?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study looks at mechanisms for improving and stabilising the financial performance of commercial banks in Tanzania. More specifically, this study aimed to assess corporate governance’s influence on financial performance regarding asset quality, efficiency use of equity, earning ability, capital adequacy, and liquidity. The study included the board aspect of governance and board control, constructs which have not been studied previously in assessing the influence of corporate governance on the performance of commercial banks. Other constructs included are the board’s gender diversity, board size, directors’ shareholding, board control, board members’ over boarding, board activities, and the existence of important board committees. Panel data were collected from published reports of 15 commercial banks covering a period of 17 and employing multiple linear regression analysis to establish causal-effect relationships among the study variables. The findings revealed that corporate governance (board aspects of governance, board members over-boarding) positively influences the financial performance of commercial banks in terms of their earning ability, asset quality, and capital adequacy. Corporate governance also negatively influences the efficient use of equity and liquidity through board gender diversity, board aspects of governance, and board control. The study recommends that corporate governance principles and mechanisms be enhanced to improve the financial performance of commercial banks.

1. Introduction

The financial performance of commercial banks is a function of several factors, including efficient and effective corporate governance structures and mechanisms (Fajriyanti et al., Citation2021). However, weak corporate governance structures and mechanisms have been reported to be a cause of failure in managing banking risks which, in the end, causes poor financial performance (FP), hence the failure of the banking industry (Tarchouna et al., Citation2022). Likewise, previous research conducted by scholars like Velliscig et al. (Citation2022) and Thaker et al. (Citation2022) indicated that the weak quality of commercial banks’ assets is associated with weak and ineffective corporate governance and turns out to affect performance negatively.

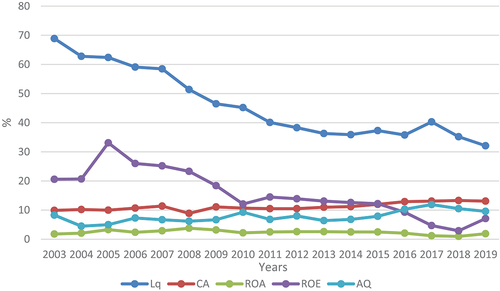

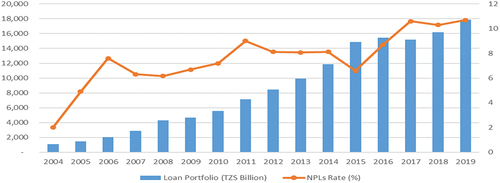

Taking the case of Tanzanian commercial banks, the Bank of Tanzania (BoT) constantly emphasises strong corporate governance significance on banks’ performance. For instance, through its circular No. FA.178/461/01/02 of 19 February 2018, banks were argued to improve their corporate governance (BOT Circular No. FA.178/461/01/02). This suggests the existence of weak or inefficiencies in corporate governance (CG) mechanisms among commercial banks (CBs) in the country, which can negatively affect the FP if not considered carefully. For instance, the industry has been experiencing a fluctuating performance in terms of return on asset (ROA), return on equity (ROE), capital adequacy (CA), asset quality (AQ), and liquidity (Lq), as shown in accompanied by a persisting rising rate of non-performing loans as presented in ; the trend which is contrary to the acceptable level of 5% prescribed by BOT (Bank of Tanzania, 2004–2022).

Figure 1. Trend of selected financial performance indicators.

Figure 2. Rates of non-performing loans and values of loan portfolio.

Literature indicates that corporate governance is among the key factors to consider for the financial performance of the banking industry (El-Chaarani et al., Citation2022; Supriyatna et al., Citation2022). However, their effect on financial performance is not adequately addressed, as previous studies provided contradicting results regarding the negative or positive relationships between CG and FP.

Further, they repetitively studied the same variables of CG, such as board size, board composition, board members’ independence, majority ownership, directors’ and executive officers’ ownership, CEO duality, and board activities, as evidenced by Al-Ahdal et al. (Citation2020), Fajriyanti et al. (Citation2021), and (El-Chaarani et al., Citation2022) hence adding no value to the arena of the effect of CG on FP.

Recent studies conducted in Tanzanian on commercial banks and financial performance are worth noting. These include works by Tegambwage and Kasoga (Citation2022), Kasoga and Elgammal (Citation2020), Viswanadham and Kasoga (Citation2020), Daniel et al. (Citation2021), and Magoma et al. (Citation2022), but their studies did not examine the influence of corporate governance on financial performance.

Given the above background, there is still a need to scrutinise how CG can effectively be utilised in improving the financial performance of CBs, as there is scant literature backed by empirical evidence on the causal-effect relationships between corporate governance and CBs’ financial performance. This study, therefore, aimed to establish the effect of corporate governance on the financial performance of commercial banks in Tanzania. More specifically, in trying to alleviate the overstudied constructs of CG in relation to FP of CBs, this study includes two constructs which are the board aspect of governance (BAG) and board control (BC), the constructs which have not been studied previously in examining the influence of corporate governance on the financial performance of commercial banks. BAG and BC have been suggested by Yılmaz (Citation2010) as essential elements in assessing the efficiency and effectiveness of corporate governance towards performance.

In the end, this study fills the knowledge gap by examining the board aspect of governance and board control together with other factors mentioned by previous studies as important factors of corporate governance; these are board’s gender diversity, board size, directors’ shareholding, board members’ over boarding, board activities, and the existence of important boards’ committees (Al-Ahdal et al., Citation2020; El-Chaarani et al., Citation2022; Fajriyanti et al., Citation2021), and their influence on the financial performance of commercial banks in Tanzania.

The findings of this study will help practitioners, especially the board members, improve the supervision and monitoring role of the board of directors in order to improve the financial performance of commercial banks in Tanzania.

The rest of the paper is organised as follows: The next section presents the literature review and hypothesis development. The methodology of the study follows it. The next section presents the findings, followed by a discussion of the findings; the final section provides a conclusion and recommendations.

2. Literature review and hypothesis development

This section presents a review of the literature pertaining to corporate governance structures and mechanisms and their relationship to the financial performance of financial institutions. It further lays out the theoretical review and hypothesis development.

2.1. Theoretical review: Resource-based theory

The resource-based view theory (RBV) hypothesises that the growth and performance of the firm are at least in part influenced by the resources it owns (Barney, Citation1991; Castanias & Helfat, Citation1991; Penrose, Citation1959; Wernerfelt, Citation1984). RBV provides that the resources or bundles of resources that a firm owns are the basis for attaining competitive advantage (Barney, Citation1986; Wernerfelt, Citation1984) and that the firm’s performance is largely driven by its resources (Barney, Citation1991). With this theory, a firm is considered a bundle of resources and capabilities that are rare, valuable, non-substitutable, and inimitable and that can result in sustainable competitive advantage attainment when strategically selected and implemented, thereby affecting the firm’s financial performance (Barney, Citation1991). Once all resources are well selected, mixed, and executed, a firm is expected to attain a sustainable competitive advantage and achieve high performance. However, precaution should be taken, as since it is true that positive hidden values (of the board of directors) that reflect intangible assets drive firm performance, it is also true that negative hidden values (intangible liabilities) limit firm performance (Haji & Ghazali, Citation2018). The theory emphasises governance structure and the board composition as a resource that can add value to the firm (Madhani, Citation2017) and that the board is regarded as a valuable resource when it is actively involved in strategic decision-making processes.

According to the theory, the board of directors can bring unique resources to the firm by properly utilising the board’s characteristics, including members’ knowledge and experience. Further, the resource-based view theory relates to the board’s characteristics in terms of personal and distinctive resources that may be sources of competitive advantage for firms. The assumption of the RBV of rare, valuable, non-substitutable, and inimitable resources can also be useful and adopted in the unique mixture of resources within the board of directors. In this regard, the board of directors is regarded as a valuable resource within an organisation, but only when the board is actively involved in strategic decision-making and monitoring and controlling the implementation of those decisions. The processes in which boards of directors are anticipated to influence organisation performance as forecasted by the resource-based view theory in terms of corporate governance are presented in Figure as adopted from Madhani (Citation2017).

