?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Societies have witnessed significant shifts in perceptions of gender diversity and gender equality. Consequently, researchers have increased interest in understanding the impact of board of director (BOD) gender diversity on various aspects of social and economic life, including corporate social responsibility (CSR). Although several studies have explored the relationship between BOD gender diversity and social responsibility, research in this area is still limited and suffers from a lack of consistency in findings. In addition, studying the financial performance as a mediating variable provides a more complex and detailed view of this relationship. This article aims to investigate and analyse the effect of BOD gender diversity on CSRD, either directly or indirectly, by financial performance as a mediator. This study investigates a panel data analysis with a sample of 31 companies listed on the Palestine Stock Exchange from 2012 to 2021. This study used the Baron and Kenny approach to test the mediator effect for financial performance between BOD gender diversity and CSR disclosure (CSRD). The results show a significant positive direct relationship between BOD gender diversity and CSRD, and a significant positive direct relationship between BOD gender diversity and financial performance. Furthermore, the results indicate that financial performance partially mediates the relationship between BOD gender diversity and CSRD in Palestinian companies. These results may encourage companies to promote gender diversity in their structures and strategies and implement policies for recruiting women to corporate boards, which has a positive impact on the financial and social sustainability of the organization.

IMPACT STATEMENT

The research paper “Board Gender Diversity Towards Corporate Social Responsibility Disclosure in Palestinian Companies: Financial Performance as Mediation” investigates the relationship between board gender diversity, corporate social responsibility (CSR) disclosure, and financial performance in Palestinian companies. By examining this relationship, the study contributes to the growing body of literature on board diversity and CSR in emerging economies, specifically in the context of Palestine.

The significance of this work lies in its potential to inform policymakers, corporate leaders, and stakeholders about the importance of promoting board gender diversity as a means to enhance CSR practices and financial performance in Palestinian companies. The findings of this study can guide organizations in developing effective strategies to achieve greater gender diversity on corporate boards, ultimately leading to improved CSR practices and better financial outcomes.

Furthermore, this research addresses a gap in existing literature by investigating the mediating role of financial performance in the relationship between board gender diversity and CSR disclosure. The insights gained from this study can contribute to a deeper understanding of the mechanisms through which board diversity influences CSR activities and organizational performance.

1. Introduction

The concept of corporate social responsibility (CSR) and its disclosure policy in financial reports (CSRD) has become an important topic among researchers, academics and corporate executives. Friedman argues that the responsibility of companies toward society is only to achieve the largest possible amount of profits (Muldoon et al., Citation2022). A debate between managers and researchers about social responsibility indicated that many concepts appeared to conflict with Friedman’s idea and showed that companies should consider the community around the company.

CSRD is a revelation of the company’s activities and policies for the benefit of society and the environment in its financial reports (Saleh et al., Citation2021). Through CSRD, the firms may improve their corporate image (Noor, Citation2019). In addition, the firms may improve the transparency and accountability of the company’s activities and thus enhance the confidence of all interested parties’ financial reports (Javaid Lone et al., Citation2016).

Globally, with the advent of globalization, companies have faced greater pressure to disclose their societal contribution (Orazalin, Citation2019). Therefore, the concepts of CSR and CSRD have become strategic for companies worldwide. Developed nations have established various measures to incentivise companies to incorporate CSR and CSRD in their financial statements. Therefore, CSR disclosure is considered a Western phenomenon; for example, the adoption of the Domini Social Index in the United States in 1990, and European countries have announced the adoption of CSR disclosure since 2005 (Mattingly, Citation2017). In addition, many developed countries sought Sustainability disclosure by disclosing incidents of environmental, social, non-discrimination and child labor.

In contrast, developing countries have not yet implemented similar initiatives. Noor (Citation2019) indicated that the concept of social responsibility in many Arab countries, such as Jordan, Egypt, Libya and Syria, is new, and this responsibility is focused on specific dimensions. It has not been fully adopted by global reporting initiatives.

On the Palestinian level, there is a lack of developed bodies working to regulate social responsibility and the absence of the oversight role of the government and laws that force Palestinian companies to allocate part of their budget in favor of social responsibility activities (Saleh et al., Citation2021). However, there is some indication of the social responsibility practices in Palestinian companies through some programs and assistance.

Researchers in various disciplines, such as law, political science, accounting, finance, economics and even philosophy, have focused their attention on the issue of corporate governance (CG). According to Gebba (Citation2015), the primary goal of a governance system is to control the management relationship with stakeholders to protect the related parties and business sustainability. In addition, Sundarasen et al. (Citation2016) indicated that CG and CSR are interdependent parts of the corporate system that requires them to adopt policies that suit and serve society as a whole. Haniffa and Cooke (Citation2005) suggest that CSR and CG help companies balance profitability goals and ethical and social practices. According to Khatib and Nour (Citation2021), the traits and composition of the BOD affect how well the CG functions.

Recently, researchers have been paying special attention to BOD gender diversity in the boards as one of the board features (Marinova et al., Citation2016; Riyadh et al., Citation2019). According to Nwude and Nwude (Citation2021), having women on the board can bring a wider range of experience and knowledge, enhancing the decision-making process. Additionally, it is expected that women would significantly impact the board’s input and output (Adams, Citation2016).

Although previous studies have emphasized the importance of BOD gender diversity, there is a lack of research in Palestine that has explored the impact of such diversity. Due to this gap, a formal quota for female representation on corporate boards of Palestinian businesses has not been set by regulatory agencies or Palestinian law. As a result, women in Palestine are underrepresented on these boards.

Numerous previous investigations have looked at the association between CSRD and BOD gender diversity (Gallego‐Álvarez & Pucheta‐Martínez, Citation2020; Katmon et al., Citation2019; Nwude & Nwude, Citation2021; Orazalin, Citation2019; Zaid et al., Citation2019). However, the results of these studies have not always been consistent. In addition, previous studies by Soare et al. (Citation2022), Khatib and Nour (Citation2021), Jabari and Muhamad (Citation2021) and Saleh et al. (Citation2021) have investigated the association between financial performance and BOD gender diversity. The results of these studies also have not always been consistent.

Financial performance can be defined as the level of business performance and success over a specified period (Nawaiseh, Citation2015). Evaluating companies’ financial performance allows decision-makers to evaluate the results of business strategies and activities, financial health and make plans to expand its activities and the ability to compare companies to make decisions from an objective and critical perspective (Palepu et al., Citation2020).

According to Marashdeh (Citation2014), companies with good financial performance are less vulnerable to risks, in addition to the positive relationship between good financial performance, company continuity and shareholders’ confidence. Nawaiseh (Citation2015) indicated that the good financial performance of the companies would provide the financial resources for the companies to spend on social and environmental causes. Wahyudi (Citation2018) and Nawaiseh (Citation2015) showed a direct positive impact on financial performance that measured (return on assets [ROA]) on CSRD.

However, to the best of the author’s knowledge, there are scarce studies on financial performance as a mediating variable between BOD gender diversity and CSRD.

