?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

While uncertainty shocks affect equity markets at various investment horizons, knowledge about the causal effects of uncertainty and equity markets in the frequency domain is scant among the Group of Twenty (G20) countries regarded as systemically important economies. This paper explores the causal relations between domestic and international (US) economic policy uncertainties (EPU) and equity market returns of G20 countries. By employing the frequency-domain causality test, with monthly data spanning January 1997 to June 2021, we reach the following conclusions: 1) irrespective of the frequency, there is more support for the equity-leading hypothesis, implying that domestic stock market volatility contributes to increasing domestic policy uncertainty, as policymakers occasionally have to alter policies in reaction to elevated stock market volatility; 2) the causality between policy uncertainty (whether domestic or international) and equity returns is sensitive to heterogeneous investment decisions and policy uncertainty across horizons in most of our sample; 3) International (US) policy uncertainty has a domineering causal effect in predicting domestic equity returns, relative to domestic policy uncertainty in the short run of about 2.5 months or less. Therefore, the prediction that stock prices fall following government policy announcements is not always supported since countries are different.

Impact statement

The G20 forum comprises major economies representing a significant part of global economic activity and playing a crucial role in global economic governance. Therefore, decisions taken at the G20 forum should represent important news for financial markets with potential effects on asset prices. Moreover, market participants in these markets react to and value information relating to policy developments heterogeneously based on the differences in the formation of their beliefs, preferences, risk tolerance abilities, information assimilation, liquidity needs, investment objectives and institutional constraints. However, previous literature has mainly assumed homogeneity in agents’ behaviour, resulting in a dearth of knowledge about the causal effects of uncertainty and equity markets in the frequency domain among the G20 countries. Therefore, this paper analyses the dependence between domestic and international policy uncertainties and equity market returns of G20 countries in the frequency domain. The results show that the dependence patterns between EPU and equity returns tend to vary across different investment horizons in support of the predictions of the fractal market hypothesis. Nonetheless, the stock price leading hypothesis is more dominant regardless of the investment horizon, suggesting that frequent interventions by policymakers to dampen market volatility during periods of high policy uncertainty may exacerbate the uncertainty. Moreover, International (US) policy uncertainty has a domineering causal effect in predicting domestic equity returns relative to domestic policy uncertainty in the short run of about 2.5 months or less. By assuming the homogeneity of market participants, this study offers a nuanced understanding of causal relationships across different time horizons. The findings challenge conventional wisdom about the impact of policy uncertainties on equity markets, revealing complex and heterogeneous effects across countries. These results have significant implications for policymakers, investors, and financial institutions by providing a more accurate and granular perspective on risk management, portfolio allocation, and policy design.

Reviewing Editor:

1. Introduction

The G20 forum comprises major economies representing a significant part of global economic activity and playing a crucial role in global economic governance. The G20 forum constitutes about 82% of world GDP and 72% of international trade, representing about a third of the world population. Therefore, decisions taken at the G20 forum should represent important news for financial markets, and asset prices reflect such news (Duca & Stracca, Citation2014). The G20's diverse membership offers a unique research environment for studying EPU and equity markets return (EMR), providing insights for portfolio allocation, risk management, and economic stability and growth policy decisions. Since the equity market is one aspect of the financial market that could be very sensitive to political nuances, uncertainty surrounding policy decisions at the G20 forum could elicit price reactions from the equity markets. Indeed, Pástor and Veronesi (Citation2012, Citation2013) theoretical and empirical findings indicate that, on average, stock prices fall when the government announces a policy change.

The existing literature has established a connection between policy uncertainty and stock prices with mixed evidence. For instance, several studies (Antonakakis et al., Citation2013; Hashmi et al., Citation2021; Ko & Lee, Citation2015; Škrinjarić & Orlović, Citation2020; Yang & Jiang, Citation2016) found an inverse relationship between stock prices and economic policy uncertainty (EPU) consistent with the predictions of Pástor and Veronesi (Citation2012, Citation2013). However, Wu et al. (Citation2016) argue that this negative effect of policy uncertainty on stock prices does not hold in all contexts since countries are different. Moreover, Kannadhasan and Das report the presence of lower-tail and upper-tail dependence between stock returns and EPU. Evidence of symmetric and asymmetry effects is reported by Aydin et al. (Citation2021), the time-varying causal effects are revealed by Antonakakis et al. (Citation2013) and Hong et al. (Citation2024), while Albrecht et al. (Citation2023) revealed the changing nature of this relationship across frequency scales.

