?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the consistency of asymmetric interest rate past-trough (IRPT) using a nonlinear autoregressive distributed lag framework. Superior to the previous studies, this study exploits the historical profile of Indonesia to enrich the analysis. Asian Financial Crisis (AFC) which crashed the country in 1998 and several monetary policy changes implemented by the government offer different perspectives to grasp IRPT. The results of this study indicate that there is a consistent upward rigidity in the long-run pass-through in Indonesia. Particularly during the AFC, it is well proven that the asymmetric behavior is fickle whether disappear or bounce back to the downward rigidity. This finding demonstrates the importance of a rolling-window approach in understanding IRPT.

PUBLIC INTEREST STATEMENT

Indonesia has experienced several important adjustments of its monetary system after the worst Asian Financial Crisis in 1998. The alteration could potentially offer fresh insights on understanding interest rate pass-through. Therefore, this study aims to test the consistency of the widely accepted phenomenon of asymmetric interest rate pass-through with in a nonlinear autoregressive distributed lag framework. The analysis shows that that structural break analysis does not capture any change in the asymmetric pass-through, while a rolling window estimation approach performs well and relates to the change in economic environment. This implies that the monetary authority should expect the asymmetric pass-through characteristics to be time-varying.

1. Introduction

Interest rate as one of transmission channels shows an important role in stabilizing inflation in Indonesia (Wulandari, Citation2012). However, as postulated by Taylor (Citation1993), central banks should give special treatment to the transmission process due to the presence of natural rigidity in the economy that prevents any immediate changes. In the context of interest rate, rigidity could be defined as the adjustment cost that arises when the bank has to change price, which made the change in policy rate not always matched to the change in commercial banks rate, or commonly mentioned in this strand of literature as an incomplete degree of pass-through (see Cottarelli and Kourelis (Citation1994)). Whether pass-through is complete or partial is a subject of immense policy interest. Regarding to this fact, the behavior of interest rate pass-through for Indonesia is still unknown.

This study aims to explore the interest rate pass-through (IRPT) because that is the common transmission between money market rate to lending rate. The term includes direct pass-through and adjustment speed,Footnote1 such as those that can be gauged from a cointegrating model (see Andries and Billon (Citation2016)). According to Gambacorta (Citation2008), the factors that could affect the degrees of IRPT and the time-varying characteristic of IRPT vary and behave asymmetrically. It is relied on the degree of competitiveness in the bank industry which both are negatively correlated. Under the imperfect competition, the lending rate is more rigid. Meanwhile under tight competition, financial institution may avoid to adjust the loan rate upwards in order to minimize the loss to consumers (Hofmann, Citation2006).

A study by Hannan and Berger (Citation1991) provides evidence for the case of downward rigidity in lending rate and produce a collusive pricing theory. On the other hand, several studies provide evidence that the case of upward rigidity in lending rate as the consequence of consumer adverse behavior (CitationNeumark and Sharpe Citation1992). Evidence from European Union countries shows that the degree of asymmetry becomes even since those countries are merged under the scheme of European Monetary Union (EMU) (Sander and Kleimeier Citation2004). Nevertheless, Apergis and Cooray (Citation2015) found out that the degree of asymmetry in American and Australuan banks are differ due to the zero-lower bound effect after the Global Financial Crisis (GFC). In the context of Indonesia, this asymmetry case had been explored by several previous studies, however there is till none of the studies which investigates the dynamic behavior (see Zulverdi et al., Citation2007; Wang & Lee, Citation2009). Therefore, this study is intended to fill up the gap by harnessing the financial crisis phenomenon that hardly hit the country and economic policy changes which has been implemented by the government to delve the evidence about the dynamic behavior of IRPT.