The problem of this study is manifested in the weak CSRD in Palestinian companies and the conflicting results of previous studies on the relationship between the gender diversity in the boards and CSRD and financial performance. In addition, there is a lack of studies on financial performance as a mediator between the characteristics of the board of directors (BODs) in general and CSR disclosure. This study investigates the direct relationship between BOD gender diversity on CSRD and financial performance in Palestinian companies. It examines whether ROA will serve as a mediator between BOD gender diversity and CSRD. Thus, to explain the theoretical relationships, this study uses the resource dependence theory.

This study contributes to filling a gap in the literature by focusing on the context of Palestinian companies. Previous research on BOD gender diversity, CSRD and financial performance has primarily concentrated on developed countries. Therefore, this study expands the understanding of these relationships in emerging economies. Additionally, examining the new approach of financial performance as a mediator between BOD gender diversity and CSRD helps to comprehend the underlying mechanisms. It sheds light on how financial performance can serve as a channel between BOD gender diversity and CSRD, and how financial performance can convey the impact of BOD gender diversity on CSRD. By addressing these gaps, this study identifies the strengths and weaknesses of previous research and provides profound insights into this intricate relationship.

The study results indicate that increasing BOD gender diversity have a positive impact on CSRD in Palestinian companies. This implies that companies should strive to achieve greater inclusion and representation of women in leadership positions to enhance CSRD and promote transparency. Furthermore, companies that exhibit higher gender diversity on their boards and demonstrate better CSRD tend to achieve superior financial performance. Hence, organizations can improve their financial outcomes by fostering gender diversity, promoting CSR initiatives, and ensuring transparent reporting. Moreover, the findings of this study carry significant implications for policymakers in Palestine. They can utilize this research to develop and implement policies that foster gender diversity on boards and encourage CSRD. By doing so, these policies can contribute to the sustainable development of the economy and enhance the competitiveness of Palestinian companies in the global market.

2. Review of the literature and hypothesis development

2.1. Corporate social responsibility Disclosure (CSRD)

Recently, companies faced a great challenge as they practice their work in a more complex and changing environment economically, politically and socially. With the increasing societal concerns, it has become unacceptable to focus on the economic goals of the organization without focusing on social and environmental goals. Hence, the completion of work using the community’s economic resources necessitates the need for the organization to contribute to its social responsibilities as stewards of the community in which it works, as much as it contributes to the economic performance (Alia & Barham, Citation2020).

CSRD is used to evaluate economic, social and environmental performance. The organization’s failure to bear its social and environmental responsibilities will negatively impact the organization and affect its reputation with the stakeholders (Tarighi et al., Citation2022).

Through CSRD, the firms may improve their corporate image (Khatib & Nour, Citation2021). In addition, it provides transparency and accountability of the company’s activities and enhances the confidence of all interested parties’ financial reports, leading to increased investment in companies that adopt CSR disclosure (Nwude & Nwude, Citation2021). According to Ullah et al. (Citation2019), the CSRD will portray its commitment to society and thus attract distinguished scientific and professional competencies and skills to work in this institution.

Overall, the level of CSRD in developing countries is quite low and inadequate (Alia & Barham, Citation2020; Alia & Mardawi, 2021). Palestine suffers from a lack of interest in CSR, which may be due to the weak culture of CSR and the companies’ lack of awareness of the benefits and principles of CSR (Alhih et al., Citation2018). Also, Palestine suffers from the lack of developed bodies working to regulate social responsibility, in addition to the absence of the oversight role of the government and the absence of laws that force Palestinian companies to allocate part of their budget in favor of social responsibility activities (Saleh et al., Citation2021). Moreover, Companies Law No. (12) of 1964 and the code of CG in Palestine did not oblige companies to allocate a percentage of their profits for social responsibility but allowed it knowing that most of its contributions are in the form of zakat and charity donations (Alia & Barham, Citation2020).

Palestine’s general agreement is that the level of CSRD is still insufficient. According to Alia and Barham (Citation2020), the rate for CSRD of Palestinian companies from 2012 to 2017 for 41 Palestinian companies is 28.1%. Another study by Barakat et al. (Citation2015) was conducted for 46 firms in the Palestine Stock Exchange and 55 firms in the first market of Jordan. They showed that CSR disclosure is low in both countries, where the percentage of disclosure in Palestine and Jordan is 33% and 50%, respectively. Clearly, the CSR disclosure rate in Palestine is low compared to Jordan and developed countries. For example, Bhatia and Makkar (Citation2020) showed a CSR disclosure rate in UK companies of 98%, 85% in US companies and 56% in Australian companies, respectively.

Hillman et al. (Citation2000) indicated that social responsibility and its disclosure in financial reports has increased over time in developed countries in response to many factors, for example, social awareness, legitimizing aims, increase in legislation, ethical investors, activities of pressure groups and media interest. So far, there is no law regulating social responsibility practices in Palestine, and the Palestine Exchange did not obligate companies to mandatory disclosure of social responsibility practices.

2.2. Board gender diversity and CSRD

There are several studies conducted on board gender diversity as one of the characteristics of boards (Marinova et al., Citation2016; Riyadh et al., Citation2019). Studies by Cuadrado-Ballesteros et al. (Citation2017), Orazalin (Citation2019) and Nwude and Nwude (Citation2021) indicate that female representation contributes to the flow of competencies to the BODs and also to presenting a different vision and diverse ideas that enhance the company’s strategies toward sustainability and companies’ implementation of more social responsibility. Moreover, women tend to be more attuned to societal, environmental and ethical issues and place greater emphasis on engaging in charitable activities (Ibrahim & Hanefah, Citation2016). Thus, it is perceived that it would positively influence the assessment of firms’ social and environmental matters (Gallego‐Álvarez & Pucheta‐Martínez, Citation2020).

The resource dependence theory supports these arguments. Hillman et al. (Citation2000) explained that the resource dependence theory shows managers’ role in obtaining the organization’s vital resources from their external environment. These resources are considered an essential element for the organization’s success.

Saleh et al. (Citation2021) highlighted the importance of gender diversity within corporate boards, emphasizing its potential to bring forth a wide array of resources, knowledge and experiences. The inclusion of women in these boards enhances the representation of diverse groups and offers multiple perspectives during the decision-making process and overall management of the organization. Consequently, the presence of women on corporate boards can bolster the organization’s capacity to make socially, environmentally and ethically sustainable decisions, as well as effectively engage with a variety of stakeholders. This increased communication and interaction are believed to foster greater transparency and disclosure of social responsibility, as the range of voices and interests represented in the decision-making process expands (Saleh et al., Citation2021).

According to Barney (Citation1991), companies include heterogeneous resources, such as company assets, experience and intelligence of staff, as well as planning, control, values, training, judgment, intelligence, relationships and insight of the managers and employees of the company. According to Saleh et al. (Citation2021), the valuable qualities that female directors hold, such as knowledge, skills, legitimacy, status and connections to external sources, make them eligible to be valued members of the BODs, and these attributes are important resources for companies.

