Abstract

The literature on overconfidence has witnessed prolific growth since the beginning of the century. This context underscores the necessity to comprehend and categorize an increasingly diverse body of overconfidence research within the financial domain. This study reviews existing literature on financial overconfidence from its inception to the present with a detailed review of 132 articles from 84 journals by examining theories, context, and methods (TCM) used in overconfidence research. Our review unpacks significant themes (i.e. determinants of overconfidence, overconfidence and risk-taking, overconfidence measures and type of investors, overconfidence in a volatile market, overconfidence, and personal financial behavior). We propose a pertinent research framework to investigate the less investigated aspects of financial overconfidence and suggest future research direction.

Impact statement

The significance of this paper lies in its potential to deepen our understanding of how psychological biases and significant overconfidence influence investment behavior and market outcomes. By synthesizing findings from multiple studies, this literature review highlights common themes, identifies gaps in knowledge, and suggests avenues for future research. Ultimately, insights gained from such a review can inform investors, financial professionals, and policymakers about the importance of recognizing and addressing overconfidence in investment decision-making processes. This understanding can lead to more informed and rational investment strategies, potentially mitigating the adverse effects of overconfidence on individual investors and market efficiency.

1. Introduction

Overconfidence bias is a cognitive bias that refers to the tendency of investors to overestimate their knowledge, skills, and abilities when making financial decisions (Kahneman & Riepe, Citation1998). Overconfidence bias has been studied extensively in psychology and was introduced to finance in the late 20th century; overconfidence among investors is a crucial notion in behavioral finance (Michailova & Schmidt, Citation2016; Statman et al., Citation2006). Pioneering research in behavioral economics and finance, such as the work of Barber and Odean (Citation2001) and Kahneman & Riepe (Citation1998), highlighted the role of overconfidence in shaping economic and financial decisions. Recognizing and dealing with overconfidence bias is critical for investors; overconfidence bias can hurt long-term investing performance. Investors who assume they are more informed or skilled than they are may take undue risks or make poor decisions (Du & Budescu, Citation2007; Pikulina et al., Citation2017). Overconfidence bias can result in various behavioral outcomes, including excessive trading (Fellner-Röhling & Krügel, Citation2014; Wilaiporn et al., Citation2021), failure to seek professional advice (Hsu, Citation2022) that may result in inadequate portfolio diversification (Pak & Chatterjee, Citation2016), increasing exposure to individual risk, and reduced value of overconfident traders (Odean, Citation1998).

Financial overconfidence can result from various antecedents or underlying variables contributing to people’s tendency to overestimate their skills. Understanding the causes of overconfidence bias is critical for individuals and organizations aiming to reduce its harmful consequences. The overconfidence of a trader changes considerably with his successes and losses (Gervais & Odean, Citation2001). The dominant factors affecting overconfidence are social comparison, experience (Pak & Chatterjee, Citation2016), and demographic factors, especially gender (Baker et al., Citation2019; Jiang et al., Citation2020), income (Ansari et al., Citation2023). Overconfidence affects the financial market; overconfidence among investors can contribute to market booms, crashes, and inefficiencies (Bouteska et al., Citation2023). Their excessive trading and risk-taking might aggravate market volatility (Filbeck et al., Citation2017). The synthesis of the diverse literature on financial overconfidence is essential to understanding its causes, effects, and potential treatments. We have conducted a systematic literature review (SLR) on overconfidence. We employed the Theory Context-Methodology (TCM) framework proposed by Paul and Rosado-Serrano in 2019 to comprehend overconfidence’s theoretical and empirical aspects. In light of this framework, our review article aims to investigate the following research questions.

RQ1. How has the literature on overconfidence evolved?

RQ2. What different theoretical perspectives are applied in the overconfidence literature?

RQ3: Which research contexts have been explored in the study of overconfidence in behavioral finance?

RQ4. What are the various methods utilized in overconfidence research in behavioral finance?

RQ5. What are the future research agendas for financial overconfidence based on the TCM framework?

This review will help promote a greater understanding of the topic by proposing a research framework and future research directions. The rest of the paper is structured as follows: it begins with a discussion of the background and definitions of overconfidence, followed by a discussion of the methodology and bibliometric analysis. In conclusion, the paper presents the proposed framework and discusses prospective research directions in overconfidence.

2. Background of financial overconfidence: definition and measures

Overconfidence is multidimensional and dynamic (Deaves et al., Citation2009). Overconfidence is one of the most common biases among individual investors (Jain et al., Citation2019; Kansal & Singh, Citation2018). ‘Three definitions of overconfidence are used in the psychological literature: overestimation, over-placement, and calibration of subjective probabilities’ (Olsson, Citation2014, p.1). Using ‘overestimation’ to describe overconfidence means comparing a person’s actual performance to how they perceive they performed (Moore & Healy, Citation2008). The second measure of overconfidence is ‘overplacement’, which is assessed by comparing an individual’s performance with that of others. Both overestimation and over-placement denote a tendency to excessively estimate one’s ability (Pikulina et al., Citation2017). Overprecision or miscalibration is the third sign of overconfidence that investors most often show. Traders overestimate how precise a private signal is and underestimate how volatile an asset is (Merkle, Citation2017).

showcases the most cited and impactful articles in the financial overconfidence field based on the citations. Among the top influential articles, one noteworthy study was conducted by Barber and Odean (Citation2001) that posits that overconfident investors engage in excessive trading and men are more prone to overconfidence. An influential work by Gervais and Odean (Citation2001) formulated a multiperiod market model and explained the development of overconfidence bias. Furthermore, Glaser and Weber (Citation2007) suggested that overconfident investors trade more than rational investors. In a related vein, the study by Barber and Odean (Citation2001) explains that high trading levels result in poor performance for overconfident retail investors and enhance market depth (Odean, Citation1998). The research papers listed comprehensively explore behavioral economics and investor psychology. Kahneman and Tversky’s seminal work on prospect theory laid the foundation for understanding how individuals make decisions in uncertain situations. Odean’s (Citation1998) delves into the psychological reluctance of investors to cut their losses. The study by Statman et al. (Citation2006) sheds light on the impact of overconfidence on trading behavior.

Table 1. List of seminal papers in the field.

Meanwhile, Tversky et al. (Citation1982) discuss cognitive shortcuts and biases that influence decision-making. Tversky and Kahneman (Citation1992) expand on their original prospect theory, while Grinblatt and Keloharju (Citation2009) investigate how sensation-seeking tendencies affect trading. Moore and Healy (Citation2008) offer insights into the challenges overconfidence poses. Odean (Citation1999) examines the phenomenon of excessive trading. Lastly, Kahneman and Riepe (Citation1998) delve into the various facets of investor psychology. Together, these papers provide a comprehensive understanding of the complexities of human decision-making and its impact on financial markets. The central message here underscores that excessive trading due to overconfidence can harm one’s wealth. Van Rooij et al. (Citation2011) examined financial literacy’s relationship to the stock market and certified that financial literacy affects financial decision-making. In conclusion, the seminal research undertaken on overconfidence has provided valuable insights into finance and decision-making.

