Abstract

Modern finance theory assumes that the stock market is efficient, and stock prices reflect all available information. However, behavioral finance theory argues that stock prices can be influenced by psychological and emotional factors. This study aims to examine the impact of behavioral finance factors on investment decisions in the Saudi equity markets through the mediating variable of risk perception. An online questionnaire was distributed to 150 individual investors, out of which 134 were returned and ready for analysis. The data is analyzed using structural equation modeling (SEM). The results show that herding, disposition effect, and blue chip bias have a significant positive impact on risk perception. Overconfidence has a significant positive effect only on investment decision making, but not on risk perception. Risk perception is found to be significantly positively related to investment decision making. All four behavioral finance factors have a significant positive indirect effect on investment decision making through risk perception. This study is conducted in a particular cultural context, namely Saudi Arabia, and may not be generalizable to other cultural contexts. Moreover, this study focused only on four behavioral finance factors, and there may be other factors that could impact risk perception and investment decision making. The results highlight the importance of considering an individual’s perception of risk when making investment decisions, as it can significantly impact their willingness to take risks and ultimately affect the performance of their investment portfolio. The results suggest the need for investors to consider their behavioral biases and for advisors and policymakers to develop strategies to mitigate their impact.

1. Introduction

The traditional finance theory assumes that investors always make rational decisions based on complete information, but behavioral finance argues that investors are influenced by their emotions, biases, and cognitive limitations (Almansour & Arabyat, Citation2017). The debate between modern finance theory and behavioral finance theory on the influence of non-financial factors on stock prices is ongoing. Modern finance theory posits that the stock market is efficient and that stock prices reflect all available information, while behavioral finance theory asserts that psychological and emotional factors can impact stock prices (Almansour, Citation2015). The impact of behavioral finance factors on investment decisions has been extensively studied in the scientific community. Researchers have identified a wide range of behavioral finance factors that can influence investment decisions, including biases, emotional biases, social influences, perception of risk, and personality traits (Ahmad, Citation2022; Lather et al., Citation2020; Menon et al., Citation2023). Numerous studies have examined the impact of these factors on investment decisions and have found that they can lead to suboptimal decision making (Goswami et al., Citation2020; Kartini & Nahda, Citation2021; Mahapatra & Mishra, Citation2020; Sharma et al., Citation2021; Singh et al., Citation2016).

Investors exhibit a risk-averse attitude when it comes to investing, preferring a smoother and more stable level of risk tendency (Wildavsky & Dake, Citation1990), risk perception (Hossain & Siddiqua, Citation2022; Putri Pa et al., Citation2022), and risk propensity (Mahmood et al., Citation2011; Vlahovic et al., Citation2021). While an investor’s risk attitude tends to remain stable, their risk perception is dynamic and can change in different situations. Increased risk perception leads to higher transaction frequency and reduced investment in the stock market (S. U. Ahmed et al., Citation2022; Cho & Lee, Citation2006). Due to a low-risk perception, market participants tend to engage in herding behavior, which adversely affects their investment decisions. Herding behavior has a significant impact on the decision-making processes of investors (Madaan & Singh, Citation2019).

The Saudi stock market, known as “Tadawul,” was established in 1985 and has become one of the largest stock markets in the Arab region (Alshammari, Citation2021). It has experienced rapid growth in recent years, reaching a market capitalization of $2.6 trillion by the end of 2022.Footnote1 However, stock market bubbles are notorious for their detrimental effects on investments and the overall economy. In financial economics, a bubble occurs when an asset’s trading price deviates systematically from its fundamental value (S. U. Ahmed et al., Citation2022; Burton, Citation2017). Specifically, a stock market bubble arises when the trading price of an asset surpasses the discounted value of expected future cash flows (Aljifri, Citation2023). Throughout history, various instances of bubbles have been observed, including the Dutch Tulip Mania in 1634, Black Monday in the 1920s, the Dot Com bubble, the Saudi stock market crash in 2006, the subprime crisis in 2008, and the COVID-19 pandemic. The crash of the Saudi stock market in 2006 was primarily attributed to investors’ irrational behaviors. Between 2003 and 2005, the Tadawul All Share Index (TASI) experienced significant growth, reaching its peak on February 25, 2006, before a market collapse ensued. By the end of that year, TASI had lost approximately 65% of its value. During this period, many Saudi investors heavily relied on borrowed funds or had to sell their assets to finance their investments. The loans granted to Saudi citizens saw a substantial increase, reaching a gross balance of US$48 billion (SAR 180 billion) by the end of 2005. These behaviors had severe consequences, particularly for average Saudi families who faced challenges in repaying their loans.

The relevance of this research is evident in emerging markets, specifically the financial markets of Saudi Arabia. This is because behavioral finance biases can have a significant impact on investors’ gains and losses (Parveen et al., Citation2020). For example, the overconfidence bias may lead to high brokerage costs and make investors vulnerable to significant losses due to excessive trading without sufficient financial knowledge. Similarly, the representativeness bias may result in the purchase of overpriced stocks due to the tendency to associate new events with known events. Suboptimal investment decisions are a critical issue that leads to poor returns for investors in stock exchanges (Jaiyeoba et al., Citation2018). In particular, investors tend to overreact to negative news and underestimate the probability of rare events, which can lead to inefficient markets and suboptimal investment decisions (Grable et al., Citation2020; Kim et al., Citation2022). Other examples of behavioral finance factors that have been studied include loss aversion, heuristics, prospect, trust, herding behavior and financial literacy (Ababio, Citation2020; Mouna & Anis, Citation2015; Ossareh et al., Citation2021; Raveendra et al., Citation2018; Stella et al., Citation2022). The financial literacy plays a significant role in shaping investors’ risk perception. When investors possess a higher level of financial literacy, they are better equipped to understand and evaluate the risks associated with investment.

Including the risk perception variable as a mediator is essential to establish the common thread between behavioral finance, risk perception, and investment decision making (S. U. Ahmed et al., Citation2022). Behavioral finance recognizes that individuals’ cognitive biases and emotional responses can influence their investment decision. Risk perception, in this context, serves as a crucial intermediary variable that helps explain how individuals perceive and interpret risks, which subsequently affects their investment decisions. By examining the relationship between risk perception and investment decision making, we gain insights into the psychological mechanisms underlying financial behavior. It allows us to understand how individuals’ subjective evaluations of risk can impact their willingness to take risks and ultimately shape their investment choices. Therefore, by considering risk perception as a mediator, we can uncover the intricate interplay between behavioral factors, risk perception, and investment decision making, providing a comprehensive understanding of the decision-making process in finance.

As far as the authors are aware, there has not been any research conducted on the mediation role of risk perception in the impact of behavioral finance factors on individual investment decisions in the Saudi equity market. The absence of research on this topic is significant because the Saudi equity market has been growing rapidly in recent years, and investors’ decision-making processes play a crucial role in shaping the market’s behavior. Behavioral finance factors have been shown to influence individual investment decisions in various contexts, but it is unclear how these factors interact with risk perception in the Saudi equity market. Therefore, further investigation into the mediation role of risk perception in the impact of behavioral finance factors on individual investment decisions in the Saudi equity market is needed to gain a more comprehensive understanding of the market’s behavior. This knowledge could help investors make more informed investment decisions, and regulators could use it to develop policies that promote a stable and sustainable equity market.

2. Literature review and hypotheses development

Behavioral finance, a branch of finance that explores the influence of psychological factors on financial decision making, reveals a significant limitation in traditional finance models. Almansour (Citation2015) argues that these models inadequately capture the irrational behavior exhibited by investors, resulting in suboptimal investment decisions. To address this shortcoming, behavioral finance theories emphasize the impact of cognitive biases, such as overconfidence, loss aversion, and herd mentality, on investors’ decision-making processes, which can lead to irrational investment choices.

