?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Vulnerable households often tend to decrease their human capital expenditures, like education and training, to maintain food and non-food (clothing and housing) expenditures when any income shock occurs. Financial inclusion acts as a safeguard to maintain the stability of human capital investments in households because it provides an opportunity to save additional resources to invest for productive purposes. This study examines the impact of financial inclusion on the expenditure pattern of slum households in Bangladesh using propensity score matching. Four outcomes—food, non-food, educational, and health expenditure—are considered in this study. A heterogeneous analysis and inverse probability weighted regression adjustment estimation were conducted as robustness checks. Our results demonstrate that financial inclusion has only a significant positive impact on slum households’ educational expenditures, while financial inclusion has no impact on food, non-food, or health expenditures.

Reviewing editor:

1. Introduction

Informal settlers like slum households, the most vulnerable households in any society because of their lack of resources to combat chronic poverty, are characterized by extreme hunger, gender inequality, low educational attainment, scarce health facilities, and low financial inclusion. Approximately one in seven people of the world are currently living in slums (this is projected to rise to one in four by 2030), with almost 1.6 billion people living without adequate shelter. In developing countries, nearly one in three people reside in slums. In certain countries, 90% of the urban population resides in slums (Thomson et al., Citation2020). In Bangladesh, 95% of slum dwellers live below the poverty line and fall within the fifth-income quintile (Bangladesh Bureau of Statistics, Citation2017). Struggling to afford food, clothing, and shelter, children from slums face an uphill battle pursuing education. Often, children born in slums have to work to support themselves, and education becomes a far-fetched dream. To uplift the living standards for slum households, both household and public educational expenditures need to be boosted. This paper examines the impact of financial inclusion on slum household expenditures and offers policy recommendations for addressing their vulnerabilities.

Financial inclusion is regarded as a vital factor in promoting a nation’s economic growth and development since it makes credit, savings, payment, and insurance alternatives more easily accessible to a wide range of individuals. The ultimate purpose of financial inclusion is to make financial services available to those who are "unbanked" so they can raise their standard of living and contribute to the growth and development of the economy. Slum dwellers are a major part of these unbanked categories. Financial inclusion is also considered a policy tool to stimulate the productive expenditure of vulnerable households. Educational investment is considered an indicator of a household’s willingness and capacity building in relation to overcoming the burden of economic vulnerability and inequality.

Financial inclusion can be defined as the accessibility, usage, and availability of financial services such as deposit, credit, and insurance products. Financial inclusion is often argued to be a policy tool for increasing the investment capacity of economically vulnerable households because it provides an opportunity to save additional resources to invest for productive purposes like education and training. However, previous research findings did not conclusively determine the impact of financial inclusion on the expenditure pattern of a vulnerable household. This study examines the impact of financial inclusion on the expenditure pattern of slum households in Bangladesh using a quasi-experimental identification strategy called propensity score matching.

The number of people living in urban slums in Bangladesh continues to grow with the influx of migrants from rural villages. Approximately 0.6 million people live in approximately 3,000 slums within Dhaka (Islam et al., Citation2021), and 75% of slum households live in a single room (Seidu et al., Citation2021). The lives of children living in slums are characterized by abuse, child labor, child marriage, school dropouts, and malnutrition. The school dropout rate of children aged 8–14 years in Bangladesh is 14% (Numan & Islam, Citation2021; Pal & Bandyopadhyay, Citation2022). The Multiple Indicator Cluster Surveys and Child Well-Being Survey indicate that living conditions for people in the urban slums of Bangladesh are worse than those in rural areas.

Based on the World Bank (WB) international poverty line ($2.15 per person per day), the poverty rate in Bangladesh is 14%. The poverty rate among slum dwellers is considerably higher than the national poverty rate. Widespread poverty in these communities hampers efforts to provide children with education, as educational investment is greatly reduced by spending on housing, food, and other basic needs. Even as wages remain constant, food prices continue to rise over time due to inflation and other causes. Most children living in slums attend government primary schools, where the quality of education is generally poor. According to the WB, 58% of Bangladeshi children aged between 10 and 14 (typically in Grades 5 − 8) are unable to read at a Grade 2 level (Mccarthy & Pearlman, Citation2022). This study examines ways to improve the education received by children living in slums by increasing household-level educational investment through financial inclusion.

Banks and microfinance institutions have established diverse ranges of financial services to reduce poverty among slum residents, who tend to reduce educational investment when any income shock occurs, preventing their children from escaping poverty through education (Duncan et al., Citation2017). Ultimately, financial inclusion leads to savings with the respective financial institutions and organizations (Dixit et al., Citation2019). Micro-financial services are similar to traditional bank accounts but are designed for individuals to deposit small amounts of money (Alawattage et al., Citation2019). These services are characterized by flexible withdrawals, no service fees, and no prescribed minimum deposit amounts (Babajide et al., Citation2015).

Apart from the dedicated microfinance institutions, private commercial banks also offer no-frills accounts targeted at economically vulnerable households, such as those in slums. Financial service users can deposit amounts as small as two cents per week. Moreover, if an individual maintains a strong relationship with the financial service provider by making consistent deposits, the account holder may be viewed as a successful candidate for a micro-loan. As such, banks and microfinance institutions provide a platform for households to save, and over the years, residents of Bangladesh have embraced them (Ahmed et al., Citation2016). These service providers hold a total of BDT (Bangladeshi Taka) 37,914 million (approximately USD 380 million) as microsavings, while BDT 176,153 million (approximately USD 1762 million) has been distributed as microloans (Hossain & Naimul Wadood, Citation2020).