In this regard, numerous nations are implementing procedures to set up corporate boards with a gender balance. For instance, 40% female representation is the minimum requirement for corporate boards of publicly traded companies in Norway, Spain and France (Hoel, Citation2008; Saleh et al., Citation2021). Unfortunately, neither the Palestinian enterprises’ law nor the code of CG in Palestine makes mention of the proportion of females on the boards of Palestinian enterprises. As a result, it is discovered that there is a very poor representation of females on the boards of Palestinian enterprises. According to Saleh et al. (Citation2021), just 9% of women were represented on the boards of directors of publicly traded Palestinian enterprises.

Numerous research (Nwude and Nwude Citation2021; Orazalin, Citation2019; Katmon et al., Citation2019; Fuente et al., Citation2017; Cuadrado-Ballesteros et al., Citation2017; Kamran et al., Citation2023) shows a positive correlation between the BOD gender diversity and CSRD. The studies verified that a higher proportion of women serving on corporate boards of directors results in a higher percentage of social responsibility disclosure. However, according to Gallego-Alvarez and Pucheta‐Martnez (2020), there is a negative and substantial correlation between CSRD and BOD gender diversity. According to studies conducted in Palestine by Alia and Mardawi (2021), and Hassan (Citation2023), CSRD and BOD gender diversity have a favorable and substantial association. According to Zaid et al. (Citation2019), BOD gender diversity affects CSRD positively but statistically insignificantly in Palestinian companies.

This study proposes a positive relationship between gender diversity and the CSRD based on resource dependence theory and prior studies.

H1: BOD gender diversity has a positive and significant impact on the level of CSR disclosures in Palestinian companies

2.3. Board gender diversity and financial performance

The presence of women as members of the boards of directors of companies leads to different points of view that enhance the quality of decisions of boards of directors (Saleh et al., Citation2021), including decisions related to enhancing the financial efficiency of companies (Ghaleb et al., Citation2021). Moreover, having women on the boards can provide a source of expertise for other board members (Dwaikat et al., Citation2021). According to Adams (Citation2016), female directors can enhance a firm’s ability to generate profits by leveraging its assets and investments, resulting in higher and sustainable levels of economic growth.

According to the resource dependency theory, a board’s independence and the independence of its decision-making processes are stronger with a greater gender diversity. In contrast to men, women possess a strong sense of self and can provide a fresh perspective on complex issues (Saleh et al., Citation2021). This can help to amend informational biases when developing strategies and solving problems, ultimately resulting in an improvement in businesses’ financial performance.

In addition, a greater representation of women on the BODs can enhance communication and engagement with customers and investors. This can make them feel that the company has a more comprehensive vision of their needs and requirements, ultimately strengthening business relationships, building trust and fostering loyalty. Consequently, this can lead to an improvement in financial performance (Dwaikat et al., Citation2021).

Furthermore, the presence of women in boardrooms can contribute to shaping the company’s long-term strategic vision. Women bring diverse perspectives and experiences, which can aid in setting sustainable goals and developing long-term growth strategies. This, in turn, can enhance the overall financial sustainability of the company (Khatib & Nour, Citation2021).

Previous research has yielded conflicting findings regarding the correlation between gender diversity and financial performance. Khatib and Nour (Citation2021) and Jabari and Muhamad (Citation2021) report positive and significant effects of BOD gender diversity on financial performance. Conversely, the empirical study of Soare et al. (Citation2022) reports a negative and significant effect of BOD gender diversity on financial performance. Shukeri et al. (Citation2012) report a positive and insignificant relationship between BOD gender diversity and financial performance.

Palestinian studies also provided mixed results for the relationship between gender diversity and financial performance. Dwaikat et al. (Citation2021), Awwad et al. (Citation2023) and Saleh et al. (Citation2021) report a significant and positive impact of BOD gender diversity on financial performance in Palestinian firms. Saleh et al. (Citation2021) report positive and insignificant effects of the BOD gender diversity on financial performance. Saleh and Islam (Citation2020) found a negative and statistically insignificant relationship between BOD gender diversity and financial performance. However, based on the Resource Dependence Theory and previous research, this study proposes a hypothesis that there is a positive correlation between gender diversity and financial performance.

H2: BOD gender diversity has a positive and significant impact on financial performance in Palestinian companies.

2.4. The mediating role of financial performance

As discussed above, previous studies have checked the direct relationships between BOD gender diversity and CSRD and financial performance. However, previous studies have not addressed the issue of the intertwining of characteristics and have ignored the mediating factors that may link the characteristics of the board to the results of the company (Post & Byron, Citation2015).

Musibah and Alfattani’s (Citation2014) study indicates that financial performance (ROA and ROE) was found to be a significant mediating factor for the relationship between Shariah Supervisory Board Effectiveness and Capital Employed Efficiency. Wahba and Elsayed’s (Citation2015) study indicates that financial performance mediates the relationship between social responsibility and ownership structure. Fahimi and Fakhari’s (Citation2017) study shows that there is no mediating effect of financial performance in the relationship between intellectual capital and market share. However, previous studies did not focus on financial performance as a mediating variable between board size and CSRD.

Carroll (Citation1991) confirms the importance of the firm’s economic responsibility as it is connected to all other business responsibilities since they become debatable considerations. According to Barnett (Citation2007), the BODs may prefer to disclose social responsibility, while shareholders prefer to have greater wealth. However, shareholders may not be concerned about social responsibility in the event that companies make profits. Therefore, the size of the profits will affect the disclosure of social responsibility (Barnett, Citation2007).

This study assumes that having financial performance, in particular, may mediate the relationships between BOD gender diversity and CSRD. Thus, the BOD gender diversity may affect CSRD through financial performance.

H3: Financial performance mediates the relationship between BOD gender diversity and Social Responsibility Disclosure in Palestinian companies

3. Design and methods of research

3.1. Proposed conceptual framework

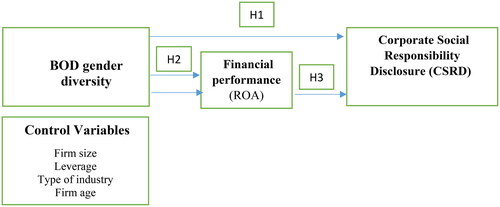

As explained in the literature review, this study employs resource dependence theory to explain BOD gender diversity to CSRD and financial performance. depicts the theorized relationships between study variables.

Figure 1. Conceptual framework.

presents the BOD gender diversity as an independent variable, CSRD as a dependent variable, and financial performance as a mediator variable. While the firm size, leverage, type of industry and firm age are control variables.

3.2. Sample and data collection

The sample consists of 31 firms listed on the Palestine Stock Exchange from 2012 to 2021. Certain industries were excluded from the study as their accounting standards differ significantly from others (Campbell & Keys, Citation2002). Details of the selection process are in .

Table 1. Process of choosing samples.