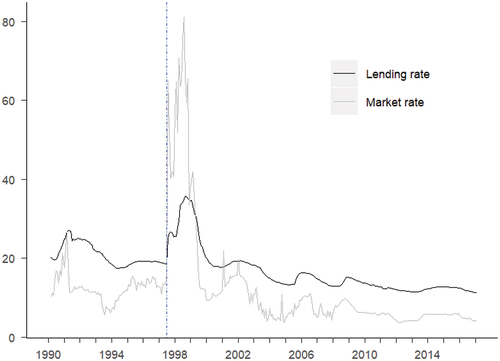

The most notable event for Indonesia in terms of crises has been the Asian Financial Crisis (AFC) in 1997–1998 and the 2007 GFC. The AFC impacted Indonesia more than the GFC because of lack of exchange rate flexibility prior to the AFC (Berkmen et al., Citation2012). At the first glance, from Figure , we can see the impact of AFC that mainly occurs on 1997:7 when the Indonesian currency starts to plunge. Aside from the obvious turmoil in the money market and lending rates, there is some evidence that loosening monetary policy is not well transmitted due to risk adverse behavior and credit crunch in the aftermath of AFC (Zulverdi et al., Citation2007). In the IRPT context, this should be depicted as an upward rigidity in the aftermath of the AFC. The monetary environment in Indonesia also has undergone one significant change recently. The central bank of Indonesia, namely, Bank Indonesia (BI), introduced a new policy rate effective from 2016:8. This policy saw a change from policy-stance rate of 1-month tenor to government bond reverse repo rate with a 7-day tenor. This change explicitly explained by BI as a priori assumption of the downward rigidity in the pass-through.Footnote2

Figure 1. Money market and lending rate from 1990:3 to 2017:2. Note: The blue dot-dashed line represents the start of AFC in 1997:7. The impact of AFC that mainly occurs on 1997:7 when the Indonesian currency starts to plunge.

Wang and Lee (Citation2009) use error-correction exponential generalized autoregressive conditional heteroskedasticity in mean (EC-EGARCH-M) model and found no asymmetric IRPT with a data sample covering 1988:2 to 2004:12. However, this study is an extending work of Wang and Lee (Citation2009) which utilize the latest dataset and approach to capture the most recent events that matter to Indonesia’s IRPT. We use the nonlinear autoregressive distributed lag (NARDL) cointegration framework to estimate based on the work of Zhang et al. (Citation2017). We choose this framework because it can capture long-run pass-through asymmetry in Indonesia’s IRPT. This measurement is important to evaluate any asymmetries in the long-run marginal effect. We also model specifically structural breaks in the data to identify the policy shifts period to avert bias estimates (see Narayan & Popp, Citation2010, Citation2013).

The results of this study indicate that there is an upward rigidity in the long-run pass-through in Indonesia. This appears to contradict Bank Indonesia’s assumption of downward rigidity. The result of upward rigidity is consistently happened when estimated using sub-samples of data as well as estimated using a rolling window approach. By the rolling-window estimation, particularly during the AFC, it is proven that the asymmetric behavior is fickle whether disappear or bounce back to the downward rigidity. This finding demonstrates the importance of a rolling-window approach in understanding IRPT.

This paper is organized as follows: Section 2 contains a brief review of the literature related to our main research question; Section 3 describes the data and methodology; Section 4 presents the results; and Section 5 concludes the findings in this paper.

2. Literature review

We provide selected studies that focus on the time-varying nature of asymmetric IRPT. These studies would potray the research gap in this literature; see summary presented in Table .

Table 1. Related studies

In this literature, early finding suggests that an asymmetric long-run relation between money market rate and commercial bank lending rate exists; see Hannan and Berger (Citation1991) and Neumark and Sharpe (Citation1992). Their results bring cross-bank evidence regarding an asymmetric adjustment in commercial bank’s rate toward any changes in money market rate. The first effort to measure this asymmetric adjustment using a cointegration framework can be attributed to Borio and Fritz (Citation1995), who found presence of downward rigidity for German, Japan, and the United States. In their research, they relate the observed asymmetry with the financial market behavior and structure, which supports both consumer adverse theory and collusive pricing theory. Recent studies (Holmes et al., Citation2015; Payne Citation2006, Citation2007b; Wang & Lee, Citation2009; Zhang et al., Citation2017) also follow this notion to explain the presence of asymmetric IRPT.

