?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines proxies of money market, capital market, and banks in Nigeria using annual data from 1961 to 2018. We employ autoregressive distributed lag (ARDL) bounds testing approach, Wald test, and vector error correction model (VECM) Granger causality technique to analyse the data. Our findings show that total subscriptions of treasury bills has a positive and negative statistically significant relationship with real gross domestic product (GDP) on the long-run and short-run, respectively. Hence, we argue that markets and banks exhibit competitive interaction in favour of markets in Nigeria. Additionally, our findings show a unidirectional short-run causality from real GDP to value of transactions on the Nigerian Stock Exchange (NSE). Furthermore, our results support the existence of growth-led finance view or demand-following hypothesis in Nigeria, as we observe a unidirectional long-run causality from real GDP to both value of money market instruments outstanding as at end-period and total subscriptions of treasury bills.

Impact statement

This study investigates finance-growth nexus in Nigeria with a particular focus on banks and markets. The findings of this research reveal that the role of markets on economic growth is superior to banks in Nigeria. Hence, banks and markets are competitive. Additionally, our empirical findings provide evidence to support the existence of growth-led finance view in Nigeria. This research explains the relevance of the financial system on economic growth in Nigeria and provides corresponding insights to policy makers.

REVIEWING EDITOR:

SUBJECTS:

1. Introduction

Historically, the relationship between finance and economic growth commenced with the studies of Bagehot (Citation1873) and Schumpeter (Citation1911), which emphasise on the role of banks as financial intermediaries within an economy. As such, Bagehot (Citation1873) and Schumpeter (Citation1911) are the first proponents of finance-led growth view. Emerging studies of Goldsmith (Citation1969), McKinnon (Citation1973), and Shaw (Citation1973) support the finance-led growth hypothesis. Robinson (Citation1952) challenges the finance-led growth hypothesis and argues that economic growth enhances financial sector development (growth-led finance). Thus, where there is economic growth, development of financial sector follows due to higher demand for financial services- which generates the growth-led finance view.

The contribution of Patrick (Citation1966) regards finance-led growth and growth-led finance views as supply-leading and demand-following hypothesis, respectively. According to Patrick (Citation1966), the interaction between these two hypotheses creates a feedback hypothesis, with the significant role of supply-leading at early stages of economic growth and demand-following taking over as growth increases. Contrary to these views, Lucas (Citation1988) argues that the role of financial system on economic growth is ‘badly over-stressed’. Thus, there is no causality between finance and growth, which explains neutrality hypothesis.

However, the debate about whether banks or markets exhibit greater influence on economic growth has led to advancement in the literature. On the bank-based perspective, studies, such as Fu et al. (Citation2018), Hao (Citation2006), Korkmaz (Citation2015), Mamman and Hashim (Citation2014), Odedokun (Citation1996, Citation1998) show a positive relationship between banks and economic growth. Whereas, studies, such as Alexiou et al. (Citation2018), Liang and Reichert (Citation2012), Mahran (Citation2012), Xu (Citation2016) reveal a negative relationship between banks and economic growth.

On the market-based perspective, studies, such as Fufa and Kim (Citation2017), Marques et al. (Citation2013), Ngare et al. (Citation2014), Pradhan (Citation2018) reveal a positive relationship between markets and economic growth. The study of Fufa and Kim (Citation2017) further shows negative relationship between markets and economic growth in non-European high income countries. Additionally, the work of Pan and Mishra (Citation2018) reveals negative relationship between markets and economic growth in China. As such, the empirical impact of banks and markets on economic growth remains inconclusive which calls for increasing scholarly attention.

In Nigeria, the financial system comprises of banks, financial markets, and other financial institutions which are regulated by the Banks and other Financial Institutions Act 1991 (BOFIA) as amended in 1997, 1998, 1999, and 2002. According to CBN (Citation2007), BOFIA commenced on 20 June 1991 after its enactment by the National Assembly of the Federal Republic. The banking sector in Nigeria is an essential part of the financial system. The motivation underpinning this research is the unresolved empirical debate on the role of banks and markets in the financial system. Additionally, this paper provides a basis to investigate the impact of money markets and capital markets in Nigeria. In this regard, this paper contributes to existing studies, particularly in Nigeria where there is little empirical evidence on the interaction of banks and markets.

The novelty of this study is the consideration of money market and capital market proxies for market-based view for robustness, rather than the widely used stock market variables in existing studies (for instance, Ailemen & Unemhilin, Citation2017; Azam et al., Citation2016; Deyshappriya, Citation2016; Fufa & Kim, Citation2017; Lazarov et al., Citation2016; Marques et al., Citation2013; Ngare et al., Citation2014; Nyasha & Odhiambo, Citation2017a, Citation2017b; Pan & Mishra, Citation2018; Pradhan, Citation2018). While the study of Arize et al. (Citation2017), also considers money market variables using domestic treasury bill rate in Nigeria, our study is different as we consider the value of money market instruments outstanding as at end-period and total subscriptions of treasury bills as money market proxies.

The rest of this paper is organised as follows. Section 2 reviews the literature on bank-based vs. market-based, and evolution of banks and markets in Nigeria, Section 3 describes the empirical model and provides information about the data, including descriptive statistics, Section 4 presents and discusses the empirical results, and Section 5 highlights the final conclusion with policy recommendations.

2. Literature review

2.1. Market-based view

The market-based view or direct finance supports the relevance of financial markets in the reduction of intrinsic inefficiencies introduced by banks on economic growth (Lee, Citation2012). The study of Arrow and Debreu (Citation1954) which builds on the market equilibrium as proposed by Walras’ Law provides a foundation to support market-based view over banks. As such, Arrow and Debreu (Citation1954) argues that due to problems associated with normative or welfare economics, Walras’ law fails to offer solutions to market equilibrium. Consequently, the study of Arrow and Debreu (Citation1954) advocates for the relevance of market-based view based on the assumptions that financial markets are complete and perfect, allocation of resources within an economy is Pareto-optimal, which provides limited capacity for financial intermediaries to enhance societal welfare. Additionally, Fama (Citation1980) asserts that market-based view is related to Modigliani-Miller theorem which allows households to offset the role of financial intermediaries by creating portfolios.

2.2. Bank-based view

The bank-based view explains the role of banks and other financial intermediaries in the transfer of funds from savings surplus units to savings deficit units. In this regard, the study of Arrow and Debreu (Citation1954) further asserts that banks and other financial intermediaries play a significant role within an economy due to the existence of imperfections in the financial markets. Nonetheless, financial intermediaries become redundant when financial markets are perfect as savers and investors possess relevant information in search of funds. According to Scholtens and Wensveen (Citation2000) that despite the increase in globalisation, increase in prominent role of public markets, and revolution of information, financial intermediaries have proven to survive within financial systems.

