Abstract

Given the pervasive effects that COVID-19 and previous pandemics had on companies, the purpose of this study was to develop pandemic-related sustainability reporting guidelines to improve corporate reporting. Pandemic-related reporting was found to be a necessary part of companies’ sustainability disclosure. However, this is not required by any South African or international sustainability framework scrutinised by the researchers. Literature proves the wide-ranging effects of pandemics on companies’ sustainability, though current reporting practices are lacking. The researchers consequently developed corporate reporting guidelines that specifically require and formalise pandemic-related disclosure, through applying grounded theory. With the lack of pandemic-related reporting requirements in existing corporate sustainability frameworks, this study is the first, according to the researchers’ knowledge, to propose corporate reporting guidelines to inform stakeholders of companies’ sustainability regarding pandemics. Framework setters could use these guidelines by incorporating it into existing reporting requirements. The guidelines serve to encourage pandemic-related disclosure by companies with a genuine interest in sustainability. Such disclosure would provide important information for stakeholders, especially given the recurring yet unprecedented nature of pandemics.

1. Introduction

COVID-19 shocked the global economy in a faster and more severe manner than the 2008 financial crises, the Second World War, and the Great Depression (Roubini, Citation2020). The pandemic and ensuing lockdown resulted in an unparalleled stock market crash (Albuquerque et al., Citation2020). With every component of demand in an unprecedented freefall, the US market plummeted by 20% within 15 days, the fastest decline in history (Roubini, Citation2020). The fiscal stimulus to companies and individuals introduced by policymakers amidst the global financial crises that took around three years to implement was implemented within a month during COVID-19 (Hassan et al., Citation2021). COVID-19 has, however, also presented several opportunities, such as shifting business models (Seetharaman, Citation2020) and realising the value of supplementing business with virtual strategies (Nguyen et al., Citation2020) and sustainable production (Rowan & Galanakis, Citation2020). Furthermore, COVID-19 emphasised the interdependency between people, the planet and profits, shifting attention towards social and environmental matters (Adams & Abhayawansa, Citation2022).

Similarly, previous pandemics have had both positive and negative effects on companies’ sustainability, which sometimes take several years to play out (Jordá et al., Citation2020; Littman & Littman, Citation1973; Quantec, Citation2020). Literature consequently evidences the vast effects of pandemics on companies’ sustainability (Moolman et al., Citation2023a).

With numerous pandemics occurring from as early as 429 B.C. (Cirillo & Taleb, Citation2020), one would think that pandemics would be expected every so often. Indeed, though it is hard to predict the onset of a pandemic, experts have repeatedly warned against it (Pinner et al., Citation2020) and data are available to assess and prepare for this risk (Pegram, Citation2020). However, COVID-19-inflicted chaos emphasised that companies are not prepared for pervasive global risks and consequently, mitigation strategies have had little to no consideration (Abhayawansa & Adams, Citation2022).

Furthermore, with biodiversity loss through land used for agricultural or urban purposes, the likelihood of zoonotic infectious diseases in humans increases (Gibb et al., Citation2020). Species are being lost 1 000 times faster than ever before and several species are on the brink of extinction (United Nations, Citation2019). Further loss in biodiversity and extinction of species is considered to be one of the greatest threats to the planet (Roberts et al., Citation2021) and human activity is the key driver thereof (Atkins et al., Citation2018). However, biodiversity loss is merely one of the current sustainability issues.

Further issues include climate change, poverty and inequality. In 2015, all United Nations Member States adopted the 2030 Agenda for Sustainable Development, which sets out 17 sustainable development goals (SDG) (United Nations, Citation2015), which work towards a more sustainable future. Sustainability is a global challenge that has attracted enormous attention in recent decades (He et al., Citation2018; Nobanee et al., Citation2021). Sustainable development became a key environmental concern during the 1980s and 1990s (Tregidga et al., Citation2014). In 1987, sustainability was defined as “meeting the needs of the present without compromising the ability of future generations to meet their own needs” (United Nations, Citation2022). Sustainability consists of four components: financial, as well as environmental, social and governance (ESG). This is as sustainability has both financial and non-financial paradigms (Tregidga et al., Citation2014), where non-financial matters generally refer to ESG matters (Hayat & Orsagh, Citation2015). Furthermore, sustainability has been linked to the interplay between people, the planet and profit (Adams & Abhayawansa, Citation2022).

As part of the drive towards sustainability, companies’ disclosures on ESG matters have exponentially increased in recent years (KPMG, Citation2017; Mattison et al., Citation2022; Solomon & Maroun, Citation2012). This signals a shift from reporting exclusively on financial performance to how companies create sustainable value (Chinn et al., Citation2021). Companies’ awareness of the impact their operations have on ESG and economic issues, as well as communicating and addressing these issues, have been dubbed with the term corporate social responsibility (CSR) (Hughen et al., Citation2014). Stakeholders are increasingly relying on non-financial data for decision-making and are pressuring companies to promote CSR (Chinn et al., Citation2021; Hughen et al., Citation2014; Mattison et al., Citation2022). While the limitations of non-financial reporting are realised, it has driven companies’ consciousness towards sustainable operations (Atkins et al., Citation2018; Higgins & Walker, Citation2012).

However, there is the concern that companies whose survival has pervasively been threatened by the pandemic-related crisis may abandon expensive environmental sustainability initiatives, undermining nature (Amankwah-Amoah, Citation2020). Yet, globally, companies that were environmentally responsible and transparent regarding sustainability activities during the indefinite COVID-19 period reaped the rewards, including reduced risk exposure and stock volatility and increased investment and stock returns (Adams & Abhayawansa, Citation2022; Broadstock et al., Citation2021; Whieldon et al., Citation2020). Furthermore, social responsiveness has been associated with long-term profits (Hassan et al., Citation2021): amidst COVID-19, the portfolios of companies with strong ESG performance significantly outperformed the rest of the market while experiencing lower return volatility (Albuquerque et al., Citation2020; Broadstock et al., Citation2021; Whieldon et al., Citation2020). Literature therefore evidences the benefit of strong ESG performance, which is communicated to stakeholders through these companies’ CSR reporting.

The social element of CSR reporting considers the effect of a company’s operations on all its stakeholders, aligning with the principles of the stakeholder theory (Elson & Goossen, Citation2017; Roberts, Citation1992). The stakeholder theory necessitates value-creation for all stakeholders through obtaining a balance between ethics and capitalism (Parmar et al., Citation2010). Furthermore, in line with the legitimacy theory, CSR reporting is also used by companies to display that they operate in accordance with societal norms, which grants them a social license to operate and access to resources that they would otherwise not be entitled to (Deegan, Citation2002, Citation2019; Ehnert et al., Citation2016; Lanis & Richardson, Citation2013).

Communication forms a key part of CSR (Hughen et al., Citation2014) and is also vital in reducing uncertainty (Maruping et al., Citation2019; Redmond, Citation2015). Furthermore, communication forms part of disaster risk management (Coppola, Citation2011). Given the unprecedented nature of pandemics and the uncertainty of their effects, it would, therefore, be expected that companies would report extensively on pandemics.

Numerous frameworks (internationally and in South Africa) exist regarding CSR disclosure, providing companies with guidelines regarding corporate sustainability reporting. The researchers scrutinised several of these (the International Integrated Reporting Framework (IIRF) (International Integrated Reporting Council [IIRC], Citation2021), the King Code (Institute of Directors South Africa, Citation2016), the Financial Times Stock Exchange/Johannesburg Stock Exchange (JSE) Responsible Investment Index Series (Financial Times Stock Exchange Russell, Citation2020), the Global Reporting Initiative (GRI) Standards (GRI, Citation2020), the Dow Jones Sustainability Indices (S&P Dow Jones Indices, Citation2019), the Organisation for Economic Co-operation and Development (OECD) Guidelines (OECD, Citation2011), the Communication on Progress (United Nations, Citation2008), ISO 26,000 (International Organization for Standardization, Citation2010) and International Financial Reporting Standards 7 (International Accounting Standards Board, Citation2020)), yet none provide pandemic-related reporting guidelines. Considering the severe effect of pandemics on companies’ sustainability and that businesses have been considering pandemics as a material risk since 2006 (World Economic Forum, Citation2021) pandemic-related reporting would be expected as part of CSR disclosures. Disregarding this lack of guidelines and without following a formal structure, companies included extensive COVID-19-related reporting in their annual reports after the pandemic’s outbreak, but pandemic-related reporting prior to the outbreak was severely lacking (Abhayawansa & Adams, Citation2022; Moolman et al., Citation2023b).

