Abstract

This paper examines the influence of financial accounting disclosures (FAD) on the investors’ reactions towards bad news (IRBN), and analytically assesses the moderation effect of the individual investor’s sentiments particularly” Subjective norms” on that relationship in project-based organizations (PBOs) listed in the UAE financial markets from a financial, and psychological perspective. Structural equation modelling (SEM) was used to analyse 310 completed questionnaires using Statistical Package for Social Sciences (SPSS) and Analysis of Moment Structures (AMOS) by multiple regression, path, and moderation analysis. Findings show that four dimensions of the studied FAD have a direct positive impact on the IRBN except for the external auditing and audit service (EAUS). Results also revealed that the subjective norms have a moderating impact on the relationship between FAD and the IRBN. Academically, this research contributes to both the reasoned action theory and the agency theory and satisfies an important gap in FAD literature. Practically, organizations, policymakers, and officials can use the findings of reliable and valid measurements of FAD, IRBN, and investors’ sentiment items to control and develop purposes, as IRBN can be controlled by healthy communication tools via different disclosure channels and healthy disclosure content. Investor Relations (IR) managers can realize if the desired disclosure is well comprehended in investors’ awareness, trust, intention, and perceptual reaction. It is one of the first empirical studies to establish a model illustrating the relationships between FAD, Subjective norms, and IRBN. The proposed model comprises processes and practices that could be used to enhance the decision-making process of investors and control their reactions that impact PBOs in the United Arab Emirates (UAE).

1. Introduction

In the last decades, the field of finance has radically transformed in its employment to correspond with the modern investors’ tactics and philosophies associated with different evolutions in general and economic progression in particular. Many scholars have already studied changes to the domain (Bolaman & Evrim Mandacı, Citation2014; Koseoglu, Citation2019; Phan & Zhou, Citation2014) using many altered methods, providing varied and sometimes conflicting results. These academic works consider an addition to economic development as such findings can enhance the investors’ involvement, investors’ thinking, and contentment, and therefore moderate the fluctuations of financial markets, and raise the quality of investment decisions by achieving rational behaviour, which contributes to improving the overall performance of the financial market. Nevertheless, investors’ behaviour necessities much interpretation, especially investors’ perceptual reactions towards bad financial news, termination of loss-making projects, fluctuation of share market price, and firm image (Verma & Chandra, Citation2018; Yang et al., Citation2020). Examining investors’ reactions could be remarkably advantageous, however it involves numerous defiances. Rendering to planned behaviour theory, behavioural intention views as a lineal preface to the next conduct. Hence, the Investors’ Reactions Towards Bad News IRBN could be counted as an acquainted dependent variable in several studies. Repeatedly, the perceptual reactions of the investors to bad financial news, such as termination of loss-making projects, fluctuations in market share price, and company image, are disclosed in financial reports, websites, or informal channels. Amongst these elements are governance and disclosure awareness, information quality, trust in firms’ disclosure channels, perceived benefits from the disclosure index, investment intentions, investors’ judgment, perceived ease-of-use, perceptions of privacy and risk, system security, and disclosure policy (Clatworthy & Jones, Citation2003; Frankel & Li, Citation2004).

Investors Sentiments IS are defined as investors’ feelings towards the upcoming cash flows and related risks of their investments without having appropriate evidence (Makau & Ambrose, Citation2018). Investors are academically and professionally weak and, in many cases, governed by emotional biases and societal or institutional influences that lead to irrational behaviour, most studies in behavioural finance have only been performed from an influencing factors angle like the self-image/firm-image co-incidence; accounting information; neutral information; advocate recommendations; and personal financial needs. The research to date has tended to focus on IRBN rather than the Financial Accounting Disclosures (FAD) with consideration of the IS and the dynamics of these sentiments, FAD and IRBN. In addition, no research has been found that surveyed additional factors that might drive investors towards a certain behaviour. So far, this method has only been applied to investigate the dynamics of FAD, SN, and IRBN.

Although a sustainable number of studies on investor behaviour have examined factors influencing individual investment decisions. However, little knowledge is available on either the role of FAD (as a key part of corporate governance and an essential tool to announce news related to firms’ performance to the investors and different stakeholders) (Healy & Palepu, Citation2001) on the IRBN or how the IS impact their reactions under different declarations of bad news. The literature points out that FAD which might not be understood by many people is a vital motorist of effective financial markets (Demaline, Citation2018; Schoenfeld, Citation2017). Indeed, it is essential to reflect on the suitable strategy of disclosure, the briefness of accounting, the financial reports’ timeliness, and any bias in financial reporting (Gigler & Hemmer, Citation2001). In general, financial accounting disclosure contributes significantly to investors’ reactions toward bad financial news (Al-Tamimi, Citation2006).

The motivation for the research originated from the UAE Securities and Commodities Authority (SCA) guidance on website disclosures (SCA, Citation2018). IS is not the only factor that impacts irrational behaviour and performance in the financial market, rather, this can be caused by FAD (Al-Tamimi, Citation2006; M. Baker & Wurgler, Citation2007, etc.), little knowledge is available on the role of FAD on the IRBN (Healy & Palepu, Citation2001). A lack of studies exists on how the sentiments of investors impact their reactions to different declarations of bad news. Despite its great significance, very limited comprehensive research examined simultaneously physiological and cognitive factors and governance factors (embodied in FAD) that impact the IRBN. A unique setting of the UAE, and the PBOs, with rapidly growing markets and government initiatives to promote the IS and protect their rights, the current study has overlooked the issue of FAD and IRBFN in the presence of IS, as recommended by a few recent scholars such as Hassan (Citation2012), and therefore, this research is aiming to review the theoretical and empirical literature on FAD, IS, and IBFN and conclude the literature gaps within these dimensions. In attempts to answer the following Research Questions (RQ): what are the emerging dimensions of the FAD, IS, and IRBN? Does FAD impacts IRBN? Does “IS- Subjective norms” moderate the relationship between FAD and IRBN? Hence, the current research aims to examine the dynamic impact of FAD, individual IS, and IRBN. The research will propose an investors reactions model that will comprise processes and practices that could be used to enhance the decision-making process of investors and control their reactions that impact PBO in UAE. The proposed model counted as the first of its sort operated on the UAE’s PBO listed in Dubai and Abu Dhabi financial markets. To the extent that the writers recognize, there have been no researches that examine comprehensively physiological and cognitive factors and governance factors (embodied in FAD) that impact the reaction and perception of IRBN; hence, it focuses on factors other than emotional and cognitive sentiments which impact IRBFN (embodied in FAD). Further, it examines the direct relationship between FAD and IRBN in PBO which has been ignored by the existing literature and therefore, demands further attention. In addition, it reveals the moderating impact of IS on the relationship between FAD and IRBN in PBO in UAE financial markets. Besides, exploring physiological and cognitive factors and governance factors (embodied in FAD) that impact the IRBFN by proposing a model of IRBN. It also highlights the behavior of individual investors in the UAE so that politicians and officials can grasp proper measures to deliver the appropriate regulation. Innovative strategies can be built based on the result of the proposed study.

