?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The paper examines the impact of central bank regulatory policies on market power in Africa. The study presents a representative sample of 52 African economies over the period 2006–2020. The study shows that the individual regulatory policies of the central bank (i.e. monetary and macro-prudential policies) enhance banks’ market power. Also, it reveals that central bank regulatory policies are better coordinated, as complements, in achieving greater market power of banks in countries with strong central bank independence (CBI) framework. However, the coordinated policies are substitutes in determining bank’s market power in countries with weak CBI framework. The policy implication is that the right policy mix of coordinated central bank regulatory policy framework is important in determining an optimal outcome of bank’s market power in both an inclusive central bank (monetary-prudential) policy targeting economies and an independent policy targeting economies.

1. Introduction

Despite considerable efforts over the past years to understand banks’ market power (Dadzie & Ferrari, Citation2019; Rakshit & Bardhan, Citation2019; Wang et al., Citation2022) and to assess the degree of impact of various policies of economic institutions (governments and the central banks) on banks’ market power (Brissimis et al., Citation2014; Delis, Citation2012), many questions remain unanswered. Specifically, the literature has so far not fully empirically examined the coordinated impacts of regulatory policy measures (i.e., monetary and macro-prudential policies) of the central bank on bank market power. This is due in part to the varying nature of regulatory policies by central banks (Anginer et al., Citation2014, Citation2019; Idun et al., Citation2022; Ofori-Sasu et al., Citation2022; Stolz & Wedow, Citation2005) and the different business conditions in which banks operate across different economies (Barczyk, Citation2018; Ofori-Sasu et al., Citation2022; Saadaoui, Citation2014). This paper contributes to the literature by providing new evidence on the impact of regulatory policies of the central bank on market power, particularly how monetary and macro-prudential policies independently and jointly (coordinated) influence market power in different central bank independence (CBI) framework.

In most economies, the government and the central bank jointly set regulatory policies, to maintain price and financial stability in the economy (Haidar, Citation2012; Lubis et al., Citation2019). Market power, a measure of the ability of a firm to successfully raise and maintain price above the level that would prevail under competition, is a key channel through which regulatory policy goals can be achieved in the economy. The study is motivated by the fact that few large banks, called the leaders, in the banking industry, may have an incentive to gain a strategic advantage over their followers when there is a change in central banks’ policy, leading to a change in banks’ market power. Over the years, in some countries, the banking sector is clearly an oligopoly (Dong et al., Citation2021), in the sense that, a major policy change on the part of industry leaders is likely to have immediate effects on the other firms (rivals) in the industry (Dong et al., Citation2021). In monopolistic competition, banks may advance any quantity or output they wish at a prevailing interest rate. This may give banks greater market power to operate. Thus, a change in the policy instrument may lead to a change in banks’ market power. In view of that, the effect of regulatory policies on banks’ exercise of market power is critical for policymakers and scholars because it provides information on how banks’ market power responds to changes in regulatory policies.

Consequently, monetary and macro-prudential policies of the central bank (i.e., regulatory policy measures) are usually taken in response to developments in credit (output) and competitive pricing behavior in the banking sector (Alter et al., Citation2018). According to Gruss and Sgherri (Citation2009), there is a tradeoff between prices (interest rate) and output (credit), so the goal of the central bank is to keep prices as stable as possible, given this tradeoff. In this case, the market power (percentage markup that is charged over marginal costs) of banks may change in response to changes in central bank policies through deposits and lending channels of interest rates. For instance, a monetary policy decision that tightens interest rates leads to an increase in the costs of borrowing. This offers few larger banks an incentive to exercise greater market power in the industry by shifting available credit to best borrowers at the high rate of interest that gives banks good returns (Corbae & D’erasmo, Citation2021). Similarly, the tightening of macro-prudential policies by the central bank implies that banks raise their capital reserves and buffers in order to reduce bank competition and provide them the incentive to exercise greater market power (Scalco et al., Citation2019). This implies that banks with more market power are less vulnerable to changes in monetary and macro-prudential policies of the central bank.

To the best of our knowledge, we note that most of the research focuses on analyzing the impact of policy instruments (monetary and macro-prudential measures) on bank loans (Auer & Ongena, Citation2019; Camors & Peydro, Citation2014; Cubillas & Suárez, Citation2018), risk-taking behavior of banks (Borio & Zhu, Citation2008; Bruno & Shin, Citation2012; Tabak & Gomes, Citation2015); or the transmission of monetary and macro-prudential policies (Duval et al., Citation2021), however, not directly on banks’ market power. Moreover, these studies were situated on developed and emerging economies. Besides that, it appears that the impact of individual policies of central banks on market power in Africa has been less focused in the literature (Idun et al., Citation2022; Ofori-Sasu et al., Citation2022). For instance, a recent study by Ofori-Sasu et al. (Citation2022) provides evidence that monetary, macro-prudential and central bank independence policies increase market power of banks in Africa, while Idun et al. (Citation2022) show that the emergence of credit information sharing institutions complements the effect of banks with market power to channel monetary policy transmission into price stability and interest rate stability in Africa. However, these studies were silent in examining the coordinated impact of different regulatory policies of the central bank on banks’ market power in Africa. Additionally, previous research has mostly used only one policy measure of the central bank (Claessens & Laeven, Citation2004; Cubillas & Suárez, Citation2018; Toolsema, Citation2004), which does not allow for the coordination of various regulatory policies and how they influence banks’ market power. Further, empirical research provides some evidence that different set of policy measures substitute or complement each other (Becher & Frye, Citation2011) in maintaining price or financial stability, hence the need to examine whether regulatory policies (monetary and macro-prudential) of the central bank are complements or substitutes to each other in affecting market power.

This paper provides novel contribution to the literature by examining the coordinated impacts of regulatory policies of the central bank on banks’ market power. One measure of institutions that plays a major role in determining the response of market power to central bank policies is the CBI framework. CBI is the central bank’s capability of controlling monetary instruments (Bernhard, Citation2002: pp21). It reflects the central bank’s powers to formulate and execute monetary policy (Warjiyo et al., Citation2019) and to promote price stability (Bodea and Higashijima, Citation2017). Thus, strong CBI framework can be a signal to investors about the future course of policy that the central bank is committed to following more credible regulatory policies that influence bank market power. While several studies have investigated the role individual policies play in driving the market power of banks (Delis, Citation2012; Wang et al., Citation2022; Scalco et al., Citation2021;), none has concentrated on the coordinated impact of regulatory policies of central banks on market power in different CBI framework.

The primary purpose of this study is to fill this research gap and to make contributions to the literature by first examining the empirical relationship between individual regulatory policies of central banks and market power. It does this by employing two measures of regulatory policies of central banks (see, Lubis et al., Citation2019; Ofori-Sasu et al., Citation2022), namely; monetary policy (Idun et al., Citation2022; Usman & Garba, Citation2014) and macro-prudential policy (Scalco et al., Citation2019), and explaining how they affect the market power of banks.

