?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to provide empirical evidence regarding the impact of the COVID-19 pandemic on banking performance in Indonesia. This study examines differences in Indonesian banking performance before and during the COVID-19 pandemic. Banking performance in this study was measured using the CAMEL measure. The analysis was carried out by conducting a different test using the SPSS application version 22.0. Based on the results of tests conducted on 205 observations on banking from 2018 to 2021, it was found that the CAR, ROA, ROE, BOPO, LDR, and Customer Deposit levels from banks in Indonesia had a significant difference between before and during the COVID-19 pandemic. However, there was no significant difference between the NPL banking level in Indonesia before and during the COVID-19 pandemic. This proves that the COVID-19 pandemic has harmed banking in Indonesia, so the government must pay attention to the current banking strength to survive and recover after the COVID-19 pandemic.

Public Interest Statement

In this study, the authors formulate empirical references and findings regarding the impact of the COVID-19 pandemic on banking performance. This study aims to focus on the impact of the COVID-19 pandemic that occurred from 2020 to 2021 on improving performance in the banking sector by using the CAMELS performance indicators (Capital, Assets, Management, Earnings, Liquidity, and Solvability) in banks that in Indonesia. This research shows that there needs to be special attention. The results of this research can be used as a reference for banking practitioners, regulators and decision makers to pay special attention to better banking management after the COVID-19 pandemic. This research is also a new reference for researchers in the future.

1. Background

Distancing to reduce the growth rate of COVID-19 cases in Indonesia. The COVID-19 pandemic has been an extraordinary phenomenon in various countries from 2020 to 2021. World Health Organization (WHO), until 1 August 2022, noted that there had been 578,142,144 confirmed cases with a death rate of 6,405,080 people or around 1.1% (WHO, 2022). The COVID-19 pandemic also occurred in Indonesia from 2019 to 1 August 2022; WHO recorded 6,229,315 confirmed cases with a death rate of 157,060 people or around 2.52% (WHO, Citation2022). Based on this, the Indonesian government 2020 to 2021 will limit community activities through social and physical implementation. This policy ultimately led to significant changes in all community activities, where the majority of activities were carried out online and at home; in the end, this condition impacted the Indonesian economy in 2020–2021.

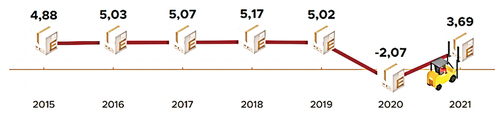

Economic growth in Indonesia from 2020 to 2021 has been shown to experience a contraction compared to the period before 2020 (Pandemic Covid-19). The Central Agency on Statistics (CAS or in Indonesia called BPS) records economic growth in terms of Gross Domestic Product (GDP) from 2015 to 2021 in Figure as follows.

The economic shock caused by the COVID-19 pandemic will ultimately impact the banking sector’s performance. Based on data owned by BPS, it shows that in 2020 Indonesia’s economic growth will drop to −2.07, and in 2021 it will increase to 3.69, although basically, this economic growth is still deficient when compared to 2015–2019. Law Number 10 of Citation1998 concerning banking in article 1 explains that “a bank is a business entity that collects funds from the public in the form of savings and distributes them to the public in the form of credit and or other forms in order to improve the standard of living of the common people ”. Thus, when the country’s economy is shaken, it will impact banking performance.

Law Number 7 of 1992 concerning Banking states in article 1, paragraph 1 that “Banks are business entities that collect funds from the public in the form of savings and distribute them to the public in the form of credit and or other forms in order to improve the standard of living of the people at large ”. Based on this understanding, the role of banking is vital for a country’s economy and has a significant influence on economic conditions. In other words, banking conditions will also decline when a country’s economy declines due to Covid-19. The chairman of the Financial Services Authority (in Indonesia called OJK) said that in the banking services sector, there was an impact from the COVID-19 pandemic, which caused the rate of banking intermediation at the end of 2020 to drop to −2.41% (Republika, Citation2022).

The existence of the COVID-19 pandemic, which impacts the economic situation in Indonesia and banking performance, can be explained theoretically based on the theory of the Harrod-Domar growth model. The theory of the Harrod-Domar growth model has several assumptions, namely (a) the economy is in complete condition, employment and capital goods in society are fully used, (b) the economy consists of two sectors, namely households and companies which means that there is no government and foreign sectors, (c) the amount of public savings is proportional to the amount of national income, (d) the tendency to save (MPS) remains the same as the capital-output ratio and the capital-output ratio (Tarigan, Citation2005, p. 49). During the pandemic, all the assumptions from the theory of the Harrod-Domar growth model were not fulfilled because there were many layoffs due to Work From Home (WFH). The amount of people’s savings decreased due to the decrease in total income so that national income would also decrease, which in the result would be a decrease in the ratio of capital—output increase as well. Thus, in the end, the economy does not experience growth and even experiences a decline which causes banking performance to decline.

The quality of banking performance can be measured using several aspects commonly referred to as CAMEL (Capital, Assets, Management, Equity and Liquidity). The financial analysis model using CAMELS is considered more efficient for establishing a transparent risk assessment system, developing and monitoring quality performance, identifying problems, and correcting deficiencies (Nair & Asghede, Citation2015). The CAMELS method is a popular performance measurement model for banking, and one of the pioneers of this model is Cole & Gunther (Citation1995). The CAMELS model was then verified by Gasbarro et al. (Citation2002) and Baral (Citation2005). Based on this, this study uses the CAMELS method to measure banking performance during the pandemic.

