?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Corruption within corporate entities continues to be a relatively overlooked yet significant issue to date. This study seeks to investigate the impact of corruption on the quality of earnings. The sample comprises 846 firm-years listed on the Indonesian Stock Exchange. Earnings quality encompasses factors such as earnings persistence, earnings value relevance, and earnings predictability. Corruption is gauged by the corruption per capita in the region where the firms are headquartered. The data analysis employs regression models incorporating firm and province effects. Broadly, the findings of this study indicate that corruption diminishes earnings quality. Heightened corruption is associated with weakened controlling and monitoring functions, increased information asymmetry, and diminished managerial quality, all contributing to a decline in earnings quality. This research not only expands upon previous studies but also reaffirms the relevance of the social capital concept while presenting new empirical evidence within a context of a country with a higher corruption perception index, such as Indonesia.

IMPACT STATEMENT

The relationship between corruption and earnings quality becomes a new insight for public. Regulator and society can maintain the good norm and value to reduce the bad impact of corruption into social capital. Indonesia has an increasing corruption perception so regulator, society, and business participants can improve the controlling and monitoring function to avoid misbehavior. Specifically, business participants can avoid misbehavior of report the lower quality earnings. It is new evidence in Indonesia and expected to be a consideration to formulate public and business policy in Indonesia

1. Introduction

The primary objective of this study is to assess the impact of corruption on earnings quality. Unlike previous studies, which predominantly examined the influence of corruption on earnings quality at the national level and conducted cross-country analyses by considering law and regulation violations (El-Helaly et al., Citation2020; Lei & Wang, Citation2019; Lourenço et al., Citation2018; Mamatzakis & Bagntasarian, Citation2022), this study focuses on the Indonesian context. Specifically, the relationship between corruption and earnings quality in Indonesia has traditionally been explored through an analysis of anti-corruption disclosures. In contrast to these earlier studies, this study uniquely delves into the impact of corruption at the local level on firms’ earnings quality. This is achieved by incorporating social capital as the principal mechanism that influences managerial behavior within firms (Cho et al., Citation2020; Jha, Citation2019). Social capital posits that corruption at the local level, where firms are headquartered, shapes social norms and values through interactions with local government institutions and is subsequently absorbed into the corporate culture of these firms.

There are some studies that find the relationship between corruption and corporate reporting. Lewellyn and Bao (Citation2017) examine the national-level corruption on earnings management globally and find corruption increases earnings management. Sousa et al. (Citation2023) find inconsistent relationship between corruption and earnings management in Latin American, North America, and Caribbean. Chen et al. (Citation2020), Hope et al. (Citation2020), and Xu et al. (Citation2019) find the relationship between corruption and reporting quality in China. Previous studies examine the relationship between corruption and corporate reporting in the context of lower diversity of cultures. Since corruption can affect reporting behavior by culture absorption, it is important to examine the relationship between corruption and corporate reporting in the context of higher diversity of cultures such as Indonesia. Different with Latin American, North America, Caribbean, and China; there are a lot diversity from culture, ethnicity, religion, to sects of belief in Indonesia that can be absorbed as corporate culture for firms (Christy et al., Citation2022; Supriatna et al., Citation2023). In this case, it is important to examine the local corruption level in the Indonesian provinces on earnings quality since each province has different social capital belief and norm that can be absorbed by firms.

In contrast, Lourenço et al. (Citation2018) suggest that corruption, which promotes a society’s misbehavior, can be prevented by firms. One solution for firms that do not absorb corrupt behavior is to have effective corporate governance (Boateng et al., Citation2021). Hofmann and Schwaiger (Citation2020) suggest that lower social capital has two impacts on firms: misbehavior by managers and firms with better corporate governance mechanisms. In this case, earnings quality can still be improved if firms in a corrupt society have good corporate governance (Asogwa et al., Citation2019; Hashmi et al., Citation2022; Lustrilanang et al., Citation2023). Furthermore, corporate governance helps firms maintain earnings quality and achieve firm stability (Thoha et al., Citation2022). Some studies have found that corporate governance, such as CEO characteristics, can improve financial reporting (Zalata et al., Citation2019a, Citation2019b, Citation2022).

This study makes several contributions. First, it extends the relationship between corruption and earnings quality, where previous studies (El-Helaly et al., Citation2020; Lei & Wang, Citation2019; Lourenço et al., Citation2018; Mamatzakis & Bagntasarian, Citation2022) do not capture social capital in the location where firms are headquartered. Second, this study contributes to the literature by providing evidence that corrupted social capital can affect firms’ culture and managers’ behavior in reporting lower-quality earnings. Third, this study contributes to extending the effect of corruption on earnings attributes. Some studies have examined the effect of corruption on earnings attributes of accrual quality (Y. Chen et al., Citation2020; Picur, Citation2004), classification shifting (Lei & Wang, Citation2019), accrual earnings management (Lourenço et al., Citation2018; A. H. Nguyen & Duong, Citation2020; H. Xu et al., Citation2019), real earnings management (H. Xu et al., Citation2019), and earnings smoothing (Picur, Citation2004). This study provides evidence of earnings attribute quality, especially the attributes of earnings persistence, value relevance, and predictability. Fourth, this study provides new evidence of corruption and earnings quality in Indonesia, where the corruption perception index continues to increase.

Earnings quality is an important issue because there are some earnings manipulation and misstatement cases that lead to earnings becoming invalid information. In 2018, PT Garuda Indonesia boosted their earnings to USD 809.85 thousand by recognizing a 15 years contract value as current revenue all at once (Uly, Citation2019). Earnings manipulation and misstatements fail to provide high-quality information to users.

In this study, earnings quality includes persistence, value relevance, and predictability. Earnings persistence is important to users of information and decision-makers by showing them that earnings are persistent, sustained, and stable. Persistent earnings show that firms can consistently maintain their business processes and recur in the future (Aharony et al., Citation2000; C. J. P. Chen et al., Citation2001; Graham & King, Citation2000). In the performance evaluation context, earnings persistence provides information on management’s ability to maintain their performance more consistently from time to time. In the performance prediction context, earnings persistence helps decision makers predict future performance more accurately because persistent earnings provide sustainability information features (Collins et al., Citation1994). When earnings are persistent and can be used to predict future performance, it is relevant to make decisions. Earnings persistence, value relevance, and predictability complement each other to provide high-quality earnings information. Since managers’ incentives can be affected by market and political forces, managers can determine accounting, including earnings and information quality, by considering the conditions of the market and political environment (Ball et al., Citation2003).

This study examines the effect of corruption on the earnings quality of manufacturing firms on the Indonesian Stock Exchange. Earnings quality includes persistence, value relevance, and predictability. Hu et al. (Citation2023) explained that most corruption and bribery occur in the supply chain process by manufacturing firms. In Indonesia, manufacturing firms such as PT Krakatau Steel and PT Grand Kartech in 2019 were corruption cases (Kompas.Com, Citation2019).

2. Background

Political force can provide managers with incentives related to cash holdings, investments, and stock prices (Fan et al., Citation2008; Jens, Citation2017; Wu et al., Citation2012; N. Xu et al., Citation2016). Local corruption is a political factor. Corruption refers to the abuse of power to gain private benefit (Cuervo-Cazurra, Citation2016).

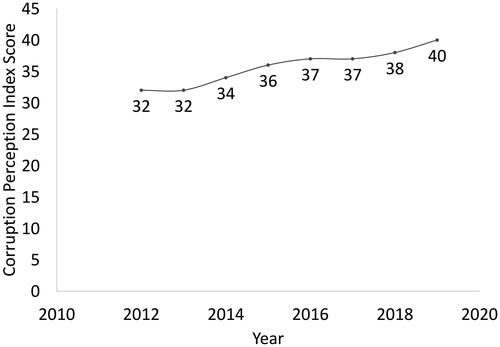

shows that Indonesia had a growing corruption perception index score from Indonesia to 2012–2019. The corruption perception index represents how corrupt the country is. A higher corruption perception index indicates a higher level of corruption in the bureaucracy of a country (Setyobudi & Setyaningrum, Citation2019). This indicates that Indonesia experienced a higher level of corruption in the last eight years.

