?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Does Indian sovereign yield volatility reflect economic fundamentals, or whether it is a self-generated force flowing through markets with little connection to such fundamentals? To answer the question, this research explores the volatility dynamics and measures the persistence of shocks to the sovereign bond yield volatility in India from 1 January 2016, to 18 May 2022, using a family of GARCH models. The empirical results indicate the high volatility persistence across the maturity spectrum in the sample period. However, upon decomposing the markets into bull and bear phases, our results support the existence of weak volatility persistence and rapid mean reversion in the bear market. This shows that the economic response policies implemented by the government during the pandemic, including fiscal measures, have a restraining effect on sovereign yield volatility. For a positive γ, the results suggest the possibility of a “leverage effect” that is markedly different from that frequently seen in stock markets. Results further indicate that the fluctuations in Indian sovereign yields cannot be dissociated from inflation and money market volatility. Our findings herein provide valuable information and implications for policymakers and financial investors worldwide.

PUBLIC INTEREST STATEMENT

The Indian financial system is changing fast, marked by strong economic growth, more robust markets, and considerably greater efficiency. Thus, analyzing the volatility of sovereign bond yields across maturities in India is worthwhile. The findings emphasize that positive shocks tend to cause volatility to rise as opposed to negative shocks of equal magnitude. The Indian financial markets, however, have recovered more quickly from the negative impact on sovereign yields post-pandemic. The market overreaction theory and market correction theory underlie the collapse and fast recovery of the markets. Besides, the results show evidence for high volatility persistence; when it rises, it remains high for a considerable time and returns to its mean only gradually in a euphoric period. Finally, the link between movements in bond yields and fundamental economic forces is examined in the current study.

1. Introduction

The eruption of the Asian financial crisis in mid-1997 had elevated uncertainties in the Asian financial markets (Tan & Hooy, Citation2004). As one of the consequences, the sovereign bond yields, among others, had also experienced amplified volatility. Besides, the instability caused by the Global Financial Crisis in the second half of 2008 and the challenges from the unprecedented COVID-19 have wobbled uncertainties in the financial market and increased the instability of the yield volatility of sovereign securities in India (Bhattacharyay, Citation2013). Therefore, this research article aims to examine the asymmetric behaviour of the Indian sovereign bond yields using a battery of GARCH specifications.

What is the relationship between the yield volatility of sovereign securities and corporate bond prices? The Standard asset pricing theories support the view that sovereign yield volatility and corporate bond prices are closely linked. On their part (Bevilaqua et al. Citation2020) and (Lithin et al. Citation2021) report that institutional investors highly demand sovereign bonds, and their yield fluctuations affect corporate bond prices. As a general rule of thumb, sovereigns are able to use corporate resources to meet their fiscal needs, which indicates that corporate borrowers are only as safe as their sovereign. It follows, therefore, from (Bedendo and Colla Citation2015) and (Eichengreen and Mody Citation2000) among others, that corporate spreads and the likelihood of bond issuances are significantly influenced by sovereign risk rating or other measures of sovereign risk. Nevertheless, it is generally accepted that there is a “sovereign ceiling,” meaning that corporate bond ratings cannot be higher than their sovereigns.Footnote1 In particular, when public and private sectors access capital markets and issue debt, sovereign ratings serve as a benchmark for capital-raising activities (Mohapatra et al., Citation2018). In this context, changes in sovereign creditworthiness affect corporate credit risk (Bedendo & Colla, Citation2015). In a nutshell, this issue has significant ramifications for companies’ access to financial markets, potentially affecting corporate borrowing costs, cash flow volatility, and corporate bond pricing uncertainty.Footnote2 On the other hand, corporates in emerging markets are more susceptible to changes in sovereign ratings than those in developed markets (Ferri & Liu, Citation2003). In view of the crucial role played by sovereign securities, it is critical to model the volatility of sovereign yields in India.

Unlike the extensive literature on the interrelationships in international sovereign bond markets and their volatility (Zaremba et al., Citation2021), and the influence of different variables on sovereign bond yield, there have been relatively few studies on sovereign bond volatility and their modelling across the maturity spectrum in relation to bond prices, particularly during periods of severe price fluctuations (Akram & Das, Citation2019). Therefore, understanding the volatility dynamics is crucial in developing hedging, derivatives trading, and portfolio optimization strategies to envision future positions (Aliyev et al., Citation2020a; J. M. Kim et al., Citation2021). Likewise, it is also interesting to investigate whether the volatility of sovereign bond yields is persistent over time; when it rises, it remains high for a considerable time and returns to its mean only gradually. Although market participants argue that bond yield volatility is higher in bear markets than in bull markets, academic research has been inconclusive so far. In light of these facts, we employ a long-memory technique, which, unlike other econometric methods, provides a direct measure of persistence in determining the volatility persistence property of sovereign yields and its volatility across bull and bear market phases.

Another, more recent strand of the literature supports the link between macroeconomic factors and sovereign yield volatility (Eichengreen & Luengnaruemitchai, Citation2004). And (Smaoui et al. Citation2017) claim that these observations may be of some interest to developed countries but exploring such a relationship in emerging markets could make a significant contribution to the literature, because developed countries feature more stable financial systems, stronger macroeconomic fundamentals, and a more robust economic and institutional foundation, which means their bond prices are least volatile in most of the cases. The question of whether markets have grown too powerful has gained more traction as a result of these instances of bond market volatility. Asking whether this volatility reflects economic fundamentals such as inflation and money market volatility or whether it is a self-generated force flowing through markets with little connection to such fundamentals is one approach to frame this question. In reality, relatively little is generally understood about the factors influencing volatility. Among these findings, there is still a significant gap in the knowledge regarding the research of volatility in fixed-income markets in general and the bond market in particular. In light of this, our objective is to move the bond volatility analysis out of its current compromising position.

Thus, we employ univariate asymmetric GARCH models and model the volatility of government bond yields over short-term, medium-term, and long-term maturities. We fit GARCH (1,1), EGARCH, IGARCH, and GJR-GARCH models to daily sovereign bond yields in the sample space from 1 January 2016, to 18 May 2022, under three different distributions, namely Normal, Student’s t, and GED. By doing this, we are bridging a gap in the literature by using asymmetric models across a long-time frame, including the 2019 crisis and its aftermath, to the volatility analysis of sovereign bond yields by decomposing the market into bull and bear phases. This article also aims to link changes in volatility across maturities to the fundamentals of the domestic economy. In this context, we take into account the bidirectional relationship between the volatility of sovereign bond yields and the overall economy; in other words, we are also interested in how traditional macroeconomic shocks impact volatility. In particular, we set out to ground sovereign bond volatility and its linkages with India’s inflation and money market volatility.

Our work is related to (Akram and Das) and (Chundakkadan and Sasidharan Citation2019) who investigated the relationship between sovereign yield volatility and their well-known determinants. Our work differs from that of (Akram and Das) and (Chundakkadan and Sasidharan Citation2019) in a number of respects. Our work is the first to objectively analyze the volatility of sovereign bond yield across various maturity periods in the Indian bond market. Second, while there is much interest in how bond yield spreads are determined, there has been little research on their volatility, persistence, and determinants of their volatility. Therefore, this study was motivated by the paucity of past empirical research on the volatility of sovereign bond yields. As a result, in accordance with the study’s primary purpose, we have four study objectives. The initial goal is to use asymmetric GARCH models to estimate the volatility of sovereign bond yields and choose the best model that fits the data. The second objective is to investigate the asymmetry in response to economic information for the period from January 2016 to May 2022. Third, upon decomposing the sample into bull and bear periods, we investigate volatility persistence at each market phase. Finally, we examine whether the selected macroeconomic determinants cause sovereign yield volatility in India and vice-versa.