2. Theoretical underpinning

The irrational performance in the financial markets has attracted a great deal of attention in the literature (Al-Tamimi, Citation2006; M. Baker & Wurgler, Citation2007, etc.), one could suggest that in developing countries the causes often originate from investors’ emotional and cognitive sentiments, and complexity of the disclosed financial reports. Several studies have already examined changes in the field (e.g., Bolaman & Evrim Mandacı, Citation2014; Koseoglu, Citation2019) using many different approaches, resulting in diverse and at times contradictory findings. The main benefits of such studies are contributions to economic development, engagement of investors, enhancement of ways of thinking, the satisfaction of stakeholders, reduction of financial market fluctuations, improvement to the quality of investment decisions, attainment of rational behavior, and overall improvement to financial market performance (Ajzen & Fishbein, Citation1980; Phan & Zhou, Citation2014). However, the chance of mitigating IRBN depends on their perception of the bad news (Phan & Zhou, Citation2014). This indicates that PBOs need conscious individual investors, who can react more rationally to bad news. One of the main weaknesses of traditional finance theory in finance and economics is that it assumes that the securities price reflects the discounted value of predictable cash flows and that illogicality in the market is cast out by arbitrageurs. A theory is needed in financial market research that will help to highlight the conditions and drivers that lead to functional behavior so that the root causes of these behaviors can be understood and influenced. Due to the variation in the understanding and behavior of investors, it is vital to understand which IS dominates the literature on behavioral finance. From the literature search, East (Citation1993), Brown and Venkatesh (Citation2005), Song and Zahedi (Citation2005), and Mahoney (Citation2011) suggest many techniques and factors that impact behavioral intent, highlight various degrees of behavioral awareness, and have been revealed by different methodologies (e.g., quantitative study of market statistics vs experiments). Lovric et al. (Citation2008) suggest a cognitive model of the individual investor and investment environment; the model roughly highlights the most significant results from the current literature on investor behaviour and delivers a prominent clarification of the decision-making process made by different stockholders from both an academic and a practical viewpoint.

According to planned behaviour theory, behavioural intention counts as a direct precursor to the upcoming action. IRBN that are most often stated in the literature to be the investors’ perception of bad news such as termination of loss-making projects, fluctuation of market share price, and firm image disclosed in firms’ financial reports or websites or other formal or informal channels concern: governance and disclosure awareness, information quality, trust in firms’ disclosure channels, perceived benefits of the disclosure index (benefits), investment intentions (behavioural intention), investors’ judgement, perceived ease of use, perceived privacy, perceived risk and system security, investors’ over- or underreaction to good and bad news (Barberis et al., Citation1998; Veronesi, Citation1999), and disclosure policy and timeliness (Clatworthy & Jones, Citation2003; Frankel & Li, Citation2004; Gigler & Hemmer, Citation2001).

Nevertheless, FAD can influence IRBN. It is important to consider the best disclosure policy, the brevity of accounting, the timeliness of financial statements, and any bias in financial reporting (Gigler & Hemmer, Citation2001). In general, FAD contributes significantly to IRBN (Al-Tamimi, Citation2006). To understand the issues outlined above, it is critical to investigate the relationship between FAD and IRBN. Also, it is important to find out the main aspects that have a moderating effect on such a significant relationship. There is a need for more research in UAE PBO listed in the financial market related to best practices in managing factors that influence the financial market progression and investor maturity that are not related to governmental efforts (Al-Tamimi, Citation2006); rather, they can be associated with behavioral factors. Further, it was critical to develop more models to understand the field of behavioral finance to expose the reasons behind insufficiencies of the competitive market setting to endogenously prompt the development of organizations that are committed to the interest of the individual investors; more research studies are needed to be undertaken to achieve this as Malmendier and Shanthikumar (Citation2003) indicate that investors are not always considering the misalignment in incentives, but rather follow deformed advice exaggeratedly.

A comprehensive review of FAD, IS, and IRBN is performed in this study to identify the qualitative and quantitative dimensions to be appraised. Moreover, there seemed to be no existing empirical evidence that shows how IRBN is impacted by their sentiments, despite the disclosure and transparency frameworks applied worldwide—that is what the current study is attentive to. Lastly, on the concept of impression management (Brennan & Merkl Davies, Citation2013), the incomplete revelation hypothesis (Bloomfield, Citation2002), and the obfuscation theory (Bayerlein et al., Citation2012) that all relate to avoiding undesirable news, there was a need for research to be more concerned about the role of IS on the relationship between FAD, including readability—the textual complexity originated from the writing method (Brennan & Merkl Davies, Citation2013)—and it’s variation within a narrative (as a control tactic), and IRBN with the spread of social media and the internet in UAE PBO. In particular, the current study focuses on the perceptual reactions of different investors about firms’ efforts to disclose bad news in a very difficult way to process it by delivering tacky readability, therefore, postponing or stopping investors from reacting negatively and consequently maintaining firms’ good reputations; this corresponds with the obfuscation hypothesis (Thoms et al., Citation2020).

