Abstract

The use of credit cards is closely connected to how well someone is doing financially. It has been associated with behaviors like excessive shopping and materialism. In India, there has been a recent increase in the number of credit cards issued. This research aims to study how Indian consumers use credit cards and how it affects their debt. The study focuses on three factors: power-prestige, credit card features, and ease of use. By understanding these factors, we can gain insights that will help both consumers and credit card issuers improve their financial well-being. The study identified three different groups of consumers based on their motivations for using credit cards. The first group is driven by a desire for power and prestige, while the second group is influenced by credit card features. The third group, which finds credit cards easy to use, has a negative impact on credit card usage. The research discovered several variables that affect how people use credit cards. By classifying consumers based on their motivations, the findings can provide a starting point for both consumers and issuers to better understand their financial well-being.

1. Introduction

The use of credit cards has become increasingly prevalent in India in recent years. As more and more individuals and households turn to credit cards for a variety of purposes, it is important to understand how credit card usage may impact financial well-being. This paper will explore the potential connections between credit card usage and financial well-being in India, drawing on available research and data. We will look at factors such as debt levels, savings rates, and financial literacy in relation to credit card usage, and examine the ways in which cultural and societal factors may shape the relationship between credit card usage and financial well-being in India. By gaining a deeper understanding of the connections between credit card usage and financial well-being in India, we can better understand the opportunities and challenges facing the Indian credit card market and identify ways to promote responsible use of credit and improve financial well-being for individuals and households.

Credit cards have shown to be an instrument to improve financial requirements. They can make transactions more convenient. India had a 27 percent surge in the number of credit cards in circulation between May 2017 and May 2018. The household debt to GDP ratio of India is particularly low in contrast to other countries. This implies the room for the credit card business to flourish in India. The credit system itself is uniquely tied to the spending habit and financial well-being of an individual. The credit utilization behaviour might consequently provide valuable insights about the market.

Previous studies have explored the relationship between credit card usage and financial well-being in developed countries, but less is known about this relationship in the Indian context. Factors such as income levels, education levels, and cultural attitudes towards debt may all play a role in shaping the relationship between credit card usage and financial well-being in India. Additionally, the banking industry in India has been rapidly changing with the implementation of new policies and regulations and an increased use of technology, which may also impact the relationship between credit card usage and financial well-being.

Prior research on credit card usage of Indian consumers have mainly focused on its relation to materialism and compulsive buying. It has also been linked to social values such as sense of belonging, being well respect, etc making up the multi-item list of values. Considering that India is still growing its market in the credit card industry, not much research however has been done on the adoption of credit cards themselves. This research aims to explore these areas.

There is a gap in the research on the relationship between credit card usage and financial well-being in India. While studies have been conducted in developed countries, the Indian context has not been extensively studied. This is important as the economic and cultural factors in India are different than other countries and therefore the relationship between credit card usage and financial well-being in India may differ. Additionally, the Indian banking industry has undergone significant changes in recent years with the implementation of new policies and regulations and an increased use of technology, which may also impact the relationship between credit card usage and financial well-being. Therefore, research is needed to examine the relationship between credit card usage and financial well-being in India specifically.

This study is intended to benefit both consumers and banks/credit card firms. Credit card businesses may obtain knowledge into various consumer behaviours. Consumers will gain a better understanding of how credit cards might benefit their financial well-being. The decline in GDP, combined with the impending recession, will undoubtedly impair its consumers’ credit capacity. There is a possibility that people will become increasingly reliant on credit because of a shortage of finances. Additionally, there may be instances where individuals are unable to handle their present finances and debts because of the recession. Thus, it is critical for both the consumer and the issuer to understand credit cards, the credit card market, and some of the factors that contribute to credit card debt. With increased financial literacy, the customer will demonstrate increased self-efficacy. With a better understanding of the variables, issuers can design credit card services that are more appropriate for the market segment they are targeting (Guttman-Kenney et al., Citation2023; Hamid & Harizan, Citation2023; Horvath et al., Citation2023; Patrikha et al., Citation2023).