Furthermore, Abhayawansa and Adams (Citation2022) noted a gap in research and devoted reporting guidance on pandemic-related disclosure. Though they commence to address this, their recommendations are limited to risk disclosures, without providing guidelines on the detail that companies should disclose (Abhayawansa & Adams, Citation2022). Adams et al. (Citation2020) also provided recommendations for SDG disclosure, explicitly addressing the communication of consequences for and impact on achieving the SDG. These recommendations were informed by the recommendations of the Taskforce on Climate-related Financial Disclosure, the GRI Standards (GRI, Citation2020), and the IIRF (IIRC, Citation2021), but still do not address pandemic-specific disclosure. The authors consequently aimed to develop pandemic-related sustainability reporting guidelines to improve corporate reporting.

Given the lack of pandemic-related reporting requirements in existing CSR disclosure frameworks, this study proposes one overarching disclosure requirement, as well as ten disclosure guidelines, serving as guidance to companies to achieve the overarching disclosure requirement. All these guidelines can be applied by companies in the presence of a current pandemic, but certain guidelines are also specified for application in the absence of a pandemic, given its frequent and recurring nature. Such disclosure would provide important information for stakeholders, especially given the recurring yet unprecedented nature of pandemics. Framework setters could use these guidelines by incorporating it into existing CSR reporting requirements. The guidelines serve to encourage companies with a genuine interest in sustainability towards the inclusion of pandemic-related disclosure as part of their CSR reporting.

In the remainder of this article, the methods employed in developing the pandemic-related sustainability reporting guidelines are set out in part 2, followed by a discussion of the results, the developed guidelines, in part 3. Part 4 concludes with the findings of the study, as well as its contribution, limitations and future research avenues.

2. Methods

In this article, grounded theory was used to compile the reporting guidelines as it was developed inductively through systematically collecting and analysing related data (Flick, Citation2011; Merriam & Tisdell, Citation2016).

2.1. Sample

This article used a combination of extant literature and annual reports of companies listed on the JSE. EDS, the foremost directory service of libraries, was used to identify relevant extant literature. On 1 March 2021, a keyword search on abstracts was conducted (Williams, Citation2019) using the following search string: pandemic OR epidemic; AND company OR entity OR organisation OR institution; AND sustainability; AND impact. Given the topical nature of pandemics, the only limits specified were for English and full-text records. After removing duplicate records and examining the records for relevance (Kauppi et al., Citation2018; Vrontis & Christofi, Citation2019), 30 relevant records remained.

Furthermore, annual reports of large companies immediately prior to and one year into, COVID-19 were included. Large companies were focussed on as their emancipatory disclosure is generally more (Abhayawansa & Adams, Citation2022). Similar to Marx (Citation2008) and Coetzee (Citation2010), this study selected the top 40 JSE-listed companies and scrutinised them per industry to ensure that at least the two largest companies per industry were included. This was done to ensure the representation of all sectors in the data. The sector JSE classification (the ICB) was used. The JSE confirmed that there was only one company in the “Additional” industry and none in the “Utilities” industry (personal communication, JSE, 2021). Consequently, the sample consisted of 45 companies (Table ).

Table 1. Company sample

2.2. Data and analysis

The grounded theory method generally applies inductive analysis, where the research process commences with data collection and repeated observation, allowing for inferences to be formed (Bowen, Citation2006; De Villiers, Citation2015; Saunders et al., Citation2019). Inductive reasoning is suited to theory building as it uses established principles to generate unproven conclusions (Saunders et al., Citation2019). The grounded theory method requires recurrent interplay between the collection and analysis of data, leading to theory building (Bowen, Citation2006). Hence, a constant comparative method was used to identify patterns, similarities and differences.

Following Glaser (Citation1965), the researchers followed four stages in conducting the constant comparative method: “(1) comparing incidents applicable to each category, (2) integrating categories and their properties, (3) delimiting the theory and (4) writing the theory”.

2.2.1. Stage 1: Comparing incidents applicable to each category

Using the selected records, the researchers focussed on pandemic-related data (pandemics, epidemics and COVID-19) as incidents. Through open coding (Kolb, Citation2012), incidents were coded to all applicable analysis categories, and while coding, it was compared with previous incidents in the same category. Therefore, incidents linked to the same code name were compared to one another, and soon, theoretical characteristics of the category emerged (Glaser, Citation1965). The researchers’ thinking regarding a category was broadened to include consideration of the circumstances that trigger the category and the related consequences, its dimensions and its relation to other categories. In a time where conflict in thought was experienced, it was not coded. Still, time was taken to reflect on thinking and the ideas were recorded in a memo to capture the researchers’ theoretical notions. This systematic recording allowed the researchers to return to the data for further coding and comparison (Glaser, Citation1965).

2.2.2. Stage 2: Integrating categories and their properties

Whereas the constant comparative units commenced from comparing incidents, it evolved to comparing incidents to characteristics of the category through the use of axial coding (Kolb, Citation2012). In time, the diverse characteristics of the category became integrated with other categories, allowing the researcher to piece data together in new ways (Glaser, Citation1965). Consequently, reasonable deductions could be made after through consideration of the data and the findings from the narrative literature review (Bowen, Citation2006).

2.2.3. Stage 3: Delimiting the theory

The final stage of coding, selective coding, allows the theory to be delimited, as it requires the core category to be established (Kolb, Citation2012), which took place at two levels. Firstly, the theory solidified as significant changes reduced while comparing the incidents of a category to the characteristics thereof. In time, modifications rather related to clarifying the categories and the details of their characteristics with interrelated categories and reduction followed. Reduction reveals concepts based on finding underlying similarities in the information to the researcher (Kolb, Citation2012). These concepts were, in turn, used to write the theory, thereby establishing its terminology. This reduction process and resulting generalising required by constant comparisons consequently led to the achievement of two key theory requirements: definition parsimony (short and exact definitions to avoid confusion) and generalisability (Wacker, Citation2008). Secondly, this stage delimits the initial list of proposed categories. As the researcher interrogated the data, the analysis became more focussed and time was dedicated to constantly compare the incidents to a smaller set of categories. Theoretical saturation, which is necessary to confirm that sufficient information has been gathered to draw appropriate deductions (Kolb, Citation2012), also assisted to establish the initial list of proposed categories. Incidents were hence only coded and compared if they pointed to a new feature of the category due to it not having further value to generating the theory.

2.2.4. Stage 4: Writing the theory

The captured memos provided detail behind the categories, which were the theory’s fundamental concepts. The drafting of the theory commenced by collating, summarising and further analysing the memos on each category, followed by writing about it. The coded data served to validate and provide illustrations regarding the theory. The drafted reporting guidelines (the theory) form a conceptual framework, being the result of a qualitative process of theorisation (Jabareen, Citation2009).

2.3. Trustworthiness of developed reporting guidelines

As described, a systematic process was followed in developing the reporting guidelines. In addition, after developing the guidelines, the guidelines were sent to industry experts on sustainability for their opinion and input. Purposive sampling, which is often used in qualitative research and involves deliberately choosing appropriate participants based on knowledge, experience and willingness (Etikan et al., Citation2016), was used to select the industry experts. Feedback was received from industry experts of three different accounting firms: an international firm with more than 200 000 staff members globally, a regional firm with two branches and 58 staff members (including seven partners) and another regional firm with two branches and 22 staff members (including four partners). The feedback received was incorporated into the developed guidelines to enhance the quality of the findings and the contribution of the study.

2.3.1. Ethical considerations

A study approval number (NWU-00884-20-A4) was awarded to this study by the North-West University’s Economic and Management Sciences Research Ethics Committee. The data used in this study involve only publicly available data, as well as comments from industry experts on sustainability. Consent for the use of the comments was obtained from the industry experts.

3. Results

The concepts included in this study formed the conceptual framework and, therefore, the pandemic-related sustainability reporting guidelines to improve corporate reporting. The reviewed data indicated that the core theoretical argument is that pandemics profoundly affect companies’ sustainability in various ways and that these effects result in certain responses by companies (and require specific disclosure in line with CSR).

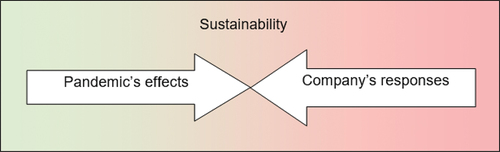

Figure displays the core theoretical argument, and that, should a pandemic’s overall negative effect be more significant than the appropriate responses introduced by a company, the company’s sustainability will be threatened. Contrarily, should a company’s appropriate responses be greater than the overall negative effects introduced by the pandemic, the company’s sustainability will be improved. This is in line with Isaac Newton’s third law of motion, stating that, for every action, there is an equal and opposite reaction (Britannica, Citation2022).

Figure 1. Pandemics affect the sustainability of companies and these effects result in certain responses by companies.

Furthermore, the core theoretical argument is informed by the fact that pandemics have a recurring nature (Cirillo & Taleb, Citation2020). The disclosure guidelines, therefore, serve to achieve:

Forward-looking, proactive disclosure relating to risk mitigation given the possibility of future pandemics (addressed in Disclosure guideline 1 to 6).

