?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examined the capabilities of six cryptocurrencies as a hedge and safe haven against the stock indices and foreign exchange rate in the East Asia-5 markets. According, MGARCH-DCC was adopted and implemented in data collection processes together with Rathner and Chiu regression method, which spanned from April 2013 to December 2019. The results revealed that these cryptocurrencies had dissimilar hedging and safe haven capabilities across various stock indices and exchange rates in the East Asia-5 markets. In particular, Bitcoin, Litecoin, and Ethereum offered strong hedge properties on most of the East Asia-5 equity indices. Moreover, Bitcoin and Litecoin only provided a safe haven for Japanese Yen currency, while Taiwanese equity indices and Chinese Yuan currency can be safely protected via an investment into Stellar.

1. Introduction

Following the introduction of Bitcoin by Nakamoto in 2008, which employed cryptographic technology, cryptocurrencies are considered as one of the alternative investment instruments that can be invested to generate an efficient investment portfolio. Furthermore, the instrument has applied blockchain technology to improve its capability, enhance security, and independence from any authority control (Lee et al., Citation2018). According to Cheah and Fry (Citation2015), the cryptocurrency market is currently operating in a highly volatile climate and in a “bubble”, rendering it suitable as an investment tool due to its potential profits for investors who are willing to take extraordinary risks. Therefore, cryptocurrencies could be an effective hedging or diversification instruments or provide a safe haven capacity for other financial assets. For instance, cryptocurrency could be an effective hedging or diversification instrument for other financial assets in the normal period of cryptocurrency that negatively or positively correlated with other financial assets. Besides, if the cryptocurrency is negatively correlated with other financial assets during the market distress, then the cryptocurrency could be a safe haven for financial assets (Baur & Lucey, Citation2010).

Some studies have further indicated that Bitcoin offered different characteristics as compared to traditional financial assets in a normal period (Corbet et al., Citation2018; Karim et al., Citation2021; Lee et al., Citation2018). Such dissimilarities are crucial for investors who seek to diversify their investment portfolio risks and maximise the portfolio returns. For instance, Karim et al. (Citation2021) revealed that cryptocurrencies provided limited diversification properties on the ASEAN-5 stock markets in the long run, but presented opportunities for diversification in the short run. In addition, some recent studies further examined the diversification effect of cryptocurrencies during the COVID-19 pandemic period (Allen, Citation2022; Goodell & Goutte, Citation2021; Vukovic et al., Citation2021). Moreover, a few studies started to study the comparison of the return and volatility transmission of (cryptocurrencies versus gold) and (Bitcoin versus crude oil) between the pre-COVID-19 and COVID-19 periods (Yousaf & Ali, Citation2020; Yousaf et al., Citation2022a).

Existing studies on cryptocurrency are not limited to their diversification benefits or hedging and safe haven capabilities against other financial assets. For instance, certain scholars have initially emphasised upon their inherent characteristics, such as weak-form efficiency of Bitcoin (Tiwari et al., Citation2018; Urquhart, Citation2016). Nevertheless, research interest in cryptocurrency has shifted to other characteristics, such as market efficiency with liquidity (Wei, Citation2018), linkages between Bitcoin returns and transactional activities (Koutmos, Citation2018), and the efficacy of technical trading strategies in today’s cryptocurrency markets (Corbet et al., Citation2019). Similarly, the correlation, which links cryptocurrencies with other financial assets has received more attention in recent times. Such information is described accordingly, such as volatility or return spill over (Corbet et al., Citation2018; Trabelsi, Citation2018), hedge diversification and hedge haven of Bitcoin (Bouri et al., Citation2017; Chan et al., Citation2019; Kliber et al., Citation2019; Shahzad et al., Citation2019; Stensas et al., Citation2019), and the contagion impact (Handika et al., Citation2019). Therefore, to avoid any influence of the “Black Swan” effect of the COVID-19 pandemic, the current study is targeted towards specifically examining the hedge and safe haven properties of six selected cryptocurrencies until the end of 2019 in the East Asia-5 markets according to their stock indices and exchange rates. This will be achieved by using a multivariate MGARCH-DCC model together with Ratner and Chiu (Citation2013) method, whereby the East Asia-5 markets were selected due to their advanced economies and development. According to the Financial Times Stock Exchange (FTSE) classification of equity markets, the financial markets of Hong Kong, Japan, and South Korea are characterised as developed markets, whereas Taiwan’s market is categorised as an advanced and emerging market. Additionally, despite its characterisation as a secondary emerging market, China remains crucial since it is the world’s second-largest economy.

This study contributes to theoretical and practical perspectives. Firstly, more comprehensive findings are provided in this study as the hedging evidence or diversification benefits and safe haven capabilities of the cryptocurrencies derived from the six selected cryptocurrencies. Although, more of the previous studies only focused on the largest cryptocurrency, Bitcoin. Secondly, limited studies had extensively and exclusively examined the East Asia-5 stock and exchange rate markets. Therefore, this study would provide more robust findings as the evidence results from the East Asia-5 markets, which were less examined in previous studies.

This study consists of five sections starting with the introduction section. The study continues with Section 2 which provides a literature review. Next, the methodology section discusses the sample and data together with the analysis technique used. Section 4 provides the analysis results and discussion. The study ends with a conclusion section covering the conclusion, implications and suggestions for future studies.