On the methodological aspect, it is important to point out the popularity of sample-split error-correction model (ECM) approach adopted by Borio and Fritz (Citation1995), which later inspired the threshold autoregression (TAR) framework (see Lim, Citation2001) and the NARDL framework (see Greenwood-Nimmo et al., Citation2010) for IRPT analysis. One difference between the TAR and the NARDL models is that in the TAR-based model the asymmetric short-run pass-through could also be measured by decomposing the first-difference of money market (Valadkhani & Anwar, Citation2012; Valadkhani & Bollen, Citation2013; Valadkhani & Worthington, Citation2014), the asymmetric long-run pass-through is still exclusive in the NARDL framework.

Another influential finding in this literature is the dynamic nature of IRPT. Some examples that support dynamic IRPT can be attributed to Sander and Kleimeier (Citation2004) and De Bondt (Citation2005). They postulate the role of a more competitive banking industry and a more stable money market rate to create a higher degree of IRPT in EU countries after the advent of European Monetary Union (EMU). Overall, the dynamic nature of IRPT is heavily related to the dynamics in its underlying factor.

Most research that focuses on the dynamics of IRPT relies on sub-period estimation with a structural break test and dummy variable-based regression (Belke et al., Citation2013; De Bondt, Citation2005; Chionis & Leon, Citation2006; Sander & Kleimeier, Citation2004). Angeloni and Ehrmann (Citation2003) use an alternative approach to measure the dynamics in the pass-through, that is through using a rolling window estimation approach to obtain a more trackable change. Interestingly, the findings from Angeloni and Ehrmann (Citation2003) are still inline with the findings from sub-period estimation in Sander and Kleimeier (Citation2004) and De Bondt (Citation2005). Though, the findings from Angeloni and Ehrmann (Citation2003) and De Bondt (Citation2005) are in contrast to the findings of Marotta (Citation2009), who found a decrease in pass-through instead when dating the break endogenously. Aside from the debate regarding the contrary results, these papers show the importance of selecting the window of estimation to avoid a bias in interpretation. This further suggests the importance of using a rolling-window estimation to track any changes in IRPT to complement the sub-period estimation based on a structural break analysis.

3. Data and methodology

3.1. Data

The data used in this paper are publicly available in the International Financial Statistics. For the lending rate, we choose working capital rate as a proxy because of its importance in the broad business sense (see Mishra et al. (Citation2014)). As for the money market rate, we choose to focus on the common interbank market rate, which is available for a longer period than the recently introduced BI interbank market rate, and the Jakarta Interbank Office Rate (JIBOR) which is unavailable prior to the AFC. The unavailability of JIBOR before the AFC is indeed the limitation of this paper. Nevertheless, we will still use the JIBOR for robustness tests (see Section 4.3). The interest rate is seasonally unadjusted, indicated that the monetary policy has deseasonalized interest rate. The data used in this paper are monthly and covers the period 1990:3 to 2017:2. The robustness test, by comparison, covers the sample period 2000:3 to 2017:2.

3.2. Asymmetric cointegration model

To capture the asymmetric cointegration and long-run pass-through, we decide to use NARDL model of Shin et al. (Citation2014). The NARDL model has the same advantage as the autoregressive distributed lag (ARDL) model in capturing any cointegrating relation. This test also supports the rolling window estimation, which does not guarantee that all variables will be non-stationary. Given this possibility the NARDL (like the ARDL) is advantageous compared to the Engle and Granger (Citation1987), Johansen (Citation1995), and any TAR-based methods.

To explain the model used, consider a long-run asymmetric relation of money market rate, , to the lending rate,

,

where and

denote upward and downward long-run pass-through, respectively. The decomposition from

to

and

follows a partial sum process suggested by Shin et al. (Citation2014):

with , and

.

According to Shin et al. (Citation2014), the NARDL model followed the ARDL model property introduced by Pesaran and Shin (Citation1999) and Pesaran et al. (Citation2001), which can be used to estimate the long and short-run model using a single equation approach. As suggested by Shin et al. (Citation2014), the underlying ARDL process of Equationequation (1)(1)

(1) could then be written as follows,

where is the autoregressive parameter;

and

are the asymmetric distributed lag parameters; and

is an iid process with zero mean and constant variance,

.