2.1. UAE disclosure index

The study of Hassan (Citation2012) has contributed to the literature on corporate governance that developed an index for corporate governance reporting (Aksu & Kosedag, Citation2006; Collett & Hrasky, Citation2005; Gandía, Citation2008; Haat et al., Citation2008; Hussainey & Al-Nodel, Citation2008; Tsamenyi et al., Citation2007). Hassan (Citation2012) has grouped the research into two groups; one group used the Organization for Economic Cooperation and Development (OECD) principles of governance to craft such an index (Chen et al., Citation2007; Cheung et al., Citation2007, Citation2010), whereas the other group has built their index of transparency and governance reporting based on Standard and Poor’s agency framework such as (Aksu & Kosedag, Citation2006; Tsamenyi et al., Citation2007); however, Hassan (Citation2012) has adopted a weighting approach to craft UAE’s corporate governance reporting index with acknowledging regulatory necessities in UAE and highlighting international governance practices addressed in the literature in addition to OECD standards simultaneously. Further, the UAE’s corporate governance reporting index crafted by Hassan (Citation2012) has also harmonized worldwide governance practices with the code of governance in UAE so that it is serviceable to UAE-listed companies. Besides, Hassan (Citation2012) highlighted the procedures followed to build that index which combines the UAE regulatory necessities with international governance implementations and practices while giving a greater rate to practices that are not mandatory governance codes in the UAE. A characteristic advantage of that index is that it has a quantifiable dimension to examine if UAE-listed companies support voluntary disclosure. The disclosure index in UAE has been crafted by Hassan (Citation2012) because of UAE governmental necessities.

2.2. Other disclosure channels

Despite the importance of the annual reports as a vital motor to corporate governance disclosure, exemplifying significant evidence for communal responsibility and transparency, comprising an inclusive particular of all the characteristics of the corporation’s operational performance and accordingly releasing the public responsibility of the management. However, the study of Hassan (Citation2012) has suggested extending their work by examining the disclosures of corporate governance by adding other disclosure channels such as press releases, TV, Radio, news about annual reports, quarterly reports, voluntary announcements, non-financial disclosure guided by different reporting regulations, corporation’ websites, financial analysis, and on-line announcements. This is harmonious with UAE regulations which require the press release on financial results or the disclosure of preliminary financial statements to be published before the opening trading session or after trading hours, to avoid suspension of Securities trading. Also, preliminary financial statements shall include the following information as a minimum requirement: (total assets, shareholders’ equity, revenues, net operating profit, net profit for the period, earnings per share, and a summary of the company’s performance for the financial period. Nevertheless, according to Heflin et al. (Citation2011), the corporation’s websites should disclose up-to-date, summarized information to analysts and the media about the materials provided, downloadable annual reports, notice of Annual General Meeting (AGM) or other general meetings, a notice of company’s constitution. The corporation’s websites, forums, blogs, and other communication channels provide information about the company s annual reports, quarterly reports, voluntary announcements, and non-financial disclosure. The study of Gandía (Citation2008) has examined the quality of online channels and the significance of the subject as a crucial factor in defining online disclosure quality. The study has developed three transparency indexes to measure the quality of corporate governance disclosure in Spain’s financial markets.

2.3. Investors’ reactions to financial markets

The behavioural intention which is recently defined as a person’s positiveness or negativism toward mental or emotional things (Phan & Zhou, Citation2014), reflects moderation to perform or not to perform the conduct in the future. According to planned behavior theory, behavioral intention counts as a direct precursor just earlier the upcoming action. This association has been evidenced and effectively accepted by several prior empirical works (Armitage & Conner, Citation2001; Phan & Zhou, Citation2014; Sheppard et al., Citation1988). This makes investors’ reactions a familiar dependent variable in several empirical works. Yang et al. (Citation2020) provided valued perceptions into the relations between investors’ perceived trust, information quality, and perceived benefits of the risk model. Results showed that the perceived benefits are affirmatively linked to investors’ intentions. Findings provided evidence about the mediating role of investors’ trust in the company’s websites. Particularly, trust moderately mediates the relationship between information quality and perceived benefits and completely mediates the link between cybersecurity awareness and perceived benefits. They provided an empirical indication that stakeholders with great trust in a firm’s website would perceive the risk, which then augments the probability of their intention to make an investment decision. These results support professionals to have an improved understanding of the impact of trust from investors’ point of view to benefit from the risk framework. Eventually, they highlighted augmented investor trust in firms that implement the risk management agenda of the Association of International Certified Professional Accountants’ (AICPA)’s cybersecurity. Hence, a further investigation of investors’ reactions theories is reviewed and discussed in the following sections. Merikas and Prasad (Citation2003) used an adapted survey to examine elements impacting investor behavior in the Athens financial market in Greece. Findings show that many economic benchmarks pooled with different factors impact investors’ decisions to purchase or sell shares in the stock market. No solo integral way is being adopted, in fact, several groups of elements (Al-Tamimi, Citation2006). Further, findings indicate the positive relationship between elements identified by behavioral finance theory and other factors studied in the mentioned research and the dynamic investor’s manners in the financial market of Athens.

2.4. Invertors’ sentiments (IS)

Sentiments of investors are defined as the views and feelings toward the upcoming cash flows and related risks of their investments without having as appropriate evidence to support their judgments (Makau & Ambrose, Citation2018). Hence, different investors tend towards a certain investment due to their sentiments therefore this could create a bubble or a state wherein a price update motivates the eagerness of an investor, diffused by emotional contagion from one to another, in the progression expanding tales that may rationalize the price upsurges and attracting more and more types of stakeholders. Hidajat (Citation2019). Has been argued that several behavioral biases contribute to such abnormal fluctuations in asset flow and therefore the share market price in the financial market.

