?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Middle East region is recognized by observers as one of the most politically unstable areas worldwide. Due to the significant growth of foreign direct investment in the MENA region during the period before the recent political turmoil, this study empirically tests the impact of these political disturbances on foreign direct investment over time across Arab Spring countries. The study uses panel techniques to estimate the regression models by applying pooled OLS, fixed effect, and random effect. In addition, the Hausman test is used in order to choose the appropriate estimated model between fixed effects and random effects. The sample covers five countries in the MENA region that experienced the Arab Spring uprising during the period (2011–2014). The whole yearly data set ranges from 1980 to 2014. The data describes the periods before and during the Arab Spring turmoil (2011–2014). According to the appropriate fixed effect approach, results show that the economic, social, and political factors are all crucial contributors to FDI movements and volumes in Arab Spring countries. Interestingly, the Arab Spring era plays a very important role in the deterioration of FDI in these countries. The movement of FDI in the Arab Spring region is related to episodes of political instability. This political unrest has created an adverse impact on foreign investment, and this indicates a lack of trust of potential international investors. This study also confirms that other economic and social factors are significant contributors to FDI in the MENA region.

PUBLIC INTEREST STATEMENT

This paper highlights the crucial importance of political conditions in regulating foreign direct investment in the MENA region. More particularly, it shows that the Arab Spring unrest had significant negative consequences for the region’s ability to attract necessary foreign direct investment. Many of the governments of this region are not able to respond to inevitable political dissatisfaction by implementing practices and policies which do not destabilize underlying political economic conditions. The study also highlights the importance of key economic and social variable in encouraging foreign direct investment. These include developing an effective education system, promoting relative economic openness, and implementing economic policies which avoid exchange rate volatility.

1. Introduction

The Middle East is considered as one of the most politically unstable regions in the world. Massive demonstrations in the region of Middle East and North Africa (MENA) have started since the “Iranian Green Movement” in 2009. These uprisings led to significant political instability in some Arab countries. Specifically, the countries of Tunisia, Egypt, Libya, and Yemen and Syria all experienced regime change (Alsoudi, Citation2014).

Most economic studies of the impact of social and political unrest find, not surprisingly, that there is an inverse relationship between political instability and GDP growth and investment (Barro, Citation1991). In addition, Lucas (Citation1990) supports the hypothesis of political risk being a barrier to capital flows between countries more than other factors related to physical capital, human capital and returns on capital. One would also expect that poor economic performance would generate a negative feedback loop that leads to greater political instability. Although such a hypothesis is plausible and is generally confirmed by rigorous empirical studies, it is also true that the link between economic performance and political unrest is complex. Large-scale empirical studies of this issue have found that the form of political governance and socio-economic conditions are also important causal factors associated with political instability (Feng, Citation1997).

UNCTAD’s world investment and trade dataFootnote1 illustrates important phenomenon of FDI in the MENA region. According to the authors’ calculations of the average growth rates of total FDI inflows, stock, and trade balance in the MENA region, an average growth of approximately 43.5% in FDI inflows and 28.2% in FDI stock occurred during the period (2004–2008) compared to an average growth of 6.8% and 9.4% of FDI inflows and stock, respectively, during the period (1998–2002). Similarly, MENA region’s total trade balance grew by an average of approximately 33.9% during (2004–2008) compared to 9.8% during (1998–2002). However, during the period (2010–2014) the average growth rates of FDI inflows and stock dropped to approximately 15% and 7.8%, respectively, and total trade balance increased by an average of 51.2%. These figures illustrate the importance of FDI in the MENA region. It grows by a larger percentage than the growth of trade, especially during the period (2004–2008).

FDI is important in the MENA region because it can strengthen the productivity of these economies and create a more sustainable relationship between exports and imports. Therefore, the severe drop in FDI inflows and stock during the period of Arab spring revolution raises questions regarding the impact of political instability on FDI in the MENA region. Even though there are other exogenous factors that affect the performance of FDI such as the decline in global production and the related drop in oil prices, the role of the disrupted political systems in the MENA region most likely affects FDI performance. That is because ineffective political systems as well as political instability can affect negatively operating costs of firms engaged with FDI (Al-Khouri, Citation2015; Butler & Joaquin, Citation1998). Also, political instability lowers foreign investors’ confidence and expectations regarding investment profitability (Brada et al., Citation2004).

As a result of political instability during the Arab spring period across some MENA countries, the severe disruptions to economic activity were accompanied by a significant decline in FDI. Therefore, the purpose of this study is to investigate empirically how the Arab spring impacting FDI for the group of countries affected by the Arab spring revolution. Given the importance of the recent political disturbances across Arab countries, this paper extends this literature to test the impact of political conflict in the Arab Spring region on the movements of FDI from 1980 to 2014. At the end of this period (2011–14), the intensity of social unrest caused severe political disturbances throughout much of the MENA region.

In this study, the impact of political unrest on FDI is examined in five countries—namely Algeria, Bahrain, Tunisia, Egypt, and Syria. All of these countries experienced significant and, in some cases, catastrophic unrest during the Arab Spring. These countries are chosen as the main representatives of Arab Spring revolutions due to the severity of turmoil taking place and its wide impact on the country’s political and economic structure. Although the countries of Libya and Yemen were dramatically affected by the Arab Spring uprisings, these countries are excluded from the study due to data unavailability. Furthermore, this study aims to address the gaps in the literature review by providing original quantitative estimates of the impact of political unrest on FDI by focusing on five important countries of the region—namely Algeria, Bahrain, Tunisia, Egypt, and Syria. A panel approach is used which accounts for both unobservable cross-country heterogeneity and common year shocks through the application of fixed and random effect methods. The study contributes to the empirical literature of the impact of political disturbances on FDI for the case of Arab Spring countries. In addition, the empirical model is estimated using two specifications in order to capture the impact of different aspects of political pressures on the dynamics and volume of FDI in the selected countries.

