?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the effects of exchange rate and net exports on manufacturing enterprises’ profitability on the Pakistan Stock Exchange (PSX). When activity-based accounting is examined using panel data techniques, the main objective is to examine the direction and magnitude of the moderating influence of exchange rate fluctuations on net exports and the return on assets. We employed 249 manufacturing companies on the Pakistan Stock Exchange from 1999 to 2019. The Pakistani economy used a multicurrency system, using the Generalize Method of Moment (GMM) regression analysis system. The number of debtors’ days, creditors’ days, the cash conversion cycle, and the company’s return on assets all link favorably. Inventory turnover days, financial leverage, net exports, exchange rate, and return on assets are all negative. The Size and age of a business have a significant positive association with profitability but a negative relationship with Return on Assets (ROA). This study suggests that activity-based accounting improves company performance. Recognizing interdependence, net exports owing to currency rate depreciation have adverse effects. Managers may construct an appropriate measure to control activity-based working according to forex market symptoms and when macro-economic factors modify micro-economic policies’ behavior to increase ROA. Hence, debtors need to be paid early, and payables need to be paid late, but in these cases, the financial management should improve the return on assets.

IMPACT STATEMENT

This paper investigates the impact of net export and exchange rate on the profitability of firms using a statistical technique called the Two-Step System Generalized Method of Moments Approach. Understanding the factors that influence firm profitability is important for investors, policymakers, and business owners. This study specifically examines the role of net export, which refers to the difference between a country’s exports and imports, and exchange rates, which determine the value of one currency in relation to another, on firm profitability. The findings of this research have significant implications for firms operating in global markets, as they highlight the importance of understanding the impact of net exports and exchange rates on profitability. The study suggests that firms may need to adjust their strategies based on fluctuations in exchange rates and focus on increasing their net export to maintain profitability. Overall, this paper provides valuable insights into the complex relationship between net export, exchange rates, and firm profitability, which has important implications for businesses and policymakers alike.

REVIEWING EDITOR:

1. Introduction

Following the world financial crisis, established and developing countries saw a dramatic decline in international commerce. The decline in manufacturing output was far less than the decline in international commerce, which naturally begs the issue of the contribution of trade financing to the ‘Great Trade Collapse’ (Di Giovanni et al., Citation2022). Important policy implications arise from knowing how much the decline in credit availability brought on by the banking crisis contributed to the decline in trade since this would suggest that recovery depends on the resumption of trade credit (Dottori et al., Citation2022). A more concerning outcome would be a similar exaggerated trade reaction after financial disruptions (Mansilla-Fernández & Milgram-Baleix, Citation2023). According to the most recent production and unemployment predictions, there may be a rise in impaired loans and public debt, which might be detrimental to banks’ balance sheets. Because of this, banks may experience higher financing costs that would limit the amount of credit available to the industry (Laeven et al., Citation2022).

Furthermore, enterprises may struggle to get bank funding in this scenario and face financial difficulties. When unfavorable trading conditions, like a drop in sales or a break in the payment chain, a firm’s liquidity comes under pressure (Abou Saleh & Al Tuwaijri, Citation2022). Liquidity measures a company’s ability to handle receivables and payables to export and avoid mass bankruptcies.

Theoretical and empirical research has put up and supported several hypotheses for the perplexing reality that financial crises have significantly impacted foreign commerce more than domestic activity during the last 10 years. The primary rationale is that selling globally incurs more costs than domestic sales. Companies entering overseas must do several tasks, including market research, creating new distribution networks, learning about administrative necessities, engaging with potential new partners, and changing product lines (González et al., Citation2022; Kassberg & Dornberger, Citation2022). These costs, often hidden in nature, make it difficult to enter the export market (Arora & Mukherjee, Citation2022). It is also why the most productive businesses self-select to export (Eegunjobi & Ngepah, Citation2022), and company heterogeneity has become a critical factor in overall exports. In addition to these sunk costs, exporters suffer additional costs due to the higher risk and extended delivery time associated with cross-border operations. Exporters must suffer a greater risk of damage and higher insurance costs, and there is less confidence that the contract will be upheld between the time of payment and the delivery of the goods (Crozet, Demir, & Javorcik, Citation2022).

Consequently, financing global transactions is more challenging than financing domestic transactions. In reality, theoretical models indicate that less financially constrained enterprises would export more often and in larger quantities than financially restricted firms since they must get external finance to meet these increased fixed and variable expenses (Sanders et al., Citation2022). Even if a company’s goods are in greater demand, it may not be able to satisfy demand if its payables and receivables are insufficient. Numerous businesses have had difficulties with activity-based accounting since the multicurrency system was implemented in February 2009.

A few empirical studies have attempted to examine the nature and scope of the link between activity-based accounting and financial leverage’s impact on profitability in Pakistan. However, the issue is becoming worse under the multicurrency system nowadays. Using firm-level data, numerous empirical studies have examined the link between financial restrictions and export behavior. These investigations broadly corroborate the theoretical hypotheses (Jafari et al., Citation2022; Lim & Morris, Citation2022; Lodi & Bertarelli, Citation2022, for a survey). Nevertheless, most studies only focus on one country at a time, which reduces the likelihood that their conclusions may be generalized to other nations (Linse et al., Citation2022). Although the research listed above implicitly suggests that financial leverage management may be crucial for exporters, both on the intense and extended margins, to our knowledge, the function of receivables and payables in financing exports has gotten little attention (Franzetti, Citation2021; Wang et al., Citation2021). Surprisingly, most studies have focused on external finance and have not paid attention to how crucial working capital management is (Huang et al., Citation2022).

Inventory trends are a big part of making trade uncertainty clear (Li, Wang, et al., 2022; Ngene & Mungai, Citation2022), while advances, a type of trade credit, affect the ability of small and medium-sized businesses to participate in exports (Crozet et al., Citation2022). If an exporter relies on inventories to react to supply or demand shocks, exporter-to-importer credits are the exporters’ most common internal financing. Exporters must reduce the time between paying for possibly imported materials and receiving payment for their sales. In contrast to previous studies, these studies focus on the ability to work capital management to generate internal cash. They are giving lengthy trade credit or keeping inventory costs exporters their chance, which would discourage them from investing in internationalization (Su, Shi, et al., Citation2022).

Additionally, businesses are encouraged to export by delaying provider payments since payables are a relatively cheap source of finance (Long et al., Citation1993). Banks would also be more willing to provide loans to businesses with trade finance since they are less likely to present a systemic risk (Shahzad et al., Citation2021). We contend that a firm’s internal capacity to finance short-term debt may significantly determine how much business it can export. This research intended to support the Pecking Order theory (Myers, Citation1984; Myers & Majluf, Citation1984) and earlier research attempting to link financial constraints to export behavior. This study also suggests that the effect of debt on exports could be substantial for companies with few resources.

Henceforth, we utilize a sample of 249 Pakistani manufacturing companies listed on the stock exchange and data from the State Bank of Pakistan’s data division for 1999 to 2019. First, we examine whether a longer paying term and shorter receivable period encourage enterprises to enter international markets and boost exports. To account for enterprises that choose to export, we quantify these processes using a system GMM estimate approach (Gao et al., Citation2022). Second, the transmission route is decoupled by examining the elements of the activity-based accounting measured. Third, we examine whether exporters with constraints face more economic importance than exporters. To do this, we also use the interaction concept, with the exchange rate and net exports functioning as interacting variables. Our primary hypothesis is verified, giving a glimpse of our findings. We discover that companies performing well are more likely to export and sell than other exporters. As predicted, trade credit agreements that include conditions for credit sales and purchases and financial leverage decrease the likelihood and volume of exports, while postponing provider payments encourages enterprises’ exports. Our findings support that exports are adversely impacted by financial limitations, in keeping with earlier studies, by demonstrating how the exchange rate depreciation affects net exports, ultimately affecting the company’s performance.

