?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The inflow of FDI brings many economic benefits including more employment opportunities, sharing of modern knowledge, and the transfer of needed capital to aid the depressing domestic investment. In view of this, the current study aims to find out the empirical impact of the governance quality of the host country on FDI inflow. The empirical analysis was arranged by sampling the 20-year (2000-2019) financial statistics of 8 South Asian economies. For regression assessment, we employ FMOLS and DOLS models and estimate the coefficients in the long run. The empirical analysis discloses the positive significant role of the aggregate governance index on FDI inflow, implying that better governance can uplift the inflow of FDI. In addition, the empirical results disclose the negative impact of the inflation rate, while the significant positive impact of trade volume, population growth, labor force, and financial development on FDI inflow. The empirical analysis yields vital policies both for domestic policy officials and foreign investors. Primarily, it is recommended to focus on improving the governance situation to attract more FDI. This study enriches the literature by showing the interplay between governance and FDI inflow and has equal policy implications for other developing economies of the world.

IMPACT STATEMENT

This study examines how governance quality influences foreign direct investment (FDI) in South Asia. The findings reveal that strong governance frameworks characterized by political stability, regulatory quality, and control of corruption, etc., significantly boost FDI inflows. By improving governance standards, South Asian countries can create a more attractive environment for foreign investors, promoting economic growth and regional development. This research underscores the critical role of governance in shaping investment inflow and provides actionable insights for policymakers aiming to enhance FDI attraction.

Reviewing Editor:

1. Introduction

Foreign direct investment plays a vital role in the economic growth of the host country. It creates more employment opportunities by establishing more industrial units in the host country and is a valuable source of technology transfer from developed to developing economies (Rao et al., Citation2020). The voluminous inflow of FDI somehow reflects the confidence and interest of foreign investors in local markets. Prevailing to optimistic return opportunities, a market with favorable economic indicators is an eye-catching for foreign investors. Foreign investors show their strong interest in those markets having some positive indicators, e.g. big market size, high population, economic stability, etc., In addition to these, the governance situation of a country can be another factor that can play its dynamic role in boosting the inflow of FDI. Better governance can attract more investors as a good governance situation demonstrates political stability, low information asymmetry issues, control of corruption, low default risk, etc., (Raza et al., Citation2021b). All these factors can positively impinge upon the investment behavior of foreign investors and thus can enhance the investment volume. Meanwhile, a better governance situation in a country reduces the law violation and enhances market stability which further has a positive spillover regarding more foreign investment. Irrespective of theoretical justification, the empirical literature is still scant on how governance can play its role in boosting foreign investment. Thus, the current study is an attempt to explore the empirical relationship between governance and foreign investment by controlling the other economic factors, e.g. market size, population growth, inflation rate, financial development, and trade volume.

Foreign direct investment with its numerous positive outcomes for developing economies not only supplements the required capital for exploring domestic investment but is also a source of technology and knowledge transfers from developed to developing economies. Therefore, the developing economies always struggle to enhance the pace of foreign investment either by policy instruments or by easing the restrictions on investment flow (Wu et al., Citation2020). Moreover, the recent development in globalization has enforced the countries to focus more on foreign investment instead of foreign aid. Normally, the developing economies are rich in unexplored natural resources and thus are in search of foreign entrepreneurs for enhancing the utilization of such resources. Parallelly, foreign investors are sought in markets having suitable economic situations for disseminating the investment. In this essence, more flow of foreign investment takes place to balance the needs of both developing and foreign investors (Qureshi et al., Citation2021; Rafei et al., Citation2022). According to WDI statistics, the FDI in India has grown to 133% in 2019 as compared to 2000. Similarly, Pakistan has experienced an increment of almost 85% in an inflow of foreign investment in 2019 as compared to 2000. These statistics reflect the orientation of these economies to boost economic diversification by inviting more foreign investment. Furthermore, the inflow of foreign investment helps in reducing the growing inflation as it enhances the production volume of industrial goods and thus balances the demand and supply difference.

South Asia region with its distinctive features, e.g. high population, low economic growth, high labor force, etc. is a prominent destination of foreign investment specifically investors from developed economies that are thrilled to invest in venture options. According to statistics offered by The World Bank, the highest average foreign investment inflow from 2000 to 2019 is 7.661% of total GDP in the Maldives, followed by India (1.630% of GDP), Bhutan (1.281% of GDP), Sri Lanka (1.272% of GDP), Afghanistan (1.189% of GDP), Pakistan (1.177% of GDP), Bangladesh (0.877% of GDP), and Nepal (0.236% of GDP). The broad aim of a country is to heighten the economic progress by exploring the attached factors, e.g. more exports, promoting the knowledge economy, and resources efficiency, etc., As likely to these factors, the FDI is another factor that can uplift the depressing economy specifically underdeveloped or developing economies. The inflow of FDI ensures the transfer of knowledge, modification of production systems, and exports diversifications. All these factors have a positive influence on economic growth (Musibau et al., Citation2019). However, the inflow of FDI is attached to many factors, i.e. economic stability, market size, and overall governance efficiency. Before indulging in any investment ventures, the foreign investors may make the costs and benefits analysis by linking the economic situation of a country. A country with a good governance situation can be approved as the first preference of foreign investors due to high resilience towards uncertainties and economic shocks, and low default risks (Fon & Alon, Citation2022). Owing to these positive outcomes of governance, this study mainly focuses on unveiling the role of governance in promoting the foreign investment.

The South Asian region is confronted with the imperative need for economic development and growth, making the attraction of FDI a cornerstone for achieving these objectives. Beyond the infusion of capital, FDI brings invaluable technological expertise and managerial know-how, fostering innovation and enhancing overall productivity. The potential impact on employment is particularly noteworthy, with increased FDI contributing to job creation and thereby addressing pressing issues of unemployment, ultimately leading to poverty reduction and bolstering socioeconomic development. The eight South Asian countries under scrutiny in this study stand out as unique destinations for FDI due to a confluence of distinctive factors. Demographic trends play a significant role, with a burgeoning population in the region presenting a vast and diverse consumer market. This demographic dividend is often viewed as an attractive feature for investors seeking to tap into the potential of a growing middle class.

