?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the inflation-hedging ability of gold in Vietnam from 2011 to 2022. In order to assess how government management has affected the domestic gold market, two local gold prices (SJC and 9999) were employed. The non-linear autoregressive distributed lags (NARDL) approach is applied to analyze the short- and long-run asymmetry between CPI and gold prices. The result reveals that the relationships between CPI and gold prices are non-linear (asymmetric) and gold can only hedge against inflation in the short run. Additionally, the global gold price fluctuations, combined with limited supply, have created a supply shock, causing domestic enterprises to proactively widen the bid-ask spread in both types of gold to mitigate risks, indirectly exacerbating the local-global price disparities.

PUBLIC INTEREST STATEMENT

In Vietnam, inflation has commonly been considered the cause of a loss of public confidence in the national currency, prompting a shift towards alternative safe haven options, with particular emphasis on gold. Nonetheless, the observed discrepancy between the domestic and international gold prices has led to increasing concern among investors regarding the reliability of this precious metal to hedge against market fluctuations. This phenomenon may potentially result in individuals retaining gold for extended periods, as opposed to engaging in frequent market transactions akin to other investment avenues, thereby rendering gold a viable “safe haven” option for mitigating market risks. As a result, the goal of this research paper is to provide more empirical evidence on the ability of gold to hedge against inflation to properly validate gold as a safe or even profitable investment in the Vietnamese market.

1. Introduction

There has been a lot of scholarly interest in the relationship between the price of gold and inflation worldwide (Hoang et al., Citation2016). Some studies have found that gold is a leading signal of inflation because the gold price incorporates information about inflation expectations (Garner, Citation1995; Mahdavi & Zhou, Citation1997; Ranson, Citation2005). Furthermore, gold is predicted to become an inflation hedge in the long term due to its being one of the most sought-after precious metals, meaning that its purchasing power can be preserved for long periods of time (Bampinas & Panagiotidis, Citation2015; Ghosh et al., Citation2004; Levin & Wright, Citation2006).

Traditionally, gold is deemed to have both material and spiritual value in Vietnam. When inflation rises, consumers lose trust in the national currency and seek alternate safe-haven assets, most notably gold, which drives up the gold price (Siregar & Nguyen, Citation2013). However, since the early 2010s, the Vietnamese gold market has been strictly regulated by the government in an attempt to stabilize the market. Particularly, the State Bank has been authorized to implement a government monopoly on the gold bar (SJC gold) production and take responsibility for granting permission to businesses importing gold material (9999 gold). In light of the present domestic circumstances, it is noteworthy that the gold prices in Vietnam, a prominent national gold brand, has exhibited a significant deviation from the prevailing world gold price, resulting in a too large of a difference compared to the benchmark price. However, the disparity noted between the prices of gold within the domestic market and those on the international market has raised significant concerns among investors regarding the reliability of the local gold market as an investment channel. Empirically, evidence from previous studies in the Vietnamese market produced mixed and inconclusive results. Currently, few studies in Vietnam have considered the non-linear relationship between the gold price and inflation. Non-linearity can be caused by macroeconomic fluctuations such as economic depression and policy adjustments (Akgul et al., Citation2015). Hence, choosing a model that specifies the non-linear relationship will appropriately examine the correlation between the gold price and inflation in Vietnam, which is an emerging market with constant changes in the macro environment and government policies.

This research is carried out using the non-linear autoregressive distributed lags model (NARDL) proposed by Hoang et al. (Citation2016) to enrich the empirical data regarding the gold’s ability as an inflation hedge in the short and long run in the Vietnamese market, thereby assisting investors in making sound judgments before engaging in gold trading activities in the context of the Vietnamese market. Additionally, we employ two principal gold products (SJC gold and 9999 gold) representing two distinct governmental degrees of control over the gold market. While SJC gold (gold bar) is exclusively manufactured by the State Bank, 9999 gold (gold material) can be imported by an array of licensed private businesses. The distinction between the linkage of each sort of gold and inflation will shed light on the government’s involvement in the domestic gold market. Thus, some policy proposals will be mentioned to guarantee the stability of the local gold market.

Two issues will be addressed in this study to analyze the link between the gold price and inflation, as well as gold’s potential to hedge against inflation risk in the short and long run. Firstly, is the link between gold prices and inflation asymmetric? Secondly, is gold a short- and long-term inflation hedge? The research will take place in the Vietnamese market, and owing to data collection constraints prior to 2011, the study period will run from January 2011 to December 2022.

Our research found that gold is not a long-term inflation hedge. In the short term, however, investors in Vietnam can utilize gold to hedge against inflation. Furthermore, unlike in other small and emerging markets, the correlations between CPI and local gold prices in Vietnam are asymmetric or non-linear, which may be due to unanticipated swings in global gold prices paired with domestic gold market management regulations. The outcomes of the investigation hold significant ramifications for state authorities as well as individual shareholders. From an investor’s perspective, SJC and 9999 gold exhibit inadequate efficacy as long-term inflation safeguards. Investors may employ the use of gold as a means of safeguarding their financial interests in the near future during periods of escalating price levels. Through the perspective of a policymaker, it is recommended that the Vietnamese government undertake a reassessment of current management approaches employed within the gold market with the aim of promoting its liberalization through the elimination of certain constraints concerning the supply of gold.

The sections are organized into the following categories. Section 2 presents the theoretical and empirical background. Section 3 details the methodological approach in this study. Section 4 specifies the analysis of statistics. Section 5 displays research findings and discussions. Sections 6 concludes the results and gives suggestions for future research.

2. Theoretical and empirical background

2.1. Theoretical background

According to Board of Governors of the Federal Reserve System (Citation2016), inflation is defined as an increase in the prices of goods and services over time. Inflation is not measured by the rise in the cost of a single product or service, or several products and services. Rather, inflation is the increase in the economy’s overall price level of goods and services. Reilly et al. (Citation1970) defined inflation in similar fashion, stating that “Inflation can be defined as an increase in the general price level, or it can be defined as a decrease in the value of the dollar”.

