?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The main objective of this quantitative study is to ascertain the effect of foreign direct investment, real exchange rate, remittances, and import on economic growth in Ghana. Secondary data on gross domestic product, foreign direct investment, real exchange rate, remittances, import, and gross capital formation from 1980 to 2018 were analyzed. The study employed Autoregressive Distributed Lag for the econometrics analysis. The study found that foreign direct investment, real exchange rate, remittances, import, and gross capital formation cointegrates with economic growth. The main findings are that foreign direct investment, real exchange rate, import, and remittances matter from growth perspective. Remittances have a positive and significant effect on economic growth in Ghana both for the short run and the long run. The study also revealed that foreign direct investment, real exchange rate, and imports have a negative and significant effect on the growth process of Ghana’s economy for both the short run and the long run. The study recommends that the Ministry of Finance, Ghana, financial analysts and other policy makers should undertake steps to reduce imports and attract more remittances inflows to attain long-run economic growth. In addition, the economy must concentrate on viable exchange rate policies such as undervaluation of currency to stimulate sustainable economic growth.

1. Introduction

The Republic of Ghana like most other sub-Saharan African countries and large developing countries has been strongly pushing to attain and sustain long-term economic growth prospects since independence in 1957. The globalization of economies across the world and at the same time the current increase in anti-globalization sentiments in some part of the globe constraint developing economies like Ghana to comprehend economic growth determinants. However, due to the broad nature of the economic growth arguments, literature on economic growth revealed that there are many indicators at play. Internal factors such as sound macroeconomic policies, quality of institutions, labour, political stability, and national saving are important economic growth stimulants (see Romer, Citation1986; Solow, Citation1956). However, in recent era, externalities, such as foreign direct investment (FDI), remittances, import, and real exchange rate are becoming important for stimulating economic growth process, specifically for small emerging economies (see Barajas et al., Citation2009). However, sustainable economic growth and development is fundamental because a healthy and progressive economy has the potential to create employment and mitigate hunger and poverty as compare to an under-performing economy. Contemporary social and economic literature argues that performing economy assists better supply of goods and services such as education and health, which encourages better standard of living of the people. A well-developed and prosperous community is obviously the fundamental objective of every economic activity.

The economy of Ghana is receiving a significant amount of foreign remittances from increasing number of its citizens dwelling and working in cross-border countries whose contribution have turned steady and is rising. For instance, from just around US$900,000 in 1980, remittances have increased to US$4,982,000 in 2015. Personal remittances received as a percentage of GDP in Ghana stood at 6.25 percent in 2020. However, this is a decline in remittances received because its value was 10.08 percent in 2015. With one-seventh of the world’s population migrating in search of better economic and social opportunities, remittance is expected to have some considerable implications for economic improvement, particularly in growing countries.

The FDI has always been cited as a preferred source of foreign capital for developing nations. However, FDI inflows to Ghana have recorded a 52% decline in 2020, leaving inflows at US$1.9 billion, from US$3.9 billion in 2019, following the economic and health constrain caused by the Covid-19 pandemic. The phenomenon of FDIs is a consequence of globalization, which includes the combination of the domestic economy with the global economic system. Foreign traders can set up commercial enterprise in the economic system via commencing up the internal economic sector and offering them with home capital. Financial globalization happens while there is a rise in capital motion within several international locations. With the assist of global monetary intermediaries, home creditors and borrowers can participate within the worldwide market. Developing nations benefit from economic globalization because of cheap labour and comparatively high returns on capital (Rogoff & Obstfeld, Citation1996). The amount of capital flowing into developing countries has multiplied in current years (Mawutor et al., Citation2021). In growing international locations, foreign funding has a considerable effect on economic growth. The presence of FDI in the economy of emerging countries like Ghana is deemed as a significant stimulant of economic growth. In addition, it forms the basis of job creation, transfer of modern technology, and economic growth and development of the beneficiary country. The presence of FDI creates environment for keener competition between indigenous and international companies. On this accord, indigenous companies are compelled to utilize their limited resources efficiently and effectively and accept modern technology (Nyeadi & Atiga, Citation2014)

Both emerging and industrialized economies’ increasing number depend upon on it for resource transfers. There are several real and potential gains from those flows, consisting of technological spillovers, new jobs, and improved managerial abilities and productivity. Due to the capital deficit in least evolved countries and the benefits accruable from those activities, they are essential for growth and improvement. Most Africans have undertaken a selection of coverage reforms to create a conducive investment surroundings to draw a large amount of FDI as a way of attracting FDI. It is situated in literature that FDI inflow is a major economic stimulant (Kulu et al., Citation2021). Bearing in mind that FDI stimulates private investment and provides new jobs and transfer knowledge and skill, it could assume a significant duty. There is a void on the effect of FDI on the beneficiary economy today. However, their role is crucial and no longer handiest in increasing production and developing jobs but also in growing the infrastructure and industries, which might be essential for economic growth (Nikolaos & Pavlos, Citation2017).

In addition, foreign imports including capital goods and intermediate input for production use specifically also assume a significant duty in the Ghanaian economy and overall growth of the economy. Thus, an increase in the value of imports implies a robust local demand and progressing economy. When the imports are categorically productive assets, including machinery and equipment, then it is more beneficiary for the economy because the productive assets will assist to improve the total productivity in the country in the long run leading to growth and development in the economy (Zhang & Zou, Citation1995). However, excess imports over exports leads to higher outflow of foreign currency than the inflows of such currency into the economy. In such case, the economy’s foreign exchange reserve reduces, leading to increase in interest rates, which worsen economic growth.

Finally, the exchange rate uncertainty also influences economic growth of a country. The theory of economic growth argues that stable exchange rates could lead to a fall in inflation rates, boost trade, and investment, which could enhance productivity and economic growth in the long run. Notwithstanding its influence on the growth of an economy and the significance of past researches on this problem, the extent of exchange rate uncertainty and its real influence on the growth of an economy is still a major concern, categorically in emerging economies such as Ghana (Alagidede & Ibrahim, 2016). This is clear in the domain of the current exchange rate uncertainty in Ghana. Emphatically, the Ghanaian cedi dwindled to the global worst performing currency to the Dollar in October 2022. The currency of the global second largest cocoa producer depreciated about 45.1% to the Dollar in 2022, the highest among 148 currencies ranked by Bloomberg, and this together with other indicators, making cost of doing business high in the country leading to the stagnation of the economy. Exchange rate uncertainty could ensue in an economic endeavour within any given period and thus requires continuous examination (Alagidede & Ibrahim, Citation2017). In the light of the aforementioned, it is important to ascertain the long-run relationship among FDI, real exchange rate, remittances, and import on economic growth, which will be relevant for government and policy decision-makers.

There are a lot of studies regarding economic stimulants on economic growth in Ghana; FDI and economic growth nexus (Antwi et al., Citation2013; Kulu et al., Citation2021); foreign remittances on economic growth (Nyeadi & Atiga, Citation2014); exchange rate volatility on economic growth (Alagidede & Ibrahim, Citation2017); and import on economic growth (Osei, Citation2012). Even though all the listed studies used the variables used in our current study, none of them combined all these variables together in the same study to ascertain their effect on economic growth creating knowledge gap in literature. Thus, the objective of the current study is to investigate the effect of FDI, remittances, import, and real exchange rate on economic growth in Ghana.

Categorically, we have contributed to the extant literature in these ways. One, the study has filled contextual-knowledge gap by making the first attempt to extend the understanding of convergence of FDI, foreign remittances, real exchange rate, and imports as significant predictors of economic growth in a developing country perspective. This new insight will aid economic policy formulation that enhances growth in context. Two, our findings have responded to calls to support the application of the Autoregressive Distributed Lag (ARDL) for the econometrics analysis to determine the long-run and short-run effect of the economic stimulants on economic growth, which have received less attention in finance literature. Three, our findings that revealed the significant roles of the predictors support the Dutch disease theory used in our study. This implies that our study’s assumption indicates that when there is rapid development of FDI, real exchange rate and imports will have negative effects on growth has been proven in our results. As the theory predicts that an economy with large natural resources might experience a fall or low economic growth, we contextualized FDI, real exchange rate, and imports as resources in large quantities that might affect economic growth. The remainder of the paper is arranged as follows: section two consists of literature review. Data sources and model estimation were discussed in section three. Results and discussion are presented in section four while section five consists of conclusions and recommendations.