This study has several results. The movement of FDI in the Arab Spring region is related to episodes of political instability. This political unrest has created an adverse impact on foreign investment, and this indicates a lack of trust of potential international investors. This study also confirms that other economic and social factors (GDP, trade openness, exchange rate, and education) are significant contributors to FDI in the MENA region.

This paper is organized as follows. Section II provides an overview of economic consequences across the Arab Spring region. Section III contains an analysis of the relevant literature that has directed this study. In section IV, the description of data is provided. In section V, the methodology and model specification are described. The empirical findings are explained in section VI, and section VII concludes with a discussion of policy implications.

2. Economic consequences of political unrest in MENA region

2.1. Arab spring overview

The term “Arab Spring” refers to a series of revolutionary acts against incumbent governments in several MENA region countries. Political turmoil started in the Maghreb countries and extended to Egypt, Mediterranean, and GCC countries. The Arab Spring revolutions varied in their severity and consequences ranging from minor protests to regime elimination to complete country devastation. Arab Spring revolutions are outcomes of the publics’ frustration at the deteriorated social, economic, and political conditions of their countries.

On December 2010, the first spark of the Arab Spring revolutions occurred in Tunisia due to citizens’ struggle with high unemployment and declining standards of living. Citizens’ unrest with the existing regime was the cause of the “Tunisian Revolution”, specifically after the death of an unemployed Tunisian citizen who was humiliated and banned from working as a street vendor for a living. The Tunisian Revolution lasted for approximately one month. There were protests against the ruling government and demands to eliminate high unemployment and corruption, improve standards of living, and create a more democratic regime. The revolution resulted in the overthrow of the government and banishment of the Tunisian president Zain Alabidin Ben Ali.

A Tunisian inspired revolution erupted early 2011 in Egypt after a labor strike and a young citizen’s suicide due to his poor economic circumstances. Anti-government protests rose to overthrow the existing regime and to end the 30 year presidency of Hosni Mubarak. The government attempted to suppress the protesters by cutting social media networks and mobile connections. These actions angered the Egyptian population and created violent battles between regime supporters and protesters. The struggles continued for 18 days and ended with the Egyptian army allying itself with the protesters. The Mubarak government collapsed, and the president was imprisoned. Soon after the regime was overthrown, the Mohamed Morsi was democratically elected as the new president of Egypt. However, Egypt erupted in protests again in 2012. Massive demonstrations against the Muslim Brotherhood president arose because he declared a temporary constitution that had limited popular support. President Morsi was ousted, and President Abdul Fatah Elsisi was elected as the new and current president of Egypt.

Similar rebellions against autocratic governments occurred in Libya and Yemen during early 2011. Violent battles started in the two countries as a result of the arrest of human rights activists. The months-long armed struggles in Libya and Yemen overthrew the ruling governments, but civil wars continue in both Libya and Yemen due to unresolved political issues.

During this period, major protests against the governments of Algeria, Bahrain, Morocco, Sudan, and Jordan took place to demand better standards of living and improved delivery of health services and education. However, political reforms were only achieved in Morocco and Jordan through constitutional amendments and the holding of democratic elections, respectively. In the case of Bahrain, protesters called for political freedom and respect of their rights. In February 2012, protesters intensified their demands, but they were confronted by national security forces. Eventually the king of Bahrain declared an emergency and sought help from the other GCC countries. This conflict resulted in political unrest in the country and civil tension between Bahrainis from different Muslim parties.

The most severe case of the Arab Spring civil uprising is the case of Syria which caused ongoing civil war and a massive destruction of the country. The Syrian revolution against the existing Ba’athist government and President Bashar Al-Assad started in early 2011 due to the autocratic and corrupt system of governance. Also, the assault and arrest of a Syrian citizen and the abuse of the group of children revolting against the government enraged much of the public. As a result, severe conflicts occurred between government advocates and anti-government protesters in several districts in Syria. The Syrian army intervened to suppress the conflict and the Free Syrian Army emerged to fight back. Bloody battles continued between the two armies and caused an ongoing civil war in Syria. The civil war killed hundreds of thousands of Syrian civilians and displaced approximately five million refugees since the beginning of the war (UNHCR, Citationn.d.).

2.2. The economic consequences of the Arab spring

Political turmoil has both short and long-term economic impacts on affected countries and their surrounding regions. Economic analysts have found that Arab Spring uprisings caused a downturn in countries’ economic activities during the unrest and the immediate post-revolutionary period. They also have found that political instability in Arab countries has had a negative impact on key macroeconomic indicators such as the risk of recession, sluggish growth during the economic recovery, and a more difficult business environment (Elbargathi & Al-Assaf, Citation2019; Hanafy & Marktanner, Citation2019; Khandelwal & Roitman, Citation2013–69; Masetti et al., Citation2013; Sidamor et al., Citation2016).

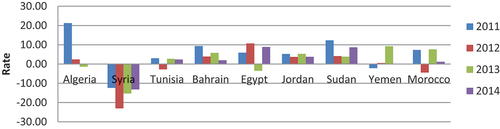

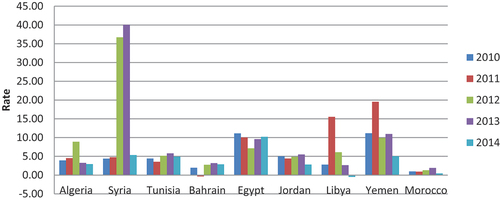

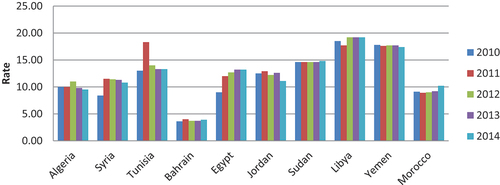

Appendix (A) shows different findings Figure shows the annual growth rate of GDP per capita for selected Arab Spring countries. As expected, Syria has experienced the most severe case of negative GDP growth rate during this period. The other Arab Spring countries experienced at least one year of negative GDP growth. The data show that Algeria in suffered through a recession in 2013 and 2014, Tunisia and Morocco in 2012, Egypt in 2013, and Yemen in 2011. Figure (A2) describes the average annual growth rate of inflation in Arab Spring countries. It shows a severe case of high inflation in Syria during the years 2012 and 2013. Other countries such as Egypt, Libya, and Yemen also had high rates of inflation exceeding 10% throughout the years of political instability. Figure shows the rate of unemployment. It remains at high levels in most of the Arab Spring countries except Bahrain. The data also indicate that job growth was anemic in most Arab Spring countries.

