?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to establish whether the effect of stock market development on the growth of economies in the Economic Community of West African States (ECOWAS) is conditioned by institutional quality threshold. To this end, we used the Hansen threshold estimation approach to assess any discontinuities in this relationship. Data are sourced from the World Development Indicators of the World Bank and cover the period from 2000–2020. We significantly contribute to the literature by examining the nonlinearities in the stock market development-growth nexus when institutional quality is the mediating variable. We established that, as long as institutional quality is below the threshold level, it serves as an impediment for financial markets to drive growth in the West African sub-region. A key implication is that the relationship between stock market development and economic growth in the West African sub-region is contemporaneous, and that the development of the stock market is relevant in the developmental agenda in the sub-region. Therefore, we recommend that at the policy level, countries in West Africa should design strategies that can improve their institutional structures in the areas of allocation of credit, increasing competition, and the implementation of proper regulations that will make it possible for financial markets to stimulate economic growth, as these seem to be important condition to drive growth in the long run.

Impact statement

Improving the financial sector is important to guarantee the sustainability of economic growth. This is not different from the Economic Community of West African States (ECOWAS). Regional blocs seek to accomplish this by developing robust and sound stock markets within a solid and healthy institutional framework. This study examines the effect of stock market developments under a strong institutional framework on the economic output of the ECOWAS region. The results show that a robust stock markets and ensuring more credit to the private sector can only improve the gross domestic product of ECOWAS member countries when there is a good institutional quality structure in place. This is crucial for ECOWAS member countries experiencing low manufacturing sector output. Robust institutional quality structures and enhanced credit to the private sector must be continually pursued by the ECOWAS to engender the growth of member economies.

1. Introduction

This study contributes to the ongoing research on the relationship between stock market development and economic growth in the ECOWAS region. According to studies, the effect on stock market development on economic growth in the region has documented mixed results. A definitive conclusion on the relationship between stock market development and economic growth in the region has not yet been established and where research is conducted to ascertain its true connection and the results are often disputed (Yartey & Adjasi, Citation2007). Although studies have found a positive relationship between stock market development and economic growth in the region (for example, Abdullahi & Fakunmoju, 2019; Asamoah, Citation2018), some studies on this relationship reveal negative effect on stock market development on economic growth. The findings are mixed because there are little empirical studies on the role of institutional quality in this relationship in question. It is been established in other jurisdictions that countries with weak institutional structures may suffer from growth-enhancing effect from the stock markets (see Assadzadeh & Pourqoly, Citation2013; Ogbuabor et al., Citation2020).

While classical theories assert that finance-growth nexus follows a demand-following hypothesis (see for instance, Hou & Cheng, Citation2010; Levine & Zervos, Citation1998; Pradhan et al. (Citation2013), another theory contend that the finance-growth nexus follows a supply-leading hypothesis (Levine & Zervos, Citation1998; Naik & Padhi, Citation2015 and among others; see: Demirgüç-Kunt & Levine, Citation1996). There have been few studies that used the Hansen (Citation2000) threshold regression to investigate the relationship between stock market development and economic growth, and none of these studies, to the best of the author’s knowledge, have focused on the mediating role of institutional quality in the relationship between stock market development and economic growth in the context of ECOWAS. It is important to assess the role of institutional quality in this relationship because investors and donor agencies make decisions on investing in countries by studying their institutional structures (Tang & Tang, Citation2018). Again, it is very significant to examine whether better institutional structures can influence the stock market development and growth nexus in ECOWAS. Countries with stronger political stability and higher government effectiveness receive a higher share of World Bank funds (Öhler & Nunnenkamp, Citation2014). Studies on ECOWAS have mostly concentrated on the relationship between stock market development and economic growth with no focus on the mediating role of institutional quality.

This research gap is the motivation for this study, which is to assess whether institutional quality has an effective role to play on why studies have documented inconsistencies of results in the relationship in question in the context of ECOWAS. We again used institutional quality to understand whether in the context of ECOWAS, the region is inclined to the demand-following or supply-leading hypothesis and how the region can leverage better on this source to reap the full benefits of the finance-growth nexus. In this study, we contribute significantly to the literature by assessing the mediating role of institutional quality in the stock market development and economic growth nexus in ECOWAS by seeking to answer the inconsistencies on previous studies in the region. By adding to the limited empirical studies on the role of institutional structures on this relationship, we shed more light on the institutional structures in the sub-region.

We contribute to literature by concentrating on the most robust stock markets in the region (Cote d’Ivoire, Nigeria, and Ghana), in contrast to most studies that concentrated on lesser stock exchanges in the region to examine this relationship. We employ Hansen (Citation1999, Citation2000) threshold regression which is able to decompose the role of institutional quality into low regime and high regime. This enable us to assess the effect on stock market development on economic growth where institutional qualities are low and where institutional qualities are high. The advantage of Hansen threshold regression is that it is based on asymptotic distribution theory and with the threshold estimation, the statistical significance of the identified thresholds can be empirically verified (Papageorgiou, Citation2002). The Hansen (Citation1999, Citation2000) threshold regression overcomes the limitations of quadratic terms which have been used in the past to measure thresholds. One disadvantage with the application of the quadratic terms was that the exact relationship and form at the point of inflection is ambiguous to identify making the validity of such results generally not reliable (Papageorgiou, Citation2002).

We contribute theoretically by applying financial liberalization theory by McKinnon (Citation1973) and (Shaw, Citation1973) financial repression theory to investigate the empirical findings derived from this research. We further compare our results to earlier studies where the mediating role of institutional quality is missing in the context of studies in ECOWAS. This will provide a better understanding of the link between stock market development and economic growth in the region. Aside the mediating role of institutional quality, we examine the threshold effect of the relationship in question. Policymakers in the ECOWAS region can effectively articulate the role of institutional structures on the association between stock market development and economic growth.

The findings of this study show that, as long as institutional quality is below the threshold level, it serves as an impediment for financial markets to drive growth in the West African sub-region. These findings can help ECOWAS heads of states as well as policy makers to improve on their institutional structures in the areas of allocation of credit, increasing competition, and the implementation of proper regulations that will make it possible for financial markets to stimulate economic growth, as these seem to be important condition to drive growth in the long run.

The remainder of this article is organized as follows. The next section reviews the pertinent literature. Section three focuses on the methodological framework. The fourth section discusses the empirical findings, and the final section concludes.

2. Literature review

To understand the relationship between the development of the stock market and economic growth in Africa, particularly in the ECOWAS sub-region where poverty is high, it is important to review the theoretical and empirical literature.

2.1. Theoretical review

The existing literature on financial development has furnished the academic community with theoretical explanations of the finance-growth nexus. The consensus among academics is that, financial systems can induce growth. In this section, we discuss theories of the relationship between financial development and economic growth.

