?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines whether conventional bank lending rates influence Islamic bank financing rates in Indonesia and Malaysia that apply the dual-banking system. We employ the ARDL, the non-linear ARDL (NARDL) model, and the Pooled Mean Group (PMG). Evidence of the long-run link between Islamic financing rate and conventional lending rate is found. However, instead of symmetry, the link between them is asymmetry. The asymmetric pricing of the Islamic financing rate and some specific contracts such as Mudharaba and Murabaha rates in Indonesia strongly follow the decrease in conventional lending rate, but it is sticky against the increase in conventional lending rate. The asymmetric pricing of the Islamic financing rate in Malaysia is obviously pegged to the conventional lending rate. The PMG results strengthen the asymmetric findings where the effect of a reduction in the conventional lending rate is larger than the effect of an increase in the conventional lending rate on the Islamic financing rate. These findings imply that Islamic bank borrowers are profit-driven borrowers in a dual-banking system. Accordingly, the Islamic financing rate is pushed to follow the conventional lending rate due to the uncompetitive Islamic financing rate.

Public Interest Statement

Indonesia and Malaysia are large Muslim countries that practice dual-banking systems consisting of conventional and Islamic banks. However, the market share of Islamic banks is relatively small. Accordingly, the products and services of Islamic banks in both countries may resemble those of conventional banks due to the established and dominated conventional banks. Hence, it is interesting to examine the response of Islamic financing rates to conventional lending rates in Indonesia and Malaysia. Our findings clearly indicate that the Islamic financing rates strictly follow the conventional lending rates in the dual-banking system.

1. Introduction

The biggest financial sector in the Islamic finance industry is Islamic banking, with a total asset of 2.349 US$ trillion, which accounted for 70% of Islamic finance industry assets in 2020. However, the fast growth of Islamic banking also received a lot of criticism for countries that practice the dual-banking system (Chong & Liu, Citation2009; Hamza, Citation2016; Khan, Citation2010; Sukmana & Ibrahim, Citation2017). First, Islamic bank products are like conventional banking products by modifying them according to shariah complaints because consumers’ Islamic banks are accustomed to products of conventional banks in a dual banking environment (Azmat et al., Citation2015; Khan, Citation2010). Second, Islamic bank claims to use a system of participation through the PLS contracts, but in practice, the PLS portion of both Mudharaba and Musharaka is smaller compared to Murabaha using the profit margin like the debt-like financing (Warninda et al., Citation2019). For instance, the shares of Musharaka and Mudharaba contracts to total financing in South East Asia were 5.60% and 11.28% in 2021, respectively. Lastly, the pricing of Islamic products tends to refer to conventional banks’ interest rates (Chong & Liu, Citation2009).

Theoretically, the products of Islamic banks should be interest-free and asset-linked instead of interest-based. Yet, empirical studies documented a strong relationship between the products of Islamic banks and interest rates. Some previous studies documented that the conventional deposit rate affects the Islamic deposit rate (Chong & Liu, Citation2009; Kasri & Kassim, Citation2009; Saeed et al., Citation2021; Saraç & Zeren, Citation2015; Sukmana & Ibrahim, Citation2017). The existing empirical studies also found that the interest rate negatively influences Islamic deposits, known as Displaced Commercial Risk (DCR) (Abduh, Citation2015; Widarjono et al., Citation2022a). The earlier studies also investigated the symmetric impact of conventional lending rates on Islamic financing rates for Malaysian cases and found that conventional lending rates strongly affect Islamic financing rates (Saeed et al., Citation2021).

This study examines the influence of conventional bank lending rate (CLR) on the Islamic bank financing rate (IFR) effects in Indonesia and Malaysia, employing the symmetric and asymmetric impacts. There are several strong motivations for conducting this research. First, empirical studies on the link between conventional bank lending rates and Islamic bank financing rates are still rare. Second, Islamic bank financing consists of profit-loss sharing (PLS) and non-PLS. The prices of both contracts are obviously different. The former contracts are ex-post schemes, and accordingly, the price of these contracts depends on the profits or losses that occurred. Conversely, the latter contracts are ex-ante schemes like debt financing, so the prices follow a fixed cost. Therefore, this paper also distinguishes the relationship between CLR and PLS and non-PLS financing rates. Third, we also analyze the asymmetric response of IFR to CLR since Islamic bank consumers are profit-driven motives (Aysan et al., Citation2018; Cevik & Charap, Citation2015). Hence, IFR will asymmetrically respond if there is an increase or decrease in CLR. Fourth, the previous research only focused on one country (Saeed et al., Citation2021), while this research investigates the two countries so the findings can be generalized properly.

There is a strong justification for selecting Indonesia and Malaysia as our sample. Indonesia, the largest Muslim country in the world with a total population of 270 million, has been practicing Islamic banks since the 1990s. Meanwhile, with a total population of 33 million, which is also a largely Muslim country, Malaysia has been starting with the practice of Islamic banks much earlier in the 1980s. Nevertheless, the market share of an Islamic bank is relatively small, at 6% and 23% in Indonesia and Malaysia in 2020, respectively. Because of established and dominated conventional banks, products of Islamic banks in both countries may resemble products of conventional banks.

Our study may contribute to the existing empirical research in some ways. To the best of our knowledge, this study is the first study to investigate the asymmetric response of Islamic financing rates to their counterpart’s conventional lending rate. Second, this study also investigates the response of some specific Islamic financing rates comprising Mudharaba, Musharaka, and Mudharaba rates to conventional lending rates. Until now, existing empirical studies haven’t linked yet any Islamic bank financing products with conventional bank interest rates. Lastly, due to similar practices in Islamic banks in both countries, we also employ panel ARDL and NARDL using the asymmetric Pooled Mean Group (PMG) method to investigate further the link between the conventional lending rate and Islamic financing rate. Our study could boost the power of tests stemming from a single time series (Maddala & Wu, Citation1999).