2. Literature review

Financial well-being of a person would be expected to be directly influenced by the individual’s financial literacy. However, one forgets that there may be many psychological, social and economic factors influencing the individual’s behaviour when assuming a direct relationship. These factors can play a major role and should not be disregarded. One way to assess an effect of these factors on the individual would be to be to study the individual’s self-efficacy. Financial self-efficacy means the competence level that the individual has of self when dealing with financial situations. Studies of college students found literacy positively affects well-being when self-efficacy is a mediating factor (Limbu, Citation2017; Limbu & Sato, Citation2019). Another study of credit card misuse among Gen Y consumers in Malaysia found knowledge and self-efficacy negatively relate to credit card misuse (Zainudin et al., Citation2019).

Another method to study credit card usage and debt would be to analyse the attitude that the consumer has towards money, or credit cards itself. Lin et al. (Citation2019). studied the attitude towards money by testing for hypotheses such as “online purchasing experience is positively related to card spending” and “card spending is positively related to cardholder’s other loans” (Lin et al., Citation2019). In another study the attitude towards a credit card itself was measured by items such as “I like using credit cards”, “The cost of using a credit card is too high”, “The very thought of using a credit card disgusts me” (Barboza, Citation2018). Lin et al. (Citation2019) found attitude toward money to be the most important factor in their research, more than socio-demographic factors and credit card features. Zainudin et al. (Citation2019) found a positive relation between “favourable” credit card attitude and credit card misuse. People tend to be less sensitive toward the cost of an item when paying for it through a credit card. This makes them feel wealthier, regardless of their actual income, and thus encourages them to spend more via credit cards (Barboza, Citation2018). Attitudes such as “price sensitivity”, “power-prestige”, “anxiety”, “retention” have also been connected to compulsive buying behaviour (Khare et al., Citation2012; Veludo de Oliveira et al., Citation2014). Anxiety defines the optimism, security and confidence one has with the presence of money. Pessimism, fear, and anxiety one has with the absence of money. Power-prestige defines the elevated status one might relate to money. Price sensitivity is the tendency of the price of the product making an impact on the consumer’s intention. Retention refers to holding money in long term investments aimed at financial security. Khare et al. (Citation2012) found power and price sensitivity to influence compulsive behaviour amongst Indian consumers. Veludo de Oliveira et al., (Citation2014) found power-prestige, retention and anxiety to be responsible of credit card misuse. Effect of risk-taking behaviour has also been hypothesised to affect credit card misuse but was not significant in the results (Palan et al., Citation2011).

Compulsive buying behaviour has been related to credit card use/misuse in previous studies. Credit card usage has been studied both as a mediator effect between money attitudes and compulsive buying behaviour (Palan et al., Citation2011; Veludo de Oliveira et al., Citation2014). There was a significant relationship between credit card usage and compulsive behaviour (Palan et al., Citation2011). Credit card usage has also been studied as a mediation effect between materialism and compulsive buying behaviour amongst Indian consumers. Partial mediation was established, thus meaning materialism leads to credit card usage which facilitates compulsive buying (Debasis Pradhan & Kumar Jena, Citation2018). Conversely, when testing for compulsive behaviour as a mediating factor between materialism and credit card usage, credit card debt; it has been established that individuals with high compulsive buying behaviour have problems with credit card usage and debt (Veludo de Oliveira et al., Citation2014; Vieira et al., Citation2016). Direct effect of materialism on credit card use has been found out to be positively related (Zainudin et al., Citation2019).

Subjective norm or social motivation is an individual’s perception of the support/acceptance towards a behaviour given by the society around him. Subjective norm towards credit cards has also been studied as a driving factor of credit card usage (Limbu & Sato, Citation2019; Nguyen & Cassidy, ; Zainudin et al., Citation2019). A positive influence was found between social norm and credit card usage amongst Gen Y consumers in Malaysia where excessive use of debt was defined as the social norm (Zainudin et al., Citation2019). Social motivation, when defined as motivation to use credit cards responsibly, was not a significant predictor of credit card usage amongst college students. It, however, did show a strong relation to credit card self-efficacy (Limbu & Sato, Citation2019).

Self-efficacy also influences credit card adoption in a transitional economy. When researching credit card adoption in the transitional economy of Vietnam and Davis, (Citation1989) adopted a model influenced by the technology acceptance model and the theory of planned behaviour model (Ajzen, Citation1991). Theory of planned behaviour links subjective norm, attitude, behavioural control to behavioural intention and actual behaviour. Technology acceptance model uses perceived ease of use of the new technology, perceived usefulness of the new technology to connect behavioural intention of a new technology and its actual use. The model adopted by Nguyen and Cassidy picked up the constructs subjective norm, attitude, perceived usefulness and perceived ease of use from the two models for their research.