In accordance with the assertions of Bodie (Citation1976), an asset is deemed to be an inflation hedge if it meets any one of the ensuing conditions. Firstly, the asset serves to safeguard the security against adverse market movements. Secondly, the inclusion of the asset has the effect of mitigating the variance of the actual return of the security within the portfolio. Thirdly, there exists a positive correlation between asset values and inflation. Bodie’s (Citation1976) third definition of an inflation hedge has garnered support from a group of studies undertaken by Reilly et al. (Citation1970), Worthington and Pahlavani (Citation2007), Wang et al. (Citation2011), Bampinas and Panagiotidis (Citation2015), as well as Hoang et al. (Citation2016). Besides, depending on the region, sector, or time horizon, certain assets are more suited to hedging inflation than others (Muckenhaupt et al., Citation2023). Indeed, while investigating the inflation-hedging properties of different asset classes, Schlanger et al. (Citation2023) found that commodities have a lower correlation of 0.34 on average, but a significantly larger inflation beta of 7.60. That is, when inflation increases by 1%, commodity prices move by 7.6% on average, making them the best tool that can help offset inflation for the entire portfolio. One of the most commonly used commodities to hedge against inflation in existing literature is gold. This is understandable since gold is widely acknowledged as a store of value and has a relatively inelastic supply, whereas gold demand is reported to be counter-cyclical with macroeconomic conditions (Phochanachan et al., Citation2022).

Another general definition of inflation hedging comes from Rodel (Citation2012), which stated that “An asset hedges against inflation if its real return moves independent of inflation”. The asset used for hedging can be tangible (metal or commodity) or intangible (financial instruments), and the real rate of return for such assets is the annual percentage of profit produced on an investment, which has been adjusted for inflation. Rodel (Citation2012) also agreed with Bodie (Citation1976) that the aim of inflation hedging is to protect existing wealth against inflation. As a result, we can infer that the precious metal, gold, could be considered to be an effective hedge against inflation if it exhibits a correlation with changes in the general price level.

In line with Fisher’s (Citation1930), it can be postulated that an anticipated inflationary trend is likely to cause an upswing in nominal asset rates, thereby inducing a corresponding shift in the value of gold that aligns with the direction and magnitude of the ensuing changes in consumer price levels. In essence, it can be posited that the correlation existing between the price level and the price of gold is indicative of a positive value of 1, thereby establishing gold as an impeccable instrument aimed at mitigating inflationary tendencies. The price of gold is subject to various determinants, including but not limited to demand and supply, interest rates, currency fluctuations, and geopolitical events (The Economic Times, Citation2021). In accordance with the findings of Hoang et al. (Citation2016), it can be inferred that gold may serve as a viable mitigation strategy against inflationary pressures, given its inherent potential to either fully or partially offset the rising in price levels.

Studies by Hoang et al. (Citation2016), Wang et al. (Citation2011), and Beckmann and Czudaj (Citation2013) have attached great importance to the recognition of time series dynamics such as non-linearity and asymmetry when researching econometric models. By definition, non-linearity is a mathematical concept that describes a scenario in which the connection between two variables is not foreseeable from a straight line (Adam, Citation2021). This means that when a linear relationship is plotted on a graph, it produces a straight line, but when a non-linear relationship is plotted, it produces a curve. Asymmetry is one type of non-linearity in which the dependent variable responds differently to the increases and decreases of the explanatory variables. Supposedly, inflation (positive change in CPI) may have a stronger effect on gold prices than deflation (negative change in CPI), which proves to be a case of an asymmetric relationship. As a result, to provide explanations for non-linear phenomena, extensive modeling and hypothesis testing are required. Non-linearity without explanation might result in unpredictable and irregular outcomes. By accounting for potential non-linearity (asymmetry) in the gold—inflation nexus, the dynamic between dependent and independent variables could be explained at a much greater depth.

2.2. Empirical background

Research, concerning the hedging ability of gold, are rich and abundance when it comes to gold’s safe-haven role in the financial market. It seems that gold can mitigate stock market losses, particularly during stressful times, due to its weak or negative correlation with stock market indexes (Yousaf et al., Citation2021). According to Elder et al. (Citation2012), gold responds to macroeconomic fluctuations in a reversed manner and functions differently from other assets, particularly shares, which validates its hedging property with financial instruments. There is evidence to suggest that gold exhibits properties of hedging in relation to Group of Seven (including Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) stock market indices, as demonstrated by Shahzad et al. (Citation2020). Moreover, during times of stability, gold has the potential to serve as a form of safe haven for equities. However, during more volatile periods, such as those characterized by financial stress, gold has been observed to act as a shelter from the risks and uncertainties of the equity market, according to findings of Beckmann et al. (Citation2015). In addition, newly emerged assets such as Bitcoin, which surprisingly shares similar characteristics to gold, has also shown its safe haven and hedging property in foreign countries like Canada (Shahzad et al., Citation2020). However, in the legal frameworks of Vietnam, particularly with respect to Bitcoin, there is no regulations that govern the realm of cryptocurrency transactions, which makes them risky and less appealing from investors’ perspective. Consequently, the conventional function of gold as a safeguard against inflation and equity continues to be the predominant subject matter of inquiry in evaluating the Vietnamese market. Nonetheless, our investigation will undertake a more comprehensive analysis of its characteristics in relation to macroeconomic fluctuations.

The link between gold and oil has been extensively examined as their roles in the economy are rather apparent. Oil is the most widely traded commodity in the world, with the most volatile price in the commodities market. Meanwhile, gold is seen as the market leader in the precious metals sector, since its rise appears to be causing parallel moves in the prices of other precious metals. As a result, oil and gold have been identified as viable possibilities for hedging against volatile financial market changes (Naeem et al., Citation2022). Since oil and gold possess lower volatility and stable returns during periods of volatility, they have become great tools to help diversify investors’ portfolios (Arfaoui et al., Citation2023). However, Naeem et al. (Citation2022) showed that after the global financial crisis, assets classified as commodities have appeared to be more volatile. This is true as Schlanger et al. (Citation2023) revealed that commodities class has the highest inflation beta of 7.60 while that of short-term Treasury inflation-protected securities (TIPS) is only 0.86. Therefore, if inflation rises by 3%, TIPS are predicted to climb 2.6%, but commodities are expected to grow by 22.8%. As a result, a portfolio allocation that favors assets with greater inflation beta would assist safeguard other asset classes, yet with the drawback of increased portfolio volatility. Due to global financial crisis, the fall in oil output has raised concerns about supply, driving up oil prices. This problem is typically harmful to the economy and has a negative influence on growth, causing stock values to fall. When equities are no longer as profitable as they once were, investors may often turn to gold as a substitute asset. Inflation appears to be the most commonly used explanation for the link between oil and gold. Because crude oil is one of the most significant essential items in the economy, as the price of crude oil rises, so does the general price level. In such case, gold is a suitable investment channel, and its price will rise proportionally. This gives rise to the role of gold as an effective hedge against inflation.

