Abstract

The agriculture sector observed the penetration of parametric weather risk financial products, including weather index insurance and weather derivatives, between the late 1990s and the early 2000s. However, the adoption of such products remains low. While the reasons for low adoption are mentioned in the extant literature, there is a lack of a theoretical framework that captures the moderators accelerating and inhibiting pricing structure and willingness to pay for parametric weather risk mitigants in agriculture. Also, the extant literature does not adequately explain the relationships or interdependencies between pricing structure and willingness to pay for parametric weather risk mitigants. This study bridges this gap by performing an integrative literature review. The review integrates the bibliometric analysis and systematic literature review and categorizes the extant literature into five focal areas: (1) weather analytics capability; (2) design, pricing, and testing; (3) users’ criteria for adoption; (4) prototyping; and (5) product efficacy of weather risk mitigation. A conceptual framework evolved from the review classifies the moderators into accelerants and inhibitors of pricing and willingness to pay. The framework hypothesizes that product design, contract specifications such as tick size and strike levels, hedge effectiveness, and instrument adoption have a recursive interaction with the willingness to pay and pricing structure. Future research directions guided by the proposed framework can motivate scholars and practitioners to explore the scope of bundling parametric (index) insurance and weather derivatives as a standalone product to enhance adoption.

1. Introduction

Weather events impact many business activities regardless of size or volume, particularly the agriculture sector spanning its pre-and post-production stages. Lazo et al. (Citation2011) estimated the sectoral output responsiveness to economic and weather parameters and showed that the impact of weather parameters on agriculture is significant. The yield-response factor reveals that if rainfall increases or decreases by 10 percent in a particular year, ceteris paribus, the sectoral production will likely increase or decrease by 2.8 percent. Insulating the agriculture sector—crops, livestock, fisheries, and forestry from climate risks is necessary to ensure food security and poverty alleviation. For climate-related disasters such as floods, droughts, and tropical hazards, the agriculture sector absorbed 25 percent of all damages and losses in Asia, Africa, and Latin America (Centre for Science and Environment, Citation2016). The World Bank (Citation2011) documented that short-duration extreme weather events such as hail, windstorms, or heavy frost cause colossal direct damage to crops, and much of the damage occurs during early and mid-crop development stages. In other words, the agriculture sector emerged as the most affected by droughts, absorbing 84 percent of the economic impact (Centre for Science and Environment, Citation2016). Therefore, the correlation between weather events and crop damage requires calibration for geographical regions, and appropriate weather risk mitigants, namely parametric insurance, are designed to indemnify the farmers’ crop or livestock losses (Jensen & Barrett, Citation2017; Lichtenberg & Iglesias, Citation2022; Miranda & Farrin, Citation2012). Formal and informal approaches to mitigating weather risks in agriculture embed a risk management framework. The framework underpins the application of risk avoidance or prevention, retention, and risk transfer and financing (Rejda & McNamara, Citation2014). Formal market-based approaches through agricultural finance, weather derivatives, and parametric insurance allow disciplined financial risk management. In contrast, informal methods influence farming communities to mitigate risks through asset sharing and pooling of losses (Dercon, Citation2002).

Parametric weather risk financial products enable pure, co-variant, and market (price) risk financing (Binswanger-Mkhize, Citation2012) and make payouts based on observable yet untradeable variables such as reference unit area, rainfall, temperature, and frost, among others. These are structured financial products (see Annexure A.1 & for a comparison of parametric insurance and weather derivatives and their working shown in a pictorial presentation). In contrast, traditional (crop or livestock) insurance is a non-parametric financial product. While developed countries initiated a programmatic intervention in implementing parametric insurance in the 1990s (Smith & Watts, Citation2019), Asian and African countries observed the penetration of parametric weather risk products between 1999 and 2003 (Dercon et al., Citation2014; McIntosh et al., Citation2013). Parametric weather risk mitigants are superior to traditional ones since the former reduces the opportunity for moral hazard,Footnote1 adverse selection,Footnote2 transaction, and administrative or participation costs.Footnote3 However, the penetration of parametric (index) insurance and weather derivatives is yet to gain traction in the agriculture sector in developing countriesFootnote4; for example, in 2017–18, 26% of the cropped area was insured in India, compared to 69% in China and 89% in the United States (Alexander, Citation2019).

Pricing and willingness to pay for parametric weather risk financial products have received considerable academic and policy attention. Several models demonstrate the deterministic and stochastic pricing of weather derivatives and parametric insurance products. Campbell and Diebold (Citation2005) developed a model for forecasting daily average temperature. Benth and Benth (Citation2007) model weather derivative pricing with a continuous autoregressive process influenced by lag structure and seasonality. Cao and Wei (Citation2004) propose a valuation framework to model the market risk premium of weather events, while Brockett et al. (Citation2009) present an indifference pricing of weather derivatives and index insurance underlying the utility difference paradigm. Previous studies on weather derivative pricing assume a zero or constant market price of risk (MPR). Cao and Wei (Citation2004), Richards et al. (Citation2004), and Härdle et al. (Citation2016) capture the stochastic behavior of the MPR attributed to the poor specification of information calibrating the market prices. Empirical works by Alaton et al. (Citation2002), Jewson and Brix (Citation2005), and Yoo (Citation2003) incorporated the seasonal forecast into weather derivative pricing. Benth and Meyer-Brandis (Citation2009) introduced information drift and risk premium into the model.

While econometric models contributed to advancing the pricing structure of parametric weather risk financial products, the extant literature on farmers’ willingness to pay for index insurance and weather derivatives adoption presents mixed findings. The rate of adoption is considerably low in developing countries. There are many reasons for the low adoption, including heterogeneity in farmers’ preferences for parametric insurance (Wang et al., Citation2020), varying degrees of farmers’ risk aversion (Clarke, Citation2016), lack of information on climate variability to future crop failures (Budhathoki et al., Citation2019), ineffective product design (Shirsath et al., Citation2019), information asymmetry between risk aggregators and farmers (Hazell et al., Citation2017; Smith & Goodwin, Citation1996), and higher actuarial risk premium and delay in claim settlement (Giné & Yang, Citation2009). Although the extant literature reveals the reasons for low adoption, there is a lack of a theoretical framework capturing the moderators that accelerate and inhibit pricing and willingness to pay for parametric weather risk mitigants in agriculture. Also, the extant literature does not adequately explicate the relationships or interdependencies between pricing and willingness to pay for parametric weather risk financial products in agriculture.

With this motivation, an Integrative Literature Review (ILR) coupling bibliometric analysis and systematic literature review is performed to identify the decisive moderators of pricing and willingness to pay for weather derivatives and parametric (index) insurance in agriculture. The review proposes a conceptual framework explicating the relationship between product design and contract specifications, hedge effectiveness, and willingness to pay for parametric weather risk financial products. The study can expand the parametric weather risk financial product pricing and adoption knowledge frontier. A total of 1,095 articles were retrieved from the Web of Science and Scopus databases and Google Scholar by relaxing the search criteria of the publication year, which implies that the search for integrative review considered all relevant research articles since the emergence of parametric insurance and weather derivatives.

The remainder of the paper is organized as follows. Section 2 presents the research design and methods utilized for an integrative review. Section 3 discusses the bibliometric analysis and bridges the transition from the bibliometric analysis to the systematic literature review. Section 4 reports the findings of the systematic literature review. Section 5 proposes a conceptual framework and discusses the future research agenda. Section 6 concludes the paper with implications and limitations.