Moreover, the natural resource endowments of these countries contribute to their appeal, as sectors such as agriculture, mining, and energy extraction offer promising investment opportunities. In addition, market size also distinguishes these countries as unique FDI destinations. With large populations, these nations offer a substantial consumer base, attracting investors seeking scale and market penetration. The unique economic structures and growth trajectories of each country contribute to the overall diversity and attractiveness of the region for foreign investors. By understanding these distinctive features, policymakers and investors can tailor their strategies to leverage the specific opportunities and challenges presented by each South Asian country, fostering a more nuanced approach to attracting and maximizing FDI.

This study considers the governance situation as a potential determinant of foreign direct investment and explores the empirical relationship between governance and FDI inflow. We employ the panel data for the years 2000 to 2019 of 8 south Asian economies and run the regression by employing the FMOLS (fully modified ordinary least square) and check the robustness through DOLS (dynamic ordinary least square) models. The empirical analysis speaks about the positive effect of the aggregate governance index on foreign investment, implying that a country with a good governance situation can attract more foreign investors. Moreover, a better governance system is an indication of market stability, control of corruption, rules enforcement, and regulatory quality. All these factors can positively derive foreign investment. In addition to governance, the empirical analysis provides robust evidence of favorable effects of other control variables, i.e. population growth rate, trade volume, labor force, and financial development while an adverse effect of inflation rate on FDI inflow.

This research significantly advances our understanding of the dynamics between governance systems and FDI in the context of the South Asian region. The exploration of the empirical role of governance in stimulating FDI inflows is particularly insightful, shedding light on potential strategies for policymakers and stakeholders to foster economic development through improved governance. The emphasis on better governance as a key factor influencing FDI trends in South Asian countries aligns with a growing recognition of the multifaceted nature of foreign investment decisions. The study’s empirical approach, utilizing FMOLS and DOLS models, adds methodological rigor to the investigation, addressing the complexities associated with the co-movement of variables over time. The utilization of cointegration analysis enhances the robustness of the findings, providing a solid foundation for the conclusions drawn. The examination of cross-section dependence, while not yielding statistically significant evidence in this particular study, adds transparency to the research process. Acknowledging the absence of such dependence is crucial in refining the understanding of the relationships between governance and FDI in South Asia. The conclusion that FMOLS and DOLS models are the most suitable for examining these relationships underscores the importance of choosing appropriate econometric methods to draw reliable inferences.

Moreover, the identification of prominent policies advocating for the improvement of governance to attract more foreign investment is a key contribution of this study. By pinpointing governance quality as a pivotal factor, the research offers actionable insights for policymakers and stakeholders in the South Asian region. The emphasis on enhancing governance aligns with global trends advocating for transparent, accountable, and efficient governance structures to create an attractive investment climate. In summary, this study significantly enriches the literature on international economics by providing a nuanced understanding of the empirical links between governance and FDI in the South Asian context. The rigorous methodology, clear presentation of findings, and actionable policy recommendations make this research a valuable resource for policymakers, researchers, and practitioners interested in promoting economic growth through foreign investment in the region.

The residual parts of the paper proceeded as: section 2 supports the theoretical framework of the study by reviewing the literature, section 3 provides the detail about the data and design of the study, and section 4 outlays the empirical findings of the study. In section 5, the empirical findings were discussed and compared with established literature. In section 6, the conclusion of the paper and emanated policies was discussed.

2. Literature review

2.1. Theoretical background

The discussion on FDI was initiated after the work of Dunning (Citation1980) in which he argued the famous varied theory of foreign investment. This theory is based upon ownership (O), location (L), and internalization (I), commonly known as OLI theory. According to OLI theory, FDI can be categorized into four types of efficiency-seeking FDI, market-seeking FDI, resource-seeking FDI, and strategic asset-seeking FDI. In efficiency-seeking FDI, foreign investors are often interested in achieving competitiveness by exploring efficient production tools. Foreign firms locate their investment in the host country to enhance their product competitiveness in terms of quality and quantity. Whereas the market-seeking FDI aims to penetrate the local market to enhance their sale and customer volume. It further aims to capture a large market share by inducing favorable market competition. In resource-seeking FDI, the foreign enterprises are often interested in the domestic natural resources like availability of specific raw materials, physical infrastructure, cheaper and excessive labor supply, etc. All these factors capture the attention of foreign investors and urge them to locate their investment ventures in a specific host country. Similarly, the strategic asset-seeking FDI endures the expansion of the regional market strategy of a firm into the global market and enhances the reputational asset volume of enterprises by seeking more markets, technologies, and management skills (Rashid et al., Citation2017). In addition to the theoretical description, many empirical studies have been witnessed in literature exploring the various determinants of FDI. In the next section, the empirical studies have been reviewed offering the specific relationship of various factors with FDI inflow.

2.2. Empirical literature

The review of existing studies on relevant determinants of FDI enhances the theoretical understanding of key determinants and their direction of contribution in determining foreign investment. In this essence, many studies emerged that explore how different country-level factors affect the FDI inflow volume. Focusing on governance literature, the study of Raza et al. (Citation2021a) demonstrates the positive role of institution quality and corruption control in attracting foreign investment. Both factors reflect the transparency in public and financial dealings by the government and thus attract foreign investors to invest in various business ventures. The empirical study of Shittu et al. (Citation2020) measures the role of governance in the nexus between FDI, globalization, and economic growth of West Africa. Their analysis indicates the positive influence of foreign investment and globalization on economic growth. In addition, they further found that better governance can improve the inflow of foreign investment which further derives positive economic growth. Siriopoulos et al. (Citation2021) have explored the trend of foreign investment in the presence of IFRS adoption and governance quality in the GCC region and found that the adoption of IFRS works as a potential determinant of foreign investment inflow. They further found that although the GCC group has less compliance with governance quality, the governance indicators serve as more prominent determinants of inviting the foreign investment.