One critical aspect related to investment decision making is risk perception, which pertains to how individuals perceive and evaluate the level of risk associated with an investment. Researchers, such as Bazley et al. (Citation2021), Gonzalez-Igual et al. (Citation2021), and Ventre et al. (Citation2023), have investigated risk perception and highlighted its multifaceted nature, influenced by various factors. These factors encompass individual characteristics, market conditions, and cognitive biases. By considering the influence of behavioral finance biases on risk perception, behavioral finance sheds light on the complexities of investors’ decision-making processes. It emphasizes that individuals’ risk perceptions are not solely determined by objective factors but are also subject to biases and heuristics that may deviate from rational decision making. Thus, the study of risk perception within the framework of behavioral finance provides valuable insights into understanding the cognitive and psychological mechanisms behind investment decisions. The mediating role of risk perception suggests that the relationship between behavioral finance and investment decision making can be explained by the way investors perceive and evaluate risk (Areiqat et al., Citation2019). For example, an overconfident investor may perceive a risky investment as less risky than it actually is, leading to a higher likelihood of making an investment that is not suitable for their risk profile. Alternatively, a loss-averse investor may perceive a low-risk investment as riskier than it actually is, leading to a missed opportunity for investment gains.

The literature on behavioral finance can be categorized into five main strands, each examining different aspects of risk perception and investment decision making. The first strand investigates the impact of herding behavior on risk perception and investment decisions, studies conducted by Balcilar et al. (Citation2013), Dickason et al. (Citation2018), Mundi et al. (Citation2022), Lim et al. (Citation2018), and Zhang et al. (Citation2022) have explored this relationship. The second strand focuses on the effect of the disposition effect on risk perception and investment decisions, researchers such as Richards et al. (Citation2017), Ullah et al. (Citation2020), and S. U. Ahmed et al. (Citation2022) have delved into this area of study. The third strand explores the influence of blue chip stocks on risk perception and investment decisions. Hau (Citation2001), Shiva and Singh (Citation2020), and S. U. Ahmed et al. (Citation2022) are among the scholars who have examined this relationship. The fourth strand centers on the impact of overconfidence on risk perception and investment decisions. Parveen et al. (Citation2020), Wattanasan et al. (Citation2020), and Areiqat et al. (Citation2019) have contributed to the understanding of this phenomenon. Lastly, the fifth strand focuses on the connection between risk perception and investment decisions. Chen et al. (Citation2018), Worawachtanakul et al. (Citation2018), and Wattanasan et al. (Citation2020) are among the researchers who have explored this relationship.

2.1. The effect of herding behavior on risk perception and investment decision

Herding behavior arises from the influence of risk perception on stock returns, as suggested by Balcilar et al. (Citation2013). Many investors tend to follow the crowd or exhibit overconfidence biases when making investment decisions. This herding behavior stems from investors’ low-risk propensity or risk avoidance, driven by their desire to minimize the risk of financial loss (Dickason et al., Citation2018). During herding, individuals who are otherwise rational start behaving irrationally by relying on the judgments of others. This behavior may stem from a lack of investment knowledge or the inclination to follow the opinions and directions of others (Wattanasan et al., Citation2020).

Balcilar et al. (Citation2014) reveal a compelling connection between herding behavior and risk-return dynamics. The authors observed that herding behavior tends to increase during periods of high market uncertainty and volatility. This increased herding behavior amplifies the potential risks associated with investments, as investors are more likely to make decisions based on market sentiment rather than objective risk assessment. Bekiros et al. (Citation2017) examine herding behavior in relation to risk and uncertainty, finding its prevalence in the US stock market. Dickason et al. (Citation2018) find that the relationship between behavior factors and investment performance is significantly mediated by risk perception. Similarly, Mundi et al. (Citation2022) shows that individual differences in risk perception can explain the relationship between overconfidence and investment decisions. Other studies by Lim et al. (Citation2018) and Zhang et al. (Citation2022) find that risk perception mediates the relationship between behavioral finance factors and investment decision making. S. U. Ahmed et al. (Citation2022) find that risk perception does not mediate the relationship between herding behavior and investment decisions. Other studies find a negative association between risk perception and the behavioral biases of individual investors (Areiqat et al., Citation2019; Gonzalez-Igual et al., Citation2021; Hossain & Siddiqua, Citation2022; Zhang et al., Citation2022). Implying that with an increase in the degree of risk perception, the probability of investors confronting behavioral biases diminishes. Therefore, the study hypothesizes:

H1.

There is a significant effect of herding on risk perception

H2.

There is a significant effect of herding on investment decision

H3.

Risk perception mediates positively the effect of herding on investment decision

2.2. The effect of disposition effect on risk perception and investment decision

The disposition effect is a behavioral bias observed in investors, characterized by a tendency to hold onto losing investments for an extended period while selling winning investments prematurely (Richards et al., Citation2017). In essence, it reflects investors’ inclination to retain stocks when prices decline and promptly dispose of them when prices increase, prioritizing the avoidance of realized losses over potential gains (Chang, Citation2020). The impact of the disposition effect is more pronounced in long positions compared to short positions (Madaan & Singh, Citation2019). Ploner (Citation2017) provides strong evidence supporting the existence of the disposition effect in investment behavior.

In a study conducted by Richards et al. (Citation2017), the disposition effect is a bias commonly observed in investment behavior. The disposition effect refers to the tendency of investors to hold onto stocks that have experienced losses for a longer period compared to stocks that have generated gains. This bias is associated with lower investment performance and is more prevalent among investors who have less experience and sophistication. The study emphasizes the use of stop losses as a means to manage susceptibility to the disposition effect. By analyzing the trading records of individual investors in the UK stock market between 2006 and 2009, the study demonstrates that incorporating stop losses into investment decisions effectively mitigates the impact of the disposition effect. Furthermore, the findings indicate that investors who employ stop losses tend to have less experience, and when they do not utilize stop losses, they exhibit a greater reluctance to realize losses compared to other investors. Ullah et al. (Citation2020) focus on behavioral biases in investment decision making, specifically examining the role of the disposition effect. The findings indicate that the disposition effect has a significant and positive impact on investment decisions. The results indicate that the positive moderating role of the overconfidence bias in investment decisions was evident. S. U. Ahmed et al. (Citation2022) find that risk perception does not mediate the relationship between disposition effect and investment decisions. Chang (Citation2020) declares that the disposition effect has a significant influence on investment decision. Grosshans and Zeisberger (Citation2018) find that the disposition has a significant impact on risk perception. Therefore, the disposition effect is found to have a strong direct relationship with investment decisions and risk perception. Therefore, the study hypothesizes:

H4.

There is a significant effect of disposition on risk perception

H5.

There is a significant effect of disposition on investment decision

H6.

Risk perception mediates positively the effect of disposition on investment decision

2.3. The effect of blue chip stocks on risk perception and investment decision

Blue chip stocks are those of well-established companies with a stable history of financial performance. However, investors may exhibit a bias towards these stocks, leading them to make investment decisions based on this perception. Shiva and Singh (Citation2020) investigate the relationship between overconfidence, risk perception, and the blue chip stocks bias. The study find that overconfident investors are more likely to exhibit a bias towards blue chip stocks, but high-risk perception investors are less likely to exhibit this bias. S. U. Ahmed et al. (Citation2022) conducted a study to investigate the relationship between behavioral biases and investment decisions among individual investors in the Pakistan Stock Exchange. Using structural equation modeling and a sample size of 450 questionnaires, the study find that risk perception mediates the relationship between blue chip stocks and investment decisions, but does not mediate the relationship between herding bias, disposition effect, and investment decisions. Lastly, Hau (Citation2001) examine the role of cognitive biases, including the blue chip stock bias, on investment decision making. The study finds that cognitive biases, along with risk perception and other behavioral factors, influence investment decisions, suggesting that these factors play a critical role in investment decision making. Therefore, the study hypothesizes:

H7.

There is a significant effect of blue chip stocks bias on risk perception

H8.

There is a significant effect of blue chip stocks bias on investment decision

H9.

