Abstract

The goal of this paper is to emphasize the importance of prioritizing pleasure and enjoyment in the properties being invested in over financial returns. This research aims to determine the impact of hedonism on an individual’s real estate investment decisions, with financial self-efficacy acting as a moderator. The study employs a quantitative, cross-sectional research approach, and data was collected from retail investors (homeowners and prospective home buyers) using a structured questionnaire. A total of 375 responses were obtained through snowball sampling. Further, PLS SEM was taken into consideration to test research hypothesis. The study’s findings indicate that an individual’s hedonism value has a significant positive influence on real estate investment decisions. Moreover, we found that financial self-efficacy has a significant negative impact on hedonism and real estate investment. One possible reason is that individuals with high financial self-efficacy may be more likely to analyse the financial details of a real estate investment carefully and make decisions based on a well-informed understanding of the potential returns and risks. It has also been observed that both age and income contribute positively to the decision to invest in real estate. This means that a young person is more likely to make risky investments like buying real estate stocks, land, etc. When individuals become older, real estate investment in the form of houses increases in order to provide a secure and comfortable living space for themselves and their families. Finally, when income rises, individuals seem to be looking for a comfortable life, pleasure, happiness, and social recognition, which significantly influence the real estate investment decision.

Public Interest Statement

The impact of hedonism and real estate investment decisions is a subject of significant interest in both academics and practitioners. This study examines the moderating role of financial self-efficacy in the relationship between hedonism and real estate investment decisions. The study finds that financial self-efficacy significantly moderates the relationship between hedonism and real estate investment decisions. Individuals with high levels of financial self-efficacy are less likely to be influenced by hedonistic factors in their real estate investment decisions. The findings suggest that financial self-efficacy plays a crucial role in shaping investment decisions, especially when hedonistic factors come into play. The study provides insights for policymakers and investors in understanding the underlying mechanisms that drive investment decisions and highlights the importance of financial literacy and education in enhancing financial self-efficacy.

1. Introduction

What motivates individual savings and which property investment options individuals’ favour have drawn the attention of financial scholars and market participants. Several real estate investment strategies are available to create wealth (Tsou & Sun, Citation2021), which include direct investments in real estate projects like buying land, apartments, homes, or commercial structures (Feng, Citation2021) for rental purposes and indirect investments like buying real estate stocks, debentures, or a Real Estate Investment Trust (REIT) (Heaney et al., Citation2012). Each kind of investment has unique benefits and drawbacks, including those related to return rate, risk, and payback duration (Rattanaprichavej et al., Citation2020). REITs can be a more logical way to invest because they are judged by financial metrics like earnings, cash flow, and net asset value (Doug & Don, Citation2004, Gibilaro & Mattarocci, Citation2021), not by emotional factors like personal pleasure and satisfaction. Direct real estate investments, on the other hand, can be easier for small investors who value personal satisfaction more than financial returns. Also, the fact that banks use real estate as collateral security when lending money has turned it into an investment (Inoguchi, Citation2011; Lee & Koh, Citation2018). This is the main justification for why real estate is an investment rather than a consumer product. The real estate industry functions in a complex environment are also a fact (Studies et al., Citation2021). While academics have stressed the importance of rational thinking (Mydhili & Dadhabai, Citation2019; Zavadskas et al., Citation2005) and cognitive factors (Jamil, Citation2021; Shim et al., Citation2008; Waheed et al., Citation2020), which impact direct real estate investment, individuals look to their investment selections for “utilitarian” (capitalize on wealth) and “expressive” (using investment as a way to express personal beliefs) advantages (Sreekumar Nair et al., Citation2014). So, the classic wealth maximisation hypothesis, which ignores human values into account, leaves out a key factor that affects investing decisions (Pasewark & Riley, Citation2010).

Since the beginning, the social sciences have put a lot of emphasis on understanding human values and how each person understands their own value system. Not just in the domains of “sociology, psychology, and anthropology,” values have a significant role in economics and finance. Proponents of human values (Crosby et al., Citation1990; Feather, Citation1995; Lane et al., Citation2015; Schwartz, Citation1992) argue effectively for the emotional and directing roles of values in all parts of an individual’s life. Values are used to describe societies and people, to monitor development over time, and to illuminate the driving forces behind attitudes and behaviour (Agyemang & Ansong, Citation2016). They proposed two scales that are commonly referred to as Schwartz’s (Citation1992) Value Survey (SVS) and Rokeach’s (1973) Value Survey. The 10 distinct values suggested by SVS are theoretically drawn from the worldwide necessities of human life. Hedonism is likely the most sophisticated human virtue that has been discussed in the literature, among all the others.

The term hedone, which means “pleasure,” “enjoyment,” or “delight” in Greek, is where hedonism gets its name (Rutkowski, Citation2017). Hedonism, in the view of Schwartz (Citation1992) is associated with “pleasant existence” and “sensual fulfilment” for oneself. In psychology, hedonism refers to as pleasure looking for, which is the key reason for individual behaviour. People who are hedonists have a favourable attitude toward pleasure and actively pursue its benefits (Veenhoven, Citation2003).

In the context of real estate investment, a hedonistic approach might involve prioritizing the enjoyment that a particular property or location will bring, rather than solely considering more practical or financial factors. For example, if an individual considers purchasing a vacation home, they prioritize the beauty of the location and opportunities for relaxation and recreation it offers, rather than solely focusing on factors, such as rental income potential or resale value. We contend that because individual investors are productive adherents of society, their decisions and behavioural progressions might be driven by their particular personal desires like hedonism. The core premise of this argument is that values guide behavioural progression and impacts one’s own choice of action. As a result, it makes sense that people might want to incorporate these deeply held personal values into their financial choices (Agyemang & Ansong, Citation2016).