Corruption has an impact on earnings quality. First, higher political corruption reflects lower regulation implementation, law enforcement, (Seligson, Citation2002) and poor government effectiveness (Friedman et al., Citation2000). This leads managers to be less concerned about the litigation risk of earnings manipulations (H. Xu et al., Citation2019). Boonlert-U-Thai et al. (Citation2006) explain that lower regulations and law enforcement lead to lower earnings information quality. Second, the secret illegal movement characteristic causes corruption, resulting in higher information asymmetry (Chaney et al., Citation2011). Third, since managers tend to have lower quality when surrounded by a politically corrupt culture (Athanasouli & Goujard, Citation2015), lower-quality managers fail to maintain earnings quality (Demerjian et al., Citation2013; Simamora, Citation2021).

3. Theoretical literature review

3.1. Corruption

Corruption is defined as the abuse of power to gain private benefits (Cuervo-Cazurra, Citation2016). Specifically, it refers to a criminal act in public government offices (Shleifer & Vishny, Citation1993). It becomes a culture for local individuals in a certain region, where corruption allows them to believe that the abuse of power is common and acceptable (DeBacker et al., Citation2015; Fisman & Miguel, Citation2007). These individuals then join firms while bringing about beliefs in unethical behavior, such as corruption (Liu, Citation2016). Pricewaterhouse Coopers (Citation2016) explains that corruption leads firms to bear the costs of law violations and have a bad reputation. Smith (Citation2016) suggested that firms in regions with higher corruption have different financial policies than those in less corrupt regions. Since corruption is identical to misbehavior in public government offices, it is often associated with political connections and forces (Y. Chen et al., Citation2020). Chaney et al. (Citation2011) found that firms’ political connections reduce their earnings quality. Hope et al. (Citation2020) found that directors who have a position in government offices have an impact on information transparency. Zhang (Citation2018) also found that corruption reduction decreases firms’ fraud. In 2020, Indonesia ranked 102nd based on the corruption perception index from a total of 180 countries (Transparency International, Citation2021). The Indonesian corruption perception index still increased from 2015 to 2019 due to the rise in political risk and the decline in law enforcement (Komisi Pemberantasan Korupsi, Citation2020).

3.2. How corruption affects corporate managers’ behavior: the concept of social capital

Social capital collectively explains the characteristics of people’s behavior in the same social group (Adler & Kwon, Citation2002; Woolcock, Citation2001). Social capital provides a norm in a specific region that promotes how people treat one another, especially in the context of the values of obligation, mutual trust, and a dense network to generate effective oversight (Jha, Citation2019). Regarding corporate activities, the values of the norm in a specific region of society where the firms are headquartered also matter (Fukuyama, Citation1995), especially to determine how firms’ managers will behave (James S. Coleman, Citation1990; Spagnolo, Citation1999).

Social capital impacts organizational actions, including financial reporting. Solomon (Citation2004) explains that people tend to consider ethical values in society when deciding on business decisions. Since firms’ culture and norms sync with the regional social norms where the firms are headquartered, managers tend to consider similar norms when they make a strategy for financial reporting (Cho et al., Citation2020; Jha, Citation2019). Jha (Citation2019) formulated the relationship between social capital and financial reporting, where better social capital brings specific norms to organizational culture.

Corruption is an indicator of social capital value. As part of society, government institutions also contribute to social capital. Corrupted government institutions can also contribute to the corrupt behavior of other members of society, including the community and firms. By interacting with society, government institutions can promote corrupt behavior in communities and firm managers. Corruption encourages society members to have lower levels of trust (Andriani, Citation2021; Banerjee, Citation2016), legal violations (Andriani, Citation2021; Bondeli et al., Citation2021), and fraud (Banerjee, Citation2016).

In the context of firms’ managers’ behavior, corruption affects managers’ behavior to perform fraudulent actions, including financial reporting, which can reduce earnings quality. There is some argument as to why corrupt social capital reduces earnings quality. Controlling and monitoring functions play important roles in maintaining earnings quality (Gaio & Raposo, Citation2011). Since firms are active responders to regulation and law dynamics (Galang, Citation2012), there is a possibility that they tend to absorb corruption culture into the organization and their managers (Y. Chen et al., Citation2020). Second, lower earnings quality can result from higher information asymmetry (H. Xu et al., Citation2019) because corruption has the characteristic of secret moves, which leads to information asymmetry (Chaney et al., Citation2011). Third, managers tend to be of lower quality in regions with higher levels of corruption (Athanasouli & Goujard, Citation2015). A corruption culture allows managers to do bribes to regulators of business contracts and benefits (H. Xu et al., Citation2019). Lower-quality managers tend to manipulate earnings because they fail to improve performance (Picur, Citation2004; Simamora, Citation2021).

3.3. Agency theory

Agency theory explains the relationship between managers and owners, especially the agency conflict that happens between managers and owners (Jensen & Meckling, Citation1976). Agency conflict occurs when managers fulfill more their interests than owners’ interests. Agency conflict can be manifested in lower earnings quality. Lower earnings quality comes from the condition of information asymmetry where managers have more information about firms’ activities than owners. Owners’ interests of higher information quality cannot be fulfilled when there is information asymmetry (Islam et al., Citation2022).

Corruption in the region where firms are headquartered enhances the condition of higher information asymmetry. First, corruption captures higher hidden transactions which indicates higher information asymmetry (Chaney et al., Citation2011). Second, corruption also is an indicator of ineffective governance since weaker law and regulation implementation occur (Seligson, Citation2002). Nguyen and Truong (Citation2022) explain that information asymmetry cannot be mitigated if there is no effective governance implementation.

3.4. Framework of theory

Framework of theory is the framework that explain the use of the theory in the context of the research. In this case, framework of theory explains how the concept of social capital and agency theory capture the relationship between corruption and earnings quality. The framework of theory can be seen in .

Figure 1. Corruption perception index score in Indonesia.

Figure 2. Framework of theory.

shows that corruption is external condition. Corruption promotes information asymmetry (secret moves) and ineffective governance (weak law and regulation enforcement). In this case, corruption becomes social capital that is also absorbed by firms’ managers. Firms’ managers have behavior that relate to corruption behavior. Since there is a conflict between managers and owners, managers fulfill their interests and avoid owners’ interests by performing corrupted behavior under internal conditions of information asymmetry and ineffective governance. The result of corrupted managers’ behavior is lower earnings quality.

4. Empirical literature review and hypothesis development

4.1. Corruption and earnings quality

Corruption captures the condition of the information environment and impacts information quality, including earnings quality. First, corruption promotes lower regulations and law enforcement (Seligson, Citation2002). Corruption shows poor governmental effectiveness (Friedman et al., Citation2000). Regulation and law enforcement are important for determining the effectiveness of controlling and monitoring functions. Controlling and monitoring functions play important roles in maintaining earnings quality (Gaio & Raposo, Citation2011). Since firms are active responders to regulation and law dynamics (Galang, Citation2012), there is a possibility that they tend to absorb corruption culture into the organization and their managers (Y. Chen et al., Citation2020). In this case, firms are less obedient to the law and regulations (Shleifer & Vishny, Citation1993), and are less concerned about litigation risk (H. Xu et al., Citation2019). Lower regulations and law enforcement lead to higher earnings manipulation (H. Xu et al., Citation2019) and lower earnings quality (Boonlert-U-Thai et al., Citation2006).

Second, lower earnings quality can result from higher information asymmetry (H. Xu et al., Citation2019) because corruption has the characteristic of secret moves, which leads to information asymmetry (Chaney et al., Citation2011). Information asymmetry captures information risk and uncertainty (Deakins & Hussain, Citation1994). Chaney et al. (Citation2011) also found that regions with higher political corruption provide higher information risk and uncertainty due to lower financial reporting quality.

Third, managers tend to be of lower quality in regions with higher levels of corruption (Athanasouli & Goujard, Citation2015). A corruption culture allows managers to do bribes to regulators of business contracts and benefits (H. Xu et al., Citation2019). This shows that managers fail to implement an effective and efficient managerial function because they use bribes rather than other lawful alternative strategies. Lower-quality managers tend to manipulate earnings because they fail to improve performance (Picur, Citation2004; Simamora, Citation2021). Demerjian et al. (Citation2013) and Simamora (Citation2021) found that lower-quality managers lead to lower earnings quality.