Supply Leading Hypothesis: The supply leading hypothesis explicitly states that financial deepening can promote growth. The proliferation and creation of financial systems can increase savings and investment. When savings and investments increased, the effective accumulation of capital is enhanced. The supply leading hypothesis contends that when there is a well-functioning financial institution, it can bring economic efficiency; it can also lead to the creation and expansion of liquidity, savings mobilization, and enhancement of capital accumulation. Well-functioning financial institutions can lead to the transfer of available resources to more contemporary growth-inducing sectors from traditional or non-growth sectors. Robust financial institutions can promote skilled entrepreneurial response in these contemporary sectors of the economy. Modern theories concerning this relationship by applying various analytical methods in finance literature have established strong evidence that financial development promotes growth (Demirgüç-Kunt & Levine, Citation1996). According to Demirgüç-Kunt and Levine (Citation1996), it is important to encourage policymakers to prioritize financial sector policies and pay attention to the policy determinants of financial development as a mechanism for promoting economic growth.

Demand-Following Hypothesis: The demand-following hypothesis on the development of the financial market is nothing more a lagged response to economic growth. In other words, when there is growth, it generates demand for financial products. This shows that there is no need to develop financial markets because this may lead to a waste of resources. At this stage, resources can be channeled to a more useful purpose during the early stages of growth. The demand-following hypothesis suggests that once the economy advances, it will trigger an increased demand for financial products, which will invariably result in greater financial development. Some studies on the finance-growth nexus postulate that economic growth is a causal factor in the development of financial institutions. Some researchers believe that, as the real sector grows, there will be an increased demand for financial services that will stimulate the financial sector. One school of thought contends that the growth of the financial sector is an outcome of an economy experiencing a surge in output, an assertion that was recently renewed by Ireland (Citation1994) and Demetriades and Hussein (Citation1996). According to this alternative opinion, when there is any development in financial institutions, it is merely a response to a growing economy.

Stage of Development Theory: According to Patrick (Citation1966), the direction of causality between financial development and economic growth is dependent on the course of development. He explains that during the initial stages of development, financial development spurs growth; however, as real growth begins to appear in the economy, it will naturally create demand for financial services. The development theory stage suggests a demand-following association between financial sector and economic growth. When there is high economic growth, there is a demand for contemporary financial institutions/products. Thus, the financial market responds to such demands, and the level of demand for services in the financial sector is largely dependent on the growth of real output, monetization of agriculture, commercialization, and other traditional substance sectors.

Financial Liberalization Theory: According to McKinnon (Citation1973) and Shaw (Citation1973), government interventions in financial markets are seen as the major obstacle to the mobilization of savings, investment drive, and ultimately the growth of economies. The major criticism of financial liberalization theory emanates from the imperfect information paradigm. Some authors disagree with the assertion that an imperfect information paradigm examines financial development problems in the context of asymmetric information. They suggested that this is costly and can lead to credit rationing. According to Stiglitz and Weiss (Citation1981), asymmetric information can result in adverse selection and moral hazard. When there is adverse selection and moral hazard, it implies that when there are information asymmetries that bother on high interest rates, it can actually follow reforms in the financial sector as well as the implementation of policies that bother on financial liberalization in particular, which can cause investors to take risk on how to use their capital and eventually threaten the stable nature of the financial system. This can result in a financial crisis, although the feedback theory proposes two-way causality between financial development and economic growth.

Financial Repression Theory: This theory suggests that when there are a number of government regulations, laws, and some restrictions that are not market related, it hinders the effective functioning of financial intermediaries in their operations. Government policies that normally cause repression in the financial sector include ceilings in interest rates, liquidity ratio requirements, capital controls, high bank reserve requirements, credit ceilings, and market entry restrictions, government directions on credit allocations, and sometimes government ownership and domination of banks. Most economists believe that financial repression can prevent efficient capital allocation, which can negatively affect economic growth (Darrat & Al-Siowadi, Citation2010; Esso, Citation2010; Okpara, Citation2010).

2.2. Empirical literature review

The demand-following hypothesis and the supply-leading hypothesis theories form the foundation for the finance-growth nexus (Demirgüç-Kunt & Levine, Citation1996; Demetriades & Hussein, Citation1996). According to these theories, the development of the financial system leads to economic growth whiles another school of thought contends that the expansion of the economy leads to development of financial institutions (Demetriades & Hussein, Citation1996; Demirgüç-Kunt & Levine, Citation1996; Ireland, Citation1994). Empirical studies on the relationship between stock market development and economic growth in the ECOWAS region have been relatively limited. Theoretically, this relationship has been a subject of discussion in the academic space, which has resulted in opposing opinions. Earlier studies investigating this relationship reported mixed results regarding the causal linkage between them. Some studies have empirically documented that stock market development spurs economic growth, whereas others contend that it prevents growth.

The study by Abdullahi and Fakunmoju (Citation2019) is an example of an empirical investigation that supports the supply leading hypothesis in the ECOWAS region. Abdullahi and Fakunmoju (Citation2019) examine the nexus between stock market development and the performance of economic activities in West African countries. The study employed secondary data and applied the panel regression method of estimation within a period of 7 years across selected countries in the region. Findings from the study revealed that stock market indicators, that is, the ratio of market capitalization to gross domestic product, all-share index, and stock turnover, have positive effects on economic performance, while the corruption perception index has a negative effect on economic performance at the 5% level of significance. This shows that stock market development positively affects economic activities and leads to growth in the region. This study revealed that corruption affects the growth of the region. According to Asamoah (Citation2018), an economy that is expanding can lead to financial development, and the advancement in financial institutions can lead to economic development in Ghana. Asamoah (Citation2018) used the Vector Error Correction Models (VECM) and Granger Causality Models on monthly time series economic data between 2000 and 2012 to investigate the relationship between the Ghana stock exchange and economic growth. The study revealed that the development of the Ghana Stock Exchange had both short and long-run impacts on economic growth and that there was a bi-directional causality between stock market development and economic growth. This study provides evidence in support of the mutual impact or feedback hypothesis, which argues that financial sector development stimulates economic growth and that economic growth promotes financial sector performance, as found by a few studies in other contexts.

More studies in ECOWAS contend that stock market development promotes growth in the region (Adefeso et al., Citation2013; Ehigiamusoea & Lean, Citation2015). In Nigeria, Adefeso et al. (2013) investigated the association between stock market development and economic growth using data from 1980 to 2010. The study used a Vector Error Correction model and cointegration techniques for estimation analysis. The study finds a long-term relationship between stock market development and banking activity variables in Nigeria. The study further concludes that economic growth granger causes both stock market development and banking activity in Nigeria, thus supporting the demand-following hypothesis. This study suggests that policy-makers should focus their attention on economic growth through the implementation of suitable regulatory and macroeconomic policies to mitigate the foresable problems that will lead to the faster sustainability of economic growth and development in Nigeria.