3.3. Data analysis

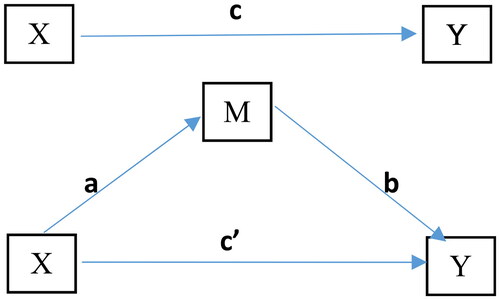

This study uses secondary data, gathered from the annual financial reports of listed Palestinian companies, which are accessible on the PEX Palestine website or the corporate web pages. For data analysis and hypothesis testing, STATA, a statistical program, will be used. The association between the variables is investigated in this study using a panel data research methodology and the ordinary least square (OLS) regression estimation method - fixed effect model regression. The fixed effect analysis solves the endogeneity issue. Hence, the model will be free of endogeneity (Saleh et al., Citation2022). This study employs the causal step technique pioneered by Baron and Kenny (Citation1986) to investigate the mediating role of financial performance in the link between BOD gender diversity and CSRD. A variable is said to be a mediator if it meets three requirements (Baron & Kenny, Citation1986). First, the dependent variable (CSRD) should be significantly impacted by the independent variable (BOD gender diversity). Second, the mediator variable (ROA) should be significantly influenced by the independent variable. Third, when both the independent and mediator variables are included in a model, the mediator variable should be significant, while the absolute value of the independent variable should be decreased. Through the third step, the type of mediation can be determined. If the independent variable has an insignificant impact on the dependent variable, researchers report that the mediator fully or completely mediates the relationship. If there is a significant impact, researchers report that the mediator partially mediates the relationship (Iacobucci, Citation2012). , adapted from Hayes (Citation2009), illustrates the framework for a simple mediation model.

Figure 2. Model of mediation.

The framework illustrated in considers X as the independent variable (BOD gender diversity), Y as the dependent variable (CSRD) and M as the mediating variable (ROA). The indirect effects are represented by Path a and b, while c’ represents the direct effect of X on Y after controlling for the mediator. The top portion of the figure displays c as the total effect of the independent variable (X) on the dependent variable (Y).

3.4. Variables definitions and measurements

3.4.1. Dependent variable CSRD

The disclosure of CSR in the annual report portrays the initiatives that companies have taken to assist society, and improve the environment, in addition to improving the company’s bottom line figure (economic) (Adnan et al., Citation2018). The World Business Council for Sustainable Development has identified areas of CSR disclosure as including areas related to CSRD toward environmental protection, CSRD toward human rights, CSRD toward community participation and CSRD toward employee rights (Gupta & Sinha, Citation2015). While the National Association of Accountants in America (NAA) identified four main areas of CSRD, which are CSRD toward society, CSRD toward the environment and natural resources, CSRD toward human resources and CSRD toward upgrading the product and consumer (Gupta & Sinha, Citation2015). Although the disclosure of CSR differs among researchers, the main areas for it are usually related to community involvement, environment, product, consumers and human resources (Bayoud, Citation2012).

The checklist has been developed in this study as an index to measure the level of CSRD for companies listed on the Palestine Stock Exchange. They are environmental disclosures, human resources disclosures, community involvement disclosures and product and consumer disclosures. The checklist has been adopted from Alia and Barham (Citation2020) but has added additional items from other CSRD studies. These dimensions identified by the NAA, in addition to being based on the GRI, which has been widely used by researchers in the CSR disclosure study (Alia & Mardawi, 2021; Alia & Barham, Citation2020; Barakat et al., Citation2015). illustrates the themes and sub-themes of CSRD used in this study.

Table 2. CSRD Index (4 dimensions and 53 items).

The content analysis method will be used to extract the required data from the annual reports of the Palestinian companies by giving each item of the checklist a value of (1) if it was disclosed in the annual report of the company and a value of (0) if it was not disclosed, then the values of all items are summed and divided by the total number of items to find the percentage of disclosure of social responsibility for each company for every year over the ten years. The final CSRD index (ICSRD) was calculated as follows:

where:

ICSRD = Index of CSRD

ej = Analysis of attributes (1 if a disclosure item is identified, 0 otherwise)

e = Maximum number of items a company can disclose (53).

3.4.2. Independent variables (BOD gender diversity)

The term ‘BOD Gender Diversity’ refers to the representation of women on corporate boards of directors (Khatib & Nour, Citation2021). The proportion of female directors on the board was computed in this study by dividing the number of female board members by the total number of board members. The definition and measurement are consistent with prior studies about the impact of CG on CSRD like Khatib and Nour (Citation2021), Jabari and Muhamad (Citation2021), Dwaikat et al. (Citation2021) and Soare et al. (Citation2022).

3.4.3. Mediating variable – financial performance (ROA)

Financial performance is the numerical assessment of how effectively a company employs its assets and produces revenue. In order to calculate a company’s overall financial performance, ROA is the most commonly utilized metric. ROA is one of the most important return on investment measures, which measures a company’s profits in relation to its total assets. This ratio indicates the quality of business performance by linking companies’ return to the invested capital (Elvin & Hamid, Citation2017). ROA is defined as income before extraordinary items divided by total assets (Saleh et al., Citation2021). This study used the same definition and measurement most used by previous studies, such as Dwaikat et al. (Citation2021) and Saleh et al. (Citation2021).

3.4.4. Control variable

Additional variables are controlled to prevent any inaccuracies in the model and to account for other factors that may inherently affect CSR disclosure. The firm size is controlled as several previous studies have confirmed the positive effect of firm size on CSRD (see Adnan et al., Citation2018; Nawaiseh, Citation2015). With geographical markets and diversified products, large companies have a wide range of stakeholders and greater societal influence (Alia & Mardawi, 2021). Therefore, these companies tend to reveal their social activities to legitimize their existence and enhance their reputation (Mohd Ghazali, Citation2007). This study, consistent with Michelon and Parbonetti (Citation2012), utilizes the measure of size (LnSIZE), represented by the logarithm of total sales, to gauge firm size. Leverage is also controlled, as Barnea and Rubin (Citation2010) indicate, as a higher level of leverage decreases, the probability of obtaining financial resources, and the lack of financial funds is an obstacle to their participation in CSR issues. The various studies in the literature used the same technique of measuring leverage by total debt to total assets (Barakat et al., Citation2015; Alia & Mardawi, 2021). This study employs the same measurement tool. It is also essential to control for firm age. According to Hamid (Citation2004), the company’s age is associated with its reputation and CSRD. Previous studies agreed that well-established companies are more committed to disclosing social responsibility (see Cuadrado-Ballesteros et al., Citation2017). Old companies received many services and benefits from society, so these companies have a greater sense of social responsibility. Many of the studies in the literature used the number of years of existence to measure the age of the firm (Cuadrado-Ballesteros et al., Citation2017). Based on previous studies, this study used the number of years of the company since its establishment to measure the firm age. Finally, as for industry types, each company has its characteristics in which accounting policies and techniques are linked, as companies adopt disclosure practices that differ from other companies according to the industry in which they specialize (Rashid, Citation2018). Another factor influencing disclosure is the type of business operations. For instance, companies with multiple product lines may have more information to disclose than those with smaller or single product lines (Dwaikat et al., Citation2021). Numerous works in the literature used the industry type as a control variable (Rashid, Citation2018), whereby dummy variable codes: Industry 1 (service) = 1, Otherwise = 0, Industry 2 (industrial) = 1, Otherwise = 0, Industry 3 (investment) = 1 and otherwise = 0 are used. This study employs the industry type by using the same measurement tool.

