with a probability of 0.839. The effect of public behaviour (Y) on public interest in Islamic banking services (Z) is 0.422 with probability. 0.000.

Indirect effect calculations are presented in Table . Based on the calculation, the effect of Islamic financial literacy (X1) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is 0.080 with a probability of 0.304. The effect of spiritual intelligence (X2) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is −0.070 with a probability of 0.336. The effect of public perception (X3) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is 0.250 with a probability of 0.001.

Total effect calculations are presented in . Based on the calculation, the total effect of Islamic financial literacy (X1) on public behaviour (Y) is 0.190, with a probability of 0.215. The total effect of Islamic financial literacy (X1) on public interest in Islamic banking services (Z) is 0.143, with a probability of 0.213. The total effect of spiritual intelligence (X2) on public behaviour (Y) is −0.165, with a probability of 0.358. The total effect of spiritual intelligence (X2) on public interest in Islamic banking services (Z) is 0.431, with a probability of 0.000. The total effect of public perception (X3) on public behaviour (Y) is 0.592, with a probability of 0.000. The total effect of public perception (X3) on public interest in Islamic banking services (Z) is 0.227, with a probability of 0.073. The effect of public behaviour (Y) on public interest in Islamic banking services (Z) is 0.422, with a probability of 0.000.

Table 12. Summary of direct, indirect, and total effect on dependent variable

For H1, the effect of Islamic financial literacy (X1) on public interest in Islamic banking services (Z) is 0.143 with a probability of 0.213. Islamic financial literacy (X1) has no significant effect on public interest in Islamic banking services (Z). H1 is rejected. The result is the same as previous studies by Abdullah and Anderson (Citation2015); Er and Mutlu (Citation2017). However, the results of this study contradict the research conducted by Nawi et al. (Citation2018); Lusardi (Citation2019). The higher people’s knowledge about Islamic finance has no impact on using an Islamic bank. They consider Islamic banks to be different from conventional banks, but this is not accompanied by a desire to use Islamic banking services. Lack of motivation or belief in Islamic banking is a separate part of literacy about Islamic banking.

For H2, the effect of spiritual intelligence (X2) on public interest in Islamic banking services (Z) is 0.501 with a probability of 0.000. Spiritual intelligence (X2) positively and significantly affects a public interest in Islamic banking services (Z). H2 is accepted. The result is the same as previous studies by Nugroho et al. (Citation2017); Agarwala et al. (Citation2019). People who have high spiritual intelligence will have a high religiosity. They will be manifested in activities and behaviour. Those who have this will always feel close to their god. In finance, they will choose things related to Islam compared to conventional banking. Their motivation in choosing an Islamic bank is to stay away from a disputed act. By choosing Islamic banking, he will feel calmer when compared to conventional banks.

For H3, the effect of public perception (X3) on public interest in Islamic banking services (Z) is 0.227, with a probability of 0.073. The public perception (X3) has no significant effect on public interest in Islamic banking services (Z). H3 is rejected. However, the results of this study contradict the research conducted by Wulandari and Subagio (Citation2015), Rahmi et al. (Citation2020), and Musa et al. (Citation2020). Customers’ perceptions of Islamic banking are not strong enough to make them interested in using Islamic banking services. Perceptions of Islamic banks are only limited to making customers give a small picture of Islamic banks. Perception is filled with prejudice and may not match reality. Prospective customers may misunderstand the difference between interest and profit-sharing, preventing public interest from using Islamic banking.For H4, the effect of Islamic financial literacy (X1) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is 0.080 with a probability of 0.304. Public behaviour (Y) has no evidence as mediating variable. H4 is rejected. Directly or indirectly, Islamic financial literacy (X1) does not significantly affect the public interest in Islamic banking services (Z). In this model, there is no partial or full mediation relationship. The result is the same as previous studies by Abdullah and Anderson (Citation2015); Er and Mutlu (Citation2017).

For H5, The effect of spiritual intelligence (X2) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is −0.070 with a probability of 0.336. Public behaviour (Y) has no evidence as mediating variable. H5 is rejected. There was only a significant direct relationship between spiritual intelligence (X2) and public interest in Islamic banking services (Z), while the indirect relationship was not proven. The result contradicted the result by Nugroho et al. (Citation2017); Agarwala et al. (Citation2019).