2.3. Bank-based vs. market-based

Under the influence of the seminal contributions of Bagehot (Citation1873) and Schumpeter (Citation1911), several theoretical views on banks and markets have emerged. For instance, diverse regulatory policies uniqueness of financial intermediaries (Klein, Citation1971); theory of financial intermediation based on ‘delegated monitoring’ (Diamond, Citation1984); modern financial intermediation theory based on three approaches: transaction costs, information problems, and regulatory factors (Scholtens & Wensveen, Citation2000, Citation2003); complete and perfect financial markets assumptions (Arrow & Debreu, Citation1954), amongst others. To reconcile the controversial role of bank-based and market-based on economic growth, the study of Scholtens and Wensveen (Citation2003) postulates that bank-based view significantly enhances economic growth at early stages of economic development. However, as economies enter maturity phase, the need for richer and more sophisticated risk management instruments for raising capital on financial markets emerges (Levine, Citation2004).

The literature of Song and Thakor (Citation2010) identifies three-dimensional interaction between banks and markets: competition, complementary, and co-evolution. According to Song and Thakor (Citation2010), the comparative advantages of banks and markets make them compete only when viewed in isolation, not when they interact through securitisation and bank capital. Hence, complementary and co-evolution dimensions are departure from the competition dimension where one grows at the detriment of the other (Allen & Gale, Citation1999; Boot & Thakor, Citation1997; Dewatripont & Maskin, Citation1995) based on securitisation and bank capital.

On the one hand, securitisation creates a benefit flow from evolution of banks to markets as improved bank screening enhances credit quality of borrowers raising capital in the financial markets, thus increasing market participation of investors (Song & Thakor, Citation2010). On the other hand, bank capital creates a benefit flow evolution of markets to banks by reducing the cost of bank equity capital, this allows banks to hold more capital and consequently reduces rationing of credit relationship with borrowers (Song & Thakor, Citation2010). Thus, the study of Song and Thakor (Citation2010) regards the feedback loop between banks and markets based on securitisation and bank capital as co-evolution interaction.

For complementary interaction, the contributions of Allen and Gale (Citation2000) and Holmstrom and Tirole (Citation1997) provide suitable explanation. The model of Holmstrom and Tirole (Citation1997) considers firms and banks as capital constrained. As such, firms with adequate equity capital can directly access the market, whereas firms with less capital can borrow partly from both banks and markets. In this regard, banks require own capital to monitor borrowers and to enable borrowers obtain market finance. Thus, the ability of borrowers to access the markets is influenced by the presence of banks in a ‘one-way complementarily’ manner. The study of Allen and Gale (Citation2000) accentuates that banks may complement markets through provision of insurance against unanticipated contingencies to individuals. Thus, eradicating the acquisition of expensive information by individuals and reducing market participation costs. As such, ‘one-way complementarily’ arises as banks provide insurance to facilitate individual participation in markets.

Drawing from the literature of Song and Thakor (Citation2010), there have been various empirical attention on the interaction between banks and markets. For instance, the studies of Al-Nasser (Citation2015), Arize et al. (Citation2017), Babagana and Alom (Citation2018), Beck (Citation2010), Matadeen and Seetanah (Citation2015), Odhiambo (Citation2014), Osoro and Osano (Citation2014), and Sahoo (Citation2014) provide empirical evidence to support complementary and co-evolving interaction between banks and markets. On the other hand, empirical evidence on competition interaction emerge in studies of Marques et al. (Citation2013), Nyasha and Odhiambo (Citation2016, Citation2017a, Citation2017b). In a similar vein to causality views, empirical evidence regarding interaction between banks and markets on economic growth remains inconclusive.

In this line of reasoning, this study argues that the continuous contrary outcomes are attributable to the selection of different proxies over diverse time span in various countries. Under the influence of this argument, this study derives a germane stance for investigation. This paper concurrently contributes to existing empirical evidence on causality views on finance-growth nexus and interaction of banks and markets in influencing economic growth. Particularly, this study builds on the studies of Arize et al. (Citation2017) and Babagana and Alom (Citation2018) in Nigeria.

2.4. Banking in Nigeria

Banking in Nigeria has undergone different developments which have shaped the operational activities of banks in Nigeria. Such developments can be classified into different phases: free banking era (1892–1952), regulation era (1952–1986), deregulation era (1986–2004), consolidation era (2004–2009), and post-consolidation era (2009 to date). Banking operations in Nigeria began in the colonial administration with the establishment of African Banking Corporation (ABC) in 1892. In 1894, ABC was taken over by Bank of British West Africa (BBWA) (now First Bank of Nigeria Plc) and another foreign bank, Bank of Nigeria (formerly Anglo-African Bank) was established in 1899 by Royal Niger Company (First Bank of Nigeria [FBN], 2018).

In 1912, BBWA acquired Bank of Nigeria which was its first competitor; hence, BBWA remained the dominant bank in Nigeria till 1971 when Colonial Bank was established. In 1925, Barclays Bank DCO (Dominion, Colonial and Overseas) was created resulting from acquisition of Colonial Bank by Barclays Bank (Union Bank, Citation2020). In 1948, another foreign bank with the name; British and French Bank Limited (BFB) commenced operations in Nigeria (now UBA Plc).

The free banking era was characterised by free entry of banks into the Nigerian banking system as there was neither a banking regulator nor legislation. As such, the foreign banks during this era were registered, headquartered, and controlled from London which made them act solely in the interest of foreign owners rather than the Nigerian economy and its citizens (Brownbridge, Citation1996). In this regard, Nigeria established its first indigenous bank in 1929 called Industrial and Commercial Bank with the aim to tackle the dominance of foreign banks. However, this bank liquidated in 1930 resulting from embezzlement, accounting incompetence, mismanagement (Newlyn & Rowan, Citation1954), and inadequate support from foreign banks.

Thus, Mercantile Bank was established in 1931 and the bank failed in 1936. The first successful indigenous bank in Nigeria was National Bank of Nigeria, established in 1933. Additionally, African Continental Bank and the Nigerian Farmers and Commercial Bank were established in 1947. In line with the ongoing discussion, Mr. G.D Patron who was an official of the Bank of England (BoE) was appointed to investigate the dwindling state of Nigerian indigenous banks in 1948. This investigation led to the introduction of 1952 Nigerian Banking Ordinance with the aim to ensure smooth commercial banking and to avoid establishment of unprofitable banks in Nigeria.

The emanation of Nigerian Banking Ordinance in 1952 led to the commencement of banking regulation era in Nigeria. As such, banks had to satisfy stringent requirements before commencing operation in Nigeria. For instance, banks were required to obtain operating license before commencing banking activities. Also, banks were required to have minimum nominal share capital of £25,000 and £200,000 for indigenous and foreign banks, respectively, among others. However, the view of Barros and Caporale (Citation2012) asserts that the regulation appeared to have an insignificant impact on the conduct of banking activities as there was no regulator to ensure compliance. Hence, the legislation to establish the Central Bank of Nigeria (CBN) was presented to the House of Representatives in March 1958 (CBN, Citation2018); the CBN commenced full operations on 1 July 1959 with the responsibility of regulating and overseeing banking activities in Nigeria.