2. Literature Review

2.1. Diversification, Hedging and Safe-Haven

Empirically, many studies had explored the hedging properties of cryptocurrencies against several traditional financial assets. As mentioned by Bouri et al. (Citation2017), the safe haven capacity of the cryptocurrencies was ignored in these studies and unable to distinguish the different properties of diversification, hedging and safe-haven. Therefore, the differences between these three concepts should be clearly defined. As per Baur and Lucey (Citation2010), diversification benefits may be provided by a financial asset to another asset only on the occasion of a positive but not perfect correlation. Similarly, Bouri et al. (Citation2017) further remarked that an asset such as cryptocurrency could be a diversifier when it had a weak positive correlation with another asset. Moreover, the diversification properties of cryptocurrency only offer during the normal period and not during market turmoil (Kliber et al., Citation2019). In contrast, a negative correlation between two financial assets may yield superior hedging capacity between them. Therefore, in this study cryptocurrencies would assumed to be an effective diversification tool if they were positively correlated with the traditional financial assets like stock indices and foreign exchange rates in the East Asia-5 markets in the normal period. While the uncorrelated or negative correlation between cryptocurrencies and other assets indicated it would be a strong hedging instrument for other assets (Kliber et al., Citation2019). Unlike the diversification and hedging properties that were measured on average, the safe haven property occurred during times of stress or extreme market conditions (Kliber et al., Citation2019). Therefore, when there was a negative significance between an asset and another during a period of market turmoil, then it showed the safe haven capacity of the asset to the other (Baur & Lucey, Citation2010).

2.2. Empirical Studies Related to Property of Cryptocurrencies

Initially, Dyhrberg (Citation2016a) work was the first to propose that Bitcoin lacks of hedging capabilities on the EUR and GBP as such properties were only observed in the short run. Meanwhile, the subsequent follow-up study (Dyhrberg, Citation2016b) compared the cryptocurrency with currency and gold, thereby disclosing some of its hedging capabilities that were similar to gold. However, it behaved similar to a currency due to its responsiveness to the US federal rate. Due to its unique characteristics, Bitcoin can thus be classified as an asset suited for managing investment portfolios, risks, and market sentiments.

In contrast, Bitcoin poor hedge capabilities were highlighted again in the work of Bouri et al. (Citation2017) against many financial assets, whereas a strong safe haven was reported in the weekly frequency data against the Asian stock markets during a period of market turmoil. In particular, Klein et al. (Citation2018) had indicated the lack of hedging capabilities for Bitcoin against the stock market indices during market distress, as well as its dissimilarities against gold that yielded hedging properties for the indices. Following this, Smales (Citation2019) suggested that Bitcoin showed a weak hedge and no safe haven capabilities as compared to other assets. This suggestion was based on their underlined findings that it was not significantly correlated with these financial assets. Besides, its varying hedging capabilities had been reported by Chan et al. (Citation2019), with strong hedge properties were observed in the monthly data and its high-frequency data had a tendency for weak hedge capabilities over the stock indices.

The benefits of diversification offered by the two largest cryptocurrencies (i.e., Bitcoin and Ethereum), alongside gold against other financial assets, were investigated by Feng et al. (Citation2018), who reported a portfolio that was potentially well-diversified due to cryptocurrency addition. Besides such effect, the hedging and safe haven properties of Bitcoin and gold against oil price changes were highlighted by Selmi et al. (Citation2018). The use of Bitcoin in local currencies had prompted Kliber et al. (Citation2019) to indicate that its safe haven occurs in Venezuela only, whereas diversifiers and weak hedge can be found in Japan, China, Sweden and Estonia, respectively. Furthermore, when Bitcoin is measured in USD, its capability becomes a weak hedge in all five indices.

According to Shahzad et al. (Citation2019), its safe haven properties, similar to gold and commodity index, differed across time and stock market indices. Such conclusion is due to Bitcoin, gold, and commodities were found to offer a weak safe haven for world stock indices but not for the developed, emerging, US, and Chinese stock markets. In contrast, Bitcoin, along with India, Zimbabwe, World, BRIC, Pacific, and Europe stock indices, Bitcoin provides a strong safe haven for the US stock index as noted by Stensas et al. (Citation2019). Conversely, the strong hedge properties of Bitcoin were only observed in the Russian, Indian, and South Korean markets, whereas the Brazilian market yielded a weak hedge.

Urquhart and Zhang (Citation2019) used the hourly data to conclusively noted Bitcoin intraday hedge capabilities for CHF, EUR, and GBP currencies, as well as a diversification effect for AUD, CAD, and JPY. Meanwhile, the safe haven properties were shown for CAD, CHF, and GBP currencies. Wu et al. (Citation2019) examined the characteristics of gold and Bitcoin against the economic policy uncertainty index (EPU) and found that their hedging and safe haven capabilities relied on market conditions (i.e., bearish or bullish). In contrast, the diversification effects were generated when the market was normal. Bitcoin has indicated strong hedging capabilities in lower EPU and a weak hedging in higher EPU, whereas its weak safe haven was noted in extreme bullish and bearish markets (i.e., higher and lower EPU). Moreover, Wang et al. (Citation2019) reported that cryptocurrencies were unable to yield hedging abilities for most international indices, whereas safe haven capability presents in larger capitalisation and higher liquidity market indices alongside developed market indices concurrently. Conversely, Bitcoin often becomes the diversifier for small market capitalisation and lower liquidity markets. Besides, Sebastiao and Godinho (Citation2020) noted that CBOE Bitcoin futures may potentially hedge against Bitcoin and other major cryptocurrencies. Additionally, Pal and Mitra’s (Citation2019) opposing study had found its hedging capacity by using gold, S&P500, and wheat, wherein the gold had more hedging capabilities.