2. Review of Literature

Islamic banks initially have been growing in Muslim countries. After practicing Islamic banks, however, some countries abolished conventional banks, such as Sudan and Pakistan, but some countries practice Islamic banks without terminating the conventional bank, such as Indonesia and Malaysia. In other words, some Islamic countries apply the dual-banking system with two monetary systems. With this dual-banking system, competition between Islamic banks and conventional banks is inevitable. As a result, Islamic bank provides products that are only imitations of conventional bank products (Azad et al., Citation2018; Azmat et al., Citation2015; Khan, Citation2010).

Several studies have examined whether the practice of Islamic banking was in accordance with Islamic principles that were free of interest rates. Islamic banks are expected to distribute their funds in the form of risk-sharing contracts such as Mudharaba and Musharaka, but in practice, Islamic banks offer many financing contracts in the form of non-PLS contracts (Aggarwal & Yousef, Citation2000; Baele et al., Citation2014;,Widarjono et al., Citation2022b). Murabaha contracts based on a margin scheme similar to the interest rate as fixed cost are preferred by Islamic banks because PLS contracts are likely to increase the financing risk because of asymmetric information, moral hazard, and adverse selection (Azmat et al., Citation2015; Sutrisno & Widarjono, Citation2018). In addition, Islamic deposits based on Mudharaba contracts indicate that the return of Islamic deposits has not fully reflected the PLS contract (Hamza, Citation2016).

The above fact occurs in countries that apply the dual-banking system. Firstly, consumers are accustomed to conventional bank products and secondly, consumer loyalty to Islamic bank products is questionable. As a result, consumers of Islamic banks are very responsive to changes in conventional bank interest rates. Several studies have shown a negative link between interest rates and Islamic bank deposits (Abduh, Citation2015; Kasri & Kassim, Citation2009; Kassim et al., Citation2009; Widarjono et al., Citation2022a). Therefore, when conventional bank interest rates increase, Islamic bank consumers take money back and then deposit their funds in conventional banks, which gives higher returns (Aysan et al., Citation2018; Ismal, Citation2011).

Accordingly, Islamic banks may employ interest rates as a benchmark in determining their Islamic bank rate in a dual-banking system. Numerous empirical studies found that Islamic deposit rates follow conventional deposit rates for Malaysian (Anuar et al., Citation2014; Chong & Liu, Citation2009; Saeed et al., Citation2021; Sukmana & Ibrahim, Citation2017; Zainol & Kassim, Citation2010), for Turkey (Cevik & Charap, Citation2015; Ergec & Kaytanci, Citation2014; Ergeç & Arslan, Citation2013; Saraç & Zeren, Citation2015), and for Indonesian (Kasri & Kassim, Citation2009). Furthermore, Saeed et al. (Citation2021), using the symmetric approach, found that the conventional lending rate persistently influences the Islamic financing rate in Malaysia. By contrast, some empirical studies documented that Islamic deposit rates are not associated with conventional deposit rates (Jawadi et al., Citation2016a, Citation2016b; Yuksel, Citation2017; Yusof et al., Citation2015). Furthermore, risk-sharing financing is interest rate-free for countries in which Islamic banks have a high market share, such as Saudi and Iran (Šeho et al., Citation2020).

The practice of interest rate as the benchmark for the Islamic bank rate also occurs in the Islamic money market. Its rate is strongly correlated and co-move with its counterpart conventional money market rate in the Malaysian money market (Bacha, Citation2008; Ito, Citation2013). Nechi and Smaoui (Citation2019) also documented the link between the Islamic interbank benchmark rate and the conventional interbank rate in five countries from the Gulf Cooperation Council. Conventional interbank rates also strongly affect Islamic interbank rates in some countries with dual-banking systems (Mohd Yusoff & Azhar, Citation2019). Moreover, in the global money market, there is evidence of the co-movement between the Islamic interbank benchmark rate (IIBR) and the London interbank offer rate (LIBOR) (Azad et al., Citation2018). However, this result is not lined with Tlemsani (Citation2020), who found a strong negative correlation between the IIBR and LIBOR, implying that the IIBR represents an alternative investment for international investors.

This study investigates the symmetric and asymmetric responses of Islamic financing to interest rates. Following the above review of literature, previous studies have not investigated the asymmetric relation between Islamic financing rates and interest rates. More importantly, we also investigate some specific Islamic financing rates, consisting of Musyaraka, Mudharaba, and Murabaha, where previous research has not addressed this issue yet.

3. Methodology and Data

3.1. Data

Our study examines the impact of conventional lending rates on Islamic financing rates in Indonesian and Malaysian banking. Islamic financing rate in both countries is the average financing rate of full-fledged Islamic banks and Islamic bank windows because data of full-fledged Islamic banks and Islamic bank windows are not available. The available data is the aggregate average data of Islamic bank financing rate in Indonesia and Malaysia. The conventional lending rate is the average lending rate of conventional banking in both countries. In addition, this study also investigates the effect of conventional lending rates for some specific Islamic financing rates, consisting of Mudharaba, Musharaka, and Murabaha rates in Indonesia. We don’t investigate those types of Islamic financing rates in Malaysia due to the unavailability of data. Our study employs the monthly time-series data, covering from January 2009 to December 2020.

The data for this empirical study are extracted from two sources. Indonesian Islamic bank financing rate data are from banking statistics published online by the Indonesian Financial Services Authority (www.ojk.go.id). Malaysian Islamic bank data are sourced from the Malaysian banking system and available online from the Bank Negara Malaysia (www.bnm.gov.my).