The current study supports the view that investors are paid off for assuming interest rate risk because long-term bonds have, on average, produced larger yields than short-term bonds. This indicates that the investors are compensated for purchasing long-term bonds in the form of a risk premium. However, because it is challenging to foresee how interest rates and the yield curve will evolve and because the risk premium is not constant, the excess return varies significantly over time. The “shape” of the yield curve continues to vary as daily market fluctuations affect the yields on bonds with various maturities. These changes offer important information about the economy’s direction.

The findings of our study further reveal that the previous volatility highly influences the current volatility or that the impact of previous news on volatility has a lasting effect. The analysis also proves that volatility shocks persist and that projections of future volatility may be made using historical volatility. Besides, we provide convincing evidence that volatility increases more when there are positive shocks. The results further show a causal bidirectional link between money market volatility and sovereign bond yield volatility. However, the causal link from sovereign yield volatility to inflation policy is shown to be much weaker. Our work is distinguished by the fact that it is concerned with the decomposition of total volatility persistence based on bear and bull market phases. Our results further support the existence of weak volatility persistence and rapid yield reversion to mean in the bear market except in the short-term. We conclude by proposing that while portfolio managers and investors consider sovereign bond yield movements, they must also be aware that their volatility is asymmetric. For portfolio managers, such phenomena offer an extra tool for positioning adjustments.

The paper is organized as follows. In section 1, we review previous studies on sovereign bond yields and their volatility modelling. In Section 2, we present a description of the empirical methods. Data and preliminary analysis are shown in Section 3. The empirical analysis discussion in Section 4 adds significance to the findings obtained from the empirical research. The concluding remarks and research directions are provided in the final section.

2. Literature review

There is a considerable body of literature on government bond yields, including the factors influencing government bond yields in emerging countries like India. It must, however, be acknowledged that the inconclusive evidence concerning the volatility of sovereign bond yields remains unresolved (Bevilaqua et al., Citation2020). As a result, we discuss how relevant recent papers on government bond yields are to the subject matter of this article by reviewing some recent papers on government bond yields.

2.1. The sovereign bond market and their yield volatility

In the opinion of (Alesina et al. Citation1992) sovereign yields are likely to remain stable for a considerable period of time since the likelihood of default on government securities is extremely low. However, understanding the volatility of sovereign bond yields across maturities, according to (Christoffersen and Diebold Citation2000) is critical in both financial and macroeconomic terms (Hong, Citation2003). Shows that domestic factors and financial market conditions jointly contribute to sovereign yield volatility.

The global financial markets have been increasingly volatile since the 2008 financial crisis (Hong, Citation2003). On their part (Ledwani et al.) show that the recent financial crises have caused severe global repercussions, and an impact has been felt across key financial time series. In light of these facts, it is evident that the sovereign debt market is not independent of the rest of the financial markets (Silvapulle et al., Citation2016). On the first level, following the bankruptcy of Lehman Brothers in late 2008, there appeared to be signs of a sovereign debt crisis, which morphed into a global credit crunch that led to the bankruptcy of many companies (Lane, Citation2012). On the second level, COVID-19, a health pandemic, inflicted the sovereign bond market in unprecedented ways (Paule-Vianez et al., Citation2021). Along with the pause in economic activities, the panic, fear, and uncertainty adversely impacted sovereign yields, discernible in the nosedive of the major global bond markets. The world has experienced epidemics and pandemics like SARS, EBOLA, and MERS before COVID-19, but COVID-19 affected sovereign bond markets in the most hazardous way, both in intensity and scale (Rout & Mallick, Citation2022).

Traces from the extant literature indicates that policymakers must understand the broader implications of sovereign yield movements to prevent the issue from spreading further. As a result (Samitas and Tsakalos Citation2013), (Philippas and Siriopoulos Citation2013), (Reboredo and Ugolini Citation2015), (Reboredo and Ugolini Citation2015) and (Engle et al. Citation2013) among others, have recently contributed to this key topic. In this context (Metiu Citation2012) posits that both global and country-specific variables influence daily yield changes (Abiad et al. Citation2009), (Broner and Ventura Citation2011) and (Bolton and Jeanne Citation2011) on the other hand, describe the interconnection of a sovereign bond market to global financial sectors.

The price volatility of a risky asset is closely connected to how its benchmark evolves. In this regard, it is critical to accurately model the randomness of sovereign yields (Bevilaqua et al., Citation2020; Lithin et al., Citation2021). The observation of the empirical series of returns (yields) is undoubtedly the preliminary stage of a good modelling exercise (Aliyev et al., Citation2020b). Several researchers have proposed that time series of asset returns or yields exhibit very peculiar properties, resulting in the presence of volatility clustering, leverage effect, and long-term memory property (see, for instance (Chundakkadan & Sasidharan, Citation2019; W. Kim et al., Citation2020). The “anti-leverage effect,” which is recognized in the extant research, has been theoretically documented by (Nelson, Citation1991) and (Glosten, Jagannathan, & Runkle, Citation1993). Over time, various studies have shown the significance of the “leverage” and “anti-leverage effect” (Ghysels et al., Citation2005; Harrison & Zhang, Citation1999; Ludvigson & Ng, Citation2007).

Scholarly studies typically analyze leverage using the debt-to-equity ratio and observe the impact of negative and positive shocks on volatility, defining a leverage effect as a scenario in which a negative shock leads to greater volatility than an equivalent positive shock (Aliyev et al., Citation2020b; Bhatia & Gupta, Citation2020; Black & Cox, Citation1976; Wang et al., Citation2022). Recent research examining sovereign debt-to-GDP ratios focuses on the volatility of sovereign yields (Bauer & Granziera, Citation2016; Pintus & Suda, Citation2013; Sun, Citation2018), and while literature has documented a leverage effect in equity returns resulting from negative shocks, it is important to note that positive shocks can also lead to leverage when examining yields rather than returns. Specifically, as the price of a sovereign bond rises, its sovereign debt-to-GDP ratio increases, leading to greater volatility, while a lower bond price results in a higher bond yield, causing a decrease in the leverage ratio and an anti-leverage effect. Therefore, it is possible that the leverage effect measured while modeling yield may not be the same as the one measured using returns, owing to the inverse relationship between yield and price (Fabozzi, Citation2021).

Nevertheless, despite the enormous progress of the literature on sovereign securities in recent years, there is a lack of evidence on the volatility of sovereign yield dynamics of the sovereign bond market. In this paper, we decompose the volatility persistence across different maturity spectrums as suggested by (Balduzzi et al., Citation2001). Based on the theoretical and empirical studies discussed above, our hypotheses concerning the volatility of sovereign yield are:

H1:

There are substantial differences in the sovereign yield volatility persistence across maturity spectrums.

H2:

A positive shock is expected to increase sovereign yield volatility more than a negative shock of the same magnitude.

2.2. Volatility persistence in bull and bear market phases

Several recent papers have examined the impact of financial market volatility on the real economy theoretically and empirically (See, for example (Basu & Bundick, Citation2017; Berger et al., Citation2020; Bloom et al., Citation2014; Gourio, Citation2013; Leduc & Liu, Citation2016). There is a large body of literature that focuses on total volatility. Nevertheless, financial market volatility shows potential differences between bull and bear market phases, with a considerable mean-reverting component (Al-Hajieh, Citation2017; Arsalan et al., Citation2022; Chaves & Viswanathan, Citation2016; Sharma et al., Citation2021).

Recent studies show that bull markets last longer than bear markets because bull markets are associated with periods of generally rising prices, while bear markets are linked to periods of generally falling prices (Gil-Alana & Yaya, Citation2014; Lunde & Timmermann, Citation2004; Pagan & Sossounov, Citation2003). The market index, according to (Wiggins Citation1992) has a critical threshold value that differentiates “up” (bull) markets from “down” (bear) markets (Silvapulle & Granger, Citation2001). divide the market into bearish and bullish periods. In Indian bull and bear markets, it is therefore of interest to determine how long sovereign bond yield volatility persists before reverting to mean. Thus, we hypotheses that,

H3:

Volatility persistence is substantially longer when the market is in a bear state than when it is in a bull state.