As suggested by Pesaran et al. (Citation2001), the error-correction form, then,could be rewritten from Equationequation (3)(3)

(3) as follow,

with ,

and

are now computed as

,

, and

. For a full calculation procedure and statistical properties, see Shin et al. (Citation2014).

From Equationequation (4)(4)

(4) , the asymmetric cointegration could be tested using the Pesaran et al. (Citation2001) bound test with the null hypothesis of

. For the asymmetric long-run pass-through, we follow Shin et al. (Citation2014) to test the null hypothesis of

using Wald test.

The optimal lags of and

are decided based on the minimal Schwarz Information Criterion (SIC). We consider a maximum of 3 lags to accommodate any dynamic effects.

3.3. Testing the consistency of asymmetric pass-through

To test the consistency of the asymmetric long-run pass-through we estimate the model in sub-samples of data. We decide on sub-samples, we undertake a structural break unit root test of Lee and Strazicich (Citation2003, Citation2013), and then use the break dates to create sub-samples.

To get more trackable results regarding any changes, we then conduct the rolling window estimation using NARDL model. The window used for estimation is set to 120, which is more than the minimum window (of 100 data points) suggested by Shin et al. (Citation2014).

4. Results

4.1. Structural break and sub-period estimation

The unit-root test results are presented in Table . As a complementary analysis for cointegration, we also report some unit-root test without structural breaks for the full-period. More specifically, we consider the augmented Dickey and Fuller (Citation1979) test, the Phillips and Perron (Citation1988) test, and Kwiatkowski et al. (Citation1992) test. From the unit root test without structural breaks, we can conclude that lending and market rates are unit root processes.

Table 2. Unit root and structural break test

On the structural break test, there is evidence of two breaks that occurred around the period of the AFC. Specifically, the first break occurs just before the peak of the downfall in the Indonesian currency in 1997:7 and the second break occurs in 2000:2 which coincides with the stabilization period after some effort by BI to manage risk perception in the banking industry. Since the period between the two breaks is relatively short and highly volatile, we exclude the short period around the break from the estimation.Footnote3 The estimation, then, covering the pre-AFC pass-through using data from 1990:3 to 1997:6, and post-AFC pass-through using data from 2000:2 to 2017:2.

The results from sub-period estimation are presented in Table . The long-run parameters from the pre-AFC period are showing an over than unitary pass-through of 114.68–131.57 percent. The asymmetric long-run pass-through test statistically confirms the asymmetry as the presence of upward rigidity. The short-run parameters show a relatively low pass-through of 1.21–7.91 percent and contrary to the upward rigidity in the long-run. While the long-run pass-through parameters are showing an exceptionally high rate, the estimated adjustment rate shows a relatively low rate in the pre-AFC period, that only 6.89 percent.

Table 3. Results from sub-period estimations

The results from the post-AFC period show a decrease in almost all parameters, except for the adjustment rate. The long-run parameters and asymmetric tests are still consistent in that they suggest the presence of upward rigidity, but the pass-through are now only ranging from 38.67 percent to 44.08 percent. The short-run parameters are now in-line with long-run parameters in suggesting the presence of upward rigidity and also happened to show a decrease to 3.19 percent in downward pass-through, while the upward one is almost zero and insignificant. The adjustment speed showing a slight improvement to 7.24 percent. These obtained parameters in the pre-AFC period differ from results reported in Wang and Lee (Citation2009). One reason for this difference is that their study does not analyze the impact of the AFC.

4.2. Rolling window estimation results

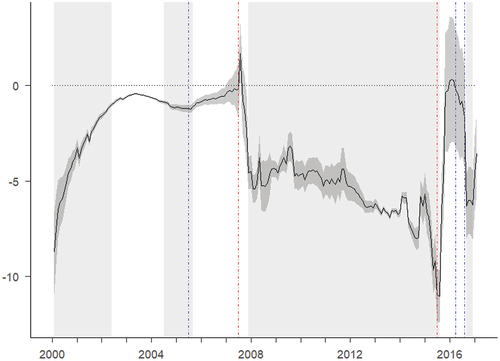

The results from sub-period estimation clearly suggest a consistent long-run upward rigidity for Indonesia, both in pre- and post-AFC. We test this consistency using a different approach—that is a rolling window estimation. Figure shows the stability of the asymmetry in (a) cointegration and (b) long-run pass-through. Specific result comparing the upward and downward pass-through is presented in Figure

Figure 2. The stability of asymmetric in cointegration and long-run pass-through. Note: The x-axis shows the last observation used in the window. For (a) bound test results, the solid line represents the estimated F-statistics that standardized to its relevant upper bound 10 percent critical value, which presented in dotted line. For (b) asymmetric long-run pass-through results, the solid line represents the p-value from Wald test, and the dotted line represents the 10 percent critical value.