The study uses propensity score matching (PSM) to examine the impact of financial inclusion on food, non-food (clothing and housing), education, and health expenditures. Bangladesh has been selected as the research area because the country represents one of many developing countries struggling to overcome extreme poverty. Financial inclusion is estimated based on a household’s access to and usage of financial services, measured by a dummy variable describing whether a household makes deposits into a bank account or a micro-financial institution. To the best of our knowledge, no previous studies have focused on slums as units of analysis in estimating the impact of financial inclusion on expenditure patterns. Our study attempts to address this research gap by focusing on financial inclusion among slum dwellers in Bangladesh. The findings suggest how policymakers in developing countries might design financial products so that financial inclusion can be an effective policy tool to ensure the welfare of vulnerable households by stimulating human capital expenditure in slum households.

2. Literature review

Numerous studies have delved into various dimensions of financial inclusion, with some focusing on the correlation between financial inclusion, economic growth, and development (Ahmad et al., Citation2020; Ifediora et al., Citation2022; Sarma & Pais, Citation2011). Sarma and Pais (Citation2011) scrutinized the close relationship between levels of human development and financial inclusion. Similarly, Ahmad et al. (Citation2020) asserted that financial inclusion is linked to economic growth and development. In contrast, Ifediora et al. (Citation2022) argued that the usage dimension of financial inclusion does not have a significant impact on economic growth. A few studies have concentrated on the impact of financial inclusion on financial stability (Ratnawati, Citation2020; Pal & Bandyopadhyay, 2022). Ratnawati (Citation2020) argued that financial inclusion has a partial association with financial stability. Similarly, Pal and Bandyopadhyay (2022) contended that financial inclusion is strongly associated with financial stability. Several studies have explored ways to achieve financial inclusion through micro-financing and financial literacy (Elzahi Saaid Ali, Citation2022; Khan et al., Citation2022a; Citation2022b; Sajuyigbe et al., Citation2020). Elzahi Saaid Ali (Citation2022) posited that Islamic micro-finance promotes financial inclusion, while Khan et al. (Citation2022a, Citation2022b) argued that financial literacy is strongly associated with financial inclusion. Furthermore, many studies (Roy & Patro, Citation2022; Saluja et al., Citation2023; Takmaz et al., Citation2022; Zeqiraj et al., Citation2022) have focused on determining factors and barriers to attaining financial inclusion. Takmaz et al. (Citation2022) explored the determinant factors of regional disparity in financial inclusion (FI), whereas Zeqiraj et al. (Citation2022) examined corruption control, effective governance, stable political situations, rule of law, regulatory quality, and transparency and accountability as determining factors of financial inclusion across seventy-three developing countries. Roy and Patro (Citation2022) highlighted a consistent gender gap in financial inclusion, while Saluja et al. (Citation2023) argued that a male-dominant societal structure, psychological factors, lack of income, lack of financial literacy, lack of financial accessibility, and ethnicity are the six main barriers to the financial inclusion of females.

Several empirical studies have been conducted lately to explore the impact of the availability of financial services on poverty. A significant study on the impact of setting up rural bank branches on poverty reduction was conducted by Burgess and Pande (Citation2005), stating that expansion of rural bank branches in India helped to reduce poverty, and opening bank branches in rural unbanked locations in India is associated with a reduction in rural poverty rates in those areas. Similarly, Allen et al. (Citation2013) argue that increased bank penetration by commercial banks has a positive and significant impact on households’ use of bank accounts and bank credit, particularly those with low income, no salaried job, and less education in Kenya, suggesting that increased bank activity can impact poverty and income. Many developing nations have launched state-led financial inclusion initiatives; however, there is a debate over how effective these programs are in raising welfare. Considering the policy initiatives on financial inclusion in India, Chakrabarty and Mukherjee (Citation2022) assess the diversification in consumption expenditure and utilize this as a welfare indicator by using Theil’s entropy-based index using panel data collected at the household level across the nation. They uncover the evidence that increased financial inclusion leads to more diversification in non-food products in India.

Financial inclusion is widely considered a policy tool for improving the living standards of economically vulnerable households, such as slum dwellers in Bangladesh. Financial inclusion helps economically vulnerable families living in slums in Bangladesh improve their lives by providing financial literacy, increasing savings, and providing access to credit during financial shocks. However, the impact of financial inclusion on the income mobility of vulnerable people remains inconclusive. The findings of previous studies in this area of research can be divided into two groups. The first group of studies claims that financial inclusion reduces poverty, whereas the second group argues that it has no impact on poverty reduction. Sarpong and Nketiah-Amponsah (Citation2022) argue that financial inclusion lead to inclusive growth and Pitt and Khandker (Citation1998) argue that micro-financial inclusion reduces the poverty of women in Bangladesh. Similarly, Nsiah et al. (Citation2021) and Dogan et al. (Citation2022) argue that financial inclusion reduces poverty. Moreover, Tran et al. (Citation2022) argue that usage of financial services reduce multidimensional poverty.