Doytch and Eren (Citation2012) studied the determinants of FDI sectoral distribution in Eastern Europe and Central Asia, focusing on the investment climate and democracy levels. The findings of their study revealed that, when accounting for human capital, the host country’s investment profile positively influences agricultural FDI, while the state of democracy has a positive impact on agricultural and manufacturing FDI. In addition, educated labor attracts services FDI, whereas cheap labor is a magnet for FDI in other sectors. Doytch (Citation2015) investigated the impact of host country business cycles on sectoral FDI inflows in South and East Asian economies from 1980 to 2011. The findings suggested countercyclical patterns in services FDI and acyclical behavior in both extractive industries and manufacturing FDI. Recently, Doytch and Ashraf (Citation2023) investigated the impact of institutional quality indicators on two modes of FDI including greenfield investment and cross-border mergers and acquisitions (M&As) across 110 countries from 2003 to 2017. The findings revealed that favorable institutional conditions for greenfield FDI in developing countries require law and order, good investment conditions, and democracy, while cross-border M&A sales demand additional factors like strict corruption control. Notably, developed countries show a comparatively smaller reliance on institutions as determinants for both FDI types, suggesting the need for distinct policies tailored to each mode of investment.

Another study arranged by Tran and Le (Citation2019) has investigated the linkage among governance systems, foreign investment, and entrepreneurship activities in emerging economies. Their analysis evidenced that better governance systems serve as a stimulator in the nexus between foreign investment and entrepreneurship activities. Contrarily, the empirical analysis of Ogbonna et al. (Citation2022) reveals that institutional governance in the economic system amplifies the adverse effects of global uncertainty on FDI inflow in Africa. Instead of mitigating the adverse effects, the institutional quality worsens the situation by hampering the effect of global uncertainty on FDI inflow. In view of the census provided by empirical literature, it can be commented that the governance system of the host country works as a main drive of foreign investment inflow.

In addition to the governance system, a list of other factors affecting the inflow of FDI has been observed in scholarly articles. Among others, inflation rate, trade volume, population growth, total labor force, and financial development are the key determinants of FDI inflow. For inflation rate, an array of literature exists explaining the negative role of inflation rate in locating the FDI inflow. The analyses of Agudze and Ibhagui (Citation2021) found that higher inflation limited the FDI inflow as inflation enhances the uncertainty and cost of business operations. Both factors have an adverse impact on foreign investment. The empirical analysis of Boateng et al. (Citation2015) asserted the negative impact of the inflation rate on FDI inflow. Another analysis by Sabir et al. (Citation2019) has found a similar impact of inflation on FDI in developing economies while an insignificant impact in developed economies. Contrarily, the study of Aziz and Mishra (Citation2016) has commented on the insignificant impact of the inflation rate on FDI inflow in Arab economies. Similarly, the study of Nguyen and Lee (Citation2021) analyzes the joint impact of policy uncertainty, and financial development on FDI inflow. Their analysis concluded that the FDI inflow allocates away from those countries having high policy uncertainty. However, the financial development attracts more FDI and stable the economic growth.

The empirical analysis of Dutta et al. (Citation2017) suggests that human capital can attract more FDI inflow. They further suggest the interactive role of corruption control in the nexus between human capital and FDI inflow. Similarly, Sadeghi et al. (Citation2020) has also investigated the role of economic complexity and human capital in driving the FDI inflow. Their analysis indicates that the economic complexity measured with two proxies, i.e. economic sophistication, and economic complexity index has a positive role in inviting the FDI. Furthermore, their analysis also reveals the fact that how countries with high human capital attract more FDI. Recently, Abbas et al. (Citation2022) makes an analysis on 103 transition and developing economies and shows that foreign enterprises are often interested in seeking cheap labor and extensive human capital while locating their business ventures in the host country. These two factors serve as the main determinants of FDI attraction. In addition to the labor force, another empirical analysis conducted by Lee et al. (Citation2022) considered the threshold effect and explored the nexus between foreign investment, income inequality, and financial development. Their analysis suggests the positive outcomes of FDI inflow regarding the reduction in income inequality. However, this beneficial role of FDI becomes weaker after a certain threshold point. In this essence, financial development plays a moderating role to harvest the better outcomes of FDI inflow in the form of reduction in income inequality.

Summarizing the empirical literature, it can be viewed that a better governance system, trade volume, human capital in form of population growth and total labor force, and financial development play a positive role whilst a high inflation rate works as a discouraging determinant of FDI inflow. Primarily, by leaning on empirical studies exploring the role of better governance in FDI inflow, it can be hypothesized that a better governance system has a positive and statistically significant effect on FDI inflow.

3. Data and methods

The empirical analysis is based upon 20 years (2000–2019) of financial information from 8 South Asian countries (Afghanistan, Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, and Sri Lanka). We select this span due to two reasons. First, the South Asian countries have experienced a massive increase in total investment during this span. Second, we limit the span to 2019 due to exclusion of the covid-19 spread effect. Due to the COVID effect, the countries may face volatility in an inflow of foreign investment and thus the inclusion of 2020 can create biased analysis and policies as well. Similarly, the motivation behind the selection of South Asian countries is as these economies have almost similar arrangements of governance systems to some extent. According to the World governance report, all south Asian economies have negative aggregate governance scores, implying the worst condition of governance in these economies. Thus, it is more useful to arrange the current analysis on South Asian countries. The data of macroeconomic variables including FDI, inflation rate, trade volume, and other control variables were sourced from WDI, The World Bank while the data of governance situation were accessed from WGI (world governance indicators). Both data sources provide authentic financial statistics on underlying variables.

