?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The current study investigates the impact of foreign direct investment on the growth of Namibia’s economy from 1990 to 2020 using the ARDL cointegration method. The results reveal that FDI, the interactive variable of FDI and trade openness, and other macroeconomic variables such as domestic investment, government consumption expenditure, human capital, a proxy for economic stability, and return on investment are responsible for Namibia’s economic growth. The article confirms the FDI-led growth and the Bhagwati hypotheses for Namibia as shown by the FDI and the interactive variable of FDI and trade openness, respectively. To reap the full benefits of FDI on economic growth in Namibia, the government must focus on improving physical infrastructure and the quality of human resources. It should also facilitate the development of an entrepreneurship culture, create a stable macroeconomic environment, and improve conditions for productive investments to accelerate economic growth and development.

1. Introduction

Foreign direct investment (FDI) has a significant role in the external financing of developing and developed nations. It is envisaged to have significant effects in various economies through increasing production, exports, and employment, improvements in the standards of living, and a decrease in poverty and inflation, ultimately leading to economic growth. Furthermore, FDI has a role to play in assisting the host nations efficiently utilise their resources by introducing new technology, facilitating access to new markets, managing their knowledge, and improving their infrastructure, among others, to achieve economies of scale (Basu et al., Citation2003; Borensztein et al., Citation1998; Herzer & Klasen, Citation2008; Lumbila, Citation2005). Over the past three decades, developing countries received increasingly significant inflows of FDI. This generated much interest from academics and researchers who have attempted to analyse the impact of FDI on economic growth in a recipient country.

Note should be taken that the growth in FDI can be attributed to the decision taken by developed country commercial banks to stop lending to developing economies in the 1980s. Because of this, most countries relaxed restrictions on FDI and commenced offering aggressive tax and subsidy-related incentives to FDI (Aitken & Harrison, Citation1999). Some specific incentives governments offer include zero or reduced corporate tax rates, exemptions from import duties, subsidised water and electricity, and infrastructure subsidies, among others. Such government incentives were based on the premise that foreign investment generates positive externalities through technology transfer. It should also be noted that FDI became the most significant source of external financing for developing countries in the 1990s when Namibia became independent. Namibia did not take time to join the bandwagon to attract FDI, as it came up with laws and legislation favourable to attracting FDI in 1990, just after gaining its independence. This is because it is envisaged that countries with more significant investment as a ratio of the gross domestic product (GDP) typically experience faster economic growth and that the efficient allocation of resources contributes to differences in growth between countries, among other factors. Shahbaz and Rahman (2010) opined that the critical role foreign capital plays in global commerce includes foreign capital inflows, access to other resources, companies' access to new markets, cheaper production facilities, new technology products, skills, and financing. In addition, Alfaro et al. (Citation2004), Omran and Bolbol (Citation2003), Hermes and Lensink (Citation2003) and Durham (Citation2004), also argued that undeveloped local financial markets could limit the economy’s potential to take advantage of potential spillovers from foreign capital inflows fully.

Namibia gained its independence in 1990, and it has grown at an average of 4% per annum between the period 1990 to 2018. This growth is primarily attributed to the growth in government expenditure since the government has been using expansionary fiscal policy during this period. During the same period, Namibia’s trade with other countries, particularly export trade, also significantly increased. This may be because Namibia received significant inflows of FDI, particularly in mining and, to a lesser extent, in manufacturing during the period in question, which assisted in boosting export trade. The fact that Namibia has received a lot of FDI in mining is not surprising, given that Namibia has rich endowments of many precious mineral resources, including gold, emeralds and diamonds, to name but a few. This article aims to analyse the impact of FDI on economic growth in Namibia by using a multivariate ARDL econometrics methodology. Several similar studies were carried out in other countries by De Vita and Kyaw (Citation2009), Iqbal Chaudhry et al. (Citation2013), Sunde (Citation2017) and Rehman et al. (Citation2021), who have produced conflicting results which affirmed and disaffirmed the importance of FDI in explaining economic growth. This lack of consensus in the results on the FDI-economic growth relationship and the fact that little has been done in terms of research on this relationship in Namibia creates a gap to be filled.

Given the above background, the current study contributes to the literature on the impact of FDI on economic growth in ways explained below. First, although a number of studies on FDI’s impact on economic growth have been conducted in various countries, very few country-specific studies have been conducted on African countries such as Namibia (see, for example, Odhiambo, Citation2022). Second, some previous studies have applied cross-country data to panel models, which fail to account for country-specific characteristics (see Liang et al., Citation2021; Lin & Benjamin, Citation2018; Makaranga, Citation2019). As reported in previous empirical studies, grouping countries at different stages of development using the panel data methodology fails to address the country-specific effects of FDI on economic growth. Additionally, when countries are studied collectively, the positive and negative effects across nations may cancel each other out, making it difficult to see how these variables interact in each country. Third, some previous early studies also disregarded long-run relationships, which is an essential cause of problems with the validity of the findings. Fourth, researchers encounter problems due to the econometric methodologies they employ and the unavailability of data. Most previous studies analysed the bivariate relationship between FDI and economic growth using the vector autoregression (VAR) methodology (see Ali & Mingque, Citation2018; Ludoșean, Citation2012; Nguyen, Citation2011; Quoc & Thi, Citation2018; Rafat, Citation2018; Zhao & Du, Citation2007). This method poses some challenges in situations where the data sample is not large enough, as is the case in most developing countries. Fifth, bivariate models between FDI and economic growth suffer from variable omission bias (see Odhiambo, Citation2022; Rangel González & López Ornelas, Citation2022) since economic growth in such a model is only explained by the lags of itself and by FDI and its lags. To overcome the challenge of variable omission bias in some previous studies, the current study incorporates other variables that explain economic growth, such as the interactive variable of FDI and trade openness (FDI_TOPEN), domestic investment, human capital development, a measure of the country’s overall economic stability (inflation) and return on investment (associated with financial development) over and above the FDI variable. According to Akinlo (Citation2004), failure to include interaction effects in the relationship between foreign direct investment and economic growth is possibly one of the reasons why previous researchers have found contradictory results. Lastly, the ARDL methodology employed in the current study is more flexible than the VAR method employed in most previous studies, which requires all the variables to be integrated of the same order. The ARDL method may be employed when all variables are integrated of order 0, integrated of order 1, or a combination of both.

