Abstract

Recent financial upheavals and economic downturns have triggered and sped up the research on financial distress in general and in the Banking industry in specific. The current review attempts to gauge and map performance trends and intellectual knowledge structure of the financial distress research in the banking industry. A hybrid approach was adopted to inventorize, analyse and evaluate the financial distress literature pertaining to the banking industry (1982–2022); the authors apply bibliometric analysis to identify critical financial distress literature articles and journals, followed by the identification of central financial distress literature research themes through co-citation analysis. We found that financial distress researchers have published 11 papers each year since 1982, and the number of citations received by the research domain has significantly risen, adding more importance to this research domain. Further, the analysis helps delineate four thematic knowledge clusters throwing light on the nomological network of the field and giving a bird’s eye-view of the intellectual structure of the field. Since this review utilised data from a single database, i.e. Scopus, any shortcomings associated with the database would undoubtedly impact the results.

1. Introduction

Accounting and finance researchers have studied financial distress prediction for the last five decades (Shi & Li, Citation2019). Numerous academic works have focused on corporate bankruptcy because of the potentially devastating effects it can have on creditors and economies. Many financial scandals had a serious impact on all economies (Al-Absy & Ntim, Citation2020; Al-Absy et al., Citation2020). Foster (Citation1986) defined financial distress as a “serious liquidation problem which is unable to be resolved without a large-scale restructuring of the operation or structure of economic entities” (Sun et al., Citation2014, p. 42). Financial distress indicates approaching bankruptcy, and its prediction can alert investors and creditors of probable losses (Zhou et al., Citation2022). The initial journey started by Beaver (Citation1966) and then extended by Altman (Citation1968) for bankruptcy prediction using financial ratios. After the global financial crisis that resulted in the recession in 2008–09, there is more need for bankruptcy prediction and corporate financial distress. In the preliminary phases of financial distress, a company’s long-term debt exceeds its cash flow, making it unable to meet its financial compulsions (Whitaker, Citation1999). Financial distress is the incapacity of a corporation to make its payments when they become due. In a broad sense, it refers to the inability to pay obligations (such as debt) when they are due (Beaver et al., Citation2010). In reality, many struggling businesses may come back from the edge of financial distress and resume normal operations. Also, 52% of sampled firms with poor financial states undergo management turnover (Gilson, Citation1989) and extensive alterations to the leadership and structure of the organisation (Wruck, Citation1990). Self-efficacy prevents firms from financial distress (Kuhnen & Melzer, Citation2018). Debt-restructured companies that continue to operate with high leverage, low investment, and poor performance may frequently enter into financial distress again (Kahl, Citation2002). A growing body of evidence suggests that mergers and acquisitions can help financially distressed and also reduce their chances of bankruptcy (Zhang, Citation2022) and; in the United States, total investment in merger and acquisition was about 5.8 trillion dollars between 2010 and 2018 and out of this total 23% firms are distressed.

Our research has revealed the five most relevant reviews of financial distress (Altman et al., Citation2017; Habib et al., Citation2020; Keasey & Watson, Citation1991; Mallinguh & Zéman, Citation2020; Sun et al., Citation2014). Altman et al. (Citation2017) in their review talked about the Z-Score model utility in an international context, particularly for banks, Sun et al. (Citation2014) reviewed the domain of financial distress prediction; Keasey and Watson (Citation1991) discuss the managerial applications and limitations of adopting financial distress prediction models, Habib et al., (Citation2020) examines determinants and consequences of financial distress, and Mallinguh and Zéman (Citation2020) discusses financial distress prediction and mitigation strategies.

Existing reviews have added to the current literature on financial distress (Altman et al., Citation2017; Habib et al., Citation2020; Yousaf et al., Citation2022). We believe a more thorough and systematic discussion in this growing field would be beneficial, so we endeavour to conduct a statistics-based analytical technique, i.e., bibliometric analysis. This technique is superior to the systematic literature review, as bibliometric reviews are “highly efficient and objective as they leverage on the power of technology for data collection” (Chopra et al., Citation2021, p. 2), especially for review articles with the large corpus (i.e., high hundreds to thousands of articles).

We argue that our study is novel and timely based on specific reasons (See Table , which provides a bird's eye view of the prior reviews on financial distress.). First, the author found no bibliometric review published in top-ranked journals, which may have explored the performance and science of financial distress and the banking industry. Second, per the author’s knowledge, no review published in the finance discipline (Journals ranked in ABDC-2022 list) has used the combination of two software, i.e., VOSviewer and bibliometrix-R software, for carrying out the analysis. Third, the authors present a hybrid assessment of quality articles covering the breadth and depth of financial distress in the banking industry, which incorporates a review procedure (i.e., bibliometric review procedure Donthu et al., Citation2021) and a review protocol (i.e., SPAR-4-SLR Paul et al., Citation2021). Fourth, we provide directions for future researchers to consider for empirical and conceptual explorations. Fifth, our research aids researchers and policymakers interested in financial distress in the banking industry. The techniques used in the study also involve specialised analysis, such as co-citation analysis, that facilitates mapping and identifying boundary lines in emerging and well-established research fields. Aligning with the above discussion and following state-of-the-art bibliometric reviews (Boubaker et al., Citation2023; Khanra et al., Citation2020; Kumar et al., Citation2019; Rasul et al., Citation2022; Trinarningsih et al., Citation2021), we intend to address the following six research questions in the present review article:

Table 1. Existing review papers relevant to the field

RQ1:

What are the publication and citation trends of financial distress research in the Banking Industry?

RQ2:

Which are the most significant articles and outlets (journals) regarding financial distress in the Banking Industry?

RQ3:

Which authors, institutions, and nations have contributed the most to the academic field of financial distress in the Banking Industry?

RQ4:

What are the descriptive trends (through several metrics like authors, words etc.) existing in the academic field of financial distress in the Banking Industry?

RQ5:

What are the most important themes (intellectual structure) regarding financial distress in the Banking Industry?

RQ6:

What are the future avenues for financial distress research within the Banking Industry?

The following section principally outlines the background of financial distress research and its existing trajectories. Further, the review methodology is elucidated and elaborated, including the protocol and procedures employed in the current review. Next, we discuss the existing trends in the field by using performance mapping techniques and present the intellectual structure through knowledge clusters (themes). The later section discusses the research gaps and potential future avenues. We conclude the review by describing the limitations and putting forward the final word.

2. Overview of financial distress research in the banking industry

2.1. Financial distress

Financial distress is a scenario where the current cash flow is insufficient to pay for immediate obligations. These include non-payment debt to contractors and workers with missed principal or interest payments (Wruck, Citation1990). The definition of financial distress also provides a company’s ability to pay for its obligations and falling market value between consecutive periods (Pindado et al., Citation2008). Companies encounter financial distress due to poor operating results or external forces (Platt & Platt, Citation2008). To conceptualise corporate financial distress, let’s use the terms default, insolvency, bankruptcy, and failure (Jackson & Lee, Citation1963; Rajasekar et al., Citation2014). A default can be legal and technical; technical default means a company broke a contract condition, whereas legal default is when loan payments are missed. Insolvency is the inability to pay its debts due to liquidity issues. Filling bankruptcy signifies a company’s financial distress. Failure occurs when income isn’t enough to cover costs (Altman & Hotchkiss, Citation2005). Difficulty in paying the dividend and firms not fulfilling their financial responsibility are initial signs of financial distress (Baldwin & Mason, Citation1983). In the early stages of financial distress, long-term debt is more than the firm’s cash flow; therefore, firms cannot perform financial responsibilities (Whitaker, Citation1999). Financial distress can cause a shakeup in the corporate hierarchy and even result in the departure of top executives (Wruck, Citation1990). Financial distress prediction models are accounting-based and market-based. Accounting-based models are (Altman, Citation1968; Beaver, Citation1966; Dietrich, Citation1984; Ohlson, Citation1980) and market-based (Bharath & Shumway, Citation2011; Black & Scholes, Citation1973; Hillegeist et al., Citation2004; Merton, Citation1974). The Z-Score model linear discriminant analysis method was used to predict financial distress. The O-Score method for analysis changed to logit analysis, and Zmijewski (Citation1984) used probit in his model analysis (Pindado et al., Citation2008). Both market-based and accounting models are very close in predictive accuracy, but the accounting model produces economic benefits over the market-based (Agarwal & Taffler, Citation2008). One of the published works by (Hillegeist et al., Citation2004) compares Z-Score (Altman, Citation1968) and O-Score (Ohlson, Citation1980) with BSM-Prob (Black & Scholes, Citation1973) and claims that the BSM-Prob model provides more information than either of the accounting-based model. Most researchers have used accounting-based models to predict financial distress, whereas market-based models are rarely used (Habib et al., Citation2020), (see Table . which provides a few seminal conceptualisations of Financial Distress.).