Figure 3. Resource-based view theory: Corporate governance through board demography.

The relevance of this theory to the current study is based on the assumption that a “bundle of resources and capabilities” that the board of directors possess are the core drivers for financial performance improvements and sustainability.

2.2. Hypothesis development

2.2.1. Corporate governance and bank performance

Hermawan et al. (Citation2021) examined the effect of good corporate governance on the financial performance of Indonesian banks. Their results revealed that corporate governance affects a firm’s financial performance; ROA was adopted as a proxy of financial performance. Their analysis showed that corporate governance significantly affects ROA upward or downward (61.6%), with the remaining 38.4% being other factors not covered by their study. According to their findings, good corporate governance leads to positive decision-making, reducing the risks facing the banks and subsequently strengthening their financial performance.

Al-Matari (Citation2020) examined if corporate performance in the financial sector can be affected by the board of directors’ characteristics. His findings revealed that board size positively and significantly affects financial performance and that big-sized boards lead to greater financial performance. Also, board meeting (frequency) was reported to have a significant relationship with the firm’s financial performance. According to his study, a high frequency of meetings helps in the assessment/monitoring of business activities at the right time and timely solving of business matters.

Also, Alqudah et al. (Citation2019) used the number of foreign members, political connections and busy directors, the board size, board independence, and board meetings to establish their impact on financial performance. Their findings revealed that, apart from the variable board size, which significantly impacted banks’ financial performance, all other variables recorded insignificant relationships with ROA, which was used to measure financial performance. However, their findings failed to indicate that the busy schedule of directors affected their time with the firm to address the firm’s matters hence affecting financial performance. The study findings recorded board members with political status as stumbling blocks for improving financial performance; the other drawback was foreign members on the board of directors. Board independence and the number of board meetings recorded insignificant association with return on assets. Based on these findings, the study expects corporate governance to affect the financial performance of commercial banks in Tanzania positively.

2.3. Gender diversity and financial performance

Elbahar (Citation2019) researched the existing association between corporate governance and financial performance. ROA and ROE measured financial performance as the dependent variables, while corporate governance (the independent variable) was measured by gender diversity, the percentage of non-executive directors, and board size. The existence of board committees (audit committee, risk committee, credit & investment committee, and Sharia Committee) also formed part of independent variables. Others are the number of political members on the board of directors and chief executive officer turnover. The study controlled for ownership structure (government or non-government ownership), bank type (Islamic or conventional), and bank size. His findings indicated that the presence of female board members on the board of directors is to a high degree associated with the good financial performance of the banks; further, there is evidence of the high level of maturity in decision-making when there are female members on board.

Mohammad et al. (Citation2018) explored the effect of women board members towards firms’ performance, purposely covering a financial crisis period and its aftershock. Return on assets was regressed against the percentage of women on the boards and the percentage of women on the top and medium-level management of the banks. Bank size, leverage rate, and the ratio of loans to total deposits were controlled during the analysis. The study, however, couldn’t provide evidence of any statistically significant relationship between the presence of women’s directorship and top management and financial performance. The study suggested that cultural factors might affect the relationship and recommended continuing to involve women on the board of directors as other studies evidenced a significant relationship. Based on the review of the above literature, the study hypothesizes the following:

H1a:

Board gender diversity positively affects capital adequacy of commercial banks.

H1b:

Board gender diversity positively affects efficiency use of equity of commercial banks.

H1c:

Board gender diversity positively affects earning ability of commercial banks.

H1d:

Board gender diversity positively affects asset quality of commercial banks.

H1e:

Board gender diversity positively affects liquidity of commercial banks.

2.4. Behavioural aspects of governance and financial performance

Marnet (Citation2004) investigated factors for the efficacy of corporate governance through the board of directors in driving financial performance. The study looked at different aspects from various literature regarding behavioural economics, cognitive research, and corporate governance. In the end, the study recommended that existing corporate governance models be adjusted to accommodate or incorporate the effects of behavioural aspects and emotional factors on the efficacy of the board of directors.

Putting more emphasis on the importance of good corporate governance on the financial performance of organisations, Yılmaz (Citation2010) developed a model called the Corporate Governance Model to try to evaluate the effectiveness of corporate governance. The model proposed the inclusion of both structural aspects of governance (such as board size, the board’s gender diversity, the number of board meetings, the independence of the board, etc.), and behavioural aspects of governance. According to him, the behavioural aspects of governance include the quality of information that leads to comprehensive decision-making, the careful scrutinisation of all alternative approaches in decision-making over organisation matters and procedures, and the results of the oversight and control functions of the board of directors. Both aspects yield positive results for firms’ performance when carefully facilitated and blended. Brown and Brown (Citation2011) added to the blending one more aspect (the cultural aspect). According to the authors, the behaviour and cultural aspects should consider equipping the board of directors with appropriate soft skills to discharge their duties and responsibilities effectively. The authors have named these soft skills to include,

… .A sense of personal responsibility and self-management; self-esteem; integrity and honesty; sociability and interpersonal skills; emotional maturity, Team player, Servant leadership, Personal habits, attitude, and ability to work with other genders and cultures … and that strength in soft skills is a needed complement to the professionalism (hard skills) of directorship; hence, it is essential to equip the board of directors with soft skills appropriately.

Based on the review of the above literature, the study expects that

H2a:

Behavioural aspects of governance positively affect capital adequacy of commercial banks.

H2b:

Behavioural aspects of governance positively affect efficiency use of equity of commercial banks.

H2c:

Behavioural aspects of governance positively affect earning ability of commercial banks.

H2d:

Behavioural aspects of governance positively affect asset quality of commercial banks.

H2e:

Behavioural aspects of governance positively affect liquidity of commercial banks.

2.5. Board over-boarding and financial performance

The effect of the busyness of board members on a firm’s performance has been assessed by Lee and Lok (Citation2020). The study employed a two-stage least squares regression and Spearman correlations to analyse the collected data. The study concluded that firms’ performance is negatively associated with busy boards. Also, firms with a busy board are experiencing higher operational risks, especially in the volatility of ROA, operating cash flows, and stock returns. Further, the firm’s life cycle stage determines the association between performance and board busyness. For infant firms, a busy board proved to be beneficial to the firm performance assumption being that busy directors are well experienced and have knowledge as well as accumulated reputation; unlike the matured firms, busy boards are evidenced to be damaging a firm’s performance. According to Mans-Kemp et al. (Citation2018), reasons behind the over-boardness of directors over-boarded directors were reported to have poor attendance at board meetings which negatively affects financial performance and that scarce talent pool of proficient as well as board diversity targets to be factors gearing the over-boarding of directors. However, the study’s findings claimed that directors’ interlocking could provide helpful access to expertise, resources, and social networks, which could offer productivity to firms. Based on the review of the above literature, the study hypothesises the following:

H3a:

Board members’ over-boarding positively affects capital adequacy of commercial banks.

H3b:

Board members’ over-boarding positively affects efficiency use of equity of commercial banks.

H3c:

Board members’ over-boarding positively affects earning ability of commercial banks.

H3d:

Board members’ over-boarding positively affects asset quality of commercial banks.

H3e:

Board members’ over-boarding positively affects liquidity of commercial banks.