Disclosure relating to present pandemics (addressed in all ten of the disclosure guidelines).

The overarching disclosure requirement is outlined in Table .

Table 2. Overarching disclosure requirement

Figure provides a visual representation of this article’s conceptual framework. While still displaying the study’s core theoretical argument, the figure also includes the seven concepts or categories identified by the researchers, which underpin the core theoretical argument. The first concept relates to companies’ responses, whereas the latter six concepts relate to pandemics’ effects. These seven underpinning concepts are subsequently discussed, followed by disclosure guidelines. These disclosure guidelines serve as guidance to companies to achieve the overarching disclosure requirement.

Figure 2. Conceptual framework for reporting guidelines to inform stakeholders of companies’ sustainability regarding pandemics.

3.1. Companies’ responses to pandemics relate to the four phases of disaster risk management: prevention or mitigation, preparedness, responses and recovery

Pandemics are sources of harm or danger (Canadian Centre for Occupational Health and Safety, Citation2020; Collins Dictionary, Citation2020) that evolves into disasters if the community’s responses thereto are insufficient (Coppola, Citation2011; Federal Emergency Management Agency, Citation2006). Pandemics consequently require disaster risk management, which is defined as “the application of disaster risk reduction policies and strategies to prevent new disaster risk, reduce existing disaster risk and manage residual risk, contributing to the strengthening of resilience and reduction of disaster losses” (United Nations Office for Disaster Risk Reduction [UNDRR], Citation2015). The four phases of disaster risk management are generally referred to as prevention or mitigation, preparedness, response and recovery (Albris et al., Citation2020; Ihlen et al., Citation2011):

Though discussing how companies prevent or mitigate pandemics may seem controversial, research shows that unsustainable practices are vital in driving pandemics (Jones et al., Citation2008; McKinsey and Company, Citation2022; Osterholm, Citation2005; Poudel, Citation2020). Consequently, disclosure of companies’ focus on sustainable practices and linking it to pandemics may inform stakeholders that the company is, at the very least, not driving the occurrence of pandemics.

Disclosure of companies’ preparedness for pandemics forces companies to consider the related risks and develop strategies to mitigate pandemics’ negative effects should they occur (Abhayawansa & Adams, Citation2022).

Effective responses to pandemics reduce the negative effects of pandemics on companies’ sustainability (UNDRR, Citation2015) and grant companies the prospect of capitalising on opportunities that pandemics may bring (Rowan & Galanakis, Citation2020; Seetharaman, Citation2020).

The recovery phase after a pandemic provides companies with an opportunity to “Build Back Better” (UNDRR, Citation2015).

Consequently, Table sets out Disclosure guideline 1.

Table 3. Disclosure guideline 1

3.2. Pandemics affect all four components of companies’ sustainability: financial, ESG

The effects that pandemics have on companies are on all components of sustainability, being financial, ESG. The combination of financial, ESG matters provides a comprehensive perspective on sustainability (Kannenberg & Schreck, Citation2019). Environmental issues involve matters around climate change, pollution and deforestation; social issues involve matters around diversity, client satisfaction and staff; and governance issues involve matters around board composition and committees and political contributions (Hayat & Orsagh, Citation2015). Previous studies identified several sustainability elements of companies that are affected by pandemics, which were categorised to the four components (Moolman et al., Citation2023a, Citation2023b). Effects on the financial component include changes in commodity demand and prices. Effects on the environmental component include the improved environmental impact due to decreased operations and companies that increased their awareness of their effect on the environment. Effects on the social component include threats to socio-economic rights and stakeholder engagement. Effects on the governance component include changes in board and shareholder meetings, as well as companies’ strategies. These effects have been encapsulated in Disclosure guideline 2 (Table ).

Table 4. Disclosure guideline 2

3.3. Pandemics’ effects comprise the effects of the pandemic itself, as well as the effects due to governmental interventions

Pandemics itself is a pervasive global threat. For example, COVID-19 was declared a global public health emergency (World Health Organisation [WHO], Citation2020a), automatically affecting companies’ stakeholders. COVID-19 did not only lead to the loss of more than six million lives (Worldometer, Citation2022) but had severe mental effects and significantly altered working environments (Giorgi et al., Citation2020; Kontoangelos et al., Citation2020). Previous pandemics also severely affected humankind (e.g., Cirillo & Taleb, Citation2020). On the other hand, governments intervene by providing fiscal support and introducing regulations to manage pandemics’ effects (e.g., Glencore, Citation2020). The International Monetary Fund (IMF, Citation2021) tracked the policy responses to COVID-19 of 197 economies. For example, the South African government assisted companies and employees through the Unemployment Insurance Fund and Industrial Development Corporation programmes (IMF, Citation2021). Regulations were also implemented to address, prevent and combat the spread of COVID-19 in terms of the Disaster Management Act 57 of (Citation2002) (2002), including several requirements regarding the restriction on the movement of persons and goods, screening and testing programmes for continuing operations, prohibition on evictions and contact tracing. Some consider these government-imposed restrictions as being primarily responsible for the economic contraction (BHP Group, Citation2020) and disruptions to companies’ operations (Azam et al., Citation2021). Quarantine, isolation and similar interventions to restrict the movement of persons and goods have been implemented during pandemics since 1374 (Alfani & Murphy, Citation2017; Correia et al., Citation2020). Table , therefore, sets out Disclosure guideline 3.

Table 5. Disclosure guideline 3

Though this guideline applies to current and future pandemics, it would not be possible for companies to foresee the specific governmental interventions of future pandemics, especially given that certain interventions can be considered irrational, like the tobacco ban that was implemented in South Africa during the lockdown (Egbe & Ngobese, Citation2020). Though companies would, therefore, only be able to describe specific government interventions for current pandemics, it is still recommended that companies disclose their awareness that government-imposed interventions may follow future pandemics.

3.4. Pandemics affect a company’s sustainability in the short, medium and long term

Though the short, medium and long term is not defined in the IIRF, it sets out considerations to determine it. Specifically, the IIRF states that time frames differ depending on the industry or sector, as well as the nature of outcomes (IIRC, Citation2021). Markgraf (Citation2019) explains that the short term is within 12 months, medium term is one to four or five years, and long term is thereafter. Literature has evidenced that pandemics have effects in all of these time frames. For example, some companies liquidate within a few months after a pandemic (Stats, Citation2021) (short term), whereas the global economy may be detrimentally affected within two years subsequent to a pandemic (Goodman, Citation2020) (medium term). Furthermore, Jordá et al. (Citation2020) noted pandemics’ effects for more than 20 years after the pandemic started (long term). Consequently, Disclosure guideline 4 is set out in Table .

Table 6. Disclosure guideline 4

3.5. Pandemics’ effects on companies’ sustainability can be negative, positive or neutral

Abundant literature evidences the negative effects of pandemics on companies. These include loss in lives and livelihoods of companies’ stakeholders (McKinsey and Company, Citation2022), extensive financial pressures (Amidei et al., Citation2020) and an increase in waste and pollution due to masks and additional packaging material used during the pandemic (Sarkodie & Owusu, Citation2020). Positive effects noted after pandemics include opportunities brought forward (PR Newswire, Citation2020) and a drop in real interest rates (Jordá et al., Citation2020). On the other hand, some changes are neutral. This includes the increased need for support and communication by stakeholders due to the uncertainties introduced by pandemics (Gow & Grant, Citation2010; Macaninch et al., Citation2020). Disclosure guideline 5, therefore, follows (Table ).

Table 7. Disclosure guideline 5

Though this guideline is applicable to current and future pandemics, it would not be possible for companies to foresee especially the positive and neutral effects of a future pandemic, as it is likely to depend on the type of pandemic and governments’ reaction thereto. Though companies would, therefore, be able to describe the detailed negative, positive and neutral effects of current pandemics, it is still recommended that companies disclose their awareness that negative, positive and neutral effects may follow future pandemics and that the company is, as far as possible, prepared to mitigate negative effects, capitalise on positive effects and implement neutral changes.

3.6. Pandemics are to be expected, yet unique, and increase a company’s risk exposure in the presence, and in the absence, of pandemics

Though future pandemics can be expected, it is, by nature, unprecedented and involves high uncertainty (Nkengasong, Citation2021). Pandemics, therefore, introduce new or increase existing risks for companies (Abhayawansa & Adams, Citation2022; Moolman et al., Citation2023b). These risks include:

Strategic risk—This is the risk that an incident intervenes with a company’s business model, hindering its value proposition (AccountingTools, Citation2022).

Liquidity and credit risk—Liquidity risk refers to the inability of a company’s assets to be converted into cash swiftly (Kenton, Citation2021), often manifesting in credit risk, pointing to the possibility of a company defaulting on its liabilities (Harper, Citation2021).

Legal risk—The potential of loss due to not applying or incorrectly applying the law (Larkin, Citation2022).