Numerous academic investigations have been conducted on the efficacy of gold as a hedge against inflation across various global regions, particularly in the advanced economies of the United States, the United Kingdom, and Japan. The classification of relevant studies pertaining to inflation hedging is based on the definition presented, resulting in two distinct groups. Various studies have been conducted to investigate the capacity of gold to serve as a hedge against inflation. The findings of these studies have been conflicting, with certain studies validating gold’s inflation-hedging capabilities, while others producing contradictory results or failing to establish a definitive correlation between inflation and the price of gold. In Vietnam, empirical research has been conducted to examine the correlation between inflation and gold prices. Nevertheless, the aforementioned studies did not employ a diverse range of models nor yield definitive, unambiguous, and consistent findings regarding the efficacy of gold as a hedge against inflation.

For the first stream of research, according to studies by Ghosh et al. (Citation2004), Levin and Wright (Citation2006), there exists a positive correlation between the price of gold and inflation, with gold being widely regarded as a long-term hedge against inflation. In an investigation of structural shifts, Worthington and Pahlavani (Citation2007) performed a study spanning two distinct timeframes: 1945–2006 and 1973–2006. The findings suggest that investing in gold in both direct and indirect manners serve as an effective strategy for investors to mitigate the impact of inflation. In their study, Beckmann and Czudaj (Citation2013) employed a Markov switching vector error correction model (MS-VECM) to examine the inflation-hedging characteristics of gold. Consequently, gold has the potential to serve as a partial hedge against inflation over a prolonged period, with the United States and United Kingdom exhibiting a stronger correlation compared to Japan and the Euro Area. Bampinas and Panagiotidis (Citation2015) posited that in conducting research within the UK and US markets, gold exhibits a proclivity to effectively hedge against headline inflation, core inflation, and expected inflation in the long-term. Additionally, it is noteworthy that this particular ability exhibits a greater degree of potency in the United States market relative to the United Kingdom market.

There is not much research in Vietnam that support the theory of gold being a hedge against inflation. Than and Le (Citation2014) demonstrated using the Granger Causality Test that rising inflation will result in rising gold prices, and vice versa. Gold is a useful hedge against both current and anticipated inflation, according to Hau et al. (Citation2013) analysis of the non-linear relationship between the gold price and inflation.

For the second stream of research, studies have not discovered any association between the price of gold and inflation, or if they have, the potential of gold to hedge inflation is rated as small or not absolute. As a result, a few studies, like Hoang et al. (Citation2016) and Wang et al. (Citation2011), indicated non-linearity in the link between the gold price and inflation.

In order to evaluate the non-linearity of the link between gold prices and inflation, Wang et al. (Citation2011) used the cointegration approach on the TC-TVECM (threshold cointegration-threshold vector error correction model) in the US and Japan. According to the findings, gold’s capacity to serve as an absolute inflation hedge relies on the market and the time of year. Gold does not function as an inflation hedge over the long run. Gold can only act as a short-term inflation hedge against US prices during periods of high momentum. Furthermore, according to research by Hoang et al. (Citation2016), gold is not a long-term inflation hedge in China, India, Japan, France, the UK, or America. The capacity of gold to hedge against inflation in the short term has varying effects among nations.

Within the Vietnamese market, studies by Siregar and Nguyen (Citation2013), Bui and Nguyen (Citation2014), and Trinh (Citation2017) demonstrate that gold’s potential to hedge inflation is negligible or extremely poor. Siregar and Nguyen (Citation2013) discovered that despite the influence of the gold price on inflation is relatively large, the volatility of inflation has no effect on the gold price when the Markov Switching VAR model (MSVAR) and Granger test are used. Similarly, Bui and Nguyen (Citation2014) found that the influence of CPI on the local gold price is minimal using the VAR model and Granger Causality Test. Trinh (Citation2017) shown, also using the VAR model and Granger test, that the volatility of inflation has no effect on the price of gold, although it marginally impacts inflation.

As a result, research on the hedging potential of gold both globally and domestically have produced contradictory and inconsistent findings. There are two key factors that might be used to account for the variance in those results. First, there are differences in the nations where the survey is conducted and in the preferred times. Time and market selection are the two primary components of an inflation hedge, according to Wang et al. (Citation2011). As a result, choosing diverse study markets and time periods leads to inconsistent or even contrasting outcomes. Second, there are many studies that have not considered the non-linear relationship between gold price and inflation. Conventional studies often assume a linear long-run relationship between gold prices and inflation. When analyzing the relationship of variables in the context of normal business cycles, the linear model can be considered a relatively good model, however, drawn from the experience of the global economic depression in 2008 and the European debt crisis, non-linear models should be given more attention because of their usefulness in observing and explaining asymmetric relationships between variables (Constancio, Citation2014). Therefore, to analyze the relationship between two volatile variables (inflation and gold price) that are strongly influenced by the global economy, political system, and government intervention, choosing a non-linear model is preferable.

2.2.1. Objectives

The main objective of the study is to analyze and evaluate the relationship between gold price and inflation in Vietnam through secondary research based on domestic and foreign research documents and data analysis. The research focuses on the hedging ability of Vietnam gold price in order to assess the feasibility as well as reliability of this precious metal as an investment option. By using both types of gold (9999 and SJC), we are able to consider the effect of State Bank’s regulations in managing the gold market on the ability of gold to hedge against market volatility. Existing studies are either scarce in domestic setting or obsolete and they suffer from data deficit. We aim to provide more updated results in the dynamic between gold price and inflation with emphasis on the impact of Vietnamese government’s management in the gold market.

Vietnam is a small market and has many similarities to the gold market of China and India, so based on the results of Hoang et al. (Citation2016), we believe that gold price and inflation have a symmetrical relationship, and gold is not an inflation hedge in the long run. Besides, a qualitative method will be conducted to investigate this relationship in the short-run to better understand the gold-inflation association. Within the scope of this study, we will use two types of gold prices representing the Vietnamese market, including (1) SJC gold (finished good) and (2) 9999 gold (material), thereby, assessing the inflation hedging of each gold type. The following four hypotheses are considered:

Hypothesis 1:

The relationship between the SJC-gold price and inflation is symmetric.

Hypothesis 2:

The relationship between the 9999-gold price and inflation is symmetric.