Moreover, studies such as Wu et al. (Citation2016) and Ulusoy (Citation2019) have established four causal outcomes between policy uncertainty and the stock market returns nexus. These include the Uncertainty-leading hypothesis (ULH), the stock price or equity-leading hypothesis (ELH), the feedback or bidirectional causality hypothesis (FBH), and the neutrality hypothesis (NTH). While the extant literature has explained some dimensions of the relationship between policy uncertainty and stock prices, they mainly focused on the time domain perspective, except those who provided evidence supporting symmetric and asymmetry frequency causality. Consequently, the literature leaves other important relationship aspects unexplained, such as the frequency dynamics. Nevertheless, Dew-Becker and Giglio (Citation2016) argue that the frequency domain is the ideal setting for analysing the dynamic effect of shocks in asset pricing literature.

Moreover, the extant literature on EPU and equity returns often relies on time-domain techniques such as the Granger causality test. Whereas these techniques are essential, they might not fully capture the dynamic nature of the relationship, particularly how the impact of EPU on equity returns might vary across different frequencies. That is at the short-, medium–, and long-term investment horizons. Nevertheless, it would be helpful to understand the causal effects of uncertainty and equity markets at different investment horizons in the interest of policymakers and investors. This knowledge is necessary because short-term and long-term changes in uncertainty may have an entirely different impact on the equity market performance and vice versa and, thus, should be regulated differently. Therefore, we envisage causality in the frequency domain because shocks to economic activity affect variables at different frequencies with varied strengths (Baruník & Křehlík, Citation2018). We believe that economic agents operate on different investment horizons represented by frequencies ranging from seconds to several years based on the formation of their preferences, beliefs, risk aversion, investment objectives, information assimilation, and institutional constraints, which tend to be heterogeneous.

Consequently, economic and financial shocks that trigger policy uncertainty can be transmitted through the stock markets, resulting in different frequency responses. On the one hand, investors with short investment horizons, such as day traders or hedge funds, typically prioritise capital preservation and focus on managing short-term volatility. These investors are more interested in the short-run operational state of the market. Therefore, they make decisions based on temporal conditions such as sporadic events or psychological factors. Consequently, such investors react to shocks in the short term. On the other hand, large institutional investors like pension funds and insurance companies are more concerned about the market’s long-term performance or prospects. As a result, they react to shocks that have long-term implications (Wang & Wang, Citation2019).

Dew-Becker and Giglio (Citation2016) also posit that a shock with strong long-run effects has high power at low frequencies. In contrast, shocks that dissipate rapidly have comparatively greater power at high frequencies. Based on this logic, we believe that sudden policy changes with long-term effects will have high power at low frequencies, and if they are transmitted to the stock market, they point to long-run causality. For example, in the case of the equity market, long-run causality could be explained by permanent changes in expectations about future dividends (Baruník & Křehlík, Citation2018). This frequency decomposition of policy shocks is natural to imagine following Barrero et al. (Citation2017) revelation that uncertainty has short and long-term components. Indeed, Albrecht et al. (Citation2023) argue that the nexus between stock market returns and uncertainty is highly volatile, with uncertainty relating to stock market returns differently for each frequency scale. Having established the need to examine the causal dynamics between EPU and EMR in the frequency domain, we now provide the linkages through which policy uncertainty from international sources, such as the US economy, can influence domestic stock prices.

Globalisation is characterised by liberalising trade and capital accounts, enabling the movement of goods, services, and capital across national borders. The increasing flow of capital across borders and a diminishing information asymmetry occasioned by advanced information communication technology have stimulated financial integration (Beine & Candelon, Citation2011). Financial integration connotes a more coordinated behaviour of equity markets across countries. However, an elevated level of cross-market linkages reduces the rewards of international diversification and triggers the risk of adverse economic shock transmission. Thus, in Lehkonen’s (Citation2015) words, market integration can be likened to a double-edged sword. He reiterates that the rewards of globalisation of markets are questionable because these markets were the ones that transmitted the tremors of the global recession to the rest of the world. The international capital markets typically exhibit significant cross-market linkages (generally referred to as contagion) following periods of adverse market conditions (Longin & Solnik, Citation2001).

Nonetheless, Forbes and Rigobon (Citation2002) argue that contagion occurs when a substantial surge in cross-market linkages follows a shock to one market. Accordingly, interdependence is the strong market comovement across different market conditions (bullish, normal, and bearish). The interdependence between markets could serve as a conduit through which macroeconomic shocks are transmitted to other markets. Therefore, uncertainty, no matter its source, could cause worry in financial markets in a world of increasing interdependence. Bloom (Citation2017) observes that a large part of the policy uncertainty tremors in every country has some foreign origin. Small countries are significantly affected by external uncertainty shocks from foreign sources compared to large countries. If this is so, we should expect to see the domestic shocks of small markets amplified by external shocks. Consequently, the causal effect of domestic and international uncertainty shocks on equity returns may evolve differently. Previous studies affirm this observation. For example, Klößner and Sekkel, (Citation2014) find that among developed economies, a more significant part of the dynamics of uncertainty is attributed to spillovers, and the US and the UK propagate a large proportion of the uncertainty shocks. In contrast, the rest of the countries are receivers of shocks.