For H6, the effect of public perception (X3) through public behaviour (Y) as mediating variable on public interest to Islamic banking services (Z) is 0.250 with a probability of 0.001. In this model, there is a complete mediation where public perception (X3) cannot influence public interest to Islamic banks without going through the mediator variable public behaviour (Y). H6 is accepted. There is no significant effect in the calculation of the direct effect, but in the indirect relationship, the opposite occurs. The results of this study same as previous studies by Wulandari and Subagio (Citation2015), Rahmi et al. (Citation2020), and Musa et al. (Citation2020). Public perception directly is not strong enough to increase public interest in using Islamic banking products. However, perceptions have a direct effect on public behaviour as indicated by changes in attitude, control of perception and subjective norms of Islamic banking. Eventually, an increase in public perception will increase public interest in Islamic banking products through changes in public behaviour.

6. Conclusion

The research examines the effect of Islamic financial literacy, spiritual intelligence, public perception, and behaviour on public interest in Islamic banking services. The results show Islamic financial literacy and public perception have no significant effect on public interest in Islamic banking services. However, spiritual intelligence has a positive and significant effect on public interest in Islamic banking services. Public behaviour fully mediates the relationship between public perception and public interest in Islamic banking services.

Islamic financial literacy is not strong enough to change the choice from conventional banks to Islamic banks. It is because financial literacy is not accompanied by the motivation and desire to use Islamic banking services. The public perception may be wrong about interest or profit-sharing, thus causing disinformation and concluding that there is no difference between conventional and Islamic banks. Spiritual intelligence embodied in religiosity can make prospective customers choose Islamic banks to avoid bank interest. Public behaviour fully mediates the relationship between public perception and public interest in Islamic banking services because public perception is not strong enough to change the choice of prospective customers. Public perception will be able to change the choice of prospective customers if public perception can improve public behaviour first.

Acknowledgements

All authors would like to thank Universitas Putra Indonesia YPTK Padang and Yayasan Perguruan Tinggi Komputer for financial support. Any remaining errors are our own.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Fitri Yeni

Fitri Yeni is a lecturer at Faculty of Economics and Business, Universitas Putra Indonesia YPTK Padang. She is a management doctoral candidate. Her research interest could be found in financial management, corporate governance and Islamic banking.

Sitti Rizki Mulyani

Sitti Rizki Mulyani is a lecturer at Faculty of Economics and Business, Universitas Putra Indonesia YPTK Padang. She is a management doctoral candidate. Her research related to financial management and human resource management.

Susriyanti Susriyanti

Susriyanti Susriyanti is a lecturer at Faculty of Economics and Business, Universitas Putra Indonesia YPTK Padang. She is a management doctoral candidate. Her research related to human resource management and corporate governance.

References

- Abdullah, M. A., & Anderson, A. (2015). Islamic financial literacy among bankers in Kuala Lumpur. Journal of Emerging Economies and Islamic Research, 3(2), 79–19. https://doi.org/10.24191/jeeir.v3i2.9061

- Agarwala, R., Mishra, P., & Singh, R. (2019). Religiosity and consumer behaviour: A summarizing review. Journal of Management, Spirituality & Religion, 16(1), 32–54. https://doi.org/10.1080/14766086.2018.1495098

- Ahmad, G., Widyastuti, U., Susanti, S., & Mukhibad, H. (2020). Determinants of the Islamic financial literacy. Accounting, 6(6), 961–966. https://doi.org/10.5267/j.ac.2020.7.024

- Alam, M. K., Ab Rahman, S., Mustafa, H., Shah, S. M., & Hossain, M. S. (2019). Shariah governance framework of Islamic banks in Bangladesh: Practices, problems and recommendations. Asian Economic and Financial Review, 9(1), 118. https://doi.org/10.18488/journal.aefr.2019.91.118.132

- Ali, M., & Raza, S. A. (2017). Service quality perception and customer satisfaction in Islamic banks of Pakistan: The modified SERVQUAL model. Total Quality Management & Business Excellence, 28(5–6), 559–577. https://doi.org/10.1080/14783363.2015.1100517

- Apuke, O. D. (2017). Quantitative research methods: A synopsis approach. Kuwait Chapter of Arabian Journal of Business and Management Review, 33(5471), 1–8. https://doi.org/10.12816/0040336

- Chaouch, N. (2017). An exploratory study of Tunisian customers’ awareness and perception of Islamic banks. International Journal of Islamic Economics and Finance Studies, 3, 2. https://doi.org/10.25272/j.2149-8407.2017.3.2.01