Hypothesis 3:

SJC gold is not a hedge against inflation in the long run.

Hypothesis 4:

9999 gold is not a hedge against inflation in the long run.

3. Methodology

Domestic studies on gold and inflation such as those of Bui and Nguyen (Citation2014), Than and Le (Citation2014), Trinh (Citation2017) conducted Vector Autoregression (VAR) technique to measure the two-way effect between these two variables. Because the VAR model is a system of equations, it allows the researcher to evaluate the influence of variables from multiple dimensions. However, the variables in the model need to be stationary at the original order I(0), and the incorporation of non-stationary variables into the model will falsify the research results. Taking into consideration the stationarity of a time series is important. If a series is not stationary, we are only evaluating its behavior in the selected period as the results cannot be applied to other portions of time, meaning that the research has no practical value. That is also the reason that a more popular model used in economic studies is the Vector Error Correction Model (VECM). This model can be considered as an extension of the VAR model, allowing the use of cointegrated non-stationary variables up to the difference of order 2 I(2) (Wang et al., Citation2011). Besides, VECM also consider the short-term relationship between the between the variables and the long-term equilibrium point. Therefore, the research results obtained from this model will have more economic meanings than the VAR model. Another model that also considers the presence of non-stationary variables is the autoregressive distributed lag (ARDL) model. Basically, ARDL is identical to VAR in running only 1 equation, with the only difference being that it allows the evaluation of linear relationships of stationary variables of order 1 I(1) (Hoang et al., Citation2016). In practice, positive or negative changes in the inflation rate will have different effects on gold prices, but all three models VAR, VECM and the original ARDL model assume that the level of influence is the same whether inflation increases or decreases by the same unit. According to Hoang et al. (Citation2016), gold price and CPI interact with each other based on many mechanisms, so the relationship between them would not necessarily be linear. There have not been many foreign studies and especially no research in Vietnam to show this feature in the relationship between the gold price and inflation. Therefore, this study is intended to use the autoregressive distributed lag model on nonlinearity (nonlinear ARDL or NARDL) built by Shin et al. (Citation2014), and applied by Hoang et al. (Citation2016) in the study of the relationship between gold price and inflation in six major gold markets in the world. Because of the ability to separate the variable into two parts, the NARDL model gives us a more detailed and specific view of the influence of the increase or decrease of the independent variable on the dependent variable.

Four benefits of the NARDL approach were outlined by Hoang et al. (Citation2016) while analyzing the correlation between the gold price and CPI. First, the NARDL model assumes that the CPI and gold prices are cointegrated. Second, it assesses the cointegration relationship’s linearity and nonlinearity. Thirdly, it distinguishes between the independent variable’s short-term and long-term effects on the dependent variable. Considering the three criteria mentioned above, the choice of NARDL has given the research topic excellent empirical data. Up until now, investigations on this connection in Vietnam have largely only employed one approach, namely the vector autoregression (VAR) model. However, even though the cointegrated VECM employed by Wang et al. (Citation2011) offers the same three benefits as those listed above, this approach may run into duplication issues or convergence issues if the equation has an excessive number of factors. NARDL does not experience this issue. Fourth, NARDL is not constrained by the need that time series have the same association order, making it feasible to use NARDL on data series with diverse association orders. This is in contrast to other error correction models.

The use of the NARDL model is completely consistent with the research purpose of the research group. Since the group is only interested in the effect of the inflation rate fluctuation on the gold price to draw conclusions about the degree of hedging of gold against inflation, the assessment of the impact of gold on inflation is not necessary and it is not essential to apply more than one equation. Besides, the NARDL model also provides the group with more information about the increase and decrease of inflation for the gold price, so the group can draw more meaningful conclusions after the analysis. At the same time, the proposed model also meets the requirement that the independent variable has a few exogenous factors and only one cointegration relationship.

3.1. NARDL model for the relationship between inflation and gold price (SJC/9999)

The complete model of the asymmetric relationship in both short and long-term between the gold price and CPI will have the following form:

In which, is the gold price variable;

is the inflation variable. Both of which are determined by the natural logarithm of the gold price and the consumer price index, respectively, to provide a more stable distribution as studied by Huynh (Citation2018) and Hoang et al. (Citation2016).

and

are asymmetric long-term parameters,

and

are asymmetric short-term parameters, the symbols (+) and (-) represent the increasing and decreasing changes.

To be regarded a perfect hedge against inflation, the positive long-term/short-term parameters must be near to one. Besides, when considering the ability of the gold to protect investors from inflation, the parameters () for positive variables (

) if negative will no longer be meaningful because when the consumer prices rise, the price of gold falls, contradicting the definition of a hedge against inflation mentioned above.

The Wald test can be used to determine if the long-term symmetric effect exists using the null hypothesis . The following variables are used to calculate the long-term coefficients for both positive and negative changes in the relationship between inflation and the price of gold:

The parameters and

, respectively, represent the short-term positive and negative changes in

, which represent the short-term adjustments of

. Similarly, the Wald test on the null hypothesis

can be used to determine if the short-term symmetry effect exists for all

.

4. Statistical analysis

Data on the SJC gold price, 9999 gold price, global gold price, and consumer price index were obtained using observational sampling for the period from January 2011 to December 2022 (144 observations). The selling price of one Troy ounce of gold at the last trading session of each month is the gold price, which is compiled by the Doji Group in Vietnam. Data for the consumer price index is derived from the websites of Trading Economics and the General Statistics Office (GSO).

The gold market in Vietnam showed a strong and vibrant development in the early 2000s but became unstable and risky during the global economic crisis. In response, the government issued a series of policies to tighten gold market activities and stabilize the economy. One of these policies was Decree 24/2012/ND-CP published in 2012 on the management of the gold business that assigned the State Bank the task of organizing and managing the domestic gold market. Accordingly, SJC gold production is under the control of the State and is subject to stringent regulation by the government. Meanwhile, 9999 gold is categorized as a regular commodity used in gold jewelry production and can be imported by private enterprises if they have authorization from the government. Nevertheless, over the past 10 years, the State has not manufactured more SJC gold and granted permits for private businesses to import 9999 gold. Therefore, there is a scarcity in the supply of both types of gold.