3. Bibliometric research method

Our research is limited to peer-reviewed papers retrieved from the Scopus database, frequently utilized for systematic literature review (Singh & Malik, Citation2022). Initially, 1,566 articles were extracted from the Scopus database using the keywords in the field (Title-Abstract-keywords). Searches for (‘overconfidence’) AND (‘finance*’ OR ‘credit’ OR ‘debt’ OR ‘stress’ OR ‘invest*’ OR ‘risk’ OR ‘literacy’ OR ‘advice’ OR ‘behavior*’ OR ‘financial knowledge’ OR ‘well-being’) were made in the database, combined with AND NOT (‘CEO’ OR ‘manager*’ OR ‘CSR’ OR ‘corporate social responsibility’ OR ‘firm’). The ‘and not’ search criteria were included to exclude articles that highlight managerial overconfidence in corporate governance and social responsibility. Managers’ overconfidence can affect investment decisions, business strategy, and the overall course of the organization. Meanwhile, an individual’s overconfidence is considerably more comprehensive and relevant in its implications for their risk-taking, investment, and saving habits. Therefore, the decision was taken to restrict the research scope to individual overconfidence in financial decision-making rather than managerial overconfidence. After the exclusion of conference papers, proceedings, and non-English journal articles, the count became 1179. Further, the subject area filter was imposed and limited to Economics, Econometrics, and Finance; Business, Management, and Accounting; Social Sciences, and Psychology; this reduced the paper count to 774. The manual screening was done by reading abstracts, keywords, and, in some cases, full articles to check the relevance of the retrieved articles. After all the filters and screening, the final sample of 132 studies from 2001 to Aug 31, 2023, was used for the analysis. The critical information about the data set is displayed below ().

Table 2. Overview of the sample.

4. Analysis

The current review study covers productivity and impact of authors, sources, and documents; coverage of theories used; bibliographic coupling to unearth the significant themes; and conceptual coverage through keyword co-occurrence.

4.1. Performance analysis

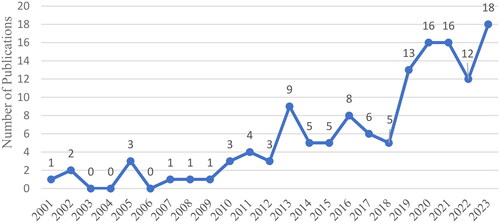

provides a comprehensive overview of the sample papers included in this systematic literature review. The table presents data on several aspects: the total number of sources, the annual growth rate of the publications, the number of authors, international collaboration, the number of author keywords, and average citations per document in the field of overconfidence bias. shows the progression of the literature on investor overconfidence bias for 2001–2023. Interest in the research on overconfidence bias picked up after 2012. There is an increasing trend in the publications, representing this as the growing field of research; close to 60% of the papers have been published in the last five years.

Figure 1. Growth of publications.

Source: Scopus Database.

presents an overview of the core zone sources in the given domain as per Bradford’s law of scattering (1934). A core zone is a small group of journals with the most relevant articles widely cited. Nine journals represent the research field’s core zone; these are the most productive and highly cited. The journals have been ranked in terms of productivity; the top three journals are Qualitative Research in Financial Markets (n = 8, 216 citations, h-index 6), Journal of Behavioral and Experimental Finance (n = 7, 93 citations, h-index 6), and Journal of Economic Behavior and Organization (n = 5, 189 citations, h-index 5). The following two journals are Finance Research Letters and Review of Behavioural Finance. indicates the most influential authors in overconfidence research. Deaves and Luders are the most influential authors, each with 234 citations, followed by Maciejovsky (133 citations).

Table 3. Core sources in the field.

Table 4. Prominent authors in financial overconfidence.

4.2. Keyword analysis

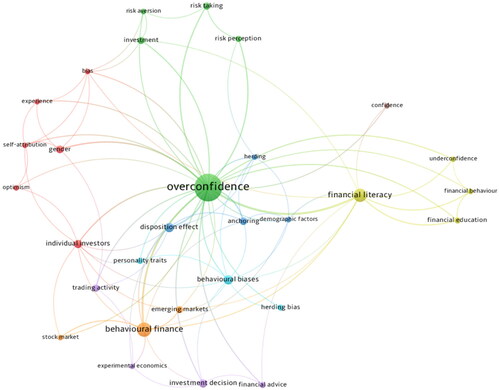

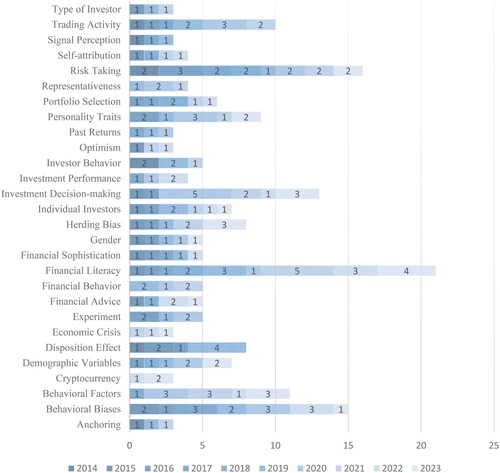

In this part of the study, the most frequently used author keywords in the overconfidence literature have been analyzed to study the conceptual structure of the given research domain (Syed et al., Citation2023). depicts the map of keyword co-occurrence for the top 30 keywords with a minimum of 3 occurrences. The most co-occurring keywords in this literature are financial literacy, behavioral biases, investment decisions, demographic factors, especially gender, risk-taking, trading activity, financial advice-seeking, financial behavior, and personality traits of the investors. In , the close distance of two terms and the thickness of the linking lines represent how closely they have been used in the literature, while the size of the nodes shows how frequently they co-occurred as keywords. Furthermore, illustrates the keywords utilized most frequently over the past decade with at least two occurrences. emphasizes the most recent patterns in the literature, whereas is a keyword-based map from 2000. shows that trading activity, risk-taking, personality traits, portfolio selection, investment decisions, herding bias, financial literacy, behavioral biases, and behavioral factors have frequently been used in overconfidence research in the decade. However, financial advice, professional overconfidence, and overconfidence in cryptocurrency have received relatively little attention in overconfidence research.

Figure 2. Keywords co-occurrence analysis.

Source: Authors compilation with the help of Scopus Database.

Figure 3. Author keywords in the last 10 years.

Source: Authors compilation with the help of Scopus Database.

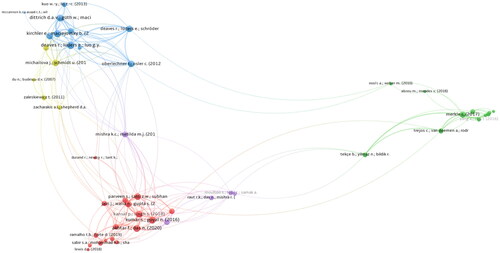

4.3. Thematic and influence structure analysis through bibliographic coupling

Bibliographic coupling is used to get the significant clusters in each literature (Syed et al., Citation2023). We conducted bibliographic coupling with a minimum of 12 citations per article, resulting in 48 articles having the most significant total link strength grouped into five clusters ().

Figure 4. Clusters identified through bibliographic coupling.

Note. Colour theme of clusters: Cluster one: red; Cluster two: green; Cluster three: blue; Cluster four: light green; Cluster five: purple.

Source: Authors compilation with the help of Scopus Database.

4.3.1. Cluster 1: Determinants of overconfidence

This cluster includes seventeen publications on overconfidence and investment decision-making behavior. This cluster demonstrates the crucial factors shaping and developing investor’s overconfidence bias. The determinants of the overconfidence bias can be listed as demographic variables (age, gender, income, occupation), financial literacy (Kawamura et al., Citation2021), personality traits (Akhtar & Das, Citation2020; Durand et al., Citation2013; Kleine et al., Citation2016), employment status (Rahman & Gan, Citation2020), profession (Prosad et al., Citation2015), investment experience (Kansal & Singh, Citation2018) and past investment performance (Parveen et al., Citation2020). Gender is the most dominant demographic factor affecting investor overconfidence (Baker et al., Citation2019; Kansal & Singh, Citation2018), where males are more prone to overconfidence (Kumar & Goyal, Citation2016). Financial literacy has proved to be a significant positive factor for overconfidence (Kawamura et al., Citation2021). Meier and De Mello (Citation2020) confirmed that overconfidence is unstable; with contradictory feedback, it vanishes, and with supportive signals, it returns.