Risk perception mediates positively the effect of blue chip stocks bias on investment decision

2.4. The effect of overconfidence on risk perception and investment decision

Overconfidence is a cognitive bias where investors overestimate their investment abilities and often take unnecessary risks. Parveen et al. (Citation2020), overconfident investors exhibit a positive risk perception and are more inclined towards adopting a risky attitude when making investment decisions. The study highlights that behavioral biases such as herd bias, anchoring, mental accounting, and overconfidence bias can significantly influence the decision-making process of investors. Wattanasan et al. (Citation2020) examine the impact of emotional and psychological factors on investors’ decisions in the securities market, focusing on biases such as conservatism bias, overconfidence bias, availability bias, herding, and level of risk-taking. They find that appreciation had a significant influence on investors’ psychology, followed by reducing tax and income generation. A study by Areiqat et al. (Citation2019) investigate the impact of behavioral finance variables, including overconfidence on stock investment decision making at the Amman Stock Exchange. According to a study, this suggests that their confidence in their abilities leads them to actively pursue investments that carry higher levels of risk. In a study conducted by Abdin et al. (Citation2017), the impact of overconfidence on the investment decisions of individuals was examined. The findings of the study revealed that overconfidence significantly influences investment decision making. This suggests that individuals who exhibit overconfidence tend to make investment choices that are influenced by their exaggerated self-belief in their own abilities. The results showed that overconfidence is one of the most significant behavioral factors affecting investment decisions. The relationship between overconfidence and investment risk taking is, therefore, mediated by perceived risk (Kirchler & Maciejovsky, Citation2002). Therefore, the study hypothesizes:

H10.

There is a significant effect of overconfidence on risk perception

H11.

There is a significant effect of overconfidence on investment decision

H12.

Risk perception mediates positively the effect of overconfidence on investment decision

2.5. The effect of risk perception on investment decision

Several studies have investigated the relationship between risk perception and investment decisions in general. Worawachtanakul et al. (Citation2018) examine the impact of environmental risk perception on investment decisions. The study find that higher environmental risk perception is associated with fewer investment decisions. Wattanasan et al. (Citation2020) explore the association between investment risk perception, financial literacy, and investment behavior in a cross-country study across several European countries. They discover that individuals with high investment risk perception were more likely to exhibit cautious investment behavior, and financial literacy moderated this relationship. Chen et al. (Citation2018) examine how the inclusion of historical risk perception data could improve investment decision making. They find that including historical risk perception data improved the accuracy of predicting investment returns, suggesting that risk perception plays a crucial role in investment decision making. Therefore, the study hypothesizes:

H13.

Risk perception is positively correlated with investment decision

In conclusion, the literature review has shown that risk perception plays a crucial role in the relationship between behavioral finance factors and investment decision making. Risk perception mediates the relationship between various behavioral finance factors such as overconfidence, loss aversion, herding behavior, and anchoring bias. The findings of the reviewed studies suggest that investors need to be aware of their own risk perception and biases when making investment decisions to avoid making irrational investment decisions.

3. Methods

3.1. Population and sample and procedure

Targeting the population refers to the process of selecting a specific group of individuals from whom data will be collected (Hair et al., Citation2015). When analyzing data, people often tend to give more importance to recent patterns while disregarding the underlying characteristics of the population that generated the data (Fama, Citation1998). In this study, the population consists of investors who are directly or indirectly involved in trading stocks in the Saudi stock market. The aim is to assess the overall level of investment behavior within this population and evaluate the presence of behavioral biases in the equity market. The sample size of the study is 150 questionnaires which were given to investors who are currently trading in the Saudi equity market, only 134 questionnaires were completely filled out by individual investors and considered for analysis. This represents a response rate of 89%. Purposive sampling is used to ensure that the sample aligns with the research objectives and can provide valuable insights and information. Researchers continue selecting respondents until data saturation is reached, meaning that additional participants are unlikely to provide new or significant information. By carefully selecting participants who closely match the topic of interest, purposive sampling enhances the trustworthiness of the data and results, thereby improving the overall rigor of the research (Campbell et al., Citation2020). Hence, in this study, purposive sampling is employed to gather data from investors in the Saudi stock market to explore the potential mediating role of risk perception in the relationship between behavioral factors and investment decision making. The data on investors are obtained from stock market brokers who provided information about both male and female investors. An online questionnaire was distributed to the brokers, who then shared it with the investors for data collection.

3.2. Instruments

The questionnaire used in the study contained 45 questions, which were designed to elicit information on a range of factors that may influence investment decisions. The questions were divided into two main categories: demographic information (Table ) and investment behavior factors. The demographic information section included questions on gender, age, education, and experience. The investment behavior factors section included questions on risk perception, herding, disposition effect, blue chip stocks bias and overconfidence. Of the 45 questions, 38 were specifically aimed at measuring the behavioral factors that influence investment decisions. These questions were designed to assess the psychological and emotional factors that may affect an investor’s decision-making process. The remaining 7 questions were focused on measuring the investment decision itself, including the types of investments made and the level of risk involved. The scale used to assess behavioral finance and investment decision dimensions ranged from 1= strongly disagree to 5 = strongly agree (Pompian, Citation2011). The collected data were tabulated and refined using SPSS. Once normality was confirmed, the dataset was utilized for advanced analysis using Structural Equation Modeling (SEM) with AMOS software to test the hypotheses of the conceptual framework.

Table 1. Demographic and Experience Profile of Individuals Involved in the Saudi Equity Market

The sample consists of 84% male and 16% female respondents, the high proportion of male respondents (84%) compared to female respondents (16%) in the study implies that there may be a gender imbalance in the participation of Saudi nationals in the equity market. This finding may reflect the cultural and social norms prevalent in Saudi Arabia, where women are generally underrepresented in the workforce and face cultural barriers in accessing financial opportunities. Such gender disparities may also impact women’s access to investment education and opportunities, ultimately leading to their lower participation in the equity market compared to men.

In terms of age, the result indicates that the majority of respondents, almost half of them (49%), are within the age range of 30–40 years old. This finding implies that the research focused on a relatively young cohort of investors who are at the beginning of their investment journey. This may have implications for the results of the study since the investment behavior of younger investors may differ from that of more experienced investors. For instance, younger investors may have a higher risk tolerance and a longer investment horizon, which can affect their decision-making processes.

In terms of education level, the fact that 73% of the respondents hold a Bachelor’s degree indicates that the study may be more representative of individuals with higher levels of education and training. It is essential to note that individuals with lower levels of education may have a different understanding and approach towards investing in the equity market. In other words, individuals with lower levels of education may have different financial goals, risk preferences, and investment strategies compared to those with higher levels of education. For instance, they may be more risk-averse and prefer safer investment options, such as savings accounts or fixed deposits, rather than investing in the stock market.

The experience level of the respondents is also an important factor to consider when evaluating the findings of the study. The fact that the majority of respondents (87%) have less than 5 years of experience in the Saudi equity market suggests that the study is capturing the behavior of relatively inexperienced investors. Additionally, it is important to note that the Saudi equity market has undergone significant changes and developments in recent years. For example, the opening of the Tadawul to foreign investors in 2015 and the inclusion of Saudi Arabia in the MSCI Emerging Markets Index in 2019 have led to increased international interest and investment in the market. Investors with more experience may have a different perspective and approach towards investing in the market in light of these developments.