Roodman and Morduch (Citation2014) question the reliability of the findings of Pitt and Khandker (Citation1998). Furthermore, Banerjee et al. (Citation2015) argue, using evidence from six studies, that the impact of microfinance on poverty is only modest but not transformative. De Mel et al. (Citation2022) used Randomized Control Trial to explore that digital financial inclusion has no significant impact on consumption. Park and Mercado (Citation2021) argue that financial inclusion has no significant impact on the reduction of income inequality, while the impact of access for the poorest to deposit products was explored by Brune et al. (Citation2011), stating that access to formal financial services through saving products enriches the life standard of poor households in rural Malawi. Moreover, Lee et al. (Citation2023) argue that financial inclusion has divergent impact on users based on their poverty levels.

Moreover, recent studies explored correlation between on financial inclusion and poverty. For instance, Omar and Inaba (Citation2020) and Polloni-Silva et al. (Citation2021) found that financial inclusion is associated with poverty reduction, using country level data. Similarly, Erlando et al. (Citation2020) and Khan et al. (Citation2022a, Citation2022b) explored association between financial inclusion, economic growth and poverty reduction, using time series data. Álvarez-Gamboa et al. (Citation2021) found that financial inclusion is associated with multidimensional poverty, using geospatial data. Though correlation studies provide some significant insights but correlation should not be considered as causation (Ksir & Hart, Citation2016). In contrast, some studies (Asongu & Odhiambo, Citation2023; Cao et al., Citation2023; Koomson & Afoakwah, Citation2023; Yang & Zhang, Citation2022) tried to explore causal analysis using instrumental variable (IV) approach. However, their IV fails to fulfill the exclusion restriction conditions as the distance of the household from the nearest bank considered as IV is supposed to have direct impact on income generation.

Most of the previous studies focused on rural borrowers or combined rural and urban borrowers; there has not yet been any independent research on Bangladesh’s urban slums. To the best of our knowledge, no comprehensive study has been conducted yet that examines the link between Bangladesh’s urban slums and financial inclusion. In light of the previous studies, three specific research gaps can be identified. First, no rigorous studies were conducted to identify the impact of financial inclusion in the context of slum households as units of analysis. Second, previous studies have focused on the impact of different financial inclusion segments, but holistic research has yet to be conducted. Third, no rigorous studies were conducted to estimate the impact of financial inclusion on expenditure patterns. This study will aim to address the three specific research gaps mentioned. Hence, we conducted a comprehensive and rigorous study to estimate the impact of financial inclusion on the expenditure pattern of households residing in Bangladesh slums.

3. Data source and covariate selection

The study covers all the districts of Bangladesh. The slum households represent the national slum population. The sample was drawn from the Household Income and Expenditure Survey (HIES) 2016–2017, a national dataset with observations of 46,076 households. After restricting the sample to households residing in slums, the sample size was reduced to 1,771 urban households. The HIES survey randomly sampled slum households, and so our study sample is representative of all slum dwellers in Bangladesh.

A household’s financial inclusion was measured by a dummy variable that describes whether a household has made deposits into a bank account or a micro-financial institution within the last 12 months. Households were assigned to the treatment group if they had deposited any amount of money in a bank or a microfinancial institution within this time frame. A total of 346 households were financially included. Various relevant explanatory variables were selected to represent the household’s characteristics: household size, cultivable land in acres, home area in acres, number of household members younger than 15 years old, number of household members younger than 40 years old, average age of household members, and the gender of the head of the household. Cultivable land refers to the land that residents of slums own in their native villages, from which they have migrated to urban areas.

The variables that influence the financial inclusion of slum households (Al-Shami et al., Citation2014) are household size, amount of cultivable land, home area, number of household members aged below 15 years, number of households aged below 40 years, average age of the household members, and male-headed households. These variables are likely to have a positive impact on financial inclusion. In addition, the selected covariates were also expected to affect the outcome variable, namely, expenditure pattern. All explanatory variables are listed in .

Table 1. Description of matching covariates.

4. Identification strategy

Households financially included (the treated group) were generally different from those that were not (the untreated group), even during the pre-treatment stage. Thus, a comparison of the treatment households with the untreated households would suffer from self-selection bias because of an imbalance in pre-treatment observed and unobserved covariates (Bari et al., Citation2022). Randomization in treatment assignment is the best gold standard (Troyer, Citation2022) to prevent self-selection bias because every unit has an equal chance of being assigned to the treated or untreated group. PSM is a matching method widely applied to reduce self-selection bias (Dehejia & Wahba, Citation2002) and aims to approximate randomization in treatment assignments to estimate causal treatment effect (Caliendo & Kopeinig, Citation2008; Dehejia, Citation2005; Kane et al., Citation2020). PSM builds matched pairs from treatment and control group to balance observed pre-treatment covariates (Rosenbaum, Citation2023). In other words, PSM is a quasi-experimental method that constructs a counterfactual outcome by matching treated units to similar untreated units, depending on pre-treatment covariates (Li, Citation2013). This study uses PSM to estimate the average treatment effect on the treated group (ATET). Three PSM methods, namely Caliper, Kernel, and nearest neighbor matching, were applied to estimate the impact of financial inclusion on educational investment. Caliper matching involves choosing an untreated unit as a match for a treated unit that remains within the caliper (propensity range) (Wang et al., Citation2013). Kernel matching (KM) is a non-parametric matching that uses weighted averages of all units in the untreated group to construct the counterfactual outcome (Caliendo & Kopeinig, Citation2008). Nearest neighbor matching involves choosing an untreated unit as a matching partner for a treated unit based on proximity to the propensity score.