In the past, researchers have made an effort to comprehend how human values affect individual investment decision-making in stock exchanges and investment choices (Agyemang & Ansong, Citation2016; Singla & Hiray, Citation2019). The significance of the study arises from the fact that behavioural finance researchers have begun to question the rationality (Barberis & Thaler, Citation2002; Bruin & Flint-Hartle, Citation2003; Zhang & Zheng, Citation2015) and market efficiency assumptions that underlie classic theories of finance and economics (Ruoxi, Citation2019). According to these academics, retail investors (non-professional) are not always logical and reasonable, and their decision-making is far more complicated than utility maximisation (Agyemang & Ansong, Citation2016; Feather, Citation1995; Kinatta et al., Citation2022; Lane et al., Citation2015; Pasewark & Riley, Citation2010; Singla & Hiray, Citation2019; Sreekumar Nair et al., Citation2014); therefore, hedonism values do influence their real estate investing decision.

Financial self-efficacy influences domain-specific activities or both direct and indirect ways to perceive satisfactory positive outcomes that individuals often anticipate due to their higher predictive ability (Bandura, Citation1977, Citation2010; Sabri et al., Citation2022). Financial self-efficacy may also help people reach their goals by controlling their behaviour (Lone & Bhat, Citation2022; Noor et al., Citation2020). Thus, decision-making requires information and confidence (Danes & Haberman, Citation2007). Previous research has suggested that self-efficacy can influence factors such as risk-taking behavior, goal setting, and decision-making confidence (Bandura, Citation1977) all of which could be relevant to the relationship between hedonism and real estate investment decisions. By considering the role of self-efficacy as a moderating variable, this study hopes to shed new light on the complex interplay between hedonism, financial self-efficacy, and real estate investment decisions.

However, previous researchers have not focused much more attention on how a hedonistic value influences an individual’s decision to make a real estate investment. So, it can be inferred that individuals with sound financial self-efficacy will be aware and make daring investment decisions. However, there is little pragmatic support for this claim. Hence, the current study addresses this gap by examining the moderating contribution of financial self-efficacy to the relationship between hedonism and real estate investing decisions. Based on the literature survey, the following are the two arising questions:

RQ1:

Does hedonism have a substantial effect on retail investor’s investment decision-making in real estate?

RQ2:

Can an individual’s level of financial self-efficacy have a noteworthy impact on hedonism to make sound real estate investment decisions either by strengthening or weakening their decision-making skills?

The remaining portions of the paper are summarized as follows: Section “Related literature” discusses theoretical background with a survey of the literature and hypothesis development, section “Research methods” talks about the population and sample, measurements, and questionnaire. Section “Research methodology” explains about data analysis. Section “Practical implication” highlights about the managerial and societal implications of the findings of the study.

2. Related literature

2.1. Theoretical background

From a theoretical perspective, the implications of hedonism on real estate investment decisions can be viewed through the lens of behavioural finance. This study of behavioural finance explores how investment decisions can be affected by psychological and emotional factors (Fu, Citation2022). One theory that may be relevant to the implications of hedonism on real estate investment decisions is prospect theory. According to Prospect theory, people have a tendency to base their decisions on their expected gains and losses they perceive, rather than on objective probabilities (Kahneman & Tversky, Citation1979; Tversky & Kahneman, Citation2000). While concerning real estate investment, hedonistic investors may be more likely to invest in properties hat offer the potential for pleasure and comfort, even if the potential returns are lower than other investment options (Alba & Williams, Citation2013).

Another theory that may be relevant is the hedonic adaptation theory, which suggests that people have a tendency to adapt to their current level of pleasure and happiness, and that the pursuit of pleasure and happiness can become a never-ending cycle (Lyubomirsky, Citation2010; Yu & Jing, Citation2016), in order to sustain a certain level of pleasure and happiness. Hence, these theories suggest that hedonistic investors may be more likely to make real estate investment decisions. Even if the potential earnings are lower than those of other investment possibilities, hedonistic investors may be more likely to invest in real estate properties that have upscale amenities and recreational areas based on the properties’ perceived potential for pleasure and comfort rather than the objective probabilities of financial returns, which can have a significant impact on the real estate market.

2.2. Literature Review and hypothesis development

2.2.1. Indian real estate market

During the year 2023, the Indian real estate market was worth $200 billion and is expected to be worth $1 trillion by 2030. By 2025, it will contribute 13% to country’s Gross Domestic Product. In real estate, there are three main categories, including residential, commercial, and retail, and it is projected that the development of nuclear families, rapid urbanization, and rising family income will continue to be the primary growth drivers of these categories (Moore et al., Citation2022). Although the sector has a remarkable profile, it lacks academic representation (Pandey & Jessica, Citation2019).

2.2.2. Hedonism and real estate investment decision

One of the values that consistently appears on scales designed to gauge value preference is hedonism. Abdolmohammadi and Baker (Citation2006) studied the correlation between the accountants’ personal values and moral reasoning and found that hedonism is one of the concerns involved in the list of terminal values, in which five parameters, such as “comfortable life, exciting life, happiness, pleasure, and social recognition” with the aim of verifying “Rockeach’s four-factor (RVS) model and seven-factor classifications” using confirmatory analysis.

Vilnai-Yavetz and Gilboa (Citationn.d..), on the other hand, examined the impacts of instrumentality, aesthetics, and symbolism and analysed how these parameters adapt to customers shopping for their dress choices and found a significant relationship existed between hedonism and perceived receptiveness for all assumed business contexts, but an insignificant relationship was found between hedonism and instrumentality, revealed that hedonists live purely for enjoyment and consumption of possessions.

Agyemang and Ansong (Citation2016) aimed to provide theoretical and practical insights into the impact of personal values on investment decisions made by shareholders in Ghana. Their research revealed that shareholders hold certain value priorities with honesty, a comfortable life, and family security being particularly significant in both their personal lives and in investment decision-making.

Sekscinska et al., (Citation2018) investigated about the people’s variations in terms of time perspectives (TPs) and risky financial decisions. The research emphases on the function that TPs play in elucidating because individuals make dangerous decisions regarding their finances. The findings indicate that chronic hedonistic TPs, both in the past and present, play a significant role in the selection of risky financial options. Even though the focus of the study was on TPs, it demonstrates a substantial effect of hedonism on risky investment choices by demonstrating a low willingness to investment and in taking financial risks.

Amatulli and Donato (Citation2019) illustrated that attitude, willingness to buy, and consumer orientation toward luxury products have been deeply measured to test the effect that exists between hedonic and utilitarian messages. Observations prove that luxury managers should follow hedonistic messaging, which builds close relationships with other managers and increases the attraction of customer perceptions towards their brand.

