?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

It has repeatedly been claimed that institutions play an important, and decisive role in economic development. Many studies have analyzed the effect of formal institution on financial development while informal institutions have received less attention. With this paper, we contribute to the effect of personal freedom as a measure for informal institutions on financial development using annual data from 40 African countries spanning 2000 to 2020. We employ the novel fixed effect panel quantile regression technique. The study documents that, in the upper quantile, personal freedom negatively and significantly affects financial development. This finding explicates that, a low level of personal freedom restricts human choices, limiting personal participation in the development of the financial system in Africa. Thus, personal freedom is important for Africa’s financial development. The study recommends that policymakers rally resolute support to defend and protect human rights and personal liberties that encourage human choices. Additionally, the findings intuitively reinforce the prerequisite for African governments regularly evaluate policies that promote financial sector development, particularly economic freedom and government expenditures.

Impact statement

This research offers a significant contribution to the understanding of the relationship between informal institutions, specifically personal freedom, and financial development in Africa. By employing data from 40 African countries over two decades, and utilising fixed-effect panel quantile regression, the study provides evidence of how personal freedom significantly influences financial development in the upper quantiles. The findings underscore the need of human rights and personal liberties in facilitating financial sector growth, suggesting that enhanced personal freedoms foster greater individual participation in financial markets, which is vital for robust financial sector development.

The findings underscore the need for policymakers to prioritising the protection and enhancement of personal freedoms as a strategy for financial sector development in Africa. This research also emphasis the necessity for continuous policy evaluation to provide a strategic roadmap for enhancing Africa’s financial infrastructure. Consequently, the study does not only advance the academic discourse on the importance of informal institutions in financial development in Africa but also, provides actionable recommendations for governance and policy in African countries, potentially stimulating financial growth and stability through the reinforcement of personal freedom.

Reviewing Editor:

1. Introduction

Over the period, extensive literature has provided empirical evidence that financial development enhances economic growth in both developed and underdeveloped economies (Oroud et al., Citation2023, Ahiakpor et al., Citation2023, Bist, Citation2018, Levine and Zervos, Citation1998). From the above, one may pose the question, why have some countries instituted growth-enhancing financial systems and others have not? Some scholars argue that identifying whether bank-based or market-based financial systems enhance growth is irrelevant but developing efficient institutions—a legal environment that enhances the operations and effectiveness of financial systems (La Porta et al., Citation1997, Citation1998, Levine, Citation2000 and Sarhangi, et al., Citation2021). Hence, the law and finance theory posits that in countries where there is support for private contractual arrangements, legal rights protection for investors and enforcement of private property rights, investors’ confidence is enhanced, thereby being influenced to effectively participate in financial markets hence, financial development. However, the African financial environment, despite several interventions that have yielded notable strides, still remains characterized by political and economic instability, and lower institutional quality compared to its counterparts, resulting in underdevelopment of its financial sector (Ofori et al., Citation2021, Aluko & Ajayi, Citation2018). Conventional knowledge derived from literature posits that greater personal freedom tends to positively correlate with higher levels of financial development. Yet empirical analysis establishing such relationship is scanty. Against this background, this study explores the personal freedom-financial development nexus in Africa to establish whether or not personal liberties are key determinant of Africa’s financial development.

A great number of empirical studies link formal institutions to financial development. Dosso (Citation2023) for instance, harnessed the impact of institutional quality on financial development in 100 resource-rich countries in the regions of Asia, Latin America, sub-Saharan Africa and the Organization for Economic Co-operation and Development (OECD). Also, Vatamanu & Zugravu (Citation2023) used a panel data approach to examine financial development, institutional quality and renewable energy consumption in 27 European (EU) member states. Similarly, Islam & Alhamad (Citation2022) investigated the impact of financial development and institutional quality on the remittance-growth nexus in top ten remittance-receiving countries. In the above mentioned studies, the worldwide governance indicators variables such as, government effectiveness, political stability, regulatory quality, voice and accountability were used to proxy formal institutions in their empirical investigations. Another strand of literature also highlights the nexus between informal institutions and financial development. Travkina et al. (Citation2023) explored how culture impacts the quality of institutions to impact financial and economic development; and highlighted that institutional quality shaped by culture is relevant for shaping financial development into a driver of robust and long-lasting economic growth. Williamson (Citation2012), explored how expanding the notion of the informal institution using McCloskey’s notion of ‘dignity and liberty’, helps to provide a more comprehensive explanation of development and, Garretsen et al. (Citation2004) examined the role of societal norms in explaining cross-country differences in financial development across 43 countries. Nonetheless, the causality between personal freedom—which gives individuals the autonomy to make relevant financial choices and inspire innovation, and financial development has not been strictly studied and is possibly inadvertently neglected in the literature.

This study contributes to the literature in diverse ways to fill this gap. First, it explores the causal relationship between financial development and informal institutions proxied by personal freedom. Empirical evidence from studies such as Hoover and Smimou (Citation2023) and Gholipour et al. (Citation2014) indicates that personal freedom plays a key role in economically relevant decision-making. However, financial development which results from the decision to participate in financial systems, is a special decision-making process that needs to be explored more empirically by examining how personal freedom affects it. Personal freedom is of key interest to this study, as countries with strong institutions—transparent legal systems and property rights protection, tend to favour higher levels of personal freedom and financial development (Acemoglu and Robinson, Citation2005).

Again, studies such as Barro and Lee (Citation2013), and Besley and Persson (Citation2011) have highlighted the role of personal freedom in creating an environment that inspires creativity, encourages entrepreneurship, fosters trust and confidence for investment and allows individuals the autonomy to participate in formal financial systems however, empirical analysis that establishes the personal freedom-financial development nexus is lacking. To establish this empirically, the personal freedom index by the Cato and Fraser Institute (Citation2022) was employed in the study due to its worldwide coverage, international comparability and broad range of personal freedom indicators covering 41 freedom variables in seven broad areas. Second, the index interaction with security, safety and rule of law enables it to capture the environment in which human freedom is meaningful and thrives. Additionally, unlike the world press freedom index, the economist democracy index and the Cingranelli-Richards human rights dataset (CIRI) which narrowly focuses on either civil or economic freedom, the Cato & Fraser Institute’s index bridges the gap between civil and economic freedoms to create a more comprehensive index (Doering, Citation2012). This makes the index more advanced than other freedom indexes, making it more plausible to provide robust results in explaining why Africa has made considerable progress in financial development but is incomparable to other regions (Mlachila, et al., Citation2016).

Third, the study focuses on Africa because of its rich diversity in culture, language, religiosity and resource endowment (Kwatia et al., Citation2024). As personal freedom is shaped by norms and culture, it is expected to be heterogeneous across various African countries, thereby presenting the opportunity to test its association with financial development across the region. Fourth, as asserted by Lyu, et al. (Citation2023), the impact of informal institutions is highlighted by weak legal framework. African states are mostly emerging economies characterised by weak formal institutions such as a poor legal system that enforces private property rights and private contractual arrangements (Fung, Citation2022). However, current literature does not provide enough empirical evidence for Africa’s surge in financial development amidst weak, unstructured and inadequate formal institutional structures. This study seeks to examine whether personal freedom plays a role in Africa’s improved financial system amidst weak and underdeveloped formal institutional structures. Fifth, divergent from the linearity documented by literature, the study assumes a non-linear relationship between financial development and personal freedom. To deal with non-linearity, panel quantile regression is employed to examine the relationship between various distributions of the explanatory variables and the dependent variable (Koenker, Citation2005).

The substantive contribution of our research resides in its rigorous empirical investigation of the intricate relationship between personal freedom and financial development and the pursuit of economic growth within Africa context. Employing a comprehensive panel quantile regression and integrate diverse data source for measuring personal freedom, this study provides pivotal insights which are poised to significantly influence policy makers, as we unravel that personal freedom correlate strongly with financial development in Africa.