As indicated earlier, uncertainty shocks originating from larger markets are not always confined to them. To this end, Forbes and Chinn (Citation2004) posit that trade-related volatility in the US affects financial markets globally. Similarly, Ehrmann and Fratzscher (Citation2009) report that monetary policy contraction in the US conveys shocks that negatively affect as many as 50 stock markets worldwide. The US is recognised as the world’s largest equity market; as a result, it is always used as the yardstick to assess the health of global stock markets. The US market is recognised because it adheres to good corporate governance practices and declining information asymmetry. Therefore, international investors always monitor the conditions of the US economy and its markets. Consequently, any volatility emanating from this market is usually reflected in the behaviour of foreign investors. The changed reaction of international investors relating to their perception of the economy’s future course and prospects could trigger a change in asset prices and an upsurge in market volatility (Das et al., Citation2019).

Therefore, this study contributes to the debate on the EPU – EMR nexus by answering the following pertinent questions: 1) what is the causality between domestic policy uncertainty and domestic equity returns? 2) what is the causal relationship between international policy uncertainty (US EPU) and domestic equity returns? 3) between domestic and international (US) policy uncertainties, which one matters in predicting returns of domestic equity markets? Based on these research questions, we formulate four hypotheses to guide the study as follows: 1) DEPU Granger causes (GC) EMR (

); 2)

3)

and 4)

The findings indicate that in the short run (2.5 months or less), the study confirms the equity leading hypothesis (ELH) in Australia, Canada, Germany, Japan, South Korea, Mexico, Brazil, Indonesia, and the US. DEPU leading hypothesis (ULH) is supported only in Italy; the feedback hypothesis (FBH) is reported in France and India, while China, Russia, the UK, Argentina, South Africa, Turkey, and the EU support the neutrality hypothesis (NTH). The equity-leading hypothesis is documented in Australia, Canada, China, Germany, Mexico, Brazil, and the EU in the transitionary period. ULH is supported in France, India, and Italy. The findings support the FBH in Japan, Korea, and the US, while the neutrality hypothesis is confirmed in Russia, Argentina, Indonesia, South Africa, Turkey, and the UK. In the long run (about 12 months and beyond), ULH is supported only in the US. ELH is found in Australia, Canada, China, Germany, India, Japan, Mexico, the UK, Brazil, and the EU. FBH is only supported in Italy and South Korea, whereas the NTH is confirmed in France, Russia, Argentina, South Africa, Turkey, and Indonesia. Regarding the US EPU-EMR causal nexus, Germany, Mexico, Brazil, and Turkey confirmed ELH in the short run. ULH is supported in China, France, Italy, Russia, and the UK. The NTH is supported in Australia, Canada, India, Japan, South Korea, Argentina, the EU, South Africa, and Indonesia, while there is no evidence in the case of the FBH. The results support the ELH in the intermediate period in Canada, Germany, Japan, Argentina, Brazil, South Africa, Turkey, and Indonesia. ULH is evident in Italy, Russia, and the UK. France and Mexico follow the FBH, while Australia, China, India, South Korea, and the EU follow the NTH. Finally, ELH dominated in the long run in Australia, Canada, Germany, India, Mexico, Russia, Argentina, Brazil, the EU, South Africa, Turkey, and Indonesia. Only Frances follows the ULH and NTH, respectively, and FBH is confirmed in Italy, Japan, South Korea, and the UK. When making optimal decisions, these results hold important implications for policymakers, investors, and other market participants.

The remainder of the paper is structured as follows: Section 2 presents a review of previous literature; Section 3 outlines the estimation strategy and data; Section 4 presents and discusses the paper’s results; and, lastly, sections 4 and 5, respectively, discusses policy implications and concludes.

2. Review of previous studies

Pástor and Veronesi (Citation2012, Citation2013) explain that high policy uncertainty leads to low stock prices. The authors clarify that policy uncertainty has two effects on stock prices—thus, the cash flow effect and the discount rate effect. The cash flow effect explains the positive effect of a new policy announcement on stock prices when the existing policy produces lower-than-expected realised profitability. In this case, changing the non-performing policy is typically interpreted as good news to investors, leading to a rise in stock prices.

