Abstract

The study aimed to analyze the perceptions of FinTech in the Middle East region, specifically its usage, and performance. To attain this objective, a strategy employed on surveys as the primary data acquisition method was implemented. The survey was conducted between November 2021 and February 2022, which allowed the researcher to gather comprehensive data from respondents during this period. In order to ensure the descriptive nature of the study, cross-sectional research was employed in its design. This design allowed the researcher to gather data at a single point in time, which was appropriate for the scope of this study. The researcher utilized a questionnaire during the inquiry to elicit information for data collection purposes. The questionnaire was designed to include semi-structured questions, which allowed the respondents to provide detailed information on their perceptions of FinTech. This study employed a survey-based technique to analyze the perceptions of FinTech in the Middle East region. Using a cross-sectional design and semi-structured questions allowed the researcher to achieve the descriptive nature of the research. Additionally, cross-tab analysis and SPSS provided an in-depth understanding of the data collected. The findings from the analysis suggest that FinTech enhances the performance of financial institutions and that digital banking is the best feature of FinTech across all customer groups.

1. Introduction

Policymakers and managers place a high premium on financial technology, or FinTech.” Due to recent technological advancements and greater use of financial software, competition has intensified while the industry’s overall performance has also improved. The business sector has witnessed substantial changes with the advent of the Internet, which has paved the way for new interaction and communication dynamics between market agents. Financial Technologies FinTech” uses technologies to enhance customer experiences and build a consistent relationship with them (Langan et al., Citation2019). They are also aggressively used to improve the performance of financial institutions. FinTech typically uses mobile phones and computer systems with internet-based interfaces to service clients and customers. The utility of digital applications influences a client’s choice of one financial institution over another. Numerous financial institutions have adapted their offerings to FinTech advances, citing increased competition.

Consequently, they can bolster their offerings and compete more effectively with other FinTech firms. Others must constantly improve their talents and work hard to stay caught up. Now, it is easy to search for new product suppliers and openly express our opinions about the experiences of a specific product or service, which affects current and potential customers for most organizations. The market rules change rapidly, and “digitalization” has changed everything. This shift is not confined to introducing new technology; using new technologies always spurs changes in consumer attitudes and behaviors (Ahmad & Murray, Citation2019) emphasized the significance of digitization on firm performance.

FinTech does not deviate much from market concepts and is an evolutionary response to economic and market changes. With a globalized economy, companies are forced to develop strategies to attract and retain customers, leading them to face new challenges and recruit new tools and approaches. Market competitiveness made marketing necessary for companies, whether they developed it broadly and structurally or as isolated activities. Marketing has become operational in planning models such as the four Ps; product, place, price, and promotion (Kotler, Citation2002). Likewise, new approaches have been developed, such as service marketing, cultural marketing, and green marketing, which have provided new tools and instruments to promote the organization’s performance, not only its economic performance. However, other dimensions, such as social and environmental performances, have also gained importance with the rise of sustainable development models (A. K. Khan, Citation2022).

According to (Straker, Citation2016), new technologies have revolutionized how companies interact and engage with customers. Attracting customers is not restricted to just launching digital campaigns; much more than that (Cuesta et al., Citation2015) states that digital services and channels help build and promote loyalty among financial institutions’ customers. FinTech is a double-edged sword that allows financial institutions to serve their customers through electronic channels and helps them attract additional customers. Also, customers’ changing habits play a role in favoring digitalized services. The millennial and X generations are more connected to their smartphones. They tend to visit financial institutions’ headquarters less, especially if they can replace this with virtual tools such as mobile phone platforms. There is mounting pressure on financial institutions to prioritize digitization as a pressing matter to stay caught up in a market that has witnessed the rise of fully-fledged technology companies and FinTech startups. Furthermore, the evolving behavioral trends of the clientele, exploring novel approaches to leverage financial services, coupled with the nascent competitive milieu these patrons have encountered (Cuesta et al., Citation2015).

The degree of technological advancement in the region, the regulatory environment, and cultural attitudes toward digital banking have all influenced how people perceive fintech in the Middle East (Abedin et al., Citation2022).In addition of another study by (Yildirim & Öztürkkal, Citation2022) states that the Middle East region has witnessed significant growth in the fintech sector in recent years, with the emergence of several startups and the adoption of digital banking solutions by traditional financial institutions. Growing demand for digital financial services, particularly among younger generations more likely to adopt new technologies, has driven this growth.

The regulatory environment in the Middle East has also played a crucial role in shaping fintech perceptions in the region. Governments and regulatory bodies have been proactive in promoting innovation and encouraging the growth of the fintech sector through regulatory sandboxes and other initiatives (Zarrouk et al., Citation2021). Cultural attitudes towards digital banking have also influenced fintech perceptions in the Middle East. While some countries in the region have been quick to embrace digital banking, others have needed to adopt new technologies due to cultural attitudes toward traditional banking practices (Oladapo et al., Citation2022).

Overall, fintech perceptions in the Middle East are generally positive, with many consumers and businesses embracing digital banking solutions and expressing confidence in the security and reliability of fintech platforms.

1.1. Need of the study

The spread of Internet services and the ubiquitous usage of new FinTech tools have impacted many traditional financial institutions and propelled them to focus on updating and improving their services. The factors that attract customers nowadays to financial institutions in this accelerated, more technological-dependent environment may differ from those used to attract customers to these financial institutions ten years before. Also, in the last ten years, there has been accelerated growth for FinTech companies, which resulted in substantial changes in traditional financial institutions and led to enormous alterations in providing financial services.

The business environment is changing rapidly in both FinTech and financial technology. Attracting and retaining new clients is becoming difficult as innovations and marketing techniques proliferate. The way financial institutions conduct business is changing as more reliance is placed on machines than humans as more technologies are available for final consumers (Chuang et al., Citation2016). The industry should adapt to the new trends in technologies and adequately conduct a marketing campaign in various ways for FinTech to improve the performance of their organizations. To achieve continuous success, the FinTech technology of financial institutions should adapt to clients’ needs by providing trustable mechanisms, security, and straightforward applications that satisfy the final consumers.

In the financial industry, there has been much discussion on the role of FinTech in the industry and whether new FinTech firms would assist and work with incumbent financial institutions or if they would represent a danger to them. The findings of this study may aid in determining the role of FinTech in the financial system. It may aid in improving and updating the relatively sluggish financial sector or create competition with favorable implications for customers. The government has been focusing on the FinTech sector in Saudi Arabia, which is embedded in its national vision for 2030. The financial institutions operating in the country heavily invest in technology (Almuhammadi, Citation2020). It becomes imperative that the perceptions of employees and customers of FinTech in these financial institutions be studied for effective decision-making and policy formulation. This study aims to provide relevant findings in this direction.