As such, the share capital of foreign banks was increased to £400,000 (Somoye, Citation2008), and the Banking Ordinance of 1952 with its different amendments transformed into Banking Decree 1969 as a constituted framework for the CBN in regulating banks (CBN, Citation2018). According to Uche (Citation2000), bank regulation during this period was supported by government support which prevented banks from failing; thus, activities in the banking sector were moderately steady. Following the assertion of Uche (2000), this study affirms that such government support was aimed at preventing systemic risk in the Nigerian banking industry as more indigenous banks were being introduced.

The Nigerian banking industry experienced a new phase with the introduction of Structural Adjustment Programme (SAP), a programme imposed on developing countries by the World Bank and the International Monetary Fund (IMF) in 1986. The emanation of SAP was experienced under the military regime of General Ibrahim Babangida with some of the bank control measures relaxed, such as interest rate regulation, entry restrictions, and sectoral allocation of credit quotas (Barros & Caporale, Citation2012). As such, there was increase in number of banks from 42 in 1986 to 120 in 1992, without a corresponding increase in supervisory and regulatory mechanisms (Oyejide, Citation1993) which led to disintermediation and systemic failure (Barros & Caporale, Citation2012).

In response to the wobbly state of the Nigerian banking system during this period, prudential measures were introduced by the government in 1991 through Banking and Other Financial Institutions Decree (BOFID), and issuance of licenses to new banks was put to a halt (Barros & Caporale, Citation2012; Hesse, Citation2007). Consequently, the number of banks in Nigeria reduced to 89 by 2004 which were characterised by poor asset quality, low capital base, insolvency, feeble corporate governance, and overdependence on foreign exchange trading and public sector deposits (Soludo, Citation2006).

Following the deteriorating state of Nigerian banks in 2004, the most remarkable banking phase in the country emerged. The consolidation era commenced with the increase of minimum capital base of banks from N2 billion to N25 billion by the end of December 2005. This was announced in July 2004 as part of the ‘13-point Reform Agenda’ aimed to reposition the CBN and the Nigerian financial system for the 21st century (Ailemen, Citation2010). As such, only banks that met the capital base requirement were issued banking license, mergers and acquisitions occurred among banks, while some banks liquidated. Thus, the banking industry recorded only twenty-five (25) banks after the capital base deadline from 89 before the consolidation.

According to Sanusi (Citation2010), the number of banks later reduced to twenty-four (24) through market-induced merger and acquisition. However, the eruption of the financial crisis in 2007/2008 necessitated another phase in the Nigerian banking industry in 2009. In line with the ongoing discussion, this study argues that the effect of the financial crisis would have contributed grave consequences on the Nigerian banking industry with the initial capital base requirement of N2 billion before consolidation. In this regard, accessing government support to prevent systemic risk would have been difficult as the government during this period relied heavily on reserves to revive the economy. Hence, the minimum capital base of N25 billion maintained by surviving banks during this period helped to reduce the effect of financial crisis on banks in Nigeria.

The post-consolidation phase commenced in June 2009 with the CBN introducing ‘The Project Alpha Initiative’ aimed to reform the Nigerian banking industry and the financial system after the 2007/2008 financial crisis. This commenced with diagnosis of the remaining twenty-four (24) banks using a three branched approach. According to Sanusi (Citation2010), the first approach involved a joint examination conducted by Nigerian Deposit Insurance Corporation (NDIC) and CBN, the investigation revealed that nine (9) out of the twenty-four (24) banks were in gross unstable situations. The second approach involved a diagnostic audit by independent consultants, the outcome of this further showed that the nine (9) banks had substantial negative asset value signifying technical insolvency. Accordingly, the CBN in collaboration with NDIC and Federal Ministry of Finance injected N620 billion into the nine (9) distressed banks.

Additionally, the Chief Executive Officers and Board of Directors of eight (8) out of the nine (9) banks were replaced with proficient managers to facilitate recovery (Sanusi, Citation2010). The third approach required a detailed and independent management account audit of the eight (8) banks with new management. Consequently, the new managers embarked on some actions with guidance of the CBN to improve operations and transparency. For instance, reduction in cost to income ratio, improvement of non-performing loans through loan ratios, de-leveraging and de-risking balance sheets, and liquidity management. In line with the ongoing discussion, ‘The Project Alpha Initiative’ of the CBN was based on four pillars: enhancing the quality of banks through risk-based supervision, establishing financial stability, enabling healthy financial sector evolution, and ensuring contribution of the financial sector on the economy.

With the continuation of the post-consolidation era in Nigeria, the banking sector recently experienced a new event as the licence of Skye Bank was revoked on 21 September 2018. Following the examination and forensic audit of Skye Bank by the CBN, the outcome revealed that Skye Bank required urgent recapitalisation. Thus, the CBN in consultation with the Nigeria Deposit Insurance Corporation (NDIC) established a bridge bank, Polaris Bank to take-over the activities of Skye Bank effective from 24 September 2018. The first intervention in this strategy was the injection of N786 billion into Polaris Bank by the Asset Management Company of Nigeria (AMCON). As of January 2022, there are twenty-two (22) commercial banks operating in Nigeria as shown in note 1 (CBN, Citation2022).

2.5. Capital markets in Nigeria

The history of financial markets in Nigeria can be traced back to the period of British colony. During this period, funds derived from the primary sector (agriculture, solid mineral mining and produce marketing) were insufficient to meet increasing financial obligations required to run local administration. As such, there was a need to expand revenue base by raising funds from the public sector which necessitated the emanation of Nigerian capital market. Particularly, the colonial government required additional funds to implement its 10-year infrastructural development and long-term capital projects. Consequently, there was floatation of £300,000 bonds by the colonial government in 1946 which gave birth to capital market in Nigeria.

On 15 September 1960, the Lagos Stock Exchange was incorporated as a private limited liability by guarantee under the provisions of the Lagos Stock Exchange Act 1960 (Esosa, Citation2007) to enhance trading on the Nigerian capital market. Informal operations commenced on 5 June 1961 with 19 listed securities which comprised of 10 industrial loans, six Government bonds, and three equities. However, formal operations later began on 25 August 1961. In 1977, the Lagos Stock Exchange was changed to Nigeria Stock Exchange (NSE) with several branches across the country. The NSE is licensed under the Investments and Securities Act (ISA) and is regulated by Securities and Exchange Commission (SEC) of Nigeria.

The NSE comprises of capital markets where long-term securities are traded. Intermediaries in the Nigerian capital markets comprises of corporate bodies and individuals who facilitate trading of securities. According to NSE (Citation2020), categories of securities listed on NSE include equities, exchange traded products, bonds and memorandum listings. As at 2020Q1, 359 securities were listed on the NSE with total market capitalization of N 25,513,173,485,365.50 (NSE, Citation2020). Additionally, as at 2020Q1, 59.82% domestic transactions occurred on the NSE, while foreign transactions were 40.18%.