4.3.2. Cluster 2: Overconfidence & risk taking

The collective findings of this cluster shed light on the complex dynamics between overconfidence, perception of risk, and investment patterns. The cluster comprises eleven publications investigating the interplay of overconfidence and risk-taking and their impact on financial decision-making (Merkle, Citation2017). The cluster is mainly focused on the two consequences of overconfidence: the risk-taking behavior of the investor and excessive trading. The research examines the impact of financial overconfidence on individuals’ risk perception and subsequent behavior (Broihanne et al., Citation2014). Moreover, the influence of traders’ overconfidence on their trading behavior may lead to increased trading activity and unfavorable results (Fellner-Röhling & Krügel, Citation2014). A fascinating finding states that overconfidence in self-financial skills increases with age and affects riskiness and equity percentage in the retirement portfolio (Pak & Chatterjee, Citation2016).

4.3.3. Cluster 3: Overconfidence measures and type of investors

This cluster with ten articles emphasizes the complexity of measuring overconfidence, its dynamism, the unrelatedness in the different measures of overconfidence, and the degree of overconfidence regarding types of investors. Kirchler and Maciejovsky (Citation2002) compared the two measures of overconfidence: subjective confidence intervals and the difference between objective and subjective certainty in the experimental asset market. The overconfidence was more frequent when subjective overconfidence intervals were used, and this overconfidence was positively correlated with the trader’s experience. Among the various measures of overconfidence, which measure is best and closer to financial behavior needs to be clarified (Deaves et al., Citation2009). The evidence on the dynamics of overconfidence is mixed and needs interpretation (Deaves et al., Citation2010). Overconfidence rises with wrong investment decisions and task complexity (Dittrich et al., Citation2005). The degree of overconfidence varies between the investor groups: Investment advisors were identified as the most overconfident group, followed by retail investors and institutional investors (Menkhoff et al., Citation2013).

4.3.4. Cluster 4: Overconfidence in a volatile market

This cluster comprises five papers focusing on the degree of overconfidence during the financial crisis and very highly volatile markets (Biais et al., Citation2005). The markets with high overconfidence have witnessed price bubbles and intense trading volumes (Michailova & Schmidt, Citation2016). Experts have shown better forecasting skills than non-experts during financial crises (Zaleskiewicz, Citation2011). Additionally, the cluster emphasizes that the overconfidence of venture capitalists leads to wrong investment decisions (Zacharakis & Shepherd, Citation2001) and the potential impact of historical volatility on investors’ price predictions (Du & Budescu, Citation2007).

4.3.5. Cluster 5: Overconfidence and personal financial behavior

This cluster encompasses five articles on cognitive biases and their impact on financial decision-making within personal finance and investment. The studies encompassed investment experience, gender, educational level, personality traits, debt capacity, and risk attitudes (Bansal & Singh, Citation2021; Mishra & Metilda, Citation2015).

Moulton et al., Citation2013 studied the borrowing capacity of first-time homebuyers and established that high overconfidence leads to more borrowing and avoidance of finance coaching classes. Individuals’ risk aversion and attitude can moderate the relationship between financial behavior and overconfidence (Ahmad, Citation2020; Mishra & Metilda, Citation2015).

5. Theory-context-methods (TCM) analysis

In this study, we employ the TCM (Paul & Rosado-Serrano, Citation2019) framework to conduct a content analysis, shedding light on the theoretical foundations and broader context of financial overconfidence while spotlighting its distinctive characteristics. We begin by examining the theoretical landscape of overconfidence research, focusing on this discipline’s commonly used theoretical foundations. Next, we investigate the geographical scope of overconfidence research, focusing on the nations where such studies have been conducted. Finally, we assess important methodological aspects within this field. The figure illustrates the framework-based content analysis.

5.1. Theories (RQ2)

Financial overconfidence is a complex behavioral phenomenon that can be comprehensively understood by synthesizing various psychological and financial theories. This section briefly discusses some of the widely used theories in this domain, as (RQ2) mentions. Utilizing a theoretical lens to explore a multifaceted phenomenon like overconfidence makes it yield more (Daniel et al., Citation1998; Ehrlinger et al., Citation2016).

Table 5. Prominent theories argued in overconfidence.

5.1.1. Prospect theory

(Duy Bui et al., Citation2021; Sabir et al., Citation2019) has significantly contributed to the field of financial benefits and losses. They have employed a widely recognized theory to investigate these concepts. The foundation of many current asset pricing models, such as CAPM and APT, relies on Utility theory principles. However, Kahneman and Tversky (Citation1979) conducted experiments that presented evidence contradicting Utility theory. Their research highlighted phenomena such as the Certainty Effect, Reflection, Isolation effect, and others, which challenge the traditional utility theory. Based on these anomalies, they introduced an alternative theory known as Prospect theory. In contrast to utility theory, Prospect theory divides the decision-making process into two phases: editing and evaluation. While expected Utility Theory focuses on rational investor expectations, Prospect theory emphasizes subjective decision-making criteria, which can be significantly influenced by an investor’s value system (Filbeck et al., Citation2005; Singh & Malik, Citation2018). Prospect theory sheds light on critical psychological factors that impact decision-making, including regret aversion, loss aversion, and mental accounting (Jain et al., Citation2019; Waweru et al., Citation2008), which have confirmed the significant influence of these factors on decision-making. The applications of Prospect theory extend to various domains, including investment decision-making (Jain et al., Citation2019), mathematical economics (Hlouskova et al., Citation2017), and decision-making within family-owned businesses (Lude & Prügl, Citation2018).

5.1.2. Behavioural finance theory

(Hala et al., Citation2020) holds that financial markets are not always rational, and psychological biases and emotions impact investor decisions. Behavioural Finance recognizes that emotions, cognitive biases, and heuristics can alter human behavior (Kourtidis et al., Citation2011). This theory uses psychological and emotional factors to examine how people and market participants make financial decisions under uncertainty. It covers loss aversion, overconfidence, herding, and cognitive errors in investment decisions. Behavioural Finance Theory explains market irregularities, asset price bubbles, and investor mood. This theory helps investors, politicians, and researchers understand financial markets and how human psychology affects them by embracing the human element in finance.

5.1.3. Heuristics theory

(Marjerison et al., Citation2023) adds to this understanding by showing how people use mental shortcuts and rules of thumb when making financial judgments. Heuristics Theory and overconfidence studies explore decision-making and cognitive processes. People employ mental shortcuts or rules of thumb to make speedy decisions. Overconfidence, on the other hand, is overestimating one’s knowledge or abilities. According to studies, these heuristics and overconfidence might lead to inefficient financial decisions. These cognitive biases can cause excessive risk-taking and market inefficiencies; thus, investors and financial professionals must understand them. Researchers want to improve financial decision-making by studying these phenomena.

5.1.4. The cognitive theory

(Costa-Cordella et al., Citation2021; Adel & Mariem, Citation2013; Grežo, Citation2021) provides insights into the mental processes at play in financial overconfidence. Cognitive theory and overconfidence studies illuminate financial decision-making biases and their effects. Researchers strive to improve finance decision-making by revealing cognitive mechanisms, allowing consumers and experts to make complex financial decisions with increased precision and awareness.

5.1.5. The attribution bias theory

(Doukas & Petmezas, Citation2007) suggests that overconfident people may attribute their successes to their talent and blame external factors for their failures, reinforcing their financial brilliance. Attribution bias theory describes how people assign results to internal or external causes, distorting their abilities and judgments. When paired with overconfidence studies, it shows how humans tend to overestimate their knowledge and abilities, which can influence financial judgments.

5.1.6. Social learning theory

(Sabir et al., Citation2019) is crucial because it examines how people learn from their social environment. The Social Learning Theory posits that humans learn by watching and copying. Paired with overconfidence research, it reveals how people absorb knowledge and cognitive biases like overestimating their abilities or social views. Understanding how group dynamics, peer influence, and market attitudes distort financial decision-making requires understanding social learning and overconfidence. In addition, the Motivation-Opportunity-Ability framework (Liyanaarachchi et al., Citation2021) suggests that overconfidence may result from motivation (such as the desire for high returns), opportunity (access to financial markets), and perceived ability (exaggerated self-assessment). These three elements increase financial risk-taking and confidence.