Secondly, it is interesting to establish the extent to which these policies are coordinated to influence banks’ market power. A comprehensive framework of the central banks’ regulatory policies is required to provide some guidance to policymakers as to how they might achieve their monetary objectives as well as enhance pricing or output strategies through banks’ market power. Moreover, it is not clear in the literature, whether monetary and macro-prudential policies should substitute or complement each other in the coordination mechanism (Lubis et al., Citation2019) in order to impact market power (see also, Nier & Kang, Citation2016; Ofori-Sasu et al., Citation2022). The study contributes to literature by testing the coordination impact of central bank regulatory policies on market power using marginal effects or plots and showing whether the coordination between the central bank regulatory policies are complements or substitutes to each other in determining market power.

Given that many governments in African countries come up with policy framework that gives central banks some level of independence, there is the need to take into account the degree of impact of the coordinated policies in different CBI framework. Hence, the study examines how regulatory policies of central banks influence banks’ market power, whether they are substitutes or complements to each other, in countries operating in stringent CBI framework and less stringent CBI framework. This is relevant to policymakers since it helps them to decide on whether to target monetary and macro-prudential policies simultaneously or focus independently on building one policy within a country (see, Lubis et al., Citation2019) and within the different CBI setup.

Finally, Africa provides an interesting case study for this empirical experiment because scholars and policymakers on the continent are now viewing coordinated policies of central banks, as an important tool for stabilizing the banking system through market power of banks. In addition, recent studies by Abor et al. (Citation2022) and Idun et al. (Citation2022), who focused on African countries, could not apply different sets of coordinated central banks’ policy framework to the African context because they were conducted in monetary targeting economies in Africa. Given the nature of African’s banking market structure and its response to changes in central banks’ regulatory policies, an examination of the influence of different regulatory policies in the determination of banks’ market power cannot be downplayed. To the best of our knowledge, the African context has not seen any empirical study that has attempted to examine the impact of coordinated regulatory policies of the central bank in determining banks’ market power. Therefore, this study makes novel contribution to the literature by extracting information from the IMF financial statistics database and Global Financial Development database of the World Bank, to examine the coordinated impact of central bank regulatory policies on the market power of banks in Africa, based on marginal effect and multiplicative analysis together with the marginal plot chart construction, which is largely limited in empirical studies in the African setting.

The rest of the paper is divided into four sections. A brief literature review is included in section 2. Section 3 is a discussion of the data and methodology. The empirical results are included in section 4, while section 5 presents the conclusion and implications of the study.

2. Literature review: theory, empirics and hypothesis development

Information gleaned from the literature indicates that banks’ market power is motivated by the prospective benefits of a bank having a greater incentive to charge markup over its marginal cost. In line with the structure-conduct-performance hypothesis, too much competition may be harmful because it reduces margins and may foster excessive risk-taking. This view suggests that less competition leads to greater market power, and this gives banks the ability to manipulate the price in the market place by manipulating the level of supply, demand or both. Thus, banks that exercise greater market power can adopt a better pricing strategy in the banking system (Caminal & Matutes, Citation2002; Simpasa, Citation2013).

From the oligopolistic competition perspective, it is not possible to predict any unique pattern of pricing behavior in the market (Freixas & Rochet, Citation2008; Klein, Citation1971). In this view, each bank tries to remain independent and to get the maximum possible profit, and this may lead to conflicting attitudes. Towards this end, banks act and react on the price-output movements of one another which reflects a continuous element of uncertainty. Again, motivated by profit maximization, each seller wishes to cooperate with his rivals to reduce or eliminate the element of uncertainty. All rival banks come into agreement with regard to price-output changes. This shows a sort of monopoly within oligopoly market. They recognize one seller as a leader at whose initiative all the other sellers raise or lower the price. Thus, a major policy change by the leader will affect the followers in the market. For instance, an increase in monetary policy rate (and interbank rate) will lead to an increase in the optimal interest rates on loans and deposits (Freixas & Rochet, Citation2008; Klein, Citation1971), causing other rival banks to follow same in the banking market.

Recent literature presents the importance of understanding market power and assess the policy transmission efficiency through the deposit channel of market power (Drechsler et al., Citation2017) and the lending channel of market power (Wang et al., Citation2020). Due to the nature of these channels, central banks’ policy could have different effects on banks with different levels of market power, and the bank market power may change in response to changes in central bank policy. In line with the impact of regulatory policies on banks’ market power, monetary policy affects the competitive behavior of banks through interest rates (Brissimis et al., Citation2014; Saadaoui, Citation2014). Haselmann and Wachtel (Citation2006) asserted that deregulation in developed countries aims to reduce market power, increase competition and enhance efficiency, whereas in developing countries, stability is achieved through the greater market power of banks. Chu and Zhang (Citation2021) assert that high policy rates adversely affect banks with less market power, causing smaller number of large banks to be dominated in the banking market over time. Liu et al. (Citation2021) explore that leaders in the industry have an incentive to gain a strategic advantage over their followers when the markup is low, leading to a rise in banks’ market power. Scalco et al. (Citation2019) indicated that macro-prudential policies to which the financial institutions are subject may affect banks market power; thus, they found that macro-prudential measures reduce bank competition by increasing the market power of banks. The study adds to the literature by investigating the individual effect of central bank policies on the market power of banks. Dadzie and Ferrari (Citation2019) showed that increasing macro-prudential policies through stringent initial capital requirements by the central banks impose entry barriers for foreign banks (Dadzie & Ferrari, Citation2019). This may restrict competition and allow existing banks to accumulate power, resulting in more prudent, and less risky behaviors (Saadaoui, Citation2014). Moreover, higher macro-prudential policies are associated with higher fixed costs of running the bank. This puts pressure on the banks to increase the rate of interest on household loans and thereby resulting in greater market power of banks (Bolt & Tieman, Citation2004). There is, however, no clear explanation as to how individual policies set by the central bank affect banks’ market power independently. A recent study by Ofori-Sasu et al. (Citation2022) provides evidence that monetary, macro-prudential and central bank independence policies positively affect the market power of banks in Africa, while Idun et al. (Citation2022) show that the effect of banks with market power to channel monetary policy transmission into price stability and interest rate stability is conditioned on the emergence of credit information sharing institutions in Africa. Despite the extant literature on the effect of a single measure of central bank policy on the market structure of banks, it is not clear how banks’ market power can respond to different regulatory policies of the central bank. For this reason, the current study formulates the following hypothesis:

H1:

Individual central bank regulatory polices are important determinants of banks’ market power.

The literature presents the design of the coordination impact of financial and economic policies by the central banks, on market power. The coordinated impact of central bank policies on market power has been ignored in the literature. However, the current study derives motivation from previous works in the literature (Agénor & Pereira da Silva, Citation2012; Andries & Melnic, Citation2019; Becher & Frye, Citation2011; Lubis et al., Citation2019). For instance, Lubis et al. (Citation2019) provide a critical and systemic review on the implementation of monetary and macro-prudential policies as a means of promoting price stability in the financial system. They argue that monetary policy alone is not sufficient to maintain macroeconomic and financial stability. Their conclusion thus indicates that macro-prudential policies are needed to supplement monetary policy. In arguing for whether a more proactive role is desirable, Agénor and Pereira da Silva (Citation2012) investigate what monetary policy should react to, to what extent it should be combined with macro-prudential regulation, and whether existing models provide adequate benchmarks for studying how these policies interact. They found that monetary policy is not a substitute to macro-prudential regulation, where it could, has undesirable side effects if used as an exclusive policy instrument. From the application of the gravity model, Becher and Frye (Citation2011) provide support that regulation and governance are complements and are consistent with the notion that regulators pressure firms to adopt effective monitoring structures. According to Andries and Melnic (Citation2019), central bank policies like monetary and macro-prudential policies can complement each other in achieving macroeconomic and financial stability. Following these arguments in the literature, regulatory policies may either act as substitute or complement to each other in the determination of market power of banks. The study adds to literature by showing how central bank regulatory policies are coordinated to impact market power.