Accordingly, Corbet et al. (Citation2018) and Aslanidis et al. (Citation2019) had constantly indicated cryptocurrencies and their positive correlation amongst themselves; however, they were not correlated with other main financial markets. Meanwhile, Ji et al. (Citation2018) had provided evidence of Bitcoin isolation as compared to other financial markets, but such relationships were time-dependent. However, Bouri et al. (Citation2018) showed that clashing results in which Bitcoin returns were not isolated from other assets as the evidence shown of a significant return spill over between them. Similar to Ji et al. (Citation2018), Bouri et al. (Citation2018) have noted that the spill over effect changed across time and market conditions. Besides, the weak integration between cryptocurrencies and other financial assets was further reported in Trabelsi (Citation2018) work, showing insignificant spill over effects. Accordingly, Kurka (Citation2019) suggested that Bitcoin hedging properties for other financial assets despite their unconditional and negligible connectivity. The emphasis on 13 Asian financial markets has allowed Handika et al. (Citation2019) to find no significant contagion effects between cryptocurrencies across these markets. However, an increasing contagion effect was noted by Matkovskyy and Jalan (Citation2019) in the context of Bitcoin and other five indices (i.e., NASDAQ100, S&P500, Euronext100, FTSE100, and Nikkei225). This may be caused by its futures introduction, which improved the efficiency of the Bitcoin market.

Moreover, recent studies have started to examine new cryptocurrencies. For example, Yousaf et al. (Citation2022b) studied the connectedness of travel and tourism tokens with other assets and found that the travel and tourism tokens do offer diversification capacities to other assets. Similarly, Yousaf et al. (Citation2022c) further examined the connectedness of energy cryptocurrencies with other financial assets and showed that energy cryptocurrencies provided diversification properties but the connectedness was changed during the shocks, such as COVID-19 and the Russia-Ukraine war. Yousaf et al. (Citation2022d) found that renewable energy digital tokens possessed a weak connection with fossil fuel markets. It would be improved if renewable energy tokens were added to the portfolio. Yousaf et al. (Citation2023) also examined the connectedness of meme tokens, meme stocks with other financial assets classes and revealed that meme stocks and meme tokens showed a time-varying connectedness with other financial assets.

3. Data and Methodology

A total of six cryptocurrencies were included in this paper, such as Bitcoin, Ripple (XRP), Litecoin, Monero, Stellar (XLM), and Ethereum, together with the equities stock indices and foreign exchange rates of the East Asia-5 markets (i.e., China, Hong Kong, Japan, South Korea, and Taiwan). The sampling period of this study was restricted to the period spanning from April 2013 until December 2019 for Bitcoin and Litecoin, while other cryptocurrencies were assessed from their inception dates to December 2019, as provided by coinmarketcap.com. The coinmarketcap.com data was suitable to be used in this research as it consists of most of the trading activity and has a similar characteristic to the main exchange platforms (Vidal-Tomas, Citation2022). During a similar study period, the daily frequency data of traditional financial assets for the equity indices and foreign exchange rates of East Asia-5 markets were downloaded from Thomson Reuters’ Datastream. As the trading period of equity indices and foreign exchange rates for the East Asia-5 markets is confined to weekdays only (i.e., five days per week), this results in data inconsistencies for the cryptocurrencies that trade at all times. As per the works of Klein et al. (Citation2018) and Smales (Citation2019), the weekend daily data of cryptocurrencies were omitted to construct consistent cryptocurrencies data set with relevant equity indices and foreign exchange rates. After confirming the readiness of the data series of all six cryptocurrencies, as well as the market indices and foreign exchange rates for the East Asia-5 markets, the data series daily returns calculation was conducted by using the capital gain yield as shown below:

Where, Rt is daily returns of cryptocurrencies, stock indices, and exchange rate series at time t; and Ptand Pt-1are closing prices/rates of the cryptocurrencies, stock indices, and exchange rates at time t and t-1, respectively.

Firstly, current study adopted the model of dynamic conditional correlation (DCC) via multivariate GARCH estimation to examine the time-varying pairwise conditional correlations linking the return series of cryptocurrencies with the equity market indices and exchange rates of East Asia-5 markets. Unlike commonly observed unconditional correlations, the DCC of MGARCH could yield a highly robust correlation regarding the changes in conditional correlation linking the pairwise return series and conditional volatility throughout the study period. Besides, the model may identify the positive or negative directions and the degree of correlation linking both return series (Saiti & Noordin, Citation2018), as well as the complementation or substitution correlation between the pairwise series (Abdullah et al., Citation2016). In MGARCH-DCC estimation, the standard residuals of the return series (i.e., cryptocurrencies, market indices, and foreign exchange rates) were estimated by using the univariate GARCH model. Therefore, the following standard residuals were utilised to calculate the time-varying conditional correlation by using the following equation:

Where, Ht is multivariate conditional covariance, Dtis conditional time-varying standardised residuals () (in a diagonal matrix), and Rt is time-varying correlation matrix (off-diagonal matrix).

Furthermore, the MGARCH-DCC model can be characterised as follows:

Where, Qt is time-varying conditional correlation of standardised residuals, is unconditional correlation of

, and a and β are non-negative parameters of

.

Lastly, the DCC linking the selected cryptocurrencies (ith) and East Asia-5 market indices or exchange rates (jth) was estimated via the equation shown below:

Where, qij is elements of the ith and jth column on the matrix Qt.

Next, the capabilities of hedging or diversification and safe haven of cryptocurrencies against the market indices or exchange rates of East Asia-5 markets were subjected to an evaluation by using EquationEquation 5(5)

(5) . EquationEquation 5

(5)

(5) is identical to the method adopted by (Bouri et al., Citation2017; Ratner & Chiu, Citation2013; Stensas et al., Citation2019). In this model, the conditional correlation of MGARCH-DCC for a pairwise series was regressed alongside three dummy variables (Q) to yield the lowest return movement in the 10th (q10), 5th (q5), and 1st (q1) percentile for specific market indices or exchange rates (jth).