2.6. Boards’ important committees and financial performance

Elamer and Benyazid (Citation2018) emphasise the importance of board committees, particularly risk committees, and Abu et al. (Citation2020) stress the impact of credit, nomination, and evaluation committees on the financial performance of financial institutions. According to Elamer and Benyazid (Citation2018), there is a negative relationship between the existence, independence, meeting frequency, and size of the risk committee and performance. The relationship was tested between return on assets and return on equity as proxies for a financial position, whereas regressors were the existence of the risk committee, the number of directors in the risk committee, the percentage of non-executive directors to the total number of directors in the risk committee, and the frequency of risk committee meetings. The study findings revealed a significant negative relationship between the aspects of the board’s risk committee and financial performance. This implies that the presence of the board’s risk committee strengthens the control, monitoring, and supervision of the management team over the quality of risk-taking and risk management procedures and policies. This, in turn, reduces agency conflicts in the banking industry due to the nature of the industry. According to Mohammad et al. (Citation2018), from a study conducted on commercial banks in Jordan, there is a positive and significant relationship between the audit committee, ROE, and ROA.

Further, their study concluded that the association between the risk committee and bank performance is insignificant. Abu et al. (Citation2020) adopted a multiple regression analysis on panel data to assess the effect of board committees on the financial performance of deposit money banks. The board audit and risk management committees were reported to have had no significant effect on financial performance. This indicates that their existence or non-existence without considering other aspects makes their impact on financial position neutral. If so, these committees might be considered an added cost to firms with no value gained. The nomination and evaluation committee and the board credit committee showed a positive and significant association with financial performance. No significant association was found between the size of the board and financial performance, while the number of board meetings is reported to affect financial performance significantly and positively.

In exploring the impact of corporate governance mechanisms on financial performance, Al-Ahdal et al. (Citation2020) analyzed secondary data focusing on corporate governance mechanisms indicated by the audit committee, board accountability, and transparency disclosure index. Findings revealed that board accountability and the audit committee do have an insignificant impact, whereas transparent disclosure had an insignificant negative impact on firms’ performance, which was measured by return on equity and Tobin’s Q.

Based on the review of the above literature, the study hypothesizes the following:

H4a:

Existence of important committees (Risk Committee, Audit Committee, and Remuneration Committee) positively affects capital adequacy of commercial banks.

H4b:

Existence of important committees (Risk Committee, Audit Committee, and Remuneration Committee) positively affects efficiency use of equity of commercial banks.

H4c:

Existence of important committees (Risk Committee, Audit Committee, and Remuneration Committee) positively affects earning ability of commercial banks.

H4d:

Existence of important committees (Risk Committee, Audit Committee, and Remuneration Committee) positively affects asset quality of commercial banks.

H4e:

Existence of important committees (Risk Committee, Audit Committee, and Remuneration Committee) positively affects liquidity of commercial banks.

2.7. Board members’ ownership and financial performance

Boards’ ownership is related to the performance of commercial banks, according to a study by Nguyen et al. (Citation2020). When there is a large concentration of ownership by the board, performance is affected positively whoever El-Chaarani et al. (Citation2022) found that ownership concentration possesses a significant negative association with banks’ performance. An inverse influence of shareholding by board members and financial performance has also been reported by Kafidipe et al. (Citation2021) from the study conducted at Nigerian listed deposit money banks while assessing corporate governance, risk management, and financial performance. From the contradicting results, this particular study expects that:

H5a:

Board Members’ Ownership positively affects capital adequacy of commercial banks.

H5b:

Board Members’ Ownership positively affects efficiency use of equity of commercial banks.

H5c:

Board Members’ Ownership positively affects earning ability of commercial banks.

H5d:

Board Members’ Ownership positively affects asset quality of commercial banks.

H5e:

Board Members’ Ownership positively affects liquidity of commercial banks.

2.8. Board activities and financial performance

The relationship between corporate governance and financial performance has been explored by Aktan et al. (Citation2018) in a study conducted in the Kingdom of Bahrain’s financial firms, covering a period between 2011 and 2016. The study employed annual secondary data to establish the relationship where the annual number of board meetings was among the independent variables measured for its contribution towards financial performance. According to the study findings, it was established that the frequency (number) of meetings held by the board of directors does have a significantly negative impact on a firm’s financial performance as measured by return on equity. Their study implies that the high frequency of board meetings is presumed to be more destruction than construction. This result was consistent with the study of Salim et al. (Citation2016), which established that a high frequency of meetings yields better performance (a positive relationship compared to banks with a low frequency of board meetings). Based on the review of the above literature, the study hypothesizes the following:

H6a:

Board activities positively affect capital adequacy of commercial banks.

H6b:

Board activities positively affect efficiency use of equity of commercial banks.

H6c:

Board activities positively affect earning ability of commercial banks.

H6d:

Board activities positively affect asset quality of commercial banks.

H6e:

Board activities positively affect liquidity of commercial banks.

2.9. Board size and financial performance

Large-sized boards of directors can create problems with coordination and control and increase the time required for decision-making, leading to declining performance (Lamichhane, Citation2018). Also, an oversized board of directors has been found to negatively affect bank performance (Hajer & Anis, Citation2018). This is due to the decreased efficiency of governance mechanisms, which leads to reduced performance, unlike Prakash et al. (Citation2013), who investigated the impact of board size and other corporate governance variables on the efficiency of commercial banks. Their findings show that a bigger board improves commercial banks’ efficiency.

Based on the review of the above literature, the study expects that:

H7a:

Board size positively affects capital adequacy of commercial banks.

H7b:

Board size positively affects efficiency use of equity of commercial banks.

H7c:

Board size positively affects earning ability of commercial banks.

H7d:

Board size positively affects asset quality of commercial banks.

H7e:

Board size positively affects liquidity of commercial banks.

2.10. Board control and financial performance

Brown and Brown (Citation2011) and Yılmaz (Citation2010) emphasised the importance of board control towards its efficacy. That is, the board of directors should regularly assess itself, the board’s committees and senior members of management (chief executive officer) as to their performance towards the achievement of the firm’s goals. However, the literature does not attest to the existence of studies conducted to assess the influence of board control on the financial performance of commercial banks. Based on this fact, this present study opts to give evidence of the influence and hypothesises the following:

H8a:

Board control positively affects capital adequacy of commercial banks.

H8b:

Board control positively affects efficiency use of equity of commercial banks.

H8c:

Board control positively affects earning ability of commercial banks.

H8d:

Board control positively affects asset quality of commercial banks.

H8e:

Board control positively affects liquidity of commercial banks.

3. Research method

Panel data were collected from 15 commercial banks fully licensed by BoT during the period covered by the study, that is, 2003 to 2019, whereby variables’ information was extracted from these banks’ annual reports. Independent and dependent variables included and adapted for establishing the association between corporate governance and financial performance are presented in Table . The study deemed it necessary to control bank size, age, and ownership as they are likely to interfere with assessing the relationship since these factors also influence performance (Mori & Towo, Citation2017). A multiple linear regression model was adopted for the analysis with the help of STATA-16. The model was developed and adopted.

Table 1. Variables operationalisation

Where;

CAit/EEit /EAit /AQit /Lqit = Financial performance of bank i at time t, measured by capital adequacy, efficient use of equity, earning ability, asset quality, and liquidity of banks, respectively.

β0 = Constant, β1 …β12 = Beta coefficient, X1 …X8 = Constructs of corporate governance for bank n at time t, namely; Behavioural Aspect of Governance (BAG), Board Control (BC), Board Members Over-Boarding (BMO), Board Activities (BA), Board Gender Diversity (BGD), Board Size (BS), Directors’ Shareholding (DS), and Existence of Board’s Important Committees (ECOM).

X9 …X12 = Control variables to be adopted in the study; Bank size (SB), Ownership of the bank (OB), and Age of bank (AB).

αi = stands for controlling individual bank’s effect, which can affect the correlation due to panel data and εit = Error term.

4. Results

4.1. Descriptive statistics

The descriptive statistics of the variables for the firms are presented in Table .