2.5. Subjective norms (SN)

According to the theory of reasoned action and planned behavior theory, Subjective Norms (SN) is considered a fundamental factor. It includes a person’s perception about whether the majority of important people believe he/she ought to or ought not to take an action towards the behaviour (Ajzen & Fishbein, Citation1980; Phan & Zhou, Citation2014; Verma & Chandra, Citation2018). This indicates that even when investors are not positive about a behaviour, they might perform it due to societal pressure (Phan & Zhou, Citation2014; Venkatesh & Davis, Citation2000). Despite the evidence provided by Mahastanti (Citation2014) about the insignificant associations between SN and investors’ intentions, the various arguments concerning the forecasting influence of SN on investors’ intent may still suggest a significant association between the two factors. It is reasonable to expect that if a stockholder observes supportive SN, the likelihood to invest will be higher than individuals who do not experience equivalent encouragement. Substantially, and according to the prior review of SN (as a part of investors’ sentiments), the current study attempts to examine how individual investors react to bad news by considering investors’ SN based on FAD disclosed via different disclosure channels. In other words, is there any moderating impact of investors’ SN on the relationship between FAD and IRBN?

Overall, and based on the above review of different IS, the current study has attempted to examine the moderation impact of investors’ SN on the relationship between FAD and IRBN. In summary, it can be argued that Subjective norms play a moderating role in the relationship between FAD and IRBNs. It can be hypothesized the following:

2.6. Direct hypotheses

The study’s principal aim is to empirically examine the relationships between financial accounting disclosures and investors’ reactions toward bad financial news in PBOs. Further, the study highlights the impact of investors’ sentiments on this relationship. Hence, the study was hypothesizing the investor is an element of examination, whereas financial accounting disclosures, investors’ sentiments, and investors’ reactions toward bad financial news in PBOs have already been recognized and tested in the literature.

The study of Clatworthy and Jones (Citation2003) underlines this notion by explaining that accounting disclosure models have filled the gap between financial accounting disclosures as an important tool to control the reactions to good and bad financial news. The first theory is relevant to investors’ reactions towards bad financial news, behavioural finance theory, which argues that sentiments and perceptive mistakes impact the decision-making processes of different investors (Koseoglu, Citation2019). Several theories relate to financial accounting disclosure; for example, Morris (Citation1987) reveals that signalling and agency theories are in fact in harmony. Following agency theory, managers might use excessively complicated descriptions to hinder and deter stakeholders’ capability of grasping bad news that might affect the firm’s stock values negatively (Bloomfield, Citation2002). Stakeholder theory could clarify the responsibilities of different groups of users (Pavlopoulos et al., Citation2019). However, to accomplish this core goal, financial accounting disclosure is assumed to be an independent variable that comprises aspects connected to the impacts of financial information on investors’ reactions toward bad financial news, as described by Hassan (Citation2012). Hence, financial accounting disclosures FAD are clustered under five global factors: ownership structure and investors’ rights, board and management structure and processes, external auditing and audit service, transparency disclosure, and other disclosure channels. Each of the global factors comprises specific dimensions associated with investors’ reactions towards bad financial news. Further, several moderating variables impact investors’ reactions towards bad financial news in PBOs related to investors’ sentiments. Investors’ sentiments moderating variables- subjective norms (IS-SN). The dependent variable is investors’ reactions towards bad financial news IRBN, which is clustered into three global factors: investors’ reactions towards the termination of loss-making projects, investors’ reactions towards fluctuation of share market price, and investors’ reactions towards the firm image. Consequently, and founded on the inclusive literature review of this study, Figure embodies the research conceptual model.

Figure 1. Research conceptual model and hypotheses.

H1:

There is a positive relationship between FAD and IRBN in PBOs in UAE.

H1-A:

There is a positive relationship between “ownership structure and investors’ rights” and IRBN in PBOs in UAE.

H1-B:

There is a positive relationship between “board and management structure and processes” and IRBN in PBOs in UAE.

H1-C:

There is a positive relationship between “external auditing and audit service” and IRBN in PBOs in UAE.

H1-D:

There is a positive relationship between “transparency disclosure” and IRBN in PBOs in UAE.

H1-E:

There is a positive relationship between “other disclosure channels” and IRBN in PBOs in UAE.

2.7. Moderators’ hypotheses

H2:

Investors’ sentiments “Subjective norms” moderate the relationship between the FAD and IRBN in PBOs in UAE. (See Figure : Research conceptual model and hypotheses).

3. Methodology and approach

3.1. Data collection instrument, procedures, and research sample

An online questionnaireFootnote1 (Survey google forms) was adopted as the prime research method to collect data, with closed-ended questions, and seven-point Likert scale (see 3 Appendix A), with 10 minutes estimated time. The questionnaire highlighted the most important factors that impact the investors reactions towards bad financial, which may have a positive or negative impact on the organization, the financial markets, and the whole economy; it is divided into three parts: (first part related to demographic data: age, gender, education Level, number of years of experience, monthly income, second part measures the financial accounting disclosure: investors’ right, board and management structure and processes, external auditing and audit service, transparency disclosure and other disclosure channels second part also measures investors’ sentiments in terms of subjective norms, while the third part measures investors’ perceptual reactions towards bad financial news related to firm-image, termination of loss-making projects and fluctuation of share market price in financial markets in terms of governance and disclosure awareness, information quality, trust in firm’s disclosure channels, perceived benefits of the disclosure index, investment intentions, investor’s judgement, perceived ease of use, perceived privacy, and perceived risk and system security. Questionnaire items were coded by specific coding systems to enter the data into SPSS software to assure the right grouping of the items under the global variables (see Appendix B). A random sampling technique was adopted. 1000 surveys were sent to random individuals of stakeholders who deal with the financial sector in the UAE that represented the selected population of the research, the response rate was 31%, 310 surveys were filled out and used for data analysis to generalize the study findings.