Several studies also carried out research on banking performance appraisal during the pandemic (Kunt et al., Citation2020, Citation2021; Xiazi & Shabir, Citation2022). Kunt et al. (Citation2020) analyzed stock prices at banks worldwide. They found that during the pandemic crisis, the banking system was under significant pressure with markedly poor banking stock performance in the domestic market. These results are supported by research from Kunt et al. (Citation2021) shows that banks need liquidity support, loan assistance and monetary easing to deal with the adverse effects of the COVID-19 pandemic crisis. Xiazi and Shabir (Citation2022) also found similar results: the COVID-19 pandemic has significantly reduced bank performance from 1,575 banks in 85 countries during 2020 Quartile 1 to 2021 Quartile 4, mainly banks with small size, capital and verified. However, the results of these previous studies have not tested banking performance by incorporating complete performance aspects. In addition, previous studies have not tested the differences in the significance of banking financial performance before and during the COVID-19 pandemic. Therefore, this research needs to be carried out especially for the Indonesian perspective which is still very rare to find similar research. The research question that will be answered in this study “Is whether there are significant differences in the CAMELS-based financial performance of banking companies in Indonesia before and during the COVID-19 pandemic?”

Based on the explanation in the previous paragraph, the researchers are interested in conducting empirical testing regarding the impact of the COVID-19 pandemic on banking performance in Indonesia. This is because researchers with an Indonesian perspective rarely carry out research related to this topic. The selection of banks will consist of various types, namely State-owned enterprises (in Indonesia called BUMN), Regional owned enterprises (in Indonesia called BUMD), private, and sharia. The results of this study are expected to contribute as a reference source for conducting similar research. In addition, the results of this study will be a source of information for policymakers to focus on increasing banking resilience. The results of this research are expected to provide information for taking follow-up actions on the impact of the pandemic on banking performance so that Deposit Insurance Agency (in Indonesia called LPS) can give confidence to the public to be sure of the funds kept in the bank guaranteed by LPS. In addition, the goal to be achieved in this research is to find empirical evidence regarding the performance comparison of banks in Indonesia before and during the COVID-19 pandemic.

2. Study of literature

2.1. Contingency theory

Contingency theory is theory has been a branch of systems theory related to the design of a system since the mid 60‘s 70s. Contingency theory begins with work by Thompson (Citation1967), who tries to reconcile the flow of open and closed systems thinking. The focus of Thompson’s work is on environmental factors that shape rational corporate actions, thus recommending that rational organizations always focus on contingency avoidance. Contingency theory experienced its golden age in the early 80s when Scott (Citation1981) stated that contingency theory is the dominant approach to the design of an organization and a contemporary theoretical approach often used to study organizations.

The general axiom of contingency theory is that organizations should have internal features with high compatibility with environmental demands in order to achieve the best adaptation; in other words it can be said that there is no universally superior strategy, regardless of environmental or corporate context (Lawrence & Lorsch, Citation1967; Scott, Citation1987; Venkatraman, Citation1989). This axiom of contingency theory can be rationally accepted because there are too many variables related to organizational structure, external environment, and internal organization. Therefore, the design of each organization varies based on the level of environmental stability. The corporate structure has two types, namely the mechanistic system suitable for a stable environment and the organic system required in a changing environment (dynamic environment).

Contingency theory is also related to the pace of technological change in both the economic sector (Staynov & Baumgarter, Citation1986), uncertain financial markets (Nam & Tatum, Citation1988), and changes in client demand to follow variations, aspirations, and purchasing power. This is reasonable because it will be difficult to manage existing businesses when the environment changes. In general, researchers who use contingency theory find that there are three elements of contingency, namely company size, the technology used, and operating environment, which are very important in influencing organizational structure.

2.2. Harrod-Dommar growth model theory

One of the well-known theories of economic growth is the theory of the Harrod-Domar growth model. This theory is a theory that seeks to be a complementary theory of Keynes’s analysis which is considered incomplete because it does not discuss solutions to address economic problems in the long term. Analysis in the theory of Harrod ‘s growth model Dommar analyzed the terms or conditions that should occur in the economy to ensure that production increases yearly. Therefore, Harrod-Dommar explained that to maximize available capital and aggregate demand, it must increase in line with the capacity of capital goods formed due to past investments. Thus, good economic growth is characterized by investment values that always increase every year. In simple terms, the Harrod-Dommar growth theory model can be written in the form . Based on this equation, it can be concluded that a positive relationship occurs between national income and the saving ratio if there is an increase in GDP so that the saving ratio will increase. Harrod-Domar explained that increasing economic growth is straightforward, namely by saving or investing as much as possible, and the rate of economic growth will increase.

2.3. Banking performance ratio

There are various banking performance ratios covering capital, assets, equity, and liquidity. One of the banking performance ratio measurements on the capital aspect is the Capital Adequacy Ratio (CAR). The capital aspect is essential for a bank because sufficient capital can support the acquisition of good profitability. Bank’s capital positively influences banking profitability, so banks will regulate the amount of retained earnings by regulating the amount of profit distribution as dividends to shareholders. The goal is that the retained earnings will be used as additional capital for banks (Abbas et al., Citation2019, Citation2020; Abbas et al., Citation2021). Buchs and Mathisen (Citation2005) explained that the Capital Adequacy Ratio (CAR) is a ratio used to determine the strength of capital owned by banks and the ability to cover risks from the business being carried out and protect the interests of customers. Thus, CAR can also be said to be a ratio that can measure the extent to which banks can cover declining assets with their equity. The higher the CAR value of a bank, the better the bank’s condition. The CAR ratio is essential because sufficient capital is an important variable for a business, especially in banking, which uses other people’s funds for operations (Umoh, Citation1991). In addition, capital adequacy also determines the scope of operational costs that can be incurred by banks (Onoh, Citation2002).