2. Literature review

2.1. Economic outlook of Ghana

Ghana’s rapid growth (7% per year in 2017–19) was truncated by the COVID-19 pandemic, in March 2020 lockdown, and a pointy decline in commodity exports. The economic slowdown had a sizable effect on families. The poverty rate is predicted to have barely extended from 25% in 2019 to 25.5%in 2020. After slowing to 0.5% in 2020, boom rebounded to 5.4% in 2021 thanks to dynamic agriculture and service sectors. The profile of Ghana’s healing turned into rather inclusive and labour-extensive, with the extractive sector making only small contributions.

In quarter one of 2022, the overall GDP grew by 3.3%, year-on-year, down from 3.6% over the same duration in 2021. Non-oil increase also bogged down significantly (from 5.3 to a few 0.7%) reflecting a slowdown in agriculture and services.

Fiscal pressures have remained excessive. Over the first half of 2022, the fiscal deficit reached 5.6% of GDP, nicely above the 3.9% target for the same time. Revenues underperformed, because the flagship e-levy was introduced overdue and confronted foremost implementation challenges. As at the end of June 2022, public debt had reached 78.3% of GDP and interest payments reached 54.4% of revenue over the first half of the year. Given developing macroeconomic imbalances, in July 2022, the Ghana government started discussions with the IMF on a likely application.

Inflation rose to 31.7% year on year (an 18–12 months excessive) in July 2022, from 12.6% at the end of 2021. The impact of hovering international commodity expenses (Ghana imports 40% of its fertilizers from Russia) has been compounded with the aid of the depreciation of the cedi which has up to now lost 24% toward the dollar in 2022 (in accordance with the Bank of Ghana records). The Government and the Bank of Ghana (BoG) have sought to dampen inflationary expectancies by way of, respectively slicing expenses, and elevating the monitoring policy rate (MPR) to 22% and banks’ primary reserve requirements from 12 to 15%.

Despite those macroeconomic headwinds, the performance of the financial sector has remained sturdy. The non-performing loans ratio stepped forward to 14.1% in June 2022, from 17% in June 2021. However, in the first quarter of 2022 credit to the non-public sector grew very slowly (at 3%). The trade openness produced a surplus balance as of end-June 2022, thanks to high oil and gold receipts. However, the overall current account recorded a deficit of 1.5 percent of GDP due to investment earnings outflows and net services account bills. As a result, the stock of gross international reserves declined by US$2 billion in the first half of 2022, to 3.4 months of imports. The depreciation of the local currency and significant increase in inflation have resulted in poor standard of living, especially for food. This has positioned widespread strain on household budgets, particularly for the poor who commit extra than half of their budget to meals. Rural farmers have also been affected by increases in the costs of fertilizer and different inputs.

GDP growth is expected to slow to 3.5% in 2022 and mean 3.3% over 2022–2024 as macroeconomic instability and corrective policy measures depress total demand. The weakening effect of high inflation and increased interest rate on personal consumption and funding can be bolstered through monetary and fiscal tightening. On the supply facet, in 2023: agriculture is anticipated to grow at 2.2%, given high input prices and particular troubles with cocoa plants; industrial output is projected to develop through 2.4% (as compared to projected 3.8% in 2022), as the oil and gas sector slowly recovers from the technical problems experienced in the past 2 years; and services are anticipated to develop through 2.7%, as excessive home inflation erodes the buying power of clients. The fiscal deficit is projected to remain excessive in 2023 (9.2% of GDP) and above. Indeed, improvements are projected to occur gradually with contributions from revenues and expenditure.

2.1.1. Theoretical review

We used the Dutch Disease Theory (DDT) of Corden and Neary (Citation1982) as the foundation for this study. This theory explains that a country with large natural resource rents may experience a de-industrialization and a lower long-term economic growth. In a simplified manner, the theory refers to the situation in which a boom in an export sector leads to a shift of production factors toward the booming sector and an increase in the prices of non-tradable goods and services (Hasanov, Citation2013). Other scholar such as Cavalcanti et al. (Citation2011) indicated that issues of corruption might set in when there is resources boom, which might decrease the quality of operations and commitment of the state institutions, mostly in non-Western economy. As situated in literature, the theory has been used in varied ways depending on the economic indicator under-investigation (Onakoya, Citation2012). In this study we operationalized DDT as FDI, real exchange rate, and imports as resources in large quantities that might affect economic growth. Undeniably, some earlier research (Hasanov, Citation2013; Inchausti-Sintes, Citation2015) have applied the DDT to explain economic growth. Evidently, all these studies have indicated the significant role DDT has played in studying economic growth. Furthering, DDT is a structural phenomenon that creates obstacles to industrialization or, if it changed into neutralized and the economy’s industrialized, however later ceased to be, provokes deindustrialization (Bresser-Pereira, Citation2013). According to the Dutch Disease, one of the resource curses concepts, influx of foreign capital flows into a country causes appreciation of the real change rate, undermining the competitiveness of the non-resource sector creating appetite for the consumption of more services and imports. According to Magud and Sosa, the appreciation of the real exchange rate could create factor allocation and drifting apart production from manufacturing. Contrarily, variability of the real exchange rate misalignment from the actual also leads to poor economic growth (Magud & Sosa, Citation2010).

Contrary to the DDT, it is predicted that the effect of foreign capital on real exchange rate appreciation on emerging economies has a differentiated effect on growth. Due to low prices associated with importing, the indigenous input- competing firms might significantly lower their cost of input, and this will therefore enhance productivity of domestic imports competing goods (Majumder & Rahman, Citation2020; Majumder et al., Citation2021). The movement of the RER in reaction to the injection of foreign capital concludes that in considering the relationship between foreign capital and economic growth, the role of exchange rate movement be given a considerable attention. Foreign capital is believed to have been demonstrating a sign of diminishing marginal returns; thus, there is such a thing as “too much aid”. If an increase in foreign capital injection into an economy is followed by a corresponding increase in public expenditure on consumer goods and other imported goods, it will result in what is called the Dutch disease effect, which marginally cripples growth in the long run.

Accordingly, calculated and well-rehearsed procedures must be used to remedy the Dutch disease effect, a robust method will create an atmosphere for a workable measure to be implemented. But poor measures will imply a fall in aid flows, hence creating a barrier in the implementation of strategic growth-oriented policies. Thus, the DDT with concentration on the studied variables of this study are worthy for investigation in this context.

2.2. Empirical review

2.2.1. Foreign direct investment and economic growth nexus

Blonigen and Piger (Citation2011) in their study examined the determinants of FDI activities. The study found out about the traditional gravity variables including cultural, distance factors, per capital GDP, relative labor endowment, and regional trade agreement. Other determinants consist of trade openness, host economy business facilitations, and ease of business, host economy infrastructure, mainly financial institutions at the extent of development and host economy institutions. Almfraji and Almsafir (Citation2014) have reviewed an extensive amount of literature on the link between FDI and economic growth from 1994 to 2012. The study revealed that the impact of FDI on economic growth is strongly positive; however, in some instances it is null or even negative. Moreover, the link between FDI and economic growth strongly depends on the interacting indicators such as the level of development of financial market, the adequate level of human capital, complementarities between domestic and foreign investment, open trade policies, quality of institutions, etc. Malik et al. (Citation2020) investigated the effect of per capital income, foreign direct investment, and oil price on emission and growth. The ARDL to cointegration and Granger causality are used for the econometrics analysis for both short and long run, using time-series data from 1971 to 2014. The study revealed that economic growth and foreign direct investment intensify carbon emission both in the short run and in the long run. This outcome reaffirms the study of Yue et al. (Citation2016) where they examined the effect of FDI on economic growth and environmental safety on 104 cities in China. The study observed a variation in green growth efficiency among the cities. FDI was found to induce green growth in the cities across China. Moreover, when the green growth efficiency is damaged down into economic performance and environmental performance, FDI promotes China’s economic growth boom through both environmental advantages and economic benefits. Finally, the impact of FDI differs in distinctive sectors. FDI within the emission-intensive region promotes green performance especially through the development of economic efficiency. FDI within the non-emission-extensive quarter promotes economic performance, environmental performance, and green efficiency.