3.2. ARDL analysis

The price of Islamic products is close to the interest rate in the dual-banking system. Numerous studies report evidence of the link between the Islamic deposit and the conventional deposit rate (Chong & Liu, Citation2009; Kasri & Kassim, Citation2009; Saraç & Zeren, Citation2015; Sukmana & Ibrahim, Citation2017). Accordingly, the link between the Islamic financing rate and conventional lending rates likely occurs. Therefore, we investigate whether the conventional lending rate is a benchmark rate for the Islamic bank in determining the Islamic financing rate. Initially, our study forms the link between IFR and CLR in the long run as:

Where is the Islamic bank financing rate, and

is the conventional bank lending rate.

The long-run relationship in Equationequation (1)(1)

(1) can be tested using the cointegration approach. The ARDL model is employed to test for cointegration following Pesaran and Shin (Citation1998). The ARDL model is as follows:

where and

show the long-run coefficients,

and

represent the short-run coefficients, and

and

are the optimal lags. Our study employs the OLS method to estimate Equationequation (2)

(2)

(2) using the general-to-specific method by consecutively dropping insignificant lag to obtain the final model. The ARDL model stems from cointegration, showing the long-run relationship. We check the cointegration using two approaches. First, we test the null hypothesis of no cointegration

using

statistic (Banerjee et al., Citation1998). Second, we apply the bound testing approach by checking the null hypothesis of no-cointegration

(Pesaran et al., Citation2001). The long-run and short-run symmetric coefficients of the conventional deposit rate are calculated by

and

, respectively.

3.3. NARDL Analysis

Price asymmetry is a common symptom because cost rise is faster than cost fall (Bacon, Citation1991; Tappata, Citation2009). The empirical literature has shown the asymmetric price in various prices such as stock and oil prices (Kumar, Citation2019), consumer and oil prices (Widarjono & Hakim, Citation2019; Widarjono et al., Citation2020b), stock prices and exchange rates (Bahmani-Oskooee & Saha, Citation2018; Sheikh et al., Citation2020), consumer prices and exchange rates (Baharumshah et al., Citation2017), and interest and deposit rates (Apergis & Cooray, Citation2015; Holmes et al., Citation2015).

The existing empirical literature also documented the asymmetric link between the Islamic deposit and the conventional deposit rate (Sukmana & Ibrahim, Citation2017). EquationEquation (2)(2)

(2) indicates that the link between the IFR and CLR is symmetric. Accordingly, the relationship between the conventional lending rate and the Islamic financing rate is likely asymmetric. Therefore, we can express the long-run asymmetric relationship between them as:

where and

are an Islamic financing rate and a conventional lending rate, respectively. Variables

and

represent partial sums of positive and negative change in

with

and

.

We employ the non-linear ARDL (NARDL) model to explore the asymmetric response of the Islamic financing rate to changes in the conventional lending rate (Shin et al., Citation2014)

Based on Equationequation (4)(4)

(4) , the long-run asymmetric coefficients of positive and negative conventional lending rates are

and

, respectively, and the short-run asymmetric coefficients of positive and negative conventional lending rates are

and

.

We take some steps to estimate the NARDL model as in Equationequation (4)(4)

(4) . First, the OLS method is employed by utilizing the general-to-specific approach by consecutively eliminating insignificant lags. Second, our study performs the two cointegration tests by testing null hypothesis

following the

statistic (Banerjee et al., Citation1998) and null hypothesis

following the

statistic (Pesaran et al., Citation2001). Then, we test the asymmetric response of Islamic financing rates to conventional lending rates. The null hypothesis of the long-run asymmetry is

and for the short-run asymmetry, the null hypothesis is

. Lastly, our study graphs the asymmetric dynamic multiplier effect for every change in conventional lending rate

;

on Islamic financing rate (Shin et al., Citation2014) as:

3.4. Panel ARDL and NARDL

This study also applies the panel method to investigate the impact of conventional lending rates on Islamic financing rates for two countries as a group because of similar practices in Islamic banks. Two estimation methods could be employed to estimate the panel data. The first method is the common panel methods, such as the static method (fixed and random effects) and the dynamic method (IV and GMM methods). These models lead to the same parameters across countries but could provide inconsistent long-term coefficients as the time series are long. The second method is the mean group estimator (MG), which averages separate estimates for each group in the panel and produces consistent estimates of the parameters’ averages (Pesaran & Smith, Citation1995). Pooled Mean Group (PMG) provides the same long-run coefficients across the country but different short-run dynamic coefficients from country to country (Pesaran et al., Citation1999). The first method is applicable for large cross-sectional units but short time-series data, while the second method is appropriate for large time-series data but small cross-sectional units (Pesaran et al., Citation1999). This study uses the PMG method, given our panel data with large time-series data but small cross-sectional objects.

A symmetric PMG model can be written in terms of the symmetric panel ARDL as

where countries and

number of observations,

show country-specific intercepts,

and

are the short-run country-specific coefficient. The long-run response of the Islamic financing rate to the conventional lending rate is calculated by

and the short-run response is measured by

.

The asymmetric PMG model accounts for the partial sum of an interest rate increase ( and an interest fall (

. Therefore, following the asymmetric panel ARDL model (the asymmetric PMG) can be expressed as:

where is the asymmetric error correction term,

and

are long-run parameters,

is group-specific adjustment to the long-run equilibrium condition

, and

and

are the short-run adjustments of Islamic financing rate to a conventional lending rate increase and fall, respectively.

There are some steps to estimate the PMG model. In the first step, we test the stationary panel data to guarantee the order of integration and employ two-panel unit root tests. Our study utilizes the LCC test that considers the unit-root process are a homogenous test for each country proposed by Levin et al. (Citation2002). We also apply the IPS test that permits the unit-root process to be heterogeneous for each country suggested by Im et al. (Citation2003). Next, we test panel cointegration to ascertain the long-run link among the variables. Our study employs the Pedroni and Westerlund panel cointegration test. The first method allows the intercept and trend coefficients to be heterogeneous across the country (Pedroni, Citation1999). The second method permits heterogeneity both in the short-run and the long-run relationship and dependence within and across the cross-sectional units (Westerlund, Citation2007).