Table 2. Some early definitions of financial distress by seminal authors

Costs related to financial distress are direct and indirect. Administrative and legal costs are direct and easily quantifiable (Almeida & Philippon, Citation2008; Bhagat et al., Citation1994; Chen & Merville, Citation1999; Pindado & Rodrigues, Citation2005). Indirect cost is due to the unpredictability of explicit and implicit warranties and includes lost sales when customers switch to competing products (Altman, Citation1984; Chen & Merville, Citation1999; Hoshi et al., Citation1990). During the economic distress period, overleveraged firms lose more market share from their modestly financed competitors (Opler & Titman, Citation1994). While addressing the issue of financial distress, the company faces a cash crisis, and during that period company is unable to fulfil its obligations (Pindado et al., Citation2008). Non-distressed firms didn’t hold more cash from cash flow than financially distressed firms (Almeida et al., Citation2004). Financial distress is not sudden for a company; there are many symptoms and signs before it faces it (Elloumi & Gueyié, Citation2001; Pindado et al., Citation2008). The predominant source of financial distress is leverage, and large firms have low chances of default (Pham Vo Ninh et al., Citation2018). Due to uncertain payoffs, R&D investments increase financial distress, and this relationship fortifies during economic downturns for constrained firms (Zhang, Citation2014). Currency hedging will reduce the chances of financial distress to a certain extent (Magee, Citation2013). Companies with good employee relations have lower chances of experiencing financial distress in the future (Kane et al., Citation2005). A positive amount of CSR activity reduces the likelihood of financial distress. A negative relationship is found between financial distress and positive CSR performance in the latter stage of firm life (Al-Hadi et al., Citation2019). Chang et al. (Citation2013) also find a negative relationship between distress risk and CSR score. Firms performing CSR practices are associated with lower distress and default risk (Boubaker et al., Citation2020). Managers in distressed firms use more earnings management techniques (Habib et al., Citation2013). Agarwal et al. (Citation2007) find different practices among Japanese banks subject to varying economic conditions. Financial statements may partially reflect the increased risk of bank distress (Ryan, Citation2016).

2.2. Banking industry

A bank is an assemblage of traders whose combination forms an institution that provides a credit deposit facility and safeguards the borrower’s actions (Boot & Thakor, Citation1997). Various financial institutions are involved in different activities like deposit taking and lending, and the most common forms of institutions are the central bank, commercial bank, retail bank, etc (Laplante & Kshetri, Citation2021). Bank performance can be measured by productivity, efficiency, profitability, and competencies (Alam et al., Citation2021). It is inefficient if a bank is not producing the desired output with the available input (Bhattacharyya & Pal, Citation2013). Return on assets can measure banking industry profitability (Alam et al., Citation2021). Profitability affects financial stability, which boosts growth and also helps influence gross domestic product (GDP) (Flannery & Rangan, Citation2008). The bank is the credit and liquidity provider to various institutions and individuals and can influence other economic actors (Zhelyazkova & Kitanov, Citation2015). Banks are service sector organisations, their socioeconomic impact is significant and varied, and they have various operations like debt management, cash flow management, and other services (Othman & Asutay, Citation2018). The nation’s growth depends on bank performance and financial activities (Hou & Cheng, Citation2017). The banking sector is prominent in the financial industry because it attracts many developing nations (Alam et al., Citation2021). Bank return on equity and return on assets both increased as a result of the creation of liquidity, effective asset management, asset quality, and bank size (El-Chaarani et al., Citation2023). El Shaarani (Citation2023) findings show that financial indicators in Islamic banks fell precipitously during the pandemic; liquidity risk, bank size, managerial efficiency ratio, and oil price shocks were the main factors influencing Islamic banks’ profitability prior to the emergence of COVID-19.

2.3. Financial distress in the banking industry

Bank’s financial distress depends on the board structure, ownership, and other top positions in banks and the different persons holding these positions (Simpson & Gleason, Citation1999). Based on a recent study, local private and public banks can better weather financial distress due to small and long-term loans from the foreign bank that provide their services (Ullah et al., Citation2021). Respondents with high perceived financial distress had a positive attitude towards banking but negatively affected service patronage (Babalola, Citation2009). Financial distress shoots up when we give extra care to investors. The distribution of work on the bank’s board between the chairman and CEO should be clearly defined, and they should work on accommodating risk (Baklouti et al., Citation2016). The failure of banks during the last financial crisis is due to weak corporate governance (OECD) report 2009. This also creates less interest in the financial market, which leads to financial distress (Kirkpatrick, Citation2009). Bank size may impact the likelihood of financial distress, and large banks positively affect financial distress (Barros et al., Citation2007). The occurrence of financial distress depends on the capital structure, i.e., the loan-to-asset ratio and its positive relation (Al-Saleh & Al-Kandari, Citation2012). Financial distress in the banking industry is due to unequal sharing of power at the top management level, and this power imbalance is due to the high percentage of shareholding (Muranda, Citation2006). Factors for bank default occurrence are macroeconomic like default risk, credit risk, and market risk of bank’s return (Porath, Citation2006). In some studies, macroeconomic information does not impact financial distress (Zaki et al., Citation2011). The financial health of banks depends on a few indicators like operating efficiency, loan management, and capital adequacy; these measures decide whether a firm falls into financial distress (Rahman et al., Citation2004). Factors important in the banking industry which affect financial distress are ownership, size, merger, and acquisition process (Wanke et al., Citation2015). High capital requirements and bank size don’t reduce financial distress but increased profitability and income diversification can do (Koju et al., Citation2018). The study suggests that conventional banking in Indonesia is facing financial distress due to the size of the board’s direction, the return on assets, and the capital adequacy ratio (Hatta et al., Citation2021). For financial stability in Brazilian banks, balance-sheet indicators are essential for early warning signs of financial distress (Rosa & Gartner, Citation2018). Paule-Vianez et al. (Citation2020) suggested that short-term financial distress can be predicted more accurately (El-Chaarani & Ragab, Citation2018). study shows that political crises and economic recession have a negative impact on the performance of Islamic banks.

3. Methodology

3.1. Systematic review

A systematic literature review (hereafter SLR) as a methodology (Snyder, Citation2019) has a significant advantage over traditional literature reviews as systematic reviews ensure coherence, generativity, and reproducibility; it not only brings transparency but minimises biases as the SLRs stand on a firm structural ground of protocols and procedures (Fan et al., Citation2022; Harari et al., Citation2020). Various forms of systematic review exist, namely domain-based, theory-based, and method-based reviews, are available to provide an overview of the literature on specific topics (Palmatier et al., Citation2018; Snyder, Citation2019), while more refined forms have also been added like meta-analysis, mixed review, conceptual review, framework-based, bibliometric and structured theme based (Paul & Criado, Citation2020). We employed the domain-based review approach to gain a holistic overview of the scientific contribution related to the research domain (Palmatier et al., Citation2018). Bibliometric analysis is essential because it highlights quantitative data and analytical tendencies in the research field (Ding et al., Citation2022; Goyal & Kumar, Citation2021). Compared to the traditional literature review methods, the bibliometric analysis yields more objective and quantitively-backed findings (Ramos-Rodríguez & Ruíz-Navarro, Citation2004). The bibliometric techniques deal with impacts (e.g., citations), locations (e.g., countries), and stakeholders (e.g., institutions) (Donthu et al., Citation2021, Citation2021).

Pritchard (Citation1969) introduced the term bibliometric in the literature, which paved the way for future research. The bibliometric analysis includes performance analysis and science mapping (Baier-Fuentes et al., Citation2019). Performance analysis uses citations and publications to compare articles, authors, countries, and journals (Baier-Fuentes et al., Citation2019; Donthu et al., Citation2021), whereas in science mapping, relationships between the different parts are highlighted (e.g., co-authorship, co-word analysis, bibliographic coupling, citation analysis, co-citation analysis) (Donthu et al., Citation2021). Descriptive analysis is also essential to bibliometric investigations (Donthu et al., Citation2020). Bibliometric methods are utilised in mapping the field of study, and then the central themes are identified to help get an essence of the domain’s knowledge structure (Baker et al., Citation2020). In a sense, quantitative analysis of the trends and knowledge structure of the relevant research domain is possible through the application of bibliometric techniques (Donthu et al., Citation2021).

3.2. Review protocol (SPAR-4-SLR)

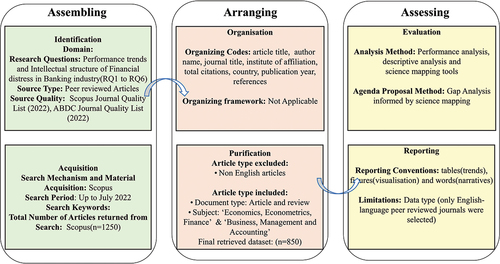

This study adopts the “Scientific Procedure and Rationales for Systematic Literature Review” (SPAR-4-SLR) to provide a structural and systematic outlook to our review (Paul et al., Citation2021); it includes the following sections: assembling, arranging, and assessing stage (See Figure ).

Figure 1. Procedure of review following the SPAR-4-SLR protocol.

3.2.1. Assembling: This stage of SPAR-4-SLR includes sub-stages of identification and acquisition.

3.2.1.1. Identification

This article delegates the area of financial distress in Banking as the primary focus (i.e., domain). The research questions will help to recognise the domain’s characteristics, relationships, agendas, and bibliometrics (Harju, Citation2022). For the collection of data, the Scopus database is used. The Scopus database was suitable for our research in contrast to WOS (Web of Science), its primary opponent, and it covers a broader range of topics and groups (Kumar et al., Citation2022). In addition, it helps in identifying journals specialising in review articles (Paul et al., Citation2021). The Scopus database includes subjects like art, science, technology, and humanities, and it has the most comprehensive citation and abstract (Fahimnia et al., Citation2015). Some features include the complete availability of bibliometric data, quality information, and stringent content selection with the procedure (Kumar et al., Citation2021).