The remaining sections of the article are organised as follows: Section 2 provides a concise summary of the empirical literature, while Section 3 discusses the data and the methodology. The study's empirical findings are presented and discussed in Section 4. Finally, Section 5 concludes the study and gives recommendations.

2. Empirical literature

Foreign direct investment significantly contributes to economic growth and development. It is widely acknowledged that FDI increases productivity and aids host nations’ development. However, the relationship between FDI and economic growth is the subject of ongoing debate. Some scholars believe the two have a positive relationship, while others believe the relationship is negative. Others find a weak or non-existent connection between these variables. Studies on FDI have yielded disparate results due to diverse methodologies, time frames studied differences in independent and control variables included in the estimations.

Using cross-section data from 64 developing countries and the ordinary least square (OLS) regression method, Balasubramanyam et al. (Citation1996) conclude that FDI positively affects the host country’s economic growth by encouraging an export promotion than an import substitution strategy. Borensztein et al. (Citation1998) examine the impact of FDI on economic growth in 69 countries over 20 years. They believe the foreign direct investment is more advantageous for technology transfer than domestic investment. Consequently, FDI contributes to economic growth if the host country utilises advanced technologies adequately.

Using panel data, Aitken and Harrison (Citation1999) examine the impact of FDI on Venezuelan plants. Foreign equity participation has been found to correlate positively with plant productivity. In addition, foreign investment reduces the productivity of domestically owned plants, and indeed, joint ventures capture all foreign investment profits. Nair‐reichert and Weinhold (Citation2001) used a mixed fixed and random (MFR) panel data estimation method to examine the causal relationship between FDI and growth. They found that the relationship between investment and economic growth in developing nations is highly heterogeneous and that this heterogeneity produces misleading results.

Choe (Citation2003) used data from 80 countries from 1971 to 1995 and a panel VAR model to conclude that there is a strong relationship between growth and FDI. This study found that economic growth causes GDI, but that GDI does not cause economic growth. Choe (Citation2003) analysed the relationship between FDI and economic growth in eight post-transition EU countries, and it was discovered that the spillover effect was the primary contributor of FDI to growth in this country. A negative correlation was also found between FDI and economic growth.

Omran and Bolbol (Citation2003) examined FDI, financial growth, and economic expansion in Arab nations. The study’s findings indicate that FDI will have a positive effect on the growth of Arab countries if it interacts with financial variables at a certain level of economic development. In addition, the study concludes that FDI-friendly policies will encourage investors to invest in these nations, leading to economic growth and financial development. Omran and Balbol’s study concludes that domestic financial reforms and liberal commercial policies encourage FDI, and similar investment measures could improve the investment climate for all investors.

Li and Liu (Citation2005)examine the relationship between foreign direct investment and economic growth. From 1970 to 1999, panel data from 84 countries were utilised in this study. They found a significant endogenous relationship economic growth and FDI which was demonstrated the use of single and simultaneous equation techniques. FDI positively affects economic growth via human resource capital and the efficient use of technology.

Chowdhury and Mavrotas (Citation2006) utilised data from Chile, Malaysia, and Thailand from 1969 to 2000. This study employs an innovative methodology to examine the connection between FDI and economic growth. Its authors conclude that Chile’s GDP causes FDI, not vice versa. However, a bidirectional causal relationship exists between GDP and FDI in Malaysia and Thailand. Axarloglou and Pournarakis (Citation2007) investigated the effect of FDI on economic growth between 1974 and 1994. The researchers conclude that its effects vary by industry. However, the results highlight the importance of industry-specific characteristics when evaluating the effects of FDI on local communities. Wang and Sunny Wong (Citation2009) examined data from 12 Asian nations between 1987 and 1997 to determine if FDI influences economic growth. Even though endogenous growth theory predicts a positive correlation between inward FDI, and economic growth, Wang and Wong contends that using total FDI may obscure its effects and produce ambiguous results. The study concluded that foreign direct investment (FDI) boosts economic growth in manufacturing but not in non-manufacturing sectors.

Using data from 66 developing countries, Duttaray et al. (Citation2008) examined the relationship between FDI and economic growth. In 29 of these countries, FDI was found to affect growth, but growth did not affect FDI. Ang (Citation2008) examines the Malaysian FDI growth nexus to comprehend the connection between FDI and financial and economic growth. The study employs time series data from 1965 to 2004, and the findings indicate that FDI and financial development have a positive long-term relationship with output. According to the study, economic growth causes FDI growth over the long term. Using annual time series data from 1970 to 2004, Ang (Citation2009) examines the relationship between foreign direct investment and financial development in Thailand. According to the study, economies with superior financial systems enjoy more significant FDI benefits. The study’s findings indicate that financial development stimulates economic development, whereas FDI has a negative long-term impact on output expansion. Using data from 126 developing countries from 1985 to 2002, De Vita and Kyaw (Citation2009) discovered that the effect of FDI and portfolio investment on economic growth is positive in developing countries with lower middle and upper middle income, but negative in those with low income. In order to achieve these outcomes, developing countries must attain a certain level of development and absorption capacity, according to the findings.