The following banking performance ratio is also determined from the aspect of asset quality which can be determined by the Nonperforming ratio Loans (NPLs). This ratio is essential for banks because this ratio is related to the high or low level of nonperforming loans owned by a bank. Nonperforming loans are identified as a factor that limits the effectiveness of banking in encouraging economic growth in many countries (Boudriga et al., Citation2010). Non-Performing Loan (NPL) has various definitions in each country. However, according to the IMF (Citation2004), NPL can occur if a loan experiences problems related to payments (principal and/or interest) that are due but have not been repaid within 90 days. The cause of NPLs is usually due to a lack of adequate supervision and control from banks, a lack of practical lending resources, weak legal infrastructure, and a lack of an efficient debt recovery strategy (Adhikari, Citation2007). A bank’s NPL level will ultimately affect profitability (Alam et al., Citation2015; Hossain, Citation2018; Laveena & Kumar, Citation2016).

Another banking performance ratio is related to the measurement of earnings and efficiency of a bank. The ratio is usually Return on Equity, Assets, and BOPO. Returns Ratio on Assets (ROA) and return on Equity (ROE) are two valuable measures for assessing the financial performance of a company (Pointer & Khoi, Citation2019). ROA focuses on measuring the efficiency of using the assets of an organization to generate revenue. In contrast, ROE focuses on the effectiveness of a company in using equity to generate income related to the health of the company (McClure, Citation2018). Thus, the higher the value of the ROA and ROE of the company indicates that the company’s condition is improving. Abbas et al. (Citation2012) found that the results of research on commercial banks in Pakistan with high levels of assets and equity tend to have better financial performance compared to commercial banks with low levels of assets and equity. The BOPO ratio measures the banking performance ratio in terms of banking efficiency. The BOPO ratio is the ratio of the total operating expenses to the bank’s operating income (Zainal et al., Citation2013: 480). The smaller the value of the BOPO ratio shows, the high efficiency of a bank. According to SE Bank Indonesia Number 6/23/DPNP/2004, the standard of the BOPO ratio is around 94% −96%. Thus, if the BOPO ratio is higher than the specified standard, it indicates that the bank is not efficient in carrying out its business activities, and vice versa if the BOPO ratio is less than 94%, then the bank is efficient in carrying out its business activities.

The last banking performance ratio is related to measuring bank liquidity. This ratio is a ratio that is no less important than other ratios. This is because this liquidity-related ratio can determine the level of banking’s ability to fulfil its short-term obligations. Banking performance ratios related to banking liquidity can be measured using Loan to Deposit Ratio (LDR) and Customer Deposits. The LDR ratio is the managers’ goal and is included in bank reports at the central bank or the Financial Services Authority in Indonesia (Manurung et al., Citation2020). The bank’s LDR ratio is influenced by several internal factors such as NIM, NPL, CAR, Risk Adjusted Return on Capital, Risk and Market Power (Mayliza et al., Citation2020; Mujeri & Younus, Citation2009; Naïmy , Citation2012; Nikolov & Popovska-Kamnar, Citation2016; Kumar & Anjum, Citation2019) as well as external factors such as exchange rates, oil prices, cement consumption, and FED rates (Sufian, Citation2011). Customer deposit is the number of customer funds deposited at a particular bank. This customer deposit can be a funding component to manage the bank so that it is even better at achieving predetermined goals and becomes a determinant of the organization’s leading performance indicators and customer satisfaction (Manurung et al., Citation2020).

2.4. Hypothesis development

The economic shock caused by the COVID-19 pandemic has impacted the banking sector’s performance. BPS data shows that in 2020 Indonesia’s economic growth fell to −2.07, and in 2021 it increased to 3.69, although this economic growth was still deficient compared to 2015–2019. This is because Law Number 10 of Citation1998 concerning banking in article 1 explains that “a bank is a business entity that collects funds from the public in the form of savings and distributes them to the public in the form of credit and or other forms in order to improve the standard of living of the people ”. Thus, when the country’s economy is shaken, it will impact banking performance.

The impact of economic shocks on banking performance is also supported by the arguments in Harrod-Domar ‘s theory of economic growth and contingency theory. Analysis in the theory of Harrod ‘s growth model Dommar analyzed the terms or conditions that should occur in the economy to ensure that production increases every year. Harrod-Dommar explained that to maximize available capital and aggregate demand, it must increase in line with the capacity of capital goods formed due to past investments. Thus, good economic growth is characterized by investment values that always increase every year. Harrod-Domar explained that increasing economic growth is straightforward, namely by saving or investing as much as possible, and the rate of economic growth will increase. Based on this explanation, when economic growth declines, it is inevitable that saving and investment activities will also be disrupted.

Another argument related to the impact of the COVID-19 pandemic on banking performance is the contingency theory argument. The general axiom of contingency theory is that organizations should have internal features with high compatibility with environmental demands in order to achieve the best adaptation in other words, it can be said that there is no universally superior strategy, regardless of environmental or corporate context (Lawrence & Lorsch, Citation1967; Scott, Citation1987; Venkatraman, Citation1989). This axiom of contingency theory can be rationally accepted because there are too many variables related to organizational structure, external environment, and internal organization. Therefore, the design of each organization varies based on the level of environmental stability, where the corporate structure has two types, namely the mechanistic system, which is suitable for a stable environment and the organic system, which is required in a changing environment (dynamic environment).