3.1. Variables of study

In the current empirical analysis, the foreign direct investment (FDI) inflow is included as a dependent variable, depending upon the governance system, and a list of control variables including inflation rate, trade volume, population growth, labor force, and financial development. The measurement of FDI inflow is a percentage inflow of foreign investment into the host country. This specific measurement of FDI is specified by WDI, The World Bank. FDI inflow is the volume of investment made by non-resident individuals to acquire the significant management interest (minimum 10% or more) of an enterprise working in a country different from the home country of the investor. It further shows the volume of long-term capital, equity capital, short-term capital, and reinvestment of funds earned by non-resident individuals and shown on the balance sheet of enterprises working in another country. The volume of FDI shows the confidence of foreign investors in the economic situation of the host country explicitly encouraging the foreign investors to locate their funds in the host country. In addition to The World Bank, the studies arranged by Azam and Haseeb (Citation2021), and Mitra and Abedin (Citation2022) have employed a similar measurement of FDI inflow. The quality of governance is our main explanatory variable and is measured with the country governance index (CGI). CGI is an aggregate governance score on six underlying indicators of governance including voice and accountability (VA), government effectiveness (GE), political stability (PS), regulatory quality (RQ), corruption control (CC), and rule of law (RL). These indices were first developed by Kaufmann et al. (Citation1999) and reflect the overall governance situation of a country.

According to WGI (world governance indicator), the governance score ranges from 2.5 (good governance situation) to −2.5 (worst governance situation). In this analysis, we have used the aggregate score on all mentioned indicators of governance as a proxy of governance quality. Explaining the indicators of governance, VA reflects the perception to what extent a country’s residents can participate in electing a new government, freedom of alliance, freedom of communication, etc. GE is a perception of policy development and implementation, quality of civil and public services, and exclusion from political pressure, etc., Similarly, PS is the stability of elected government whilst RQ shows the accountability on the break of regulations. It further shows the commitment of a government to developing the private sector. CC is an indicator to measure the check on unfavorable gains while RL shows the adoption and compliance of rules by society complied by the central government. It further demonstrates the protection of property rights, contract enforcement, and accountability for crime and violence, etc., The analyses of Bah and Kpognon (Citation2021), and Tran and Le (Citation2019) demonstrate the similar measurement of CGI and cohesiveness with FDI inflow.

To measure the inflation rate, the CPI (consumer price index) was used which shows the annual percentage volatility in prices of goods consumed by end consumers. It further shows the increment in the cost of a basket of goods and services. Generally, the Laspeyres formula is used to calculate the CPI. A higher inflation rate has a close link with FDI inflow as the inflation rate reflects the change in both costs of raw materials and general prices of industrial goods which further determines the investment behavior of foreign investors. Trade volume is the sum of the total volume of exports and imports during a specific year. It comprises all inflow and outflow transactions of goods and services between a home country and the rest of the world. To stabilize the values, we use the logarthematic expression of trade volume. The population growth rate reflects the percentage increment in the total population of a country during a year. Its measurement is based upon a de facto definition of population, which considers all inhabitants of a country regardless of citizenship and legal status. A higher population growth rate demonstrates the high volume of consumers for industrial goods and may attract foreign investors for investment.

Similarly, the total labor force (TLF) exhibits the number of workers having age 15 or older who are actively participating and offering their services in various economic activities. It comprises both employed and unemployed and is actively seeking new jobs. In TLF calculation, we often omit the students, family workers, and unpaid workers who are working voluntarily. A high labor force can also attract foreign entrepreneurs seeking to locate labor-intensive entrepreneurial activities in the host country. Lastly, the financial development demonstrates the volume of credit extended by banks to the private sector including various industrial sectors. A country in which banks offer higher credit at low financing costs can be categorized as financially developed and vice versa. The measurement of all these variables has been specified by WDI, The World Bank. All these variables have been used by a list of studies as potential determinants of FDI inflow (Boateng et al., Citation2015; Dang & Nguyen, Citation2021; Mitra & Abedin, Citation2022; Xu et al., Citation2021). In , the summarized description of these variables has been provided.

Table 1. Variables of study.

3.2. Model estimation

To estimate the empirical relationship between variables, the following equation can be developed.

(1)

(1)

In EquationEquation (1)(1)

(1) , FDI is an acronym for foreign direct investment, CGI is aggregate governance index, IFR is the inflation rate, TDV is trade volume, PG is population growth, TLF is total labor force, and FSD is a financial sector development. Whereas

is a symbol of residual term, and subscripts J is for the country while t is for time.

To estimate the regression among variables, we start the analysis by employing a simple OLS (ordinary least square) model. To validate the OLS model, it is necessary to employ the various diagnostic tests validating that either the OLS model is appropriate or further techniques should be applied. Given that, we first check the stationarity status of variables by employing the unit root testing and adopt the (Im, Pesaran and Shin W-stat, Im et al., Citation2003), and (ADF – Fisher Chi-square, Dickey & Fuller, Citation1979) techniques. The analysis shown in implies that most variables are stationary at the first difference (I (1)). In this essence, the implication of the OLS model is spurious and processed to check the cointegration among variables. To check the cointegration, we run the Johansen cointegration test (Johansen, Citation1988) and select the Kao-residual technique. The statistical analysis shown in rejects the null hypothesis, i.e. no cointegration among variables, and suggests the presence of cointegration among variables. Based on empirical suggestions provided by pre-estimation techniques, we employ the FMOLS (fully modified ordinary least square) model argued by Phillips and Hansen (Citation1990) and check the robustness through DOLS (dynamic ordinary least square) model. FMOLS model can tackle the said issues of serial correlation and potential endogeneity. Both FMOLS and DOLS models are long-run coefficient estimation techniques, therefore the estimated results should be considered as a long-run strategy. In the current analysis, as the sample contains various countries of a group (South Asia), therefore there are more chances of cross-section dependence. Given that, we employ the cross-section dependence test and report the results in Table. The insignificant probability values of the Breusch-pagan LM test (Breusch & Pagan, Citation1980), and other companion techniques vow that no cross-section dependence exist.