In conclusion, overconfidence in finances is a multifaceted issue that may be examined using multiple psychological and financial theories. Despite progress, new theoretical lenses are needed to identify financial overconfidence.

5.2. Context (RQ3)

The context of overconfidence research, in terms of the geographical classification of literature, is considered valuable for identifying the intensity of global research, as mentioned in (RQ3). A comprehensive study on financial overconfidence encompassed a range of developed and emerging economies, including the UK, Italy, New Zealand, the UAE, Taiwan, France, Finland, Indonesia, South Africa, Japan, USA, Spain, Australia, Brazil, Germany, China, India, Malaysia, Hong Kong, Poland, and Canada. This multi-national approach aimed to investigate the prevalence, underlying causes, and cultural variations related to financial overconfidence. As reported in , most overconfidence research set in India (12.71%), the USA (11.86%), and Australia (10.17%) emerged as the leading nations in research on financial overconfidence, followed by Indonesia (5.93%), Germany (5.08%), Pakistan (5.08%), Malaysia (5.08%), China (4.24%), Brazil (2.54%), and Taiwan (2.54%). Existing evidence indicates that investors’ reactions to information depend on their socioeconomic status and psychological characteristics and that these factors also differ across geographic regions. The characteristics of the investor might influence how they trade and what they learn (Abreu & Mendes, Citation2012) and are affected by their surrounding environment (Goetzmann & Kumar, Citation2008). Regarding information, Peress (Citation2004) shows that affluent investors value it more than poor investors, and investors’ irrational behavior decreases drastically as they gain trading experience (Nicolosi et al., Citation2004). Research on investor overconfidence in developing nations and underdeveloped stock markets may have gained appeal for these reasons. Since developing countries’ markets are less efficient than developed countries’, there are also more instances of information asymmetry. Consequently, there is a call for other countries to expand their research efforts in financial overconfidence.

Table 6. Financial overconfidence research & nations.

5.3. Methods (RQ4)

Methods include empirical and non-empirical research methods. The body of research on overconfidence has demonstrated the various methods used to conduct the study, including quantitative and qualitative approaches, as mentioned in (RQ4). The research on financial overconfidence often uses the PLS-SEM, CB-SEM, ANOVA, OLS regression, cluster analysis, MANOVA, EFA & CFA, T-Test, Probit regression, and GARCH models. Financial overconfidence is complicated and multidimensional, but these tools have helped us understand its causes and effects (). The theoretical basis of our investigation influences the use of analytical methodologies. PLS-SEM and CB-SEM may resonate with prospect theory, which describes how individuals behave when choosing alternative investment opportunities, while social learning theory states that cognitive characteristics shape the behavior of an individual’s complexity (Sabir et al.,Citation2019). Based on the expected utility theory and the behavioral theories, the cluster analysis is used to understand the natural homogenous groupings of the investors in terms of their biases (Sahi & Arora, Citation2012). MANOVA can illuminate social judgment theory dynamics (Zacharakis and Shepherd (Citation2001), and T-test and Probit regression can investigate attribution biases. Finally, GARCH models can explain financial markets’ complex relationships driven by people’s thoughts and actions. However, previous research needs machine learning algorithms, a mixed method approach, hierarchical linear modeling, and multi-level SEM, which may help reveal fresh overconfidence insights.

Table 7. Type of statistical methods used by previous studies.

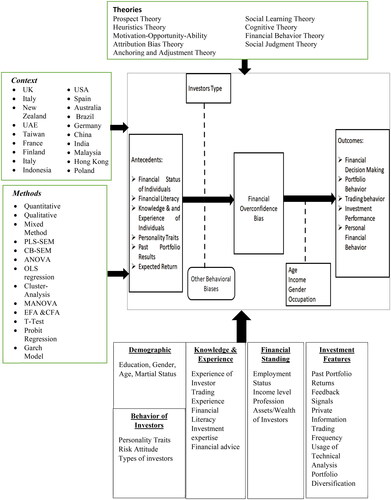

6. Proposed conceptual integrated framework

represents the proposed framework for financial overconfidence, which is substantiated by the Theory-Context-Methods (TCM) analysis and keyword analysis. The antecedent and outcome variables are determined by keyword analysis (4.1) and coupling clusters (4.2). The literature provides adequate information about the formation of overconfidence and its impact on financial and market outcomes. There are inconsistent findings related to the relationship of overconfidence and its antecedents. Males may overestimate their financial expertise more than females (Baker et al., Citation2019; Barber & Odean, Citation2001). Overconfidence bias is more common in older individuals; one study (Pak & Chatterjee, Citation2016) examined how it affects the retirement portfolio.

Figure 5. Proposed conceptual integrated framework for future research.

In contrast, age was negatively associated with overconfidence bias (Wilaiporn et al., Citation2021) and not with overconfidence (Kansal & Singh, Citation2018) since ability may not depend on age. Moreover, investors’ personality attributes affect their cognitive biases during their investment choices (Durand et al., Citation2013). Research suggests that personality is linked to overconfidence (Akhtar & Das, Citation2020). People with high extroversion are often overconfident (Pan & Statman, Citation2013). The knowledge and expertise level of the investors play a vital role in shaping overconfidence. Trading and investment experience affects overconfidence bias differently. Experience has a negative relationship with overconfidence bias (Gervais & Odean, Citation2001; Menkhoff et al., Citation2013), but (Baker et al., Citation2019; Glaser & Weber, Citation2007) have found a positive association. Investors’ focus on historical portfolio returns explains how perceived portfolio gains affect overconfidence (Merkle, Citation2017). The two main consequences of overconfidence are an increase in trading volume and lower expected returns. Overconfidence in market timing or stock selection leads to excessive buying and selling (Khan et al., Citation2017).

7. Future research directions (RQ5)

In light of the importance of overconfidence in financial decision-making over the next decade (Ainia & Lutfi, Citation2019), the current study aims to shed light on various dimensions of the TCM framework. In this section, we summarize and present the propositions and probable future research questions that may be explored respectively (RQ5).

7.1. Theory

Future research on overconfidence in financial decision-making should focus on further exploring and integrating various psychological and financial theories (Tomar et al., Citation2021; Puaschunder, Citation2017). This comprehensive approach will enhance our understanding of the complex phenomenon of financial overconfidence. Researchers should continue synthesizing and integrating psychological theories such as Prospect Theory, Behavioural Finance Theory, Heuristics Theory, Cognitive Theory, Attribution Bias Theory, and Anchoring and Adjustment Theory. This interdisciplinary integration of the theories can provide a more holistic understanding of the factors contributing to financial overconfidence. Therefore, we posit the following proposition:

Proposition 1:

Overconfidence is a multifaceted concept synthesizing and integrating psychological theories that influence investor decision-making.

Further investigation should also address social judgment theory, which highlights the tendency of individuals to evaluate themselves relative to others, potentially exacerbating overconfidence. Lastly, research should continue to explore the Motivation-Opportunity-Ability(MOA) framework to understand how motivation, opportunity, and perceived ability contribute to excessive risk-taking and overconfidence in financial decision-making (Chen et al., Citation2021). By synthesizing these theories and conducting empirical studies, researchers can provide more robust theoretical frameworks and valuable insights to help practitioners and individuals better understand and mitigate the detrimental effects of financial overconfidence. Future research should need Meta-analytical insights to understand what theories/models have the highest value for financial decision-making.

Thus, we posit the following proposition:

Proposition 2:

Applying various frameworks can efficiently unravel the causes and effects of overconfidence on investors.