In a country-specific study, some studies identify the supply-leading hypothesis to be the leading theory in the finance-growth nexus in the region (Abina & Maria, Citation2019; Nwamuo, Citation2018; Okoh & Eke, Citation2015). Okoh and Eke (2015) assessed the link between capital markets and GDP growth in Nigeria and revealed in their study that capital market variables are positively correlated and have a significant association with economic growth. Abina and Maria (Citation2019) studied for the period 1985–2017 on the relationship between stock market development and economic growth in Nigeria and found that capital market is a strong determinant of economic development. Furthermore, Nwamuo (Citation2018) reveals that capitalization and the number of deals have a positive effect on economic growth in Nigeria.

A study conducted in Cote d’voire and Nigeria by Ehigiamusoea and Lean (Citation2015) on stock market development and economic growth reported in their findings the presence of long-run cointegration between stock market/financial development and economic growth in the studied countries. The study revealed that stock market development/financial development granger causes economic growth in Cote D‘Ivoire while the reverse is the case for Nigeria. Thus, the supply-leading hypothesis is established for Cote D‘Ivoire while the demand-following hypothesis is also established for Nigeria. The study therefore suggests that Cote D‘Ivoire should make the financial sector more robust in order to make it more growth-enhancing. In Nigeria, there should be a re-evaluation of the policies in the financial sector as well as reforms with a view to repositioning the sector to help improve the growth of the economy. The limitation of this study is that, it is two-country analysis and cannot be used to generalize for the ECOWAS region. We seek to improve on this study by expanding the countries understudy.

Nabieu and Barnor (Citation2016) use Granger causality and Vector Error Correction Model (VECM) to determine whether stock market development is a cause of economic growth in Ghana by employing time series data from 2000 to 2012. Unlike previous methods that failed to determine the direction of influence in this relationship, their method simultaneously determines the relationship between stock market development and economic growth. The causality test showed a bidirectional relationship between the two variables, implying that there is a correlation between capital market development and economic growth in Ghana.

Adusei (Citation2014) used data from 2006 to 2013 to assess how the stock market contributes to economic growth in Ghana. The study employed the bounds cointegration and Granger causality methods, and the results of the cointegration test shows that there is a long-term relationship between stock market development and economic growth, while the findings of the causality test revealed unidirectional causality from stock market development to economic growth. Adusei’s (2014) study ended in 2013; therefore, we found a gap in knowledge based on the study period to confirm these results if it is the same as in 2023.

Using the Johansen cointegration test, Okonkwo et al. (Citation2014) investigated whether the role and contributions of the stock market in Nigeria induce growth in the economy. The data for the study were from 1981 to 2012, and the Johansen cointegration methodology was used to estimate the long-term equilibrium relationships among the variables. The study concluded that stock market size is an important indicator of how the stock market impacts economic growth and, indeed has a significant influence on economic growth. However, the study revealed that stock market capitalization and economic growth have no causal relationship. The results of this study support the no-feedback hypothesis.

Employing Ordinary Least Squares (OLS) regression and using data spanning 1984 to 2008, Popoola (Citation2014) examined the effects of stock market development on economic growth in Nigeria. The results of the estimation show that the explanatory variables account for approximately 95.77% of the variation in economic growth. The study revealed that growth in market capitalization, total market turnover, all share index, and openness of the Nigerian economy to foreign investment have a significant positive effect on economic growth at the 5% level of significance.

Although some studies identify positive effect of stock market development on growth in the ECOWAS region, others argue that, stock market development has little or no positive effect on economic growth in the West Africa region (see for instance, Menyah et al., Citation2014, Owusu, Citation2016; Ofori-Abebrese et al., Citation2016). Therefore, the demand-following hypothesis or the supply-leading hypothesis theories in the finance-growth nexus may not be effective determinant in policy decisions. According to Owusu and Odhiambo (Citation2014), the question of whether stock market development influences growth or it is growth that influences stock market development is not fully understood in the region. Their study employed the recently developed autoregressive distributed lag (ARDL) bounds testing approach and multi-dimensional stock market development proxies to examine this linkage. The study finds that, in the long run, stock market development and capital account liberalization policies have no positive effect on economic growth in Ghana. However, the study concluded that it is the increase in credit to the private sector, rather than stock market development that drives real sector development in Ghana.

Similarly, Owusu (Citation2016) examines the relationship between stock market evolution and sustainable economic growth in Nigeria by employing autoregressive distributed lag (ARDL)-bounds testing approach and a combined stock market indicators index to examine the relationship. He finds that, in the long run, the stock market has no positive effect on Nigeria’s economic growth.

Ofori-Abebrese et al. (2016) investigated the association between Stock Exchange and Economic Growth in Ghana. This study used the ARDL model coupled with the Granger causality test to examine this linkage for the period from 1991 to 2011. The finding of this study is that, in the long run, stock market development has a negative effect on economic growth, which was confirmed by the causality test that there was no relationship between stock market development and economic growth in Ghana during the study period.

Menyah et al. (Citation2014) used panel causality to examine the causal relations between stock market development and economic growth for some countries in Sub-Sahara Africa, which has Cote D‘Ivoire and Nigeria included in the study. This study reports the absence of causality running from stock market development to economic growth in Cote D‘Ivoire and Nigeria. The study of Jibril et al. (Citation2015) when they examined the impact of stock exchange development in Nigeria on economic growth used data that span for 20 years from 1990–2010. Their study applied ordinary least square (OLS) techniques. The stock market capitalization ratio was adopted as a proxy for market size, while the value-traded ratio and turnover ratio were used to capture market liquidity. The study revealed that market capitalization and the value-traded ratio have a negative correlation with economic growth, while the turnover ratio has a strong positive correlation with economic growth.

Despite the fact that most studies have found a positive relationship between stock market development and economic growth, some studies have found that stock market development has little or no impact on economic activities in the West African region (see for instance, Owusu & Odhiambo, Citation2014; Owusu, Citation2016; Ofori-Abebrese, Kamasa & Pickson, 2016; Asamoah, Citation2018 and among others). Most of these studies have found inconsistencies in their findings. In this study, we anticipate that, these inconsistencies in the results may be due to the non-existence of the role institutional quality plays in the stock market development and growth nexus in the region.

A thorough review of the literature in the context of ECOWAS shows that most studies are salient on the role of institutional quality in the stock market development and growth nexus. However, studies such as Effiong (Citation2015), and Omoteso and Ishola Mobolaji (Citation2014) in other jurisdictions have considered institutional quality as a control variable when dealing with the finance-growth nexus. Their study utilized the GMM method and the fixed and random effects method respectively, and realized that institutional quality, when coupled with stock market development, can promote economic growth. Second, the threshold level of institutional quality in the relationship in question is missing in the literature with regards to ECOWAS. In this study, we consider whether the effect of stock market development on economic growth in ECOWAS is conditioned on a certain institutional quality threshold.