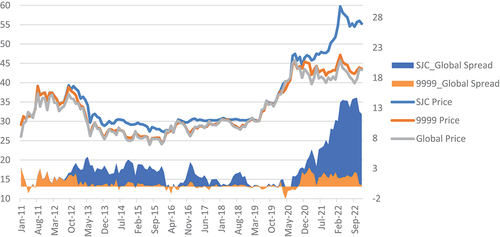

Vietnamese culture has a long-established affinity with gold. Traditionally, Vietnamese people frequently hoard gold as a dowry for their offspring or to protect their assets from devaluation in the context of macroeconomic turbulence. Despite the substantial demand, imports account for the bulk of the domestic gold supply. Therefore, domestic gold prices (9999 gold and SJC gold) follow the same trend as the price of global gold (Figure ), however in recent years, the prices of these two forms of gold, particularly SJC gold prices, have unexpectedly increased significantly relative to the worldwide price.

Figure 1. Gold price (Unit: VND million per troy ounce).

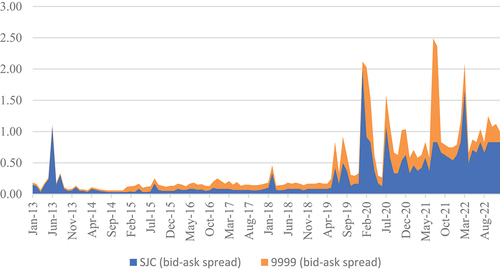

An explanation is that businesses in Vietnam are very risk-aversion and are worried about the unpredictable global gold prices and limited local supply, thereby actively reserving gold and raising the selling price far beyond the buying to avoid risks (Figure ). Additionally, in recent years, the demand for SJC gold and 9999 gold has surged as a result of the removal of pandemic limitations and worries about rising inflation. In particular, in 2022, WGC reported a high record of an increase of 52% in gold jewelry demand and 32% in gold bars demand (World Gold Council, Citation2022). These reasons explain the phenomenon that the domestic gold price, particularly SJC, has increased significantly relative to the world price since 2020.

Figure 2. Bid–ask spread (Unit: VND million per troy ounce).

Since 2013, there has been a decline in the prices of gold at the regional level subsequent to a peak that was attained in 2011 and 2012. One plausible explanation for the aforementioned phenomenon is that during the period of inflationary stability, the Vietnamese currency retained its value and ceased to depend heavily on gold reserves. Moreover, the financial and currency markets across the globe displayed instability, while crude oil prices exhibited a persistent decline, thereby adversely affecting the value of gold. Moreover, as the value of currency escalates beyond a specific threshold, there is a tendency among investors to liquidate their gold holdings in favor of more profitable ventures, resulting in a downward spiral of gold prices.

According to Figure , in 2019, the escalation of gold prices can be attributed, in part, to worldwide geopolitical conditions, including the tense relationship between the United States and North Korea, military confrontations in Central America, the United Kingdom’s exit from the European Union (Brexit), and ongoing protests in Hong Kong. In 2020, the value of gold experienced a significant increase as a result of the global economic crisis, prompting investors to seek refuge in secure assets.

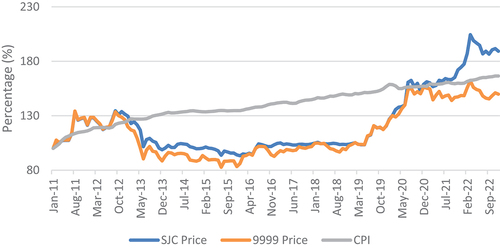

Figure 3. Gold price and CPI.

5. Results and discussions

The ARDL cointegration model, as posited by Nkoro and Uko (Citation2016), is a suitable approach for incorporating integrated variables of differing orders (i.e., those at either root I(0) or first difference I(1)) into an analysis. The proposed model exhibits limitations in its applicability to variables situated at the second difference of integration, denoted as I(2), as the F-statistic in this context would lack interpretability. In the present study, the stationary tests employed for two distinct variables pertaining to gold prices and CPI follow the same approach as utilized by Huynh (Citation2018), comprising the utilization of ADF (Augmented Dickey-Fuller) and PP (Philips-Perron) tests. In addition, the KPSS (Kwiatkowski-Phillips-Schmidt-Shin) test has also been incorporated for the aforementioned purpose.

In Table , the ADF and PP tests’ interpretation is as follow:

H0:

There is a unit root (Series is non-stationary)

H1:

There is no unit root (Series is stationary)

Table 1. Unit root test

If the estimated p-value is less than the 5% level of significance, we reject H0 and accept the alternative hypothesis H1. Both the ADF and the PP reject the null hypothesis that the observed time series is autocorrelated and preserve the alternative hypothesis that it is stationary.

The KPSS test stands apart from the other two tests in that it does not pertain to the identification of unit roots. The null hypothesis of the KPSS test, which posits that the time series is stationary, represents a marked differentiation from the ADF test’s null hypothesis. Thus, the two methods of interpreting p-values can be deemed equivalent. In the event that the p-value exceeds the level of significance, it can be concluded that the series is non-stationary. Nevertheless, the scrutinized sequence would demonstrate stationarity in the ADF test.

The analysis results reveal that the gold price variables have exhibited stationary behavior at the first differencing level (I(1)) across all three tests. However, the CPI variable has demonstrated stationarity at the zeroth differencing level (I(0)) according to both ADF and PP tests, and at the first differencing level (I(1)) according to the KPSS test. The disparity in outcomes with regards to the unit root test conducted on cpit could potentially stem from the existence of structural interruptions in the time series of said macroeconomic indicator. The issue is addressed in greater depth within Table . Upon integration of the identified structural breaks into the unit root analysis of the chosen variables, it remains feasible to execute a NARDL regression model.

Table 3. Structural break

5.1. Test for the long-run and short-run symmetry of the time series

It may be inferred that, in contrast to other nations in Asia (China and India), as noted in Hoang et al. (Citation2016)’s research, the influence of inflation on gold prices in Vietnam is asymmetric or non-linear in both the short and long run. As a result, both hypotheses 1 and 2 are rejected. Although the three markets share numerous cultural parallels, according to Hoang et al. (Citation2016), India and China have already liberalized the gold market for over 20 years. On the contrary, the management policy of tightening supply continues to dominate the Vietnamese gold market. According to the analysis, the supply shock widened the gap between domestic and worldwide gold prices. The link between gold and inflation in the country may differ from that in other countries due to how the market is managed.