The globalization of the economy in recent years and the growing importance of exports in its expansion have caused substantial changes in the Pakistani economy. However, the link between financial limitations and export behavior is still being discussed in the research. Although some research has shown that financial considerations may constrain a company’s capacity to expand into new markets via exports, other studies have stated that this connection may rely on elements like the firm’s capital structure and the exchange rate regime. Using a two-step system generalized method of moments methodology, this research intends to evaluate the moderating impacts of net exports and currency rates on the link between financial restrictions and company profitability in the Pakistani setting. With Pakistan’s current economic issues, such as the COVID-19 pandemic’s effects, changes in the currency rate regime, and the need to encourage exports to sustain economic development, this research is especially pertinent.

The pecking order theory of capital structure also offers a theoretical framework for comprehending how organizations finance their investments and how financial limitations may impact their capacity to do so. This research intends to add knowledge on the Pecking Order theory and its relevance in the Pakistani context by investigating the moderating effects of net exports and currency rates on the link between financial constraints and company profitability. In conclusion, the ongoing debate in the literature about the connection between financial constraints and export behavior, the recent changes in the Pakistani economy, and the need to comprehend how firms finance their investments, as well as the role that financial constraints play in this process, all support the need for this study.

The current study contributes to the body of literature by employing a sample from a developing country to support the idea that the little effect of firms’ external environmental factors (detail in next para) may initially change such entities’ internal financial structures.

Some examples of the external environment that may impact enterprises are Factors influencing the economy, including tax, inflation, interest, and currency rates. Changes in consumer habits, as well as technological developments and disruptive technologies. Things like government rules, trade policy, labor laws, and political stability are examples of political and legal variables. Factors of a social and cultural nature include shifting demographics, consumer tastes, evolving ways of life, and established cultural mores. Factors in the natural environment include global warming, loss of natural resources, pollution, and sustainability concerns. Market concentration, obstacles to entry, and the intensity of competition are all examples of competitive variables. Supply chain dynamics changes, customer demand variations, and new product or service introductions are all examples of industry-specific variables. Changes in economic and political climates throughout the globe and varying consumer tastes in various parts of the world are examples of global influences. These external influences may significantly affect how a firm runs, performs well, and is profitable. Organizations must be aware of these aspects to stay competitive and successful and adjust their plans appropriately.

The model’s capabilities are only generally applicable to the findings of our inquiry. Last but not least, the study’s chosen period (1999–2019) has experienced several economic swings, including a recession and a change in government policy as a result of the election of new governments from various political parties, both of which may happen under a regular business or economic conditions. The currency rate and net exports, which operate as an interaction vector for enterprises’ financial management in short-term accounting transactions, are used in this research to assess the efficacy of activity-based accounting. Thus, this work adds to the corpus of earlier research on the subject. This study fills a gap in industry-related analysis by being one of the few academic ones to examine the interaction between the exchange rate and net export. And how it affects the financial performance of corporations using activity-based accounting, company financial leverage, and the impact on firm sales.

The article then continues as follows: The study’s theoretical foundations and hypothesis are discussed in Section 2, which is then followed by the presentation of the research’s hypotheses, data, and empirical framework in Section 3. The critical empirical findings are described in Section 4, and a conclusion is presented in Section 5.

2. Literature review and hypothesis

2.1. Theoretical background

2.1.1. New trade theory

Melitz (Citation2003) asserts that a new source of trade benefits has arisen. When trade barriers are lifted to increase global competition, low-productivity firms previously shielded by trade barriers are compelled to leave the market, enabling high-productivity firms to increase their production volume. As a result, a country’s overall average production increases. This increase in average productivity translates to an increase in people’s actual income; individuals get more prosperous due to the global natural selection of enterprises. According to Melitz (Citation2003), providing a domestic sector with a high level of protection may stifle natural selection and prevent productivity growth. During the year 2000, a new trade theory was proposed. This theory’s primary goal is to prove that the firm’s productivity level varies throughout the enterprise. Going to export is accomplished by a small number of firms with outstanding productivity (Ranjan & Raychaudhuri, Citation2016; Olyanga et al., Citation2022).

2.1.2 Tradeoff theory and pecking order theory

Kraus and Litzenberger (Citation1973) initially used the tradeoff idea to determine whether debt or equity was preferable. It was determined how much weight each source of income should be given so that the company might profit from its responsibilities and save money on taxes. Tradeoff and pecking order theories were employed in numerous studies.

The tradeoff hypothesis is explained through a cost-benefit analysis (Izhakian et al., Citation2022). The capital structure stays the same financing must be balanced if a company funds with debt or plenty of stock. The idea states that trade credit may be a less expensive alternative to bank lending. The business has access to a flexible source of finance by deferring payments to suppliers. On the other hand, trade credit prevents the company from receiving discounts for making a timely or early payment, which prevents the company from potentially saving money. A flexible trade credit policy and interest on receivables are expected to boost sales with accounts receivable (Farooq et al., Citation2022). However, this method could be expensive since money is held up in accounts receivable and accounts payable (Ahmed & Mwangi, Citation2022). The best inventory level for the company to maintain in terms of management is one that achieves a balance between profit and liquidity (Hämäläinen, Citation2022). Maintaining a vast inventory necessitates borrowing money to pay for it and other expenses, including transportation, insurance, storage, and spoiling (Haider & Siddiqui, Citation2020). On the other hand, maintaining a low inventory level might result in lost sales and stockouts (Ramos et al., Citation2020), affecting profitability.

Myers and Majluf investigated the link between debt and profitability using the pecking order hypothesis in 1984. It is envisaged that enterprises with higher net profits and more robust retained earnings could effectively address the issue of debt funding dependency. As a result, the pecking order hypothesis suggests that using internal money rather than borrowing to support corporate operations is ideal for all organizations (Su, Yan, et al., Citation2022). It is often held that an increase in a company’s leverage has a significant and detrimental effect on the latter’s profitability (Indomo & Lubis, Citation2022; Myers & Majluf, Citation1984).

2.2. Hypothesis development

Having a competitive product is just half the fight for exporting. For businesses to fulfill orders, pay for resources, bridge the period between trade and payment, and be protected from financial default by partners, extra trade finance services are needed when they export. The research linking firms’ financial needs with credit arrangements with global trading partners and the literature linking financial frictions with trade operations provide a framework for this research. Even though their objectives are comparable, the processes for enhancing a firm’s performance abroad and at home may vary. Export insurance might lower the business risk for exporters, and export loans might make it easier for them to do business.