In this study, we contribute to recent relationship between stock market development and economic growth studies in the ECOWAS region by adopting Hansen (Citation1999, Citation2000) threshold regression method. When compared to other frequently used methods to examine the finance-growth nexus (Ofori-Abebrese et al., 2016; Owusu, Citation2016; Owusu & Odhiambo, Citation2014), the Hansen (Citation1999, Citation2000) threshold provides more superior, consistent, and robust results in the threshold terrane because the nature of the nonlinear relationship is not imposed on the model unlike previous methods. Furthermore, the literature reviewed shows that the mediating role of institutional quality in the stock market development and growth nexus is not replete in the literature in the context of studies in ECOWAS despite the fact that institutional structures play a critical role in nation’s development. Our study therefore addresses these limitations.

3. Estimation techniques and data properties

This section presents the methodological framework adopted to analyze the data-set used in this study.

3.1. Threshold regression

The estimation of threshold regression has in the past been dominated by the use of quadratic terms; however, one disadvantage with the application of the quadratic terms was that the exact relationship and form at the point of inflection is ambiguous to identify because the validity of such results is generally not reliable (Hansen, Citation1999, Citation2000). Hansen’s (Citation1999, Citation2000) threshold regression estimation overcomes this deficiency because the nature of the nonlinear relationship is not imposed on the model. Another advantage of the Hansen threshold estimation is that the statistical significance of the identified thresholds can be empirically verified. The uniqueness of Hansen threshold regression is that it is based on asymptotic distribution theory (Papageorgiou, Citation2002).

We begin by specifying a basic economic growth model as;

(1)

(1)

GDP is GDP per capita, SMD is the stock market development indicator (market capitalization, stock turnover ratio, and stock traded value), and IQ is the institutional quality variable. We augment this functional relationship to include; foreign direct investment, inflation and domestic credit to the private sector, EquationEquation (1)(1)

(1) becomes,

(2)

(2)

We compactly rewrite EquationEquation (2)(2)

(2) as;

Where is a vector of the other control variables as indicated in EquationEquation (2)

(2)

(2) (including a constant term), θ, and α are the parameters to be estimated, and

is the idiosyncratic error term. ′θ′ measures the effect of the stock market development (SMD) on economic growth (GDP per capita); we augment EquationEquation (2)

(2)

(2) so that the growth effect of stock market development is refereed by institutional quality. Therefore, institutional quality is our threshold variable given as ′π′, which is a continuous distribution. The parameters in the equation are therefore split into two (2) regimes conditional on ′π′. We specify this as;

(3)

(3)

Where I(.) denotes the indicator function of the dummy variable that adopts the value of 1 when the argument of the indicator function is satisfied and 0 when the argument is not satisfied. The threshold variable is represented by π whiles the value of the threshold is denoted by ’. EquationEquation (3)

(3)

(3) permits for the effect of stock market development on economic growth to be disintegrate into two (2). The first effect assesses the impact when the level of stock market development is below the threshold, and the second analyze the impact when stock market development is beyond the threshold.

and

measure the effect of stock market development on economic growth in both low regime and high regime periods respectively. Where π ≤

and π ≥

denotes both regimes respectively

Ibrahim and Alagidede (Citation2018) and Alagidede et al. (Citation2018), began by testing the existence of a threshold against linearity. In this study, we followed the procedure of Alagidede et al. (Citation2018) and Ibrahim and Alagidede (Citation2018) by testing the significance of the threshold parameter, which is expressed in equation form as =

and

.

We, therefore, rewrite EquationEquation (3)(3)

(3) as

(4)

(4)

where

=

=

denotes the threshold effect. We, therefore, solve it as

→ 0 when n →

→

we again specify EquationEquation (3)

(3)

(3) in a matrix form as an n × 1 vector of Y and ε by stacking them and then in an n × m matrices X and Y, respectively. We, therefore, estimate again EquationEquation (4)

(4)

(4) as;

(5)

(5)

θ, δ, and is derived by the least-squares estimator (θ, δ,

). This derivation therefore reduces the sum of squares errors in EquationEquation (6)

(6)

(6) as;

(6)

(6)

The threshold test is therefore restricted to be a bounded set [= ψ in the minimization process. This study, therefore, employ the concentration approach application to evaluate the least square estimate (θ, δ,

) where

minimizes

(

) which is uniquely determined as;

(7)

(7)

Where =

{

} the slopes are estimated as

=

(

) and

=

(

) the likelihood ratio test is therefore employed by this study, we, therefore, test the hypothesis

=

applying the likelihood test ratio

(8)

(8)

The null hypothesis was rejected for large values of (

the reliability of the threshold was mainly determined by the values of the confidence interval. Its determination is by employing the Wald or ‘t’ test statistics. Hansen (2000) posits that, asymptotic sampling distribution depends on unknown estimators. The Wald statistics may not be an adequate determinant because it has finite sample performance, which is likely to exacerbate if the parameter has a region with a failed identification. Therefore, we resort to Hansen’s (2000) newly developed threshold technique to address the problem. An asymptotic confidence level (c) for ϒ employing the

(ϒ) set at

= {ϒ:

(ϒ) ≤ C}

One of the preconditions of Hansen’s (2000) threshold regression estimate is that the variables under study should be stationary. Therefore, we determine the order of integration of the variables using Levin-Lin-Chu (LLC), Im-Pesaran-Shin (IPS), ADF-Fisher chi-square, and PP-Fisher chi-square.

3.2. Data and statistical properties

In this study, we utilized three ECOWAS member states (Ghana, Côte d‘Ivoire, and Nigeria) for the period 2000-2020 for the analysis due to the availability of consistent data for these countries. These countries are chosen because they have the most developed stock markets in West Africa and are considered the frontier markets in the sub-region. The annual data were sourced from the World Bank’s World Development Indicators. We employed stock market capitalization (MC), stock turnover ratio (STO), and stock traded value (TVL) to represent stock market development, and per capita gross domestic product (GDP) to represent economic growth as used by Ibrahim and Alagidede (Citation2018), and Alagidede et al. (Citation2018). Following King and Levine (Citation1993), and Demetriades and Hussein (Citation1996), we also introduce some control variables. These are inflation (INF), the ratio of foreign direct investment (FDI) to GDP, and domestic credit to the private sector. The inclusion of domestic credit to the private sector measures the overall relationship between financial development and economic growth. We employed Principal Component Analysis (PCA) to develop one index to represent institutional quality (IQ) from the six indicators gleaned from the World Governors’ Indicators (WGI), which is shown in Appendix 1.

3.2.1. Descriptive statistics

This section discusses the summary statistics of the variables involved in investigating the relationship between stock market development and economic growth in ECOWAS. presents the statisticds. From , it can be observed that all variables have positive average values. The summary statistics indicate that among the ECOWAS sub-regions, domestic credit to the private sector has the highest mean value (13.03), while stock traded value has the lowest (0.728). GDP has a mean of 2.31 with the highest value of 3.00 and the lowest value of −7.60. This means that the contributions of GDP to economic growth among the ECOWAS member countries are not encouraging. Market capitalization has a mean value of 12.13% of GDP, with the highest/lowest values of 30.80% and 2.48%, respectively. This shows that in the sub-region, the stock market is still in its infancy since market capitalization is relatively small. The stock turnover ratio has a mean value of 6.90%, with a maximum of 34.78% and minimum of 0.35%. Inflation has a mean value of 10.15%, which means that it is difficult to achieve single-digit inflation, which is one of the conditions for the introduction of a single currency.