2.6. Money markets in Nigeria

At pre-independence, the financial system in Nigeria was mostly owned by foreigners due to the lack of structured domestic markets in Nigeria. During this period, there was existence of a market linked to the London money market for the transfer of funds between London and Nigeria to finance export of farm produce (Afiemo, Citation2013). As such, there was a need to domicile funds travelling to Nigeria for potential investment and economic development. Consequently, the Nigerian money market was officially established in April 1960 with the issuance of the first CBN Treasury bill. In 1962, the CBN designated the Call Money Fund Market to allow participating institutions to keep surplus balances with the CBN temporarily. These idle balances were further invested in short-term money market instruments. Thus, the scheme provided investment opportunity for investors and served as a means for absorbing excess liquidity pressures in the money market (Afiemo, Citation2013).

The CBN further introduced the Finance Bill Scheme in 1962 as a source of finance for marketing boards to improve export of agricultural produce. In 1968, Treasury Certificates were issued for the first time to help bridge the loopholes in fiscal operations of the government as short-to-medium term securities. Between 1974 and 1976, other money market instruments, such as Certificates of Deposits (CDs), Bankers Unit Fund (BUF), and Special Deposits with the CBN were introduced. The increasing importance of money markets as a secondary market in Nigeria and its significance in the conduct of monetary policy was apparent in 1993, following implementation of Open Market Operations (OMO) using government securities.

As of January 2022, the regulatory and supervisory bodies on the Nigerian money market include CBN, NDIC, and Federal Ministry of Finance. Institutions in the Nigerian money market include Debt Management Office (DMO), Deposit Money Banks (DMBs), and discount houses (Afiemo, Citation2013). Additionally, money market instruments in Nigeria include Treasury Bills (TBs), Treasury Certificate (TC), Commercial Papers (CP), or Commercial Bills and Certificates of Deposits (CD) (CBN, 2013). Furthermore, the Nigerian money market consists of an inter-bank market as a sub-set of the market where banks and discount houses trade in unsecured money.

3. Empirical model and data

The empirical model of this study follows the simplified theoretical framework of Bagehot (Citation1873) and Schumpeter (Citation1911) to capture the role of banks in enhancing economic growth, and Arrow and Debreu (Citation1954) to capture the role of markets in fostering economic growth as expressed in EquationEquation (1)(1)

(1) :

(1)

(1)

where

t denotes the real gross domestic product,

t is bank-based proxies,

t is market-based proxies and

is the time period.

Based on theoretical underpinning, this study involves five variables- t is the real gross domestic product,

t is the value of money market instruments outstanding as at end-period,

t is the value of transactions at the Nigerian Stock Exchange,

t is the total subscriptions of treasury bills and aggregate loans and

t advances of commercial banks in Nigeria. All the variables are measured in million, Nigerian Naira (N Million). Thus, the empirical model for this study is expressed in EquationEquation (2)

(2)

(2) as:

(2)

(2)

Converting EquationEquation (2)(2)

(2) into an econometric model and taking logs, we have EquationEquation (3)

(3)

(3) :

(3)

(3)

where the parameter

is the intercept, the parameters

,….,

are the slope coefficients of the explanatory variables and

is the error term. We use annual data for

from the World Bank database, and data for all the explanatory variables from the Annual Statistical Bulletins of the Central Bank of Nigeria (CBN). The data span the period 1961–2018 with 58 observations.

reports key summary statistics for the variables under investigation in our model. The mean and the median values of all series are close together, indicating symmetrical distributions. The values of skewness and kurtosis are consistent with the small differences between the mean and median values. On the one hand, although skewness has positive and negative values for all variables, these values are close to zero. On the other hand, the kurtosis of all data series is platykurtic, <3.

Table 1. Descriptive statistics.

Distribution displays fewer and less extreme outliers than does the normal distribution. In addition, the normality test reported is based on Doornik and Hansen (Citation2008), instead of the commonly used Jarque-Bera (JB) test which is only appropriate in data with large number of observations. Doornik and Hansen’s (Citation2008) omnibus test for normality adjusts and controls well for sample size as low as 10 observations. Normality test indicates that normality is not rejected at 1% level for all variables, except for

4. Methodology and empirical results

4.1. Unit root tests

The empirical estimation of this study commences with unit root tests, which is essential to prevent spurious regression. As such, this study adopts Dickey-Fuller unit root test (Dickey & Fuller, Citation1979; Said & Dickey, Citation1984) and Phillips-Perron unit root test (Phillips & Perron, Citation1988). The DF unit root test is a parametric approach which solves serial correlation and heteroscedasticity in an error term, while the PP unit root test is a non-parametric approach that corrects serial correlation and heteroscedasticity by directly modifying the test statistics. The unit root test results in show that the variables are integrated processes of order one or I(1).

Table 2. Unit root test results.

4.2. Bounds testing approach

Under the influence of the seminal contribution of Pesaran et al. (Citation2001), this study adopts bounds testing approach to test for cointegration among the variables under investigation. According to Pesaran et al. (Citation2001), the approach is suitable whether the regressors are purely I(0), purely I(1), or mutually cointegrated, but not I(2). In this line of reasoning, this study pre-tests unit root to ensure that there are no I(2) variables in the model as shown in . As such, the unit root test results in validate the application of the bounds testing approach to test for cointegration among variables in the model. The Autoregressive Distributed Lag (ARDL) models used in this study are specified in EquationEquations (4a)–(4e) as:

(4a)

(4a)

(4b)

(4b)

(4c)

(4c)

(4d)

(4d)

(4e)

(4e)

where

and

remain as earlier defined; the symbol

is the first difference operator; the parameters

where

are short-run coefficients;

where

are long-run coefficients;

is the error term; m, n, o, p, and q are number of lags. The appropriate lag length is determined using Akaike information criterion (AIC). Hence, the lag length for the variables are 1, 0, 0, 3, and 0 for

and

respectively. As such, this study tests for cointegration among the variables using the hypotheses: H0:

=

=

=

=

= 0 (null: no co-integration or levels relationship), against H1:

≠

≠

≠

≠

≠ 0 (alternative: co-integration or levels relationship exists). This can also be denoted as:

\

The decision of the bounds testing approach is based on the null hypothesis that there exists no level relationship under two asymptotic critical values of I(0) and I(1). Thus, if the value of F-statistic is less than critical value for I(0) regressors, then the null hypothesis cannot be rejected. However, the null hypothesis can be rejected if F-statistic exceeds critical value for I(1) regressors, which implies existence of cointegration or levels relationship. Given the fairly small sample size in our study (58 observations), we consider the critical values of Narayan (Citation2004, Citation2005) for 30 observations to 80 observations. As such, the critical values of Pesaran and Pesaran (Citation1997), and Pesaran et al. (Citation2001) for 500 observations 1000 observations, respectively, are unsuitable for the sample size of our study. The bounds testing results for the model are shown in .