The research shows how reliant on outside financial resources exporting operations are. Theoretically, one reason why the state of the external economy has such a significant impact on trade is the requirement to fund the fixed and variable expenses related to exporting operations. So, according to Roberts and Tybout (Citation1997), exporters must incur permanent costs related to market analysis, technological and administrative standard adaptation, distribution system search, partner negotiating, product range modification, etc., to enter foreign markets. The most productive companies are the ones that can control these buried costs and access export markets (Rachbini, Citation2020). Along with these initial expenses, exporters must additionally deal with higher variable expenses such as transportation charges, customs, and freight insurance. Due to the difficulty of monitoring a foreign partner and the risks associated with currency changes and contracts involving several countries, they also face different hazards (Ogeya et al., Citation2021). Due to lengthier delivery durations, exporters also have more short-term contractual demands than domestic producers (Swazan & Das, Citation2022). Firms need external finance to cover these additional expenditures. Therefore, it stands to reason that only financially secure businesses can access international markets and that financially secure businesses export more than financially secure ones (Yuan & Pan, Citation2022). Empirical research using data from specific companies has been conducted to comprehend how a credit crunch or liquidity crisis affects international trade (Pietrovito & Pozzolo, Citation2021; Thang & Ha, Citation2022). With a few notable exceptions, these studies conclude that a lack of external financing affects an enterprise’s chances of exporting and its overseas sales. Researchers like Jinjarak and Wignaraja (Citation2016) and Pietrovito and Pozzolo (Citation2021) have used firm-level data from various developing or emerging countries. Most of these studies, such as those by Máñez and Vicente-Chirivella (Citation2020) and Guo et al. (Citation2022), concentrate on specific countries. Pietrovito and Pozzolo (Citation2021) developed a method for dealing with endogeneity problems caused by export credit constraints.

The articles above mainly discuss businesses’ options for obtaining external loans but do not consider the function trade-specific financial instruments perform (Kurban, Citation2022). However, exporters often use trade credits to secure letters of credit from intermediaries via payment in advance or open-account conditions (Franzetti, Citation2021). By concentrating on the role played by short-term loan agreements as a capability to produce internal funds in enterprises’ export behavior, we aim to close this gap. Short-term credit agreements include administering accounts receivable and payable to pay for inputs before receiving output revenues. Except for Doan et al. (Citation2020), who used data from the World Bank Enterprise Survey to examine the impact of payment in advance on the involvement of small and medium-sized companies in exports from 56 developing countries, this subject has been ignored in the literature. Our research is grounded on the capital structure theory known as the Pecking Order, which claims that businesses choose internal capital resources over external ones owing to adverse selection (Myers, Citation1984; Myers & Majluf, Citation1984). Businesses may improve their short-term sales if they prolong their customers’ payment terms or postpone investments in fixed capital, but they must consider the opportunity costs.

On the other hand, deferring payments to suppliers may be a cheap and adaptable source of funding for the business (Settle, Citation2022). The growing body of research on export generally concludes that short-term financing is a good indicator of a company’s future financial needs (Phan, Citation2022). The transmission channel under investigation’s core comprises short-term activity for two reasons. In the first place, enterprises’ ability to store and sell products is limited by the duration of the manufacturing processes for technical reasons, which supports short-term financing operations. Second, a company is more likely to depend on short-term debt for financing the more significant its level of financial leverage (Hussain et al., Citation2022). Firms may be comparatively overexposed to collective risk if deteriorating financing availability makes obtaining capital more difficult or results in losses when delaying loan maturity (Mansilla-Fernández & Milgram-Baleix, Citation2023). Commercial lenders can often assess their clients’ financial standing before determining whether to provide financial help (Grassi et al., Citation2022). It’s interesting to note that recent research shows that enterprises with relatively significant financial leverage rely more on outside funding, which enhances their risk (Saxena & Bhattacharyya, Citation2022).

Using panel data analysis, Kiani and Khan (Citation2014) examined the relationship between exchange rate volatility and firm profitability in Pakistan. Their results showed that exchange rate volatility significantly negatively impacts firm profitability. Arshad et al. (Citation2016) investigated the impact of exchange rate fluctuations on the profitability of Pakistani firms using a sample of 200 firms listed on the Karachi Stock Exchange. They found that exchange rate fluctuations significantly negatively impact firm profitability.

Ali and Anwar (Citation2016) examined the impact of net exports on firm profitability in Pakistan using panel data analysis. Their results showed that net exports significantly positively impact firm profitability. Shujaat et al. (Citation2017) explored the moderating effects of exchange rate fluctuations on the relationship between firm Size and profitability in Pakistan using a sample of 149 manufacturing firms. Their results showed that exchange rate fluctuations significantly negatively impact the profitability of small and medium-sized firms but not large firms.

Azhar and Muhammad (Citation2019) investigated the impact of exchange rate fluctuations on the profitability of Pakistani firms using a sample of 40 manufacturing firms listed on the PSX. Their results showed that exchange rate fluctuations significantly negatively impact firm profitability. Overall, the literature suggests that net exports and exchange rate fluctuations can significantly impact firm profitability in Pakistan. Exchange rate fluctuations, in particular, are likely to have a negative impact on profitability, while net exports can have a positive impact. The moderating effects of these variables on the relationship between other factors (such as firm Size) and profitability may also be essential to consider in future research.

These studies show how financial limits affect exports. Kohn et al. (Citation2022) investigate how financial frictions affect international trade. They begin by discussing the relationship between export decisions and access to external finance. They then use the analytical framework they provide to examine the impact of financial constraints on firm export decisions. This article examines how financial frictions affect global trade dynamics between enterprises and sectors. It includes theoretical, empirical, and quantitative studies. This study examines how financial limitations affect export sales. The present study intends to contribute to the existing body of knowledge by illustrating how the temporary arrangement of conditions for collection between credit sales and debtors and credit buyers influences a company’s capacity to export goods and services. This is one of the first pieces to examine how creditors and creditors interact regarding net exports, specifically when both imports and exports are considered. So, the test’s hypothesis may be stated as follows:

Hypothesis 1, The Net Export interacts with the nexus of the debtor’s turnover ratio and return on assets at the firm’s level.

Hypothesis 2: The Net Export interacts with the nexus of the creditor’s turnover ratio and return on assets at the firm’s level.

Hypothesis 3, The Exchange Rate interacts with the nexus of the debtor’s turnover ratio and return on assets at the firm’s level.

Hypothesis 4: The Exchange Rate interacts with the nexus of the creditor’s turnover ratio and returns on assets at the firm’s level.

The second study issue is whether having limited resources may make the effects of credit purchases and sales on exports more pronounced. This paper supports earlier studies showing the value of financial leverage, especially when capital markets are unreliable (Khan & Chakraborty, Citation2022; Kuantan et al., Citation2021; Shcherbakov, Citation2022). Similarly, using several financial constraint criteria, Chiu et al. (Citation2022) show that financially constrained businesses save more money than those not. The degree to which cash flow can partly capture possible investment opportunities will influence the amount of sensitivity (Machokoto & Areneke, Citation2020). However, it has been shown that companies with solid credit ratings have easier access to financial markets.

Consequently, these companies must maintain lower cash flow than those with restricted resources (Guizani & Abdalkrim, Citation2021). These findings are supported by Nemlioglu and Mallick (Citation2021); the relationship is more vital for restricted enterprises than unconstrained ones. More financial leverage is linked to higher levels of investment for constrained firms. Likewise, more leveraged enterprises tend to have more extended credit agreements and smaller funding deficits, according to research by Bichsel et al. (Citation2022). In addition, firms short on cash used it more quickly and relied more heavily on credit lines out of worry for the financial institutions that provided the loans. In addition, to obtain money for their company, they would have to sell other assets (Liu et al., Citation2021). It is noteworthy that trade creditors will often evaluate their customers’ financial situations before deciding whether or not to provide credit to their customers. It is predicted that credit limitations would make exports more susceptible to fluctuations in working capital. As a result, the following is one possible way to state the second hypothesis of this research:

Hypothesis 5, The Exchange Rate interaction with the nexus between financial leverage and return on assets at the firm’s level

Hypothesis 6, The Net Export interaction is the nexus between financial leverage and return on assets at the firm’s level

In inference, this study intends to further the field of research by demonstrating how activity-based accounting management affects exports. This article makes a vital hypothesis: financial limitations may act as a catalyst for the impact of debtors and creditors on exports and the likelihood that firms will internationalize. This idea says that activity-based accounting management is a better way for companies to keep track of their financial leverage.

