?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The establishment of the pilot financial reform zone is aimed at promoting regional financial supply-side structural reform. By giving localities broader financial autonomy, local governments are incentivized to target the “pain points and blockages” in financial services to the real economy, thus having a significant impact on the development and transformation of micro enterprises. Based on micro data of A-share listed manufacturing enterprises in Shanghai and Shenzhen from 2010–2021, this paper uses the double difference method (DID) to explore the impact of the establishment of a comprehensive financial reform pilot zone on the digital transformation of micro manufacturing enterprises and its mechanism. The results found that the pilot zone of comprehensive financial reform significantly improved the digitalization of manufacturing enterprises. Specifically, it effectively promotes the digital transformation of enterprises by reducing their financing costs and promoting their physical investment levels. In particular, it has had a stronger positive impact on the digital transformation of non-state-controlled enterprises, competitive enterprises, and labor-intensive and technology-intensive manufacturing enterprises. The results of the present study can provide a reference experience for other regions to carry out financial reforms to serve the transformation and upgrading of enterprises.

1. Introduction

With the continuous emergence and application of digital technologies such as artificial intelligence, blockchain, cloud computing and big data, the output value of digital economy has reached 43.7% of global GDP in 2021, and the digital economy is becoming the innovation high point that countries are competing for. In the era of digital economy, digital transformation determines the future business performance, market value and innovation efficiency of enterprises (Mikalef & Pateli, Citation2017; Zhao et al., Citation2021; Ziyao & Lisha, Citation2022), and is the winning strategy for enterprises to achieve breakthrough innovation and competitive advantage (Hanelt et al., Citation2021). In particular, the sudden public health crisis in 2020 has caused impact on the world economy, and many enterprises are in production and operation difficulties, and the application of digital technology will help to alleviate these problems and ensure the survival and development of many micro-entities.

In response to the opportunities and challenges brought by the development of the digital economy, digital transformationFootnote1 of enterprises has entered the fast track of development. In the past four years, the average score of the Digital Transformation Index has increased from 37 to 54,Footnote2 which shows that digitalization is being deeply integrated into the development of enterprises. However, it is by no means easy for enterprises to carry out digital transformation. According to Accenture’s “China Enterprise Digital Transformation Index Study 2021”, only 16% of benchmark enterprises in China have achieved digital transformation results, and most are still in the exploration period of digital transformation. The main reason is that the digital R&D activities based on digital transformation, as well as the institutional reform and innovation that accompany it, require a large amount of capital investment, which is unaffordable for enterprises and has become a major problem on the way of digital transformation. The key to solving these problems lies in providing a high-quality financial supply (Demirguc–Kunt & Maksimovic, Citation1998), effectively reducing the financing costs of the real economy (Levine, Citation2005), and promoting the digital innovation momentum of enterprises. However, in China’s existing financial system, there is a clear mismatch between the low risk appetite of the banking sector and the high-risk characteristics of enterprises’ digital transformation; at the same time, the high financing threshold of the capital market makes it difficult to meet the capital needs of enterprises’ digital transformation, which leads to the inefficiency of financial support for the real economy (e.g., digital transformation). Therefore, it becomes inevitable in the digital era to promote the reform of the financial system to adapt to the transformation and needs of microeconomic actors.

The establishment of the pilot zone for comprehensive financial reform provides a good basis for solving the above problems. By exploring diversified reform paths, the pilot financial comprehensive reform zones provide replicable experiences for reform in other regions, thereby enhancing the efficiency of financial support to the real economy. However, compared with pilot reforms such as special economic zones and free trade zones, the promotion of comprehensive financial reform pilot zones is more cautious, and the academic community has yet to conduct in-depth research on the effects of institutional design and the mechanism of action of this new type of financial system reform, and the existing literature has different evaluations of regional financial reforms. On the one hand, it lies in the fact that the change of China’s financial institutional mechanism is an important institutional driver of financial and economic development, which has effectively promoted local economic development (X. Wang et al., Citation2020a), and regional financial reforms have also played a role in enhancing the innovation and production efficiency of micro-entities (Ang, Citation2010). On the other hand, the economic effects of regional financial reforms hold only in some provinces (Yeting et al., Citation2018), possibly because financial reforms have intensified the competition for financial resources (Shu Song et al., Citation2005), distorting the efficiency of the existing financial structure and allocation to some extent. Thus, it can be seen that existing studies have not reached consistent conclusions and need to be explored in depth.

The establishment of the pilot financial reform zone can build a financial system and organization that matches the current economic structure of China, broaden the channels of financial services (Tang et al., Citation2020), alleviate information asymmetry and resource mismatch in the financial market (Gomber et al., Citation2018), provide a new model for enterprise financing, and play an important role in the digital transformation of enterprises (Hongming et al., Citation2022). By giving local governments broader financial autonomy and encouraging them to target problems in the real economy of financial services, it can have a significant impact on the development and change of micro enterprises. On the one hand, the pilot zone of comprehensive financial reform has introduced a series of combined policies in terms of financial system reform, financing channel expansion and financial industry innovation, which broaden the financing channels of real enterprises by relaxing financing constraints and encouraging the free flow of funds, laying the financial foundation for enterprise innovation and effectively promoting the digital transformation of enterprises. On the other hand, the pilot zone of comprehensive financial reform fully empowers local governments institutionally, stimulates local governments to optimize administrative efficiency and improve supervision accordingly, which is conducive to creating a good innovation ecology for enterprises, thus creating a gaining effect on their digital transformation. It can be inferred that there is a logical connection between the pilot financial reform zone and the digital transformation paradigm of enterprises, and the exploration of the above issues undoubtedly provides empirical evidence for the optimization of financial system reform and micro-enterprise transformation, and thus has high theoretical value and practical significance.

The innovative contribution of this paper is that, Firstly, it innovatively explores the impact of the establishment of the pilot financial reform zone on the digital transformation of enterprises in a quasi-natural experiment, so as to be able to examine the correlation mechanism between the design of the financial system and the transformation behavior of micro-enterprises; Secondly, based on the heterogeneity perspective, the nature of enterprise property rights, differences in industry characteristics and differences in industry nature are taken into account to examine the differentiated impact of the financial comprehensive reform pilot zone on the digital transformation of manufacturing enterprises in a multi-dimensional manner; thirdly, the mechanism of the role of the financial comprehensive reform pilot zone in influencing the digital transformation of enterprises is explored from the perspectives of enterprise finance as well as enterprise investment.