The rest of the paper is organised as follows: section 2 delves into the literature review, section 3 covers the methodology by describing the econometric approach and data employed in the analysis, section 4 presents the results and discussion and section 5 presents the conclusions and policy implications of the study.

2. Literature review

2.1. Theoretical review

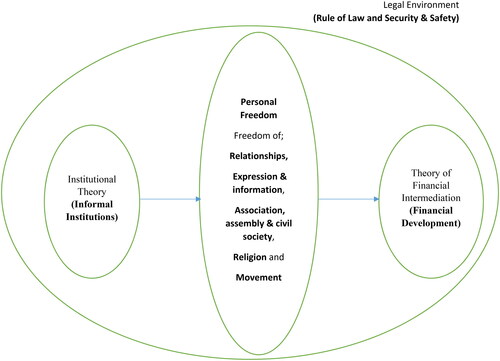

Researchers have disputed the association between financial development and economic growth and other predictors of growth; however, financial development has been proven to be related to growth (see Adu et al., Citation2013; Puatwoe and Piabuo, Citation2017; Khan and Senhadji, Citation2000). Tracing back to Schumpeter (Citation1911) and Goldsmith (Citation1969) on the debate, Schumpeter (Citation1911) put forward that, a well-developed financial system enhances technical innovation and is able to allocate capital from less productive areas to more productive ones fostering economic growth. Goldsmith (Citation1969) on the other hand, studied 35 countries between 1860-1963 and found a positive relationship between financial development and economic growth. Theoretically, literature has shown that, the finance-growth nexus is largely influenced by institutions, notably La Porta et al. (Citation2013) and North (Citation1990). Following their prior research on the legal protection of investors, and it economic outcomes –which set the pace for debate on how legal institutions influence finance, La Porta et al. (Citation2013) provided a cohesive summary of the empirical investigations subsequent to their studies. They concluded that, various countries have diverse legal rules and regulations peculiar to their environment. These are significantly influenced by their legal origins and historical differences; and the diversity in legal environment, impacts social and economic outcomes (Beck et al., Citation2001; Beck et al., Citation2003). North (Citation1990) on the other hand explored the role of institutions—formal rules, informal norms and enforcement mechanisms that are critical for economic development. He argues that both formal and informal institutions evolve and interact over time to influence economic outcomes. Thus external shocks and internal pressures trigger both formal and informal institutional transitions for societies, impacting development. Additionally, the theory of financial intermediation which adapts from information asymmetry and agency theories applies to this study. The theory, puts forward that, path-dependency and history are crucial in establishing financial systems. It also stresses that, market imperfections discourage investors and savers to trade directly making financial intermediaries more active in resource allocation such as domestic credit to private sector (Gurley & Shaw, Citation1960 and Scholtens & Van Wensveen, Citation2003). To this end, this study draws from the above theoretical framework by focusing on how informal institutional measures captured by North (Citation1990) within the enforcement mechanism of legal environment emphasized by La Porta et al. (Citation2013), impacts financial sector development highlighted by Gurley & Shaw (Citation1960) and Scholtens & Van Wensveen (Citation2003), in Africa. This is depicted pictorially in .

Figure 1. Theoretical framework of personal freedom and financial development. Legal Environment. (Rule of Law and Security & Safety). Authors’ Own Construct.

2.2. Empirical review

Literature has documented that the potential determinants of financial development to include macroeconomic, geographic and institutional factors (Huang, Citation2010). Following the aforementioned, we classify the empirical review into three sub-sections.

2.3. Financial development-macroeconomic factors nexus

The macroeconomic factors have been highlighted through policies. For instance, Majeed et al. (Citation2021) employed feasible generalized least squares and augmented mean group techniques to examine the impact of foreign direct investment (FDI) on financial development in 102 Belt & Road Initiative (BRI) countries in Asia, Africa, Europe and Lartin America from 1990 to 2017. They found that, FDI significantly increases financial development in Asia, Europe and Latin America but decreases in Africa. However, the income-wise results indicated that, due to high factor costs, low and middle income economies received more FDI than high income countries. On the other hand, Islam et al. (Citation2020) investigated the moderating role of institutional quality proxied by the world governance and political risk indicators on the financial development-FDI nexus among 79 BRI countries. The study concluded that, institutions play a significant role in the nexus hence, sound financial institutions are more attractive to FDI inflows relative to financial markets. Rajan and Zingales (Citation2003), studied the relationship between trade openness and financial development from 1913 to 1999 and found that trade openness is correlated with financial development particularly when unrestricted capital transfers across borders are encouraged. More recently, Tongurai and Vithessonthi (Citation2023) used the estimation of systems of equations to examine the finance openness and financial development nexus and found a positive bidirectional relationship between financial openness and financial development proxying financial development with the banking sector.

Similarly, a bidirectional and positive relationship is recorded between financial openness and the stock market but divergently, a negative relationship is reported between financial openness and the bond market studying countries from 1960 to 2020. In addition, empirical evidence proves that economies characterized by high inflation rates are likely to have under-developed financial systems that are small, less active and less efficient (Hung, Citation2003 and Ibrahim, et al., Citation2022). Aduba et al. (Citation2023) examined the impact of recent innovations in digital financial technologies (FinTech) on financial development using data from emerging and developing economies and found that FinTech drives financial development and strongly impacts the financial development of countries with low financial inclusion and weak financial sector performance. Consistently, Lavrinenko et al. (Citation2023) examined the impact of FinTech on financial development in European Union (EU) countries using frequency and correlation analysis in 2020 and found a favorable linear relationship between FinTech and financial market sub-index, financial market depth, financial market efficiency and financial institutions depth. Similarly, Khan et al. (Citation2024), employed both linear and dynamic regressions to investigate the relationship between institutional quality, innovative technologies and financial market development in 22 emerging economies from 2006 to 2017. The study found that, the interaction between institutional quality, innovation and technology, enhances financial development in emerging markets. In support of the above, Zhang and Liang (Citation2023), found that technological innovations have a positive association with financial development throughout quantiles and are key to financial market development. The study employed the bootstrap quantile regression technique on four economies from 1990 to 2020. Jemiluyi & Jeke (Citation2023), assessed the mediating role of digital technology in the remittance-financial development nexus in 35 Sub-Saharan African (SSA) countries. Employing the generalized method of moment (GMM) analysis on digital technology proxied by fixed broadband and mobile cellular subscription, and financial development proxied by domestic credit to the private sector and money supply, from 2011 to 2020. The study found that, in SSA, digital technology spurs remittance to stimulate financial development and is complementary in promoting financial development in the sub-region.

2.4. Financial development-geographical factors nexus

Regarding geographical factors, Bennett et al. (Citation2017) employed a two-stage least square (2SLS) estimate to investigate geographical factors, institutions and economic development and found that the impact of settlement conditions on institutional quality is stronger in former British colonies than that of European colonies. Again, the authors found the presence of both direct and indirect effects of geographical factors on economic development. Isiksal (Citation2023), employed the cross-sectionally augmented autoregressive distributed lag technique on Central Asian states from 1996 to 2020 to test the relationship between natural resources and financial development and conclude the relationship is not linear. The empirical results reported an inverted U-shaped relationship between natural resources and finance implying, that natural resources initially foster financial development and later impede it. Adekunle et al. (Citation2021) employed an augmented mean group (AMG) estimator in 20 African countries from 1996 to 2018 and found that geographical factors have a positive relationship with financial development; thus, geography leads to financial development in Africa.