In this study, we aim to contribute uniquely to the existing research on fintech perceptions by focusing on the Middle East region. While there is an increasing body of research on fintech adoption and performance globally, only some studies have explicitly focused on the Middle East region, despite its growing importance in the fintech sector. Furthermore, it is essential to note that the Middle East region has a unique blend of economic structures and cultural backgrounds compared to other regions. The region has many high-net-worth individuals and a thriving entrepreneurial ecosystem. The various Islamic finance principles widely practiced in the region add to its uniqueness and allow fintech companies to develop Sharia-compliant products and services. These factors make the Middle East region a potentially lucrative market for fintech companies, and thus, studying fintech adoption and performance in this region can provide valuable insights for the industry as a whole.

1.2. Objective of the study

This study aims to analyze the perceptions of FinTech in the Middle East region and investigate its usage and performance. The primary objective is to identify the factors that influence the adoption of FinTech in the region and assess its impact on the performance of financial institutions.

2. Literature review

The use of FinTech to promote financial inclusion has a positive impact on firms’ sales growth in non-Asian regions. However, financial innovation negatively affects firms involved in financial inclusion in non-Asian developing countries. The study also examines the impact of FinTech on small and medium-sized firms and medium-sized vs. large-sized firms in certain Asian countries and non-Asian countries (Lee et al., Citation2020). Any business must use the potential and available solutions provided by new information technologies, improve customer relationships, and increase the quality of services offered (Thakor, Citation2020). Addressed many advantages for financial institutions in enhancing the technologies he focused on in his paper. He states that upcoming technology will provide cheaper and more secure information transmissions and achieve economies of scale in gathering and using extensive data. The current digital era enables organizations to reach various clients through many channels, such as websites, search engines, emails, and social media (Herhausen et al., Citation2020). The advantages of FinTech are many, as the organization can quickly contact a large group of customers at a lower cost than traditional marketing channels. The tools of FinTech used in the financial sector are many; here are the most important of them (Luo et al., Citation2021). Show how digital financial capability positively impacts business ownership, performance, and innovation in their household economic survey. They focus on micro-businesses concerning employment and economic development in the digital era (Barbu et al., Citation2021). Studied customer experience regarding FinTech using the Stimulus-Organism-Response (SOR) approach and found that perceived value, customer support, assurance, speed, and perceived firm innovativeness are positively related to customer experience in FinTech.

(Sahay et al., Citation2020) hold that FinTech is a concept of online promotion and advertising that applies through digital and online media. They also suggest a dynamic system involving constant innovation and change. The changing behavior of consumers should be addressed, and organizations should accept the influence of FinTech and frequently find new ways of attracting their targeted consumers (Almuhammadi, Citation2020). suggests that high-speed internet and widespread information technology are changing the world. The mobile payment system is another example of FinTech, which attracts customers because of its features such as security, ease of use, speediness, and universality. For financial institutions such as banking, the “emerging technological landscape in the financial world will be a formidable challenge, including its cost factor, and, at the same time, a huge opportunity.” (Kumar, Citation2017) The author suggests that the financial industry is experiencing a gradual integration of novel technological innovations, including but not limited to Big Data, Artificial Intelligence, Blockchain Technology, Cloud-based Computing, and the Internet of Things. The utilization of cloud computing is increasingly gaining popularity. The banking industry is gradually incorporating technological advancements, per the information. It is imperative for the banking sector and financial institutions to consistently advance FinTech to improve their performance and deter potential competition.

2.1. FinTech and the financial institutions

For financial institutions, constant improvement and development are substantial components that propel the company’s operations to thrive and flourish in the future, making FinTech an indispensable element in any financial institution. FinTech is a compound term that joins the first syllables of financial and technology; thus, it means the latest financial technology that offers innovative financial products and services (Chen et al., Citation2021). The study findings indicate that Chinese financial institutions exhibit a high level of perceived utility (PU) towards FinTech while simultaneously displaying low perceived difficulty of use (PD) for the technology. The argument posits that the perspective mentioned above results from the convergence of elevated levels of customer contentment and diminished levels of consumer anticipation (A. K. Khan & Faisal, Citation2021). FinTech can be defined as technology-enabled business model innovations and digital innovations in the financial sector. It serves as a singular illustration.

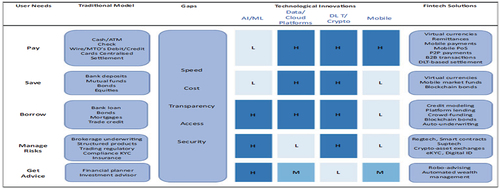

Implementing financial technology has significantly impacted financial institutions’ operational efficiency while enhancing interconnectivity among their clientele. As a result, contemporary consumers possess a more extraordinary array of alternatives compared to previous eras regarding managing their personal finances and the associated expenses. Consequently, this enhances the efficacy of most financial institutions and reinforces the bond between the corporation and its customers. The International Monetary Fund (IMF) examined financial technology’s (FinTech) effects on the financial services industry in 2019. The visual representation depicted in Figure illustrates a comparative and contrasting analysis of the user’s expectations regarding various financial services, including payment, savings, borrowing, risk mitigation, and assistance. The user requirements are delineated concerning both existing and novel FinTech alternatives. In 2019, the International Monetary Fund (IMF) conducted a study revealing that numerous countries are beginning to experience advantages from implementing FinTech solutions. Potential benefits include enhanced economic growth and increased financial accessibility for a larger population.

Figure 1. Customers’ demands for financial services are categorized into segments for conventional technology and emerging ones.

FinTech enterprises can attain their objectives using inventive commercial frameworks and technological advancements. These corporations offer advanced financial services to individuals and governmental entities. The advancements facilitated by FinTech have resulted in individuals having an increased level of autonomy over their financial situations. As per the International Monetary Fund (IMF), this facilitates novel modes of economic and financial engagement, thereby decreasing non-monetary outlays, deferrals in financial transaction execution, and transactional expenses. The utilization of digital technology by FinTech enables it to extend its reach to segments of the populace that lack access to traditional financial services. Consequently, this ultimately results in an augmentation of financial inclusivity (Sahay et al., Citation2020). Certain FinTech services can potentially jeopardize the security of a user’s assets and, in some cases, may be utilized to conceal funds or facilitate illicit transactions. The regulation of this industry poses a significant challenge, as it encompasses not only the mitigation of potential risks but also the facilitation of competition, innovation, and economic equity. Individuals new to the FinTech sector may discover employment opportunities in various areas such as foreign exchange, remittances, mobile wallets, crowdfunding, payments, online marketplace lending, mobile applications, financing, investments, blockchain, digital currencies, artificial intelligence, and robotics. These opportunities may be available in businesses that specialize in finance, insurance, and wealth management. (Digital Finance Institute, 2016).