The average treatment effect on the treated group (ATET) was estimated as follows using PSM:

(1)

(1)

Where Y refers to four expenditures, namely, food, non-food, health, and education expenditures in BDT (the outcome), N refers to the set of pre-treatment covariates, and T is the treatment dummy variable that describes a household’s financial services usage. T = 1 means that a household is financially included within the last 12 months. T = 0 means that a household is not. refers to the expenditure of the treated units.

refers to the expected expenditure of the best-matched untreated units.

Under the PSM model, it is assumed that there are no systematic differences between the treated and untreated groups after matching based on the pre-treatment covariates.

The following model is applied to estimate ATET under propensity score

(2)

(2)

The study uses PSM to examine the impact of financial inclusion on food, non-food (clothing and housing), education, and health expenditures.

5. Results

5.1. Summary statistics

compares the summary statistics of the relevant explanatory variables between treated and untreated slum households. Treated households comprise 19.54% of all households that remained financially included within the last 12 months. Untreated households that remained financially excluded represent most households (80.46%). The average food, non-food, and educational expenditures of treated households were greater than those of untreated households. Only the health expenditure of untreated households was greater than that of treated households. Treated households were greater (4.30 members) than untreated households (3.91 members) on average. The size of cultivable land and the total home area of treated households exceeded those of untreated slum households. As the number of household members younger than 15 years is crucial in determining educational expenditure, the summary statistics demonstrate that treated households residing in slums have more members younger than 15 years than untreated households. In addition, treated households have more members younger than 40 years than untreated households. The average age of untreated households (29.32 years) was also greater than that of treated households (25.77 years). Finally, there was a greater proportion of male heads in the treated households than in the untreated households.

Table 2. Summary statistics.

5.2. Main results

illustrates the ATET group. The table reports Caliper, Kernel, and nearest neighbor matching results. The results indicate that financial inclusion has a statistically significant positive impact on only educational expenditure at the 1% significance level. According to Caliper, Kernel, and nearest neighbor matching, slum households in Bangladesh that are financially included invest more than those financially excluded. The average impact of financial inclusion on educational expenditure is estimated to be at least BDT 901.04 (USD 9.01) and at most BDT 989.49 (USD 9.89). Therefore, the results across all matching methods demonstrate that slum households in Bangladesh that are financially included invest more in education than those that are financially excluded.

Table 3. Impact of financial inclusion on expenditure pattern.

The impact of financial inclusion on the other three outcomes—food, non-food, and health expenditures—is not statistically significant. reports that the use of financial services does not have a statistically significant impact (p > 0.10) on food, non-food, and health expenditures.

5.3. Balance check

The covariates used in the impact estimation must be balanced in PSM matching. presents the balancing properties of the treated and untreated groups before and after the matching. Apart from cultivable land area, the means of all pre-treatment variables were significantly different between the treated and untreated groups before matching. After matching, the means of the pre-treatment variables were much more similar.

Table 4. Balancing properties of matching variables.

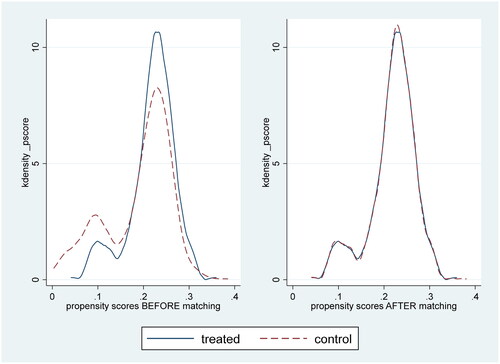

The propensity score graphs of the matching covariates are illustrated below in . The graphs demonstrate that, before matching, the distribution of covariates was not homogeneous between the untreated and treated groups. After matching, the distribution becomes homogeneous.

Figure 1. Distribution of pre-treatment variables before and after matching.

6. Robustness checks

6.1 Heterogeneous analysis

A heterogeneous analysis was conducted to investigate the impact of financial inclusion among two groups of households classified based on the usage of credit facilities. The first group comprises households that availed of credit, and the second group comprises households that did not avail of any credit. Nearest neighbor matching has been applied. illustrates that the use of financial services has a significant positive impact on the educational investments of slum households that availed of credit facilities. However, it does not significantly impact the educational investment of slum households that did not avail of any credit facilities.

Table 5. Heterogeneous impact of financial inclusion on expenditure pattern.

6.2 Inverse probability weighted regression adjustment

Inverse probability weighted regression (IPWR) adjustment estimation was conducted to check the robustness of the study. The inverse probability weighted regression adjustment (IPWRA) method can be a solution if there is misspecification in PSM (Moahid et al., Citation2023). The IPWR result demonstrated in is consistent with our main result. The result shows that financial inclusion increases educational expenditures while other expenditures remain unchanged.

Table 6. Impact of financial inclusion on expenditure pattern.

7. Discussion and conclusion

Families residing in slums spend most of their income on addressing their children’s basic needs, including food, clothing, and shelter. This study found that slum households that use financial services, specifically savings accounts and microsaving services, can invest more in education than those that do not. Household-level educational investment is considered to be an indication of a household’s willingness and capacity building with respect to overcoming economic vulnerability and inequality. As a result of savings in bank accounts or in micro-financial institutions, slum households can invest in their children’s education ().