2. Institutional background and literature review

2.1. System background

The financial comprehensive reform pilot zone is an important part of China’s comprehensive supporting reform pilot zone. The executive meeting of the State Council proposed initiatives to build a diversified financial system and encourage the development of new financial organizations, which aims to alleviate the problem of difficult and expensive financing for enterprises by increasing the supply of financial resources, so as to achieve a balance between supply and demand of funds, which is ultimately beneficial to the stable and healthy development of the economy.

The executive meeting of the State Council in March 2012 approved the establishment of the first financial comprehensive reform pilot zone in Wenzhou to guide the standardized development of private financing, enhance the ability of financial services to the real economy and provide experience for national financial reform. For one thing, the establishment of the pilot financial reform zone can build a financial system and organization that matches China’s current economic structure and broaden the channels of financial services. Second, the financial reform will decentralize the power of financial system design, financial resources allocation, financial supervision, and financial risk prevention and disposal, enhance the financial service capacity and overall risk prevention and control capacity of each region, promote the improvement of regional financial environment, and then enhance the ability of financial services to the real economy.

In the same year, the State also established pilot zones for comprehensive financial reform and innovation in the Pearl River Delta and Quanzhou, Fujian, marking the beginning of the advancement of regional financial system reform in China. Subsequently, from 2013 to 2016, the State Council approved the establishment of comprehensive financial reform pilot zones in Yunnan and Guangxi along the border, Qingdao in Shandong, Taizhou in Jiangsu and Lankao in Henan, aiming at exploring cross-border finance, building a wealth management system with Chinese characteristics, promoting financial services for the real economy and experimenting with inclusive finance, among other functions.In 2019, the State Council in Ningde and Longyan in Fujian and Ningbo in Zhejiang approved the establishment of the latest batch of national pilot zones for comprehensive financial reform, marking a new stage in the reform of China’s regional financial system.

The establishment of the pilot financial reform zone focuses more on encouraging local governments to innovate financial mechanisms based on their own resource endowments, adopting the model of “piloting first, then summarizing, then promoting”, with the goal of respecting market laws and adhering to market orientation, promoting the overall optimization of the financial system, financial industry, financial supervision, etc., and playing the role of the government’s “visible hand” with a series of differentiated policies that have their own focus.

2.2. Literature review

Digital transformation of manufacturing enterprises is characterized by long cycle, high risk and high investment (Hui & Dandan, Citation2020), which requires higher capital and cost control than other production and innovative projects. The establishment of a comprehensive financial reform pilot zone can achieve the reduction of financing constraints and financing costs, thus promoting the digital transformation of enterprises. In the traditional financial system, there is a problem of inadequate financial supply, which creates resistance for enterprises to carry out reform and transformation.

In this scenario, the establishment of a comprehensive financial reform pilot zone, which aims to deepen the reform of the financial mechanism and system, can provide micro enterprises with richer and more personalized financial products and services, and help them to carry out innovative activities such as digital transformation (Xiao & Lin, Citation2022). Specifically, the establishment of pilot zones for comprehensive financial reform, which decentralize the power of financial systems, financial resource allocation, and financial supervision, can enhance the ability of financial services to enterprises. The pilot zones can create financial products and financial services that meet the needs of local enterprises, thus reducing the financing constraints of enterprises, alleviating the problems of difficult and expensive financing, and improving the motivation of digital transformation of enterprises, especially for areas in high marketization and high financial development levels and high-tech industries.

The supply and allocation of financial resources in the pilot zone will pay more attention to the long-term project investment needs (e.g., digital transformation) that can help improve the productivity of enterprises, instead of using short-term performance as a reference for resource allocation. The establishment of the pilot financial reform zone will guide more financial resources to be injected into enterprises with innovation and transformation preferences (with digital transformation needs), which can greatly alleviate the financing constraints of enterprises (Huang & Shen, Citation2022) and thus provide financial assistance for their digital transformation. In addition, the good financial supply environment created by the pilot financial reform zone can help reduce the cost of financial services for real enterprises, prompting them to make investments (digital transformation) without bearing high financing costs, and laying a good resource support for the digital transformation point of enterprises.

Moreover, the establishment of a comprehensive financial reform pilot zone can effectively broaden financing channels and reduce financing costs, which will lead to the improvement of financial stability and internal control of enterprises. The improved financial stability of enterprises will help managers invest in digital transformation, a high-risk and high-investment economic activity. More importantly, the pilot financial reform zone pays more attention to the optimization of the financial system and improves the efficiency of administrative approval (X. Wang et al., Citation2020b), which helps to create an open and transparent investment environment, allowing the market to better perform its resource allocation function, accurately identify high-quality enterprises and support them. Therefore, as the “visible hand” of the government, it takes the initiative to improve the environment for digital transformation of enterprises and provides policy level and technical support for enterprises, and this policy orientation will greatly improve the willingness of enterprises to digital transformation (Zeng & Dolado, Citation2023) and avoid market failure. The government will put in government subsidies at different levels to promote the digital transformation of enterprises (Zhiyuan & Yongfan, Citation2023), reduce the information asymmetry of enterprises, and set up pilot zones such as the National Big Data Comprehensive Pilot Zone (Linqi et al., Citation0000) to enhance the ability of enterprises to collaborate with industry, academia and research institutes and accelerate the pace of digital transformation of enterprises.

In summary, comprehensive financial reform pilot zones can give local governments a certain degree of financial autonomy and stimulate them to develop finance appropriate for local development, thus facilitating micro enterprises to engage in high-risk and high-investment digital transformation activities. At the same time, however, it is important to note that China’s financial reform strategy is incremental, even as many dilemmas arise in the reform process, and the pilot zones for comprehensive financial reform are no exception. Any financial reform is aimed at building a financial system and organization that matches the current economic structure; therefore, in the context of the burgeoning digital economy, exploring the impact of the pilot zone for comprehensive financial reform on the digital transformation of manufacturing firms has a high theoretical function and application value.

3. Research hypothesis

3.1. The relationship between the comprehensive financial reform pilot area and the financial status of enterprises

Digital transformation of enterprises is a systematic and continuous change and innovation, which has the characteristics of long cycle, information asymmetry, high risk, high failure rate and positive externality (Tu & Yan, Citation2022), etc. The existence of such characteristics will lead to market failure and weaken the motivation of digital transformation of enterprises, which requires the government to play the role of its “visible hand”. First, the financial comprehensive reform pilot zone can promote the diversified development of enterprise financing channels, reduce financing costs and improve financing efficiency (Han & Fan, Citation2020). The existence of financing thresholds and financing barriers in traditional financial institutions has made corporate financing cost high and financing more difficult. However, in the pilot zone, the government has introduced new financial institutions, financial products and financial services to enhance the ability of financial institutions to provide services to the real economy, while reducing the operating costs of enterprises, which will prompt manufacturing enterprises to have more funds for digital transformation as a corporate behavior.