2.3. Symmetric and asymmetric GARCH-type models

In financial econometrics, the time-varying volatility of stock returns has garnered the attention of several academicians and researchers. The Researchers have examined volatility characteristics using several econometric models; nevertheless, no model is found to be superior to others. Previous studies emphasize the significance of the GARCH model and its variants in modeling and predicting the volatility of a stock’s returns as it is cut above the ARCH model (Alberg et al., Citation2008; J. -C. Liu, Citation2009). However, the GARCH model evolved following the ground-breaking work of (Engle Citation1982) who proposed a model to measure the varying conditional variance with Auto-Regressive Conditional Variance. The subsequent empirical findings demanded a superior ARCH model to capture the dynamic behaviour of conditional variance. Accordingly (Bollerslev Citation1986) suggested a model superior to the ARCH model as it assumed the number of expected parameters to be two, and he named it the Generalized ARCH model. However, despite the fact that both models could be employed to measure volatility clustering, they failed to capture the effect of positive and negative shocks. Subsequently, the standard GARCH model was evolved into several asymmetric GARCH-type models, including the GJR-GARCH model by (Glosten, Jagannathan, and Runkle Citation1993) and the Exponential GARCH (EGARCH) model by (Nelson) and so on, to estimate the conditional variance regardless of the skewness of the return series (Gokcan, Citation2000). Therefore, another key issue in this area is choosing the most effective GARCH specification to model sovereign yield volatility in India. Thus, our next hypothesis becomes:

H4:

All the GARCH models are equally effective in modelling India’s sovereign yield volatility.

2.4. Macroeconomic fundamentals and volatility

Several studies have sought to explain the relationship between macro variables and various types of bonds. Nonetheless, there is no consensus on what factors impact government bond yields. Existing research suggests that the inflation rate influences the yield on government securities (Gruber & Kamin, Citation2012; Hautsch & Ou, Citation2012; Jaramillo & Weber, Citation2013; Poghosyan, Citation2014).

According to (Paisarn Citation2012) the rate of inflation significantly impacts the yield on government securities (Siahaan & Panahatan, Citation2020). showed similar results after analyzing bonds with similar characteristics. Accordingly (Kurniasih and Restika Citation2015) demonstrate the close relationship between inflation and bond yields. However, the opposite result was reached by (Permanasari and Kurniasih Citation2021) reporting that inflation does not affect sovereign yields.

In light of this (Baldacci and Kumar Citation2010) propose that inflation expectations may cause government bond yields to rise, particularly when output deviations are positive or there are worries about the monetization of debt. Investors want to be compensated for the growing prices, which is why this occurs. The inflation and interest rate expectations of a nation are, nevertheless, indicated by the yields on government bonds. Higher rates are required from newer debt issuances during periods of extreme inflation. Therefore, a reverse effect is also possible. Accounting for these facts, we suppose the following hypotheses:

H5:

The inflation rate granger causes yield volatility of Indian sovereign securities.

H6:

The yield volatility of Indian sovereign securities granger causes inflation rate.

A similar claim can be made for money market volatility to the extent that it, too, contributes to the level of yields. Money market volatility can cause bond yield volatility, but the reverse is also possible (Borio & McCauley, Citation1996). According to (Akram & Das, Citation2015a, Citation2015b), changes in interest rates are key predictors of variations in sovereign yields in India. Whereas (Akram and Das) showed similar results for long-term sovereign securities. For emerging countries (Kurniasih and Restika Citation2015) found that short-term interest rates have a favourable influence since rising interest rates cause bond prices to fall and bond yield volatility to rise. Besides (Chakraborty Citation2012) and (Vinod and Chakraborty Citation2014) among others, report similar results. Therefore, our next hypotheses based on the above discussion are:

H7:

The money market volatility granger causes yield volatility of Indian sovereign securities.

H8:

The yield volatility of Indian sovereign securities granger causes money market volatility.

3. Empirical methods

Financial time series may exhibit asymmetries. The Moving average (MA) and autoregressive (AR) models assume that constant conditional variances cannot gauge the nonlinear dynamics due to the frequent volatility of financial market data. In financial time series, linear models cannot explain characteristics like leverage effects, volatility clustering, long memory, and leptokurtosis (Zivot, Citation2009). More multifaceted approaches are necessary since linear models are constrained in their flexibility and ability to explain such nonlinear phenomena. In order to depict nonlinear patterns as non-constant volatility, financial time series may exhibit asymmetries. This motivates applying more multifaceted approaches to explain such nonlinear phenomena in the time series data. Moreover, the changing conditional variance has garnered the attention of several researchers, particularly in econometric models (Benlagha & Chargui, Citation2016). Thus, the present study using a battery of GARCH specifications explores the asymmetric behaviour of the Indian sovereign bond yields across the maturity spectrum.

Prediction and modelling of conditional volatility have become standard practices using GARCH models (Benlagha & Chargui, Citation2016). Therefore, the most popular univariate conditional volatility models are used in the current study. Some of the widely used extensions are GARCH, EGARCH, GJR GARCH, and IGARCH (So & Yu, Citation2006). These models allow for the risk premium to be affected by the changing conditional variance directly (J. Liu & Serletis, Citation2019). Volatility can be estimated and forecasted using these models. Furthermore, they can be used to capture asymmetry, the difference in the impact of positive and negative effects of equal magnitude on conditional volatility, and leverage, which is a negative correlation between returns shocks and subsequent volatility shocks.

3.1. GARCH (standard GARCH model)

(Bollerslev, Citation1986) suggested a model that can capture the propensity for volatility clustering in financial time series. In particular, the model allows a long memory volatility process with flexible lag order. Additionally, the model can capture the time-varying volatility since it considers the conditional variance as a GARCH process to capture such volatility in the financial time series. A simplistic GARCH model’s expression for the variance is as follows:

In the equation, the conditional variance is assumed to be , the return residual is assumed to be,

, and the parameters

,

, and

are to be estimated. The model variance requires non-negative values of

,

, and

parameters, and the model is considered to be valid if

+

is less than 1, as the value above one implies that the volatility patterns are non-stationary (So & Yu, Citation2006). The higher values of the

coefficient indicates that market shocks will persist for a longer duration, whereas larger values of the

coefficient shows a stronger sensitivity of volatility to market shocks.

The simplest and most popular model, GARCH (1,1), may be stated as follows:

Mean equation

Variance equation

with ,

, and

being positive.

The asset’s return at time t is represented by , the average return by μ, and the residual return by

. Since

the variance at time t is contingent on information from time t-1, known as a conditional variance. In the conditional variance equation,

is a constant term, along with

(ARCH term), which is the lag of the residuals squared, and the variance

(GARCH term). In the model, the ARCH and GARCH terms demonstrate that the conditional variance at time t is the function of both the volatility-related news and conditional variance from the previous period. Thus, the GARCH (1,1) model is evident in most prior studies that attempted to measure and forecast the volatility in financial time series data (So & Yu, Citation2006).

3.2. Asymmetric GARCH models

In conventional GARCH models, positive and negative error terms are considered to have a symmetric influence on volatility. However, due to a number of factors, including transaction costs, arbitrage restrictions, market frictions, and others, financial time series generally show asymmetrical nonlinear patterns (Aliyev et al., Citation2020a). This suggests that “bad news” or adverse shocks may have a long-lasting impact on conditional volatility than “good news” or positive shocks of a similar magnitude and is termed as “leverage effect.” The standard GARCH model fails to account for this leverage impact. This necessitates the usage of asymmetric GARCH family models such as EGARCH and GJR-GARCH models.