Slum households, which are generally vulnerable households, often fail to spend on education because of the non-availability of investment funds. The use of financial services helps to build savings habits, and the savings in the deposit accounts help to invest more in education. This finding strengthens our claim that financial services follow the family investment model (Guo & Harris, Citation2000), in which authors argue that small financial arrangements, such as financial inclusion, increase investments in human capital, such as education, instead of increasing expenditure on food, non-food, and health.

Slum households that use credit facilities benefit more from financial inclusion in terms of increasing educational expenditure (). The usage of credit facilities increases when the usage of financial services increases because the usage of financial services creates a banker–customer relationship, which is essential to availing of credit facilities. Moreover, the usage of financial services increases financial literacy, which acquaints one with the procedure to avail credit facilities. A credit facility helps a vulnerable household arrange more resources to invest in product sectors like education. The study further concludes that savings products with both conventional and microfinance characteristics are more effective at increasing educational investment than financial service products consisting of only the characteristics of conventional or microfinance savings products.

The households using financial services will make a larger educational investment, even when they experience financial difficulties, because they build up financial reserves for their children’s education. Such households will also avoid diverting finances meant for education to other essentials, such as food and health expenditures, possibly because their financial inclusion makes them eligible to take out loans against their savings. The findings are consistent with Chakrabarty and Mukherjee (Citation2022), who argue that financial inclusion diverts the expenditure pattern of vulnerable households from too much expenditure on food items to human capital development expenditure.

Our present study is strongly supported by Financial Inclusion and Income Inequality Theory propounded by Kling et al. (Citation2022) arguing that savings or loan taken from financial institutions are invested immediately on human capital and human capital investment later translates in income based on the amount of investment. Sweetland (Citation1996) argue that education is the prime sector of human capital investment. This study shows that financial inclusion increases investment on education or human capital immediately. No impact on food, non-food and health expenditure reflects that households prefer educational investment more than food, non-food or health expenditure. Our findings is further supported by the family investment model (Guo & Harris, Citation2000) arguing that small financial arrangements, such as financial inclusion, increase investments in human capital, such as education, instead of increasing expenditure on food, non-food, and health.

The study has the limitation that the spillover effect cannot be estimated. The spillover effect could have been estimated if the spatial location of each household were available in the dataset. However, the dataset does not provide the spatial location of each household. Furthermore, the internal validity of the study findings may be compromised because PSM depends on a strong assumption of no systematic differences between the treated and untreated groups after matching. Further research needs to be conducted regarding the impact of financial service availability on different facets of well-being among slum dwellers in Bangladesh.

8. Policy implications

As policymakers contemplate financial inclusion as a strategic tool to achieve Sustainable Development Goals and uplift the living standards of those in extreme poverty, especially residents of slums, our findings bolster the assertion that financial inclusion exerts a significant positive impact on enhancing educational investment among slum dwellers, who represent the most impoverished segment of the population in Bangladesh. Specifically, this study proposes that financial inclusion can serve as a policy instrument to realize Sustainable Development Goal 4, which emphasizes quality education (Saini et al., Citation2023), by augmenting household-level expenditures on education. The study advocates that policymakers in developing countries should devise comprehensive and targeted financial inclusion strategic plans, addressing both short-term and long-term goals, to advance financial inclusion as a social protection mechanism. It recommends the creation of inclusive deposit products tailored to enhance financial inclusion among vulnerable households in developing nations. Initiatives such as the introduction of no-frill accounts, simplified documentation processes, refinance schemes catering to slum dwellers’ financial inclusion, hassle-free account opening facilities and the incorporation of profit-loss sharing Islamic accounts are suggested to foster financial inclusion among slum dwellers. This study underscores the importance of future research endeavors to explore the strategies and policies essential for ensuring the financial inclusion of vulnerable slum households.

Author contributions

Conceptualization: MD Abdul Bari, Ghulam Dastgir Khan; Formal Analysis: MD Abdul Bari; Methodology: MD Abdul Bari, Ghulam Dastgir Khan, Yuichiro Yoshida; Visualization: MD Abdul Bari; Supervision: Ghulam Dastgir Khan, Yuichiro Yoshida; Writing—original draft: MD Abdul Bari; and Writing—review & editing: Mohammad Ajmal Khuram, Md. Jahedul Islam

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study are available from the corresponding author, upon reasonable request.

Disclosure of interest

No potential conflict of interest was reported by the author(s).

References

- Ahmad, A. H., Green, C., & Jiang, F. (2020). Mobile money, financial inclusion and development: A review with reference to African experience. Journal of Economic Surveys, 34(4), 753–792. https://doi.org/10.1111/joes.12372

- Ahmed, J. U., Nisha, N., & Rifat, A. (2016). The Dhaka mercantile co-operative bank limited: A case of Islamic Shari’ah banking in Bangladesh. International Journal of Financial Innovation in Banking, 1(1/2), 62–79. https://doi.org/10.1504/IJFIB.2016.076622

- Alawattage, C., Graham, C., & Wickramasinghe, D. (2019). Microaccountability and biopolitics: Microfinance in a Sri Lankan village. Accounting, Organizations and Society, 72, 38–60. https://doi.org/10.1016/j.aos.2018.05.008

- Allen, F., Carletti, E., Cull, R., Qian, J., Senbet, L., & Valenzuela, P. (2013). Resolving the African financial development gap: Cross-country comparisons and a within-country study of Kenya (World Bank Policy Working Paper No. 6592). World Bank.