3. Literature review

Historical and recent literatures are rich with studies emphasizing the importance of political and institutional factors in determining the level of foreign direct investments. Schneider and Frey (Citation1985); Singh and Jun (Citation1995); Chan and Gemayel (Citation2004); Busse and Hefeker (Citation2007); Bokhari et al. (Citation2021); Bakari et al. (Citation2013); Bouchoucha and Ben Ammou (Citation2015) empirically show the significance of political instability in determining the level of foreign direct investment inflows in developing countries; with Chan & Gemayel (Citation2004); Bouchoucha and Ben Ammou (Citation2015) concentrating on the MENA region. Moreover, Baklouti and Boujelbene (Citation2020), Bénassy-Quéré et al. (Citation2005); Naude and Krugell (Citation2007); Ramirez (Citation2010); Mohamed and Sidiropoulos (Citation2010) emphasize the importance of countries’ institutional factors in determining FDI inflows in developing countries in general (Bashir, Citation1999). This has been confirmed by the study of Mohamed and Sidiropoulos (Citation2010) in the MENA countries as well.

Studies on the impact of political risk on FDI inflows have received large attention from empirical researchers because it plays such an important role in determining the outlook of potential foreign investors. Brada et al. (Citation2004) find that political instability resulting from domestic and international conflicts is associated inversely with FDI inflows in the case of Central Europe and the Balkan region. Simultaneously, political reforms have a positive impact on FDI inflows into those counties. Karifa-Schneider et al. (Citation2010) empirically show that low level of political risk is positively associated with FDI inflows in 33 developing and emerging countries. Goswami and Haider (Citation2014) investigate the risk of governance failure, cultural conflict, and partner’s attitude in hindering FDI inflows for a group of developing and developed countries using pooled OLS and fixed effect techniques. The findings show that cultural conflicts and partner’s attitude are significant factors in hindering FDI inflows into the countries, and interestingly, governance failure is seen to be encouraging FDI under the fixed effect assumption. Baek and Qian (Citation2011) find that political risks affect FDI inflows for developed and developing countries in different ways, but high levels of democracy and a favorable investment profile are the common political characteristics that attract FDI in developed and developing countries. Also, they find that since the September eleventh attacks, political violence has been an important factor in determining foreign investments decisions, particularly in developed countries. Vadlamannati (Citation2012) uses micro level data for US multinational companies investing in 101 developing countries to assess the impact of political instability on the US foreign investments. The author finds that lower political risk at the host country is associated with greater US multinational FDI and a higher rate of return. Interestingly, Hraiba et al. (Citation2019) also find that political risk (including the Arab Spring) negatively affected the outward flow of FDI from countries affected directly or indirectly by this upheaval.

Other studies investigate the relationship between the quality of institutions and corruption affect FDI. Bissoon (Citation2011) investigates the role of good governance and quality of institutions for attracting FDI in a group of 45 developing countries in Asia, Africa, and Latin America. Using univariate OLS estimation technique, the author concludes that the quality of institutions composed of regulatory quality, control of corruption, and political stability within the host country has a highly significant positive impact on FDI inflows. Gangi & Abdulrazak (2012) study the impact of good governance on foreign investments decisions in 50 African countries using pooled OLS, fixed, and random effect techniques. They find that among the World Bank’s governance indicators, the institutional factors are significant in determining the level of FDI in the African countries. Similarly, Wernick et al. (Citation2014) find a direct impact of the World Bank’s governance indicators on FDI inflows in a sample of 53 African countries. In another study by Kayani and Ganic (Citation2021), the direct relationship is found between some of the institutional factors and FDI flows for the case of China. However, due to the political system in China which relays on one-party government, the political stability variable turns to have no effect on FDI. Enora and Chiu (Citation2016) also present findings which support the connection between good governance and growth for the Middle East and North Africa. This long-term institutional analysis is confirmed by the working paper of Cobham and Zouache (Citation2015).

With regards to the relationship between corruption and FDI, Habib and Zurawicki (Citation2002) find a negative relationship between corruption and FDI inflows. Similarly, Quazi (Citation2014) examines the effect of corruption on FDI inflows in East Asia and South Asia by taking into account the two opposing hypotheses. The first is the “grabbing hand” hypothesis, which states that corruption depresses FDI through by increasing uncertainty and transaction costs. The second is the “helping hand “hypothesis, which states that corruption facilitates FDI under the conditions of weak regulations. The findings support the “grabbing hand” hypothesis. Corruption deters FDI inflows to the countries under study. Interestingly, Egger and Winner (Citation2005) support the “helping hand” hypothesis by finding a positive long-run relationship between corruption and FDI stock for a group of 73 developed and developing countries. That is due to investors’ ability to avoid restrictive laws and regulations under the control of a corrupt government. Similarly, Haksoon (Citation2010) find that countries with relatively corrupt governments and low level of democracy attract more FDI.

As with the study of the impact of corruption, investigations examining the relationship between democracy and FDI yield mixed and contradicting results. For Example, a study by Jensen (Citation2003) empirically examines the impact of political regimes on FDI inflows using pooled OLS technique, and conclude that the more democratic the political system, the more the attraction of FDI inflows. Similarly, Madani and Nobakht (Citation2014) find the same result for upper middle income countries. On the other hand, Busse (Citation2003) studies the causal relationship between FDI and democracy for a sample of 69 developing and emerging market economies and gets inconclusive results because the findings differ from one period to another. Similarly, Molaie and Ahmadi (Citation2013) find a positive impact of democracy on FDI inflows in developed countries but a negative relationship in developing countries for a sample of 138 countries. By using spatial econometrics techniques, Mathur and Singh (Citation2013) find that countries with more democratic regimes attract smaller inflows of FDI.