Mohammed and Mahfuzul (Citation2016) used annual time series data for the period running from 1973 to 2014, as well as the cointegration method, to estimate the effect of FDI on the economy of Bangladesh. The study’s findings suggest that trade and FDI significantly impacted Bangladesh’s economic performance, and the study also indicates a long-term relationship among the variables used in the model. The study concludes by recommending that Mauritania’s government should put policies in place that would potentially make the country’s macroeconomic environment competitive to encourage FDI.

Abdouli and Hammami (Citation2017), using panel data and a dynamic model, determined the role of economic growth, human capital and the environment in attracting FDI inflows for four selected African Mediterranean countries from 1990–2013. The analysed estimated results suggest that higher human capital attracts FDI inflows in the four countries considered in the study. Furthermore, the results indicate that weak environmental regulations increase FDI inflows. Besides, the findings demonstrate that FDI inflows do not lead to economic growth in the countries considered in the study. In another study on an African country, Sunde (Citation2017) examined the nexus between foreign direct investment, exports, and economic growth. The article empirically investigated the relationship between foreign direct investment and exports and South Africa’s economic growth. The study found that FDI in South Africa impacts economic growth in both the short- and long-run. In addition, the VECM Granger causality test revealed unidirectional foreign direct investment-economic growth causal relationship running from FDI to economic growth. This study, therefore, confirmed the FDI-led growth hypothesis for South Africa.

After reviewing the existing literature on FDI and economic growth, it is possible to conclude that the FDI and economic growth relationship is influenced by various factors, as political and economic conditions vary from country to country. Some empirical studies find a positive relationship between foreign direct investment and economic growth, while others find a negative relationship. This article examines the foreign direct investment and economic growth relationship in Namibia and attempts to determine whether the FDI and economic growth relationship is long- or short-run.

3. Data and methodology

3.1. Data sources and justification of variables

Foreign direct investment’s impact on economic growth in Namibia was examined using annual data for the period 1990 to 2020. The majority of the study’s data came from the World Development Indicators. This data’s authenticity was verified by comparing it with data from the Namibia Statistical Agency (NSA) and the World Bank Economic Statistics. Data for variables such as FDI, GDP, Gross fixed capital formation (KAP), government consumption expenditure (GOVC), human capital (HCAP), trade openness (TOPEN), a proxy for economic stability (INFL), and return on investment (RETOI) was collected. I initially experimented with more variables and the ones that are listed here are the ones that performed well in the initial analysis. The next part of the section discusses all the variables that are utilised in this study.

Infrastructure development (INFRUST): Good infrastructure facilitates the production, reduces operating costs, and thus encourages foreign direct investment (see Démurger, Citation2001). Infrastructure boosts the efficiency of investment and, consequently, economic growth. In the literature, the number of telephones per one thousand inhabitants is frequently used to measure infrastructure development. This measure is flawed because it does not account for the increase in the number of mobile phones and only measures the facility’s availability and not its dependability. The literature also uses electric power transmission and distribution losses as an additional metric. Given the availability of data, I proxied this variable with the electric power consumption per capita. This metric addresses availability and I anticipate a direct correlation between this metric and economic growth.

The openness of the host economy to trade (TOPEN): As is standard in the literature, the ratio of trade (imports and exports) to GDP is used to measure this variable. In the literature on growth accounting, exports have been considered an explanatory variable. It is anticipated that FDI inflows will enhance the export competitiveness of host countries. Exports and investments will have a multiplier effect on GDP as they increase. Additionally, increased exports and investments could generate foreign currency that can be used to import capital goods. Furthermore, employment will increase if the additional investment incorporates neutral/labour-intensive techniques. I expect this variable to have a direct positive relationship with economic growth.

Government size (GOVC): This is the government consumption as a percentage of GDP. It includes all current government expenditures for purchases of goods and services. It also includes most national defence and security expenditures but excludes government military expenditures that are part of government capital formation. It is anticipated to have a direct correlation with economic growth. This is because a higher level of government consumption ought to result in the provision of more social capital, which should stimulate production and growth.

Human capital (HCAP): Population enrollment in secondary and tertiary institutions indicates the importance of education to economic development. However, the current study only uses primary and secondary school enrollment due to tertiary institutions’ data unavailability. Balasubramanyam et al. (Citation1996), Nair‐reichert and Weinhold (Citation2001) and Akinlo (Citation2004) included this variable in their growth equations and discovered a direct relationship between it and economic growth. However, Borensztein et al. (Citation1998) discovered a conditional relationship in which the association was indirect below a certain threshold and positive thereafter. Bende‐nabende et al. (Citation2001) discovered an indirect relationship between human capital and economic growth in Taiwan. I expect the human capital variable to affect economic growth positively.

Return on investment (RETOI). FDI will flow to countries with higher capital returns which is also associated with a higher level of financial development. I assume that a higher return on capital indicates a higher level of productivity and, consequently, a greater economic growth potential. The return on investment in the rest of the world serves as an opportunity cost for potential investors in Namibia, who can use the rate to compare what is available in other regions of the world. I assume a direct relationship between per capita income and the rate of return on capital. Bende‐nabende et al. (Citation2001) discovered a positive relationship between the return on capital and FDI suggesting that higher GDP per capita is associated with a more favourable outlook for FDI in the host economy.