7.2. Context

Overconfidence research in finance should explore cultural differences and their effects. The current study provides a valuable overview of overconfidence across nations and raises questions regarding cultural causes that cause these disparities. Cultural factors, including individuality vs. collectivism, uncertainty avoidance, and power distance, can be examined to see how they affect financial overconfidence (Beckmann et al., Citation2008). This study direction can discover cultural characteristics that affect overconfidence in financial decision-making, improving our understanding of its global impact. Future studies should go beyond descriptive analysis and offer culturally relevant interventions and educational programs. Understanding how cultural variables, human attributes, and economic conditions affect overconfidence might help create successful interventions. Researchers can examine whether culturally specific approaches reduce overconfidence and encourage reasonable financial behavior. Thus, we formulate the following proposition:

Proposition 3:

The effects of overconfidence in investors differ in various settings, such as between cross-cultural and cross-national contexts.

7.3. Methods

This review identifies many empirical studies in the current literature in this field. The study of overconfidence in finance needs to improve its methods to comprehend this complex phenomenon better. Future research should adopt and execute novel ideas regarding methodologies and research design, such as advanced machine learning and NLP (Natural language processing) techniques for large-scale financial and textual data analysis, which seem promising (Khalil & Pipa, Citation2022). Researchers can acquire real-time insights on market sentiment, investor behavior, and the effects of news events on overconfidence by mining financial reports, news articles, and social media sentiment. Thus, the following proposition is advanced:

Proposition 4:

Using NLP and textual analysis to reveal investor sentiment toward their decision-making

Data-driven analysis can provide a more dynamic and timely view of the causes of financial overconfidence. Integrating physiological and behavioral experiments is another crucial direction (Duxbury, Citation2015). More qualitative work (e.g. in-depth interviews, observations, discourse analysis, laddering techniques, ethnography, case studies, and qualitative comparative analysis) is needed to understand the overconfidence that quantitative methodologies may need to capture. These methods can assist researchers in identifying overconfident decision-making moments and physiological indications when used with typical experimental designs. Therefore, we posit the following proposition:

Proposition 5:

Applying diverse research methods can efficiently provide deeper insights into investor decision-making.

8 Implications

This study highlights the multidimensional nature of overconfidence in financial decision-making by synthesizing evolving ideas and integrating the bibliometric and TCM frameworks. This improved comprehension is critical for academics and practitioners in the financial industry. The research successfully bridges the gap between psychological theories and the financial decision-making process by incorporating the TCM frameworks. This synthesis of theoretical approaches offers a more in-depth comprehension of the cognitive processes that contribute to the development of overconfidence in individuals. This work presents the new research pathways to be investigated in financial overconfidence and opens up new possibilities in this field.

Further, Investors, financial advisors, and legislators must deeply comprehend the complexities of displaying excessive confidence in one’s financial situation. When investing, it is beneficial for investors to be aware of their biases and take action to battle overconfidence in their decision-making. Being aware of their biases and trying to combat overconfidence may be found here. Financial advisers can use this information to help their clients better by giving them more educated counsel, which is made possible using the information. Investing in financial literacy programs can effectively enhance investor awareness and promote more rational decision-making. By equipping investors with the knowledge to recognize and mitigate overconfidence, policymakers can contribute to a more stable and resilient financial system (Cwynar et al., Citation2020; Vörös et al., Citation2021). Also, insights from behavioral economics into policy-making procedures can yield a more holistic comprehension of how psychological biases, such as overconfidence, impact economic behavior. Policymakers can design interventions that consider investors’ cognitive limitations and work towards creating a more resilient financial ecosystem. With the help of this tactic, scholars who specialize in a wide range of fields are encouraged to collaborate to contribute to a more in-depth understanding of the part that behavioral biases play in finance.

9. Conclusions

The current hybrid systematic review utilizes bibliometric tools and content analysis, employing the TCM framework to examine and synthesize overconfidence research. This review contributes deeper insights into critical contributors (journals, authors, articles) of financial overconfidence research, serving as a valuable reference for academic scholars and industry professionals seeking expert opinions (Merkle, Citation2017). The article addresses five research questions through a systematic procedure, where our review evaluates the literature, highlights performance trends, and explains the intellectual structure of overconfidence research. Furthermore, discovering five significant clusters in this research field and identifying keyword co-occurrence add robustness to the clusters’ contents. Additionally, we conducted in-depth content analysis using the TCM framework, presenting the most prominent theories, geographical context, and impactful methods used in overconfidence research.

10. Limitations

Even though the required protocol was followed and a comprehensive literature analysis was performed, the findings of this study are nevertheless restricted in several ways. First, only the SCOPUS database is used for bibliometric analysis research. In subsequent studies, investigators might look at articles sourced from single or numerous databases, such as Web of Science or EBSCO. Second, there is a possibility that particular research has been omitted due to the use of filters and keywords. Third, this investigation was limited to papers written in English; as a result, we may have overlooked any pertinent publications initially published in languages other than English.

Author contributions

Dr. Dharmendra Singh: Conceptualizing our thoughts in the manuscript, retrieving data from Scopus, conducting bibliometric analysis, and performing performance analysis. Dr. Garima Malik: Cluster Analysis and Comprehensive TCCM Analysis, Proofreading, and Formatting. Dr. Prateek Jain: Future Research Directions and Implications. Dr. Mahmoud Abouria: Revised the manuscript as per the recommended revisions.

Data availability statement

The data for the study were retrieved from SCOPUS within the specified period (as mentioned in the manuscript), following the proper procedure for data retrieval, including keywords. Subsequently, a data filtering process was conducted. Anyone can retrieve the data from SCOPUS by applying the same criteria used in the study.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Dharmendra Singh

Dr. Dharmendra Singh is an Associate Professor and program head (Finance) at Modern College of Business and Science, Muscat (Oman). He possesses rich professional experience of over 23 years in the field of finance. He holds a Ph.D. (Finance), professional certifications like Certified Financial Planner (CFP), an associate diploma (life insurance) from the Insurance Institute of India, and a CFA. He has published several articles & research papers in ABDC, CABS, and Scopus Q1-ranked international and refereed journals. He has published five edited books with renowned publishers. His research areas include banking, corporate finance, entrepreneurial finance, and financial markets.

Garima Malik

Dr. Garima Malik is an Assistant Professor in the Marketing area at Birla Institute of Technology Management (BIMTECH), Greater Noida. She is a Fellow of Xavier School of Management, XLRI Jamshedpur, India, and a recipient of the K.V. Raju (Narajuan Award) Gold Medal awarded to an outstanding Ph.D. student. She has more than twenty years of academic experience. Her research interests span various areas, including gamification, marketing analytics, customer engagement, destination marketing, and gaming marketing experience. She authored more than 80+ research papers. In addition to her research contributions, Dr. Malik has written five books, two of which are textbooks, and four are case study books.

Prateek Jain

Dr. Prateek Jain is working as Associate Professor of Strategy & Entrepreneurship at Birla Institute of Management Technology (BIMTECH), Greater Noida. Before joining Academics he had worked in Corporate sector for 23 years in various Industries & sectors. Dr. Prateek had done his PhD from IIT Delhi and MBA from IIM Lucknow. He had done his graduation in Mechanical Engineering. Dr. Prateek had also authored 3 Books in the area of Management & Strategy.

Mahmoud Abouraia

Dr. Mahmoud Abouraia is a Professor and head of the Ph.D. program at the Modern College of Business and Science, Muscat (Oman). He has published several papers in reputed journals. His research areas include banking, corporate finance, and financial markets.