Earnings quality refers to the ability of earnings information to inform a firm of its condition (Menicucci, Citation2020; Schipper & Vincent, Citation2003). Based on agency theory, the lower controlling and monitoring functions provided by corruption cultures fail to reduce agency conflict and information asymmetry, leading to lower earnings quality. The types of earnings quality depend on the context and earnings information users (Menicucci, Citation2020). In this study, earnings quality includes persistence, value relevance, and predictability.

Damijan (Citation2023) explained the concept of corruption. In the early stage, corruption was defined as the abuse of power by the government because the government has greater power than other institutions, including law and regulation violations. Damijan (Citation2023) also explains that the corruption definition was developed in the 19th century as a systematic process to use privileges for private benefits. In the 20th century, corruption not only covered the government’s behavior but also individuals, including private organizations (Damijan, Citation2023). Based on the definition of corruption, the corruption concept is initiated from the abuse of power by government institutions, and it also applies to individuals in private organizations, including firms’ managers. Firms’ managers can be corrupted by breaking laws or abusing their powers. In the concept of social capital, corrupted firm managers come from the social norms around firms that have been absorbed, leading managers to report lower-quality earnings.

4.2. Hypotheses

Earnings persistence refers to the ability of earnings to recur (Francis et al., Citation2004). This also shows the relationship between current and future earnings. Earnings persistence evaluates how persistent, sustained, and consistent the earnings are. Earnings persistence is useful in predicting future earnings using current earnings information. Earnings persistence can be reduced if firms face higher levels of uncertainty. This uncertainty makes it difficult for firms to engage in persistent and sustainable business activities (Canina & Potter, Citation2019). The risk of business uncertainty can be attributed to the culture of organizational corruption. As corruption promotes weaker regulation implementation and law enforcement, firms will absorb it by implementing weaker monitoring and controlling functions. Strict monitoring and controlling functions are needed to ensure persistent and sustainable business activities. Weaker monitoring and controlling functions lead firms to fail in mitigating uncertain business conditions and unpredictable events. Eldridge et al. (Citation2013) found that a control system was related to uncertainty mitigation. Lower earnings persistence also comes from lower manager ability (Demerjian et al., Citation2013; Simamora, Citation2021), especially in corrupt regions, since most lower-ability managers are in regions with higher corruption levels (Athanasouli & Goujard, Citation2015).

H1: Corruption reduces earnings persistence

Earnings value relevance refers to the relevance of earnings to be used in decision making. In the stock market context, decision making occurs when investors use earnings information to make stock investment decisions (Francis et al., Citation2004). Investors’ decisions are reflected in stock returns, which are represented as the earnings response coefficient (Collins et al., Citation1994). The negative responses of investors to earnings information show that earnings are less relevant to decision-making. Lower earnings relevance comes from firms that absorb corrupt culture into their organizations. Cao et al. (Citation2019) found that the stock market responds negatively to firms headquartered in corrupt regions. Investors’ assessment of irrelevant earnings information comes from the argument that corruption provides lower controlling and monitoring functions, higher asymmetric information, and lower managerial quality. Previous studies have found that lower controlling and monitoring functions (Ujan & Mukhlasin, Citation2019), higher information asymmetry (Lin et al., Citation2007), and lower managerial quality (Fanani & Merbaka, Citation2020; Simamora, Citation2021) lead to lower earnings value relevance.

H2: Corruption reduces earnings value relevance

Earnings predictability is the ability of earnings to predict future performance. Future performance is reflected in the relationship between current stock returns and future earnings as a future earnings response coefficient (Collins et al., Citation1994). Future earnings responses show how far future earnings can be reflected in the current stock returns. As corruption brings a lower reputation (Pricewaterhouse Coopers, Citation2016) and higher earnings manipulation(H. Xu et al., Citation2019), earnings cannot be used to predict future performance. In addition, lower earnings predictability can be attributed to the arguments that corruption provides lower controlling and monitoring functions, higher information asymmetry, and lower managerial quality. Previous studies have found that lower controlling and monitoring functions (Suh & Fernando, Citation2013), higher information asymmetry), and lower managerial quality (Fanani & Merbaka, Citation2020; Simamora, Citation2021) lead to lower earnings predictability.

H3: Corruption reduces earnings predictability

5. Research design

5.1. Sample

The research sample included manufacturing firms listed on the Indonesian Stock Exchange from to 2008–2016. Manufacturing firms always adjust their selling prices because of market uncertainty from the distributor to the end customer (Rasmussen, Citation2013). In this case, there is higher revenue and earnings variability (H. Ahmed & Azim, Citation2015). It leads to lower earnings persistence and is hard to be used to predict future performance. First, revenue and earnings variability in manufacturing sectors can bring uncertainty for managers and lead to opportunist behavior of earnings management that can reduce earnings quality (Rigamonti et al., Citation2024). Second, complex characteristic of supply chain manufacturing sector can also bring risk of bribery and corruption, such as government subside or price control that bring firms to political transaction (Arsandi, Citation2022; Demir et al., Citation2022; Kim et al., Citation2023; Mauro, Citation1997). The total sample included 846 manufacturing firm years, as shown in .

Table 1. Sample.

5.2. Empirical model

This study examined the effects of corruption on earnings quality. Earnings quality is measured using a model of earnings persistence, earnings value relevance, and predictability. The earnings persistence model is shown in EquationEquation (1)(1)

(1) (Demerjian et al., Citation2013; Francis et al., Citation2005; Li, Citation2019). The earnings value relevance and predictability model is shown in EquationEquation (2)

(2)

(2) (Collins et al., Citation1994).

(1)

(1)

(2)

(2)

Coefficient b1 in EquationEquation (1)(1)

(1) represents earnings persistence, which shows the relationship between current and future earnings. Coefficient b2 in EquationEquation (2)

(2)

(2) represents earnings value relevance, which shows the current earnings response coefficient. Coefficient b3 in EquationEquation (2)

(2)

(2) represents earnings predictability, which shows the future earnings response coefficient. To examine the effect of corruption on earnings quality, we adjust EquationEquations (1)

(1)

(1) and Equation(2)

(2)

(2) with corruption. The effect of corruption on earnings persistence is examined in EquationEquation (3)

(3)

(3) , while the effect of corruption on earnings value relevance and predictability is examined in EquationEquation (4)

(4)

(4) .

(3)

(3)

(4)

(4)

EquationEquations (3)(3)

(3) and Equation(4)

(4)

(4) are run by firm and province fixed effects regressions. Firm fixed effects aim to control for different accounting and financial statement policies in different firms. Province fixed effects aim to control the different corruption cultures in different provinces because the data on corruption cases are based on provinces’ regions, as reported by the Indonesian Corruption Eradication Committee.

The control variables in EquationEquations (3)(3)

(3) and Equation(4)

(4)

(4) include firm characteristics, performance variability, agency cost, and monitoring by chief executive officer (CEO) and chief financial officer (CFO). A firm’s characteristics are proxied by its size. Firm size controls the fact that bigger firms have a greater reputation to maintain higher earnings quality (Collins et al., Citation1994; H. Xu et al., Citation2019). Performance variability controls for earnings uncertainty. Performance variability is proxied by sales, earnings, and operating cash flow volatility (Demerjian et al., Citation2013). Agency costs control agency conflicts, which lead to information asymmetry. Agency costs are proxied by free cash flow (Kalash, Citation2019) and asset growth (Fama & French, Citation2002; Kalash, Citation2019). Monitoring by CEO and CFO controls the responsibility of CEO and CFO on corporate reporting. Monitoring by CEO and CFO are proxied by female CEO and female CFO by considering females bring more effective monitoring of earnings quality (Zalata et al., Citation2019a, Citation2019b, Citation2022). The hypothesis H1 is accepted if the coefficient value of b2 in EquationEquation (3)

(3)

(3) is negative and significant. The hypothesis H2 is accepted if the coefficient value of b6 in EquationEquation (4)

(4)

(4) is negative and significant. H3 is accepted if the coefficient of b7 in EquationEquation (4)

(4)

(4) is negative and significant. The details of the variable measurements are shown in . Financial data are accessed from financial reports published on the firms’ website or the Indonesian Stock Exchange website (www.idx.co.id). Corruption data were accessed from the corruption level report published on the Indonesian Corruption Eradication Committee website (www.kpk.go.id).