3.3. EGARCH

Nelson’s Exponential GARCH (EGARCH) model being an asymmetric GARCH model, explains the asymmetrical influence of news (Nelson, Citation1991). This model allows for asymmetric conditional variance response to shocks, and the conditional variance in the model may be stated in logarithm form as:

Mean equation

Variance equation )

The leverage effects, which are responsible for the model’s asymmetry, are represented by γ and is the predominant advantage of this model. The suggests that positive shocks (good news) cause more volatility than negative shocks (bad news), wherein,

indicates that negative shocks are more disruptive than positive shocks when modelling returns (Aliyev et al., Citation2020b). Further, the model is said to be symmetric when

. However,

can be negative, as the model removes the restriction on the conditional variance to be non-negative, and other parameters have no sign restrictions (Benlagha & Chargui, Citation2017).

3.4. GJR-GARCH

The GJR-GARCH model, which considers asymmetries, was proposed by (Glosten, Jagannathan, & Runkle, Citation1993). The model, which allows the conditional variance to respond differently to previous positive and negative shocks, is a straightforward expansion of the conventional GARCH model. The model’s conditional variance may be expressed as follows:

is a dummy variable that is assigned 1 if

and 0 if

. The coefficients

and

represent the leverage effect and asymmetric shocks, respectively.

,

,

and

+

are the conditions for nonnegativity (Brooks, Citation2008, p. 405).

3.5. IGARCH

An additional restriction imposed by (Engle and Bollerslev Citation1986) is . This means that the usual GARCH model supports the characteristic of persistent conditional variance over all finite horizons. Combining the conditional variance

in a standard GARCH model with the abovementioned restriction (Engle and Bollerslev Citation1986) developed the Integrated GARCH (1,1) or IGARCH model. The model can be written as follows:

In the IGARCH model if , then the residuals are covariance stationary. As the sum of ARCH term (

and Beta term (

approaches close to one, the greater the persistence of shocks to volatility. However, their sum is more than unity accounts for non-stationary in the conditional variance (Choudhry, Citation1995).

4. Data and preliminary analysis

To measure the volatility in Indian Sovereign Bonds, we use daily bond yield data from 1 January 2016, to 18 May 2022, for four different maturities: the 3-month treasury yield, 2-year sovereign bond yield, 10-year sovereign bond yield, and 24-year sovereign bond yield. The Sovereign bond yield data were sourced from Investing.com. Besides, the Inflation and Money market rate data were collected from FRED (Federal Reserve Economic Data).

In order to determine the shape of any yield curve, two critical elements must be considered: level and slope. The yield curve’s slope is a gauge of the economy’s overall interest rate environment. Short-term interest rates are represented by the 3-month treasury yield (Short-term interest rate). On the other hand, a substitute for the yield curve’s slope is the difference between the yield on a 10-year bond and the yield on a 2-year bond (Slope of the yield curve). The yield curve’s slope is a reflection of what the market believes the long-term economic outlook would be. Therefore, the volatility of yield curve components with an emphasis on the 3-month treasury yield, 2-year sovereign bond yield, and 10-year sovereign bond yield should therefore be examined to match the empirically weak link between the level and slope of the yield curve. Volatility, however, is dynamic and alters significantly over time. Although it goes through high and low phases, it also has a long-term mean to which it reverts. As a result, the 24-year benchmark sovereign bond yield series was also found preferable to use in the study since, in addition, volatility tends to rise as a market experiences a significant decrease over the long run. Hence, 24-year sovereign bonds are used to characterize the yield curve’s long-term behaviour. Considering these factors, the data are broken down into three categories: short-term (3-month treasury yield), medium-term (2-year and 10-year sovereign bond yield), and long-term (24-year sovereign bond yield). This gives us 1593 observations for each series.

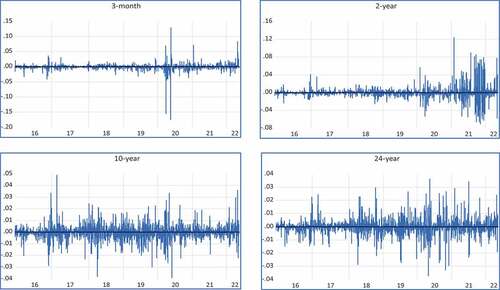

Table presents a descriptive summary of the Indian benchmark sovereign bonds. Referring to the findings, the average yield for sovereign bonds is 5.3% for the 3-month treasury, 6% for the 2-year sovereign bond, 6.8% for the 10-year sovereign bond, and 7.4% for the 24-year sovereign bond. The data clearly show that the mean yield rises with maturity. This is so because a bond owned for a longer period may pose a higher risk to investors. When a yield curve with an upward slope is comparatively flat, the difference between short- and long-term bonds’ yield is minimal. Figure plots the pattern of Sovereign bond yield series graphs at first difference. It is important to note that the degree of standard deviation for a short-term sovereign bond is significantly high, indicating that short-term sovereign bonds are more prone to economic conditions and expectations. This is not the case with long-term yields, as fluctuations can be easily evened out with time. The 3-month treasury has the highest standard deviation of 1.4%, followed by a 2-year sovereign bond with a standard deviation of 1.1%, a 10-year sovereign bond with a standard deviation of 0.6%, and a 24-year bond with the least standard deviation of 0.5%.

Figure 1. Sovereign bond yield series graphs at first difference.

Table 1. Descriptive statistics (across maturities)

In contrast, (O’sullivan & Papavassiliou, Citation2019) find that volatility increases as maturity buckets increase from shorter to longer. However, their study also revealed that this result is more pronounced during quiet periods. They demonstrate a sharp increase in standard deviation as they move from a calm period into a turbulent one. This indicates that the recent outbreak of the COVID-19 pandemic has pushed uncertainty into the financial market, and this uncertainty has wobbled unprecedented movement in the bond market volatility (Zaremba et al., Citation2021). Therefore, 3-month treasury and 2-year sovereign bond yields are subject to higher fluctuation levels during the study period since economic activities can directly and immediately impact these rates. In other words, bonds with very long maturities (so-called buy-and-hold bonds) appear to have lower standard deviations because the selling pressure is not as high as bonds with shorter maturities (Friewald et al., Citation2012). found similar results during the subprime crisis. They found that bonds with shorter maturities were more vulnerable to the crisis than those with longer maturities. The standard deviation values increased from the pre-crisis period to the crisis period, indicating greater volatility. This effect, however, is more apparent during times of crises.

Moreover, the summary statistics show that the non-positively skewed distribution of the yield series is likely to deliver significant negative returns to investors and is more prone to volatility. The high kurtosis ratios show the fatter-tailed distributions of the sovereign bond yield series, which are leptokurtic. In a leptokurtic distribution, outliers are likely to occur, and as a result, distribution tends to be non-normal.

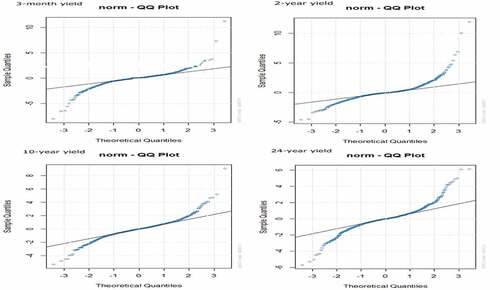

Further, Jarque-Bera test results show t-statistic values of 188.6329 for 3-month treasury yield, 121.0368 for 2-year bond yield, 102.1540 for 10-year bond yield, and 73.56480 for 24-year bond yield with a significant p-value, allowing us to reject the null hypothesis, i.e., distribution follows a normal distribution. As a further instrument to analyze the distributional properties, we use Quantile-Quantile (QQ) graph to check if bond yield series data differ from normality. The QQ plot is a scatter plot that shows the empirical and theoretical quantiles for a given distribution (Alexander, Citation2001). The results of the QQ plot presented in Figure show the deviation of residuals from the normality line. The greater the deviation from the line, the greater the chance to reject the null hypothesis of the normality assumption. Thus, the graphical representation confirms the findings of the Jarque-Bera test, i.e., Indian Sovereign bond yield data are not normal. These findings support the decision to use an alternate distribution, such as students-t and GED-based GARCH models.

Figure 2. QQ plots of the EGARCH residuals.