Gross fixed capital formation (KAP): includes all those activities or actions by the state to improve infrastructure, human capital and commercial activities, as well as improving social and security status within the country. This variable is anticipated to have a positive effect on overall economic growth.

Inflation rate (INFL): I included the inflation rate (INFL) to measure the country’s overall economic stability. I anticipate an indirect relationship between inflation and economic expansion.

3.2. Long-run dynamics

In this section, the long run ARDL model used to test for cointegration is specified. It must be noted that the most common methods for determining whether two variables are cointegrated or not are those developed by Engle and Granger (Citation1987) and Johansen and Juselius (Citation1990). However, for these techniques to be applicable, all the variables in the model must be stationary in first differences [I(1)]. When the sample size is small, these methods perform poorly, according to Chaudhry and Choudhary (Citation2006). The latter limitation is not present in the autoregressive distributed lag (ARDL) methodology for cointegration. The ARDL approach has gained popularity over the other techniques due to its various econometric benefits, one of which is that it does not require that all variables be stationary in first differences [I(1)]. This is because it can be applied when all variables are integrated of order zero [I(0)], integrated of order 1 [I(1)], or a combination of both. The following model is therefore presented in light of the benefits of the ARDL approach to cointegration mentioned earlier.

where,

ECONG = GDP per capita = economic growth

FDI = percentage of FDI/GDP.

FDI_TOPEN = interactive variable for FDI and trade openness.

All the other variables are as described above.

is the constant.

are the short-run parameters.

To test for cointegration, I use the following hypotheses for derived from EquationEquation 1(1)

(1) :

:

(There is no cointegration)

:

(The null hypothesis is not true)

The non-standard F-statistic distribution proposed by Pesaran et al. (Citation2001) is used in the ARDL test for cointegration. This is because the F-statistic presupposes that variables are stationary in levels [I(0)], or after first-differencing [(I(1))], or a hybrid of both, as previously indicated. The no cointegration hypothesis may be accepted if the estimated F-statistic is smaller than the lower critical bound (LCB). Cointegration exists if the estimated F-statistic exceeds the upper critical bound (UCB). If the estimated F-statistic falls between the lower and upper critical bounds, the results are inconclusive.

3.3. Short-run dynamics

If the test for cointegration points to the fact that the variables included in the ARDL equation are cointegrated, this is the greenlight needed to specify and estimate the autoregressive distributed lag-error correction model (ARDL-ECM). It must be noted that Engle and Granger (Citation1987) were the first to establish the connection between cointegration and error correction. The ECM essentially provides information about the variables’ causal factors, and the error correction term which is negative and significant ensures that the model’s variables can form a long-run relationship. This is a simple method for demonstrating variable cointegration (Banerjee et al., Citation1998). An error correction term among cointegrated variables depicts the changes in the dependent variable in relation to the independent variables. This represents the deviation in the dependent variable from the long-run equilibrium relationship over a short period. Granger pointed out that variable cointegration implies the existence of information about long-run and short-run Granger causation (Masih & Masih, Citation1997). The ARDL model is used in this study to investigate whether foreign direct investment impact or Granger causes economic growth in Namibia. The Granger method is used to create the following ARDL-error correction representation for empirical purposes:

where,

all the other variables and characters are as described above.

Short-run causality exists in EquationEquation 2(2)

(2) if the independent variables in the first differences in the ARDL-ECM are significant. In contrast, long-run causality is demonstrated by significant t-statistics of the error correction term lagged once (ECMt-1).

4. Empirical results

The current section discusses the study’s empirical findings. The first part gives a discussion of the unit root tests based on the Augmented Dickey-Fuller and Phillips Peron tests. The second part discusses cointegration tests using the ARDL bounds test. The third part discusses only the signs of the estimated long-run coefficients, as these results are meaningless from an economic standpoint. The fourth part elaborates on the ARDL-ECM model’s results. Finally, the section concludes with a discussion of diagnostic tests for the estimated ARDL-ECM equation.

4.1. Unit root tests and the bounds test for cointegration

Checking the stationarity of a series is a prerequisite for any econometrics application. According to Granger and Newbold (Citation1974), working with non-stationary variables may produce erroneous results and incorrect inferences. It is, therefore, crucial that the series be stationary, as spurious results indicate a high value, highly significant t-ratios, and the absence of interdependencies between the variables of the proposed model. The study determines the order of variable integration using the ADF and PP unit root tests. Table below presents the results of these two tests, and they show that five of the variables are stationary after first differencing (integrated of order [I(1)], while three are stationary in levels (integrated of order zero [I(0)]). The fact that some of the variables are I(1) while others are I(0) and that no variables are integrated of order two [I(2)] validates the application of the ARDL methodology. The study then applied the Pesaran et al. (Citation2001) and Pesaran et al. (Citation1996) ARDL approach to cointegration (the bounds test procedure) to test for the existence of a long-run economic relationship. The bounds test results in Table suggest that the null hypothesis of no cointegration should be rejected in the estimated equation at a 1% significance level. This means that the ARDL bounds testing method can be used since the variables used in the estimated equation have a long-run economic relationship.