3.2.1.2. Acquisition

Scopus was used for the search and data acquisition due to the breadth of the outcomes provided (Paul et al., Citation2021). Data was collected from Scopus, and the search period was kept till July 2022, since the field’s inception, to (1) incorporate early and seminal works in the domain and (2) not miss any relevant study in the domain. We used Boolean operators (Ramos et al., Citation2021) and truncation techniques (Frerichs & Teichert, Citation2021) to search the articles on Scopus. Our search keywords were “financial distress”, “financial distress prediction”, “financial distress strategies”, “Bank*”, “Bank* industry”, and “Bank* sector”. This filtration and keyword strategy resulted in 1250 articles.

3.2.2. Arranging: This stage of SPAR-4-SLR includes sub-stages of organisation and purification.

3.2.2.1. Organisation

The codes were organised for article title, author name, journal title, institute of affiliation, total citations, country, publication year, and references (Harju, Citation2022; Paul et al., Citation2021).

3.2.2.2. Purification

We excluded non-English articles, and this filtration follows the suggestions by Donthu et al. (Citation2021). The document types considered were reviews and articles, and we have considered taking articles from subject areas of ‘Economics, Econometrics, Finance & ‘Business, Management, and Accounting. Applying these filters resulted in a corpus of 850 articles.

3.2.3. Assessing: This stage of SPAR-4-SLR includes sub-stages of evaluation and reporting

Evaluation. We conducted performance analysis, descriptive analysis, and science mapping to evaluate the corpus of the literature on financial distress in the banking industry. In performance analysis, we check what value is added by research components, such as metrics related to citations, publications and most influential metrics (Noyons et al., Citation1999). We also conducted descriptive analysis and analysed specific patterns related to authors and publications concerning the domain under review. In contrast, relations between various parts are highlighted with the help of science mapping techniques, such as co-authorship, co-citation, authorship, and citation.

Reporting. In this section, we present the review’s findings using words, tables, and figures, while at the end, we point out article limitations and cite supporting articles for evidence.

4. Performance analysis of financial distress in the banking industry

4.1. Publication and citation trends (RQ1)

After retrieving the bib file, the first step was gathering preliminary data on the research topic. The compilation included 850 documents written by 1718 authors and published between 1982 and 2022, approximately 39.8 years. The annual growth rate for article publications is 11.17%, and there are 366 total journals comprising these articles. The average number of citations per article received is 23.95, and the total number of citations received is 19,854 (See Table ).

Table 3. Trends for citations and publications

4.2. Most influential articles and outlets (Journals) on financial distress in the banking industry (RQ2)

Article influence was evaluated using citation counts (Chabowski et al., Citation2013). Articles with the most citations in the Scopus database were considered the most influential. Table shows the highly cited papers, and most of these papers are discussed in other sections. The most significant article, “The role of banks in reducing the costs of financial distress in Japan,” has gained total 574 citations authored by Hoshi et al. (Citation1990), followed by “A Theory of Bank Capital” with 530 citations written by Diamond and Rajan (Citation2000.

Table 4. Top articles

Scopus-based citations of leading journals in the field of financial distress in the banking industry are presented in Table . Journal of Financial Economics ranked first with 3505 papers, whereas the Journal of Banking and Finance ranked second with 1847 citations. Journal of Finance and Journal of Corporate Finance have secured 3rd and 4th positions with citations of 1329 and 753, respectively. In terms of productivity, the Journal of Banking and Finance, with 33 publications, leads the list. The second spot is jointly held by the Journal of Corporate Finance and the Journal Of Financial Economics, with 29 publications each.

Table 5. Top outlets (Journals)

4.3. Most prolific authors, institutions and nations on financial distress in the banking industry (RQ3)

Table also shows the most prolific authors who have gained the highest number of citations are David Scharfstein having affiliation from the Massachusetts Institute of Technology (USA), having a total of 971 citations with two publications, followed by Takeo Hoshi, having affiliations from University of California (USA) with total citations 566 on 1 article. Table also shows the most prolific authors in terms of publications. David Scharfstein has topped the list with the highest number of citations. Table shows the institutions with the most publications; Boston College and the University of Chicago have topped the list with 11 publications each. New York University and the University of California ranked second in the table with 10 publications each.

Table 6. Top authors

Table 7. Top institutions

The top 10 countries with the highest publication numbers and citations are also shown in Table . The United States of America, with 507 publications, garnered 8795 citations in total, followed by the United Kingdom, with 133 publications garnering 1502 citations; these two countries are the leading contributors. Researchers from developing and developed countries participating in financial distress research indicate its global significance.

Table 8. Top nations

5. Descriptive analysis of financial distress in the banking industry (RQ4)

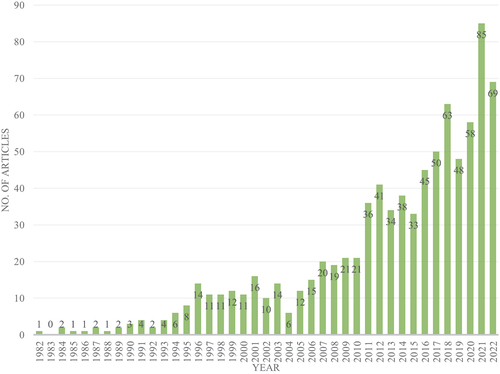

5.1. Annual scientific production

The annual scientific production of research publications related to financial distress in the banking industry began in 1982, the growth in the literature base was observed, but it was slow until 2010; since then, there has been an exponential rise with an uptrend after that. The probable reason behind this surge could be the global financial crisis of 2008, which caused a lot of chaos and fear in the banking industry and may have caught the attention of finance researchers. Further, the recent rise in the literature on financial distress may be attributed to the COVID-19 pandemic, which also caused fear in the markets and industries worldwide (Goyal et al., Citation2021). The highest number of published articles was 85 last year, i.e., 2021 (See Figure ). The annual growth rate of financial distress in the banking industry, as indicated by BiblioShiny software, is 87.89%.

Figure 2. Scientific production over the years.

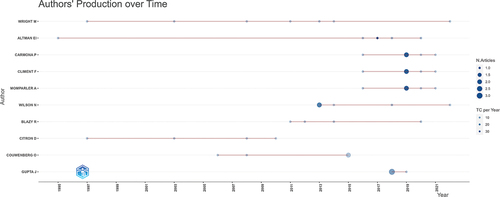

5.2. Authors’ production over time

Figure shows the writers’ active chronology across the years regarding the number of articles. The bubbles and their sizes correspond to the number of articles, while the line shows an author’s timeline. The number of citations every year is precisely proportional to the colour intensity. Since 2010, there has been a lot of activity, and 2021 has been the most fruitful year. From 2017 to 2021, Carmona P., Climent F., and Momparler A. were the most successful authors. All of the top 10 authors’ writings about financial distress in the banking industry are included in this collection. Identifying the writers and researchers in the field who have recently published using interpretations of this data may be possible. Furthermore, related publications can be used as reference materials by upcoming researchers.

Figure 3. Authors’ production over time.

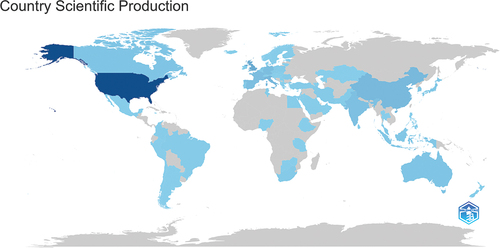

5.3. Country-wise scientific production

Figure shows the outcomes of the contributions made by various nations to the study of financial distress in the banking sector. The United States, United Kingdom, Italy, China and France are the top five nations making the most significant contributions to this recently burgeoning field of research.

Figure 4. Country scientific production of financial distress in banking industry.

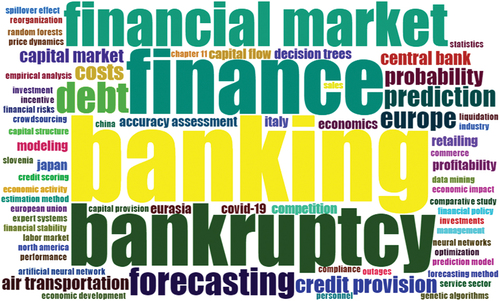

5.4. Word cloud in financial distress in the banking industry

Figure depicts a word cloud of the authors’ keywords. Potential and significant research on financial distress in the banking industry revolves around bankruptcy, forecasting, financial markets, capital market etc. Altman’s model, signalling theory, and information asymmetry are the primary theoretical lenses that help understand financial distress-related issues. Financial distress research has also been conducted in countries from the European region and far-east Asian nations like Japan and South Korea.

Figure 5. Word Cloud.