4. Results and Discussion

The descriptive statistics as a preliminary analysis of the data are reported in Table . Except for the Indonesian Musharaka rate, the average IFR is higher than CLR but the standard deviation of the IFR is higher than CLR, indicating that the IFR is more varied than CLR. The Islamic and conventional rates are highly correlated, implying that Islamic financing rates may follow conventional lending rates in both countries. To do so, we employ ARDL, NARDL, and PMG as dynamic time-series methods to investigate the impact of conventional lending rates on Islamic bank financing rates in Indonesia and Malaysia, which adopt the dual-banking system.

Table 1. Descriptive statistics

We, initially, must check the stationary data to guarantee that our data fit the model. Table reports the unit-root test using both Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) without and with the trend. The test results indicate that some data are not stationary, and the other data are stationary at level data. Yet, all variables are stationary at the first difference and none of the variables is stationary at the second difference. The findings of unit-root tests indicate that the ARDL and NARDL are suitable models.

Table 2. Unit root test

4.1. ARDL and NARDL Results

We select lag order up to 12 to estimate the ARDL in Equationequation (2)(2)

(2) and the findings are reported in Table . The cointegration test using both

and

may conclude that a long-run link between all types of Islamic financing rates and conventional lending rates is not found. However, our findings reject the null hypothesis of no effect of interest rate on the Islamic financing rate and all types of financing rates such as the Mudharaba, Musharaka, and Murabaha rates in Indonesia. Rise (fall) in the conventional lending rate by 1% leads to rising (falling) Islamic financing rates by 1.674% and 1.597% in Indonesia and Malaysia, respectively.

Table 3. ARDL: Islamic financing rate

Table presents the NARDL results, diagnostic test, cointegration test, asymmetric test, and long-run coefficients. The null hypotheses of no cointegration using both and

test statistics are rejected, except for the Musharaka rate in Indonesia, meaning that the long-run relationship between Islamic financing rates and conventional lending rates is established. The null hypothesis of no long-run asymmetric effect is rejected for all financing products, following the Wald F-test statistic. These results may conclude that the Islamic financing rates asymmetrically respond to changes in the conventional lending rates in both countries. The null hypotheses of the short-run asymmetric effect are also rejected for financing rate, Mudharaba, and Murabaha.

Table 4. NARDL: Islamic financing rate

The long-run coefficients of the financing rate increase are not significant for all types of Islamic financing rates, while the long-run coefficients of the financing rates decrease

are significant for financing rate, Mudharaba, and Murabaha in Indonesia. The associated long-run coefficients of interest rate reduction

are −0.994, −1.597, and −0.671, meaning that a reduction in conventional lending rate lowers the Indonesian Islamic financing rates, Mudharaba, and Murabaha rates by 0.994%, 1.597 %, and 0.671%, respectively. The long-run coefficients of

and

in Malaysia are significant, and the associated coefficients are 0.429 and −0.902, respectively. Our results imply that a conventional lending rate upturn of 1% raises the Malaysian Islamic financing rate by 0.429%, while a conventional lending rate downturn of 1% reduces the Malaysian Islamic financing rate by 0.902%.

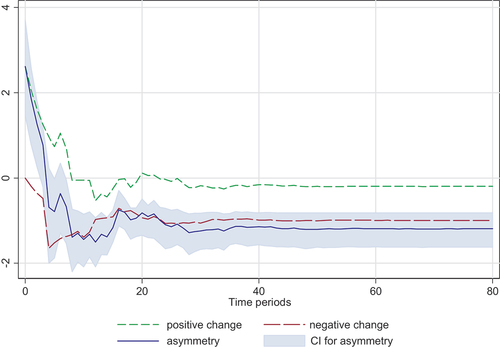

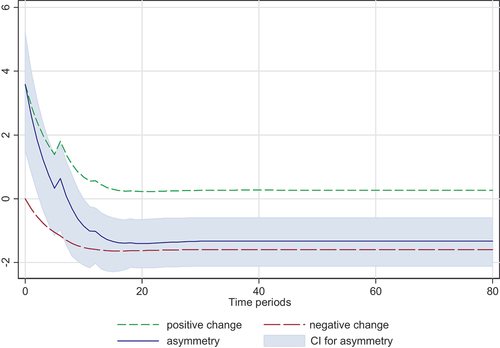

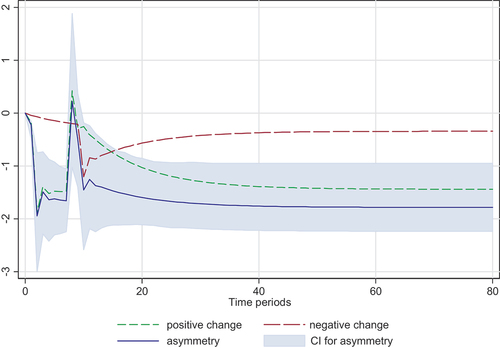

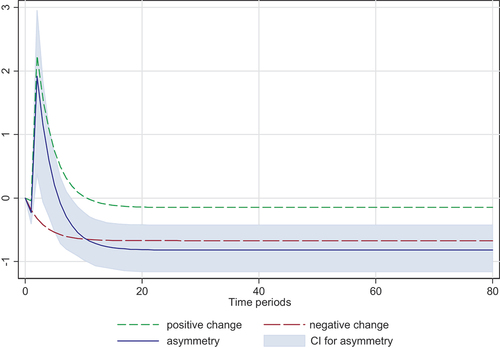

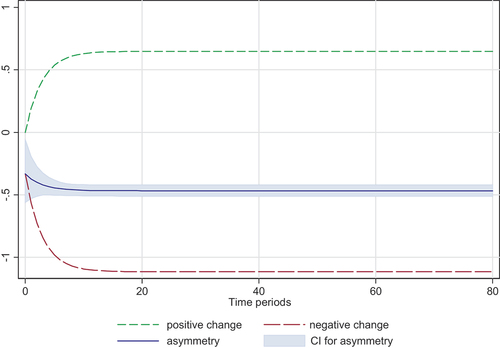

Next, we present Figures that report the asymmetric dynamic multipliers of the Islamic financing rate in reaction to a rise and fall in the conventional lending rate. Those figures demonstrate the changes in the downward and upward movements of the Islamic financing rate over the 80-month horizon with a 90% confidence interval. Those graphs demonstrate that the Indonesian Islamic financing rate, including the Mudharaba and Murabaha rates, obviously follows the conventional lending rate as it decreases but fails to raise as it increases. However, it is not clear for the Musharaka rate. However, the Malaysian IFR follows CLR upturn and downturn but the impact of CLR upturn on the Islamic financing rate is smaller than the impact of CLR downturn.