Nonetheless, because of the uncertainty about the prospects of the new policy on profitability, a policy change may raise the discount rate, leading to a fall in stock prices, which is the discount rate effect. Pástor and Veronesi (Citation2012, Citation2013) further argue that the discount rate effect is larger than the cash flow effect, causing stock prices to fall at the announcement of a government policy change. Positive announcement returns tend to be small as investors mostly anticipate policy changes that cause stock price rises. Additionally, because new policies can add extra uncertainty and increase the volatility of the random discount factor, risk premia increases, stock return volatilities get elevated, and correlations become stronger among firms.

Having discussed the theory linking policy uncertainty to stock prices, we next consider the fractal market hypothesis (FMH) proposed by Peters (Citation1994) as the theoretical basis underpinning the frequency domain approach that the study adopted. Contrary to the efficient market hypothesis (EMH) that assumes homogeneity of all investors, it suggests that all investors use the available information similarly and operate on the same investment horizon. However, investors in the capital markets, particularly those in the stock market, comprise various investors with different investment horizons, ranging from seconds (market makers), minutes (noise traders), days and weeks (technical traders), monthly (fundamental analyst) up to several years (pension funds). These groups of investors value and treat information differently. Similarly, each group has unique trading rules and strategies. While one group may interpret information as severe losses, it could mean profitable opportunities for others. The FMH asserts that liquidity maintains the market’s stability, which ensures smooth pricing processes; a lack of liquidity can lead to extreme market movements. FMH emphasises the heterogeneity of investors, focusing on their investment horizons. Market participants have varying horizons, from seconds to years. Investors with different horizons react differently to information, with short-term investors focusing on technical information and crowd behaviour and long-term investors focusing on fundamental information. The existence of investors with diverse horizons ensures market stability, as dominant horizons may cause price collapse. Therefore, the FMH suggests that stable market phases involve equal representation of investment horizons, while unstable periods, like crises, result in inefficient clearing of supply and demand among investors.

Earlier studies by Wu et al. (Citation2016) and Ulusoy (Citation2019) classify the causal nexus between economic policy uncertainty and equity returns into four causal outcomes or hypotheses as follows: 1) unidirectional causality running from uncertainty to equity market returns, which they labelled as uncertainty leading hypothesis, 2) unidirectional causal relationship from equity markets returns to uncertainty, which refers to termed as the equity or stock price leading hypothesis, 3) studies that find a bidirectional relationship between economic policy uncertainty and equity market returns, which we referred to as the feedback hypothesis, and 4) finally, studies that find no causal relationship between the economic policy uncertainty and equity market returns, which we christened as neutrality hypothesis.

In contrast to Pástor and Veronesi (Citation2012, Citation2013) prediction that stock prices fall at the announcement of a government policy change, Wu et al. (Citation2016) argue that this theory does not hold in all contexts since countries are different. The authors’ findings support the stock market-leading hypothesis in India, Italy, and Spain using the bootstrap panel Granger causality approach to examine the causal nexus between EPU and stock prices in nine countries. The economic policy uncertainty leading hypothesis was only confirmed for the UK, while the neutrality hypothesis was supported in Canada, China, France, Germany, and the US. However, the paper rejected the feedback hypothesis. Similarly, following the same method, Ulusoy (Citation2019) found strong evidence in support of the stock price leading hypothesis in the US, Canada, Sweden, South Korea, Brazil, India and Chile, while the EPU leading hypothesis and feedback hypothesis were detected only in Hongkong and Singapore, respectively. The neutrality hypothesis was associated with most countries, including Germany, the UK, Italy, Australia, Russia, Mexico, Spain, the Netherlands, and Ireland. The authors argue that the forward-looking nature of stock prices may act as a leading indicator of uncertainty. They suggested that this predictive power may imply that causality runs from stock returns to EPU as stock markets mature in developed and emerging countries and influence, even master, the behaviour of all stakeholders, including policymakers. In a related study, Saeed et al. (Citation2023) Granger causality test results confirm a unidirectional causality from stock prices to economic policy uncertainty in India. This result implies that the stock market predicts the EPU, not vice versa. The paper concludes that investors should consider economic policy uncertainty a systematic risk when making investment decisions.

While prior studies mainly used time-domain approaches, Aydin et al. (Citation2021) examine the EPU–stock prices nexus using symmetric and asymmetric frequency domain approaches in BRIC countries. The results of the symmetric test confirm one-way permanent causality from EPU to stock prices in Brazil and India, while the asymmetry test reveals no causal relationship between EPU and stock prices in the case of China. The asymmetry results for Brazil and India show unidirectional long-run causal relations originating from positive shocks from EPU to positive shocks in stock price. Moreover, Brazil exhibits unidirectional short-run causality from adverse shocks from EPU to negative shocks in stock prices. India also records short-run causality but in the opposite direction.