Where, DCC is conditional correlation of cryptocurrency and market indices or exchange rates, is return series of the market indices or exchange rates (jth), and

is error term.

The cryptocurrency (ith) is an effectual diversification tool against market indices or exchange rates (jth) when β0 is positive and significant. However, the negative significance of β0 indicates that cryptocurrency (ith) is a strong hedging instrument for other assets. Moreover, the negative significance of β1, β2and β3 further indicates that cryptocurrency (ith) offers a strong safe haven for market indices or exchange rates (jth), whereas a weak safe haven is yielded by cryptocurrency (ith) if they are insignificant from zero.

4. Results and Discussion

Table presents the descriptive statistics obtained for all return series utilised in the current study, which included six cryptocurrencies in Panel A, the equity market indices of East Asia-5 markets in Panel B, and foreign exchange rates in Panel C. Amongst the three types of financial asset return series, the selected cryptocurrencies showed the highest average daily returns, whereby Ripple and Ethereum were found to be the two most profitable cryptocurrencies. They obtained an average daily return of 0.53% and 0.50% (equivalent to 128% and 121% annually), respectively. It was noted that Bitcoin only recorded at 0.26% of average daily returns, which was the second-lowest amongst the six cryptocurrencies, while Litecoin and Monero reported values of 0.27% and 0.23%.

Table 1. Descriptive statistics for all return series

In contrast to cryptocurrencies, the East Asia-5 market indices revealed a lower average daily returns ranged from 0.01% to 0.04%. In context of the East Asia-5 markets, CSI300 and Nikkei225 reported the highest average daily returns of 0.0399% and 0.0385% (9.58% and 9.24% annually), followed by Taiwan and Hong Kong’s stock indices (0.0261% and 0.0182%), respectively. During the same period, the South Korean index (KOSPI) merely generated 0.0098% of the average daily returns. In the case of the foreign exchange rates of East Asia-5 markets, the lowest average daily returns were generated for all three types of return series. The highest value was obtained by JPY at a mere 0.0077%, followed by the CNY (0.0072%). While the moderate average daily returns were reported for South Korean Won (KRW, 0.0034%), the TWD and Hong Kong dollar (HKD) were the least profitable currencies, at merely 0.0009% and 0.0002%, respectively.

In terms of the total risks as a proxy for standard deviation, all cryptocurrencies were posited to yield similar risk characteristics; with the exception of Bitcoin, which had the lowest standard deviation of 4.57%, other cryptocurrencies obtained values ranged from 6.89% to 8.30%. In line with the “risk-return trade-off” theory, the standard deviation of the five market indices was also lower as compared to the cryptocurrencies; in particular, the CSI300, Hang Seng, and Nikkei225 were noted as the riskiest indices, while TAIEX and KOSPI were reported as the least risky indices.

The most riskless return series identified in this work was the foreign exchange rates of five currencies, whereby HKD (0.0362%) had the lowest standard deviation and JPY being the riskiest currency (0.5558%). Moreover, as per Trabelsi (Citation2018), all of the cryptocurrencies skewed to the right in which the positive skewness values were generated alongside two currencies of the East Asia-5 markets, namely the CNY and KRW. Meanwhile, negative skewness was observed for all market indices, as well as the HKD, JPY, and TWD currencies. In addition, the fat-tailed of the return series or leptokurtic was detected in all of the return series, regardless of the cryptocurrencies, stock market indices, or foreign exchange rates as all Kurtosis values were greater than 3.

The MGARCH-DCC was used to calculate the unconditional volatilities of each return series and unconditional correlation, linking the pairwise return series of cryptocurrencies and market indices or exchange rates. The results are presented in Table . As displayed in Table , Panel A yielded the unconditional correlation between cryptocurrencies and market indices, whereas Panel B exhibits an unconditional correlation of cryptocurrencies with the exchange rates of East Asia-5 markets. Additionally, the unconditional volatilities of the East Asia-5 markets indices and exchange rates are shown in the last column, while the unconditional volatilities of cryptocurrencies are depicted in the last row.

Table 2. Summary of unconditional volatilities and correlations for all return series

In short, the unconditional correlation of cryptocurrencies was dissimilar in linking the market indices and exchange rates of the East Asia-5 markets. For instance, Bitcoin was positively correlated with CSI300; however, this correlation was merely reported with CNY, KRW, and TWD currencies. Similarly, Ripple and Stellar showed positive correlations with all five market indices (except Nikkei225) and a negative correlation with all of the exchange rates of East Asia-5 (except HKD with Stellar). Next, Litecoin showed a negative correlation with all five East Asia-5 market indices, except for HKD and JPY. Similarly, the negative correlation between cryptocurrency and East Asia-5 markets currency rates was found for Monero (except for TWD) and Ethereum (except for CNY and KRW). Meanwhile, Monero and Ethereum revealed a positive correlation with CSI300 and Hang Seng.

Accordingly, Stellar was noted with the highest unconditional volatilities (8.2865) amongst all cryptocurrencies, with Bitcoin being the least volatile cryptocurrency (4.1154). This supported the prior findings of standard deviation presented in Table . In contrast, CSI300 was the market index of the highest volatility. Amongst all of the exchange rates, KOSPI generated the lowest unconditional volatility, whereas JPY generated the highest unconditional volatility. These findings were consistent with the standard deviation values shown in Table .