Latief and Lefen (Citation2019) ascertained whether FDI inflows improve energy generation in Pakistan. The study also examined the causal relationship between FDI inflows and energy generation from 1990 to 2017. The energy sector according to the results was the highest beneficiary of FDI inflows. The study also found a direct bidirectional causal relationship between economic growth and energy generation in the short run. The long run result also identified a causality among the variables. Suggestions were made for policy formulation to keep minimum debt threshold and dissuade loan-based investment. Such methodology could assist to handle the energy constraints and induce economic growth.

Wu et al. (Citation2020) in their study on China examined whether FDI drive economic growth. According to their result, FDI has a negative U shape relationship with economic growth. The study revealed that international companies account for a significant share of domestic capital formation in Chinese economy. The study further reported that FDI strongly crowds out government expenditure. Also, Liang et al. (Citation2021) explored the link between foreign direct investment and economic growth using panel data on developing countries from 2000 to 2019. The Hausman fixed effect and instrumental variables two-stage least square were used for the econometrics analysis. According to their result, foreign direct investment had a positive effect on economic growth in developing countries. The study argued that a percentage increase in foreign direct investment inflow would lead to an upsurge in economic growth in developing countries. The study also revealed that unemployment has a negative effect on economic growth.

Azam and Feng (Citation2021) investigated the role of foreign direct investment on economic growth in developing countries. Cross-sectional data were examined for 37 developing economies consisting of lower middle-income and upper middle-income group from 1985 to 2018. According to the result, foreign direct investment has a positive and significant impact on the economic growth of lower middle-income group countries, while the negative effect of foreign direct investment was found on economic growth of upper middle-income countries. Latief et al. (Citation2021) used panel data on Asian economy to ascertain the effect of carbon emission on economic growth in the presence of foreign direct investment. The study also investigated the causal link of economic growth, carbon emission, and foreign direct investment. The study identified a causal link between economic growth and carbon emission. It further revealed a causal effect of urban population and energy consumption with carbon emission. Moreover, inflation and domestic capital are found to Granger cause economic growth. Lastly, a causal relationship exists between foreign direct investment and domestic capital.

Ibrahim and Acquah (Citation2021) using a panel data of 45 developing countries from 1980 2016 titled their paper Re-examining the causal relationships among FDI, economic growth and financial sector development in Africa. The panel Granger non-causality test result revealed that the causal relationship between foreign direct investment and economic growth is contingent on the determinants of economic growth. Meanwhile the study also discovers a causality between foreign direct investment and financial sector development and economic growth within the period of the study. Based on our computation, an increase in foreign direct investment retards economic growth by 1.21%.

2.2.2. Remittances and economic growth nexus

Fayissa and Nsiah (Citation2010) using panel data on developing countries explored the relationship between remittance and economic growth from 1980 to 2004, with data consisting of 36 African countries. According to the result, remittance had a direct effect on economic growth in the African countries sampled in the study. Javid et al. (Citation2012) also explored the effect of remittances on economic growth and poverty reduction. The ARDL to cointegration approach was used for the econometrics analysis from 1973 to 2010. According to the result, remittance had a positive and significant effect on economic growth. The result also revealed that remittance had a positive and strong effect on poverty reduction.

Salahuddin and Gow (Citation2015) studied the link between economic growth and remittances in the presence of cross-sectional dependence. CIPS panel unit root test and the Pooled (PMG) regression approach were used for the econometrics analysis. The study revealed a positive and significant effect of remittance on economic growth within the period of the study. The study further revealed that deviation in economic growth in the short run is corrected by about −0.037% in the long run; this was confirmed by the sign of the error correction term. Comes et al. (Citation2018) investigated the relationship among foreign direct investment, remittance, and economic growth in seven economies from Central and Eastern Europe whose GDP per capital is less than US$ 25000. The study found a positive effect of foreign direct investment, remittance, and economic growth within the period of the study. However, the contribution of foreign direct investment on economic growth is found to be more significant.

Imran et al. (Citation2021) deployed panel data to ascertain the relationship between remittances and economic growth in South Asian economies from 1994 to 2017. The fixed effect and random effect based on Hausman specification test were used for the econometrics analysis. The findings are that remittances had a positive and significant effect on economic growth of South Asian countries within the period of the study. Export and employment have direct and strong effects on economic growth. Inflation, however, correlates indirectly with economic growth. Their study recommended that since remittance stimulates economic growth and employment, it is necessary for the government to device a policy aimed at reducing the cost of wiring remittances to prevent informal channels of remittance transfer.

Adeseye (Citation2021) add to remittance and economic growth debate by examining the relationship between migrant remittance and economic growth in Nigeria from 1990 to 2018. Secondary data on remittance, inflation, import, export, and GDP were examined. The quantitative study revealed a positive and significant effect of remittance on GDP, export, and import within the period of the study in Nigeria. Inflation however had an insignificant effect on remittance keeping other variables same. The paper recommended among other things for policy decision-makers of the country to deploy the influx of remittance to stimulate economic growth.

2.2.3. Exchange rate and economic growth nexus

Gyimah-Brempon and Gyapong (Citation1993) explored exchange rate distortion and economic growth using Ghana as a case study. The study revealed that exchange rate distortion retards economic growth in Ghana. Rapetti et al. (Citation2012) critically looked at the effect of exchange rate uncertainty on economic growth. The study deployed an alternative classification approach and empirical strategies to ascertain the existence of asymmetries between groups of countries. According to the result, significant effect of currency undervaluation on economic growth was reported for developing countries. However, the nexus between real exchange rate undervaluation and per capital income is non-monotonic and marginally scarce for least developing economies.

Sharifi-Renani and Mirfatah (Citation2012) examined the effect of exchange rate uncertainty on FDI and argued that exchange rate instability reduces FDI flows contrary to the results of Al-Abri and Baghestani (Citation2015) who in their investigation explored the link between FDI and exchange rate volatility in Asia using both time series and panel data set from 1980 to 2011. The study found that FDI account for a reduction in the volatility of the exchange rate in countries such as Malaysia, Singapore, South Korea, China, and India. However, induces exchange rate uncertainty in Indonesia, Philippines, and Thailand.

Abdul-Mumuni (Citation2016) also explored the relationship between exchange rate volatility and the performance of the manufacturing sector in Ghana. The study deployed the ARDL to cointegration test approach from 1986 to 2013. According to the result, exchange rate volatility and manufacturing firm performance cointegrate but in the short run and the long run within the period of the study. Hence, appreciation in exchange rate leads to a corresponding increase in the performance of the manufacturing sector in Ghana while the reverse is true. The study recommends among other things that importation of goods produced domestically should be regulated so as to help empower the production capacity of the manufacturing sector. Moreover, the central government should constantly supply electricity, good road network, water, and robust telecommunication system as these amenities would boost the performance of the manufacturing sector, which would translate into a sustainable economic growth.