In the empirical literature, Wang et al. (Citation2022) estimated a dynamic banking model in which monetary policy affects imperfectly competitive banks’ funding costs. They show that banks optimize the pass-through of their costs to borrowers and depositors, while facing capital and reserve regulation. They provide evidence to support that bank’s market power explains much of the transmission of monetary policy to borrowers, with an impact comparable to that of bank’s capital relation. Further, Wang et al. (Citation2022) show that when the federal fund rate falls below 0.9 percent, market power interacts with capital regulation to produce a reversal of the effect of monetary policy. Duval et al. (Citation2021) used the firm-level data for the U.S. and a large cross-country firm-level dataset for 14 advanced economies to examine monetary policy transmission of market power. They argued that the impact of a firm’s markup on its response to a monetary policy shock is large enough to affect monetary policy transmission. They show that firms’ market power dampens the response of their output to monetary policy shocks. Scalco et al. (Citation2021) examined the effect of macro-prudential measures on market power. They show that more competitive banking system hinges on macro-prudential measures. They found that the effect of macro-prudential policy measures is to reduce bank competition by increasing the market power of the banks. Nier and Kang (Citation2016) explore the interaction between monetary policy and macro-prudential policy and found that there are strong complementarities between these policies, such that where both policies are used actively, their overall effectiveness is enhanced relative to a world in which any one policy acts without the support of the other. Oduor et al. (Citation2017) studied capital requirement, bank competition and stability in Africa using data from 167 banks in African countries. They found that increased regulatory capital improves competitive pricing for foreign-owned banks in Africa. Agoraki et al. (Citation2011) examined whether regulations have an independent effect on bank risk-taking or whether their effect is passed through the market power of banks. They applied data from the banking sector of some European countries from 1998 to 2005. They empirically established that banks with market power tend to reduce credit risk. Moreover, higher activity restrictions (regulations) in combination with more market power reduce credit risk. Although these studies have looked at the market power response to different sets of regulatory framework in developed and developing economies, it is not clear, whether different regulatory policies of the central bank should be coordinated to yield desired results for banks’ market power, particularly in Africa—thus, the current study attempts to fill this gap

Banks’ behavior in response to regulatory policies varies across different CBI frameworks. In the literature, most of the works have shown the determinants of CBI in developed countries (Bernhard & Leblang, Citation2002; Pistoresi et al., Citation2011). Although there is agreement regarding the possibility that the determinants of CBI are different in developed and developing countries, the present study allows us to test the impact of regulatory policies on market power in different CBI settings. One way of achieving output-price stability is through CBI. In the presence of CBI, policymakers focus on the long-term, and short-term bumps in inflation using interest rate hikes. An independent central bank, as a major veto player, can contribute to having broad institutional stability and price stability through banks’ market power. For that reason, countries with more independent central banks tend to have greater influence on market power response to regulatory policies.

Based on this review, it is clear that research on the use of interactions between central bank regulatory policies in explaining the market power of banks is still developing. This serves as a motivation to examine the empirical relationship between central bank regulatory policies and market power in Africa. Further, the coordinated impacts of different sets of central bank regulatory policies on banks’ market power in different CBI economies have empirically been ignored in the literature. Therefore, the following hypothesis is formulated:

H2:

The coordination of central bank regulatory policies is significant in determining banks’ market power in different CBI framework.

3. Data and methodology

The study constructed a panel dataset for 52 African economiesFootnote1 from 2006 to 2020. The selection of countries and study period is based on data availability. Following Akhter (Citation2019), the model of this present study is estimated using the three-stage least square (3SLS) estimation. The motivation and theoretical underpinning for adopting this approach is to control for potential endogeneity in all regressors, reduce potential biases of the difference estimator in small samples and control for cross-country differences. The 3SLS estimator recognizes the endogeneity of central bank regulatory policy variables and market power, in a simultaneous equation framework. The 3SLS further provides consistent estimates (Zellner & Theil, Citation1992). The residuals in our 3SLS model produce a line of good fit.

3.1. Model, measurements and data sources

First, the study examined the independent impact of individual regulatory policies of the central bank on market power. The equation is specified as:

where subscript j denotes cross-sectional dimension (country specifics), j = 1, … , M; and denotes the time series dimension (time specifics),

= 1, … , T.

represent the regression coefficients of three central bank regulatory policy variables;

:

, are regression parameters for vector X (control variables) to be estimated;

is the country-fixed effect; and

is the time-fixed effect; and

is an idiosyncratic error term, which controls for unit-specific residual in the model for the banks in the jth country at period t.

3.1.1. Dependent variable: market power

The dependent variable is market power, which is measured with the Lerner index. The Lerner index is a measure of market power in the banking sector of each country. The Lerner index represents the markup of price (interest rate) over the marginal cost a bank may charge its customers, which indicates the market power of banks (Elzinga & Mills, Citation2011). Following Berger et al. (Citation2009) and Amidu and Wolfe (Citation2013), the Lerner index is constructed as follows:

where, is the price of aggregated total assets of banks in country i at time t; and

is the marginal cost of producing an additional unit output, which can be derived based on a translog cost function:

The marginal cost is calculated for each bank aggregated at country level as:

where, is the natural logarithm of aggregated total cost (interest expense/payments) for country i at time t;

is the natural logarithm of aggregated bank output (total assets) for country i at time t;

, k = 1.3, is the natural logarithm of the kth input price (input price = deposit funds, price of labour and price of capital);

= technological progress of the various years, computed as year dummies for the technological transfer or technological changes in the banking sector across the years of a specific country;

= variance of individual bank aggregated at country-level;

= time variance error term; and

= idiosyncratic error term.

Data on the Lerner index were obtained from the Global Financial Development Database. The Lerner index is interpreted to mean that an index that has a higher value indicates greater market power of banks and less competitive and vice versa.

Following the works of Simpasa (Citation2013) and Dong et al. (Citation2021), banks generally have combined, but not an individual, market power. According to Dong et al. (Citation2021), if a few larger banks’ market power changes in response to changes in central bank policies, all other banks act and react to the policy changes of one another. This creates true competition as the other banks react to the moves of the leaders. Therefore, we expect that changes in central bank policies and other factors should influence the ability of banks to exercise a degree of market power.

3.1.2. Impact of central bank regulatory policies on market power

From Equationequation 1(1)

(1) , the study decomposes central bank regulatory policy variables into two: (1) Monetary policy and (2) Macro-prudential policy.

Monetary policy is measured as monetary policy rates of the central banks in Africa and data was obtained from the International Financial Statistics of the International Monetary Fund (IMF). Monetary policy rates range between 0 and 1 (i.e., 0% and 100%), with higher values indicating tightening of the policy rates. The study expects a positive relationship between monetary policy and market power. This suggests that countries with tight monetary policy rates may increase market power of banks. This agrees with Wang et al. (Citation2022) who argued that, under oligopoly market condition, industry leaders may optimally choose how much of a rate increase to pass on to borrowers (Wang et al., Citation2022) that would maximize possible profit. Again, Freixas and Rochet (Citation2008) indicated that an increase in monetary policy rates, which reflects an increase in the interbank rates, leads to an increase in the optimal interest rates on loans and deposits, causing banks to increase risk-taking by selecting best clients, which in turn leads to a rising market power (Chu & Zhang, Citation2021). Therefore, an increase in monetary policy rates may increase market power of industry leaders, while the rivals (or others) in the industry respond accordingly.