- Al-Shami, S. S. A., Majid, I. B. A., Rashid, N. A., & Hamid, M. S. R. B. A. (2014). Conceptual framework: The role of microfinance on the well-being of poor people case studies from Malaysia and Yemen. Asian Social Science, 10, 230. https://doi.org/10.5829/idosi.wasj.2014.30.icmrp.54

- Álvarez-Gamboa, J., Cabrera-Barona, P., & Jácome-Estrella, H. (2021). Financial inclusion and multidimensional poverty in Ecuador: A spatial approach. World Development Perspectives, 22, 100311. https://doi.org/10.1016/j.wdp.2021.100311

- Asongu, S., & Odhiambo, N. M. (2023). The role of financial inclusion in moderating the incidence of entrepreneurship on energy poverty in Ghana. Journal of Entrepreneurship in Emerging Economies, https://doi.org/10.1108/JEEE-03-2023-0089

- Babajide, A. A., Taiwo, J. N., & Isibor, J. A. (2015). Microsavings mobilization innovations and poverty alleviation in Nigeria. Mediterranean Journal of Social Sciences, 6, 375. https://doi.org/10.5901/mjss.2015.v6n4p375

- Banerjee, A., Duflo, E., Glennerster, R., & Kinnan, C. (2015). The miracle of microfinance? Evidence from a randomized evaluation. American Economic Journal: Applied Economics, 7(1), 22–53. https://doi.org/10.1257/app.20130533

- Bangladesh Bureau of Statistics. (2017). Preliminary report on household income and expenditure survey 2016. http://www.bbs.gov.bd/site/page/648dd9f5-067b-4bcc-ba38-45bfb9b12394/Income,-Expenditure-&-Poverty.

- Bari, M. A., Khan, G. D., He, B., & Yoshida, Y. (2022). The impact of unconditional cash and food assistance on contraceptive expenditure of rural households in Coastal Bangladesh: Evidence from fuzzy RDD. PloS One, 17(1), e0262031. https://doi.org/10.1371/journal.pone.0262031

- Brune, L., Giné, X., Goldberg, J., & Yang, D. (2011). Commitments to save: A field experiment in rural Malawi (World Bank Policy Research Working Paper No. 5748). World Bank.

- Burgess, R., & Pande, R. (2005). Do rural banks matter? Evidence from the Indian social banking experiment. American Economic Review, 95(3), 780–795. https://doi.org/10.1257/0002828054201242

- Caliendo, M., & Kopeinig, S. (2008). Some practical guidance for the implementation of propensity score matching. Journal of Economic Surveys, 22(1), 31–72. https://doi.org/10.1111/j.1467-6419.2007.00527.x

- Cao, Y., Cai, J., & Liu, X. (2023). Financial inclusion role on energy efficiency financing gaps in COVID-19 period: Empirical outcomes of emerging nations. Environmental Science and Pollution Research, 30(25), 67279–67289. https://doi.org/10.1007/s11356-023-26772-1

- Chakrabarty, M., & Mukherjee, S. (2022). Financial inclusion and household welfare: An entropy-based consumption diversification approach. European Journal of Development Research, 34, 1486–1521.

- De Mel, S., McIntosh, C., Sheth, K., & Woodruff, C. (2022). Can mobile-linked bank accounts bolster savings? evidence from a randomized controlled trial in Sri lanka. The Review of Economics and Statistics, 104(2), 306–320. https://doi.org/10.1162/rest_a_00956

- Dehejia, R. (2005). Practical propensity score matching: A reply to Smith and Todd. Journal of Econometrics, 125(1-2), 355–364. https://doi.org/10.1016/j.jeconom.2004.04.012

- Dehejia, R. H., & Wahba, S. (2002). Propensity score-matching methods for nonexperimental causal studies. Review of Economics and Statistics, 84(1), 151–161. https://doi.org/10.1162/003465302317331982

- Dixit, P., Al-Kake, F., & Ahmed, R. R. (2019). Micro finance institutions and their importance in growing economic development: A study of rural Indian economy. Russian Journal of Agricultural and Socio-Economic Sciences, 90(6), 216–225. https://doi.org/10.18551/rjoas.2019-06.27

- Dogan, E., Madaleno, M., & Taskin, D. (2022). Financial inclusion and poverty: Evidence from Turkish household survey data. Applied Economics, 54(19), 2135–2147. https://doi.org/10.1080/00036846.2021.1985076

- Duncan, G. J., Magnuson, K., & Votruba-Drzal, E. (2017). Moving beyond correlations in assessing the consequences of poverty. Annual Review of Psychology, 68(1), 413–434. https://doi.org/10.1146/annurev-psych-010416-044224

- Elzahi Saaid Ali, A. (2022). Islamic microfinance: Moving beyond the financial inclusion. In Empowering the Poor through financial and social inclusion in Africa: An Islamic perspective (pp. 11–24). Springer International Publishing.