Table 1. Basic statistics of the variables under study.

This justifies the reason for exploring the introduction of the ‘ECO’ from an ex-post perspective. Foreign direct investment in the sub-region is relatively low; the mean value recorded for FDI is 2.55%, with a maximum value of 9.46% and a minimum value of 0.19%. Domestic credit to the private sector (DCPS) is 13.03%, which indicates that the private sector has been regarded as the engine of growth in West Africa. The mean value of 13.03% for domestic credit to the private sector is relatively high, with a maximum value of 21.13% and a minimum value of 8.08% whereas the institutional quality variable has a mean of 1.4% with a maximum value of 3.5% and a minimum value of −3.2%. This implies that the institutional structures in the sub-region are relatively weak. In other words, institutional structures are not as robust as they are in the developed countries. Based on the standard deviation, inflation is the most volatile (8.40%), while the total value traded on the stock market is the least volatile (0.98%). In addition, the results indicate that, with the exception of GDP, all the variables have positive skewness. Furthermore, with the exception of GDP and domestic credit to the private sector, which have a normal distribution, all other series failed to conform to the Gaussian distribution. In general, data are not normally distributed based on skewness and kurtosis.

3.2.2. Stationarity test of the series

The Levin-Lin-Chu (LLC), Im-Pesaran-Shin (IPS), ADF-Fisher chi-square and PP-Fisher chi-square unit root test results are presented in . The null hypothesis of the presence of unit roots in GDP per capita, stock turnover ratio, stock traded value, foreign direct investment, and domestic credit to the private sector variables cannot be rejected by using the Levin-Lin-Chu (LLC), Im-Pesaran-Shin (IPS), ADF-Fisher chi-square and PP-Fisher chi-square at levels with intercepts only and with intercepts and trends. This indicates that at the 5% significance level, all the variables are not stationary at levels except for market capitalization and inflation, which are stationary at levels. This makes it possible for all the other variables, with the exception of market capitalization and inflation, to be differenced to make the variables stationary. However, when all the variables are differenced once, they become stationary. This is manifested by a p-value of less than 5%. These results, confirm that GDP per capita, stock turnover ratio, stock traded value, foreign direct investment and domestic credit to the private sector variables are I (1) variables, unlike the other two variables, market capitalization and inflation.

Table 2. Stationarity test.

3.2.3. Correlation analysis

Correlation analysis mitigates the problems of multicollinearity and endogeneity (when the independent variables themselves affect each other) associated with a number of econometric models. Therefore, this study conducted a correlation analysis to critically examine the magnitude, strength, and nature of co-movements between and among stock market development and economic growth variables in the ECOWAS sub-region. Correlation coefficients can take any value from +1 to −1, with the sign of the coefficient indicating the direction of the relationship between the variables used to establish the relationship between stock market development and economic growth. A positive coefficient implies that the variables move in the same direction whereas a negative coefficient indicates the movement of variables in opposite directions (Stead, 2007). presents the empirical correlation matrix between stock market development and economic growth indicators in the ECOWAS sub-region from 2000–2020.

Table 3. Correlation matrix.

As shown in , GDP correlates significantly and positively with the stock turnover ratio and stock traded value in the ECOWAS sub-region. GDP has a positive but insignificant relationship with market capitalization, foreign direct investment and domestic credit to the private sector. However, it had a negative and insignificant relationship with inflation. Market capitalization, stock turnover ratio, and stock traded value, which represent stock market development, have a positive and significant relationship with domestic credit to the private sector, which is used as proxy for financial development. However, the impact of the stock turnover ratio on domestic credit to the private sector is not significant in the ECOWAS region. These results indicate a positive correlation between banking sector development and stock market development indicators. This can be explained by the positive coefficients found in co-movements between market capitalization (MCAP) with a coefficient value of 0.34 (0.0063), stock traded value of 0.30 (0.0149) and banking credit to the private sector. Therefore, these results validate the findings of Demirgüç-Kunt and Levine (Citation1996) and Levine and Zervos (Citation1998), who postulated that stock market development measures were positively correlated with banking sector development measures. There is a negative and insignificant correlation between GDP and inflation. There is a negative and statistically significant relationship between market capitalization (MC), stock traded value (TVL) and institutional quality (IQ) with coefficients of −0.270 (0.0320) and −0.276 (0.0284), respectively. Stock turnover ratio (STO) also has a negative correlation with IQ, albeit with an insignificant P-value. This shows that stock market development is affected by institutional quality within the sub-region. Inflation, foreign direct investment and domestic credit to the private sector have positive and statistically significant correlations with institutional quality (IQ) with coefficients of 0.276 (0.0283), 0.009 (0.0000), and 0.442 (0.0003), respectively. This shows that when institutional quality is good, FDI and financial institutions thrive in the sub region. Since most of the correlation coefficients were at most 66%, it can be confirmed that no multicollinearity existed between or among the variables used to establish the relationship between stock market development and economic growth in ECOWAS. P-values are reported in the parentheses.

4. Results and discussion

4.1. Threshold estimation results

This section discusses the results of the relationship between stock market development and economic growth when the institutional quality index is the threshold variable. First, we attempt to establish the statistical significance of the threshold estimate through the P-value by employing the bootstrap method with 5000 replications and 15% trimming. The results of the threshold model are displayed in . We find the threshold in the model estimated because the bootstrap P-value indicates that the P-value is statistically significant at any conventional level of significance (0.0018). This means that we are unable to rely on the global OLS estimator, which we use as a comparator in because of the existence of asymmetry.

Table 4. Results of the threshold regression when Institutional Quality Index is the threshold variable (dependent variable-GDP).

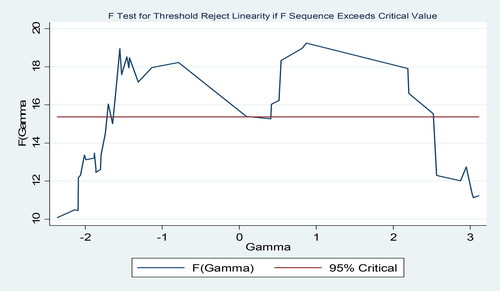

provides a graphical representation of the F-test for the existence of a threshold in a model. In the Figure, the F-statistics cross the critical line in the model, which indicates the existence of a threshold in the model. We can ascertain that there are discontinuities in the relationship between stock market development and economic growth in the ECOWAS sub region when the institutional quality index is the threshold variable.

Figure 1. F test for threshold. Source: Figure generated from Stata 14 (A copyright license was obtained for its use in the estimation process).