Features related to credit cards themselves have been studied by Christopher et al. (Citation2016); Khare et al. (Citation2012) and Lin et al. (Citation2019). Features were defined by hypotheses “credit card limit is positively related to spending”, “overdraft capability is positively related to spending”, “shopping discounts are positively related to higher credit card spending” etc. Only the hypothesis of credit limit being positively related to credit card usage and debt was supported (Lin et al., Citation2019). Another research chose to study payment due date, credit limit, length of credit cards usage, and number of credit cards as the features of credit cards; testing for their effect on revolving credit. Credit limit and number of credit card were found out to be positively related whereas length of credit card use was negatively related (Christopher et al., Citation2016).

Online shopping is widely growing as the first choice for consumers. It can be a major contributing factor to credit card use as credit is an easy payment option. The effect of internet has been studied on credit card delinquency and credit card balance (Basnet & Donou-Adonsou, Citation2016, Citation2018; Donou-Adonsou & Basnet, Citation2019). The access to internet increases chances of a positive credit card balance by 4–5% (Donou-Adonsou & Basnet, Citation2019). There are other factors that influence this relationship. For example, income seems to negligibly increase the card balance whereas education seems to decrease it (Donou-Adonsou & Basnet, Citation2019).

The most basic way to study a population is to gain insights from its demographics. Age, gender, household size, level of education have been considered in most of the studies (Lin et al., Citation2019, Gan et al., Citation2016). Other demographics have been used in various combinations. Besides the before mentioned aspects, nature of employer and income (Gan et al., Citation2016; Lin et al., Citation2019), race and marital status have been studied (Basnet & Donou-Adonsou, Citation2016.). A combination of only age, income, occupation and marital status has been studied (Ming-Yen Teoh et al., Citation2013). Another combination included social class, profession and lifecycle stage along with other more common demographics (Wang et al., Citation2011).

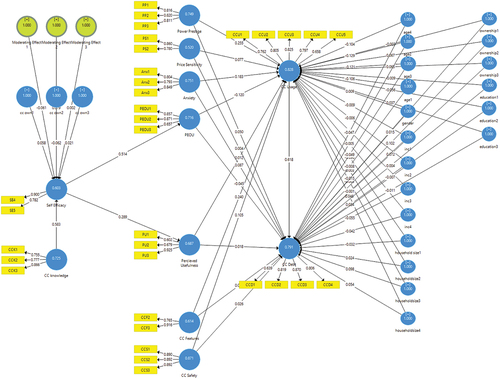

The constructs finally used in the research that directly affect credit card usage and debt are perceived ease of use, perceived usefulness, attitude towards credit cards, credit card safety and credit card features as shown in figure . The demographic factors studied include age, gender, monthly income, lifecycle stage, household size, house ownership, and level of education. The construct attitude towards credit include the factors of power prestige, price sensitivity and anxiety.

Figure 1. Conceptual model.

The constructs have been defined as follows for this research.

Perceived ease of use is defined as the degree to which an individual believes that using credit cards is free from effort.

Perceived usefulness is defined as the degree to which an individual believes credit cards will aid or improve their job performance.

Power prestige is defined as an individual’s belief of having a higher status when using a credit card.

Price sensitivity is defined as the perceived cost an individual associates to an item bought using credit cards.

Anxiety is defined as the pessimism an individual feels when using credit cards.

Credit card features are defined as the degree of use associated to benefits and incentives related to credit cards.

Credit card safety is defined as the degree of security an individual feels when using a credit card.

Credit card usage has items which express relatively improper practices when using credit cards. Credit card debt has items which relate missing payments.

Following are the hypotheses which will be tested in the research.

H1:

Power prestige will have a positive relationship on credit card usage.

H2:

Anxiety will have a positive relationship on credit card usage.

H3:

Price sensitivity will have a negative relationship on credit card usage.

H4:

Perceived ease of use will have a positive relationship on credit card usage.

H5:

Credit card features will have a positive relationship on credit card usage.