Table 2. Variables’ descriptive statistics results

According to the results presented in Table , the mean value of capital adequacy is 0.13 (13%) with a minimum value of −1.8 and a maximum of 0.84, whereas the dispersion of values from the mean value is about 0.144. This value varies by 1% above the recommended ratio by the BoT as per the BoT’s banking sector supervision reports (2019), which recommend a minimum ratio of 12% for total capital adequacy. This implies that the studied banks possess adequate minimum capital for their operations.

Earning ability across all banks recorded a mean value of 0.03 (3%) with a minimum value of −0.53, the maximum value of 0.25, whereas the dispersion of value from the mean value is 0.52. The recommended ratio, according to BoT guidelines, is at least 5%; however, banks are advised to have a ratio of 0.2 (20%) for safe and sound operations of a bank (Banking sector supervision reports, 2019). With a mean value of 2%, it indicates the inefficient use of available assets of banks (Oyetade et al., Citation2021).

Efficiency use of equity (ROE) depicts the management’s ability to generate income from the available equity of the firm; the recommended ratio ranges from 15% to 20% (Moussu & Petit-Romec, Citation2017). ROE recorded a mean value of 0.17 (17%), indicating fair use of available equity in generating income for the studied commercial banks.

The mean value of the non-performing loan (asset quality) stood at 13.1% with a minimum value of 0% and a maximum of 99%, whereas the BoT’s recommended rate is 5% (Banking sector supervision reports, 2004 – 2019). This implies that commercial banks have a variation of at least 8% regarding NPLs. The liquidity ratio recorded a minimum value of 1.4% and the maximum value of 20%, with a mean of 11%. The comfort zone for the minimum required ratio of liquidity, according to BoT, is 20% (Banking sector supervision reports, 2012). This ratio explains the ability of banks to use available liquid assets to pay off short-term obligations; hence, liquidity ratio of 11% shouldn’t be considered satisfactory as it is only 11% of obligations (short term) that can be paid off by the available liquid assets (Durrah et al., Citation2016).

The percentage of women directors on the board is as low as 0% and as higher as 71%, with a mean of 20%. The state at which directors are being served with terms of reference for behavioural expectations of directorship, the proportion of members on the board who are senior leaders and non-senior leaders and the existence and execution of the annual board training budget have been measured at a mean value of 56% with a maximum of 1 and minimum of 0; 23% with a maximum 67% of and a minimum of 0%; 54% with a maximum of 1 and minimum of 0, respectively.

On average, the board of directors evaluates its performance and those of senior management at 60% with a minimum value of 0 and maximum of 1, whereas on average, 57% of the board’s chairpersons serve on more than two boards at the same time. The existence of important boards’ committees (audit, risk, remuneration, finance, and nomination committees) on average was 87% of all 15 banks in their board of directors. With control variables, banks included in the study have, on average, been in operation for 14 years and have an average size of Tanzania Shillings 316,227,766,016.8 (log 11.5), 27% of the studied banks were locally owned banks, and 73% were foreign-owned banks.

4.2. Variables’ correlation

The Spearman test has been adopted for checking for variable correlation (Table ) to describe how variables respond to each other and how they behave in response to any change in another variable.

Table 3. Variables’ correlation

The association observed is moderately positive and negative; no single indicator of CG showed a totally positive direction or negative association with FP. For instance, the number of meetings held annually affects the attributes of FP in positive and negative directions (0.054, −0.001, −0.061, −0.082, and 0.134 in terms of CA, EA, EE, AQ, and Lq, respectively). This implies that there is a weak to moderately positive association between the number of meetings and CA and Lq and a weak negative association with EE, EA, and AQ.

Bank size shows a positive relationship with CA (0.06), EA (0.06), and Lq (0.00). There was a negative association between EE (0.02) and AQ (0.00); hence, the larger the bank, the better capital adequacy, earning ability, and liquidity, and vice versa. Surprisingly, the age of the bank has an inverse relationship with EE (−0.03), EA (−0.00), and AQ (0.00), suggesting that the older the bank gets, the lower its EE, EA, and AQ are, and vice versa. This is contrary to Mori and Towo (Citation2017). Bank age has a positive association with only capital adequacy (0.27); type of ownership has a negative association with CA (0.08), EA (0.04), AQ (0.04), and Lq (0.26) but a positive association with EE (0.00). Also, according to Field (Citation2013), these correlation results confirm the variables’ non-multicollinearity since no high correlation (>0.8) between the variables has been recorded.

4.3. Diagnostic tests

Tests were conducted for the normality assumption, multicollinearity assumption, linearity assumption, heteroscedasticity assumption, and independence assumption (Yao & Li, Citation2014), and the test results are presented in Table .

Table 4. Data diagnostic test results

According to the results, the data were confirmed to be normally distributed since the Shapiro–Wilk test gave a result of p > 0.05. Since the variance inflation factor values are less than 10, the data is confirmed to be free from the multicollinearity problem (Daoud, Citation2018; Field, Citation2009)

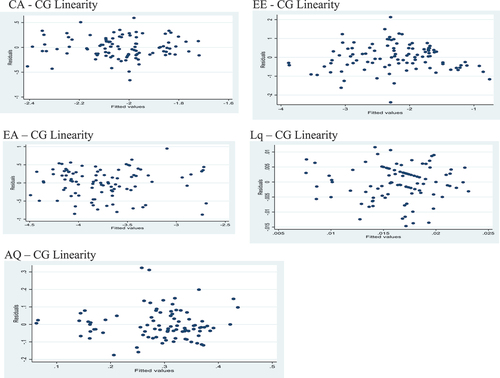

The Breusch–Pagan test confirmed the non-presence of heteroskedasticity since the calculated p-values are greater than 0.05 hence the presence of homoscedastic (Daoud, Citation2018). Durbin and Watson’s test results confirm no-serial dependence between variables; however, all five values are not close enough to two (2), hence the study’s adoption of the Newey command for regression in Stata (Bertrand et al., Citation2004). The Im-Pesaran-Shin (IPS) test was employed to check data stationarity (Pesaran, Citation2011). The significance p-value (p < 0.05) confirms stationarity; hence, the data have no unit root (Table ). Scatter plots were fitted for the linearity tests of financial performance and corporate governance indicators, whereby the test output (Figure ) suggests the linearity of the model since the scattered points move up and down alongside zero horizontally. The residual plot does not suggest a non-linear relationship between the fitted values and the residuals (Casson & Farmer, Citation2014).

Figure 4. Scatter plots for study variables.

4.4. Model fitness

Three tests were conducted to accurately decide which model should be chosen between the common, random, and fixed models. Results are presented in Table , in which a stepwise test was performed from the Chow test (to decide between common and fixed effects) to the Hausman test (to decide between fixed and random effects) and finally, the Breusch and Lagrange multiplier test, where the common effect model is picked since p-values are greater than 0.05.

Table 5. Model fitness test results

4.5. Regression model results

This part presents the models’ results which show the general correlation between independent and dependent variables. It presents the results of the five study models, which attempt to establish the association between FP and CG while controlling for bank size, bank age, and type of bank ownership, as shown in Table .

Table 6. Regression results for model one to five

According to the results, with the study’s model 1, CA is statically and negatively correlated with BAGi and DS at a 10% and 5% significance level, respectively, whereas it is positively associated with BMO at a 10% significance level. Taking abroad the existence of all constructs and holding them constantly, CA is positively influenced by AB and OB at 5% and 10% significance levels, respectively. The analysis failed to establish any significant association between CA and GDB, BC, ECOM, BS, and BAGiii. The resulting R2 of 0.24 implies that the ten studied corporate governance indicators can predict 24% of the commercial banks’ CA.

Banks’ EE, according to the analysis, is significantly positively associated with BAGi at a 1% level of significance, whereas BAGii, BC, BS, DS, and ECOM were reported to have a negative association with EE at 10%, 5%, 5%, 5%, and 1% levels of significance, respectively. Other constructs of GC did not reveal any association with EE. The obtained R2 of 0.34 implies that the variance-efficient use of equity in commercial banks can be predicted by the ten studied constructs of corporate governance by 34%.