When the COVID-19 pandemic hit Indonesia, the business environment experienced enormous uncertainty due to a policy limiting community activities through social and physical implementation distancing to reduce the growth rate of COVID-19 cases in Indonesia. This policy ultimately led to significant changes in all community activities, where most activities were carried out online and at home. In the end, this condition impacted the Indonesian economy in 2020–2021. Thus, the banking world needs to adjust quickly to respond to uncertain conditions. In this condition, not all banks are ready to provide a system to adapt to the new business environment due to the COVID-19 pandemic, causing a possible shock to banking performance.

The argument for the impact of COVID-19 on banking performance in Indonesia from the contingency theory and the Harrod-Dommar theory of economic growth has been tried to be examined by several previous studies such as (Anitha, Citation2021; Haider & Mohammad, Citation2022; Kunt et al., Citation2021; Tanor & Purba, Citation2022; Xiazi & Shabir, Citation2022). The results of research that has been conducted show that the COVID-19 pandemic has negatively impacted the financial performance of banking companies in several countries (Anitha, Citation2021; Haider & Mohammad, Citation2022; Kunt et al., Citation2021; Xiazi & Shabir, Citation2022). However, research from Tanor and Purba (Citation2022) tried to test the financial performance of pharmaceuticals in Indonesia before and during the COVID-19 pandemic but found no adverse effects. Based on this explanation, the research model (Figure ) and research hypothesis is as follows:

H1: There are significant differences between the financial performance in terms of banking capital in Indonesia before and during the COVID-19 pandemic

H2: There are significant differences between the financial performance in terms of the quality of banking assets in Indonesia before and during the COVID-19 pandemic

H3: There are significant differences between the financial performance in terms of earnings and banking efficiency in Indonesia before and during the COVID-19 pandemic

H4: There are significant differences between the financial performance in terms of banking liquidity in Indonesia before and during the COVID-19 pandemic

Figure 2. Research Model.

3. Method

3.1. Types of research

This research is quantitative research to find answers to the research problem formulation. The quantitative approach used in this study is used to answer whether or not there was a significant difference in the performance of banks listed on the Indonesia Stock Exchange before the COVID-19 pandemic occurred and during the COVID-19 pandemic from 5 aspects, namely capital, asset quality, earnings and efficiency, liquidity, and market value.

3.2. Research data

The data used in this study is secondary data, where the data used are annual reports from banks listed on the Indonesia Stock Exchange. The annual banking reports used in this study are the annual banking reports for 2018, 2019, 2020 and 2021. The 2018 and 2019 annual reports will be used to determine banking performance two years before the pandemic, while the 2020 and 2021 annual banking reports will be used to determine performance during the COVID-19 pandemic. The data used in this study comes from the Indonesia Stock Exchange’s official website or banking websites. The data collection technique used in this study is the documentation technique of the annual reports of banking companies listed on the Indonesia Stock Exchange. The list of banks used in this study are 42 banks.

4. Variable operational definitions

This study uses several variables to measure banking financial performance: CAR, NPL, Gross NPL, ROE, ROA, BOPO, LDR, and Customer Deposits. The operational definitions of variables in this study are as follows

1) Capital aspect

the aspect of banking capital will be measured using several measurements, namely the Capital Adequacy Ratio (CAR). CAR is a ratio that measures the adequacy of bank capital or the ability of banks related to capital to cover possible losses in credit or securities trading (Wardiah, Citation2013: 295). The CAR ratio is calculated by dividing total capital by RWA, where RWA is the total value of the bank’s assets after each, multiplied by the risk weight from 0% to 100%. The mathematical method for calculating CAR from banks is as follows (Wardiah, Citation2013: 295):

2) Asset quality aspects

The aspect of banking asset quality will be measured using several measurements, namely Non- Performing Loan (Net) and NPL to Gross Ratio loans. NPL is a ratio that describes the occurrence of problems in credit, which means that customers cannot make credit payments (principal and/or interest) that are due but have not made payments within 90 days. The way to calculate Net and Gross NPLs is as follows:

3) Earning and efficiency aspects

aspects of earning and banking efficiency will be measured using several measurements, namely Return on Equity (ROE), Return on Assets (ROA), and BOPO. ROA focuses on measuring the efficiency of using the assets of an organization to generate revenue. In contrast, ROE focuses on the effectiveness of a company in using equity to generate income related to the health of the company (McClure, Citation2018). While the BOPO ratio is the ratio of the total operating expenses to the bank’s operating income (Zainal et al., Citation2013: 480). The calculation of the ROE, ROA and BOPO ratios is as follows (Abbas et al., Citation2019, Citation2022):

4) Liquidity aspect

the aspect of banking capital will be measured using several measurements, namely the Loan Deposit Ratio and Customer Deposits. The LDR ratio is the managers’ goal and is included in bank reports at the central bank or the Financial Services Authority in Indonesia (Manurung et al., Citation2020). This customer deposit can be a funding component to manage the bank so that it is even better at achieving predetermined goals and becomes a determinant of the organization’s leading performance indicators and customer satisfaction (Manurung et al., Citation2020). The formula for calculating loan to Deposit Ratio and Customer Deposit are as follows:

5. Data analysis technique

The data analysis technique used in this study is descriptive statistics, data normality test, and independent t-test different test. Descriptive statistical tests in this study were used to describe the collected research data, including the minimum, maximum, mean and standard deviation values. The data normality test in this study was carried out to ensure that the research data that had been collected had a normal data distribution. The data normality test was performed using the Kolmogorov test Smirnov. Furthermore, the difference test in this study was determined from the results of the normality test produced, if the test results stated normal, then the independent t-test would be used, but if the test results found abnormal results, then the Mann -Whitney test would be used. The different test in this study was used to determine whether there was a significant difference in banking performance on the IDX before and during the COVID-19 pandemic. Decision-making on the independent t-test is based on a significance value of 5%.