Figure 1. Indonesian Islamic financing-lending rate dynamic multiplier.

Figure 2. Indonesian Mudharaba-lending rate dynamic multiplier.

Figure 3. Indonesian Musharaka- lending rate dynamic multiplier.

Figure 4. Indonesian Murabaha-lending rate dynamic multiplier.

Figure 5. Malaysian Islamic financing-lending rate dynamic multiplier.

4.2. Panel ARDL and NARDL results

Table presents panel unit roots using LLC and IPS methods and the findings report that the IFR and the CLR are the first difference stationary. Next, Table shows the Pedroni and Westerlund tests to check the panel cointegration and the findings may conclude the evidence of a long-run link among the variables being studied. Table reports the symmetric PMG results. These results show that the CLR positively affects the IFR, implying that a 1% rise (fall) in CLR generates approximately a 1.727% rise (fall) in IFR. Turning to asymmetric PMG, our results indicate that rise and fall in CLR have an asymmetric effect on the IFR. Particularly, the impact of CLR decrease is larger than the impact of CLR increase on IFR. The results suggest that a 1% increase in CLR leads to roughly a 0.453% increase in IFR and a 1% fall in CLR generates approximately a 0.927% reduction in IFR.

Table 5. Panel unit root

Table 6. Panel cointegration test

Table 7. Pool mean group (PMG) estimation

4.3. Robustness check

Because of the different compositions of financing products, the Islamic financing rates are not the same in both countries. This condition leads to heterogeneous characteristics. Accordingly, some problems such as heteroscedasticity, autocorrelation, and endogeneity are likely expected to happen in our estimation (Stock & Watson, Citation1993). Our study employs the fully modified OLS (FMOLS) and Dynamic OLS (DOLS) methods to investigate the robustness of the long-run coefficient of the PMG method.

Table exhibits the results of FMOLS and DOLS estimation. The conventional lending rate is positive and significant for the symmetric approach. The coefficients of conventional lending rates are 1.350 and 1.376 in the FMOLS and DOLS, respectively. Our results imply that a 1% increase in the conventional lending rate generates a 1.350% increase in the Islamic financing rate in the FMOLS method and a 1.376% increase in the Islamic financing rate in the DOLS method. Turning to the asymmetric method, FMOLS and DOLS report that Islamic financing rates respond differently to rising and falling conventional lending rates. Our finding concludes that conventional lending rates have an asymmetric effect on the Islamic financing rate. Predominantly, the impact of falling lending rates is stronger than the impact of rising lending rates on Islamic financing rates. For instance, the DOLS results suggest that a 1% increase in the conventional rate generates approximately a 0.422% increase in the Islamic financing rate and a 1% reduction in the conventional rate results in roughly a 1.115% decrease in the Islamic financing rate. These findings are obviously close to PMG’s results.

Table 8. Panel cointegration results

4.4. Discussion

Indonesian Islamic financing rates negatively respond to a reduction in the conventional lending rate, but the pass-through conventional lending rate to Islamic financing rates fails when it increases. By contrast, the asymmetric pricing of the Malaysian Islamic financing rate strictly follows a rise and fall in the conventional lending rate. The PMG results reinforce the NARDL results where the effect of CLR decrease is larger than the impact of CLR increase on IFR. The results show that Islamic financing rates in both countries are very sensitive to a decrease in the conventional lending rate due to a less competitive Islamic financing rate. As the latest player in the dual-banking system, Islamic banks have not achieved their economies of scale (Ibrahim et al., Citation2017; Čihák & Hesse, Citation2010). Accordingly, they encounter high operating costs and then cannot charge low prices for their products (Johnes et al., Citation2014; Lassoued, Citation2018).

What can we infer from these results? These findings certainly show that Islamic bank customers are profit-driven customers in the dual-banking environment (Aysan et al., Citation2018; Widarjono et al., Citation2022a). Islamic bank borrowers always find the lowest cost of capital in their financing based on the behavior of Islamic bank customers. Indonesian Islamic banks, with a small market share of about 5.6%, perform both pricing as well as non-pricing strategy to content with conventional banks. The fatwa of the Indonesian Ulema Council regarding the prohibition of interest rates started in 2003, but this religious branding is, to some extent, not effective in supporting Islamic banks (Utomo et al., Citation2021). Accordingly, as the lending interest rate rises, Islamic banks do not automatically increase the financing rate to retain customers and they reduce much larger financing rates as the conventional lending rate falls to attract new customers.

IFR is influenced by CLR in the Malaysian banking industry because of the presence of profit-driven customers (Cevik & Charap, Citation2015; Sukmana & Ibrahim, Citation2017). More interestingly, the pass-through CLR to IFR is higher for a reduction in CLR than an increase in CLR because the market share of Islamic banks is moderate (23%). Islamic banks are pushed to peg their financing rate to conventional lending rate due to the tradeoff between religious motives and the profit-driven motives of rational customers (Saeed et al., Citation2021). Accordingly, Malaysian Islamic banks must lower the larger financing rate as interest rates fall more than the financing rate increases as interest rates increase. This strategy is taken to maintain the Islamic bank customers since the IFR is much higher than their counterpart CLR.