As with model 3 of the study, the existence and execution of an annual board training budget on soft skills are positively and significantly associated with EA (p < 0.01), whereas DS is significantly associated (positively) with EA (p < 0.05). BS is statistically and significantly associated with EA at a 1% significance level. The remaining corporate governance constructs didn’t indicate a significant association with EA, as shown in Table . Age and bank ownership are negatively associated with EA at 5% and 10%, respectively, whereas bank size doesn’t significantly affect earning ability. Further, 46% (R2 = 0.46) of EA is predicted by the studied constructs of CG.

The association of QA and GC (Model 4) is reported to be statistically and significantly negative through BGD and BMO at a 1% and 5% level of significance, respectively,

When board members are served with terms of reference for behavioural expectations of directorship, board size, and board members’ shares-holding are positively and statistically associated with QA (5%, 1%, and 1%), respectively. The rest of the constructs of CG are not associated with AQ at any level of significance, as indicated in Table .

The association of AQ with control variables is positive at a 5% significance level with bank age only. Through the studied constructs, GC can predict the AQ of commercial banks by 45% (R2 = 0.45), which indicates the strength of corporate governance in explaining the financial performance of commercial banks (asset quality).

According to the analysis of the results, banks’ liquidity positively and significantly correlates with BS (5% significance level), whereas it is negatively associated with DS at a 5% significance level.

Other constructs did not record any significant association with the Lq of banks. As with control variables, only AB records a negative association with Lq (10% significance level). According to the results, only 15% (R-squared = 0.15) of the commercial banks’ liquidity variance can be predicted by the ten studied corporate governance constructs.

5. Discussion and hypothesis results

The influence of corporate governance on financial performance has been investigated through the ten and five constructs of corporate governance and financial performance, respectively. This discussion focuses on elaborating on the results and comparing the current results with previous studies to provide a better ground for hypothesis decision-making, and conclusion thereafter. According to the data analysis results, corporate governance’s influence on financial performance is multifaceted, varying from one indicator to another of both independent and dependent variables.

According to the analysis, Board Gender Diversity, as measured by the proportion of women directors to male directors, has been recorded to have a significant (1%) statistical negative correlation with AQ as measured by the ratio of non-performing loans with a coefficient of −0.03 and a p-value of 0.01 hence confirming H1d and rejecting H1a H1b H1c and H1e (Table ). These results indicate that an additional number of women directors on the board will mean a reduction in the ratio of non-performing loans, the opposite being true. This indicates that boards with a good number of women directors are in a good position to supervise and monitor credit risk, reducing the possibility of bad loans.

Table 7. Board gender diversity hypothesis results

These results are consistent with studies conducted by (Elbahar, Citation2019), who concluded that female board members are associated with the bank’s good financial performance to a greater degree and that the presence of women directors is associated with a high level of maturity in decision-making. Mori and Olomi (Citation2012) also reported a significant positive association between female board members and financial performance. Assenga et al. (Citation2018) also reported that the presence of women directors on the board significantly affects the financial performance of commercial banks.

BGD did not record any statistically significant association with CA, EE, EA, and Lq.

The behavioural aspects of governance were measured in three different ways that attempted to establish (i) whether members are being served with terms of reference for behavioural expectations of directorship (BAGi), (ii) the proportion of board members who are senior leaders or greater entrepreneurs to those who are not (BAGii), and (iii) the existence and execution of the annual board’s training budget on soft skills (BAGiii). This aspect is still new regarding its link to financial performance; hard and soft skills and emotional factors are considered to have a relationship with the efficacy of the board of directors (Marnet, Citation2004). According to the study’s findings, 56% of the boards of commercial banks included in the study were found to have been serving every new director with terms of reference for behaviour expectations. This aspect has also been studied as to its impact on the financial performance of banks; the regression analysis provided both types of associations with regard to the indicators of financial performance used in the study. BAGi has a negative association with CA at a 10% significance level with a coefficient of −0.01 and a p-value of 0.05. On the other hand, regression analysis provided a positive correlation with EE at a 1% significance level (coefficient = 1.31 and p-value of 0.00) and a positive relationship with AQ at a 5% level of significance, coefficient of 0.11 and p-value of 0.02. The positive correlation implies that providing terms of reference for behavioural expectations of directorship to members of the board is beneficial for financial performance through AQ and EE, bearing in mind that the major revenue to the banking business comes from loans which make up to 60% of total assets of the bank.

The proportion of senior leaders to non-senior leader board members (BAGii) was found at an average ratio of 0.23 to 0.77 from all 15 banks included in the study.

Regression analysis reports a positive statistical association between BAGii and CA at a 5% level of significance with a coefficient of 0.06 and p-value of 0.03, indicating that those types of members (senior leadership) influence beneficial business ventures. However, the same construct is reported by findings analysis to have an inverse relationship with financial performance with respect to EE, at a 10% level of significance, a coefficient of −0.59 and a p-value of 0.07.

The sense of personal responsibility, self-management, integrity, honesty, team player-ship, servant leadership, personal habits and attitudes, and ability to work with other genders and cultures (soft skills) have been measured by the existence of the annual board training budget and the execution of the same. On average, 50% of banks provided evidence of the budget’s existence and an annual training calendar for the same.

Results of regression analysis show a statistically positive influence at a 1% level of significance between BAGiii and earning ability of CBs (coefficient = 0.55 and p-value of 0.00), implying that possession of these types of soft skills by the board of directors does increase the bank’s profitability.

These findings cement previous studies that recommended a need for carefulness in the composition of the board of directors in terms of their political, senior leadership, and entrepreneurial effects on the board’s efficacy (Alqudah et al., Citation2019; Brown & Brown, Citation2011; Marnet, Citation2004; Yılmaz, Citation2010). These statistical results confirm hypotheses H2a; H2b; H2c, and H2d and reject hypothesis H2e as presented in Table and the hypothesis decision made thereof presented in Table .

Table 8. Behavioural aspects of governance hypothesis results

Board Control was found to have a statistically positive association with liquidity and earning ability at the coefficient of 0.03 (p-value of 0.02) and 0.02 (p-value of 0.01), respectively, confirming H8c and H8e (Table ). This cements the significance of having a clear line of responsibilities between organs which enables the top organ to conduct self-assessment as well assessment of the performance of their subordinates.

Table 9. Board control hypothesis results

Formally evaluating its activities is crucial for a board of directors to cultivate accountability. The board, its committees, and individual members can be assessed for overall effectiveness through a well-conducted board evaluation. This process can reveal areas for improvement and ensure that the board is carrying out its responsibilities proficiently. Furthermore, regular evaluations can foster alignment between the board’s actions and the organization’s values, define expected behaviors, set the tone for the organization, and encourage openness, honesty, and trust.

However, it was established that some of the banks do not conduct the assessment as measured by board control (BC), as the study results reported that only 60% of banks perform the performance assessment or evaluation as evidenced by the clause in their annual reports. Despite the emphases by Brown and Brown (Citation2011) and Yılmaz (Citation2010) on the importance of board control towards its efficacy, an insignificant inverse relationship has also been established by the study on the aspect of efficient use of equity and asset quality, which implies that board control is not a total motivation factor for financial performance as measure by efficiency use of equity and asset quality.

The influence of the board of directors (CG) has also been assessed throng Board members’ over-boarding (total number of boards in which directors have a membership), which is a construct whose past reference does not show its association with the performance of banks as an aspect of CG but rather as an aspect of an effective and efficient board of directors. According to Brown and Brown (Citation2011) and Yılmaz (Citation2010), when board members sit on many boards at the same with the performance of banks as an aspect of corporate governance but rather as an aspect of an effective and efficient board of directors. According to Brown and Brown (Citation2011) and Yılmaz (Citation2010), when board members sit on many boards simultaneously, it tends to reduce the effectiveness of the directors, thereby impacting the performance of entities that are served by such boards. Study findings report that at least43% of board’s chairpersons served on more than two boards at varying times throughout the duration covered by the study. Regression analysis provided a statistically significant influence of BMO in both directions. Firstly is a positive correlation with CA (coefficient = 0.15* and p-value = 0.07); secondly, a negative correlation with QA (coefficient = −0.11*** and p-value = 0.00). To these results, doubts regarding a director’s capability to carry out their duties effectively are justified when considering the substantial time commitment required for each directorship. Research has indicated that businesses with directors or executives who hold too many board positions may experience subpar performance.