3.2. Data analysis

After checking the missing data (no missing data of all of the study variables), no measurement was eliminated from the study. Univariate detection was selected, and data outliers were checked using the SPSS Boxplots that confirmed the absence of any outliers among the data. All of the study measures have passed the Cronbach alpha test, as the value for each measurement is greater than 0.7. Thus, all measurements are reliable and there is no need to eliminate any item (investors’ rights: 0.85; board and management structure and processes: 0.81; external auditing and audit service: 0.76; transparency disclosure: 0.90; other disclosure channels; 0.79; IS-Subjective norms or narrative fallacy: 0.94; investors ‘reactions towards the termination of loss-making projects: 0.886; investors ‘reactions towards fluctuation of share market price: 0.741, 0.837; investors reactions towards firm image: governance and disclosure awareness 0.854, perceived benefits of the disclosure index (benefits) 0.842, investment intentions 0.826), this indicates that all the constructs on the questionnaire are reliable based on Cronbach’s alpha test’s results. Further, by applying Harman’s single factor common method bias test, the results demonstrate that the single factor explains only (24.525%) which is less than 50%, which means that there is no common method bias in the data used in this research. Moreover, descriptive statistics of the control variables were conducted, (see Table 1 in Appendix C which provides a summary of the study participants profile, besides normality tests to all variables (see Table 2 in Appendix D that lists all variables with their corresponding skewness and kurtosis values). Accordingly, normality can be assumed for the study data.

3.3. Testing the research hypotheses

The structural models were applied to the measurement of this study using Amos 23. The structural models included direct structural paths from FAD (Investor’s Reaction (IR), Board and Management Structure and Procedures (BOMS), External Auditing and Audit Services (EAUS), Transparency Disclosure (TPD), and Other Disclosure Channels (ODCH)) and the dependent variables of IRBN. Results showed a positive significant relationship at a 99% confidence level between FAD (IR, BOMS, EAUS, TPD, and ODCH) and the dependent variables of IRBN (.439). In addition, there is not a significant relationship between external auditing and audit service (EAUS) and FAD (.010, p-value = 0.805). There is a good positive significant relationship at a 99% confidence level between other disclosure channels (ODCH) and FAD (0.916); board and management structure and processes (BOMS) and FAD (0.935); transparency disclosure (TPD) and FAD (0.862); ownership structure and investors’ rights (IR) and FAD (0.766). Further, there is a good positive significant relationship at a 99% confidence level between IRBN dimensions and IRBN (0.779; 0.843;0.783; 0.850; 0.730). From the above, it can be stated that H1 is supported by the data and there is a positive relationship between FAD and IRBN in PBOs in the UAE. Likewise, H1-A is supported by the data and ownership structure and investors’ rights have an impact on IRBN in PBO in the UAE. H1-B is also supported by the data with a positive significant relationship at a 99% confidence level between board and management structure and processes (BOMS) and FAD (.935). Correspondingly, H1-C, the direct positive relationship between external auditing and audit service and IRBN was tested. At a 99% confidence level, the results show no significant relationship between external auditing and audit service (EAUS) and FAD (.010, p-value = 0.805), Therefore, H1-C is not supported by the data and external auditing and audit service plays no role in IRBN. Similarly, H1-D, the positive relationship between transparency disclosure and IRBN was tested. The results show a good positive significant relationship between transparency disclosure (TPD) and FAD (0.862); therefore, H1-D is supported by the data, and transparency disclosure plays a role in IRBN in PBO in the UAE. In terms of H1-E, the results show that there is a positive significant relationship between other disclosure channels (ODCH) and IRBN (0.916). Hence, H1-E is supported by the data. The structural model fit results for FAD and IRBN are as follow: (CMIN 2695.080; CMIN/DF 2.533; TLI 0.878; CFI 0.890; RMSEA 0.070)Footnote2 (see Appendix E). The findings were within the acceptable cut-off values and thus confirm that these models displayed an acceptable model fit for FAD and IRBN.

4. Results

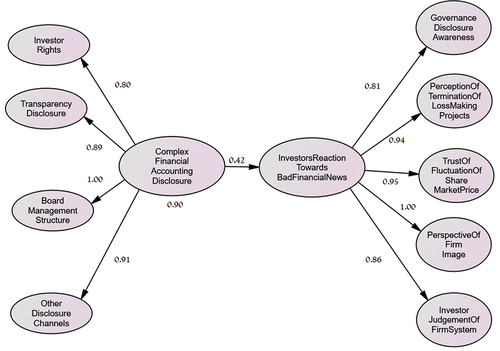

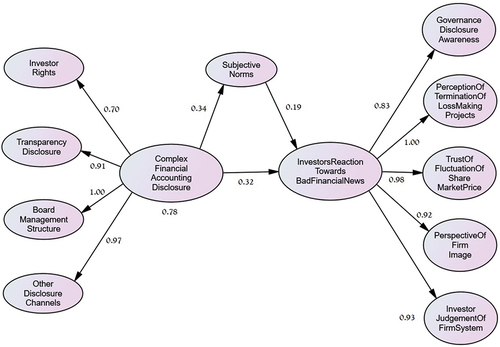

The study’s overall model is shown in Figures . This model is broken down into two models: The first model demonstrates the positive direct relationship between the FAD components and IRBNs in PBOs, as shown in Figure . The second model illustrates investors’ sentiments as a moderator of the relationship between FAD and IRBNs, as shown in Figure .

Figure 2. The study model before moderation.

Figure 3. The study model after moderation.

All terms shown in Figure & 3 are specifically linked to their specific meaning in the coding scheme in Appendix B. From the models shown in Figures , the overall findings indicate first, a significant positive direct relationship between FAD and IRBNs. Several scholars indicate that there is a relationship between FAD and IRBNs (Al-Tamimi, Citation2006; Tan & Tan, Citation2009; Yang et al., Citation2020). Second, “investors” sentiments” moderate the relationship between FAD and IRBNs. The relationship between FAD and IRBN before moderation is significant. However, after moderation, the relationship between FAD and IRBN is still significant. Numerous scholars have implied that IS can moderate the relationship between FAD and IRBNs (Ajzen & Fishbein, Citation1980; Phan & Zhou, Citation2014). However, at this stage, the conceptual model shown in Figure can be modified in accordance with the findings of the current study. Thus, the modified study model is illustrated in Figure .