We now turn to the specific Islamic financing rates such as Mudharaba, Musharaka, and Murabaha rates in Indonesia. The effect of conventional lending rates on those rates is not clear. The Mudharaba and Murabaha rate pegs to the conventional rate as it falls, but the Musharaka rate does not follow the interest rate. The plausible reasons are that the Mudharaba contract leads to principal–agent problems such as adverse selection, moral hazard, and asymmetric information because Islamic banks cannot control projects and bear all risk capital (Azmat et al., Citation2015; Widarjonoet al., Citation2020a). In addition, Islamic bank performance in Indonesia is regulated as a conventional bank. To avoid this risk of capital due to non-performing financing and poor financial performance, therefore, Islamic bank charges the Mudharaba rate, which is likely pegged to the conventional lending interest rate (Sutrisno & Widarjono, Citation2018). As the largest portion of Islamic financing, the Murabaha contract is easy for Islamic banks and customers because it applies margins or marks up in determining the Islamic financing rate. Therefore, this contract is exactly similar to a conventional bank interest system, and the margin rate has to respond to the interest rate because of profit-driven customers in a dual-banking system. Meanwhile, the Musharaka contract may not cause the principal–agent problem because both an Islamic bank and an entrepreneur jointly contribute capital and manage a project. The profit and/or loss then are jointly determined by both parties and consequently, it is interest-free (Šeho et al., Citation2020).

5. Conclusion

Islamic banks’ products, to some extent, mimic conventional banks. This present study examines the effect of conventional lending rates on Islamic financing rates in a dual-banking system employing the ARDL, NARDL, and PMG models. The asymmetric pricing of the Indonesian Islamic financing rate and some specific contracts, such as Mudharaba and Murabaha rates, strongly follows the conventional lending rate as it falls. The asymmetric pricing of Malaysian Islamic financing obviously follows the conventional lending rate increase and fall.

The results are important regarding the price of Islamic bank financing in the dual-banking system when the market share of Islamic banks is relatively small. Islamic bank consumers always compare the cost of capital in their financing. In addition to religious branding and non-price strategy, price strategy is the key to the success of Islamic banks in competing with the dominated and established conventional banks. As long as Islamic banks can offer competitive financing rates through improving operating efficiency, Islamic banks may be alternate sources of financing for profit-driven consumers in the dual-banking environment.

Musharaka, Mudharaba, and Murabaha financing rates are not available in Malaysian Islamic banking. Consequently, this study fails to give a clear picture of these specific financing rates in response to conventional lending rates in Malaysia, where Islamic bank consumers are profit-driven-like Islamic bank consumers in Indonesia.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Agus Widarjono

Agus Widarjono is a professor at the Department of Economics, Faculty of Business and Economics, Universitas Islam Indonesia (UII). His research interests are in Islamic banking and finance and Islamic Economics. He has published some papers in the Journal of Islamic Marketing, Asian Economic and Financial Review, and Cogent Economics and Finance.

Abdur Rafik

Abdur Rafik is a lecturer at the Department of Management, Faculty of Business and Economics, Universitas Islam Indonesia (UII). His research interest is finance. He has published some papers in the International journal of Innovation Science, Management Research Review, Afro-Asian Journal of Finance and Accounting.

References

- Abduh, M. (2015). Determinants of Islamic banking deposit: Empirical evidence from Indonesia. Middle East Journal of Management, 2(3), 240–17. https://doi.org/10.1504/mejm.2015.072462

- Aggarwal, R. K., & Yousef, T. (2000). Islamic banks and investment financing. Journal of Money, Credit, and Banking, 32(1), 93–120. https://doi.org/10.2307/2601094

- Anuar, K., Mohamad, S., & Shah, M. E. (2014). Are deposit and investment accounts in Islamic banks in Malaysia interest free? Journal of King Abdulaziz University, Islamic Economics, 27(2), 27–55. https://doi.org/10.4197/Islec.27-2.2

- Apergis, N., & Cooray, A. (2015). Asymmetric interest rate pass-through in the U.S., the U.K. and Australia: New evidence from selected individual banks. Journal of Macroeconomics, 45, 155–172. https://doi.org/10.1016/j.jmacro.2015.04.010

- Aysan, A. F., Disli, M., Duygun, M., & Ozturk, H. (2018). Religiosity versus rationality: Depositor behavior in Islamic and conventional banks. Journal of Comparative Economics, 46(1), 1–19. https://doi.org/10.1016/j.jce.2017.03.001

- Azad, A. S. M. S., Azmat, S., Chazi, A., & Ahsan, A. (2018). Can Islamic banks have their own benchmark? Emerging Markets Review, 35, 120–136. https://doi.org/10.1016/j.ememar.2018.02.002

- Azmat, S., Skully, M., & Brown, K. (2015). Can Islamic banking ever become Islamic? Pacific Basin Finance Journal, 34, 253–272. https://doi.org/10.1016/j.pacfin.2015.03.001

- Bacha, O. I. (2008). The Islamic inter bank money market and a dual banking system: The Malaysian experience. International Journal of Islamic and Middle Eastern Finance and Management, 1(3), 210–226. https://doi.org/10.1108/17538390810901140

- Bacon, R. W. (1991). Rockets and feathers: The asymmetric speed of adjustment of UK retail gasoline prices to cost changes. Energy Economics, 13(3), 211–218. https://doi.org/10.1016/0140-9883(91)90022-R

- Baele, L., Farooq, M., & Ongena, S. (2014). Of religion and redemption: Evidence from default on Islamic loans. Journal of Banking and Finance, 44(1), 141–159. https://doi.org/10.1016/j.jbankfin.2014.03.005