At the same time, the pilot financial reform zone will provide a more relaxed policy environment and regulatory mechanism to encourage financial institutions to explore the economic characteristics and development needs of the region, and then produce financial products and services with targeted development, which promotes the innovation of financial products and services, improves the enterprise financing environment, and helps manufacturing enterprises to graft on financial resources to achieve digital transformation. Moreover, after obtaining the support of local financial resources, enterprises can reduce the financial pressure in the transformation, improve their financial situation, create a relaxed digital transformation environment, alleviate the problem of expensive financing and reduce the financing cost of enterprises (Xiaolong & Xiaojing, Citation2023), and then prompt enterprises to carry out digital transformation, which is a high-risk and high-investment activity for sustainable development.

Therefore, the establishment of a comprehensive financial reform pilot zone can send positive signals to enterprises, promote the rational allocation of financial resources in the market through strong government support, give full play to the coordination of financial system resources, enable enterprises to obtain financing support in financing, alleviate financing constraints, and optimize their financial situation (Shu & Yu, Citation2022), such as government subsidies, tax preferences, and special financial allocations to reduce the cost of enterprise financing, prompting enterprises to invest more funds in digital transformation and upgrading. In general, the pilot financial reform zone reduces the cost of enterprise financing and optimizes the financial status of enterprises through different ways mentioned above, and the optimization of the financial status of enterprises can improve the liquidity of enterprises. Moreover, after the optimization of enterprise financial status, the credit rating and borrowing ability of enterprises increase, and it is easier to obtain external financial support, which further reduces the operating cost of enterprises, optimizes resource allocation, improves the quality of decision making, and then provides financial and decision support to the digital transformation of enterprises, and helps the smooth development of digital transformation of enterprises. Therefore, hypothesis 1 is proposed.

Hypothesis 1:

The establishment of a comprehensive financial reform pilot zone will help reduce the financing costs of enterprises, optimize their financial position, and facilitate their digital transformation.

3.2. The relationship between the financial comprehensive reform pilot area and real investment

The digital transformation of enterprises itself is a complex and long-lasting systemic project that requires continuous investment and renewal of communication equipment and hardware facilities, and therefore requires continuous support from the external environment and policies. The creation of the pilot financial reform zone has effectively improved the financial market in the region, optimizing the financial structure and making it more complete (Jia et al., Citation2022). At the same time, the high concentration of financial resources has intensified competition among financial institutions, making them take the initiative to innovate financial tools and be able to tailor financial service solutions to the current situation of enterprises, providing support for the physical investments made by enterprises for digital transformation, which in turn pulls the degree of digital transformation of enterprises.

In addition, the reform pilot zones can promote financial innovation in the region, broaden the financial service channels and explore new financing methods, most of these new financing methods opportunity Internet and other emerging technology platforms, through information technology and digital means to reduce information asymmetry, break the barriers of traditional financing channels, and thus improve the efficiency and accuracy of enterprise financing (J & SHIN, Citation2004; Tang et al., Citation2022). Through the complementary advantages of different financial industries, the pilot financial reform zone combines financial products that meet the characteristics of enterprises’ digital transformation, establishes innovative financial service systems and financing methods, provides enterprises with more convenient and diversified financing services, eases the bottlenecks and restrictions of traditional financing channels, accelerates the docking of capital and the real economy, and promotes the development of manufacturing enterprises’ digital transformation.

Furthermore, the pilot zone of comprehensive financial reform has promoted the opening and competition of the financial market, providing more financing channels for the real economy. By introducing foreign investment and opening up the financial market, the pilot zone promotes the competition and development of the financial market, which provides more financing channels for the real economy and enriches the financing methods of enterprises, and then enterprises use different channels of financing funds for medium- and long-term digital transformation and upgrading, which promotes enterprises to be able to continuously invest in digital transformation projects and accelerate the pace of digital transformation of enterprises. Therefore, hypothesis 2 is proposed.

Hypothesis 2:

A comprehensive financial reform pilot zone can facilitate physical investment in enterprises and thus promote their digital transformation.

4. Study design

4.1. Measurement model setting

Based on the theoretical analysis above, a double difference model (DID) is used to test the relationship between the establishment of a comprehensive financial reform pilot zone and the digital transformation of enterprises, and a two-way fixed model of time and individuals is chosen to reduce the interference of endogeneity problems, and a benchmark regression model is constructed as follows:

where denotes the firm and

denotes the year;

denotes the degree of digital transformation of enterprises and is the explanatory variable of this paper;

is the policy shock variable and the core explanatory variable of interest in this paper;

denotes the policy effect of establishing a comprehensive financial reform pilot zone;

、

denote constant terms and control variables, respectively, and

denotes firm fixed effects to control for micro factors that do not vary over time;

denotes time fixed effects to control for time factors that do not vary with the firm;

is the residual term.

4.2. Variable description

(1) Explained variables

Enterprise Digital Transformation (DCG). In this paper, we refer to Wu, F. et al. (2021) (Fei et al., Citation2021) and use the word frequency share of digitization-related terms in annual reports to measure the digital transformation of enterprises. The specific method is as follows: First, download the annual reports of A-share listed companies in Shanghai and Shenzhen from Juchao Consulting, and convert them to text file format. Second, based on the digitization lexicon constructed by Wu Fei et al. including artificial intelligence, big data, cloud computing, blockchain, and digital technology usage, word frequency statistics of digitization-related words were conducted and digitization-related words not appearing in our company’s digitization words, such as shareholder names, executive biographies, subsidiary names, and customer and supplier names, were eliminated. Ultimately, data extraction is performed using Python on the text of annual reports of listed companies to form a data pool. Based on different digitized thesaurus feature words, search, matching and word frequency counting are performed, and then the word frequencies of key technology directions are classified and grouped together, and the final cumulative word frequencies are formed. In this way, an index system for the digital transformation of enterprises is constructed. Due to the typical “right bias” characteristics of the data, the data is logarithmically processed and the digital word frequency data is tailor-made to obtain an overall indicator that portrays the digital transformation of the enterprise.

(2) core explanatory variables

Comprehensive Financial Reform Pilot Zone (DID). In this paper, the manufacturing industries in the 32 prefectural-level cities that are in the 2012–2019 national pilot financial reform zone are treated as the treatment group, and the manufacturing industries in the remaining prefectural-level cities are the control group. In terms of time, it is determined in accordance with the year of the financial comprehensive reform pilot zone established by the state, setting the year of manufacturing enterprises in prefecture-level cities that are in the state determined to establish a financial comprehensive reform pilot zone and subsequent years as 1, otherwise it is 0.