References

- Abdallah, S., &Hilu, K. (2015). Exploring Determinants to Explain Aspects of Individual Investors’ Financial Behaviour. Australasian Accounting, Business and Finance Journal, 9(2), 4–22. https://doi.org/10.14453/aabfj.v9i2.2

- Abreu, M., & Mendes, V. (2012). Information, overconfidence, and trading: Do the sources of information matter? Journal of Economic Psychology, 33(4), 868–881. https://doi.org/10.1016/j.joep.2012.04.003

- Adel, B., & Mariem, T. (2013). The impact of overconfidence on investors’ decisions. Business and Economic Research, 3(2), 53. https://doi.org/10.5296/ber.v3i2.4200

- Ahmad, F. (2020). Personality traits as a predictor of cognitive biases: The moderating role of risk-attitude. Qualitative Research in Financial Markets, 12(4), 465–484. https://doi.org/10.1108/QRFM-10-2019-0123

- Aini, N. S. N. & Lutfi, L. (2019). The influence of risk perception, risk tolerance, overconfidence, and loss aversion towards investment decision making. Journal of Economics, Business, & Accountancy Ventura, 21(3), 401–413. https://doi.org/10.14414/jebav.v21i3.1663

- Akhtar, F., & Das, N. (2020). Investor personality and investment performance: From the perspective of psychological traits. Qualitative Research in Financial Markets, 12(3), 333–352. https://doi.org/10.1108/QRFM-11-2018-0116

- Ang, A., Gorovyy, S., & Van Inwegen, G. B. (2011). Hedge fund leverage. Journal of Financial Economics, 102(1), 102–126. https://doi.org/10.1016/j.jfineco.2011.02.020

- Ansari, Y., Albarrak, M. S., Sherfudeen, N., & Aman, A. (2023). Examining the relationship between financial literacy and demographic factors and the overconfidence of Saudi investors. Finance Research Letters, 52, 103582. https://doi.org/10.1016/j.frl.2022.103582

- Baker, H. K., Kumar, S., Goyal, N., & Gaur, V. (2019). How financial literacy and demographic variables relate to behavioral biases. Managerial Finance, 45(1), 124–146. https://doi.org/10.1108/MF-01-2018-0003

- Bansal, R., & Singh, D. (2021). Efficiency drivers of insurers in GCC: An analysis incorporating company-specific and external environmental variables. Cogent Economics & Finance, 9(1), 1922179. https://doi.org/10.1080/23322039.2021.1922179

- Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261–292. https://doi.org/10.1162/003355301556400

- Beckmann, D.,Menkhoff, L., &Suto, M. (2008). Does culture influence asset managers’ views and behavior?. Journal of Economic Behavior & Organization, 67(3-4), 624–643. https://doi.org/10.1016/j.jebo.2007.12.001

- Biais, B., Hilton, D., Mazurier, K., & Pouget, S. (2005). Judgemental overconfidence, self-monitoring, and trading performance in an experimental financial market. Review of Economic Studies, 72(2), 287–312. https://doi.org/10.1111/j.1467-937X.2005.00333.x

- Bourova, E.,Anderson, ME.,Ramsay, I., &Ali, P. ( 2018). Impacts of financial literacy andconfidence on the severity of financial hardship in Australia. Australasian Accounting, Business and Finance Journal, 12(4), 4–23. https://doi.org/10.14453/aabfj.v12i4.2

- Bouteska, A., Harasheh, M., & Abedin, M. Z. (2023). Revisiting overconfidence in investment decision-making: Further evidence from the US market. Research in International Business and Finance, 66, 102028. https://doi.org/10.1016/j.ribaf.2023.102028

- Broihanne, M.-H., Merli, M., & Roger, P. (2014). Overconfidence, risk perception and the risk-taking behavior of finance professionals. Finance Research Letters, 11(2), 64–73. https://doi.org/10.1016/j.frl.2013.11.002

- Chen, Y.,Mandler, T., &Meyer-Waarden, L. (2021). Three decades of research on loyalty programs: A literature review and future research agenda. Journal of Business Research, 124, 179–197. https://doi.org/10.1016/j.jbusres.2020.11.057

- Combrink, S., &Lew, C. (2020). Potential Underdog Bias, Overconfidence and Risk Propensity in Investor Decision-Making Behavior. Journal of Behavioral Finance, 21(4), 337–351. https://doi.org/10.1080/15427560.2019.1692843

- Costa-Cordella, S., Arevalo-Romero, C., Parada, F. J., & Rossi, A. (2021). Social support and cognition: A systematic review. Frontiers in Psychology, 12, 637060. https://doi.org/10.3389/fpsyg.2021.637060

- Cwynar, A., Cwynar, W., Patena, W., & Sibanda, W. (2020). Young adults’ financial literacy and overconfidence bias in debt markets. International Journal of Business Performance Management, 21(1/2), 95–113. https://doi.org/10.1504/IJBPM.2020.106117

- Daniel, K., Hirshleifer, D., & Subrahmanyam, A. (1998). Investor psychology and security market under‐ and overreactions. The Journal of Finance, 53(6), 1839–1885. https://doi.org/10.1111/0022-1082.00077

- Deaves, R., Lüders, E., & Luo, G. Y. (2009). An experimental test of the impact of overconfidence and gender on trading activity. Review of Finance, 13(3), 555–575. https://doi.org/10.1093/rof/rfn023

- Deaves, R., Lüders, E., & Schröder, M. (2010). The dynamics of overconfidence: Evidence from stock market forecasters. Journal of Economic Behavior & Organization, 75(3), 402–412. https://doi.org/10.1016/j.jebo.2010.05.001

- Dittrich, D. A., Güth, W., & Maciejovsky, B. (2005). Overconfidence in investment decisions: An experimental approach. The European Journal of Finance, 11(6), 471–491. https://doi.org/10.1080/1351847042000255643

- Doukas, J. A., & Petmezas, D. (2007). Acquisitions, overconfident managers and self‐attribution bias. European Financial Management, 13(3), 531–577. https://doi.org/10.1111/j.1468-036X.2007.00371.x

- Du, N., & Budescu, D. V. (2007). Does past volatility affect investors’ price forecasts and confidence judgements? International Journal of Forecasting, 23(3), 497–511. https://doi.org/10.1016/j.ijforecast.2007.03.003[Mismatch[InsertedFromOnline

- Durand, R., Newby, R., Tant, K., & Trepongkaruna, S. (2013). Overconfidence, overreaction, and personality. Review of Behavioral Finance, 5(2), 104–133. https://doi.org/10.1108/RBF-07-2012-0011

- Duxbury, D. (2015). Behavioral finance: insights from experiments I: Theory and financial markets. Review of Behavioral Finance, 7(1), 78–96. https://doi.org/10.1108/RBF-03-2015-0011

- Duy Bui, L., Chi Le, T., Ngoc Quang, A. H., & Wong, W.-K. (2021). Determinants of the possibilities by investors’ risk-taking: Empirical evidence from Vietnam. Cogent Economics & Finance, 9(1), 1917106. https://doi.org/10.1080/23322039.2021.1917106

- Ehrlinger, J., Mitchum, A. L., & Dweck, C. S. (2016). Understanding overconfidence: Theories of intelligence, preferential attention, and distorted self-assessment. Journal of Experimental Social Psychology, 63, 94–100. https://doi.org/10.1016/j.jesp.2015.11.001

- Fellner-Röhling, G., & Krügel, S. (2014). Judgmental overconfidence and trading activity. Journal of Economic Behavior & Organization, 107, 827–842. https://doi.org/10.1016/j.jebo.2014.04.016

- Filbeck, G., Hatfield, P., & Horvath, P. (2005). Risk aversion and personality type. Journal of Behavioral Finance, 6(4), 170–180. https://doi.org/10.1207/s15427579jpfm0604_1

- Filbeck, G., Ricciardi, V., Evensky, H. R., Fan, S. Z., Holzhauer, H. M., & Spieler, A. (2017). Behavioral finance: A panel discussion. Journal of Behavioral and Experimental Finance, 15, 52–58. https://doi.org/10.1016/j.jbef.2017.07.008