Several empirical studies concentrate on the case of the MENA region due to its exposure to numerous political shocks and instabilities throughout the decades. Historical studies as Kassicieh and Nassar (Citation1983) conclude that the Iran–Iraq war had a slight negative impact on the investment activities of MNCs in the major oil producing gulf countries. Meon and Sekkat (Citation2004) conclude that the MENA countries’ low attractiveness of FDI is due to the deterioration of the quality of institutions within the region. Similarly, Daniele and Marani (Citation2006) empirically find a negative relationship between quality of institutions and FDI inflows in the MENA region, which is a source of weakness in attracting FDI in comparison to other countries such as Eastern European countries, China, and India. Samimi et al. (Citation2013) find a bridged relationship between good governance and FDI in a sample of 16 MENA countries. Better governance positively affects the financial development of the country which in turn influences the level of FDI inflows. Al-Khouri (Citation2015) studies the impact of political risk on foreign direct and indirect investments in 16 MENA countries. Using GMM estimation technique, the author finds a significant impact of law and order, ethnic tension, and internal conflicts in FDI inflows into the countries. Alshubiri (Citation2022) finds that political a negative relationship between political stability and FDI inflows across GCC region.

Other researches take into account the Arab Spring in studying the relationship between political factors and FDI in MENA countries. Burger et al. (Citation2013) study the effect of Arab Spring on the performance of different economic sectors across the MENA countries. Using OLS estimation for data related to Greenfield investments in MENA countries, the study finds that the Arab Spring is negatively correlated with investments in MENA countries’ manufacturing sectors. Similarly, Bouyahiaoui and Hammache (Citation2014) statistically study the performance of FDI into the MENA region under the conditions of the Arab Spring. The authors conclude that political shocks in Egypt, Tunisia, Libya, and Yemen, as well as the unresolved political tension in the Mediterranean countries, Iraq, Iran, and Bahrain are major challenges that divert FDI away from the MENA region. According to the survey conducted by the Multilateral Investment Guarantee Agency on the impact of Arab Spring on FDI in MENA region, Barbour et al. (Citation2012) find a negative relationship between political instability and the future attraction of FDI. Our study adds to this literature by placing the impact of the Arab Spring on FDI in a broader historical context. By examining data over a longer time period, we are able to get more robust results.

4. Data description

A summary of data specifications is provided in Appendix (B). This study uses annual data covering the period (1980–2014) for five countries representing the Arab Spring turmoil in the MENA region. These countries are Algeria, Bahrain, Egypt, Syria, and Tunisia. Selecting such countries across the MENA region is based on the severity of the political turmoil during the 2011–14 period on the county’s wellbeing as well as on data availability for each country. Data for the dependent variables used in the different specifications which are FDI inflows and FDI stock are obtained from the World Bank database. With regards to the independent variables, the study includes real GDP, exchange rate, inflation rate, openness to trade, and school enrollment. Data for these variables are obtained from the World Bank database and International Financial Statistics published by the IMF. The indicators of political instability, which are a government crisis index, factionalism, and democracy index, are used in the estimated model interchangeably at the two specifications. The data for factionalism is obtained from the Polity IV Project (Marshall et al., Citation2015). The Government crisis index is obtained by Cross National Time Series Data (Banks & Wilson, Citation2015). The Democracy index is represented by the DEMOC variable in the Polity IV Project (Marshall et al., Citation2015).

5. Methodology

The theoretical formation of determinants of FDI depends on different economic theories. Specifically, these include Heckscher—Ohlin theorem, international capital inflows, and portfolio management (Kayani & Ganic, Citation2021). Particularly, the determinants of FDI is well related to the theory of portfolio management which identifies factors affecting the movements of FDI flows at a country specific characteristics (Markowitz, Citation1959; Tobin, Citation1958). The estimated models in this study uses panel regression techniques such as pooled OLS, fixed effect, and random effect. The Hausman test is also used to select between the findings of fixed effects and random effects. The estimated model in this study closely follows the work of Del Bo (Citation2009) for studying the impact of political risk and exchange rate volatility on FDI in a number of developed and developing countries. The explanatory variables that are adopted from the study are real GDP, openness to trade, gross enrollment in primary education, exchange rate, and political risk. However, to be consistent with the source of political instability at the Arab Spring countries, which are all caused by protests against ruling governments, the variable institutional index, indicating political risk in the original model, is replaced by the government crisis index. Also, due to the fundamental nature of a host country’s price level as a main determinant of country’s macroeconomic position, an inflation rate variable is added to the model such as in the study of Brada et al. (Citation2004).

Thus, the model used to study the impact of political instability on FDI inflows at Arab Spring countries is as follows:

The dependent variable represented by “FDI” measures the inflows of foreign direct investment. The variable “GDP” indicates the size of economy in the host country and is measured by the real GDP; the variable “Exchange Rate” denotes the currency volatility in nominal rates; the variable “Trade Openness” refers to how far the economy is open to trade and is measured by the total of imports plus exports in nominal terms divided by GDP; the factor “School Enrollment” denotes the education equality in the country measured by primary school enrollment in the country; “Inflation rate” measures changes of the Consumer Price Index (CPI); the “Political Instability” variable represents the political risk indicator in the country which is measured by the government crisis index.

Explanatory variables in the above model are classified into three groups. These include economic factors such as real GDP, openness, exchange rate, and inflation rate. While the real GDP and trade openness are positively related to FDI, exchange rate volatility and inflation rate are expected to negatively affect FDI. Second, the social factor which represents the quality of education is expected to have a positive relationship with FDI attraction. This social factor is measured by the primary school enrollment rate. Finally, the political factor represented by the political instability index is expected to negatively affect FDI.