Reputational risk—The likelihood of a negative public perception, negative publicity or an event that adversely affects a company’s reputation (Sickler, Citation2019).

Fraud risk—The potential of loss due to an act of deliberate deception to take advantage of a victim (Chen, Citation2022).

Cyber risk—The risk of loss due to a failure of a company’s information technology systems (Institute of Risk Management, Citation2022).

Health and safety risk—The potential for an individual to suffer harm or an adverse health effect through exposure to a hazard (SafetyWallet, Citation2021).

Retention and attraction risk—The likelihood that an entity cannot retain or attract the necessary human resource talent (SIAPartners, Citation2021).

Succession risk—The potential that a vacancy in a key role cannot be filled appropriately within an acceptable period (State Service Authority, Citation2015).

The following serves as an example to explain how these risks are triggered during a pandemic:

A pandemic threatens people’s health, especially the already vulnerable (Vahia et al., Citation2020; World Health Organization [WHO], Citation2020b) (triggering health and safety risks). Governments consequently introduce laws and regulations during a pandemic, e.g., the Disaster Management Act 57 of (Citation2002) (2002) (non-compliance triggers legal and reputational risks). These government-imposed restrictions limit the movement of persons and goods, and companies that require on-site employees cannot continue with or uphold production (Anglogold Ashanti, Citation2020) (triggering strategic risk). Furthermore, while limiting employees’ exposure to the pandemic, these restrictions may interfere with set occupational health and safety regulations, e.g., hindering emergency services (BHP Group, Citation2020) (triggering health and safety risk). Pandemics trigger an increase in competition for critical skills (Firstrand, Citation2020) (triggering retention risk) and also limit companies’ ability to recruit necessary employees (Vodacom Group, Citation2020) (triggering attraction and succession risk). Companies consequently utilise digitisation to continue operations (Brown, Citation2020; Macaninch et al., Citation2020) but are then required to protect the movement of sensitive and confidential information (Amidei et al., Citation2020) (triggering legal, cyber, reputational and fraud risks). Companies also apply for external funding to secure additional cash flow and liquidity to alleviate the pandemic’s financial consequences (Sarkodie & Owusu, Citation2020) (triggering liquidity and credit risks).

Pandemics also drive further uncertainties regarding assets’ value, affecting provisions and impairments (Barloworld, Citation2020). The pervasive threat to a company’s sustainability also threatens its ability to continue as a going concern (BID Corporation, Citation2020).

Risk evaluation and mitigation are not only necessary during a pandemic but also in the absence of a pandemic. Given the severe threats presented by pandemics, companies need to be prepared to swiftly and appropriately respond to reduce the havoc that follows amidst a pandemic (Abhayawansa & Adams, Citation2022; Chanyasak et al., Citation2021). Companies, therefore, need to display their awareness of the likelihood of future pandemics and the strategies in place to evidence their preparedness for such a pervasive global risk (Abhayawansa & Adams, Citation2022).

Given the unprecedented nature of pandemics, communication is essential as it reduces uncertainty (Maruping et al., Citation2019; Redmond, Citation2015). Therefore, knowledge sharing is crucial throughout the phases of disaster risk management of pandemics. In the prevention and preparedness phases, it assists to achieve mutual perceptions when evaluating risks and engaging stakeholders (Albris et al., Citation2020). When responding to pandemics, accurate and timely information is necessary to co-ordinate crises management. During recovery, information allows for reflection and restoration (Albris et al., Citation2020).

Table , therefore, sets out Disclosure guideline 6, along with detailed considerations of effects and responses that companies can incorporate in their disclosure.

Table 8. Disclosure guideline 6

3.7. Pandemics affect a company’s operating environment, input, operations and output

This is in line with the IIRF’s process through which value is created, conserved or destroyed (IIRC, Citation2021), which specifically refers to the external environment (operating environment), inputs, business activities (operations), and output.

3.7.1. Operating environment

A company’s external operating environment affects its ability to create value and may be influenced by factors including economic conditions, competition, the pace of technological change, the regulatory environment and societal issues, needs and interests (Machuki & Aosa, Citation2011; IIRC, Citation2021). Accordingly, companies are required to adapt to its environment to attain success (Janković et al., Citation2016).

During pandemics, this environment is generally unfavourable, indirectly impacting companies’ operations. Governments introduce several policy responses to assist companies and individuals, as well as legal and regulatory requirements to manage the effect of pandemics (IMF, 2021). Among others, these governmental interventions may introduce screening, isolation and quarantine measures and limit the movement of persons and goods, pervasively affecting operations (e.g., Disaster Management Act 57 of Citation2002). Pandemics contract economic growth severely (Correia et al., Citation2020) and the effects are often not short-lived (Prosus, Citation2020), increasing the risk of global recessions (Ajam, Citation2020; Fernandes, Citation2020). Companies consequently operate in an environment where the pandemic has wreaked havoc on their stakeholders as well, resulting in decreased spending available for companies’ commodities (Ajam, Citation2020; Chanyasak et al., Citation2021; Fernandes, Citation2020; Nicola et al., Citation2020; Stats, Citation2021).

Since COVID-19 played out during the fourth industrial revolution and hence a time of swift technological change (Lavopa & Delera, Citation2021), it provided companies with the opportunity of different business approaches, including conducting business from an e-commerce platform and remote working, which ensured continuity (Quilter PLC, Citation2020). Though such strategies may ensure companies’ survival (GMO Research, Citation2020), it also broadens competition (Standard Bank Group, Citation2020). Similarly, future pandemics may introduce opportunities and threats to a company’s operating environment.

Consequently, Table sets out Disclosure guideline 7, along with detailed effects and responses that can be considered as part of corporate disclosure.

Table 9. Disclosure guideline 7

3.7.2. Inputs

Input refers to the elements used in the process of generating a specific product or service (Ackermann, Citation2022). During pandemics, the most pertinent change to input (both material and labour) often relates to its scarcity and increased or volatile costs. A company may not be able to source another company’s output due to their production being hindered (Islam, Citation2021), and labour availability may be restricted through travel restrictions and quarantine requirements (Harmony, Citation2020). Product price shocks occur due to the significantly altered demand (Azam et al., Citation2021; Bhosale, Citation2020). Personnel-related costs increase due to increased sick leave (Gow & Grant, Citation2010), companies wanting to reward staff for their work during the climax of pandemics (e.g., Clicks Group, Citation2020), and substantial amounts are spent on health care to protect companies’ employees from the pandemic (e.g., Montauk Holdings, Citation2020). Disclosure guideline 8 follows, including detailed effects and responses to be considered (Table ).

Table 10. Disclosure guideline 8

3.7.3. Operations

Operations are the daily activities that companies engage in to create value (Coroporate Finance Institute, Citation2022) and are not only hindered by the effects of the pandemic itself but also through government-imposed restrictions (Azam et al., Citation2021). These policies restrict travel and limit on-site staff, hindering production (AngloGold Ashanti, Citation2020). Where possible, operations are adapted, e.g., through digitising operations by enabling employees to work from home and conducting virtual meetings and training (Brown, Citation2020; Macaninch et al., Citation2020). While working from home, employees face increased personal issues as they must balance online working and home-schooling their children, while their well-being is threatened, causing companies to deal with increased employee issues (Amidei et al., Citation2020; Prosus, Citation2020). Furthermore, some activities, such as certain training and stakeholder engagement activities, cannot be digitised, leading to it being cancelled or delayed (Aspen Pharmacare Holdings, Citation2020; Brown, Citation2020).

The pressure of a pandemic tends to reveal companies’ weaknesses, e.g., in a company’s adaptability or structure (Coetzee et al., Citation2021; Macaninch et al., Citation2020), and therefore creates an opportunity for these to be addressed and improve operations (Barry, Citation2010; Coetzee et al., Citation2021).

Pandemics as a result require companies to implement strategic management by giving due attention to pervasive matters affecting the company’s long-term health (Gluck et al., Citation1980). Responses may include suspending non-essential operations, adding new product or service lines (following changed consumer demand), securing liquidity and leveraging fiscal support (Chanyasak et al., Citation2021).

Consequently, Table presents Disclosure guideline 9, including detailed effects and responses to be considered as part of corporate disclosures.

Table 11. Disclosure guideline 9

3.7.4. Output

Input and output correlate strongly (Ackermann, Citation2022) and as pandemics pressure both companies’ input and operations, a severe drop in global production is to be expected (Islam, Citation2021). In addition, the drop in demand for companies’ commodities further hinders companies’ output (Kenny, Citation2020). Consequently, the selling prices of companies’ output become volatile. Companies are urged to increase their selling prices where supply shortages are experienced (Anglo American, Citation2020), the demand increased (Sibanye-Stillwater, Citation2020), or input and operational costs increased. Contrarily, the drop in demand for certain commodities forces selling prices down (Azam et al., Citation2021). These considerations are brought together in Disclosure guideline 10 (Table ).