This article further contributes to the body of knowledge by examining selected macro-related forces driving the volatility of bond yields. Therefore, Table presents the key descriptive statistics for inflation and Money market volatility in the study at the quarterly frequency. The mean inflation rate reported for the sample period is 4.7514%, with a standard deviation of 1.1598%, implying moderate volatility. Further, the money market rate proxied by the 3-month LIBOR shows an average rate of 1.3616% with a standard deviation of 0.9806%. The descriptive statistics also show evidence for the data normality. It is important to note that a prerequisite for performing the Granger Causality test is that the data need to be normal.

Table 2. Descriptive statistics (macro-economic indicators and sovereign yields at quarterly frequency)

Furthermore, the descriptive statistics for yields across maturities at a quarterly frequency are presented in Table , indicating that the mean and standard deviation exhibit little variation from those reported for daily data; nevertheless, it should be highlighted that while the daily series show non-normal characteristics, the quarterly yield data conform to a normal distribution. Consequently, the linkage between the above macroeconomic determinants and sovereign yield across the maturity spectrum is examined in the study.

Table displays unit root tests performed for each series of Indian sovereign bonds. The Augmented-Dickey Fuller (ADF) and Phillips-Perron (PP) tests were used at a 5% level to examine the stationarity of sovereign bonds of different maturities used in the study. The results of unit root tests show that the calculated values of ADF and PP test statistics are less than the critical value at 5%, implying that all the series are stationarity. Further, the results of the unit root in Table suggest that our data do not meet the stationarity requirements for Granger causality testing. Therefore, original data are transformed using the first differences prior to testing. The results conform to prior expectations, and the coefficients are significant at a 5% level of significance, indicating stationarity for the GDP and 3-month LIBOR series.Footnote3

Table 3. Unit root test results

Table 4. Unit root test results for macroeconomic variables

Following the unit root test, we applied the Lagrange multiplier (LM) test to check for the presence of the ARCH effect in our data set. The reported results in Table show the prevalence of the ARCH effect in all yield series. Thus, to assess the conditional volatilities of the Indian sovereign bond yield over four distinct maturities, GARCH family models (standard GARCH, IGARCH, EGARCH, and GJR-GARCH) are applied.

Table 5. ARCH LM test results

5. Empirical analysis and discussion

5.1. Model selection, volatility persistence, and leverage

5.1.1. Preliminary analysis and model selection

As reported, data in Table provides strong evidence against the null hypothesis, i.e., data are homoscedastic; we conclude that the government bond yield series shows heteroscedasticity, or the presence of the ARCH effect is confirmed. Thus, to model this conditional variance, we proceed with the GARCH family models. Further, we estimate models based on the maximum likelihood approach under the assumption of GED (Since AIC and BIC values under GED are lower over the student’s t distribution). The GARCH (1,1) model results with GED and Student’s t distribution are reported in the Appendices (2, 3, 4, and 5). The GARCH model shows that the ARCH term and GARCH term are statistically significant across maturities. This implies that the conditional variance of the bond yield series is significantly impacted by the lagged conditional variance and squared disturbances, implying that volatility news of previous time periods impacts the current days’ volatility. Further, the sum of α and β coefficients across four maturities is less than unity, implying the validity of the GARCH (1,1) model. However, symmetric GARCH models cannot differentiate the impact of the “leverage effect” on the conditional variance of bond yield data. Hence, we further proceed by applying popular asymmetric-type GARCH models to measure the impact of positive and negative shocks. The results of asymmetric GARCH models are presented in the Appendix. We have applied the maximum likelihood approach to choose the best model that fits our data set (Maximum likelihood value, refer to Appendix). The EGARCH model is the best model across 3-month, 2-year, 10-year, and 24-year sovereign series.

5.1.2. Empirical analysis on GARCH (1,1), IGARCH and GJR-GARCH

The dynamics of the volatility of sovereign yields and their persistence across maturity buckets are examined using GARCH (1,1), IGARCH, and GJR-GARCH.Footnote4 The results of the GARCH (1,1) model show that all the coefficients are highly significant (Refer to appendix 2, 3, 4, and 5). The stated α measures how much a volatility shock of the current day affects volatility in the following period (Campbell et al., Citation1997). The coefficients of the 3-month, 2-year, 10-year, and 24-year sovereign series are 0.084712, 0.104348, 0.119837, and 0.083868, demonstrating the presence of volatility clustering. However, the coefficients for IGARCH and GJR-GARCH show comparable results. For identical maturity periods, the coefficients for IGARCH are 0.06464, 0.105391, 0.120626, and 0.167508, whereas the coefficients for GJR-GARCH are 0.052954, 0.054199, 0.126086, and 0.149875. The coefficient has been significant for the series, demonstrating that historical lags cannot affect future volatility. However, the negative estimate on the “alpha” component indicates that adverse shocks provide lower next-period conditional variance than positive shocks of the same sign (Brooks, Citation2019).

The β coefficient estimate implies that the variance has a long memory. However, the GARCH term is statistically significant for each maturity spectrum across different GARCH specifications employed in the current study. For 3-month, 2-year, 10-year, and 24-year sovereign series, the estimated GARCH coefficients for GARCH (1,1) are 0.897382, 0.89454, 0.879163, and 0.910881, suggesting that changes in current volatility have a long-term impact on future volatility. Furthermore, the β coefficients for IGARCH and GJR-GARCH are approximately comparable to the GARCH (1,1) and EGARCH results. For 3-month, 2-year, 10-year, and 24-year sovereign series, the IGARCH coefficients are 0.93536, 0.894609, 0.879374, and 0.802731, respectively. Besides, the coefficients for GJR-GARCH for the same maturity frame are 0.890587, 0.911427, 0.880148, and 0.800982, indicating that volatility shocks are quite persistent. Nevertheless, the results support the growing body of literature documenting that shocks are not immediately absorbed.

Moreover, the results of the GJR-GARCH model, an alternative to the EGARCH model, are in accordance with EGARCH results, particularly for the measurement of asymmetric volatility. The reported results show that the leverage coefficient γ (gamma) is significant and positive across all the maturities, implying that the positive shocks create higher volatility than the negative ones.

5.1.3. Volatility persistence and asymmetry based on EGARCH results

Based on the AIC and BIC values (lowest value), the EGARCH model with GED is considered in the study (Refer to Table ). However, the Log-Likelihood is maximum under Student’s t for the 10-year bond. It is also important to note that their performance is almost identical due to the negligible difference in the AIC and BIC values between GED and Student’s t. Moreover, the EGARCH is often the superior model for predicting volatility in a single phase.

Table 6. EGARCH results

Table 7. Distribution selection under EGARCH

The EGARCH model results are shown in Table for the yields series on 3-month, 2-year, 10-year, and 24-year treasury securities (Columns 3, 4, 5, and 6). The adoption of the asymmetric volatility model is supported by the fact that the leverage coefficient γ for each type of government security is statistically significant at the 1% level. In the model, the stated α measures how much a volatility shock today affects volatility in the following period (Campbell et al., Citation1997). The α coefficients for our series of sovereign yields, which include 3-month, 2-year, 10-year, and 24-year, are −0.26038, −0.016005, 0.003112, and −0.01833, respectively. The coefficient is statistically significant for the 3-month benchmark yield while insignificant for other sovereign bond yields across maturities, demonstrating that historical lags can affect future volatility only in the near term. However, the negative estimate on the “alpha” component indicates that negative shocks provide lower next-period conditional variance than positive shocks of the same size (Brooks, Citation2019).

The estimation of the β coefficient indicates a long memory in the variance. The correlation structure of a specific series at long lags is referred to as having a “long memory.” Distance observations have persistent temporal dependency if a series demonstrates long memory. The potential for long-term dependence on sovereign yield significantly impacts the financial time series. The long-memory quality of financial time series has been studied in the existing literature. Security returns, for instance, exhibit a positive correlation over short time horizons and a negative correlation over long time horizons, according to Poterba (Poterba & Summers, Citation1988). As the holding period increases, the negative serial correlation between sovereign yields becomes more pronounced. This result is implied by the mean-reverting model’s long-term memory property. According to (Lo Citation1991) long-horizon yields may be characterized by long cycles and potentially predictable components.