Figure 3. The dynamics of asymmetric long-run pass-through across period. Note: The x-axis shows the last observation used in the window. The solid line represents the difference between upward and downward pass-through, with darker shade represents its standard errors. The light shades represent a window in which the asymmetric long-run pass-through is statistically significant. The blue dot-dashed lines represent the events related to last observation in the window, that is the introduction of ITF, the announcement to change the policy rate, and the effective change in the policy rate respectively. The red dot-dashed lines represent the events related to first observation in the window, that is the start of AFC crisis, and the introduction of ITF respectively.

From Figure we can conclude that the asymmetric cointegration is statistically significant in all periods, while the asymmetric long-run pass-through is only statistically significant in several periods. Results in Figure further explain that the observed significances of asymmetric long-run pass-through tests are inline with the changes in the degree of asymmetry.

Following the work of Angeloni and Ehrmann (Citation2003), we will present the results using the last date of the windows, and see if there is any related economic events at that date. But as we can see from Figure , the level change in the degree of asymmetry could also be explained using the first date of the window, similar to sub-period estimation approach with structural break context. Thus, we will also consider any economic events that related to the first date of the window.

From Figure , we can conclude that the asymmetric long-run pass-through is not consistently present in Indonesia, contrary to the results of sub-period estimation. The asymmetry, however, happens to be related to changes in monetary environment and AFC. For instance, after the last observation in the window passed the Inflation Targeting Framework (ITF) implementation date in 2005:7, the degree of asymmetry is disappears gradually then becoming statistically insignificant, which shows the success of BI’s ITF (that is, to control inflation through the higher interest rate). Later, after the first observation in the window becomes the start of AFC (1997:7), the degree of asymmetry shows a spike into a downward rigidity that represents the crisis period, when the monetary stances are mostly set to be tightening. The degree of asymmetry stabilizes when the last observation in the window is 1999:10.

However, once the first observation in the window leaves the pre- ITF period, the degree of asymmetry becomes statistically insignificant which implies that the ITF implementation consistently minimized the degree of asymmetry. This suggests that the ITF implementation has had an impact similar to the post-AFC period. We also find the period between the post-AFC and pre-ITF to be highly in favor of upward rigidity, while the post-ITF period is more likely to show no asymmetry in the long-run pass-through.

Like the ITF implementation, the latest change in policy rate could also be seen altering the degree of asymmetry. When the last observation in the estimation window enters the date of the latest policy rate change (2016:8), the lending rate in the post-ITF period becomes more responsive to loosening policy, which is also supported by asymmetric test results. Interestingly, this effect is already set in after the announcement of the change in 2016:4, showing the market expectation towards a more loosening policy stance.

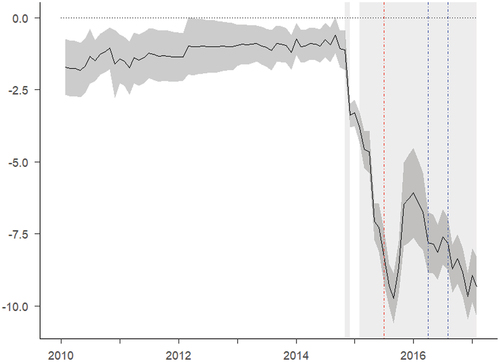

4.3. Robustness check

For robustness check, we use JIBOR as an alternative proxy for market rate. Due to data availability, we only conduct rolling window estimation and focus the analysis on the period 2000:3 to 2017:2. The result is presented in Figure . The post-AFC and pre-ITF periods do not show a significant upward rigidity as in the previous result. Also, in the post-ITF period, degree of asymmetry does not become insignificant as in the previous result. These results show that the overall upward rigidity is not as strong as in common money market rate case. Nevertheless, the obtained result shows a very similar dynamic as in the previous results and still suggests the consistency of upward rigidity across the period.