Table 3. Bounds testing approach results.

In the case of this study with I(1) regressors, we focus on upper bound critical values. As shown in , the F-statistic value, = 7.733 is greater than critical values for I(1) regressors at 1, 5, and 10% levels of significance. Thus, the null hypothesis of no cointegration or levels relationship is rejected. As such, the bounds testing results show that there is the existence of cointegration among real GDP, value of money market instruments outstanding as at end-period, value of transactions at the Nigerian Stock Exchange, total subscriptions of treasury bills and aggregate loans and advances of commercial banks in Nigeria.

Following the bounds testing results, this study adopts ARDL-error correction model (ECM) to examine long-run and short-run coefficients among the variables can be as specified as:

(5)

(5)

where λ is the parameter for speed of adjustment which measures the convergence of the variables towards equilibrium;

is lagged error correction term and

is the error term.

4.3. Long-run and short-run estimates

The long-run and short-run coefficients from the ECM model are shown in . The coefficient of error correction term or speed of adjustment towards equilibrium is −0.75 and statistically significant at 1% level. This denotes that disequilibrium among the variables in the previous year would converge to long-run equilibrium at a speed of 75% in the current year. For the short run, only coefficients of are shown in as

and

have lags of zero (0).

Table 4. Long-run and short-run estimates (dependent variable = ).

The short-run estimates show that has a statistically significant negative relationship with

at 5, 1, and 1% levels for lags 1, 2, and 3, respectively. As such, a 1% increase in

in the short run would decrease

in Nigeria by 0.09, 0.08, and 0.04% for lags 1, 2, and 3, respectively. In the long-run, there is a positive and statistically significant relationship between

and

As such, a 1% increase in

would increase

by 0.10% in Nigeria in the long run. However,

and

do not have significant positive relationship with

in the long run.

From , this study shows that total subscriptions of treasury bills have a statistically significant negative short-run and significant positive long-run relationship on economic growth in Nigeria. The short-run coefficients can be associated with high investment level of retail and institutional investors in Nigerian treasury bills, which concurrently reduces the available finance to boost short-run output in the economy. However, at maturity, individuals and institutional investors receive returns on investment which encourages spending and output in the long run. Additionally, the Nigerian government on issuance of treasury bills is expected to fund various projects with the debt obligation to boost output in the economy in the long run.

The empirical evidence in shows that treasury bills as a market-based proxy has significant relationships on economic growth in Nigeria at the detriment of other regressors. As such, based on the literature of Song and Thakor (Citation2010), this study finds evidence to support existence of competitive interaction between bank-based and market-based in Nigeria. Thus, this study argues that banks and markets in Nigeria are viewed in isolation, as they do not interact through securitisation and bank capital which contradicts the views of Allen and Gale (Citation2000) and Holmstrom and Tirole (Citation1997). Additionally, this study argues the postulation of Song and Thakor (Citation2010) that there is non-existence of feedback loop between banks and markets in Nigeria. In line with the foregoing discussion, the evidence of this study supports the studies of Marques et al. (Citation2013) and Nyasha and Odhiambo (Citation2016, Citation2017a, Citation2017b), for Kenya.

4.4. Granger causality tests

Further to the ECM results, this study conducts Granger causality tests to address the common phrase in statistics: ‘correlation does not imply causation’. Based on the existence of cointegrating relationship among the variables under investigation, this study conducts the VECM Granger causality framework and Wald test to examine long-run and short-run causality, respectively among the variables. The VECM Granger causality framework is specified as:

(6)

(6)

where

is the difference operator and

is lagged error correction term derived from the long-run equation. Thus, statistical significance of the coefficient for the

shows the long-run causality. Additionally, short-run causality is determined by the statistical significance of the joint chi-square values using Wald test. shows the outcome of the Granger causality tests. The Wald test results show that there is a unidirectional short-run causality running from

to

as the p-value is statistically significant at 5% level. However, none of the explanatory variables Granger causes

in the short run. On the other hand, the VECM Granger causality test results show a unidirectional long-run causality running from

to

and

to

as the p-values are statistically significant at 1 and 10% levels, respectively. In a similar vein to the short-run results, none of the explanatory variables Granger causes

in the long run.

Table 5. Granger causality test results.

The causality empirical evidence of this study supports the growth-led finance assertion of Robinson (Citation1952) and demand-following hypothesis of Patrick (Citation1966). In light of this evidence, this study argues that economic growth enhances financial sector development in Nigeria. Thus, on the one hand, the causality findings of this study argue against the finance-led growth postulation of Bagehot (Citation1873), Schumpeter (Citation1911), Goldsmith (Citation1969), McKinnon (Citation1973), and Shaw (Citation1973), and supply-leading hypothesis of Patrick (Citation1966). On the other hand, the causality findings of this study argue against the neutrality hypothesis of Lucas (Citation1988).

4.5. Diagnostic and model stability tests

shows the diagnostic tests of the model under investigation. The Breusch-Godfrey test shows a p-value of 0.9992, this denotes that the null hypothesis of ‘no serial correlation’ cannot be rejected as the p-value is not statistically significant. The result implies that there is no serial correlation in the residuals of the model. The White’s test with a p-value of 0.4856 examines the null hypothesis of homoscedasticity in the model. As such, the null hypothesis cannot be rejected as the p-value is not statistically significant. Hence, the test implies that the residuals of the model are homoscedastic or there is no heteroscedasticity in the model. From , the Breusch-Godfrey is further supported by Breusch-Pagan/Cook-Weisberg test to show that there is no heteroscedasticity in the model.

Table 6. Diagnostic tests.

Additionally, this study conducts Ramsey test to examine model misspecification for the null hypothesis of no omitted variables. From , the p-value of 0.4171 denotes that the null hypothesis cannot be rejected as the p-value is not statistically significant. As such, this further implies that the model of this study is well-specified with relevant variables. Furthermore, this study checks for multicollinearity among variables in the model using Variance Inflation Factor (VIF). From , the VIFs of the variables are not >10 and the mean VIF is >1. Following the assertion of Chatterjee and Hadi (Citation2012), this result implies that there is no multicollinearity among the variables in the model. By and large, the diagnostic results denote that the model under investigation is valid and reliable for prediction.