3.3. Measurements

The measurement of behavioral finance factors and investment decisions in this study was informed by previous researches that utilized similar questions to assess the variables of interest. The investment decision questions were adapted from Almansour and Arabyat (Citation2017), Khawaja and Alharbi (Citation2021) and Liang and Reiner (Citation2009). The questions pertaining to herding behavior were derived from Almansour and Arabyat (Citation2017), Balcilar et al. (Citation2013), Kumari et al. (Citation2022) and Marjerison et al. (Citation2023). The disposition effect questions were adapted from Adil et al. (Citation2022), Ballis and Verousis (Citation2022), Paraboni and da Costa (Citation2021) and Verma and Verma (Citation2018). The assessment of blue chip stocks questions involved the utilization of 5 items that were adapted from S. U. Ahmed et al. (Citation2022), Chua et al. (Citation2023) and Shiva and Singh (Citation2020). The measurement of overconfidence was derived from Adil et al. (Citation2022), Liang and Reiner (Citation2009), Mushinada and Veluri (Citation2019) and Renu Isidore and Christie (Citation2018), consisting of a total of 7 items. Finally, the measure of risk perception was derived from (Gonzalez et al., Citation2021; Hossain & Siddiqua, Citation2022; Oyekale, Citation2022; Putri Pa et al., Citation2022), comprising a total of 10 items. The specific variables and their corresponding literature sources are presented in Table .

Table 2. Variables and Literature Sources Used for Measurement

4. Data analysis

4.1. Preliminary analysis

Table presents the Cronbach’s alpha coefficients for the measured factors, which indicates the level of reliability for each factor. By conducting this analysis, the study ensured that the collected data was reliable and could be utilized to draw valid conclusions about the behavior factors that impact investment decisions in the Saudi equity market.

Table 3. Results of Measurement Testing

In order to examine the hypotheses outlined in the research model, the study employed structural equation modeling (SEM). First, confirmatory factor analysis (CFA) was performed to assess the measurement model’s quality, including the convergent and discriminant validity of constructs. Subsequently, a structural model was developed to investigate the direct effects of behavioral finance components on investment decisions. Lastly, a mediating model was constructed to examine both the overall and specific indirect effects of risk perception. The results demonstrate that the sample size was adequate for factor analysis, as evidenced by Kaiser-Meyer-Olkin’s (KMO) value of 0.809, surpassing the recommended threshold of 0.5 (Sarstedt et al., Citation2019). This was further confirmed by a significant Bartlett’s test of Sphericity (p < 0.001) (Hair et al., Citation2015).

4.2. Descriptive statistics

In the context of Table , it summarizes the descriptive statistics of six variables that were measured in the study. The mean score for investment decision, herding effect, blue chip stocks, risk perception, and overconfidence were all in the range of moderate to moderately high.

Table 4. Descriptive statistics

The table above shows the descriptive statistics for various factors related to behavior finance and investment decisions in the Saudi equity market. The figures suggest that, on average, the participants in the survey had a moderate level of investment decision, herding effect, disposition effect, and blue chip stocks. However, they exhibited a higher level of overconfidence and risk perception. The skewness and kurtosis values suggest that the figures are slightly skewed and has a moderate level of Peakedness. Overall, the table provides insights into the behavioral finance factors that influence investment decisions in the Saudi equity market.

4.3. Hypotheses testing and discussion

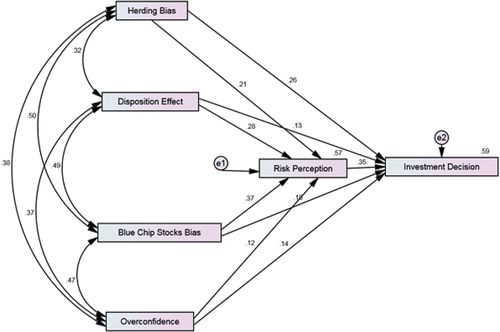

Following the establishment of the measures’ validity and reliability, the study proceeds to test the proposed relationships through a structural model, which is visually represented in Figure . This model serves as a valuable tool for exploring the complex interplay between the behavioral finance factors and their impact on risk perception and investment decision making. By utilizing this model, the study can examine the relationships between the various constructs under investigation, providing a more comprehensive understanding of the factors that influence investment behavior. The goodness-of-fit indices were analyzed, and it was observed that they met the recommended guidelines as suggested by Wang and Wang (Citation2012) (Table ), thereby confirming the appropriateness of the structural model for the data.

Figure 1. Structural model.

Table 5. Testing model fit

Table summarizes the regression results on the direct effect (Panel 1) and indirect effect (Panel 2). Panel 1 shows the results of the direct effect which displays the effect of behavior finance factors on risk perception and investment decision without considering the mediator. Panel 2 shows the results of the indirect effect which displays the effect of behavior finance factors on the investment decision that is mediated by risk perception.

Table 6. Hypotheses confirmation

The findings reveal that herding, disposition effect, and blue chip bias are all associated with a significant positive impact on risk perception, as indicated by their corresponding coefficient values of 0.18, 0.223, and 0.274, respectively. The acceptance of these hypotheses at the 1% and 5% levels of significance, suggesting that these behavioral finance factors can have a significant impact on an individual’s perception of risk when making investment decisions. The positive coefficient values for herding, disposition effect, and blue chip bias indicate that these behavioral finance factors contribute to an increase in risk perception among investors. This means that investors who exhibit these behaviors are more likely to perceive investments as riskier than they may objectively be, potentially leading to suboptimal decision making and portfolio outcomes. The combination of herding behavior and blue chip bias results in a lack of diversification in investors’ portfolios, making them more vulnerable to market downturns and specific risks (Cristiana, Citation2021). The disposition effect leads to missed opportunities for growth as investors hold on to underperforming assets instead of exploring better prospects (Mavruk, Citation2022). These biases also increase sensitivity to market movements, causing reactive decision making based on short-term fluctuations. Furthermore, the concentration in blue chip stocks amplifies losses during market downturns, making portfolios more susceptible to the performance of a few large companies. This result is in line with other studies findings (Areiqat et al., Citation2019; Gonzalez-Igual et al., Citation2021; Hossain & Siddiqua, Citation2022; Zhang et al., Citation2022). Interestingly, the overconfidence demonstrates a statistically significant positive impact on investment decision making, while no significant association is observed between overconfidence and risk perception. This implies that overconfidence does not directly contribute to an augmentation in perceived risk, but it does influence the frequency of investment decisions made by investors. However, the lack of a substantial effect of overconfidence on risk perception suggests that overconfident individuals may possess an inadequate ability to accurately evaluate and acknowledge the risks inherent in their investment decisions. They may tend to underestimate potential downsides or overestimate their competence in managing and mitigating those risks. This result is in line with other study findings (Areiqat et al., Citation2019; Wattanasan et al., Citation2020).

The findings highlight also a noteworthy outcome concerning the relationship between risk perception and investment decision making. The result reveals a significant positive association between risk perception and investment decision making, as evidenced by the coefficient value of 0.442, which is accepted at the 1% level of significance. This implies that individuals who possess a heightened perception of risk are inclined to exercise greater caution when making investment decisions. Delving deeper into this relationship, it becomes crucial to consider the implications for Saudi investors in the context of the Saudi stock market. The significance of risk perception in shaping investment behavior is particularly relevant for Saudi investors who operate within the unique dynamics of the local stock market. Factors such as geopolitical events, market volatility, regulatory changes, and macroeconomic conditions specific to Saudi Arabia contribute to the overall risk landscape (Nekhili, Citation2020; Trabelsi, Citation2019). The significant positive relationship between risk perception and investment decision making carries notable implications for various stakeholders in the Saudi financial landscape. Financial institutions, regulatory bodies, and investment advisors should recognize and address the influence of risk perception on investor behavior. This entails providing comprehensive investor education programs that promote a thorough understanding of risk and its implications, as well as offering appropriate tools and resources for risk assessment and management. Moreover, stakeholders in the Saudi stock market can develop strategies to support Saudi investors in navigating the complexities and uncertainties inherent in the market. This includes facilitating access to timely and accurate information, promoting transparency and disclosure, and fostering a culture of risk aware investing. By aligning their efforts with the cautious investment approach influenced by risk perception, stakeholders can empower Saudi investors to make informed decisions and navigate the Saudi stock market with greater confidence. This result is consistent with the principles of modern portfolio theory, which suggest that investors tend to seek higher returns for higher levels of risk (Worawachtanakul et al., Citation2018). As such, the study highlights the importance of considering an individual’s perception of risk when making investment decisions, as it can significantly impact their willingness to take risks and ultimately affect the performance of their investment portfolio.