Figure 4. The dynamics of asymmetric long-run pass-through across period using different proxy for money market. Note: The x-axis shows the last observation used in the window. The solid line represents the difference between upward and downward pass-through, with darker shade represents its standard errors. The light shades represent a window in which the asymmetric long-run pass-through is statistically significant. The blue dot-dashed lines represent the events related to last observation in the window, that is the announcement to change the policy rate, and the effective change in the policy rate respectively. The red dot-dashed line represents the event related to first observation in the window, that the introduction of ITF.

5. Conclusion

In this paper we test the hypothesis that interest rate pass-through for Indonesia is asymmetric. This hypothesis is motivated by not only lack of evidence on understanding Indonesia’s interest rate pass-through but also given the role potentially played by financial crises (which in Indonesia’s case are not modelled to-date) and recent monetary policy changes.

Using data from 1990:3 to 2017:2, we demonstrate the use of sub-period and rolling window estimation in testing the asymmetry and its consistency. From the results, we conclude that upward rigidity is exist in overall period of 1990:3 to 2017:2. However, the rolling window estimation shows that the tendency of downward rigidity exists in aftermath of the AFC and post-ITF period, though it is not statistically significant. These results are robust to the proxy selection for money market rate. Our results contradict Bank Indonesia’s a priori assumption of downward rigidity in the lending rate. The findings, instead, suggest that there is a tendency of zero lower bound, which should constitute an important consideration for Bank Indonesia’s future policy move.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

R. Dimas Bagas Herlambang

Dimas Bagas Herlambang is an independent researcher and Risk Advisory Associate at Deloitte Indonesia. His research interests are in the field of macroeconomics and monetary policy.

Rudi Purwono

Rudi Purwono is a senior lecturer at Faculty of Economics and Business of Airlangga University, Indonesia. He is one of the vice deans of the faculty. He has published articles, among others, in Economic Change and Restructuring, The Journal of Asian Finance, Economics, and Business, Journal of Advances in Social Science and Humanities, and Seoul Journal of Economics.

Rumayya

Rumayya is a lecturer Faculty of Economics and Business of Airlangga University, Indonesia. He holds a doctorate degree in economics from University of Western Australia. He has published article in International Journal of Financial Studies.

Notes

1. In interest rate adjustment, it should be noted that there is a main distinction between direct pass-through and speed of adjustment. The direct pass-through context refers to marginal cost theories (see Freixas & Rochet, Citation2008), while the adjustment speed refers to the stickiness in the adjustment (see Cottarelli & Kourelis, Citation1994).

2. This assumption is expressed in its monetary operating procedure by using a wider gap in deposit facility rate, which represents the floor price. The BI also claim that the significant drop in the new rate is needed in order to ease the reduction in lending rate. See BI press release for August 2016 for further details regarding this change (https://www.bi.go.id/en/ruang-media/siaran-pers/Pages/sp_186716.aspx).

3. While the small sample in that period could be handled using procedure in Narayan (Citation2005), the turmoil during that period made the estimation results hard to be interpreted economically. Thus, we follow Alberola et al. (Citation2008) to exclude this period. However, the estimation result is available upon request.

References

- Alberola, E., Chevallier, J., & Chèze, B. (2008). Price drivers and structural breaks in european carbon prices 2005–2007. Energy Policy, 36(2), 787–12. https://doi.org/10.1016/j.enpol.2007.10.029

- Andries, N., & Billon, S. (2016). Retail bank interest rate pass-through in the euro area: An empirical survey. Economic Systems, 40(1), 170–194. https://doi.org/10.1016/j.ecosys.2015.06.001

- Angeloni, I., & Ehrmann, M. (2003). Monetary transmission in the euro area: Early evidence. Economic Policy, 18(37), 469–501. https://doi.org/10.1111/1468-0327.00113_1