Table 1. Unit root tests results

Table 2. The bounds test for cointegration

4.2. The estimation of long-run coefficients

The overarching objective of this article is to determine the impact of FDI on Namibia’s economic growth. To analyse the relationship between FDI and economic growth, I included additional macroeconomic variables that explain growth as control variables. Infrastructure served as an explanatory variable in the initial model, the results of which were not reported. However, I had to drop this variable from the final estimation because it failed to explain Namibia’s economic growth significantly, and its coefficient did not match the a priori assumptions. The results of this estimation are spurious since the adjusted R-squared () is greater than the DW statistic, and this implies that the significance of these results cannot be discussed. Table summarises the final model’s estimated results. The findings demonstrate that FDI positively impacts Namibia’s long-term economic growth. The results demonstrate that the interactive variable (LNFDI_TOPEN) positively impacts Namibia’s long-run economic growth. Thirdly, the proxy for human capital (LNHCAP) has the correct sign for explaining long-term economic growth. Fourthly, government consumption as a proportion of GDP has the correct positive sign as a determinant of economic growth. Fifthly, it is discovered that the proxy for economic stability (LNINFL) has a negative impact on economic growth. Finally, the return-on-investment variable impacts economic growth positively in Namibia.

Table

4.3. The short-term coefficients

Table shows the results of the autoregressive distributed error correction model (ARDL-ECM). First, at the 1% significance level, the FDI in levels positively and significantly impact Namibian economic growth in the short run. However, the first FDI lag negatively and significantly impacts Namibia’s economic growth at the 5% significance level. The results indicate that the cumulative short-run impact multiplier of FDI on economic growth in Namibia is 0.229, which implies that a 1 percent increase in FDI will result in a 0.229 percent increase in economic growth after 1 year. The empirical literature strongly corroborates this finding (see Basu et al., Citation2003; De Gregorio, Citation1992; Blomstrom etal., Citation1994; Balasubramanyam etal., Citation1996; Hansen & Rand, Citation2006; Sunde, Citation2017).

Table 3. The ARDL-ECM with an interactive variable ΔFDI_TOPEN

Second, the interaction term obtained by multiplying FDI and trade openness (FDI_TOPEN) was included in the estimated model to validate the Bhagwati hypothesis in the context of the Namibian economy. This is critical because the nature of the recipient country’s trade policy regime heavily influences the impact of FDI on growth (Kohpaiboon, Citation2003). This interactive variable in levels and its first lag have positive and negative impacts on short-run economic growth at 1% and 5% significance levels, respectively. The cumulative short-run impact multiplier of the interactive variable is positive (0.02032), implying that a 1 percent increase in FDI_TOPEN will lead to a 0.02032 percent increase in economic growth. This implies that FDI and trade openness complement each other in stimulating short-run economic growth in Namibia, emphasising the importance of trade integration into FDI initiatives.

Third, at the 10% significance level, the findings show that domestic investment (LNKAP) positively and significantly impacts short-term economic growth. This demonstrates how domestic investment complements foreign direct investment in stimulating Namibian economic growth. This finding is supported by Shabbir et al. (Citation2021), Uddin et al. (Citation2021), and Majumder et al. (Citation2022), among others, in empirical literature. Fourth, human capital (LNHCAP), as measured by primary and secondary school enrolments, has a positive and significant impact on Namibian economic growth in the short-run at the 1% significance level. Studies by Balasubramanyam et al. (Citation1996), Masih and Masih (Citation1997), Borensztein et al. (Citation1998), Nair‐reichert and Weinhold (Citation2001), Liu et al. (Citation2002), and Akinlo (Citation2004) support this finding.

Fifth, at the 1% significance level, the first difference of return on investment (LNRETOI) is found to have a significant positive impact on Namibian economic growth in the short-run. Additionally, the first lag of the first difference of return on investment is also marginally significant in explaining economic growth at a 10% significance level. This variable’s significance implies that return on investment, which is associated with financial development, may have positively affected Namibian productivity growth. The cumulative short-run impact of RETOI on economic growth is 0.4448, implying that a 1 percent increase in the return on investment in Namibia leads to a 0.4448 percent increase in economic growth. This result is corroborated by Asiedu’s research findings (2001).

Sixth, the study discovered a strong inverse relationship between inflation (LNINFL) and short-term economic growth. This finding confirms that Namibia’s economy remained relatively stable during the study period (1990–2020). This is also illustrated by statistical data on Namibia, which shows that inflation has remained below 6% per year for the greater part of the period studied. This finding is also corroborated in economic literature by Mohammed and Mahfuzul (Citation2016) and Majumder et al. (Citation2022). Seventh, the general government consumption (LNGOVC) positively impacts economic growth in Namibia in the short run at the 10% significance level. Empirical literature also supports this finding (see Bove & Elia, Citation2017; Majumder et al., Citation2022).

Finally, the results show a long-run equilibrium relationship between economic growth and the independent variables that explain it in Namibia. More specifically, the results show that the coefficient of the error correction term of 0.3070 is negative and significant at the 5% significance level. This implies that economic growth adjusts towards its long-run equilibrium at 30.7% per annum, which implies that full equilibrium will be reached in the fourth year.

4.3.1. Diagnostic tests

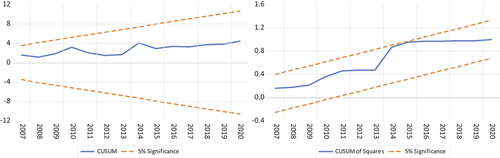

As explained below, the ARDL-ECM equation reported in Table passes a battery of diagnostic tests. First, the Ramsey RESET test indicates that the estimated model has no general specification error. Second, the Jarque-Bera test confirms residual normality in the estimated equation residuals. Third, the no serial correlation null hypothesis in the estimated equation residuals is not rejected by the Breusch-Godfrey LM test. Fourth, the ARCH test for heteroscedasticity rejects heteroscedasticity’s presence in the estimated equation’s residuals. Finally, to test for the stability of the estimated parameters of the ARDL-ECM, I used the CUSUM and CUSUM of squares tests developed by Brown et al. (Citation1975). The results of the CUSUM and the CUSUM of squares plots in Figure indicate parameter constancy and model stability in the estimated ARDL-ECM. All the diagnostic tests show that the estimated equation results are robust and reliable.