Singla and Hiray (Citation2019) examined impact of the value of hedonism (exciting life, pleasure, comfortable life, happiness, and social recognition), age, gender, and income on preferences of investments like stock exchange, bullion, gold, real estate, and fixed income options in India through structured equation modelling. The findings of the study found to be there was a substantial correlation between hedonism and investment preferences, like stock and property investments. It also found that age and income effect hedonism negatively.

A questionnaire study was done by A. Khan et al. (Citation2022) to learn about customers' intention to buy and how their perceptions of currency values were impacting their shopping trips in Pakistan. New perspectives on hedonism’s nature, repurchase intentions, and the evolution of more enticing purchasing tactics that encourage customers to fully appreciate their purchases were revealed by the research.

N Mahalakshmi and Munuswamy (Citation2022) carried out a questionnaire survey to determine the influence of decision-making style on the choice of stock investments and found that hedonism had a negative influence on the choice of stock investment among millennial investors. Although the studies mentioned may not be directly related to investment decision-making, the research suggests that hedonism does indeed play a crucial role in the real estate decision-making process as a cognitive mechanism. “Happiness” is the main focus of hedonism (Bramble, Citation2016) and having wealth helps people be happier to some extent. Wealth creation is the goal of investment decision;

With an extensive literature survey on hedonism measurement, there are various interpretations employed from various situations, which show that studies on examining the association between hedonism and real estate investment decisions are countable; as a result, there is a glaring knowledge deficit in this area. Thus, this article aims to explore how an individual’s value of hedonism affects the person’s decision to invest in real estate in India.Based upon the literature the hypothesis has been set as

H1:

Hedonism shows the significant effect on retail investors’ investment decision in real estate.

2.2.3. Financial self-efficacy

The impression of self-efficacy in behavioural psychology, once mentioned as intelligence of self-agency, stood in a confidence that individual can achieve a given job and further generally cope with life’s tasks (Lone & Bhat, Citation2022). Financial self-efficacy is the belief in one’s ability to effectively manage their financial affairs (Zia-Ur-Rehman et al., Citation2021). Individuals with higher levels of financial self-efficacy are less likely to be influenced by hedonistic desires in their real estate investment decisions. They are more likely to consider the long-term financial implications of their investments and make decisions based on their financial goals and objectives as they are more likely to focus on the potential long-term appreciation and rental income of the property. In contrast, a person with low financial self-efficacy may be more susceptible to making investment decisions based on immediate gratification, such as the attractiveness of the property or the lifestyle it offers. Recent research has found that financial self-efficacy acts as a key role in financial decisions, such as financial management behaviour (Fathul Bari et al., Citation2020; Noor et al., Citation2020; Kusairi et al., Citation2020), women’s financial behaviour (Farrell et al., Citation2016), financial satisfaction (Mubarik et al., Citation2020; Rehman et al., Citation2020), financial well-being (Lone & Bhat, Citation2022), investment intention (Elfahmi et al., Citation2020) and investment decisions (N. Khan et al., Citation2021). Therefore, financial self-efficacy can serve as a moderating factor in the relationship between hedonism and real estate investment decision-making. On seeing the above literature on financial self-efficacy, the hypothesis has been set as

H2:

Financial self-efficacy displays a significant outcome on weakening the influence of hedonism on retail investors’ investment decision in real estate.

2.2.4. Control variables

In previous studies, demographic factors like age, gender, income, education, and risk tolerance had a significant impact on investment choices and decision-making (Chavali & Mohanraj, Citation2016; Geetha & Ramesh, Citation2012; Kellerman et al., Citation2020; Nasage, Citation2019; Wubie et al., Citation2015). Also, studies have been done in which demographic factors like age and income have an insignificant impact on investment choices (Singla & Hiray, Citation2019). This study uses the control variables age and income to evaluate how age and income affect respondents’ real estate investment decisions. The hypothesized model is illustrated in Figure

Figure 1. The hypothesized Research Model with moderating effect.

3. Research method

Researchers in the current study want to comprehend how hedonism affects individuals’ real estate investment decisions in India and the part played by financial self-efficacy of individuals in strengthening or weakening the association.

3.1. Population and sample

The study’s target audience consists of Indians, who prefer real estate as a form of investment. A sampling unit for the survey consisted of individuals who had invested in or were planning to invest in real estate (land, a flat, apartment, or constructing floors for rentals etc.). There is no reliable source in India where information about those who invest in real estate can be accessed. Therefore, there was no sampling frame available for the intended population. Multistage (in three stages) stratified sampling is employed to gather the data. The study adopted the sampling technique from a previous research paper (Pandey & Jessica, Citation2019). The first and second stages of stratification are based on region and location, respectively, and the third stage involves contacting the respondents using snowball and purposive sampling. The study used the sample size of the sample-to-item ratio (1:10) (F. Hair et al., Citation2014; Memon et al., Citation2020). Four hundred and one investors in real estate participated in the online poll and responded. Due to response issues, such as erroneous data, missing data, and incomplete polls, some responses are eliminated. Finally, 375 replies meet the criteria for further investigation, with a response rate of 93%. The questionnaire contains preliminary questions to determine potential participants for the study. These questions inquire whether individuals have invested in real estate or plan to do so, the type of real estate they have invested in or intend to invest in, and the timing of their investment, specifically whether they are first-time investors or not. If respondents answered affirmatively to question (i) regarding real estate investment, those respondents were considered a sample for the study.

3.2. Measurements and questionnaire

The hedonism was measured on a 1–5 Likert scale, with 5 representing “very high importance” and 1 signifying “very low importance” in the data collection process. A self-administered questionnaire was used and adopted from Singla and Hiray (Citation2019). The scale measured on a Likert scale of “strongly disagree” to strongly agree” for investment decisions on real estate was adapted from Wangzhou et al. (Citation2021) and financial self-efficacy was measured from Lown (Citation2011). A list of constructs with their items is listed in Table .

