?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Digital transformation remains a passion. Globally, science and technology are transforming businesses to make them more competitive and conducive to sustainable development. However, rapid advancements in financial technology have enabled financial institutions to steal customers from traditional banks, resulting in their demise. Consequently, this study employs the System GMM-two step estimator and data from 118 Chinese banks from 2014 to 2021 investigate the issue. Empirical evidence suggests that banks’ digital transformation has a negative impact on their profitability to some extent, but digital inclusive finance has enabled the bank to change its digital transformation behavior and enhance its operational performance. Therefore, banks must continue to strengthen their digital transformation by expanding online customer services, increasing the use of e-accounts and mobile applications, providing digital offline services, strengthening digital risk management and privacy and security controls, reducing customer psychological risk, and promoting financial inclusion. Financial inclusion should simultaneously achieve reduced financial exclusion of customers and increased financial literacy of customers. All these factors will help banks to maintain profitability by leveraging synergies with financial inclusion in the process of digital transformation.

1. Introduction

1.1. Research background

The UN’s “World Economic Situation and Prospects 2023” study predicts that global economic growth is expected to reach 1.9 percent, one of the lowest in decades. In the past century, economists have been delving deeply into the relationship between finance and the economy (Levine, Citation1997, Citation2005). Some economists argue that when the financial sector expands beyond a certain point, it may have detrimental effects on overall economic well-being Lucas (Citation1988). On the other hand, the financial sector is widely regarded as the central engine of economic growth (Berger et al., Citation2020). As stated by Bernanke (Citation2007), “We should always be mindful of the enormous economic benefits brought about by a robust and innovative financial sector.”

In the 1950s, the pioneers in the study of technical efficiency are Koopmans (Citation1951), Debreu (Citation1951) and Farrell (Citation1957). About Digital Transformation, Jafari-Sadeghi et al. (Citation2021), Tsou and Chen (Citation2023) agree that digital transformation is a revolutionary revolution that accelerates the activities, processes, and capacities of an organization. There is no currently accepted standard for the concept of digital transformation. As shown by the birth of the phrase “financial technology,” digital transformation may be seen as an extension of the continual development of financial technology, which represents the union of “finance” and “information technology.” (Jafari-Sadeghi et al., Citation2021; Nambisan et al., Citation2019) FinTech, at its heart, is the delivery of new and enhanced financial services via the use of technology. Utilizing science and technology, it increases and improves financial operations (Thakor, Citation2020). According to some academics, digital transformation is a combination of enterprise and IT transformation. Using digital transformation technology, the goal is to convert consumer information and data into trustworthy information for companies to make applicable decisions, as well as to build new business models adapted to client requests (Demlehner & Laumer, Citation2020; Tsou & Chen, Citation2023). In addition to technological change, some experts claim that digital transformation connects to the company itself. The digital transformation process cannot be completed just via the use of digital technologies. Additionally, the acquisition of digital skills of digital skills, digital strategy, digital culture, and digital talent is essential (Drechsler et al., Citation2020; Hinings et al., Citation2018).

Regarding the effects of digital transformation on the banking industry, there is currently no consensus. In the digital world, banks may more effectively employ technological tools to decrease costs and increase efficiency, so enhancing their own profitability (Del Gaudio et al., Citation2021; Huang, Citation2023; Lee et al., Citation2021; Peter et al., Citation2023; Prakash et al., Citation2021; Wang et al., Citation2021). There is other pertinent research that has shown that the advancement of technology does not benefit businesses (Do et al., Citation2022; Gupta et al., Citation2018). Digital transformation of banks can more effectively achieve finance inclusion, provide high-quality financial services to a wider customer base, and increase bank profits. In turn, the demand for finance inclusion may also push banks to carry out deeper digital transformation to reduce risks and improve profitability. This reminds us that digital transformation may be affected by financial inclusion, producing dynamic changes in profitability. This becomes the central idea of this study. Therefore, while digital transformation presents great opportunities, not all banks will be able to successfully realize this transformation. This calls for an in-depth study of the impact of digital transformation on bank profitability and whether financial inclusion plays a role in moderating the impact on profitability.

1.2. Research significance

Digital transformation is the primary technique for increasing organizational efficacy, decreasing costs, and supporting long-term economic development. More digital transformation means that firms will be able to operate for a prolonged length of time in a hard economic environment while simultaneously providing more value, supporting the national economy, and improving the lives of people. In essence, most countries are aware of the state of digital transformation, which has greatly assisted firms seeking long-term development in the face of intense competition in avoiding bankruptcy and layoffs. Commercial banks must embrace digital transformation if they want to boost their overall strength and promote sustainable growth. Numerous banks have raised digital transformation to the rank of a strategic project and continue to do comprehensive, relevant, and substantial research in this area.

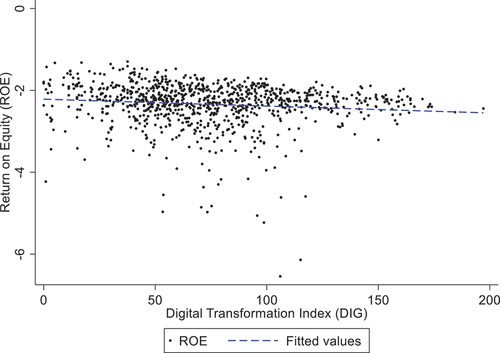

Despite hints of digital transformation beneficial role in improving profitability, it doesn’t sound that effective and even exist negative (Figure ). Digital transformation may increase the efficiency and customer happiness of banks, but it does not inevitably increase their profitability. First, banks may be required to invest substantial funds and resources in digital transformation, which may temporarily diminish their profitability. Second, banks may meet hurdles such as cybersecurity and data privacy problems (Johri et al., Citation2023; Lallie et al., Citation2021), as well as the necessity to reorganize business models and corporate cultures while undergoing digital transformation. These constraints may hinder the profitability of a bank. In addition, other elements, such as risk, market climate, competition, and laws and rules, may also impact banks’ profitability. Even when banks undertake digital transformation, these issues may impact their profitability. Financial inclusion, as one of the externalities of digital transformation, may moderate the direct effect of digital transformation on bank profitability. Through digital transformation, finance inclusion can be improved, and it is a breakthrough tool for the development of finance inclusion (Afawubo et al., Citation2020; Sodokin et al., Citation2022). In turn, finance inclusion will also promote digital transformation of banks, reduce risks and increase profits (Demirgüç-Kunt et al., Citation2020; Marcelin et al., Citation2022). Current literature study focuses on the effect of financial technology on bank profitability when internal and external of financial technology are separated. Therefore, this essay will integrate internal and external influences to examine the impact of digital transformation on profitability, fill a gap in the literature, and offer banks valuable reference material.

Figure 1. Digital transformation (DIG) vs ROE.