- Dhiman, S. (2019). Doing the Right Thing: Leaders’ Moral and Spiritual Anchorage. In Bhagavad Gītā and Leadership. Palgrave Studies in Workplace Spirituality and Fulfillment. Cham: Palgrave Macmillan. https://doi.org/10.1007/978-3-319-67573-2_9

- Dinc, Y., Çetin, M., Bulut, M., & Jahangir, R. (2021). Islamic financial literacy scale: An amendment in the sphere of contemporary financial literacy. ISRA International Journal of Islamic Finance, 13(2), 251–263. http://dx.doi.org/10.1108/IJIF-07-2020-0156

- Er, B., & Mutlu, M. (2017). Financial inclusion and Islamic finance: A survey of Islamic financial literacy index. International Journal of Islamic Economics and Finance Studies, 3, 2. https://doi.org/10.25272/j.2149-8407.2017.3.2.02

- Ezeh, P. C., & Nkamnebe, A. D. (2019). Islamic bank selection criteria in Nigeria: A model development. Journal of Islamic Marketing, 11(6), 1837–1849. https://doi.org/10.1108/JIMA-06-2019-0123

- Hair, J. J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hanefar, S. B., Sa’ari, C. Z., & Siraj, S. (2016). A synthesis of spiritual intelligence themes from Islamic and western philosophical perspectives. Journal of Religion and Health, 55(6), 2069–2085. https://doi.org/10.1007/s10943-016-0226-7

- Hassenzahl, M., Wiklund-Engblom, A., Bengs, A., Hägglund, S., & Diefenbach, S. (2015). Experience-oriented and product-oriented evaluation: Psychological need fulfillment, positive affect, and product perception. International Journal of human-computer Interaction, 31(8), 530–544. https://doi.org/10.1080/10447318.2015.1064664

- Hosen, M. N., Lathifah, F., & Jie, F. (2019). Perception and expectation of customers in Islamic bank perspective. Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-12-2018-0235

- Kaakeh, A., Hassan, M. K., & van Hemmen Almazor, S. F. (2018). Attitude of Muslim minority in Spain towards Islamic finance. International Journal of Islamic and Middle Eastern Finance and Management, 11(2), 213–230. https://doi.org/10.1108/IMEFM-11-2017-0306

- Kashif, M., Rehman, M. A., & Pileliene, L. (2016). Customer perceived service quality and loyalty in Islamic banks: A collectivist cultural perspective. The TQM Journal, 28(1), 62–78. https://doi.org/10.1108/TQM-01-2014-0006

- Ltifi, M., Hikkerova, L., Aliouat, B., & Gharbi, J. (2016). The determinants of the choice of Islamic banks in Tunisia. International Journal of Bank Marketing, 34(5), 710–730. https://doi.org/10.1108/IJBM-11-2014-0170

- Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. https://doi.org/10.1186/s41937-019-0027-5

- Mahadin, B. K., & Akroush, M. N. (2019). A study of factors affecting word of mouth (WOM) towards Islamic banking (IB) in Jordan. International Journal of Emerging Markets, 14(4), 639–667. https://doi.org/10.1108/IJOEM-10-2017-0414

- Mahasneh, A. M., Shammout, N. A., Alkhazaleh, Z. M., Al-Alwan, A. F., & Abu-Eita, J. D. (2015). The relationship between spiritual intelligence and personality traits among Jordanian university students. Psychology Research and Behaviour Management, 8, 89. https://doi.org/10.2147/PRBM.S76352

- Mha, K. (2015). A mobile banking adoption model in the Jordanian market: An integration of TAM with perceived risks and perceived benefits. The Journal of Internet Banking and Commerce, 20(3), 1. https://doi.org/10.4172/1204-5357.1000128

- Musa, M. A., Abd Sukor, M. E., Ismail, M. N., & Elias, M. R. F. (2020). Islamic business ethics and practices of Islamic banks: Perceptions of Islamic bank employees in Gulf cooperation countries and Malaysia. Journal of Islamic Accounting and Business Research, 11(5), 1009–1031. https://doi.org/10.1108/JIABR-07-2016-0080

- Nawi, F. A. M., Daud, W. M. N. W., Ghazali, P. L., Yazid, A. S., & Shamsuddin, Z. (2018). Islamic financial literacy: A conceptualization and proposed measurement. International Journal of Academic Research in Business and Social Sciences, 8(12), 629–641. http://dx.doi.org/10.6007/IJARBSS/v8-i12/5061