Table 1. List of constructs with its items

3.3. Methodology

The methodology involved in the analysis of data can be segmented into two parts. The first part involves sociodemographic profiling, and their results are shown in Table . In the second part, structural equation modelling is conducted in two stages. The first of which involves an investigation to validate reliability, discriminant validity, and convergent validity for a measurement model using PLS 3.0, the partial least squares (PLS). In the second stage, the structural model was then calculated for its path coefficient and propensity to predict a significance threshold of 5% (J. F. Hair et al., Citation2017).

Table 2. Investors’ Socio demographic profiling

4. Empirical analysis

4.1. Investors Socio demographic profiling

The current research segments the respondents’ age as ranging from 20 to above 60 years, which means that while a higher percentage (28) of the respondents belongs to 31–40 age group, 26% fall in the category of 41–50 years. Those between 51 and 60 years of age constitute 20% of the total sample size, and only 9% of the respondent population is from 20 to 30 years of age and comprised of 65.6% males and 34.4% females. Government and private sector employees constitute 25% and 21%, respectively, and the remainder belong to other groups. Out of the total respondents, 46% earn monthly incomes above INR 2 lakhs, 20% from the monthly income category of 150,001–200000 and the rest from other groups that are listed in Table .

4.2. Measurement model Analysis (outer model)

4.2.1. Reliability and validity

The measurement model was assessed by indicator reliability, construct reliability, convergent validity, and discriminant validity. The indicator reliability, which was measured using factor loading, ranged from 0.830 to 0.882, i.e., over the 0.70 threshold (J. F. Hair et al., Citation2017), which validates the indicator reliability. The constructed reliability can be evaluated by Cronbach’s alpha and composite reliability. The study had a composite reliability of 0.931, 0.936, and 0.942, respectively, which exceeds 0.8 for each latent variable meeting the criterion (Henseler et al., Citation2009). As a result, construct reliability was achieved. Next, for determining convergent validity, average variance extracted (AVE) was considered. Convergent validity is achieved if the constructs’ AVE is 0.5 or above (Henseler et al., Citation2009). All conceptions had AVE values over 0.50. Hence, convergent validity was achieved. Finally, the values of the variance inflation factor (VIF) were less than 5, indicating multicollinearity was not present. The values of CA, CR, AVE, and VIF were listed in Table .

Table 3. Measurement model assessment

4.2.2. Discriminant validity

To assess the discriminant validity of the study, the Fornell-Larcker criterion and cross-loadings were considered. By considering the Fornell—Larcker criterion, which includes comparing the square roots of each construct’s AVE with the correlation between constructs, discriminant validity was validated. Table shows the findings of the Fornell-Larcker criterion.

Table 4. Discriminant validity

Cross loading is also another method to ensure discriminant validity (F. Hair et al., Citation2014). As a result, establishing discriminant validity at the item level requires that items related to the same construct have a high correlation and items related to distinct constructs have a very low correlation. With this, discriminant validity was justified in the model. Table highlights the discriminant validity using cross loading.

Table 5. Cross loading Tabulation

For the model fit, the SRMR value for the model was found to be 0.06, which is less than 0.08. So, the model was found to be fit.

4.3. Structural model analysis (inner model)

4.3.1. Hypothesis scrutiny

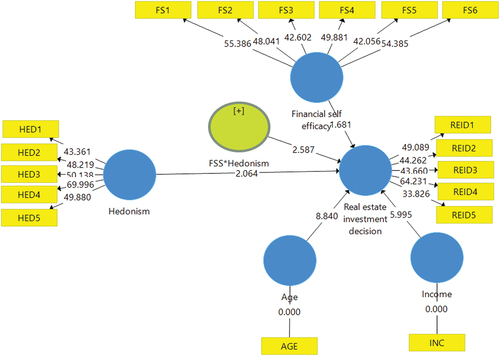

Structural model analysis was implemented to evaluate the relationships within the conceptual framework after validating the variables’ accuracy and reliability. Partial least square (PLS) analysed path coefficients and t-values at 5% level of significance. Hypothesis H1 intends to determine whether hedonism has a substantial impact on real estate investment decision-making. The findings revealed that the influence of hedonism on real estate investment decisions is 0.215 with a t-statistics value of 2.064, which means that hedonism and real estate investment decisions have an encouraging and statistically significant impact (β = 0.215, t = 2.064, p < 0.05). Thus, hedonism has a hugely positive and substantial influence on real estate investment decisions. Further, according to the effect size (f2), the research construct displays a low effect size (Cohen, Citation1988) on real estate investment decisions (f2 = 0.037). The values are noted and illustrated in Table .

Table 6. Evaluation of structural models

4.3.2. Moderation effect analysis

A moderator is a third variable that alters the strength of exogenous and endogenous variables. In the study, it was hypothesized that financial self-efficacy moderates the relationship between hedonism and real estate investment decisions. The results showed a significant negative interaction effect of financial self-efficacy on hedonism and real estate investment decision (REID) (β = −0.153, t = 2.587, p < 0.05), indicating that the relationship between these variables is weakened by financial self-efficacy. This finding supports hypothesis H2 and is presented in Table . Figure shows the interaction between hedonism and financial self-efficacy.

Figure 2. Structural model.

Table 7. Moderation effect

4.3.3. Control variables on real estate investment decision

The assessment of the sociodemographic factors (age and income) that were used as a control variable was used in the study. Based on the results of the analysis, both age (β = 0.390, t = 8.840, p < 0.01) and income (β = 0.320, t = 5.995, p < 0.01) were found to have significant differences on the real estate investment decision-making of the retail investors, which is shown in Table . The final structural research model is shown in Figure , as follows:

Table 8. Control variable Effect

4.4. Analysis of coefficient of determination (R-square)

R square statistics reveals how much of the change in the exogenous variable is explained by the endogenous variable. According to Hair et al., (Citation2011), in academic research, an R-squared value of 0.75,0.50, and 0.25 for a dependent variable can be considered substantial, moderated, and weak, respectively. The calculation results of the R square value of individual real estate investment decisions are 0.56, which suggests that the real estate investment decisions (REID) could be described by up to 56% of their predictor variable hedonism, and the model is found to be moderately fit as shown in Table .