(3) Control variables

With regard to the choice of control variables, other factors in a company’s production and operation activities can also have an impact on the digital transformation of the company. Therefore, this paper selects firm size (Size, equal to the logarithm of the firm’s total assets); firm age (Age, equal to the logarithm of the firm’s current year minus the year of listing); net profit margin of total assets (Roa, equal to net profit/total assets); operating profit (Profit); gearing ratio (Lev, total liabilities/total assets); cash holdings (Cash, cash holdings = (money capital + trading financial assets)/total assets); Tobin’s Q (Tobin, the sum of total market value and total liabilities of the firm/total assets); number of independent directors (Inde, number of independent directors—all persons in the year); and the shareholding ratio of the first largest shareholder (Top1, the number of shares held by the first largest shareholder/total shares of the firm) as control variables.

4.3. Data sources

The research object of this paper is Chinese listed manufacturing companies in Shanghai and Shenzhen A-shares during 2010–2021, and the empirical analysis is conducted by establishing micro-level panel data, after excluding financial, ST and *ST companies and retaining manufacturing companies and samples with missing key variables, on this basis, in order to eliminate the influence of extreme values on the main continuous variables, we adopt the tailing treatment to process them and finally obtain a sample consisting of 13,911 observations. Among them, the various types of financial data of enterprises required for the study are obtained from the Wind database and the annual reports published by listed companies to the public. Descriptive statistics are shown in Table .

Table 1. Descriptive statistics

5. Empirical analysis

5.1. Baseline regression

Based on the previous analysis, a benchmark regression model (1) was used to test the degree of influence of the financial comprehensive reform pilot zone on the digital transformation of enterprises, and the regression results have been listed in Table . In Table , the first column controls for firm fixed effects only; the second column controls for both firm fixed effects and time fixed effects; the third column further adds firm-level control variables and still controls for firm fixed effects; and the fourth column adds time fixed effects to the third column. From the results, it is easy to find that the DID coefficients are all significantly positive, indicating that the comprehensive financial reform pilot zone has a significant role in promoting the digital transformation of enterprises.

Table 2. Baseline regression results

5.2. Robustness tests

5.2.1. Parallel trend hypothesis test

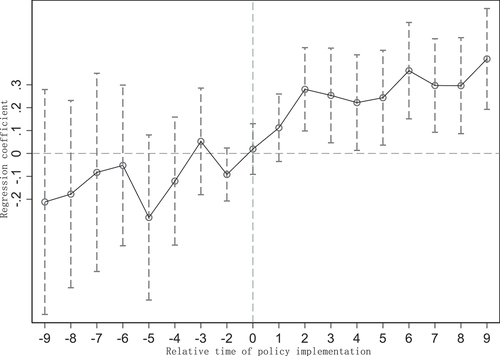

In this paper, we draw on Serfling (SERFLING, Citation2016) to test the parallel trend assumption for the experimental group sample (firms in the test area) and the control group sample (firms not in the test area). Figure reports the related results. From the results, the coefficients of the interaction terms show insignificant performance before the policy implementation, while they show a significant positive effect afterwards, which indicates that there is no significant difference in the trend of digital transformation level changes between the experimental and control groups before the establishment of the financial comprehensive reform pilot zone, thus verifying the parallel trend test hypothesis.

Figure 1. Parallel trend test.

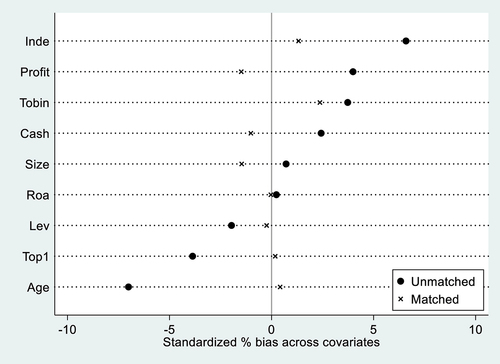

5.2.2. PSM-DID test

Referring to Shi, DaQian et al. (Citation2018) (DaQian et al., Citation2018), the variability among firms was reduced by using the propensity matching score method (PSM). The specific idea is to screen the enterprises according to their business characteristics, select the enterprises with similar characteristics to the experimental group and then adjust the bias of sample selection to get the matched sample data, and then analyze the test with the matched sample. The subsequent common trend identification test indicates that the more significant differences are not present in the matched experimental and control groups, and the PSM-DID used in the article is valid. The results in column (1) of Table show that the regression results of PSM-DID are less different from the baseline regression results, indicating that the empirical results are robust. Figure shows the results of PSM one-to-four nearest neighbor matching method.

Figure 2. PSM (pairwise four nearest neighbor matching method).

Table 3. Robustness tests

5.2.3. Excluding other policy distractions

The implementation of this policy will, to a certain extent, help enhance the ability of enterprises to achieve green production or innovation with digital technology, including the establishment or introduction of different types of digital enterprises to have a positive effect on the digital transformation of the manufacturing industry in the region. Therefore, the article refers to Riming Cui et al. (Citation2021) (Cui et al., Citation2021), and in order to exclude the interference of green financial reform pilot zones, this paper excludes the enterprises that are in the green financial reform pilot zones according to the listing registration of manufacturing enterprises. Column (2) of Table indicates the regression results after exclusion, where the DID coefficient is still significantly positive, indicating that the digital transformation results of manufacturing enterprises are indeed triggered by the financial comprehensive reform pilot area, which again confirms the robustness of the results.

5.2.4. Replace the explanatory variable

The digital transformation indicator system was replaced with Yuan Chun et al. (Citation2021) (Chun et al., Citation2021) digital transformation, and the explanatory variables were re-measured by replacing the original explanatory variables and re-regressing them. The first step is to build a dictionary of digital terms for the enterprise. A dictionary of enterprise digitisation terms was constructed using the national policy semantic system, and 30 important national-level digital economy-related policy documents released between 2012 and 2018 were manually screened to extract keywords related to enterprise digitisation by searching the websites of the Central People’s Government and Industry and Information Technology. After python word separation processing and manual recognition, the final selection of 197 each frequency greater than or equal to 5 times of the enterprise digital related vocabulary, these words constitute the enterprise digital terminology dictionary. Secondly, a textual analysis of the relevant passages of the annual report was carried out. At the same time, the 197 terms in the above digital terminology dictionary were expanded into the “jieba” Chinese lexical database of the Python package, and then machine learning methods were used to analyse the text of the “Management Discussion and Analysis” (MD&A) section of the annual reports of listed companies to obtain the frequency of the 197 terms related to corporate digitalisation in the annual reports. Third, the construction of indicators of the degree of digitisation of the enterprise. Taking into account the difference in text length in the MD&A section of the annual report, after extracting the frequency of occurrence of each keyword in each listed company’s annual report each year, the combined frequency of words related to corporate digitalisation was used to divide the length of the MD&A segment of the annual report to measure the degree of digital transformation of micro enterprises (Digital). For presentation convenience, the indicator was multiplied by 100. The higher the value of the Digital indicator, the more digital the company is. The regression results in column (3) of Table show that the explanatory variables are significant within 10%, indicating that the significance of the core variables and coefficients are consistent with the baseline regression results.