Figure 4. Research outcome: a conceptual model.

In comparison, in the conceptual model, the FAD items (from the literature view) were organized into five clusters: ownership structure and investors’ rights, board and management structure and processes, external auditing and audit service, transparency disclosure, and other disclosure channels). In the revised study model, there are four clusters of FAD items (see Figure ). Similarly, IRBNs items (from the literature review) were organized into three clusters: investors’ reactions towards the termination of loss-making projects, investors’ reactions towards fluctuation of share market price, and investors’ reactions towards the firm image. In the revised study model, there are five clusters for IRBN items: investors’ perception of firm image, investors’ awareness of governance and disclosure, investors’ perception of termination of loss-making projects, investors’ judgement of firms’ systems, and investors’ trust towards fluctuation of share market price in financial markets.

5. Discussion of the findings and the study’s implications

Using the results obtained from the models shown in Figure , the overall findings indicate the main conclusions.

Scholars point out many abnormalities in the behaviour of individual investors that take them away from reasonable and sensible decisions and contravene standard financial theory. These abnormalities are the cognitive mistakes or biases that impact investors’ decisions. S. Kumar and Goyal (Citation2015) developed prospect theory and explain individuals’ resolutions and the process of making decisions in risky and uncertain situations. In contrast, accounting literature suggests that the enhanced governance practices that may lead to improved financial accounting disclosures and extra corporate reporting transparency can, in turn, deliver better liquidity and investment creation in developing markets (Aksu & Kosedag, Citation2006). Hence, corporate governance is crucial to many parties and stakeholders, such as investors, brokers, officials, creditors, clients, workforces, etc. Hence, similar phenomena were examined by both accounting and behavioural finance theories from opposing theoretical views. Therefore, there is a growing scholarly impetus to contribute to this stance that interprets behaviours from both accounting and behavioural finance perspectives (Phan & Zhou, Citation2014). The study’s findings illustrate that the components of financial accounting disclosure in the study models—ownership structure and investors’ rights, board and management structure and processes, transparency disclosure, and other disclosure channels—have a significant positive relationship with investors’ reactions towards bad financial news; they have the role of an antecedent for investors’ reactions towards bad financial news. In other words, the components of financial accounting disclosure influence the individual’s perception of bad financial news.

Therefore, the study sheds light on the type of relationships and influences that exist between financial accounting disclosure, and investors’ sentiments, while further supporting the existence of the coevolution theory between the two perspectives of accounting and behavioural finance theory. In addition, the study provides empirical evidence that demonstrates that integrating accounting and behavioural finance theory will enhance our understanding of the studied phenomena. This finding is in line with the work of Al-Tamimi (Citation2006), who examined the previous literature and presents the idea of a coevolution theory between accounting and behavioural finance that combines both perspectives in an evolutionary account of a dynamic process of mutual influence.

6. Conclusion and recommendations

Behavioral finance handles the behavioral and psychological parts of the process of making investment decisions. Scholars point out many abnormalities in the behavior of individual investors that take them away from reasonable and sensible decisions and contravene standard financial theory. These abnormalities are the cognitive mistakes or biases that impact investors’ decisions. S. Kumar and Goyal (Citation2015) refer to the work of Kahneman and Tversky (Citation1979), which developed prospect theory and explain individuals’ resolutions and the process of making decisions in risky and uncertain situations. In contrast, accounting literature suggests that the enhanced governance practices that may lead to improved FAD and extra corporate reporting transparency can, in turn, deliver better liquidity and investment creation in developing markets (Aksu & Kosedag, Citation2006; Hussainey, Citation2004). Hence, corporate governance is crucial to many parties and stakeholders, such as investors, brokers, officials, creditors, clients, workforces, etc. Hence, similar phenomena were examined by both accounting and behavioral finance theories from opposing theoretical views. Therefore, there is a growing scholarly impetus to contribute to this stance that interprets behaviors from both accounting and behavioral finance perspectives (Al-Tamimi, Citation2006; Phan & Zhou, Citation2014). The current study contributes to improving our understanding of the relationship between FAD (agency theory) and IS (SN) in predicting investors’ reactions toward bad financial news. The study’s findings illustrate that the components of FAD in the study models—ownership structure and investors’ rights, board and management structure and processes, transparency disclosure, and other disclosure channels—have a significant positive relationship with IRBN; they have the role of an antecedent for IRBN. In other words, the components of FAD influence the IRBN. Meanwhile, the study’s results show that IS has a moderating role in the relationship between the components of FAD and IRBN. Therefore, the study sheds light on the type of relationships and influences that exist between FAD (agency theory), and IS (SN), while further supporting the existence of the coevolution theory between the two perspectives of accounting and behavioral finance theory. In addition, the study provides empirical evidence that demonstrates that integrating accounting and behavioral finance theory will enhance our understanding of the studied phenomena. This finding is in line with Al-Tamimi (Citation2006), who examined the previous literature and presents the idea of a coevolution theory between accounting and behavioral finance that combines both perspectives in a coevolutionary account of a dynamic process of mutual influence.

To conclude, the following remarks can be made. It is recommended for future research to investigate the impact of FAD on investors’ reactions to good news and also to examine the impact of FAD on IRBN by quantifying the effects of IS using a different measurement tool. Further, using the study’s conceptual framework in a different context would validate its results at an international level. Besides, it is recommended for policymakers and industry pay more attention to the diversity of IS. So that to mitigate the IRBNs. This requires integration between theory and practice, in addition, it is important to enhance the FAD concept in the UAE, this can be implemented through financial market authorities and agencies. Also, it is significant for financial markets to ensure that the existing laws allow investors to develop new ways of reacting to bad news; by spreading awareness of disclosure practices within the sector.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. Ethics approval for the questionnaire used in this study was obtained from the Research Ethics committee in the British University in Dubai on 12 December 2021.