Table 2. Research variables.

6. Empirical results and discussion

6.1. Descriptive statistics

shows that the highest corruption (COR) is 0.00000183. In this research, Jakarta is the province that has the highest corruption cases, especially in 2016. It happens because Jakarta is the center of national politics and economics where most government offices and businesses are headquartered in Jakarta. The lowest corruption (COR) is 0.00000000. In this research, some provinces have zero corruption cases, such as West Java in 2010, 2012, 3013, and 2015; East Java in 2010–2013, Jakarta in 2014–2015, West Kalimantan in 2008–2016, and Banten in 2008–2010. The average value of corruption (COR) is 0.00000035.

Table 3. Descriptive statistics.

6.2. Regression analysis

provides the regression in two conditions of future earnings: a return on assets period of t + 1 (ROAt+1) and an average return on assets period of t + 1 to t + 3 (ROAt+1,t+3). After involving corruption as a moderating variable, in the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) has a coefficient value of −125,725.9000 with a t-statistic of −2.1811 (significant at 0.05). This indicates that corruption reduces current earnings persistence in the following year’s earnings. In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt × COR) has a coefficient value of −251,440.8000 with a t-statistic of −5.6569 (significant at 0.01). This indicates that corruption reduces current earnings persistence, on average, for the next three years’ earnings. shows that corruption reduces earnings persistence.

Table 4. Earnings persistence and corruption.

provides the earnings value relevance as the coefficient of the current earnings price ratio (Et-1). After involving corruption as a moderating variable, the results show that the interaction between the current earnings price ratio and corruption (Et × COR) has a coefficient value of −95,224.5000, with a t-statistic of −0.6600 (insignificant). This indicates that corruption does not affect the relevance of the earnings value. also provides earnings predictability for the coefficient value of the total earnings price ratio in the next three years (Et+1,t+3). After involving corruption as a moderating variable, the results show that the interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) has a coefficient value of −609,796.6000 with a t-statistic of −7.8250 (significant at 0.01). This finding indicates that corruption reduces the predictability of earnings.

Table 5. Earnings value relevance and predictability and corruption.

6.3. Regression analysis (including national government corruption cases)

This study also examines the effect of corruption on earnings quality by involving corruption at the national level. In the main analysis, this research measures the corruption level using the corruption case in each province region where the firms are headquartered. Most sample firms are headquartered in Jakarta Province. Jakarta province is the capital of Indonesia, which has both local (Jakarta) and national governmental offices. Corruption cases in Jakarta include both local and national government officers. This research once again examines the model of EquationEquations (3)(3)

(3) and Equation(4)

(4)

(4) by adding the national-level corruption cases to the observation sample where the firms are headquartered in Jakarta. The results for earnings persistence and corruption are shown in , while the results for earnings value relevance, predictability, and corruption are shown in .

Table 6. Earnings persistence and corruption (including national government corruption cases).

Table 7. Earnings value relevance and predictability and corruption (including national government corruption cases).

Based on , in the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) has a coefficient value of −102,911.1000 with a t-statistic of −2.9138 (significant in 0.01). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) has a coefficient value of −157,252.1000 with a t-statistic of −5.7668 (significant at 0.01). This indicates that the results in are consistent with the main result in , where corruption reduces current earnings persistence in the next year and the average earnings of the next three years.

The results in show that the interaction between the current earnings price ratio and corruption (Et × COR) has a coefficient value of −225,880.6000 with a t-statistic of −3.5157 (significant at 0.01). This finding indicates that corruption reduces the relevance of earnings values. also shows that the interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) has a coefficient value of −4,643.6530, with a t-statistic of −0.1161 (insignificant). This indicates that corruption does not affect earnings predictability. The results in are not consistent with the main result in , where corruption (before involving the national government corruption cases) has no effect on earnings value relevance, but has an effect on earnings predictability. The results in are sensitive to corruption measurements that involve national government corruption cases in the Jakarta province.

6.4. Regression analysis (state-owned vs. private-owned)

This study also examines the effect of corruption on earnings quality in different case of state-owned and private-owned firms. Since corruption is also connected by political interaction, state-owned firms have more possibilities to be exposed by political interaction. In Indonesia, state-owned firms are also managed politically by Indonesian Ministry of State-Owned Enterprises. Some studies find that political culture affect earnings quality (Doan et al., Citation2020; Harianto, Citation2022). In this research, there are 180 state-owned firms and 666 private-owned firms. This research once again examines the model of EquationEquations (3)(3)

(3) and Equation(4)

(4)

(4) by separating the sample into groups of state-owned and private-owned firms. The results for earnings persistence and corruption are shown in , while the results for earnings value relevance, predictability, and corruption are shown in .

Table 8. Earnings persistence and corruption (state-owned firms vs. private-owned firms).

Table 9. Earnings value relevance and predictability and corruption (state-owned firms vs. private-owned firms).

Based on , in the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) for state-owned firms has a coefficient value of –139,891.9000 with a t-statistic of −5.8990 (significant in 0.01). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) for state-owned firms has a coefficient value of −251,440.8000 with a t-statistic of −7.9827 (significant at 0.01). This indicates that the results for state-owned firms are consistent with the main result in , where corruption reduces current earnings persistence in the next year and the average earnings of the next three years for state-owned firms.

In the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) for private-owned firms has a coefficient value of −109,878.1000 with a t-statistic of −2.9872 (significant in 0.05). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) for private-owned firms has a coefficient value of −109,321.1000 with a t-statistic of −2.9668 (significant at 0.05). This indicates that the results for state-owned firms are consistent with the main result in , where corruption reduces current earnings persistence in the next year and the average earnings of the next three years for private-owned firms.

In general, the effect of corruption on earnings persistence occurs more for state-owned firms. The effect of the interaction variable between the current return on assets and corruption is bigger for state-owned firms than private-owned ones. The model of state-owned firms also has bigger explanatory power of adjusted R-squared than private-owned ones.

The results in show that the interaction between the current earnings price ratio and corruption (Et × COR) for state-owned firms has a coefficient value of −222,113.5000 with a t-statistic of −2.0339 (significant at 0.05). This finding indicates that corruption reduces the relevance of earnings values for state-owned firms. The interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) for state-owned firms has a coefficient value of −98,923.4210, with a t-statistic of −2.3891 (significant at 0.05). This finding indicates that corruption reduces the earnings predictability for state-owned firms.

also shows that the interaction between the current earnings price ratio and corruption (Et × COR) for private-owned firms has a coefficient value of −111,889.3110 with a t-statistic of −1.0077 (insignificant). This finding indicates that corruption has no effect on the relevance of earnings values for private-owned firms. The interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) for private-owned firms has a coefficient value of −3,441.4440, with a t-statistic of −0.9872 (insignificant). This finding indicates that corruption has no effect on earnings predictability for private-owned firms. In general, the effect of corruption on earnings value relevance and predictability occurs more for state-owned firms than private-owned ones.

6.5. Regression analysis (under heteroscedasticity condition)

This study also examines the effect of corruption on earnings quality under heteroscedasticity condition. The potential of heteroscedasticity comes from the involvement of time series data where earnings quality measurement uses period of t + 1 to period of t + 3, for example ROA period of t + 1 and Earnings Per Share period of t + 1. To get robust result, this research examines the regression by using Huber-White test under heteroscedasticity condition. The results for earnings persistence and corruption are shown in , while the results for earnings value relevance, predictability, and corruption are shown in .

Table 10. Earnings persistence and corruption (under heteroscedasticity condition).

Table 11. Earnings value relevance and predictability and corruption (under heteroscedasticity condition).

Based on , in the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) has a coefficient value of −125,725.9000 with a t-statistic of −2.8981 (significant in 0.01). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) has a coefficient value of −251,440.8000 with a t-statistic of −2.5068 (significant at 0.05). This indicates that the results in are consistent with the main result in , where corruption reduces current earnings persistence in the next year and the average earnings of the next three years.