From , the point estimate of the threshold value of institutional quality for the three countries under study is −2.092, with a corresponding 95 percent confidence interval [−2.36113811, 3.16721511] for the West African region. This implies that when the region has a threshold value less than −2.092, the region is classified as having weak institutions and therefore categorized into the low institutional quality regime, while values greater than −2.092 are classified as having a high institutional quality regime. First, we discuss the threshold model, which uses the overall level of economic growth as a dependent variable, as demonstrated in and reported in . The dictate of this model is that any improvement towards the institutional structures in the region would enable the development of the stock market to promote growth. Concerning the moderating effect of institutional quality on stock market development and the economic growth nexus, beginning with our variable of interest, we establish that market capitalization (MC), stock turnover ratio (STO), and stock traded value (TVL) have a negative and statistically significant relationship with economic growth when institutional quality is below the threshold variable. The coefficients of market capitalization, stock turnover ratio, and stock traded value with their corresponding standard errors are −21.357 (8.702), −21.011 (8.247), −20.095 (8.154), respectively, implying that a 1% increase in market capitalization, stock turnover ratio, and stock traded value will reduce GDP by 21.35%, 21.01%, and 20.09%, respectively, below the threshold level. However, when institutional quality is above the threshold, market capitalization {0.343 (0.220)}, stock turnover ratio {0.280 (0.109)}, and stock traded value {0.311 (0.120)} have positive and statistically significant relationships with economic growth. This finding indicates that higher institutional structures in the ECOWAS sub-region can help stock market development to promote economic growth. This implies that weak institutional structures in the region have a profound negative effect on how stock market development influences economic growth. The findings that weak institutional quality hinders economic growth support the work of Assadzadeh and Pourqoly (Citation2013), Ogbuabor et al. (2020). The results clearly support financial development theory, which contend that financial development under good institutional framework enhances growth (McKinnon, Citation1973; and Shaw, 1973). This is made evidenced when institutional quality is beyond the threshold; stock market development has a positive effect on growth in the region.

Concerning the other control variables, we find no relationship between inflation and economic growth for both regimes, which is below the threshold level and above the threshold level; however, when the effect on economic growth is positive below the threshold, it has a negative effect above the threshold, albeit insignificant. We establish that below the threshold, FDI has a negative and statistically significant relationship with GDP, but no relationship exists beyond the threshold. This implies that when institutions are weak, a 1% increase in FDI will reduce GDP by 1.86%. This observation can be attributed to weaker regulations on capital flights since, in West Africa; our regulations on capital flights are not strong enough to prevent investors from such activities. Furthermore, the negative effect of stock market development on growth in the West African region when FDI is below the threshold level can be attributed to investors’ lack of confidence in doing business which hinders spillover of knowledge, technology, and innovation that can impact productivity and growth (Bournakis et al., Citation2018).

Domestic credit to the private sector, which is used here to gauge the overall effect on financial development, has a negative and statistically significant relationship with GDP when institutional quality is below the threshold; however, it has a strong and positive relationship with economic growth beyond the threshold, that is, a 1% increase in domestic credit to the private sector, increases GDP in the sub-region by 1.62% above the threshold. This implies that good institutions help financial institutions to promote economic growth in the ECOWAS region. The relationship between financial development, which is proxy in this study as domestic credit to the private sector, and economic growth was asserted authoritatively in the theoretical foundation of the financial development model propounded by McKinnon (Citation1973) and Shaw (1973), which states that financial development promotes growth, which invariably accounts for the strong positive relationship between these two variables in the sub-region when better institutional structures are instituted. Chen and Chen (Citation2018) argue that when economies are characterized by good institutional structures, it increases the likelihood of investors investing in the stock markets. This again can be attributed to the financial development model, which contends that good institutions drive economic agents to work harder to improve on their capital accumulation.

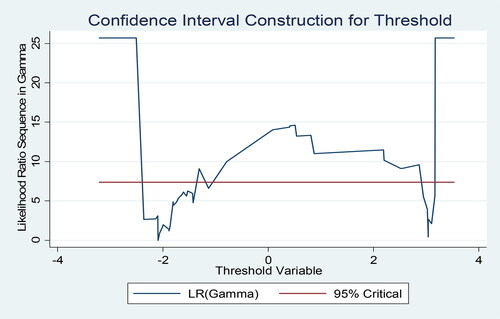

Investing in economies where institutional quality is high has several benefits for the various stakeholders. Investors have confidence in the economic system and risk in generating revenue is minimised. Policy makers in the ECOWAS region should strengthen the institutional structures and put in measures to entrench democratic principles, clamp down corruption in our institutions to foster economic growth. These findings will be beneficial to ECOWAS heads of states when making disbursement decisions on revenue generation from taxes. We support studies that have documented that higher institutional quality helped the stock market development to have a greater positive effect on growth in other jurisdictions. We present the graphical presentation of the confidence interval construction of the thresholds in .

Figure 2. Graphical representation of confidence interval construction of the threshold. Source: Generated by Stata 14.

5. Conclusions and policy recommendations

The paper investigated whether the relationship between stock market development and economic growth in the ECOWAS region is conditioned by institutional quality using Hansen (2000) threshold regression method. We categorized institutional quality into low regime and high regime to assess both impact on how stock market development influences growth in low regime and high regime respectively. The lack of empirical consensus on whether stock market development influences economic growth in the ECOWAS region necessitated this investigation. The missing link in this relationship motivated this study, which was to investigate whether institutional quality plays a helpful, benign, or malign role in the stock market development and economic growth relationship. We contribute to the literature in the context of ECOWAS by providing some clarity to previous studies. We departed from most studies on stock market development and economic growth in ECOWAS that focus on the relationship without factoring into the link the role of institutional quality. We also employ Hansen (2000) threshold regression which provides more robust results. We contribute theoretically to the literature by highlighting the theories in this study (Financial liberialization theory, financial repression theory, demand-following hypothesis and supply-leading hypothesis) to appreciate the empirical findings on how institutional quality mediate the stock market development and economic growth nexus in ECOWAS. We extend our understanding on the theories of the finance-growth nexus by using institutional quality to examine the relationship between stock market development and economic growth. ECOWAS heads of states and important stakeholders in the stock markets will benefit from this study finding because the findings explain the role of institutional quality on the finance-growth nexus, which will allow for proper and effective policies in the area of fiscal, regulatory, and monetary policies to be formulated.

We have drawn significant findings from the analysis, in the macro-level analysis, the empirical results indicate a significant institutional quality threshold in the stock market development-economic growth nexus. In a micro-level analysis, for institutions below the threshold, stock market development has a negative and significant effect on economic growth. However, stock market development has statistically significant influence on the growth of institutions above the threshold level. These findings suggest that the stock market development and economic growth nexus is contingent on institutional quality. Thus, the quality of the stock market is important for economic growth, and better institutional quality is effective in ensuring the efficiency of stock exchanges in promoting growth. The results also demonstrate that low-quality institutions tend to distort the ability of foreign direct investment (FDI) and domestic credit to the private sector, which is used in this study as a proxy for financial development, to have any positive significant effect on growth. We established that high-quality institutions enhance the ability of domestic credit to the private sector to positively influence growth while inflation is indifferent in the relationship between stock market development and economic growth when institutions serve as mediating variables. The empirical findings are robust to alternative economic growth and the dimensions of institutional quality variables as well as the estimation technique used in this study.