This study uses the organizational structure shown below. Part 2 is a literature review and Part 3 presents the research methodology. Part 4 presents the results of the study, Part 5 the limitations and policy implementation of this study, and Part 6 the conclusion.

2. Literature review

Currently, digital transformation has become an urgent strategic task for traditional commercial banks (Tan et al., Citation2022; Wang et al., Citation2021; Xie & Wang, Citation2023). The digital transformation of banks is essentially a financial innovation driven by technology (Abdulquadri et al., Citation2021; Do et al., Citation2022; Du & Liu, Citation2022; Vial, Citation2019). Digital technology only offers the possibility of success. If done right, this will be promising. If it’s not done well, it’s even worse (Huang, Citation2021). Scholars generally study the impact of internal financial technology and external financial technology on bank profitability separately, and there is no consensus.

From an internal financial technology perspective, one perspective posits that the digital revolution has positively influenced bank profitability (Bandara, Citation2016; Broeders & Khanna, Citation2015; Mylonakis, Citation2018). More and more commercial banks are beginning to use financial technology within their organizations to transform and upgrade, thereby improving their operating performance (Li et al., Citation2017). Technologies such as mobile information communication and big data analysis can enhance operational performance in traditional commercial banking (Yang & Liu, Citation2018). FinTech applications can reshape traditional banking by reducing costs and increasing efficiency (Zhang et al., Citation2019). As a new product of the bank’s digital transformation driven by business innovation and product innovation, Mobile Financial Services has brought long-tail customer groups to the bank and improved the bank’s business coverage and profitability (Jagtiani & Lemieux, Citation2018; Konte & Tetteh, Citation2023; Shaikh et al., Citation2023). On the contrary, some researchers propose that the digital revolution has negatively impacted bank profitability (Elfeituri, Citation2018; Li & Jia, Citation2018). Beccalli (Citation2007) posits that the relationship between investments in new technology and bank profitability is tenuous, and Hajli et al. (Citation2015) highlight that the benefits of digital transformation-driven growth are limited to select businesses. Kriebel and Debener (Citation2019) suggest that efficiency improvements may take several years to materialize, with difficulties in digital transformation potentially leading to declines in efficiency and profitability. As Cao et al. (Citation2022) state, not all banks are successful in technology investments and implementations.

When discussing the impact, academics exclusively consider the effects of direct financial technology deployment. Although it may improve profitability in future trends, there are other considerations to consider, such as the inherent dangers of the technology (Mishchenko et al., Citation2021). In mobile financial services, for instance, when clients input their cell phone numbers improperly, privacy problems may be compromised or transactions may fail, negatively impacting the customer experience. Integrity issues, monetary crime risks (such as terrorist financing), financial crime risks (such as data breaches and digital financial services debt), and privacy and data regulations are further examples (Ebong & Babu, Citation2020; Johri et al., Citation2023). All these factors will affect bank profitability. Based on the literature, we propose the following hypotheses:

Hypothesis 1:

Digital transformation has a negative impact on bank profitability to a certain extent.

From the perspective of external financial technology, most scholars mainly study the impact of external inclusive finance on bank profits. Financial inclusion refers to the process of providing basic financial services to marginalized and excluded members of society and ensuring that vulnerable groups in society have access to sufficient lines of credit at a reasonable cost (Malladi et al., Citation2021; Rumbogo et al., Citation2021). Regional disparities in traditional commercial banks’ distribution of financial resources, which can be addressed through digital financial inclusion (Vincent & Cull, Citation2011). Leveraging digital technology in the financial sector can substantially reduce the cost of financial services, extend financial coverage, and increase penetration (Das & Das, Citation2020). Wang and Xie (Citation2021) also argue that regional digital finance expansion enhances innovation among commercial banks, promoting product and management innovations. Through digital channels, banks can reach these customers more easily and expand their customer base. This means more savings accounts, loan applications and other financial products, thus increasing potential profit opportunities. As financial inclusion grows, the amount of risk carried by commercial banks will stabilize and the development of inclusive finance allows more poor people and small businesses in need of lending to resolve their financial difficulties in a stable manner (Ahamed & Mallick, Citation2019; Demirgüç-Kunt et al., Citation2020; Marcelin et al., Citation2022). For mobile financial services, through digital financial inclusion, stronger identity verification, better customer data management and more timely notifications can be achieved to reduce transaction issues caused by entering incorrect mobile phone numbers. These measures have indirectly improved the bank’s profitability. Based on the literature, we propose the following hypotheses:

Hypothesis 2:

Digital inclusive finance plays a moderation role in mitigating the negative impact of digital transformation on bank profitability.

Some scholars have also conducted research on the factors that affect bank profitability. Asset liability management emerges as a crucial determinant (Owusu & Alhassan, Citation2021), and the size of a bank is seen as a significant predictor of performance (Adelopo et al., Citation2018). Capital adequacy ratios help banks mitigate operational risks cost-effectively (Tecles & Tabak, Citation2010), and non-interest income enhances profitability (Abedifar et al., Citation2018). Wahyudin et al. (Citation2021) find that net interest margin has a positive and significant impact on profitability.

Previous studies have shown that digital transformation plays a positive and significant positive role in improving bank performance (Huang, Citation2023; Khattak et al., Citation2023; Mirza et al., Citation2023; Xie & Wang, Citation2023). However, our study focuses more on the moderating role of financial inclusion in the relationship between banks’ digital transformation and bank performance than previous studies. This research perspective is different from the work of Guo and Zhu (Citation2022), Lu et al. (Citation2023), Guo et al. (Citation2023). None of the above literature has examined the impact on bank profitability from the perspective of combining internal digital transformation and external financial inclusion. In contrast, our study finds that financial inclusion plays a key role between digital transformation and bank performance, which provides a new perspective to previous studies. This suggests that the successful implementation of digital transformation requires not only consideration of technological factors, but also a focus on financial inclusion measures that ensure that broader social groups can benefit.

Therefore, our study distinguishes itself from prior research on the topic in two notable ways, thereby addressing a critical gap in the existing body of knowledge.

First, none of the earlier research on the impact of digital transformation on business performance provided quantifiable empirical data. Current research primarily relies on case studies. For instance, Mirković et al. (Citation2019) illustrate the example of DBS Bank in Singapore, a renowned leader in digital transformation and considered one of the world’s premier digital banks. Second, when assessing the influence of digital technology on profitability, many researchers have examined internal digital transformation and external financial inclusion development as separate entities. However, banks do not operate in isolation; they require both internal and external collaborations to enhance their efficiency. This article bridges the gap by integrating research on banks’ internal digital transformation with the growth of external inclusive finance, offering a more comprehensive perspective and valuable reference points for businesses.