- Baharumshah, A. Z., Sirag, A., & Soon, S. V. (2017). Asymmetric exchange rate pass-through in an emerging market economy: The case of Mexico. Research in International Business and Finance, 41, 247–259. https://doi.org/10.1016/j.ribaf.2017.04.034

- Bahmani-Oskooee, M., & Saha, S. (2018). On the relation between exchange rates and stock prices: A non-linear ARDL approach and asymmetry analysis. Journal of Economics and Finance, 42(1), 112–137. https://doi.org/10.1007/s12197-017-9388-8

- Banerjee, A., Dolado, J. J., & Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19(3), 267–283. https://doi.org/10.1111/1467-9892.00091

- Cevik, S., & Charap, J. (2015). The behavior of conventional and Islamic bank deposit returns in Malaysia and Turkey. International Journal of Economics and Financial Issues, 5(1), 111–124. https://doi.org/10.5089/9781455293704.001

- Chong, S., & Liu, M. (2009). Islamic banking: Interest-free or interest-based? Pacific-Basin Finance Journal, 17(1), 125–144. https://doi.org/10.1016/j.pacfin.2007.12.003

- Čihák, M., & Hesse, H. (2010). Islamic banks and financial stability: An empirical analysis. Journal of Financial Services Research, 38(2), 95–113. https://doi.org/10.1007/s10693-010-0089-0

- Ergeç, E. H., & Arslan, B. G. (2013). Impact of interest rates on Islamic and conventional banks. Applied Economics, 45(17), 2381–2388. https://doi.org/10.1080/00036846.2012.665598

- Ergec, E. H., & Kaytanci, B. G. (2014). The causality between returns of interest-based banks and Islamic banks: The case of Turkey. International Journal of Islamic and Middle Eastern Finance and Management, 7(4), 443–456. https://doi.org/10.1108/IMEFM-07-2014-0072

- Hamza, H. (2016). Does investment deposit return in Islamic banks reflect PLS principle? Borsa Istanbul Review, 16(1), 32–42. https://doi.org/10.1016/j.bir.2015.12.001

- Holmes, M. J., Iregui, A. M., & Otero, J. (2015). Interest rate pass through and asymmetries in retail deposit and lending rates: An analysis using data from Colombian banks. Economic Modelling, 49, 270–277. https://doi.org/10.1016/j.econmod.2015.04.015

- Ibrahim, M. H., Aun, S., & Rizvi, R. (2017). Do we need bigger Islamic banks? An assessment of bank stability. Journal of Multinational Financial Management, 40, 77–91. https://doi.org/10.1016/j.mulfin.2017.05.002

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Ismal, R. (2011). Depositors’ withdrawal behavior in Islamic banking: Case of Indonesia. Humanomics, 27(1), 61–76. https://doi.org/10.1108/08288661111110187

- Ito, T. (2013). Islamic rates of return and conventional interest rates in the Malaysian deposit market. International Journal of Islamic and Middle Eastern Finance and Management, 6(4), 290–303. https://doi.org/10.1108/IMEFM-11-2012-0113

- Jawadi, F., Cheffou, A. I., & Jawadi, N. (2016a). Can the Islamic bank be an emerging leader? A panel data causality analysis. Applied Economics Letters, 23(14), 991–994. https://doi.org/10.1080/13504851.2015.1125426

- Jawadi, F., Cheffou, A. I., & Jawadi, N. (2016b). Do Islamic and conventional banks really differ? A panel data statistical analysis. Open Economies Review, 27(2), 293–302. https://doi.org/10.1007/s11079-015-9373-9

- Johnes, J., Izzeldin, M., & Pappas, V. (2014). A comparison of performance of Islamic and conventional banks 2004-2009. Journal of Economic Behavior & Organization, 103, S93–107. https://doi.org/10.1016/j.jebo.2013.07.016

- Kasri, R., & Kassim, S. (2009). Empirical determinants of saving in the Islamic Banks: Evidence from Indonesia. Journal of King Abdulaziz University-Islamic Economics, 22(2), 181–201. https://doi.org/10.4197/islec.22-2.7

- Kassim, S. H., Shabri, M., Majid, A., & Yusof, R. M. (2009). Impact of monetary policy shocks on the conventional and Islamic banks in a dual banking system: Evidence from malaysia. Journal of Economic Cooperation and Development, 30(1), 41–58.

- Khan, F. (2010). How “Islamic” is Islamic Banking? Journal of Economic Behavior & Organization, 76(3), 805–820. https://doi.org/10.1016/j.jebo.2010.09.015

- Kumar, S. (2019). Asymmetric impact of oil prices on exchange rate and stock prices. The Quarterly Review of Economics and Finance, 72, 41–51. https://doi.org/10.1016/j.qref.2018.12.009

- Lassoued, M. (2018). Comparative study on credit risk in Islamic banking institutions: The case of Malaysia. The Quarterly Review of Economics and Finance, 70, 267–278. https://doi.org/10.1016/j.qref.2018.05.009

- Levin, A., Lin, C., & Chu, C. J. (2002). Unit root tests in panel data: Asymptotic and ÿnite-sample properties. Journal of Econometrics, 108(1), 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7

- Maddala, G. S., & Wu, S. (1999). A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(S1), 631–652. https://doi.org/10.1111/1468-0084.0610s1631

- Mohd Yusoff, Z. Z., & Azhar, N. I. (2019). Relationship between conventional and Islamic Interbank rates of a dual banking system in Malaysia, middle east, and western countries. Journal of International Business, Economics and Entrepreneurship, 4(2), 38. https://doi.org/10.24191/jibe.v4i2.14313

- Nechi, S., & Smaoui, H. E. (2019). Interbank offered rates in Islamic countries: Is the Islamic benchmark different from the conventional benchmarks? The Quarterly Review of Economics and Finance, 74, 75–84. https://doi.org/10.1016/j.qref.2018.05.003

- Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61(s1), 653–670. https://doi.org/10.1111/1468-0084.61.s1.14

- Pesaran, M. H., & Shin, Y. (1998). An autoregressive distributed-lag modelling approach to cointegration analysis. Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium. https://doi.org/10.1017/ccol0521633230.011

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. https://doi.org/10.1080/01621459.1999.10474156

- Pesaran, M. H., & Smith, R. (1995). Econometrics Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113. https://doi.org/10.1016/0304-4076(94)01644-F

- Saeed, S. M., Abdeljawad, I., Hassan, M. K., & Rashid, M. (2021). Dependency of Islamic bank rates on conventional rates in a dual banking system: A trade-off between religious and economic fundamentals. International Review of Economics and Finance forthcomming. https://doi.org/10.1016/j.iref.2021.09.013.