Table 12. Disclosure guideline 10

4. Conclusion and contributions

Sustainability has become a key consideration to stakeholders and companies increasingly engage in CSR, including disclosing these initiatives (Chinn et al., Citation2021; Hughen et al., Citation2014; Mattison et al., Citation2022). However, pandemics are a pervasive threat to companies’ sustainability, given its recurring nature and severe effects (Abhayawansa & Adams, Citation2022; Cirillo & Taleb, Citation2020; Pegram, Citation2020; Pinner et al., Citation2020). In the absence of formal pandemic-related corporate sustainability guidelines, disclosure in times of pandemics is largely emancipatory, following no specific structure (Moolman et al., Citation2023b). Furthermore, disclosure in the absence of pandemics is severely lacking (Abhayawansa & Adams, Citation2022; Moolman et al., Citation2023b). A lack of reporting generally displays companies’ unpreparedness, indicating the need to make the requirement for pandemic-related reporting explicit (Abhayawansa & Adams, Citation2022; Adams et al., Citation2020), especially given society’s augmented expectation of companies to increase their CSR in times of pandemics (Sibanye-Stillwater, Citation2020). Consequently, this study provided detailed pandemic-related sustainability reporting guidelines to improve corporate reporting.

As part of CSR disclosure, a company should describe pandemics’ effects on the company’s sustainability, including its responses thereto.

In describing the company’s responses to a pandemic:

a company should disclose its disaster risk management strategies in the four phases: prevention or mitigation, preparedness, responses and recovery.

In describing the effects of pandemics on a company’s sustainability and the company’s responses, it should be considered that:

Pandemics affect all four components of sustainability: financial, ESG.

Pandemics’ effects comprise the effects of the pandemic itself, as well as the effects of government-imposed interventions.

Pandemics affect a company’s sustainability in the short, medium and long term.

Pandemics’ effects on a company’s sustainability can be negative, positive or neutral.

Pandemics are to be expected, yet unique, and increase a company’s risk exposure in the presence, and in the absence, of pandemics.

Pandemics affect a company’s operating environment, input, operations and output.

The disclosure guidelines (1 to 10) provided in this study can be used in the presence, but also in the absence of pandemics. More specifically, during pandemics, companies should consider all the guidelines provided (disclosure guidelines one to ten), whereas companies should consider Disclosure guidelines 1 to 6 for future pandemics.

Given that the data underlying the study included consideration of all industries, the researchers contend that these guidelines could be generalised to any industry. Furthermore, though the study focussed on pandemics, the researchers contend that these guidelines could be generalised to any major communicable disease. The researchers also assert that including these guidelines in corporate sustainability frameworks would encourage the necessary disclosure of such a pervasive global threat in companies’ reporting. Such pandemic-related disclosure as part of companies’ value creation story would be of interest to stakeholders concerned about the company’s sustainability (Abhayawansa & Adams, Citation2022; IIRC and Kirchhoff Consult AG, Citation2020). Though regulatory intervention may not improve disclosure quality, the researchers are of the opinion that companies with a genuine awareness of sustainability would work towards providing the necessary disclosure in the interest of stakeholders (Panfilo & Krasodomska, Citation2022). Furthermore, while these guidelines would be an emerging form of CSR reporting, even these are able to change perceptions and work towards creating an improved world (Atkins et al., Citation2018).

Implementing the recommended pandemic-related disclosure guidelines would, however, result in additional costs related to non-financial reporting. Companies would therefore be required to consider this cost versus the benefit of providing stakeholders with information regarding the companies’ preparedness for, and, where applicable, responses to such a pervasive risk. Companies’ focus should remain on providing information regarding its sustainability which is relevant to stakeholders’ decision-making (e.g., IIRC, Citation2021). Another factor that may affect companies’ pandemic-related disclosures, is cultural dimension. In this sense, Pizzi et al. (Citation2022) found that companies with a long-term orientation and an appropriate balance between indulgence and restraints would more likely disclose SDG information.

The methods employed in this study may be considered a limitation thereto. Firstly, given that grounded theory was used to develop the guidelines, the underlying data influences the findings of the study, and therefore also the proposed guidelines. However, the authors contend that robust processes were followed to determine the underlying data and to develop the guidelines. Furthermore, considering that purposive sampling was applied in selecting the industry experts, the findings regarding the trustworthiness of the developed guidelines may have been different using another sampling method. However, given that the experts included feedback from an industry expert from an international firm, it is contended that the feedback is appropriate.

Some areas for further research follow. Research relating to quantifying the effects of pandemics and government-imposed interventions on companies’ sustainability may encourage companies to be effectively responsive to future pandemics (Atkins et al., Citation2015). Studies on separating the effects of pandemics itself versus government-imposed interventions may aid governments in evaluating the appropriateness of the interventions. Finally, evaluating pandemic-related effects on companies’ sustainability per industry may be helpful in developing industry-specific disaster risk management preparation in light of future pandemics.

Author contributions

A. M. acquired, analysed and interpreted the data (the majority of the research). J.F. contributed towards the conception and design of the study. V. L. assisted with the systematic review methodology, analysis and interpretation of the data. All authors contributed towards drafting the works.

Disclaimer

The views expressed in the submitted article are the authors’ own and not an official position of the institution or funder.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study are openly available in the public domain and details are provided in the references.

Additional information

Funding

References

- Abhayawansa, S., & Adams, C. (2022). Towards a conceptual framework for non-financial reporting inclusive of pandemic and climate risk reporting. Meditari Accountancy Research, 30(3), 711–21. https://doi.org/10.1108/MEDAR-11-2020-1097

- AccountingTools. (2022). Strategic risk definition. Retrieved August 23, 2022, from https://www.accountingtools.com/articles/strategic-risk

- Ackermann, N. (2022). How does input and output work?. Retrieved July 26, 2022, from https://study.com/academy/lesson/input-output-model.html

- Adams, C. A., & Abhayawansa, S. (2022). Connecting the COVID-19 pandemic, environmental, social and governance (ESG) investing and calls for ‘harmonisation’of sustainability reporting. Critical Perspectives on Accounting, 82, 102309. https://doi.org/10.1016/j.cpa.2021.102309

- Adams, C. A., Druckman, P. B., & Picot, R. C. (2020), Sustainable development goal disclosure (SDGD) recommendations. Retrieved July 18, 2022, from https://www.integratedreporting.org/wp-content/uploads/2020/01/Adams_Druckman_Picot_2020_Final_SDGD_Recommendations.pdf

- Ajam, T. (2020). The economic costs of the pandemic–and its response. South African Journal of Science, 116(7–8), 3–4. https://doi.org/10.17159/sajs.2020/8490

- Albris, K., Lauta, K. C., & Raju, E. (2020). Strengthening governance for disaster prevention: The enhancing risk management capabilities guidelines. International Journal of Disaster Risk Reduction, 47, 101647. https://doi.org/10.1016/j.ijdrr.2020.101647

- Albuquerque, R., Koskinen, Y., Yang, S., & Zhang, C. (2020). Resiliency of environmental and social stocks: An analysis of the exogenous COVID-19 market crash. The Review of Corporate Finance Studies, 9(3), 593–621. https://doi.org/10.1093/rcfs/cfaa011

- Alfani, G., & Murphy, T. E. (2017). Plague and lethal epidemics in the pre-industrial world. The Journal of Economic History, 77(1), 314–343. https://doi.org/10.1017/S0022050717000092

- Amankwah-Amoah, J. (2020). Stepping up and stepping out of COVID-19: New challenges for environmental sustainability policies in the global airline industry. Journal of Cleaner Production, 271, 123000. https://doi.org/10.1016/j.jclepro.2020.123000

- Amidei, C., Arzbaecher, J., Maher, M. E., Mungoshi, C., Cashman, R., Farrimond, S., Kruchko, C., Tse, C., Daniels, M., Lamb, S., Granero, A., Lovely, M., Baker, J., Payne, S., & Oliver, K. (2020). The brain tumor not-for-profit and charity experience of COVID-19: Reacting and adjusting to an unprecedented global pandemic in the 21st century. Neuro-Oncology Advances, 3(1), 1–11. https://doi.org/10.1093/noajnl/vdaa166

- Anglo American. (2020), Integrated annual report 2020. Retrieved July 7, 2021, from https://www.angloamerican.com/~/media/Files/A/Anglo-American-Group/PLC/investors/annual-reporting/2021/aa-annual-report-full-2020.pdf

- Anglogold Ashanti. (2020), Integrated report 2020. Retrieved July 7, 2021, from https://www.angloamericanplatinum.com/investors/annual-reporting/reports-archive/2020

- Aspen Pharmacare Holdings. (2020). Integrated report 2020. Retrieved July 7, 2021, from https://www.aspenpharma.com/investor-information/