2. CMIN = Chi-square Minimum; CMIN/DF = Chi-square Minimum with Degree of Freedom; TLI = Tucker-Lewis Index; CFI = Comparative Fit Index; RMSEA = Root Mean Square Error Approximation.

References

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behaviour (Englewood Cliffs). Prentice-Hall.

- Aksu, M., & Kosedag, A. (2006). Transparency and disclosure scores stock exchange. Corporate Governance, 14(4), 277–34. https://doi.org/10.1111/j.1467-8683.2006.00507.x

- Al-Tamimi, H. A. H. (2006). Factors influencing individual investor behavior: An empirical study of the UAE financial markets. Business Review, 5(2), 225–233. https://api.semanticscholar.org/CorpusID:168825812

- Armitage, C. J., & Conner, M. (2001). Efficacy of the theory of planned behaviour: A meta‐analytic review. British Journal of Social Psychology, 40(4), 471–499. https://doi.org/10.1348/014466601164939

- Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of Economic Perspectives, 21(2), 129–151. https://doi.org/10.1257/jep.21.2.129

- Barberis, N., Shleifer, A., & Vishny, R. (1998). A model of investor sentiment. Journal of Financial Economics, 49(3), 307–343. https://doi.org/10.1016/S0304-405X(98)00027-0

- Bayerlein, L., Davidson, P., & Hussainey, K. (2012). The influence of connotation on readability and obfuscation in Australian chairman addresses. Managerial Auditing Journal, 27(2), 175–198. https://doi.org/10.1108/02686901211189853

- Bloomfield, R. J. (2002). The “Incomplete Revelation Hypothesis” and financial reporting. Accounting Horizons, 16(3), 233–243. https://doi.org/10.2308/acch.2002.16.3.233

- Bolaman, Ö., & Evrim Mandacı, P. (2014). Effect of investor sentiment on stock markets. Finansal Araştırmalar ve Çalışmalar Dergisi, 6(11), 51–64. https://doi.org/10.14784/JFRS.2014117327

- Brennan, N. M., & Merkl Davies, D. M. (2013). Accounting narratives and impression management (1st ed.). London. The Routledge Companion to Accounting Communication.

- Brown, S. A., & Venkatesh, V. (2005). Model of adoption of technology in households: A baseline model test and extension incorporating household life cycle. MIS Quarterly, 29(3), 399–426. https://doi.org/10.2307/25148690

- Chen, A., Kao, L., Tsao, M., & Wu, C. (2007). Building a corporate governance index from the perspectives of ownership and leadership for firms in Taiwan. Corporate Governance an International Review, 15(2), 251–261.. https://doi.org/10.1111/j.1467-8683.2007.00572.x

- Cheung, Y. L., Connelly, J. T., Limpaphayom, P., & Zhou, L. (2007). Do investors really value corporate governance? Evidence from the Hong Kong market. Journal of International Financial Management & Accounting, 18(2), 86–122.. https://doi.org/10.1111/j.1467-646X.2007.01009.x

- Cheung, Y. L., Jiang, P., & Tan, W. (2010). A transparency disclosure index measuring disclosures: Chinese listed companies. Journal of Accounting and Public Policy, 29(3), 259–280.. https://doi.org/10.1016/j.jaccpubpol.2010.02.001

- Clatworthy, M., & Jones, M. J. (2003). Financial reporting of good news and bad news: Evidence from accounting narratives. Accounting and Business Research, 33(3), 171–185.. https://doi.org/10.1080/00014788.2003.9729645

- Collett, P., & Hrasky, S. (2005). Voluntary disclosure of corporate governance practices by listed Australian companies. Corporate Governance an International Review, 13(2), 188–196. https://doi.org/10.1111/j.1467-8683.2005.00417.x

- Demaline, C. J. (2018). Firm performance and readability of the manager ’ s disclosures : A causal-comparative study. [ Doctoral dissertation]. Grand Canyon University.1–283.

- East, R. (1993). Investment decisions and the theory of planned behaviour. Journal of Economic Psychology, 4(2), 337–375.. https://doi.org/10.1016/0167-4870(93)90006-7

- Frankel, R., & Li, X. (2004). Characteristics of a firm’s information environment and the information asymmetry between insiders and outsiders. Journal of Accounting and Economics, 37(2), 229–259.. https://doi.org/10.1016/j.jacceco.2003.09.004.

- Gandía, J. L. (2008). Determinants of internet-based corporate governance disclosure by Spanish listed companies. Online Information Review, 32(6), 791–817. https://doi.org/10.1108/14684520810923944

- Gigler, F. B., & Hemmer, T. (2001). Conservatism, optimal disclosure policy, and the timeliness of financial reports. The Accounting Review, 76(4), 471–493.. https://doi.org/10.2308/accr.2001.76.4.471

- Haat, M. H. C., Rahman, R. A., & Mahenthiran, S. (2008). Corporate governance, transparency and performance of Malaysian companies. Managerial Auditing Journal, 23(8), 744–778. https://doi.org/10.1108/02686900810899518

- Hassan, M. K. (2012). A disclosure index to measure the extent of corporate governance reporting by UAE listed corporations. Journal of Financial Reporting and Accounting, 10(1), 4–33. https://doi.org/10.1108/19852511211237426

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440.. https://doi.org/10.1016/S0165-4101(01)00018-0

- Heflin, F., Shaw, K. W., & Wild, J. J. (2011). Credit ratings and disclosure channels. Research in Accounting Regulation, 23(1), 20–33. https://doi.org/10.1016/j.racreg.2011.03.004

- Hidajat, T. (2019). Behavioural biases in bitcoin trading. Fokus Ekonomi. Fokus Ekonomi : Jurnal Ilmiah Ekonomi, 14(2), 337–354.. https://doi.org/10.34152/fe.14.2.337-354

- Hussainey, K. (2004). A study of the ability of (partially) automated disclosure scores to explain the information content of annual report narratives for future earnings. Manchester University of Manchester, 1–230. 0000 0001 3585 2009.