3. Methodology

3.1. Model specification

According to the long-tail theory Anderson (Citation2004), long-term accumulation and development, the market composed of products with few sales volume may exceed the mainstream market in terms of market size, and the huge demand will bring considerable benefits to enterprises. 20% of the large customers of commercial banks create 80% of the bank’s revenue, but the remaining 80% of small customers should also attract the attention of banks, which can be improved through the development of financial technology. Commercial banks may employ financial technology to rebuild financial value and produce more tailored financial goods and services for typical client groups, therefore enhancing their customers’ experience and happiness over time and generating greater profit margins. Inevitably, digital technology will influence the evolution of commercial banks. This point of view can obtain a certain theoretical basis and support through the theory of financial innovation. The theories of financial profitability and corporate profitability are relevant to the banking sector as well. In the 1990 Harvard Business Review article “Enterprise Core Competence,” it was said that the core competitiveness of organizations is to allow firms to achieve more rapid growth while continually decreasing their costs, so that their own costs are lower than those of their rivals. If these two points are achieved, the probability of the company’s acquisition of core competitiveness will be greatly increased. According to the IT capability view, a company’s IT capability determines how effectively it can organize and integrate its internal and external resources as well as how simple it is to gain ongoing comparative advantages in market competition, all of which contribute to a higher level of business performance (Bharadwaj, Citation2000). These talents may be used by more efficient businesses to save expenses and become cost leaders in their sector (Barney, Citation1991). These ideas may give a stronger theoretical foundation for the link between investment in digital transformation and profitability. The following is a broad representation of the hypothesis’ structure:

where PR is ROE, Y is degree of digital transformation (DIG, DIGS, DIGM, DIGB) and Z is an indicator of all the other influencing variables. Y*INDEX indicates that firms are not independent entities, and the variety of their external environment may also contribute to variances in business innovation. To date, however, it has not been thoroughly debated whether technological advancement in the external environment encourages digital development in the same way that it encourages innovation in conventional firms. This is due to the fact that current research frequently considers technical growth to be uniform across domains (DeYoung & Hasan, Citation1998; Wang & Xie, Citation2021). The digital financial business model discussed in this article has a super-geographical service scope, but its development degree is still impacted by geospatial variables, and the amount of digital financial development in various locations varies (Guo et al., Citation2020). This article explores the impact of digital transformation on the profitability of commercial banks in a geographically varied scenario. Using the methodologies outlined in the literature, I will include an interactive project into the PR equation: DIG*INDEX. We predict that the interaction item predominantly determines the impact of the digital financial sector in the region when commercial banks undergo digital transformation, and we want to investigate the effect of the interaction item on ROE. Therefore, we get the following model: Based on what we have learnt from the literature, we may alter EquationEquation (1)(1)

(1) to read:

where INDEX, SIZE, LEV, NIM, NI, CAR represent that financial inclusion index (City), bank size, assets and liabilities, net interest margin, proportion of non-interest income, capital adequacy ratio, respectively. This part will focus on the topic of digital transformation and its link to bank performance since that is the primary objective of this study. The estimating model may be rewritten as follows:

and

are parameters to be estimated.

refers to bank and

denotes time. Years capture a vector of time dummies.

is an individual characteristic that does not change with time,

is a random error item. In this study, we use a method called “panel estimation” to figure out Eq (3). Panel data models are favoured over other models owing to their many advantages, such as their capacity to compensate for variances between banks at the individual level, their abundance of supplementary information and flexibility, and their low degree of variable overlap (Baltagi, Citation2008). This research use system generalised moment estimation to calculate the model’s parameters since it is more effective than differential generalised moment estimation. Phan et al. (Citation2020) establish a dynamic panel model by incorporating the first-order lag items of the proxy variables that measure commercial bank performance into explanatory variables. This research used the system generalised moment estimation (System GMM-two step) approach to examine the influence of digital transformation on operational performance, since the operating performance of commercial banks exhibits temporal continuity and may be susceptible to endogenous challenges.

On the right side of the dynamic panel model are dependent variables whose values have evolved through time. are parameters to be estimated. Where

is the coefficient of the lagged dependent variable.

As profitability metrics for commercial banks, most current mainstream academic research favors return on total assets (ROA, Return on Assets) or return on net assets (ROE, Return on Equity). In this paper, return on equity (ROE) is selected as the explained variable.

Banks have historically used various ratios to assess the strength of profitability. Among them, ROE is more widely accepted because of its simple and intuitive characteristics. According to relevant research, there are several elements that influence the profitability of banks. Borio and Gambacorta (Citation2017) discovered in their empirical analysis of commercial bank profitability that asset size, financial innovation capabilities, and risk tolerance all have a role. Karakaya and Er (Citation2013) show that asset size, cost-to-income ratio, and non-performing loan ratio have the most obvious impact on the profitability of commercial banks. Lu et al. (Citation2023) take listed banks as samples, the impact of internal competitive pressure calculated by Lerner index and external competitive impact calculated by digital financial inclusion index on the digital transformation of commercial banks shows that: internal competitive pressure and the impact of external competition will significantly prompt commercial banks to adopt digital transformation strategies. Meslier et al. (Citation2014) further point out that the financial innovation of commercial banks in developing countries is significantly positively correlated with the risk-adjusted profitability of the banks themselves. Wang and Xie (Citation2021) use the digital financial coverage index constructed based on the data of Ant Financial Services explores the impact of external digital financial development on the digital innovation behavior of traditional commercial banks and its mechanism, Behavior has a positive impact.

3.2. Estimation technique

This essay will use the GMM (generalized moment estimation) regression model. In several economic models, explanatory factors may be associated with error terms, leading to endogeneity issues. Thus, choices about digital transformation may be influenced by unobservable variables that also influence bank profitability. GMM is a robust estimating technique that can successfully address endogeneity issues. Using instrumental variables (IV), it may resolve the endogeneity issue, allowing for a more precise estimation of the effect of digital transformation on profitability. This study’s data consists of dynamic panel data. Our data collection includes several time points and observation units. GMM is an excellent estimating approach. It is capable of handling single fixed effects in panel data and permits the explanatory factors to become lagged dependent variables. When evaluating panel data, GMM models can often manage difficulties such as heteroskedasticity and serial correlation. By considering these factors, GMM models may provide more accurate estimations. The GMM estimator may be implemented in either a one-step or two-step format, giving users a choice between the two. Since the two-step estimator uses optimum weighting matrices, it has the potential to provide conclusions that are theoretically capable of being more accurate than those produced by the one-step estimator. Consequently, we use the two-step procedure. Two types of specification tests, the Hansen test, and the serial correlation test, determine whether or not the GMM estimator is dependable. If the Hansen test for over-identifying limits does not reject the null hypothesis, then the instruments are reliable, and the model is well described. Additionally, the GMM estimator permits the presence of first order serial correlation, often known as AR(1). However, the absence of second order serial correlation, commonly known as AR(2), is essential for the GMM estimator to be consistent (Subramaniam & Masron, Citation2021).