2.2. The role of FinTech in improving the performance of financial institutions

The evolution of FinTech can be categorized into three periods (Arner et al., Citation2015). The first era can be categorized as the period (1886–1967) when technologies such as railroads, steamships, telegraphs, and railroads were used to conduct financial transactions and send information across borders. The first electronic system was developed, relying on Morse code and the telegraph, which provided a breakthrough by introducing an ancient credit card form. Due to this, the ‘Master Card” firm completely transformed the credit card market in 1966.

Earlier in 1964, Xerox introduced the first commercial fax machine, and in 1967, Barclays Bank in the UK introduced the first ATM.

The second era can be categorized as the period from 1967 to 2008, also called ‘the development of traditional digital financial services (Arner et al., Citation2015). The introduction of the Automatic Teller Machine (ATM) and Society of Worldwide Interbank Financial Telecommunication (SWIFT) banking was a significant development in this era. With the introduction of online banking, the FinTech landscape changed completely during this era.

The third era of the FinTech evolution can be categorized as 2008 onward. In this era, FinTech reached the masses. New players entered the market alongside conventional banks. Consumer preferences changed dramatically in this era when smartphones were invented, leading to the introduction of mobile financial services. Mobile financial services give retail customers unlimited access to financial information, decreasing loyalty to specific banks or financial service providers (Alt et al., Citation2018). Following the creation of numerous cryptocurrencies, Bitcoin significantly impacted this era in 2009 (Gomber et al., Citation2018). believe that financial technologies will revolutionize financial services operations.

The current regulation and further improvement of FinTech, such as artificial intelligence, will provide them with more opportunities to retain their clients, improve their services, and increase their revenues and performance in the following years. All these technological changes in different eras enabled the financial services industry to focus more on providing more value to their customers, which positively reflected their performance and growth.

Despite the significant advancements in FinTech in recent years, there still needs to be a research gap in understanding the impact of these changes on the traditional banking industry. While many studies have explored the emergence and adoption of FinTech, few have examined the implications for traditional banks and how they can adapt to these changes. Furthermore, there needs to be more research on the impact of FinTech on financial inclusion, especially in developing countries where access to banking services is still a significant challenge. Therefore, there is a need for further research to understand the potential opportunities and challenges for traditional banks in the evolving FinTech landscape, as well as the impact on financial inclusion and access to banking services.

3. Research methodologies

The study did not explicitly state the type of sampling method used. It is important to note that the sampling method used in a study can affect the representativeness and generalizability of the results.

However, based on the information provided, the authors likely used a convenience sampling method. It is because the study collected data from respondents from the Middle East region from November 2021-February 2022. Convenience sampling is a non-probability sampling technique that involves selecting participants based on their accessibility and willingness to participate. As the study collected data through an online questionnaire, it is possible that the authors reached out to individuals who were easily accessible through online platforms and were interested in Fintech. It is important to note that convenience sampling can lead to biases in the sample, and the results may only be generalizable to some of the population.

The primary objective of the research is to analyze the perception of customers and employees toward FinTech for policy interventions. Additionally, the research aims to investigate the influence of FinTech to motivate a customer to choose a specific financial institution. Additionally, it aims to identify FinTech’s role in improving financial institutions’ performance. Similar studies were conducted by (Vives, Citation2017; Yasmin et al., Citation2015) (Khan, AL ABOUD, & Faisal, A. K. A. Khan et al., Citation2018), (Breidbach et al., Citation2020), and (Murinde et al., Citation2022), However, very few studies (Al-Dmour et al., Citation2021) are focused on the Middle East region, and no study was found focusing on the impact of demographics on FinTech perceptions (See Figure ).

The two broad research questions answered in the study are,

Q1: The role of FinTech in attracting consumers to a financial institution.

Q2: The role of FinTech in improving a financial institution’s performance.

The study elicited responses to its questions from various individuals with different backgrounds and managerial levels. The participants included employees from different financial institutions and banks. The reason is to determine how the administrations of these financial institutions used FinTech to attract more customers and inquire about the role that FinTech plays in developing the services provided by these institutions.

In light of the research objective, a related questionnaire-based survey was used to collect data from respondents, primarily in the Middle East. The survey instrument was validated in consultation with two domain experts, and a questionnaire was finalized with nine questions, which included four questions on the demographics of the respondents. Categorical factors were used in order to assess people’s reactions. All nine factors in the research were coded using SPSS 21.0 as categorical variables. From November 2021 through February 2022, 600 participants were surveyed through an online survey (per COVID-19 methodology), yielding 305 usable replies (or 51%). The final sample comprised 305 employees, 255 of whom worked in financial and 50 non-financial institutions. The reliability statistics of the sample were calculated as 0.56, which is considered acceptable (Classics Cronbach, Citation1951) (Chen et al., Citation2021). did a similar study on customers’ and employees’ perceptions of FinTech Products (FTP), while (Al-Dmour et al., Citation2021) did a similar study on a UAE sample. Consequently, the Chi-square test was applied to study the association between the four demographic variables and the five perception variables on FinTech.

4. Selection of middle east regarding fintech perceptions in the region

Several factors support the study’s choice of the Middle East as its focal point. Firstly, the Middle East region has experienced significant growth in the fintech sector in recent years, with the emergence of several startups and the adoption of digital banking solutions by traditional financial institutions. Growing demand for digital financial services, particularly among younger generations more likely to adopt new technologies, has driven this growth.

Secondly, the Middle East region is home to diverse cultures and regulatory environments, making it an interesting case study for analyzing fintech perceptions and adoption across different contexts. It allows for a more nuanced understanding of the factors that influence fintech adoption and the impact of fintech on financial institutions in the region.

However, there are also some issues regarding fintech perceptions in the Middle East region. One issue is the lack of regulatory frameworks and the need for more streamlined regulations to ensure the safe and secure adoption of new technologies. There are also cultural barriers to adopting new technologies, with some preferring traditional banking practices over digital banking solutions.