Several studies (Antonakakis et al., Citation2013; Hashmi et al., Citation2021; Ko & Lee, Citation2015; Škrinjarić & Orlović, Citation2020; Yang & Jiang, Citation2016) posit an inverse relationship between stock prices and economic policy uncertainty (EPU). Many of these studies report that higher uncertainty episodes are associated with sharp declines in stock returns, and this relationship is more robust when US EPU overlaps with the domestic policy uncertainty of other countries. For instance, Ko and Lee (Citation2015) posit that the correlation between stock returns and EPU is stronger when US EPU commoves with other countries’ EPUs. Colombo (Citation2013) reported similar findings regarding the EPU spillover between the US and the Eurozone. Extending the work of Ko and Lee (Citation2015), Das and Kumar (Citation2018) find that emerging stock markets are more sensitive to local policy uncertainty (DEPU) relative to international EPU, while developed markets tend to be more susceptible to global EPU shocks. Consistent with these results, Hong et al. (Citation2024) maintain that Global EPU significantly impacts developed equity markets relative to domestic EPU. They added that the causal impact of DEPU and GEPU on equity markets manifests mainly in the long run. However, the stock price leading hypothesis is confirmed for almost the entire sample. In contrast, the uncertainty-leading hypothesis is evident in only half of the sample, albeit in a time-varying context. These results bring to the fore the crucial role of emerging economies as a hub for risk reduction via diversification by international investors.

Scores of studies have investigated the impact of external shocks, particularly those emanating from policy uncertainty on equity markets in emerging and developed financial markets. For instance, Kannadhasan and Das examine the differential impact of EPU and GPR on Asian equity markets and report the presence of lower tail and upper tail dependence between stock returns and EPU and GPR, respectively. They also document an asymmetric dependence between uncertainty measures and equity returns. Also, Das et al. (Citation2019) examine the effects of US EPU, GPR, and financial stress (FR) on emerging markets and report the heterogeneous effect of the different uncertainty shocks on equity market returns in various countries regarding their causal impact and intensity. However, the reaction of EPU was found to be stronger compared with the other tremors. They also find causality-in-mean to be more robust than the causality-in-variance, and these shocks’ prediction ability is limited to the extreme upper tail. In Africa, Asafo-Adjei et al. (Citation2020) find that global EPU correlates with most of the stock returns of African equity markets in the long term. This result implies that short-term investments in African equity markets are less sensitive to global EPU shocks and, thus, suitable for hedging purposes by international investors.

Turning to the causal relations between domestic economic policy uncertainty and domestic equity returns, scores of studies (Ajmi et al., Citation2015; Li et al., Citation2016; Ongan & Gocer, Citation2017) find mixed results. For instance, Ajmi et al. (Citation2015) investigate the causal nexus between economic policy uncertainty and US equity market uncertainty (EMU) using daily data from 1/01/1985 to 14/06/2013. The Granger causality test results document reverse causality between the two series. However, short-run parameter instability makes the linear model results unreliable. Therefore, they employ a nonlinear test and find unidirectional causality from EMU to EPU.

Contrary to the findings of Ajmi et al. (Citation2015), Ongan and Gocer (Citation2017) examine the causal relations between EPU and returns of various stock indices in the US, relying on linear and nonlinear rolling window causality approaches and find evidence of causality originating from EPU to stock returns. Specifically, US EPU causes the change in the Nasdaq 100 index both in the short and long term. They also find some evidence supporting causality from stock returns to EPU during the period 2008–2013, when the effect of the global financial crisis was at its peak. The overall conclusion from this study is that there is some modicum of bidirectional causality between US EPU and own-stock returns. Li et al. (Citation2016) report similar evidence of bidirectional causality. Li et al. (Citation2016) find reverse causality between EPU and the returns of the equity markets in China and India when the rolling window approach is used. However, a weak correlation between EPU and stock returns is uncovered when the Granger causality approach is employed. Implying that heightened economic uncertainty will reduce stock returns just as elevated stock market volatility will amplify economic policy uncertainty.