Habib et al. (Citation2017) using a 5-year mean data explored the relationship between exchange rate volatility and economic growth based on panel data of 150 countries during the post Bretton Woods era. The result revealed that a percentage increase (depreciation) reduces (increases) strongly economic growth which was represented as annual GDP growth, higher than previous findings in literature. The study thus concluded that the findings collaborate the effect just for emerging economies.

Alagidede and Ibrahim (Citation2017) on the strands of exchange rate also investigated on the causes and effects of exchange rate volatility on economic growth: Evidence from Ghana. The quantitative time-series data analysis result revealed that while shocks to the exchange rate are mean reverting, the rate at which disequilibrium get to equilibrium is very sluggish in the short run as policy-makers recalibrate their consumption and investment decisions. The authors argued that greater percentage of the shocks say three quarter to the real exchange rate phenomenon are self-driven, while other factors which account for one quarter such as public spending and growth of money supply, terms of trade, and output shock also contribute to the real exchange risk condition in Ghana. The study also supports the notion that excessive volatility retards economic growth, but to a level as growth-enhancing impact could ensue from innovation and prudent allocation of resources in the economy.

Wesseh and Lin (Citation2018) examined exchange rate fluctuations, oil price shocks, and economic growth in a small net-importing economy. It was found that a percentage increase in oil price leads to an increase in economic growth. The study also revealed that depreciation in the real exchange rate results in a fall in the economic growth while appreciation in the real exchange rate triggers an increase in economic growth holding other variables same. Finally, consumer price index has a direct effect on economic growth. Vasani et al. (Citation2019) explored the effect of real exchange rate on economic growth indicators such as consumer price index, import, inflation, international reserve, money supply, balance of payment, and export in India from quarter one 2005 to quarter four 2017. The study deployed the Johansen cointegration test, Granger causality, and ADF stationary test for the econometrics analysis. According to the result, real exchange rate had a linear relationship between economic growth indicators within the period of the study, except balance of payment.

Latief and Lefen (Citation2018) explored the impact of exchange rate uncertainty on foreign trade and FDI in emerging economies. According to the results, exchange rate uncertainty induces both foreign trade and FDI strongly. However, indirectly in one belt one road (OBOR) associated economies, it correlates with the monetary principle arguing that trade charge volatility may additionally harm global exchange and FDI. It can be concluded that exchange rate uncertainty can adversely trigger global trade and FDI inflows in OBOR-associated international locations. Ribeiro et al. (Citation2020) investigated the effect of real exchange rate misalignment on economic growth in developing countries. The panel data were analyzed using the System General Methods of Movement (GMM). According to their result, real exchange rate misalignment has an insignificant direct effect on economic growth in developing countries within the period of the study keeping other variables same. The study also discovered that the real exchange rate only affects economic growth negatively through its effects on functional income distribution and technological innovation.

Nuhu and Bukari (Citation2021) investigated the relationship among export, import and exchange rate oscillation in Ghana using monthly data from 2005 to 2019. According to the result, while merchandise export affects real effective exchange rate adversely, merchandise imports have a positive relationship with exchange rate. However, both were found to be perpetual and the magnitude of their effect on exchange rate varies, where import shocks are quicker than export shocks. The study recommends that for an import-oriented country like Ghana, import ordinarily may not necessarily have an adverse effect on real exchange rate, because significant quantity of import may also serve as a major source of raw material for production. The Granger causality test discovers unidirectional relationship with export, foreign exchange reserve, and money supply. The study among other thing recommends that since the relationship between real exchange rate and economic growth indicators is positive, agents of the economy must give a considerable attention to these indicators, so as to develop robust strategies for the growth and development of the Indian economy in the long run.

Ybrayev (Citation2021) add to the body of literature on real exchange rate management and economic growth nexus including the role of the change in the behavior of exchange rate in line with the introduction of inflation targeting monetary policy and shifting to the flexibility exchange rate regime domestic currency in Kazakhstan. According to the result, a percentage increase in undervaluation of the real exchange rate causes about 0.05% increase in the growth rate of export from the manufacturing sector keeping other variables same. Also, a percentage increase in the real exchange rate triggers about 0.08% increase in the performance of the primary product industries, while a percentage depreciation of the real exchange rate results in 0.14% increase in the performance of the high-tech manufacturing industries. The study additionally found a support for the notion that highly volatile exchange rate regime retards the development of capital-intensive sectors. The researcher suggested that a macroeconomic policy targeting a sustainable and competitive real exchange rate may be useful for the development of highly technologically intensive industries and enhance price competitiveness for the country.

2.2.4. Import and economic growth nexus

The effect of imports on economic growth is marginally contingent on the kind of imports. In the case of consumable imports, the probability that such imports will induce economic growth in the beneficiary country will be low; notwithstanding, if the imported goods are made up of capital goods and modern technology, this may assist the beneficiary’s economy in ancillary ways. According to Zhang and Zou (Citation1995), foreign technology imports augment economic progress. Also, the extent of economic development varies between advancing and advanced countries, and in the case of advancing countries, importation of plants and equipment as well as borrowing international technology contributes to economic fortune of the recipient country. On the other hand, Siddiqui and Iqbal (Citation2005) argued that international trade (imports and exports) and economic growth are loosely associated. Notwithstanding, imports are with no doubts vital for economic fortune. Modern technology and equipment intended for development of local industrial sector can only be achieved with the support of improved import.

Uğur (Citation2008) deplored the multivariate VAR econometrics analysis to ascertain the nexus between import and economic growth using Turkey as a case study. The results found a support for cointegration between import and export in Turkey. It was also concluded that bidirectional causality exits from economic growth and investment goods import and raw material import, while unidirectional causality runs from consumption goods import and other good import. Kogid et al. (Citation2011) investigated imports and economic growth nexus in Malaysia. The study used the bivariate cointegration and causality approach based on the Engle–Granger two steps, Johansen, Toda–Yamamoto and Hsiao’s Granger causality method to ascertain the relationship between economic growth and import from 1970 to 2007. According to the result, economic growth does not cointegrate with import within the period of the study. Furthermore, the study reported that import had a negative effect on economic growth within the period of the study. Finally, it was revealed that import could retard economic growth negatively, while economic growth could stimulate import.

Osei (Citation2012) adds to the body of literature by testing the null hypothesis that import has no significant effect on economic growth in Ghana. According to the result, import was found to stimulate economic growth. The Johansen cointegration test revealed a long-run cointegration among import, income, foreign reserve, exchange rate, and domestic price. The researcher suggested among other things that are dependent on tariffs from import and nontariff procedures as a medium to stimulate import of raw materials in the medium to long run. El Alaoui (Citation2015) examined the causal direction and cointegration between export, import, and economic growth using Morocco as a case study. The study used the Granger causality and the Vector Error Correction Model (VECM) for the econometrics analysis. The result found that the variables are cointegrated. The Granger causality test results revealed a bidirectional causality running from economic growth to export and unidirectional causality running from export to import. The study however found no causal relationship between economic growth and export.

Devkota (Citation2019) examined the Impact of Export and Import on Economic Growth. The study deployed time-series data from 1996 to 2019 for China. The Augmented Dicey Fuller (ADF) and Phillips–Parron (PP) unit root test, Johansen Cointegration and the Vector Error Correction Model (VECM) to ascertain the causality between the variables were used for the econometrics analysis. The study reported that export, import and economic growth cointegrate one another. The Granger Causality test result revealed a unidirectional relationship emanating from economic growth to import within the period of the study. This suggests that a percentage increase in the income of the studied country, government expenditure will increase, and some of the expenditure will be made on import.

Aluko and Adeyeye (Citation2020) explored the relationship between import and economic growth in Africa. The study deployed the Granger causality test approach to ascertain the direction of causality. The study found that there exists unidirectional causality emanating from import and economic growth for 7 countries in the short run while 5 countries in the long run, and 10 countries in the long run. Furthermore, unidirectional causality emanates from economic growth to import in 4 countries for the short run and 10 countries for the long run. Bidirectional causality in the short run was documented in just single country and three countries for the long run. Finally, the study found support for no causality for 29 countries in the short run and 23 countries in the long run. The researcher concluded that the neutrality hypothesis is valid for the short run and long run within the period of the study. They suggested that attention must be paid critically on the volatility of causality behavior between import and economic growth over time before developing and implementing policies.