Given these results, we establish that there are discontinuities in the relationship between stock market development and economic growth in the ECOWAS sub-region. As long as institutional quality variables are below the threshold, it serves as an impediment for financial markets to drive growth in the West African sub-region. This is correct because, overall, as countries move beyond the institutional quality threshold, investors may demand more financial services, thereby improving the intermediation of the financial markets, which invariably may be an enabler for financial institutions to impact growth in West Africa.

Another key implication is that the relationship between stock market development and economic growth in the West African sub-region is contemporaneous, and that the development of the stock market is relevant to the developmental agenda in the sub-region. Therefore, at the policy level, countries in West Africa should design strategies that can improve the allocation of credit, increase competition, and implement proper regulations that will make it possible for financial markets to stimulate economic growth, as these seem to be important conditions to drive growth in the long run.

While the relationship between stock market development and economic growth is well documented in the extant literature, empirical literature is silent on the nonlinearities in the stock market development and economic growth relationship caused by the threshold variables in the West African sub-region.

Our findings are of crucial importance to the heads of ECOWAS states with regard to the optimum level of institutional quality needed to vigorously improve the economy through financial markets. From Critical policy decision making, these three leading countries in ECOWAS should make frantic efforts to make their institutions work effectively and become robust, which will allow these economies to reap the full anticiapted benefits of stock markets to induce higher growth. That is, considering that financial systems accelerate economic growth when controlling for corruption, government effectiveness, and political stability, rule of law, regulatory quality, voice and accountability are improved, it is recommended that policy makers and governments in ECOWAS institute policy measures geared toward improving the effectiveness and performance of institutions in the sub-region.

The main policy implication of our findings is that institutional structures in the ECOWAS region require reforms for stock market development to have a significant role to play in growth process of the sub-region. Policymakers should focus on how to enhance the efficiency of the institutions. This can be achieved by instituting stringent measures such as proper accountability from public sector workers, punitive measures for those who infrindge on our laws, entrenching rule of law to boost confidence in the economic activities and also ensuring transparency of the stock markets which will enable effective information flow between market participants. Again the stock stock market in the ECOWAS region needs reform in the area of size. The size of the stock market in the region is significantly small. We recommend that, the not-too-significant listing requirements should be removed to entice more firms to consider been listed on the stock market. This can help improve its size with possible concomitant positive contribution to the growth process of the ECOWAS region.

Despite the fact that the Hansen (2000) threshold regression produces reliable, consistent, and robust results, its limitation is that it is unable to identify causality in series, quantifying information flows among variables, lead/lag time switches in frquency time domains. Due to these limitations, we are unable to identify causality in stock market development and economic growth relationship as well as the direction of information flow in this relationship in question. Our future study will be focusing on the information flow between stock market development and economic growth when institutional quality serves as mediating variable in the ECOWAS region.

Author contributions

Conception and design: Richard Eshun (Corresponding author). Analysis and interpretation of the data: Richard Eshun (Corresponding author). The drafting of the paper: Richard Eshun (Corresponding author) Revising it critically for intellectual content: Richard Eshun (Corresponding author). Final approval of the version to be published: George Tweneboah. Richard Eshun, the corresponding author and George Tweneboah, who read the final work, agree to be accountable for all aspects of the work.

Disclosure statement

Richard Eshun and George Tweneboah declare that this manuscript is original, has not been published before and is not currently being considered for publication elsewhere. We wish to confirm that there are no conflicts of interest associated with this publication, and there has been no significant financial support that could have influenced its outcome.

Data availability statement

The data for this work were sourced from the World Development Indicators from the World Bank. Data is available from the authors upon request.

Additional information

Funding

Notes on contributors

Richard Eshun

Richard Eshun is a Lecturer at the School of Graduate Studies, Ghana Baptist University College, Kumasi, Ghana. He holds a Master of Business Administration (MBA, Finance) degree from the Kwame Nkrumah University of Science and Technology (KNUST) in Kumasi, Ghana. He also obtained a Master of Management by Research degree from the Wits Business School at the University of Witwatersrand, Johannesburg. Currently, Richard is pursuing a PhD at the Wits Business School, focusing on time-series modelling. His research interests include economic integration and asymmetry. Email: [email protected]

George Tweneboah

Dr. George Tweneboah holds the position of Senior Lecturer at the Wits Business School, located within the University of Witwatersrand, Johannesburg. He has prolific publication records in well-regarded academic journals and provides daily supervision to PhD students. Dr.Tweneboah’s research interests are primarily centered on various areas, including time-series modelling, exchange rate management, economic integration, financial market development, and fiscal sustainability. Email: [email protected]

References

- Abdullahi, I. B., &Fakunmoju, Sk. (2019). Stock market development and economic performance of west African countries: a dynamic panel data analysis. Journal of Management, Economics and Industrial Organization, 3(3), 12–26.

- Abina, A., & Maria, L. (2019). Capital market and performance of Nigerian economy. International Journal of Innovative Finance and Economic Research, 7(2), 51–66.

- Adefeso, H. A., Egbetunde, T., & Alley, I. (2013). Stock market development and growth in Nigeria: A causal analysis. Arabian J. Bus. Manag. Rev, 2, 78–94.

- Adusei, M. (2014). Does stock market development promote economic growth in Ghana. International Journal of Economics and Finance, 6(6), 119–126. https://doi.org/10.5539/ijef.v6n6p119

- Alagidede, P., Mensah, J. O., & Ibrahim, M. (2018). Optimal deficit financing in a constrained fiscal space in Ghana. African Development Review, 30(3), 291–303. https://doi.org/10.1111/1467-8268.12337

- Asamoah, G. (2018). Impact of Ghana stock exchange development on economic growth: a robust time series econometric analysis. Interdisciplinary Research Journal of Theology, Apologetics, Natural & Social Sciences, 1(1 & 2).

- Assadzadeh, A., & Pourqoly, J. (2013). The relationship between foreign direct investment, institutional quality and poverty: case of MENA countries. Journal of Economics, Business and Management, 1(2), 161–165. https://doi.org/10.7763/JOEBM.2013.V1.35

- Bournakis, I., Christopoulos, D., & Mallick, S. (2018). Knowledge spillovers and output per worker: An industry-level analysis for OECD countries. Economic Inquiry, 56(2), 1028–1046. https://doi.org/10.1111/ecin.12458

- Chen, H.-Y., & Chen, S.-S. (2018). Quality of government institutions and spreads on sovereign credit default swaps. Journal of International Money and Finance, 87, 82–95. https://doi.org/10.1016/j.jimonfin.2018.05.008

- Darrat, A. F., & Al-Sowaidi, S. S. (2010). Information technology, financial deepening and economic growth: Some evidence from a fast growing emerging economy. Journal of Economics and International Finance, 2(2), 028–035.