H6:

Credit card safety will have a negative relationship on credit card usage.

H7:

Credit card usage will have a positive relationship on credit card debt.

H8:

Self-efficacy will have negative relationship on credit card usage.

3. Methodology

A self-administered questionnaire dealt with collection of quantitative data. To deal with ordinal data, items were developed using the literature review based on a 5-point Likert scale. The items were taken from the previous research papers (Appendix A). The questionnaire was reviewed by two experts before collecting responses. For the pilot study responses were collected from 39 participants. The measurement model was developed on SmartPLS. An attempt was made to study the predictive effects of the demographic data. Hence, the demographic variables were directly included in the measurement model. The model is mix of reflective and single item constructs. Because the model did not have only reflective constructs, standard PLS algorithm is used. Indicator reliability is assessed by the outer loadings. Any item with outer loading below 0.4 should be discarded; outer loading between 0.4–0.7 should be discarded if the Cronbach’s alpha improves; outer loadings above 0.7 should be kept (Hair et al., Citation2021). Few of the items had to be discarded and were rephrased for the final questionnaire. Internal reliability can be measured by parameters Cronbach’s alpha and Composite reliability. Both the parameters have a maximum value of 1 and minimum value of 0. A value of Cronbach’s alpha greater than 0.6 falls is acceptable in explanatory analysis (Hair et al., Citation2021) However, a value of alpha between 0.5–0.6 also shows moderate reliability (Hinton et al., Citation2004). Cronbach’s alpha is a conservative way to assess reliability because it depends on the number of items; assumes all items to be equally reliable but PLS prioritizes items on individual loadings. It also tends to underestimate reliability. Using Composite reliability solves these problems. A composite reliability between 0.6–0.7 is acceptable in explanatory analysis, 0.7–0.9 is satisfactory and above 0.9 is not desirable as it points to possible redundancy of items (Hair et al., Citation2021). Below are the internal reliability test values. The constructs “Credit card features” and “Price sensitivity” did not meet the internal reliability criteria. The items of both the constructs were re-phrased and re-developed for the main study. After the pilot study analysis, for the main study, 380 responses were collected out of which 364 full responses were considered for further analysis. Since many of the study predictors are endogenous, it could affect the interpretation of these relationships. Tables show the final results obtained for internal reliability and convergent validity, discriminant validity, and indicator reliability followed by the measurement model.

Table 1. Internal reliability and convergent validity check for model with complete data

Table 2. Fornell-larcker criteria

Table 3. Outer loadings

Every construct except price sensitivity has an acceptable and above Cronbach’s alpha. Price sensitivity is moderately reliable with alpha > 0.5 and hence it is kept in the model. The outer loadings are all greater than 0.5. AVE for each construct is more 0.5. The constructs also fulfil the Fornell-Larcker criteria.

Figure shows the final measurement model with demographic predictors used for evaluation.

Figure 2. Measurement model used with demographic predictors.

Table show both the R square and adjusted R square values. 55% and 44% of variance in credit card usage and credit card usage is explained by the model respectively. Only 8% of variance in perceived usefulness is explained by the model.

Table 4. R2 values

Since most of the demographic data besides age does not have a significant relationship as observed from the lack of other demographic data in Table , it seems demographic data does not have strong predictive quality. This is further supported when all the demographic data have less than small f2 effect size as observed from the lack of demographic data in Table .

Table 5. Small and above f2 values

The study identified three different groups of consumers based on their motivations for using credit cards. The first group is driven by a desire for power and prestige, while the second group is influenced by credit card features. The third group is the one which finds credit cards easy to use. On comparing the R2 values of credit card usage and credit card debt for the three segments, moderate increase is observed for two segments. Though an increase in R2 for all the segments is preferred to validate the need of heterogenous study, we move ahead for exploratory analysis.

The following Table shows the hypothesis results in context of the basic PLS-SEM analysis.