The results in show that t the interaction between the current earnings price ratio and corruption (Et × COR) has a coefficient value of −95,324.5000, with a t-statistic of −0.1906 (insignificant). This indicates that corruption does not affect the relevance of the earnings value. The interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) has a coefficient value of −601,796.6000 with a t-statistic of −2.1440 (significant at 0.05). This finding indicates that corruption reduces the predictability of earnings. The result of is consistent with main result of .

6.6. Regression analysis for each province

This study also examines the effect of corruption on earnings quality for each province since this research uses corruption in the local government level. In this research, there are 4 provinces of Jakarta, East Java, West Java, and East Kalimantan. There are 684 samples for Jakarta, 99 samples for East Java, 54 samples for West Java, and 9 samples for East Kalimantan. This research only examines the effect of corruption on earnings quality separately for Jakarta and East Java. East Kalimantan cannot be examined separately since the corruption case in this province is 0. Number of samples for West java and East Kalimantan do not provide enough variance of the variables. The results for earnings persistence and corruption are shown in , while the results for earnings value relevance, predictability, and corruption are shown in .

Table 12. Earnings persistence and corruption for each province.

Table 13. Earnings value relevance and predictability and corruption for each province.

Based on , in the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) for group of samples in Jakarta has a coefficient value of −159,092.2910 with a t-statistic of −4.8373 (significant in 0.01). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) for group of samples in Jakarta has a coefficient value of −138,891.6000 with a t-statistic of −5.8373 (significant at 0.01). This indicates that the results in are consistent with the main result in , where corruption reduces current earnings persistence in the next year and the average earnings of the next three years.

In the regression model of ROAt+1, the interaction variable between the current return on assets and corruption (ROAt × COR) for group of samples in East Java has a coefficient value of −80,787.3100 with a t-statistic of −1.0872 (insignificant). In the regression model of ROAt+1,t+3, the interaction variable between the current return on assets and corruption (ROAt x COR) for group of samples in East Java has a coefficient value of −72,717.1200 with a t-statistic of −1.0526 (insignificant). There is no effect of corruption on earnings persistence for group of samples in East Java. In general, the effect of corruption on earnings persistence occurs more in Jakarta than East Java where Jakarta has more corruption level than East Java.

The results in show that the interaction between the current earnings price ratio and corruption (Et × COR) for group of samples in Jakarta has a coefficient value of −216,374.1000 with a t-statistic of −2.0324 (significant at 0.05). This finding indicates that corruption reduces the relevance of earnings values for group of samples in Jakarta. The interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) for state-owned firms has a coefficient value of −87,372.1000, with a t-statistic of −2.4211 (significant at 0.05). This finding indicates that corruption reduces the earnings predictability for group of samples in Jakarta.

also shows that the interaction between the current earnings price ratio and corruption (Et × COR) for group of samples in East Java has a coefficient value of −98,762.7610 with a t-statistic of −1.0133 (insignificant). This finding indicates that corruption has no effect on the relevance of earnings values for group of samples in East Java. The interaction between the total earnings price ratio in the next three years and corruption (Et+1,t+3 x COR) for private-owned firms has a coefficient value of −7,326.1000, with a t-statistic of −0.7632 (insignificant). This finding indicates that corruption has no effect on earnings predictability for group of samples in East Java. In general, the effect of corruption on earnings value relevance and predictability occurs more for group of samples in Jakarta than East Java where Jakarta has more corruption level than East Java.

6.7. Discussion

The first result shows that the interaction between corruption and current earnings negatively affects future earnings. It indicates H1, that state corruption reduces earnings persistence. A corruption culture promotes weaker monitoring and controlling functions, leading to a higher risk of business uncertainty. A higher risk of business uncertainty causes firms to fail to mitigate uncertain business conditions and unpredictable events. The risk of business uncertainty leads to lower persistence and sustainability of earnings. This result was consistent with that reported by Xu et al. (Citation2019) who find that local corruption reduces the earnings quality of persistence.

The second result shows that the interaction between corruption and current earnings does not affect stock return. It indicates H2, that state corruption reduces earnings value relevance and that it is rejected. However, the role of corruption culture in reducing earnings value relevance occurs when corruption cases at the national level are involved. This result indicates that stock market participants use earnings information to make decisions based on the national level of corruption. The arguments that explain this finding are as follows: First, earnings value relevance explains the direct relationship between earnings and stock market responses;(S. Ahmed, Citation2015) second, stock market responses in Indonesia are affected by the joint factors of micro- and macro-economic variables (Yusfiarto, Citation2020). Thus, corruption at the local and national levels can explain earnings value relevance more than corruption at the local level alone. Investors assess that local and national corruption levels can promote lower controlling and monitoring functions and higher asymmetry information, which leads to lower earnings value relevance. This result is consistent with those of Ujan and Mukhlasin (Citation2019) and Lin et al. (Citation2007) They find that lower controlling and monitoring functions and higher asymmetry information have a negative effect on earnings value relevance.

The third result shows that the interaction between corruption and future earnings negatively affects stock returns. It indicates H3, that state corruption reduces earnings predictability. Earnings predictability indicates that future earnings are reflected in current stock returns. As corruption lowers reputation, higher earnings manipulation, lower controlling and monitoring functions, higher asymmetry information, and lower managerial quality, earnings cannot be reflected in the current stock return and cannot be used to predict future performance. This result is consistent with those of Suh and Fernando (Citation2013), Fanani and Merbaka (Citation2020), and Simamora (Citation2021) who find that lower controlling and monitoring functions, higher information asymmetry, and lower managerial quality lead to lower earnings predictability.

Regarding earnings persistence, corruption has a greater effect on the relationship between current earnings and earnings three years ahead than one year ahead because the coefficient of interaction between corruption and current earnings has a larger absolute coefficient value on earnings three years ahead (251440.8000) than one year ahead (125725.9000), as shown in . This finding indicates that corruption explains why firms have a lower ability to maintain persistent earnings further ahead. The argument that explains this finding is that earnings persistence is important in measuring the ability to generate recurring earnings in the future (Fatma & Hidayat, Citation2019).

Since earnings value relevance and predictability are in the same regression model, this study compares whether corruption has a greater effect on earnings value relevance or earnings predictability. Based on the results in , the corruption effect occurs more in earnings predictability than earnings value relevance. This indicates that earnings value relevance is difficult for investors in emerging markets to have institutional deficiencies such as disclosure inadequacy; in some cases, poor accounting standards, audit quality has generally been perceived as low, and investors are too naive and irrational to accounting information (Aharony et al., Citation2000; C. J. P. Chen et al., Citation2001; Graham & King, Citation2000). On the other hand, economic predictability is more important in emerging markets because it provides information on future stability (Rehman et al., Citation2022).

This study finds that corruption reduces earnings quality. This is consistent with previous studies, which (Y. Chen et al., Citation2020; Lei & Wang, Citation2019; Lourenço et al., Citation2018; A. H. Nguyen & Duong, Citation2020; Picur, Citation2004; H. Xu et al., Citation2019) find that corruption has a negative effect on earnings quality attributes. Some arguments explain why corruption reduces the quality of earnings. First, higher corruption captures lower regulation implementation and law enforcement, leading managers to be less concerned about the litigation risk of earnings manipulation. Second, the secret illegal movement characteristic causes corruption to provide higher information asymmetry, leading to lower information quality. Third, since managers tend to have lower quality when surrounded by a politically corrupt culture, lower-quality managers fail to maintain earnings quality.

The result implies the literature. This research confirms the concept of social capital, in which corrupt behavior becomes societal norms and values and is absorbed by firms to corrupt managers. Corrupted managers promote fraud and lawbreaking, which leads managers to report lower-quality earnings. Firms that absorb corrupted societal norms and values have a lower capability to monitor and control the financial reporting process, which leads to lower earnings quality. Therefore, it is important to achieve higher earnings quality. Higher earnings quality leads to lower information asymmetry and helps firms to gain easier access to funding resources from creditors and investors (Scott, Citation2014). Higher earnings quality can also reduce the costs of conflicts between firms and stakeholders (Scott, Citation2014). Higher earnings quality can also improve a firm’s value (Dewi & Devie, Citation2017), financial performance (Dewi & Devie, Citation2017; Huynh, Citation2018), and reputation (Huynh, Citation2018). The benefits of easier funding resources (Scott, Citation2014), conflict reduction (Scott, Citation2014), firm value (Dewi & Devie, Citation2017), financial performance (Dewi & Devie, Citation2017; Huynh, Citation2018), and reputation (Huynh, Citation2018) can maintain organizational stability, including financial stability (Siekelova, Citation2021). If firms have lower earnings quality, they will have difficulty accessing funding and incur more costs of conflict. This can disturb a firm’s stability.