However, the positive correlation indicates an advantage of directors sitting on many boards, which might mean gaining expanded experience, knowledge, and positive information about the market and other related matters on the business, which have a positive impact gained from other directorships. Alqudah et al. (Citation2019) also failed to establish a direct relationship between directors’ busyness and firms’ performance in their study.

Board members’ over-boarding has been confirmed to positively affect the financial performance of CBs through the bank’s asset quality, as shown in Table through the results of hypothesis testing.

Table 10. Board members over-boarding hypothesis results

The presence of audit, risk, and remuneration committees (ECOM) in the board of directors, according to Pearson correlation, exhibited a significant positive association with CA (coefficient = 0.2) and a negative association with EE (coefficient = −0.26). As with regression analysis results, a statistically significant negative association at a 1% confidence level has been established between ECOM and EE (coefficient = −1.5 and p-value = 0.00), supporting H4b (Table ). This implies that the existence of these committees has a positive influence on a bank’s capital adequacy and that the removal of one or more committees will equally minimize the capital adequacy levels. The study examined the existence of any three committees, with risk and audit committees being necessary. According to these results, these three committees negatively and positively influence FP. These committees are designed to enhance corporate governance mechanisms, reduce risks, and ensure executives’ accountability for their roles. Their essence includes providing independent oversight of the bank’s financial reporting process and internal controls, monitoring and managing the bank’s risks, setting executive compensation policies, and ensuring that they align with the bank’s long-term objectives, motivating executives to work towards maximising shareholder value. However, the presence of these committees, if not adequately structured, can increase costs and bureaucracy, reducing efficiency and ultimately affecting financial performance. Conflicts of interest can also compromise committees’ ability to perform their duties effectively.

Table 11. Existence of important committees hypothesis results

The negative association as per this study’s results is consistent with the findings of the study conducted by Abu et al. (Citation2020), who reported that the board audit committee and risk management committee are reported to have no significant effect on the financial performance and recommended cost adding element by their existence. But the nomination and evaluation committees were reported to impact financial performance positively. There were no reported significant associations of ECOM with EA, AQ, or Lq.

Board size has been observed to average at eight directors, with a maximum of fifteen and a minimum of four. According to the results, it was during the early 2000s when boards had fewer directors compared to recent years. According to the analysis, the board size has an inverse correlation with efficient use of equity (coefficient = −1.74 and p-value of 0.01) at a 0.05 significance level and with earning ability (coefficient = −1.3 and p-value of 0.00) at a 0.05 level of significance. The analysis also exposed a positive relation between board size and asset quality with a 1% significance level, 0.23 coefficient, and a p-value of 0.00. No significant relationship was exposed between board size with CA and Lq; these results support H7b, H7c and H7d (Table ).

Table 12. Board size hypothesis results

The analysis results suggest that a small board of directors is associated with good performance, and many directors are associated with poor financial performance. The negative association is consistent with the results of Alqudah et al. (Citation2019), whereas the positive association is consistent with studies done by Al-Matari (Citation2020), Elbahar (Citation2019), and Khatun and Ghosh (Citation2019).

Director shareholding at banks where they practice directorship is expected to influence performance positively. The highest recorded per cent of shares held by directors as per this study was 60%, a minimum of 0%, with a mean value of 5.5, meaning that for a large portion of the studied banks, the majority of directors are not shareholders.

The analysis results disclose a positive correlation between directors’ shareholding and earning ability as well as asset quality at 0.05 and 0.01 levels of confidence, coefficients of 0.05 and 0.02, and p-value of 0.05 and 0.00, respectively. Director’s shareholding also positively impacts financial performance through EE at a 5% significance level, 0.02 p-value, and a coefficient of 0.19. These statistical results support H5b, H5c, and H5d (Table ), implying that when part of the directors are shareholders (owners) of the bank, their efficacy on supervision, decision-making, and business overseeing is significantly effective hence better performance.

Table 13. Board members’ ownership hypothesis results

However, surprisingly, the results also reported a negative association of directors’ shareholding with capital adequacy of banks at coefficient = −0.03, a p-value of 0.03 and a 0.05 significance level, and with earning ability (coefficient = −1.3 and p-value of 0.00) at a 0.05 level of significance. The same negative correlation has been exposed on liquidity levels with a coefficient of −0.04, a p-value of 0.04, and a 5% significance level, meaning their relationship is inverse, which lessens the propositions of agency theory.

Previous studies that had similar results as the current study includes Habtoor (Citation2021), whose study concluded an inverse relationship between directors’ shareholding and ROA and ROE, whereas Habtoor (Citation2021) reported a positive association at a 5% level of significance between the presence of directors who are shareholders and bank performance.

Board Members’ Ownership has been confirmed to have a positive effect on the financial performance of CBs through the bank’s efficiency use of equity, banks’ earning ability, and banks’ asset quality, as shown in Table through the results of hypothesis testing.

Averagely, according to descriptive analysis, the board of directors meet five times annually with a minimum of two and a maximum of eleven meetings. The number of meetings the board of directors held annually was used as a measure of Board activities. According to regression analysis, board activities are reported to statistically significantly and positively correlate with earning ability (coefficient of 0.7, p-value of 0.00) and banks’ liquidity (coefficient of 0.04, p-value of 0.05) at 1% and 5% significance levels, respectively, hence supporting H6c and H6e (Table ).

Table 14. Board activities hypothesis results

This means that as the number of meetings increases, so do the levels of liquidity and earnings of banks, and vice versa. These findings are consistent with those of other previously conducted studies, including those conducted by Al-Matari (Citation2020) and Abu et al. (Citation2020). However, the findings contradict those of Alqudah et al. (Citation2019), whose study revealed an insignificant influence of the number of meetings on financial performance. Prakash et al. (Citation2013) also concluded in their study that board meetings’ minimum frequency (one meeting per quarter) leads to better performance. The analysis failed to indicate any significant association between the number of meetings and the commercial banks’ capital adequacy, efficient use of equity, and asset quality.

4.6. Controlled variables

The study controlled for Bank age, bank size, and board members’ citizenship which were analyzed by both Pearson and multiple linear regression analysis, whereas a type of ownership was only analyzed by Pearson because it did not meet the assumption of multiple linear regression analysis. These four variables were used in the study as control variables to take care of individual banks’ effects regarding their difference in size, age, and type of ownership, as previous studies reported they affected financial performance. Alqudah et al. (Citation2019) reported a significant negative correlation between age and performance; also, a positive correlation was reported between the firm’s size and performance, and the age of the bank positively affected ROA. Mori and Towo (Citation2017) also reported a positive association between age and the financial performance of banks. Sunday and Godwin (Citation2017) reported that the presence of foreign board members on the board had a significant and positive association with the financial performance of banks.

The size of the bank as measured by the log of assets was found to have a positive association with capital adequacy, earning ability, and liquidity as measures of financial performance at 10% (coefficient = 0.12), 10% (coefficient = 0.12), and (coefficient = 0.4) 1% significance levels, respectively. However, a negative association with efficient use of equity (10% significance level and −0.15 coefficient) and asset quality (1% level of confidence and −0.3 coefficient) was recorded according to the Pearson correlation. The MLR analysis results show a negative association between bank size and financial performance (CA) at a 5% significance level with a coefficient of −1.86 and a p-value of 0.05.