5.5. Most frequent words through treemap in financial distress in the banking industry

Figure depicts the top words by frequency, shown in the treemap format. Author keywords, which include words that most accurately summarise the document’s content from the author’s perspective, were selected to list the most often used words. For instance, Figure depicts that words like banks, debt, financial markets, and forecasting are among the most frequently used terms in the domain, but they all refer to the same entity under study. With this consideration, banking was the most used author keyword with a frequency of 25, followed by the terms like financial crisis and finance with 23 and 19 occurrences, respectively.

Figure 6. Tree map.

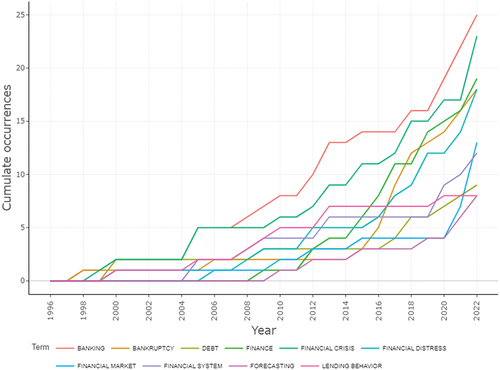

5.6. Word dynamics in financial distress in the banking industry

The rise and fall in word usage by authors between 1982 and 2022 regarding the financial distress in the banking industry research are depicted in the word dynamics graph based on author keyword occurrences each year. The growth of the most frequently used words is shown in Figure . Since the domain’s inception, banking, bankruptcy, and debt have consistently grown as the most commonly used words. At the same time, there has been a drastic rise in terms like the financial market, financial systems and forecasting after 2015.

Figure 7. Word Dynamics.

6. Science mapping of financial distress in the banking industry (RQ5)

6.1. Co-occurrence (co-word) analysis

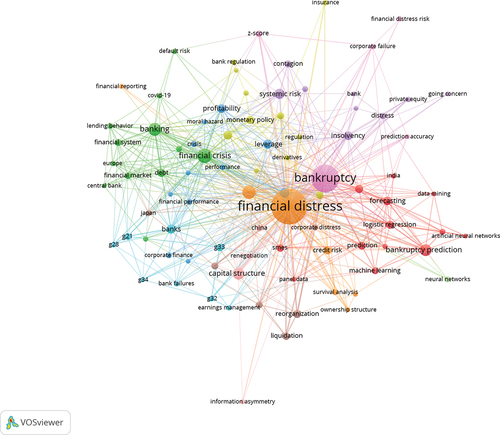

Keyword co-occurrence involves the analysis of author keywords which may reveal specific and valuable patterns in the evidence available for disseminating knowledge (Kumar et al., Citation2020). Strozzi et al. (Citation2017) verified that the author’s chosen keyword is a highly illustrative indicator of the paper’s subject matter or the article’s relevance to the research question. The co-occurrence of the author keyword may indicate that the documents share a common research theme, which may indicate a general pattern in the field’s research (Ding et al., Citation2001). As a result, we have also utilised author keyword analysis to determine the direction of research on financial distress in the banking industry. First, we extracted the author keywords from 829 relevant articles; then, using VOSviewer software, we constructed an author keyword network. For this analysis, we required a minimum of five co-occurrence keywords. The 829 papers revealed a co-occurrence network for author-generated keywords that occurred more than five times each. Out of 1813 keywords, 71 met our criteria. The keywords “financial distress” and “bankruptcy” were the most frequently co-occurring, appearing 257 and 152 times, respectively. The author’s keyword co-occurrence network is depicted in Figure .

Figure 8. Co-occurrence network (co-word analysis).

The map shows that the largest node on the network is “financial distress” followed by “bankruptcy.” Keywords with the same colour belong to the same group. A keyword network analysis yielded numerous results. First, it demonstrated that the concept of financial distress had been studied along the related topics such as bankruptcy, financial crisis, corporate distress, credit risk, bankruptcy prediction, financial distress risk, and systematic risk. Second, artificial neural networks, bankruptcy prediction, financial distress prediction, financial ratios, Z-score, and logistic regression are used to measure financial distress. Third, capital structure, insolvency, liquidation, risk management, reorganisation, and corporate governance, form distinct groups that represent the evolution of the study of this diverse field of financial distress. SMEs, earning management, covid-19, and survival analysis are also found in the same group. These examples highlight the wide variety of topics covered by studies of financial distress in the banking industry.

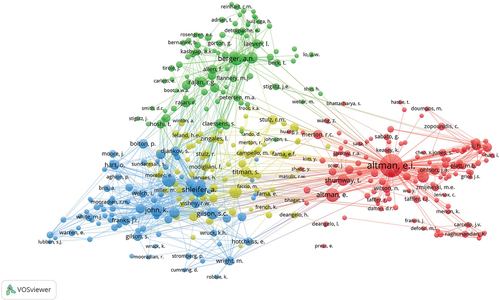

6.2. Co-citation analysis

To create a scientific road map, scientists use co-citation analysis, which operates under the premise that highly-cited works are conceptually related (Hjørland, Citation2013). Through references or co-citations, semantic or cognitive associations between articles reveal the theoretical underpinnings of a scientific field (Goodell et al., Citation2021). A co-citation analysis determines how often two articles are cited together (Small, Citation1973). Co-cited papers are two papers cited by a third. The more they appear together in citations, the closer they are. The co-citation analysis clusters consisted of co-cited papers with similar concepts and methodologies (Small, Citation1980). Co-citation analysis focuses only on highly-cited publications, leaving out recent or niche publications (Donthu et al., Citation2021). Co-citation analysis helps business scholars find seminal publications and knowledge foundations. Articles with at least 20 citations were used to create a co-citation network, and 94 articles met the 20-citation criteria out of 32,723 cited references (see Figure for the co-citation network).. Due to the sheer volume of cited papers in review, it is necessary to set the standard that financial distress articles are included when cited a minimum of x times by other financial distress articles. This criterion is also congruent with the method adopted by Hollebeek et al. (Citation2022).

Figure 9. Co-citation network.

6.2.1. Cluster 1: FD prediction/models of FD (red in the figure)

The first cluster, FD prediction/Models of FD (shown in Red), included 30 articles. Several articles in this collection create FD prediction models, accounting and market-based. Accounting-based models (Altman, Citation1968; Beaver, Citation1966; Ohlson, Citation1980) and these model use financial ratios for the prediction of financial distress, and market-based models (Bharath & Shumway, Citation2011; Black & Scholes, Citation1973; Hillegeist et al., Citation2004; Merton, Citation1974) and these models have used market-based variable for predicting financial distress. Although the forecast accuracy of the market-based and accounting models is relatively similar, the accounting model generates more significant economic benefits (Agarwal & Taffler, Citation2008). To predict financial distress, most academicians have employed accounting-based models; in contrast, market-based models are rarely used (Habib et al., Citation2020).

6.2.2. Cluster 2 financial distress and bankruptcy (green in the figure)

The second cluster, titled banking industry financial distress and Bankruptcy (shown in green in the figure), included 25 articles. Most FD researchers extended their research to find bankruptcy and economic crisis in the banking industry (Berger et al., Citation2001; Cao, Citation2021; Diamond & Rajan, Citation2000; Kroszner & Strahan, Citation2001). Bank distress doesn’t appear to impact small and large borrowers more. However, small firms may react to bank distress by borrowing from numerous banks (Berger et al., Citation2001). A recent study in China shows that the banking sector’s distress depends on real estate losses, suggesting that a rise in real estate losses would increase banking sector losses (Cao, Citation2021). Firms with well-built ties with banks perform better in distress than firms with weak ties (Hoshi et al., Citation1990). Banks take on financially distressed companies with various approaches, some of which are quite distinct depending on the organisation structure and lending technologies, and bank size appears to be much less relevant (Micucci & Rossi, Citation2016). Although more bank capital lowers the likelihood of financial distress, it also slows the rate at which new liquidity can be created. The optimal capital structure of a bank balances the impact of liquidity creation and the cost of bank distress (Diamond & Rajan, Citation2000).

6.2.3. Cluster 3: Resolution of financial distress/rejuvenating from bankruptcy (yellow in the figure)

The third cluster consists of 20 articles representing financial distress and bankruptcy rejuvenation. Significant studies in this cluster are Hoshi et al. (Citation1990); Paul et al. (Citation1994); DeAngelo et al. (Citation1995); Claessens et al. (Citation1999); Bolton and Freixas (Citation2000); Baird and Morrison (Citation2001); Couwenberg and Lubben (Citation2015); Liu et al. (Citation2021); Meuleman et al. (Citation2022) and Welch (Citation1997). During bankruptcy, the shutdown decision as the use of actual option offers new justification for being dubious about the merit of Chapter 11 (Baird & Morrison, Citation2001). Companies use the bank as a source of investment when facing financial distress, and the banks take responsibility for the cost of capital (Bolton & Freixas, Citation2000). Bank-owned and group-affiliated firms are less likely to file for bankruptcy after controlling some firms’ characteristics (Claessens et al., Citation1999). Capital expenditure reduction, merger, asset sales, and private and public debt restructuring are a few ways to avoid bankruptcy (Paul et al., Citation1994). The lower the cost of financial distress, the low the creditor conflict among themselves (Hoshi et al., Citation1990). Private equity firms engaged in fundraising activities during financial distress are less likely to declare bankruptcy in the following years (Meuleman et al., Citation2022).