Apriliana et al. (Citation2021) explored the effect of export and import on economic growth in Indonesia. The multiple linear regression approach was used for the econometrics analysis from 2019 to 2021. According to the results, a percentage increase in export will lead to a fall in economic growth. However, a percentage increase in import triggers an increase in economic growth keeping other variables same. Okyere and Jilu (Citation2020) examined the relationship among export, import, and economic growth in Ghana from 1998 to 2018. The study found an insignificant causal relationship between import and economic growth in Ghana. Export was, however, found to have a strong causal relationship with economic growth within the period of the study.

Ali et al. (Citation2021) using the ARDL to cointegration explored the link among export, import, and economic growth in Ghana. The Johansen co-integration and Granger causality test were used for the analysis. According to the result, export, import, and economic growth are cointegrated, and this relationship is statistically 5%. The Granger causality test revealed that there exists no causal relationship among export, import, and economic growth.

The reviewed examinations failed to provide consistent evidence in support of a robust relationship between economic stimulants such as FDI, real exchange rate, remittances, and imports and economic growth for Ghana economy. The findings of some of the studies confirm that FDI, real exchange rate, remittances, and imports stimulate economic growth positively while some others indicate that these externalities retard economic growth. Hence, empirical examination of the relationship among FDI, remittances real exchange, rate import, and economic growth is vital.

3. Data and methodology

3.1. Data collection method

Data on economic growth, FDI, real exchange rate, remittances, gross capital, and import were sourced from the data base of the World Development Indicators (WDI) for 38 years period from 1980 to 2018. The reason for the time span is based on availability of data for the selected variables.

3.2. Data analysis techniques

Eview 10 was used to analyzed the data. ARDL was deployed to ascertain the effect of FDI, real exchange rate, remittances, and import on economic growth in Ghana. The ADF and PP were also used to test unit root in the series based on the 5% level of significance.

3.3. Model specification

The main objective of the study is to investigate the effect of FDI, real exchange rate, remittances, and import on economic growth. Based on data availability, FDI, real exchange rate, remittances, and import on economic growth are considered in the examination. The model for the empirical examination is specified as:

Where

= GDP growth (Gross Domestic Product)

FDI = foreign direct investment

EXC = real exchange rate

RM = remittances

GCFM = gross capital formation

IMPR = imports

In EquationEquation (1)(1)

(1) , real GDP represents the dependent variable. FDI is measured as net inflows as a percentage of GDP. Remittances is measured as foreign remittances as a percentage of GDP, gross capital formation is measured as gross capital formation as a percentage of GDP, and imports is measured as total goods and services imported as a percentage of GDP.

3.4. Description of the variables

The inclusion of the variables was based on literature. These include variables that were best found to significantly stimulate economic growth (Alagidede & Ibrahim, Citation2017; Apriliana et al., Citation2021; Azam & Feng, Citation2021; Fayissa & Nsiah, Citation2010; Liang et al., Citation2021; Ribeiro et al., Citation2020; Salahuddin & Gow, Citation2015; Vasani et al., Citation2019). The dependent variable was measured as GDP as a percentage of annual growth. GDP is included to ascertain its long-run effect of GDP. Thus, it is expected that past GDP will stimulate current economic growth.

FDI is a major domestic investment stimulant, which is significant to propel economic growth in the recipient country. FDI is associated with the transfer of modern technology and also help in controlling poverty in the host economy. Azam and Feng (Citation2021) found a positive effect of FDI on economic growth, hence

Real exchange rate affects the economy via its impacts on major economic indicators, including employment, inflation, and specifically economic growth. Volatility in the real exchange rate affects the competitiveness of domestic products, leading to an increase in export or import, affecting trade balance and growth. Strong exchange rate can depress economic growth reason being that export becomes more expensive and, hence, less demand for export. Cheaper import could lead to demand for imported products leading to decline in demand for domestic products. However, high interest rates will dwindle the level of economic growth. Thus, real exchange rate is expected to have a direct effect on economic growth (Ribeiro et al., Citation2020; Vasani et al., Citation2019), hence .

Remittances would lead to increase in foreign exchange reserve, which in turn stimulate growth of the economy. (Azam & Feng, Citation2021; Fayissa & Nsiah, Citation2010; Liang et al., Citation2021; Salahuddin & Gow, Citation2015) found a positive effect of remittance on economic growth, hence, . Gross capital formation is expected to increase consumer spending and cross-border trade, and firms that increase their capital investment spending can influence the level of production of goods and services, hence,

. Imports are expected to stimulates the growth of an economy, especially, where the imported goods contain capital goods and technology, therefore,

.

3.5. Estimation for the ARLD model

To examine the effect of FDI, real exchange rate, remittances, and gross capital formation on economic growth in Ghana, the study deployed the Bound Test Approach developed by Pesaran et al. (Citation1999) and later extended by (Pesaran et al., Citation2001). The study adopted this approach because it is simple as compared to other multivariate cointegration methods. The use of the bound test allows the cointegration relationship to be ascertained by OLS after the lag order of the model is identified. ARDL was deployed and for ARDL to be used, the dependent variable must be a function of the explanatory variables and past values of the independent variable. The current study deploys secondary time-series annual data, a lag of the dependent variable was added to the function. The ARDL model is specified as:

= intercept

= error term

= vector of the independent variables which can either be I(1), I(0)

= vector of a dependent variable

= coefficients

K= the optimal lags used for the dependent variable

P= the optimal lags for the independent variables

The method by Pesaran et al. (Citation2001) motivated the use of an ARDL to estimate an Error Correction Model (ECM). The ARDL model for both the log run and the short run was estimated as:

Where

= represent the constant,

= the deference operator

= the coefficient to be estimated

= are the optimal lags for the independent variables

= vector of the error term

= economic growth

= foreign direct investment

= real exchange rate

= remittances

= gross capital formation

= imports

contains the measurement, and source of the variables employed in the study.

Table 1. Variable, measurement and sources of data

3.6. Diagnostic test

Diagnostic tests which explain the robustness of the estimated coefficients were performed. Diagnostic tests provide evidence to support the assertion about the robustness of the estimated coefficients (Shrestha & Bhatta, Citation2018). According to Shrestha and Bhatta (Citation2018), lag structure, coefficient diagnostic, and residual diagnostic are the most significant types of diagnostic tests. Residual diagnostic test is considered important in modeling economic data because the regression model seeks to mitigate errors. The stochastic error term should be independently and identically distributed, and this outcome is determined by residuals diagnostic test. For the purpose of the current study, the main tests approach for the residual diagnostics such as Lagrange multiplier, heteroscedasticity, and normality, which explain the robustness of the estimated coefficient, were performed. These are explained below.

3.6.1. Autocorrelation test

Autocorrelation occurs when the presence value of the residuals is correlated with any of the best values. When this occurs, the assumption of OLS of no autocorrelation will be violated. The standard errors will be invalid and the t-statistics become unreliable in the presence of autocorrelation. The Langrange Multiplier was employed in this case because it is easier to estimate the restricted model which help in evaluating the robustness of the model specification (Shrestha & Bhatta, Citation2018). Breusch–Godfred Serial Correlation LM Test was utilized to check for autocorrelation in the dataset. Hence, the statistics showed a value of which is greater than 0.05% means the model is free from autocorrelation as indicated in Tables .