Table 9. Coefficient of determination (R-Square)

5. Discussions

This study seeks to examine the impact of hedonism on real estate investment decisions of retail investors and the moderating effect of financial self-efficacy on hedonism and real estate investment decisions. The outcomes positively answer RQ1: Does hedonism impact real estate investment decisions? The findings demonstrate that hedonism has a positive and substantial impact on real estate investment decisions, which is also in line with previous research on hedonism and investment choices (Singla & Hiray, Citation2019). The possible reason is that real estate investment is a high-risk investment that creates pleasure, excitement, a comfortable life, and social recognition that individual endeavour for because of capital appreciation and the generation of passive income from rentals (Rattanaprichavej et al., Citation2020). The fundamental financial fund approach includes both risky and risk-free assets (Hu et al., Citation2021). This means that an individual who subscribes to hedonistic principles and prioritizes pleasure and enjoyment in their decision-making may be more likely to take risks and pursue investments that align with their personal preferences.

Addressing the study question RQ2, “Is financial self-efficacy a significant factor in strengthening or weakening retail investors’ investment decision-making in real estate?” The findings show that financial self-efficacy has a strong detrimental impact on hedonism and real estate investment decisions. Relying on the research findings, it can be explained that a real estate investor’s financial self-efficacy gives them greater control over their decision-making; they may affect it and make a better choice irrespective of pleasure, excitement, and adventures. In addition, individuals with high financial self-efficacy are more likely to make informed decisions based on their financial goals and objectives, while those with low financial self-efficacy may be more susceptible to making impulsive decisions based on their hedonistic desires. So, financial self-efficacy can play a crucial role in direct real estate investment decisions, particularly in moderating the effects of hedonism.

Age demographics have been demonstrated to have a significant influence on real estate investing decisions. An individual at a young age seems to take risky investment choices and decisions so that they will invest in real estate stocks, land, etc. When the ages of individuals grow, because of family size and commitment, their investment in real estate in the form of houses increases. In terms of income, when income increases, individuals seem to look for a comfortable life, pleasure, happiness, and social recognition, which significantly influences real estate investment decisions.

6. Practical implications

6.1. Implication from real estate investors’ perspective as a buyer

If real estate investors as a buyer prioritize hedonistic desires, it may result in more emotionally driven decision-making. For example, a buyer might be more likely to choose a property that offers a luxurious lifestyle, regardless of whether it is a sound financial investment. However, it is also possible that a hedonistic perspective could lead buyers to prioritize properties that offer a high degree of comfort and relaxation, which could ultimately contribute to their overall well-being and happiness. Real estate investors should be aware of the potential impact of hedonism on real estate investment decisions and seek to balance personal enjoyment with financial considerations to make informed investment decisions that align with their values and lead to greater satisfaction. Furthermore, real estate investors with high levels of financial self-efficacy may be better equipped to make investment decisions that balance personal enjoyment with financial considerations, potentially leading to better investment outcomes.

6.2. Implication from real estate investors’ perspective as a seller

The implications of hedonism on real estate investment decisions from a seller’s perspective may include the following:

Understanding buyer preferences: If sellers can identify which aspects of a property are most likely to provide hedonic value to buyers, they can tailor their marketing strategies to highlight those features.

Pricing strategy: Hedonic value can impact the perceived value of a property, which may influence pricing decisions. Sellers may choose to price their property higher if they believe it offers unique hedonic benefits that are not readily available in other properties.

Property maintenance: Maintaining the hedonic value of a property is important to attract buyers. Sellers should invest in maintaining the aesthetics, functionality, and overall ambiance of their property to ensure it continues to provide hedonic benefits to buyers.

6.3. Managerial implication

Managerial implications of hedonism in real estate investment decisions include prioritizing properties that offer amenities that appeal to hedonistic investors, such as luxury features and recreational facilities. One could expect that an individual’s values could have an impact on the investments they make. As a result, the study gives advice to the managers who provide investing services to their investors to make sure that in addition to looking at a person’s demographics and risk profile, they also consider their value system. This will enable them to better serve and target their customers. Marketing properties in a way that emphasizes their hedonistic appeals, such as by highlighting the property’s proximity to recreational activities or its luxurious amenities. Being aware that hedonistic investors may be willing to pay a premium for properties that offer a high level of pleasure and comfort. Also, the interventions have to enhance FSE, which means intensifying the degree of individuals. Given that financial self-efficacy is reliant on an individual’s financial knowledge and expertise, efforts aimed at developing financial capability and strengthening investment stance skills should be targeted towards persons with lower levels of FSE. However, FSE may have a crippling impact due to a misalignment between investors’ perceived capacity to bear financial distress and their levels of monetary understanding (Hu et al., Citation2021; Tang et al., Citation2019). Effective interference strategies may necessitate an additional precise alignment of perceived financial self-efficacy. However, it is important to note that hedonism can be a double-edged sword, as too much emphasis on pleasure and comfort can lead to overindulgence and financial problems. Therefore, it is important for real estate investors and managers to consider both the short-term and long-term consequences of their investment decisions.

6.4. Societal implications

Increased demand for properties that offer luxury amenities and recreational facilities, leading to the development of more high-end properties and the revitalization of certain neighbourhoods. As a consequence of the rise in demand for luxury properties, employment in the construction and hospitality sectors will be created. The potential for increased property values in areas where luxury properties are being developed, which can benefit local residents and businesses. However, there can also be negative societal implications associated with hedonism in real estate investment decisions, such as: Displacement of lower-income residents and small businesses as a result of gentrification and rising property values in certain neighbourhoods. Widening income and wealth inequality as luxury properties become increasingly unaffordable for most people. Overdevelopment and the erection of enormous luxury properties have an adverse impact on the environment and natural resources. It is important to consider these potential societal implications when making real estate investment decisions and to strive for balance and sustainable development.