Figure 1. CUSUM and CUSUM of squares.

5. Conclusions and future research

This article aimed to empirically explore FDI’s impact on economic growth in Namibia. Overall, the analysis shows the existence of short- and long-run relationships between economic growth, FDI, gross fixed capital formation, human capital, trade openness, government size, return on investment and the country’s overall economic stability. This article, therefore, concludes that FDI alone is not enough to influence economic growth and that some other factors are needed to complement or inhibit FDI’s impact on growth. The article further concludes that the extent to which the country would take advantage of FDI depends on human capital development, trade openness, government size, return on investment and economic stability (inflation). It should be noted that macroeconomic instability was found to affect economic growth negatively. This helps emphasise the important role a stable macroeconomic environment plays in attracting FDI and hence the growth of the economy.

Another important finding is that the interaction term obtained by multiplying FDI and trade openness positively impacts Namibian economic growth. This implies that the Bhagwati hypothesis is validated in Namibia, which means that FDI and trade openness complement each other in stimulating short-run economic growth in Namibia, emphasising the importance of trade integration into FDI initiatives. It should be noted that trade openness also leads to an increase in foreign capital inflow and exports, which have multiplier effects on economic growth.

Another important finding is that FDI is essential for achieving economic growth, provided absorptive capacity is created through increased exports, increased capital goods imports, trade liberalisation policies and human capital development. The positive impact of human capital development on economic growth perhaps reflects an increase in public investment in education and training or the increasing specialisation in the educational system in Namibia. This implies that if there is a flexible labour market, firms can benefit from trade and institutional reforms.

This article has some limitations. The first one being that it does not include all the factors that affect economic growth, and this was because some of the critical variables did not perform very well in the preliminary estimation. However, despite this, we tried to include variables most relevant to Namibia’s economic situation. The study is also limited in generalizability to other countries in Southern Africa or globally because it focuses on a small open economy in Southern Africa with a unique context. However, it offers compelling evidence and discussion points that could interest future researchers conducting similar studies in other regions of the world.

For FDI to significantly contribute to economic growth in Namibia, the government must focus on improving physical infrastructure and the quality of human resources. It should also facilitate the development of an entrepreneurship culture, create a stable macroeconomic environment, and improve conditions for productive investments to accelerate economic growth and development.

Disclosure statement

No potential conflict of interest was reported by the author.

Data availability statement

The data used in the study is accessible through the following provided link: https://data.mendeley.com/datasets/j6d6j2bb6c/1.

Additional information

Notes on contributors

Tafirenyika Sunde

Tafirenyika Sunde is an Associate Professor at the Namibia University of Science and Technology (NUST), formerly known as the Polytechnic of Namibia. He also serves as an Extraordinary Associate Professor at South Africa’s North-West University (NWU). Prior to joining the then Polytechnic of Namibia in 2008, he worked as a Teaching Assistant at the University of Zimbabwe (UZ) and as a Lecturer at the Midlands State University (MSU). His research interests include macroeconomics, energy economics, econometrics, and public policy. Sunde has published several research articles in peer-reviewed local and international journals. This article on the influence of FDI on economic growth belongs to the macroeconomics genre. He holds a DLitt et Phil in Economics from the University of South Africa and an MSc and a BSc from the University of Zimbabwe.The article investigated the impact of FDI on economic growth in Namibia. This is a fascinating topic to researchers and the country as the study tries to illustrate the importance of attracting FDI to a developing country that does not have enough resources to fund investment domestically. It is known that a country that can invest either through domestic or foreign capital is likely to create the desperately needed jobs in most developing countries and grow the economy and hence the country’s GDP. The study results indicate that FDI is significant in explaining economic growth in Namibia. Additionally, the other control variables that were included in the model were also found to positively influence economic growth in Namibia, which suggests that besides FDI, some other variables are important in explaining economic growth.

References

- Abdouli, M., & Hammami, S. (2017). The impact of FDI inflows and environmental quality on economic growth: An empirical study for the MENA countries. Journal of the Knowledge Economy, 8(1), 254–15. https://doi.org/10.1007/s13132-015-0323-y

- Aitken, B. J., & Harrison, A. E. (1999). Do domestic firms benefit from direct foreign investment? Evidence from Venezuela. The American Economic Review, 89(3), 605–618. https://doi.org/10.1257/aer.89.3.605

- Akinlo, A. E. (2004). Foreign direct investment and growth in Nigeria: An empirical investigation. Journal of Policy Modeling, 26(5), 627–639. https://doi.org/10.1016/j.jpolmod.2004.04.011

- Alfaro, L., Chanda, A., Kalemli-Ozcan, S., & Sayek, S. (2004). FDI and economic growth: The role of local financial markets. Journal of International Economics, 64(1), 89–112. https://doi.org/10.1016/S0022-1996(03)00081-3

- Ali, N., & Mingque, Y. (2018). Does foreign direct investment lead to economic growth? Evidence from Asian developing countries. International Journal of Economics and Finance, 10(3), 109–119. https://doi.org/10.5539/ijef.v10n3p109

- Ang, J. B. (2008). Determinants of foreign direct investment in Malaysia. Journal of Policy Modeling, 30(1), 185–189. https://doi.org/10.1016/j.jpolmod.2007.06.014