3.5. Regression model specification

This study tests three models as follows:

The first model tests the effect of independent variables represented in BOD gender diversity on the dependent variables represented in CSRD as follows:

CSRD = β0 + β1 BODgd + β2LnSIZE + β3LEVERAGE + β4Ag + β5TYPE + ε

CSRD = corporate social responsibility disclosure

BODgd = BOD gender diversity.

LnSIZE = firm size.

LEVERAGE = Leverage

Ag = Firm age

TYPE = Type of industry

The second model tests the effect of independent variables represented in BOD gender diversity on the mediator variable represented in corporate financial performance (ROA) as follows:

CP = β0 + β1 BODgd + β2LnSIZE + β3LEVERAGE + β4Ag + β5TYPE + ε

CP = corporate financial performance.

BODgd = BOD gender diversity.

LnSIZE = firm size.

LEVERAGE = Leverage.

Ag = Firm age.

TYPE = Type of industry.

The third model tests the extent to which companies’ financial performance mediates the relationship between BOD gender diversity and CSRD as follows:

CSRD = β0 + β1 BOgd + β2CP + β3LnSIZE + β4LEVERAGE + β5Ag + β6TYPE + ε

CSRD = corporate social responsibility disclosure

BODgd = BOD gender diversity.

CP = corporate financial performance.

LnSIZE = firm size.

LEVERAGE = Leverage

Ag = Firm age

TYPE = Type of industry

4. Empirical results and discussion

4.1. Descriptive statistics

provides the descriptive analysis for all variables used in this study (CSRD, BOD gender diversity, ROA, firm size, leverage, firm age and type of industry).

Table 3. Descriptive analysis variables.

Through descriptive analysis, it is clear that Palestinian corporations’ CSRD average is 29.5%, indicating that the volume of CSR disclosure is still quite inadequate and there is room for improvement in the Palestinian context. This result is close to the results of Palestinian studies conducted in this context. For example, Alia and Barham (Citation2020) indicated that the rate of CSRD in Palestinian companies is 28.1%. Another study by Barakat et al. (Citation2015), showed that CSRD is 33% in Palestinian companies. Meanwhile, in developed countries, for example, Bhatia and Makkar (Citation2020) showed a CSRD rate 98% in UK companies and 85% in US companies. The results also showed that the percentage of BOD gender diversity within the BODs is 7% on average. This means that the representation of women within the boards of directors of the Palestinian companies included in the study sample is very low; perhaps this is due to the fact that the law does not oblige Palestinian companies to specify a specific percentage of women’s representation on boards of directors. This result is close to the study of Saleh et al. (Citation2021), which was conducted in Palestine, which indicated that the percentage of women’s representation on the boards of directors of Palestinian companies is only 9%, while these percentages are very low compared to other countries, for example, Hoel (Citation2008) indicated that the percentage of women’s representation in Norway, Spain and France ranges from the 40%. Regarding the ROA, the average ROA for the companies included in the study sample is 2.9%, which means that the companies within the study sample achieve an average return of 2.9% of their total assets. This percentage is close to Barakat et al.’s (Citation2022) study, which indicated that the ROA for companies in Palestine is 3%. Descriptive statistics related to control variables can be observed in .

The skewness and kurtosis values offer insight into the distribution of the data. Skewness indicates the symmetry of the data distribution, while kurtosis indicates its peakedness (Gorondutse & Hilman, Citation2012). This study’s skewness values range from −0.726 to 1.8, while the kurtosis values range from 1.722 to 5.38. These values suggest that the data distribution is normal.

4.2. Correlation analysis

provides the correlation analysis for all variables used in this study.

Table 4. Correlation matrix between the proposed variables.

shows the correlation matrix between the variables. The results indicate that the CSRD was shown to have a positive correlation with BOD gender diversity, ROA, firm size and leverage. On the other hand, the company’s age and type of industry negatively correlate with CSRD. also shows that ROA, leverage and type of industry positively correlate with BOD gender diversity. On the other hand, firm size and company age negatively correlate with BOD gender diversity. The results indicate that firm size and company age positively correlate with ROA, and leverage and type of industry negatively correlate with ROA.

Regarding control variables, correlation results show that leverage has a positive correlation with firm size and company age and type of industry have a negative correlation with firm size. The result also shows that company age and type of industry negatively correlate with leverage. The results also show that the type of industry negatively correlates with company age. It is noted from the correlation matrix above that all values of the correlation coefficients between the variables are non-high, which is less than 80%, and this indicates that there is no problem of linear overlap between the study variables.

4.3. Regression analysis models

4.3.1. Model 1: Association of BOD gender diversity and CSRD (H1)

shows that BOD gender diversity is statistically significant and that there is a positive relationship between BOD gender diversity and CSRD at a significant level of 10%, with a coefficient value of 0.45 and a corresponding t-statistic value of 1.88. Therefore, H1 is accepted. This outcome suggests that the level of CSRD increased with BOD gender diversity in Palestinian companies that are listed on the Palestine Exchange PEX. This result supports previous studies conducted in Palestine (e.g. Alia & Mardawi, 2021) and is also consistent with past studies in other countries (Nwude & Nwude, Citation2021; Orazalin, Citation2019), which confirmed that the presence of a greater percentage of women on the BODs of companies contributes to an increase in the percentage of CSRD. These findings are also consistent with the resource dependence theory, which indicates that the presence of women on boards of directors is considered to be a good promoter of CSR issues because women possess knowledge, skills and ability to communicate with the external environment and that they are more sensitive, moral and cooperative than men (Peterson & Philpot, Citation2007).

Table 5. Fixed effect model regression for BOD gender diversity and CSRD.

4.3.2. Model 2: association of BOD gender diversity and financial performance (H2)

shows that the BOD gender diversity is positively and significantly related to ROA at (p < 5%) with a coefficient value of 0.105 and a t-statistic value of 2.31. Therefore, H2 is accepted. This outcome suggests that the level of ROA increased with BOD gender diversity in Palestinian companies listed on PEX. This result supports previous studies conducted in Palestine (Dwaikat et al., Citation2021; Saleh et al., Citation2021) and is consistent with previous studies conducted in other countries (Jabari & Muhamad, Citation2021; Khatib & Nour, Citation2021), which confirmed that ROA is positively and significantly affected by the BOD gender diversity. These findings are in line with the Resource Dependence Theory, which suggests that the inclusion of women on boards can bring a fresh perspective to complex issues solve problems and increase the financial performance of companies (Dwaikat et al., Citation2021).

Table 6. Fixed effect model regression for BOD gender diversity and ROA.