7. Conclusion, limitations, and future scope

This research study seeks to study the influence of hedonism and real estate investment decision-making while considering the moderating effects of financial self-efficacy, age, and income as control variables. The required data has been gathered through an online questionnaire, and a sample of 375 individual investors was used to confirm the model using SEM. The findings indicate that all aspects of hedonism have a substantial impact on real-estate investing decisions. Financial self-efficacy, which symbolises an investor’s self-control and financial status, assists them in sustaining a positive attitude toward investment. However, financial self-efficacy has negatively eroded the correlation between hedonism and real estate investing decisions. Furthermore, age and income affect real estate investing decisions. This research has quite a few limitations. To start with, the study was cross-sectional in nature; longitudinal research would be preferable to capture changes and differences in human behaviour over time. It is vital to note that this study was restricted to individuals who were keen to share their real estate investment details. Next, while hedonism is one potential factor that could influence real estate investment decisions, it is important to consider a variety of other factors as well, including financial goals, property features, and location. Further studies can be done by using other variables like risk absorption capacity, financial literacy as a mediating variable, and other sociodemographic variables like occupation and education.

Disclosure statement

The author(s) did not disclose any possible conflict of interest.

Additional information

Funding

Notes on contributors

Sharmila Devi R

Sharmiladevi R is pursuing a Ph.D. at the Vellore Institute of Technology (VIT), Vellore, Tamil Nadu, under the supervision of Dr. Swamy Perumandla on the topic of Direct Real Estate Investment Decisions. She has completed bachelor’s degree in B. Tech (Chemical Engineering) from Madras University and Master’s Degree in MBA (Finance and Human resources) affiliated with Anna University. Her research interests include investment decisions in stock and real-estate markets and personal financial management behaviour.

Swamy Perumandla

Perumandla Swamy is an Assistant Professor of Finance at VIT-Business School (VITBS), Vellore Institute of Technology (VIT), Vellore, Tamil Nadu, India. He received his Ph.D. in Finance from the National Institute of Technology Warangal (NIT-W), India. His research and teaching interests include Financial Econometrics, Development Economics, and International Financial & Commodity Derivative Markets.

References

- Abdolmohammadi, M. J., & Baker, C. R. (2006). Accountants’ value preferences and moral reasoning. Journal of Business Ethics, 69(1), 11–18. https://doi.org/10.1007/s10551-006-9064-y

- Agyemang, O. S., & Ansong, A. (2016). Role of personal values in investment decisions: Perspectives of individual Ghanaian shareholders. Management Research Review, 39(8), 940–964. https://doi.org/10.1108/MRR-01-2015-0015

- Alba J. W., & Williams, E. F. (2013). Pleasure principles: A review of research on hedonic consumption. Journal of Consumer Psychology, 23(1), 2–18. https://doi.org/10.1016/j.jcps.2012.07.003

- Amatulli, C., & Donato, C. (2019). An investigation on the effectiveness of hedonic versus utilitarian message appeals in luxury product communication. https://doi.org/10.1002/mar.21320

- Bandura, A. (1977). Self-efficacy: Toward a unifying theory of behavioral change. Psychological Review, 84(2), 191–215. https://doi.org/10.1037/0033-295x.84.2.191

- Bandura, A. (2010). Self‐efficacy. Corsini Encyclopedia of Psychology, 1–3. https://doi.org/10.1002/9780470479216.corpsy0836

- Barberis, N., & Thaler, R. (2002). Chapter 18 A survey of behavioral finance. Handbook of the Economics of Finance, 1(Part B), 1053–1128 . https://doi.org/10.3386/w9222

- Bramble B. (2016). A New Defense of Hedonism about Well-Being. Ergo, an Open Access Journal of Philosophy, 3(20201214). https://doi.org/10.3998/ergo.12405314.0003.004

- Bruin, A., & Flint-Hartle, S. (2003). A bounded rationality framework for property investment behaviour. Journal of Property Investment & Finance, 21(3), 271–284. https://doi.org/10.1108/14635780310481685

- Chavali, K., & Mohanraj, M. P. (2016). Impact of demographic variables and risk tolerance on investment decisions: An empirical analysis. International Journal of Economics and Financial Issues, 6(1), 169–175.

- Cohen, J. (1988). Statistical Power Analysis for the Behavioral Sciences (2nd Ed.). Routledge. https://doi.org/10.4324/9780203771587

- Crosby, L. A., Bitner, M. J., & Gill, J. D. (1990). Organizational structure of values. Journal of Business Research, 20(2), 123–134. https://doi.org/10.1016/0148-2963(90)90056-J

- Danes, S. M., & Haberman, H. R. (2007). Jamestown 7-24-09 parking lot view. Journal of Financial Counseling & Planning, 18(2), 48–60.

- Doug, W., & Don, J. (2004). Home ownership and the decision to invest in REITs. Journal of Real Estate Portfolio Management, 10(2), 129–144. https://doi.org/10.1080/10835547.2004.12089696

- Elfahmi, R., & Ikin Solikin, N. (2020). Model of student investment intention with financial knowledge as a predictor that moderated by financial self-efficacy and perceived risk. Dinasti International Journal of Economics, Finance & Accounting, 1(1), 165–175. https://doi.org/10.38035/DIJEFA

- Farrell, L., Fry, T. R. L., & Risse, L. (2016). The significance of financial self-efficacy in explaining women’s personal finance behaviour. Journal of Economic Psychology, 54, 85–99. https://doi.org/10.1016/j.joep.2015.07.001

- Fathul Bari, A., Yunanto, A., & Shaferi, I. (2020). The role of financial self efficacy in moderating relationships financial literacy and financial management behavior. International Sustainable Competitiveness Advantage, 2018, 51–60.

- Feather, N. T. (1995). Values, valences, and choice: The influence of values on the perceived attractiveness and choice of alternatives. Journal of Personality & Social Psychology, 68(6), 1135–1151. https://doi.org/10.1037/0022-3514.68.6.1135

- Feng, Z. (2021). How does local economy affect commercial property performance? The Journal of Real Estate Finance & Economics, 65(3), 361–383. https://doi.org/10.1007/s11146-021-09848-y

- Fu, C. (2022). Behavioural finance: A synthetic review of literature and future development. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4107830

- Geetha, N., & Ramesh, M. (2012). A study relevance of demographic factors in investment decisions. Perspectives of Innovations, Economics & Business, 10(1), 14–27. https://doi.org/10.15208/pieb.2012.02

- Gibilaro, L., & Mattarocci, G. (2021). Institutional investors and home-biased REITs. Journal of Real Estate Portfolio Management, 27(2), 104–120. https://doi.org/10.1080/10835547.2021.1986347

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM). thousand oaks. Sage, 165.