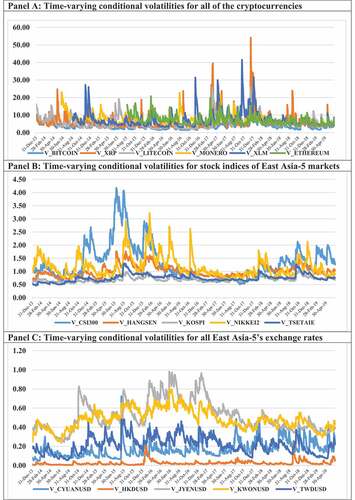

The time-varying conditional volatilities of all return series for this study are displayed in Appendix A. They consist of Panel A showed all six selected cryptocurrencies, Panel B showed the East Asia-5 market indices, and Panel C showed the exchange rates of the East Asia-5 markets. In Panel A, all of the cryptocurrencies showed a tendency for lower conditional volatilities during the initial period, whereby they rose higher from March 2017 until February 2018 observed, with a few exceptional high peaks. However, the conditional volatilities for all of the cryptocurrencies decreased following this until end of the period. Similar to the unconditional volatilities in Table , Stellar emerged as the most volatile cryptocurrency, while Bitcoin was reported having the lowest volatility as exhibited in Panel A. Besides the conditional volatilities of the cryptocurrencies, Nikkei225 and CSI300 were the two most volatile cryptocurrencies and showed the highest time-varying conditional volatilities as shown in Panel B. Initially, Nikkei225 generated the highest volatility, which was cutover by CSI300 since December 2014. However, the former had bounded back and showed the highest volatility in April 2016 until April 2018, before being passed by Hang Seng and CSI300. Then, the CSI300 remained with the highest volatility until June 2019 due to cutover by Hang Seng. In Panel B, KOSPI remained as the least volatile market index throughout the study period, whereas Panel C showed that JPY and KRW generated the highest conditional volatilities during this period. Meanwhile, HKD yielded the lowest conditional volatility and moderate volatilities were obtained for CNY and TWD.

Next, the study examined whether these six selected cryptocurrencies successfully proven their properties of hedging or diversifier and safe haven for the market indices and exchange rates of East Asia-5 markets. A summary of the results is presented in Table , which is divided into six panels to distinguish the distant properties of each cryptocurrency. In Panel A, Bitcoin was highlighted as a hedging tool for all East Asia-5 market indices (except for CSI300) with a positive significance, thereby implying that it offered diversification benefits for the Chinese stock markets. Instead of being a strong hedge, Bitcoin has a tendency for being an effectual diversifier for all East Asia-5 markets exchange rates, except HKD and TWD. Moreover, its strong safe haven capability was only presented for JPY and KOSPI in the 1st percentile.

Table 3. Summary on the hedge and safe haven of cryptocurrencies on East Asia-5 markets

In Panel B, Ripple was observed to yield similar results; in contrast, it served as a strong diversifier for CSI300 and TAIEX only, while being a strong hedging tool for the remaining three indices. Its strong hedge capacity was also for all of the East Asia-5 markets exchange rates with a negative significance, except for JPY. Although Ripple showed dissimilar hedge and diversifier capabilities linking the East Asia-5 market indices and exchange rates, it could not offer a safe place for all of the East Asia-5 market indices and exchange rates.

Next, Litecoin was observed to be a strong hedging asset for all of the East Asia-5 equity markets due to its negatively significant correlations, except for the insignificant outcome for CSI300. However, such capacity was merely observed for HKD, although it remained an effectual diversifier for the other exchange rates. Similar to Bitcoin, Litecoin merely yielded a safe haven for JPY in the 1st percentile.

Furthermore, the strong hedging capacity of Monero was merely observed for Nikkei225, KOSPI, and TAIEX, whereas its diversification benefit was reported for CSI300 and Hang Seng indices. However, dissimilar results were concluded for the exchange rates of East Asia-5 markets; here, Monero possessed strong hedge properties against CNY and HKD (i.e., effectual diversifier in their equity indices) and JPY (i.e., strong hedge in their equity index). Additionally, it was an effective diversifier for the KRW, yielding a strong hedge in the equity index. In the context of Monero capacity as a safe haven, it merely yielded a safe haven for CSI300 in the 1st percentile and TWD in the 5th percentile.

Similarly, Stellar was observed to merely exhibit as a strong hedging asset for Hang Seng and Nikkei225, while leaning towards being an effective diversifier for the other three market indices. Nonetheless, its hedge property disappeared in JPY (alongside being an effective diversifier for CNY), while remaining a strong hedge for HKD, KRW, and TWD. Additionally, Stellar merely yielded a safe haven for TAIEX and Chinese Yuan in the 10th percentile of the lowest movements.

Finally, Ethereum showed a tendency for being a strong hedging asset for the East Asia-5 equity markets, while serving as an effective diversifier for the CSI300. However, it provided diversification benefits for all of the exchange rates in the East Asia-5 markets, except for its strong hedging capacity against HKD and JPY. Accordingly, the safe haven of Ethereum was merely observed on the Hang Seng and KOSPI indices at 1st percentile.

A comparison of the current outcomes to those of previous studies indicated that the diversification effect offered by several cryptocurrencies against the Chinese Yuan and CSI300 was consistent with studies by (Bouri et al., Citation2017; Feng et al., Citation2018; Kliber et al., Citation2019; Stensas et al., Citation2019). However, it contradicted the work by Chan et al. (Citation2019), which reported a strong hedge capacity for Shanghai A-Shares in its monthly data. The possible reasons for this inconsistent finding were due to the data frequency as monthly data that were used in Chan et al. (Citation2019), while this study used the daily data. Moreover, a weak hedging in the weekly and daily data alongside weak hedge abilities were depicted for Bitcoin in the US dollar (Kliber et al., Citation2019).