The findings also indicate that all four behavioral finance factors have a significant positive indirect effect on investment decision making through risk perception. Specifically, herding, disposition effect, blue chip bias, and overconfidence have indirect effects on investment decisions with coefficient values of 0.622, 0.665, 0.716, and 0.548, respectively. All of these indirect effects are accepted at the 5% level of significance or better. To elaborate further, the results of the study suggest that the impact of behavioral finance factors on investment decision making is not only direct but also indirect through an individual’s perception of risk. This means that behavioral finance factors influence how investors perceive risks associated with their investment decisions, which in turn affects their actual investment decisions. For example, herding behavior can influence an individual’s perception of risk by creating a sense of safety in numbers. Investors may perceive the risk of deviating from the herd as being too high, leading to a lack of diversification in their investment portfolio. The study demonstrates that such herding behavior indirectly affects investment decision making through its influence on risk perception. When investors witness a significant number of individuals engaging in a particular investment strategy or trend, it creates a perception of reduced risk. This perception stems from the belief that if many others are making similar investment choices, the probability of negative outcomes or losses may be lower. Understanding the prevalence and impact of herding behavior in investment decisions can help identify market inefficiencies and vulnerabilities. Investors can mitigate herding biases by being aware of the risks and adopting an independent decision-making approach. Policymakers and regulators can design interventions to reduce negative consequences through transparency, investor education, and promoting independent thinking.

Similarly, the result indicates that the disposition effect has a significant indirect effect on investment decisions through risk perception. The coefficient value of 0.665 suggests that for every one-unit increase in the disposition effect, there is a 0.665-unit increase in the likelihood of making an investment decision through the mediating factor of risk perception. This relationship is accepted at the 5% level of significance, indicating a strong statistical relationship. This behavior can lead to a skewed perception of risk as investors tend to overestimate the potential for a recovery in losing investments while underestimating the potential risks associated with winning investments. This, in turn, can lead to more investment decisions based on a flawed perception of risk. The finding suggests that investors who exhibit the disposition effect may perceive risks in a biased manner, which leads them to make investment decisions that are not necessarily aligned with their financial goals or risk tolerance. The disposition effect can distort investors’ perception of risk. Investors exhibiting this behavior often overestimate the potential for a recovery in their losing investments while underestimating the risks associated with their winning investments. This biased perception of risk can lead to more investment decisions based on flawed assumptions. For instance, investors may hold on to losing investments in the hope of a future rebound, even when the rational decision might be to cut losses and reallocate their capital. Conversely, they may prematurely sell winning investments, missing out on potential future gains. These decisions are influenced by the skewed perception of risk caused by the disposition effect.

The result shows that blue chip bias has a significant indirect effect on investment decisions through risk perception. The coefficient value of 0.716 suggests that for every one-unit increase in blue chip bias, there is a 0.716-unit increase in the likelihood of making an investment decision through the mediating factor of risk perception. This relationship is accepted at the 1% level of significance, indicating a strong statistical relationship. Blue chip bias is a phenomenon where investors have a preference for investing in well-established, large-cap companies with a strong brand reputation. This behavior can lead to a biased perception of risk as investors may perceive these companies to be less risky than other investment options, which may not necessarily be the case. As a result, investors may make investment decisions that are not aligned with their risk tolerance or financial goals. The finding suggests that blue chip bias can lead investors to perceive risks in a biased manner, which, in turn, affects their investment decision making. Investors exhibiting the blue chip bias may prioritize investing in these large-cap companies based on their reputation, track record, and perceived stability. However, this bias can result in an imbalanced perception of risk. By predominantly focusing on blue chip stocks, investors may underestimate the risks associated with these investments and disregard other opportunities that may better align with their risk tolerance and financial goals. For example, investors may perceive blue chip stocks as less risky due to their established brand presence, market dominance, and historical performance. This perception can create a sense of safety and stability, leading investors to allocate a significant portion of their portfolio to these stocks. However, this concentration in a particular segment of the market may expose investors to undiversified risks, such as industry-specific risks or the potential impact of adverse events on these companies. By understanding the indirect effect of blue chip bias on investment decision making through risk perception, financial advisors can provide more targeted advice to clients to help them make more informed investment decisions.

The result shows that overconfidence have a significant positive indirect effect on investment decision making through risk perception in the context of the Saudi stock market. This indicates that overconfidence influences how investors perceive risks associated with their investment decisions, ultimately impacting their actual decision-making process. Specifically, the coefficient value of 0.548 with a significance level of 10% indicates that these forms of overconfidence indirectly affect investment decisions through the mediating factor of risk perception. When investors are overconfident, they may perceive risks as being lower than they actually are, leading to a higher likelihood of making investment decisions that may not be adequately aligned with the level of risk involved. For example, an overconfident investor may believe that their stock-picking abilities are superior and that they can consistently outperform the market. This belief can lead them to take on higher levels of risk by investing in more volatile or speculative stocks without fully considering the potential downside. Their overconfidence creates a skewed perception of risk, leading to investment decisions that may not be commensurate with the actual risks present in the market. This overconfidence-driven biased perception of risk can have significant implications for investment outcomes. Investors who are overconfident may engage in excessive trading, have a higher likelihood of making poor investment choices, and experience greater portfolio volatility. This behavior can lead to potential losses in the long run, especially if the investor continues to make investment decisions based on overconfidence rather than objective analysis of the market and individual investments.

By considering the indirect effects of these behavioral finance factors on investment decision making, the study provides a more nuanced understanding of the complex relationships between these factors and risk perception. This understanding is important for financial practitioners and policymakers as it provides insights into how investors make decisions and the factors that influence these decisions. By recognizing the importance of risk perception, practitioners and policymakers can design interventions that better align with investors’ decision-making processes and lead to more optimal investment outcomes.

5. Conclusion, implications, and recommendations for future studies

In conclusion, this study examined the impact of four behavioral finance factors, namely herding behavior, disposition effect, blue chip bias, and overconfidence, on risk perception and investment decision making. The findings suggest that these behavioral finance factors have a meaningful impact on an individual’s perception of risk and investment decision making. Specifically, herding behavior, disposition effect, and blue chip bias were all found to have a significant positive impact on risk perception, whereas overconfidence had a significant positive effect only on investment decision making. Furthermore, the results indicate that risk perception has a significant positive relationship with investment decision making.

Interestingly, the study also found that all four behavioral finance factors have a significant positive indirect effect on investment decision making through risk perception. This suggests that these behavioral finance factors influence how investors perceive risks associated with their investment decisions, which in turn affects their actual investment decisions. Therefore, the study highlights the importance of considering an individual’s perception of risk when making investment decisions, as it can significantly impact their willingness to take risks and ultimately affect the performance of their investment portfolio. It is also important for investors to be aware of their own behavioral biases and to take steps to mitigate their impact on their investment decision making. For example, investors should diversify their portfolio to avoid the negative impact of herding behavior and should develop a disciplined approach to buying and selling investments to mitigate the impact of the disposition effect.

Despite the significant findings and contributions of this study, there are several limitations that should be acknowledged. One limitation is the use of self-reported data, which could be subject to social desirability bias and may not accurately reflect participants’ actual behaviors. Additionally, the study was conducted in a specific cultural context (Saudi Arabia) and therefore may not be generalizable to other cultural contexts. Furthermore, the study only focused on individual investors and did not consider the impact of institutional investors or market trends on investment decision making. Finally, the study only examined the impact of four specific behavioral finance factors and did not consider the impact of other potential factors that could influence investment decision making.