The study also confirms the causal nexus between international EPU and stock returns. For example, relying on non-structural vector autoregression (VAR) and Vector Granger causality tests (VGC), Alqahtani and Taillard (Citation2019) study the impact of US EPU on stock market returns of Gulf Cooperation Council (GCC) countries. Results of the VAR model suggest that, except for Bahrain, US EPU has a marginal effect on the GCC's equity markets. The VGC test reveals that changes in US policy uncertainty affect Qatar’s stock market returns. Moreover, using the Granger causality test and the nonparametric causality-in-quantile approaches to examine the causal effect of domestic and international EPU on stock returns and its volatility, Balcilar, Gupta et al. (Citation2019) find no evidence of domestic EPU explaining changes in stock returns in South Korea when Granger causality test is applied. However, the study detects strong evidence of causality from EPU to stock returns volatility in Malaysia and found that both stock returns and volatility are along with some aspects of the conditional distributions for South Korea.

On the other hand, the study found no evidence of causality between domestic and global EPUs and stock returns and volatility in Hong Kong. In the presence of nonlinearity, the results from the causality-in-quantile tests are considered more robust relative to the Granger causality test. Also, Albrecht et al. (Citation2023) document that during global financial turbulence, particularly in the US, Japan, and Germany, the EPU predicts short- and long-term equity markets, while Hashmi et al. (Citation2021) find a time-varying correlation between GEPU and Indonesian stock returns.

In brief, while the extant literature has explained some dimensions of the relationship between policy uncertainty and stock prices, it leaves other important aspects unexplained, such as the frequency dynamics. It is this knowledge gap that this present study seeks to fill by employing the frequency domain approach of Breitung and Candelon (Citation2006).

3. Methodology

3.1 Estimation procedure

To test the causal nexus between domestic and international (US) economic policy uncertainty and equity market returns (EMR), we adopt the Breitung and Candelon (Citation2006) frequency-domain approach, which is an extension of Geweke (Citation1982) and Hosoya’s (Citation1991) causality frameworks. Gokmenoglu et al. (Citation2019) highlighted the following as the advantages of the frequency-domain causality test (also known as spectral BC causality test) over the time-domain approach: (i) while the frequency-domain approach determines the degree of specific variation in the time series, the time-domain approach identifies when a particular variation happened within a time series. (ii) The frequency-domain approach permits the observation of asymmetries and decomposes the causality test statistics into different frequencies. (iii) The frequency domain can eliminate seasonal pattern variations associated with short series. These advantages and the fact that the spectral framework can capture the bidirectional association between variables motivated its selection for our study. Specifically, we adopted the spectral BC framework and followed the empirical path of Gokmenoglu et al. (Citation2019) and Ibrahim et al. (Citation2021). Using the exposition and notation in Breitung and Candelon (Citation2006) to capture the causal relationship between EPU and EMR among selected G20 countries, we permit be the two-dimensional covariance-stationary vector variables that assume a finite-order VAR(p) process:

(1)

(1)

where

is a

lag polynomial with

denotes the vector of the error term, which is normally distributed with a zero mean (

and a positive definite covariance (

We ignore the deterministic terms in EquationEq. (1)

(1)

(1) to simplify the explanation.

We allow to denote the lower triangular matrix of the Cholesky decomposition.

such that

and

If the system’s stationarity assumption holds, then we represent its Moving Average (MA) representation as

(2)

(2)

(3)

(3)

where

and

Using this representation, we express the spectral density of

as

Geweke (Citation1982) and Hosoya (Citation1991) proposed a measure of causality:

(4)

(4)

The measure of causality will be zero if so that we indicate that EPU does not Granger cause EMR at the frequency

If the elements of

are integrated, then

has a unit root. In this case, given the frequency domain, we define the measure of causality based on the following orthogonalised MA representation:

(5)

(5)

where

Engle and Granger (Citation1987) state that, in a bivariate co-integrated system

where

is a co-integrated vector such that

is stationary. Thus, the resulting causality measure is given by:

(6)

(6)

Thus, we test the hypothesis that EPU does not Granger cause EMR at the frequency by expressing our null hypothesis within the bivariate framework as follows:

(7)

(7)

Breitung and Candelon (Citation2006) show that the hypothesis in EquationEq. (7)(7)

(7) is identical to the following linear restriction:

(8)

(8)

where

and

The null hypothesis in EquationEq. (7)(7)

(7) can be verified using F-statistic or Wald test statistics, which is approximately distributed as F(2, T-2p) for

where T denotes the number of observations in the series needed to estimate the VAR model of order P, and 2 is the number of restrictions imposed on the VAR estimator. In this paper, we select P based on the Akaike information criterion (AIC).