Besides, the weak safe haven property of cryptocurrencies echoed the outcomes of Bouri et al. (Citation2017), Stensas et al. (Citation2019), and Shahzad et al. (Citation2019). Similarly, the strong hedging capabilities of the cryptocurrencies on Nikkei225 were identified, whereby the findings were obtained via monthly and daily data, respectively (Bouri et al., Citation2017; Chan et al., Citation2019). However, this was inconsistent with the outcomes of Feng et al. (Citation2018), Stensas et al. (Citation2019), and Kliber et al. (Citation2019), which had observed the diversification benefit of cryptocurrencies on the Japanese market. The different study periods could be the reason for this contradicting results. The movement of the Nikkei225 fell by approximately 17% in 2018, and this could be the main reason for the inconsistent findings as the study period was until the end of 2019. Additionally, the current study observed the strong hedge capacity of cryptocurrencies on Japanese Yen that was limited to Monero and Ethereum, while being an effective diversifier for the other four cryptocurrencies.

Regarding the safe haven property, it was merely observed in Bitcoin and Litecoin on Japanese currency, whereas other cryptocurrencies had a tendency to show their weak safe haven properties on Nikkei225. This is consistent with similar findings by (Bouri et al., Citation2017; Urquhart & Zhang, Citation2019). This finding indicated that cryptocurrencies could be used as the safe haven for Japanese currency and stock indices during the financial crisis. Besides, the strong hedge capability of cryptocurrencies against KOSPI was consistent with Stensas et al. (Citation2019); while the scholar had observed Bitcoin to yield a weak safe haven capacity on KOSPI. The results also showed that Bitcoin and Ethereum revealed a strong safe haven capacity for the market in the 1st percentile.

In brief, six selected cryptocurrencies in this study yielded dissimilar hedge or diversification benefit properties against East Asia-5 market indices and their respective exchange rates. In particular, Bitcoin, Litecoin, and Ethereum showed a tendency for a strong hedge capacity in the East Asia-5 market indices but not for their exchange rates, whereas opposing results were observed for Ripple and Stellar. Then, the safe haven of cryptocurrencies depicted a similar scenario: Bitcoin and Litecoin merely yielded a safe haven capacity for the Japanese Yen, but not for their respective market indices. Besides, Ripple was unable to offer any strong safe haven ability for all market indices and exchange rates of the East Asia-5 markets. Meanwhile, Stellar merely depicted their safe haven abilities for the Chinese Yuan, whereas a strong safe haven for Hang Seng was yielded by Ethereum. Additionally, Monero merely generated a strong safe haven for the CSI300 and Taiwan exchange rates.

5. Conclusion and Implications

The current study examined the hedging or diversification benefits and safe haven properties of six The current study examined the hedging or diversification benefits and safe haven properties of six selected cryptocurrencies against the market indices and exchange rates of East Asia-5 markets. It successfully yielded a highly robust evidence due to exclusive assessment of six cryptocurrencies against East Asia-5 markets by using their equity market indices and exchange rates, which was achieved via the MGARCH-DCC model.

First, it can be concluded that cryptocurrencies have slightly dissimilar characteristics compared to equity market indices and exchange rates, especially in the context of the average daily returns, risks, and the skewness and Kurtosis values. The unconditional correlation linking the cryptocurrencies with market indices was marginally dissimilar to the unconditional correlation of cryptocurrencies and exchange rates. Herewith, Ripple, Monero, and Stellar had a tendency for a negative correlation with the East Asia-5 market exchange rates; however, they were positively correlated with the East Asia-5 equity market (except for Monero).

Besides, the hedge and safe haven properties of cryptocurrencies against market indices and exchange rates were in the same direction. In particular, Bitcoin, Litecoin, and Ethereum have a tendency to yield a strong hedging capacity for most East Asia-5 market indices but not for their exchange rates, whereas Ripple and Stellar possessed a strong hedging ability in most of the exchange rates. In terms of the safe haven capacity, Bitcoin and Litecoin could not yield outcome for the East Asia-5 equity market indices (except KOSPI by Bitcoin) but they could offer this for Japanese Yen. Additionally, Stellar could only offer a safe haven for the Taiwanese market index.

This study provided some important implications. By focusing on the theoretical perspective, the findings provided new evidence in literature regarding the hedge and safe haven capabilities of cryptocurrencies towards traditional financial assets. Moreover, it also offered a more comprehensive understanding towards the hedge and safe haven properties of cryptocurrencies by concentrating on the East Asia-5 markets.

From the practical perspective, cryptocurrencies can be considered as a new investment asset besides the traditional options of financial assets. Therefore, current study may benefit from the presence of several stakeholders in the financial market, especially the investors and professional fund managers. Meanwhile, the findings of its hedging and safe haven capabilities against the market indices and exchange rates can be shaped into a clear guidance towards formulating an efficient investment portfolio capable of maximising their portfolio returns or minimising the investment risks. Similarly, market regulators and relevant authorities may implement the current study findings for enhancing their cryptocurrency rules as they are heavily utilised as digital currency and investment tools in the financial markets. Besides, scholars interested in the dissimilar hedging and safe haven properties of cryptocurrencies may extend the relevant literature on the topic, as well as on portfolio management. This is due to different cryptocurrencies having varying capabilities on the market indices and exchange rates of the East Asia-5 markets.

There are several limitations to this study. Firstly, as this study focused on the period before COVID-19 pandemic, future studies could consider making a comparison between the period before COVID-19, during COVID-19, and after COVID-19, to produce more comprehensive findings. Besides that, by including more markets could be considered in the future study as this could further discover the hedge and safe haven properties of the cryptocurrencies on traditional financial assets such as stock indices and foreign exchange rates. This is because this study only focused on the five markets in East Asia. In addition, different regions may possess different characteristics and features, it will be an interesting study if the future study could make a comparison between markets in different regions.