- Erlando, A., Riyanto, F. D., & Masakazu, S. (2020). Financial inclusion, economic growth, and poverty alleviation: Evidence from eastern Indonesia. Heliyon, 6(10), e05235. https://doi.org/10.1016/j.heliyon.2020.e05235

- Guo, G., & Harris, K. M. (2000). The mechanisms mediating the effects of poverty on children’s intellectual development. Demography, 37(4), 431–447. https://doi.org/10.1353/dem.2000.0005

- Hossain, B., & Naimul Wadood, S. (2020). Impact of urban microfinance on the livelihood strategies of borrower slum dwellers in the Dhaka city, Bangladesh. Journal of Urban Management, 9(2), 151–167. https://doi.org/10.1016/j.jum.2019.12.003

- Ifediora, C., Offor, K. O., Eze, E. F., Takon, S. M., Ageme, A. E., Ibe, G. I., & Onwumere, J. U. (2022). Financial inclusion and its impact on economic growth: Empirical evidence from sub-Saharan Africa. Cogent Economics & Finance, 10(1), 2060551. https://doi.org/10.1080/23322039.2022.2060551

- Islam, S., Emran, G. I., Rahman, E., Banik, R., Sikder, T., Smith, L., & Hossain, S. (2021). Knowledge, attitudes and practices associated with the COVID-19 among slum dwellers resided in Dhaka City: A Bangladeshi interview-based survey. Journal of Public Health (Oxford, England), 43(1), 13–25. https://doi.org/10.1093/pubmed/fdaa182

- Kane, L. T., Fang, T., Galetta, M. S., Goyal, D. K. C., Nicholson, K. J., Kepler, C. K., Vaccaro, A. R., & Schroeder, G. D. (2020). Propensity score matching: A statistical method. Clinical Spine Surgery, 33(3), 120–122. https://doi.org/10.1097/BSD.0000000000000932

- Khan, I., Khan, I., Sayal, A. U., & Khan, M. Z. (2022b). Does financial inclusion induce poverty, income inequality, and financial stability: Empirical evidence from the 54 African countries? Journal of Economic Studies, 49(2), 303–314. https://doi.org/10.1108/JES-07-2020-0317

- Khan, F., Siddiqui, M. A., & Imtiaz, S. (2022a). Role of financial literacy in achieving financial inclusion: A review, synthesis and research agenda. Cogent Business & Management, 9(1), 2034236. https://doi.org/10.1080/23311975.2022.2034236

- Kling, G., Pesqué-Cela, V., Tian, L., & Luo, D. (2022). A theory of financial inclusion and income inequality. The European Journal of Finance, 28(1), 137–157. https://doi.org/10.1080/1351847X.2020.1792960

- Koomson, I., & Afoakwah, C. (2023). Can financial inclusion improve children’s learning outcomes and late school enrolment in a developing country? Applied Economics, 55(3), 237–254. https://doi.org/10.1080/00036846.2022.2086683

- Ksir, C., & Hart, C. L. (2016). Correlation still does not imply causation. The Lancet. Psychiatry, 3(5), 401. https://doi.org/10.1016/S2215-0366(16)30005-0

- Lee, C. C., Lou, R., & Wang, F. (2023). Digital financial inclusion and poverty alleviation: Evidence from the sustainable development of China. Economic Analysis and Policy, 77, 418–434. https://doi.org/10.1016/j.eap.2022.12.004

- Li, M. (2013). Using the propensity score method to estimate causal effects: A review and practical guide. Organizational Research Methods, 16(2), 188–226. https://doi.org/10.1177/1094428112447816

- Mccarthy, A. S., & Pearlman, R. (2022). Multiplying siblings: Exploring the trade-off between family size and child education in rural Bangladesh. The Journal of Development Studies, 58(9), 1831–1856. https://doi.org/10.1080/00220388.2022.2048652

- Moahid, M., Khan, G. D., Bari, M. A., & Yoshida, Y. (2023). Does access to agricultural credit help disaster-affected farming households to invest more on agricultural input? Agricultural Finance Review, 83(1), 96–106. https://doi.org/10.1108/AFR-12-2021-0168

- Nsiah, A. Y., Yusif, H., Tweneboah, G., Agyei, K., & Baidoo, S. T. (2021). The effect of financial inclusion on poverty reduction in Sub-Sahara Africa: Does threshold matter? Cogent Social Sciences, 7(1), 1903138. https://doi.org/10.1080/23311886.2021.1903138

- Numan, A. Q., & Islam, M. S. (2021). An assessment of the teaching and learning process of public and BRAC primary schools in Bangladesh. Education 3-13, 49(7), 845–859. https://doi.org/10.1080/03004279.2020.1809488

- Omar, M. A., & Inaba, K. (2020). Does financial inclusion reduce poverty and income inequality in developing countries? A panel data analysis. Journal of Economic Structures, 9(1), 37. https://doi.org/10.1186/s40008-020-00214-4

- Pal, S., & Bandyopadhyay, I. (2022). Impact of financial inclusion on economic growth, financial development, financial efficiency, financial stability, and profitability: an international evidence. SN Business & Economics, 2(9), 139. https://doi.org/10.1007/s43546-022-00313-3

- Park, C. Y., & Mercado, R. V. (2021). Financial inclusion: New measurement and cross-country impact assessment 1. In Financial inclusion in Asia and beyond (pp. 98–128). Routledge.