By contrast, Han et al. (Citation2022) used panel data from the top 10 natural resource-abundant countries from 1990 to 2020 and found that natural resources reduce financial development in natural resource-abundant countries. Likewise, Oben (Citation2022) used a global sample of all countries to examine the impact of natural resources on financial development from 1980 to 2019 and found that, global natural resource rent has a significant negative association with financial development especially in the long-run, confirming the financial resource curse. The conclusions were drawn after employing several econometric analysis including; unit root and stationarity test, Johansen test for cointegration, granger causality test, vector autoregressive (VAR) and vector error correction model (VECM). In support of the above, Zhang and Liang (Citation2023) also find a negative association between natural resources and financial market development using the non-parametric bootstrap quantile regression technique in four South Asian economies from 1990 to 2020. However, the empirical findings revealed that improved institutional quality significantly reduces the negative impact of natural resources on financial development. In line with the above, Dosso (Citation2023), used panel data from 100 countries from 1996 to 2017 to estimate a non-linear panel model with endogenous threshold variables and concludes; that even if the impact of natural resources on financial development is negative, enhanced institutional quality reduces the negative impact. Also, Khan et al. (Citation2020) explored the critical role of the impact of institutional quality in the resource-finance nexus using a sample of 87 emerging and developing economies (EMDEs) from 1984 to 2018. They found evidence of the natural resource curse hypothesis. However, institutional quality positively moderated the resource-finance nexus by turning the curse into a blessing. The results additionally, documented evidence of a threshold effect for institutional quality, below which natural resources impedes financial development.

2.5. Financial development-institutional quality nexus

In their study, Islam and Alhamad (Citation2022) employed the pooled mean group (PMG) technique and Dumitrescu-Hurlin (D-H) causality check on a panel data of the ten largest remittance-earning economies and found that, financial development caused economic growth through the channel of institutional quality. Bennett et al. (Citation2017) explored the potential impact of economic institutions on economic development using a two-stage least square (2SLS) estimate and found that there is a positive relationship between economic institutions and economic development thus, a standard deviation increase in economic institutions is associated with three-fourth standard deviation increase in economic development. Iwegbu et al. (Citation2022) employed the fixed effect panel quantile regression to examined whether regional financial development and integration have a greater impact on the expansion of industrial sectors in 15 Economic Community of West African States (ECOWAS) member countries with high institutional quality than those with low institutional quality. They found that, the ECOWAS member nations with solid institutional quality framework experience increased industrial output deepening financial development. Similarly, Kutan et al. (Citation2017), explored the linkages of institutional quality in the finance-growth nexus in 21 Middle East and North African (MENA) countries from 1980-2012. They concluded that, in the presence of institutional quality, all measures of financial development support growth. Correspondingly, Khan et al. (Citation2019) found institutional quality to exert positive impact on financial development in 15 emerging and growth-leading economies (EAGLEs) employing 2SLS estimator.

Bekana (Citation2013) explored the effect of governance quality (general, political, economic and institutional) on financial development using quantile regression and the general method of moments estimations on a dataset of 45 African countries from 1996 to 2018 and found, positive effects of the quality of governance institution on financial development implying that poorly governed countries with weak rule of law and regulatory quality performs poorly in financial sector development consistent with La Porta et al. (Citation1997 & 1998), Demirgüç-Kunt and Maksimovic (Citation1998), Beck and Levine (Citation2002), Claesssens & Laeven (Citation2003), and Khan et al. (Citation2024), which highlight that legal institutions enhance financial development. On the informal institution-finance nexus, Hoover and Smimou (Citation2023) found that informal institutions (personal freedom) have a consistently sizeable positive impact on financial development by employing datasets from 13 economies, totaling 764 funds from 2001 to 2015, subject to different regressions such as sequential regression, squared Sharpe ratio, and principal component regression. In line with above, Khan et al. (Citation2022) showed that, national culture and institutional quality promotes financial markets development within emerging markets. The 2SLS regression with instrumental variable was employed on a data of 21 emerging markets from 1984 to 2020.

Úbeda et al. (Citation2022) studied the moderating role of formal and informal institutions on sustainable banking and financial development in 46 countries from 2010 to 2018 and found empirical evidence that sustainable banking affects financial development only in countries with strong formal institutions nonetheless, informal institutions promote trust in the banking sector and allows sustainable banking to positively affect financial development. Similarly, Feng, et al. (Citation2023) found that informal institutions such as religious beliefs significantly increase household engagement in the financial sector such as willingness to borrow, using microdata from China Family Panel Studies (CFPS) and subjecting it to a series of tests such as propensity score matching, panel-fixed effect and instrumental variables regression. Kwatia et al. (Citation2024), investigated the impact of religiosity proxied by religious freedom, on financial development in a panel of 42 African countries from 2000 to 2020. The results of the panel quantile estimator showed that, freedom matters for financial development in Africa. Also, religious freedom was found to be negatively associated with financial development. In exploring the relationship between democracy, freedom and economic development, Kabir and Alam (Citation2021) employed panel regression on 115 countries from 2006 to 2018 and found that democracy matters for economic development. The study also found that economic freedom had a significant positive relationship with economic development while personal freedom had detrimental effects on growth in low-freedom countries but acted as a catalyst for growth when countries reached high levels of personal freedom. Heckelman (Citation2000) employed the Grager-causality tests on 147 countries to confirm whether freedom causes growth or otherwise, or whether the two are jointly determined and found that, on average, freedom precedes economic growth. Khan et al. (Citation2020) used a panel threshold estimator to examine the relationship between economic freedom and financial development from 1984 to 2018 in 87 developing countries. They found that, economic freedom wields a favourable effect on financial development.

By far, existing literature on the drivers of financial development has focused on economic variables other than institutions. The available studies that consider how institutions impact financial development have also predominantly investigated the interconnectedness between formal institutions and financial development, with scant literature exploring informal institutions as a driver of financial development. Although a general consensus has been reached among researchers on the crucial role of informal institutions in financial development, empirical studies supporting this concept are still in progress. This study adds to the ongoing debate by examining how informal institutions proxy by personal freedom impact financial development in Africa. As most African states are characterized by weak economic, political and legal institutional frameworks, it is expected that the impact of personal freedom in shaping financial development in the region will be highlighted.

3. Methodology

3.1. Empirical estimation

To examine the relationship between personal freedom and financial development, we utilize panel quantile regression (PQR) to allows us to explore the range of conditional quantiles, thus revealing different forms of conditional heterogeneity, and controlling the unobserved individual effects (Kato et al., Citation2012). The control of individual heterogeneity through fixed effects and the study of heterogeneous covariates within the PQR framework offer more flexible approaches to panel data analysis than the traditional Gaussian estimation of fixed effects and random effects (Kato et al., Citation2012). The standard linear regression focuses on estimating the conditional mean, assuming constant variations and a normal distribution of errors, however the quantile regression offers a more flexible approach and deals with the effect of observed covariates in different quantiles of regressands (Armah & Amewu, Citation2024), whiles it handles varying variance and non-normal data and accommodates nonlinear relationships in different parts of the distribution (Raghutla et al., Citation2022). In this study we focus on the estimation of common parameters of the PQR model of individual effects. The resulting estimate is called the Fixed Effect Quantile Regression (FE-QR) estimate. This method allows more complete analysis of the impact of different factors on the outcome variable in various parts of its distribution, taking into account the non-observable fixed effect (Akram et al., Citation2021).

Given that from a panel of n individuals, i = 1,…n. over time period. The conditional quantile is as follows:

(1)

(1)

Where represent the logarithm of FD for country i at a year t,

is px1 vector of the independent variable and

represents the unobserved country fixed effect, which controls for the time-variant of unobserved heterogeneity. From we observe that the skewness is −0.284, implying that the distribution of regressand variable departs from the Gaussian distribution. also shows that the series are leptokurtic meaning that the distribution has a fatter tail. This supports Jarque and Bera’s (Citation1980) argument that normality tests are significantly non-normally distributed hence the assumption of the normal distribution of error terms in ordinary least squares (OLS) is not a guarantee since it may produce misleading results. In this regard, quantile regression methods are more effective than OLS methods when the residual series are non-normal and possess heavy-tailed distribution (Rejeb, & Arfaoui, Citation2016). In addition, quantile regression has a more innate appeal, especially in panel regression, which stratifies the distributive effect of the variables independent of the dependent variables in different quantile distributions, which will aid policymakers (Gómez & Rodríguez, Citation2020). In view of the distinct advantage of quantile regression over least squares regression, we employ a fixed effect version of conditional quantile distribution (Koenker, Citation2005), which is more appropriate for measuring the varying effect on variables at the effects points of the conditional distribution and provides more information about the relationship between the nexus (Albulescu et al., Citation2019).