2. Research design and empirical strategy for analysis

This study adopted an eclectic research design to perform an integrative literature review. An ILR integrates a bibliometric analysis of extant literature and a systematic scoping literature review. Broome (Citation1993) defines the ILR as “summarizes past empirical or theoretical literature to provide a greater comprehensive understanding of a particular phenomenon.” Torraco (Citation2005) concurs with Broome (Citation1993) that ILR is systematically reviewing, critiquing, and synthesizing the extant literature drawn from a universe of the topic of interest. The synthesis helps produce new conceptual frameworks and perspectives on the topic/thematic areas generated. Yorks (Citation2008) argues that ILR is different from other forms of review in its capacity to be called new research that encompasses the boundaries of the subject. In the ILR, the researcher traces the selected topic back to its origin. Suppose the chosen topic is relatively newer or evolving. In that case, the extant literature review should (i) encompass the realm of the topic in its entirety and for developed areas, (ii) the topic needs to be reviewed chronologically, or (iii) one of the concepts of the topic needs to be the focus of the study. Whittemore and Knafl (Citation2005) and Toronto and Remington (Citation2020) maintain that the ILR is focused on a phenomenon of interest rather than a systematic review that expands the scope for diverse results containing theoretical and methodological literature to address the review’s aim. In other words, it supports a broad-based inquiry, such as the definition and connotation of concepts, reviewing theories, and analyzing methodological issues.

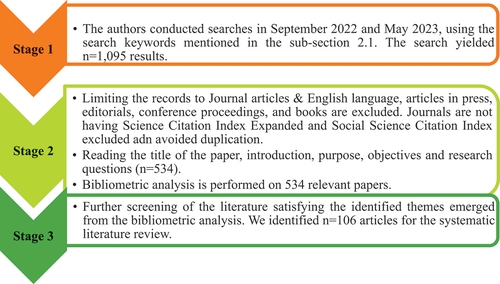

The integrative literature review couples the bibliometric and systematic literature review to create a new conceptual framework and offers new research frontiers in the domain of research interest. The bibliometric analysis helps map and decipher the amassed knowledge by interpreting similar or dissimilar data to create a meaningful explanation of the subject, exposing the patterns, identifying potential gaps, and providing motive with methods for further investigation Donthu et al. (Citation2021). A researcher needs to feed extensive bibliometric data to unleash its potential fully. Biases affect this method if the number of the dataset is less. Snyder (Citation2019) suggests that for systematic review, the number of papers should be between tens [e.g., 40] or low hundreds [e.g., 100–300]). Going by this rationale, a large dataset should constitute papers in the high hundreds [e.g., >300] for bibliometric analysis. To ensure the pragmatism and unbiasedness of this review, we performed a bibliometric analysis using 534 articles and a systematic review of 106 articles that fit the inclusion criteria chosen for the review.

We initiated the literature search with a few questions to list the categories and corresponding thematic mapping as part of bibliometric analysis. The identified papers tried to address at least one of the three questions noted below, and the scoping review guided us to identify the research questions raised by empirical studies. For example, Turvey (Citation2001), Mahul (Citation2001), Odening et al. (Citation2007), and Barnett and Mahul (Citation2007) tried to answer the following research questions in their studies.

RQ1:

What is the rationale for parametric (area-based yield and index) insurance and weather derivatives in agriculture?

Miranda and Vedenov (Citation2001). Vedenov and Barnett (Citation2004) and Musshoff et al. (Citation2011) attempted to address:

RQ2:

Why should farmers or agricultural farms subscribe or buy parametric weather risk products?

Alaton et al. (Citation2002). Zapranis and Alexandridis (Citation2008, Citation2009) tried to answer:

RQ3:

How are index insurance and weather derivatives priced to influence the adoption? What is the value proposition, and how can it affect the product design and contract specifications?

These research questions helped us to categorize five hundred thirty-four articles, as shown in Figure , for thematic mapping. On the one hand, the bibliometric analysis enabled us to identify influential authors and their publications and citations. On the other hand, authors’ keywords or co-occurrence analysis provided insights into the common language utilized by researchers and facilitated us to sort and categorize publications for thematic mapping or identifying emerging or waning themes, niche themes, and basis and motor themes (Donthu et al., Citation2021; Esfahani et al., Citation2019). The analysis traced the evolution of scientific production, and thematic mapping addressed the problem of subjectivity inherent in authors’ keywords or co-occurrence analysis. The bibliometric analysis uncovered categories of research articles published in parametric (index) insurance and weather derivatives guided by the three research questions, and four research categories led to evolving important themes. The underlying themes helped us to present a comprehensive list of moderators of pricing and willingness to pay for parametric weather risk financial products. The performance analysis and science mapping through the bibliometric analysis motivated us to perform the systematic literature review of extant literature embracing emerging (waning) and niche themes related to pricing models and valuation, users’ criteria for adoption, and instrument (product) efficacy of weather risk mitigation. The systematic literature review minimized biases by employing extensive and systematic tools while reviewing articles and drawing reliable findings.

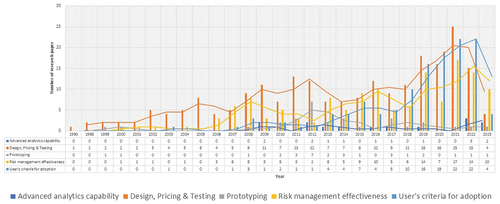

Figure 2. Year-wise publication of research articles on weather derivatives and parametric insurance in agriculture.

2.1. Search criteria

Considering the following keyword search string, we searched the Web of Science, Scopus databases, and Google Scholar in September 2022 and May 2023.

“Weather*” AND “Index insurance*” AND “Agriculture*”

“Weather*” AND “Derivatives*” AND “Agriculture*”

“Parametric insurance*” AND “Agriculture*”

“Pricing*” AND “Weather derivative*” OR “Index insurance*”AND “Agriculture*”

“Hedging*” AND “Weather derivative*” OR “Index insurance*” AND “Agriculture*”

“Parametric insurance*” OR “Weather derivative*” AND “Willingness to pay *” AND “Agriculture*”

We relaxed the search criteria of the publication year, which implies that the search for integrative review considered all relevant research articles since the emergence of parametric insurance and weather derivatives. The guided search yielded 1,095 articles, including research monographs, books, conference proceedings, and early-view articles. Using the inclusion-exclusion criteria (refer to Figure ), we selected 534 articles for bibliometric analysis and 106 articles for a systematic literature review.

Figure 1. Inclusion and exclusion criteria for literature review.

3. Bibliometric analysis

The bibliometric analysis encompasses citation analysis, scientific production, cooccurrence or keywords analysis, pricing models used in weather derivatives, and parametric insurance products specific to the farm sector. The analysis captures a year-wise scientific production of research papers on parametric weather risk financial products in agriculture. Five hundred thirty-four research articles retrieved for bibliometric analysis since the 1990s fell into five focal areas of research: (1) weather analytics capability; (2) design, pricing, and testing; (3) users’ criteria for adoption; (4) prototyping; and (5) product or instrument efficacy of weather risk mitigation (see Figure ). Notably, the design, pricing, and testing of parametric weather risk products, risk management effectiveness, and users’ criteria for adoption emerged as dominant themes in developed internal linkages or high density and more considerable external ties or high centrality. It may be noted that the degree of correlation between different topics indicates a centrality measure, while the cohesiveness of thematic areas is measured by density (Esfahani et al., Citation2019). The significant contribution to scientific production comes from the United States, the United Kingdom, Germany, China, and a few developing countries. Categorization of the papers and representing them into themes are discussed in sub-section 3.3.