Since the model is estimated using two different specifications, the model under the second specification is estimated by replacing the dependent variable FDI inflows with FDI stock which measures the volume of FDI. Political Instability is estimated by using three different variables interchangeably which are a dummy variable “Arab Spring”, democracy index, and factionalism. The dummy variable “Arab Spring” indicates the epoch of the political turmoil which started in year 2011 onwards to 2014. The variable democracy index is chosen to assess the net impact of democracy score on FDI volume. The variable factionalism, which represents partisan conflicts occurring at Arab Spring countries to take over the leadership, is used to examine its impact on FDI volume. All other variables in the model remain unchanged.

6. Empirical results

Table (1) in Appendix (C) displays the summary statistics for the estimated variables used in the study. In Table (2), findings of the benchmark model are shown using pooled Ordinary Least Square (OLS), fixed effect, and random effect regressions. In order to control for concerns such as heterogeneity and lack of normality assumptions, all regressions are estimated with White robust standard errors.

Through the three regression methods used in Table (2), all the estimated coefficients for the determinants of FDI inflows in the Arab Spring region are statistically significant and show the expected signs except for inflation rate. Findings show that real GDP growth, exchange rate volatility, trade openness, school enrollment, and government crisis are the main determinants of FDI inflows across the Arab Spring countries. These outcomes are robust to different specifications using fixed and random effect testing methods.

As far as macroeconomic factors (real GDP, exchange rate, trade openness, and inflation rate), findings show that real GDP and trade openness are positively affecting FDI inflows across the Arab Spring region. On the other hand, results show that inflation pressure has no impact on movements of FDI in this region. With regards to the social indicator represented by primary school enrollment in the country, findings show that the variable school enrollment is positively related to FDI movements. This indicates that foreign investors give an important role for education when deciding to invest into the Arab Spring region. This is crucial especially when attracting skilled and educated labor from the job market. Very importantly, the variable of political instability represented by government crisis index appears to be statistically significant with a negative impact on FDI inflows across Arab Spring region. This result supports the findings of Burger et al. (Citation2013); Bouyahiaoui and Hammach (Citation2014); Chan and Gemayel (Citation2014); Bouchoucha and Ben Ammou (Citation2015).

According to Table (3), a Hausman test is implemented to choose the suitable estimated model between fixed effects and random effects. The test supports the use of fixed effect technique as the Prob>chi2 is equaled to 0.0002 which is less than 0.05.

Accordingly, findings will be interpreted based on the fixed effect approach in Table (2). Thus, explanations for the significant estimated coefficient of economic factors include real GDP, exchange rate volatility, and trade openness. The estimated coefficient for real GDP is shown to be statistically significant with a positive sign at the 1 percent level. This finding indicates that higher economic activities across Arab Spring countries lead to more FDI inflows into these countries. Specifically, finding states that when real GDP increases by 1 percent, FDI inflows increase by 4.7 percent. This finding is consistent with the location advantage hypothesis of FDI. On the other side, the estimated coefficient of exchange rate volatility appears to be statistically significant with a negative influence on FDI at the 1 percent level. This result is supported with the findings of Del Bo (Citation2009) which finds a negative impact of exchange rate volatility on FDI attraction in a number of developed and developing countries. On average, the higher the exchange rate volatility of the Arab Spring countries by 1 percent, the lower the FDI inflows by 1.4 percent over time. This result is consistent with the theoretical aspect that FDI dependents on costs of operations. Therefore, the higher the volatility of price levels in host countries, the more the risk for foreign firms to invest. As for the trade openness variable, the estimated coefficient is statistically significant at 1 percent level using the fixed effect approach. Therefore, the increase of trade openness factor by 1 percent leads to a 7.5 percent increase in FDI inflows across Arab Spring region.

With respect to the social indicator, the estimated coefficient of the education variable represented by primary school enrollment appears to be statistically significant at 1 percent level with a positive influence on FDI inflows. This can be interpreted as a 1 percent increase in school enrollment rate would lead to 8.2 percent increase in FDI inflows to the Arab Spring region. Such finding is consistent with the findings of Goswami and Haider (Citation2014) that social infrastructure indicated by primary school enrollment has a positive influence on FDI inflows in 16 OECD and non-OECD countries. Also, it is consistent with the result of Brada et al. (Citation2004) as quality of education have a positive impact on FDI inflows in European countries in transition.

As for the political factor, the estimated coefficient of the political instability is statistically significant at the 1 percent level with a negative sign. This result is highly significant and consistent using pooled OLS and fixed effects approaches. This finding supports the hypothesis of Lucas (Citation1990) that political risk is the only factor that contributes to the limitation of capital transfers between countries. Also, it is consistent with the more recent empirical studies of political instability and FDI inflows such as Goswami and Haider (Citation2014); Del Bo (Citation2009); Naude and Krugell (Citation2007) which conclude a negative impact of government instability, poor quality of institutions, and political risk in attracting FDI, respectively. This finding shows that Arab Spring countries that suffer from weak political systems experience less FDI inflows on average; a result that is consistently robust to different specifications of OLS, fixed, and random effects. In terms of the estimated quantitative impact of the political instability impact on FDI, the estimated coefficient can be explained as a 1 percent increase in the political instability index leads to a 6.3 percent reduction in the FDI inflows across the Arab Spring region.

In order to achieve more robustness, the study re-tests the estimated model using different specifications in Table (4) at which the dependent variable is replaced by the FDI stock, whereas the political instability factor is replaced interchangeably by a dummy for the Arab Spring period (starting from year 2011 up to 2014), democracy index, and factionalism index. The model is estimated using the appropriate fixed effect approach. Notably, the Arab Spring dummy reflects the recent revolution in the Middle East region that started in year 2011. Findings show that the Arab Spring dummy is significantly affecting the FDI stock in this region with a negative sign.Footnote2 For the estimated quantitative impact, the influence of the Arab spring instability during the period from 2011 to 2014 was estimated to make FDI lower by 12.7% than the FDI stocks for the period prior to 2011.