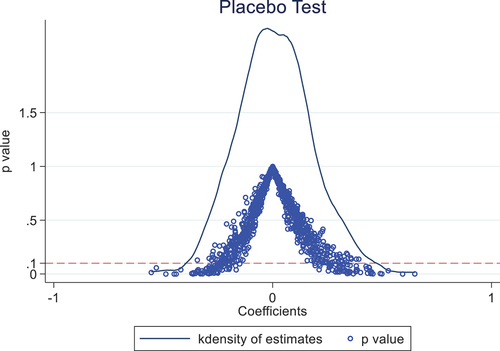

5.2.5. Placebo test

To maximise the examination of whether random factors between different cities play a role, the test of Li et al. (LI et al., Citation2016) was followed, with 32 cities randomly selected from the corresponding policy years as the treatment group and the others as the control group, and 1000 regressions were estimated and the estimated coefficients were plotted as kernel density plots to observe the distribution of the coefficient means and compare them with the baseline regression coefficients, Figure reports the corresponding results. The results show that the estimated coefficients based on the random sample are distributed around 0. The baseline regression of 0.24 falls on the right-hand side of the distribution, indicating the robustness of the baseline regression results.

Figure 3. Placebo test.

5.3. Mechanism test

The baseline regression results indicate that the Comprehensive Financial Reform Pilot Zone has a positive effect on the digital transformation of manufacturing firms, so does the Comprehensive Financial Reform Pilot Zone promote the digital transformation of firms by reducing their financing costs and increasing their physical investment, as we hypothesized in the previous section? Therefore, drawing on the approach proposed by Jiang (2022) (Ting, Citation2022), a mechanism test was conducted and an attempt was made to construct the following model:

Where is the mechanism variable, Equationequation (2)

(2)

(2) verifies the effect of the comprehensive financial reform pilot zone on the two mechanism variables, and the specific estimation results are shown in Table below. Column (1) and column (2) of Table indicate that the pilot financial reform zone has reduced the financing cost of enterprises in the region and promoted their physical investment, respectively.

Table 4. Intermediary mechanism test

6. Optimizing the financial position of your business

Examine whether the financial comprehensive reform pilot zone can reduce the cost of financing and optimize the financial situation of enterprises. On the one hand, the establishment of a comprehensive financial reform zone will provide a more liberal policy environment, introduce new financial institutions, financial products and financial services to the local area, inject flexibility and coordination into the development of local finance, and increase the capacity of financial services to the real economy. On the other hand, the establishment of the pilot zone provides local enterprises with specialized financial products and financial services, easing their financing constraints, reducing their financing costs, increasing their liquidity, optimizing their financial costs, and prompting them to invest more funds in digital transformation and upgrading. In this paper, we refer to Wang, S. et al. (Ting, Citation2022) and use the financial expense ratio (Cost) to reflect the comprehensive cost incurred by the firm when financing. The results in column (1) of Table show that the comprehensive financial reform pilot zone significantly reduces the financial costs of enterprises and optimizes their financial status. This verifies hypothesis 1.

6.1. Entity investment effect

Examine whether the financial comprehensive reform pilot zone influences the degree of digital transformation of enterprises by promoting business investment. Enterprise digital transformation is a highly uncertain process, and transformation capital, communication equipment, hardware facilities and other elemental investments are important conditions that determine digital transformation. Therefore, the investment effect of business entities plays a crucial role in the digital transformation of enterprises. In this paper, the entity investment refers to the method of Yang, Dapeng (2023) (Dapeng et al., Citation0000), using the investment rate representation (Invt, the ratio of the sum of funds paid for fixed assets, intangible assets and other long-term assets to total assets). From the results in column (2) of Table , it is clear that the financial comprehensive reform pilot zone raises the proportion of physical investment in manufacturing enterprises, which in turn increases the investment in digital equipment and accelerates the pace of digital transformation of enterprises. This verifies hypothesis 2.

6.2. Heterogeneity analysis

As there are differences in the needs and capabilities of different enterprises for digital transformation, in order to further explore which factors affect the micro effects of the integrated financial reform pilot zones, this paper looks at two aspects one is the nature of property rights and the other is the differences in industry characteristics to explore the heterogeneous role of the integrated financial reform pilot zones respectively.

6.2.1. Nature of property rights

As the key targets of local governments and financial institutions, state-owned enterprises are to some extent more likely to be supported by bank credit resources (Zhang et al., Citation2013), while private enterprises face higher financing costs and financing constraints.

To explore the differences in the impact of the financial comprehensive reform pilot zone on the digital transformation of enterprises with different ownership, they are divided into state-controlled enterprises as well as non-state-controlled enterprises according to the nature of their ownership. The results in Table (1) show that the comprehensive financial reform pilot zone significantly promotes the digital transformation of non-state-controlled enterprises, while the effect is not significant in the sample group of state-controlled enterprises. The difference that leads to this situation is that non-state-controlled enterprises are more flexible compared to state-controlled enterprises. Non-state-controlled enterprises usually do not have large government agencies or complex decision-making hierarchies, and therefore can more easily adapt their strategies and business models to the needs of digital transformation.

Table 5. Heterogeneity analysis

In contrast, state-controlled companies typically have more rigid structures and decision-making mechanisms, making it difficult to adapt quickly to new market trends and technological changes. At the same time, non-state-controlled companies are more inclined to use venture capital and other forms of capital market financing to support digital transformation. Non-state-controlled enterprises usually do not have as abundant resources and capital reserves as state-controlled enterprises, so they need external financial support more to achieve digital transformation.

Moreover, state-controlled enterprises can rely on government financial support and bank loans to achieve digital transformation, so they are less dependent on financial policies. In the digital transformation among non-state-owned enterprises, the financial comprehensive reform pilot zone has effectively lowered the threshold of financial resources that restrict the digital transformation of non-state-controlled enterprises, largely alleviated the dilemma of financing constraints faced by private enterprises, and provided support for non-state-controlled enterprises to carry out digital transformation. The regression results are shown in Table (1).