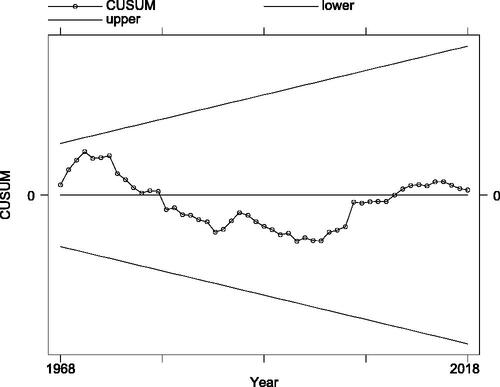

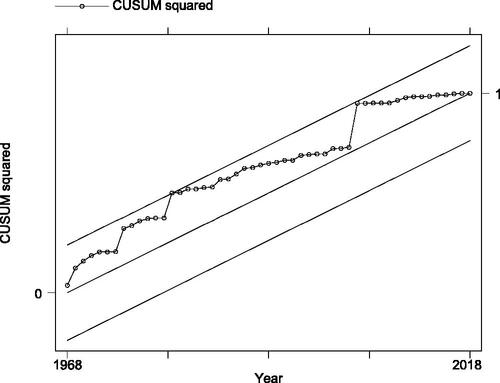

Under the influence of the seminal contribution of Brown et al. (Citation1975), this study examines stability of the model under investigation using cumulative sum of recursive residuals (CUSUM) and cumulative sum of squares of recursive residuals (CUSUMQ). From and , the plots of CUSUM and CUSUMQ statistics show that the residuals are within the critical boundaries at 5% significance level (represented by the straight lines). Hence, and imply that all coefficients in the ECM model are stable over the period under investigation.

Figure 1. Cumulative sum of recursive residuals (CUSUM) plot.

Source: Authors’ calculations.

Figure 2. Cumulative sum of squares of recursive residuals (CUSUMQ) plot.

Source: Authors’ calculations.

5. Conclusion and policy recommendations

This paper provides an empirical contribution to the debate on bank-based vs. market-based by considering proxies of capital market, money market, and banks in Nigeria. As such, this paper builds on the studies of Arize et al. (Citation2017), and Babagana and Alom (Citation2018) in Nigeria. The two key studies underpinning this study are finance-growth causality hypotheses of Patrick (Citation1966) and three-dimensional interactions between banks and markets of Song and Thakor (Citation2010).

Drawing on the literature of Patrick (Citation1966), the short-run causality results show the existence of unidirectional causality from P to

which supports demand-following hypothesis. This implies that economic growth in Nigeria has a short-run causal impact on value of transactions at the Nigerian Stock Exchange. Thus, investment activities of retail and institutional investors on the Nigerian Stock Exchange are caused by economic growth in Nigeria only in the short run. Additionally, the long-run causality results also support demand-following hypothesis of Patrick (Citation1966) due to existence of long-run unidirectional causality from

to

and

to

This implies that investment activities of retail and institutional investors in money market instruments and treasury bills are caused by economic growth in Nigeria in the long run.

In light of this evidence, this study further supports growth-led finance assertion of Robinson (Citation1952) as we argue that economic growth enhances financial sector development in Nigeria. Specifically, we argue that economic growth causes trading activities on Nigerian capital market while economic growth causes trading activities on money market in Nigeria. Thus, this study argue the finance-led growth postulation or supply-leading hypothesis, and neutrality hypothesis causality between finance and economic growth.

Based on the literature of Song and Thakor (Citation2010), our findings show that has short and long-run relationship on economic growth in Nigeria. Thus, we argue that markets and banks exhibit competitive interaction in favour of Nigerian money market. In this regard, our study opposes the studies of Arize et al. (Citation2017) and Babagana and Alom (Citation2018) which show complementary and co-evolving interaction between banks and markets in Nigeria. Based on our research findings, we further argue that the relevance of

on economic growth in Nigeria is due to the strong demand and oversubscription for treasury bills in Nigeria, while stringent bank lending practices among commercial banks has reduced the demand for bank loans. However, policy recommendations of this study will be based on causality findings between finance and growth rather than relationship.

Following the causality findings of this study, we argue that the role of banks and markets in enhancing economic growth in Nigeria is sloppy and ineffective. Thus, the CBN and other regulatory authorities in Nigeria should implement expansionary measures to boost the role of finance on growth in Nigeria. However, with inflation rate of 11.4% in 2019 (World Bank, Citation2019), such expansionary measures should be carefully implemented to prevent hyperinflationary pressures. For instance, expansionary monetary policy by the CBN which reduces interest rate or increases money supply through lowering reserve requirements will increase bank lending. Consequently, retail and institutional investors will be encouraged to borrow funds for investment purposes.

In this regard, banks and markets in Nigeria will tend to exhibit complementary and co-evolution dimensions rather than competitive as revealed in this study. In line with the reasoning of Oyebowale (Citation2019), this study further recommends the adoption of moral suasion by the CBN as a ‘watchdog’ of its expansionary policy measures. As such, Future research could focus on panel data consisting of some selected African countries to provide further investigation on the role of banks and markets within the continent.

Whilst this study provides valuable insights into the interaction of banks and markets on economic growth in Nigeria, the major limitation is data availability which restricted the authors to a time span of 1961–2018. Additionally, other proxies of banks and markets were considered during the research, however, the proxies are not included in the empirical model due to a lack of data. Further studies could extend our empirical model to other countries using panel data to examine the interaction between banks and markets on economic growth among countries in a selected region.

Markets and Banks.xlsx

Download MS Excel (12 KB)Acknowledgements

The authors are solely responsible for comments, suggestions, and views in this paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data for this study are available on request from the authors.

Additional information

Funding

Notes on contributors

Adeola Y. Oyebowale

Dr. Adeola Y. Oyebowale is a Senior Lecturer in Finance and Risk Management at Sheffield Business School, Sheffield Hallam University, UK. His research interests include time series analysis, finance-growth nexus, corporate finance, financial regulation, and portfolio analysis.

Amr S. Algarhi

Dr. Amr S. Algarhi is a Senior Lecturer in Economics at Sheffield Business School, Sheffield Hallam University, UK. His research interests are largely concentrated on applied econometrics, time series analysis, and macroeconomics. Amr specialises in financial econometrics and time series analysis, economic growth, economic policy, international economics, environmental economics, and governance.

Notes

1 The commercial banks in Nigeria as at January 2022 are Access Bank Plc, Citibank Nigeria Limited, Ecobank Nigeria Plc, Fidelity Bank Plc, First Bank Nigeria Limited, First City Monument Bank Plc, Globus Bank Limited, Guaranty Trust Bank Plc, Heritage Banking Company Ltd, Key Stone Bank, Polaris Bank, Providus Bank, Stanbic IBTC Bank Ltd, Standard Chartered Bank Nigeria Ltd, Sterling Bank Plc, SunTrust Bank Nigeria Limited, Titan Trust Bank Ltd, Union Bank of Nigeria Plc, United Bank for Africa Plc, Unity Bank Plc, Wema Bank Plc, Zenith Bank Plc (CBN, Citation2022).

References

- Afiemo, O. O. (2013). The Nigerian money market. The Central Bank of Nigeria, No. 27.

- Ailemen, I. (2010). Bank consolidation/capitalization in the Nigerian Commercial Bank (1986-2006): causes, consequences and implication for the future. Manager Journal, Faculty of Business and Administration, University of Bucharest, 12(1), 54–71.