Table 6. Hypotheses results

4. Results

The most significant and relatively strong relationship is of credit usage relating to credit card debt as depicted in Table . This is expected as the construct credit card usage measures relatively unsound financial credit card practices. The factors affecting credit card usage with highest impact are power prestige and credit card features. Both are positively related with path coefficients greater than 0.2. This is moderately strong enough in cases of behaviour models. According to the analysis results, power prestige is the biggest motivation for individuals to use their credit cards. Individuals feel a sense of supremacy when using credit cards. This leads to a greater chance of individuals allowing improper use despite professing competent self-efficacy. Power prestige has also been found to positively impact compulsive buying tendencies. Credit card features is the next factor with strongest impact on credit card usage. Credit card features are advertised to decrease cost of purchase and aim to provide benefits to the consumer when making a transaction. The individual would expect to ultimately save money via the benefits of credit card features. The pain of spending is lessened. Consumers slowly develop the tendency to make purchases because benefits are being offered on them via a credit card transaction. This increases the tendency to use credit cards inefficiently.

Table 7. Significant relationships

Anxiety and credit card safety also positively affect credit card usage, though with coefficients between 0.1 and 0.2. Anxiety measures the degree to which an individual feels pessimistic when using credit cards. Credit card safety measures the degree to which an individual believes credit card transactions are safe. One would expect both anxiety and credit cards safety to negatively affect improper credit card usage. However, that is not the case. This can be explained by the possibility that individuals are already making unsound decisions regarding a credit card. They are thus anxious about making such decisions in the future. Self-efficacy has a very small but negative effect on credit card usage (−0.58). This explains that knowledge about credit cards negatively affects improper usage.

4.1. Results of model testing for heterogeneity (FIMIX procedure)

When looking at path coefficients, all the three segments have significant effects shown by anxiety and credit card features. However, segment one shows a weaker effect in the case of anxiety. In the case of credit card features, both segment one and segment three show considerably weaker effect. Though, credit card usage has a strong positive significant effect on credit card debt in all the three segments, credit card features have a weak negative effect on credit card debt in segment two. This might be explained by the possibility that users of segment two adeptly manage benefits availed on credit card usage (Palos-Sanchez et al., Citation2018; Sarstedt & Ringle, Citation2010). Credit card safety has a low positive effect on credit card usage in segment one. Perceived ease of use has a lower negative effect in segment one and higher effect in segment three. Power prestige has a considerable effect in segment one and three.

Thus, segment one is driven by power prestige the most, more so than the other two segments with anxiety, credit card features and credit card safety also playing a role. The individuals belonging to this segment associate power and prestige to owning a card and hence use it. Segment two is driven by credit card features, more so than the other two segments. However, credit card features have a minute negative effect on credit card debt. Thus, the individuals belonging to this segment use credit cards because of the associated benefits and are adept at availing the benefits without indulging in improper credit card usage behaviour. Segment three has the strongest negative effect of perceived ease of use on credit card usage. The more individuals belonging to this segment are at ease with using credit cards, more responsible will their credit card usage be; more so than the other two segments.

Segment one has a significant strong negative relationship with monthly income falling between Rs 20,000 and Rs 50,000; and significant strong relationship with lifecycle stages of bachelor/bachelorette and divorcee/solitary survivor. Segment one would thus be characterised by an individual who does not have a partner. The more likely such an individual earns between Rs 20,000 and Rs. 50,000, the less likely he/she belongs to segment one. Segment two has a significant acceptable negative relationship with monthly income falling between Rs 20,000 and Rs 50000; and a significant acceptable positive relationship with lifecycle stage “married with child”. Segment two would thus be characterised by an individual who is married with a child. The more likely such an individual earns between Rs 20,000 and Rs. 50000, the less likely he/she belongs to segment two. Segment three has a significant strong positive relationship with household size two and a significant strong negative relationship with lifecycle stage “married with child”. This makes sense as the lifecycle stage “married with child” would relate to a household size of at least 3.

5. Discussions

Credit cards are found to be associated with prestige, status, and power (Fogel Mayer Schneider, Citation2011; Gan et al., Citation2016). Consumers have also been found to their anxiety related to money by showing compulsive buying tendencies (Khare et al., Citation2012; Veludo de Oliveira et al., Citation2014). Compulsive buying has often been linked as having a significant effect on compulsive buying (Khare et al., Citation2012; Veludo de Oliveira et al., Citation2014). In a research conducted on college students, it was found that higher levels of money anxiety related to higher levels of disposable income; and greater levels of disposable income increased the possibility of irresponsible credit card use. It has also been supported that the desire to attain social status through materialism increases the use of credit cards (Vieira et al., Citation2016) In the context of attitude towards credit cards, our findings also reach to similar results. In both the kinds of analysis, power prestige and anxiety have come out to play a significant role on irresponsible credit card use and debt.