6.2.4. Cluster 4: Post-financial distress/bankruptcy conditions of a firm (blue in the figure)

The fourth cluster comprises 19 articles devoted to post-financial distress and bankruptcy conditions. This cluster consists of several significant articles such as Kaplan (Citation1994); DeAngelo et al. (Citation2002); Asvanunt et al. (Citation2011); Blazy et al. (Citation2011); Zhang (Citation2022) and Zhou et al. (Citation2022). Firms facing financial distress are more likely to make acquisitions to diversify their product offerings and reduce their reliance on a single revenue stream due to the pressure to meet their debt obligations (Zhang, Citation2022). Financial distress may occur any number of times in the same firm. Accounting and market-based variables are not particularly useful for forecasting future distress. Still, factors like recovery time, restructuring events, and their interaction with accounting and macroeconomic factors substantially impact recurrence risk (Zhou et al., Citation2022). During the situation of financial distress, if default may result in still more chances are in favour of the continuation of the firm, and the global recovery rate is primarily determined by the firm’s ex-ante characteristics at the time of triggering of financial distress (Blazy et al., Citation2011). All immediate and long-term expenses related to the bankruptcy and financial distress are factored into the post-bankruptcy, indicating minimal costs associated with the bankruptcy (Kaplan, Citation1994).

7. Future research directions (RQ6)

Future research is encouraged to evaluate further the efficacy of various artificial intelligence or machine learning algorithms for financial distress prediction leading to bankruptcy. Our findings also suggest that the effectiveness of several accounting-based and market-based variables is significantly influenced by any litigation and restructuring events that distressed firms may have experienced in the past. This insight offers future researchers a fresh perspective from which to investigate the field of financial distress. Future research could include an automatic process that searches articles based on meta keywords and co-occurrences of keywords from literature databases. Importantly, suppose we see that research in the field of financial distress has been conducted in developed countries. In that case, there is still a dearth of literature and research from developing nations. Future researchers may also study the impact of the COVID-19 pandemic on causing financial distress in the banking industry.

Further, Not only are the financial and macroeconomic circumstances at the time of crisis turnaround connected to the probability of a recurrence of the distress but changing operational conditions and the broader economic environment are also directly tied to this risk. As a result, a time-dependent model could be considered for the pursuance of future research (Zhou et al., Citation2022). Also, Researchers have suggested that future studies should incorporate endogeneity issues and competing risks while looking to mitigate the risk of distress (Yousaf et al., Citation2022).

8. Conclusion

Based on the literature on financial distress, the authors proposed that research interest in financial distress (and their prediction) is increasing and will continue to increase in the future. Over the past half-century, researchers worldwide have focused on predicting financial distress. Bibliometrics has a leg up on competing methods because it can collect seemingly objective data with minimal effort from the researchers (Farrukh et al., Citation2023; Zaidi & Azmi, Citation2022). Many scholars have tried refining the financial distress prediction models over time (Shi & Li, Citation2019). To contribute to the existing knowledge, this study provides a comprehensive review of literature about financial distress published over the last 40 years using different bibliometric techniques. As a part of this investigation, we answered six research questions by providing a snapshot of state of the art in the field of financial distress research; this study answers RQ1 as a publication and citation trend in the research domain by providing a broad overview of the current literature on financial distress in the banking industry, identifying the most significant articles, most essential journals, relevant affiliations. RQ2 and RQ3 are addressed in sections 4.1 and 4.2, in which the top papers and journals are identified in terms of citations. RQ3 is discussed in terms of two parameters: the highest number of publications and the highest number of citations by author, institution, and nation, as shown in Tables .

We found that David Scharfstein tops the list regarding the highest citations received. Mike Wright tops the list of the highest publications during this period. Boston College has topped the list of institutions with the most publications, and the University of Chicago has 11 publications each. The United States of America has the highest number of publications. i.e., 502. To address RQ4, authors have conducted a descriptive analysis to find the most important words, authors and countries. Authors have also performed co-citation analysis and identified the themes as per the literature (RQ5), as shown in (Figure ). Based on cluster analysis, four clusters have emerged. Addressing RQ6 provides a concise and non-exhaustive overview of the study’s implications and potential future directions for research in financial distress in banking.

8.1. Implications for policymakers in the banking industry

This study highlighted the substantial progress in the domain of financial distress recorded by several finance journals throughout the years. It supplied the necessary information for future researchers to consider and publish. Additionally, this work is meant to direct academics working in the field of financial distress in the banking industry toward new topical areas, and it is also meant to support the development of knowledge on financial distress by enabling more space for empirical and conceptual articles. This study provides a few practical implications for bank managers and policymakers by building on the work of previous academics.

First, the policy of disclosures should be chosen by managers; however, this choice should be made with prudence since there is a nonlinear connection between transparency and disclosure and financial difficulty (Rastogi & Kanoujiya, Citation2022). Second, Unwise disclosures may not improve the banks’ capacity to remain stable. In light of the banking sector’s obvious competitive fragility, regulators may decide to limit competition there. The banking business is unlike other industries where competition benefits all parties involved; hence policymakers shouldn’t encourage competition there (Rastogi & Kanoujiya, Citation2022). Third, banks and financial institutions must have a financial distress model for SMEs to minimise their anticipated and unexpected losses (Ragab & Saleh, Citation2022). SME managers may be concerned about adopting financial distress models for corrective action planning and planning and regulating present operations to prevent potential financial collapse. Fourth, Our research also has consequences for society at large since increasing diversity in organisations may help protect the interests of various stakeholders by reducing the likelihood that businesses would experience financial distress (Guizani & Abdalkrim, Citation2023). Fifth, According to the data, the firm’s FD is improved by more promoter ownership. As a result, any unusual behaviour by managers acting in their interests might worsen the firm’s financial situation. It won’t be advantageous for managers in such a circumstance. Alternatively, it might result in future corporate failure (Kanoujiya et al., Citation2022).

8.2. Theoretical and research contributions

We followed Mukherjee et al. (Citation2022) to incorporate and highlight the relevant contributions made by the current review. This bibliometric review contributes to the financial distress literature in myriad ways. First, we made an objective discovery of thematic knowledge clusters in the domain; these clusters help us unpack the most relevant insights which may give a reader a bird’s eye view of the domain. Second, we objectively assessed and reported the impact and productivity of research in the domain through performance analysis. Third, we also delineated crucial knowledge gaps that may help future researchers conduct empirical and non-empirical investigations in the domain. Fourth, this research demonstrated the necessity to see “financial distress” as a significant area of investigation, which has become more relevant than ever due to recent events.

8.3. Limitations of the study

The discussion so far highlights the study’s contribution but has some limitations. First, the analysis only considers papers that use the phrase “financial distress,” financial distress prediction,” and “financial distress strategies” somewhere in the paper’s title, abstract, or keyword, leaving out articles that use the keywords financial crisis, failure, default, and bankruptcy. So, future researchers should also incorporate these keywords while conducting the research. Secondly, this study presents a future research direction for financial distress in banking based on our knowledge of the field and the trends in the keywords used to find that knowledge. Given that author could not read everything published on the topic, we recommend that future research conduct an objective and systematic literature review to provide a comprehensive overview of the topic’s major contextual and geographical themes utilising CAQDA (Computer-assisted qualitative data analysis) methods. Finally, the analysis uses bibliographic data from 1982 to 2022. Only articles from peer-reviewed journals were included in our study, and articles from conferences and books were ignored; these can be considered in future works.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Agarwal, S., Chomsisengphet, S., Liu, C., & Ghon Rhee, S. (2007). Earnings management behaviors under different economic environments: Evidence from Japanese banks. International Review of Economics and Finance, 16(3), 429–24. https://doi.org/10.1016/j.iref.2005.08.003

- Agarwal, V., & Taffler, R. (2008). Comparing the performance of market-based and accounting-based bankruptcy prediction models. Journal of Banking and Finance, 32(8), 1541–1551. https://doi.org/10.1016/j.jbankfin.2007.07.014

- Al-Absy, M. S. M., Almaamari, Q., Alkadash, T., & Habtoor, A. (2020). Gender diversity and financial stability: Evidence from Malaysian listed firms. The Journal of Asian Finance, Economics & Business, 7(12), 181–193. https://doi.org/10.13106/jafeb.2020.vol7.no12.181

- Al-Absy, M. S. M. (2020). The board chairman’s characteristics and financial stability of Malaysian-listed firms. Cogent Business & Management, 7(1), 1823586. https://doi.org/10.1080/23311975.2020.1823586

- Alam, M. S., Rabbani, M. R., Tausif, M. R., & Abey, J. (2021). Banks’ performance and economic growth in India: A panel cointegration analysis. Economies, 9(1), 1–14. https://doi.org/10.3390/economies9010038

- Al-Hadi, A., Chatterjee, B., Yaftian, A., Taylor, G., & Monzur Hasan, M. (2019). Corporate social responsibility performance, financial distress and firm life cycle: Evidence from Australia. Accounting and Finance, 59(2), 961–989. https://doi.org/10.1111/acfi.12277

- Almeida, H., Campello, M., & Weisbach, M. S. (2004). The cash flow sensitivity of cash. The Journal of Finance, LIX(4), 1777–1804. https://doi.org/10.1111/j.1540-6261.2004.00679.x

- Almeida, H., & Philippon, T. (2008). Estimating risk‐adjusted costs of financial distress.Pdf. Journal of Applied Corporate Finance, 20(4), 105–109. https://doi.org/10.1111/j.1745-6622.2008.00208.x

- Al-Saleh, M. A., & Al-Kandari, A. M. (2012). Prediction of financial distress for commercial banks in Kuwait. World Review of Business Research, 2(6), 26–45.

- Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–609. https://doi.org/10.1111/j.1540-6261.1968.tb00843.x

- Altman, E. I. (1984). A Further empirical investigation of the bankruptcy cost question. The Journal of Finance, 39(4), 1067–1089. https://doi.org/10.1111/j.1540-6261.1984.tb03893.x

- Altman, E. I., & Hotchkiss, E. (2005). Corporate financial distress and bankruptcy: Predict and avoid bankruptcy, analyze and invest in distressed Debt, Third Edition. Corporate Financial Distress and Bankruptcy: Predict and Avoid Bankruptcy, Analyze and Invest in Distressed Debt, Third Edition. https://doi.org/10.1002/9781118267806

- Altman, E. I., Iwanicz-Drozdowska, M., Laitinen, E. K., & Suvas, A. (2017). Financial distress prediction in an International context: A review and empirical analysis of Altman’s Z- Score model. Journal of International Financial Management & Accounting, 28(2), 131–171. https://doi.org/10.1111/jifm.12053

- Asvanunt, A., Broadie, M., & Sundaresan, S. (2011). Managing corporate liquidity: Strategies and pricing implications. International Journal of Theoretical and Applied Finance, 14(3), 369–406. https://doi.org/10.1142/S0219024911006589

- Babalola, S. S. (2009). Perception of financial distress and customers’ Attitude toward banking. International Journal of Business & Management, 4(10). https://doi.org/10.5539/ijbm.v4n10p81

- Baier-Fuentes, H., Merigó, J. M., Amorós, J. E., & Gaviria-Marín, M. (2019). International entrepreneurship: A bibliometric overview. International Entrepreneurship & Management Journal, 15(2), 385–429. https://doi.org/10.1007/s11365-017-0487-y

- Baird, D. G., & Morrison, E. R. (2001). Bankruptcy decision making. Journal of Law, Economics, & Organization, 17(2), 356–372. https://doi.org/10.1093/jleo/17.2.356

- Baker, H. K., Kumar, S., & Pandey, N. (2020). A bibliometric analysis of managerial finance: A retrospective. Managerial Finance, 46(11), 1495–1517. https://doi.org/10.1108/MF-06-2019-0277

- Baklouti, N., Gautier, F., & Affes, H. (2016). Corporate governance and financial distress of European commercial banks. Journal of Business Studies Quarterly, 7(3), 75–96.

- Baldwin, C. Y., & Mason, S. P. (1983). The resolution of claims in financial distress the case of massey ferguson. The Journal of Finance, 38(2), 505–516. https://doi.org/10.1111/j.1540-6261.1983.tb02258.x

- Barros, C. P., Ferreira, C., & Williams, J. (2007). Analysing the determinants of performance of best and worst European banks: A mixed logit approach. Journal of Banking and Finance, 31(7), 2189–2203. https://doi.org/10.1016/j.jbankfin.2006.11.010

- Beaver, W. H. (1966). Financial ratios as predictors of failure authors (s): William H. Beaver source. Journal of Accounting Research, 4(1966), 71–111. Vol. 4, Empirical Research in Accounting : Selected Published by : Wiley on behalf of Accounting Research Center, Booth School of Busi’, Journal of Accounting ResearchAvailable at. http://www.jstor.org/stable/2490171

- Beaver, W. H., Correia, M., & McNichols, M. F. (2010). Financial statement analysis and the prediction of financial distress. Foundations & Trends in Accounting, 5(2), 99–173. https://doi.org/10.1561/1400000018

- Berger, A. N., Klapper, L. F., & Udell, G. F. (2001). The ability of banks to lend to informationally opaque small businesses. Journal of Banking and Finance, 25(12), 2127–2167. https://doi.org/10.1016/S0378-4266(01)00189-3

- Bhagat, S., Brickley, J. A., & Coles, J. L. (1994). The costs of inefficient bargaining and financial distress. Evidence from corporate lawsuits. Journal of Financial Economics, 35(2), 221–247. https://doi.org/10.1016/0304-405X(94)90005-1

- Bharath, S. T., & Shumway, T. (2011). Forecasting default with the KMV-Merton model. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.637342

- Bhattacharyya, A., & Pal, S. (2013). Financial reforms and technical efficiency in Indian commercial banking: A generalized stochastic frontier analysis. Review of Financial Economics, 22(3), 109–117. https://doi.org/10.1016/j.rfe.2013.04.002

- Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637–657. https://doi.org/10.1086/260062

- Blazy, R., Chopard, B., Fimayer, A., & Guigou, J.-D. (2011). Employment preservation vs. creditors’ repayment under bankruptcy law: The French dilemma? International Review of Law and Economics, 31(2), 126–141. https://doi.org/10.1016/j.irle.2011.03.002

- Bolton, P., & Freixas, X. (2000). Equity, bonds, and bank debt: Capital structure and financial market equilibrium under asymmetric information. Journal of Political Economy, 108(2), 324–351. https://doi.org/10.1086/262121

- Boot, A. W. A., & Thakor, A. V. (1997). Financial system architecture. The Review of Financial Studeis, 10(8), 693–733. https://doi.org/10.1093/rfs/10.3.693

- Boubaker, S., Cellier, A., Manita, R., & Saeed, A. (2020). Does corporate social responsibility reduce financial distress risk? Economic Modelling, 91(May), 835–851. https://doi.org/10.1016/j.econmod.2020.05.012

- Boubaker, S., Goodell, J. W., Kumar, S., & Sureka, R. (2023). COVID-19 and finance scholarship: A systematic and bibliometric analysis. International Review of Financial Analysis, 85, 102458. https://doi.org/10.1016/j.irfa.2022.102458

- Cao, Y. (2021). Measuring systemic risk and dependence structure between real estates and banking sectors in China using a CoVaR-copula method. International Journal of Finance and Economics, 26(4), 5930–5947. https://doi.org/10.1002/ijfe.2101

- Chabowski, B. R., Samiee, S., & Hult, G. T. M. (2013). A bibliometric analysis of the global branding literature and a research agenda. Journal of International Business Studies, 44(6), 622–634. https://doi.org/10.1057/jibs.2013.20

- Chang, T. C., Yan, Y. C., & Chou, L. C. (2013). Is default probability associated with corporate social responsibility? Asia-Pacific Journal of Accounting and Economics, 20(4), 457–472. https://doi.org/10.1080/16081625.2013.825228

- Chen, G. M., & Merville, L. J. (1999). An analysis of the underreported magnitude of the total indirect costs of financial distress. Review of Quantitative Finance & Accounting, 13(3), 277–293. https://doi.org/10.1023/A:1008370531669

- Chopra, M., Saini, N., Kumar, S., Varma, A., Mangla, S. K., & Lim, W. M. (2021). Past, present, and future of knowledge management for business sustainability. Journal of Cleaner Production, 328(July), 129592. https://doi.org/10.1016/j.jclepro.2021.129592

- Claessens, S., Djankov, S., & Klapper, L. (1999). Resolution of corporate distress in East Asia. Journal of Empirical Finance, 10(1–2), 199–216. https://doi.org/10.1016/S0927-5398(02)00023-3

- Couwenberg, O., & Lubben, S. J. (2015). Corporate bankruptcy tourists. The Business Lawyer, 70(3), 719–750. https://medium.com/@arifwicaksanaa/pengertian-use-case-a7e576e1b6bf

- DeAngelo, H., DeAngelo, L., & Gilson, S. C. (1995). DeAngeloDeAngeloGilson96.pdf. Journal of Financial Economics, 41(3), 475–511. https://doi.org/10.1016/0304-405X(95)00866-D

- DeAngelo, H., DeAngelo, L., & Wruck, K. H. (2002). Asset liquidity, debt covenants, and managerial discretion in financial distress: The collapse of L.A. Gear. Journal of Financial Economics, 64(1), 3–34. https://doi.org/10.1016/S0304-405X(02)00069-7

- Diamond, D. W., & Rajan, R. G. (2000). A theory of bank capital. The Journal of Finance, 55(6), 2431–2465. https://doi.org/10.1111/0022-1082.00296

- Dietrich, J. R. (1984). Discussion of methodological issues related to the estimation of financial distress prediction models. Journal of accounting research, 22, 83. https://doi.org/10.2307/2490860

- Ding, Y., Chowdhury, G. G., & Foo, S. (2001). Bibliometric cartography of information retrieval research by using co-word analysis. Information Processing and Management, 37(6), 817–842. https://doi.org/10.1016/S0306-4573(00)00051-0

- Ding, L., Zhao, Z., & Wang, L. (2022). A bibliometric review on institutional investor: Current status, development and future directions. Management Decision, 60(3), 673–706. https://doi.org/10.1108/MD-09-2020-1302

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133, 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