- Demetriades, P. O., & Hussein, A. K. (1996). Does financial development cause economic growth? Time series evidence from 16 countries. Journal of Development Economics, 51(2), 387–411. https://doi.org/10.1016/S0304-3878(96)00421-X

- Demirgüç-Kunt, A., & Levine, R. (1996). Stock market, corporate finance and economic growth: An overview. The World Bank Economic Review, 10(2), 223–239. https://doi.org/10.1093/wber/10.2.223

- Effiong, E. (2015). (). Financial development, institutions and economic growth: Evidence from Sub-Saharan Africa. MPRA Paper No. 66085.

- Ehigiamusoea, K. U., & Lean, H. H. (2015). Does Financial Development Promote Economic Growth in West Africa? Evidence from Cote D’Ivoire and Nigeria [Paper presentation]. Proceedings of USM International Conference of Social Sciences (USM-ICOSS) 2015,

- Esso, L. J. (2010). Cointegrating and causal relationship between financial development and economic growth in ECOWAS countries. Journal of Economics and International Finance, 2, 036–048.

- Hansen, B. E. (2000). Sample splitting and threshold estimation. Econometrica, 68(3), 575–603. https://doi.org/10.1111/1468-0262.00124

- Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. Journal of Econometrics, 93(2), 345–368. https://doi.org/10.1016/S0304-4076(99)00025-1

- Hou, H., & Cheng, S. Y. (2010). The roles of stock market in the finance-growth nexus: time series cointegration and causality evidence from Taiwan. Applied Financial Economics, 20(12), 975–981. https://doi.org/10.1080/09603101003724331

- Ibrahim, M., & Alagidede, P. (2018). Nonlinearities in financial development–economic growth Nexus: Evidence from Sub-Saharan Africa. Research in International Business and Finance, 46, 95–104. https://doi.org/10.1016/j.ribaf.2017.11.001

- Ireland, P. N. (1994). Money and growth: An alternative approach (pp. 47–65). American Economic.

- Jibril, S. R., Salihi, A. A., Wambai, U. S., Ibrahim, F. B., Muhammad, S., & Ahmad, T. H. (2015). An assessment of Nigerian stock exchange market development to economic growth. American International Journal of Social Science, 4(2), 51–58.

- King, R. G., &Levine, R. (1993). Finance, entrepreneurship and growth. Journal of Monetary Economics, 32(3), 513–542. https://doi.org/10.1016/0304-3932(93)90028-E

- Levine, R., & Zervos, S. (1998). Stock markets, banks, and economic growth. American Economic Review, 88(3), 537–558.

- McKinnon, R. (1973). Money and capital in economic development. Brookings Institution, Washington, District of Columbia.

- Menyah, K., Nazlioglu, S., & Wolde-Rufael, Y. (2014). Financial development, trade openness and economic growth in African countries: new insights from a panel causality approach. Economic Modelling, 37(2), 386–394. https://doi.org/10.1016/j.econmod.2013.11.044

- Nabieu, G. A., & Barnor, C. (2016). The effect of stock market performance on economic growth in Ghana. International Journal of Financial Economics, 5(1), 12–32.

- Naik, P. K., & Padhi, P. (2015). On the linkage between stock market development and economic growth in emerging market economies: Dynamic panel evidence. Review of Accounting and Finance, 14(4), 363–381. https://doi.org/10.1108/RAF-09-2014-0105

- Nwamuo, C. (2018). Impact of capital market on economic growth in Nigeria: An empirical analysis. IOSR Journal of Economics and Finance, 9(5), 48–59.

- Ofori-Abebrese, G., Kamasa, K., & Pickson, R. B. (2016). Investigating the Nexus between stock exchange and economic growth in Ghana. British Journal of Economics, Finance and Management Sciences, 11(1).

- Ogbuabor, J. E., Orji, A., Manasseh, C. O., & Anthony-Orji, O. I. (2020). Institutional quality and growth in West Africa: What happened after the great recession? International Advances in Economic Research, 26(4), 343–361. https://doi.org/10.1007/s11294-020-09805-0

- Öhler, H., & Nunnenkamp, P. (2014). Needs-based targeting or favoritism? The regional allocation of multilateral aid within recipient countries. Kyklos, 67(3), 420–446. https://doi.org/10.1111/kykl.12061

- Okoh, J., & Eke, R. (2015). Capital market and economic growth nexus: Evidence from Nigeria. IOSR Journal of Business and Management, 17(11), 31–38.

- Okonkwo, O. N., Ogwuru, H. O., & Ajudua, E. I. (2014). Stock market performance and economic growth in Nigeria: An empirical appraisal. European Journal of Business and Management, 6, 33–42.

- Okpara, G. C. (2010). The effect of financial liberalization on selected macroeconomic variables: Lesson from Nigeria. The International Journal of Applied Economics and Finance, 4(2), 53–61. https://doi.org/10.3923/ijaef.2010.53.61

- Omoteso, K., & Ishola Mobolaji, H. (2014). Corruption, governance and economic growth in Sub-Saharan Africa: A need for the prioritisation of reform policies. Social Responsibility Journal, 10(2), 316–330. https://doi.org/10.1108/SRJ-06-2012-0067

- Owusu, E. L. (2016). Stock Market and sustainable economic growth in Nigeria. Economies, 4(4), 25. https://doi.org/10.3390/economies4040025

- Owusu, E. L., & Odhiambo, N. M. (2014). Stock market developments and economic growth in Ghana: An ARDL-bound testing approach. Applied Economics Letters, 21(4), 229–234. https://doi.org/10.1080/13504851.2013.844315

- Papageorgiou, C. (2002). Trade as a threshold variable for multiple regimes. Economics Letters, 77(1), 85–91. https://doi.org/10.1016/S0165-1765(02)00114-3

- Patrick, H. T. (1966). Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change, 14(2), 174–189. https://doi.org/10.1086/450153

- Popoola, O. T. (2014). The effects of stock market on economic growth and development of Nigeria. Journal of Economics and Sustainable Development, 5(15).

- Pradhan, R. P.,Arvin, M. B.,Bele , S., &Taneja, S. (2013). The stock market development on inflation and economic growth of 16 Asian countries, A panel VAR approach. Applied Econometrics and International Development, 13(1), 203–220.

- Shaw, E. (1973). Financial deepening in economic development. New York: Oxford University Press.

- Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. Oxford Review of Economic Policy, 5(4), 55–68. https://doi.org/10.1093/oxrep/5.4.55

- Tang, R., & Tang, S. (2018). Democracy’s unique advantage in promoting economic growth: Quantitative evidence for a new institutional theory. Kyklos, 71(4), 642–666. https://doi.org/10.1111/kykl.12184

- Yartey, C. A., & Adjasi, C. K. (2007). The institutional and macroeconomic determinants of stock market development in Africa. In Okpara, J. (Ed.), Management and economic development in Sub-Saharan Africa: Theoretical and applied perspectives. Adonis and Abbey.