Macro-prudential policy is an aggregate index of 17 indicators of macro-prudential action. Data were obtained from the iMaPP database constructed by Alam et al. (Citation2019), integrating information from major existing databases (i.e., the Global Macro-prudential policy instruments, IMF annual macro-prudential policy survey and national sources from Alam et al., Citation2019; Lim et al., Citation2011, Citation2013). The importance of macro-prudential policy instruments is that it can overlap with other policies (International Monetary Fund (IMF), Citation2017). The integrated macro-prudential policy database provides dummy-type indices of country-level averages for 17 macro-prudential policy instruments and their subcategories.Footnote2 The indicator records tightening actions (+1), loosening actions (−1), and no change (0). The index varies between −1 and 1, with positive values (values >0) indicating tightening or stringent policy action and negative values indicating loosening of the policy action (Alam et al., Citation2019).

The study expects a positive relationship between macro-prudential policy and banks’ market power. This suggests that an increase in macro-prudential policy leads to an increase in market power. The central bank set macro-prudential policies to tame the risky behavior of banks. The expected positive relationship means that tightening macro-prudential actions of central banks offers banks in the banking industry the opportunity to lower risk, generate higher profits, and in turn increase market power. Again, raising macro-prudential policy allows banks to raise more capital in their buffers and reserves by shifting investments to best clients at higher rates that yield more profits. This increases the markups and hence gives banks greater market power. This reveals the importance of macro-prudential policy in strengthening the banks’ market power (S. Hansen et al., Citation2011; Silalahi, Citation2013).

3.1.3. Control variables

In Equationequation 1(1)

(1) , X (vector of control variables) includes deposit funds (ratio of deposits to total assets); credit risk (ratio of nonperforming to gross loan); bank concentration (the ratio of asset of the three largest commercial banks to total commercial banking assets in a country); foreign bank entry (measured as dummy, 1 = year of foreign bank entry, 0 otherwise); money supply (broad money (M2+) to GDP ratio); and inflation (consumer price index). Data on these control variables were obtained from the World Bank Global Financial Development Database. The study also controls for central bank independence (de jure central bank independence), regulatory quality and business cycle. The study also obtained central bank independence from the IMF’s Central Bank Law database and the CWN legal CBI index constructed from Garriga’s (Citation2016) database. Data on regulatory quality was obtained from the Global Financial Development Database of the World Bank. In this study, the business cycle is measured as real GDP growth rate. Data on real GDP growth rate was obtained from the Global Financial Development Database.

The study expects a positive impact of deposit funds on market power. This implies that banks that mobilize more deposits may have more funds in their capital base, increase their market share and concentration, hence, leading to greater market power. The study expects a negative impact of credit risk on market power. Thus, higher credit risk exposures may endanger the intermediation margins of banks and reduce market power. Another expectation is that of a positive impact between concentration and market power. This means that a more concentrated banking system increases market power through greater mark-ups. A negative impact between foreign bank entry and market power is also expected. This implies that countries that allow free entry of foreign banks may increase banking competition which may induce lower market power in the banking market structure. The study expects a negative relationship between money supply and market power. This shows that countries that increase money supply can lower interest rates to meet the demand in the credit market; this leads to less market power of banks. The inflation rate is expected to positively affect market power. This suggests that countries with high inflation rates induce greater market power of banks.

As indicated earlier, the study controls for central bank independence and regulatory quality. Central bank independence is an index capturing the central bank’s ability to formulate independent policies; usually, policies that control monetary instruments, and limit the government’s influence on the management of monetary policy by the central bank. It is a measure of de jure central bank independence, which is based on a weighted aggregation of 16 legal indicators, using the criteria and weights in the Cukierman, Webb and Neyapti (CWN) index. The index varies between 0 and 1 (i.e., 0% and 100%), with larger values indicating greater level of central bank independence or more independent central bank. It is expected that higher levels of central bank independence will have a positive impact on the market power of banks. The independent function of central banks allows them to monitor the opportunistic behavior of managers, control excessive risk-taking behaviours and generate optimal returns. This requires that banks lower outputs (loans/lending) while they increase prices (interest rates) to yield more returns, and thus, induces greater banks’ market power. Therefore, a positive impact suggests that countries that allow the strict independent function of central bank tend to increase market power of banks.

More so, regulatory quality captures perceptions of the ability of institutions (government and central banks) to formulate and implement sound policies and regulations that permit and promote private development. The study expects either a positive or negative relationship between the regulatory quality and market power is expected. A positive relationship suggests that institutions with strong regulatory quality fight for price stability through greater market power, whereas a negative relationship suggests that institutions may drive competitive pricing policy by ensuring that banks lower their interest rates in order to reduce markups and market power.

Business cycle is a cycle of fluctuations in the Gross Domestic Product (GDP) around its long-term natural growth rate. In a business cycle, banks are driven differently, either counter-cyclically or pro-cyclically. The study expects a positive relationship between business cycle and market power. This implies that countries that increase their levels of business cycle tend to maintain their capital buffers by increasing interest rates and thereby leading to greater market power of banks. This agrees with Moudud-Ul-Huq (Citation2019), who indicates that higher levels of economic activities (expansionary phases) push more money into the banking sector and thus, increasing credit money and profits for banks. This gives industry leaders the incentive to exercise greater market power, indicating a positive relationship between business cycle and market power.

3.1.4. Coordinated impact of central bank regulatory policies on market power

Following the recent argument of Agenor and Pereira da Silva (Citation2012) and Lubis et al. (Citation2019), monetary and macro-prudential tools are set independently. Thus, close coordination between monetary and macro-prudential policies needs to be enforced to influence market power. For this reason, the study introduced an interaction term between monetary and macro-prudential policies into the model. This was done to capture the coordination impact of the policy variables (see Equationequation 3(3)

(3) ). Thus, Equationequation 2

(2)

(2) is specified as follows:

where, and

represent the coefficients of the linear terms of monetary policy and macro-prudential policy, respectively;

denotes the respective coefficients of the interaction terms (i.e. coordination terms) between monetary policy and macro-prudential policy.

, k = 1, … , N are the coefficients of the control variables (for vector C);

is the individual country effects;

is the time fixed effects and

is the composite error term.

From Equationequation 5(5)

(5) , the study is interested in understanding whether these policies complement or substitute each other to affect market power in the coordination process. In assessing whether the coordinated policies complement or substitute each other, the study follows the work by Compton and Giedeman (Citation2011) by considering the signs associated with the coefficients of the constitutive terms (unconditional effect) and the interaction terms (see, Compton & Giedeman, Citation2011). Furthermore, the study estimates the marginal effects to understand the true impact of the coordinated policies on market power. Following Brambor et al. (Citation2006), the study expects different marginal impacts of the coordinated policies on market power.