6. Results and analysis

6.1. Description of the research sample

The population in this study are banks in Indonesia. The sample for this research is banks listed on the Indonesia Stock Exchange and state and regional government-owned banks during 2018–2021. Thus, the number of banks included in this study was 51 during 2018–2021, so the number of observations made was 205. The research sample selection process is as follows (Table ).

Table 1. Sampling Process

6.2. Descriptive statistics

This section describes the results of the descriptive statistical tests that have been carried out in this study. The following table presents the results of sampling process and the descriptive statistical tests that have been carried out.

Table bellow shows the results of the descriptive statistical tests that have been carried out in this study. The capital Adequacy variable Ratio (CAR) in this study is a proxy to measure the level of capital of banks in Indonesia. The highest CAR value was 0.72, which Bank OK owned in 2018, and the lowest value was 0.01 for Bank Capital in 2018, while the average bank CAR value from 2018–2021 was 0.25. The standard value for a banking ratio is said to be in a healthy condition if it is more than 0.08. Thus, in general, when viewed from the average CAR value, banks in Indonesia during 2018–2021 were in a healthy condition based on the CAR value.

Table 2. Descriptive Statistical Test Results

The descriptive statistical tests also show the results for the NPL and gross NPL variables. These two variables are proxies to measure the level of assets in banking. The highest value for NPL is 0.08, namely for bank Mega in 2021, and the lowest value is −0.03, namely for bank Amar in 2019. While the highest value for gross NPL is 0.3, namely bank DKI in 2021, and the lowest value is 0.00, namely bank capital in 2020 and 2021. Furthermore, the average banking NPL and gross NPL values during 2018–2021 were 0.033 and 0.07. The results of the descriptive statistical tests that have been carried out show that, generally, the NPL value of banks in Indonesia during 2018–2021 is still below 10%. Therefore, banking health in Indonesia during 2018–2021 is generally still in good condition.

Variables in this study are also used to proxy the quality of earnings generated by banks during the 2018–2021 period. The highest value for ROE is 0.31, namely the BTPN Syariah bank in 2019, and the lowest score is −0.61, namely the Banten bank in 2019. Meanwhile, the highest value for ROA was 0.14, namely the BTPN Syariah bank in 2019, and the lowest value was −0.09, namely the QNB bank in 2019. In general, the average ROE and ROA values of banks in Indonesia during 2018–2021 were 0.07 and 0.015. Thus, when viewed from the average value of ROE and ROA, the banking condition can still be healthy because it is still greater than 0.

The BOPO variable is a proxy for measuring banks’ efficiency level in Indonesia during 2018–2021. The table shows that the highest BOPO score was 2.28 for QNB banks in 2021, and the lowest score was 0.52 for Mestika bank in 2021. Meanwhile, the average BOPO score is 0.876. Based on this, in general, based on the average score from BOPO, it is known that banking in Indonesia during 2018–2021 was in an efficient condition because it was less than 0.94.

The LDR and customer deposit variables are proxies for measuring the level of liquidity of Indonesian banking during 2018–2021. The table shows that the highest value of LDR is 1.62, namely bank Woori Saudara in 2020, and the lowest value is 0.12, namely bank Capital in 2021, while the average value is 0.857. Furthermore, the highest value for customer deposits is 20.85, namely bank BRI in 2021, and the lowest value is 11.75, namely bank Artha Graha in 2021. Furthermore, the average value for the customer deposit variable is 16.835. Based on the descriptive statistical test results, it can be seen from the average LDR value obtained; it can be concluded that the banking conditions are in liquid condition.

6.3. Performance analysis before vs during the COVID-19 pandemic

Analysis of banking performance before and during the COVID-19 pandemic in this study was carried out by conducting paired sample t-test. The differential test is carried out after the normality test is carried out to ensure that the research data to be tested has a standard data distribution or not. The results of the normality test in this study are as follows (Table ).

Table 3. Normality Test

The next test carried out was a different test related to banking performance in Indonesia before and during the COVID-19 pandemic. The following table presents the different tests that have been carried out using the paired sample t-test.

Table above shows the results of the paired sample t-test correlation test that has been carried out. Table shows that the CAR, Gross Loan, ROE, ROA, BOPO, LDR, and Customer Deposit variables before and during the COVID-19 pandemic had a strong and positive correlation, however, there was no correlation for the NPL variable.

Table 4. Paired Samples Correlations

Table above shows that the CAR and LDR measures have a significant value at the 1% level. In contrast, the ROE, ROA, and BOPO measures have a significant value at the 5% level, and the NPL, gross NPL, and customer deposits are found to be insignificant. Thus, it can be concluded that there were significant differences in banking performance in Indonesia before and during the COVID-19 pandemic in terms of CAR, ROE, ROA, BOPO, and LDR aspects. Table shows that the average for each ratio after the presence of COVID-19 is smaller than before the presence of COVID-19, so that the mean value for each ratio becomes negative.