The economic implications of the study’s findings are significant. By highlighting the impact of behavioral finance factors on investment decision making, the study challenges the notion of market efficiency and rational decision making. This implies that financial markets may not always operate efficiently, as investor behavior influenced by biases can lead to mispricing and market inefficiencies. This mispricing can result in economic distortions, affecting resource allocation and potentially leading to market bubbles. Understanding the influence of behavioral biases on investment decisions is crucial for investors, financial institutions, and policymakers to make informed decisions and promote market stability.

The social implications of the study’s findings are noteworthy. Behavioral biases can have widespread consequences for individual investors and society as a whole. When investors succumb to herding behavior or overconfidence, it can lead to suboptimal investment decisions, jeopardizing their financial well-being. This can have broader societal implications, as individuals may suffer financial losses, impacting their overall economic stability and quality of life. By raising awareness of these biases, the study encourages individuals to adopt a more independent and objective decision-making approach. Improved financial literacy and investor education programs can empower individuals to make more informed investment decisions, promoting financial well-being and reducing the potential social costs associated with biased decision making.

The study’s findings have important implications for financial advisors, fund managers, and other professionals in the investment industry. Recognizing the impact of behavioral finance factors on risk perception and investment decision making, these professionals can adapt their strategies and practices accordingly. Financial advisors should educate their clients about the biases inherent in decision-making processes and work towards mitigating their influence. They can emphasize the importance of diversification, disciplined investment strategies, and long-term thinking to counteract biases such as herding behavior, disposition effect, and overconfidence. Fund managers can integrate behavioral finance insights into their investment processes to optimize portfolio construction and risk management. By considering behavioral biases, investment professionals can enhance their clients’ investment outcomes and foster long-term financial success.

Based on the findings of this study, there are several recommendations for future studies in the field of behavioral finance and investment decision making. Firstly, future studies could investigate the impact of other behavioral finance factors on risk perception and investment decision making. This study focused on four behavioral finance factors, namely herding, disposition effect, blue chip bias, and overconfidence. However, there are many other behavioral finance factors that could also impact these variables, such as anchoring, framing, and confirmation bias. Therefore, future studies could investigate these factors and their impact on risk perception and investment decision making. Secondly, future studies could investigate the impact of cultural differences on the relationship between behavioral finance factors, risk perception, and investment decision making. The current study was conducted in a specific cultural context, namely Saudi Arabia. It is possible that the impact of behavioral finance factors on risk perception and investment decision making could differ in other cultural contexts. Therefore, future studies could investigate this issue by conducting cross-cultural comparisons. Thirdly, future studies could investigate the impact of different types of investments on the relationship between behavioral finance factors, risk perception, and investment decision making. The current study focused on stock investments. However, other types of investments, such as real estate or commodities, may have different relationships with behavioral finance factors, risk perception, and investment decision making. Therefore, future studies could investigate the impact of these different types of investments. In addition, it is also suggested that future research endeavors consider the potential role of entrepreneurship spirit in relation to risk factors. This aspect should be further explored in the context of both traditional and modern financial theories, in order to gain a deeper understanding of the relationship between entrepreneurship and risk in financial markets. By addressing these research gaps, future studies could provide a more comprehensive understanding of the factors that influence risk perception and investment decision making, and inform the development of more effective investment strategies and policies. Finally, future studies could investigate the impact of financial education and literacy on the relationship between behavioral finance factors, risk perception, and investment decision making. It is possible that individuals who are more financially educated and literate may be less susceptible to the biases associated with behavioral finance factors. Hence, it is recommended that future studies explore this issue by conducting comparative analyses among individuals with varying levels of financial education and literacy. This research can shed light on the extent to which financial knowledge and literacy influence the relationship between behavioral finance factors, risk perception, and investment decision making. Understanding how individuals with different levels of financial education navigate behavioral biases can provide valuable insights for designing effective educational programs and interventions aimed at improving decision-making abilities and promoting overall financial well-being.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

References

- Ababio, K. A. (2020). Behavioural portfolio selection and optimisation: Equities versus cryptocurrencies. Journal of African Business, 21(2), 145–20. https://doi.org/10.1080/15228916.2019.1625018

- Abdin, S. Z. U., Farooq, O., Sultana, N., & Farooq, M. (2017). The impact of heuristics on investment decision and performance: Exploring multiple mediation mechanisms. Research in International Business and Finance, 42, 674–688. https://doi.org/10.1016/j.ribaf.2017.07.010

- Adil, M., Singh, Y., & Ansari, M. S. (2022). How financial literacy moderate the association between behaviour biases and investment decision? Asian Journal of Accounting Research, 7(1), 17–30. https://doi.org/10.1108/AJAR-09-2020-0086

- Ahmad, M. (2022). The role of cognitive heuristic-driven biases in investment management activities and market efficiency: A research synthesis. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-07-2020-0749

- Ahmed, S. U., Ahmed, S. P., Abdullah, M., & Karmaker, U. (2022). Do socio-political factors affect investment performance? Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2113496

- Aljifri, R. (2023). Investor psychology in the stock market: An empirical study of the impact of overconfidence on firm valuation. Borsa Istanbul Review, 23(1), 93–112. https://doi.org/10.1016/j.bir.2022.09.010

- Almansour, B. Y. (2015). The impact of market sentiment index on stock returns: An empirical investigation on kuala Lumpur stock exchange. Journal of Arts, Science and Commerce, VI(July 2015), 1–28. https://www.researchgate.net/publication/331166420_THE_IMPACT_OF_MARKET_SENTIMENT_INDEX_ON_STOCK_RETURNS_AN_EMPIRICAL_INVESTIGATION_ON_KUALA_LUMPUR_STOCK_EXCHANGE_INTRODUCTION

- Almansour, B. Y., & Arabyat, Y. A. (2017). Investment decision making among Gulf investors: Behavioural finance perspective. International Journal of Management Studies, 24(1), 41–71. https://doi.org/10.32890/ijms.24.1.2017.10476

- Alshammari, T. (2021). State ownership and bank performance: Conventional vs Islamic banks. Journal of Islamic Accounting and Business Research, 13(1), 141–156. https://doi.org/10.1108/JIABR-06-2021-0161

- Areiqat, A. Y., Abu-Rumman, A., Al-Alani, Y. S., & Alhorani, A. (2019). Impact of behavioral finance on stock investment decisions applied study on a sample of investors at Amman stock exchange. Academy of Accounting & Financial Studies Journal, 23(2).

- Balcilar, M., Demirer, R., & Hammoudeh, S. (2013). Investor herds and regime-switching: Evidence from Gulf Arab stock markets. Journal of International Financial Markets, Institutions and Money, 23(1), 295–321. https://doi.org/10.1016/j.intfin.2012.09.007

- Balcilar, M., Demirer, R., & Hammoudeh, S. (2014). What drives herding in oil-rich, developing stock markets? Relative roles of own volatility and global factors. The North American Journal of Economics & Finance, 29, 418–440. https://doi.org/10.1016/j.najef.2014.06.009

- Ballis, A., & Verousis, T. (2022). Behavioural finance and cryptocurrencies. Review of Behavioral Finance, 14(4), 545–562. https://doi.org/10.1108/RBF-11-2021-0256

- Bazley, W. J., Cronqvist, H., & Mormann, M. (2021). Visual finance: The pervasive effects of red on investor behavior. Management Science, 67(9), 5616–5641. https://doi.org/10.1287/mnsc.2020.3747

- Bekiros, S., Jlassi, M., Lucey, B., Naoui, K., & Uddin, G. S. (2017). Herding behavior, market sentiment and volatility: Will the bubble resume? The North American Journal of Economics & Finance, 42, 107–131. https://doi.org/10.1016/j.najef.2017.07.005

- Burton, N. (2017). A History of Financial Crises. In An Analysis of Charles P. Kindleberger's Manias, Panics, and Crashes. https://doi.org/10.4324/9781912281145

- Campbell, S., Greenwood, M., Prior, S., Shearer, T., Walkem, K., Young, S., Bywaters, D., & Walker, K. (2020). Purposive sampling: Complex or simple? Research case examples. Journal of Research in Nursing: JRN, 25(8), 652–661. https://doi.org/10.1177/1744987120927206