Although the factor of democracy index is not statistically significant, its sign turns out to be positive indicating that higher democracy level in this area may lead to higher FDI. Surprisingly, the factor of factionalism which indicates an example of a separated society within the country that has not been able to promote institutions for democracy has a positive relationship with the FDI stock. The result suggests that the higher the degree of factionalism for Arab Spring countries, the higher the probability for attracting FDI in that region. For the estimated quantitative impact, a 1 percent increase in the degree of factionalism index leads to a 0.1 percent increase in the FDI stocks across the Arab Spring region. This finding may indicate that factionalism is associated with a greater degree of corrupt favorable treatment. The finding is consistent with the study of Lucas (Citation1990) as he finds that countries facing high level of corruption have promoted higher flows of FDI. Moreover, empirical studies such as Egger and Winner (Citation2005); Haksoon (Citation2010) show support to the hypothesis of corruption being a “helping hand” to promote FDI due to the possibility to pass constraints under corrupted regimes.

7. Conclusion

This study investigates the impact of political instability on FDI movements across the Arab Spring region. Specifically, the paper investigates the determinants of FDI focusing on the influence of political instability index across the Arab Spring region, namely Egypt, Libya, Syria, Tunisia, and Yemen. The study tests predictions of the model using yearly data for 1980 to 2014. Findings of the study reveal that economic factors, social factors, and political factors are important determinants of FDI movements in the Arab Spring region. Real GDP and trade openness are directly influencing FDI inflows to the region; whereas exchange rate volatility is inversely related to FDI inflows. The social factor is important in attracting FDI as well. This is represented by education quality as foreign investors feel more attracted when the education levels are higher in this region. On one hand, the findings of this paper support other studies such as Burger et al. (Citation2013); Bouyahiaoui and Hammach (2013); Chan and Gemayel (Citation2014); Bouchoucha and Ben Ammou (Citation2015) that conclude that political instability leads to less FDI in the MENA region. The study provides evidence that political unrest is a crucial component to affect and weaken the flows of FDI into Arab Spring countries. Importantly, these findings show that the recent political instability of the Arab Spring has an inverse influence on attracting direct investments into these countries.

This paper demonstrates that it is important to understand the influence of political dynamics on FDI in the Arab Spring region. It is shown that the political system in the Arab Spring region is harmful to the development of the economy. Long run sustainable economic policies are needed to stabilize economic activities so that the spillover from negative political effects may be isolated. In addition, no doubt that the political settings across Arab spring countries require to separate any political shocks from the process of economic development. Based on the findings, political instability caused distortion in FDI flows though influencing the foreign investors’ confidence causing a panic to the financial system and macroeconomic fundamentals. Therefore, improving the political quality and institutions may support the environment of doing business which eventually boost more FDI flows. This is can be implemented through establishing a policy responsiveness mechanism based on a time and action to response to political shocks by taken economic policies and regulations needed.

Future studies should take into consideration the inclusion of more variables to provide more explanation of the behavior of the FDI movements in the Arab Spring region. For example, future research could use UNCTAD’s world investment and trade data to study the linkages between FDI and the trade balance under the circumstances of political instability in the MENA region in general and the Arab Spring countries in particular.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Nayef AlShammari

Nayef Alshammari is Associate Professor of Economics at Kuwait University. He has taught at Sciences Po’s Paris School of International Affairs (PSIA) in France. He previously served as Associate Dean of Student Affairs at Kuwait University, and worked as a Research Fellow at American University. He has also worked as Assistant Manager of the Economics Research Department at the Central Bank of Kuwait. His research interests include macroeconomics, with a focus on political and economic stabilization policies. He collaborates actively with other researchers in diverse disciplines of economics, researching Arab spring economies, bilateral trade, government intervention effectiveness, and FDI.

John Willoughby

John Willough by is Professor of Economics at American University in Washington, DC. He has taught at the American University in Cairo, the American University of Sharjah, and Zayed University in Dubai. His research on the MENA region has focused on the labor migration systems of the GCC countries. In addition, he has explored the role that increased female labor participation in the region might begin to limit (although not halt) inflows of labor from South Asia. His recent work with Professor Nayef al Shammari has focused on the links between political unrest and economic outcomes.

Mariam S. Behbehani

Mariam Behbehani is a research associate at the Techno-Economics department at Kuwait Institute for Scientific Research (KISR). She is taking a role as both task leader and task member in implementing a variety of socio-economic research projects in the fields of public policy and development strategies. She also assists KISR’s other divisions in implementing the economic and financial feasibility analysis related to their fields. Mariam has completed her MSc. in economics studies in 2019 from the University of Edinburgh (Scottish Graduate Program in Economics). She also earned an MA in Applied International and Financial Economics from Kuwait University in 2014.

Notes

1. Data is obtained from UNCTAD’s statistical database, and it includes data for FDI inflows, stock, and total trade for 22 Arab League States. Data for FDI stock for Iraq is unavailable for the years (1998–2002). Trade balance excludes data for the countries Comoros, Iraq, and Lebanon due to large deficiencies within the datasets.

2. Arab Spring dummy takes the value one if the year is from 2011 and above and zero otherwise.

References

- Al-Khouri, R. (2015). Determinants of foreign direct and indirect investment in the MENA region. Multinational Business Review, 23(2), 148–17. https://doi.org/10.1108/MBR-07-2014-0034

- Alshubiri, F. (2022). The impact of the real interest rate, the exchange rate and political stability on foreign direct investment inflows: A comparative analysis of G7 and GCC Countries. Asia-Pacific Financial Markets, 29(3), 1–35. https://doi.org/10.1007/s10690-022-09360-0

- Alsoudi, D. A. (2014). The impact of Arab spring on the political future of the muslim brotherhood in the middle east: Jordan as a case study. Journal of Islamic Thought and Civilization, 4(1), 01–29. https://doi.org/10.32350/jitc.41.01

- Baek, K., & Qian, X. (2011). An analysis on political risks and the flow of foreign direct investment in developing and industrialized economies. Economics, Management, & Financial Markets, 6(4), 60–91.