Acknowledgements

The authors wish to acknowledge that this study is funded by the UTS University Research Grant (UTS/RESEARCH/4/2022/09).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abdullah, A. M., Saiti, B., & Masih, M. (2016). The impact of crude oil price on Islamic stock indices of South East Asian countries: Evidence from MGARCH-DCC and wavelet approaches. Borsa Istanbul Review, 16(4), 219–16. https://doi.org/10.1016/j.bir.2015.12.002

- Allen, D. E. (2022). Cryptocurrencies, Diversification and the COVID-19 Pandemic. Journal of Risk and Financial Management, 15(3), 103. https://doi.org/10.3390/jrfm15030103

- Aslanidis, N., Bariviera, A. F., & Martinez-Ibanez, O. (2019). An analysis of cryptocurrencies conditional cross correlations. Finance Research Letters, 31, 130–137. https://doi.org/10.1016/j.frl.2019.04.019

- Baur, D. G., & Lucey, B. M. (2010). Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. The Financial Review, 45(2), 217–229. https://doi.org/10.1111/j.1540-6288.2010.00244.x

- Bouri, E., Das, M., Gupta, R., & Rouband, D. (2018). Spillovers between Bitcoin and other assets during bear and bull markets. Applied Economics, 50(55), 5935–5949. https://doi.org/10.1080/00036846.2018.1488075

- Bouri, E., Molnar, P., Azzi, G. R., & Hagfors, L. I. (2017). On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters, 20, 192–198. https://doi.org/10.1016/j.frl.2016.09.025

- Chan, W. H., Le, M., & Wu, Y. W. (2019). Holding Bitcoin longer: The dynamic hedging abilities of Bitcoin. The Quarterly Review of Economics and Finance, 71, 107–113. https://doi.org/10.1016/j.qref.2018.07.004

- Cheah, E. T., & Fry, J. (2015). Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental values of Bitcoin. Economics Letters, 130, 32–36. https://doi.org/10.1016/j.econlet.2015.02.029

- Corbet, S., Eraslan, V., Lucey, B., & Sensoy, A. (2019). The effectiveness of technical trading rules in cryptocurrency markets. Finance Research Letters, 31, 32–37. https://doi.org/10.1016/j.frl.2019.04.027

- Corbet, S., Meegan, A., Larkin, C., & Lucey, B. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165, 28–34. https://doi.org/10.1016/j.econlet.2018.01.004

- Dyhrberg, A. H. (2016a). Hedging capabilities of Bitcoin. Is it the virtual gold? Finance Research Letters, 16, 139–144. https://doi.org/10.1016/j.frl.2015.10.025

- Dyhrberg, A. H. (2016b). Bitcoin, gold and the dollar – A GARCH volatility analysis. Finance Research Letters, 16, 85–92. https://doi.org/10.1016/j.frl.2015.10.008

- Feng, W., Wang, Y., & Zhang, Z. (2018). Can cryptocurrencies be a safe haven: A tail risk perspective analysis. Journal of Applied Economics, 50(44), 4745–4762. https://doi.org/10.1080/00036846.2018.1466993

- Goodell, J. W., & Goutte, S. (2021). Diversifying equity with cryptocurrencies during COVID-19. International Review of Financial Analysis, 76, 101781. https://doi.org/10.1016/j.irfa.2021.101781

- Handika, R., Soepriyanto, G., & Havidz, S. A. H. (2019). Are cryptocurrencies contagious to Asian financial markets? Research in International Business and Finance, 50, 416–429. https://doi.org/10.1016/j.ribaf.2019.06.007

- Ji, Q., Bouri, E., Gupta, R., & Roubaud, D. (2018). Network causality structures among Bitcoin and other financial assets: A directed acyclic graph approach. The Quarterly Review of Economics and Finance, 70, 203–213. https://doi.org/10.1016/j.qref.2018.05.016

- Karim, B. A., Abdul-Rahman, A., Hwang, J. Y. T., & Kadri, N. (2021). Portfolio Diversification Benefits of Cryptocurrencies and ASEAN-5 Stock Markets. Journal of Asian Finance, Economics and Business, 8(6), 567–577. https://doi.org/10.13106/jafeb.2021.vol8.no6.0567

- Klein, T., Thu, P. H., & Walther, T. (2018). Bitcoin is not the New Gold – A comparison of volatility, correlation and portfolio performance. International Review of Financial Analysis, 59, 105–116. https://doi.org/10.1016/j.irfa.2018.07.010

- Kliber, A., Marszalek, P., Musialkowska, I., & Swierczynska, K. (2019). Bitcoin: Safe haven, hedge or diversifier? Perception of bitcoin in the context of a country’s economic situation – A stochastic volatility approach. Physica A: Statistical Mechanics and Its Applications, 524, 246–257. https://doi.org/10.1016/j.physa.2019.04.145

- Koutmos, D. (2018). Bitcoin returns and transaction activity. Economics Letter, 167, 81–85. https://doi.org/10.1016/j.econlet.2018.03.021

- Kurka, J. (2019). Do cryptocurrencies and traditional asset classes influence each other? Finance Research Letters, 31, 38–46. https://doi.org/10.1016/j.frl.2019.04.018

- Lee, D. K. C., Guo, L., & Wang, Y. (2018). Cryptocurrency: A new investment opportunity? Journal of Alternative Investments, 20(3), 16–40. https://doi.org/10.3905/jai.2018.20.3.016