3.3. Data source

The balanced panel data of 118 commercial banks in my nation from 2014 to 2021 is used as the study sample in this work. The digital transformation index of this work constructs an index system using the three commercial bank dimensions, and it utilizes the digital transformation index of the commercial banks affiliated with Peking University (Xie & Wang, Citation2023). Strategy digitalization index (DIGS), Business digitalization index (DIGB), Management digitalization index (DIGM). DIGS focuses on the degree to which a bank gives digital technology strategic consideration. It is calculated by tallying the number of times digital technology-related terms appear in the annual report of the bank. This enables DIGS to concentrate on the extent to which the bank pays strategic attention to digital technologies. DIGB examines the degree to which banks integrate digital technology into the financial services they provide. DIGM examine how banks use digital technology into their governance frameworks and organizational management (Xie & Wang, Citation2023). Regarding the impact of financial formats in various regions on the digital transformation of banks, finance index constructed by Ant Financial Services data are used to represent the impact of financial formats (Guo et al., Citation2020; Lu et al., Citation2023, Xie & Wang, Citation2023; Wang & Xie, Citation2021). Other indicator data are from Annual reports from CSMAR databases, bank-wide databases, World Bank, and commercial bank disclosures. To guarantee the accuracy and exhaustiveness of the data, some commercial banks that did not disclose information technology investment data in the annual report and missing data were automatically screened. To ensure the accuracy of the empirical results, all raw data were logarithmically processed to reduce heteroskedasticity. Systematic GMM two-step regression was run using Stata 17.

4. Empirical results

Table shows the definitions and sources of each variable. Table presents the descriptive statistics for the data in this investigation. The overall digital transformation degree index is significantly distributed between its lowest and maximum values, as indicated. The minimum value of DIG is 0, the maximum value is 197.10, while the subordinate branch The minimum value of DIGS is 0 and the maximum value is 532.90. There are some banks whose digital transformation degree levels are too high, and the degree of transformation is too low in some places.

Table 1. List of variables definition and source

Table 2. List of descriptive statistics

In addition, Table correlation study demonstrates that bank asset size (SIZE), net interest margin (NIM), Assets and liabilities (LEV) are positively correlated indicating that all bank indicators contribute to the bank’s operating efficiency. The findings of these indicators align with those of the relevant literature. Correlated with degree of digital transformation (DIG), inclusive Financial Bond Index (INDEX), and capital adequacy ratio (CAR) are adversely correlated. We conclude that the digital transformation of commercial banks has not considerably increased their overall profitability (Carlson et al., Citation2001; Hernando & Nieto, Citation2007; Sathye, Citation2005). The causes may include commercial banks lack of internal technological development and the external rivalry posed by new technology enterprises. First, commercial banks have made substantial investments in the nascent stage of creating financial technology, since they will certainly introduce high-tech employees if they want to boost technological investment, resulting in higher bank expenses. Second, commercial banks have been in existence for many years, their operation size is huge, and their platform system is upgraded slowly, resulting in a lag in profitability improvement. Thirdly, emergent financial technology businesses are expanding fast, eroding commercial banks’ profit margins. Serving customers who are difficult for conventional banks to reach has resulted in a massive client base.

Table 3. Correlation analysis

The empirical findings of the model (EquationEquation 4(4)

(4) ) using dynamic panel GMM are shown in Table . All the diagnostic tests point to the conclusion that the models that are being considered have accurate definitions; the Hansen test does not rule out the over-identification limitations; It is not possible to refute the existence of a first-order serial correlation, but it is possible to establish the absence of a second-order serial correlation. Given that the number of available instruments is less than the number of cross-section dimensions, the proliferation of instruments does not influence the estimate.

Table 4. Regression results of main analysis [DV: ROE]

Table displays the results of our investigation. Digital transformation and financial inclusion interact significantly, demonstrating that their combined influence increases the profitability of commercial banks. This is due to digital transformation which enables banks to reduce operating expenses, increase efficiency, and expand their service offerings by offering more online and mobile banking services. It facilitates the expansion of financial services to rural and low-income populations, thereby promoting financial inclusion. In addition, digital transformation allows banks to innovate and provide new financial products and services to meet the needs of various consumer segments. Among them are mobile payments, peer-to-peer lending systems, and virtual currencies. Most importantly, digital transformation enables banks to monitor and manage risks, such as fraud and credit risk more effectively. This contributes to the financial system’s security and stability.

In turn, financial inclusion provides banks with a large customer base, allowing them to serve a greater number of long-tail consumers and generate potentially lucrative opportunities. At the same time, banks can reduce losses from customer default risk by analyzing consumer profiles based on massive customer data. This dual effect greatly increases the profitability of banks. Financial inclusion can help banks bridge the digital divide and provide convenient digital financial services to everyone in China’s large market. This will make banks more socially responsible, increase their customer base, and enable sustainable growth. This study illustrates the relationship between digital transformation and financial inclusion in the banking industry, highlighting potential synergies that could increase profitability. In addition, it implies that continued investments and strategies in these areas may benefit additional institutions. Hypothesis 2 holds.

In addition, without considering any moderating variables, the degree of digital transformation of commercial banks is significantly negatively correlated with the return on net assets at the level of 1%, and the negative coefficient indicates that for every 1% increase in the level of digitalization of commercial banks, the return on net assets will decrease by 4.168%, which is consistent with the reasons described in the previous section. At present, China’s digital transformation is still in the primary stage and there is a lag. The lack of endogenous momentum is not conducive to the growth of bank profitability. At the same time, digital transformation consumes huge costs in the early stage and the risks encountered are numerous, which contribute to the decline of bank profitability. Hypothesis 1 holds.

Columns (2) to (4) show the impact of digital transformation of business, management and strategy on bank profitability. Operational digital transformation is significantly positively at the 1 % level correlated with the moderating effect of financial inclusion. This also suggests that commercial banks should continue to increase business support for digital transformation of banks to target long-tail customers through digitization to compete with other FinTech and reduce the consequences of external competition. Management digitization and strategy digitization are not significant, in the context of financial inclusion. Partly reason is digital transformations of corporate management and strategy have indirect impacts on business operations. When a company’s profitability and viability are in jeopardy, firms are more likely to priorities rapidly growing revenue streams and strengthen their competitiveness via the closely related digital transformation of the organization. The result is a minor cushion against shocks in the financial industry. Moreover, strategic digital transformation is a top-down shift, including organizational structure, corporate culture, etc., so the moderation of financial inclusion is not obvious and still takes a long time to become apparent. Digitalization at the strategic and management levels offers a little buffer, but banks must continue to increase their digitalization-focused strategy and management awareness (Xie & Wang, Citation2023).