- Ang, J. B. (2009). Do public investment and FDI crowd in or crowd out private domestic investment in Malaysia? Applied Economics, 41(7), 913–919. https://doi.org/10.1080/00036840701721448

- Axarloglou, K., & Pournarakis, M. (2007). Do all foreign direct investment inflows benefit the local economy? The World Economy, 30(3), 424–445. https://doi.org/10.1111/j.1467-9701.2006.00824.x

- Balasubramanyam, V. N., Salisu, M., & Sapsford, D. (1996). Foreign direct investment and growth in EP and is countries. The Economic Journal, 106(434), 92–105. https://doi.org/10.2307/2234933

- Banerjee, A., Dolado, J., & Mestre, R. (1998). Error‐correction mechanism tests for cointegration in a single‐equation framework. Journal of Time Series Analysis, 19(3), 267–283. https://doi.org/10.1111/1467-9892.00091

- Basu, P., Chakraborty, C., & Reagle, D. (2003). Liberalisation, FDI, and growth in developing countries: A panel cointegration approach. Economic Inquiry, 41(3), 510–516. https://doi.org/10.1093/ei/cbg024

- Bende‐nabende, A., Ford, J., & Slater, J. (2001). FDI, regional economic integration and endogenous growth: Some evidence from Southeast Asia. Pacific Economic Review, 6(3), 383–399. https://doi.org/10.1111/1468-0106.00140

- Blomstrom, M., Lipsey, R., & Zegan, M. (1994). What Explains Developing Country Growth? National Bureau for Economic Research, NBER Working Paper No. 4132.

- Borensztein, E., De Gregorio, J., & Lee, J. W. (1998). How does foreign direct investment affect economic growth? Journal of International Economics, 45(1), 115–135. https://doi.org/10.1016/S0022-1996(97)00033-0

- Bove, V., & Elia, L. (2017). Migration, diversity, and economic growth. World Development, 89, 227–239. https://doi.org/10.1016/j.worlddev.2016.08.012

- Brown, R. L., Durbin, J., & Evans, J. M. (1975). Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society Series B Methodological, 37(2), 149–163. https://doi.org/10.1111/j.2517-6161.1975.tb01532.x

- Chaudhry, M. A., & Choudhary, M. A. (2006). Why the State Bank of Pakistan should not adopt inflation targeting. SBP Research Bulletin, 2(1), 195–209.

- Choe, J. I. (2003). Do foreign direct investment and gross domestic investment promote economic growth? Review of Development Economics, 7(1), 44–57. https://doi.org/10.1111/1467-9361.00174

- Chowdhury, A., & Mavrotas, G. (2006). FDI and growth: What causes what? The World Economy, 29(1), 9–19. https://doi.org/10.1111/j.1467-9701.2006.00755.x

- De Gregorio, J. (1992). Economic growth in Latin America. Journal of Development Economics, 39(1), 59–84. https://doi.org/10.1016/0304-3878(92)90057-G

- Démurger, S. (2001). Infrastructure development and economic growth: An explanation for regional disparities in China? Journal of Comparative Economics, 29(1), 95–117. https://doi.org/10.1006/jcec.2000.1693

- De Vita, G., & Kyaw, K. S. (2009). Growth effects of FDI and portfolio investment flows to developing countries: A disaggregated analysis by income levels. Applied Economics Letters, 16(3), 277–283. https://doi.org/10.1080/13504850601018437

- Durham, J. B. (2004). Absorptive capacity and the effects of foreign direct investment and equity foreign portfolio investment on economic growth. European Economic Review, 48(2), 285–306. https://doi.org/10.1016/S0014-2921(02)00264-7

- Duttaray, M., Dutt, A. K., & Mukhopadhyay, K. (2008). Foreign direct investment and economic growth in less developed countries: An empirical study of causality and mechanisms. Applied Economics, 40(15), 1927–1939. https://doi.org/10.1080/00036840600949231

- Engle, R. F., & Granger, C. W. (1987). Cointegration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society, 55(2), 251–276. https://doi.org/10.2307/1913236

- Granger, C. W., & Newbold, P. (1974). Spurious regressions in econometrics. Journal of Econometrics, 2(2), 111–120. https://doi.org/10.1016/0304-4076(74)90034-7

- Hansen, H., & Rand, J. (2006). On the causal links between FDI and growth in developing countries. The World Economy, 29(1), 21–41. https://doi.org/10.1111/j.1467-9701.2006.00756.x

- Hermes, N., & Lensink, R. (2003). Foreign direct investment, financial development and economic growth. The Journal of Development Studies, 40(1), 142–163. https://doi.org/10.1080/00220380412331293707

- Herzer, D., & Klasen, S. (2008). In search of FDI-led growth in developing countries: The way forward. Economic Modelling, 25(5), 793–810. https://doi.org/10.1016/j.econmod.2007.11.005

- Iqbal Chaudhry, N., Mehmood, A., & Saqib Mehmood, M. (2013). Empirical relationship between foreign direct investment and economic growth: An ARDL co‐integration approach for China. China Finance Review International, 3(1), 26–41. https://doi.org/10.1108/20441391311290767

- Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration--with applications to the demand for money. Oxford Bulletin of Economics and Statistics, 52(2), 169–210.