Singh and Rastogi (Citation2022) proved that managers might add value by lowering their accounts’ past due days. Their findings are resistant to the presence of endogeneity. Additionally, it was discovered that dropping the cash conversion sequence increased the firm’s profitability. The research found that businesses may increase their profits by managing their CCC more effectively by lowering the tolerable minimum of the debtors and inventory turnover days (Musa & Ibrahim, Citation2022). According to Naumoski et al. (Citation2022), firm profitability and CCC variables have a significant adverse relationship. They found that the company’s profitability decreases as the cash conversion cycle lengthens. To improve shareholder value, managers may minimize the cash conversion cycle.

Nesbitt et al. found a negative association between firm profitability and capital adequacy in investment and financing strategies in 2022. Potwana et al. (Citation2022) discovered a negative link between profitability and customer payment time, a positive relationship between profitability and inventory-to-sales time, and a positive relationship between profitability and creditor payment time. The research found a nonlinear relationship between trade finance and firm development. Using a supplier’s credit to help a company expand is controversial. This argument says trade credit benefits businesses. According to the financial advantage idea, trade credit is a crucial source of short-term operating cash. With more trade credit, enterprises may allocate credit to development inputs, as buyers are less likely to confiscate or redirect cash credit. Fast-growing enterprises may use trade credit when alternative funding options are insufficient. According to finance theory, trade credit is an alternative to bank lending during a financial crisis and a source of development capital for enterprises with restricted resources. Companies using supplier credit may grow more quickly throughout a financial crisis because they can maintain operational consistency and have fewer liquidity problems (Li et al., Citation2022).

The interaction between export behavior and financial limitations and potential connections to the pecking order hypothesis of capital structure. According to the Pecking Order hypothesis, businesses prefer to finance investments first with internal resources, then with debt, and ultimately with equity. Nonetheless, businesses may have financial limitations that make it difficult to finance new initiatives if internal resources are inadequate. Previous studies have investigated the connection between financial limitations and export behavior. According to several studies, a company’s capacity to expand into new markets via exports may be constrained by financial considerations. The current research, however, makes the case that this link could be influenced by things like the organization’s capital structure and the exchange rate regime. In other words, depending on how companies fund their investments and how the exchange rate influences their profitability, financial limitations may be more or less significant for businesses. The study makes the case that examining the moderating effects of net exports and exchange rates on the relationship between financial constraints and firm profitability can add new insight to this debate and offer a more nuanced understanding of the connection between financial constraints and export behavior.

3. Data and methodology

3.1. Data and variables

Whether these companies are from a specific index is conceivable that the sample includes companies from that index, but it is not always the case. Other selection criteria, such as Size, industry, or data accessibility, may or may not be connected to a particular stock index may have been used. Two hundred forty-nine manufacturing enterprises were chosen as part of the sample from a group of businesses registered on the Pakistan Stock Exchange (PSX). Companies from thirteen different industrial groups were to be chosen, and those that were on hold or inactive on the stock market were to be excluded.

The majority of the data included in the research came from corporate websites, financial statements, and the website of the State Bank of Pakistan. Financial research often uses publicly accessible financial data as a source of knowledge. The study also used ratios as dependent and explanatory variables to help researchers better comprehend the organization’s financial and operational variables. Ratio analysis is a popular method in financial analysis for assessing business performance by contrasting various financial statement components.

The Pakistan Stock Exchange (PSX) is included in several indexes that monitor the performance of various Pakistani stock market divisions. The PSX's primary indicators are:

The performance of the top 100 businesses listed on the PSX, ranked by market capitalization, is tracked by the KSE-100 Index, the benchmark index of the Pakistani stock market. KSE-30 Index: Based on market capitalization, this index measures the performance of the top 30 companies listed on the PSX. KMI-30 Index: Based on market capitalization, this index measures the performance of the top 30 Islamic finance businesses listed on the PSX. KSE All Share Index: The performance of every company listed on the PSX is monitored by this index. Further sector-specific indexes measure the performance of businesses in certain areas, such as the KSE Oil and Gas Index and the KSE-Technology Index.

3.1 A. Operational definitions ()

3.2 Descriptive statistics and correlations

The effect of the cash conversion cycle on asset return is shown through descriptive data. According to descriptive statistics, 5229 observations were used to track the emotions. The sample contains a variety of industrial enterprises, which might significantly influence trade credit trends. The inconsistent operating cycles, manufacturing technology, market structure, seasonality, product characteristics among sectors, and the variability across customs credit unions, further support these results. Return on assets, the dependent variable, has an average of 1.88 and a variance of 0.96. This standard deviation shows that ROA varied widely across businesses over the research period. The broader range of maximum and minimum equity return levels supports this diversity even more. With a standard variation of 1.929 days, the observed average cash conversion period is 5.452 days long. According to the average inventory turnover of 4076, firms must convert their inventory into cash in 4,076 days. Detailed figures show that it takes, on average, 4.004 days to recover money from its receivables. Firms in the sample from many industrial sectors may alter how other businesses carry out their regular business activities. The average time businesses take to settle their obligations is 4.559 days. The average amount of financial leverage is 3609, with a variance of 1,996. The average net exports of manufacturing enterprises are 3.193%, with a standard deviation of 1.302%. To examine the decline in exchange rates impacts a corporation’s financial performance, macroeconomic variables with a value of 4.386 and a variance of 0.323 are employed.

Additionally, identical mean values for days-old receivables and days-old payments suggest that suppliers are the primary source of commercial credit for manufacturing organizations rather than end users. It suggests that some of the credit obtained by the business from its suppliers is given to customers. This attitude is consistent with the assumption that big businesses would use their monopoly status to enhance the conditions of their commercial credit constraints and to get more favorable commercial loan terms for their customers. The average age of companies is 3.333, with a variance of 0.658%. The size distribution has a mean and a standard deviation of 10.851 and 4.277, respectively. The findings show that enterprises’ maximum and lowest financial leverage levels are widely variable, but their high debt levels over the research period differ significantly between companies. The ROA also confirms the enormous disparity between the minimum and highest values for the largest Size. Through a more open and practical currency conversion cycle, the idea promotes the significant average value of major organizations. As a result, banks extend them additional credit.

The link between the variables may be determined using the correlation coefficients in . According to a correlation study, Pakistan’s chosen manufacturing enterprises have an expected link between return on assets and profitability and various short-term activity-based accounting measure components. Profitability and the cash conversion cycle are shown to be positively correlated. Cutting the time spent on purchasing raw materials and collecting revenue from sales of products might increase profitability. shows the correlation matrix, which looks at the coefficients of the factors that affect the cash conversion cycle and profitability.

Table 2. Correlation matrix.