3.1. Authors’ citation analysis

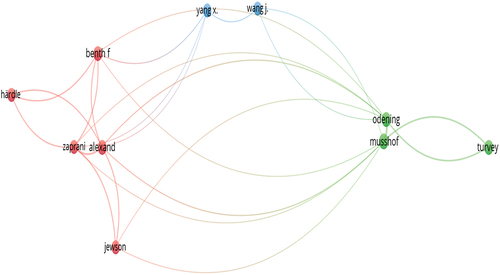

To identify the top eleven influential authors, we ran multiple iterations on a minimum number of documents (3 4, or 5) and a minimum number of citations (45 or 50). We were interested in the authors whose contribution has the highest total link strength.Footnote5 Figure shows influential authors. The red and green venn exhibit the dominant authors’ collaborative networks, followed by the blue ones. Table presents influential authors, top-cited publications, and citations in descending order.

Figure 3. Authors’ citation network.

Table 1. Influential authors, their top-cited publications, and citations

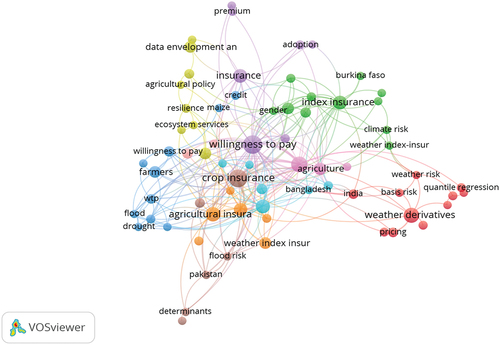

3.2. Authors’ keywords analysis

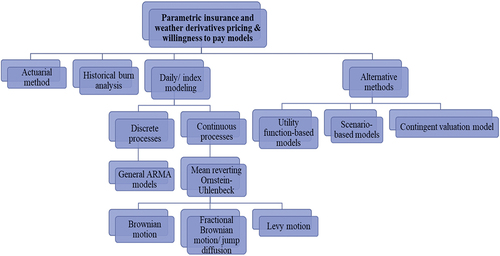

Authors’ keywords analysis is reported in Figure . “Willingness to pay,” “crop (area-based yield) insurance,” “climate risk,” “index insurance,” “weather derivatives,” and “agricultural policy” are frequently occurring keywords. Additionally, tools and techniques used in modelling parametric weather risk financial products are depicted in Figure . Weather derivative and index insurance pricing models follow the actuarial method, historical burn analysis, and daily or index weather derivative price modelling (Alexandridis & Zapranis, Citation2013). Alternative methods become popular in modelling temperature or rainfall derivative pricing. This method considers utility-based function and scenario-based models. Interestingly, the contingent valuation model and quantile regression model show the willingness to pay for parametric weather risk financial product adoption (Budhathoki et al., Citation2019).

Figure 4. Authors’ keywords analysis.

Figure 5. Models used in weather derivative and parametric insurance pricing and willingness to pay.

3.3. Theme identification and mapping

The bibliometric analysis helped the authors to organize 534 articles into four categories, enabled by authors’ keywords, bibliometric coupling, and authors’ understanding of the subject (Donthu et al., Citation2021; Esfahani et al., Citation2019). The four categories emerged from three important issues highlighted in the extant literature: (1) reasons to introduce, (2) reasons to buy, and (3) logic to price the parametric weather risk financial products. The first category is product suitability. The second category is product performance, while the third is product design. The fourth category is product adoption. Each category has underlying attributes identified from 534 research articles.

3.3.1. Cat1: product suitability

Attributes are risk prevention, risk retention, risk financing, or securitization by transferring risk to capital markets or re-insurance agencies.

3.3.2. Cat2: product performance

Attributes are risk mitigation efficacy or hedge effectiveness, adoption benefits, ex-ante estimation of economic loss of farmers, and index-triggered payout with actual loss.

3.3.3. Cat3: product design

Attributes include weather variables, weather station, compensation criteria, the usability of real-time climate data, product accessibility, and acceptability.

3.3.4. Cat4: product adoption

Attributes are demand estimation, subsidies, and willingness to pay.

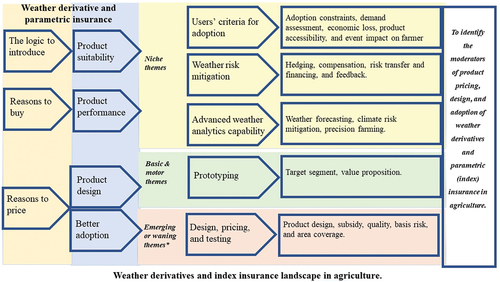

The four categories led to the evolution of four themes guided by research questions and categorization of area-wise scientific production. These themes embrace focal research areas in weather derivatives and index insurance in the agriculture sector. The theme identification rationalized the transition from the bibliometric analysis to the systematic literature review. In other words, themes that emerged as bibliometric analysis outcomes motivated us to systematically review more than a hundred articles embracing emerging and niche themes. The centrality and density measures are used to identify the following themes (Donthu et al., Citation2021).

Basic and motor themes: Prototyping like product suitability, value proposition, target users, and evaluation. These fundamental and sophisticated themes contain transversal topics, indicating high density and centrality.

Emerging or waning research themes: Product design and pricing structure. These themes contain low density and low centrality and are yet to be developed.

Niche themes: Users’ criteria for adoption, risk mitigation, and farm performance. These themes have high internal linkages (high density) but negligible external ties or low centrality.

These underlying themes helped us identify decisive factors that moderate pricing structure, valuation, willingness to pay for weather derivatives, and parametric (index) insurance in agriculture (see Figure ).

Figure 6. Thematic mapping of weather derivatives and parametric insurance landscape in the agriculture sector.

4. Systematic literature review

Following a bibliometric analysis, we conducted a systematic literature review on a niche, emerging themes, classifying them into the pricing of parametric weather risk financial products (emerging themes), willingness to pay underlying the users’ criteria for adoption, analytics capability, and hedge effectiveness of parametric weather risk mitigants (niche themes). We have not considered basic and motor themes for systematic literature review since these themes are matured, and there has been considerable scientific production. A summary of one-hundred-six research articles is presented in a supplementary file, S.1.

4.1. Pricing and valuation of parametric weather risk products

A systematic review of pricing models used in weather derivatives and insurance products is presented below.

4.1.1. Option pricing and actuarial burn rate models

The study developed a dynamic path of cooling or heating and growing degree days for Toronto using local weather station data from 1840 to 1996. The author measured the intra-year volatility of a degree day. A variance ratio test identifies whether degree day follows a random walk. Davis (Citation2001) opines that the Black-Scholes-Merton (BSM) model cannot be used for pricing weather derivatives as the underlying asset is non-tradable. However, if we assume Brownian motion-based expected utility maximization and drift rate (includes the natural growth rate of the degree day measure, spot price, and firm profit), the degree day option can be ascertained using the BSM model.

Turvey (Citation2001) explained that the weather variable has an expected value embedded in a quadratic equation. A discount rate of 6.5% and a 92-day expiration option premium were calculated. The premium was also computed using the actuarial burn rate and BSM. Turvey (Citation2001) concluded that the option pricing model gives a value that is 3.85 times less than the option premium value derived from the burn rate for the utilized data between 1840 and 1996. However, for data between 1930 and 1996, the burn rate overestimated the premium by 2.66 times compared to the option pricing model. This finding also highlighted illiquid weather options due to an increased bid-ask spread.