According to the study findings, the age of the bank had a significantly positive association with capital adequacy at a 1% level of significance (coefficient of 0.22 and p-value = 0.08) and asset quality at a 5% level of significance (coefficient of 0.09 and p-value = 0.03). These statistical results indicate that the more years the bank survives, the better its capital levels and, as a measure of asset quality, the lower its non-performing loans.

Surprisingly, the age of a bank is negatively associated with earning ability at a 5% level of significance (coefficient of −0.39 and p-value = 0.0) and liquidity at a 1% level of significance (coefficient of −0.26 and p-value = 0.06). The implication of these results can be related to the proposition of agency theory on the self-serving of managers’ interests and jeopardizing owners’ interests on the grounds that if managers stay longer in the managerial position, it becomes easier to work on self-interest.

6. Robustness of the findings

Previous studies on the association between financial performance and corporate governance raised the alarm about the potential existence of endogeneity problems, particularly a study by Hermalin and Weisbach (Citation2003) and Aljughaiman (Citation2019). This current study opted to be more precise with the financial performance estimates, hence adopting the Generalized Method of Moment’s regression for the purpose.

The Generalized Method of Moments Regression (GMM) Analysis, specifically a one-step GMM David (Citation2009) system, has been adopted. Further, to check for the assumptions behind the GMM estimators, specifically the instruments’ joint exogeneity, the Hansen (Citation1982) and Sargan (Citation1958) J-test over-identifying restrictions test has been performed (results presented in Table ), which failed to reject the null hypothesis, hence confirming the GMM adoption.

The Arellano—Bond tests (Arellano & Bond, Citation1991; Arellano & Bover, Citation1995) were also performed for the first-order serial correlation (AR1) and the second-order correlation (AR2) with the purpose of autocorrelation assessment. As per the tests’ results (Table ), null hypotheses couldn’t be rejected, implying that the original error term is serially uncorrelated and the moment conditions are correctly specified (that is, the value of AR(2)>0.05)

According to the GMM results, the study first established the association between financial performance and t-1-lagged financial performance. As presented in Table , it has been established that there is a highly positive association between the current year’s financial performance and the previous year’s financial performance, specifically with the earning ability of banks. This indicates that good performance in the previous year is likely to fuel good performance in the current year by at least 51% with a 1% level of significance. Unlike for efficient use of equity and asset quality, where the association between past and current performance is negative at 1% and 10%, respectively, liquidity, on the other hand, has been revealed to have a positive association between the previous year’s recorded rates of liquidity and the current year’s financial performance; this is at a 10% level of significance with a 0.201 (20%) coefficient. The test failed to establish any association between the previous year’s and the current year’s capital adequacy.

Further to the above findings, the GMM regression has confirmed several significant associations between the dependent and independent variables. According to the presented results in Table , the robustness test confirmed a significant association between the quality of credit process control and asset quality (1% level of significance) and the adequacy of the recovery process and asset quality (5% level of significance) and also the association between the behavioural aspect of governance and efficient use of equity (1% level of significance), the behavioural aspect of governance and asset quality (5% level of significance), and directors’ shareholding with earning ability at 1% level of significance. With these results, it suggests that the listed constructs of independent variables corporate governance and credit risk management practices do have a positive and significant influence on financial performance, even though some of the financial performance indicators are driven by previous years’ performance.

Risk assessment and liquidity ratios, boards’ aspects of governance and efficient use of equity, board members over-boarding and asset quality, board size and efficient use of equity, and the proportion of directors who are shareholders and liquidity have as well been confirmed to have a negative association at different levels of significance.

As with control variables, the GMM analysis confirmed positive associations between the size of banks and liquidity (1% level of significance), the age of banks and capital adequacy (1% level of significance), the age of banks and asset quality (1% level of significance), as well as the type of banks’ ownership and efficiency use of equity (5% level of significance). A negative association has also been confirmed by the GMM regression analysis between the size of the bank and capital adequacy at a 1% level of significance, as well as the age of the bank at a 1% level of significance. However, GMM results differ from MLR results on several reported associations between dependent and independent variables, as in Table , in the highlighted cells.

Table 15. Robustness of empirical study findings

7. Conclusion and recommendations

Based on the empirical evidence generated from the statistical analysis, discussion, and hypothesis tests, the study concludes that, generally, corporate governance influences the financial performance of commercial banks in Tanzania.

Specifically, the number of meetings held by the board of directors was found to affect banks’ earning ability. The presence of female directors on the board influences the asset quality of commercial banks. The behavioural aspect of governance affects banks’ financial performance through capital adequacy, earning ability, efficient use of equity, and asset quality. Assessment and self-evaluation of board members also influence financial performance, specifically the efficient use of equity at commercial banks. The study also concludes that the fact that the chairperson of the board sits on too many boards does affect financial performance in terms of banks’ capital adequacy and the quality of their assets. Finally, the existence of the board’s important committees (audit, risk, and remuneration committees) affects banks’ financial performance, especially the efficient use of equity. The study recommends that corporate governance principles and mechanisms be enhanced to improve the financial performance of commercial banks.

8. Implications for managers and policymakers

According to the findings, the supervision and monitoring role of the board of directors, directly and indirectly, impact performance. Therefore, there is a need for corporate governance principles and mechanisms to be enhanced for the betterment of the financial performance of commercial banks. Specifically, the introduction of a behavioral aspect of governance in the field of the study reflected a strong impact on performance; therefore, the following are recommended for owners of banks.

Chairpersons of boards are not to sit on more than two boards at a time as participating on many boards reduces the efficiency and productivity of members, which jeopardises the performance of banks.

Senior government leaders are not to be considered for the board of directors, as their presence on the board has an inverse relationship with financial performance.

Enrichment of directors with soft skills (board-room expectations) and enforcement of the board’s self-assessment is recommended to be insisted by regulators as these two demonstrated to impact banks’ performance.

Central bank is advised to reconsider the minimum number of members to the board of directors of CBs, the study recommends for a small board of directors (nine to eleven members) as big-sized board presents an inverse association with performance; however, a precaution is advised for the board to be of sufficient size to allow for non-co-members of the audit committee to enhance committees of independence.

9. Implications for future researchers

This current study focused on identifying the influence and association between corporate governance and the financial performance of commercial banks utilizing panel data; however, the approach came with its associated challenges. To overcome those challenges, future studies are encouraged to adopt a proper mix of secondary and primary data and utilize short-range data. This will enable obtaining valid and meaningful supplementary information from primary data to support and explain secondary data.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abu, S. O., Alhassan, A. S., & Okpe, J. U. (2020). Board committees and financial performance of listed deposit money banks in Nigeria. Journal of Management Sciences, 2(2), 33–31.

- Aktan, B., Turen, S., Tvaronavičienė, M., Celik, S., & Alsadeh, H. A. (2018). Corporate governance and performance of the financial firms in Bahrain. Polish Journal of Management Studies, 17(1), 39–58. https://doi.org/10.17512/pjms.2018.17.1.04

- Al-Ahdal, W. M., Alsamhi, M. H., Tabash, M. I., & Farhan, N. H. S. (2020). The impact of corporate governance on financial performance of Indian and GCC listed firms: An empirical investigation. Research in International Business and Finance, 51, 1–13. https://doi.org/10.1016/j.ribaf.2019.101083

- Aljughaiman, A. A. (2019). Effects of corporate governance mechanisms on financial flexibility, risk-taking behaviour and risk management effectiveness: A comparison study between conventional and Islamic banking systems [ PhD thesis]. Newcastle University.