Table 1. Summary statistics for financial development and personal freedom in Africa.

In order to investigate the relationship between personal freedom and financial development we developed the quantile regression model from Equationequation (1)(1)

(1) as follows:

(2)

(2)

Where i and t depicts country and year respectively and denotes unobservable individual effect.

The conventional quantile regression introduced by Koenker and Bassett (Citation1978) is an extension of least square regression on the conditional mean for different quantile functions. The quantile regression estimate

is the solution to the following minimization problem

(3)

(3)

Where represents the parameter (0<

which denotes the quantile size. Quantile regression is more indulgent than OLS because it is relatively sensitive to outliers and distributions with heavy tails (Lv & Xu, Citation2017). Thus we employ the penalized panel quantile regression with a fixed effect to build up our model and address the penalized version of the estimator by the following equation.

(4)

(4)

where

represents the piecewise linear quantile loss function of Koenker and Bassett (Citation1978) and

controls the relative influence of the quantile on the estimation of the

which is defined as:

(5)

(5)

(6)

(6)

The penalty term shrink the individual effects to 0 and the degree of shrinkage is controlled by the turning parameter

when

with fixed effect estimator

and penalized estimator when

We select optimal

to minimize variance as follows:

(7)

(7)

Where is the trace of the co-variance matrix obtained through bootstrap.

The study follows three stages of empirical methodology starting with cross-sectional dependence (CSD). Panel data are vulnerable to CSD, which is a common phenomenon in empirical estimates. The CSD dilemma is related to unobserved elements and local and global economic shocks in one cross-sectional affect the cross-section (Pata et al., Citation2023). Analyzing first-generation panel data that does not take into account CSD and the effects of shocks propagating throughout the country, such as the economic crisis, can lead to biased results. Therefore, it is necessary to investigate the presence of CSD in order to avoid biased estimates. For this purpose, we used Pesaran CD test which is presented as follows;

(8)

(8)

Where N is the number of countries, T is the period and is the pairwise correlation of the residuals. EquationEquation (7)

(7)

(7) provides CD test statistic with a null hypothesis of ‘cross-sectional independence’. In addition, employ Pesaran, & Yamagata, (Citation2008) method to test the slope of heterogeneity. The Ha and Ho of the test are the ‘slope for all cross-sectional homogeneous’ and the ‘slope for all is not cross-sectional homogeneous’. The test statistics is described as follows:

(9)

(9)

(10)

(10)

(11)

(11)

The delta tilde and adjusted, modified delta statistics form the basis of Pesaran, & Yamagata, (Citation2008) test.

3.2. Data and variables

This sections gives and insight into the variables employed in the empirical analysis and their sources. It has been sub-sectioned into two as follows.

3.3. Variable description

Personal freedom is the main regressor. The index measures 41 personal freedom variables including freedom of relationships, expression and information, association, assembly and civil society, religion and movement. The indicator rates from 0 to 10, with 0 representing least freedom and it covers 98.1% of the world’s population in 165 jurisdictions. For the purpose of objectivity, Cato & Fraser institutes do not produce the data variables themselves, rather they use weights and averaging to convert to a scale of 0 to 10, the original data from reliable data sources such as the; World justice project index, Economic freedom of the world index, Varieties of democracy index, Civil liberty database and Bertelsmann Stiftung’s transformation index, to form a more robust, comprehensive and all-encompassing index that fills gap in existing literature. The dataset is preferred over other freedom indices because of its comprehensive nature, global comparability and interaction with security and safety and the rule of law. Without the rule of law, security and safety, there is no safeguarded environment that will provide the needed and fundamental essentials that will provide reasonable assurance that personal life is protected, for the vast array of freedom to be lived out, in a practical sense (Vásquez et al., Citation2022).

The regressand is financial development. This is measured by domestic credit to the private sector as a percentage of GDP. Seven and Coskun (Citation2016) argue that in less developed countries, which is typical in the African region, private credit to GDP is a better indicator of financial development, as traditional lending and borrowing remain key activity in the financial system and stock markets do not perform well. Additionally, as postulated by Mallela et al. (Citation2023), the private credit to GDP ratio denotes the credit availability, distribution and intermediation taking place within financial institutions as opposed to other proxies in literature such as liquid liabilities and several deposits that capture savings and non-yield-bearing investments.

Six variables that have been documented to have a potential impact on financial development—gross domestic product growth, foreign direct investment, general government expenditure, inflation, trade openness and economic freedom—are added to control the validity of the effect of personal freedom on financial development in the analysis.

3.4. Data sources

A panel of 40 African countries are examined from 2000 to 2020 using data from different sources. The personal freedom index is sourced from Cato and Fraser Institute (Citation2022). Domestic credit to the private sector is sourced from the World Development Indicators (WDI) of the World Bank. All control variables, except for economic freedom, which is sourced from the Cato and Fraser Institute (Citation2022), are sourced from World Development Indicators (WDI).

4. Results and discussions

4.1. Preliminary analysis

From , we establish the characteristics of the variables of interest. We observe that the variance for the variables is relatively large, with financial development, inflation and trade openness dominating with high variability among the variables. From the summary statistics, we observe that the series are leptokurtic distributions except for personal and economic freedom meaning that the distribution has a fatter tail. This supports Jarque and Bera’s (Citation1980) argument that normality tests are significantly non-normally distributed. We check the stationary properties for all the variables and detail the results of Levin, Lin, and Chut (Levin et al., Citation2002), Im, Pesaran, and Shin W-stat (Im et al., Citation2003), ADF-Fisher Chi-square (Choi, Citation2001), and PP - Fisher Chi-square (Pesaran, Citation2007) in . We find that INFL, GDPG series are I(0) while the rest of the series I(1).

Table 2. Panel unit root test.

The cross-sectional dependency test in the suggest that there is no evidence of cross-sectional dependence among the variables used in the studies. The results presented suggest that the assumption of cross-sectional independency is satisfied, which is imperative for the validity of the regression results. Due to the absence of cross-sectional dependence, the calculated coefficients are not distorted and standard error estimates are properly estimated, ensuring that regression analysis conclusions are reliable and valid.

Table 3. Test for cross-sectional dependence.

The slope of heterogeneity reported in indicates that the values of the delta and the modified delta are statistically significant. The results of the assessment confirmed the rejection of the null hypothesis (H0) of the homogeneous slope coefficient.

Table 4. Slope of heterogeneity test.

4.2. Empirical results

In this section, we show the empirical analysis of our investigation of the non-linear relationship between personal freedom and financial development. presents the results of the panel quantile regression. The results are presented in 19 quantiles with; Q0.050-Q0.350, Q0.400-Q0.650 and Q0.700-Q0.950 indicating low, medium and high levels of financial development respectively. From the aforementioned, it is observed that, in the lower and medium quantiles, personal freedom has no significant effect on financial development. It was again observed that, in the lower quantiles of Q0.050-Q0.350, five out of seven quantiles depicted an insignificant negative relationship while two quantiles (Q0.150 and Q0.200) depicted an insignificant positive relationship. However, in the higher quantiles of Q0.700 to Q0.900, the effect of personal freedom on financial development became significantly negative. This is depicted by five out of six higher quantiles, showing negative significance with four quantiles depicting significance at the 1% level, while a positive significance at the 10% level is observed at the 95th quantile. This results gives evidence of non-linearity in the nexus and further indicates how key personal freedom is, at higher levels of financial development in Africa.

Table 5. Panel Quantile Regression (PQR) estimation.