- Saraç, M., & Zeren, F. (2015). The dependency of Islamic bank rates on conventional bank interest rates: Further evidence from Turkey. Applied Economics, 47(7), 669–679. https://doi.org/10.1080/00036846.2014.978076

- Šeho, M., Bacha, O. I., & Smolo, E. (2020). The effects of interest rate on Islamic bank financing instruments: Cross-country evidence from dual-banking systems. Pacific Basin Finance Journal, 62(December 2019), 101292. https://doi.org/10.1016/j.pacfin.2020.101292

- Sheikh, U. A., Asad, M., Ahmed, Z., Mukhtar, U., & McMillan, D. (2020). Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008: Evidence from Pakistan. Cogent Economics and Finance, 8(1), 1757802. https://doi.org/10.1080/23322039.2020.1757802

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a Nonlinear ARDL framework. In <. I. I. A. I. <. Sickels & <. I. I. A. I. <. Horrace (Eds.), Festschrift in honor of Peter Schmidt: Econometric methods and applications (pp. 281–314). Springer. https://doi.org/10.1007/978-1-4899-8008-3

- Stock, J. H., & Watson, M. W. (1993). A simple estimator of cointegrating vectors in higher order integrated systems. Econometrica, 61(4), 782–820. https://doi.org/10.2307/2951763

- Sukmana, R., & Ibrahim, M. H. (2017). How Islamic are Islamic banks? A non-linear assessment of Islamic rate – conventional rate relations. Economic Modelling, 64, 443–448. https://doi.org/10.1016/j.econmod.2017.02.025

- Sutrisno, S., & Widarjono, A. (2018). Maqasid Sharia Index, Banking risk and performance cases in Indonesian Islamic Banks. Asian Economic and Financial Review, 8(9), 1175–1184. https://doi.org/10.18488/journal.aefr.2018.89.1175.1184

- Tappata, M. (2009). Rockets and feathers: Understanding asymmetric pricing. The Rand Journal of Economics, 40(4), 673–687. https://doi.org/10.1111/j.1756-2171.2009.00084.x

- Tlemsani, I. (2020). Evaluation of the Islamic interbank benchmark rate. International Journal of Islamic and Middle Eastern Finance and Management, 13(2), 249–262. https://doi.org/10.1108/IMEFM-06-2018-0203

- Utomo, S. B., Sekaryuni, R., Widarjono, A., Tohirin, A., & Sudarsono, H. (2021). Promoting Islamic financial ecosystem to improve halal industry performance in Indonesia: A demand and supply analysis. Journal of Islamic Marketing, 12(5), 992–1011. https://doi.org/10.1108/JIMA-12-2019-0259

- Warninda, T. D., Ekaputra, I. A., & Rokhim, R. (2019). Do Mudarabah and Musharakah financing impact Islamic Bank credit risk differently? Research in International Business and Finance, 49, 166–175. https://doi.org/10.1016/j.ribaf.2019.03.002

- Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69(6), 709–748. https://doi.org/10.1111/j.1468-0084.2007.00477.x

- Widarjono, A., & Hakim, A. (2019). Asymmetric oil price pass-through to disaggregate consumer prices in emerging market: Evidence from Indonesia. International Journal of Energy Economics and Policy, 9(6), 310–317. https://doi.org/10.32479/ijeep.8287

- Widarjono, A., Mifrahi, M. N., & Perdana, A. R. A. (2020a). Determinants of Indonesian Islamic Rural Banks ’ Profitability: Collusive or Non- Collusive Behavior? The Journal of Asian Finance, Economics and Business, 7(11), 657–668. https://doi.org/10.13106/jafeb.2020.vol7.no11.657

- Widarjono, A., Suharto, S., & Wijayanti, D. (2022a). Do Islamic banks bear displaced commercial risk? Evidence from Indonesia. Banks and Bank Systems, 17(3), 102–115. https://doi.org/10.21511/bbs.17(3).2022.09

- Widarjono, A., Susantun, I., Ruchba, S. M., & Rudatin, A. (2020b). Oil and Food Prices for a Net Oil Importing-country: How are Related in Indonesia? International Journal of Energy Economics and Policy, 10(5), 255–263. https://doi.org/10.32479/ijeep.9557

- Widarjono, A., Wijayanti, D., & Suharto, S. (2022b). Funding liquidity risk and asset risk of Indonesian Islamic rural banks. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2059911

- Yuksel, S. (2017). The causality between returns of interest-based banks and Islamic banks: The case of Turkey. International Journal of Islamic and Middle Eastern Finance and Management, 10(4), 519–535. https://doi.org/10.1108/IMEFM-12-2013-0133

- Yusof, R. M., Bahlous, M., & Tursunov, H. (2015). Are profit sharing rates of mudharabah account linked to interest rates? An investigation on Islamic banks in GCC Countries. Jurnal Ekonomi Malaysia, 49(2), 77–86. https://doi.org/10.17576/JEM-2015-4902-07

- Zainol, Z., & Kassim, S. H. (2010). An analysis of Islamic banks’ exposure to rate of return risk. Journal of Economic Cooperation and Development, 31(1), 59–84.