6.2.2. Differences in industry characteristics

The difference in the degree of competition in the industry may lead to the progress of digital transformation of enterprises. In competitive industries, companies will accelerate the pace of digital transformation and increase spending on digital equipment, communication devices, etc. in order to increase productivity to dominate the market, thus improving the overall competitiveness of the company. In contrast, in regulated industries, digital transformation is often inhibited.

The reasons for this are mainly the following: First, legal and regulatory restrictions as well as consideration of issues such as public interest and security. Second, digital transformation in regulated industries requires huge investment costs, and these costs may further increase due to the requirements of government regulations and regulatory needs. For example, industries such as aviation and railroads require significant investments to upgrade equipment and systems to ensure safety and reliability, compared to competitive industries where the cost of digital transformation is typically lower. Third, security and privacy issues. The regulated industry involves important issues such as public safety and privacy, so digital transformation needs to meet higher security and privacy standards. This may require more technology and resources to ensure data security and privacy, which can increase the cost and complexity of digital transformation. In contrast, competitive industries typically do not need to meet such high security and privacy standards, and the process of digital transformation is relatively straightforward. Fourth, regulated industries often require the use of specific technologies and systems that may require highly specialized talent to support them. This makes the process of digital transformation more challenging. Competitive industries, on the other hand, typically use common technologies and systems, which makes digital transformation easier to achieve.

To verify the above speculation, this paper divides the sample into regulated and competitive industries based on industry characteristics this paper draws on Ke et al. (2017) (Ke et al., Citation0000). The results in column (2) of Table show that in competitive industries, the coefficient of DID is 0.287 and significant at the 1% level; in contrast, in regulated industries, the coefficient of DID is not significant. These results suggest that comprehensive financial reform pilot zones have had a more significant effect on digital transformation in competitive industries than in regulated industries.

6.2.3. Industry nature differences

The needs and transformation capabilities of manufacturing companies for digital transformation will vary by the nature of the industry. In order to explore the impact of the financial comprehensive reform pilot zone on the differences of digital transformation of manufacturing enterprises of different nature. We divide manufacturing enterprises into labor-intensive manufacturing enterprises, capital-intensive manufacturing enterprises, and technology-intensive manufacturing enterprises and conduct empirical tests based on reference to Yang Ligao (Yang et al., Citation2018) and other practices.

The results in column (3) of Table show that the financial comprehensive reform pilot zone significantly promotes the digital transformation of labor-intensive manufacturing enterprises as well as technology-intensive manufacturing enterprises, while the effect on the digital transformation of capital-intensive manufacturing enterprises is not significant. The reason for this difference may be that labor-intensive manufacturing companies usually face higher labor cost pressure, and digital transformation can help these companies improve productivity, reduce labor costs and enhance competitiveness. Comprehensive financial reform pilot zones may provide these enterprises with the capital and resources needed for digital transformation by providing financial support, policy support, and other measures. Technology-intensive manufacturing enterprises rely more on high-tech and innovation capabilities, and digital transformation can help these enterprises improve their production processes, optimize product design, and achieve innovation in smart manufacturing.

Comprehensive financial reform pilot zones may facilitate the digital transformation of these enterprises by introducing technology innovation platforms and supporting R&D and technology cooperation. Capital-intensive manufacturing enterprises, on the other hand, usually require large capital investment for equipment renewal and production expansion, and the scale of investment required for digital transformation is larger. Comprehensive financial reform pilot zones may carry out reform experiments in the financial sector, but for capital-intensive manufacturing enterprises, the capital requirements for digital transformation may be beyond the scope of the pilot zones or the support capacity of the financial system.

7. Conclusions and policy recommendations

7.1. Conclusions

With more and more enterprises joining the wave of digital development, the deep integration of financial reform and real economy has become an important development trend in the future. Manufacturing enterprises can effectively complete digital transformation after obtaining effective support from finance. Based on the micro data of A-share listed manufacturing enterprises in Shanghai and Shenzhen from 2010 to 2021, this paper uses Python software to analyze the annual reports of listed entities for text recognition, and more objectively and comprehensively portrays the degree of digital transformation of manufacturing enterprises, while using the double difference method to empirically investigate the impact of the financial comprehensive reform pilot zone on the digital transformation of manufacturing enterprises, using the quasi-natural experiment of the financial comprehensive reform pilot zone. The study also investigated the impact and mechanism of the financial reform pilot zone on the digital transformation of manufacturing enterprises using the double difference method.

The results of the study show that the financial comprehensive reform pilot zone has played a positive role in promoting the digital transformation of manufacturing enterprises. The mechanism analysis shows that the pilot zone of comprehensive financial reform has promoted the digital transformation of manufacturing enterprises by reducing their financing costs and enhancing their physical investment. Heterogeneity analysis shows that the impact of the pilot zones on the digital transformation of non-state holding companies, competitive industry enterprises, and labor-intensive and technology-intensive manufacturing enterprises is more significant.

7.2. Policy recommendations

Based on the above findings, the following policy implications are offered:

First, for the financial comprehensive reform pilot zone can promote the digital transformation of manufacturing enterprises, so it is necessary to expand the scope of pilot cities of financial comprehensive reform pilot zone to promote the digital transformation of manufacturing enterprises nationwide. The expansion of the pilot scope should give priority to the eastern coastal region, which is because the eastern coastal region has a more perfect financial structure, stable financial system and organization, and strong risk-carrying ability, and has the foundation of financial reform. The government should focus on deepening the reform of the financial system, continuously optimizing the external business environment of enterprises, fundamentally reducing the external transaction costs faced by enterprises, and then fully exploiting the potential of digital transformation of enterprises. At the same time, it should give full play to the positive role of comprehensive financial reform policies to reduce enterprise financing costs and external transaction costs, alleviate the problem of resource constraints, and give appropriate resource support to “escort” enterprises to better apply digital technology.

Second, for the financial comprehensive reform pilot zone for different property rights nature, different industry characteristics and different industry nature of the digital transformation of manufacturing enterprises differences, the financial comprehensive reform pilot zone should adopt differentiated financial policies to stimulate. The digital transformation of manufacturing enterprises is limited by the supply of funds, and those enterprises with insufficient funds have slow digital transformation and insufficient transformation. The central government has set up the National Data Bureau, and the Ministry of Industry and Information Technology has also triggered the “Digital Transformation Guide for Small and Medium Enterprises”, which should be used as an opportunity to vigorously promote digital development, accelerate digital empowerment and increase policy assistance, especially for the backward areas in the central and western regions and enterprises with shortage of funds for digital transformation.