Regarding the relationship between GDP growth and financial development, a negative nexus is reported in all quantiles. However, except for quantiles (Q0.050, Q0.100, Q0.400 and Q0.950) all the other quantiles report a significant negative relationship between economic growth and financial development with the higher quantiles reporting more significance at the 1% level. Foreign direct investment (FDI) also reported a negative relationship with financial development at all quantiles, with the lower quantiles reporting an insignificant relationship. A significant negative relationship was recorded within the middle and upper quantiles (Q0.40-Q0.95) with 8 out of 12 quantiles showing significance. Again, in the higher quantiles of Q0.700-Q0.950, more significance at the 1% level is reported depicted by 4 out of 6 quantiles. General government expenditure on the other hand, reports a statistically positive significant relationship at the 1% level with financial development in all quantiles. However, Inflation shows a positive relationship with financial development in all the lower and upper quantiles with lower quantiles of 5-15th and upper quantiles of 75-90th showing a significant positive relationship while the middle quantiles showed an insignificant negative relationship. Trade openness also reports a positive relationship with financial development in all quantiles except for the 95th quantile. Eight out of the twelve quantiles in the middle and upper quantiles showed a significant positive relationship. Economic freedom also reported a positive relationship with financial development at all quantiles. Again, this positive relationship was statistically significant at the 1% significance level in all the quantiles.

4.3. Discussion of results

The empirical investigation on the personal freedom-financial development nexus, has extended the scope of literature on the determinants of financial development in Africa. This has provided primary knowledge on how personal liberties influence financial systems and financial sector engagement in the region—key for governments, policymakers and market participants to understand the freedoms needed for financial development.

Overall, the results imply that personal freedom plays a key role as a driver of financial development in Africa, particularly at higher levels of financial development. The results highlight the low levels of personal freedom dominant in Africa and unfavorable for financial progression. This probably suggests that low levels of personal freedom narrow human choices in the region, thereby inhibiting personal participation in financial systems as they develop; possibly explaining why Africa has been making strides in financial sector development, but it has not been accompanied by the needed growth (Mlachila, et al., Citation2016). The findings additionally confirm Freedom House (Citation2023) documentation that, Africa has few countries that are characterized free thus, only 7% of Africans live in countries considered free, 43% in partly free countries, and the remaining 50% reside in countries classified as not free. These empirical findings are consistent with the findings of Kwatia et al. (Citation2024) who found that, freedom matters for financial development in Africa. Additionally, the study findings are in line with Kabir & Alam (Citation2021) who found that, personal freedom hinders development in countries that have lower levels of freedom and spurs development in countries with higher levels of personal freedom.

Moving to the control variables, the findings of GDP growth–financial development nexus implies that, there is no clear indication that financial development is spurred by economic growth, possibly because of the dominance of underdeveloped economies within the region. The findings rather give evidence of a significant negative relationship between GDP growth and financial development in the region. This is divergent from the conventional findings of positive relationship in the nexus, as seen in Estrada et al. (Citation2010) and Guru & Yadav, (Citation2019). The current results are consistent with those of Wen et al. (Citation2022), Baltagi et al. (Citation2007) and Favara (Citation2003) who also found a negative link between GDP growth and financial development. On FDI, the negative relationship reported with financial development at all quantiles with significance at the middle and higher quantiles imply that, the high volatility in Africa’s financial sector may not be able to attract the needed investment the will boost financial sector development in the region. This is in line with the findings of Dutta and Roy (Citation2011) who also found FDI inflows to have a negative impact at a higher threshold of financial development but divergent to the study findings of Majeed et al. (Citation2021) who found that FDI has positive relationship with financial development in BRI countries in Asia, Africa, Europe and Lartin America.

General government expenditure reports a 1% positive significance at all quantiles, implying that, African governments tend to focus on spending more on higher productive expenditures such as technological innovations that supports financial sector development, in order to maintain a favorable development rate to make up for restrained private investment in the region. This is in support of Chen et al. (Citation2019) and Kwatia et al. (Citation2024) but divergently Kapaya (Citation2023) WHO highlights a negative association between government spending and financial development. Additionally, the results imply that, higher levels of inflation in Africa might impact the nominal measures of financial depth in the region, as higher prices may lead to increased transactions and higher values in the financial market, possibly indicating financial sector development in the lower and higher quantiles, which is consistent with Cecchetti and Kharroubi (Citation2015). This is contrary to the general expectation that the prevalence of high inflation rates in the region will have a negative relationship with financial development, as observed in the middle quantiles of Q0.400-Q0.550, which adversely impacts interest rates and alters the redistributive role of financial intermediaries, consistent with studies such as Ibrahim et al. (Citation2022), Hami (Citation2017) and Khan (Citation2015). The results on trade openness imply that, trade liberalization is key for financial development at medium and high levels of financial development. This is consistent with the studies of Rajan and Zingales (Citation2003), Thuy & Trong (Citation2021) and Kar et al. (Citation2014) who found a positive relationship between trade openness and financial development but divergent from Tongurai and Vithessonthi (Citation2023), Kim et al. (Citation2010) and Tongurai & and Ehigiamusoe et al., (Citation2021), who found a negative effect of trade on finance. On economic freedom, the study results possibly imply that economic liberty favours a more developed and efficient financial system at all levels of financial development in Africa. This is consistent with the studies of Kabir and Alam (Citation2021), Oussama et al. (Citation2017) and Khan et al. (Citation2020) who also confirmed that, economic freedom supports financial sector growth and development.

5. Conclusion and policy implication

5.1. Conclusion

The determinants of financial development within and among countries have been a longstanding debate in the economics and finance literature because of the key impact of financial development on economic growth. Using domestic credit provided by financial intermediaries to the private sector, we analyze the potential relevance of personal freedom as an informal institution in explaining financial development. The starting point was the observation that the literature on the drivers of financial development might have taken a myopic view of the impact of institutions and that informal institutions are perhaps unduly neglected. Prompted by the resurgence of financial development in Africa amidst poor, inadequate and unstructured formal institutional structures, this study examines whether personal freedom drives financial development in the region. This study uses a panel quantile regression model to investigate the relationship between financial development and personal freedom in Africa while accounting for the effects of GDP growth, foreign direct investment, general government expenditure, inflation, trade openness and economic freedom from 2000 to 2020.

The findings can be summarized as follows. First, a statistically negative and significant relationship at the 1% level is reported between personal freedom and financial development at the higher quantiles (Q0.70-Q0.95). This implies that personal freedom is key for financial development in Africa, and possibly suggests that, improved personal liberties in the region will enhance personal choices and participation in financial systems, leading to financial development. Additionally, the findings reveal that GDP growth and FDI have a negative association with financial development, possibly implying that, the prevalence of underdeveloped economies characterized by high volatility in the region’s financial sector, hinders FDI inflows and economic growth by stifling Africa’s financial development. On the contrary, general government expenditure, inflation, trade openness and economic freedom have a positive effect on financial development in Africa, implying that the more liberated African economies are, coupled with trade liberalization, right government spending and controlled inflation, there will be higher financial progression in the region.

5.2. Policy implications

This study’s findings have some policy implications. They suggest that African governments should work to enhance personal freedom indicators such as freedom of movement, rule of law, security and safety, expression and information, association, assembly and civil society, relationships and religion in their countries. This will help move their countries towards attaining a free-nation status to foster financial sector development that is needed to support growth in the region. Policymakers should map out strategies that support personal freedom; strengthen assistance to regions, countries and human rights advocates in difficult times; and rally unwavering efforts to protect and defend them. Additionally, it is recommended that policies that spur financial sector development in Africa be pursued. Government expenditure should focus on productive expenditure that supports welfare and growth-enhancing expenditure. Efforts should be made to lower inflation rates and promote the adoption of proper monetary policies that will reduce the adverse effects of inflation on financial development. Finally, the findings suggest that African governments should enact policies that favor economic and trade liberalization to attract the FDI inflows needed to enhance the region’s economic growth rate, which will spur financial development.

5.3. Limitation of the study & future research direction

This study explored the non-linearity between personal freedom and financial development in Africa. The findings showed that the relationship varied at different quantiles, giving evidence of a possible threshold effect which was not explored in this study. It will be of interest to investigate the threshold effects between personal freedom and financial development. This presents an interesting gap for further research.