4.1. Heterogeneity analysis

While this study employed the GMM model to explore the main relationships, we encountered certain limitations in conducting heterogeneity analysis due to a small sample size and a relatively large number of instrumental variables. In our endeavor to gain insights into potential sources of heterogeneity, we opted to conduct preliminary explorations using the fixed effects model. Despite not being an ideal solution, the fixed effects model can still offer valuable insights, particularly in cases of limited sample size, aiding in our preliminary understanding of potential variations among different subgroups. However, considering these limitations, we will expand the sample size in future research endeavors to facilitate more accurate and robust analyses of heterogeneity. Next, we will analyze the heterogeneity of the total sample according to the size classification of the total asset and the digital transformation index, to see if the interaction effects differ between samples, if any. The classification is based on the average of the total assets and the digital transformation index.

Table shows that in the subsample, banks with larger total assets show that business digital transformation and strategic digital transformation have a significantly positive impact on bank profitability under the adjustment of finance inclusion. For banks with smaller total assets, only the interaction term between management digital transformation and inclusive finance has a significant positive impact on bank profitability. The reason for this is that larger banks typically have more resources and market share, and therefore may have taken a more holistic and strategic approach to digital transformation. They may have better met the needs of different customer segments, especially those with limited access to financial services, by investing in highly innovative digital solutions, expanding FinTech partnerships, and introducing a wider variety of financial products and services. This may have led to significant positive effects of operational digital transformation and strategic digital transformation in the area of financial inclusion, with a positive impact on profitability. Comparatively, smaller banks may be somewhat constrained in terms of resources and market share, and therefore may be more focused on improving internal management efficiencies and reducing costs. While managing digital transformation may help them improve operational efficiency, due to their smaller size, they may not have sufficient resources to pursue a more comprehensive digital strategy, for example, launching new digital products or expanding their market share. Therefore, among small banks, only the interaction term between managing digital transformation and financial inclusion has a significant positive impact on profitability, while other digital transformation may not have a significant impact on profitability.

Table 5. Regression results of subsample analysis [DV: ROE]

Table examines the impact of the financial inclusion interaction on banks with a high and low digital transformation. The analysis demonstrates that for banks with a high DIG, DIGINDEX has a significant positive effect on ROE. DIGBINDEX has a significant positive effect on ROE. For banks with lower digital transformation indexes, DIGINDEX is not significant, while both sub-indices DIGBINDEX and DIGSINDEX are significant. This is because highly digitized banking institutions seem to be better at leveraging better value in concert with financial inclusion. Banks can serve low-income and poor customers through digital services that are more accessible, affordable and personalized. Financial inclusion in turn pushes banks faster to continue their digital transformation. For highly digitized banks, the interaction term between business digital transformation and financial inclusion significantly shows that digitalization is more than just a technological update; it also improves business processes, introduces new products and services, and helps banks get closer to the goal of financial inclusion.

Table 6. Regression results of subsample analysis [DV: ROE]

Banks with lower levels of digital transformation may still be in the early stages of the digitization process and have yet to see synergies between technology and financial inclusion. However, there are still substantial interactions between financial inclusion and the sub-indicators of operational and strategic digitization. This is because, despite the overall low level of digitization, some banks that are just beginning their digital transformation may have started to offer specialized financial products and services to particular markets (e.g. low-income earners or marginalized people). A digitally simplified version of the account-opening process can win over customers who find the standard account-opening process too time-consuming and labor-intensive. In addition, strategic digitization enables financial institutions to reallocate resources and experiment more quickly with new inclusive financial business models. Therefore, even if banks are not highly digitally transformed, they will make appropriate changes in certain areas to respond to market changes.

4.2. Robustness check

In addition to the overall index of digital financial inclusion, the Beijing Inclusiveness Index includes the breadth of digital financial coverage, the depth of digital financial use, and the degree of digitalization of financial inclusion. In this study, sub-indices are utilized in lieu of interaction items, and demonstrates that the findings of each variable are consistent with those of the main test and pass the robustness test. Next, we retested the bank’s profitability using return on total assets (ROA) rather than return on equity (ROE). The findings demonstrated that each variable’s results were consistent with those of the main test, passing the robustness test.

5. Limitation of the study and policy implications

Our study examines digital transformation and bank profitability using a GMM model. This model can handle endpoint problems and work with panel and time series data. We must consider our study’s limitations. Due to the small sample size, our results may not be representative. Due to limited extrapolation, the findings should be interpreted and applied with caution. We used a fixed effects model to address heterogeneity, but we may have missed some factors. Psychological risk factors and customer satisfaction surveys were also excluded from our study. These factors may affect digital transformation and bank performance, but data limitations prevented us from analyzing them. Finally, our Digital Transformation Index only covers 2021, and rapid digital changes may cause future trends to change. Therefore, time factors must be carefully considered when interpreting study results.

While this study provides important insights into the relationship between digital transformation and bank performance, there are still many directions for future research that could further expand knowledge in this area. The role of financial inclusion could be the focus of future research. Further research could delve into the impact of different financial inclusion policies on digital banking and examine how these policies can be optimized to facilitate the spread of digital financial services. The impact of digital transformation could also be studied by incorporating psychological risk factors. To drive the digital transformation of banks more effectively, this paper offers the following recommendations:

The expansion of people’s access to financial services is inextricably linked to the promotion of digital financial services; therefore, policymakers should increase their support for this economic sector. This would not only increase the bank’s earnings, but it would also help more individuals become economically integrated. Smaller financial institutions may require additional skills and face additional obstacles during the digital transformation process. Governments and regulators should consider providing small banks with specialized technical and financial assistance in order to facilitate their digital transformation. Large banks should be incentivized to support innovative digital finance projects, particularly those aimed at underserved communities and geographically dispersed populations, through the establishment of specialized funds and the formation of partnerships with FinTech companies. Additionally, policymakers should promote financial education to improve financial literacy, reduce psychological risk factors for customers, and ensure that all customers have access to, understand, and can safely use digital financial services. Ensuring that customers are not exposed to unwarranted financial risks as a result of utilizing the aforementioned services necessitates a further crucial step: enhancing consumer protection. In light of the rapid development of digital transformation and financial inclusion, governments and regulators should establish feedback mechanisms to evaluate the effectiveness of pertinent policies and make any necessary adjustments.

6. Conclusion

We collected data from 118 Chinese commercial banks from 2014 to 2021 to determine how digital transformation affects profitability. We empirically investigate digital transformation using long-tail theory, financial innovation theory, and a two-step GMM model. First, digital transformation reduces the profitability of commercial banks to some extent. Second, the interaction term between digital transformation and digital financial inclusion is positive, indicating that financial inclusion affects digitalization to a certain extent thereby increasing bank profitability. Third, the heterogeneity analysis using the fixed-effects model shows that banks with high digital transformation indexes interact more with financial inclusion.