4. Empirical analysis

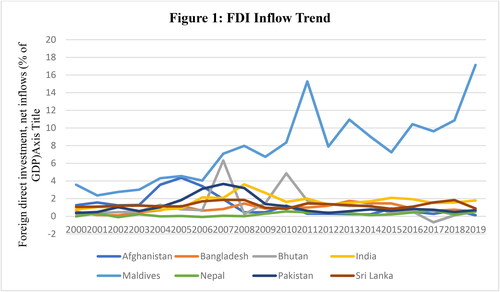

presents the summary of statistics for all the variables of the study. The average inflow of FDI is 1.189% of GDP while this percentage changes when we look at the statistics across the countries. The average statistical values shown in demonstrate that Maldives has the highest percentage of FDI inflow (7.662%) while Nepal has the lowest average value of FDI inflow (0.231%). The mean value of CGI is -0.552, implying the bad governance situation in the sample countries. If we compare the CGI across the countries (shown in ), Afghanistan has the worst governance score of -1.622 while Bhutan has a positive governance score of 0.253 implying a good governance situation in Bhutan. The mean value of the inflation rate is 5.649% with a maximum value of 26.418% (in Afghanistan in 2008) and a minimum value of -18.108 (in Bhutan in 2004). The mean value of trade volume is 10.363 which is a logarithmic value indicating the volume of total exports and imports. The mean value of the population growth rate is 1.663. If we compare the average statistics of PG shown in , the Maldives has the highest population growth rate of 3.316, followed by Afghanistan (3.172), Pakistan (2.231), Bhutan (1.390), India (1.372), Bangladesh (1.321), Nepal (0.981), and Sri Lanka (0.777). The logarithmic mean value of TLF is 7.219 while FSD has a mean value of 31.433%. shows the trend of FDI inflow in sample countries from the year 2000 to 2019. In addition, the correlation analysis has been presented in . Most of the correlation statistics are less than the benchmark value of 0.70, rejecting the existence of multicollinearity among the variables.

Figure 1. FDI inflow trend.

Table 2. Descriptive statistics.

Table 3. Mean values across the countries.

Table 4. Correlation analysis.

4.1. Regression analysis

Before regression estimation, some pre-estimation techniques, e.g. unit root testing, cointegration analysis, and cross-section dependence test, were applied to validate the implication of a specific regression model. The statistical analysis shown in demonstrates that some variables bear the stationarity status at the first difference, advising checking the cointegration among variables. The cointegration among variables was assessed by employing the Johansen cointegration test. The statistical outputs reveal the presence of cointegration, advocating the implication of the FMOLS model. In addition, the cross-section dependence was also tested by employing a series of mentioned approaches (In ). The probability values shown in reject the existence of cross-section dependence. Therefore, we finally employ the FMOLS model and check the robustness by applying the DOLS model. The coefficient values reported in reveal the direction and nature of the significance of explanatory variables. The coefficient value of governance is 0.407 which is significant at a 1% level and implies that a one-unit increase in aggregate governance of a country can enhance the volume of FDI inflow by 40.7%. This specific direction of relationship and level of significance of governance was found robust even after employing the DOLS model. The coefficient value of the inflation rate is -0.030, suggesting a statistically significant but inverse relationship with FDI inflow. However, the residual control variables, i.e. trade volume, population growth, labor force, and financial development show a positive and significant relationship with FDI inflow. Their coefficient values are 0.339, 0.741, 1.705, and 0.026 relatively. Overall, the empirical results show robust evidence of the promising role of better governance in enhancing the FDI inflow.

Table 5. Unit root testing.

Table 6. Johansen cointegration test.

Table 7. Cross-section dependence test.

Table 8. Effect of governance on FDI inflow.

5. Discussion on results

This study explores the empirical relationship between governance quality and FDI inflow by controlling the inflation rate, trade volume, population growth, labor force, and financial development. For empirical analysis, we employ the panel FMOLS model and check the robustness through the DOLS model. The empirical analysis presented in vows that the aggregate governance index has a positive significant impact on FDI inflow. A better governance system always encourages foreign investors to locate their investment activities. Moreover, the good governance system is an indication of the low problem of information asymmetry, fewer chances of default, and protection of property rights, etc., all these factors positively derive the investment behavior of foreign investors. Meanwhile, the good governance situation reflects better institutional quality which inhibits the unnecessary delay in the execution of business activities (Tran & Le, Citation2019). This factor positively attracts foreign investors to transfer their investment in such economies. Similarly, a country with better governance quality ensures the protection of investors’ rights, the supremacy of higher legislative authorities, and the treatment of inhabitants based on merit. These factors substantially induce the optimistic views of foreign entrepreneurs who are in search of locating their investment ventures. In other words, the good governance situation is an indication of transparency in public operations and strict prohibition of law violations. Both factors enhance the ease of business doing and reduce the transaction cost of investment and thus motivate the foreign investors to position their investment activities in the host country (Mengistu & Adhikary, Citation2011). In this essence, the empirical analyses of Mishra and Ratti (Citation2011), Peres et al. (Citation2018), and Fon and Alon (Citation2022) support the similar impact of governance on FDI inflow.

Explaining the effect of control variables, the inflation rate has a negative coefficient value, suggesting the adverse effect of a higher inflation rate on FDI inflow. According to an empirical study by Boateng et al. (Citation2015), a higher inflation rate has a negative impact on FDI inflow. A higher inflation rate is an indication of market instability and low real earnings in terms of local currency. Both factors hamper the investment behavior of foreign investors. Moreover, high inflation signals the increment in prices of raw materials and tough price competition for foreign enterprises. It becomes more complex to enhance the sale volume during high inflation rate due to increments in production cost and end consumer price. Therefore, foreign investors are less interested in those economies experiencing high inflation rates. Contrarily, the coefficient sign of trade volume is positive, implying the positive role of higher trade volume in boosting the FDI inflow. Higher trade volume reflects the trade orientation of a country which is a key driver of foreign investment. Moreover, higher trade volume indicates that the specific country is more focusing on enhancing its trade activities and has an opportunistic future regarding industrial development. According to the strategic asset-seeking motive of FDI inflow, the foreign investors transfer their investment activities to such economies (Xu et al., Citation2021).