Author contributions

Benard Ohene Kwatia: Conceptualization, Validation, Formal Analysis, Data curation, Writing-original draft, Writing-review & editing. Godfred Amewu: Validation, Formal Analysis, Data curation, Writing-review & editing, supervisionMohammed Armah: Methodology, Validation, Formal Analysis, Data curation, Writing-review & editing.

Disclosure statement

The authors declared that there were no conflicts of interest.

Data availability statement

The data used in the study will be made available on request.

Additional information

Funding

Notes on contributors

Benard Ohene Kwatia

Benard Ohene Kwatia is a doctoral research candidate with interests in religiosity, freedom, equality, financial development, institutions and financial econometrics. He holds MBA in Finance and a Fellow of the Association of Chartered Certified Accountants – UK, a member of the Institute of Chartered Accountant and the Institute of Internal Auditors – Ghana.

Godfred Amewu

Godfred Amewu is a Senior Lecturer in finance at the University of Ghana Business School. He is currently leading the efforts in the development of impact investing as an asset class in Africa. His research interests are in corporate finance, corporate governance, risk management, capital market, and corporate social investments.

Mohammed Armah

Mohammed Armah is a doctoral research student at the Ghana Institute of Management and Public Administration (GIMPA). He holds MPhil and MBA in Finance from Kwame Nkrumah University of Science and Technology and Coventry University College. His research interests are in the areas of financial market integration, monetary policy, and financial economies.

References

- Acemoglu, D. J., & Robinson, J. A. (2005). Institutions as a fundamental cause of long-run growth. In Handbook of economic growth (Vol. 1, pp. 385–472). Elsevier.

- Adekunle, A. I., Yinusa, G. O., Williams, O. T., & Folami, A. R. (2021). On the determinant of financial development in Africa: Geography, Institutions and Macroeconomic policy relevance. African Governance and Development Institute Working Papers, 21(054), African Governance and Development Institute.

- Adu, G., Marbuah, G., & Mensah, J. T. (2013). Financial development and economic growth in Ghana: does the measure of financial development matter? Review of Development Finance, 3(4), 192–203. https://doi.org/10.1016/j.rdf.2013.11.001

- Aduba, J. J., Asgari, B., & Izawa, H. (2023). Does FinTech penetration drive financial development? Evidence from panel analysis of emerging and developing economies. Borsa Istanbul Review, 23(5), 1078–1097. https://doi.org/10.1016/j.bir.2023.06.001

- Ahiakpor, F., Nordjo, R., & Alnaa, E. (2023). Financial development and growth: evidence from Bayesian modelling. Cogent Economics & Finance, 11(2) https://doi.org/10.1080/23322039.2023.2261798

- Akram, R., Chen, F., Khalid, F., Huang, G., & Irfan, M. (2021). Heterogeneous effects of energy efficiency and renewable energy on economic growth of BRICS countries: A fixed effect panel quantile regression analysis. Energy, 215, 119019. https://doi.org/10.1016/j.energy.2020.119019

- Albulescu, C. T., Tiwari, A. K., Yoon, S. M., & Kang, S. H. (2019). FDI, income, and environmental pollution in Latin America: Replication and extension using panel quantiles regression analysis. Energy Economics, 84(xxxx), 104504. https://doi.org/10.1016/j.eneco.2019.104504

- Aluko, O. A., & Ajayi, M. A. (2018). Determinants of banking sector development: Evidence from Sub-Saharan African Countries. Borsa Istanbul Review, 18(2), 122–139. https://doi.org/10.1016/j.bir.2017.11.002

- Armah, M., & Amewu, G. (2024). Asymmetries Quantile dependence and asymmetric connectedness between global financial market stress and REIT returns: Evidence from the COVID-19 pandemic. The Journal of Economic Asymmetries, 29(January), e00352. https://doi.org/10.1016/j.jeca.2024.e00352

- Baltagi, B., Demitriades, P., & Law, S. H. (2007). Financial development, openness and institutions: evidence from panel data [Paper Presentation]. Conference on New Perspectives on Financial Globalization by IMF and Cornell University. https://www.imf.org/external/np/seminars/eng/2007/finglo/btpdsl.pdf

- Barro, R. J., & Lee, J. W. (2013). A new data set of educational attainment in the world, 1950-2010. Journal of Development Economics, 104, 184–198. https://doi.org/10.1016/j.jdeveco.2012.10.001

- Beck, T., & Levine, R. (2002). Industry growth and capital allocation: Does having a market- or bank-based system matter? Journal of Financial Economics, 64(2), 147–180. https://doi.org/10.1016/S0304-405X(02)00074-0

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2003). Law and finance: why legal origin matter? Journal of Comparative Economics, 31(4), 653–675. https://doi.org/10.1016/j.jce.2003.08.001

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2001). Legal theories of financial development. Oxford Review of Economic Policy, 17(4), 483–501. https://doi.org/10.1093/oxrep/17.4.483

- Bekana, M. D. (2013). Governance quality and financial development in Africa. World Development Sustainability, 2, 100044.). https://doi.org/10.1016/j.wds.2023.100044

- Bennett, L. D., Faria, J. H., Gwartney, D. J., & Morales, R. D. (2017). Economic institutions and comparative economic development: A post-colonial perspective. World Development, 96, 503–519. https://doi.org/10.1016/j.worlddev.2017.03.032

- Besley, T., & Persson, T. (2011). Pillars of Prosperity: The Political Economics of Development Clusters. Princeton University Press.

- Bist, J. P. (2018). Financial development and economic growth: evidence from a panel of 16 African and non-African low-income countries. Cogent Economics & Finance, 6(1), 1449780. https://doi.org/10.1080/23322039.1449780

- Cecchetti, S. G., & Kharroubi, E. (2015). Why Does Financial Sector Growth Crowd Out Real Economic Growth? BIS Working Papers, 490. Bank for International Settlement.

- Chen, Z., Lv, B., & Liu, Y. (2019). Financial development and the composition of government expenditures: theory and cross-country evidence. International Review of Economics & Finance, 64, 600–611. https://doi.org/10.1016/j.ref.2019.09.006

- Choi, I. (2001). Unit root tests for panel data. Journal of International Money and Finance, 20(2), 249–272. https://doi.org/10.1016/S0261-5606(00)00048-6

- Claesssens, S., & Laeven, L. (2003). Financial development, property rights and growth. Journal of Finance, 58(6), 2401–2436.

- Demirgüç-Kunt, A., & Maksimovic, V. (1998). Law, finance and firm growth. Journal of Finance, 53, 2107–2137.

- Dosso, D. (2023). Institutional quality and financial development in resource-rich countries: A nonlinear panel data approach. International Economics, 174, 113–137. https://doi.org/10.1016/j.inteco.2023.03.005

- Dutta, N., & Roy, S. (2011). Foreign direct investment, financial development and political risks. Journal of Developing Areas, 44(2), 303–327.

- Ehigiamusoe, K. U., Guptan, V., & Narayanan, S. (2021). Rethinking the impact of GDP on financial development: Evidence from heterogeneous panels. African Development Review, 33(1), 1–13. https://doi.org/10.1111/1467-8268.12469

- Estrada, G., Park, D., & Ramayandi, A. (2010). Financial Development and Economic Growth in Developing Asia. ADB Economics Working Paper Series, 233. Asian Developing Bank.

- Favara, G. (2003). An Empirical Reassessment of the Relationship between Finance and Growth. IMF Working Paper WP/03/123. International Monetary Fund.

- Feng, D., Gao, M., & Zhou, L. (2023). Religion and household borrowing: Evidence from China. International Review of Economics & Finance, 88, 60–72. https://doi.org/10.1016/j.iref.2023.06.006

- Cato and Fraser Institute. (2022). The human freedom index 2022: A global measurement of personal, civil, and economic freedom. https://www.fraserinstitute.org/studies/economic-freedom.