- Atkins, J., Atkins, B. C., Thomson, I., Maroun, W. (2015). “Good” news from nowhere: Imagining utopian sustainable accounting. Accounting Auditing & Accountability Journal, 28(5), 651–670. https://doi.org/10.1108/AAAJ-09-2013-1485

- Atkins, J., Maroun, W., Atkins, B. C., & Barone, E. (2018). From the Big Five to the Big four? exploring extinction accounting for the rhinoceros. Accounting Auditing & Accountability Journal, 31(2), 674–702. https://doi.org/10.1108/AAAJ-12-2015-2320

- Azam, A., Ahmed, A., Wang, H., Wang, Y., & Zhang, Z. (2021). Knowledge structure and research progress in wind power generation (WPG) from 2005 to 2020 using CiteSpace based scientometric analysis. Journal of Cleaner Production, 295, 126496. https://doi.org/10.1016/j.jclepro.2021.126496

- Barloworld. (2020). Integrated report 2020. Retrieved July 7, 2021, from https://www.barloworld.com/investors/integrated-reports/

- Barry, J. M. (2010). The next pandemic. World Policy Journal, 27(2), 10–12. https://doi.org/10.1162/wopj.2010.27.2.10

- Bhosale, J. (2020). Prices of agricultural commodities drop 20% post COVID-19 outbreak. Retrieved December 3, 2020, from https://economictimes.indiatimes.com/news/economy/agriculture/prices-of-agricultural-commodities-drop-20-post-covid-19-outbreak/articleshow/74705537.cms

- BHP Group. (2020). Annual report 2020. Retrieved July 7, 2021, from https://www.bhp.com/investors/annual-reporting/annual-report-2020/annual-report-2020

- BID Corporation. (2020), Annual integrated report 2020. Date of access 7 July 2021 https://www.bidcorpgroup.com/integrated-reports.php

- Bowen, G. A. (2006). Grounded theory and sensitizing concepts. International Journal of Qualitative Methods, 5(3), 12–23. https://doi.org/10.1177/160940690600500304

- Britannica. (2022). Newton’s laws of motion. Retrieved August 23, 2022, from https://www.britannica.com/science/Newtons-laws-of-motion

- Broadstock, D. C., Chan, K., Cheng, L. T., & Wang, X. (2021). The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Research Letters, 38, 101716. https://doi.org/10.1016/j.frl.2020.101716

- Brown, S. (2020). Pandemic to hit ability to meet KPIs on ESG loans. GlobalCapital, 5 Nov, Retrieved March 5, 2021, from https://www.globalcapital.com/article/28mudmf4ppazk1ughqlfk/investment-grade-loans/pandemic-to-hit-ability-to-meet-kpis-on-esg-loans

- Canadian Centre for Occupational Health and Safety. (2020). Hazard identification. Retrieved October 8, 2020, from https://www.ccohs.ca/oshanswers/hsprograms/hazard_identification.html

- Chanyasak, T., Koseoglu, M. A., King, B., & Aladag, O. F. (2021). Business model adaptation as a strategic response to crises: Navigating the COVID-19 pandemic. International Journal of Tourism Cities, 8(3), 616–635. https://doi.org/10.1108/IJTC-02-2021-0026

- Chen, J. (2022). What is fraud?. Retrieved August 23, 2022, from https://www.investopedia.com/terms/f/fraud.asp

- Chinn, L., Carpenter, A., & Dunn, A. D. (2021). ESG trends: Improving and standardizing disclosure. Retrieved July 19, 2022, from https://www.reuters.com/legal/legalindustry/esg-trends-improving-standardizing-disclosure-2021-10-20/

- Cirillo, P., & Taleb, N. N. (2020). Tail risk of contagious diseases. Nature Physics, 16(6), 606–613. https://doi.org/10.1038/s41567-020-0921-x

- Clicks Group. (2020). Integrated annual report 2020. Retrieved July 7, 2021, from https://www.clicksgroup.co.za/investor-relations/ir-financial-results.html

- Coetzee, G. P. (2010). A risk-based audit model for internal audit engagements. [ Thesis – PhD], University of the Free State. http://hdl.handle.net/11660/4229

- Coetzee, J., Neneh, B., Stemmet, K., Lamprecht, J., Motsitsi, C., & Sereeco, W. (2021). South African universities in a time of increasing disruption. South African Journal of Economic and Management Sciences, 24(1), 1–12. https://doi.org/10.4102/sajems.v24i1.3739

- Collins Dictionary. (2020). Definition of ‘hazard’, Retrieved October 8, 2020, from https://www.collinsdictionary.com/dictionary/english/hazard

- Coppola, D. P. (2011). Introduction to international disaster management (2nd ed.). Butterworth-Heinemann. https://doi.org/10.1016/B978-0-12-382174-4.00018-5

- Coroporate Finance Institute. (2022). Business operations. Retrieved August 1, 2022https://corporatefinanceinstitute.com/resources/knowledge/strategy/business-operations/

- Correia, S., Luck, S., & Verner, E. (2020) Pandemics depress the economy, public health interventions do not: Evidence from the 1918 flu. Retrieved August 17, 2020, from https://www.sbmfc.org.br/wp-content/uploads/2020/03/SSRN-id3561560.pdf

- Deegan, C. (2002). The legitimising effect of social and environmental disclosures: A theoretical foundation. Accounting, Auditing, Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

- Deegan, C. M. (2019). Legitimacy theory: Despite its enduring popularity and contribution, time is right for a necessary makeover. Accounting Auditing & Accountability Journal, 32(8), 2307–2329. https://doi.org/10.1108/AAAJ-08-2018-3638

- De Villiers, R. R. (2015). Evaluating the effectiveness of a newly developed simulation in improving the competence of audit students. [ Thesis – PhD], North-West University.

- Disaster Management Act 57 of. 2002.

- Egbe, C. O., & Ngobese, S. P. (2020). COVID-19 lockdown and the tobacco product ban in South Africa. Tobacco Induced Diseases, 18(May), 39. https://doi.org/10.18332/tid/120938

- Ehnert, I., Parsa, S., Roper, I., Wagner, M., & Muller-Camen, M. (2016). Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. The International Journal of Human Resource Management, 27(1), 88–108. https://doi.org/10.1080/09585192.2015.1024157

- Elson, C. M., & Goossen, N. J. (2017). E. Merrick Dodd and the rise and fall of corporate stakeholder theory. The Business Lawyer, 72(3), 735–754.

- Etikan, I., Musa, S. A., & Alkassim, R. S. (2016). Comparison of convenience sampling and purposive sampling. American Journal of Theoretical Applied Statistics, 5(1), 1–4. https://doi.org/10.11648/j.ajtas.20160501.11

- Federal Emergency Management Agency. (2006), What are hazards?. Retrieved July 4, 2023, from https://training.fema.gov/hiedu/docs/hazdem/session%202%20–%20what%20are%20hazards.doc

- Fernandes, N. (2020). Economic effects of coronavirus outbreak (COVID-19) on the world economy, working paper no. WP-1240-E, IESE Business School, University of Navarra. https://doi.org/10.2139/ssrn.3557504

- Financial Times Stock Exchange Russell. (2020). ESG ratings and data model. Retrieved July 15, 2020, from https://research.ftserussell.com/products/downloads/ESG-ratings-overview.pdf?987

- Firstrand. (2020). Annual integrated report 2020. Retrieved July 7, 2021, from https://www.firstrand.co.za/investors/annual-reporting/

- Flick, U. W. E. (2011). Introducing research methodology: A beginner’s guide to doing a research project. Sage.

- Gibb, R., Redding, D. W., Chin, K. Q., Donnelly, C. A., Blackburn, T. M., Newbold, T., & Jones, K. E. (2020). Zoonotic host diversity increases in human-dominated ecosystems. Nature, 584(7821), 398–402. https://doi.org/10.1038/s41586-020-2562-8

- Giorgi, G., Lecca, L. I., Alessio, F., Finstad, G. L., Bondanini, G., Lulli, L. G., Arcangeli, G., & Mucci, N. (2020). COVID-19-related mental health effects in the workplace: A narrative review. International Journal of Environmental Research and Public Health, 17(21), 7857. https://doi.org/10.3390/ijerph17217857

- Glaser, B. G. (1965). The constant comparative method of qualitative analysis. Social Problems, 12(4), 436–445. https://doi.org/10.2307/798843

- Glencore. (2020). Annual report 2020. Retrieved July 7, 2021, from https://www.glencore.com/publications

- Global Reporting Initiative. (2020). GRI sustainability reporting standards, Retrieved July 15, 2020, from https://www.globalreporting.org/

- Gluck, F. W., Kaufman, S. P., & Walleck, A. S. (1980). Strategic management for competitive advantage. Retrieved August 1, 2022, from https://hbr.org/1980/07/strategic-management-for-competitive-advantage