Following Ciner (Citation2011) and Ibrahim et al. (Citation2021), we conduct our causal examination at three different frequencies (i.e., ω: ω = 2.5;1.5 and 0.5) to investigate the causal dynamics at the short-run, intermediate period, and long-term investment horizons. Accordingly, our paper estimates the Wald test statistic at low (ω = 0.5), medium (ω = 1.5) and high frequencies (ω = 2.5), consistent with Ciner (Citation2011) and Ibrahim et al. (Citation2021). The test statistics correspond to wavelengths of 12 months, 4.5 months, and 2.5 months at these frequencies, respectively. If we can establish the causality between EPU and EMR over the different frequencies, the BC causality would have resolved the lapses associated with the traditional Granger causality approach. Therefore, for each frequency (ω), it is possible to decipher four causal outcomes following the categorisation of Ulusoy (Citation2019) and Wu et al. (Citation2016). First, this is the case where economic policy uncertainty causes equity returns, which we denote as the uncertainty-leading hypothesis (ULH). The second is the situation where equity returns Granger causes uncertainty, termed the equity-leading hypothesis (ELH). Next is the feedback hypothesis (FBH), where there is bidirectional causality between EPU and EMR. The neutrality hypothesis (NTH) is the final causal outcome, with independent policy uncertainty and equity returns.

3.2 Data

We obtained data from 19 G20 countriesFootnote1 to conduct the study. For the EPU indices, we adopt monthly data from January 1997 to April 2021 from the EPU website at http://www.policyuncertainty.com. The data at this site is available for Australia, Canada, China, France, Germany, Brazil, Japan, India, Italy, Mexico, Russia, South Korea, the UK, and the US. We obtained the rest of the data from individuals and institutions who have developed the indices following the methodology of Baker et al. (Citation2016). For instance, Hlatshwayo and Saxegaard (Citation2016) constructed South Africa’s EPU index. Kurniati (Citation2018) proposed Indonesia’s EPU Index. Jirasavetakul and Spilimbergo (Citation2018) and Andres et al. (Citation2022) constructed Turkey and Argentina’s EPU indices. Finally, Dumayiri et al. (Unpublished) developed the EU EPU index. Following (Das & Kumar, Citation2018), we performed the natural logarithmic transformation of the EPU index series. We sourced the stock price (SP) index data from Thomson Reuters DataStream. The SP series were converted into returns using the continuously compounded returns formula. The Asian financial crisis triggered the formation of the G20 forum in 1997. Accordingly, we start our analysis using 1997 as the beginning point. However, we selected the study’s endpoint (2021) based on data availability in the countries of interest. We use the US EPU as the proxy for International EPU because the US economy is the world’s largest economy, and investors typically use the US equity market as the barometer to assess the health of global equity markets. All the series are stationaryFootnote2.

4. Results and discussions

4.1 Preliminary analysis

shows descriptive statistics for the EPU and EMR series. Considering the results presented in panel A, the 19 countries’ Logarithmic EPU series exhibit different means and standard deviations, signifying disparate policy uncertainty changes. Especially, Brazil, the UK, France, Russia, Germany, China, and South Korea have relatively larger average EPUs. In contrast, Mexico, India, Italy, Japan, Indonesia, and Australia have a smaller average EPU, implying that the study observed more volatile economic risk conditions in Brazil, the UK, France, Russia, Germany, China, and South Korea. Furthermore, Argentina has the highest absolute and relative volatilities as indicated by its standard deviation (87) and Coefficient of variation (CV) (1250.43), reflecting the possible increase in policy uncertainty following Argentina’s unemployment crisis and the historic defeat of the incumbent president Mauricio Macri by Alberto Ángel Fernández. Comparing all countries’ maximum and minimum values suggests more fluctuation with some modicum of instability over time. The skewness statistics show that the EPU series for Argentina, Brazil, Canada, the EU, Germany, Indonesia, Italy, South Korea, Turkey, Mexico, and the US are positively skewed. In contrast, the remaining countries are negatively skewed. The kurtosis statistics show that, except for France, which has platykurtic distribution, the rest of the series have excess kurtosis and leptokurtic. The Jargue-Bera statistic confirms normality for Canada, Brazil, Germany, Russia, and the UK. However, the EPU series for the rest of the countries are non-normally distributed. , Panel B, displays the descriptive statistics of the equity returns series.

Table 1. Descriptive statistics.

Mean returns show that all countries record positive average returns, with Argentina and Turkey recording the highest average returns of 2.69 and 2.04%, respectively. Nonetheless, we observed a significant difference between the maximum and minimum values for all the countries, indicating their exposure to high volatilities and outliers with no sign of stability over time. Comparing the means to the standard deviations for all countries shows high absolute volatiles, with Russia showing the highest absolute volatility of returns. However, the values of the Coefficient of variation (CV) of 47.65 and 3.90, respectively, show Turkey and Italy as the countries with the lowest and highest relative returns volatilities.