Table 2. Descriptive statistics table

Table 3. Correlation matrix

Table 4. Unit root test result

Table 5. Cointegration test result

Table 6. Results of estimated long-run coefficients

Table 7. Results of estimated short-run coefficient

Table 8. Serial correlation and heteroskedasticity test results

3.6.2. Heteroscedasticity test

It is a requirement to test for heteroscedasticity of residuals when you construct the linear regression version. The cause is we want to check if the model for this reason constructed is unable to explain some pattern within the reaction variable (Y) that in the end shows up in the residuals. This would result in an inefficient and unstable regression model that might yield weird predictions in a while. The graphical approach and the statistical approach are the two ways of testing for heteroskedasticity. The graphical approach uses graphs and plots to determine the presence of heteroskedasticity. While the statistical method uses tests like Breusch–Pagan–Godfrey approach to test for heteroskedasticity. In our study we employed the Breusch–Pagan–Godfrey approach to test for heteroskedasticity. This approach is preferable because it is easy to use to check for the presence of heteroskedasticity in a linear regression model and assume that the error terms are distributed normally. The result for the heteroscedasticity indicates that the model is not suffering from heteroskedasticity because the probability value is greater than 0.05% level of significance as shown in Table .

3.6.3. Functional form test

Functional form of the model was used to check for heteroscedasticity for the purpose of the study. Level models are more often than not heteroskedastic; hence, the study controlled for that by transforming the model on log-level to control for the issue of heteroskedasticity. The result as shown in Table indicates the absence of heteroskedasticity because the probability value is greater than 0.05% level of significance.

Table 9. Heteroskedasticity test Breusch–Pagan–Godfrey (functional form)

3.6.4. Model stability test

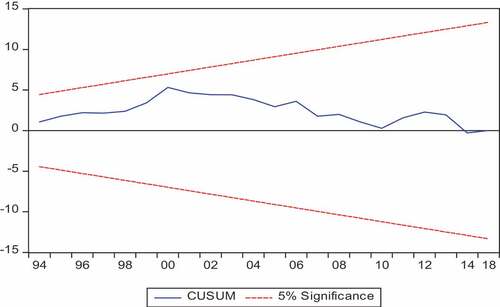

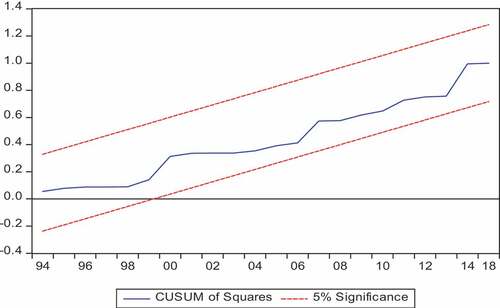

Stability tests are used to ascertain whether the parameters of the estimated series are statistically stable overtime. The reason for doing this is to ensure that the model is robust and can be relied upon for policy decision-making. Hence, the study used CUSUM test and cumulative sum of square (CUSUMSQ) of recursive residuals as suggested by (Brown et al., Citation1975) to check for the stability of the model. The plot of the CUSUM and the CUSUMSQ lies within the 5% critical value of significance as indicated in the graph in the Appendices in Figures , respectively, in the Appendix. This suggests that the model is stable over time.

3.6.5. Normality test

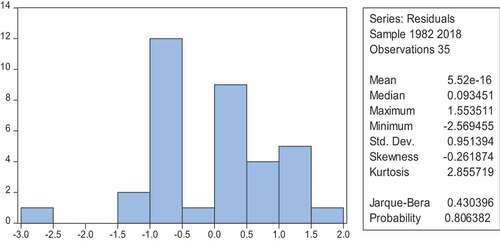

Normality test was deployed to test if normally, the model residuals are distributed to ensure that the assumptions of the OLS are not violated. Skewness and kurtosis were applied to statistically check if the residuals for the skewness and kurtosis are significantly far from the normally distributed residuals of the model. The results showed that all the probability values for the study is above 0.05% showing no deviation from normality as shown in Figure in the Appendix.

4. Results and discussions descriptive statistics

From the descriptive statistics (Table ), the standard deviation of FDI and real exchange rate are closer to their means. However, the standard deviation for the remaining variables such as GDP, remittances, gross capital formation, and imports were distanced from their respective means. Hence, a variation in the individual values strongly influenced the proceeding period’s values. This significant volatility could lead to uncertainty in prediction. Examination of the minimum and maximum values suggests that there are fluctuations in all the variables. Furthermore, while a relatively higher mean values for household consumption expenditure and gross capital formation are important for the economic outlook, same cannot be said for imports.

4.1. Correlation matrix

The study also employed Pearson correlation matrix to assess the strength of association among the variables and to check if there exists a higher association in order to prevent issues of multicollinearity. The results are presented in Table . The results revealed that there exists a positive and significant association between GDP and each of FDI, real exchange rate, remittances, gross capital formation, and imports. Finally, none of the variables exhibits a higher coefficient value that could lead to issues of multicollinearity and thus, the study estimates an ARDL model for both short run and long run.

4.2. Unit root test

The likelihood of the presence of unit root problem in the variables is checked through ADF and PP tests. Although ARDL approach does not demand the pre-testing of non-stationarity problem, it is still relevant to perform the above-mentioned tests to ensure that none of the variables are integrated at order two I(2). The results based on the ADF and PP tests are shown in Table .

According to the results, both ADF and PP tests are considered to intercept and trend simultaneously and also to intercept only. The results revealed that all the variables examined suffered from unit root problem at levels, except for exchange rate and foreign remittance. However, the rest of the variables became stationary after first difference. This suggests that the variables are integrated at different orders, I(0) and I(1), which is required for the cointegrating test.

4.3. Cointegration test result

The result on the ARDL cointegration test is presented in Table . The cointegration bound test had an F-statistics value of 3.83, which is greater than the lower and the upper bounds values at 5% significant level. Hence, the null hypothesis of no cointegration is rejected in favor of the alternative hypothesis of cointegration (see, Pesaran et al., Citation2001). Hence, there is an evidence of a long run relationship among all the variables used for the study. Evidence of cointegration indicates that the variables are related and may be combined in a linear fashion. It also means that any shock in the short run that could affect the movement of the variables will converge in the long run. Thus, the ARDL cointegration approach was used to ascertain both the short- and long-run relationship among the variables.

4.4. Results of estimated long-run coefficients

Table presents the long run estimates of the variables where FDI had a negative and significant effect on economic growth (GDP), and this contradicts with literature (Azam & Feng, Citation2021; Liang et al., Citation2021). The result reveals that 1% increase in FDI will lead to 1.16% decrease in economic growth. The result indicates that FDI inflows worsen economic growth in Ghana. There are numerous channels through which the recipient gains from FDI inflows. An efficient manufacturing system and advanced technology in remote economies such as Ghana could only be attained and implemented through attracting FDI from advancing economies that are developed and big. The Ghana government must put measures in place to revive the ailing economy through stability of the exchange rate and reduction in inflationary rate which lead to increase in cost of doing business in the economy. Also, government must demonstrate through laws and reforms in safeguarding the investment of the foreign investors and by making available better physical and financial infrastructure. Thus, it is imperative for the government to prioritize investing a sizeable sum of its resources into agriculture to assist in correcting the gap in production deficiency and reduce its current account balance deficit. Thus, such policies could potentially assist in reviving the Ghanaian economy to its potential root for economic recovery.

The study also found that the exchange rate had a negative and significant effect on economic growth and this is consistent with literature (Alagidede & Ibrahim, Citation2021). Thus, 1% increase in exchange rate volatility will revert economic growth by 0.88% all things being equal. Thus, a strong exchange rate can retard economic growth because it leads to higher cost of export and lower the cost of importation. Such situation will lead to more demand for imported goods to the detriment of locally produced products leading to a fall in aggregate demand in the economy.