Table 5. Paired Sample t-test Result

The results of this study indicate that there is an impact of the COVID-19 pandemic on banking performance. Thus, the results of this study support the arguments in Harrod-Domar’s theory of economic growth and contingency theory. The study results show that banking financial performance in the capital, earnings and efficiency, and liquidity experienced significant differences before and during the COVID-19 pandemic. These results follow the explanation from Harrod ‘s growth model theory Dommar that the increase in economic growth is related to the savings and investments made. During the COVID-19 pandemic, the economy in Indonesia was in turmoil marked by negative economic growth, which showed that the funds circulating in the community were significantly reduced, which in the end would have an impact on the savings in banks. The limited input of capital from the public causes banks to experience the problem of limited funds, which in turn disrupts their financial performance.

The results of this study also support other arguments from the contingency theory. The general axiom of contingency theory is that organizations should have internal features with high compatibility with environmental demands in order to achieve the best adaptation in other words, it can be said that there is no universally superior strategy, regardless of environmental or corporate context (Lawrence & Lorsch, Citation1967; Scott, Citation1987; Venkatraman, Citation1989). During the COVID-19 pandemic that hit Indonesia, the level of uncertainty that occurred in the banking business environment became very large. This is due to the existence of various policies limiting community activities through social and physical implementation distancing to reduce the growth rate of COVID-19 cases in Indonesia. This policy ultimately led to significant changes in all community activities, forcing the banks to also overhaul the operational system of existing business activities. Banking unpreparedness and rapid environmental changes ultimately disrupted banking performance.

The results of this study have implications for stakeholders in the banking industry. The research results show that the COVID-19 Pandemic has had a profound impact on aspects of banking capital. This needs to be a concern for all parties because capital is related to the achievement of banking performance. Bank’s capital positively influences banking profitability, so banks will regulate the amount of retained earnings by regulating the amount of profit distribution as dividends to shareholders. The goal is that the retained earnings will be used as additional capital for banks (Abbas et al., Citation2019, Citation2020; Abbas et al., Citation2021). Therefore, these results provide input for the need to regulate the amount of capital in accordance with post-Covid-19 pandemic conditions. Moudud-Ul-Huq et al. (Citation2022) explained that the COVID-19 pandemic had a negative impact on banks, thus demanding more capital to reduce existing risks. Abbas et al. (Citation2019) also believes that bank capital has a positive effect on banking performance, especially to strengthen banking performance in times of crisis.

The next implication of the results of this research is to provide insight to banks to always pay attention to their liquidity conditions. This is because the level of banking liquidity has an impact on the ability of banks to pay off existing short-term obligations to third parties and customers. Abbas et al. (Citation2020) explained that banking liquidity has a positive impact on banking capital. Therefore, banks must be able to maintain liquidity and capital conditions in order to produce good performance and reduce banking risk.

Several studies that have been conducted show that the COVID-19 pandemic has hurt the financial performance of banking companies in several countries (Anitha, Citation2021; Haider & Mohammad, Citation2022; Kunt et al., Citation2021; Xiazi & Shabir, Citation2022). The results of this study regarding the impact of COVID-19 on banking performance in Indonesia are in accordance with several previous studies. However, the results of this study provide new evidence from an Indonesian perspective that is different from research from Tanor and Purba (Citation2022).

7. Conclusion

The results of research conducted on 205 observations from banks in Indonesia from 2018 to 2021 show that the COVID-19 pandemic has had a significant impact on banking performance. This is indicated by the existence of a significant influence on several aspects of financial performance, including capital, earnings, and liquidity. Banking performance in these three aspects has proven to have significant differences between before and during the COVID-19 pandemic. Therefore, based on the research results obtained, banks need to improve their performance during the post-Covid-19 pandemic to improve performance in the next period. In addition, the government, represented by the Financial Services Authority and Bank Indonesia, must also pay special attention to several banks that are suspected of experiencing financial difficulties based on their financial ratios as a result of the COVID-19 pandemic attack. This is done with the aim that there is no bank collapse that can harm customers and reduce the quality of the country’s economy.

The results of this study have implications for stakeholders in the banking industry. The research results show that the COVID-19 Pandemic has had a profound impact on aspects of banking capital. This needs to be a concern for all parties because capital is related to the achievement of banking performance. These results provide input for the need to regulate the amount of capital in accordance with post-Covid-19 pandemic conditions. The next implication of the results of this research is to provide insight to banks to always pay attention to their liquidity conditions. This is because the level of banking liquidity has an impact on the ability of banks to pay off existing short-term obligations to third parties and customers. Therefore, banks must be able to maintain liquidity and capital conditions in order to produce good performance and reduce banking risk.

The results of this study can be used as a reference source for further research by taking into account some of the shortcomings they have. As for some of the shortcomings that are owned in this study first, there are several banks that need to present complete research data so that it reduces the number of observations made to decrease because the number of companies with incomplete data is quite a lot. Thus, further research is expected to add to the number of years of research to increase the variation in the existing data. The second limitation is that the results of this study only include measures of banking performance that can be measured financially. Future research is expected to be able to add to banking performance which is measured non-financially so that it can be seen whether the COVID-19 pandemic has also had an impact on banking non-financial performance.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Susanti

Susanti, S.Pd. M.Si – is a lecturer with a doctorate degree in the Accounting Education Study Program, Faculty of Economics and Business, UniversitasNegeri Surabaya. The focus of researches are financial literacy, banking, taxation and information systems. This article is one of the research projects entitled banking in the era of the COVID-19 pandemic.