The above findings show that financial inclusion bridges digital transformation and bank performance. The development of financial inclusion is crucial for the digital transformation of banks. Banks reach more customers through digital transformation, especially those without financial services. Utilizing digital technologies to enhance data security and privacy protection to safeguard customer data and overcome customer psychological risk factors. Prevent network outage failures that result in failed transactions and provide digital offline services. At the same time, focusing on financial inclusion ensures that different social groups have access to digital financial services. Narrow the digital divide, enhance financial literacy, improve financial literacy, overcome financial exclusion, and provide digital financial tools to marginalized groups. To enhance the overall competitiveness of banks, it is important to synergize the dual effects of digital transformation and financial inclusion.

Code availability (software application or custom code)

The custom code and/or software application generated during and/or analyzed during the current study are the data analysis is run with STATA 17 and the data results are output, and the running code can be obtained from the corresponding author separately.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The datasets generated during and/or analyzed during the current study are available.

Financial data of commercial banks can be obtained through CSMAR: http://www.gtarsc.com/#/index

China Money Network Rating Report: https://www.chinamoney.com.cn/

Digital Transformation Index of commercial banks can be obtained through Peking University Digital Finance Research Center. [email protected]; [email protected]

References

- Abdulquadri, A., Mogaji, E., Kieu, T. A., & Nguyen, N. P. (2021). Digital transformation in financial services provision: A Nigerian perspective to the adoption of chatbot. Journal of Enterprising Communities: People and Places in the Global Economy, 15(2), 258–22. https://doi.org/10.1108/JEC-06-2020-0126

- Abedifar, P., Molyneux, P., & Tarazi, A. (2018). Non-interest income and bank lending. Journal of Banking & Finance, 87, 411–426. https://doi.org/10.1016/j.jbankfin.2017.11.003

- Adelopo, I., Lloydking, R., & Tauringana, V. (2018). Determinants of bank profitability before, during, and after the financial crisis. International Journal of Managerial Finance, 14(4), 378–398. https://doi.org/10.1108/IJMF-07-2017-0148

- Afawubo, K., Couchoro, M. K., Agbaglah, M., & Gbandi, T. (2020). Mobile money adoption and households’ vulnerability to shocks: Evidence from Togo. Applied Economics, 52(10), 1141–1162. https://doi.org/10.1080/00036846.2019.1659496

- Ahamed, M. M., & Mallick, S. K. (2019). Is financial inclusion good for bank stability? International evidence. Journal of Economic Behavior & Organization, 157, 403–427. https://doi.org/10.1016/j.jebo.2017.07.027

- Anderson, C. (2004). The long tail. Wired Outubro. Available: http://www.wired.com/wired/archive/12.10/tail.html

- Baltagi, B. H. (2008). Forecasting with panel data. Journal of Forecasting, 27(2), 153–173. https://doi.org/10.1002/for.1047

- Bandara, H. H. (2016). Digital banking: Enhancing customer value. Proceedings of the 28th Anniversary Convention (pp. 123–133).

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Beccalli, E. (2007). Does IT investment improve bank performance? Evidence from Europe. Journal of Banking & Finance, 31(7), 2205–2230. https://doi.org/10.1016/j.jbankfin.2006.10.022

- Berger, A. N., Molyneux, P., & Wilson, J. O. (2020). Banks and the real economy: An assessment of the research. Journal of Corporate Finance, 62, 101513. https://doi.org/10.1016/j.jcorpfin.2019.101513

- Bernanke, B. (2007). Regulation and financial innovation. Board of Governors of the Federal Reserve System (US).

- Bharadwaj, A. S. (2000). A resource-based perspective on information technology capability and firm performance: An empirical investigation. MIS Quarterly, 24(1), 169–196. https://doi.org/10.2307/3250983

- Borio, C., & Gambacorta, L. (2017). Monetary policy and bank lending in a low interest rate environment: Diminishing effectiveness? Journal of Macroeconomics, 54, 217–231. https://doi.org/10.1016/j.jmacro.2017.02.005

- Broeders, H., & Khanna, S. (2015). Strategic choices for banks in the digital age. McKinsey and Company, 7. https://www.mckinsey.com/industries/financial-services/our-insights/strategic-choices-for-banks-in-the-digital-age

- Cao, T., Cook, W. D., & Kristal, M. M. (2022). Has the technological investment been worth it? Assessing the aggregate efficiency of non-homogeneous bank holding companies in the digital age. Technological Forecasting and Social Change, 178, 121576. https://doi.org/10.1016/j.techfore.2022.121576

- Carlson, J., Furst, K., Lang, W. W., & Nolle, D. E. (2001). Internet banking: Market developments and regulatory issues. In Manuscript, the society of government economists. Washington DC.

- Das, A., & Das, D. (2020). Perception, adoption, and pattern of usage of FinTech services by bank customers: Evidences from Hojai District of Assam. Emerging Economy Studies, 6(1), 7–22. https://doi.org/10.1177/2394901520907728

- Debreu, G. (1951). The coefficient of resource utilization. Econometrica: Journal of the Econometric Society, 19(3), 273–292. https://doi.org/10.2307/1906814

- Del Gaudio, B. L., Porzio, C., Sampagnaro, G., & Verdoliva, V. (2021). How do mobile, internet and ICT diffusion affect the banking industry? An empirical analysis. European Management Journal, 39(3), 327–332. https://doi.org/10.1016/j.emj.2020.07.003

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2020). The global findex database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review, 34(Supplement_1), S2–S8. https://doi.org/10.1093/wber/lhz013

- Demlehner, Q., & Laumer, S. (2020). Why context matters: Explaining the digital transformation of the manufacturing industry and the role of the industry’s characteristics in it. Pacific Asia Journal of the Association for Information Systems, 12(3), 57–81. https://doi.org/10.17705/1pais.12303

- DeYoung, R., & Hasan, I. (1998). The performance of de novo commercial banks: A profit efficiency approach. Journal of Banking & Finance, 22(5), 565–587. https://doi.org/10.1016/S0378-4266(98)00025-9

- Do, T. D., Pham, H. A. T., Thalassinos, E. I., & Le, H. A. (2022). The impact of digital transformation on performance: Evidence from Vietnamese commercial banks. Journal of Risk and Financial Management, 15(1), 21. https://doi.org/10.3390/jrfm15010021

- Drechsler, K., Gregory, R., Wagner, H.-T., & Tumbas, S. (2020). At the crossroads between digital innovation and digital transformation. Communications of the Association for Information Systems, 47, 521–538. https://doi.org/10.17705/1CAIS.04723

- Du, L., & Liu, Z. (2022). The impact of digital finance on commercial banks’ credit risk and operating efficiency. Studies of International Finance, 6, 75–85. https://doi.org/10.16475/j.cnki.1006-1029.2022.06.004

- Ebong, J., & Babu, G. (2020). Demand for credit in high-density markets in Kampala: Application of digital lending and implication for product innovation. Journal of International Studies, 13(4), 295–313. https://doi.org/10.14254/2071-8330.2020/13-4/21

- Elfeituri, H. (2018). Market concentration, foreign ownership and determinants of bank financial performance: Evidence from MENA countries. Corporate Ownership & Control, 15(3), 9–22. https://doi.org/10.22495/cocv15i3art1

- Farrell, M. J. (1957). The measurement of productive efficiency. Journal of the Royal Statistical Society Series A (General), 120(3), 253–281. https://doi.org/10.2307/2343100

- Guo, F., Kong, T., & Wang, Q. (2020). Analysis of Internet finance spatial agglomeration effect: Evidence from Internet finance development index. Quarterly Journal of Economics, 19(4), 1401–1418.