This research also confirms agency theory where corruption enhance the agency conflict between managers and owners. The corruption characteristics of low law and regulation enforcement (ineffective governance) and high hidden transactions (information asymmetry) are absorbed by managers (in the context of social capital). In internal condition, the corruption characteristics increase agency conflict between managers and owners and lead managers to report low quality earnings information. This result implies literature, especially to capture the concept of social capital and agency theory comprehensively to explain the relationship between corruption and earnings quality. This result also implies business practice, especially to improve effective governance for firms that are headquartered in high corruption level region. This study further substantiates the principles outlined in agency theory, wherein instances of corruption exacerbate the agency conflict existing between managerial entities and company proprietors. The identifiable traits of corruption, notably stemming from lax law enforcement and regulatory oversight (reflecting ineffective governance), coupled with a prevalence of clandestine transactions (evidencing information asymmetry), are typically assumed by managerial agents within the framework of social capital dynamics. Within this internal milieu, these corruption-related attributes contribute to an escalation in the agency conflict between managerial agents and company owners, consequently prompting managers to furnish financial reports characterized by diminished quality. This outcome underscores the significance of scholarly literature in comprehensively elucidating the interplay between corruption and the quality of reported earnings, particularly in integrating notions of social capital and agency theory. Furthermore, this finding bears significant implications for business practices, notably emphasizing the imperative of enhancing governance mechanisms within firms operating in regions characterized by elevated levels of corruption.

7. Summary and conclusion

The primary objective of this study is to assess the impact of corruption on earnings quality, encompassing elements such as earnings persistence, earnings value relevance, and earnings predictability within the context of Indonesia. Broadly, corruption diminishes both earnings persistence and predictability. Moreover, corruption specifically reduces earnings value relevance when instances of corruption are associated with both local and national levels. The findings suggest that corruption fosters diminished controlling and monitoring functions, heightened information asymmetry, and a decline in managerial quality, all contributing to a reduction in earnings quality. The implications of the results suggest that firms, particularly those headquartered in regions with elevated corruption levels, should enhance their controlling and monitoring functions to alleviate increased information asymmetry and enhance overall earnings quality. Furthermore, the findings suggest a need for improved anti-corruption initiatives by regulators in Indonesia, particularly spearheaded by entities such as the Corruption Eradication Committee (Komite Pemberantasan Korupsi), to curb corrupt practices within government offices and prevent the proliferation of a corrupt culture into business activities; however, it is essential to acknowledge the limitations of this research. First, the study focuses on explaining corruption culture in the region where firms are headquartered, assuming that the corruption culture within firms is absorbed from the local context. Organizational culture within firms has not been directly examined. Second, the research does not distinguish between firms involved in corruption cases or those that have associations with corrupt government offices and those that do not. Third, this study does not compare earnings quality in firms not involved in corruption cases in different regions to assess the potential absorption of local corruption culture into these firms. Suggestions for future research include an in-depth examination of the corruption culture at the firm level, a focused analysis of firms engaged in corruption cases to accurately capture the corruption culture affecting earnings quality, and an assessment of firms not involved in corruption cases to determine the potential absorption of the local corruption culture as part of their organizational culture.

Authors’ contributions

Eko Arief Sudaryono contributes to do the conception and design, analysis and interpretation of the data, the drafting of the paper, revising it critically for intellectual content, and the final approval of the version to be published. Wahyu Widarjo contributes to do the conception and design, analysis and interpretation of the data, revising it critically for intellectual content, and the final approval of the version to be published. Agung Nur Probohudono contributes to do the conception and design, analysis and interpretation of the data, revising it critically for intellectual content, and the final approval of the version to be published. Adhitya Agri Putra contributes to do analysis and interpretation of the data and revising it critically for intellectual content. Frank Aligarh contributes to do analysis and interpretation of the data and revising it critically for intellectual content. All authors agree to be accountable for all aspects of the work.

Data availability statement

Financial data are accessed from financial reports published on the firms’ website or the Indonesian Stock Exchange website (www.idx.co.id). Corruption data were accessed from the corruption level report published on the Indonesian Corruption Eradication Committee website (www.kpk.go.id).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Eko Arief Sudaryono

Eko Arief Sudaryono is a lecturer in Faculty of Economics and Business, Universitas Sebelas Maret (UNS), Indonesia. Research interests including financial accounting, financial reporting, corporate tax, corporate social responsibility, and corporate governance.

Wahyu Widarjo

Wahyu Widarjo holds a PhD in Accounting from Universitas Sebelas Maret (UNS) in Surakarta and is a Lecturer in the Faculty of Economics and Business at Universitas Sebelas Maret.

Agung Nur Probohudono

Agung Nur Probohudono holds a PhD from Curtin University, Australia, and is a Professor in the Faculty of Economics and Business at Universitas Sebelas Maret in Surakarta, Indonesia.

Adhitya Agri Putra

Adhitya Agri Putra is a lecturer in Faculty of Economics and Business, Universitas Riau, Indonesia. Currently, he is attending a doctoral program in Faculty of Economics and Business, Universitas Sebelas Maret, Indonesia. Research interests including financial accounting, financial reporting, corporate social responsibility, and corporate governance.

Frank Aligarh

Frank Aligarh is an assistant professor at the Universitas Islam Negeri Raden Mas Said Surakarta, Indonesia. The author’s interest research mainly concentrates on Financial Technology, Behavioral Accounting, and Accounting Information Systems. Frank Aligarh is pursuing his PhD at Universitas Sebelas Maret (UNS) Surakarta, Indonesia.

References

- Adler, P. S., & Kwon, S.-W. (2002). Social capital: Prospects for a new concept. Academy of Management Review, 27(1), 17–40. https://doi.org/10.5465/amr.2002.5922314

- Aharony, J., Lee, C.-W. J., & Wong, T. J. (2000). Financial packaging of IPO firms in China. Journal of Accounting Research, 38(1), 103. https://doi.org/10.2307/2672924

- Ahmed, S. (2015). Determinants of the quality of disclosed earnings and value relevance across transitional Europe. Journal of Accounting in Emerging Economies, 5(3), 325–349. https://doi.org/10.1108/JAEE-09-2011-0044

- Ahmed, H., & Azim, M. (2015). Earnings management behavior: A study on the cement industry of Bangladesh. International Journal of Management, Accounting and Economics, 2(4), 265–276. http://www.ijmae.com/article_115478.html

- Andriani, L. (2021). Corruption aversion, social capital, and institutional trust in a dysfunctional institutional framework: Evidence from a Palestinian survey. Journal of Economic Issues, 55(1), 178–202. https://doi.org/10.1080/00213624.2021.1875728

- Arsandi, S. A. (2022). Regional head corruption and industrial growth: Evidence from Mojokerto regency and city. Integritas: Jurnal Antikorupsi, 8(1), 103–112. https://doi.org/10.32697/integritas.v8i1.857

- Asogwa, C. I., Ofoegbu, G. N., Nnam, J. I., & Chukwunwike, O. D. (2019). Effect of corporate governance board leadership models and attributes on earnings quality of quoted Nigerian companies. Cogent Business & Management, 6(1), 1683124. https://doi.org/10.1080/23311975.2019.1683124

- Athanasouli, D., & Goujard, A. (2015). Corruption and management practices: Firm level evidence. Journal of Comparative Economics, 43(4), 1014–1034. https://doi.org/10.1016/j.jce.2015.03.002

- Ball, R., Robin, A., & Wu, J. S. (2003). Incentives versus standards: Properties of accounting income in four East Asian countries. Journal of Accounting and Economics, 36(1–3), 235–270. https://doi.org/10.1016/j.jacceco.2003.10.003

- Banerjee, R. (2016). Corruption, norm violation and decay in social capital. Journal of Public Economics, 137, 14–27. https://doi.org/10.1016/j.jpubeco.2016.03.007