- Ally, Z. (2014). Determinants of banks’ profitability in a developing economy: Empirical evidence from Tanzania. European Journal of Business and Management, 6(31), ( Online). www.iiste.org

- Al-Matari, E. M. (2020). Do characteristics of the board of directors and top executives have an effect on corporate performance among the financial sector? Evidence using stock. Corporate Governance (Bingley), 20(1), 16–43. https://doi.org/10.1108/CG-11-2018-0358

- Alqatamin, R. M. (2018). Audit Committee effectiveness and company performance: Evidence from Jordan. Accounting & Finance Research, 7(2), 48. https://doi.org/10.5430/afr.v7n2p48

- Alqudah, A. M., Azzam, M. J., Aleqab, M. M., & Shakhatreh, M. Z. (2019). The impact of board of directors characteristics on banks performance: Evidence from Jordan. Academy of Accounting & Financial Studies Journal, 23(2), 1–16. Print ISSN: 1096-3685; Online ISSN: 1528-2635.

- Arellano, M., & Bond, S. (1991). Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. The Review of economic studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Arellano, M., & Bover, O. (1995). Another Look at the Instrumental Variable Estimation of Error-Component Models. Journal of econometrics, 68, 29–52. https://doi.org/10.1016/0304-4076(94)01642-D

- Assenga, M. P., Aly, D., & Khaled, H. (2018). The impact of board characteristics on the financial performance of Tanzanian firms. Corporate Governance, 18(6), 1089–1106. https://doi.org/10.1108/CG-09-2016-0174

- Balagobei, S. (2019). Corporate governance and non-performing loans: Evidence from listed banks in Sri Lanka. International Journal of Accounting & Business Finance, 5(1), 72–85. https://doi.org/10.4038/ijabf.v5i1.40

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Barney, J. B. (1986). Strategic factor markets: Expectations, Luck, and business strategy. Management Science, 32(10), 1231–1241. https://doi.org/10.1177/014920639101700108

- Bertrand, M., Duflo, E., & Mullainathan, S. (2004). How much should we trust differences-in-differences estimates? The Quarterly Journal of Economics, 119(1), 249–275. http://qje.oxfordjournals.org/

- Brown, D. L., & Brown, D. A. (2011). Boardroom behaviours and governance. Governance Solutions BGI Publishing Inc, 1–7. https://www.governancesolutions.ca/governance-solutions/publications/pdfs/Behaviour%20and%20Governance.pdf

- Casson, R. J., & Farmer, L. D. M. (2014). Understanding and checking the assumptions of linear regression: A primer for medical researchers. Clinical and Experimental Ophthalmology, 42(6), 590–596. https://doi.org/10.1111/ceo.12358

- Castanias, R. P., & Helfat, C. E. (1991). Managerial resources and rents. Journal of Management, 17(1), 155–171. https://doi.org/10.1177/014920639101700110

- Chou, T.-K., & Buchdadi, A. D. (2017). Independent board, Audit committee, risk Committee, the meeting attendance level and its impact on the performance: A study of listed banks in Indonesia. International Journal of Business Administration, 8(3), 24–36. https://doi.org/10.5430/ijba.v8n3p24

- Daniel, C. J., Kalistus, M. A., & Kira, A. R. (2021). The influence of CAMEL ratios on credit rating evaluation in Tanzanian commercial banks: An empirical analysis. International Journal of Multidisciplinary Research and Explorer, 1(10), 6–15. https://doi.org/10.1118/IJMRE.2021983932

- Daoud, J. I. (2018). Multicollinearity and regression analysis. Journal of Physics Conference Series, 949(1), 012009. https://doi.org/10.1088/1742-6596/949/1/012009

- David, R. (2009). How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136.

- Durrah, O., Aziz, A., Rahman, A., Jamil, S. A., & Ghafeer, A. (2016). Exploring the relationship between liquidity ratios and indicators of financial performance: An analytical study on food industrial companies listed in Amman Bursa. International Journal of Economics and Financial Issues |, 6(2), 435–441. http://www.econjournals.com

- Elamer, C. A. ;, & Benyazid, A. A. (2018). The impact of risk committee on financial performance of UK financial institutions. International Journal of Accounting and Finance, 8(2), 161–180. https://doi.org/10.1504/IJAF.2018.093290

- Elbahar, E. R. (2019). Board of director’s characteristics and bank performance: Evidence from GCC region. Corporate Ownership & Control, 17(1), 14–23. https://doi.org/10.22495/cocv17i1art2

- El-Chaarani, H., Abraham, R., & Skaf, Y. (2022). The impact of corporate governance on the financial performance of the Banking sector in the MENA (Middle Eastern and North African) region: An immunity test of banks for COVID-19. Journal of Risk and Financial Management, 15(2), 82. https://doi.org/10.3390/jrfm15020082

- Fajriyanti, N., Sukoharsono, E. G., & Abid, N. (2021). Examining the effect of diversification, corporate governance and intellectual capital on sustainability performance. International Journal of Research in Business and Social Science, 10(2), 12–20. https://doi.org/10.20525/ijrbs.v10i2.1053

- Field, A. P. (2009). Discovering statistics using SPSS : (And sex and drugs and rock “n” roll). SAGE Publications.

- Habtoor, O. S. (2021). The influence of board ownership on bank performance: Evidence from Saudi Arabia. The Journal of Asian Finance, Economics & Business, 8(3), 1101–1111. https://doi.org/10.13106/jafeb.2021.vol8.no3.1101

- Hajer, C., & Anis, J. (2018). Analysis of the impact of governance on bank performance: Case of commercial Tunisian banks. Journal of the Knowledge Economy, 9(3), 871–895. https://doi.org/10.1007/s13132-016-0376-6

- Haji, A. A., & Ghazali, N. A. M. (2018). The role of intangible assets and liabilities in firm performance: Empirical evidence. Journal of Applied Accounting Research, 19(1), 42–59. https://doi.org/10.1108/JAAR-12-2015-0108

- Hansen, L. P. (1982). Large Sample Properties of Generalized Method of Moments Estimators. Econometrica, 50(4), 1029–1054. https://doi.org/10.2307/1912775

- Hermalin, B. E., & Weisbach, M. S. (2003). Boards of directors as an endogenously determined institution: A survey of the economic literature. FRBNY Economic Policy Review, 9(1), 7–26. https://ssrn.com/abstract=794804

- Hermawan, S., Hanif, A., Biduri, S., & Wijayanti, P. (2021). Intellectual capital, corporate social responsibility, and good corporate governance on banking financial performance in Indonesia. Advances in Economics, Business and Management Research, 183(1), 10–16. https://doi.org/10.2991/aebmr.k.210717.003

- Kabir, A., & Dey, S. (2012). Performance analysis through CAMEL rating: A comparative study of selected private commercial banks in Bangladesh. Journal of Politics & Governance, 1(2/3), 14–25. .

- Kafidipe, A., Uwalomwa, U., Dahunsi, O., Okeme, F. O., & Ntim, C. G. (2021). Corporate governance, risk management and financial performance of listed deposit money bank in Nigeria. Cogent Business & Management, 8(1). https://doi.org/10.1080/23311975.2021.1888679

- Kapaya, S. M., & Raphael, G. (2016). Bank-specific, industry-specific and macroeconomic Determinants of banks profitability: Empirical evidence from Tanzania. International Finance and Banking, 3(2), 100–119. https://doi.org/10.5296/ifb.v3i2.9847

- Kasoga, P. S., & Elgammal, M. M. (2020). Does investing in intellectual capital improve financial performance? Panel evidence from firms listed in Tanzania DSE. Cogent Economics & Finance, 8(1), 1802815. https://doi.org/10.1080/23322039.2020.1802815

- Khatun, A., & Ghosh, R. (2019). Corporate governance practices and non-performing loans of banking sector of Bangladesh: A panel data analysis. International Journal of Accounting and Financial Reporting, 9(2), 12–28. https://doi.org/10.5296/ijafr.v9i2.14503

- Lamichhane, P. (2018). Corporate governance and financial performance in Nepal. NCC Journal, 3(1), 108–120. https://doi.org/10.3126/nccj.v3i1.20253