4.3.3. Model 3: mediation analysis of financial performance between BOD gender diversity and CSRD

Based on Baron and Kenny (Citation1986), the first two conditions for mediation analysis have been verified in the above tables that examined the relationship of the independent variable (BOD gender diversity) on the dependent variable (CSRD) in model one in and the independent variable (BOD gender diversity) on the mediator variable (ROA) that examined in model two in . Concerning the third condition, shows the fixed effect model of multiple regression for IV on the DV with the addition of the mediator to the model.

Table 7. Fixed effect model regression for mediation (Step 3).

In the first condition, BOD gender diversity (IV) and CSRD (DV) should be significantly associated. The regression in shows that BOD gender diversity is positively and significantly related to CSRD at (p < 10%) with a coefficient value of 0.45 and a t-statistic value of 1.88. Hence, the first condition is met and thus proceeds to the second condition. In the second condition, the BOD gender diversity (IV) and the ROA (MV) should have a significant relationship. shows that BOD gender diversity is positively and significantly related to ROA at p < 5% with a coefficient value of 0.105 and a t-statistic value of 2.31. Therefore, the first and second conditions are satisfied and thus proceed with the final condition. The ROA (MV) should be significantly associated with the CSRD (DV) after including the BOD gender diversity (IV) in a model, and the absolute value of the independent variable should be reduced. The results shown in indicate that after controlling for the effect of BOD gender diversity, ROA has a significant and positive relationship with CSRD at p < 5% with a coefficient value of 0.16 and a t-statistic value of 2.57. In addition, the absolute value of BOD gender diversity after including the mediator variable is reduced. BOD gender diversity is significantly associated with the CSRD at p < 5% with a coefficient value of 0.113 and a t-statistic value of 2.39. Therefore, the type of mediator is partial. Therefore, H3 is accepted. shows the summaries of statistical steps for the mediation process.

Table 8. Summaries of statistical steps for the mediation process.

5. Conclusions

This article aimed to examine the level of CSRD in Palestine and analyse the impact of BOD gender diversity on CSRD and financial performance and the extent of the impact of financial performance as a mediating variable between BOD gender diversity and CSRD. The results of this study revealed that the CSRD rate was 29.5% in the companies included in the study sample, with 98% in the UK companies. In the US companies, it was 85%, followed by 50% in Jordan companies. The findings also indicated that BOD gender diversity enhances CSRD and financial performance, as measured by ROA. Furthermore, the regression analyses suggest that financial performance partially mediates the relationship between BOD gender diversity and CSRD in Palestinian companies from 2012 to 2021. These findings are in agreement with resource dependency theory, which indicates that women possess a wide base of knowledge, skills, legitimacy, relationships and access to external resources, and they consider themselves good promoters of CSR issues besides their ability to enhance the financial performance of companies. The study contributes to clarifying the relationship between BOD gender diversity and CSRD by analyzing the available data and literature, in addition to providing strong theoretical evidence confirming the relationship between these two variables. In addition, the study helps identify the influential factors that reflect the mediating effect of financial performance in this relationship. The study provides practical guidance for institutions and organizations on how to promote gender diversity and social responsibility. The results can help inform employee development policies and practices, promote equity and develop sustainable communities. Like all empirical research, this study has its limitations. In this study, only ROA was used to measure financial performance, so future research can use other tools to measure financial performance, such as ROE and EPS. Furthermore, this study had limitations regarding the nature of the firms, as the data only pertained to companies in three specific sectors: services, industry and investment. Therefore, further research is suggested to examine this issue in banks and insurance sectors to ascertain whether there are disparities in the findings. Finally, this study categorically recommends the need to amend the current CG code in Palestine and the Palestinian companies’ law and follow the developed countries by determining a high percentage of women within the boards of directors of Palestinian companies due to their important role in increasing the CSR disclosure and financial performance as well.

Author contributions statement

[Omar Tarda] conceptualization, data collection, analysis, funding acquisition, methodology, conceived and designed the study and wrote the manuscript. [Hasnah Haron] contributed to the study design, conducted statistical analyses, conceptualization, investigation and methodology, wrote the manuscript, and provided critical revisions to the manuscript. [Nathasa Mazna Ramli] assisted in data collection, performed data interpretation, conceptualization and investigation, and contributed to the drafting of the manuscript. [Supiah Salleh] contributed to the study design, provided expertise in the subject matter, investigation and revised the manuscript for important intellectual content. All authors read and approved the final version of the manuscript.

Disclosure statement

No interest to declare.

Data availability statement

The authors are committed to sharing the data in a responsible and transparent manner with qualified researchers who meet the criteria for access.

Additional information

Funding

Notes on contributors

Omar Tarda

Omar Tarda is a PhD student in accounting from Universiti Sains Islam Malaysia. Originally from Palestine, he currently works as a lecturer at Palestine Technical University - Palestine. His research interests revolve around the field of governance and social responsibility.

Hasnah Haron

Hasnah Haron, Nathasa Ramli, and Supiah Salleh are Associate Professors of Accounting and Governance at Universiti Sains Islam Malaysia. They hail from Malaysia and have extensive experience in their respective fields. Their research interests include Accounting, Shariah Audit & Governance, Fellow, Governance, Integrity and Reporting. They have published numerous articles in renowned academic journals and have received recognition for their contributions to the field.

Nathasa Ramli

Hasnah Haron, Nathasa Ramli, and Supiah Salleh are Associate Professors of Accounting and Governance at Universiti Sains Islam Malaysia. They hail from Malaysia and have extensive experience in their respective fields. Their research interests include Accounting, Shariah Audit & Governance, Fellow, Governance, Integrity and Reporting. They have published numerous articles in renowned academic journals and have received recognition for their contributions to the field.

Supiah Salleh

Hasnah Haron, Nathasa Ramli, and Supiah Salleh are Associate Professors of Accounting and Governance at Universiti Sains Islam Malaysia. They hail from Malaysia and have extensive experience in their respective fields. Their research interests include Accounting, Shariah Audit & Governance, Fellow, Governance, Integrity and Reporting. They have published numerous articles in renowned academic journals and have received recognition for their contributions to the field.

References

- Adams, R. B. (2016). Women on boards: The superheroes of tomorrow? The Leadership Quarterly, 27(3), 371–386. https://doi.org/10.1016/j.leaqua.2015.11.001

- Adnan, S. M., Hay, D., & van Staden, C. J. (2018). The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. Journal of Cleaner Production, 198, 820–832. https://doi.org/10.1016/j.jclepro.2018.07.057

- Alhih, M., Tambi, A. M. B. A., & Abueid, A. I. S. (2018). Corporate social responsibility in Palestinian public schools. American Based Research Journal, 7(12).