5. Data analysis

The data collected through the survey has been analyzed using SPSS version 21.0, while analysis of descriptive statistics and cross-tabulations has been conducted for data interpretation due to the nature of the questions.

Based on the descriptive data in Table , Figure , females comprised 33% of the survey’s participants. When compared, we find that 67% of respondents are male, 40% are under the age of 35, 60% are over the age of 35 (Figure ), 54% have a bachelor’s degree or higher, 19% have a master’s degree or higher, and 9% have an intermediate or lower level of education (See Figure ). About 48% of respondents have more than 15 years of experience, while 27% have 0–5 years of experience refer to figure . About 63% of respondents agree that “digital marketing” and 17% agree that “social media” come to mind when they think/hear about FinTech (See Figure ).

Most of the respondents (99%) agree that FinTech is improving the performance of financial institutions refer to Figure . About 56% of respondents agree that “ease of use” and “security” are the two crucial features of a financial institution’s technology. About 70% of respondents agree that digital marketing helps them choose a financial institution (See Figure ). About 51% of respondents (employees) feel that social media is the most preferred digital marketing campaign.

5.1. Cross tab analysis

In the cross-tab analysis (Table ) from the respondent’s perspective, about 22% of female and 48% of male respondents agree that the digital marketing campaigns have affected their decision to choose a Financial Institution. About 28% of respondents who are less than 35 and 43% who are more than 35 also hold this perspective. Additionally, 38% of respondents who are Bachelor qualified and 17% of whom are Master qualified, and 32% of respondents with more than 15 years of work experience agree that the digital marketing campaign has affected their decision to choose a financial institution (See Table ).

The male and female employees’ most preferred digital marketing campaign was social media. About 21% of respondents under 35 and 30% older than 35 agree that social media is the most preferred digital marketing campaign. About 26% of respondents whom are Bachelor qualified and 9% who are Master qualified employees agree on social media. Social media was also observed as the preferred digital marketing campaign for all experience groups refer to Table .

When they encounter the term/concept of “FinTech,” digital banking is the first perspective/thought that comes to mind for 23% of female and 39% of male respondents. The same perspective holds for 22% of respondents under 35 years old and 40% of those over 35 years of age. The second such thought about “FinTech” is ‘automated trading.” About 34% of respondents who hold a bachelor’s degree and 13% who hold a master’s degree also agree that digital banking is what they think about “FinTech.” The same perspective holds for respondents in all experience groups.

About 98% of respondents believe that “FinTech” helps improve financial institutions’ performance. About 98% of respondents of all age groups, 54% of Bachelor’s degree holders, and 19% of Master’s degree holders agree with the same thought. About 36% of respondents who are more than 15 years of age, 26% of respondents with between 5–15 years of experience, and 27% of respondents who possess up to 5 years of work experience also agree that “FinTech” helps in improving the performance of financial institutions refer to Figure .

‘Easy to use” is the best feature of the “FinTech” used by respective financial institutions, as indicated by 14% of females and 35% of males. About 23% of respondents under 35 years of age and 31% over 35 agree on ‘ease of use as the best feature of “FinTech.” Also, ‘easy to use is the preferred feature for people from all work experience groups. About 22% of respondents with a bachelor’s degree found ‘easy to use, and 12% of respondents found “security” as the two best features of “FinTech.” Additionally, 10% of respondents with a master’s degree found it ‘easy to use, followed by 6% of respondents for “security” as the two best features of “FinTech.”

The Chi-square test results indicated a positive association between the gender of the respondents and their first thoughts on FinTech (Pearson’s Chi-square value = 0.09) and in identifying the attracting feature of FinTech (Pearson’s Chi-square value = 0.05). Similarly, a positive association was found between the years of experience and the first thought on FinTech (Pearson’s Chi-square value = 0.07) and in identifying the attracting feature of FinTech (Pearson’s Chi-square value = 0.09).

6. Discussion

Around 33.33% of the sample consists of individuals who identify as female. In contrast, it was found that 67% of the participants were male, with 40% of them being under the age of 35 and 60% being over the age of 35 (See Table and Figure ). Furthermore, the findings revealed that 54% of participants possessed a bachelor’s degree, 19% held a master’s degree, and 9% had intermediate or lower qualifications. Approximately 48% of the participants possess over 15 years of professional experience, while roughly 27% of the respondents have acquired between 0–5 years of experience. The sample size is deemed reliable for demographic analysis based on meeting the necessary criteria. The results of the Chi-square analysis revealed a significant correlation between gender and years of work experience and their impact on the participants’ initial perceptions of FinTech and their ability to identify its appealing characteristics. The results indicate a positive correlation between respondents’ initial perceptions of FinTech and their recognition of its attractive features. Similarly, the scenario mentioned above was observed during the survey, where participants were requested to select the most attractive aspect of FinTech. It is imperative for FinTech companies offering goods and services to consider the demographics, gender, and profession of their customers as mentioned in Tables and Figure .

Approximately 63% of participants associate the term “digital banking” with FinTech, while 17% of respondents associate the term “social media” with the same. The participants were unable to establish a correlation between the alternative options presented in the query, such as Bitcoin, automated trading, or data analysis. The results of this investigation can assist policymakers in directing their efforts toward these specific regions. The overwhelming consensus among respondents, comprising 99% of the sample, is that FinTech is enhancing the operational efficiency of financial institutions. Those mentioned above can be attributed to the fundamental characteristic of Financial Technology (FinTech), which involves providing services digitally. As a result of technological developments and the digitalization of business operations in the financial services sector, physical and virtual worlds are fast converging, as stated by. The integration of digital technology in the financial industry has resulted in the emergence of novel digitized business models and strategies alongside innovative digital products and services. Over the last decade, there has been a significant surge in the adoption of digital advisory and trading systems, artificial intelligence and machine learning, peer-to-peer lending, crowdfunding, mobile payment systems, and various forms of digital currency, including Bitcoin and other crypto-assets. Utilizing digital channels for customer engagement is prevalent in current markets and presents a more economical option. On the contrary, they constitute a significant and steadily expanding segment of the retail clientele industry globally. This phenomenon has a worldwide reach. The term “FinTech” denotes the services offered by various high-tech start-ups. These enterprises employ state-of-the-art methodologies in their business and digital platform models.

About 56% of respondents agree that “easy to use, and 25% of respondents agree that “Security” are the two important features of a financial institution’s technology. “Speed” of transactions could not be identified as the most attractive feature; financial institutions can include this in their marketing strategies. About 70% of respondents agree that digital marketing helps choose a financial institution. Thus, financial institutions should use digital marketing for competitive advantage. When a company develops marketing strategies, two important points should be considered: customer acquisition and retention. While customer acquisition, which can achieve through FinTech techniques, is intended to increase the customer base over time, customer retention seeks to keep the current portfolio of customers in force since it is easier to sell to a customer than to a non-customer individual.