Rediyanto Putra

Rediyanto Putra, SE., MSA – is a lecturer with a Master of Accounting degree. Rediyanto Putra has a research focus in the fields of financial accounting, capital markets and banking. This article is one of the researchprojects entitled banking in the era of the COVID-19 pandemic.

Moh. Danang Bahtiar

Moh. Danang Bahtiar, S.Pd., M.Pd – is a lecturer with a Master ofEducation degree. Moh. Danang has a research focus in the fields of taxation and banking. This article is one of the research projects entitled banking in the era of the COVID-19 pandemic.

References

- Abbas, F., Ali, S., & Ahmad, M. (2021). Does economic growth affect the relationship between banks' capital, liquidity and profitability: Empirical evidence from emerging economies. Journal of Economic and Administrative Sciences. https://doi.org/10.1108/JEAS-03-2021-0056

- Abbas, F., Ali, S., Yousaf, I., & Wong, W. K. (2022). economics of risk-taking, risk-based capital and profitability: Empirical evidence of Islamic Banks. Asian Academy of Management Journal of Accounting and Finance, 18(1), 1–15. https://doi.org/10.21315/aamjaf2022.18.1.1

- Abbas, F., Iqbal, S., & Aziz, B. (2020). The role of bank liquidity and bank risk in determining bank capital: Empirical analysis of asian banking industry. Review of Pacific Basin Financial Markets and Policies, 23(3), 2050020. https://doi.org/10.1142/S0219091520500204

- Abbas, F., Iqbal, S., Aziz, B., & Yang, Z. (2019). The impact of bank capital, bank liquidity and credit risk on profitability in postcrisis period: a comparative study of US and Asia. Cogent Economics & Finance, 7(1), 1–18. https://doi.org/10.1080/23322039.2019.1605683

- Abbas, F., Tahir, M., & Rahman, M. (2012). A comparison of financial performance in the banking sector: Some evidence from Pakistani commercial banks. Journal of Business Administration and Education, 1(1), 1–14. http://www.infinitypress.info/index.php/jbae/article/view/4

- Adhikari, B. K. (2007). Nonperforming loans in the banking sector of Bangladesh: Realities and challenges. BIBM, 8(1), 75–95.

- Alam, S., Haq, M. M., & Kader, A. (2015). Nonperforming loan and banking sustainability: Bangladesh perspective. International Journal of Advanced Research, 3(8), 1197–1210.

- Anitha, S. (2021). A study on banking sector performance during Covid-19 pandemic period with special. Journal of Emerging Technologies and Innovative Research (JETIR), 8(9), 560–568.

- Badan Pusat Statistik. (2022). Berita Resmi Statistik Badan Pusat Statistik 2022. https://www.bps.go.id/website/materi_ind/materiBrsInd-20220509115801.pdf

- Baral, K. J. (2005). Health check-up of commercial banks in the framework of CAMEL: A case study of joint venture banks in Nepal. Journal of Nepalese Business Studies, 2(1), 41–55. https://doi.org/10.3126/jnbs.v2i1.55

- Boudriga, A., Boulila Taktak, N., & Jellouli, S. (2010). Banking supervision and nonperforming loans: A cross-country analysis. Journal of Financial Economic Policy, 1(4), 286–318. https://doi.org/10.1108/17576380911050043

- Buchs, T., & Mathisen, J. (2005). Competition and efficiency in banking: Behavioral evidence from Ghana. IMF Working Paper WP/05/17, African Department

- Cole, R. A., & Gunther, J. A. (1995). A CAMEL Rating’s Shelf Life.MPRA Paper No. 24693, Retrieved from http://mpra.ub.uni-muenchen.de/24693/

- Gasbarro, D., Sadguna, I., & Zumwalt, J. (2002). The changing relationship between CAMEL ratings and bank soundness during the Indonesian banking crisis. Review of Quantitative Finance and Accounting, 19(3), 247–260. https://doi.org/10.1023/A:1020724907031

- Haider, J., & Mohammad, K. U. (2022). The effect of Covid-19 on bank profitability determinants of developed and developing economies. IRASD Journal of Economics, 4(2), 187–203. https://doi.org/10.52131/joe.2022.0402.0072

- Hossain, M. T. (2018). The trend of default loans in Bangladesh: Way forward and challenges. International Journal of Research in Business Studies and Management, 5(6), 24–30.

- IMF. (2004) Global financial stability report, April 2004: Market developments and issues: International monetary fund

- Kumar, S., Anjum, B., & Nayyar, S. (2019). Financing decisions: study of pharmaceutical companies in India. International Journal of Marketing, Financial Services & Management Research, 1(1), 14–28. https://doi.org/10.15373/22778179/OCT2013/23

- Kunt, A. D., Pedraza, A., & Ortega, C. R. (2020). Banking sector performance during the Covid-19 Crisis. Ymer, 21(7), 213–227. https://doi.org/10.37896/YMER21.07/16

- Kunt, A. D., Pedraza, A., & Ortega, C. R. (2021). Banking sector performance during the COVID-19 crisis. Journal of Banking and Finance, 133(January), 1–22. https://doi.org/10.1016/j.jbankfin.2021.106305

- Laveena, & Kumar, H. (2016). Management of nonperforming assets on the profitability of public and private sectors banks. International Journal of Research in Management & Technology, 6(2), 86–93.