- Boateng, A., Wang, Y., Ntim, C., & Glaister, K. W. (2021). National culture, corporate governance and corruption: A cross‐country analysis. International Journal of Finance & Economics, 26(3), 3852–3874. https://doi.org/10.1002/ijfe.1991

- Bondeli, J. V., Havenvid, M. I., & Solli-Sæther, H. (2021). Corruption in interaction: The role of social capital in private–public relationships. Journal of Business & Industrial Marketing, 36(11), 2098–2110. https://doi.org/10.1108/JBIM-05-2019-0255

- Boonlert-U-Thai, K., Meek, G. K., & Nabar, S. (2006). Earnings attributes and investor-protection: International evidence. International Journal of Accounting, 41(4), 327–357. https://doi.org/10.1016/j.intacc.2006.09.008

- Canina, L., & Potter, G. (2019). Determinants of earnings persistence and predictability for lodging properties. Cornell Hospitality Quarterly, 60(1), 40–51. https://doi.org/10.1177/1938965518791729

- Cao, P., Qin, L., & Zhu, H. (2019). Local corruption and stock price crash risk: Evidence from China. International Review of Economics & Finance, 63, 240–252. https://doi.org/10.1016/j.iref.2018.11.006

- Chaney, P. K., Faccio, M., & Parsley, D. (2011). The quality of accounting information in politically connected firms. Journal of Accounting and Economics, 51(1–2), 58–76. https://doi.org/10.1016/j.jacceco.2010.07.003

- Chen, C. J. P., Chen, S., & Su, X. (2001). Is accounting information value-relevant in the emerging Chinese stock market? Journal of International Accounting, Auditing and Taxation, 10(1), 1–22. https://doi.org/10.1016/S1061-9518(01)00033-7

- Chen, Y., Che, L., Zheng, D., & You, H. (2020). Corruption culture and accounting quality. Journal of Accounting and Public Policy, 39(2), 106698. https://doi.org/10.1016/j.jaccpubpol.2019.106698

- Cho, H., Choi, S., Lee, W.-J., & Yang, S. (2020). Regional crime rates and corporate misreporting. Spanish Journal of Finance and Accounting/Revista Española de Financiación y Contabilidad, 49(1), 94–123. https://doi.org/10.1080/02102412.2019.1582194

- Christy, N. N. A., Andi Wibowo, R., & Wu, M.-C. (2022). A study on social capital of Indonesian entrepreneurs. TEM Journal, 11(1), 272–281. https://doi.org/10.18421/TEM111-34

- Coleman, J. S. (1990). Foundations of social theory. Harvard University Press.

- Collins, D. W., Kothari, S. P., Shanken, J., & Sloan, R. G. (1994). Lack of timeliness and noise as explanations for the low contemporaneuos return-earnings association. Journal of Accounting and Economics, 18(3), 289–324. https://doi.org/10.1016/0165-4101(94)90024-8

- Cuervo-Cazurra, A. (2016). Corruption in international business. Journal of World Business, 51(1), 35–49. https://doi.org/10.1016/j.jwb.2015.08.015

- Damijan, S. (2023). Corruption: A review of issues. Economic and Business Review, 25(1), 1–10. https://doi.org/10.15458/2335-4216.1314

- Deakins, D., & Hussain, G. (1994). Risk assessment with asymmetric information. International Journal of Bank Marketing, 12(1), 24–31. https://doi.org/10.1108/02652329410049571

- DeBacker, J., Heim, B. T., & Tran, A. (2015). Importing corruption culture from overseas: Evidence from corporate tax evasion in the United States. Journal of Financial Economics, 117(1), 122–138. https://doi.org/10.1016/j.jfineco.2012.11.009

- Demerjian, P., Lev, B., Lewis, M., & McVay, S. (2013). Managerial ability and earnings quality. Accounting Review, 88(2), 463–498. https://doi.org/10.2308/accr-50318

- Demir, F., Hu, C., Liu, J., & Shen, H. (2022). Local corruption, total factor productivity and firm heterogeneity: Empirical evidence from Chinese manufacturing firms. World Development, 151, 105770. https://doi.org/10.1016/j.worlddev.2021.105770

- Dewi, A. K., & Devie. (2017). Pengaruh earnings quality terhadap firm value dengan financial performance sebagai variabel intervening pada perusahaan yang terdaftar pada perusahaan LQ 45. Business Accounting Review, 5(2), 649–660.

- Doan, A.-T., Lin, K.-L., & Doong, S.-C. (2020). State-controlled banks and income smoothing. Do politics matter? North American Journal of Economics and Finance, 51, 101057. https://doi.org/10.1016/j.najef.2019.101057

- Eldridge, S., van Iwaarden, J., van der Wiele, T., & Williams, R. (2013). Management control systems for business processes in uncertain environments. International Journal of Quality & Reliability Management, 31(1), 66–81. https://doi.org/10.1108/IJQRM-03-2012-0040

- El-Helaly, M., Ntim, C. G., & Al-Gazzar, M. (2020). Diffusion theory, national corruption and IFRS adoption around the world. Journal of International Accounting, Auditing and Taxation, 38, 100305. https://doi.org/10.1016/j.intaccaudtax.2020.100305

- Fama, E. F., & French, K. R. (2002). Testing trade-off and pecking order predictions about dividends and debt. Review of Financial Studies, 15(1), 1–33. https://doi.org/10.1093/rfs/15.1.1

- Fan, J. P. H., Rui, O. M., & Zhao, M. (2008). Public governance and corporate finance: Evidence from corruption cases. Journal of Comparative Economics, 36(3), 343–364. https://doi.org/10.1016/j.jce.2008.05.001

- Fanani, Z., & Merbaka, Z. R. (2020). The effect of managerial ability and tone of earnings announcements towards market reaction. Jurnal Akuntansi Dan Keuangan, 22(1), 10–17. https://doi.org/10.9744/jak.22.1.10-17

- Fatma, N., & Hidayat, W. (2019). Earnings persistence, earnings power, and equity valuation in consumer goods firms. Asian Journal of Accounting Research, 5(1), 3–13. https://doi.org/10.1108/AJAR-05-2019-0041

- Fisman, R., & Miguel, E. (2007). Corruption, norms, and legal enforcement: Evidence from diplomatic parking tickets. Journal of Political Economy, 115(6), 1020–1048. https://doi.org/10.1086/527495

- Francis, J., LaFond, R., Olsson, P. M., & Schipper, K. (2004). Costs of equity and earnings attributes. Accounting Review, 79(4), 967–1010. https://doi.org/10.2308/accr.2004.79.4.967

- Francis, J., LaFond, R., Olsson, P., & Schipper, K. (2005). The market pricing of accruals quality. Journal of Accounting and Economics, 39(2), 295–327. https://doi.org/10.1016/j.jacceco.2004.06.003

- Friedman, E., Johnson, S., Kaufmann, D., & Zoido-Lobaton, P. (2000). Dodging the grabbing hand: The determinants of unofficial activity in 69 countries. Journal of Public Economics, 76(3), 459–493. https://doi.org/10.1016/S0047-2727(99)00093-6

- Fukuyama, F. (1995). Social capital and the global economy. Foreign Affairs, 74(5), 89–103. https://doi.org/10.2307/20047302

- Gaio, C., & Raposo, C. (2011). Earnings quality and firm valuation: International evidence. Accounting & Finance, 51(2), 467–499. https://doi.org/10.1111/j.1467-629X.2010.00362.x

- Galang, R. M. N. (2012). Victim or victimizer: Firm responses to government corruption. Journal of Management Studies, 49(2), 429–462. https://doi.org/10.1111/j.1467-6486.2010.00989.x

- Graham, R. C., & King, R. D. (2000). Accounting practices and the market valuation of accounting numbers: Evidence from Indonesia, Korea, Malaysia, the Philippines, Taiwan, and Thailand. International Journal of Accounting, 35(4), 445–470. https://doi.org/10.1016/S0020-7063(00)00075-3

- Harianto, S. (2022). Political connection, auditor quality, family ownership, and earnings management: Real and accrual. Journal of Economics, Business, & Accountancy Ventura, 25(2), 204–216. https://doi.org/10.14414/jebav.v25i2.3012