3.1.5. Robustness checks

In line with differences in CBI frameworks across regions, the study conducts a robust exercise by examining the coordinated impact of central bank regulatory policies on market power in countries with stringent CBI and less stringent CBI framework. The study splits the dataset into countries operating in stringent CBI framework and those operating in a less stringent CBI framework. In this case, it was expected that the policies jointly enhance market power in a more stringent independent central bank while they jointly reduce market power in a less stringent independent central bank.

In Equationequation 5(5)

(5) , C is a vector of control variables. It is expected that there are similar results of the relationship between the control variables and bank market power, as explained in Equationequation 2

(2)

(2) .

3.2. Estimation techniques

The Three Stage Least Square (3SLS) was used for the specification models by selecting the robust standard errors of under the estimator to correct for heteroskedasticity and autocorrelation. The study controls for unobserved heterogeneity in terms of country-specific effects as well as unobserved time fixed effects. Based on the above model, the study formed four structural equations outside market power, with three endogenous variables and eight exogenous variables (controls). The equations were identified based on the order conditions and rank conditions in order to determine whether the parameters can be estimated from their reduced form.Footnote3 Further, the parameters of the model were estimated by a 3SLS to handle possible endogeneity. By following Greene (Citation2003, pp. 413) and Iyoha (Citation2004, pp.118–9), the study uses a system of equations to control for endogeneityFootnote4. In addition to the variables employed for the study, the 3SLS simultaneous equation model produces estimates from a three-step process and helps to explicitly specify the instruments within the system of equations. First, it develops instrumented values for all endogenous variables; then obtains a consistent estimate for the covariance matrix in the equation disturbances, and finally, performs a GLS-type estimation using the covariance matrix. Two instruments that are found in the literature to affect market power and regulatory reforms are used: banking activity restrictions and financial freedom. Amidu and Wolfe (Citation2013) and Schaeck and Čihák (Citation2010) use similar instruments with a 2SLS estimator. Activity restrictions measures the limits imposed on commercial banks to participate in the financial market. This measure varies from 4 to 16 with higher scores indicating more restrictions. The financial freedom variable provides an overall measure of the openness of the financial sector and the extent to which financial institutions are free to operate their business. It ranges from 0 percent (lowest freedom) to 100 percent (highest freedom). Data were obtained from the IMF database and the Global Financial Development of the World Bank. For the purpose of the study, we report on the estimated specify in our equations above. We check the validity of our instruments by using the Sargan (Citation1958) test which reports for overidentifying restriction measures. In this context, the overidentifying restrictions are tested via the commonly employed J statistics of L. P. Hansen (Citation1982). The N. Hansen (Citation1990) test is distributed as chi-square under the null that the instruments are valid. Thus, the results as shown under the results (Tables ) suggest that none of the reform measures appears endogenous.

Table 1. Descriptive statistics

Table 2. Pairwise Correlation Matrix

Table 3. Impact of Individual Central Bank Regulatory Policies on Market Power

Table 4. Impact of Coordinated Central Bank Regulatory Policies on Market Power

4. Empirical results

This section discusses the results obtained from empirical estimations. First, it presents the summary statistics, followed by the correlation matrix and finally, the regression results.

4.1. Summary statistics and correlation matrix

Table reveals the descriptive statistics. For instance, in Table , the average market power of banks in our sample is 0.47, ranging from −4.383 to 9.665. In terms of regulatory policies of the central bank, monetary policy rates recorded a mean of 8.54%, ranging between 0 and 1. Macro-prudential policy action index recorded an average of 0.012. This suggests that the average macro-prudential policy action in Africa is neutral (not far from 0) or the macro-prudential policy action may not change across Africa, given a range from −1 (loosening policy action), 0 (no change in policy action) and 1 (tightening policy action) in our sample.

The study does not report on the descriptive statistics because of space.

In general, the summary statistics do not show any evidence of outliers and the Shapiro Wilk (SWILK) normality test indicates that the variables are normally distributed around their mean. Table reports the Pearson Correlation Coefficient matrix to check for possible multicollinearity between the explanatory variables. From the matrix, there is no evidence of multicollinearity as confirmed by the VIF below the threshold of 10 (see Table ). The correlation only shows the association between two explanatory variables without controlling for the effects of other variables.

4.2. Regression results

This section shows the relationship between central bank regulatory policies and market power. These are discussed as follows.

4.2.1. Impact of central bank regulatory policies on market power

The study examines the impact of individual central bank regulatory policies on market power. From Table , the individual central bank regulatory policies were positively linked to market power (see Models 1–3). For instance, in model 1, monetary policy is positively linked to market power. This shows that contractionary monetary policy offers banks the incentive to increase the interest rate, reduce the possibility of default and increase their markups. This in turn gives banks greater market power. Thus, an increase in the policy rate, which reflects an increase in price of a product makes it more expensive in relation to other products. This makes banks shift to best clients, make greater markups and thus, exercise greater degree of market power. For this reason, a tightening of monetary policy (i.e. an increase in policy rates) leads to greater market power. This agrees with the work by Dalla et al. (Citation2013) who found that monetary policy increases banks’ interbank rates, increases the optimal level of interest rates on loans and deposits, leading to greater market power (Haldane et al., Citation2018) in the banking system.

In Model 2, macro-prudential policy has a positive and significant direct impact on market power. This is true because the central bank sets macro-prudential policy to reduce the risk-taking activities of banks. By so doing, the tightening of the policy action gives banks the power to raise capital by simultaneously reducing outputs while increasing their prices (interest rates) in order to yield more returns/markups. This leads to greater market power. This implies that countries that increase their macro-prudential policy may induce greater market power. The study agrees with the research of European Central Bank (ECB) (2020) that macro-prudential policy aims at achieving price stability and eliminates the need for extremely low interest rates. Thus, countries that increase the level of macro-prudential policies are able to enforce price (interest rate) stability in the banking system, leading to greater market power.

4.2.2. Control variables

In terms of the controls, the study finds a positive relationship between deposit funds and bank market power (Models 1–3). This shows that banks with greater deposit base are able to exercise greater market power. Credit risk was negatively and significantly linked to bank market power. This is because higher levels of non-performing loans (credit risk exposures) tend to negatively impact banks’ margins, leading to lower market power. The study found a positive relationship between bank concentration and bank market power (Model 1–3). This is because a concentrated banking system may lead to greater market power (Shehzad et al., Citation2009). Foreign bank entry negatively impact market power. Foreign bank entry increases competition, which in turn lowers banks’ incentives to exercise market power. Money supply has a negative impact on market power (Models 1–3). This suggests that banks are able to increase market power when there is lower money supply. Inflation has positive effect on market power (Model 1–3). Central Bank Independence has a positive and significant effect on market power. This shows that countries that instill more independent function of the central bank tend to increase the market power of banks. This is because, reforms that strengthens the independent function of central bank ensure discipline in the banking system and therefore central bank independence induces greater market power in the banking market. Regulatory quality reduces market power of banks (Models 1–3). It is observed that the business cycle has a positive impact on market power (Model 1–3). This shows that an increase in average levels of business cycle increases market power of banks, implying that banks have a greater incentive to exercise market power in a growing business environment.

During average levels of business cycle, economic agents, may supply more funds to the financial sector and may demand higher interests (Saadaoui, Citation2014). This forces banks to identify investment and credit opportunities that may give them greater returns and markups, resulting in greater market power.