About 51% of respondents (also employees) feel that social media is the most preferred digital marketing campaign, but the remaining 49% of respondents prefer emails, websites, and other channels. Corporations could leverage this finding. These findings are consistent with (Sohail & Shanmugham, Citation2003), who found that banks have responded to the fierce competition by adopting a strategy that focuses on building customer satisfaction through FinTech (Moşteanu et al., Citation2020). Argues that COVID-19 implications have changed many people’s views of financial institutions on behalf of more digitalized institutions. As the lockdown restrictions have been imposed worldwide, many people began to rethink the importance of digitalized services that their financial institutions offer and even shift to the more digitalized ones, leaving the conventional ones. The current study found that the financial institutions’ marketing campaigns affect costumer’s selection of the financial institution, which means that the bank with the best marketing efforts will have a more remarkable customer base than the banks that either do not promote at all or do so on a small scale (Yasmin et al., Citation2015) concluded that FinTech is vital for every financial organization. Businesses need to establish social media accounts to communicate with their clients, share commercials and promotional films with them, and more easily field any questions or comments they may have. Because some consumers have trouble with new technologies, marketing and FinTech campaigns must always emphasize using user-friendly applications and posting films to demonstrate how to use all of its digital channels (A. K. Khan & Faisal, Citation2021).

Millions visit social media platforms, and even billions of people visit them daily. It is usual for social media sites to have a more significant impact on people than websites do (A. K. A. Khan et al., Citation2018). states that more than 2 billion people use social media. This large quantity draws customers to financial institutions. Today, more and more people get their information, connect with others, and pass the time by using social networking sites. Users may engage with their banks and credit unions on social media to learn about new features and services and receive answers to frequently asked questions. The primary aim of social networks is not to generate revenue through the sale of goods or services but to establish a user community that is emotionally invested in and aligned with the brand. It opposes the objective of generating revenue through the vending of a commodity or amenity. One of the aims of financial institutions’ social media accounts is to convert unknown individuals into acquaintances, then acquaintances into clients, and ultimately clients into brand advocates. This strategy could promote a financial establishment and its offerings on social media channels to enhance brand recognition, augment web traffic, and generate fresh clientele for the financial institution or enterprise, ultimately increasing revenue. Contemporary financial institutions provide various services by utilizing diverse forms of digital technology. The widespread internet usage by a significant proportion of the population presents a favorable opportunity for digital enterprises to acquire fresh clientele. Using social media platforms to sell products and services, offer customer support, and conduct sales is increasingly becoming a customary practice among companies (A. K. A. Khan et al., Citation2018). Through this, companies are getting all the required information first-hand, which they might require for analysis.

Also, companies create and promote brands and engage customers to an extent. Customers buy products and services worldwide through the Internet, expanding the business market. As a result, businesses can now compete globally. The current research found that employees working in financial institutions prefer to launch marketing campaigns through social media more than through websites and emails. The preceding year witnessed an increase of 18% in the volume of social media posts that required a response from the affiliated companies, according to (Sprout social, Citation2016). Despite the persistent rise in consumer expectations across various industries, there has been a notable decline in brand response rates. Only 11% of social media messages receive a response.

Historically, financial institutions have refrained from engaging in social media due to apprehensions regarding privacy and adherence to regulatory standards. However, with recent technological developments, this stance has evolved. The publication of recommendations by the Federal Financial Institutions Examination Council (FFIEC) brought about a significant transformation in financial institutions’ approach toward expanding their technical and social outreach while mitigating potential risks. The abovementioned recommendations are intended to assist financial institutions in enhancing their market reach in both domains. Financial institutions must allocate time and financial resources and exert effort to sustain a social media presence and execute marketing initiatives effectively (Sprout social, Citation2016). The results also found that customers and employees choose social media as the best marketing tool, followed by websites and emails. This result is consistent with those (Roque & Raposo, Citation2016), who found that the most crucial marketing tools are Facebook, Twitter, YouTube, and Google Plus. Social platforms are closer to individuals than company websites and emails. Websites are only served and visited when a person wants a specific service from the company. Also, most websites do not offer an opportunity to interact and inquire about products, whereas social media sites do.

The current study found that most financial institution employees see their organizations focusing more on digital applications and mobile solutions. According to (Dapp et al., Citation2014), financial institutions have already moved to position themselves in this financial sector transformation promoted by FinTech. The FinTech market is dynamic and competitive. The consumer has different options, depending on their needs and preferences. Although FinTech companies are usually accessible, the amount and quality of information available on the Internet may vary. One of the most attractive aspects of FinTech services is the possibility of accessing them through mobile devices like smartphones or tablets.

It should be noted that all financial services companies have a web page accessible from everywhere. Because of digital applications, FinTech companies have become very important due to the opportunities they bring. In recent years, FinTech companies have developed tools and offered new opportunities to use new technologies that improve processes in the financial sector (Varga, Citation2017). The current research questioned whether FinTech helped improve financial institutions’ performance, and 99% of respondents said that the advent of FinTech helped financial institutions improve their performance (Kiilu, Citation2018). FinTech has helped these enterprises cut intermediation costs and boost financial access (Vives, Citation2017). attributes this efficiency to FinTech’s role in addressing information asymmetries and significant difficulty in banking. FinTech businesses handle customers’ money quicker, more quickly, and openly. Its strength is offering more rapid solutions with fewer resources and less money. Financial institutions tried to outrun FinTech because they feared being rendered obsolete. So, improvement in the performance of the financial institutions came in two different ways: from taking advantage of the digitalized services that FinTech and the fear that they go out of the playground because of their obsolete solutions.

Overall, the study’s empirical findings provide valuable insights into fintech perceptions in the Middle East region and highlight the need for continued research and investment in the fintech sector in the region. By addressing regulatory and cultural barriers to adoption and focusing on digital banking solutions, financial institutions in the Middle East region can harness the potential of fintech to enhance their performance and better serve their customers.

7. Conclusions

The purpose of this research is to explore how FinTech attracts clients to particular financial institutions, the role that FinTech plays in improving the overall performance of financial institutions, and an evaluation of the perceptions linked to these subjects. The current research found that digital applications are the main reason customers prefer one financial institution over another. The developments in the FinTech sector have led many financial institutions to update their services and feel threatened. As a result, these financial institutions were able to advance their offerings and triumph over rival FinTechs. When fierce rivals challenge people, they are motivated to improve and work harder for fear of being left behind.