- Hashmi, M. A., Brahmana, R. K., Ansari, T., Hasan, M. A., Abdullah. (2022). Do effective audit committees, gender-diverse boards, and corruption controls influence the voluntary disclosures of Asian banks? The moderating role of directors’ experience. Cogent Business & Management, 9(1), 2135205. https://doi.org/10.1080/23311975.2022.2135205

- Hofmann, C., & Schwaiger, N. (2020). Religion, crime, and financial reporting. Journal of Business Economics, 90(5–6), 879–916. https://doi.org/10.1007/s11573-020-00982-2

- Hope, O., Yue, H., & Zhong, Q. (2020). China’s anti‐corruption campaign and financial reporting quality. Contemporary Accounting Research, 37(2), 1015–1043. https://doi.org/10.1111/1911-3846.12557

- Hu, W., Wagner, S. M., & Shou, Y. (2023). Manufacturing firms’ credibility towards customers and operational performance: The counteracting roles of corruption and ICT readiness. International Journal of Logistics Research and Applications, 1–17. https://doi.org/10.1080/13675567.2023.2169666

- Huynh, Q. L. (2018). Earnings quality with reputation and performance. Asian Economic and Financial Review, 8(2), 269–278. https://doi.org/10.18488/journal.aefr.2018.82.269.278

- Islam, R., Haque, Z., & Moutushi, R. H. (2022). Earnings quality and financial flexibility: A moderating role of corporate governance. Cogent Business & Management, 9(1), 2097620. https://doi.org/10.1080/23311975.2022.2097620

- Jens, C. E. (2017). Political uncertainty and investment: Causal evidence from U.S. gubernatorial elections. Journal of Financial Economics, 124(3), 563–579. https://doi.org/10.1016/j.jfineco.2016.01.034

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jha, A. (2019). Financial reports and social capital. Journal of Business Ethics, 155(2), 567–596. https://doi.org/10.1007/s10551-017-3495-5

- Kalash, I. (2019). Firm leverage, agency costs and firm performance: An empirical research on service firms in Turkey. İnsan ve Toplum Bilimleri Araştırmaları Dergisi, 8(1), 624–636. https://doi.org/10.15869/itobiad.513268

- Kim, A. C., Sanchez, I., & Centola, D. (2023). Bribery and corruption risks in the manufacturing sector. Chief Executive Logo. https://chiefexecutive.net/bribery-and-corruption-risks-in-the-manufacturing-sector/

- Komisi Pemberantasan Korupsi. (2020). Laporan Tahunan KPK 2019.

- Kompas.Com. (2019). 2 Tersangka Kasus Krakatau Steel Segera Disidang. https://nasional.kompas.com/read/2019/05/21/21580161/2-tersangka-kasus-krakatau-steel-segera-disidang

- Lei, X., & Wang, H. (2019). Does the government’s anti-corruption storm improve the quality of corporate earnings?—Evidence from Chinese listed companies. China Journal of Accounting Studies, 7(4), 542–566. https://doi.org/10.1080/21697213.2019.1748910

- Lewellyn, K. B., & Bao, S. (2017). The role of national culture and corruption on managing earnings around the world. Journal of World Business, 52(6), 798–808. https://doi.org/10.1016/j.jwb.2017.07.002

- Li, V. (2019). The effect of real earnings management on the persistence and informativeness of earnings. British Accounting Review, 51(4), 402–423. https://doi.org/10.1016/j.bar.2019.02.005

- Lin, Y.-C., Huang, S. Y., Chang, Y.-F., & Tseng, C.-H. (2007). The relationship between information transparency and the informativeness of accounting earnings. Journal of Applied Business Research (JABR), 23(3), 23–32. https://doi.org/10.19030/jabr.v23i3.1388

- Liu, X. (2016). Corruption culture and corporate misconduct. Journal of Financial Economics, 122(2), 307–327. https://doi.org/10.1016/j.jfineco.2016.06.005

- Lourenço, I. C., Rathke, A., Santana, V., & Branco, M. C. (2018). Corruption and earnings management in developed and emerging countries. Corporate Governance: The International Journal of Business in Society, 18(1), 35–51. https://doi.org/10.1108/CG-12-2016-0226

- Lustrilanang, P., Suwarno, L. T., Omar, N., Said, J., & Darusalam, R. (2023). The role of control of corruption and quality of governance in ASEAN: Evidence from DOLS and FMOLS test. Cogent Business & Management, 10(1), 2154060. https://doi.org/10.1080/23311975.2022.2154060

- Mamatzakis, E., & Bagntasarian, A. (2022). An international study on the impact of corruption on analysts’ forecasts. Journal of International Accounting, Auditing and Taxation, 48, 100486. https://doi.org/10.1016/j.intaccaudtax.2022.100486

- Mauro, P. (1997). Why worry about corruption? In Economic issue (Vol. 6). International Monetary Fund.

- Menicucci, E. (2020). Earnings quality: How to define. In Earnings Quality (pp. 1–22). Springer International Publishing. https://doi.org/10.1007/978-3-030-36798-5_1

- Nguyen, A. H., & Duong, C. T. (2020). provincial governance quality and earnings management: Empirical evidence from Vietnam. Journal of Asian Finance, Economics and Business, 7(2), 43–52. https://doi.org/10.13106/jafeb.2020.vol7.no2.43

- Nguyen, D. T., & Truong, T. H. H. (2022). The mitigation of agency problem by using corporate governance in emerging markets: Evidence from Vietnam. Afro-Asian Journal of Finance and Accounting, 12(2), 143. https://doi.org/10.1504/AAJFA.2022.123070

- Picur, R. D. (2004). Quality of accounting, earnings opacity and corruption. Review of Accounting and Finance, 3(1), 103–114. https://doi.org/10.1108/eb043397

- Pricewaterhouse Coopers. (2016). Assessing the risk of bribery and corruption to your business.

- Rasmussen, S. J. (2013). Revenue recognition, earnings management, and earnings informativeness in the semiconductor industry. Accounting Horizons, 27(1), 91–112. https://doi.org/10.2308/acch-50291

- Rehman, M. Z., Tiwari, A. K., & Samontaray, D. P. (2022). Directional predictability in foreign exchange rates of emerging markets: New evidence using a cross-quantilogram approach. Borsa Istanbul Review, 22(1), 145–155. https://doi.org/10.1016/j.bir.2021.03.003

- Rigamonti, A. P., Greco, G., Pierotti, M., & Capocchi, A. (2024). Macroeconomic uncertainty and earnings management: Evidence from commodity firms. Review of Quantitative Finance and Accounting, 62(4), 1615–1649. https://doi.org/10.1007/s11156-024-01246-8

- Schipper, K., & Vincent, L. (2003). Earnings quality. Accounting Horizons, 17(s-1), 97–110. https://doi.org/10.2308/acch.2003.17.s-1.97

- Scott, W. R. (2014). Financial accounting theory (7th ed.). Prentice Hall.

- Seligson, M. A. (2002). The impact of corruption on regime legitimacy: A comparative study of four Latin American countries. Journal of Politics, 64(2), 408–433. https://doi.org/10.1111/1468-2508.00132

- Setyobudi, C. R., & Setyaningrum, D. (2019). E-government and corruption perception index: A cross-country study. Jurnal Akuntansi & Auditing Indonesia, 23(1), 11–20. https://doi.org/10.20885/jaai.vol23.iss1.art2

- Shleifer, A., & Vishny, R. W. (1993). Corruption. The Quarterly Journal of Economics, 108(3), 599–617. https://doi.org/10.2307/2118402

- Siekelova, A. (2021). The impact of the financial stability on the earnings management practices. SHS Web of Conferences, 129, 03028. https://doi.org/10.1051/shsconf/202112903028

- Simamora, A. J. (2021). Managerial ability, real earnings management, and earnings quality. JFBA: Journal of Financial and Behavioural Accounting, 1(1), 1–28.

- Smith, J. D. (2016). US political corruption and firm financial policies. Journal of Financial Economics, 121(2), 350–367. https://doi.org/10.1016/j.jfineco.2015.08.021

- Solomon, R. C. (2004). Aristotle, ethics and business organizations. Organization Studies, 25(6), 1021–1043. https://doi.org/10.1177/0170840604042409