There is one significant breakpoint when the natural logarithms of prices of SJC shift unexpectedly, which is March 2020. In the case of 9999 gold price, the break is in January 2020. The structural breaks in 2020 appear to be influenced by the potential economic impacts of the COVID-19 epidemic, which coupled with the limited gold supply have forced prices of this precious metal to be inflated. During the first quarter of 2020, a new strain of coronavirus broke out in many countries around the world, causing the stock market and energy market to go down due to concerns about the impact of this disease on the global economy. The first quarter of 2020 is also the time when the trade war between U.S and China started to settle down, yet its impact on the global economy remains.

Since dummy variables corresponding to structural break are significant, it is safe to assume that gold prices in Vietnam react to the fluctuations of global gold prices as they reflect the macro trends in the economy, and this theory will be tested by incorporating new independent variable to the regression model to represent the global price of gold throughout the researching period.

5.2. Test for the ability to hedge against inflation of gold prices in short-run and long-run

Two variables, and

, represent the long-term asymmetry in gold prices. The coefficient for positive changes in the association between the price of 9999 gold and CPI is not significant. When the SJC price is used in the NARDL model, a substantial and negative long-run impact coefficient associated to positive changes in the CPI on gold prices (

) can be seen. However, this demonstrates that when the CPI rises, the price of SJC falls, which goes against the section 2 and 3 definition of inflation hedge. As a result, neither gold price could be viewed as a long-term hedge against Vietnam’s inflation. This solidifies hypotheses 3 and 4. Moreover, in both instances, the coefficients linked to negative fluctuations (

) are considerably negative. This means that gold prices would move in the other direction during periods of falling CPI (deflation), and it appears that the price of SJC is more sensitive to inflation than the price of 9999.

The short-run effects of CPI on gold prices are significant in both cases as shown in and

coefficients. As previously stated, there are asymmetric relationships of both SJC (case 1) and 9999 (case 2) with CPI. Since all positive variables of CPI are positive and significant, investors would be able to benefit from investing in SJC gold in times of inflation in the short-run. In the second case, the coefficients depicting the positive changes of CPI in the short-run are significant. This indicates that 9999 could also be used as protection for investors during times of inflation.

Although both types of gold indicate a short-run correlation with inflation variables, the different lag length with which these coefficients are significant (3 in SJC case and 0 in 9999 case) show that SJC and 9999 react to inflation in dissimilar nature. This can be explained by the fact that SJC gold bar is regarded as a special commodity and is strictly regulated by the government, while 9999 gold is gold material and is categorized as a normal commodity. Even though their supply are both limited by the Government, the degree of control State Bank has on SJC is far higher than that on 9999. SJC is chosen as a national brand and only the State Bank of Vietnam has the right to produce it. This regulation could potentially interfere with the relationship between the price of SJC and the rate of inflation in Vietnam as we analyze in section 4.

The influence of CPI on the value of 9999 gold is distinct from that observed for SJC. The determination of the long-term equilibrium between gold prices and the CPI is facilitated through the use of the SJC methodology, whereas such equilibrium cannot be ascertained with respect to 9999 gold (as shown by the insignificant ). The result show that the long-run relationship between the price of 9999 gold and CPI does not exist yet. This could mean that holding SJC gold for a long period of time will probably be more beneficial for investors in stressful periods of the economy. The primary goal of short-term analysis is to evaluate the immediate impacts of changes in exogenous variables, namely the CPI, on the dependent variable of gold prices. Conversely, the long-term analysis aims to assess the duration and velocity of the adaptation process towards an equilibrium point. The concept of a short-term relationship between gold prices and inflation suggests a swift response of gold prices to fluctuations in inflation, whereas the notion of a long-term relationship implies an equilibrium correlation between these two factors over a prolonged duration.

From the Table we can see that long-run coefficients ( and

) and short-run coefficients (

and

) of global price variable are all statistically significant. This means that the global price of gold is confirmed to have a big influence on the domestic price of gold in Vietnam. One percent point increase in global price leads to a 0.8799 percent point increase in SJC price (positive relation), and a 1 percent point decrease in global price leads to a 1.1560 percent point decrease SJC price (also positive relation). In the case of 9999 gold, the correlation for positive changes is 1.03% while the correlation for negative changes is 1.07%. Both types of gold react in a similar fashion to the increase/decrease of the global price of gold, which testifies to the fact that prices of this metal in Vietnam respond closely to the fluctuations in the world market. Also, it is important to note that by inserting the new variable into the regression model, its overall R squared, and Adjusted R square have increased significantly, implementing that

is indeed a valuable independent variable to include in the research model.

Table 5. Estimation of NARDL model (Local gold prices – Global gold price – CPI)

When global gold price is added, none of the inflation coefficients are significant in the model. We can further conclude that both types of gold are not eligible for inflation hedging in Vietnam. The findings contradict those of Ghosh et al. (Citation2004), Levin and Wright (Citation2006), Worthington and Pahlavani (Citation2007), and Bampinas and Panagiotidis (Citation2015), who found that gold might serve as a long-term inflation hedge in an American context. However, a number of studies, including those by Hoang et al. (Citation2016), Wang et al. (Citation2011), and Beckmann and Czudaj (Citation2013), share the same result that gold is not a long-term inflation hedge.

In summary, hypotheses 1 and 2 regarding the symmetric correlations between inflation and each type of local gold price are rejected. In addition, the hypothesis 3 and hypothesis 4 were supported by the results. This finding confirms the conclusion of Hoang et al. (Citation2016) that gold is not a long-term inflation hedge. Also, it may be said that gold can be used by investors to reduce the risk of inflation in the short term. Furthermore, the relationship between gold prices and CPI in Vietnam shows an asymmetric manner. This is because the increase in the global gold price, along with the limited supply due to the Government management policies have caused a supply shock, which made domestic enterprises proactively widen the bid-ask spread in both types of gold to reduce risks. Besides, following the outbreak, the domestic demand for gold increased, but the supply did not. As a result, the domestic gold price rose and is currently substantially higher than the international gold price.

Since 2020, domestic gold prices has been moving in an unexpected and volatile manner, which can be explained by the fact that both types of gold are subjected to the fluctuations of global gold price due to the supply shortage as a result of the Government’s control on the gold market. To accommodate the current status of the Vietnamese gold market, the policy should be reviewed and updated in the sense of increasing supply for both types of gold. In particular, the Government may think about letting go of SJC’s exclusive role and enabling qualified companies to produce their own gold bar brands. In addition, we suggest creating the National Gold Exchange in order to address concerns about the 9999 gold and allowing private companies to trade gold materials there for the purpose of producing gold jewelry.