Price sensitivity towards money was found to be more prevalent in individuals with lowest level and higher levels of income than in those of the middle range. When studying for an effect on compulsive buying through the mediation of credit card usage, it did not have any significant impact (Veludo de Oliveira et al., Citation2014). Our results are similar to the latter. In the basic PLS SEM analysis, price sensitivity did not have a significant effect on irresponsible credit card use.

Self-efficacy has proven to be negatively related to irresponsible credit card use (Limbu & Sato, Citation2019Zainudin et al., Citation2019). Amongst affluent Chinese consumers, credit cards were more convenient than cash. Our results from the basic PLS SEM analysis fall in line with previous research to show that self-efficacy has negative effect on irresponsible credit card use. Self-efficacy is significantly positively related to PEOU in segment one and three; and PEOU is significantly negatively related to credit card use. This would mean an indirect relation of self-efficacy to credit card use which again falls in line with previous research. However, previous research suggests an increase in convenience would lead to increase in credit card use. One possible explanation for this contrast to such results may be the fact that though a lot of Indian consumers possess a credit card, only few of them use it regularly. Hence, even though credit cards might be convenient for them to use, they will not lead to irresponsible behaviour.

Credit card limit has been found to be positively related to credit card misuse amongst the Chinese consumers. Increase in a card’s limit may create “income illusion” which encourages them to spend more now (Wang et al., Citation2011.). Young affluent Chinese respondents strongly agree that there are more attached advantages to paying with a credit card than paying with cash like reward points. Such credit card features have been found to have a positive relationship to use. Our results also further validate this by showing an acceptable positive effect.

Theoretically, this study will contribute to the literature on credit card usage and financial well-being by providing a better understanding of the relationship between these factors in the Indian context. The study will also help to identify the unique cultural and societal factors that shape credit card usage and financial well-being in India, which may be different than other countries. By exploring the relationship between credit card usage and financial well-being in India specifically, this study will add to the existing literature on this topic and provide new insights on the potential drivers of credit card usage and financial well-being.

From a practical perspective, this study will have several important contributions. The findings of this study will be useful for financial institutions, merchants, and policymakers in developing strategies to promote responsible use of credit and increase access to credit for those who may be underserved. The study will inform policies and strategies that may help to improve financial well-being for individuals and households, by providing a better understanding of the factors that influence credit card usage and financial well-being in India. Additionally, the study will also provide insights on the impact of technology and government policies on credit card usage and financial well-being in India, which can be used by the industry to adapt to these changes.

6. Conclusion and future scope

The research looked at the financial behaviour of credit card consumers, collecting data from Indian users. Various possible factors were tested for their effect on credit card usage. Constructs taken from technology acceptance model were used to gain insight in adoption of credit cards. However, no significant results were concluded for the latter. Two kinds of model were tested, one where demographic data was incorporated into the model itself and the other where demographic data was used to test for heterogeneity.

Power prestige, credit card features, anxiety, and credit card safety were the recognised factors in the first model approach. The second model approach produced three segments. The first segment was driven by power prestige. The second segment was driven by credit card features. The strongest relationship of the third segment was a negative one of perceived ease of use with credit card usage. Segment one is characterised by single individuals whose monthly income is less likely to fall between Rs. 20000–50,000. Segment two is characterised by a parent whose monthly income is less likely to fall between Rs. 20000–50,000. Segment three is characterised by consumers who live in a household of size two.

There is a huge scope of future work in this field with possibility of different models. This research would have benefitted if the certain items were better defined. Such items were deleted from the model to pass the internal reliability check. Certain constructs could also have been better adapted to the Indian society like that of credit card features. The construct could have focused on cash back, air miles, reward points and shopping discounts rather than just on shopping discounts, overdraft capability etc. The construct could also have then checked for formative trait. Formative convergent validity test requires a global single item measure for redundancy analysis. Since such a measure was not included in the questionnaire, the possibility of formative construct could not be explored in this paper. The study could also have been specific to a more limited age group and tested for patterns in younger groups following the example of previous research.