While the actuarial burn rate overstates the option pricing, assuming the history repeats itself, the exercise makes it a backward-looking approach. In contrast, the author’s approach used probability distribution and thought that infinitely new patterns could emerge randomly. For burn rate, in more specific words, history repeats itself, and therefore, it does not require an estimate of the initial weather index. The burn rate model assumes that a derivative price should equal the present value of its expected payoff at the expiry, where the expectation is calculated using historical data. Hence, the option pricing model suggested by Turvey (Citation2001) assumed a numerical starting point from which variability can be measured, and the price of the option is sensitive to that starting point.

4.1.2. Two-factor model

Groll et al. (Citation2016) followed an incremental progression approach for temperature-based derivatives suggested by Hell et al. (Citation2012). Groll et al. (Citation2016) model the complete temperature forecasting curve dynamics using a consistent factor model. The forecast includes market-known information that can be derived from the forecast curve as one of the factors. This curve follows a martingale process (mean and drift). The data used for estimation purposes is the daily closing prices of the New York JFK airport Heating Degree Days (HDD) and Cooling Degree Days (CDD) from the Chicago Mercantile Exchange Group. The two-factor model used in modelling pricing of temperature derivatives considers deseasonalized temperature and ensures that the random spikes are normalized; the second factor incorporates forward-looking information that assumes that all the information available in the market is known to all market participants and hence, an efficient price discovery. Estimating the market price of risk, the authors inferred that any irregularity in evaluating the market price of risk could arise due to the misspecification and lack of forward-looking information. Diebold-Mariano test was performed to compare the accuracy of forecasting. It is observed that a two-factor model outperformed the burn rate and BSM since the mean squared error and predictive performance of the two-factor model scores over other models. Groll et al. (Citation2016) advocated using the two-factor model in pricing weather derivatives as it includes forward-looking information and index estimation.

4.1.3. Lucas’s general equilibrium model

Richards et al. (Citation2004) adopted Lucas’s general equilibrium valuation of the full-pricing weather derivative model requiring an aggregate dividend or economic activity. Aggregate economic activity is affected by weather, so any contingent claim on the weather index extends the claims on economic activity. The sample period included from 1979 to 2000, and the location was Fresno, United States of America. A stochastic model, namely mean-reverting Brownian motion with a lognormal jump and time-varying volatility jumps in temperature, was used that could follow the Poisson process with an average arrival (using a dampening factor) rate of lambda (λ). Time-varying volatility is incorporated by specifying first-order ARCH processes. This model assumes a pure exchange economy where agents control the production output and set the upper bound of utility. Any claim on output is equilibrated against asset prices. In equilibrium, consumption is equal to the aggregate dividend or economic activity. A risk-averse consumer often chooses a consumption function to maximize the present value of expected utility. Richards et al. (Citation2004) assume that if the aggregate dividend is no longer related to weather, then the market price of risk would be zero. The authors concluded that mean-reverting Brownian motion with first-order autoregressive and log-normally distributed jump is a robust model for capturing daily average temperature. As temperature and yield have a non-linear relationship, the producer must adopt a straddle option strategy utilizing buying (selling) a call option and buying (selling) a put option with the same strike and expiry to delimit the downside exposure.

4.1.4. Peer group analysis

Peer group analysis helps in identifying peers based on some similarity of events. Mahalanobis’s method establishes a covariance matrix by estimating the correlation between variables. Hong and Sohn (Citation2013) used historical weather data to replicate the Mahalanobis method. Forty-seven cities using weather derivatives are traded in the Chicago Mercantile Exchange. Hong and Sohn (Citation2013) used Seoul’s average weather data for 30 years and 47 cities and estimated a peer distance over various intervals. A “Seoul weather index” was created using daily average data for three years. The monthly and seasonal weather indexes of 47 cities were used to derive the weather index. Five cities among 47 had similar weather conditions to that of Seoul city. These are the peer groups of Seoul. The cities stood Little Rock City, Dallas, Washington DC, Hiroshima, and Osaka. It was assumed that if three or more than three cities of the peer group are using a particular type of weather derivative, it is considered that Seoul also needs that derivative. Hong and Sohn (Citation2013) concluded that factors like previous payout and weather forecasting influence the pricing of weather derivatives. The authors recommended introducing monthly cooling degree day and heating degree day futures with seasonal strips, as three out of five cities presented a similar pattern. They proposed the price to consider the average historical weather data of the town and its peer cities in the last three years to minimize prediction error. The pricing model’s prediction error is minimal as data needed for this analysis was available from the Chicago Mercantile Exchange.

4.2. Comparison of pricing models

The crop (corn) is temperature sensitive, and low or high temperature is detrimental to crop yield. A farmer could ensure against hot or cold seasons by holding a put option based on the number of growing degree days (GDD). The objective is to compare the three-pricing model viz: weather index method using historical average called burn analysis, stochastic process with Monte Carlo simulation, and econometric approach with a sine function. A Monte Carlo simulation employed an algorithm that used repeated random sampling to obtain the likelihood of a range of occurrences. For example, if two dice are rolled together, there can be 36 possibilities.Footnote6 Burn analysis indicates future payoffs based on the past gains made by the exact derivative. Growing degree day measures the heat exposure of crops during the growing season. Sun and van Kooten (Citation2015) concluded that the GDD historical average was 9% less than the GDD of Monte Carlo and 14.7% less than the GDD obtained from the stochastic model, and it is observed that the GDD historical average was very close to the actual GDD.

4.3. Market price of risk

This approach introduced Autoregressive Conditional Heteroscedasticity (ARCH) and Generalized Autoregressive Conditional Heteroscedasticity (GARCH) into the temperature model suggested by Alaton et al. (Citation2002). Options pricing concerning the expected mean and standard deviation of HDD and CDD was calculated. The model incorporates the market price of risk to arrive at a fair option price. Huang et al. (Citation2008) then compare the difference in option pricing with constant variance assumption and the variance following an ARCH process. The authors used Taiwan weather data from 1974 to 2003. The premise is that the trend of gradual temperature increases is linear, and sine functions capture seasonality. The authors introduce a seasonality factor into the Alaton et al. (Citation2002) equation and assume that this factor follows a GARCH process. By submitting this factor, the author makes the long-term Alaton et al. (Citation2002) model into a short-term, and a correlation coefficient is established between the short-term and the long-term model. The understanding is that the climate condition of two adjacent dates exhibits a similar and significant autocorrelation. The risk premium is calculated using asset pricing and the martingale models.

The authors applied the martingale method, known as the unknown arbitrage approach. To calculate the market price of risk, the author used the Sharpe ratio (mean-excess return to standard deviation of portfolio risk), where the standard deviation average stock return and a risk-free rate of Taiwan Nationalized Bank were used to arrive at a proxy market price of risk. Intuitively, we know that bad weather has a significant effect on the volatility of the Stock Exchange. Hence, this proxy market price of risk will always be higher than the actual market price of risk. For this study, the reference temperature of heating (HDD) and cooling degree days (CDD) increased to 23°C from 18°C as Taiwan sustains a humid temperature. The author concluded that if the conditional variance used in the ARCH is more than the fixed conditional variance, the case market price of risk will be more than zero, and one can have a higher expected value for HDD options and a low for CDD options and vice versa. If this market price of risk equals zero, there will be no effect of conditional variance on the expected temperature.