- Bakari, H. R., Chamalwa, H. A., & Jackson, S. Y. (2013). Determinants of Foreign Direct Investment (FDI) inflows to Nigeria (1970-2010). IOSR Journal of Mathematics (IOSR-JM), 9(1), 24–35. https://doi.org/10.9790/5728-0912435

- Baklouti, N., & Boujelbene, Y. (2020). An econometric study of the role of the political stability on the relationship between democracy and economic growth. Panoeconomicus, 67(2), 187–206. https://doi.org/10.2298/PAN170308015B

- Banks, A. S., & Wilson, K. A. (2015). Cross-nationaltime-series data archive ( Databanks International). https://www.databanksinternational.com/

- Barbour, P. A., Economou, P., Jensen, N. M., & Villar, D. (2012). The Arab spring: How soon will foreign investors return?. Vale Columbia Center on Sustainable International Investment.

- Barro, R. J. (1991). Economic growth in a cross section of countries. The Quarterly Journal of Economics, 106(2), 407–443. https://doi.org/10.2307/2937943

- Bashir, A. M. (1999). Foreign direct investment and economic growth in some MENA Countries: Theory and evidence. Topics in Middle Eastern and North African Economies, 1.

- Bénassy-Quéré, A., Coupet, M., & Mayer, T. (2005). Institutional determinants of foreign direct investment. CEPII, CEPII, Working Paper No 2005–05.

- Bissoon, O. (2011). Can better institutions attract more Foreign Direct Investments (FDI)? Evidence from developing countries. International Conference on Applied Economics, 11, 59–70.

- Bokhari, S. A. A., Aftab, M., & Shahid, M. (2021). Political instability and inward foreign direct investment: The perspective of government corruption from an emerging economy. Industry Promotion Research, 6(4), 69–81.

- Bouchoucha, N., & Ben Ammou, S. (2015). Political and institutional determinants of foreign direct investment: An application for MENA region countries. International Journal of Science and Research (IJSR), 4(8), 1866–1871.

- Bouyahiaoui, N., & Hammache, S. (2014). The impact of country risk on foreign direct investment in the MENA region. Economics, Commerce and Trade Management: An International Journal (ECTIJ), 1(1).

- Brada, J. C., Kutan, A. M., & Yigit, T. M. (2004). The effects of transition and political instability on foreign direct investment inflows: Central Europe and the Balkans. ZEI - Center for European Integration Studies, University of Bonn, ZEI working paper, No. B 33-2004.

- Burger, M., Ianchovichina, E., & Rijkers, B. (2013). Risky business: Political instability and greenfield foreign direct investment in the Arab World. The World Bank, Policy Research Working Paper 6716.

- Busse, M. (2003). Democracy and FDI. Hamburg Institute of International Economics, HWWA Discussion Paper 220.

- Busse, M., & Hefeker, C. (2007). Political risk, institutions and foreign direct investment. European Journal of Political Economy, 23(2), 397–415. https://doi.org/10.1016/j.ejpoleco.2006.02.003

- Butler, K. C., & Joaquin, D. C. (1998). A note on political risk and the required return on foreign direct investment. Journal of International Business Studies, 29(3), 599–606. https://doi.org/10.1057/palgrave.jibs.8490009

- Chan, K. K., & Gemayel, E. R. (2004). Risk instability and the pattern of foreign direct investment in the middle east and north africa region. International Monetary Fund. IMF Working Papers, 4(139), 3. IMF Working Paper: WP/04/139. https://doi.org/10.5089/9781451856071.001

- Cobham, D., & Zouache, Z. (2015). Economic factors of the Arab spring. Economic Research Forum: Working Paper No. 975. Retrieved September 15, 2022, from https://erf.org.eg/publications/economic-features-of-the-arab-spring/.

- Daniele, V., & Marani, U. (2006). Do institutions matter for FDI? A comparative analysis for the MENA countries. Bridging the Gap: The Role of Trade and FDI in the Mediterranean Naples: MPRA. https://doi.org/10.2139/ssrn.917581

- Del Bo, C. (2009). Foreign direct investment, exchange rate volatility, and political risk. Annual Conference of European Trade Study Group (ESTG), September 7-8, Rome, Italy.

- Egger, P., & Winner, H. (2005). Evidence on corruption as an incentive for foreign direct investment. European Journal of Political Economy, 21(4), 932–952. https://doi.org/10.1016/j.ejpoleco.2005.01.002

- Elbargathi, K., & Al-Assaf, G. (2019). The impact of political instability on the economic growth: An empirical analysis for the case of selected Arab Countries. International Journal of Business and Economics Research, 8(1), 14–22. https://doi.org/10.11648/j.ijber.20190801.13

- Enora, N., & Chiu, I. (2016). The impact of governance on economic growth: The case of middle eastern and North African Economies. Topics in Middle Eastern and North African Economies, 18(3), 126–144.