5.3. Robustness check

In this section, as applied by Hoang et al. (Citation2016), we will investigate the time-frequency dependency of the previous results by employing a new quarterly data set, instead of monthly. Overall, the results of unit root test and structural breaks remain the same, which allows us to move on to checking the symmetric relations through Wald tests and NARDL results.

From Tables , it appears that the asymmetry still exists in both the long- and short-run correlation between the two types of gold prices and CPI. Therefore, we can conclude that the time frequency of data does not exhibit a significant effect on the determination of the NARDL model.

Table 6. Wald test for short- and long-run symmetry (with quarterly data)

Table 2. Wald test for short- and long-run symmetry

When we compare NARDL results in Table to those obtained with monthly data (Table ), we find no discernible difference in the hedging property of both types of gold against inflation. In both cases the long-term coefficients related to positive changes ( and

) are not statistically significant, meaning that SJC and 9999 gold do not serve as a hedge against inflation in the long run. The short-term coefficients, however, are positive and significant at different lags. This indicates that people can invest in either type of gold to hedge against periods when the general price level in the Vietnamese market goes up. Based on the results in Tables , we could conclude that with regards to the function of gold as a hedge against inflation, the impact of changes in data frequency varies in accordance with the domestic gold market.

Table 7. Estimation of NARDL model (Local gold prices – Global gold price—CPI) (with quarterly data)

Table 4. Estimation of NARDL model (Local gold prices and CPI)

6. Conclusions

Geopolitical difficulties, economic uncertainty, the pandemic, and Central Banks’ quantitative easing policies have all contributed to the increased emphasis given to inflation worries in recent years. In light of this, gold, one of the most valuable and long-lasting assets, has been considered to be an inflation hedge.

This study examined the correlation between the inflation index and the prices of different kinds of gold in Vietnam, focusing in particular on the value of gold as an inflation hedge from January 2011 to December 2022. The two types of gold used in this study article are SJC (gold bars) and 9999 (gold materials), which are the two primary gold products in the Vietnamese market.

The study’s findings have implications for both governments and individual investors. From the standpoint of the investor, SJC and 9999 gold are both ineffective long-term inflation hedges. Investors might use gold to safeguard themselves in the short term while the price level is rising.

From the policymaker’s standpoint, Vietnamese government should reevaluate the management measures implemented on the gold market to liberalize it by removing some constraints regarding the gold supply. In terms of SJC gold, in order to balance supply and demand and satisfy the public’s appetite for investment and hoarding, the authorities should take into consideration revoking the monopoly and instead, licensing competent private companies to produce gold bars. With regard to 9999 gold, the Government should consider establishing a National Gold Exchange to meet the demand for gold as raw material for jewelry production.

The analysis of the regression model’s results reveals that, given the low R squared criterion, the single inflation variable is insufficient to fully account for the swings in gold prices on the Vietnamese market. Because of the unique characteristics, the gold price in Vietnam in particular and the relationship between gold and domestic inflation are very different from those of other markets in the region like India and China.

Future studies are advised to incorporate additional independent factors including exchange rates, interest rates, import taxes, oil price volatility, and stock market volatility into account. While describing the changes in domestic gold prices, it is important to have a complete understanding of how the gold market functions. New conclusions and insights may be drawn from the study model by including other variables, as a consequence, more precise and beneficial suggestions for bodies of authority could be inferred.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgments

This work was supported by the National Economics University, Hanoi, Vietnam. The authors report there are no competing interests to declare.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study are openly available in figshare at https://doi.org/10.6084/m9.figshare.22720519.v1

Additional information

Funding

Notes on contributors

Minh Duc Do

Do Minh Duc is the General Director of DOJI Group, Vietnam, and is currently a PhD student at NEU. Under the guidance of Prof. Dat, Mr. Duc is working on a topic related to the gold market in Vietnam, with the help of other postgraduate students: Ms. Nhung, Ms. Mai and Mr. Hieu. This paper is part of his research project.

Tho Dat Tran

Tran Tho Dat is a Professor and the Chairman of University’s Academic Board, Co-Director of CFVG (French-Vietnamese Center for Management Education), National Economics University (NEU), Hanoi, Vietnam. Prof. Dat received his PhD in Statistics from NEU in 1991 and a PhD in Economics from the Australian National University in 2000. His publications have appeared in various international journals, and conference proceedings. His research interests include higher education financing, credit markets, growth models, monetary policy, knowledge management, innovation management, economics of climate change, digital economy, and environmental sustainability.

References

- Adam, H. (2021, November 17). Nonlinearity. Investopedia. https://www.investopedia.com/

- Akgul, I., Bildirici, M., & Ozdemir, S. (2015). Evaluating the nonlinear linkage between gold prices and stock market index using Markov-Switching Bayesian VAR models. Procedia-Social & Behavioral Sciences, 210, 408–18. https://doi.org/10.1016/j.sbspro.2015.11.388

- Arfaoui, N., Yousaf, I., & Jareno, F. (2023). Return and volatility connectedness between gold and energy markets: Evidence from the pre- and post-COVID vaccination phases. Economic Analysis and Policy, 77, 617–634. https://doi.org/10.1016/j.eap.2022.12.023

- Bai, J., & Perron, P. (2003). Computation and analysis of multiple structural change models. Journal of Applied Econometrics, 18(1), 1–22. https://doi.org/10.1002/jae.659

- Bampinas, G., & Panagiotidis, T. (2015). Are gold and silver a hedge against inflation? A two-century perspective. International Review of Financial Analysis, 41, 267–276. https://doi.org/10.1016/j.irfa.2015.02.007

- Beckmann, J., Berger, T., & Czudaj, R. (2015). Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16–24. https://doi.org/10.1016/j.econmod.2014.10.044

- Beckmann, J., & Czudaj, R. (2013). Gold as an inflation hedge in a time-varying coefficient framework. The North American Journal of Economics & Finance, 24, 208–222. https://doi.org/10.1016/j.najef.2012.10.007

- Board of Governors of the Federal Reserve System. (2016). federalreserve.gov/faqs/economy_14419.htm.