- Donthu, N., Kumar, S., Pandey, N., Pandey, N., & Mishra, A. (2021). Mapping the electronic word-of-mouth (eWOM) research: A systematic review and bibliometric analysis. Journal of Business Research, 135(July), 758–773. https://doi.org/10.1016/j.jbusres.2021.07.015

- Donthu, N., Reinartz, W., Kumar, S., & Pattnaik, D. (2020). A retrospective review of the first 35 years of the International Journal of Research in Marketing. International Journal of Research in Marketing’, International Journal of Research in Marketing, 38(1), 232–269. https://doi.org/10.1016/j.ijresmar.2020.10.006

- El-Chaarani, H., Abraham, R., & Azzi, G. (2023). The role of liquidity creation in managing the COVID-19 banking crisis in selected mena countries. International Journal of Financial Studies, 11(1), 39. https://doi.org/10.3390/ijfs11010039

- El-Chaarani, H., & Ragab, N. S. (2018). Financial resistance of Islamic banks in middle east region: A comparative study with conventional banks during the Arab Crises. International Journal of Economics and Financial Issues, 8(3), 207–218. http://www.econjournals.com

- Elloumi, F., & Gueyié, J. P. (2001). Financial distress and corporate governance: An empirical analysis. Corporate Governance The International Journal of Business in Society, 1(1), 15–23. https://doi.org/10.1108/14720700110389548

- El Shaarani, H. (2023). Determinants of Islamic Banks Profitability in MENA Region Before and During the COVID-19 Pandemic Period. Islamic Accounting and Finance: A Handbook, 623–652. https://doi.org/10.1142/9781800612426_0021

- Fahimnia, B., Sarkis, J., & Davarzani, H. (2015). Green supply chain management: A review and bibliometric analysis. International Journal of Production Economics, 162, 101–114. https://doi.org/10.1016/j.ijpe.2015.01.003

- Fan, D., Breslin, D., Callahan, J. L., & Iszatt‐White, M. (2022). Advancing literature review methodology through rigour, generativity, scope and transparency. International Journal of Management Reviews, 24(2), 171–180. https://doi.org/10.1111/ijmr.12291

- Farrukh, M., Raza, A., Mansoor, A., Khan, M. S., & Lee, J. W. C. (2023). Trends and patterns in pro-environmental behaviour research: a bibliometric review and research agenda. Benchmarking: An International Journal, 30(3), 681–696. https://doi.org/10.1108/BIJ-10-2020-0521

- Flannery, M. J., & Rangan, K. P. (2008). What caused the bank capital build-up of the 1990s?. Review of Finance, 12(2), 391–429. https://doi.org/10.1093/rof/rfm007

- Foster, G. (1986). Financial Statement Analysis. https://www.scribd.com/presentation/393387239/Financial-Statement-Analysis.

- Frerichs, I. M., & Teichert, T. (2021). Research streams in corporate social responsibility literature: A bibliometric analysis. Management Review Quarterly, 73(1), 231–261. https://doi.org/10.1007/s11301-021-00237-6

- Gilson, S. C. (1989). Management turnover and financial distress. Journal of Financial Economics, 25(2), 241–262. https://doi.org/10.1016/0304-405X(89)90083-4

- Goodell, J. W., Kumar, S., Lim, W. M., & Pattnaik, D. (2021). Artificial intelligence and machine learning in finance: Identifying foundations, themes, and research clusters from bibliometric analysis. Journal of Behavioral and Experimental Finance, 32, 100577. https://doi.org/10.1016/j.jbef.2021.100577

- Gopalan, R., Nanda, V., & Seru, A. (2006). Affiliated firms and financial support: Evidence from Indian business groups. Journal of Financial Economics, 86(3), 759–795. https://doi.org/10.1016/j.jfineco.2006.09.008

- Goyal, K., & Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. International Journal of Consumer Studies, 45(1), 80–105. https://doi.org/10.1111/ijcs.12605

- Goyal, K., Kumar, S., Rao, P., Colombage, S., & Sharma, A. (2021). Financial distress and COVID-19: evidence from working individuals in India. Qualitative Research in Financial Markets, 13(4), 503–528. https://doi.org/10.1108/QRFM-08-2020-0159

- Guizani, M., & Abdalkrim, G. (2023). Does gender diversity on boards reduce the likelihood of financial distress? Evidence from Malaysia. Asia-Pacific Journal of Business Administration, 15(2), 287–306. https://doi.org/10.1108/APJBA-06-2021-0277

- Habib, A., Costa, M. D., Huang, H. J., Bhuiyan, M. B. U., & Sun, L. (2020). Determinants and consequences of financial distress: review of the empirical literature. Accounting and Finance, 60(S1), 1023–1075. https://doi.org/10.1111/acfi.12400

- Habib, A., Uddin Bhuiyan, B., & Islam, A. (2013). Financial distress, earnings management and market pricing of accruals during the global financial crisis. Managerial Finance, 39(2), 155–180. https://doi.org/10.1108/03074351311294007

- Harari, M. B., Parola, H. R., Hartwell, C. J., & Riegelman, A. (2020). Literature searches in systematic reviews and meta-analyses: A review, evaluation, and recommendations. Journal of Vocational Behavior, 118(January 2019), 103377. https://doi.org/10.1016/j.jvb.2020.103377

- Harju, C. (2022). The perceived quality of wooden building materials—A systematic literature review and future research agenda. International Journal of Consumer Studies, 46(1), 29–55. https://doi.org/10.1111/ijcs.12764

- Hatta, A. J., Emilia, S. P., & Junaidi, J. (2021). Analysis of the effect of bank soundness and macroeconomics on financial distress in conventional commercial banks. International Journal of Business, Humanities, Education and Social Sciences (IJBHES), 3(1), 27–32.

- Hertzel, M. G., LI, Z., OFFICER, M., & RODGERS, K. (2008). Inter-firm linkages and the wealth effects of financial distress along the supply chain. Journal of Financial Economics, 87(2), 374–387. https://doi.org/10.1016/j.jfineco.2007.01.005

- Hillegeist, S. A., Keating, E. K., Cram, D. P., & Lundstedt, K. G. (2004). Assessing the probability of bankruptcy. Review of Accounting Studies, 9(1), 5–34. https://doi.org/10.1023/B:RAST.0000013627.90884.b7

- Hjørland, B. (2013). Facet analysis: The logical approach to knowledge organization. Information Processing and Management, 49(2), 545–557. https://doi.org/10.1016/j.ipm.2012.10.001

- Hollebeek, L. D., Sharma, T. G., Pandey, R., Sanyal, P., & Clark, M. K. (2022). Fifteen years of customer engagement research: A bibliometric and network analysis. Journal of Product & Brand Management, 31(2), 293–309. https://doi.org/10.1108/JPBM-01-2021-3301

- Hoshi, T., Kashyap, A., & Scharfstein, D. (1990). The role of banks in reducing the costs of financial distress in Japan. Journal of Financial Economics, 27(1), 67–88. https://doi.org/10.1016/0304-405X(90)90021-Q

- Hou, H., & Cheng, S. Y. (2017). The dynamic effects of banking, life insurance, and stock markets on economic growth. Japan and the World Economy, 41, 87–98. https://doi.org/10.1016/j.japwor.2017.02.001

- Iyer, D. N., & Miller, K. D. (2008). Performance feedback, slack, and the timing of acquisitions. Academy of Management Journal, 51(4), 808–822. https://doi.org/10.5465/AMJ.2008.33666024

- Jackson, T. M., & Lee, W. H. (1963). Major thermal burns: A mortality appraisal and review. Archives of Surgery, 87(6), 937–948. https://doi.org/10.1001/archsurg.1963.01310180053010

- JOHN, T. A., & JOHN, K. (1993). Top‐Management compensation and capital structure. The Journal of Finance, 48(3), 949–974. https://doi.org/10.1111/j.1540-6261.1993.tb04026.x

- Kahl, M. (2002). Economic distress, financial distress, and dynamic liquidation. The Journal of Finance, 57(1), 135–168. https://doi.org/10.1111/1540-6261.00418

- Kane, G. D., Velury, U., & Ruf, B. M. (2005). Employee relations and the likelihood of occurrence of corporate financial distress. Journal of Business Finance and Accounting, 32(5–6), 1083–1105. https://doi.org/10.1111/j.0306-686X.2005.00623.x

- Kanoujiya, J., Singh, K., & Rastogi, S. (2022). Does promoters’ ownership reduce the firm’s financial distress? Evidence from non-financial firms listed in India. Managerial Finance, 49(4), 643–660. https://doi.org/10.1108/MF-05-2022-0220

- Kaplan, S. N. (1994). Campeau’s acquisition of Federated. Post-bankruptcy results. Journal of Financial Economics, 35(1), 123–136. https://doi.org/10.1016/0304-405X(94)90020-5

- Keasey, K., & Watson, R. (1991). Financial distress prediction models: A review. British Journal of Management, 2(1990), 89–102. https://doi.org/10.1111/j.1467-8551.1991.tb00019.x

- Khanra, S., Dhir, A., & Mäntymäki, M. (2020). Big data analytics and enterprises: a bibliometric synthesis of the literature. Enterprise Information Systems, 14(6), 737–768. https://doi.org/10.1080/17517575.2020.1734241