First, the cash conversion cycle, one of the typical management indicators for working capital, correlates favorably with asset return at a rate of 0.002, with a statistically significant level of 1%. Furthermore, it correlates negatively with ER-0.500 (Doruk & Ergün, Citation2019). At the 1% level, CCC exhibits a strong negative link with NE (−0.192) and a significant relationship (0.791) between RD and PD. The critical components of CCC are ITR, RD, and PD; when one of these variables rises, CCC will as well, since CCC = (ITR + RD-PD). CCC will naturally increase due to the value of RD, the critical component of CCC, since RD and CCC have a positive correlation. It represents the truth if businesses operate well and reduce the time it takes to collect money from RD.

On the one hand, a rise in payable days slows the cash conversion cycle and makes managing working capital easier. As the CCC falls, businesses will have more money to expand their production operations, helping boost asset returns. A decline in CCC and ROA are entirely connected, so a decline in CCC would effectively manage working capital and increase the company’s profitability. The relationship between CCC and the ER is unfavorable and noticeable. The coefficient value is −0.500, favoring a shortening in the CCC due to an increased currency rate (Widyastuti et al., 2017). The outcome suggests that typical businesses should try to buy inventory at a trim level, lower the RD, and increase the PD to shorten the CCC time.

High depreciation of exchange rates is detrimental to the profitability of businesses. Assume that corporations do not employ risk management measures, such as swaps, hedging, forward again and futures contracts, options, etc., to regulate currency prices. Corporate accounting management should work differently under these conditions. According to the data presented, returns on assets have a significant negative association with leverage of −0.023 and a dynamic, positive correlation with RD of 0.059. ROA has a substantial negative connection with FL, ER, Age, and NE but a positive correlation with RD, PD, & CCC Size. A little negative association between ROA and the age of the enterprises was discovered in the present research. The relationship between business size and return on assets (ROA) is positive and substantial, indicating that larger organizations have much higher ROAs than smaller ones.

Additionally, RD*ER and PD*ER were utilized to examine how the variables used to examine how NE and ER impact various activity-based accounting components interacted with one another. These are positively and crucially related to ROA. It has been found in the current research that ER and NE have a bad association. As was previously noted, there is a negative link between the two; a rise in ER (devaluation in PKR) would raise the NE. It supports the latest trade theory in economics.

The exchange rate, net export age, and financial leverage affect ROA. It can be because the firm needs more credit purchases as it expands. As the exchange rate changes, the short-term financial situation changes the long-term because an early payment to creditors is required. The exchange rate and return on assets are inversely correlated. Because the net export will grow as the exchange rate depreciates and the depreciated ER input cost may fall, the ROA will decline as ER increases. In a typical scenario, NE growth will raise the firm’s sales volume, enhancing profitability.

The ROA is parallelly associated with NE and ER (profitability). The corporation devalued due to currency rates should reduce its inventory, significantly influencing ROA. If a significant depreciation in the exchange rate is anticipated, a negative correlation between the ER and ITR benefits the company. The company has to spend more on inventory stock and manage inventory on a cash basis. A business wishes to utilize fewer ITRs since it spends money on keeping the stock stuck with it rather than recycling it for the inventory stock sold. Let’s say the finance manager wishes to lower the amount of inventory. In such a situation, they need to exercise caution about a few new elements, including inventory stock’s carrying costs, market demand, a lack of supply, and cost considerations about perishable inventory stock.

Furthermore, RD and NE −0.229 have a negative correlation. This study’s contribution is that it is nonsensical for the net export to decline as RD rises. Export companies should concentrate on it and manage it according to the circumstances. Here, net exports and CCC also have a negative connection, suggesting that exports will decrease and make sense as CCC increases. When an exchange rate depreciates, the instance company should adjust its export strategy. This relationship between RD and ROA is favorable; nevertheless, it is not advised because the companies’ earnings increased due to debtors delaying payments. However, it is acceptable if the payment arrangement is agreed on the home currency in cases of significant domestic currency depreciation. The corporation wouldn’t have enough funds to take the procedures forward. The productivity would thus support ER financial theories if it had a negative relationship with ER.

If businesses establish good relationships with their debtors, they will make more money because they pay their bills on time. At 1%, the correlation between PD and ER is negative (−0.489) and highly significant. Furthermore, there is a strong positive association between ROA and PD. Businesses will be more profitable due to having more PD since it will last longer to cover their payables. As businesses regularly want to recoup significant savings in prompt payments, the high-speed payment procedure may increase the ROA for industrial organizations. When a value is considered a kind of monetary revenue that might affect operating income, caution should be used. While a rise in PD benefits a company by giving it more time to pay off its obligations, it also hurts its reputation for making payments when they’re supposed to ().

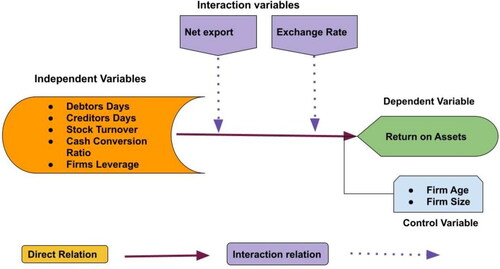

Figure 1. Conceptual model (Source: Authors).

3.3. Methods

To examine the interaction impact of export growth on the sales and profits of the chosen manufacturing companies from 1999 to 2019. we combine time series of cross-section analyses to create a balanced panel data set that offers ‘more relevant data, more fluctuation, less collinearity between variables, more degrees of freedom, and more efficiency’. Our economic estimate is based on the following model (Equaiton 1):

(1)

(1)

Where t is the period identifier, and i is the cross-section identifier, denoting the ith company for I = 1, 2, …, 249 t = 1, 2, 3, …, 21. ROA = Return on Assets, RD = Debtors turnover ratio, ITR = Stock Turnover ratio, PD = Creditors turnover ratio, CCC = Cash Conversion Cycle, FL = Financial Leverage Ratio, Size = Natural Logarithm of Sales, NE = Net Exports, ER = Exchange Rate (Open Market rate) Age = Numbers of years to be incorporate the business of the firms.

It was necessary to decide between using the Fixed Effects Method and the Random Effects Method to estimate EquationEquation 1(1)

(1) . We verify (Gujarati’s, 2004) results that estimates from the two methodologies may diverge when N is significant, and T is small. In cases when cross-sectional elements are not randomly selected from a larger sample, the fixed effects method is used. The Gujarati observations for our data set were supported or refuted using the Hausman specification test. Other diagnostic tests were also run on the data. Assuming that the coefficient estimates stay the same but the intercept changes from business to business, we could indeed account for how each business is distinct. EquationEquation 1

(1)

(1) is then changed to EquationEquation 2

(2)

(2) in the following way:

(2)

(2)

EquationEquations 5(5)

(5) and Equation6

(6)

(6) below illustrate the moderator variable in the regression model, also known as the interaction model, created using the variable interaction approach, an alternative to linear regression, to EquationEquation 2

(2)

(2) .

The impact of activity-based accounting on the bottom lines of the sampled businesses was examined using a panel data analytic approach. All of the data variables were logarithmically transformed. We combined the OLS, RE, and FE models for the panel data analysis. All summaries, evaluations, and determinations made during the research were based on the system GMM outcomes. Approaches based on dynamic data panel analysis were used to determine the existence of correlations between the study’s variables. The study above used a System GMM Estimation of Arellano, Bover, Blundell, and Bond (1995) to examine the interrelationships between the variables (1998). The model’s dependent variable was the difference in return on assets over time (L.ROA), while the independent variables were the initial difference in return on assets (L.ROA).

Estimating model parameters using the generalized method of moments (GMM) involves finding the slightest difference between the instrumental variables’ population moment and the sample moment. The GMM estimator is described in further depth below.