4.4. Return volatility model

Benth and Benth (Citation2007) modelled seasonal volatility by applying a Fourier series curtailing the peaks. A Fourier series helps decompose any periodic function into Sine and Cos adequately, representing seasonality in the data. In the Fourier series number of cycles is finite with an integer. If this number of cycles becomes infinite, the Fourier series will merge with the Fourier transformation. The idea behind truncating the data is to provide an efficient algorithm for evaluating polynomials in any number of distant points. Truncation helps eliminate the jump in complexity. Thus, it reduces the error. Truncated means to cut short or end abruptly when the value of any function or functional derivative differs from numerical approximation or reality. The truncation error is the difference between these two values. As a first step, Benth and Benth (Citation2007) used 45 years of daily data from Stockholm, Sweden, collected as this city trades in the Chicago Mercantile Exchange. The author calibrates the model using this data and compares it with the quoted market data from the Chicago Mercantile Exchange. Benth and Benth (Citation2007) utilize the Fourier transformation to estimate future prices for the delivery period of interest. The authors employed the Ornstein-Uhlenbeck model to map the temperature evolution. This model captures the temperature change and includes factors like seasonality trend, mean reversion, the daily average temperature of maximum and minimum, volatility, and random walk. The data were fed into MATLAB software, and the author estimated the HDD index, Cumulative Average Temperature index, and CDD index for five European and two Japanese cities. Benth and Benth (Citation2007) concluded that HDD future prices are higher when seasonal volatility is considered complete; this difference doubled during summer. The seasonal maturity effect is attributed to the volatility in the futures prices. They explained that the volatility factor is significant when it is close to delivery, like the maturity effect in the commodity market, as most of the information is already revealed to market participants.

4.5. Willingness to pay and adoption

Willingness to pay is a critical factor that depends on reducing overall farm risk post-application of weather index insurance. Seth et al. (Citation2009) concluded that group schemes are preferred to an individual plan that assures inclusion and togetherness while adopting some new risk management tool. The adoption rate improves with a broader coverage period. Bank and Wiesner (Citation2010) studied weather index insurance adoption by small and medium enterprises. The authors highlighted that the transaction and participation costs for obtaining the relevant information to interpret price versus benefits are essential parameters. Also, the lack of institutional framework and difficulty in pricing leads to poor adoption of this innovative risk mitigation tool. Ghosh et al. (Citation2021) studied a farmer’s requirement in the developing eco. They concluded that farmers understand various sources, origins, and types of risk to their crops. Hence, they demand a tool with an extension to cover significant risks and not just the risks of excess or low rainfall or high or low temperature. Timely payout against expected crop loss improves the synchronization of weather derivative contracts with a willingness to pay for such products. Cole et al. (Citation2014) advocate that adopting (rainfall) index insurance can be a complex mechanism as payouts depend on readings at local rainfall stations rather than consumers’ actual losses. Budhathoki et al. (Citation2019) suggest that premium is not an inhibiting factor of willingness to pay; instead, gender role in decision-making influences the adoption of index insurance.

4.6. Hedge effectiveness and farm performance

Weather index insurance is prone to basis risk, including geographical (locational), production (crop-specific), and temporal basis risk. Doms et al. (Citation2018) introduced one more basis risk, the economic basis risk, and defined it as a residual risk that remains even after applying the risk mitigation tool. In the seminal paper on hedging efficacy by Ederington (Citation1979), hedging efficacy is defined as a proportional reduction in the volatility of a variable post-hedging. In this paper, Doms et al. (Citation2018), while studying the farm operation risk, stressed that the focus should be on the gross margin from the entire farm instead of just focusing on the yield loss of a specific crop. A farmer is assumed to take up many operations on the farm, like the production of crops, cattle rearing, hatchery or layering, and pre-processing setup.

Several dimensions of weather index insurance are dependent on the sources of systemic (basis) and idiosyncratic risk (Jensen & Barrett, Citation2017). Approaches used to design contracts, the robustness of utilized models that help capture the real-time weather variables influencing the farming regions, and contract design and demand for the subscription. Here, the performance of the whole farm is studied after the application of the risk management tool. Here, the author emphasized the type of contract design. There are two types of contract design. In standardized type, the contract is based on an expert understanding of how a weather condition will affect crop growth. The strike level used is an arithmetic mean of past data. This data can be actual or synthetic based on secondary data of regional yield. However, a customized contract is based on individual farm and weather data. Farm-specific data defines tick and strike levels so that insurance payment compensates for maximum losses incurred by a farmer. Doms et al. (Citation2018) concluded that the correlation between the payoff from the weather index insurance and the farm yield data could not be trusted. Doms et al. (Citation2018) firmly highlighted that standardized contracts were inapt to mitigate the farm’, which understates the standardized contracts based on an expert understanding of crop growth is less appropriate. Hence, farmers may not pay any additional loading.

5. Conceptual framework and research agenda

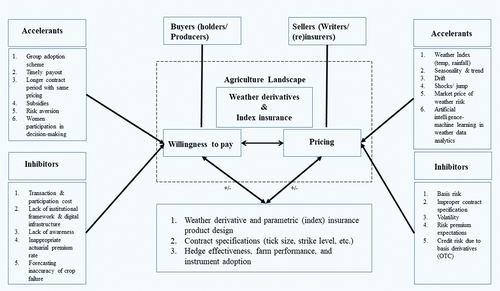

The Integrative Literature Review helped the authors to derive a conceptual framework by dovetailing supply- and demand-side moderators, classifying them into accelerants and inhibitors, influencing willingness to pay, and pricing of weather derivatives. The framework drawn in Figure hypothesizes an association or relationship between the willingness to pay and the pricing of weather derivatives and parametric (index) insurance influenced by a slew of accelerants and inhibitors. The supply-side accelerants embracing weather volumetric parameters include weather index, seasonality, drift or jumps, shocks, trends, risk premium, and the role of artificial intelligence—machine learning in weather data analytics. The inhibitors contain basis risk, improper parameter specifications, return volatility, risk premium expectations, and credit risk attributed to basis derivatives as over-the-counter products. These supply-side accelerants and inhibitors affect the pricing structure of weather derivatives or index insurance products.

Figure 7. Moderators of pricing and willingness to pay for weather derivatives and index insurance in agriculture.

The demand-side accelerants and inhibitors also impact willingness to pay for parametric weather risk financial products. The accelerants include bundling of the scheme or standalone offering, group adoption scheme, timely pay-out or claim settlement, extended contract periods without variable pricing, subsidies, risk aversion, and gender role in household decision-making. The inhibitors are transaction and participation or administrative costs, lack of institutional framework, awareness of weather index products, inappropriate actuarial premium rate, and forecasting inaccuracy of crop damage.

The conceptual framework hypothesizes that pricing affects willingness to pay, and willingness to pay influences pricing structure. Furthermore, weather derivatives and index insurance product design, contract specifications such as tick size and strike levels, hedge effectiveness, farm performance, and instrument adoption have a recursive interaction with pricing and the willingness to pay.

5.1. Future research questions

The future research agenda can stimulate scholars and practitioners to examine the nature and degree of the interaction between willingness to pay, pricing structure or premium level, product design, contract specifications, hedge effectiveness, farm performance, and instrument adoption. The following research questions are proposed to expand research endeavours in pricing and willingness to pay.

Which factors affect farmers’ risk aversion for parametric weather risk financial products? Is there any significant difference in risk aversion quotient between men and women farmers for willingness to pay?