- Khwaja, A. I., & Mian, A. (2008). Tracing the impact of bank liquidity shocks: Evidence from an emerging market. American Economic Review, 98(4), 1413–1442. https://doi.org/10.1257/aer.98.4.1413

- Kirkpatrick, G. (2009). The Corporate Governance Lessons from the Financial Crisis Main conclusions. OECD Journal: Financial Market Trends, 1(February), 61–87. https://doi.org/10.1787/fmt-v2009-art3-en

- Koju, L., Koju, R., & Wang, S. (2018). Does banking management affect credit risk? Evidence from the Indian banking system. International Journal of Financial Studies, 6(3), 67. https://doi.org/10.3390/ijfs6030067

- Kroszner, R. S., & Strahan, P. E. (2001). Bankers on boards: Monitoring, conflicts of interest, and lender liability. Journal of Financial Economics, 62(3), 415–452. https://doi.org/10.1016/S0304-405X(01)00082-4

- Kuhnen, C. M., & Melzer, B. T. (2018). Noncognitive abilities and financial delinquency: The role of self-efficacy in avoiding financial distress. The Journal of Finance, 73(6), 2837–2869. https://doi.org/10.1111/jofi.12724

- Kumar, P., Hollebeek, L. D., Kar, A. K., & Kukk, J. (2022). Charting the intellectual structure of customer experience research. Marketing Intelligence & Planning, 41(1), 31–47. https://doi.org/10.1108/MIP-05-2022-0185

- Kumar, S., Pandey, N., Lim, W. M., Chatterjee, A. N., & Pandey, N. (2021). What do we know about transfer pricing? Insights from bibliometric analysis. Journal of Business Research, 134(March), 275–287. https://doi.org/10.1016/j.jbusres.2021.05.041

- Kumar, P., Sharma, A., & Salo, J. (2019). A bibliometric analysis of extended key account management literature. Industrial Marketing Management, 82(January), 276–292. https://doi.org/10.1016/j.indmarman.2019.01.006

- Kumar, S., Sureka, R., & Colombage, S. (2020). Capital structure of SMEs: a systematic literature review and bibliometric analysis. Management Review Quarterly, 70(4), 535–565. https://doi.org/10.1007/s11301-019-00175-4

- Laplante, P., & Kshetri, N. (2021). Open Banking : Definition and. Computer, 54(10), 122–128. https://doi.org/10.1109/MC.2021.3055909

- Lau, A. H., Journal, S., & Spring, N. (1987). ‘A Five-State Financial Distress Prediction Model Stable URL Linked references are available on JSTOR for this article : You may need to log in to JSTOR to access the linked references. Journal of accounting research, 25(1), 127–138. https://doi.org/10.2307/2491262

- Liu, G., Liu, Y., Zhang, C., & Zhu, Y. (2021). Social insurance law and corporate financing decisions in China. Journal of Economic Behavior and Organization, 190, 816–837. https://doi.org/10.1016/j.jebo.2021.08.019

- Magee, S. (2013). The effect of foreign currency hedging on the probability of financial distress. Accounting and Finance, 53(4), 1107–1127. https://doi.org/10.1111/j.1467-629X.2012.00489.x

- Mallinguh, E. B., & Zéman, Z. (2020). Financial distress, prediction, and strategies by firms: A systematic review of literature. Periodica Polytechnica: Social & Management Sciences, 28(2), 162–176. https://doi.org/10.3311/PPSO.13204

- Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance, 29(2), 449. https://doi.org/10.2307/2978814

- Meuleman, M., Wilson, N., Wright, M., & Neckebrouck, J. (2022). When the going gets tough: Private equity firms’ role as agents and the resolution of financial distress in buyouts. Journal of Small Business Management, 60(3), 513–540. https://doi.org/10.1080/00472778.2020.1717242

- Micucci, G., & Rossi, P. (2016). Debt Restructuring and the Role of Banks’ Organizational Structure and Lending Technologies. Journal of Financial Services Research, 51(3), 339–361. https://doi.org/10.1007/s10693-016-0250-5

- Mukherjee, D., Lim, W. M., Kumar, S., & Donthu, N. (2022). Guidelines for advancing theory and practice through bibliometric research. Journal of Business Research, 148(May), 101–115. https://doi.org/10.1016/j.jbusres.2022.04.042

- Muranda, Z. (2006). Financial distress and corporate governance in Zimbabwean banks. Corporate Governance The International Journal of Business in Society, 6(5), 643–654. https://doi.org/10.1108/14720700610706126

- Noyons, E. C. M., Moed, H. F., & Van Raan, A. F. J. (1999). Integrating research performance analysis and science mapping. Scientometrics, 46(3), 591–604. https://doi.org/10.1007/BF02459614

- Ohlson, J. A. (1980). Financial ratios and the probabilistic prediction of bankruptcy. Journal of accounting research, 18(1), 109. https://doi.org/10.2307/2490395

- Opler, T. C., & Titman, S. (1994). Financial distress and corporate performance. The Journal of Finance, 49(3), 1015–1040. https://doi.org/10.1111/j.1540-6261.1994.tb00086.x

- Othman, J., & Asutay, M. (2018). Integrated early warning prediction model for Islamic Banks: The Malaysian case. Journal of Banking Regulation, 19(2), 118–130. https://doi.org/10.1057/s41261-017-0040-5

- Palmatier, R. W., Houston, M. B., & Hulland, J. (2018). Review articles: purpose, process, and structure. Journal of the Academy of Marketing Science, 46(1), 1–5. https://doi.org/10.1007/s11747-017-0563-4

- Paul, J., & Criado, A. R. (2020). The art of writing literature review: What do we know and what do we need to know?. International Business Review, 29(4), 101717. https://doi.org/10.1016/j.ibusrev.2020.101717

- Paule-Vianez, J., Gutiérrez-Fernández, M., & Coca-Pérez, J. L. (2020). Prediction of financial distress in the Spanish banking system: An application using artificial neural networks. Applied Economic Analysis, 28(82), 69–87. https://doi.org/10.1108/AEA-10-2019-0039

- Paul, A., Gertner, R., & Scharfstein, D. (1994). Anatomy of financial distress: An examination of junk-bond issuers. Quarterly Journal of Economics, 109(3), 625–658. https://doi.org/10.2307/2118416

- Paul, J., Lim, W. M., O’Cass, A., Hao, A. W., & Bresciani, S. (2021). Scientific procedures and rationales for systematic literature reviews (SPAR-4-SLR). International Journal of Consumer Studies, 45(4). https://doi.org/10.1111/ijcs.12695

- Pham Vo Ninh, B., Do Thanh, T., & Vo Hong, D. (2018). Financial distress and bankruptcy prediction: An appropriate model for listed firms in Vietnam. Economic Systems, 42(4), 616–624. https://doi.org/10.1016/j.ecosys.2018.05.002

- Pindado, J., & Rodrigues, L. (2005). Determinants of financial distress costs. Financial Markets and Portfolio Management, 19(4), 343–359. https://doi.org/10.1007/s11408-005-6456-4

- Pindado, J., Rodrigues, L., & de la Torre, C. (2008). Estimating financial distress likelihood. Journal of Business Research, 61(9), 995–1003. https://doi.org/10.1016/j.jbusres.2007.10.006

- Platt, H., & Platt, M. (2008). Financial distress comparison across three global regions. Journal of Risk and Financial Management, 1(1), 129–162. https://doi.org/10.3390/jrfm1010129

- Porath, D. (2006). Estimating Probabilities of Default for German Savings Banks and Credit Cooperatives. Schmalenbach Business Review, 58(3), 214–233. https://doi.org/10.1007/BF03396732

- Pritchard, A. (1969). Statistical bibliography or bibliometrics?. Journal of Documentation, 25(4), 348–349.

- Ragab, Y. M., & Saleh, M. A. (2022). Non-financial variables related to governance and financial distress prediction in SMEs–evidence from Egypt. Journal of Applied Accounting Research, 23(3), 604–627. https://doi.org/10.1108/JAAR-02-2021-0025

- Rahman, S., Tan, L. H., Hew, O. L., & Tan, Y. S. (2004). Identifying financial distress indicators of selected banks in Asia. Asian Economic Journal, 18(1), 45–57. https://doi.org/10.1111/j.1467-8381.2004.00181.x

- Rajasekar, T., Ashraf, S., & Deo, M. (2014). An empirical enquiry on the financial distress of Navratna Companies in India. Journal of Accounting and Finance, 14(3), 100–110.

- Ramos, E., Dien, S., Gonzales, A., Chavez, M., & Hazen, B. (2021). Supply chain cost research: a bibliometric mapping perspective. Benchmarking: An International Journal, 28(3), 1083–1100. https://doi.org/10.1108/BIJ-02-2020-0079

- Ramos-Rodríguez, A.-R., & Ruíz-Navarro, J. (2004). Changes in the intellectual structure of strategic management research: A bibliometric study of the Strategic Management Journal, 1980–2000. Strategic Management Journal, 25(10), 981–1004. https://doi.org/10.1002/smj.397

- Rastogi, S., & Kanoujiya, J. (2022). Corporate disclosures and financial distress in banks in India: The moderating role of competition. Asian Review of Accounting, 30(5), 691–712. https://doi.org/10.1108/ARA-03-2022-0064