Defining the link between the dependent and independent variables is the first step of the GMM estimator’s model formulation. Fitting a set of moment conditions is how the GMM framework estimates model parameters. The underlying economic link between variables is captured by the moment conditions, which are functions of the model parameters and data. Some qualities must be satisfied by the moment conditions, such as the ability to isolate the parameters of interest and the presence of adequately informative moment circumstances. A collection of instrumental variables uncorrelated with the error term but associated with the independent variable in the model is needed for the GMM estimator. Moment conditions are built with the use of instrumental variables. The GMM estimator uses a weight matrix to assign relative importance to individual moment states. Many weight matrices, such as the identity matrix, the ideal weight matrix, and the iterated optimal weight matrix, are accessible and may affect the estimator’s performance.

The GMM estimator minimizes the difference between the population moments and the sample moments by determining the values of the model parameters. To do this, we must determine the range of values for the model parameters that satisfy the moment criteria. A quality function, often the square of the difference between the population and sample moments, measures how far apart the two sets of moments are. When the model parameters have been estimated using the GMM estimator, they may be tested for validity and significance using hypothesis testing. The GMM estimator provides a versatile and practical approach to parameter estimation in models with available moment conditions and instrumental variables. It has widespread usage in economics, finance, and other areas where nonlinear interactions between variables need parameter estimation.

3.3.1. Dynamic panel model

Numerous organizations, financial institutions, economies, and banking systems are character-driven issues that employ data panel structures to concentrate on adjustments. It is essential to allow dynamics to assess several parameters during the primary phase continuously. The carriage of a lag-dependent variable and the explanatory variables shows dynamic relationships. The evaluation of the following equations exemplifies this technique of assessment.

(3)

(3)

(4)

(4)

In the nonlinear dynamic model, the net exports and exchange rate have an interaction (moderator) influence ().

(5)

(5)

(6)

(6)

Table 3. Descriptive statistics.

4. Empirical results and discussions

4.1. Estimated regression results

There are 249 companies in the sample. The similar intercept (1) in EquationEquation 3(3)

(3) above must be eliminated in the FE Panel Regression. This strategy displayed our findings; hence, a similar intercept was kept. The estimates of the coefficients produced by the combined OLS, FE, and RE estimations for endogeneity were inaccurate and biased. No matter how endogenous the system is or how persistent the dependent variable is, the GMM estimate system is the most dependable option in these circumstances (Kwenda & Holden, Citation2014). It is particularly true when the dependent variable’s initial lag is the coefficient of interest. For system-GMM estimations, several corporate characteristics, such as RD, ITR, PD, CCC, Age, Size, NE, ER, and FL, are employed as endogenous types (in both one and two steps). Firms and year dummies are simultaneously included in system models as exogenous variables. According to GMM estimations, 249 enterprises in the system utilize 201 instruments. For the system GMM instrument, all individual endogenous variables’ second to fourth lags are employed (individual instruments for each period unless collapsed) ().

Table 4. Simple leaner regression.

shows the results of system GMM diagnostic tests. All approximation factors are jointly significant at the 0.01 level, as determined by the Wald test. According to the F test, the model has been accurately fitted. The AR (1) and AR (2) serial correlation tests reveal no second-order autocorrelation issues. It is conclusive evidence of the instruments’ accuracy and the validity of both system GMM model versions. Similarly, the Sargan result confirmed the validity and noncorrelation of the system GMM estimation tools with residuals. A two-step system GMM estimate with robust options produces more accurate estimates in heteroscedasticity residuals than a one-step system GMM estimator.

The system GMM and FE estimated results are reported in . There are two reasons why RE's findings are excluded. First, the LM test determines that a RE estimate is inappropriate, and any coefficients acquired by this estimate are identical to those provided by the pooled OLS. According to the Hausman test, RE estimator estimates do not outperform FE estimator estimates. According to the estimation above, the relationship direction between all firm-specific characteristics was robust. The selection of the dynamical panel model (DPM) in this study was supported by the positive and statistically significant (p0.01) coefficient of the first leg of ROAt-1 calculations. There were discrepancies in the ROAt-1 coefficient sizes amongst estimators. In the presence of an upwardly skewed connection between the first lag of ROA and unobserved moment firm-level variability, the FE estimator produced coefficients of 0.3019 and 0.4349 for the first leg of the dependent variable (Bond, 2002).

Additionally, the FE estimation performed adverse when there was a small panel. The coefficients of the OLS Estimator and FE estimators were 0.284 and 0.3430, respectively, obtained using the two-step system GMM. Consequently, the two-step system GMM's coefficient seemed unlikely to be skewed. contains the findings of the two-step system GMM estimation, and owing to the two-step system GMM estimation’s superiority, only these results were discussed. It was significant to the 0.01 level and had a beta of 0.284 for ROAt-1. The positive and sub-unity coefficients suggested that Pakistani manufacturers sought (ideal) ROA ratios that would persist over time. The initial lag of the ROA coefficient, or (1 – 0.282), was used to calculate how quickly enterprises altered their ROA ratio. These positive coefficients demonstrated that manufacturing companies in Pakistan modified their trade lending criteria from 72% to 73% to meet their profit objectives.

The coefficients for ROAt-1 were higher than 0.282. Businesses or companies listed on PSX have shown that they like their strategies to make money reliable and consistent. It may be because making adjustments is less expensive now. Many firms cannot afford significant adjustments to reach their objectives or achieve their ideal ROA. Due to the complexity of organizations’ ROA policies and the high cost of making changes, it can be assumed that companies only make small, slow changes to their policies.

RD was positively connected with ROA to their clientele, with the coefficients being significantly positive at the 0.01 level. Companies’ ROA would increase based on the metric, 1 unit drop in RD, while all other elements remained constant. The data supported the debtors’ (trade credit) concept, demonstrating that if businesses extend more payment terms, they should do so in anticipation of a higher return on their assets. Under the findings, firms used the tradeoff strategy, financed payables with accounts receivable (financial assets) (current liabilities). Companies that made more credit purchases were willing to sell credit to customers. A positive correlation between RD and ROA also supported the idea that companies who owed outstanding debts to their suppliers would extend this to their consumers by enabling them to pay later.

PD is also included in the regression model with ROA as the dependent variable to evaluate the activity-based accounting finance method. The PD coefficient’s positive value means that adjustments (delays in payments of one day) impact the profit by 1.3% on one payable day. It shows that businesses fall behind in a forward-thinking financial plan. When ROA is the dependent variable, this regression Equation 8 considers PD's exercise accounting financing strategy. When considering the cash conversion cycle, the number of days due by account must be as high as is practical. However, past studies’ results are mixed; some find positive effects, while others find negative ones.

Since the value of FL increased by 2.71% in ROA, the company’s success is negatively correlated with FL. The FL has a regression association and significant value because a one-unit increase in FL would lead to a 2.71% increase in ROA. The company’s performance improves, and vice versa. Increased debt has a favorable effect on a company’s profitability. The findings support the tradeoff and pricking order theories by demonstrating that growing deficits enhance business performance. The business’s debt and outcomes are both subpar. Numerous studies show a negative relationship between dividends paid and leverage. The dividend payment degradation brought on by financing costs may be detected early when businesses must cover fixed costs. The tradeoff theory backs up this assertion.