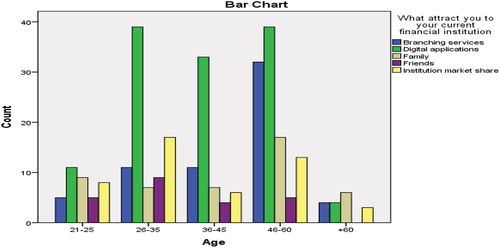

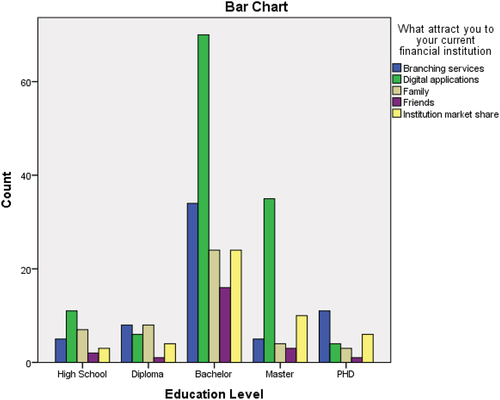

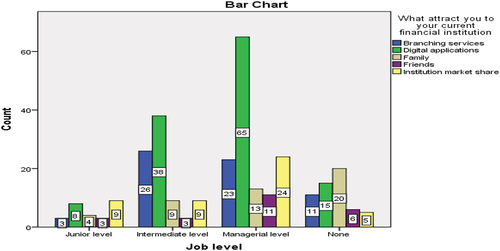

Respondents with bachelor’s or master’s degrees choose financial institutions based on digital applications, branching services, and the institutions’ market share. In contrast, those with Ph.D. degrees prefer branching services, followed by institution market share. The results show that digital apps, branching services, and institutions’ market share are the three most important variables for respondents with a bachelor’s degree or above when choosing a financial institution. Preferring financial institutions, digital applications, and branching services have been vital factors across various job levels. Digital applications, branching services, and institution market share have also been critical factors across various age groups in preferring financial institutions.

7.1. Managerial implications

Knowing the drivers that motivate customers to select a specific banking institution helps the management develop solutions that fulfil the customer’s needs. Also, having a deep knowledge of FinTech’s impact on customers helps managers stimulate growth at their institutions by accelerating transactions and procedures, improving the customer’s experience, and increasing profitability. FinTech can help reduce costs and increase productivity. It also helps managers identify and realize the challenges FinTech poses to established, traditional financial institutions, coupled with the opportunities regarding the growth of the financial services industry.

Some of the specific findings from the study can help corporate decision-makers to improve the effectiveness of FinTech. These decision-makers should focus more on increasing the awareness of customers and employees on data analysis tools used by the respective financial institution, automated trading platforms, and cryptocurrency platforms. “Speed” of transactions could not be identified as the most attractive feature; financial institutions can include this in their marketing strategies. The findings from the association among the study variables suggest that the gender and work experience of employees/customers should be considered while formulating FinTech policies.

7.2. New findings

The study provides several new findings about Fintech perceptions in the Middle East region.

Firstly, the study found that fintech enhances the performance of financial institutions in the Middle East region. It suggests that fintech is well-liked by clients and staff and may enhance the overall effectiveness of financial institutions in the area.

Secondly, the study found that digital banking is the most popular feature of fintech across all customer groups. It indicates a growing demand for digital banking solutions in the Middle East region, consistent with global trends in the fintech sector.

Thirdly, the study found that younger customers are more likely to use fintech services than older customers.

7.3. Limitations and scope for future research

The study has a few limitations. There were financial constraints and mobility constraints due to the COVID-19 pandemic. The sample used is non-representative and based on convenience. Rather than conducting interviews with prominent leaders of the financial and banking sectors, a purely quantitative study was done as the researcher intended. Furthermore, it is necessary to increase the sample size to extrapolate the findings to other countries. The statement above suggests that the investigation outcomes have potential applicability across a wide range of settings. However, it is essential to note that the deductions drawn from the study are specific to the geographical location in which the research was carried out. The choice to use cross-tab analysis and chi-square tests in this study was likely based on the nature of the research question and the data collection type. These statistical techniques were appropriate for analyzing categorical data and determining relationships between categorical variables. Other statistical tests may not have applied to the research question or the type of data collection. The study did not explicitly state the type of sampling method used. It is important to note that the sampling method used in a study can affect the representativeness and generalizability of the results.

However, based on the information provided, the authors likely used a convenience sampling method. The study collected data from respondents from the Middle East region from November 2021-February 2022. Convenience sampling is a non-probability sampling technique that involves selecting participants based on their accessibility and willingness to participate.

As the study collected data through an online questionnaire, it is possible that the authors reached out to individuals who were easily accessible through online platforms and were interested in fintech. It is important to note that convenience sampling can lead to biases in the sample, and the results may only be generalizable to some of the population.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Syed Akmal

Dr. Syed Akmal is a certified professional in supply chain management SCM-Pro and Quality Matters. He has spent more than a decade with leading MNCs in the teaching and corporate world. Since 2014, he has been working as an Assistant Professor at Saudi Electronic University, Kingdom of Saudi Arabia, a premier blended learning university in the Middle East. He has written several papers on subjects ranging from e-commerce to digital marketing to technology to CRM and published in international journals indexed with Web of Science, SCOPUS, & ABDC.

He launched his web portal, based on education & technology, and has professionally survived working at the intersection of technology and marketing.

He has a lifetime membership and association with ISTE (Indian Society for Technical Education).

References

- Abedin, M. J., Rahman, S. M., & Ahmed, R. (2022). Fintech in Islamic banking in bangladesh. Digital Transformation in Islamic Finance: A Critical Analytical View.

- Ahmad, M. U., & Murray, J. (2019). Understanding the connect between digitalisation, sustainability and performance of an organisation. International Journal of Business Excellence, 17(1), 83–26. https://doi.org/10.1504/IJBEX.2019.096909

- Al-Dmour, A., Al-Dmour, R. H., Al-Dmour, H. H., & Ahmadamin, E. B. (2021). The effect of big data analytic capabilities upon bank performance via FinTech innovation: UAE evidence. International Journal of Information Systems in the Service Sector (IJISSS), 13(4), 62–87. https://doi.org/10.4018/IJISSS.2021100104

- Almuhammadi, A. (2020). An overview of mobile payments, fintech, and digital wallet in Saudi Arabia. Paper presented at the 2020 7th International Conference on Computing for Sustainable Global Development (INDIACom), India.