- Nouman, M., Ullah, K., & Gul, S. (2018). Why Islamic banks tend to avoid participatory financing? A demand, regulation, and uncertainty framework. Business & Economic Review, 10(1), 1–32. http://dx.doi.org/10.22547/BER/10.1.1

- Nugroho, A. P., Hidayat, A., & Kusuma, H. (2017). The influence of religiosity and self-efficacy on the saving behaviour of the Islamic banks. Banks and Bank Systems (open-access), 12(3), 35–47. http://dx.doi.org/10.21511/bbs.12(3).2017.03

- Pitchay, A. B. A., Thaker, M. A. B. M. T., Azhar, Z., Mydin, A. A., & Thaker, H. B. M. T. (2019). Factors persuade individuals’ behavioural intention to opt for Islamic bank services: Malaysian depositors’ perspective. Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-02-2018-0029

- Py Lai, K., & Samers, M. (2017). Conceptualizing Islamic banking and finance: A comparison of its development and governance in Malaysia and Singapore. The Pacific Review, 30(3), 405–424. https://doi.org/10.1080/09512748.2016.1264455

- Rahmi, M., Azma, N., Obad, F. M., Zaim, M., & Rahman, M. (2020). Perceptions of Islamic banking products: Evidence from Malaysia. The Journal of Business Economics and Environmental Studies, 10(3), 35–42. https://doi.org/10.13106/jbees.2020.vol10.no3.35

- Raza, S. A., Shah, N., & Ali, M. (2019). Acceptance of mobile banking in Islamic banks: Evidence from modified UTAUT model. Journal of Islamic Marketing, 10(1), 357–376. https://doi.org/10.1108/JIMA-04-2017-0038

- Sarofim, S., Minton, E., Hunting, A., Bartholomew, D. E., Zehra, S., Montford, W., Cabano, F., & Paul, P. (2020). Religion’s influence on the financial well‐being of consumers: A conceptual framework and research agenda. Journal of Consumer Affairs, 54(3), 1028–1061. https://doi.org/10.1111/joca.12315

- Selvanathan, M., Nadarajan, D., Zamri, A. F. M., Suppramaniam, S., & Muhammad, A. M. (2018). An exploratory study on customers’ selection in choosing Islamic banking. International Business Research, 11(5), 42–49. https://doi.org/10.5539/ibr.v11n5p42

- Setiawati, R., Nidar, S. R., Anwar, M., & Masyita, D. (2018). Islamic financial literacy: Construct process and validity. Academy of Strategic Management Journal, 17(4), 1–12. https://www.abacademies.org/articles/islamic-financial-literacy-construct-process-and-validity-7384.html

- Sirine, H., & Kurniawati, E. P. (2018). The importance of spirituality dimensions in the development of entrepreneurship. Diponegoro International Journal of Business, 1(2), 55–70. https://doi.org/10.14710/dijb.1.2.2018.55-70

- Suzuki, Y., Uddin, S. S., & Sigit, P. (2019). Do Islamic banks need to earn extra profits? A comparative analysis on banking sector rent in Bangladesh and Indonesia. Journal of Islamic Accounting and Business Research, 10(3), 369–381. https://doi.org/10.1108/JIABR-01-2017-0003

- Usman, H., Tjiptoherijanto, P., Balqiah, T. E., & Agung, I. G. N. (2017). The role of religious norms, trust, importance of attributes and information sources in the relationship between religiosity and selection of the Islamic bank. Journal of Islamic Marketing, 8(2), 158–186. https://doi.org/10.1108/JIMA-01-2015-0004

- Vasconcelos, A. F. (2020). Spiritual intelligence: A theoretical synthesis and work-life potential linkages. International Journal of Organizational Analysis, 28(1), 109–134. https://doi.org/10.1108/IJOA-04-2019-1733

- Wulandari, D., & Subagio, A. (2015). Consumer decision making in conventional banks and Islamic bank based on quality of service perception. Procedia-Social and Behavioural Sciences, 211, 471–475. https://doi.org/10.1016/j.sbspro.2015.11.062

- Zarrouk, H., Jedidia, K. B., & Moualhi, M. (2016). Is Islamic bank profitability driven by same forces as conventional banks? International Journal of Islamic and Middle Eastern Finance and Management, 9(1), 46–66. https://doi.org/10.1108/IMEFM-12-2014-0120