- Feng, Y. (1997). Democracy, political stability and economic growth. British Journal of Political Science, 27(3), 391–418. https://doi.org/10.1017/S0007123497000197

- Goswami, G. G., & Haider, S. (2014). Does political risk deter FDI inflows? An analytical approach using panel data and factor analysis. Journal of Economic Studies, 41(2), 233–252. https://doi.org/10.1108/JES-03-2012-0041

- Habib, M., & Zurawicki, L. (2002). Corruption and Foreign direct investment. Journal of International Business Studies, 33(2), 291–307. https://doi.org/10.1057/palgrave.jibs.8491017

- Haksoon, K. (2010). Political stability and foreign direct investment. International Journal of Economics and Finance, 2(3), 59–71. https://doi.org/10.5539/ijef.v2n3p59

- Hanafy, S., & Marktanner, M. (2019). Sectoral FDI absorptive capacity and economic growth–empirical evidence from Egyptian governorates. The Journal of International Trade & Economic Development, 28(1), 57–81. https://doi.org/10.1080/09638199.2018.1489881

- Hraiba, A., Ganic, M., & Brankovic, A. (2019). Does the Arab spring wave affect outward Foreign Direct Investment (FDI)? Empirical evidence from the mideast and north Africa. Ekonomski Pregled, 70(3), 411–430. https://doi.org/10.32910/ep.70.3.3

- Jensen, N. M. (2003). Democratic governance and multinational corporations: Political regimes and inflows of foreign direct investment. International Organization, 57(3), 587–616. https://doi.org/10.1017/S0020818303573040

- Karifa-Schneider, H., Matei, I., & MATEI, I. (2010). Business climate, political risk and FDI in developing countries: Evidence from Panel Data. International Journal of Economics and Finance, 2(5). https://doi.org/10.5539/ijef.v2n5p54

- Kassicieh, S. K., & Nassar, J. R. (1983). Revolution and war in the persian gulf: The effect on MNCs. California Management Review, XXVI(1), 88–99. https://doi.org/10.2307/41165052

- Kayani, F. N., & Ganic, M. (2021). The impact of governance on Chinese inward FDI: The generalized method of moments technique. Humanities and Social Sciences Letters, 9(2), 175–184. https://doi.org/10.18488/journal.73.2021.92.175.184

- Khandelwal, P., & Roitman, A. (2013-69). The economics of political transitions: Implications for the Arab Spring. International Monetary Fund, 13(69), 1. https://doi.org/10.5089/9781475569643.001

- Lucas, R. E. (1990). Why doesn’t capital flow from rich to poor countries? American Economic Review, 80(2), 92–96.

- Madani, S., & Nobakht, M. (2014). Political regimes and FDI inflows: Empirical evidence from upper middle income countries. Journal of Finance and Economics, 2(3), 75–82. https://doi.org/10.12691/jfe-2-3-4

- Markowitz, H. (1959). Portfolio selection: Efficient diversification of investments. John Wiley & Sons.

- Marshall, M., Jaggers, K., & Gurr, T. (2015). Polity IV: Dataset user’s manual. Center for Systemic Peace and Societal-Systems Research.

- Masetti, O., Körner, K., Forster, M., & Friedman, J. (2013). Two years of Arab Spring where are we now? What’s next? Deutsche Bank AG DB Research Management 1–15 .

- Mathur, A., & Singh, K. (2013). Foreign direct investment, corruption and democracy. Applied Economics, 45(8), 991–1002. https://doi.org/10.1080/00036846.2011.613786

- Meon, P.-G., & Sekkat, K. (2004). Does the quality of institutions limit the MENA’s integration in the world economy? The World Economy, 27(9), 1475–1498. https://doi.org/10.1111/j.0378-5920.2004.00661.x

- Mohamed, S. E., & Sidiropoulos, M. G. (2010). Another look at the determinants of foreign direct investment in MENA Countries: An empirical investigation. Journal of Economic Development, 35(2), 75–95. https://doi.org/10.35866/caujed.2010.35.2.005

- Molaie, B., & Ahmadi, A. (2013). The effect of democracy, economic stability and political stability on foreign direct investment evidence from 138 world’s countries. Journal of Business & Economics, 4(9), 881–894.

- Naude, W. A., & Krugell, W. F. (2007). Investigating geography and institutions as determinants of foreign direct investment in Africa using panel data. Applied Economics, 39(10), 1223–1233. https://doi.org/10.1080/00036840600567686

- Quazi, R. M. (2014). Corruption and foreign direct investment in East Asia and South Asia: An econometric study. International Journal of Economics and Financial Issues, 4(2), 231–242.

- Ramirez, M. D. (2010). Economic and institutional determinants of FDI Flows to Latin America: A panel study. Trinity College Department of Economics, Trinity College Department of Economics Working Paper 10–13.

- Samimi, A. J., Amiri, A. G., & Rezanejad, Z. (2013). Financial development, FDI and Governance in MENA region. Applied Mathematics in Engineering, Management and Technology, 1(4), 208–212.

- Schneider, F., & Frey, B. (1985). Economic and political determinants of foreign direct investment. World Development, 13(2), 161–175. https://doi.org/10.1016/0305-750X8590002-6

- Sidamor, Z., Lemtaouch, L., & Bensouici, H. (2016). The economic consequences of the political instability in Arab region. Procedia-Social & Behavioral Sciences, 219, 694–699. https://doi.org/10.1016/j.sbspro.2016.05.053

- Singh, H., & Jun, K. W. (1995). Some new evidence on determinants of foreign direct investment in developing countries. The World Bank: International economics department, Policy Research Working Paper 1531.

- Tobin, J. (1958). Liquidity preference as behavior towards risk. The Review of Economic Studies, 25(2), 65–86. https://doi.org/10.2307/2296205

- UNHCR. (n.d.). The UN refugee agency. http://unhcr.org

- Vadlamannati, K. C. (2012). Impact of political risk on FDI revisited—an aggregate firm-level analysis. International Interactions, 38(1), 111–139. https://doi.org/10.1080/03050629.2012.640254

- Wernick, D. A., Haar, J., & Sharma, L. (2014). The Impact of governing institutions on foreign direct investment flows: Evidence from African Nations. International Journal of Business Administration, 5(2). https://doi.org/10.5430/ijba.v5n2p1

Appendix A

Figure A1. Economic growth.

Figure A2. Inflation rate.

Figure A3. Unemployment rate across selected MENA Countries.

Figure A4. Net official assistant and official aid received (% of GDP).

Appendix B:

Data Descriptions

Table B1. Data description of the dependent variables

Appendix C:

Results

Table C1. Summary statistics

Table C2. Benchmark results: pooled sample, time fixed effect, random effect

Table C3. Results using Hausman test

Table C4. Extended results