- Alt, R., Beck, R., & Smits, M. T. (2018). FinTech and the transformation of the financial industry (Vol. 28). Springer.

- Arner, D. W., Barberis, J., & Buckley, R. P. (2015). The evolution of Fintech: A new post-crisis paradigm. Geochimica Journal International, 47, 1271. https://doi.org/10.2139/ssrn.2676553

- Barbu, C. M., Florea, D. L., Dabija, D. -C., & Barbu, M. C. R. (2021). Customer experience in fintech. Journal of Theoretical & Applied Electronic Commerce Research, 16(5), 1415–1433. https://doi.org/10.3390/jtaer16050080

- Breidbach, C. F., Keating, B. W., & Lim, C. (2020). Fintech: Research directions to explore the digital transformation of financial service systems. Journal of Service Theory & Practice, 30(1), 79–102. https://doi.org/10.1108/JSTP-08-2018-0185

- Chen, X., You, X., & Chang, V. (2021). FinTech and commercial banks’ performance in China: A leap forward or survival of the fittest? Technological Forecasting & Social Change, 166, 120645. https://doi.org/10.1016/j.techfore.2021.120645

- Chuang, L. -M., Liu, C. -C., Kao, H. -K.J.I.J.O.M., & Sciences, A. (2016). The adoption of fintech service: TAM perspective. 3(7), 1–15.

- Classics Cronbach, L. (1951). Coefficient alpha and the internal structure of tests. Psychometrika, 16(3), 297–334. https://doi.org/10.1007/BF02310555

- Cuesta, C., Ruesta, M., Tuesta, D., & Urbiola, P. (2015). The digital transformation of the banking industry. BBVA Research, 1, 1–10.

- Dapp, T., Slomka, L., AG, D. B., & Hoffmann, R. (2014). Fintech–The digital (r) evolution in the financial sector. Deutsche Bank Research, 11, 1–39.

- Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), 220–265. https://doi.org/10.1080/07421222.2018.1440766

- Herhausen, D., Miočević, D., Morgan, R. E., & Kleijnen, M. H. P. (2020). The FinTech capabilities gap. Industrial Marketing Management, 90(March), 276–290. https://doi.org/10.1016/j.indmarman.2020.07.022

- Khan, A. K. (2022). A changing role of artificial intelligence in the function of an accountant since ancient times in the perspective of international accounting standard. Journal of Positive School Psychology, 6(5), 2557–2565.

- Khan, A. K. A., ABOUD, J., & Faisal, S. M. (2018). An empirical study of technological innovations in the field of accounting-boon or bane. Business & Management Studies, 4(1), 51–58. https://doi.org/10.11114/bms.v4i1.3057

- Khan, A. K., & Faisal, S. M. (2021). The impact on the employees through the use of AI tools in accountancy. Materials Today: Proceedings, India. https://doi.org/10.1016/j.matpr.2021.07.044

- Kiilu, N. (2018). Effect of Fintech Firms on Financial Performance of the Banking Sector in Kenya. University of Nairobi.

- Kotler, P. (2002). Marketing places: Simon and Schuster. 9781439105160.

- Kumar, A. (2017). Changing landscape of banking: a futuristic perspective. Vinimaya, 38(4), 5–10.

- Langan, R., Cowley, S., & Nguyen, C. (2019). The state of digital marketing in academia: An examination of marketing curriculum’s response to digital disruption. Journal of Marketing Education, 41(1), 32–46. https://doi.org/10.1177/0273475318823849

- Lee, C. -C., Wang, C. -W., & Ho, S. -J. (2020). Financial inclusion, financial innovation, and firms’ sales growth. International Review of Economics & Finance, 66, 189–205. https://doi.org/10.1016/j.iref.2019.11.021

- Luo, Y., Peng, Y., & Zeng, L. (2021). Digital financial capability and entrepreneurial performance. International Review of Economics & Finance, 76, 55–74. https://doi.org/10.1016/j.iref.2021.05.010

- Moşteanu, D., Roxana, N., Faccia, D., Cavaliere, L. P. L., & Bhatia, S. (2020). Digital technologies’ implementation within financial and banking system during social distancing restrictions–back to the future. International Journal of Advanced Research in Engineering and Technology, 11(6), 307–315.

- Murinde, V., Rizopoulos, E., & Zachariadis, M. (2022). The impact of the FinTech revolution on the future of banking: Opportunities and risks. International Review of Financial Analysis, 81, 102103. https://doi.org/10.1016/j.irfa.2022.102103

- Oladapo, I. A., Hamoudah, M. M., Alam, M. M., Olaopa, O. R., & Muda, R. (2022). Customers’ perceptions of FinTech adaptability in the Islamic banking sector: Comparative study on Malaysia and Saudi Arabia. Journal of Modelling in Management, 17(4), 1241–1261. https://doi.org/10.1108/JM2-10-2020-0256

- Roque, V., & Raposo, R. (2016). Social media as a communication and marketing tool in tourism: An analysis of online activities from international key player DMO. Anatolia, 27(1), 58–70. https://doi.org/10.1080/13032917.2015.1083209

- Sahay, M. R., von Allmen, M. U. E., Lahreche, M. A., Khera, P., Ogawa, M. S., Bazarbash, M., & Beaton, M. K. (2020). The promise of fintech: Financial inclusion in the post COVID-19 era: International Monetary Fund.

- Sohail, M. S., & Shanmugham, B. (2003). E-banking and customer preferences in Malaysia: An empirical investigation. Information Sciences, 150(3–4), 207–217. https://doi.org/10.1016/S0020-0255(02)00378-X

- Sprout social. (2016). Shunning Your Customers on Social?. The Sprout Social Index (VI ed). Sprout Social.

- Straker, K., & Wrigley, C. (2016). Emotionally engaging customers in the digital age: The case study of “Burberry love”. Journal of Fashion Marketing & Management, 20(3), 276–299.

- Thakor, A. V. (2020). Fintech and banking: What do we know? Journal of Financial Intermediation, 41, 100833. https://doi.org/10.1016/j.jfi.2019.100833

- Varga, D. (2017). Fintech, the new era of financial services. Vezetéstudomány-Budapest Management Review, 48(11), 22–32. https://doi.org/10.14267/VEZTUD.2017.11.03

- Vives, X. (2017). The impact of FinTech on banking. European Economy, 3(2), 97–105.