- Ailemen, M., & Unemhilin, D. (2017). Impact of market-based financial structure on the growth of Nigerian economy: An econometric analysis. Economic Affairs, 62(2), 207–217. https://doi.org/10.5958/0976-4666.2017.00003.1

- Alexiou, C., Vogiazas, S., & Nellis, J. (2018). Reassessing the relationship between the financial sector and economic growth: Dynamic panel evidence. International Journal of Finance & Economics, 23(2), 155–173. https://doi.org/10.1002/ijfe.1609

- Allen, F., & Gale, D. (1999). Diversity of opinion and the financing of new technologies. Journal of Financial Intermediation, 8(1–2), 68–89. https://doi.org/10.1006/jfin.1999.0261

- Allen, F., & Gale, D. (2000). Comparing financial systems. MIT Press.

- Allen, F., & Santomero, A. (1997). The theory of financial intermediation. Journal of Banking & Finance, 21(11–12), 1461–1485. https://doi.org/10.1016/S0378-4266(97)00032-0

- Al-Nasser, O. (2015). Stock markets, banks and economic growth: Evidence from Latin American countries. International Journal of Economics and Finance, 7(2), 100–112.

- Arize, A., Kalu, E., & Nkwor, N. (2017). Banks versus markets: Do they compete, complement or co-evolve in the Nigerian financial system? An ARDL approach. Research in International Business and Finance, 45, 427–434. https://doi.org/10.1016/j.ribaf.2017.07.174

- Arrow, K., & Debreu, G. (1954). Existence of an equilibrum for a competitive economy. Econometrica, 22(3), 265–290. https://doi.org/10.2307/1907353

- Azam, M., Haseeb, M., Samsi, A., & Raji, J. (2016). Stock market development and economic growth: Evidences from Asia-4 countries. International Journal of Economics and Financial Issues, 6(3), 1200–1208.

- Babagana, A., & Alom, F. (2018). Financial structure and economic growth nexus in Nigeria. Institutions and Economies, 10(1), 111–136.

- Bagehot, W. (1873). Lombard street: A description of the money market. E.P Dutton and Company.

- Barros, C., & Caporale, G. (2012). Banking consolidation in Nigeria, 2000–2010. Mais Working Papers CEsA Disponiveis em, 99, 1–19.

- Beck, T. (2010). Financial development and economic growth: Stock markets versus banks? Africa’s Financial Markets: A Real Development Tool, No. 5.

- Boot, A., & Thakor, A. (1997). Financial system architecture. Review of Financial Studies, 10(3), 693–733. https://doi.org/10.1093/rfs/10.3.693

- Brown, R., Durbin, J., & Evans, J. (1975). Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society Series B: Statistical Methodology, 37(2), 149–163. https://doi.org/10.1111/j.2517-6161.1975.tb01532.x

- Brownbridge, M. (1996). The impact of public policy on the banking system in Nigeria. Institute of Development Studies Working Paper Issue 31. https://www.ids.ac.uk/publications/the-impact-of-public-policy-on-the-banking-system-in-nigeria/.

- CBN (2018). CBN educational resources. Retrieved September 23, 2020, from https://www.cbn.gov.ng/Educational.asp

- CBN. (2007). Banks and other financial institutions Act 1991. https://www.cbn.gov.ng/out/publications/bsd/1991/bofia.PDF.

- CBN (2022). List of financial institutions – commercial banks. Retrieved January 1, 2022, from https://www.cbn.gov.ng/Supervision/Inst-DM.asp

- Chatterjee, S., & Hadi, S. (2012). Regression analysis by example (5th ed.). John Wiley & Sons, Inc.

- Dewatripont, M., & Maskin, E. (1995). Credit and efficiency in centralized and decentralized economies. Review of Economic Studies, 62(4), 541–555.

- Deyshappriya, N. P. (2016). The causality direction of the stock market-growth nexus: Application of GMM dynamic panel data and the panel Granger non-causality tests. Margin-The. Journal of Applied Economic Research, 10(4), 446–464.

- Diamond, D. (1984). Financial intermediation and delegated monitoring. Review of Economic Studies, 51(3), 393–414.

- Dickey, D., & Fuller, W. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366), 427–431. https://doi.org/10.2307/2286348

- Doornik, J., & Hansen, H. (2008). An omnibus test for univariate and multivariate normality. Oxford Bulletin of Economics and Statistics, 70(s1), 927–939. https://doi.org/10.1111/j.1468-0084.2008.00537.x

- Esosa, B. (2007). Capital markets: African and global. Bookhouse Company.

- Fama, E. (1980). Banking in the theory of finance. Journal of Monetary Economics, 6(1), 39–57. https://doi.org/10.1016/0304-3932(80)90017-3

- Fu, X., Lin, Y., & Molyneux, P. (2018). The quality and quantity of bank intermediation and economic growth: Evidence from Asia Pacific. Applied Economics, 50(41), 4427–4446. https://doi.org/10.1080/00036846.2018.1450486

- Fufa, T., & Kim, J. (2017). Stock markets, banks and economic growth: Evidence from more homogenous panels. Research in International Business and Finance, 44, 504–517. https://doi.org/10.1016/j.ribaf.2017.07.120

- Goldsmith, R. (1969). Financial structure and development. Yale University Press.

- Hao, C. (2006). Development of financial intermediation and economic growth: The Chinese experience. China Economic Review, 17(4), 347–362. https://doi.org/10.1016/j.chieco.2006.01.001

- Hesse, H. (2007). Financial intermediation in the pre-consolidated banking sector in Nigeria. Working Paper. World Bank.

- Holmstrom, B., & Tirole, J. (1997). Financial intermediation, loanable funds and the real sector. Quarterly Journal of Economics, 112(3), 663–691.

- Klein, M. (1971). A theory of the banking firm. Journal of Money, Credit and Banking, 3(2), 205–218. https://doi.org/10.2307/1991279

- Korkmaz, S. (2015). Impact of bank credits on economic growth and inflation. Journal of Applied Finance and Banking, 5(1), 51–63.

- Lazarov, D., Miteva-Kacarski, E., & Nikoloski, K. (2016). An empirical analysis of stock market development and economic growth: The case of Macedonia. South East European Journal of Economics and Business, 11(2), 71–81. https://doi.org/10.1515/jeb-2016-0012

- Lee, B. (2012). Bank-based and market-based financial systems: time-series evidence. Pacific-Basin Finance Journal, 20(2), 173–197. https://doi.org/10.1016/j.pacfin.2011.07.006

- Levine, R. (2004). Finance and growth: Theory and evidence. National Bureau of Economic Research.

- Levine, R., & Zervos, S. (1998). Stock markets, banks and economic growth. American Economic Review, 88(3), 537–558.

- Liang, H., & Reichert, A. (2012). The impact of banks and non-bank financial institutions on economic growth. The Service Industries Journal, 32(5), 699–717. https://doi.org/10.1080/02642069.2010.529437

- Lucas, R. (1988). On the mechanisms of economic development. Journal of Monetary Economics, 22(1), 3–42. https://doi.org/10.1016/0304-3932(88)90168-7

- Mahran, H. (2012). Financial intermediation and economic growth in Saudi-Arabia: An empirical analysis, 1968–2010. Modern Economy, 3(5), 626–640. https://doi.org/10.4236/me.2012.35082

- Mamman, A., & Hashim, Y. (2014). Impact of bank lending on economic growth in Nigeria. Research Journal of Finance and Accounting, 5(18), 174–182.