- Guo, L., & Zhu, K. (2022). FinTech, bank risks, and business performance: From the perspective of inclusive finance. China Economic Transition= Dangdai Zhongguo Jingji Zhuanxing Yanjiu, 5(2), 242–261.

- Guo, F., Zhuang, X., & Wang, R. (2023). Bank digital transformation, exogenous FinTech and credit risk governance: Empirical test based on text mining and machine learning. Securities Market Herald, 4, 15–23. . https://kns.cnki.net/kcms/detail/44.1343.F.20230412.1204.004.html

- Gupta, S. D., Raychaudhuri, A., & Haldar, S. K. (2018). Information technology and profitability: Evidence from Indian banking sector. International Journal of Emerging Markets, 13(5), 1070–1087. https://doi.org/10.1108/IJoEM-06-2017-0211

- Hajli, M., Sims, J. M., & Ibragimov, V. (2015). Information technology (IT) productivity paradox in the 21st century. International Journal of Productivity & Performance Management, 64(4), 457–478. https://doi.org/10.1108/IJPPM-12-2012-0129

- Hassan, T. A., Hollander, S., Van Lent, L., & Tahoun, A. (2019). Firm-level political risk: Measurement and effects. The Quarterly Journal of Economics, 134(4), 2135–2202. https://doi.org/10.1093/qje/qjz021

- Hernando, I., & Nieto, M. J. (2007). Is the Internet delivery channel changing banks’ performance? The case of Spanish banks. Journal of Banking & Finance, 31(4), 1083–1099. https://doi.org/10.1016/j.jbankfin.2006.10.011

- Hinings, B., Gegenhuber, T., & Greenwood, R. (2018). Digital innovation and transformation: An institutional perspective. Information and Organization, 28(1), 52–61. https://doi.org/10.1016/j.infoandorg.2018.02.004

- Huang, Y. (2021). Several viewpoints on the innovation and development of China’s Digital Finance. Finance Forum, 26(11), 3–5+36. . https://doi.org/10.16529/j.cnki.11-4613/f.2021.11.001

- Huang, Z. (2023). Research on the impact of digital transformation of commercial banks on profitability. Proceedings of the SHS Web of Conferences, Les Ulis. EDP Sciences. https://doi.org/10.1051/shsconf/202316302015

- Jafari-Sadeghi, V., Garcia-Perez, A., Candelo, E., & Couturier, J. (2021). Exploring the impact of digital transformation on technology entrepreneurship and technological market expansion: The role of technology readiness, exploration and exploitation. Journal of Business Research, 124, 100–111. https://doi.org/10.1016/j.jbusres.2020.11.020

- Jagtiani, J., & Lemieux, C. (2018). Do FinTech lenders penetrate areas that are underserved by traditional banks? Journal of Economics and Business, 100, 43–54. https://doi.org/10.1016/j.jeconbus.2018.03.001

- Johri, A., Kumar, S., & Yan, Z. (2023). Exploring customer awareness towards their cyber security in the Kingdom of Saudi Arabia: A study in the era of banking digital transformation. Human Behavior and Emerging Technologies, 2023, 1–10. https://doi.org/10.1155/2023/2103442

- Karakaya, A., & Er, B. (2013). Noninterest (nonprofit) income and financial performance at Turkish commercial and participation banks. International Business Research, 6(1), 106. https://doi.org/10.5539/ibr.v6n1p106

- Khattak, M. A., Ali, M., Azmi, W., & Rizvi, S. A. R. (2023). Digital transformation, diversification and stability: What do we know about banks? Economic Analysis and Policy, 78, 122–132. https://doi.org/10.1016/j.eap.2023.03.004

- Konte, M., & Tetteh, G. K. (2023). Mobile money, traditional financial services and firm productivity in Africa. Small Business Economics, 60(2), 745–769. https://doi.org/10.1007/s11187-022-00613-w

- Koopmans, T. C. (1951). An analysis of production as an efficient combination of activities. Activity Analysis of Production and Allocation, 33–97. https://cir.nii.ac.jp/crid/1572824499992043008

- Kriebel, J., & Debener, J. (2019). The effect of digital transformation on bank performance. SSRN Electronic Journal, Available at SSRN 3461594. https://doi.org/10.2139/ssrn.3461594

- Lallie, H. S., Shepherd, L. A., Nurse, J. R., Erola, A., Epiphaniou, G., Maple, C., & Bellekens, X. (2021). Cyber security in the age of COVID-19: A timeline and analysis of cyber-crime and cyber-attacks during the pandemic. Computers & Security, 105, 102248. https://doi.org/10.1016/j.cose.2021.102248

- Lee, C.-C., Li, X., Yu, C.-H., & Zhao, J. (2021). Does FinTech innovation improve bank efficiency? Evidence from China’s banking industry. International Review of Economics & Finance, 74, 468–483. https://doi.org/10.1016/j.iref.2021.03.009

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688–726.

- Levine, R. (2005). Finance and growth: Theory and evidence. Handbook of Economic Growth, 1, 865–934. https://doi.org/10.1016/S1574-0684(05)01012-9

- Li, M., & Jia, S. (2018). Resource orchestration for innovation: The dual role of information technology. Technology Analysis & Strategic Management, 30(10), 1136–1147. https://doi.org/10.1080/09537325.2018.1443438

- Li, Y., Spigt, R., & Swinkels, L. (2017). The impact of FinTech start-ups on incumbent retail banks’ share prices. Financial Innovation, 3(1). https://doi.org/10.1186/s40854-017-0076-7

- Lucas, R. E., Jr. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22(1), 3–42. https://doi.org/10.1016/0304-3932(88)90168-7

- Lu, M., Sun, Z., & Liu, X. (2023). Internal Competitive Pressure or External Competitive Shock_——Research on the Motives of Digital Transformation of Commercial Banks. Dongyue tribune. https://kns.cnki.net/kcms/detail/37.1062.C.20230406.1729.032.html

- Malladi, C. M., Soni, R. K., & Srinivasan, S. (2021). Digital financial inclusion: Next frontiers—challenges and opportunities. CSI Transactions on ICT, 9(2), 127–134. https://doi.org/10.1007/s40012-021-00328-5

- Marcelin, I., Sun, W., Teclezion, M., & Junarsin, E. (2022). Financial inclusion and bank risk-taking: The effect of information sharing. Finance Research Letters, 50, 103182. https://doi.org/10.1016/j.frl.2022.103182

- Meslier, C., Tacneng, R., & Tarazi, A. (2014). Is bank income diversification beneficial? Evidence from an emerging economy. Journal of International Financial Markets, Institutions and Money, 31, 97–126. https://doi.org/10.1016/j.intfin.2014.03.007

- Mirković, V., Lukić, J., & Martin, V. (2019). Reshaping banking industry through digital transformation. Proceedings of the 6th International Scientific Conference - FINIZ 2019, Belgrade, Singidunum University, Serbia (pp. 31–36).