- Chang, H.-H. (2020). Application of structural equation modeling in behavioral finance: A study on the disposition effect. In Handbook of financial econometrics, mathematics, statistics, and machine learning (Vol. 4). https://www.scopus.com/inward/record.uri?eid=2-s2.0-85096272880&doi=10.1142%2F9789811202391_0016&partnerID=40&md5=abbd1dff2168cfac5de5f40d43e435bb

- Chen, Y.-J., Chen, Y.-M., Tsao, S.-T., & Hsieh, S.-F. (2018). A novel technical analysis-based method for stock market forecasting. Soft Computing, 22(4), 1295–1312. https://doi.org/10.1007/s00500-016-2417-2

- Cho, J., & Lee, J. (2006). An integrated model of risk and risk-reducing strategies. Journal of Business Research, 59(1), 112–120. https://doi.org/10.1016/j.jbusres.2005.03.006

- Chua, A. Y. K., Pal, A., & Banerjee, S. (2023). AI-enabled investment advice: Will users buy it? Computers in Human Behavior, 138, 138. https://doi.org/10.1016/j.chb.2022.107481

- Cristiana, T. (2021). Investors’ trading activity and information asymmetry: Evidence from the romanian stock market. Risks, 9(8), 149. https://doi.org/10.3390/risks9080149

- Dickason, Z., Ferreira, S., & McMillan, D. (2018). Establishing a link between risk tolerance, investor personality and behavioural finance in South Africa. Cogent Economics & Finance, 6(1), 1–13. https://doi.org/10.1080/23322039.2018.1519898

- Fama, E. F. (1998). Market efficiency, long-term returns, and behavioral finance. The comments of Brad Barber, David Hirshleifer, S.P. Kothari, Owen Lamont, Mark Mitchell, Hersh Shefrin, Robert Shiller, Rex Sinquefield, Richard Thaler, Theo Vermaelen, Robert Vishny, Ivo Welch. Journal of Financial Economics, 49(3), 283–306. https://doi.org/10.1016/S0304-405X(98)00026-9

- Gonzalez-Igual, M., Corzo Santamaria, T., & Rua Vieites, A. (2021). Impact of education, age and gender on investor’s sentiment: A survey of practitioners9. Heliyon, 7(3), e06495. https://doi.org/10.1016/j.heliyon.2021.e06495

- Gonzalez, R., Kurtovic, K., Habib, A. S., Ryan, E. S., Foote, J., Pandya, D., Broadwater, G., & Havrilesky, L. J. (2021). A quality improvement initiative to reduce venous thromboembolism on a gynecologic oncology service. Gynecologic Oncology, 162(1), 120–127. https://doi.org/10.1016/j.ygyno.2021.04.035

- Goswami, S., Goswami, B. K., Panicker, A., & Sharma, A. (2020). Exploring the role of emotions and psychology in financial investment decisions in Indian securities market. International Journal of Advanced Science & Technology, 29(1), 532–547.

- Grable, J. E., Joo, S.-H., & Kruger, M. (2020). Risk tolerance and household financial behaviour: A test of the reflection effect. IIMB Management Review, 32(4), 402–412. https://doi.org/10.1016/j.iimb.2021.02.001

- Grosshans, D., & Zeisberger, S. (2018). All’s well that ends well? On the importance of how returns are achieved. Journal of Banking and Finance, 87, 397–410. https://doi.org/10.1016/j.jbankfin.2017.09.021

- Hair, J. F., Celsi, M. W., Money, A. H., Samouel, P., & Page, M. J. (2015). Essentials of business research methods (2nd ed.). https://www.scopus.com/inward/record.uri?eid=2-s2.0-85136103165&doi=10.4324%2F9781315704562&partnerID=40&md5=2d0f34eb49c76fd027fbc0ba8ca8471c

- Hau, H. (2001). Location matters: An examination of trading profits. The Journal of Finance, 56(5), 1959–1983. https://doi.org/10.1111/0022-1082.00396

- Hossain, T., & Siddiqua, P. (2022). Exploring the influence of behavioral aspects on stock investment decision-making: A study on Bangladeshi individual investors. PSU Research Review. https://doi.org/10.1108/PRR-10-2021-0054

- Jaiyeoba, H. B., Adewale, A. A., Haron, R., & Che Ismail, C. M. H. (2018). Investment decision behaviour of the Malaysian retail investors and fund managers: A qualitative inquiry. Qualitative Research in Financial Markets, 10(2), 134–151. https://doi.org/10.1108/QRFM-07-2017-0062

- Kartini, K., & Nahda, K. (2021). Behavioral biases on investment decision: A case study in indonesia. The Journal of Asian Finance, Economics & Business, 8(3), 1231–1240.

- Khawaja, M. J., & Alharbi, Z. N. (2021). Factors influencing investor behavior: An empirical study of Saudi Stock Market. International Journal of Social Economics, 48(4), 587–601. https://doi.org/10.1108/IJSE-07-2020-0496

- Kim, J. J., Dong, H., Choi, J., & Chang, S. R. (2022). Sentiment change and negative herding: Evidence from microblogging and news. Journal of Business Research, 142, 364–376. https://doi.org/10.1016/j.jbusres.2021.12.055

- Kirchler, E., & Maciejovsky, B. (2002). Simultaneous over- and underconfidence: Evidence from experimental asset markets. Journal of Risk and Uncertainty, 25(1), 65–85. https://doi.org/10.1023/A:1016319430881

- Kumari, A., Goyal, R., & Kumar, S. (2022). Review on behavioral factors and individual investors psychology towards investment decision making. ECS Transactions, 107(1), 8009–8023. https://doi.org/10.1149/10701.8009ecst

- Lather, A. S., Jain, S., & Anand, S. (2020). The effect of personality traits on cognitive investment biases. Journal of Critical Reviews, 7(2), 221–229. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85080124551&doi=10.31838%2Fjcr.07.02.39&partnerID=40&md5=27af52495ee4fcf4f236f3bf3479dbbc

- Liang, X., & Reiner, D. (2009). Behavioral issues in financing low carbon power plants. Energy Procedia, 1(1), 4495–4502. https://doi.org/10.1016/j.egypro.2009.02.267

- Lim, T. S., Mail, R., Abd Karim, M. R., Ahmad Baharul Ulum, Z. K., Jaidi, J., & Noordin, R. (2018). A serial mediation model of financial knowledge on the intention to invest: The central role of risk perception and attitude. Journal of Behavioral and Experimental Finance, 20, 74–79. https://doi.org/10.1016/j.jbef.2018.08.001

- Madaan, G., & Singh, S. (2019). An analysis of behavioral biases in investment decision-making. International Journal of Financial Research, 10(4), 55–67. https://doi.org/10.5430/ijfr.v10n4p55

- Mahapatra, M. S., & Mishra, R. (2020). Behavioral influence and financial decision of individuals: A study on mental accounting process among Indian households. Cogent Economics and Finance, 8(1), 1827762. https://doi.org/10.1080/23322039.2020.1827762

- Mahmood, I., Ahmad, H., Khan, A. Z., & Anjum, M. (2011). Behavioral implications of investors for investments in the stock market. European Journal of Social Sciences, 20(2), 240–247. https://www.scopus.com/inward/record.uri?eid=2-s2.0-79953134370&partnerID=40&md5=d9df8ed7c822d1541508d1d73c187691

- Marjerison, R. K., Han, L., & Chen, J. (2023). Investor behavior during periods of crises: The chinese funds market during the 2020 pandemic. Review of Integrative Business and Economics Research, 12(1), 71–91. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85148047689&partnerID=40&md5=1d270920ea912d737c29e2fd142ea915

- Mavruk, T. (2022). Analysis of herding behavior in individual investor portfolios using machine learning algorithms. Research in International Business and Finance, 62. https://doi.org/10.1016/2Fj.ribaf.2022.101740