- Doering, D. (2012). Why do we measure freedom? In Towards a worldwide index of human freedom, 3–6. https://www.fraserinstitute.org/sites/default/filesch1-why-do-we-measure-freedom.pdf.

- Freedom House (. (2023). New report: Freedom in Africa improved slightly in 2002 but challenges persist. https://freedomhouse.org/article/new-report-freedom-africa-improved-slightly-2022-challenges-persist

- Fung, C. (2022). Legal pluralism and the rule of law in Sub-Saharan Africa. Rule of Law Journal, 3, 18–24.

- Garretsen, H., Lensink, R., & Sterken, E. (2004). Growth, financial development, societal norms and legal institutions. International Financial Markets. Institutions and Money, 14(2), 165–183. https://doi.org/10.1016/j.intfin.2003.06.002

- Gholipour, F. H., Tajaddini, R., & Al-Mulali, U. (2014). Does personal freedom influence outbound tourism? Tourism Management, 41, 19–25. https://doi.org/10.1016/j.tourman.2013.08.010

- Goldsmith, R. W. (1969). Financial structure and development. Yale University Press.

- Gómez, M., & Rodríguez, J. C. (2020). The ecological footprint and Kuznets environmental curve in the USMCA countries: A method of moments Quantile regression analysis. Energies, 13(24), 6650. https://doi.org/10.3390/en13246650

- Gurley, J. G., & Shaw, E. S. (1960). Money in a theory of finance. Brookings.

- Guru, B. K., & Yadav, I. S. (2019). Financial development and economic growth: panel evidence from BRICS. Journal of Economics, Finance and Administrative Science, 24(47), 113–126. https://doi.org/10.1108/JEFAS-12-2017-0125

- Hami, M. (2017). The effect of inflation on financial development indicators in Iran (2000-2015). Studies in Business and Economics, 12(2), 53–62. https://doi.org/10.1515/sbe-2017-0021

- Han, J., Raghutla, C., Chittedi, R. K., Tan, Z., & Koondhar, A. M. (2022). How natural resources affect financial development? Fresh evidence from top 10 natural resource abundant countries. Resources Policy, 76, 102647. https://doi.org/10.1016/j.resourpol.220102647

- Heckelman, J. C. (2000). Economic freedom and economic growth: a short-run causal investigation. Journal of Applied Economics, 3(1), 71–91. https://doi.org/10.1080/15140326.2000.12040546

- Hoover, G. A., & Smimou, K. (2023). Socially conscious investment funds and home country institutions. Economic Analysis and Policy, 79, 395–417. https://doi.org/10.1016/j.eap.2023.06.008

- Huang, Y. (2010). Determinants of financial development. Palgrave Macmillan, UK.

- Hung, F.-S. (2003). Inflation, financial development and economic growth. International Review of Economics & Finance, 12(1), 45–67. https://doi.org/10.1016/S1059-0560(02)00109-0

- Ibrahim, M., Aluko, A. O., & Vo, V. X. (2022). The role of inflation in financial development – economic growth link in sub–Saharan Africa. Cogent Economics & Finance, 10(1), 2093430. https://doi.org/10.1080/23322039.2022.2093430

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Isiksal, Z. A. (2023). The role of natural resources in financial expansion: evidence from Central Asia. Financial Innovation, 9(1) https://doi.org/10.1186/s40854-023-00482-6

- Islam, S. M., & Alhamad, A. I. (2022). Impact of financial development and institutional quality on remittance-growth nexus: evidence from the topmost remittance-earning economies. Heliyon, 8(12), e11860. https://doi.org/10.1016/j.heliyon.2022.e11860

- Islam, M. A., Khan, M. A., Popp, J., Sroka, W., & Oláh, J. (2020). Financial development and foreign direct investment – the moderation role of quality institutions. Sustainability, 12(9), 3556. https://doi.org/10.3390/su12093556

- Iwegbu, O., Justine, K., & Cardoso, L. C. B. (2022). Regional financial integration, financial development and industrial sector growth in ECOWAS: does institutions matter? Cogent Economics & Finance, 10(1) https://doi.org/10.1080/23322039.2022.2050495

- Jarque, C. M., & Bera, A. K. (1980). Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters, 6(3), 255–259. https://doi.org/10.1016/0165-1765(80)90024-5

- Jemiluyi, O. O., & Jeke, L. (2023). How catalytic is digital technology in the nexus between migrants’ remittance and financial development in Sub-Saharan African Countries? Economies, 11(3), 74. https://doi.org/10.3390/economies11030074

- Kabir, M. A., & Alam, N. (2021). The efficacy of democracy and freedom in fostering economic growth. Emerging Economy Studies, 7(1), 76–93. https://doi.org/10.1177/23949015211057942

- Kato, K., Galvao, A. F., Jr,., & Montes-Rojas, G. V. (2012). Asymptotics for panel quantile regression models with individual effects. Journal of Econometrics, 170(1), 76–91. https://doi.org/10.1016/j.jeconom.2012.02.007

- Kapaya, S. M. (2023). Government expenditure impacts on financial development: Do population age structure moderations matter? Review of Economics and Political Science, 8(5), 330–352. https://doi.org/10.1108/REPS-01-2023-0008

- Kar, M., Nazlioglu, S., & Agir, H. (2014). Trade openness, financial development and economic growth in Turkey: Linear and nonlinear causality analysis. Journal of BRSA Banking and Financial Markets, Banking Regulation and Supervision Agency, 8(1), 63–86.

- Khan, H. (2015). The impact of inflation on financial development. International Journal of Innovation and Economic Development, 1(4), 42–48. https://doi.org/10.18775/ijied.1849-7551-7020.2015.14.2004

- Khan, M. A., Gu, L., Khan, M. A., & Oláh, J. (2020). Natural resources and financial development: The role of institutional quality. Journal of Multinational Financial Management, 56(C), 100641. https://doi.org/10.1016/j.mulfin.2020.100641

- Khan, M. A., Haddad, H., Odeh, M., Haider, A., & Khan, M. A. (2022). Institutions, culture or interaction: what determines the financial market development in emerging market? Sustainability, 14(23), 15883. https://doi.org/10.3390/su142315883

- Khan, M. A., Islam, M. A., & Akbar, U. (2020). Do economic freedom matters for finance in developing economies: a panel threshold analysis. Applied Economics Letters, 28(10), 840–843. https://doi.org/10.1080/13504851.2020.1782335

- Khan, M. A., Khan, M. A., Khan, M. A., Hussain, S., & Fenyves, V. (2024). Justice and finance: Does judicial efficiency contribute to financial system efficiency? Borsa Istanbul Review, 24(2), 248–255. https://doi.org/10.1016/j.bir.2023.12.013

- Khan, M. A., Kong, D. M., & Xiang, J. (2019). Impact of Institutional Quality on Financial Development: Cross-Country Evidence based on Emerging and Growth-Leading Economies. Emerging Markets Finance and Trade, 56(15), 1–17.

- Khan, M. A., Máté, D., Abdulahi, M. E., Sadaf, R., Khan, M. A., Popp, J., & Oláh, J. (2024). Do institutional quality, innovation and technologies promote financial market development? European J. of International Management, 22(3), 484–507. https://doi.org/10.1504/EJIM.2024.136453

- Khan, M. S., & Senhadji, A. S. (2000). Financial development and economic growth: An overview. International Monetary Fund (IMF) Working Paper WP/00/209.

- Kim, D.-H., Lin, S.-C., & Suen, Y.-B. (2010). Are financial development and trade openness complements or substitutes? Southern Economic Journal, 76(3), 827–845. https://doi.org/10.4284/sej.2010.76.3.827

- Koenker, R. (2005). Quantile regression. Cambridge University Press. https://doi.org/10.1017/cbo9780511754098.011

- Koenker, R., & Bassett, G. Jr, (1978). Regression quantiles. Econometrica, 46(1), 33–50. https://doi.org/10.2307/1913643

- Kutan, A. M., Samargandi, N., & Sohag, K. (2017). Does institutional quality matter for financial development and growth? Further evidence from MENA countries. Australian Economic Papers, 56(3), 228–248. https://doi.org/10.1111/1467-8454.12097

- Kwatia, B. O., Amewu, G., & Armah, M. (2024). Religiosity and financial development in Africa: Evidence from panel quantile regression. Cogent Business & Management, 11(1) https://doi.org/10.1080/23311975.2024.2315313

- La, Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2013). Law and finance after a decade of research. In Handbook of the economics of finance (Vol. 2, pp. 425–491). Elsevier.