- Alia, M. A., & Mardawi, Z. (2021). The impact of ownership structure and board characteristics on corporate social responsibility disclosed by Palestinian companies. Jordan Journal of Business Administration, 17(2), 254–277. https://doi.org/10.35516/0338-017-002-006

- Alia, M. A., & Barham, O. (2020). The effect of earnings management and corporate governance on the relationship between corporate social responsibility disclosure of companies listed on Palestine exchange (PEX) and the value of the company. An-Najah University Journal for Research - B (Humanities), 36(11), 2313–2358. https://doi.org/10.35552/0247-036-011-002

- Awwad, B. S., Binsaddig, R., Kanan, M., & Al Shirawi, T. (2023). Women on boards: An empirical study on the effects on financial performance and corporate social responsibility. Competitiveness Review: An International Business Journal, 33(1), 147–160. https://doi.org/10.1108/CR-06-2022-0084

- Barakat, F. S., Hussein, J., Mahmoud, O. A., & Bayyoud, M. (2022). Analysis of the factors affecting the financial performance of insurance companies listed on the Palestine stock exchange. Indian Journal of Finance and Banking, 9(1), 213–229. https://doi.org/10.46281/ijfb.v9i1.1679

- Barakat, F. S. Q., López Pérez, M. V., & Rodríguez Ariza, L. (2015). Corporate social responsibility disclosure (CSRD) determinants of listed companies in Palestine (PXE) and Jordan (ASE). Review of Managerial Science, 9(4), 681–702. https://doi.org/10.1007/s11846-014-0133-9

- Barnea, A., & Rubin, A. (2010). Corporate social responsibility as a conflict between shareholders. Journal of Business Ethics, 97(1), 71–86. https://doi.org/10.1007/s10551-010-0496-z

- Barnett, M. L. (2007). Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Academy of Management Review, 32(3), 794–816. https://doi.org/10.5465/amr.2007.25275520

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Bayoud, N. S. M. (2012). Corporate social responsibility disclosure and organisational performance: The case of Libya, a mixed methods study. University of Southern Queensland.

- Bhatia, A., & Makkar, B. (2020). CSR disclosure in developing and developed countries: A comparative study. Journal of Global Responsibility, 11(1), 1–26. https://doi.org/10.1108/JGR-04-2019-0043

- Campbell, T. L., II., & Keys, P. Y. (2002). Corporate governance in South Korea: The chaebol experience. Journal of Corporate Finance, 8(4), 373–391. https://doi.org/10.1016/S0929-1199(01)00049-9

- Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48. https://doi.org/10.1016/0007-6813(91)90005-G

- Cuadrado-Ballesteros, B., García-Sánchez, I.-M., & Martínez-Ferrero, J. (2017). The impact of board structure on CSR practices on the international scale. European J. of International Management, 11(6), 633–659. https://doi.org/10.1504/EJIM.2017.087559

- Dwaikat, N., Qubbaj, I. S., & Queiri, A. (2021). Gender diversity on the board of directors and its impact on the Palestinian financial performance of the firm. Cogent Economics & Finance, 9(1), 1948659. https://doi.org/10.1080/23322039.2021.1948659

- Elvin, P., & Hamid, N. I. N. A. (2017). Review on ownership structure, corporate governance and firm performance. Jurnal Kemanusiaan, 15(1).

- Fahimi, S. M., & Fakhari, H. (2017). The mediating effect of financial performance on the relationship between intellectual capital & market Share: Evidence from Tehran Stock Exchange. Risk Governance and Control: Financial Markets and Institutions, 7(4–1), 153–162. https://doi.org/10.22495/rgc7i4c1art7

- Fuente, J. A., García-Sánchez, I. M., & Lozano, M. B. (2017). The role of the board of directors in the adoption of GRI guidelines for the disclosure of CSR information. Journal of Cleaner Production, 141, 737–750. https://doi.org/10.1016/j.jclepro.2016.09.155

- Gallego‐Álvarez, I., & Pucheta‐Martínez, M. C. (2020). Environmental strategy in the global banking industry within the varieties of capitalism approach: The moderating role of gender diversity and board members with specific skills. Business Strategy and the Environment, 29(2), 347–360. https://doi.org/10.1002/bse.2368

- Gebba, T. R. (2015). Corporate governance mechanisms adopted by UAE national commercial banks. Journal of Applied Finance and Banking, 5(5), 23.

- Ghaleb, B. A. A., Qaderi, S. A., Almashaqbeh, A., & Qasem, A. (2021). Corporate social responsibility, board gender diversity and real earnings management: The case of Jordan. Cogent Business & Management, 8(1), 1883222. https://doi.org/10.1080/23311975.2021.1883222

- Gorondutse, A. H., & Hilman, H. (2012). The influence of Business Social Responsibility (BSR) on Organisational Performances: A pilot Study. International Journal of Business Communication [Internet].

- Gupta, U., & Sinha, R. (2015). A comparative study on factors affecting consumer’s buying behavior towards home loans (with special reference to state bank of India and life insurance corporation, Allahabad). IOSR Journal of Business and Management (IOSR-JBM), e-ISSN, 13–17. https://doi.org/10.9790/487X-17211317

- Hamid, F. Z. A. (2004). Corporate social disclosure by banks and finance companies: Malaysian evidence. Corporate Ownership and Control, 1(4), 118–130.

- Haniffa, R. M., & Cooke, T. E. (2005). The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5), 391–430. https://doi.org/10.1016/j.jaccpubpol.2005.06.001

- Hassan, Y. (2023). Do women on boards matter for corporate social responsibility reporting? Evidence from Palestine. EuroMed Journal of Business, https://doi.org/10.1108/EMJB-02-2023-0053

- Hayes, A. F. (2009). Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Communication Monographs, 76(4), 408–420. https://doi.org/10.1080/03637750903310360

- Hillman, A. J., Cannella, A. A., & Paetzold, R. L. (2000). The resource dependence role of corporate directors: Strategic adaptation of board composition in response to environmental change. Journal of Management Studies, 37(2), 235–256. https://doi.org/10.1111/1467-6486.00179

- Hoel, M. (2008). The quota story: Five years of change in Norway. Women on corporate boards of directors: International research and practice (pp. 79–87). Edward Elgar Publishing.

- Iacobucci, D. (2012). Mediation analysis and categorical variables: The final frontier. Journal of Consumer Psychology, 22(4), 582–594. https://doi.org/10.1016/j.jcps.2012.03.006

- Ibrahim, A. H., & Hanefah, M. M. (2016). Board diversity and corporate social responsibility in Jordan. Journal of Financial Reporting and Accounting, 14(2), 279–298. https://doi.org/10.1108/JFRA-06-2015-0065

- Jabari, H. N., & Muhamad, R. (2021). Gender diversity and financial performance of Islamic banks. Journal of Financial Reporting and Accounting, 19(3), 412–433. https://doi.org/10.1108/JFRA-03-2020-0061

- Javaid Lone, E., Ali, A., & Khan, I. (2016). Corporate governance and corporate social responsibility disclosure: evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 16(5), 785–797. https://doi.org/10.1108/CG-05-2016-0100

- Kamran, M., Djajadikerta, H. G., Mat Roni, S., Xiang, E., & Butt, P. (2023). Board gender diversity and corporate social responsibility in an international setting. Journal of Accounting in Emerging Economies, 13(2), 240–275. https://doi.org/10.1108/JAEE-05-2021-0140

- Katmon, N., Mohamad, Z. Z., Norwani, N. M., & Farooque, O. A. (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. Journal of Business Ethics, 157(2), 447–481. https://doi.org/10.1007/s10551-017-3672-6

- Khatib, S. F. A., & Nour, A. (2021). The impact of corporate governance on firm performance during the COVID-19 pandemic: Evidence from Malaysia. Journal of Asian Finance, Economics and Business, 8(2), 943–952.