- Marques, L., Fuinhas, J., & Marques, A. (2013). Does the stock market cause economic growth? Portugese evidence of economic regime change. Economic Modelling, 32, 316–324. https://doi.org/10.1016/j.econmod.2013.02.015

- Matadeen, J., & Seetanah, B. (2015). Stock market development and economic growth: Evidence from Mauritius. The Journal of Developing Areas, 49(6), 25–36. https://doi.org/10.1353/jda.2015.0120

- McKinnon, R. (1973). Money and capital in economic development. The Brookings Institution.

- Narayan, P. K. (2004). Reformulating critical values for the bounds F-statistics approach to cointegration: An application to the tourism demand model for Fiji. Department of Economics Discussion Papers No. 02/04, Monash University, Melbourne, Australia.

- Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. https://doi.org/10.1080/00036840500278103

- Newlyn, W., & Rowan, D. (1954). Money & banking in British colonial Africa. Oxford @ Clarendon Press.

- Ngare, E., Nyamongo, E., & Misati, R. (2014). Stock market development and economic growth in Africa. Journal of Economics and Business, 74, 24–39. https://doi.org/10.1016/j.jeconbus.2014.03.002

- NSE (2020). NSE Q1 2020 fact sheet. Retrieved August 2, 2020, from https://www.nse.com.ng/market_data-site/other-market-information-site/NSE%20Fact%20Sheet/Q1%20Fact%20Sheet%202020.pdf

- Nyasha, S., & Odhiambo, N. (2016). Financial systems and economic growth: Empirical evidence from Australia. Contemporary Economics, 10(2), 163–174. https://doi.org/10.5709/ce.1897-9254.207

- Nyasha, S., & Odhiambo, N. (2017a). Are banks and stock markets complements or substitutes? Empirical evidence from three countries. Managing Global Transitions, 15(1), 81–101. https://doi.org/10.26493/1854-6935.15.81-101

- Nyasha, S., & Odhiambo, N. (2017b). Bank versus stock market development in Brazil: An ARDL bounds testing technique. South East European Journal of Economics and Business, 12(1), 7–21. https://doi.org/10.1515/jeb-2017-0001

- Odedokun, M. (1996). Alternative econometric approaches for analysing the role of the financial sector in economic growth: Time-series evidence from LDCs. Journal of Development Economics, 50(1), 119–146. https://doi.org/10.1016/0304-3878(96)00006-5

- Odedokun, M. (1998). Financial intermediation and economic growth in developing countries. Journal of Economic Studies, 25(3), 203–224. https://doi.org/10.1108/01443589810215351

- Odhiambo, N. (2014). Financial systems and economic growth in South Africa: a dynamic complementarity test. International Review of Applied Economics, 28(1), 83–101. https://doi.org/10.1080/02692171.2013.828681

- Osoro, J., & Osano, E. (2014). Bank-based versus market-based financial system: Does evidence justify the dichotomy in the context of Kenya? Kenya Bankers Association Centre for Research on Financial Markets and Policy.

- Oyejide, T. (1993). Effects of trade and macroeconomic policies on African agriculture. In R. Bautista & A. Valdes (Eds.), The bias against agriculture: Trade and macroeconomic policies in developing countries (pp. 241–262). Institute for Contemporary Studies Press.

- Oyebowale, A. Y. (2019). Determinants of bank lending in Nigeria. Global Journal of Emerging Market Economies, 12(3), 378–398. https://doi.org/10.1177/0974910120961573

- Pan, L., & Mishra, V. (2018). Stock market development and economic growth: Empirical evidence from China. Economic Modelling, 68, 661–673. https://doi.org/10.1016/j.econmod.2017.07.005

- Patrick, H. (1966). Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change, 14(2), 174–189. https://doi.org/10.1086/450153

- Pesaran, M., & Pesaran, B. (1997). Working with Microfit 4.0: Interactive econometric analysis. Oxford University Press.

- Pesaran, M., Shin, Y., & Smith, R. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Phillips, P., & Perron, P. (1988). Testing for a unit root in times series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Pradhan, R. (2018). Development of stock market and economic growth; The G-20 evidence. Eurasian Economic Review, 8(2), 161–181. https://doi.org/10.1007/s40822-018-0094-4

- Robinson, J. (1952). The generalization of the general theory, the rate of interest and other essays. Macmillan.

- Sahoo, S. (2014). Financial intermediation and growth: Bank-based versus market-based systems. The Journal of Applied Economic Research, 8(2), 93–114.

- Said, S. E., & Dickey, D. A. (1984). Testing for unit roots in autoregressive moving-average models with unknown order. Biometrika, 71(3), 599–607. https://doi.org/10.1093/biomet/71.3.599

- Sanusi, L. (2010). Global financial meltdown and the reforms in the Nigerian banking sector. Retrieved August 25, 2020, from https://www.bis.org/review/r110124c.pdf

- Scholtens, B., & Wensveen, D. (2000). A critique on the theory of financial intermediation. Journal of Banking & Finance, 24(8), 1243–1251. https://doi.org/10.1016/S0378-4266(99)00085-0

- Scholtens, B., & Wensveen, D. (2003). The theory of financial intermediation: An essay on what it does (not) explain. No. 2003/1 SUERF Studies, The European Money and Finance Forum.

- Schumpeter, J. (1911). The theory of economic development. Harvard University Press.

- Shaw, E. (1973). Financial deepening in economic development. Oxford University Press.

- Soludo, C. (2006). Beyond banking sector consolidation in Nigeria. Paper presented at the 12th Annual Nigerian Economic Summit, Transcorp Hilton, Abuja, Nigeria.

- Somoye, R. (2008). The performances of commercial banks in post-consolidation period in Nigeria: An empirical review. European Journal of Economics, Finance and Administrative Sciences, 14(1), 62–73.

- Song, F., & Thakor, A. (2010). Financial system architecture and the co-evolution of banks and capital markets. The Economic Journal, 120(547), 1021–1055. https://doi.org/10.1111/j.1468-0297.2009.02345.x

- Uche, C. (2000). Banking regulation in an era of structural adjustment: The case of Nigeria. Journal of Financial Regulation and Compliance, 8(2), 157–159. https://doi.org/10.1108/eb025040

- Union Bank (2020). History. Retrieved August 3, 2020, from https://www.unionbankng.com/about/history/

- World Bank (2019). Inflation-consumer prices (annual %)-Nigeria. Retrieved August 3, 2020, from https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG?locations=NG

- Xu, H. (2016). Financial intermediation and economic growth in China: New evidence from panel data. Emerging Markets, Finance and Trade, 52(3), 724–732.