How can weather forecasting error, crop classification, and claim settlement speed reduce the opportunity for moral hazard and adverse selection and enhance farmers’ willingness to pay?

How do weather data analytics improve farmers’ expectations of crop loss and risk premium, influencing their willingness to pay for parametric weather risk financial products?

Can bundling parametric (index) insurance and weather derivatives improve agricultural farm performance and optimize yield and income loss indemnification?

How can bundled instruments be priced to maximize farmers’ utility by mitigating pure, co-variant, and market (price) risks? Does a stochastic pricing model score over historical (actuarial) burn analysis in the pricing of parametric weather risk financial products?

6. Conclusions, limitations, and implications

This study conducted an integrative literature review to explore the moderators of pricing and willingness to pay for weather derivatives and parametric (index) insurance in agriculture. The integrative review employed a bibliometric analysis of five hundred thirty-four research articles and a systematic literature review of one hundred-six papers to attain the study’s objectives. As the bibliometric analysis brought subjectivity or potential bias due to keywords-based analysis and their co-occurrence, the systematic literature review was performed to overcome the subjectivity in the review process (Liberati et al., Citation2009). The review presented a conceptual framework containing a comprehensive list of moderators of pricing and willingness to pay for parametric weather risk mitigants and hypothesized a bi-directional relationship between product design, contract specifications, adoption, willingness to pay, and the pricing structure of weather risk financial products. The integrative review concurs with the extant literature that since there is heterogeneity in farmers’ risk and product preferences (Wang et al., Citation2020), the length of the growing period or protection period selection against the crop-loss ratio must be considered in constructing the weather index insurance or derivatives products underlying the volumetric non-tradable weather parameters (WB, Citation2011). To create such tailored parametric products, an ex-ante framework is crucial to establish the relationship or association between pricing and willingness to pay for parametric weather risk products (Jensen & Barrett, Citation2017; Lichtenberg & Iglesias, Citation2022; Miranda & Farrin, Citation2012).

The bibliometric analysis embraced citation analysis, scientific production, co-occurrence or keywords analysis, and thematic mapping of research publications. The study revealed that Alaton, Alexandridis, Campbell, Davis, Härdle, Jewson, and Zapranis, among others, are influential contributors, and the empirical exploration of the pricing and willingness to pay models of weather derivatives and parametric (index) insurance has stemmed from the scholars of the United States, United Kingdom, and China. Weather derivatives and index insurance pricing models vary from historical, time-invariant models to stochastic higher-order models. Implied option pricing, or Black-Scholes-Merton option pricing, on the other hand, is relevant to capture implied volatility in weather options, especially rainfall and temperature options. Ornstein-Uhlenbeck’s process utilizes the mean reversion property of the weather variable and incorporates it into a random walk model with a stochastic trend. It allows options writers, namely (re) insurance firms, to protect the downside risk against extreme weather events. Also, the wavelet network allows decomposing the weather data into more relatable different frequency components, which can be used to value weather derivatives contracts by predicting value based on the coefficients of parameters estimated by the wavelet.

The systematic literature review was performed on pricing and valuation models of weather derivatives and index insurance, willingness to pay, and hedge effectiveness of parametric weather risk financial products. Several pricing and valuation models computed the strike price and premium (for option) of weather derivatives and index products. Concerning comparing various pricing models of weather derivatives, the relationship between cop or livestock yields and weather parameters can derive and calibrate premium and strike levels for growing degree day weather options. While pricing and valuation models were under consideration for a systematic review, the market price of risk or risk premium computation indicated a difference in options pricing under variance assumptions. The literature review of willingness to pay inferred that if the cost of such a derivative or index product for the specific crop is well-researched, it can be possible to introduce or implement this instrument without government subsidy. The review also reported that standardized contracts cannot hedge the performance risk of agricultural farms. The ex-post-adjusted contracts perform better. Other than the index type, option premium, and strike level, the hedge effectiveness of the whole farm depends on the production exposure to pure, co-variant, and market (price) risks and the level of indemnities or premium to claim ratio. Decreasing the tick size of weather derivative or index insurance contracts could not affect premium pricing.

This study has implications for researchers and practitioners. First, scholars can understand parametric weather risk financial products’ nuances, prices, and valuation models. Second, the moderators of pricing and willingness to pay for parametric weather risk mitigants can help the insurance agencies and commodity exchanges to design a robust weather index with appropriate actuarial risk premia and strike levels specific to the crop, season, and geographical regions or landscape in a manner that the index-triggered pay-out should cover the loss arising from systemic risk and farm-specific risk (some extent). Future research would investigate how product design, contract specifications such as tick size and strike level, hedge effectiveness, farm performance, and instrument adoption can influence the pricing models and willingness to pay for parametric weather risk financial products and alternative risk transfer instruments such as special purpose vehicles and indemnity bonds.

Supplemental Material

Download MS Word (87.7 KB)Acknowledgments

The authors are thankful to the Senior Editor and two anonymous reviewers of this journal, Professor Sanjeev Kapoor and Professor Jalaj Pathak of the Indian Institute of Management Lucknow, for highly relevant comments that helped the authors improve the earlier version of the manuscript significantly. The authors avoided using AI-assisted literature search and synthesis using Consensus AI or Elicit. The usual disclaimer applies.

Disclosure statement

The authors declare that they have no financial or non-financial competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Supplementary material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23322039.2023.2254579.

Additional information

Funding

Notes on contributors

Gaurav Gairola

Gaurav Gairola is pursuing his doctoral program at the Indian Institute of Management Lucknow. His current research explores weather derivatives and index insurance pricing and valuation models and tries to establish a relationship with the stakeholder’s willingness to pay for index insurance and derivatives. His co-authored work has appeared in Applied Economics Letters on a bibliometric analysis of price discovery and hedging in various asset classes.

Kushankur Dey

Kushankur Dey is an Assistant Professor and former Chairman of the Centre for Food and Agribusiness Management at the Indian Institute of Management Lucknow. To his credit, he has more than 20 peer-reviewed research articles, which appeared in the Journal of Cleaner Production, Journal of Behavioural and Experimental Finance, Journal of Rural Studies, Economic and Political Weekly, and Applied Economics Letters. His research interests lie in climate change adaptation and mitigation, blended financing, commodity pricing and risk management, and platform-enabled agribusiness.

Notes

1. The indemnity or index-triggered payout does not depend on the individual producer’s realized yield.

2. The indemnity is based on widely available information, so there are few informational asymmetries to be exploited.

3. Underwriting and inspections of individual farms are not required.

4. Insurance penetration as a percentage of premium to GDP in Asia and Africa is only 4–5%, while the United States and the United Kingdom reported the penetration to 10–12% (India Insure, 2022)

5. Total link strength (TLS) indicates the total strength of the co-authorship links of a given researcher with other researchers. We calculated the TLS by referring to the VoS Viewer manual.

6. If the dice is rolled for, say, 100 or 1000, or 10,000 times or more, the probability of a particular outcome can be more easily predicted close to the accuracy using the Monte Carlo simulation.