Population growth rate shows a positive correlation with FDI inflow. Higher population growth reflects a wider consumer market for industrial products. Moreover, the growing population requires more industrial products, and thus demand for industrial products increases. In view of the market-seeking objective of FDI, the higher population growth provides a big market for product penetration and enrichment of business operations. Thus, it can be asserted that higher population growth attracts more foreign enterprises to establish their capital business activities in the host country. Supporting this, the study of Asongu (Citation2013) resulted in a similar impact of population growth rate on foreign public investment. Similarly, the total labor force (TLF) has a positive link with FDI inflow. According to resource seeking objective of FDI, a country with more human capital attracts foreign investors for establishment of investment activities. A TLF is an indication of excessive availability of human capital which can utilize to boost industrial activities. Moreover, a country with more TLF attracts foreign investors by offering comparative cheap labor for completing industrial tasks. A higher labor force can approve as a driving force of FDI inflow by entailing more employment opportunities for the local population which is curious to work even at low wages. Supporting this, the empirical study of Nguyen (Citation2021) documents the similar impact of the labor force on FDI inflow.

Lastly, the financial development reveals a positive relationship with FDI inflow. Lee et al. (Citation2022) documents the moderating role of financial development in reducing income inequality due to FDI inflow. They further suggest that financial development can enhance the FDI inflow by enhancing the transparency in business operations and offering more financial services like loan availability at low financing costs to establish the industrial operations. Similarly, another study by Nguyen and Lee (Citation2021) asserted that financial development boosts the FDI inflow by mitigating the uncertainty in an economic environment. They also found the moderating impact of financial development in the nexus of uncertainty and FDI inflow. Concluding the discussion, it can be argued that a better governance system augments the inflow of FDI. Similarly, population growth rate, trade volume, labor force, and financial development have a positive while the inflation rate has a negative impact on FDI inflow.

6. Conclusion

The significant volume of FDI inflow plays a key role in boosting the economic growth of the host country. Therefore, each country struggles to enhance the volume of FDI to ensure economic growth and employment. In this essence, literature has suggested some factors that can affect the inflow of FDI. Among others, a better governance system is a vital factor that can boost the inflow of FDI. Given that, the current analysis explores the empirical relationship between the governance system and FDI inflow by sampling the South Asian economies and employing the FMOLS and DOLS models. The empirical results reveal the significant positive effect of the aggregate governance index on FDI inflow, implying that better governance can enhance the volume of FDI inflow. A better governance system reflects the stability of economic policies and better institutional quality, reduces the default risk and problem of information asymmetric, and enhances the ease of business doing. All these factors positively drive the FDI inflow. In addition to the governance system, the current analysis indicates the significant negative effect of the inflation rate while a positive significant impact of trade volume, population growth, labor force, and financial development on FDI inflow in South Asian economies. The empirical analysis proves the alternative hypothesis, i.e. governance has a positive role in enhancing the FDI inflow.

6.1. Implications

The empirical analysis outlined in this study carries significant policy implications for both domestic policy officials in South Asian economies and foreign investors contemplating investment ventures abroad. The observed low FDI inflow in most South Asian economies, attributed to factors such as poor governance, a dearth of skilled labor, and high policy uncertainty, necessitates urgent attention. In response, South Asian nations should prioritize enhancing governance quality, focusing on the effective enforcement of laws, robust corruption control measures, and the improvement of institutional quality. These measures collectively contribute to creating a favorable economic environment conducive to attracting increased FDI. To address the challenge of low FDI inflow, South Asian economies are urged to implement policies aimed at establishing technical education institutions. This strategic move would bolster the availability of skilled labor, a crucial factor in attracting foreign investors seeking a skilled workforce. Additionally, policy officials should concentrate on fostering financial development, controlling inflation rates, and promoting trade activities, as these factors demonstrate a positive correlation with increased FDI inflow.

Furthermore, international investors are advised to consider countries with high population growth rates for their investment activities. Such nations signify a large and growing consumer market for industrial products, offering lucrative opportunities for foreign investors. As this study focuses on the collective trends of South Asian economies, future analyses could enhance comprehensiveness by examining individual FDI trends in each country. Moreover, the integration of additional factors, such as the economic complexity index, and addressing the current analysis’s limitations could contribute to a more nuanced understanding of the dynamics influencing FDI inflow in the region. Overall, the policy recommendations derived from this study provide actionable insights for fostering a more conducive environment for FDI in South Asia.

6.2. Limitations and future research

Despite its contributions, this study is not without limitations. Firstly, the analysis lacks an examination of individual trends in FDI for each South Asian economy, thereby potentially overlooking country-specific nuances that could influence investment dynamics. Additionally, the study does not incorporate certain relevant factors, such as the economic complexity index, which could provide a more comprehensive understanding of the forces shaping FDI in the region. Furthermore, the empirical analysis, while insightful, may not capture the full spectrum of determinants influencing FDI, leaving room for other unexplored variables to play a role.

In terms of future research, an avenue for exploration could involve a more detailed examination of individual South Asian economies, shedding light on specific factors influencing FDI trends in each nation. Moreover, incorporating additional variables, such as the economic complexity index, and addressing the identified limitations, would contribute to a more nuanced and holistic understanding of the FDI landscape in the region. Additionally, future studies could delve into the evolving dynamics of FDI in the context of changing global economic conditions and geopolitical landscapes, providing valuable insights into the adaptability of South Asian economies in attracting foreign investments. Lastly, exploring the impact of emerging technologies and industries on FDI patterns could be a fruitful area for research, offering a forward-looking perspective on the factors shaping future investment trends in the South Asian region.

Authors’ contributions

Mosab I. Tabash: supervision, writing original draft, data curation; Umar Farooq: conceptualization, data curation, writing-original draft preparation; Ali Matar: supervision, reviewing and grammar check, methodology, funding acquisition; Mujeeb Saif Mohsen Al-Absy: funding, statistical analysis, policy recommendations.

Informed consent

We hereby grant the consent and acknowledge that paper should be sent for peer review, or any other publication process required by journal.

Data availability statement

Data that support the findings of this study available at public domains name World Development Indicators, and World Governance Indicators, The World Bank.