- Kohpaiboon, A. (2003). Foreign trade regimes and the FDI–growth nexus: A case study of Thailand. The Journal of Development Studies, 40(2), 55–69. https://doi.org/10.1080/00220380412331293767

- Liang, C., Shah, S. A., & Bifei, T. (2021). The role of FDI inflow in economic growth: Evidence from developing countries. Journal of Advanced Research in Economics and Administrative Sciences, 2(1), 68–80. https://doi.org/10.47631/jareas.v2i1.212

- Li, X., & Liu, X. (2005). Foreign direct investment and economic growth: An increasingly endogenous relationship. World Development, 33(3), 393–407. https://doi.org/10.1016/j.worlddev.2004.11.001

- Lin, B., & Benjamin, I. N. (2018). Causal relationships between energy consumption, foreign direct investment and economic growth for MINT: Evidence from panel dynamic ordinary least square models. Journal of Cleaner Production, 197, 708–720. https://doi.org/10.1016/j.jclepro.2018.06.152

- Liu, X., Burridge, P., & Sinclair, P. J. (2002). Relationships between economic growth, foreign direct investment and trade: Evidence from China. Applied Economics, 34(11), 1433–1440.

- Ludoșean, B. M. (2012). A VAR analysis of the connection between FDI and economic growth in Romania. Theoretical and Applied Economics, 19(575), 115–130.

- Lumbila, K. N. (2005). Risk, FDI and economic growth: A dynamic panel data analysis of the determinants of FDI and its growth impact in Africa. American University.

- Majumder, S. C., Rahman, M. H., & Martial, A. A. A. (2022). The effects of foreign direct investment on export processing zones in Bangladesh using Generalized Method of Moments Approach. Social Sciences & Humanities Open, 6(1), 100277. https://doi.org/10.1016/j.ssaho.2022.100277

- Makaranga, J. (2019). Foreign Direct Investment (FDI), Quality of Institutions and Economic Growth: Evidence from African Economies ( Doctoral dissertation).

- Masih, A. M., & Masih, R. (1997). On the temporal causal relationship between energy consumption, real income, and prices: Some new evidence from Asian-energy dependent NICs based on a multivariate cointegration/vector error-correction approach. Journal of Policy Modeling, 19(4), 417–440. https://doi.org/10.1016/S0161-8938(96)00063-4

- Mohammed, E. H., & Mahfuzul, H. (2016). Foreign direct investment, trade, and economic growth: An empirical analysis of Bangladesh. Economies, 4(4), 36–49. https://doi.org/10.3390/economies4020007

- Nair‐reichert, U., & Weinhold, D. (2001). Causality tests for cross‐country panels: A New look at FDI and economic growth in developing countries. Oxford Bulletin of Economics and Statistics, 63(2), 153–171. https://doi.org/10.1111/1468-0084.00214

- Nguyen, H. T. (2011). Exports, imports, FDI and economic growth. Department of Economics, University of Colorado at Boulder. Center for Economic Analysis

- Odhiambo, N. M. (2022). Foreign direct investment and economic growth in Kenya: An empirical investigation. International Journal of Public Administration, 45(8), 620–631. https://doi.org/10.1080/01900692.2021.1872622

- Omran, M., & Bolbol, A. (2003). Foreign direct investment, financial development, and economic growth: Evidence from the Arab countries. Review of Middle East Economics and Finance, 1(3), 231–249. https://doi.org/10.1080/1475368032000158232

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Pesaran, M. H., Smith, R. J., & Shin, Y. (1996). Testing for the Existence of a long run Relationship. DAE Working Paper No.9622, Department of Applied Economics, University of Cambridge.

- Quoc, C. H., & Thi, C. D. (2018). Analysis of foreign direct investment and economic growth in Vietnam. International Journal of Business, Economics and Law, 15(5), 19–27.

- Rafat, M. (2018). The interactive relationship between economic growth and foreign direct investments (FDI): A VAR analysis in Iran. Iranian Economic Review, 22(1), 163–185.

- Rangel González, E., & López Ornelas, L. F. (2022). Foreign direct investment and labour productivity in the regional manufacturing industry. EconoQuantum, 19(1), 20–52. https://doi.org/10.18381/eq.v19i1.7252

- Rehman, A., Ma, H., Ahmad, M., Ozturk, I., & Işık, C. (2021). Estimating the connection of information technology, foreign direct investment, trade, renewable energy and economic progress in Pakistan: Evidence from ARDL approach and cointegrating regression analysis. Environmental Science and Pollution Research, 28(36), 50623–50635. https://doi.org/10.1007/s11356-021-14303-9

- Shabbir, M. S., Bashir, M., Abbasi, H. M., Yahya, G., & Abbasi, B. A. (2021). Effect of domestic and foreign private investment on economic growth of Pakistan. Transnational Corporations Review, 13(4), 437–449. https://doi.org/10.1080/19186444.2020.1858676

- Sunde, T. (2017). Foreign direct investment, exports and economic growth: ADRL and causality analysis for South Africa. Research in International Business and Finance, 41, 434–444. https://doi.org/10.1016/j.ribaf.2017.04.035

- Uddin, M. A., Ali, M. H., & Masih, M. (2021). Institutions, human capital and economic growth in developing countries. Studies in Economics and Finance, 38(2), 361–383. https://doi.org/10.1108/SEF-10-2019-0407

- Wang, M., & Sunny Wong, M. C. (2009). What drives economic growth? The case of cross‐border M&A and greenfield FDI activities. Kyklos, 62(2), 316–330. https://doi.org/10.1111/j.1467-6435.2009.00438.x

- Zhao, C., & Du, J. (2007). Causality between FDI and economic growth in China. The Chinese Economy, 40(6), 68–82. https://doi.org/10.2753/CES1097-1475400604