- Apergis, N., & Cooray, A. (2015). Asymmetric interest rate pass-through in the US, the UK and Australia: New evidence from selected individual banks. Journal of Macroeconomics, 45, 155–172. https://doi.org/10.1016/j.jmacro.2015.04.010

- Belke, A., Beckmann, J., & Verheyen, F. (2013). Interest rate pass-through in the EMU–new evidence from nonlinear cointegration techniques for fully harmonized data. Journal of International Money and Finance, 37, 1–24. https://doi.org/10.1016/j.jimonfin.2013.05.006

- Berkmen, S. P., Gelos, G., Rennhack, R., & Walsh, J. P. (2012). The global financial crisis: Explaining cross-country differences in the output impact. Journal of International Money and Finance, 31(1), 42–59. https://doi.org/10.1016/j.jimonfin.2011.11.002

- Borio, C. E. V., & Fritz, W. (1995). The response of short-term bank lending rates to policy rates: A cross-country perspective. working paper No. 27, 21 May, Bank for International Settlement.

- Chionis, D. P., & Leon, C. A. (2006). Interest rate transmission in Greece: Did EMU cause a structural break? Journal of Policy Modeling, 28(4), 453–466. https://doi.org/10.1016/j.jpolmod.2005.10.003

- Cottarelli, C., & Kourelis, A. (1994). Financial structure, bank lending rates, and the transmission mechanism of monetary policy. Staff Papers, 41(4), 587–623. https://doi.org/10.2307/3867521

- De Bondt, G. J. (2005). Interest rate pass‐through: Empirical results for the euro area. German Economic Review, 6(1), 37–78. https://doi.org/10.1111/j.1465-6485.2005.00121.x

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74, 427–431. https://doi.org/10.2307/2286348

- Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society, 55(2), 251–276. https://doi.org/10.2307/1913236

- Freixas, X., & Rochet, J. C. (2008). Microeconomics of banking. MIT press.

- Gambacorta, L. (2008). How do banks set interest rates? European Economic Review, 52(5), 792–819. https://doi.org/10.1016/j.euroecorev.2007.06.022

- Greenwood-Nimmo, M., Shin, Y., & van Treeck, T. (2010). The great moderation and the decoupling of monetary policy from long-term rates in the US and Germany. working paper, IMK.

- Hannan, T. H., & Berger, A. N. (1991). The rigidity of prices: Evidence from the banking industry. The American Economic Review, 81, 938–945. https://www.jstor.org/stable/2006653

- Hofmann, B. (2006). EMU and the transmission of monetary policy: Evidence from business lending rates. Empirica, 33(4), 209–229. https://doi.org/10.1007/s10663-006-9002-3

- Holmes, M. J., Iregui, A. M., & Otero, J. (2015). Interest rate pass through and asymmetries in retail deposit and lending rates: An analysis using data from Colombian banks. Economic Modelling, 49(Suppl. C), 270–277. https://doi.org/10.1016/j.econmod.2015.04.015

- Johansen, S. (1995). Identifying restrictions of linear equations with applications to simultaneous equations and cointegration. Journal of Econometrics, 69(1), 111–132. https://doi.org/10.1016/0304-4076(94)01664-L

- Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics, 54(1–3), 159–178. https://doi.org/10.1016/0304-4076(92)90104-Y

- Lee, J., & Strazicich, M. C. (2003). Minimum lagrange multiplier unit root test with two structural breaks. Review of Economics and Statistics, 85(4), 1082–1089. https://doi.org/10.1162/003465303772815961

- Lee, J., & Strazicich, M. C. (2013). Minimum LM unit root test with one structural break. Economics Bulletin, 33(4), 2483–2492. http://www.accessecon.com/pubs/eb/2013/volume33/eb-13-v33-i4-p234.pdf

- Lim, G. C. (2001). Bank interest rate adjustments: Are they asymmetric? Economic Record, 77(237), 135–147. https://doi.org/10.1111/1475-4932.00009

- Marotta, G. (2009). Structural breaks in the lending interest rate pass-through and the euro. Economic Modelling, 26(1), 191–205. https://doi.org/10.1016/j.econmod.2008.06.011