- Pitt, M. M., & Khandker, S. R. (1998). The impact of group-based credit programs on poor households in Bangladesh: Does the gender of participants matter? Journal of Political Economy, 106(5), 958–996. https://doi.org/10.1086/250037

- Polloni-Silva, E., da Costa, N., Moralles, H. F., & Sacomano Neto, M. (2021). Does financial inclusion diminish poverty and inequality? A panel data analysis for Latin American countries. Social Indicators Research, 158(3), 889–925. https://doi.org/10.1007/s11205-021-02730-7

- Ratnawati, K. (2020). The impact of financial inclusion on economic growth, poverty, income inequality, and financial stability in Asia. The Journal of Asian Finance, Economics and Business, 7(10), 73–85. https://doi.org/10.13106/jafeb.2020.vol7.no10.073

- Roodman, D., & Morduch, J. (2014). The impact of microcredit on the poor in Bangladesh: Revisiting the evidence. The Journal of Development Studies, 50(4), 583–604. https://doi.org/10.1080/00220388.2013.858122

- Rosenbaum, P. R. (2023). Propensity score. In Handbook of matching and weighting adjustments for causal inference (pp. 21–38). Chapman and Hall/CRC.

- Roy, P., & Patro, B. (2022). Financial inclusion of women and gender gap in access to finance: A systematic literature review. Vision: The Journal of Business Perspective, 26(3), 282–299. https://doi.org/10.1177/09722629221104205

- Saini, M., Sengupta, E., Singh, M., Singh, H., & Singh, J. (2023). Sustainable Development Goal for Quality Education (SDG 4): A study on SDG 4 to extract the pattern of association among the indicators of SDG 4 employing a genetic algorithm. Education and Information Technologies, 28(2), 2031–2069. https://doi.org/10.1007/s10639-022-11265-4

- Sajuyigbe, A. S., Odetayo, T. A., & Adeyemi, A. Z. (2020). Financial literacy and financial inclusion as tools to enhance small scale businesses’ performance in southwest, Nigeria. Finance & Economics Review, 2(3), 1–13. https://doi.org/10.38157/finance-economics-review.v2i3.164

- Saluja, O. B., Singh, P., & Kumar, H. (2023). Barriers and interventions on the way to empower women through financial inclusion: A 2 decades systematic review (2000–2020). Humanities and Social Sciences Communications, 10(1), 1–14. https://doi.org/10.1057/s41599-023-01640-y

- Sarma, M., & Pais, J. (2011). Financial inclusion and development. Journal of International Development, 23(5), 613–628. https://doi.org/10.1002/jid.1698

- Sarpong, B., & Nketiah-Amponsah, E. (2022). Financial inclusion and inclusive growth in sub-Saharan Africa. Cogent Economics & Finance, 10(1), 2058734. https://doi.org/10.1080/23322039.2022.2058734

- Seidu, A. A., Agbadi, P., Duodu, P. A., Dey, N. E. Y., Duah, H. O., & Ahinkorah, B. O. (2021). Prevalence and sociodemographic factors associated with vision difficulties in Ghana, Gambia, and Togo: A multi-country analysis of recent multiple Indicator cluster surveys. BMC Public Health, 21(1), 2148. https://doi.org/10.1186/s12889-021-12193-7

- Sweetland, S. R. (1996). Human capital theory: Foundations of a field of inquiry. Review of Educational Research, 66(3), 341–359. https://doi.org/10.3102/00346543066003341

- Takmaz, S., Sarı, E., & Alataş, S. (2022). Financial inclusion in Turkey: Unpacking the provincial inequality and its determinants. Applied Economics Letters, 1–9. https://doi.org/10.1080/13504851.2022.2141442

- Thomson, D. R., Kuffer, M., Boo, G., Hati, B., Grippa, T., Elsey, H., Linard, C., Mahabir, R., Kyobutungi, C., Maviti, J., Mwaniki, D., Ndugwa, R., Makau, J., Sliuzas, R., Cheruiyot, S., Nyambuga, K., Mboga, N., Kimani, N. W., de Albuquerque, J. P., & Kabaria, C. (2020). Need for an integrated deprived area “slum” mapping system (IDEAMAPS) in low- and middle-income countries (LMICs). Social Sciences, 9(5), 80. https://doi.org/10.3390/socsci9050080

- Tran, H. T. T., Le, H. T. T., Nguyen, N. T., Pham, T. T. M., & Hoang, H. T. (2022). The effect of financial inclusion on multidimensional poverty: The case of Vietnam. Cogent Economics & Finance, 10(1), 2132643. https://doi.org/10.1080/23322039.2022.2132643

- Troyer, M. (2022). The gold standard for whom? Schools’ experiences participating in a randomised controlled trial. Journal of Research in Reading, 45(3), 406–424. https://doi.org/10.1111/1467-9817.12395

- Wang, Y., Cai, H., Li, C., Jiang, Z., Wang, L., Song, J., & Xia, J. (2013). Optimal caliper width for propensity score matching of three treatment groups: A Monte Carlo study. PloS One, 8(12), e81045. https://doi.org/10.1371/journal.pone.0081045

- Yang, T., & Zhang, X. (2022). FinTech adoption and financial inclusion: Evidence from household consumption in China. Journal of Banking & Finance, 145, 106668. https://doi.org/10.1016/j.jbankfin.2022.106668

- Zeqiraj, V., Sohag, K., & Hammoudeh, S. (2022). Financial inclusion in developing countries: Do quality institutions matter? Journal of International Financial Markets, Institutions and Money, 81, 101677. https://doi.org/10.1016/j.intfin.2022.101677