- Yasmin, A., Tasneem, S., & Fatema, K. (2015). Effectiveness of digital marketing in the challenging age: An empirical study. International Journal of Management Science and Business Administration, 1(5), 69–80.

- Yildirim, C., & Öztürkkal, B. (2022). Regional expansion of emerging market banks: Evidence from the Middle East. Journal of East-West Business, 28(1), 30–60. https://doi.org/10.1080/10669868.2021.1982103

- Zarrouk, H., El Ghak, T., & Bakhouche, A. (2021). Exploring economic and technological determinants of FinTech startups’ success and growth in the United Arab Emirates. Journal of Open Innovation: Technology, Market,complexity, 7(1), 50. https://www.worldbank.org/en/publication/globalfindex

Annexure

To determine the Characteristics of Participants, frequencies and percentages were calculated as follows:

Table A1. The distribution of the overall study sample according to their demographic characteristics

Table (1) showed the participants respondents according to their demographic characteristics, as follows:

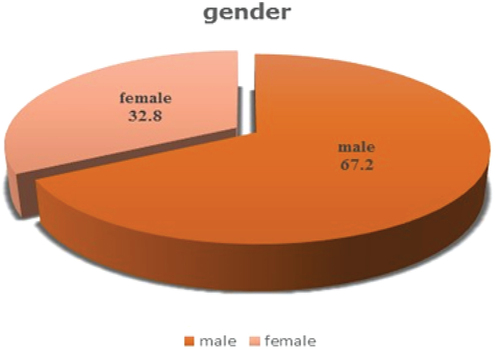

Regarding the gender component, the findings revealed that 67.2% of respondents were male, and 32.8% were female.

Figure A1. The distribution of the overall study sample according to gender.

Regarding the AGE variable, the majority of the study sample’s participants fell under the age range of (46-60 years), which had a percentage of (34.8%, followed by (26-35 years), which had a percentage of (27.2%), category age of (36-45 years), which had a percentage of (20.0%), category age of (21-25 years), which had a percentage of (12.5%), and category age of (60+), which had a percentage of (5.6%).

Figure A2. The distribution of the overall study sample according to age.

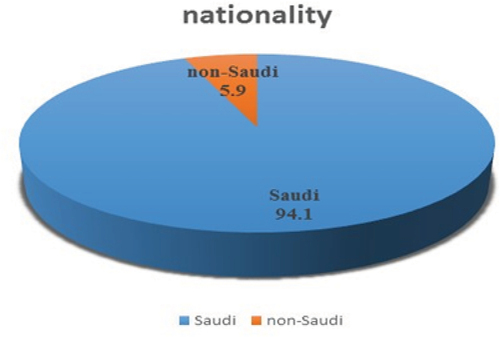

Regarding the nationality variable, most respondents (94,1 %) were Saudi nationals, while just 5.9 % were non-Saudi nationals.

Figure A3. The distribution of the overall study sample according to nationality.

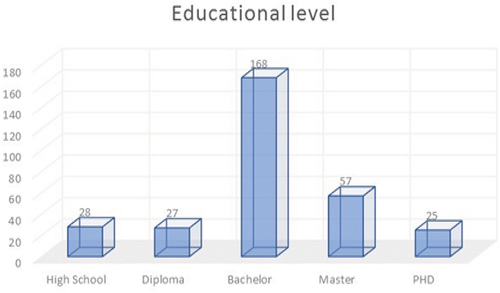

Regarding the Educational level variable, more than half of respondents had a bachelor’s degree (55.1%), a master’s degree (18.7%), a high school diploma (8.9%), and a doctorate (8.2%).

Figure A4. The distribution of the overall study sample according to education level.

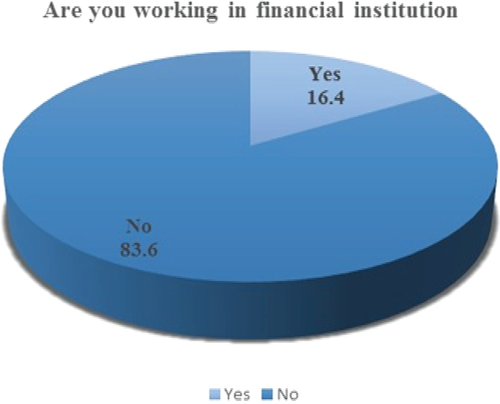

Regarding the working in financial institution variable, the great majority of respondents (83.6%) do not work in financial institutions, while just 16.4% do.

Figure A5. the distribution of the overall study sample according to work in the financial institution.

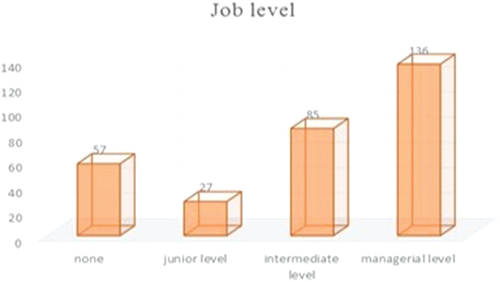

Regarding the variable Job level, about half of the respondents (44.6%) work at the management level, while (27.9) work at the intermediate level, (8.9%) work at the junior level, and (18.7%) do not have a job level.

Figure A6. The distribution of the overall study sample according to job level.

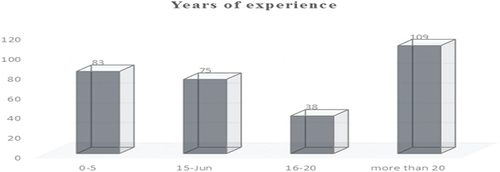

Regarding the variable of years of experience, 35.7% of answers were (+20) years, 27.2% were between (5-5) years, 24.6% were between (6-15) years, and 12.5% were between (16-20) years.

Figure A7. The distribution of the overall study sample according to years of experience.

Study questions: To determine the talents and resources necessary for the development of social businesses, as well as, the skills the company may invest in, the frequency and percentage of the respondents’ replies were computed as follows:

Table A2. How does Fintech attract consumers to a specific financial institution?

Table A3. Summary for Chi square test: At 5 % level of significance (0.05) Education Level

Figure A8. Characteristics of Participants, frequencies and percentages.

Table A4. Summary for Chi square test: At 5 % level of significance (0.05) Job level

Figure A9. Characteristics of Participants, frequencies and percentages.

Table A5. Summary for Chi square test: At 5 % level of significance (0.05) Age

Figure A10. Characteristics of Participants, frequencies and percentages.