Based on the results presented in , policymakers and decision-makers in the financial management of businesses should consider the following implications:

Concentrating on firm-specific traits: There was a vital link in every direction between all firm-specific traits. To increase a company’s profitability, regulators and decision-makers should concentrate on key factors, such as the cash conversion cycle, debt-to-equity ratio, and accounts receivable. Think about the tradeoff technique: According to the research, businesses use the technique to finance payables using accounts receivable (financial assets) (current liabilities). While handling a company’s finances, policymakers and decision-makers should consider this approach. Pay attention to payment delays: The PD coefficient’s positive value means that adjustments (one-day payment delays) reduce earnings by 1.3% on a single payable day. Hence, the effect of late payments on a company’s profitability should be taken into consideration by legislators and decision-makers.

Effective debt management: The findings demonstrate that rising debt benefits a company’s profitability. But, legislators and decision-makers should efficiently manage debt and avoid letting it get out of control since doing so might hurt a company’s performance. To increase a company’s profitability, policymakers and decision-makers involved in financial management should employ the two-step system GMM estimator, concentrate on firm-specific traits, take into account the tradeoff strategy, pay attention to payment delays, and manage debt skillfully.

4.1.1. Interaction effects of exchange rate and net exports

Overall, the findings in indicate that the rate of exchange and net exports function as moderators and mitigate the influence of receivables on the financial performance of manufacturing enterprises. It has a calming influence on Pakistani manufacturing companies’ credit purchasing and sales behavior toward clients at home and abroad. This section will discuss the moderation regression analysis technique’s estimated findings and explore the effects of the exchange rate, net exports, and other micro-variables on company performance. The findings of ’s mathematical Equations 9 and 10 indicate that the length of the payables’ coefficient had a favorable rather than a negative impact on the corporation’s performance as measured by the ROA. In contrast, the coefficients for receivables had a negative impact. It states that the ratio of payables to receivables should also be decreased when CCC is decreased. In activity-based accounting, a reduction in PD will shorten the time cash is twisted, which will aid in raising ROA. But the most recent research results show that the CCC, RD, and ITR have had an inverse relationship with the ROA. The positive correlation between ITR and ROA indicates that when inventory stock increases, ROA is favorably impacted. It, in turn, leads to increased sales prospects for the business, demonstrating improved financial performance. As a company, improving its turnover ratio of inventories raised the cost of maintaining inventory goods, which had a detrimental effect on its financial position. The businesses’ financial operations will also impact them.

Table 5. Interaction effect by Net Export.

It is clear from the data in and the discussion that the currency rate and net exports serve as moderators that lessen the impact of receivables on the financial performance of Pakistani manufacturing companies. This moderating impact has a soothing effect on Pakistani manufacturing enterprises’ credit buying and sales conduct toward customers locally and worldwide. The data also reveals that although receivables negatively influence the company’s financial success, the duration of payables has a positive effect. It is suggested that businesses reduce the payables to receivables ratio to maximize their cash conversion cycle (CCC) and, as a result, their return on assets (ROA). However, the current study’s findings indicate an adverse link between ROA and CCC, inventory turnover ratio (ITR), and receivables turnover ratio (RTR). The relationship between ITR and ROA is favorable, indicating that as inventory stock rises, ROA is positively influenced, resulting in better financial performance.

The effect of inventory management on financial performance must also be considered. Although raising the cost of keeping inventory products may negatively impact the company’s financial situation, boosting inventory turnover ratios can also result in higher sales opportunities and better financial performance. The results indicate that businesses should examine possible trade-offs between inventory management and financial performance and control their payables, receivables, and inventory levels to increase their CCC and ROA ().

Table 6. Interaction effect by Exchange Rate.

Table 7. Hypothesis tests.

The element of ER interacts with RD in the second moderate regression equation model, which is investigated. The independent variables are RD, ITR, PD, CCC, FL, NE, ER, Age, Size, and (RD*ER). The first interaction variable displays ROA lag’s beta value of ROA 0.0485 when (RD*ER), PD*ER, and FL* ER are applied. At 1%, it is substantial (Lin & Wang, Citation2021). The beta value of ER is considerable, with ROA −1.812 and NE −0.0550. If ER increases by one unit, ROA increases by 18.12%, whereas it falls by 5% in the case of net export. It implies that ER is interfering with the company’s ROA. The significant beta value of NE is (−0.0550). Equations 9 and 10 show that ER moderates the firm’s financial performance since RD*ER, PD*ER, and FL*ER have large beta values in both circumstances. These results support earlier research that showed that receivables behavior benefits a corporation’s economic success. We don’t reject the null hypothesis because all interaction coefficients are significant in all regression models.

The experimental Equations 9 and 10 in and further investigate the significance of the beta value of a lag-dependent variable, demonstrating the consistency of the system GMM model in the analysis to infer the study’s findings. The correlation issue is irrelevant if the system GMM tests for AR2 P values are negligible. The results of two alternative tests of overidentifying constraints are then examined, along with the consequences of choosing to lower the number of the estimated model used to calculate the Sargan test statistic. The standard test linked to Sargan (Citation1958) and Hansen (Citation1982) (the Sargan test), the test given by the minimized value of the GMM similarity measure under the continuous automatic update procedure (Hansen et al., Citation1996), and the reliable ‘Exponential Rotating Parameter’ test proposed by Hirano et al., are all taken into account in this study (1998).

After employing the company’s unique intercept during the study of the system GMM, the beta of RD is negative and substantial. Let’s compare our findings to financial regulations at the point when businesses begin to collect receivables. Enhancing its cash position and enabling the company to acquire and sell more merchandise improves trade activity. The firm will expand if the amount of activity in the business increases. The receivable days’ coefficients are negative. It demonstrates that if there is a delay in receiving payment from accounts receivable, postponing paying its bill may result in the retention of cash discounts and significantly impact the cash inflows to this business’s operations, potentially disrupting profitability. ITR has a substantially positive and considerable effect on ROA. Because the ER affects the ITR, it indicates that profit may be raised by regulating the ITR or maintaining inventory for a long time. After all, when the (RD*ER) is regressed, the beta value drops, increasing company profitability. Numerous studies have revealed that ITR significantly increases a company’s ROA.

The fact that the PD factor is positive suggests that decreasing profitability would result from extending the payment time. Because the business takes longer to pay its debtors, activity-based accounting volume decreases, increasing profitability, which is why these results defy financial theory. Numerous types of research simultaneously find a negative and substantial association. An interaction variable called RD*ER regresses the coefficient value that has a beneficial impact on ROA. This ER has an interaction impact since it shifts the beta values of every other variable in the model. The coefficient values of every other variable change as the exchange rate devalues. For every one-unit reduction in FL, the ROA fell by −7.2%, and vice versa. Increased FL indicates that excessive debt levels negatively influence corporate earnings. Firms’ ROA declined when age grew by 1% because age negatively correlates with ROA. The firm’s profitability will rise by 5% for every unit that Size’s value rises, and vice versa. The interaction term coefficients ER*RD, ER*PD, and ER*FL deviate considerably from zero at the 0.01 level. ER is thus not a pure moderator but rather a quasi-moderator. The coefficient of RD is calculated by Equation 10 to be 0.405, which is significant at the 0.01 level. The coefficient of RD shows that as ER increases, the relationship between RD and ER gets more robust, and the coefficient for the interaction term is positive and significant.