4.2.3. Coordination impact of central bank regulatory policies on market power

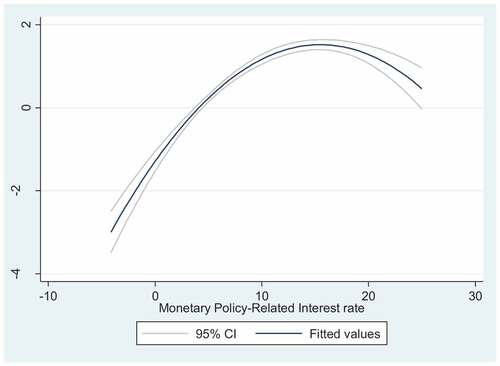

In this section, the study argues that the impact of the individual regulatory policies alone is not conclusive in the determination of market power. The study shows that the policies are coordinated in the determination process of market power. First, the study introduces the interaction terms between the individual central bank regulatory policies and then tests whether they are complements or substitutes. For instance, from Table , monetary policy has a positive coefficient (Model 4) while the coefficient of the interaction term between monetary policy and macro-prudential policy actions is positive (Model 4). This suggests that monetary policy and macro-prudential policy action are complements in the determination of banks’ market power. This agrees with the work by Nier and Kang (Citation2016) who explored the interactions between monetary policy and macro-prudential policy and found that these policies are complements. They argued that monetary policy and macro-prudential policy pursue different primary objectives—price (and output) stability for monetary policy and financial stability for macro-prudential policy. Nonetheless, the conduct of each policy can have “side effects” on the objective of the other. They show that in the presence of such side effects, effective monetary and macro-prudential policies complement each other, yielding superior outcomes to a world where monetary policy—or macro-prudential policy—is pursued on its own and in the absence of the other policy. Drawing from the work of Nier and Kang (Citation2016), the study provides evidence to support that monetary policy and macro-prudential policy action are complements in shaping the market power of banks.

Consistent with Brambor et al. (Citation2006), there is the need to examine the marginal effect of the coordinated policies. In terms of marginal plots, monetary policy increases market power when macro-prudential policy tightens (see Figure ). In practice, there is no single tool that influences all financial behavior or price-output behavior consistently, a variety of tools are needed. Therefore, the implication from the results means that additional macro-prudential tools will be helpful in complementing monetary policy in order to yield an optimal bank’s market power.

Figure 1. Marginal Plots: Coordinated Impact of Monetary and Macro-prudential Policies on Market Power.

In general, our results are close to the empirical studies by Greenwood-Nimmo and Tarassow (Citation2016) who argue that when monetary policy is used alongside various policies, the financial fragility may diminish in the short run. Therefore, the right policy mix between monetary and macro-prudential policies is important in explaining market power within a coordination mechanism of central bank regulatory policies.

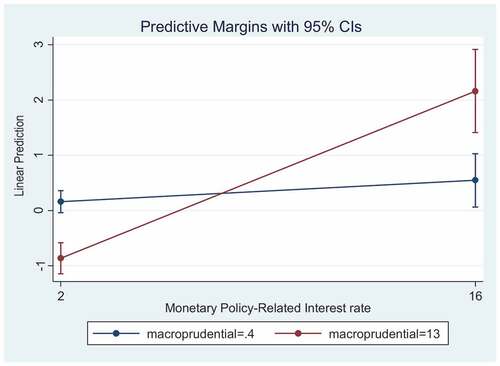

4.2.4. Robustness check: coordinated impact in different CBI framework

Policy independence reflects the central bank’s power to formulate and execute monetary policy and to restrict government’s influence on central bank’s management of monetary instruments. This includes the central bank’s ability to set the goals and/or choose the instruments of monetary and prudential instruments. Given that central bank’s regulatory designs vary across these dimensions, resulting in different levels of CBI, the study computes the marginal effects of the coordinated policies in different CBI settings (see Table ). The interpretations were based on the marginal effect estimations and marginal plots as demonstrated by Brambor et al. (Citation2006).

In model 4, we control for CBI, and observe that monetary and macro-prudential policies are complements to each other in enhancing market power.

In model 5, the marginal effect of monetary policy on market power is less positive in countries with weak independent central bank compared to those with stringent independent central bank (Model 5 vs. Model 6). This implies that countries with government inference (weak CBI framework) tend to reduce market power through the coordination of monetary and macro-prudential policies while those stringent CBI framework are able to increase market power through the coordination of monetary and macro-prudential policy. Figure shows that the coordinated impacts of the monetary and macro-prudential policies increase market power relatively more in the stringent CBI framework compared to the weak CBI framework.

Figure 2. Marginal Plots of the Coordination of Monetary and Macro-prudential in Different CBI Framework.

The results in Models 5 clearly show that the monetary and macro-prudential policies are substitutes to each other in determining bank’s market power in countries with weak CBI framework. However, the monetary and macro-prudential policies are complements to each other in the determination of bank’s market power in a more independent central bank framework. It can be deduced that CBI is the central bank’s capability of controlling monetary instruments and improving price and financial stability. This induces a positive impact on market power when the policies are coordinated; thus, a complementarity effect is necessary in a more independent central bank framework. However, a weak CBI framework supports the idea that coordinated policies are substitutes in the determination of market power.

5. Conclusion and policy implications

The study examines the impact of central bank regulatory policies on market power of banks. The study provides novel contribution to the literature by testing the coordinated impact of central bank regulatory policies on market power of banks. The study found that monetary and macro-prudential have a positive and significant impact on market power. The study found that monetary and macro-prudential policies of the central bank are better coordinated in increasing banks’ market power. It was observed that the extent of the marginal effect of the policies depended on the substitutability and complementarity of the coordinated policies. In view of that, the study provides evidence that monetary policy and macro-prudential policy action are complements in shaping the market power of banks. The study found that monetary and macro-prudential policies increase market power when they are coordinated in countries with a strong independent central bank framework but they decrease market power when they are coordinated in a weak CBI framework. The study clearly shows that the regulatory policies are complements to each other in determining bank’s market power in countries with a stringent CBI framework while they are substitutes in determining bank’s market power in countries with a weak CBI framework.

The policy implication is that additional macro-prudential tools will be helpful in complementing monetary policy in order to yield an optimal bank’s market power. Therefore, policymakers and regulators should provide the right policy mix of monetary and macro-prudential policies to determine an optimal outcome of bank’s market power in Africa and other regions in the world. Further, there is a wake-up call for countries with weak CBI framework to strengthen their regulatory policy frameworks through a coordination mechanism that enhance banks’ market power. Such a step will enable them better strategize through a coordination process in order to target optimal market power of banks. Finally, policymakers and regulators should put forward a careful assessment and comprehensive determination of banks’ market power through a coordinated central bank regulatory policy framework that can synthesize the desired outcome or optimal level of bank’s market power in both an inclusive central bank (monetary-prudential) policy targeting economies and an independent central bank policy targeting economies.

Availability of data and materials

The datasets used and/or analysed during the current study are available (with corresponding author) on reasonable request.

Supplemental Material

Download MS Word (13.7 KB)Disclosure statement

No potential conflict of interest was reported by the authors.