- Mishra, P., Montiel, P., Pedroni, P., & Spilimbergo, A. (2014). Monetary policy and bank lending rates in low-income countries: Heterogeneous panel estimates. Journal of Development Economics, 111, 117–131. https://doi.org/10.1016/j.jdeveco.2014.08.005

- Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. https://doi.org/10.1080/00036840500278103

- Narayan, P. K., & Popp, S. (2010). A new unit root test with two structural breaks in level and slope at unknown time. Journal of Applied Statistics, 37(9), 1425–1438. https://doi.org/10.1080/02664760903039883

- Narayan, P. K., & Popp, S. (2013). Size and power properties of structural break unit root tests. Applied Economics, 45(6), 721–728. https://doi.org/10.1080/00036846.2011.610752

- Neumark, D., & Sharpe, S. A. (1992). Market structure and the nature of price rigidity: Evidence from the market for consumer deposits. The Quarterly Journal of Economics, 107(2), 657–680. https://doi.org/10.2307/2118485

- Payne, J. E. (2006). The response of the conventional mortgage rate to the federal funds rate: Symmetric or asymmetric adjustment? Applied Financial Economics Letters, 2(5), 279–284. https://doi.org/10.1080/17446540600647037

- Payne, J. E. (2007a). More on the monetary transmission mechanism: Mortgage rates and the federal funds rate. Journal of Post Keynesian Economics, 29(2), 247–257. https://doi.org/10.2753/PKE0160-3477290204

- Payne, J. E. (2007b). Interest rate pass through and asymmetries in adjustable rate mortgages. Applied Financial Economics, 17(17), 1369–1376. https://doi.org/10.1080/09603100601018872

- Pesaran, M. H., & Shin, Y. (1999). An autoregressive distributed-lag modelling approach to cointegration analysis. Econometric Society Monographs, 31, 371–413. https://doi.org/10.1017/CCOL521633230.011

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Sander, H., & Kleimeier, S. (2004). Convergence in euro-zone retail banking? What interest rate pass-through tells us about monetary policy transmission, competition and integration. Journal of International Money and Finance, 23(3), 461–492. https://doi.org/10.1016/j.jimonfin.2004.02.001

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In R. C. Sickles & W. C. Horrace (Eds.), Festschrift in honor of peter schmidt (pp. 34). Springer.

- Taylor, J. B. (1993). Discretion practice versus policy rules in practice. Carnegie-Rochester conference series on public policy, Vol. 9, (pp. 195–214).

- Valadkhani, A., & Anwar, S. (2012). Interest rate pass-through and the asymmetric relationship between the cash rate and the mortgage rate. Economic Record, 88(282), 341–350. https://doi.org/10.1111/j.1475-4932.2012.00823.x

- Valadkhani, A., & Bollen, B. (2013). An alternative approach to the modelling of interest rate pass through and asymmetric adjustment. Economics Letters, 120(3), 491–494. https://doi.org/10.1016/j.econlet.2013.06.006

- Valadkhani, A., & Worthington, A. (2014). Asymmetric behavior of Australia’s big-4 banks in the mortgage market. Economic Modelling, 43, 57–66. https://doi.org/10.1016/j.econmod.2014.07.044

- Wang, K.-M., & Lee, Y.-M. (2009). Market volatility and retail interest rate pass-through. Economic Modelling, 26(6), 1270–1282. https://doi.org/10.1016/j.econmod.2009.06.002

- Wulandari, R. (2012). Do credit channel and interest rate channel play important role in monetary transmission mechanism in Indonesia?: A structural vector autoregression model. Procedia-Social and Behavioral Sciences, 65, 557–563. https://doi.org/10.1016/j.sbspro.2012.11.165

- Zhang, Z., Tsai, S.-L., & Chang, T. (2017). New evidence of interest rate pass-through in Taiwan: A nonlinear autoregressive distributed lag model. Global Economic Review, 46(2), 129–142. https://doi.org/10.1080/1226508X.2017.1278710

- Zulverdi, D., Gunadi, I., & Pramono, B. (2007). Bank portfolio model and monetary policy in Indonesia. Journal of Asian Economics, 18(1), 158–174. https://doi.org/10.1016/j.asieco.2006.12.006