The outcomes align with expectations: a decline in the value of the Pakistani Rupee causes an increase in ROA. As a result, more consumers are using the alternative credit (trade credit) available. Manufacturing companies boost their trade credit to increase credit sales in reaction to declining ROA and vice versa. Growing collection days, therefore, have a favorable impact on ROA for Pakistani manufacturing companies. and provide the findings of the estimations of Equations 10 and 9 to investigate the NE moderating impact of ER on the link between ROA and RD. Only criterion (1) was validated as accurate. Equation 9's moderating regression analysis guideline states that the ER coefficient was significantly different from zero at the 0.01 level but was not significantly different from Equation 10.

In contrast, at the 0.01 level, the interaction term coefficient (RD*ER) did not vary substantially from zero. Similar in all instances of interaction factors. As ER increased, the interaction term coefficient showed a connection between ROA and RD Progressive. One reason for this change in the relationship’s strategy might be that increased RD decreased consumer demand for their goods. On the other hand, the link between ROA and RD is significantly moderated by ER. Overall, there is agreement that ER acts as moderation and, to some degree, has a considerable buffering influence on manufacturing businesses’ credit sales behavior.

The results of equation 10 indicate an inverse link between ROA and ER for industrial companies. At the 1% level, the RD coefficient of 0.405 is noteworthy. This outcome is in line with expectations: a growth in RD causes increased exports from domestic markets to foreign markets. Consequently, those markets have more demand for the goods local businesses produce than vice versa. If a manufacturing company’s ROA reflects the demand for its goods from its clients, its RD rises as its financial standing increases. The information that came before indicates that the manufacturing company’s ER and RD ties have led to a significant boost in ROA. A moderating regression analysis approach is used to assess the moderating influence of ER and NE on the connection between RD, PD, FL, and ROA, utilizing the findings of Equations 10 and 9 provided in and . The findings demonstrate that Equations 10 and 9 differ (i.e., 0).

Consequently, it was shown that the framework for moderating regression analysis is sound. It indicates that suppliers to manufacturing companies expanded supplies on a credit basis when the value of the Pakistani Rupee fell. A coefficient value for the interaction effect ER*PD shows that manufacturing businesses use fewer credit sales and more trade credit when ROA increases.

4.1.2. Implications of the study

Various implications of the study can be derived from the paper ‘Moderating Impacts of Net Export and Exchange Rate on Profitability of Firms: A Two-Step System Generalized Method of Moments Approach’. Exchange rates significantly influence the profitability of enterprises. The research discovered that changes in exchange rate directly impacted a company’s profitability, with an increase in profitability after a currency depreciation. It suggests businesses should monitor exchange rate swings and modify their operations as necessary. Net export has a favorable impact on a company’s profitability. According to the research, businesses that participate in international commerce are more likely to be profitable than those that do not. It implies that businesses should increase their export-related operations to boost profitability. The relationship between net export and exchange rate modifies company profitability significantly. According to the research, a depreciated exchange rate environment has a more beneficial impact on profitability than a stable one. It suggests that businesses involved in net export activity might profit from a depreciated exchange rate.

The results of this research have consequences for those who decide on policy. According to the research, governments may increase company profitability by fostering a climate encouraging net export business. It may be accomplished by establishing rules that promote exports while discouraging imports. Investors might also benefit from the research. Investors may use the results of this research to make investment choices by taking the exchange rate and net export operations of the companies they are investing in into account. Businesses participating in net exports and operating in a depreciating environment will likely be more lucrative and more appealing to investors. This research emphasizes the significance of considering the moderating impacts of net export and exchange rate on business profitability in general. By comprehending these consequences, businesses may make educated decisions to boost their profitability, and investors and governments can utilize this information to make smarter choices.

5. Conclusion

The value of activity-based accounting management in corporate financial management cannot be overstated. Managing the tradeoff between return on assets and short-term funding is crucial at the business level. This research aimed to examine the relationship between foreign credit sales and credit purchases in a relationship with return on assets having an interaction effect of exchange rate and net export. It would help enterprises understand the nature and magnitude of the effect of net export components (firm-level total exports minus total imports) on firm return on assets. This acquaintance is vital for managers seeking to increase their earnings; eventually, it is worth it. We found that as the exchange rate (Pak Rupee) depreciates, the net export negatively impacts the firms’ return on assets. Financial leverage does have a negative impact, proving that shareholder funds are very supportive in such circumstances. The debtors need to get the money they owe back when the credit sales agreements were made in a strong currency while they were due.

The exchange rate and the return on assets are negatively correlated. It suggests that high profits are associated with low exchange rates. Still, it is reasonable to consider that Pakistan’s manufacturing sector accounts for most of its foreign currency inputs and Pakistan Rupee turnover under high exchange rates. When system GMM research techniques were applied, it would also demonstrate a negative relationship between net export and the company’s return on assets: when exchange rates depreciate, business earnings decline, current costs increase, and a poorer return on assets is recorded. Exchange rate depreciation and net exports substantially impact the relationship between CCC and the company’s return on assets. The findings demonstrated that a robust CCC management approach gives companies a greater return on assets. It may imply that the Pakistani manufacturing sector is not incentivized to produce a lot of CCC, which is not the case. Businesses use high levels of financial leverage when they are having financial problems or when the exchange rate is high, but this has a negative effect on their return on assets, exposes them to significant business risks, or causes them to default on payments owing to cash flow issues, for a more convincing conclusion on the impact of the CCC and financing arrangements on the company’s return on assets.

Additionally, various factors must be categorized to understand the ROA variation better. The impact will be more adverse if we include net export as an interaction variable in an empirical model. Positive implications of exchange rates include improved returns on assets when the Pakistani Rupee depreciates and businesses lengthen the cash conversion time.

This work contributes significantly to the literature by offering suggestions for developing this new subject to influence further investigations and actions. This longitudinal study’s key finding is that, although the field is expanding significantly, most of it is doing so quickly. The current research shows that when the currency’s value declines, businesses may settle their debts earlier and earn more significant returns on their assets. This study adds to the body of knowledge in that field by showing that the exchange rate and net export have a calming effect on the firm’s return on assets.

The macroenvironment has impacted the internal financial choices of the corporation. According to Melitz (Citation2003), it also helps expand a new trade theory. When trade barriers are removed to increase global competition, low-productivity companies previously shielded from the competition are forced to leave the market, enabling high-productivity companies to increase their revenue. Consequently, it raised the nation’s total average productivity on a macro level. Individuals become wealthier due to the natural selection of businesses worldwide; this increase in average productivity corresponds to an increase in people’s income. As a firm selects less debt and more equity financing, it may enhance costs and benefits when the exchange rate depreciates in an economy like Pakistan, where the currency depreciates substantially. This research also adds to the tradeoff theory of capital structures. It has also been shown that Pakistan’s manufacturing sector should fund internally using retained profits rather than borrowing money from external sources before issuing fresh equity into the market.

Limitations of the study

As indicated below, no research can be devoid of challenges.

Since the State Bank of Pakistan personnel were the source of the secondary data used in this study, the investigation focuses only on the validity and correctness of the secondary data. The research is limited to 20 years of data, i.e., from 1999 to 2019; as a result, a complete investigation comprising an average time, which may provide somewhat mixed outcomes, could not produce significant inferences. The impact of the data source may alter estimate results and explain analysis findings.

This study is based on 249 manufacturing enterprises in Pakistan, also taken from businesses registered with the PSX. As a result, the sample-picked businesses’ data determines how accurate the judgments are. The results can be somewhat equivocal if the prospective researcher spends more time on the sample units.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Table 1. Operational definitions of the variables.

Additional information

Funding

Notes on contributors

Sarfraz Hussain