References

- Alaton, P., Djehiche, B., & Stillberger, D. (2002). On modeling and pricing weather derivatives. Applied Mathematical Finance, 9(1), 1–23. https://doi.org/10.1080/13504860210132897

- Alexander, S. (2019). Crop insurance schemes need better planning. Live mint. July 10, 2019. Retrieved from July 6, 2023 https://www.livemint.com/industry/agriculture/why-crop-insurance-needs-to-be-better-designed-1562741755465.html

- Alexandridis, K. A., & Zapranis, A. D. (2013). Pricing approaches of temperature derivatives. Weather Derivatives: Modelling and Pricing Weather-Related Risk, 55–85. https://doi.org/10.1007/978-1-4614-6071-8_4

- Bank, M., & Wiesner, R. (2010). The use of weather derivatives by small-and medium-sized enterprises: Reasons and obstacles. Journal of Small Business & Entrepreneurship, 23(4), 581–600. https://doi.org/10.1080/08276331.2010.10593503

- Barnett, B. J., & Mahul, O. (2007). Weather index insurance for agriculture and rural areas in lower-income countries. American Journal of Agricultural Economics, 89(5), 1241–1247. https://doi.org/10.1111/j.1467-8276.2007.01091.x

- Benth, F. E., & Benth, J. Š. (2007). The volatility of temperature and pricing of weather derivatives. Quantitative Finance, 7(5), 553–561. https://doi.org/10.1080/14697680601155334

- Benth, F. E., & Meyer-Brandis, T. (2009). The information premium for non-storable commodities. The Journal of Energy Markets, 2(3), 111–140. https://doi.org/10.21314/JEM.2009.021

- Benth, F. E., & Šaltytė‐Benth, J. (2005). Stochastic modelling of temperature variations with a view towards weather derivatives. Applied mathematical finance, 12(1), 53–85. https://www.duo.uio.no/bitstream/handle/10852/10324/1/stat-res-01-04.pdf

- Binswanger-Mkhize, H. P. (2012). Is there too much hype about index-based agricultural insurance? Journal of Development Studies, 48(2), 187–200. https://doi.org/10.1080/00220388.2011.625411

- Brockett, P. L., Goldens, L. L., Wen, M. M., & Yang, C. C. (2009). Pricing weather derivatives using the indifference pricing approach. North American Actuarial Journal, 13(3), 303–315. https://doi.org/10.1080/10920277.2009.10597556

- Broome, M. E. (1993). Integrative literature reviews for the development of concepts. In B. L. Rodgers & K. A. Knafl (Eds.), Concept development in nursing (2nd ed., pp. 231–250). W. B. Saunders.

- Budhathoki, N. K., Lassa, J. A., Pun, S., & Zander, K. K. (2019). Farmers’ interest and willingness-to-pay for index-based crop insurance in the lowlands of Nepal. Land Use Policy, 85, 1–10. https://doi.org/10.1016/j.landusepol.2019.03.029

- Caballero, R., Jewson, S., & Brix, A. (2002). Long memory in surface air temperature: detection, modeling, and application to weather derivative valuation. Climate Research, 21(2), 127–140. https://www.int-res.com/articles/cr2002/21/c021p127.pdf

- Campbell, S. D., & Diebold, F. X. (2005). Weather forecasting for weather derivatives. Journal of the American Statistical Association, 100(469), 6–16. https://doi.org/10.1198/016214504000001051

- Cao, M., & Wei, J. (2004). Weather derivatives valuation and market price of weather risk. Journal of Futures Markets: Futures, Options, and Other Derivative Products, 24(11), 1065–1089. https://doi.org/10.1002/fut.20122

- Centre for Science and Environment. (2016). Insuring agriculture in times of climate change: A scoping study on the role of agriculture insurance in protecting farmers of Asia and Africa from extreme weather events. Retrieved July 18, 2023. http___cdn.cseindia.org_attachments_0.06496100_1520415651_Report-on-Agricultural-Insurance.pdf.

- Clarke, D. J. (2016). A theory of rational demand for index insurance. American Economic Journal: Microeconomics, 8(1), 283-306. 283–306. https://doi.org/10.1257/mic.20140103

- Cole, S., Stein, D., & Tobacman, J. (2014). Dynamics of demand for index insurance: Evidence from a long-run field experiment. American Economic Review: Papers and Proceedings, 104(5), 284–290. https://doi.org/10.1257/aer.104.5.284

- Davis, M. (2001). Pricing weather derivatives by marginal value. Quantitative Finance, 1(3), 305–308. https://doi.org/10.1080/713665730

- Dercon, S. (2002). Income risk, coping strategies, and safety nets. The World Bank Research Observer, 17(2), 141–166. https://doi.org/10.1093/wbro/17.2.141

- Dercon, S., Hill, R. V., Clarke, D., Outes-Leon, I., & Taffesse, A. S. (2014). Offering rainfall insurance to informal insurance groups: Evidence from a field experiment in Ethiopia. Journal of Development Economics, 106, 132–143. https://doi.org/10.1016/j.jdeveco.2013.09.006

- Doms, J., Hirschauer, N., Marz, M., & Boettcher, F. (2018). Is the hedging efficiency of weather index insurance overrated? A farm-level analysis in regions with moderate natural conditions in Germany. Agricultural Finance Review, 78(3), 290–311. https://doi.org/10.1108/AFR-07-2017-0059

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133, 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

- Ederington, L. H. (1979). The hedging performance of the new futures markets. The Journal of Finance, 34(1), 157–170. https://doi.org/10.1111/j.1540-6261.1979.tb02077.x

- Esfahani, H., Tavasoli, K., & Jabbarzadeh, A. (2019). Big data and social media: A scientometrics analysis. International Journal of Data & Network Science, 3(3), 145–164. https://doi.org/10.5267/j.ijdns.2019.2.007

- Ghosh, R. K., Gupta, S., Singh, V., & Ward, P. S. (2021). Demand for crop insurance in developing countries: New evidence from India. Journal of Agricultural Economics, 72(1), 293–320. https://doi.org/10.1111/1477-9552.12403

- Giné, X., & Yang, D. (2009). Insurance, credit, and technology adoption: Field experimental evidence from Malawi. Journal of Development Economics, 89(1), 1–11. https://doi.org/10.1016/j.jdeveco.2008.09.007

- Groll, A., López-Cabrera, B., & Meyer-Brandis, T. (2016). A consistent two-factor model for pricing temperature derivatives. Energy Economics, 55, 112–126. https://doi.org/10.1016/j.eneco.2015.12.020

- Härdle, W. K., & Cabrera, B. L. (2012). The implied market price of weather risk. Applied mathematical finance, 19(1), 59–95. https://www.econstor.eu/bitstream/10419/25317/1/590227564.PDF

- Härdle, W. K., López Cabrera, B., Okhrin, O., & Wang, W. (2016). Localizing temperature risk. Journal of the American Statistical Association, 111(516), 1491–1508. https://doi.org/10.1080/01621459.2016.1180985

- Hazell, P., Sberro-Kessler, R., & Varangis, P. (2017). When and how should agricultural insurance be subsidized? Issues and good practices. World Bank. https://elibrary.worldbank.org/doi/abs/10.1596/31438

- Hell, P., Meyer-Brandis, T., & Rheinländer, T. (2012). Consistent factor models for temperature markets. International Journal of Theoretical and Applied Finance, 15(4), 1250027. https://doi.org/10.1142/S0219024912500276

- Hong, S. J., & Sohn, S. Y. (2013). Peer group analysis for introducing weather derivatives for a city. Expert Systems with Applications, 40(14), 5680–5687. https://doi.org/10.1016/j.eswa.2013.04.033

- Huang, H. H., Shiu, Y. M., & Lin, P. S. (2008). HDD and CDD option pricing with market price of weather risk for Taiwan. Journal of Futures Markets, 28(8), 790–814. https://doi.org/10.1002/fut.20337