Another finding of the study is that remittances had a positive and significant effect of (2.46 with a t-statistics of 6.41) on economic growth. Thus, 1% increase in remittances will stimulate economic growth by 2.46% and this is consistent with literature (Azam & Feng, Citation2021; Fayissa & Nsiah, Citation2010; Liang et al., Citation2021). In the case of remittances, it assists households, augments local savings, and increases economic growth prospect in Ghana. Because remittances come in a form of foreign currency, it boosts the foreign exchange earnings which supports the huge import cost. Finally, Ghana is relatively blessed with labor and human capital. Therefore, it is worthy for policy-makers and the central government to ensure robust development of platform for citizens to work overseas and make infrastructure available for existing migrants to strategically trigger the remittances inflows. The study further found that gross capital formation had a positive and insignificant effect on economic growth.

Imports signal total amount of goods and services imported into the country; priori to our expectation is negative and statistically significant, thus, indicating that an increase in importation has a negative effect on the economic prospect of the country contrary to the results of (Apriliana et al., Citation2021). Based on economic theory, imports inflow is vital for countries that are in their infant stages of growth. However, it is difficult for anyone to understand why imports worsen economic growth. One sure way of making this a reality is by taking into account the numerous types of foreign imports. In the case where an economy imports more of consumable goods, then this is not probable to boost economic growth agenda. However, when the foreign imports contain goods such as capital, technology nature of goods, and intermediate inputs, it is probable that such imports would boost economic growth agenda. Also, it is worthy to note that the economic growth trend distance from big advancing and advanced countries to small advancing sub-Saharan economies. In the case of advancing sub-Saharan economies, importing capital goods and technology and learning better ways of doing things are imperative for economic growth.

4.5. Result of estimated short-run coefficients

The coefficient of the ECM is negative (−0.91) as shown in Table . This implies that there is a convergence of the variables in the long run and it is statistically significant at 1%. The coefficient of the ECM (−1) which is equal to (−0.91) for the short run implies that a deviation in economic growth in the short run is corrected by 0.9% yearly and in the long run all other factors being constant. Moreover, the negative sign of the adjustment coefficient signals a cointegrating nexus between economic growth and each of the explanatory variables.

The result indicates that in the short run, FDI, real exchange rate, and imports have a negative and significant effect on economic growth. As Ghana attracts FDI inflows from different countries, international firms could also fly out their investment from the country. Therefore, the negative effect of FDI on economic growth in the country could be as a result of excess outflows of FDI over the net inflows of FDI into the country. Other factors such as corruption, poor human capital, high cost of doing business, and poor infrastructure could be the major cause of the negative nexus between FDI and economic growth in Ghana (Rahman, Citation2015). The negative effect of imports on economic growth could results from excessive importation of consumable goods, which could have been produced internally leading to negative balance of payment (Apriliana et al., Citation2021). Also, the negative effect of real exchange rate on economic growth is because the traded goods in most worldwide transactions are the usage of the currency of the exporting or importing country. Therefore, unexpected changes and volatility in trade prices ought to adversely affect international trade flows and economic growth due to their effect on earnings. Finally, the results found that foreign remittances produced a positive and significant effect on economic growth in the short run. This finding is confirmatory of existing literature.

5. Conclusion and recommendations

The study investigated the effect of FDI, real exchange rate, remittances, and imports on economic growth using the ARDL approach. Secondary time-series annual data from 1980 to 2018 were examined. The study found that FDI, exchange rate, imports, and remittances matter in sustaining long-run economic growth in Ghana. Remittances, FDI, and imports are economic stimulants in Ghana. The study found imports to have an adverse and significant effect on economic growth. This finding differs from the study of Apriliana et al. (Citation2021) who found a positive nexus between imports and economic growth; thus, this is a contribution of the study to knowledge gap. This result is difficult to explain, but the issue is that Ghana is known as an import-reliant economy, which largely relies on imported goods such as plant, machinery, and consumables. It is impossible to reduce the importation of these goods due to absence of local production and also the inability to locally produced them. The top imports of Ghana are refined petroleum costing US$669 million, rice US$391, delivery trucks US$238 million, and coated flat-rolled iron US$273 million. Moreover, data and measurement associated problem could be potentially responsible indicator.

The study additionally revealed that foreign remittances have positive effects on the growth of the economy in Ghana. This scenario is played in other sub-Saharan Africa economies with huge population of their citizens working overseas and remitting remittances to their households. Hence, decision-makers in Ghana and others in sub-Saharan countries must be meticulous in implementing robust policy plans to attracts remittances inflows. Furthermore, real exchange rate negatively and strongly worsens economic growth of Ghana and this is consistent with the Theory of Dutch Disease effect. Thus, the implication of this finding is that the Ghanaian economy is susceptible to exchange rate uncertainty.

Based on the outcome of the study, we recommend that, first, in Ghana, a robust policy action should be implemented by the Ministry of Finance Ghana, financial analysts, financial practitioners, and businesses to sustain steady remittances inflows. For instance, charging low transaction fees, setting up adequate information and communication technology, and liberalizing the home financial system to connect remittances receivers to financial service providers. Second, imports are essential for emerging countries in their infant stage of development and categorically where majority of the imported goods are made up of intermediate inputs and capital goods. Government, businesses, financial analysts, and financial practitioners should all make sure there is efficiency in the use of imported capital goods and produce locally consumable goods to avoid over reliance on imported consumables.

Third, it is recommended that the Ministry of Finance of Ghana, financial analysts, financial practitioners, and businesses should boost the confidence of investors by restoring confidence in the economy through stability of real exchange rate, cost of doing business, and collaboration with key relevant policymakers on the premise of mutual gains, which will largely improve the confidence of the investors.

There is the need for the Ministry of Finance Ghana, financial practitioner, businesses, and financial analysts to inject efficiency in the management of the Ghanaian economy. This will help to promote the fundamental growth of the overall economy. This in the long run will reduce investors’ appetite to hedge their investments in foreign currencies. This will help to curb the uncertainty associated with the local exchange rate.

5.1. Theoretical implications

Generally, the study deployed the DDT to ascertain the effect of FDI, foreign remittances, real exchange rate, and imports (Corden & Neary, Citation1982) on economic growth in Ghana. Even though the DDT has been employed in the previous examinations of economic growth stimulants, the literature from the perspective of the convergence studied variables as significant predictors of economic growth in a non-western country perspective remain insubstantial. Therefore, the application of the DDT from non-western economy perspective serves as one of the key theoretical implications of this study. Second, the DDT was applicable as well as needful in ascertaining the impact of the studied variables on economic growth relationship in Ghana. This is evident in how these economic stimulants induce economic growth in Ghana. Evidently, majority of the previous studies (Antwi et al., Citation2013; Kulu et al., Citation2021); foreign remittances on economic growth (Nyeadi & Atiga, Citation2014); exchange rate volatility on economic growth (Alagidede & Ibrahim, Citation2017); and import on economic growth (Osei, Citation2012) on Ghana failed to combined these stimulants together in the same model to ascertain their effect on economic growth creating knowledge gap in literature. Thus, our study has filled contextual-knowledge gap by making the first attempt to extend the understanding of convergence of the studied variables as significant predictors of economic growth in a non-western country perspective. This new insight will aid economic policy formulation that enhances growth in context as well as similar geographical environments.