- Hussainey, K., & Al-Nodel, A. (2008). Corporate governance online reporting by Saudi listed companies. Research in Accounting in Emerging Economies, 8, 39–64. https://doi.org/10.1016/S1479-3563(08)08002-X

- Kahneman, D., & Tversky, A. (1979). On the interpretation of intuitive probability: A reply to Jonathan Cohen. Cognition, 7(4), 409–411. https://doi.org/10.1016/0010-0277(79)90024-6

- Koseoglu, S. D. (2019). Behavioral finance vs. traditional finance. Behavioral Finance and Decision-Making Models (pp. 1–23). IGI Global.

- Kumar, S., & Goyal, N. (2015). Behavioural biases in investment decision making–a systematic literature review. Qualitative Research in Financial Markets, 7(1), 88–108. https://doi.org/10.1108/QRFM-07-2014-0022

- Lovric, M., Kaymak, U., & Spronk, J. (2008). A conceptual model of investor behavior. 1-52. ERIM Report Series. Reference No. ERS-2008-030-F&A.

- Mahastanti, L., & Hariady, E. (2014). Determining the factors which affect the stock investment decisions of potential female investors in Indonesia. International Journal of Process Management and Benchmarking. https://doi.org/10.1504/IJPMB.2014.060407

- Mahoney, M. L. (2011). An examination of the determinants of top management support of information technology projects. ProQuest LLC. 789 East Eisenhower Parkway, PO Box 1346.

- Makau, M. M., & Ambrose, J. (2018). Systematic risk factors, investor sentiment and stock market. International Journal of Management & Commerce Innovations, 5(2), 132–1143. http://ir-library.ku.ac.ke/handle/123456789/20120

- Malmendier, U., & Shanthikumar, D. (2003). Are small investors naïve About Incentives? NBER Working Paper, 10812(2003), 1–31. http://www.nber.org/papers/w10812

- Merikas, A., & Prasad, D. (2003). Factors influencing Greek investor behaviour on the Athens Stock Exchange. The Journal of Business, 66(1), 1–20.. https://doi.org/10.4236/me.2014.513113

- Morris, R. D. (1987). Signalling, agency theory and accounting policy choice. Accounting and Business Research, 18(69), 47–56.

- Pavlopoulos, A., Magnis, C., & Iatridis, G. E. (2019). Integrated reporting: An accounting disclosure tool for high quality financial reporting. Research in International Business and Finance, 49, 13–40.

- Phan, K. C., & Zhou, J. (2014). Factors influencing individual investor behavior: An empirical study of the Vietnamese stock market. American Journal of Business and Management, 3(2), 77–94.. https://doi.org/10.11634/216796061403527

- Schoenfeld, J. (2017). The effect of voluntary disclosure on stock liquidity: New evidence from index funds. Journal of Accounting and Economics, 63(1), 51–74. https://doi.org/10.1016/j.jacceco.2016.10.007

- Securities and Commodities Authority. (2018). Regulations, UAE government. https://www.sca.gov.ae/

- Sheppard, B. H., Hartwick, J., & Warshaw, P. R. (1988). The theory of reasoned action: A meta-analysis of past research with recommendations for modifications and future research. The Journal of Consumer Research, 15(3), 325–343.. https://doi.org/10.1086/209170

- Song, J., & Zahedi, F. (2005). A theoretical approach to web design in E-commerce: A belief reinforcement model. Management Science, 51(8), 1219–1235. https://doi.org/10.1287/mnsc.1050.0427

- Tan, H.-T., & Tan, S.-K. (2009). Investors’ reactions to management disclosure corrections: Does presentation format matter? Contemporary Accounting Research, 26(2), 1–43. https://doi.org/10.1111/j.1475-679X.2009.00350.x

- Thoms, C., Degenhart, A., & Wohlgemuth, K. (2020). Is bad news difficult to read? A readability analysis of differently connoted passages in the annual reports of the 30 DAX companies. Journal of Business and Technical Communication, 34(2), 157–187.. https://doi.org/10.1177/1050651919892312

- Tsamenyi, M., Enninful-Adu, E., & Onumah, J. (2007). Disclosure and corporate governance in developing countries: Evidence from Ghana. Managerial Auditing Journal, 22(3), 319–334. https://doi.org/10.1108/02686900710733170

- Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management science, 46(2), 186–204.

- Verma, V. K., & Chandra, B. (2018). An application of theory of planned behavior to predict young Indian consumers’ green hotel visit intention. Journal of Cleaner Production, 172, 1152–1162. https://doi.org/10.1016/j.jclepro.2017.10.047

- Veronesi, P. (1999). Stock market overreaction to bad news in good times: A rational expectations equilibrium model. The Review of Financial Studies, 12(5), 975–1007.. https://doi.org/10.1093/rfs/12.5.975

- Yang, L., Lau, L., & Gan, H. (2020). Investors’ perceptions of the cybersecurity risk management reporting framework. International Journal of Accounting & Information Management, 28(1), 167–183. https://doi.org/10.1108/IJAIM-02-2019-0022

Appendix A:

Questionnaire

Research QuestionnairePlease provide an appropriate response to each section

Part One: Demographic data

Part Two

First Group: Financial accounting disclosure

To what extent do you agree with the following general statements in relation to the financial accounting disclosure, please indicate (i.e. tick ✓) the extent of level of agreement on each statement.

Second group: Investors’ sentiments

To what extent do you personally agree or degree that following statements. Please indicate (i.e. tick ✓) the extent of level of agreement on each statement.

Part Three

Third Group: investors’ perceptual reactions towards bad financial news

To what extent do you personally agree or degree that following statements. Please indicate (i.e. tick ✓) the extent of level of agreement on each statement.

Thank you very much for taking part in this survey. If you would like a summary of the results, please enter your name and contact details below:

Name:Contact Details:

Appendix B:

Coding scheme

Appendix

Appendix D:Table 2: Skewness and Kurtosis scores

Appendix E: Model Fit Summar

CMIN

RMR, GFI

Baseline Comparisons

Parsimony-Adjusted Measures

NCP

FMIN

RMSEA

AIC

ECVI

HOELTER