- Menon, M., Huber, R., West, D. D., Scott, S., Russell, R. B., & Berns, S. D. (2023). Community-based approaches to infant safe sleep and breastfeeding promotion: A qualitative study. BMC Public Health, 23(1). https://doi.org/10.1186/s12889-023-15227-4

- Mouna, A., & Anis, J. (2015). The factors forming investor’s failure: Is financial literacy a matter? Viewing test by cognitive mapping technique. Cogent Economics and Finance, 3(1), 1057923. https://doi.org/10.1080/23322039.2015.1057923

- Mundi, H. S., Kaur, P., & Murty, R. L. N. (2022). A qualitative inquiry into the capital structure decisions of overconfident finance managers of family-owned businesses in India. Qualitative Research in Financial Markets, 14(3), 357–379. https://doi.org/10.1108/QRFM-02-2020-0019

- Mushinada, V. N. C., & Veluri, V. S. S. (2019). Elucidating investors rationality and behavioural biases in Indian stock market. Review of Behavioral Finance, 11(2), 201–219. https://doi.org/10.1108/RBF-04-2018-0034

- Nekhili, R. (2020). Systemic risk and interconnectedness in Gulf Cooperation Council banking systems. Banks and Bank Systems, 15(1), 158–166. https://doi.org/10.21511/bbs.15(1).2020.15

- Ossareh, A., Pourjafar, M. S., & Kopczewski, T. (2021). Cognitive biases on the iran stock exchange: Unsupervised learning approach to examining feature bundles in investors’ portfolios. Applied Sciences (Switzerland), 11(22). https://www.scopus.com/inward/record.uri?eid=2-s2.0-85119833241&doi=10.3390%2Fapp112210916&partnerID=40&md5=535c9e691a402b51d7849be21eb396f5

- Oyekale, A. S. (2022). Factors influencing willingness to be vaccinated against Covid-19 in Nigeria. International Journal of Environmental Research and Public Health, 19(11), 6816. https://doi.org/10.3390/ijerph19116816

- Paraboni, A. L., & da Costa, N. J. (2021). Improving the level of financial literacy and the influence of the cognitive ability in this process. Journal of Behavioral and Experimental Economics, 90, 101656. https://doi.org/10.1016/j.socec.2020.101656

- Parveen, S., Satti, Z. W., Subhan, Q. A., & Jamil, S. (2020). Exploring market overreaction, investors’ sentiments and investment decisions in an emerging stock market. Borsa Istanbul Review, 20(3), 224–235. https://doi.org/10.1016/j.bir.2020.02.002

- Ploner, M. (2017). Hold on to it? An experimental analysis of the disposition effect. Judgment and Decision Making, 12(2), 118–127. https://doi.org/10.1017/S1930297500005660

- Pompian, M. M. (2011). Behavioral finance and wealth management: How to Build investment strategies that account for investor biases.

- Putri Pa, A. N., Wiksuana, I., Suartana, I. W., & Sri Artini, L. G. (2022). The influence of social and personal factors in individual investment decision making. Quality - Access to Success, 23(191), 80–88. https://doi.org/10.47750/QAS/23.191.10

- Raveendra, P. V., Rizwana, M., Singh, P., Santhosh Kumar, S., & Vijaya Kumar, G. (2018). Performance appraisal biases and behavioral biases in decision making: An empirical study. International Journal of Mechanical Engineering and Technology, 9(6), 312–318. https://www.iaeme.com/IJMET/index.asp

- Renu Isidore, R., & Christie, P. (2018). Investment behavior of secondary equity investors: An examination of the relationship among the biases. Indian Journal of Finance, 12(9), 7–20. https://doi.org/10.17010/ijf/2018/v12i9/131556

- Richards, D. W., Rutterford, J., Kodwani, D., & Fenton O’Creevy, M. (2017). Stock market investors’ use of stop losses and the disposition effect. European Journal of Finance, 23(2), 130–152. https://doi.org/10.1080/1351847X.2015.1048375

- Sarstedt, M., Hair, J. F., Cheah, J.-H., Becker, J.-M., & Ringle, C. M. (2019). How to specify, estimate, and validate higher-order constructs in PLS-SEM. Australasian Marketing Journal, 27(3), 197–211. https://doi.org/10.1016/j.ausmj.2019.05.003

- Sharma, D., Misra, V., & Pathak, J. P. (2021). Emergence of behavioural finance: A study on behavioural biases during investment decision-making. International Journal of Economics and Business Research, 21(2), 223–234. https://doi.org/10.1504/IJEBR.2021.113140

- Shiva, A., & Singh, M. (2020). Stock hunting or blue chip investments?: Investors’ preferences for stocks in virtual geographies of social networks. Qualitative Research in Financial Markets, 12(1), 1–23. https://doi.org/10.1108/QRFM-11-2018-0120

- Singh, H. P., Goyal, N., & Kumar, S. (2016). Behavioural biases in investment decisions: An exploration of the role of gender. Indian Journal of Finance, 10(6), 51–62. https://doi.org/10.17010/ijf/2016/v10i6/94879

- Stella, G. P., Cervellati, E. M., Magni, D., Cillo, V., & Papa, A. (2022). Shedding light on the impact of financial literacy for corporate social responsibility during the Covid-19 crisis: Managerial and financial perspectives. Management Decision, 60(10), 2801–2823. https://doi.org/10.1108/MD-12-2021-1681

- Trabelsi, N. (2019). Dynamic and frequency connectedness across Islamic stock indexes, bonds, crude oil and gold. International Journal of Islamic & Middle Eastern Finance & Management, 12(3), 306–321. https://doi.org/10.1108/IMEFM-02-2018-0043

- Ullah, S., Elahi, M. A., Ullah, A., Pinglu, C., & Subhani, B. H. (2020). Behavioral biases in investment decision making and moderating role of investor’s type. Intellectual Economics, 14(2), 87–105. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85104486964&doi=10.13165%2FIE-20-14-2-06&partnerID=40&md5=1a8726a3cc95acf2a0580465b713ef8b

- Ventre, V., Martino, R., Castellano, R., & Sarnacchiaro, P. (2023). The analysis of the impact of the framing effect on the choice of financial products: An analytical hierarchical process approach. Annals of Operations Research. https://doi.org/10.1007/s10479-022-05142-z

- Verma, R., & Verma, P. (2018). Behavioral biases and retirement assets allocation of corporate pension plans. Review of Behavioral Finance, 10(4), 353–369. https://doi.org/10.1108/RBF-01-2017-0009

- Vlahovic, N., Brozovic, V., & Skavic, F. (2021). Investor classification model based on behavioural finance studies. 2021 44th International Convention on Information, Communication and Electronic Technology, MIPRO 2021 - Proceedings, 1271–1276.

- Wang, J., & Wang, X. (2012). Structural equation modeling: Applications using mplus. Structural Equation Modeling: Applications Using Mplus. https://doi.org/10.1002/9781118356258

- Wattanasan, P., Bhupesh, L., & Pallela, S. (2020). An explorational study on influencing factors in financial investment decisions in thailand securities market. International Journal of Advanced Science & Technology, 29(3), 8237–8243. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85083356382&partnerID=40&md5=3ec1e1b5bb0145578bd9dfc3a3f0a91d

- Wildavsky, A., & Dake, K. (1990). Theories of risk perception: Who fears what and why?Daedalus, 119(4), 41–60

- Worawachtanakul, P., Likitapiwat, T., & Lawsirirat, C. (2018). Supporting the understanding investor behavior and the effective communication. JP Journal of Heat and Mass Transfer, 15(Special Issue 1), 95–100. https://doi.org/10.17654/HMSI118095

- Zhang, M., Nazir, M. S., Farooqi, R., & Ishfaq, M. (2022). Moderating role of information asymmetry between cognitive biases and investment decisions: A Mediating effect of risk perception. Frontiers in Psychology, 13. https://doi.org/10.3389/2Ffpsyg.2022.828956