Supplemental data

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23322039.2023.2196851

Notes

1. See list of countries in Appendix II.

2. See Alam et al. (2018) for more details 16 indicators include: countercyclical capital buffer, requirements for banks to maintain a capital conservation buffer, capital requirements, limits on leverage of banks, loan loss provision requirements, limits on foreign currency, limits to the loan-to-value ratios, debt service-to-income ratios, minimum requirements for liquidity coverage ratios, limits to the loan–deposit ratio, limits to net or gross open foreign exchange positions, reserve requirements, loan restrictions, risk measures, taxes and levies applied to specified transactions, and macro-prudential measures not captured in the above categories.

3. See Greene, 2003: 413; Iyoha (2004a).

4. See Appendix I.

References

- International Monetary Fund(I. M. F.) (2017): “Increasing resilience to large and volatile capital flows: The role of macroprudential policies”, IMF Policy Paper, July.

- Abor, J. Y., Agoba, A. M., Mumuni, Z., & Yawson, A. (2022). Monetary Policy, Central Banks’ Independence, and Financial Development in Africa. In J. Y. Abor & Adjasi C. D. (Eds.), The Economics of Banking and Finance in Africa: Developments in Africa’s Financial Systems (pp. 227–23). Cham: Springer International Publishing.

- Agénor, P. R., & Pereira da Silva, L. A. (2012). Macroeconomic stability, financial stability, and monetary policy rules. International Finance, 15(2), 205–224. https://doi.org/10.1111/j.1468-2362.2012.01302.x

- Agénor, P. R., & Pereira da Silva, L. A. (2012). Macroeconomic stability, financial stability, and monetary policy rules. International Finance, 15(2), 205–224.

- Agoraki, M. E. K., Delis, M. D., & Pasiouras, F. (2011). Regulations, competition and bank risk-taking in transition countries. Journal of Financial Stability, 7(1), 38–48. https://doi.org/10.1016/j.jfs.2009.08.002

- Akhter, N. (2019). Assessing the relationship between efficiency, capital and risk of commercial banks in Bangladesh. International Journal of Business and Management, 14(1), 55–63. https://doi.org/10.5539/ijbm.v14n1p55

- Alam, Z., Alter, A. E., Gelos, J., Kang, G., Narita, H., Nier, M., & Wang, N. (2019). Digging deeper – Evidence on the effects of macro-prudential. Monetary and capital markets department. IMF Working Paper

- Alter, A., Feng, A., & Valckx, N. (2018). Understanding the macro-financial effects of household debt: A global perspective. IMF Working Paper, WP/18/76 (International Monetary Fund)

- Amidu, M., & Wolfe, S. (2013). The impact of market power and funding strategy on bank-interest margins. European Journal of Finance, 19(9), 888–908. https://doi.org/10.1080/1351847X.2011.636833

- Andries, A. M., & Melnic, F. (2019). Macroprudential policies and economic growth. Review of Economic and Business Studies, 12(1), 95–112. https://doi.org/10.1515/rebs-2019-0084

- Anginer, D., Bertay, A. C., Cull, R., Demirguc-Kunt, A., & Mare, D. S. (2019). Bank regulation and supervision ten years after the global financial crisis. World Bank Policy Research Working Paper, (9044).

- Anginer, D., Demirguc-Kunt, A., & Zhu, M. (2014). How does competition affect bank systemic risk? Journal of Financial Intermediation, 23(1), 1–26.

- Auer, R., & Ongena, S. (2019). The countercyclical capital buffer and the composition of bank lending. Available at SSRN 3345189. https://doi.org/10.2139/ssrn.3467948

- Barczyk, R. (2018). The business cycle and cycles in the banking sector in the polish economy in the years 2000‒2017. Folia Oeconomica Stetinensia, 18(2), 106–120. https://doi.org/10.2478/foli-2018-0022

- Becher, D. A., & Frye, M. B. (2011). Does regulation substitute or complement governance? Journal of Banking & Finance, 35(3), 736–751. https://doi.org/10.1016/j.jbankfin.2010.09.003

- Berger, A. N., Klapper, L. F., & Turk-Ariss, R. (2009). Bank Competition and Financial Stabil- ity. Journal of Financial Services Research, 35(2), 99–118. https://doi.org/10.1007/s10693-008-

- Bernhard, W., Broz, J. L., & Clark, W. R. (2002). The political economy of monetary institutions. International Organization, 56(4), 693–723.

- Bernhard, W., & Leblang, D. (2002). Political parties and monetary commitments. International Organization, 56(4), 803–830.

- Bodea, C., & Higashijima, M. (2017). Central bank independence and fiscal policy: Can the central bank restrain deficit spending?. British Journal of Political Science, 47(1), 47–70.

- Bolt, W., & Tieman, A. F. (2004). Banking competition, risk, and regulation. The Scandinavian Journal of Economics, 106(4), 783–804.

- Borio, C., & Zhu, H. (2008): “Capital regulation, risk-taking and monetary policy: A missing link in the transmission mechanism?”, BIS Working Paper, no 268.

- Brambor, T., Clark, W. M., & Golder, M. (2006). Understanding interaction models: Improving empirical analyses. Political Analysis, 14(1), 63–82.

- Brissimis, S. N., Iosifidi, M., & Delis, M. D. (2014). Bank market power and monetary policy transmission. Available at SSRN 2858468.

- Bruno, V., & Shin, H. S. (2012): “Capital flows and the risk-taking channel of monetary policy”, 11th BIS Annual Conference, Bank for International Settlements, Basel.

- Caminal, R., & Matutes, C. (2002). Market power and banking failures. International Journal of Industrial Organization, 20(9), 1341–1361.

- Camors, C., & Peydro, J. (2014). Macroprudential and monetary policy: Loan-level evidence from reserve requirement. Mimeo Universitat Pompeu Fabra. URL https://pdfs.semanticscholar.org/d508/61639bb4e7453a7a39184edf9b0c1e7016a6.pdf

- Chu, Y., & Zhang, T. (2021). Monetary policy and bank concentration. Available at SSRN 3704020.

- Claessens, S., & Laeven, L. (2004). What drives bank competition? Some international evidence. Journal of Money, Credit, and Banking, 36(1), 563583.

- Compton, R. A., & Giedeman, D. C. (2011). Panel evidence on finance, institutions and economic growth. Applied Economics, 43(25), 3523–3547.

- Corbae, D., & D'Erasmo, P. (2021). Capital buffers in a quantitative model of banking industry dynamics. Econometrica, 89(6), 2975–3023.

- Cubillas, E., & Suárez, N. (2018). Bank market power and lending during the global financial crisis. Journal of International Money and Finance, 89, 1–22.

- Dadzie, J. K., & Ferrari, A. (2019). Deregulation, efficiency and competition in developing banking markets: Do reforms really work? A case study for Ghana. Journal of Banking Regulation, 20(4), 328–340.

- Dallas, S. L., Prideaux, M., & Bonewald, L. F. (2013). The osteocyte: An endocrine cell… and more. Endocrine Reviews, 34(5), 658–690.

- Delis, M. D. (2012). Bank competition, financial reform, and institutions: The importance of being developed. Journal of Development Economics, 97(2), 450–465.

- Dong, M., Huangfu, S., Sun, H., & Zhou, C. (2021). A macroeconomic theory of banking oligopoly. European Economic Review, 138, 1–23.