- Lawrence, P. R., & Lorsch, J. W. (1967). Differentiation and integration in complex organizations. Administrative Science Quarterly, 12(1), 1–47. https://doi.org/10.2307/2391211

- Manurung, A. H., Hutahayan, B., Deniswara, K., & Kartika, T. R. (2020). Determinant of net interest margin in Indonesia bank moderated by risk. International Journal of Advanced Science and Technology, 29(5), 11317–11328. https://www.researchgate.net/publication/342305670_Determinantof_Net_Interest_Margin_in_Indonesia_Bank_Moderated_by_Risk

- Mayliza, C. S., Manurung, A. H., & Hutahayan, B. (2020). Analysis of the effect of financial ratios to probability default of Indonesia’s coal mining company. Journal of Applied Finance and Banking, 10(5), 167–179. https://search.proquest.com/docview/2404395300?accountid=17242

- McClure, B. (2018). How ROA and ROE give a clear picture of corporate health. Investopedia. http://Retrieved from www.investodpedia.com on July 18, 2019.

- Moudud-Ul-Huq, S. K., Chowdhury, M. A. F. M., Sohail, H., Biswas, T., & Abbas, F. (2022). How do banks’ capital regulation and risk-taking respond to COVID-19? Empirical insights of ownership structure. International Journal of Islamic and Middle Eastern Finance and Management, 15(2), 406–424. https://doi.org/10.1108/IMEFM-07-2020-0372

- Mujeri, M. K., & Younus, S. (2009). An analysis of interest rate spread in the banking sector in Bangladesh. Bangladesh Development Studies, 32(4), 1–33.

- Naïmy, V.Y. (2012). Gaussian copula vs loans loss assessment: A simplified and Easy-To-Use model. Journal of Business & Financial Affairs, 01(03), 1–5. https://doi.org/10.4172/2167-0234.1000105

- Nair, S. T. G., & Asghede, S. Y. (2015). CAMELS and bank performance measurement: A case study of bank of Baroda. International Journal of Banking, Risk and Insurance, 3(1). https://doi.org/10.21863/ijbri/2015.3.1.001

- Nam, C. H., & Tatum, C. B. (1988). Major characteristics of constructed products and resulting limitations of construction technology. Construction Management and Economics, 6(2), 133–147. https://doi.org/10.1080/01446198800000012

- Nikolov, M. ;, & Popovska-Kamnar, N. (2016). Determinants of NPL growth in Macedonia. Journal of Contemporary Economic and Business Issues, 3(2), 5–18. http://hdl.handle.net/10419/193465

- Onoh, J. K. (2002). Dynamics of money, banking and finance in Nigeria: An emerging market. Astra Meridian Publishers.

- Pointer, L. V., & Khoi, P. D. (2019). Predictors of return on assets and return on equity for banking and insurance companies on Vietnam stock exchange. Entrepreneurial Business and Economics Review, 7(4), 185–198. https://doi.org/10.15678/EBER.2019.070411

- President of the Republic of Indonesia. (1998). Law Number 7 Year 1992 about Banking.

- Republika. (2022). Lima Tahun OJK: Tantangan Perbankan di Tengah Pandemi Covid-19. https://www.republika.co.id/berita/r94fma440/lima-tahun-ojk-tantangan-perbankan-di-tengah-pandemi-covid19

- Scott, W. R. (1981). Organizations: Rational, Natural, and Open Systems. Pearson Education, Inc.

- Scott, W. R. (1987). Organizations: Rational, Natural and Open Systems. NJ, Prentice Hall.

- Staynov, S., & Baumgarter, K. (1986). Long-term perspectives for human settlements development in the ECE Region: Economic Commission of Europe (1986). United Nations.

- Sufian, F. (2011). Financial depression and the profitability of the banking sector of the Republic of Korea: Panel evidence on bank-specific and macroeconomic determinants. Asia-Pacific Development Journal, 17(2), 65–92. https://doi.org/10.18356/1025290d-en

- Tanor, L. A. O., & Purba, P. M. (2022). Before and During the COVID-19 Pandemic : Indonesia ’ s Pharmaceutical Financial Performance Analysis. 03045.

- Tarigan, R. (2005). Ekonomi Regional Teori dan Aplikasi Edisi Revisi. PT Bumi Aksara.

- Thompson, J. D. (1967). Computers can tell you what will happen before it happens. Modern Hospital, 109(6), 102–105.

- Umoh, P. (1991). Capital standards and bank deposit insurance scheme. NDIC Quarterly, 1(2), 18–25.

- Venkatraman, N. (1989). Strategic Orientation of Business Enterprises: The Construct, Dimensionality, and Measurement. Management Science, 35(8), 942–962. https://doi.org/10.1287/mnsc.35.8.942

- Wardiah, M. L. (2013). Dasar-dasar Perbankan. Pustaka Setia.

- World Health Organization, 2022 WHO Coronavirus (COVID-19) Situation by Region, Country, Territory & Area Accessed 10 august 2022 https://covid19.who.int/table

- Xiazi, X., & Shabir, M. (2022). Coronavirus pandemic impact on bank performance. Frontiers in Psychology, 13(October). https://doi.org/10.3389/fpsyg.2022.1014009

- Zainal, V. R., Basir, S., Sudarto, S., & Veithzal, A. P. (2013). Commercial Bank Management Manajemen Perbankan Dari Teori Ke Praktik. Rajawali Press. https://opac.perpusnas.go.id/DetailOpac.aspx?id=853705