6. Limitation

There are other factors that could enhance the effect of economic stimulants on economic growth. These factors include quality of institutions, political stability, good governance, and accountability. However, the study failed to control for any of these variables in the study. Future studies should control for these variables. Furthermore, future studies could examine the threshold level of these growth determinants that will induce economic growth in Ghana.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

John Kwaku Mensah Mawutor

John Kwaku Mensah Mawutor is an Associate Professor of Accounting at the University of Professional Studies, Accra (UPSA). He is currently the Pro-Vice-Chancellor and a member of the Faculty of Accounting and Finance. Prior to his promotion to the position of Pro-Vice-Chancellor, Prof. Mawutor served as the Dean of the School of Graduate Studies (2016-2022), a program coordinator at the School of Graduate Studies (UPSA) from the year 2012 to 2015. He also served as a Hall Tutor (Opoku Ampomah Hall) from 2008 to May 2019. Apart from these administrative roles, he has also served on several university statutory committees from 2004 to date. He served on the University’s Governing Council from 2003 to 2004 and from 2015 to 2019. With his astute background in Governance, Accounting and Finance, he also served on a number of the Council’s sub-committee such as the Finance committee, Audit committee, 2015 search party, budget committee, and others. He has been a member of the University’s Academic Board since 2015 and Executive Committee Member to date. As a researcher and academic with penchant for practically oriented research, Prof. John Kwaku Mensah Mawutor has published in several indexed and ranked journals. His publications have been accepted and published by Journals ranked by Australian Business Deans Council (ABDC) and Scopus. He has also presented several papers in a number of conferences and seminars. He is a regular writer in Ghana’s premier newspaper publishing firm (Daily Graphic) on finance and accounting-related issues. Prof. Mawutor has also authored one (1) Book. Currently, Prof. Mawutor’s area of research focus is on capital flight in Ghana and Sub-Sahara African countries. He is an astute anti-corruption crusader. He is also an Associate member of the Institute of Fraud Examiners (USA).

References

- Abdul-Mumuni, A. (2016). Exchange rate variability and manufacturing sector performance in Ghana: Evidence from cointegration analysis. Issues in Economics and Business, 2(1), 1–27. https://doi.org/10.5296/ieb.v2i1.9626

- Adeseye, A. (2021). The effect of migrants remittance on economy growth in Nigeria: An empirical study. Open Journal of Political Science, 11(01), 99. https://doi.org/10.4236/ojps.2021.111007

- Al-Abri, A., & Baghestani, H. (2015). Foreign investment and real exchange rate volatility in emerging Asian countries. Journal of Asian Economics, 37, 34–47. https://doi.org/10.1016/j.asieco.2015.01.005

- Alagidede, P., & Ibrahim, M. (2017). On the causes and effects of exchange rate volatility on economic growth: Evidence from Ghana. Journal of African Business, 18(2), 169–193. https://doi.org/10.1080/15228916.2017.1247330

- Ali, B. J., Hasan, H., & Oudat, M. S. (2021). Relationship among export, import and economic growth: Using co-integration analysis. Psychology and Education Journal, 58(1), 5126–5134. https://doi.org/10.17762/pae.v58i1.2068

- Almfraji, M. A., & Almsafir, M. K. (2014). Foreign direct investment and economic growth literature review from 1994 to 2012. Procedia-Social and Behavioral Sciences, 129, 206–213. https://doi.org/10.1016/j.sbspro.2014.03.668

- Aluko, O. A., & Adeyeye, P. O. (2020). Imports and economic growth in Africa: Testing for granger causality in the frequency domain. The Journal of International Trade & Economic Development, 29(7), 850–864. https://doi.org/10.1080/09638199.2020.1751870

- Antwi, S., Mills, E. F. E. A., Mills, G. A., & Zhao, X. (2013). Impact of foreign direct investment on economic growth: Empirical evidence from Ghana. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(1), 18–25. https://doi.org/10.5539/ijef.v5n3p90

- Apriliana, T., Saudi, M. H., & Sinaga, O. (2021). The effect of export-import on economic growth during the covid-19 pandemic in Indonesia: An investigation from multiple geographical settings in Indonesia and across borders. Review of International Geographical Education Online, 11(1), 595–600.

- Azam, M., & Feng, Y. (2021). Does foreign aid stimulate economic growth in developing countries? Further evidence in both aggregate and disaggregated samples. Quality & Quantity.

- Barajas, A., Chami, R., Fullenkamp, C., Gapen, M., & Montiel, P. J. (2009). Do workers’ remittances promote economic growth? Available at SSRN 1442255.

- Blonigen, B. A., & Piger, J. (2011). Determinants of foreign direct investment (No. w16704). National Bureau of Economic Research Doi, 10, w16704.

- Bresser-Pereira, L. C. (2013). The value of the exchange rate and the Dutch disease. Revista de Economia Política, 33(3), 371–387. https://doi.org/10.1590/S0101-31572013000300001

- Brown, R. L., Durbin, J., & Evans, J. M. (1975). Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society Series B (Methodological), 37(2), 149–163. https://doi.org/10.1111/j.2517-6161.1975.tb01532.x

- Cavalcanti, T. V. D. V., Mohaddes, K., & Raissi, M. (2011). Growth, development and natural resources: New evidence using a heterogeneous panel analysis. The Quarterly Review of Economics and Finance, 51(4), 305–318. https://doi.org/10.1016/j.qref.2011.07.007

- Comes, C. A., Bunduchi, E., Vasile, V., & Stefan, D. (2018). The Impact of foreign direct investments and remittances on economic growth: A case study in central and eastern Europe. Sustainability, 10(1), 238. https://doi.org/10.3390/su10010238

- Corden, W. M., & Neary, P. J. (1982). Booming sector and deindustrialization in a small open economy. The Economic Journal, 92(368), 825–848. https://doi.org/10.2307/2232670

- Devkota, M. L. (2019). Impact of export and import on economic growth: Time series evidence from India. Dynamic Econometric Models, 19, 29–40. https://doi.org/10.12775/DEM.2019.002

- El Alaoui, A. (2015). Causality and cointegration between export, import and economic growth: Evidence from Morocco. Journal of World Economic Research, 4(3), 83. https://doi.org/10.11648/j.jwer.20150403.14

- Fayissa, B., & Nsiah, C. (2010). The impact of remittances on economic growth and development in Africa. The American Economist, 55(2), 92–103. https://doi.org/10.1177/056943451005500210

- Gyimah-Brempon, K., & Gyapong, A. O. (1993). Exchange rate distortion and economic growth in Ghana. International Economic Journal, 7(4), 59–74. https://doi.org/10.1080/10168739300000014

- Habib, M. M., Mileva, E., & Stracca, L. (2017). The real exchange rate and economic growth: Revisiting the case using external instruments. Journal of International Money and Finance, 73, 386–398. https://doi.org/10.1016/j.jimonfin.2017.02.014

- Hasanov, F. (2013). Dutch disease and the Azerbaijan economy. Communist and Post-Communist Studies, 46(4), 463–480.

- Ibrahim, M., & Acquah, A. M. (2021). Re-examining the causal relationships among FDI, economic growth and financial sector development in Africa. International Review of Applied Economics, 35(1), 45–63. https://doi.org/10.1080/02692171.2020.1822299

- Imran, M., Zhong, Y., & Moon, H. C. (2021). Nexus among foreign remittances and economic growth indicators in south Asian countries: An empirical analysis. Korea International Trade Research Institute, 17(1), 263–275. https://doi.org/10.16980/jitc.17.1.202102.263

- Inchausti-Sintes, F. (2015). Tourism: Economic growth, employment and Dutch disease. Annals of Tourism Research, 54, 172–189. https://doi.org/10.1016/j.annals.2015.07.007

- Javid, M., Arif, U., & Qayyum, A. (2012). Impact of remittances on economic growth and poverty. Academic Research International, 2(1), 433.

- Kogid, M., Mulok, D., Ching, K. S., Lily, J., Ghazali, M. F., & Loganathan, N. (2011). Does import affect economic growth in Malaysia. The Empirical Economics Letters, 10(3), 297–307.

- Kulu, E., Mensah, S., & Sena, P. M. (2021). Effects of foreign direct investment on economic growth in Ghana: The role of institutions. Journal of Economics of Development, 20(1), 23–34. https://doi.org/10.21511/ed.20(1).2021.03

- Latief, R., Kong, Y., Javeed, S. A., & Sattar, U. (2021). Carbon emissions in the SAARC countries with causal effects of FDI, economic growth and other economic factors: Evidence from dynamic simultaneous equation models. International Journal of Environmental Research and Public Health, 18(9), 4605. https://doi.org/10.3390/ijerph18094605