Disclosure statement

All authors hereby declare that that we have no conflict of interest that can interrupt the review process or publication process.

Additional information

Notes on contributors

Mosab I. Tabash

Mosab I. Tabash is currently working as MBA Director and Associate Professor of Finance at the College of Business, Al Ain University, UAE. He obtained his Doctor of Philosophy (Ph.D.) in Finance from the Faculty of Management Studies (FMS Delhi). His research interests include Islamic banking and finance, monetary policies, corporate governance, financial performance, investments, tourism and risk management.

Umar Farooq

Umar Farooq is a Ph.D. (applied economics) scholar at the school of Economics and Finance, Xian Jiaotong University, China. Currently, his Ph.D. is at the final stage. His main research interest includes corporate finance and investment, financial economics, environmental economics, and macroeconomic theory and practices. He has recently published papers in peer-reviewed journals including the Borsa Istanbul Review, Research in International Business and Finance, Journal of Cleaner Production, International Journal of Finance and Economics, Energy Policy, Energy, Bulletin of Economic Research, International Review of Administrative Sciences, Resources Policy. He is also working as an active reviewer in several peer-reviewed journals.

Ali Matar

Ali Matar is an Associate professor in Financial Economic and currently he is the Dean of Scientific Research at Jadara University, Irbid, Jordan.

Mujeeb Saif Mohsen Al-Absy

Mujeeb AL-Absy is an assistant professor, Department of Business Management, Abs Community College, Hajjah, Yemen, currently working as a visiting faculty member in the Department of Accounting and Finance, College of Administrative and Financial Sciences, Gulf University, Bahrain. He obtained his Master and PhD degrees from the School of Accountancy, College of Business, Universiti Utara Malaysia, Malaysia and a BSc degree from the College of Commerce and Economics, majoring in accounting, from Hodeidah University, Yemen. Dr. Mujeed has several articles published in Scopus journals; some of them also indexed by ISI. He has presented his working ideas at several international conferences in Malaysia. He has reviewed several international papers published in high-indexed journals. Professionally, Dr. Mujeeb has 6 years of working experience as an accountant at Salah Al-Awadi industrial complex, Hodeidah, Yemen.

References

- Abbas, A., Moosa, I., & Ramiah, V. (2022). The contribution of human capital to foreign direct investment inflows in developing countries. Journal of Intellectual Capital, 23(1), 9–26. https://doi.org/10.1108/JIC-12-2020-0388

- Agudze, K., & Ibhagui, O. (2021). Inflation and FDI in industrialized and developing economies. International Review of Applied Economics, 35(5), 1–16. https://doi.org/10.1080/02692171.2020.1853683

- Asongu, S. A. (2013). How would population growth affect investment in the future? Asymmetric panel causality evidence for Africa. African Development Review, 25(1), 14–29. https://doi.org/10.1111/j.1467-8268.2013.12010.x

- Azam, M., & Haseeb, M. (2021). Determinants of foreign direct investment in BRICS – Does renewable and non-renewable energy matter? Energy Strategy Reviews, 35, 100638. https://doi.org/10.1016/j.esr.2021.100638

- Aziz, O. G., & Mishra, A. V. (2016). Determinants of FDI inflows to Arab economies. Journal of International Trade & Economic Development, 25(3), 325–356. https://doi.org/10.1080/09638199.2015.1057610

- Bah, M., & Kpognon, K. (2021). Public investment and economic growth in ECOWAS countries: Does governance Matter? African Journal of Science, Technology, Innovation and Development, 13(6), 713–726. https://doi.org/10.1080/20421338.2020.1796051

- Boateng, A., Hua, X., Nisar, S., & Wu, J. (2015). Examining the determinants of inward FDI: Evidence from Norway. Economic Modelling, 47(June), 118–127. https://doi.org/10.1016/j.econmod.2015.02.018

- Breusch, T. S., & Pagan, A. R. (1980). The Lagrange multiplier test and its applications to model specification in econometrics. Review of Economic Studies, 47(1), 239–253. https://doi.org/10.2307/2297111

- Dang, V. C., & Nguyen, Q. K. (2021). Determinants of FDI attractiveness: Evidence from ASEAN-7 countries. Cogent Social Sciences, 7(1). https://doi.org/10.1080/23311886.2021.2004676

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366), 427–431. https://doi.org/10.2307/2286348

- Doytch, N. (2015). Sectoral FDI cycles in South and East Asia. Journal of Asian Economics, 36(Feb), 24–33. https://doi.org/10.1016/j.asieco.2014.12.002

- Doytch, N., & Ashraf, A. (2023). Do institutions impact differently inward greenfield FDI and cross-border M&A sales? A study of five institutional quality indicators in developed and developing countries. Journal of Financial Economic Policy, 15(6), 501–529. https://doi.org/10.1108/JFEP-06-2023-0161

- Doytch, N., & Eren, M. (2012). Institutional determinants of sectoral FDI in Eastern European and Central Asian Countries: The role of investment climate and democracy. Emerging Markets Finance and Trade, 48(sup4), 14–32. https://doi.org/10.2753/REE1540-496X4806S402

- Dunning, J. H. (1980). Toward an eclectic theory of international production: Some empirical tests. Journal of International Business Studies, 11(1), 9–31. https://doi.org/10.1057/palgrave.jibs.8490593

- Dutta, N., Kar, S., & Saha, S. (2017). Human capital and FDI: How does corruption affect the relationship? Economic Analysis and Policy, 56(December), 126–134. https://doi.org/10.1016/j.eap.2017.08.007

- Fon, R., & Alon, I. (2022). Governance, foreign aid, and Chinese foreign direct investment. Thunderbird: International Business Review, 64(2), 179–201.

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Johansen, S. (1988). Statistical analysis of co-integrating vectors. Journal of Economic Dynamics and Control, 12(2–3), 231–254. https://doi.org/10.1016/0165-1889(88)90041-3

- Kaufmann, D., Kraay, A., & Zoido-Lobaton, P. (1999). Aggregating governance indicators. World Bank Policy Research Working Paper.