- Jensen, N., & Barrett, C. (2017). Agricultural index insurance for development. Applied Economic Perspectives and Policy, 39(2), 199–219. https://doi.org/10.1093/aepp/ppw022

- Jewson, S., & Brix, A. (2005). Weather derivative valuation: The meteorological, statistical, financial and mathematical foundations. Cambridge University Press. https://doi.org/10.1017/CBO9780511493348

- Lazo, J. K., Lawson, M., Larsen, P. H., & Waldman, D. M. (2011). US economic sensitivity to weather variability. Bulletin of the American Meteorological Society, 92(6), 709–720. https://doi.org/10.1175/2011BAMS2928.1

- Liberati, A., Altman, D. G., Tetzlaff, J., Mulrow, C., Gøtzsche, P. C., Ioannidis, J. P. A., Clarke, M., Devereaux, P. J., Kleijnen, J., & Moher, D. (2009). The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. Annals of Internal Medicine, 151(4), W–65. https://doi.org/10.7326/0003-4819-151-4-200908180-00136

- Lichtenberg, E., & Iglesias, E. (2022). Index insurance and basis risk: A reconsideration. Journal of Development Economics, 158, 102883. https://doi.org/10.1016/j.jdeveco.2022.102883

- Mahul, O. (2001). Optimal insurance against climatic experience. American Journal of Agricultural Economics, 83(3), 593–604. https://doi.org/10.1111/0002-9092.00180

- McIntosh, C., Sarris, A., & Papadopoulos, F. (2013). Productivity, credit, risk, and the demand for weather index insurance in smallholder agriculture in Ethiopia. Agricultural Economics, 44(4–5), 399–417. https://doi.org/10.1111/agec.12024

- Miranda, M. J., & Farrin, K. (2012). Index insurance for developing countries. Applied Economic Perspectives and Policy, 34(3), 391–427. https://doi.org/10.1093/aepp/pps031

- Miranda, M., & Vedenov, D. V. (2001). Innovations in agricultural and natural disaster insurance. American Journal of Agricultural Economics, 83(3), 650–655. https://doi.org/10.1111/0002-9092.00185

- Musshoff, O., Odening, M., & Xu, W. (2011). Management of climate risks in agriculture–will weather derivatives permeate? Applied Economics, 43(9), 1067–1077. https://doi.org/10.1080/00036840802600210

- Odening, M., Mußhoff, O., & Xu, W. (2007). Analysis of rainfall derivatives using daily precipitation models: Opportunities and pitfalls. Agricultural Finance Review, 67(1), 135. https://www.researchgate.net/profile/Oliver-Musshoff/publication/227352509_Analysis_of_rainfall_derivatives_using_daily_precipitation_models_Opportunities_and_pitfalls/links/00b49521f7014eb3b0000000/Analysis-of-rainfall-derivatives-using-daily-precipitation-models-Opportunities-and-pitfalls.pdf

- Rejda, G. E., & McNamara, M. J. (2014). Principles of risk Management and insurance. Pearson Education.

- Richards, T. J., Manfredo, M. R., & Sanders, D. R. (2004). Pricing weather derivatives. American Journal of Agricultural Economics, 86(4), 1005–1017. https://doi.org/10.1111/j.0002-9092.2004.00649.x

- Seth, R., Ansari, V. A., & Datta, M. (2009). Weather‐risk hedging by farmers: An empirical study of willingness‐to‐pay in Rajasthan, India. The Journal of Risk Finance, 10(1), 54–66. https://doi.org/10.1108/15265940910924490

- Shirsath, P., Vyas, S., Aggarwal, P., & Rao, K. N. (2019). Designing weather index insurance of crops for the increased satisfaction of farmers, industry, and the government. Climate Risk Management, 25, 100189. https://doi.org/10.1016/j.crm.2019.100189

- Smith, V. H., & Goodwin, B. K. (1996). Crop insurance, moral hazard, and agricultural chemical use. American Journal of Agricultural Economics, 78(2), 428–438. https://doi.org/10.2307/1243714

- Smith, V. H., & Watts, M. (2019). Index-based agricultural insurance in developing countries: Feasibility, scalability, and sustainability. Gates Open Res, 3(65), 65. https://gatesopenresearch.org/documents/3-65

- Snyder, H. (2019). Literature review as a research methodology: An overview and guidelines. Journal of Business Research, 104, 333–339. https://doi.org/10.1016/j.jbusres.2019.07.039

- Sun, B., & van Kooten, G. C. (2015). Financial weather derivatives for corn production in Northern China: A comparison of pricing methods. Journal of Empirical Finance, 32, 201–209. https://doi.org/10.1016/j.jempfin.2015.03.014

- Toronto, C. E., & Remington, R. (Eds.). (2020). A step-by-step guide to conducting an integrative review. Springer International Publishing. https://doi.org/10.1007/978-3-030-37504-1_1

- Torraco, R. J. (2005). Writing integrative literature reviews: Guidelines and examples. Human Resource Development Review, 4(3), 356–367. https://doi.org/10.1177/1534484305278283

- Turvey, C. G. (2001). The pricing of degree‐day weather options. Agricultural Finance Review, 65(1), 59–85. https://doi.org/10.1108/00214660580001167

- Turvey, C. G. (2001). Weather derivatives for specific event risks in agriculture. Applied Economic Perspectives and Policy, 23(2), 333–351. http://wiki.leg.ufpr.br/lib/exe/fetch.php/projetos:procad:turvey_2001.pdf

- Vedenov, D. V., & Barnett, B. J. (2004). Efficiency of weather derivatives as primary crop insurance instruments. Journal of Agricultural and Resource Economics, 387–403. https://www.jstor.org/stable/40987240

- Wang, H. H., Liu, L., Ortega, D. L., Jiang, Y., & Zheng, Q. (2020). Are smallholder farmers willing to pay for different types of crop insurance? An application of labelled choice experiments to Chinese corn growers. The Geneva Papers on Risk and Insurance-Issues and Practice, 45(1), 86–110. https://doi.org/10.1057/s41288-019-00153-7

- Whittemore, R., & Knafl, K. (2005). The integrative review: Updated methodology. Journal of Advanced Nursing, 52(5), 546–553. https://doi.org/10.1111/j.1365-2648.2005.03621.x

- World Bank. (2011). Weather index insurance for agriculture: Guidance for development practitioners. Agriculture and rUral development discussion Paper 50, The World Bank. https://elibrary.worldbank.org/doi/abs/10.1596/26889.

- Yoo, S. (2003). Weather derivatives and seasonal forecast. Department of Applied Economics and Management, Cornell University.

- Yorks, L. (2008). What we know, what we don’t know, what we need to know—integrative literature reviews are research. Human Resource Development Review, 7(2), 139–141. https://doi.org/10.1177/1534484308316395

- Zapranis, A., & Alexandridis, A. (2008). Modelling the temperature time‐dependent speed of mean reversion in the context of weather derivatives pricing. Applied Mathematical Finance, 15(4), 355–386. https://doi.org/10.1080/13504860802006065

- Zapranis, A., & Alexandridis, A. (2009). Weather derivatives pricing: Modeling the seasonal residual variance of an Ornstein–Uhlenbeck temperature process with neural networks. Neurocomputing, 73(1–3), 37–48. https://doi.org/10.1016/j.neucom.2009.01.018

Annexures

Table A1. Commonalities and differences between weather derivatives and index insurance

Annexure A.2.The process flow chart of working of index insurance and weather derivatives in the agriculture sector.