- Drechsler, I., Savov, A., & Schnabl, P. (2017). The deposits channel of monetary policy. The Quarterly Journal of Economics, 132(4), 1819–1876.

- Duval, M. R. A., Furceri, D., Lee, R., & Tavares, M. M. (2021). Market power and monetary policy transmission. International Monetary Fund.

- Elzinga, K. G., & Mills, D. E. (2011). The Lerner index of monopoly power: Origins and uses. The American Economic Review, 101(3), 558–564.

- Freixas, X., & Rochet, J. C. (2008). Microeconomics of banking. MIT press.

- Garriga, A. C. (2016). Central bank independence in the world: A new data set. International Interactions, 42(5), 849–868.

- Greene, W. H. (2003). Econometric Analysis (5th ed.). Prentice Hall.

- Greenwood-Nimmo, M., & Tarassow, A. (2016). Monetary shocks, macroprudential shocks and financial stability. Economic modelling, 56, 11–24.

- Gruss, B., & Sgherri, S., (2009), The volatility costs of procyclical lending standards: An assessment using a DSGE model, IMF Working Paper, 09/35.

- Haidar, J. I. (2012). The impact of business regulatory reforms on economic growth. Journal of the Japanese and International Economies, 26(3), 285–307.

- Haldane, A., Aquilante, T., Chowla, S., Dacic, N., Masolo, R., Schneider, P., & Tatomir, S. (2018). Market power and monetary policy. Speech, Bank of England.

- Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, 1029–1054.

- Hansen, N. (1990). Do producer services induce regional economic development? Journal of Regional Science, 30(4), 465–476.

- Hansen, S., Kashyap, A., & Stein, J. (2011). A macroprudential approach to financial regulation. Journal of Economic Perspective, 25(1), 3–28.

- Haselmann, R., & Wachtel, P. (2006). Bank risk and bank management in transition: A progress report on the EBRD banking environment and performance survey. Manuscript, Stern School of Business, New York Univeristy.

- Idun, A. A. A., Agyei, S. K., Gossel, S. J., & Abor, J. Y. (2022). Bank market power and monetary policy transmission in Africa in the wake of information sharing institutional arrangements. In Abor, J.Y., and Adjasi, C.D., (Eds.), The Economics of Banking and Finance in Africa: Developments in Africa’s Financial Systems (pp. 269–310). Cham: Springer International Publishing.

- Iyoha, M. A. (2004). Applied econometrics. Mindex Publishing.

- Klein, M. A. (1971). A theory of the banking firm. Journal of Money, Credit, and Banking, 3(2), 205–218.

- Lim, C. H., Costa, A., Columba, F., Kongsamut, P., Otani, A., Saiyid, M., & Wu, X. (2011). Macroprudential policy: What instruments and how to use them? Lessons from country experiences.

- Lim, C. H., Krznar, M. I., Lipinsky, M. F., Otani, M. A., & Wu, M. X. (2013). The macroprudential framework: Policy responsiveness and regulatory arrangements. International Monetary Fund.

- Liu, W., Liang, Y., Tang, O., Shi, V., & Liu, X. (2021). Cooperate or not? Strategic analysis of platform interactions considering market power and precision marketing. Transportation Research Part E: Logistics and Transportation Review, 154, 102479.

- Lubis, A., Alexiou, C., & Nellis, J. (2019). Early view online) ‘What can we learn from the implementation of monetary and macro-prudential policies: A systematic literature Review. Journal of Economic Surveys, 33 (4), 1123–1150.

- Moudud-Ul-Huq, S. (2019). Banks’ capital buffers, risk, and efficiency in emerging economies: Are they counter-cyclical? Eurasian Economic Review, 9(4), 467–492.

- Nier, E. W., & Kang, H. (2016). Monetary and macroprudential policies–exploring interactions. BIS Paper, (86e).

- Oduor, J., Ngoka, K., & Odongo, M. (2017). Capital requirement, bank competition and stability in Africa. Review of Development Finance, 7(1), 45–51.

- Ofori-Sasu, D., Agbloyor, E. K., Kuttu, S., & Abor, J. Y. (2022). Central bank policies and market power over the business cycle in Africa. Journal of Emerging Market Finance. https://doi.org/10.1177/09726527221086492

- Pistoresi, B., Salsano, F., & Ferrari, D. (2011). Political institutions and central bank independence revisited. Applied Economics Letters, 18(7), 679–682.

- Rakshit, B., & Bardhan, S. (2019). Bank competition and its determinants: Evidence from Indian banking. International Journal of the Economics of Business, 26(2), 283–313.

- Saadaoui, Z. (2014). Business cycle, market power and bank behavior in emerging countries. International Economics, 139, 109–132.

- Sargan, J. D. (1958). The estimation of economic relationships using instrumental variables. Econometrica: Journal of the Econometric Society, 393–415.

- Scalco, P. R., Tabak, B. M., & Teixeira, A. M. (2019). The dark side of prudential measures. NEPEC/FACE/UFG Goiânia –, Junho de 2019.

- Scalco, P. R., Tabak, B. M., & Teixeira, A. M. (2021). Prudential measures and their adverse effects on bank competition: The case of Brazil. Economic modelling, 100, 105495.

- Schaeck, K., & Čihák, M. (2010). Competition, efficiency, and soundness in banking: An industrial organization perspective. Center for Economic Research.

- Shehzad, C. T., Scholtens, B., & De Haan, J. (2009). Financial crisis and Bank earnings volatility, the role of bank size and market concentration. Working Paper No. 1470727.

- Silalahi, T. (2013). Does macroprudential instruments and market power matter on banks’ performance: An empirical evidence on Indonesian banking firms. Available at SSRN 2322612.

- Simpasa, A. M. (2013). Increased foreign bank presence, privatisation and competition in the Zambian banking sector. Managerial Finance, 39(8), 787–808.

- Stolz, S. P., & Wedow, M. (2005). Banks’ regulatory capital buffer and the business cycle: Evidence for German savings and cooperative banks. Discussion Paper Series 2: Banking and Financial Studies No 07/2005. Deutsche Bundesbank, Wilhelm-Epstein-Strasse 14, 60431 Frankfurt am Main, Postfach 10 06 02, 60006 Frankfurt am Main

- Tabak, B., & Gomes, G. (2015). The impact of market power at bank level in risk-taking: The Brazilian case. International Review of Financial Analysis, 40, 154.

- Toolsema, L. (2004). Monetary policy and market power in banking. Journal of Economics, 83, 71–83.

- Usman, A. H., & Garba, M. (2014). Monetary policy and price stability in Nigeria.

- Wang, Y., Whited, T. M., Wu, Y., & Xiao, K. (2020). Bank market power and monetary policy transmission: Evidence from a structural estimation. National Bureau of Economic Research.

- Wang, Y. W., Wu, T. M., & Xiao, K. (2022). Bank market power and monetary policy transmission: Evidence from a structural estimation. The Journal of Finance, 77(4), 2093–2141.

- Warjiyo, P., & Juhro, S. M. (2019). Monetary Policy Transmission Mechanism. In Central Bank Policy: Theory and Practice (pp. 115–158). Emerald Publishing Limited.

- Zellner, A., & Theil, H. (1992). Three-stage least squares: Simultaneous estimation of simultaneous equations (pp. 147–178). Springer Netherlands.

Appendix Appendix I

Appendix II. List of Countries