- GMO Research. (2020). How the e-commerce industry saved businesses in Asia during the global pandemic. Retrieved July 26, 2022, fromhttps://gmo-research.com/news-events/articles/how-e-commerce-industry-saved-businesses-asia-during-global-pandemic

- Goodman, D. (2020). World economy faces $5 trillion hit: That’s like losing japan. Retrieved April 6, 2020, from https://www.bloombergquint.com/global-economics/world-economy-faces-5-trillion-hit-that-is-like-losing-japan

- Gow, J., & Grant, B. (2010). Human-resources strategies for managing HIV/AIDS: The case of the South African forestry industry. African Journal of AIDS Research, 9(3), 285–295. https://doi.org/10.2989/16085906.2010.530184

- Harmony. (2020). Integrated annual report 2020. Retrieved July 7, 2021, from https://www.harmony.co.za/invest/annual-reports

- Harper, D. R. (2021). Understanding liquidity risk. Retrieved August 23, 2022, from https://www.investopedia.com/articles/trading/11/understanding-liquidity-risk.asp

- Hassan, A., Elamer, A. A., Lodh, S., Roberts, L., & Nandy, M. (2021). The future of non‐financial businesses reporting: Learning from the covid‐19 pandemic. Corporate Social Responsibility and Environmental Management, 28(4), 1231–1240. https://doi.org/10.1002/csr.2145

- Hayat, U., & Orsagh, M. (2015), Environmental, social, and governance issues in investing: A guide for investment professionals. Retrieved June 9, 2021, from https://www.cfainstitute.org/-/media/documents/article/position-paper/esg-issues-in-investing-a-guide-for-investment-professionals.ashx

- He, P., He, Y., & Xu, F. (2018). Evolutionary analysis of sustainable tourism. Annals of Tourism Research, 69, 76–89. https://doi.org/10.1016/j.annals.2018.02.002

- Higgins, C., & Walker, R. (2012). Ethos, logos, pathos: Strategies of persuasion in social/environmental reports. Accounting Forum, 36(3), 194–208. https://doi.org/10.1016/j.accfor.2012.02.003

- Hughen, L., Lulseged, A., & Upton, D. R. (2014). Improving stakeholder value through sustainability and integrated reporting. The CPA Journal, 84(3), 57–61.

- Ihlen, Ø., Bartlett, J. L., & May, S. (Ed.). (2011). The handbook of communication and corporate social responsibility. Wiley-Blackwell. https://doi.org/10.1002/9781118083246

- IIRC and Kirchhoff Consult AG. (2020) Closing the gap: The role of integrated reporting in communicating a company’s value creation to investors Retrieved August 1, 2022, from https://integratedreporting.org/wp-content/uploads/2020/12/IIRC_Kirchhoff_Investor_Reseach.pdf

- Institute of Directors South Africa. (2016). King IV report on corporate governance for South Africa 2016. Retrieved July 4, 2023, from https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/684B68A7-B768-465C-8214-E3A007F15A5A/IoDSA_King_IV_Report_-_WebVersion.pdf

- Institute of Risk Management. (2022). Cyber risk. Retrieved August 23, 2022, from https://www.theirm.org/what-we-say/thought-leadership/cyber-risk/

- International Accounting Standards Board. (2020). IFRS 7 - financial instruments: disclosures. Retrieved September 22, 2020, from http://eifrs.ifrs.org/eifrs/bnstandards/en/IFRS7.pdf

- International Integrated Reporting Council. (2021). International framework. Retrieved March 5, 2021, from https://integratedreporting.org/wp-content/uploads/2021/01/InternationalIntegratedReportingFramework.pdf

- International Monetary Fund. (2021). Policy responses to COVID-19. Retrieved September 7, 2022, from https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19

- International Organization for Standardization. (2010). ISO 26000 guidance on social responsibility. Retrieved July 7, 2020, from https://iso26000.info/wp-content/uploads/2017/06/ISO-26000_2010_E_OBPpages.pdf

- Islam, A. M. (2021). Impact of covid-19 pandemic on global output, employment and prices: An assessment. Transnational Corporations Review, 13(2), 189–201. https://doi.org/10.1080/19186444.2021.1936852

- Jabareen, Y. (2009). Building a conceptual framework: Philosophy, definitions, and procedure. International Journal of Qualitative Methods, 8(4), 49–62. https://doi.org/10.1177/160940690900800406

- Janković, M., Mihajlović, M., & Cvetković, T. (2016). Influence of external factors on business of companies in Serbia. Ekonomika, 62(4), 31–37. https://doi.org/10.5937/ekonomika1604031J

- Jones, K. E., Patel, N. G., Levy, M. A., Storeygard, A., Balk, D., Gittleman, J. L., & Daszak, P. (2008). Global trends in emerging infectious diseases. Nature, 451(7181), 990–993. https://doi.org/10.1038/nature06536

- Jordá, Ó., Singh, S. R., & Taylor, A. M. (2020). The long economic hangover of pandemics. Finance & Development, 57(2), 12–15.

- Kannenberg, L., & Schreck, P. (2019). Integrated reporting: Boon or bane? A review of empirical research on its determinants and implications. Journal of Business Economics, 89(5), 515–567. https://doi.org/10.1007/s11573-018-0922-8

- Kauppi, K., Salmi, A., & You, W. (2018). Sourcing from Africa: A systematic review and a research agenda. International Journal of Management Reviews, 20(2), 627–650. https://doi.org/10.1111/ijmr.12158

- Kenny, C. (2020). “Form 8-K: United Airlines Holdings, Inc. And United Airlines, Inc Retrieved July 2, 2020, from https://ir.united.com/static-files/440c2464-a618-4c55-afa0-4eaff0210d3e

- Kenton, W. (2021). Liquidity risk Retrieved August 23, 2022, from https://www.investopedia.com/terms/l/liquidityrisk.asp

- Kolb, S. M. (2012). Grounded theory and the constant comparative method: Valid research strategies for educators. Journal of Emerging Trends in Educational Research and Policy Studies, 3(1), 83–86. https://journals.co.za/doi/abs/10.10520/EJC135409

- Kontoangelos, K., Economou, M., & Papageorgiou, C. (2020). Mental health effects of COVID-19 pandemia: A review of clinical and psychological traits. Psychiatry Investigation, 17(6), 491–505. https://doi.org/10.30773/pi.2020.0161

- KPMG. (2017), The road ahead: The KPMG survey of corporate responsibility reporting 2017. Retrieved July 3, 2020, from https://assets.kpmg/content/dam/kpmg/be/pdf/2017/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf

- Lanis, R., & Richardson, G. (2013). Corporate social responsibility and tax aggressiveness: A test of legitimacy theory. Accounting Auditing & Accountability Journal, 26(1), 75–100. https://doi.org/10.1108/09513571311285621

- Larkin, M. (2022). Understanding legal risk: What every business needs to know. Retrieved August 23, 2022, from https://www.kochiesbusinessbuilders.com.au/understanding-and-managing-legal-risk-what-every-business-needs-to-know/

- Lavopa, A., & Delera, M. (2021). What is the fourth industrial revolution? Retrieved July 26, 2022, from https://iap.unido.org/articles/what-fourth-industrial-revolution

- Littman, R. J., & Littman, M. L. (1973). Galen and the Antonine plague. The American Journal of Philology, 94(3), 243–255. https://doi.org/10.2307/293979

- Macaninch, E., Martyn, K., & Lima Do Vale, M. (2020). Exploring the implications of COVID-19 on widening health inequalities and the emergence of nutrition insecurity through the lens of organisations involved with the emergency food response. BMJ Nutrition, Prevention & Health, 3(2), 374–382. https://doi.org/10.1136/bmjnph-2020-000120

- Machuki, V. N., & Aosa, E. (2011), “The influence of the external environment on the performance of publicly quoted companies in Kenya”, working paper, School of Business, University of Nairobi. http://hdl.handle.net/11295/9901

- Markgraf, B. (2019), “Short-term, medium-term and long-term planning in business, Retrieved August 23, 2022, from https://smallbusiness.chron.com/shortterm-mediumterm-longterm-planning-business-60193.html

- Maruping, L. M., Daniel, S. L., & Cataldo, M. (2019). Developer centrality and the impact of value congruence and incongruence on commitment and code contribution activity in open source software communicties. MIS Quarterly, 43(3), 951–976. https://doi.org/10.25300/MISQ/2019/13928

- Marx, B. (2008). An analysis of the development, status and functioning of audit committees at large listed companies in South Africa. [ Thesis – PhD], Univerisity of Johannesburg.

- Mattison, R., De Longevialle, B., Bastit, B., Hall, L., Ly, L., Munday, P., & Thomson, B. (2022). Key trends that will drive the ESG agenda in 2022. Retrieved March 13, 2022, from https://www.spglobal.com/esg/insights/featured/special-editorial/key-esg-trends-in-2022

- McKinsey and Company. (2022). COVID-19: Implications for business. Retrieved May 12, 2022, from https://www.mckinsey.com/business-functions/risk-and-resilience/our-insights/covid-19-implications-for-business

- Merriam, S. B., & Tisdell, E. J. (2016). Qualitative research: A guide to design and implementation (4th ed.). Jossey-Bass.