- La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W. (1997). Legal determinants of external finance. The Journal of Finance, 52(3), 1131–1150. https://doi.org/10.2307/2329518

- La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W. (1998). Law and finance. Journal of Political Economy, 106(6), 1113–1155. https://doi.org/10.1086/250042

- Lavrinenko, O., Čižo, E., Ignatjeva, S., Danileviča, A., & Krukowski, K. (2023). Financial technology (FinTech) as a financial development factor in the EU countries. Economies, 11(2), 45. https://doi.org/10.3390/economies11020045

- Levine, R. (2000). Bank-Based or Market-Based Financial Systems: Which is Better?. Mimeo, World Bank.

- Levine, R., & Zervos, S. (1998). Stock markets, banks and economic growth. American Economic Review, 88, 537–558.

- Levin, A., Lin, C.-F., & Chu, C.-S J. (2002). Unit root tests in panel data: asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7

- Lv, Z., & Xu, T. (2017). A panel data quantile regression analysis of the impact of corruption on tourism. Current Issues in Tourism, 20(6), 603–616. https://doi.org/10.1080/13683500.2016.1209164

- Lyu, X., Ma, J., & Zhang, X. (2023). Social trust and corporate innovation: An informal institution perspective. North American Journal of Economics and Finance, 64 https://doi.org/10.1016/j.najef.2022.101829

- Majeed, A., Jiang, P., Ahmad, M., Khan, M. A., & Olah, J. (2021). The impact of foreign direct investment on financial development: New evidence from panel cointegration and causality analysis. Journal of Competitiveness, 13(1), 95–112. https://doi.org/10.7441/joc.2021.01.06

- Mallela, K., Singh, S. H., & Srivastava, A. (2023). Remittances, financial development, and income inequality: A panel quantile regression approach. International Economics, 175, 171–186. https://doi.org/10.1016/j.inteco.2023.07.003

- Mlachila, M., Cui, L., Jidoud, A., Newiak, M., Radzewicz-Bak, B., Takebe, M., Ye, Y., & Zhang, J. (2016). Financial development in sub-Saharan African: promoting inclusive and sustainable growth. International Monetary Fund.

- North, D. C. (1990). Institutions, Institutional Change and Economic Performance. Cambridge University Press.

- Oben, R. J. (2022). The impact of natural resources on financial development: The global perspective. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.4249880

- Ofori, I. K., Quaidoo, C., & Ofori, P. E. (2021). What Drives Financial Sector Development in Africa? Insights from Machine Learning. African Governance and Development Institute, Working Paper, WP/21/074.

- Oroud, Y., Ahmad Almahadin, H., Alkhazaleh, M., & Shneikat, B. (2023). Evidence from an emerging market economy on the dynamic connection between financial development and economic growth. Research in Globalization, 6, 100124. https://doi.org/10.1016/j.resglo.2023.100124

- Oussama, Z., Ahmed, H., & Fatma, H. (2017). Financial development, economic freedom and economic growth: New evidence from Tunisia. Economic Review: Journal of Economics and Busness, 15(2), 7–18.

- Pata, U. K., Alola, A. A., Erdogan, S., & Kartal, M. T. (2023). The influence of income, economic policy uncertainty, geopolitical risk, and urbanization on renewable energy investments in G7 countries. Energy Economics, 128, 107172. https://doi.org/10.1016/j.eneco.2023.107172

- Pesaran, M. H., & Yamagata, T. (2008). Testing slope homogeneity in large panels. Journal of Econometrics, 142(1), 50–93. https://doi.org/10.1016/j.jeconom.2007.05.010

- Pesaran, M. H. (2007). Simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 21(August), 1–21. https://doi.org/10.1002/jae

- Puatwoe, J. T., & Piabuo, S. M. (2017). Financial sector development and economic growth: evidence from Cameron. Financial Innovation, 3(1) https://doi.org/10.1186/s40854-017-0073-x

- Raghutla, C., Padmagirisan, P., Sakthivel, P., Chittedi, K. R., & Mishra, S. (2022). The effect of renewable energy consumption on ecological footprint in N-11 countries: Evidence from Panel Quantile Regression Approach. Renewable Energy. 197, 125–137. https://doi.org/10.1016/j.renene.2022.07.100

- Rajan, R. G., & Zingales, L. (2003). The great reversals: the politics of financial development in the twentieth centry. Journal of Financial Economics, 69(1), 5–50. https://doi.org/10.1016/S0304-405X(03)00125-9

- Rejeb, A. B., & Arfaoui, M. (2016). Financial market interdependencies: A quantile regression analysis of volatility spillover. Research in International Business and Finance, 36, 140–157. https://doi.org/10.1016/j.ribaf.2015.09.022

- Sarhangi, K., Mohaghegh Niya, M. J., & Amiri, M. (2021). The effect of effective governance and quality of regulations on financial development in the current economic conditions of Iran. Advances in Mathematical Finance and Applications, 6(4), 831–850.

- Scholtens, B., & Van Wensveen, D. (2003). The Theory of Financial Intermediation: An Essay on What It Does (Not) Explain. The European Money and Finance Forum.

- Schumpeter, J. A. (1911). The Theory of Economic Development. Harvard University Press.

- Seven, U., & Coskun, Y. (2016). Does financial development reduce income inequality and poverty? Evidence from emerging countries. Emerging Markets Review, 26, 34–63. https://doi.org/10.1016/j.ememar.2016.02.002

- Thuy, D. P. T., & Trong, H. N. (2021). Impact of openness on financial development in developing countries: using a Bayesian model averaging approach. Cogent Economics & Finance, 9(1) https://doi.org/10.1080/23322039.2021.1937848

- Tongurai, J., & Vithessonthi, C. (2023). Financial openness and financial market development. Journal of Multinational Financial Management, 67, 100782. https://doi.org/10.1016/j.mulfin.2023.100782

- Travkina, E. V., Fiapshev, A. B., Belova, M. T., Dubova, & S., E. (2023). Culture and institutional changes and their impact on economic and financial development trajectories. Economies, 11(1), 14. https://doi.org/10.3390/economies11010014

- Úbeda, F., Forcadell, J. F., & Suárez, N. (2022). Do formal and informal institutions shape the influence of sustainable banking on financial development? Finance Research Letters, 46, 102391. https://doi.org/10.1016/j.frl.2021.102391

- Vásquez, I., McMahon, F., Murphy, R., & Schneider, S. G. (2022). The Human Freedom Index 2022: A Global Measurement of Personal, Civil, and Economic Freedom. Cato Institute and Fraser Institute.

- Vatamanu, F. A., & Zugravu, G. B. (2023). Financial development, institutional quality and renewable energy consumption. A panel data approach. Economic Analysis and Policy, 78, 765–775. https://doi.org/10.1016/j.eap.2023.04.015

- Wen, J., Mahmood, H., Khalid, S., & Zakaria, M. (2022). The impact of financial development on economic indicators: a dynamic panel data analysis. Economic Research-Ekonomska Istraživanja, 35(1), 2930–2942. https://doi.org/10.1080/1331677X.2021.1985570

- Williamson, R. C. (2012). Dignity and development. The Journal of Socio-Economics, 41(6), 763–771. https://doi.org/10.1016/j.socec.2011.12.013

- Zhang, C., & Liang, Q. (2023). Natural resources and sustainable financial development: Evidence from South Asian Economies. Resources Policy, 80, 103282. https://doi.org/10.1016/j.resourcepol.2022.103282