- Gerrans, P., &Heaney, R. (2019). The impact of undergraduate personal finance education on individual financial literacy, attitudes and intentions. Accounting & Finance, 59(1), 177–217. https://doi.org/10.1111/acfi.12247

- Gervais, S., & Odean, T. (2001). Learning to be overconfident. Review of Financial Studies, 14(1), 1–27. https://doi.org/10.1093/rfs/14.1.1

- Glaser, M., & Weber, M. (2007). Overconfidence and trading volume. The Geneva Risk and Insurance Review, 32(1), 1–36. https://doi.org/10.1007/s10713-007-0003-3

- Gloede, O., & Menkhoff, L. (2014). Financial professionals’ overconfidence: Is it experience, function, or attitude? European Financial Management, 20(2), 236–269. https://doi.org/10.1111/j.1468-036X.2011.00636.x

- Goetzmann, W. N., & Kumar, A. (2008). Equity portfolio diversification. Review of Finance, 12(3), 433–463. https://doi.org/10.1093/rof/rfn005

- Grežo, M. (2021). Overconfidence and financial decision-making: A meta-analysis. Review of Behavioral Finance, 13(3), 276–296. https://doi.org/10.1108/RBF-01-2020-0020

- Grinblatt, M., & Keloharju, M. (2009). Sensation seeking, overconfidence, and trading activity. The Journal of Finance, 64(2), 549–578. https://doi.org/10.1111/j.1540-6261.2009.01443.x

- Hala, Y., Abdullah, M. W., Andayani, W., Ilyas, G. B., & Akob, M. (2020). The financial behavior of investment decision making between real and financial assets sectors. The Journal of Asian Finance, Economics and Business, 7(12), 635–645. https://doi.org/10.13106/jafeb.2020.vol7.no12.635

- Hamilton, E. L., & Winchel, J. (2019). Investors’ processing of financial communications: A persuasion perspective. Behavioral Research in Accounting, 31(1), 133–156. https://doi.org/10.2308/bria-52211

- Hlouskova, J., Fortin, I., & Tsigaris, P. (2017). The consumption–investment decision of a prospect theory household: A two-period model. Journal of Mathematical Economics, 70, 74–89. https://doi.org/10.1016/j.jmateco.2017.02.003

- Hsu, Y.-L. (2022). Financial advice seeking and behavioral bias. Finance Research Letters, 46, 102505. https://doi.org/10.1016/j.frl.2021.102505

- Jain, J., Walia, N., & Gupta, S. (2019). Evaluation of behavioral biases affecting investment decision-making of individual equity investors by fuzzy analytic hierarchy process. Review of Behavioral Finance, 12(3), 297–314. https://doi.org/10.1108/RBF-03-2019-0044

- Jiang, J., Liao, L., Wang, Z., & Xiang, H. (2020). Financial literacy and retail investors’ financial welfare: Evidence from mutual fund investment outcomes in China. Pacific-Basin Finance Journal, 59, 101242. https://doi.org/10.1016/j.pacfin.2019.101242

- Kahneman, D., & Riepe, M. W. (1998). Aspects of investor psychology. The Journal of Portfolio Management, 24(4), 52–65. https://doi.org/10.3905/jpm.1998.409643

- Kahneman, D., & Tversky, A. (1979). Intuitive prediction: Biases and corrective procedures. TIMS Studies in Management Science, 1, 2,313–327.

- Kahneman, D., & Tversky, A. (2013). Prospect theory: An analysis of decision under risk. In Handbook of the fundamentals of financial decision making: Part I (pp. 99–127).

- Kansal, P., & Singh, S. (2018). Determinants of overconfidence bias in Indian stock market. Qualitative Research in Financial Markets, 10(4), 381–394. https://doi.org/10.1108/QRFM-03-2017-0015

- Kawamura, T., Mori, T., Motonishi, T., & Ogawa, K. (2021). Is financial literacy dangerous? Financial literacy, behavioral factors, and financial choices of households. Journal of the Japanese and International Economies, 60, 101131. https://doi.org/10.1016/j.jjie.2021.101131

- Khalil, F., & Pipa, G. (2022). Is deep-learning and natural language processing transcending the financial forecasting? Investigation through lens of news analytic process. Computational Economics, 60(1), 147–171. https://doi.org/10.1007/s10614-021-10145-2

- Khan, M. T. I., Tan, S. H., & Chong, L. L. (2017). How past perceived portfolio returns affect financial behaviors—The underlying psychological mechanism. Research in International Business and Finance, 42, 1478–1488. https://doi.org/10.1016/j.ribaf.2017.07.088

- Kirchler, E., & Maciejovsky, B. (2002). Simultaneous over-and underconfidence: Evidence from experimental asset markets. Journal of Risk and Uncertainty, 25(1), 65–85. https://doi.org/10.1023/A:1016319430881

- Kleine, J., Wagner, N., & Weller, T. (2016). Openness endangers your wealth: Noise trading and the big five. Finance Research Letters, 16, 239–247. https://doi.org/10.1016/j.frl.2015.12.002

- Kourtidis, D., Šević, Ž., & Chatzoglou, P. (2011). Investors’ trading activity: A behavioural perspective and empirical results. The Journal of Socio-Economics, 40(5), 548–557. https://doi.org/10.1016/j.socec.2011.04.008

- Kumar, S., & Goyal, N. (2016). Evidence on rationality and behavioural biases in investment decision making. Qualitative Research in Financial Markets, 8(4), 270–287. https://doi.org/10.1108/QRFM-05-2016-0016

- Liyanaarachchi, G., Deshpande, S., & Weaven, S. (2021). Online banking and privacy: Redesigning sales strategy through social exchange. International Journal of Bank Marketing, 39(6), 955–983. https://doi.org/10.1108/IJBM-05-2020-0278

- Lude, M., & Prügl, R. (2018). Why the family business brand matters: Brand authenticity and the family firm trust inference. Journal of Business Research, 89, 121–134. https://doi.org/10.1016/j.jbusres.2018.03.040

- Marjerison, R. K., Han, L., & Chen, J. (2023). Investor behavior during periods of crises: The Chinese funds market during the 2020 pandemic. Review of Integrative Business and Economics Research, 12(1), 71–91.

- Meier, C., & De Mello, L. (2020). Investor overconfidence in experimental asset markets across market states. Journal of Behavioral Finance, 21(4), 369–384. https://doi.org/10.1080/15427560.2019.1692845

- Menkhoff, L., Schmeling, M., & Schmidt, U. (2013). Overconfidence, experience, and professionalism: An experimental study. Journal of Economic Behavior & Organization, 86, 92–101. https://doi.org/10.1016/j.jebo.2012.12.022

- Merkle, C. (2017). Financial overconfidence over time: Foresight, hindsight, and insight of investors. Journal of Banking & Finance, 84, 68–87. https://doi.org/10.1016/j.jbankfin.2017.07.009

- Michailova, J., & Schmidt, U. (2016). Overconfidence and bubbles in experimental asset markets. Journal of Behavioral Finance, 17(3), 280–292. https://doi.org/10.1080/15427560.2016.1203325

- Mishra, K. C., & Metilda, M. J. (2015). A study on the impact of investment experience, gender, and level of education on overconfidence and self-attribution bias. IIMB Management Review, 27(4), 228–239. https://doi.org/10.1016/j.iimb.2015.09.001

- Moore, D. A., & Healy, P. J. (2008). The trouble with overconfidence. Psychological Review, 115(2), 502–517. https://doi.org/10.1037/0033-295X.115.2.502

- Moulton, S., Loibl, C., Samak, A., & Michael Collins, J. (2013). Borrowing capacity and financial decisions of low-to-moderate income first-time homebuyers. Journal of Consumer Affairs, 47(3), 375–403. https://doi.org/10.1111/joca.12021