- Marashdeh, Z. M. S. (2014). The effect of corporate governance on firm performance in Jordan. University of Central Lancashire.

- Marinova, J., Plantenga, J., & Remery, C. (2016). Gender diversity and firm performance: Evidence from Dutch and Danish boardrooms. The International Journal of Human Resource Management, 27(15), 1777–1790. https://doi.org/10.1080/09585192.2015.1079229

- Mattingly, J. E. (2017). Corporate social performance: A review of empirical research examining the corporation–society relationship using Kinder, Lydenberg, Domini social ratings data. Business & Society, 56(6), 796–839. https://doi.org/10.1177/0007650315585761

- Michelon, G., & Parbonetti, A. (2012). The effect of corporate governance on sustainability disclosure. Journal of Management & Governance, 16(3), 477–509. https://doi.org/10.1007/s10997-010-9160-3

- Mohd Ghazali, N. A. (2007). Ownership structure and corporate social responsibility disclosure: Some Malaysian evidence. Corporate Governance: The International Journal of Business in Society, 7(3), 251–266. https://doi.org/10.1108/14720700710756535

- Muldoon, J., Gould, A. M., & Yonai, D. K. (2022). Conjuring-up a bad guy: The academy’s straw-manning of Milton Friedman’s perspective of corporate social responsibility and its consequences. The American Economist, 68(2), 171–188. https://doi.org/10.1177/05694345221145008

- Musibah, A. S., & Alfattani, W. S. B. W. Y. (2014). The mediating effect of financial performance on the relationship between Shariah supervisory board effectiveness, intellectual capital and corporate social responsibility, of Islamic banks in Gulf Cooperation Council countries. Asian Social Science, 10(17), 139. https://doi.org/10.5539/ass.v10n17p139

- Nawaiseh, M. E. (2015). Do firm size and financial performance affect corporate social responsibility disclosure: Employees’ and environmental dimensions? American Journal of Applied Sciences, 12(12), 967–981. https://doi.org/10.3844/ajassp.2015.967.981

- Noor, A. (2019). The level of corporate social responsibility implementation in all social responsibility aspects in Jordan’s Zain telecommunication company. Gazdaság és Társadalom, 30(4), 88–113. https://doi.org/10.21637/GT.2019.4.04

- Nwude, E. C., & Nwude, C. A. (2021). Board structure and corporate social responsibility: Evidence from developing economy. SAGE Open, 11(1), 215824402098854. https://doi.org/10.1177/2158244020988543

- Orazalin, N. (2019). Corporate governance and corporate social responsibility (CSR) disclosure in an emerging economy: Evidence from commercial banks of Kazakhstan. Corporate Governance: The International Journal of Business in Society, 19(3), 490–507. https://doi.org/10.1108/CG-09-2018-0290

- Palepu, K. G., Healy, P. M., Wright, S., Bradbury, M., & Coulton, J. (2020). Business analysis and valuation: Using financial statements. Cengage AU.

- Peterson, C. A., & Philpot, J. (2007). Women’s roles on US Fortune 500 boards: Director expertise and committee memberships. Journal of Business Ethics, 72(2), 177–196. https://doi.org/10.1007/s10551-006-9164-8

- Post, C., & Byron, K. (2015). Women on boards and firm financial performance: A meta-analysis. Academy of Management Journal, 58(5), 1546–1571. https://doi.org/10.5465/amj.2013.0319

- Rashid, A. (2018). The influence of corporate governance practices on corporate social responsibility reporting. Social Responsibility Journal, 14(1), 20–39. https://doi.org/10.1108/SRJ-05-2016-0080

- Riyadh, H. A., Sukoharsono, E. G., & Alfaiza, S. A. (2019). The impact of corporate social responsibility disclosure and board characteristics on corporate performance. Cogent Business & Management, 6(1), 1647917. https://doi.org/10.1080/23311975.2019.1647917

- Saleh, M. W., Eleyan, D., & Maigoshi, Z. S. (2022). Moderating effect of CEO power on institutional ownership and performance. EuroMed Journal of Business, https://doi.org/10.1108/EMJB-12-2021-0193

- Saleh, M. W. A., & Islam, M. A. (2020). Does board characteristics enhance firm performance? Evidence from Palestinian listed companies. International Journal of Multidisciplinary Sciences and Advanced Technology, 1(4), 84–95.

- Saleh, M. W. A., Zaid, M. A. A., Shurafa, R., Maigoshi, Z. S., Mansour, M., & Zaid, A. (2021). Does board gender enhance Palestinian firm performance? The moderating role of corporate social responsibility. Corporate Governance: The International Journal of Business in Society, 21(4), 685–701. https://doi.org/10.1108/CG-08-2020-0325

- Shukeri, S. N., Shin, O. W., & Shaari, M. S. (2012). Does board of director’s characteristics affect firm performance? Evidence from Malaysian public listed companies. International Business Research, 5(9), 120. https://doi.org/10.5539/ibr.v5n9p120

- Soare, T. M., Detilleux, C., & Deschacht, N. (2022). The impact of the gender composition of company boards on firm performance. International Journal of Productivity and Performance Management, 71(5), 1611–1624. https://doi.org/10.1108/IJPPM-02-2020-0073

- Sundarasen, S. D. D., Je-Yen, T., & Rajangam, N. (2016). Board composition and corporate social responsibility in an emerging market. Corporate Governance: The International Journal of Business in Society, 16(1), 35–53. https://doi.org/10.1108/CG-05-2015-0059

- Tarighi, H., Appolloni, A., Shirzad, A., & Azad, A. (2022). Corporate social responsibility disclosure (CSRD) and financial distressed risk (FDR): Does institutional ownership matter? Sustainability, 14(2), 742. https://doi.org/10.3390/su14020742

- Ullah, M. S., Muttakin, M. B., & Khan, A. (2019). Corporate governance and corporate social responsibility disclosures in insurance companies. International Journal of Accounting & Information Management, 27(2), 284–300. https://doi.org/10.1108/IJAIM-10-2017-0120

- Wahba, H., & Elsayed, K. (2015). The mediating effect of financial performance on the relationship between social responsibility and ownership structure. Future Business Journal, 1(1–2), 1–12. https://doi.org/10.1016/j.fbj.2015.02.001

- Wahyudi, S. (2018). Analysis of effect of firm size, institutional ownership, profitability, and leverage on firm value with corporate social responsibility (CSR) disclosure as intervening variables (study on banking companies listed on BEI period 20122016). Jurnal Bisnis Strategi, 27(2), 95. https://doi.org/10.14710/jbs.27.2.95-109

- Zaid, M. A., Wang, M., & Abuhijleh, S. T. (2019). The effect of corporate governance practices on corporate social responsibility disclosure: Evidence from Palestine. Journal of Global Responsibility, 10(2), 134–160. https://doi.org/10.1108/JGR-10-2018-0053