Thirdly, the policy focus of the financial comprehensive reform pilot zone should be placed on easing the financing constraints of enterprises, improving their physical investment, enhancing the level of internal control and the stability of their financial situation, etc., and focusing on creating a more favorable digital innovation environment, promoting enterprises to increase their digital innovation, which in turn will have a significant gain effect on their digital transformation. This will help enterprises to carry out digital transformation.

Fourth, the digital transformation of other industries such as agriculture or service industry is less explored in this paper, which is also a small part of the limitations of this paper, and this paper provides some ideas for other scholars to explore the digital transformation of other industries subsequently. This paper mainly focuses on the impact and mechanism of action of the financial comprehensive reform pilot zone on the digital transformation of manufacturing enterprises. This is because compared with other industries, the manufacturing industry has a stronger demand for digital transformation, and there are problems in the process of digital transformation of manufacturing industry, such as the difficulty of digital transformation of traditional industrial equipment, insufficient supply capacity of industrial software and hardware equipment, non-uniform interface of industrial system platform, and insufficient innovation capacity of industrial big data development, which require a large amount of capital for investment, and thus deeply affect the digital transformation of manufacturing industry The process of digital transformation of manufacturing industry. Therefore, it is important to explore how the financial system in the pilot financial reform zone can influence the transformation of manufacturing enterprises.

Fifth, the current financial system in China is actually a single bank credit, and is dominated by large state-owned banks, small and medium-sized banks are weak, a large number of empirical analysis shows that there is a specialized division of labor in the banking industry based on scale, that is, large banks are mainly to provide loans to large enterprises, while small banks are mainly to small business loans, large banks and small banks to provide financial services, there are obvious systemic differences. Small banks have smaller assets and are unable to provide large loans, and even if they have the ability to provide large loans, it is difficult for the industry to effectively diversify financial risks, as banks need to diversify risks through their asset portfolios. Therefore, the financial comprehensive reform pilot zone may, to a certain extent, be more conducive to the digital transformation of large manufacturing enterprises, while the financial resources for small enterprises may be less supportive, and therefore, it also provides a certain research basis for subsequent scholars to explore the impact of the financial comprehensive reform pilot zone on SMEs.

At the same time, the establishment of the financial comprehensive reform pilot zone can accelerate the construction of a Chinese-style modernized financial system to fully serve the real economy. The main connotation of the Chinese-style modernized financial system as well as the focus is to focus on accelerating the construction of an industrial system with synergistic development of the real economy, science and technology innovation, modern finance and human resources. It is a financial system with high adaptability, competitiveness and universality. It is mainly based on serving the real economy, preventing and controlling financial risks, deepening financial reform as well as returning to the origin, optimizing structure, strengthening regulation and market orientation, so as to promote high-quality financial development.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Jianjiang Liu

Jianjiang Liu is a Professor and Doctoral supervisor at the School of Economics and Management of Changsha University of Technology. His vast research interest include but not limited to Industrial transformation and upgrading, Sino US Economics and Trade Relations, High Housing Prices.

Jie Cheng

Jie Cheng is Master candidate at the School of Economics and Management of Changsha University of Science and Technology. His research area includes Applied economics,industrial economics.

Fidelis Ayangbah

Fidelis Ayangbah is a Ph.D. candidate at the School of Economics and Management of Changsha University of Science and Technology. His rich professional experience cut across operations and Finance. His main research interests include Strategic Management, Enterprise Management, Trade Relations, and International Finance. Email: [email protected]

Notes

1. The concept of “digital transformation” was first introduced by Negroponte (1997), who considered the use of digital technologies in the production process and in business interactions, i.e., the reorganization of digitalization for various production relationships, as digital transformation.

2. Source from the “2021 China Enterprise Digital Transformation Index Research Report” jointly compiled by Accenture and the National Industrial Information Security Development Research Center under the Ministry of Industry and Information Technology.

References

- Ang, J. B. (2010). Research, technological change and financial liberalization in South Korea. Journal of Macroeconomics, 32(1), 457–19. https://doi.org/10.1016/j.jmacro.2009.06.002

- Chun, Y., Tusheng, X., Chunxiao, G., & Sheng, Y. (2021). Digital transformation and corporate division of labor: Specialization or vertical integration. China Industrial Economics, (9), 137–155. https://doi.org/10.19581/j.cnki.ciejournal.2021.09.007

- Cui, R. M., Chen, Y. S., & Li, D. (2021). The establishment of pilot free trade zone and regional economic growth: A study based on dynamic mechanism and spatial driving effect. International Trade Issues, (11), 1–20. https://doi.org/10.13510/j.cnki.jit.2021.11.001

- Dapeng, Y., Mengtao, C., & Mengzhou, X. Can the digital transformation of enterprises inhibit the “de-realization” - an empirical study based on A-share listed companies. Zhejiang Journal, 2023(2), 144–152. https://doi.org/10.16235/j.cnki.33-1005/c.2023.02.022

- DaQian, S., Hai, D., Ping, W., & Jianjiang, L. (2018). Can smart city construction reduce environmental pollution. China Industrial Economy, (6), 117–135. https://doi.org/10.19581/j.cnki.ciejournal.2018.06.008

- Demirguc–Kunt, A., & Maksimovic, V. (1998). Law, finance, and firm growth. Journal of Finance, 53(6), 2107–2137. https://doi.org/10.1111/0022-1082.00084

- Fei, W., Huizhi, H., Huiyan, L., & Xiaoyi, R. (2021). Corporate digital transformation and capital market performance-empirical evidence from stock liquidity. Management World, 37(7), 130-144+10.11–1235. https://doi.org/10.19744/j.cnki.11-1235/f.2021.0097

- Gomber, P., Kauffiman, R. J., Parker, C., & Weber, B. W. (2018). On the FinTech revolution: interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 1(1), 220–265. https://doi.org/10.1080/07421222.2018.1440766

- Hanelt, A., Bohnsack, R., Marz, D., & Antunes, C. (2021). A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. Journal of Management Studies, 58(5), 1159–1197. https://doi.org/10.1111/joms.12639

- Han, R.-D., & Fan, B. (2020). Can regional financial reforms alleviate capital allocation distortions? International Financial Studies, (10), 14–23.