The GARCH term (β) is statistically significant for sovereign yield series across maturity buckets considered in the study. The estimated coefficients are 0.90361, 0.988233, 0.975297, and 0.948029 for the 3-month, 2-year, 10-year, and 24-year series, respectively. Further, the coefficients are close to unity, implying that changes in the current volatility will have a long-term impact on the future volatility or that the impact of previous news on the current volatility is long-lasting. Besides, a high long-memory coefficient shows that the asset exhibits a long positive or negative stray from equilibrium. As a result of its inability to effectively protect investors from volatile market conditions, such security is no longer considered a good hedge or safe haven.

Moreover, long memory qualities and asymmetric impacts are stylized facts likely to result in significant financial outcomes. A time series is regarded as having long memory and asymmetric behaviour when its corresponding autocorrelation function is non-integrable. In reality, the fundamental result of long memory is its nonlinear dependence during the first and second moments (Elder & Serletis, Citation2008). The results, however, confirm that shocks to sovereign yields may take longer to dissipate, but they are not permanent. If a shock to a given system is lasting, volatility is highly persistent, and the behaviour of volatility in the past can be utilized to forecast future volatility. However, normal times with relatively stable pricing may be followed by periods with significant volatility. Because information decays slowly in such markets, old information is more important than new knowledge. This is evidence of so-called long memory behaviour. In view of the financial implications of these coefficients, investors can construct future positions in anticipation of this feature. In contrast, low volatility persistence suggests that the shock response function could decay quickly. Low persistence equates to rapid decay and quick reversion to the mean.

5.1.4. EGARCH asymmetry, leverage, and shocks

The result for the EGARCH asymmetry term (γ) shows a positive coefficient for different maturities considered in the study. According to the EGARCH results reported in Table , positive shocks/news cause more volatility in the subsequent period than negative return shocks or news of the same size. For each bond across all maturities, γ is positive and statistically significant at the 0.01 level. Further, γ the leverage coefficient is as high as 0.81360 for the 3-month treasury, 0.257037 for the 2-year bond, 0.210311 for the 10-year bond, and 0.30120 for the 24-year bond.

The leverage effect refers to the well-established negative relationship between return and future volatility. The relation is usually explained by the increased leverage ratio that arises from a drop in the share price for a firm. As the price of a stock falls, its debt-to-equity ratio rises, increasing the volatility of returns to equity holders (Black & Cox, Citation1976). A stylized characteristic of financial volatility is that negative shocks (bad news) influence volatility more than positive shocks (good news), where the focus is on equity returns (Aliyev et al., Citation2020b; Bhatia & Gupta, Citation2020; Wang et al., Citation2022).

However, in this paper, we concentrate on sovereign bond yields. This contradicts the assumption of the Black and Scholes model, where the focus is on the corporate debt-to-equity ratio (Black & Cox, Citation1976; Black & Scholes, Citation1973). This article defines leverage as the ratio of sovereign debt-to-GDP (Bauer & Granziera, Citation2016; Pintus & Suda, Citation2013; Sun, Citation2018). In the context of sovereign bonds, a decrease in yield increases the expected future volatility. A lower yield is often perceived as an indicator of higher risk and lower income. However, a low yield may have resulted from a rising market value of the sovereign bond, which increases the total sovereign debt and leads to the leverage effect (i.e., a higher sovereign debt-to-GDP ratio). Therefore, a positive shock leads to increasing sovereign bond prices and induces, by statistical definition, a lower yield.

According to (Cecchetti and Zampolli Citation2011) low and moderate levels of debt help promote welfare and economic growth, whereas high levels can be a disaster. The study suggests that a lower debt-to-GDP ratio can reduce the likelihood of a financial crisis, indicating a threshold effect of debt. When the debt level exceeds the threshold value, it has negative impacts on GDP and raises leverage, ultimately leading to a more disturbed economy. While the attention of policymakers following the recent crisis has been on reducing systemic risk stemming from a highly leveraged financial system, the system demands less leveraged and ultimately less risky economies.

Our findings are the exact opposite of what one would expect when applying a GARCH model to a set of stock returns. The impact of positive shocks is recognized in the extant research as the “anti-leverage” effect, as theoretically documented by (Nelson, Citation1991) and (Glosten, Jagannathan, & Runkle, Citation1993). Over time, various studies have shown the significance of such an effect on the relationship between corporate bonds and equity (Ghysels et al., Citation2005; Harrison & Zhang, Citation1999; Ludvigson & Ng, Citation2007). However, this paper uses yields rather than returns, and a price rise is associated with a yield fall (Fabozzi, Citation2021), which leads to “regular leverage”. In summary, our findings suggest that a positive policy shock elicits greater volatility in sovereign yields relative to negative shocks of equivalent magnitude.

According to our findings in this section, the amount of persistence differs across the type of sovereign yield series, with medium-term and long-term possessing more persistence than short-term series. Besides, the type of GARCH model employed is a critical choice in modelling conditional volatility. The EGARCH model with GED (3-month, 2-year, and 24-year) and Student’s t (10-year) was found to be the best-fit model to the yield data as it exhibits lower forecast errors and provides a better description for the conditional volatility. Overall, investors should be aware that the volatility of the Indian sovereign yield is more sensitive to good news across the maturity spectrum to cover potential losses. However, it is important to examine the properties of the yield in both bull and bear periods to better understand how it behaves in different market conditions. Therefore, we examine the properties in the bull and bear periods, testing if the degree of persistence is different in these periods in our series in the next section.

5.2. Volatility persistence and mean-reversion: Comparison between bull and bear markets

This section deals with the analysis of volatility persistence in the bull and bear phases of the Indian sovereign yield series across different maturity specifications. Since the COVID-19 pandemic, the globe has recently seen one of its worst bear markets, making it especially important to academic research. We assume that there are bull and bear market phases and that each market phase is a regime that is influenced by particular market forces. These market forces produce negative news, which causes panic and prompts investors to sell off bonds quickly. When there is no more bad news, markets bounce back. However, investors retain bonds during bull markets when a string of good news generates optimism, while they sell bonds during bear markets due to pessimism.

This sample period selected for the study saw a significant surge and a sharp decline in the market as COVID-19 unfolded. It provides a perfect context to investigate whether the relationship differs in bull and bear markets. We divide the sample period into bull and bear phases using the methods proposed by (Conlon et al. Citation2021) and (Conlon & McGee, Citation2020). Accordingly, the bull market lasted from 1st April 2016 to 10th March 2020, while the bear market lasted from 11 March 2020 to 18 May 2022. This isolates the impact of the COVID-19 pandemic and captures the bear market.Footnote5 In line with (Rahman and Lee Citation2002) our findings show that the EGARCH (1,1) model best captures volatility with GED distribution over maturities for both phases.

For the purpose of modelling financial time series, the study of persistence and half-life is pivotal. They aid in figuring out how long it takes to return to the mean and whether the estimated GARCH model is stable. A model that gauges the average time (also known as the mean reversion speed) of the yields under investigation is the half-life volatility of the EGARCH model. Therefore, we quantify the days in which yields revert to the mean in accordance with (Bhar and Nikolova Citation2009), Fakhfekh et al. Citation2016) and (Jane & Ding, Citation2009). The volatility of the half-life can be expressed as

However, the sovereign yield series shows evidence of long-memory behaviour during the bull market, as reported in Table . The results show that volatility persistence in bull phases is longer in general throughout the reference period. Gains during market expansions outnumber losses during market cycles’ bear phases. This study shows that when news enters the market during a bullish period, investors in Indian government bonds do not react to new information until a market trend is well established. As a result, a large amount of information is gathered and unexpectedly established in the market, causing volatility in sovereign yields across maturities.