- Hair, F., Jr, J., Sarstedt, M., Hopkins, L., & G Kuppelwieser, V. (2014). Partial least squares structural equation modeling (PLS-SEM). European Business Review, 26(2), 106–121. https://doi.org/10.1108/ebr-10-2013-0128

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/mtp1069-6679190202

- Heaney, R., Higgins, D., & DiIorio, A. (2012). Investment portfolios and three dimensions of real estate investment: An Australian perspective. Pacific Rim Property Research Journal, 18(4), 335–354. https://doi.org/10.1080/14445921.2012.11104366

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20(2009), 277–319. https://doi.org/10.1108/S1474-7979(2009)0000020014

- Hu, J., Quan, L., Wu, Y., Zhu, J., Deng, M., Tang, S., & Zhang, W. (2021). Financial self-efficacy and general life satisfaction: The sequential mediating role of high standards tendency and investment satisfaction. Frontiers in Psychology, 12. https://doi.org/10.3389/fpsyg.2021.545508

- Inoguchi, M. (2011). Influence of real estate prices on domestic bank loans in Southeast Asia. Asian-Pacific Economic Literature, 25(2), 151–164. https://doi.org/10.1111/j.1467-8411.2011.01308.x

- Jamil, N. (2021). Impact of cognitive dissonance bias on investors’ decisions: moderating role of emotional intelligence. Pakistan Social Sciences Review, 5(III), 538–552. https://doi.org/10.35484/pssr.2021(5-iii)040

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263. https://doi.org/10.2307/1914185

- Kellerman, D., Dickason-Koekemoer, Z., Ferreira, S., & McMillan, D. (2020). Analysing investment product choice in South Africa under the investor lifecycle. Cogent Economics & Finance, 8(1), 1848972. https://doi.org/10.1080/23322039.2020.1848972

- Khan, A., Abbas, B., Jabeen, A., Syed, F., Ali, G., Faisal, M., & Saleem, A. (2022). Hedonism and repurchase: Determining value for money and repurchase intentions in shopping malls. International Journal of Innovations in Science and Technology, 4(3), 943–964. https://doi.org/10.33411/ijist/2022040314

- Khan, N., Usman, A., & Farooq Jan, M. (2021). The impact of investor’s personality traits over their investment decisions with the mediating role of financial self efficacy and emotional biases and the moderating role of need for cognition and the individual mood in Pakistan stock exchange. Multicultural Education, 7(8), 2021. https://doi.org/10.5281/zenodo.5392291

- Kinatta, M. M., Kaawaase, T. K., Munene, J. C., Nkote, I., & Nkundabanyanga, S. K. (2022). Cognitive bias, intuitive attributes and investment decision quality in commercial real estate in Uganda. Journal of Property Investment & Finance, 40(2), 165–187. https://doi.org/10.1108/JPIF-11-2020-0129

- Kusairi, S., Ahmad, N., & Kae, T. J. (2020). The linkages of financial self-efficacy and financial decision behaviour: Learning from female lecturers in East Coast Malaysia. International Journal of Organizational Leadership, 9, 273–287. https://doi.org/10.33844/ijol.2020.60511

- Lane, R. E., Sep, N., Review, S., Political, A., The, S., & Lane, R. E. (2015). The nature of human values. by Milton Rokeach. (New York: The Free Press, 1973. Pp. 438. journal3.95.). 1976 Book Reviews, 70(3), 965–966. https://doi.org/10.2307/1959882

- Lee, H., & Koh, S. (2018). The effect of housing finance regulation on mortgage loan of non-banking sector. The Journal of Korea Real Estate Analysts Association, 24(1), 5–22. https://doi.org/10.19172/kreaa.24.1.1

- Lone, U. M., & Bhat, S. A. (2022). Impact of financial literacy on financial well-being: A mediational role of financial self-efficacy. Journal of Financial Services Marketing, 0123456789. https://doi.org/10.1057/s41264-022-00183-8

- Lown, J. M. (2011). 2011 oustanding AFCPE® Conference paper: Development and validation of a financial self-efficacy scale. Journal of Financial Counseling & Planning, 22(2), 54–63.

- Lyubomirsky, S. (2010). Hedonic adaptation to positive and negative experiences.Oxford Handbooks Online. https://doi.org/10.1093/oxfordhb/9780195375343.013.0011

- Memon, M. A., Ting, H., Cheah, J. -H., Thurasamy, R., Chuah, F., & Cham, T. H. (2020). Sample size for survey research: Review and recommendations. Journal of Applied Structural Equation Modeling, 4(2), ix–xx. https://doi.org/10.47263/jasem.4(2)01

- Moore, A., Giannoni, C., Kirby, N., & Doffman, N. (2022). Real Estate. Artificial Intelligence: Law and Regulation, (July), 378–396. https://doi.org/10.4337/9781800371729.00032

- Mubarik, F., Rehman, M. Z. U., Baig, S. A., Hashim, M., & Shafaqat, S. (2020). Financial inclusion and financial satisfaction: Moderating role of the financial self-efficacy. RADS Journal of Business Management, 2(2), 111–123.

- Mydhili, V., & Dadhabai, S. (2019). Research on determinants of property purchases. International Journal of Innovative Technology and Exploring Engineering, 8(6), 68–73.

- Nasage, N. N. (2019). Influence of demographic factors on individual’s investment decisions in wa municipality, the upper West Region of Ghana. Texila International Journal of Management, 5(2), 197–211. https://doi.org/10.21522/tijmg.2015.05.02.art020

- N Mahalakshmi, T., & Munuswamy, S. (2022). An empirical analysis of the decision-making style of millennials on the choice of financial products. Indian Journal of Marketing, 52(11), 26. https://doi.org/10.17010/ijom/2022/v52/i11/172432

- Noor, N., Batool, I., Arshad, H. M., & McMillan, D. (2020). Financial literacy, financial self-efficacy and financial account ownership behavior in Pakistan. Cogent Economics & Finance, 8(1), 1806479. https://doi.org/10.1080/23322039.2020.1806479

- Pandey, R., & Jessica, V. M. (2019). Sub-optimal behavioural biases and decision theory in real estate: The role of investment satisfaction and evolutionary psychology. International Journal of Housing Markets and Analysis, 12(2), 330–348. https://doi.org/10.1108/IJHMA-10-2018-0075

- Pasewark, W. R., & Riley, M. E. (2010). It’s a matter of principle: The role of personal values in investment decisions. Journal of Business Ethics, 93(2), 237–253. https://doi.org/10.1007/s10551-009-0218-6

- Rattanaprichavej, N., Teeramungcalanon, M., & Foroudi, P. (2020). An investment decision: Expected and earned yields for passive income real estate investors. Cogent Business & Management, 7(1), 1786331. https://doi.org/10.1080/23311975.2020.1786331

- Rehman, F., Baig, M. Z., Hashim, S. A., & Shafaqat, M. (2020). Financial inclusion and financial satisfaction: Moderating role of the financial self-efficacy. RADS Journal of Business Management, 2(2), 111–123.