- Matkovskyy, R., & Jalan, A. (2019). From financial markets to Bitcoin markets: A fresh look at the contagion effect. Finance Research Letters, 31, 93–97. https://doi.org/10.1016/j.frl.2019.04.007

- Nakamoto, S. (2008). A Peer-to-Peer Electronic Cash System. Bitcoin. https://bitcoin.org/bitcoin.pdf

- Pal, D., & Mitra, S. K. (2019). Hedging Bitcoin with other financial assets. Finance Research Letters, 30, 30–36. https://doi.org/10.1016/j.frl.2019.03.034

- Ratner, M., & Chiu, J. C. C. (2013). Hedging stock sector risk with credit default swaps. International Review of Financial Analysis, 30, 18–25. https://doi.org/10.1016/j.irfa.2013.05.001

- Saiti, B., & Noordin, N. H. (2018). Does Islamic equity investment provide diversification benefits to conventional investors? Evidence from the multivariate GARCH analysis. International Journal of Emerging Markets, 13(1), 267–289. https://doi.org/10.1108/IJoEM-03-2017-0081

- Sebastiao, H., & Godinho, P. (2020). Bitcoin futures: An effective tool for hedging cryptocurrencies. Finance Research Letters, 33, 101230. https://doi.org/10.1016/j.frl.2019.07.003

- Selmi, R., Mensi, W., Hammoudeh, S., & Bouoiyour, J. (2018). Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Economics, 74, 787–801. https://doi.org/10.1016/j.eneco.2018.07.007

- Shahzad, S. Y., Bouri, E., Roubaud, D., Kristoufek, L., & Lucey, B. (2019). Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis, 63, 322–330. https://doi.org/10.1016/j.irfa.2019.01.002

- Smales, L. A. (2019). Bitcoin as a safe haven? Is it even worth considering? Finance Research Letters, 30, 385–393. https://doi.org/10.1016/j.frl.2018.11.002

- Stensas, A., Nygaard, M. F., Kyaw, K., & Treepongkaruna, S. (2019). Can Bitcoin be a diversifier, hedge or safe haven tool? Cogent Economics & Finance, 7(1). https://doi.org/10.1080/23322039.2019.1593072

- Tiwari, A. K., Jana, R. K., Das, D., & Roubaud, D. (2018). Informational efficiency of Bitcoin – An extension. Economics Letters, 163, 106–109. https://doi.org/10.1016/j.econlet.2017.12.006

- Trabelsi, N. (2018). Are they any volatility spill-over effects among Cryptocurrencies and widely traded asset classes? Journal of Risk and Financial Management, 11(4), 66. https://doi.org/10.3390/jrfm11040066

- Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letter, 148, 80–82. https://doi.org/10.1016/j.econlet.2016.09.019

- Urquhart, A., & Zhang, H. (2019). Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis, 63, 49–57. https://doi.org/10.1016/j.irfa.2019.02.009

- Vidal-Tomas, D. (2022). Which cryptocurrency data sources should scholars use? International Review of Financial Analysis, 81, 102061. https://doi.org/10.1016/j.irfa.2022.102061

- Vukovic, D., Maiti, M., Grubisic, Z., Grigorieva, E. M., & Frommel, M. (2021). COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave. Sustainability, 13(15), 8578. https://doi.org/10.3390/su13158578

- Wang, P., Zhang, W., Li, X., & Shen, D. (2019). Is cryptocurrency a hedge or a safe haven for international indices? A comprehensive and dynamic perspective. Finance Research Letters, 31, 1–18. https://doi.org/10.1016/j.frl.2019.04.031

- Wei, W. C. (2018). Liquidity and market efficiency in cryptocurrencies. Economics Letters, 168, 21–24. https://doi.org/10.1016/j.econlet.2018.04.003

- Wu, S., Tong, M., Yang, Z., & Derbali, A. (2019). Does gold or Bitcoin hedge economic policy uncertainty? Finance Research Letters, 31, 171–178. https://doi.org/10.1016/j.frl.2019.04.001

- Yousaf, I., Abrar, A., & Goodell, J. W. (2022b). Connectedness between travel & tourism tokens, tourism equity, and other assets. Finance Research Letters. https://doi.org/10.1016/j.frl.2022.103595

- Yousaf, I., & Ali, S. (2020). The COVID-19 outbreak and high frequency information transmission between major cryptocurrencies: Evidence from the VAR-DCC-GARCH approach. Borsa Istanbul Review, 20(1), S1–S10. https://doi.org/10.1016/j.bir.2020.10.003

- Yousaf, I., Ali, S., Bouri, E., & Saeed, T. (2022a). Information transmission and hedging effectiveness for the pairs crude oil-gold and crude oil-Bitcoin during the COVID-19 outbreak. Economic Research-Ekonomska Istrazivanja, 35(1), 1913–1934. https://doi.org/10.1080/1331677X.2021.1927787

- Yousaf, I., Nekhili, R., & Umar, M. (2022d). Extreme connectedness between renewable energy tokens and fossil fuel markets. Energy Economics, 114, 106305. https://doi.org/10.1016/j.eneco.2022.106305

- Yousaf, I., Pham, L., & Goodell, J. W. (2023). The connectedness between meme tokens, meme stocks, and other asset classes: Evidence from a quantile connectedness approach. Journal of International Financial Markets, Institutions and Money, 82, 101694. https://doi.org/10.1016/j.intfin.2022.101694

- Yousaf, I., Riaz, Y., & Goodell, J. W. (2022c). Energy cryptocurrencies: Assessing connectedness with other asset classes. Finance Research Letters. https://doi.org/10.1016/j.frl.2022.103389

Appendix A