- Hongming, W., Pengbo, S., & Huifang, G. (2022). How can digital finance enable digital transformation of enterprises? –Empirical evidence from Chinese listed companies. Finance and Economics Series, 10, 1–14. https://doi.org/10.13762/j.cnki.cjlc.20220311.001

- Huang, Y., & Shen, Y. (2022). Have financial reform policies eased corporate financing constraints? –A quasi-natural experiment based on the establishment of a comprehensive financial reform pilot zone. Southern Finance, (8), 3–18. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=GDJR202208001&DbName=CJFQ2022

- Hui, L., & Dandan, L. (2020). Mechanisms, paths and countermeasures for digital transformation of enterprises. Guizhou Social Science, 10, 120–125. https://doi.org/10.13713/j.cnki.cssci.2020.10.017

- Jia, Z., Niannian, S., & Fei, W. (2022). Financial market reform and enterprises’ “short loans and long investments”-Chinese experience based on the perspective of interest rate marketization. Business Research, (5), 103–113.

- J, K. O. O., & SHIN, S. (2004). Financial liberalization and corporate investments: Evidence from Korean firm data. Asian Economic Journal, 18(3), 277–292. https://doi.org/10.1111/j.1467-8381.2004.00193.x

- Ke, B., Liu, N. and Tang, S. The effect of anti -corruption campaign on shareholder value in a weak institutional environment evidence from China[R]. SSRN Working Paper,2017.

- Levine, R. (2005). Finance and Growth: Theory and Evidence. In Eds. Handbook of economic growth, edition 1 (Vol. 1. pp. 865–934). Elsevier. https://doi.org/10.1016/S1574-0684(05)01012-9

- LI, P., LU, Y., & WANG, J. (2016). Does flattening government improve economic performance? evidence from China. Journal of Development Economics, 123, 18–37. https://doi.org/10.1016/j.jdeveco.2016.07.002

- Linqi, H., Guangbin, C., & Yali, W. How national-level big data comprehensive pilot zone empowers digital transformation of enterprises[J/OL]. Science and Technology Progress and Countermeasures, 1–11. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=KJJB20220923000&DbName=CAPJ2022

- Mikalef, P., & Pateli, A. (2017). Information technology-enabled dynamic capabilities and their indirect effect on competitive performance: Findings from PLS-SEM and fsQCA. Journal of Business Research, 70(1), 1–16. https://doi.org/10.1016/j.jbusres.2016.09.004

- SERFLING, M. (2016). Firing costs and capital structure decisions. The Journal of Finance, 71(5), 2239–2286. https://doi.org/10.1111/jofi.12403

- Shu Song, B., Xiaohong, L., and Baokun, N., (2005). A Study of the Interaction between Local Governance and Banking Reform in China’s Financial System during the Transition Period. Journal of Financial Studies.

- Shu, X., & Yu, B. (2022). Financing constraints, uncertainty and firm investment structure: An empirical test based on a panel threshold regression model. Research in Financial Economics, 37(4), 80–95. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JIRO202204006&DbName=CJFQ2022

- Tang, S., Qing, L., & Fei, W. (2022). Financial market-oriented reform and digital transformation of enterprises–Empirical evidence from interest rate marketization in China. Journal of Beijing University of Technology and Business (Social Science Edition), 37(1), 13–27. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=BJSB202201002&DbName=CJFQ2022

- Tang, S., Wu, X. C., & Jia, Z. (2020). Digital finance and corporate technology innovation - structural characteristics, mechanism identification and differences in effects under financial regulation. Management World, 5, 52–66+9. https://doi.org/10.19744/j.cnki.11-1235/f.2020.0069

- Ting, J. (2022). Mediating and moderating effects in empirical studies of causal inference [in Chinese]. China Industrial Economics, 5, 100–120. https://doi.org/10.19581/j.cnki.ciejournal.2022.05.005

- Tu, X. Y., & Yan, X. L. (2022). Digital transformation, knowledge spillover and total factor productivity of firms - Empirical evidence from listed manufacturing companies. Industrial Economics Research, 2, 43–56. https://doi.org/10.13269/j.cnki.ier.2022.02.010

- Wang, X., Wang, M., & Zheng, L. (2020a). Have financial reforms promoted high-quality local economic development? Evidence from the establishment of national comprehensive financial reform pilot zones. Comparative Economic and Social Systems. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JJSH202004003&DbName=DKFX2020

- Wang, X., Wang, M., & Zheng, L. (2020b). Have financial reforms promoted high-quality local economic development? –Evidence from the establishment of the National Comprehensive Financial Reform Pilot Zone. Comparative Economic & Social Systems, (4), 11–20. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JJSH202004003&DbName=DKFX2020

- Xiao, N., & Lin, T. A. (2022). A study on the impact of comprehensive financial reform projects on firm innovation - a quasi-natural experiment based on panel data of prefecture-level cities. Technology Economics, 41(7), 34–47. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JSJI202207004&DbName=CJFQ2022

- Xiaolong, L., & Xiaojing, H. (2023). Zheng Qiang Can financial reform policies promote common prosperity? –Empirical evidence from the establishment of national financial reform pilot zones. Xinjiang Social Science, (3), 59–69+150.

- Yang, L. G., Gong, S. H., Wang, P., & Chao, Z. S. (2018). Human capital, technological progress and manufacturing upgrading. China Soft Science, (1), 138–148. https://doi.org/10.16235/j.cnki.33-1005/c.2023.02.022

- Yeting, C., Rui, Z., & Zhigang, S., et al. (2018). Research on the impact of financial reform on total factor productivity—Based on empirical data from five national financial reform pilot zones. China Management Science, 9. https://doi.org/10.16381/j.cnki.issn1003-207x.2018.09.003

- Zeng, H., & Dolado, J. J. (2023-04-3). Revisiting the public-private wage gap in Spain: New evidence and interpretation, Finance and Economics Series. 1–25. https://doi.org/10.1007/s13209-023-00277-z

- Zhang, J., Liu, Y. C., Zhai, F. X., & Lu, Z. (2013). Bank discrimination, business credit and firm development. The World Economy, 36(9), 94–126. https://doi.org/10.19985/j.cnki.cassjwe.2013.09.006

- Zhao, C.-Y., Wang, W.-C., & Xue-Song, L. (2021). How digital transformation affects total factor productivity of enterprises. Finance & Trade Economics, (7). https://doi.org/10.19795/j.cnki.cn11-1166/f.20210705.001

- Zhiyuan, Z., & Yongfan, M. (2023). Government subsidies and firms’ digital transformation–a signaling-based perspective. Economic and Management Studies, 44(1), 111–128. https://doi.org/10.13502/j.cnki.issn1000-7636.2023.01.007

- Ziyao, X., & Lisha, Z. (2022). Digital transformation and corporate expense stickiness - an analysis based on management self-interest perspective. Research in Financial Economics, (4). https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JIRO202204009&DbName=CJFQ2022