Lastly, rather than combining factors taken from the technology acceptance model with others, a separate full analysis could have been done taking data from new Indian consumers of credit card. This might have led to a better understanding of adoption of credit cards in India. The other factors would then be tested using another causal model. This research also did not include internet as a possible factor affecting credit card usage, which can be done in future studies.

The findings might help the issuers to grow their market share by appealing to the factor of power prestige in an individual. They can better incentivise the transactions. However, it should be done with utmost responsibility. Individuals equally need to understand these factors as ones that may lead to irresponsible credit card use. Credit if well managed can enable an individual to achieve his aspirations in life. Poor managed credit on the other hand is easily capable to trap an individual in never ending cycles of debt. Looking at the wide opportunity for growth in the credit card market of India, it is very important that one does not blindly follow the West when expanding our market as our current debt status is very much different from them. For a consumer, it is very important to understand credit and manage it efficiently to attain a better quality of life.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Sriram K.V

K.V Sriram is a Professor at the Department of Humanities & Management, Manipal Institute of Technology, Manipal. He holds an MBA and a doctorate degree in Marketing.

Riddhima Singh

Ridhima Singh is a graduate in Electrical and Electronics Engineering from Manipal Institute of Technology, Manipal Academy of Higher Education, Manipal.

Vibha

Vibha is an Assistant Professor at the Department of Information and communication Technology, Manipal Institute of Technology, Manipal. Her areas of interest are Machine Learning, Natural Language processing, Deep Learning, and Integrating Management and ICT.

Giridhar B Kamath is an Associate Professor at the Department of Humanities & Management, Manipal Institute of Technology, Manipal. He also holds an MBA and a doctorate degree in Marketing.

Giridhar B Kamath

Giridhar B Kamath is an Associate Professor at the Department of Humanities & Management, Manipal Institute of Technology, Manipal. He also holds an MBA and a doctorate degree in Marketing.

References

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–18. https://doi.org/10.1016/0749-5978(91)90020-T

- Barboza, G. (2018). I will pay tomorrow, or maybe the day after. Credit card repayment, present biased and procrastination. Economic Notes: Review of Banking, Finance and Monetary Economics, 47(2–3), 455–494. https://doi.org/10.1111/ecno.12106

- Basnet, H. C., & Donou-Adonsou, F. (2016). Internet, consumer spending, and credit card balance: Evidence from US consumers. Review of Financial Economics, 30(1), 11–22. https://doi.org/10.1016/j.rfe.2016.01.002

- Basnet, H. C., & Donou-Adonsou, F. (2018). Marriage between credit cards and the internet: Buying is just a click away! Review of Financial Economics, 36(3), 252–266. https://doi.org/10.1002/rfe.1019

- Christopher, E. C., Gan David, A., Hu, C. B., Tran, M. C., Dong, W., & Wang, A. (2016). The relationship between credit card attributes and the demographic characteristics of card users in China. International Journal of Bank Marketing, 34(7), 966–984. https://doi.org/10.1108/IJBM-09-2015-0133

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology.MIS. Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

- Debasis Pradhan, D. I., & Kumar Jena, A. (2018). Materialism and compulsive buying behaviour: The role of consumer credit card use and impulse buying. Asia Pacific Journal of Marketing & Logistics, 30(5), 1239–1258. https://doi.org/10.1108/APJML-08-2017-0164

- Donou-Adonsou, F., & Basnet, H. C. (2019). Credit card delinquency: How much is the internet to blame?. The North American Journal of Economics and Finance, Elsevier, 48(C), 481–497.

- Fogel Mayer Schneider, J. (2011). Credit card use: Disposable income and employment status. Young Consumers, 12(1), 5–14. https://doi.org/10.1108/17473611111114740

- Gan, X., Zuo, J., Chang, R., Li, D., & Zillante, G. (2016). Exploring the determinants of migrant workers’ housing tenure choice towards public rental housing: A case study in Chongqing, China. Habitat International, 58, 118–126. https://doi.org/10.1016/j.habitatint.2016.10.007

- Guttman-Kenney, B., Firth, C., & Gathergood, J. (2023). Buy now, pay later (BNPL)… on your credit card. Journal of Behavioral and Experimental Finance, 37, 100788. https://doi.org/10.1016/j.jbef.2023.100788

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hamid, F. S., & Harizan, S. H. M. (2023). BEHAVIORAL BIASES and CREDIT CARD REPAYMENTS AMONG MALAYSIANS. International Journal of Banking and Finance, 18(2), 53–78. https://doi.org/10.32890/ijbf2023.18.2.3

- Hinton, P., Brownlow, C., McMurray, I., & Cozens, B. (2004). SPSS explained Routledge. Inc, East Sussex.