Table 8. EGARCH results during pre-COVID-19

The findings of our half-life approach calculation of mean reversion speed are reported in Table . The findings show that the 10-year government bond yield has the highest coefficient (0.984466); as a result, it takes the longest period (44.2738 days) to return to half of its mean among all maturities during a bull market. The 3-month Treasury yield, in comparison, has the lowest value of 0.864455 because it takes the least amount of time (4.7588 days) to return to half of its mean when compared to other maturities during a bullish phase. However, the yields on sovereign bonds with a 2-year and 24-year maturity return to half of their mean in 21.9006 and 29.7157 days, respectively.

This suggests that investors in 10-year sovereign bonds must initiate a position at 0 days and close after 88.5476 days because the yield on 10-year sovereign bonds shows that the yields returned to half their mean value within 44.2738 days. The slowest mean reversion process occurs in the 3-month treasury yield; therefore, investors should start at 0 days and close after 9.5176 days. Thus, compared to the 3-month treasury yield, which offers the least time period for investors to act freely, the 10-year sovereign bond gives them maximum operating leverage.

Based on the results (Table ) for the EGARCH parameters and the trajectory of COVID-19, we discover that yield volatility is more persistent in bull market than in bear market except in 3-month series. Recent literature is consistent with the size of the volatility persistence as shown by for the Indian sovereign bond market (see (Koulakiotis & Molyneux, Citation2006). Intriguingly, during times of stress (a bear market), certain yield series across different maturities, such as the 3-month Treasury yield, 2-year Sovereign Bond yield, 10-Year Sovereign Bond yield, and 24-Year Sovereign Bond yield, tend to have lower levels of volatility persistence (0.914978, 0.951023, 0.965075, and 0.655224, respectively), indicating that they are better able to withstand the shocks to which they are exposed (see (Taing & Worthington, Citation2005; Young & Johnson, Citation2004).

Table 9. EGARCH results during the COVID-19 era

The findings further (Table ) indicate that the mean-reversion process has been proven to exist for each of the four sovereign yield maturities. In contrast to the bullish phase, which exhibits a faster mean reversion rate across similar maturities, the yields on Indian sovereign bonds across maturities indicate moderate volatility and sluggish mean reversion. The 10-year sovereign bond has the lowest mean reversion in days, whereas the 3-month treasury yield has the highest mean reversion in days. The 3-month Treasury yield returns to its mean position in 15.6016 days, according to the half-life calculation, while the 2-year Sovereign Bond Yield does so in 27.606 days. In 38.9962 days, the 10-year sovereign bond yield returns to its mean level, whereas the 24-year sovereign bond yield comes back to its mean value in 3.279 days. Our results are consistent with those of (Ledwani et al., Citation2021), who show that the detrimental effects of COVID-19 had diminished more quickly in the Indian financial markets, supporting the market correction following the panic-induced decline. The market overreaction theory and market correction theory explain the markets’ collapse and quick rebound. The government’s implementation of strong control measures has effectively curtailed the spread of COVID-19 and decreased the volatility of sovereign yields across the maturity buckets. The various fiscal support policies implemented by governments around the world have also played a positive role in curbing sovereign yield fluctuations. Based on the results of the empirical and theoretical analyses in this article, government interventions can effectively reduce the uncertainty and panic caused by COVID-19, and send positive signals to the markets and investors, resulting in faster mean reversion. However, a low level of government intervention and lack of access to other markets contribute to the high volatility and slow mean reversion in emerging economies. The findings are in line with those of (Al-Hajieh, Citation2017; Chaves & Viswanathan, Citation2016; Sharma et al., Citation2021). Through the above contributions, we offer concrete recommendations for the implementation of government policies in the future.

According to Iyiegbuniwe et al., (Citation2012), market booms in developing markets cause greater volatility than market declines, which is justified by the idea that investors think booms act more like speculative bubbles. In contrast to the findings (Nelson Citation1991) claims that volatility is higher in bearish phases because investors are more likely to engage in panic selling during these times. According to the findings, the Indian sovereign bond yields experienced volatility during the pandemic era. However, when comparing the COVID-19 period to the pre-COVID period, we discovered that mean reversion is slower in the pre-COVID-19 period than during the COVID-19 period. In this regard, the outcomes of bull and bear market cycles are states with persistent and statistically significant variations in mean returns.

As we confirm from our well-established volatility analysis, the speed of mean reversion varies with the market phase under study. We find that volatility generally responds more markedly to shocks during the period under stress (a bear market). In contrast, sovereign yield volatility during the bullish phase is highly persistent; when it rises, it remains high for a considerable time and returns to its mean only gradually. These findings suggest that the Indian sovereign bond yield is influenced by a range of economic factors and that its behaviour may change over time. Therefore, we seek to empirically analyse the linkage between the sovereign bond yield volatility and selected macroeconomic determinants in India across maturity spectrum in the next section.

5.3. Macro-related forces and sovereign yield volatility

In this section, we take a first step towards answering a research question of the paper: how do macroeconomic shocks affect sovereign yield volatility across the maturity spectrum? The Granger causality test is widely used in research to identify such a relationship, as stated by (Bui, Citation2018). We test here for Granger causality between interest rate volatility (3-month LIBOR), as well as the inflation, on the one hand, and the sovereign yield volatility (computed either using a 3-month or a 2-year or a 10-year or a 24-year window), on the other hand.Footnote6 The role of this step is to establish, in a bivariate setting, whether the selected macroeconomic variables have predictive power with respect to the sovereign yield volatility across the maturity spectrum and vice-versa.Footnote7

The results for Granger causality are shown in Tables . The non-existence of unit roots justifies the approach as reported in Table for macroeconomic determinants and Appendix 1 for quarterly yield series. This is a common approach to determine whether a particular series is stationary, whether a trend characterizes it, or takes the shape of a stochastic trend or a deterministic or linear trend. The Granger causality test would produce inaccurate results if there were a unit root, which suggests non-stationarity.

Table 10. Granger casualty test for the linkage between sovereign bond yield volatility and inflation

Table 11. Granger casualty test for the linkage between sovereign bond yield volatility and money market volatility

5.3.1. Sovereign bond yield volatility and inflation

Over time, the link between movements in bond yields and fundamental economic forces, such as expectations about inflation, is not as well established as over the long-term or across countries at a point in time. For instance, debate continues about whether the change in the level of yields over the last couple of years is explicable in terms of such fundamentals. In general, the shorter the time horizon, the more likely it is that market participants generate yield movements themselves. The close association between the long-term inflation record and the level of bond yields across countries supports this relationship. At the same time, there is considerable evidence that bond yields play an important role in setting the background level of volatility, pointing to a role for inflation.

The findings of testing for Granger causality are shown in Table . The findings suggest that Granger causality exists for inflation. Across the maturity spectrum, the evidence is robust. In contrast, there is no evidence of Granger causality from sovereign yield volatility to inflation. In these cases, the link is probably disturbed by the sharp but short-lived movements in short-term rates in response to strains in the other macroeconomic determinants.

Our findings align with (Wesso, Citation1998) and (Zhou Citation2021) who investigate the relationship between expected inflation and yield behaviour. According to the analysis, inflationary pressures are not predicted by sovereign yield. However, it has been found that inflation positively and considerably impacts sovereign yields in India. However (Ntshakala and Harris Citation2018) contend that the slope of the yield curve affects expected inflation, rejecting the idea that the term structure determines the direction of inflation.

The findings show that long-term and short-term bond yield volatility is increased by an economy’s inflation history and expectations and that changes in inflation are likely to have the strongest impact on bond yields. Additionally, the inflation rate has an impact on government bond yields because investors consider it as a proxy for uncertainty and instability, which raises risk premiums and, as a result, the level of yields (Baldacci & Kumar, Citation2010; Baldacci et al., Citation2008; Cantor & Packer, Citation1996).