- Bodie, Z. (1976). Common stocks as a hedge against inflation. The Journal of Finance, 31(2), 459–470. https://doi.org/10.1111/j.1540-6261.1976.tb01899.x

- Bui, K. Y., & Nguyen, K. H. (2014). Quan ly gia vang nhin tu goc do kinh te vi mo [Gold price management from macroeconomics perspective]. Tap chi Phat trien va Hoi nhap, 19(29), 67–75. https://user-cdn.uef.edu.vn/newsimg/tap-chi-uef/2014-11-12-19/9.pdf

- Constancio, V. (2014, December 15). Nonlinearities in macroeconomics and finance. European Central Bank. https://www.ecb.europa.eu/home/html/index.en.html

- The Economic Times. (2021, May 13). 5 factors that influence price of gold. https://economictimes.indiatimes.com/wealth/invest/5-factors-that-influence-price-of-gold/articleshow/82341650.cms

- Elder, J., Miao, H., & Ramchander, S. (2012). Impact of macroeconomics news on metal futures. Journal of Banking & Finance, 36(1), 51–65. https://doi.org/10.1016/j.jbankfin.2011.06.007

- Fisher, I. (1930). The theory of interest. Macmillan.

- Garner, C. A. (1995). How useful are leading indicators of inflation? Federal Reserve Bank of Kansas City Economic Review, 80(2), 5–18.

- Ghosh, D., Levin, E. J., Macmillan, P., & Wright, R. E. (2004). Gold as an inflation hedge? Studies in Economics and Finance, 22(1), 1–25. https://doi.org/10.1108/eb043380

- Hau, L. L., Ceuster, M. J. K. D., Annaert, J., & Amonhaemanon, D. (2013). Gold as a hedge against inflation: The Vietnamese case. Procedia Economics and Finance, 5, 502–511. https://doi.org/10.1016/S2212-5671(13)00059-2

- Hoang, T. H. V., Lahiani, A., & Heller, D. (2016). Is gold a hedge against inflation? New evidence from a nonlinear ARDL approach. Economic Modelling, 54, 54–66. https://doi.org/10.1016/j.econmod.2015.12.013

- Huynh, T. H. (2018). Bang chung moi ve tac dong bat doi xung cua thay doi ty gia hoi doai len gia chung khoan tai Viet Nam [New evidence for the asymmetric impact of change exchange rate to securities prices in Vietnam]. Journal of Asian Business and Economic Studies, 29(2), 40–62. https://digital.lib.ueh.edu.vn/handle/UEH/58339

- Levin, E. J., & Wright, R. E. (2006). World Gold Council. https://www.researchgate.net/publication/255647201_Short-run_and_Long-run_Determinants_of_the_Price_of_Gold

- Mahdavi, S., & Zhou, S. (1997). Gold and commodity prices as leading indicators of inflation: Tests of long-run relationship and predictive performance. Journal of Economics and Business, 49(5), 475–489. https://doi.org/10.1016/S0148-6195(97)00034-9

- Muckenhaupt, J., Hoesli, M., & Zhu, B. (2023). Listed real estate as an inflation hedge across regimes. Swiss Finance Institute Research Paper No. 23-13.

- Naeem, M. A., Hasan, M., Arif, M., Suleman, M. T., & Kang, S. H. (2022). Oil and gold as a hedge and safe-haven for metals and agricultural commodities with portfolio implications. Energy Economies, 105, 105758. https://doi.org/10.1016/j.eneco.2021.105758

- Nkoro, E., & Uko, A. E. (2016). Autoregressive Distributed Lag (ARDL) cointegration technique: Application and interpretation. Journal of Statistical and Econometric Methods, 5(4), 63–91.

- Phochanachan, P., Pirabun, N., Leurcharusmee, S., & Yamaka, W. (2022). Do Bitcoin and traditional financial assets act as an inflation hedge during stable and turbulent Markets? Evidence from high cryptocurrency adoption countries. Applied Mathematics in Finance and Economics, 11(7), 339. https://doi.org/10.3390/axioms11070339

- Ranson, D. (2005). Inflation protection: Why gold works better than ‘linkers’. H.C. Wainwright & Co. working paper.

- Reilly, F. K., Johnson, G. L., & Smith, R. E. (1970). Inflation, inflation hedges, and common stocks. Financial Analysts Journal, 26(1), 104–110. https://doi.org/10.2469/faj.v26.n1.104

- Rodel, M. G. (2012). Inflation hedging: An empirical analysis on inflation nonlinearities, infrastructure, and international equities. Technische Universitat Munchen.

- Schlanger, T., Li, C., Maciulis, V., & Ahluwalia, H. (2023). Constructing inflation-resilient portfolios. Vanguard Research. https://corporate.vanguard.com/content/dam/corp/research/pdf/constructing_inflation_resilient_portfolios.pdf

- Shahzad, S. J. H., Bouri, E., Roubaud, D., & Kristoufek, L. (2020). Safe haven, hedge and diversification for G7 stock markets: Gold versus Bitcoin. Economic Modelling, 87, 212–224. https://doi.org/10.1016/j.econmod.2019.07.023

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Springer Science & Business Media, 281–314. https://doi.org/10.1007/978-1-4899-8008-3_9

- Siregar, R., & Nguyen, T. K. C. (2013). Inflationary implication of gold price in Vietnam. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2265689

- Than, T. T. T., & Le, T. T. H. (2014). Kiem dinh moi quan he giua vang va lam phat tai Viet Nam [Testing the relationship between gold price and inflation in Vietnam]. An Giang University Journal of Science, 3(2), 58–62. https://www.zun.vn/tai-lieu/kiem-dinh-moi-quan-he-giua-gia-vang-va-lam-phat-tai-viet-nam-53687/

- Trinh, T. P. T. (2017). Moi quan he giua gia vang va lam phat tai Viet Nam [The relationship between gold price and inflation in Vietnam] [ Master thesis]. Available from Ho Chi Minh University of Banking’s database.

- Wang, K. M., Lee, Y. M., & Nguyen, T. B. N. (2011). Time and place where gold acts as an inflation hedge: An application of long-run and short-run threshold model. Economic Modelling, 28(3), 806–819. https://doi.org/10.1016/j.econmod.2010.10.008

- World Gold Council. (2022, March 28). Gold demand trends full year 2022. https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2022.

- Worthington, A. C., & Pahlavani, M. (2007). Gold investment as an inflationary hedge: Cointegration evidence with allowance for endogenous structural breaks. Applied Financial Economics Letters, 3(4), 259–262. https://doi.org/10.1080/17446540601118301

- Yousaf, I., Bouri, E., Ali, S., & Azoury, N. (2021). Gold against Asian stock markets during the covid-19 outbreak. Journal of Risk and Financial Management, 14(4), 186. https://doi.org/10.3390/jrfm14040186