- Nguyen, D. V., Dang, D. Q., Pham, G. H., & Do, D. K. (2020). Influence of overconfidence and cash flow on investment in Vietnam. The Journal of Asian Finance, Economics and Business, 7(2), 99–106. https://doi.org/10.13106/jafeb.2020.vol7.no2.99

- Nicolosi, G., Peng, L., & Zhu, N. (2004). Do individual investors learn from their trading experience? Yale ICF Working Paper no. 03–32

- Odean, T. (1998). Are investors reluctant to realize their losses? The Journal of Finance, 53(5), 1775–1798. https://doi.org/10.1111/0022-1082.00072

- Odean, T. (1999). Do investors trade too much? American Economic Review, 89(5), 1279–1298. https://doi.org/10.1257/aer.89.5.1279

- Olsson, H. (2014). Measuring overconfidence: Methodological problems and statistical artifacts. Journal of Business Research, 67(8), 1766–1770. https://doi.org/10.1016/j.jbusres.2014.03.002

- Pak, T.-Y., & Chatterjee, S. (2016). Aging, overconfidence, and portfolio choice. Journal of Behavioral and Experimental Finance, 12, 112–122. https://doi.org/10.1016/j.jbef.2016.10.003

- Pan, C. H., & Statman, M. (2013). Investor personality in investor questionnaires. Journal of Investment Consulting, 14(1), 48–56.

- Parveen, S., Satti, Z. W., Subhan, Q. A., & Jamil, S. (2020). Exploring market overreaction, investors’ sentiments, and investment decisions in an emerging stock market. Borsa Istanbul Review, 20(3), 224–235. https://doi.org/10.1016/j.bir.2020.02.002

- Paul, J., & Rosado-Serrano, A. (2019). Gradual Internationalization vs Born-Global/International new venture models: A review and research agenda. International Marketing Review, 36(6), 830–858. https://doi.org/10.1108/IMR-10-2018-0280

- Peress, J. (2004). Wealth, information acquisition, and portfolio choice. Review of Financial Studies, 17(3), 879–914. https://doi.org/10.1093/rfs/hhg056

- Pertiwi, T. K.,Yuniningsih, Y., &Anwar, M. (2019). The biased factors of investor’s behavior in stock exchange trading. Management Science Letters, 835–842. https://doi.org/10.5267/j.msl.2019.3.005

- Pikulina, E., Renneboog, L., & Tobler, P. N. (2017). Overconfidence and investment: An experimental approach. Journal of Corporate Finance, 43, 175–192. https://doi.org/10.1016/j.jcorpfin.2017.01.002

- Prosad, J. M., Kapoor, S., & Sengupta, J. (2015). Behavioral biases of Indian investors: A survey of Delhi-NCR region. Qualitative Research in Financial Markets, 7(3), 230–263. https://doi.org/10.1108/QRFM-04-2014-0012

- Puaschunder, J. M. (2017). Socio-psychological motives of socially responsible investors. In Global corporate governance (pp. 209–247). Emerald Publishing Limited.

- Rahman, M., & Gan, S. S. (2020). Generation Y investment decision: An analysis using behavioural factors. Managerial Finance, 46(8), 1023–1041. https://doi.org/10.1108/MF-10-2018-0534

- Robinson, A. T., &Marino, L. D. (2015). Overconfidence and risk perceptions: do they really matter for venture creation decisions?. International Entrepreneurship and Management Journal, 11(1), 149–168. https://doi.org/10.1007/s11365-013-0277-0

- Sabir, S. A., Mohammad, H. B., & Shahar, H. B. K. (2019). The role of overconfidence and past investment experience in herding behaviour with a moderating effect of financial literacy: Evidence from Pakistan stock exchange. Asian Economic and Financial Review, 9(4), 480–490. https://doi.org/10.18488/journal.aefr.2019.94.480.490 [InsertedFromOnline

- Sahi, S. K., & Arora, A. P. (2012). Individual investor biases: A segmentation analysis. Qualitative Research in Financial Markets, 4(1), 6–25.

- Shah, S. Z. A., Ahmad, M., & Mahmood, F. (2018). Heuristic biases in investment decision-making and perceived market efficiency: A survey at the Pakistan stock exchange. Qualitative Research in Financial Markets, 10(1), 85–110. https://doi.org/10.1108/QRFM-04-2017-0033

- Sharma, D., Misra, V., & Pathak, J. P. (2021). Emergence of behavioural finance: A study on behavioural biases during investment decision-making. International Journal of Economics and Business Research, 21(2), 223–234. https://doi.org/10.1504/IJEBR.2021.113140

- Singh, D., & Malik, G. (2018). Technical efficiency and its determinants: A panel data analysis of Indian public and private sector banks. Asian Journal of Accounting Perspectives, 11(1), 48–71. https://doi.org/10.22452/AJAP.vol11no1.3

- Singh, D., & Malik, G. (2022). A systematic and bibliometric review of the financial well-being: Advancements in the current status and future research agenda. International Journal of Bank Marketing, 40(7), 1575–1609. https://doi.org/10.1108/IJBM-06-2021-0238

- Statman, M., Thorley, S., & Vorkink, K. (2006). Investor overconfidence and trading volume. Review of Financial Studies, 19(4), 1531–1565. https://doi.org/10.1093/rfs/hhj032

- Syed, R. T., Singh, D., Agrawal, R., & Spicer, D. P. (2023). Entrepreneurship development in universities across Gulf Cooperation Council countries: A systematic review of the research and way forward. Journal of Enterprising Communities: People and Places in the Global Economy, 17(5), 1045–1062. https://doi.org/10.1108/JEC-03-2022-0045

- Syed, R. T., Singh, D., & Spicer, D. (2023). Entrepreneurial higher education institutions: Development of the research and future directions. Higher Education Quarterly, 77(1), 158–183. https://doi.org/10.1111/hequ.12379

- Tekçe, B.,Yılmaz, N., &Bildik, R. (2016). What factors affect behavioral biases? Evidence from Turkish individual stock investors. Research in International Business and Finance, 37, 515–526. https://doi.org/10.1016/j.ribaf.2015.11.017

- Tomar, S., Baker, H. K., Kumar, S., & Hoffmann, A. O. (2021). Psychological determinants of retirement financial planning behavior. Journal of Business Research, 133, 432–449. https://doi.org/10.1016/j.jbusres.2021.05.007

- Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4), 297–323. https://doi.org/10.1007/BF00122574

- Tversky, A., Kahneman, D., & Slovic, P. (1982). Judgment under uncertainty: Heuristics and biases (pp. 3-20).

- Van Rooij, M., Lusardi, A., & Alessie, R. (2011). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449–472. https://doi.org/10.1016/j.jfineco.2011.03.006

- Vörös, Z., Szabó, Z., Kehl, D., Kovács, O. B., Papp, T., & Schepp, Z. (2021). The forms of financial literacy overconfidence and their role in financial well-being. International Journal of Consumer Studies, 45(6), 1292–1308. https://doi.org/10.1111/ijcs.12734

- Waweru, N. M., Munyoki, E., & Uliana, E. (2008). The effects of behavioural factors in investment decision-making: A survey of institutional investors operating at the Nairobi Stock Exchange. International Journal of Business and Emerging Markets, 1(1), 24. https://doi.org/10.1504/IJBEM.2008.019243

- Wilaiporn, P., Nongnit, C., & Surachai, C. (2021). Factors Influencing retail investors’ trading behaviour in the Thai stock market.

- Zacharakis, A. L., & Shepherd, D. A. (2001). The nature of information and overconfidence on venture capitalists’ decision making. Journal of Business Venturing, 16(4), 311–332. https://doi.org/10.1016/S0883-9026(99)00052-X

- Zaleskiewicz, T. (2011). Financial forecasts during the crisis: Were experts more accurate than laypeople? Journal of Economic Psychology, 32(3), 384–390. https://doi.org/10.1016/j.joep.2011.02.003