- Ruoxi, Q. (2019). Behavior analysis of real estate investors. Mfssr, 308–312. https://doi.org/10.25236/mfssr.2019.065

- Rutkowski, I. (2017). Scale for testing hedonic-consumerism values – a new measurement instrument in the consumers ’ behavior. Proceedings International Marketing Trends, 0–27.

- Sabri, M. F., Wijekoon, R., Abd Rahim, H., Burhan, N. A., Madon, Z., & Hamsan, H. H. (2022). Financial literacy, financial behavior, self-efficacy, and financial health among Malaysian households: The mediating role of money attitudes. The International Journal of Academic Research in Business & Social Sciences, 12(13). https://doi.org/10.6007/ijarbss/v12-i13/14150

- Schwartz, S. H. (1992). Universals in the content and structure of values: Theoretical advances and empirical tests in 20 countries. Advances in Experimental Social Psychology, 25(C), 1–65. https://doi.org/10.1016/S0065-2601(08)60281-6

- Sekścińska, K., Rudzinska-Wojciechowska, J., & Maison, D. (2018). Individual differences in time perspectives and risky financial choices. Personality and Individual Differences, 120, 118–126. https://doi.org/10.1016/j.paid.2017.08.038

- Shim, G. Y., Lee, S. H., & Kim, Y. M. (2008). How investor behavioral factors influence investment satisfaction, trust in investment company, and reinvestment intention. Journal of Business Research, 61(1), 47–55. https://doi.org/10.1016/j.jbusres.2006.05.008

- Singla, H. K., & Hiray, A. (2019). Evaluating the impact of hedonism on investment choices in India. Managerial Finance, 45(12), 1526–1541. https://doi.org/10.1108/MF-07-2019-0324

- Sreekumar Nair, A., Ladha, R., Lenssen, G., Nijhof, A., Roger, L., & Kievit, H. (2014). Determinants of non-economic investment goals among Indian investors. Corporate Governance (Bingley), 14(5), 714–727. https://doi.org/10.1108/CG-09-2014-0102

- Studies, D., Das, J. K., Datta, R. N., & Studies, M. (2021). Investment decisions in real estate: A study in Kolkata. International Journal of Management and Development Studies, 10(11), 1–8. https://doi.org/10.53983/ijmds.v10n11.001

- Tang, S., Huang, S., Zhu, J., Huang, R., Tang, Z., & Hu, J. (2019). Financial self-efficacy and disposition effect in investors: The mediating role of versatile cognitive style. Frontiers in Psychology, 9(JAN), 1–6. https://doi.org/10.3389/fpsyg.2018.02705

- Tsou, W. L., & Sun, C. Y. (2021). Consumers’ choice between real estate investment and consumption: A case study in taiwan. Sustainability (Switzerland), 13(21), 11607. https://doi.org/10.3390/su132111607

- Tversky, A., & Kahneman, D. (2000). Loss aversion in riskless choice: A reference-dependent model. Choices, Values, and Frames, 143–158. https://doi.org/10.1017/cbo9780511803475.008

- Veenhoven, R. (2003). Hedonism and happiness. Journal of Happiness Studies, 4(4), 437–457. https://doi.org/10.1023/b:johs.0000005719.56211.fd

- Vilnai-Yavetz, I., & Gilboa, S. (n.d.). Relating hedonism and business context to customer. Services Marketing Quarterly, 37(3), 141–155. https://doi.org/10.1080/15332969.2016.1184539

- Waheed, H., Ahmed, Z., Saleem, Q., Din, S. M. U., & Ahmed, B. (2020). The mediating role of risk perception in the relationship between financial literacy and investment decision. International Journal of Innovation, Creativity & Change, 14(4), 112–131.

- Wangzhou, K., Khan, M., Hussain, S., Ishfaq, M., & Farooqi, R. (2021). Effect of regret aversion and information cascade on investment decisions in the real estate sector: The mediating role of risk perception and the moderating effect of financial literacy. Frontiers in Psychology, 12(October), 1–15. https://doi.org/10.3389/fpsyg.2021.736753

- Wubie, A. W., Dibabe, T. M., & Wondmagegn, G. A. (2015). The influence of demographic factors on saving and investment decision of high school teachers in Ethiopia: A case study on Dangila Woreda. Research Journal of Finance & Accounting, 6(9), 64–69.

- Yu, Y., & Jing, F. (2016). Development and application of the hedonic adaptation theory. Advances in Psychological Science, 24(10), 1663–1669.

- Zavadskas, E. K., Ginevičius, R., Kaklauskas, A., & Banaitis, A. (2005). Analysis and modeling of the Lithuanian real estate sector. Journal of Business Economics and Management, 6(3), 135–143. https://doi.org/10.3846/16111699.2005.9636102

- Zhang, Y., & Zheng, X. (2015). A study of the investment behavior based on behavioral finance. European Journal of Business and Economics, 10(1). https://doi.org/10.12955/ejbe.v10i1.557

- Zia-Ur-Rehman, M., Latif, K., Mohsin, M., Hussain, Z., Baig, S. A., & Imtiaz, I. (2021). How perceived information transparency and psychological attitude impact on the financial well-being: Mediating role of financial self-efficacy. Business Process Management Journal, 27(6), 1836–1853. https://doi.org/10.1108/bpmj-12-2020-0530