- Mirza, N., Umar, M., Afzal, A., & Firdousi, S. F. (2023). The role of FinTech in promoting green finance, and profitability: Evidence from the banking sector in the euro zone. Economic Analysis and Policy, 78, 33–40. https://doi.org/10.1016/j.eap.2023.02.001

- Mishchenko, S., Naumenkova, S., Mishchenko, V., & Dorofeiev, D. (2021). Innovation risk management in financial institutions. Investment Management & Financial Innovations, 18(1), 191–203. https://doi.org/10.21511/imfi.18(1).2021.16

- Mylonakis, J. (2018). Digital transformation of the Greek retail banking: An evaluation of systemic banks’ websites. Business Management and Strategy, 9(2), 117–128. https://doi.org/10.5296/bms.v9i2.14100

- Nambisan, S., Wright, M., & Feldman, M. (2019). The digital transformation of innovation and entrepreneurship: Progress, challenges and key themes. Research Policy, 48(8), 103773. https://doi.org/10.1016/j.respol.2019.03.018

- Owusu, F. B., & Alhassan, A. L. (2021). Asset-liability Management and bank profitability: Statistical cost accounting analysis from an emerging market. International Journal of Finance & Economics, 26(1), 1488–1502. https://doi.org/10.1002/ijfe.1860

- Peter, O., Pradhan, A., & Mbohwa, C. (2023). Industrial internet of things (IIoT): Opportunities, challenges, and requirements in manufacturing businesses in emerging economies. Procedia Computer Science, 217, 856–865. https://doi.org/10.1016/j.procs.2022.12.282

- Phan, D. H. B., Narayan, P. K., Rahman, R. E., & Hutabarat, A. R. (2020). Do financial technology firms influence bank performance? Pacific-Basin Finance Journal, 62, 101210. https://doi.org/10.1016/j.pacfin.2019.101210

- Prakash, N., Singh, S., & Sharma, S. (2021). Technological diffusion, banking efficiency and Solow’s paradox: A frontier-based parametric and non-parametric analysis. Structural Change and Economic Dynamics, 58, 534–551. https://doi.org/10.1016/j.strueco.2021.07.007

- Rumbogo, T., McCann, P., Hermes, N., & Venhorst, V. (2021). Financial inclusion and inclusive development in Indonesia. In R. L. Holzhacker & W. G. Z. Tan (Eds.), Challenges of governance: Development and regional integration in Southeast Asia and ASEAN (pp. 161–181). Springer International Publishing.

- Sathye, M. (2005). The impact of internet banking on performance and risk profile: Evidence from Australian credit unions. Journal of Banking Regulation, 6(2), 163–174. https://doi.org/10.1057/palgrave.jbr.2340189

- Shaikh, A. A., Glavee-Geo, R., Karjaluoto, H., & Hinson, R. E. (2023). Mobile money as a driver of digital financial inclusion. Technological Forecasting and Social Change, 186, 122158. https://doi.org/10.1016/j.techfore.2022.122158

- Sodokin, K., Koriko, M., Lawson, D. H., & Couchoro, M. K. (2022). Digital transformation, banking stability, and financial inclusion in sub‐Saharan Africa. Strategic Change, 31(6), 623–637. https://doi.org/10.1002/jsc.2531

- Subramaniam, Y., & Masron, T. A. (2021). Food security and environmental degradation: Evidence from developing countries. GeoJournal, 86(3), 1141–1153. https://doi.org/10.1007/s10708-019-10119-w

- Tan, N. N., Ngan, H. T. T., Hai, N. S., & Anh, L. H. (2022). The impact of digital transformation on the Economic growth of the countries. Prediction and Causality in Econometrics and Related Topics, 983, 670–680.

- Tecles, P. L., & Tabak, B. M. (2010). Determinants of bank efficiency: The case of Brazil. European Journal of Operational Research, 207(3), 1587–1598. https://doi.org/10.1016/j.ejor.2010.06.007

- Thakor, A. V. (2020). FinTech and banking: What do we know? Journal of Financial Intermediation, 41, 100833. https://doi.org/10.1016/j.jfi.2019.100833

- Tsou, H.-T., & Chen, J.-S. (2023). How does digital technology usage benefit firm performance? Digital transformation strategy and organisational innovation as mediators. Technology Analysis & Strategic Management, 35(9), 1114–1127. https://doi.org/10.1080/09537325.2021.1991575

- Vial, G. (2019). Understanding digital transformation: A review and a research agenda. Journal of Strategic Information Systems, 28(2), 118–144. https://doi.org/10.1016/j.jsis.2019.01.003

- Vincent, K., & Cull, T. (2011). Cell phones, electronic delivery systems and social cash transfers: Recent evidence and experiences from Africa. International Social Security Review, 64(1), 37–51. https://doi.org/10.1111/j.1468-246X.2010.01383.x

- Wahyudin, A., Kiswanto, K., & Nuhaaya, A. (2021). Net interest margin and capital adequacy ratio: Mediating influence of return on asset. Jurnal Dinamika Akuntansi, 13(2). Article 2. https://doi.org/10.15294/jda.v13i2.32404

- Wang, C., Qiao, C., Ahmed, R. I., & Kirikkaleli, D. (2021). Institutional quality, bank finance and technological innovation: A way forward for fourth industrial revolution in BRICS economies. Technological Forecasting and Social Change, 163, 120427. https://doi.org/10.1016/j.techfore.2020.120427

- Wang, S. H., & Xie, X. L. (2021). Economic pressure or social pressure: The development of digital finance and the digital innovation of commercial banks. The Economist, 1, 100–108. https://doi.org/10.16158/j.cnki.51-1312/f.2021.01.011

- Xie, X., & Wang, S. (2023). Digital transformation of commercial banks in China: Measurement, progress and impact. China Economic Quarterly International, 3(1), 35–45. https://doi.org/10.1016/j.ceqi.2023.03.002

- Yang, D., & Liu, Y. (2018). Why can Internet plus increase performance. China Industrial Economy, 5, 80–98. https://doi.org/10.19581/j.cnki.ciejournal.2018.05.005

- Zhang, X., Wu, Q., & Yu, X. (2019). the logic of cross-boundary disrupt innovation of enterprises at Internet Age. China’s Industrial EconomyChina Industrial Economics, 3, 156–174. https://doi.org/10.19581/j.cnki.ciejournal.2019.03.019