- Montauk Holdings. (2020), Form 10-K, Retrieved July 7, 2021, from https://ir.montaukrenewables.com/financial-information/annual-reports

- Moolman, A. M., Fouché, J. P., & Leendertz, V. (2023a). Sustainability elements of companies that are affected by pandemics. Journal of Economic and Financial Sciences, 16(1), a828. https://doi.org/10.4102/jef.v16i1.828

- Moolman, A. M., Fouché, J. P., & Leendertz, V. (2023b). Sustainability elements reported on by JSE-listed companies that are affected by pandemics. Review of Economics and Finance, 16(1), In press. https://doi.org/10.4102/jef.v16i1.828

- Nguyen, K. D., Enos, T., Vandergriff, T., Vasquez, R., Cruz, P. D., Jacobe, H. T., & Mauskar, M. M. (2020). Opportunities for education during the COVID-19 pandemic. JAAD International, 1(1), 21–22. https://doi.org/10.1016/j.jdin.2020.04.003

- Nicola, M., Alsafi, Z., Sohrabi, C., Kerwan, A., Al-Jabir, A., Iosifidis, C., Agha, M., & Agha, R. (2020). The socio-economic implications of the coronavirus pandemic (COVID-19): A review. International Journal of Surgery, 78, 185–193. https://doi.org/10.1016/j.ijsu.2020.04.018

- Nkengasong, J. N. (2021). COVID-19: Unprecedented but expected. Nature Medicine, 27(3), 364–364. https://doi.org/10.1038/s41591-021-01269-x

- Nobanee, H., Al Hamadi, F. Y., Abdulaziz, F. A., Abukarsh, L. S., Alqahtani, A. F., AlSubaey, S. K., Alqahtani, S. M., & Almansoori, H. A. (2021). A bibliometric analysis of sustainability and risk management. Sustainability, 13(6), 3277. https://doi.org/10.3390/su13063277

- Organisation for Economic Co-operation and Development. (2011). OECD guidelines for multinational enterprises. Retrieved July 7, 2020, frmo https://www.oecd.org/daf/inv/mne/48004323.pdf

- Osterholm, M. T. (2005). Preparing for the next pandemic. New England Journal of Medicine, 352(18), 1839–1842. https://doi.org/10.1056/NEJMp058068

- Panfilo, S., & Krasodomska, J. (2022). Climate change risk disclosure in Europe: The role of cultural-cognitive, regulative, and normative factors. Accounting in Europe, 19(1), 226–253. https://doi.org/10.1080/17449480.2022.2026000

- Parmar, B. L., Freeman, R. E., Harrison, J. S., Wicks, A. C., De Colle, S., & Purnell, L. (2010). Stakeholder theory: The state of the art. The Academy of Management Annals, 4(1), 403–445. https://doi.org/10.5465/19416520.2010.495581

- Pegram, N. (2020). ESG data disclosure demands continue to evolve as investors focus on non financial risks. Retrieved July 15, 2022, from https://www.esgtoday.com/guest-post-esg-data-disclosure-demands-continue-to-evolve-as-investors-focus-on-non-financial-risks/

- Pinner, D., Rogers, M., & Samandari, H. (2020). Addressing climate change in a post-pandemic world. McKinsey Quarterly, Retrieved July 11, 2021, from http://acdc2007.free.fr/mckclimate420.pdf

- Pizzi, S., Del Baldo, M., Caputo, F., & Venturelli, A. (2022). Voluntary disclosure of sustainable Development Goals in mandatory non-financial reports: The moderating role of cultural dimension. Journal of International Financial Management & Accounting, 33(1), 83–106. https://doi.org/10.1111/jifm.12139

- Poudel, B. S. (2020). Ecological solutions to prevent future pandemics like COVID-19. Banko Janakari, 30(1), 1–2. https://doi.org/10.3126/banko.v30i1.29175

- PR Newswire. (2020). The reshaping of industries caused by COVID-19. Retrieved December 7, 2022, from https://www.reportlinker.com/p05967978/The-Reshaping-of-Industries-Caused-by-COVID-19.html

- Prosus. (2020). Annual report 2020. Retrieved July 7, 2021, from https://www.prosus.com/news/investors-annual-reports/

- Quantec. (2020). Lockdown and COVID-19 in South Africa: Economic impact underestimated. Retrieved March 5, 2021, from https://www.quantec.co.za/post/3771/lockdown-and-covod-19-in-south-africa/

- Quilter PLC. (2020). Annual report 2020. Retrieved July 7, 2021, from https://plc.quilter.com/investor-relations/annual-reports-archive/

- Redmond, M. V. (2015). Uncertainty reduction theory. Retrieved September 22, 2020, from https://lib.dr.iastate.edu/cgi/viewcontent.cgi?article=1005&context=engl_reports

- Roberts, R. W. (1992). Determinants of corporate social responsibility disclosure: An application of stakeholder theory. Accounting, Organizations & Society, 17(6), 595–612. https://doi.org/10.1016/0361-3682(92)90015-K

- Roberts, L., Hassan, A., Elamer, A., & Nandy, M. (2021). Biodiversity and extinction accounting for sustainable development: A systematic literature review and future research directions. Business Strategy and the Environment, 30(1), 705–720. https://doi.org/10.1002/bse.2649

- Roubini, N. (2020). Coronavirus pandemic has delivered the fastest, deepest economic shock in history. The Guardian, 25 Mar. Retrieved July 19, 2022, from https://www.theguardian.com/business/2020/mar/25/coronavirus-pandemic-has-delivered-the-fastest-deepest-economic-shock-in-history

- Rowan, N. J., & Galanakis, C. M. (2020). Unlocking challenges and opportunities presented by COVID-19 pandemic for cross-cutting disruption in agri-food and green deal innovations: Quo Vadis? Science of the Total Environment, 748, 141362. https://doi.org/10.1016/j.scitotenv.2020.141362

- SafetyWallet. (2021). What is a health and safety risk?. Retrieved August 23, 2022, from https://www.safetywallet.co.za/Blog/Health-and-Safety-Risk

- Sarkodie, S. A., & Owusu, P. A. (2020). Global assessment of environment, health and economic impact of the novel coronavirus (COVID-19). Environment Development and Sustainability, 23(4), 5005–5015. https://doi.org/10.1007/s10668-020-00801-2

- Saunders, M. N. K., Lewis, P., & Thornhill, A. (2019). Research methods for business students (8th ed.). Pearson.

- Seetharaman, P. (2020). Business models shifts: impact of covid-19. International Journal of Information Management, 54, 102173. https://doi.org/10.1016/j.ijinfomgt.2020.102173

- SIAPartners. (2021). Attraction and retention may no longer be sufficient. Retrieved August 23, 2022, from https://www.sia-partners.com/en/news-and-publications/from-our-experts/attraction-and-retention-may-no-longer-be-sufficient

- Sibanye-Stillwater. (2020). Integrated report 2020. Retrieved July 7, 2021, from https://www.sibanyestillwater.com/news-investors/reports/annual/2020/

- Sickler, J. (2019). What is reputational risk and how to manage it. Retrieved August 23, 2022, from https://www.reputationmanagement.com/blog/reputational-risk/

- Solomon, J., & Maroun, W. (2012), “Integrated reporting: The influence of King III on social, ethical and environmental reporting”, Association of Chartered Certified Accountants. http://hdl.handle.net/10023/3749

- S&P Dow Jones Indices. (2019). Dow Jones sustainability indices methodology. Retrieved July 7, 2020, from https://www.spglobal.com/spdji/en/documents/methodologies/methodology-dj-sustainabilityindices.pdf

- Standard Bank Group. (2020). Annual integrated report 2020. Retrieved July 7, 2022, form https://reporting.standardbank.com/results-reports/annual-reports/

- State Service Authority. (2015). Succession risk management. Accessed 13 Ocober 2022, from https://vpsc.vic.gov.au/wp-content/uploads/2015/03/Fact_sheets_all.pdf

- Stats, S. A. (2021). Statistics of liquidations and insolvencies (Preliminary). Retrieved June 11, 2021, from http://www.statssa.gov.za/publications/P0043/P0043April2021.pdf

- Tregidga, H., Milne, M., & Kearins, K. (2014). (Re) presenting ‘sustainable organizations’. Accounting, Organizations & Society, 39(6), 477–494. https://doi.org/10.1016/j.aos.2013.10.006

- United Nations. (2008). The practical guide to the United Nations global Compact communication on progress (COP): Creating, sharing and posting a COP. Retrieved July 7, 2020, from https://digitallibrary.un.org/record/677390?ln=en