- Horvath, A., Kay, B., & Wix, C. (2023). The Covid-19 shock and consumer credit: Evidence from credit card data. Journal of Banking & Finance, 152, 106854. https://doi.org/10.1016/j.jbankfin.2023.106854

- Khare, A., Khare, A., & Singh, S. (2012). Factors affecting credit card use in India. Asia Pacific Journal of Marketing & Logistics, 24(2), 236–256. https://doi.org/10.1108/13555851211218048

- Limbu, Y. B. (2017). Credit card knowledge, social motivation, and credit card misuse among college students: Examining the information-motivation-behavioral skills model. International Journal of Bank Marketing, 35(5), 842–856. https://doi.org/10.1108/IJBM-04-2016-0045

- Limbu, Y. B., & Sato, S. (2019). Credit card literacy and financial well-being of college students: A moderated mediation model of self-efficacy and credit card number. International Journal of Bank Marketing, 37(4), 991–1003. https://doi.org/10.1108/IJBM-04-2018-0082

- Lin, L., Dian Revindo, M., Gan, C., & Cohen, D. A. (2019). Determinants of credit card spending and debt of Chinese consumers. International Journal of Bank Marketing, 37(2), 545–564. https://doi.org/10.1108/IJBM-01-2018-0010

- Ming-Yen Teoh, W., Chong, S.-C., Mid Yon, S., & Baumann, C. (2013). Exploring the factors influencing credit card spending behavior among Malaysians. International Journal of Bank Marketing, 31(6), 481–500. https://doi.org/10.1108/IJBM-04-2013-0037

- Palan, K. M., Morrow, P. C., Trapp, A., & Blackburn, V. (2011). Compulsive buying behavior in college students: The mediating role of credit card misuse. Journal of Marketing Theory & Practice, 19(1), 81–96. https://doi.org/10.2753/MTP1069-6679190105

- Palos-Sanchez, P., Martin-Velicia, F., & Saura, J. R. (2018). Complexity in the acceptance of sustainable search engines on the internet: An analysis of unobserved heterogeneity with FIMIX-PLS. Complexity, 2018, 1–19. https://doi.org/10.1155/2018/6561417

- Patrikha, F. D., RWW, E. T. D., Soetjipto, B. E., & Haryono, A. (2023). Analysis of impulse buying behavior of credit card users in modern retail. Baltic Journal of Law and Politics, 16(3), 2454–2460.

- Sarstedt, & Ringle. (2010). Treating unobserved heterogeneity in PLS path modelling: A comparison of FIMIX-PLS with different data analysis strategies. Journal of Applied Statistics, 37(8), 1299–1318. https://doi.org/10.1080/02664760903030213

- Veludo de Oliveira, T. M., Falciano, M. A., & Villas Boas Perito, R. (2014). Effects of credit card usage on young Brazilians’ compulsive buying. Young Consumers, 15(2), 111–124. https://doi.org/10.1108/YC-06-2013-00382

- Vieira, K. M., de Oliveira, Olivia Rovedder, M., & Kunkel. (2016). Franciele Inês Reis, “the credit card use and debt: Is there a trade-off between compulsive buying and ill-being perception?. Journal of Behavioral and Experimental Finance, Elsevier, 10(C), 75–87.

- Wang, L., Wei, L., & Malhotra, N. K. (2011). Demographics, attitude, personality and credit card features correlate with credit card debt: A view from China. Journal of Economic Psychology, Elsevier, 32(1), 179–193. https://doi.org/10.1016/j.joep.2010.11.006

- Zainudin, R., Shahnaz Mahdzan, N., & Yeap, M.-Y. (2019). Determinants of credit card misuse among Gen Y consumers in urban Malaysia. International Journal of Bank Marketing, 37(5), 1350–1370. https://doi.org/10.1108/IJBM-08-2018-0215