- Lee, C. C., Lee, C. C., & Cheng, C. Y. (2022). The impact of FDI on income inequality: Evidence from the perspective of financial development. International Journal of Finance & Economics, 27(1), 137–157. https://doi.org/10.1002/ijfe.2143

- Mengistu, A. A., & Adhikary, B. K. (2011). Does good governance matter for FDI inflows? Evidence from Asian economies. Asia Pacific Business Review, 17(3), 281–299. https://doi.org/10.1080/13602381003755765

- Mishra, A. V., & Ratti, R. A. (2011). Governance, monitoring and foreign investment in Chinese companies. Emerging Markets Review, 12(2), 171–188. https://doi.org/10.1016/j.ememar.2011.02.005

- Mitra, R., & Abedin, M. T. (2022). Does a shrinking labor force reduce FDI inflows in OECD countries? Applied Economics Letters, 29(17), 1654–1658. https://doi.org/10.1080/13504851.2022.2025996

- Musibau, H. O., Yusuf, A. H., & Gold, K. L. (2019). Endogenous specification of foreign capital inflows, human capital development and economic growth: A study of pool mean group. International Journal of Social Economics, 46(3), 454–472. https://doi.org/10.1108/IJSE-04-2018-0168

- Nguyen, C. H. (2021). Labor force and foreign direct investment: Empirical evidence from Vietnam. Journal of Asian Finance, Economics and Business, 8(1), 103–112.

- Nguyen, C. P., & Lee, G. S. (2021). Uncertainty, financial development, and FDI inflows: Global evidence. Economic Modelling, 99(June), 105473. https://doi.org/10.1016/j.econmod.2021.02.014

- Ogbonna, O. E., Ogbuabor, J. E., Manasseh, C. O., & Ekeocha, D. O. (2022). Global uncertainty, economic governance institutions and foreign direct investment inflow in Africa. Economic Change and Restructuring, 55(4), 2111–2136. https://doi.org/10.1007/s10644-021-09378-w

- Peres, M., Ameer, W., & Xu, H. (2018). The impact of institutional quality on foreign direct investment inflows: Evidence for developed and developing countries. Economic Research-Ekonomska Istraživanja, 31(1), 626–644. https://doi.org/10.1080/1331677X.2018.1438906

- Phillips, P. C., & Hansen, B. E. (1990). Statistical inference in instrumental variable regression with I(1) processes. Review of Economic Studies, 57(1), 99–125. https://doi.org/10.2307/2297545

- Qureshi, F., Qureshi, S., Vo, X. V., & Junejo, I. (2021). Revisiting the nexus among foreign direct investment, corruption and growth in developing and developed markets. Borsa Istanbul Review, 21(1), 80–91. https://doi.org/10.1016/j.bir.2020.08.001

- Rafei, M., Esmaeili, P., & Lorente, D. B. (2022). A step towards environmental mitigation: How do economic complexity and natural resources matter? Focusing on different institutional quality level countries. Resources Policy, 78, 102848. https://doi.org/10.1016/j.resourpol.2022.102848

- Rao, D. T., Sethi, N., Dash, D. P., & Bhujabal, P. (2020). Foreign aid, FDI and economic growth in South-East Asia and South Asia. Global Business Review, 24(1), 31–47. https://doi.org/10.1177/0972150919890957

- Rashid, M., Looi, X. H., & Wong, S. J. (2017). Political stability and FDI in the most competitive Asia Pacific countries. Journal of Financial Economic Policy, 9(02), 140–155. https://doi.org/10.1108/JFEP-03-2016-0022

- Raza, M. A., Yan, C., Abbas, H. S., & Ullah, A. (2021a). Impact of institutional governance and state determinants on foreign direct investment in Asian economies. Growth and Change, 52(4), 2596–2613. https://doi.org/10.1111/grow.12541

- Raza, S. A., Shah, N., & Arif, I. (2021b). Relationship between FDI and economic growth in the presence of good governance system: Evidence from OECD countries. Global Business Review, 22(6), 1471–1489. https://doi.org/10.1177/0972150919833484

- Sabir, S., Rafique, A., & Abbas, K. (2019). Institutions and FDI: Evidence from developed and developing countries. Financial Innovation, 5(1), 1–20. https://doi.org/10.1186/s40854-019-0123-7

- Sadeghi, P., Shahrestani, H., Kiani, K. H., & Torabi, T. (2020). Economic complexity, human capital, and FDI attraction: A cross country analysis. International Economics, 164(December), 168–182. https://doi.org/10.1016/j.inteco.2020.08.005

- Shittu, W. O., Agboola, H., Houssein, A. E., & Hassan, S. (2020). The impacts of foreign direct investment and globalisation on economic growth in West Africa: Examining the role of political governance. Journal of Economic Studies, 47(7), 1733–1755. https://doi.org/10.1108/JES-09-2019-0446

- Siriopoulos, C., Tsagkanos, A., Svingou, A., & Daskalopoulos, E. (2021). Foreign direct investment in GCC countries: The essential influence of governance and the adoption of IFRS. Journal of Risk and Financial Management, 14(6), 264. https://doi.org/10.3390/jrfm14060264

- Tran, N. H., & Le, C. D. (2019). Governance quality, foreign direct investment, and entrepreneurship in emerging markets. Journal of Asian Business and Economic Studies, 26(2), 238–264. https://doi.org/10.1108/JABES-09-2018-0063

- Wu, W., Yuan, L., Wang, X., Cao, X., & Zhou, S. (2020). Does FDI drive economic growth? Evidence from city data in China. Emerging Markets Finance and Trade, 56(11), 2594–2607. https://doi.org/10.1080/1540496X.2019.1644621

- Xu, C., Han, M., Dossou, T. A., & Bekun, F. V. (2021). Trade openness, FDI, and income inequality: Evidence from sub-Saharan Africa. African Development Review, 33(1), 193–203. https://doi.org/10.1111/1467-8268.12511