5.3.2. Sovereign bond yield volatility and money market volatility

We next examine the link between money-market volatility and bond yield volatility. Just as one can ask what happens to the bond rate when short-term rates change, so one can trace the movements of the volatility of the bond rate associated with changes in money-market volatility. Volatile money markets create more volatile bond markets. In theory, such money market volatility can be linked to the modus operandi; of monetary policy, but the precise nature of the link remains an important research subject. The precise interpretation of the link between the money market and bond yield volatility will partly depend on the measure of volatility used. In keeping with our emphasis on uncertainty, we employed a forward-looking indicator, a 3-month LIBOR (Bandholz et al., Citation2009). In fact, this rate can be taken as an admittedly rough approximation to market expectations of the money market volatility.

We examine the relationship between sovereign yield volatility and money market volatility in the Indian credit market for government bonds. The test results reported in Table show that there is Granger causation between sovereign yield volatility and money market volatility in general. However, for each series, we found a bidirectional link between these two factors.

Keynes’s claim is supported by a number of recent empirical studies on the dynamics of government bond yields, which show that after adjusting for relevant macroeconomic and financial variables, there is a substantial correlation between interest rates and sovereign yields. These findings are relevant to macroeconomic theory and policy (Akram, Citation2021). These findings support the conclusions of (Akram & Das, Citation2015a, Citation2015b, Citation2019), who state that interest rates play a leading role in driving fluctuations in sovereign bond yields in India. The conclusions are consistent with those obtained in research by (Chakraborty (Citation2012) and (Vinod and Chakraborty Citation2014) despite the fact that the econometric and statistical approaches used are somewhat different. This finding has significant policy concerns. It suggests, for instance, that decisions about money market rates affect yields over the medium- and long-term, in addition to their direct impact on short-term yields. As a result, the key finding that the interest rate is the main factor influencing sovereign bond yields remains true regardless of the maturity parameters.

The results reported in Table also generate predictions about the strength of granger casualty from sovereign yield volatility to money market volatility. In particular, our results reveal strong causation from 3-month sovereign yield volatility to money market volatility. The intuition behind the strong linkage between sovereign yield volatility and money market volatility is straightforward. An information event that alters the sovereign yield volatility directly affects the money market volatility measured using 3-month LIBOR. Since both sovereign yield volatility and money market volatility are strongly correlated, it might seem reasonable to attribute the linkages solely to common information. Stronger linkages occur with higher levels of common information and information spillover. The common information flow should be high between markets with security values driven by similar underlying fundamentals (Fleming et al., Citation1998). However, the results based on time-series estimates of the information suggest that the relationship becomes weaker as the sovereign yield maturity increases.

Our paper concludes that the Indian sovereign yields cannot be dissociated from inflation and money market volatility. Since, in the long-term, inflation performance and expectations are probably the main influence on yields, a similar claim can be made for money market volatility to the extent that it, too, contributes to the volatility of yields. Money market volatility can cause bond yield volatility, and our results show that the reverse is also possible. Each market is influenced by macroeconomic information, and the characteristics of these markets are conducive to cross-market hedging. Therefore, we expect to observe strong volatility linkages. Hence, the link between such fundamental economic factors and their movements cannot be taken for granted. In summary, given the strong linkage between sovereign yield volatility and money market volatility, the common determinants affecting these variables need to be determined in future research. However, it is also worth noting that there may be other macroeconomic determinants that could also have an impact on the Indian sovereign yields, such as GDP growth, exchange rates, and fiscal policy. It is important to consider these other factors as well, as they can provide a complete picture of the market dynamics.

6. Conclusions

In this paper, we model and estimate the volatility of sovereign bond yields across short, medium, and long-term maturities. The findings demonstrate that the yield series on sovereign bonds deviates from normality and exhibits volatility clustering with varying residual variance. Further, the conditional variance of the returns exhibits a nonlinear structure which necessitates the need to use the appropriate models for effectively estimating volatility in the Indian government bond yields. In order to account for the long-memory and asymmetric effects, our research has focused on the GARCH-family models. The EGARCH with GED is the best model fit for the 3-month, 2-year, and 24-year sovereign yield volatility series after applying four GARCH specifications with different related error distributions, including the GARCH (1,1), EGARCH, IGARCH, and GJR-GARCH models. On the other hand, with the 10-year bond, the Log-Likelihood is at its highest under Student’s t distribution, which can be ignored as there is a negligible difference in AIC and BIC values. However, the EGARCH model is frequently the best model for making predictions within a single phase.

The mean-reverting process is supported by the estimates of the model parameter β, which demonstrate that the series variance has a long memory and that volatility shocks are highly persistent for medium and long-term series but non-unity. The short-term series decays faster compared to the strong volatility persistence of the medium and long-term maturity. Furthermore, it has been found that volatility tends to rise in reaction to positive shocks as opposed to negative shocks of equal magnitude, suggesting the possibility of a “leverage effect” that is markedly different from that frequently seen in stock markets.

Besides, results indicate that, as inflation and expectations are the primary influence on yields, bond yield volatility rises as revisions in market expectations about inflation take place. Further, money market volatility causes bond yield volatility and vice-versa. We relate this finding to the presence of heightened market discipline within the Indian credit market and money market. Building on the well-developed analysis of volatility, we confirm that when bond volatility rises, it returns to its mean quickly during the period under stress (a bear market) except for the 3-month sovereign yield. As opposed to that, during bullish periods, Indian sovereign bond yields are highly persistent; when they rise, they remain high for a long period and then return to their mean only gradually.

Our research also explores the relationships among COVID-19, government intervention, and sovereign yield volatility during the bearish phase. For government responses, our research supports faster mean reversion during the bearish phase. When a government adopts various intervention policies for COVID-19, it should fully consider the resultant impacts and make an effort to eliminate any adverse ones on the overall economy.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Lithin B M

Lithin B M (First Author) is a Doctoral Scholar. His area of research is corporate finance and is currently pursuing his Ph.D. from theManipal Academy of Higher Education, Manipal, India

Suman Chakraborty

Suman Chakraborty (Corresponding Author) is working as an Associate Professor at the Department of Commerce, Manipal Academy of Higher Education, India. His research areas are Corporate Finance, Financial Markets, and Business Valuation.

Vishwanathan Iyer

Vishwanathan Iyer is a senior Associate Professor in the area of Accounting and Finance and currently the Dean (Accreditation) at the Great Lakes Institute of Management. His research interests are Portfolio Optimization, Earnings Management, Information content of text-based narrative in Annual reports, and the role of inspirational potency in communication to stock market participants.

Nikhil M N

Nikhil M N is currently pursuing his Ph.D. from the Department of Commerce, Manipal Academy of Education, Karnataka, India. Nikhil’s research is on capital structure and firm performance.

Sanket Ledwani

Lithin B M (First Author) is a Doctoral Scholar. His area of research is corporate finance and is currently pursuing his Ph.D. from theManipal Academy of Higher Education, Manipal, India

Sanket Ledwani is currently pursuing his Ph.D. from the Department of Commerce, Manipal Academy of Education, Karnataka, India. Sanket’s research is on Equity Level expected returns and Earnings Predictability.

Notes

1. In fact, this was an explicit policy of rating agencies until 1997. Although this relationship persisted after 1997, empirically document it. In a recent paper, examine the influence of sovereign risk on corporate risk in emerging markets with option-adjusted spreads. More recently, examined the characteristics of bonds rated higher than their sovereigns.

2. There is a reason why sovereign credit risk spills over to corporate credit risk, which is called the “transfer risk”: By increasing corporate taxes, imposing foreign exchange controls, and even expropriating private investment, a government in financial distress will likely shift the debt burden onto corporations.

3. Stationarity results for Sovereign yields quarterly series are reported in Appendix 1.

4. The results of GARCH (1,1), IGARCH and GJR-GARCH are reported in Appendx 2, 3, 4, and 5.