The skewness and kurtosis statistics reveal that all the returns series are negatively skewed, have excess kurtosis, and are highly leptokurtic. This statistic indicates a relatively higher probability of obtaining extremely negative returns than extremely positive returns. Finally, the Jargue-Bera statistic confirms that all returns series are non-normally distributed. This indicates the presence of heavy- tails and excess kurtosis, implying the existence of nonlinearity. Given these data features, applying linear or constant parameter models in the analysis could produce spurious results. This informs us of our choice of the BC Spectral Causality test.

4.2 Frequency domain causality results

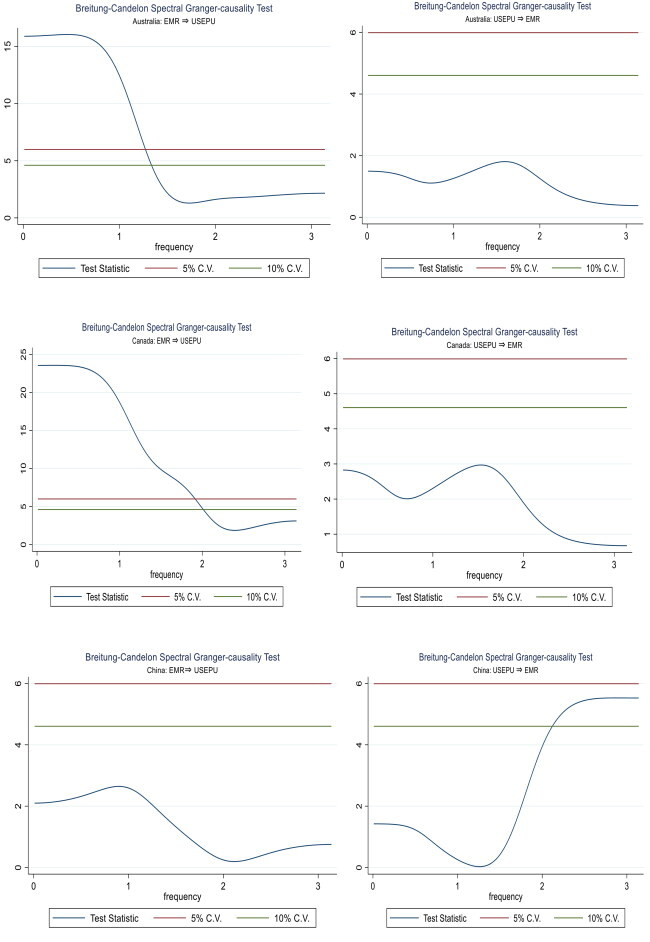

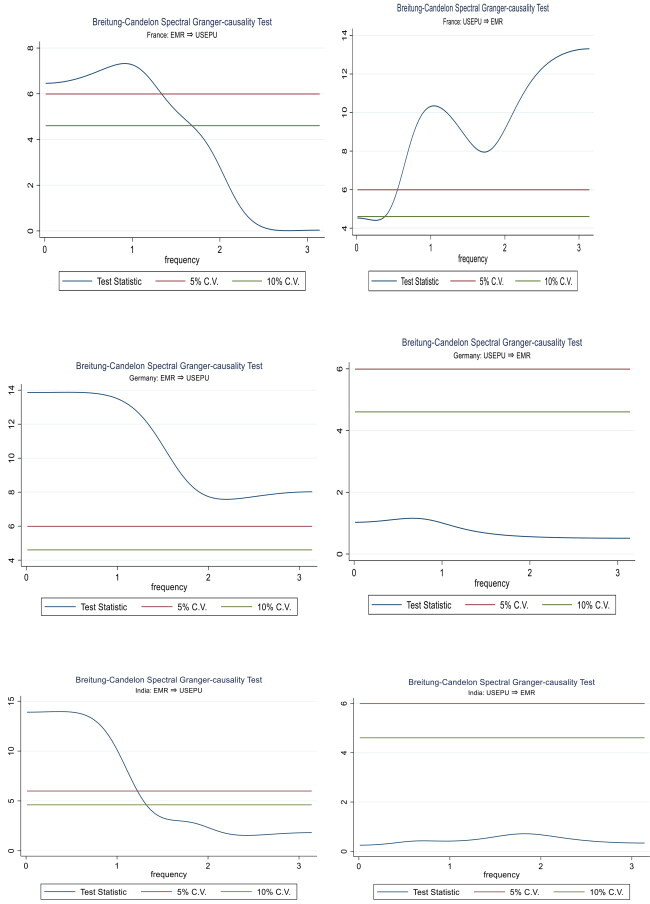

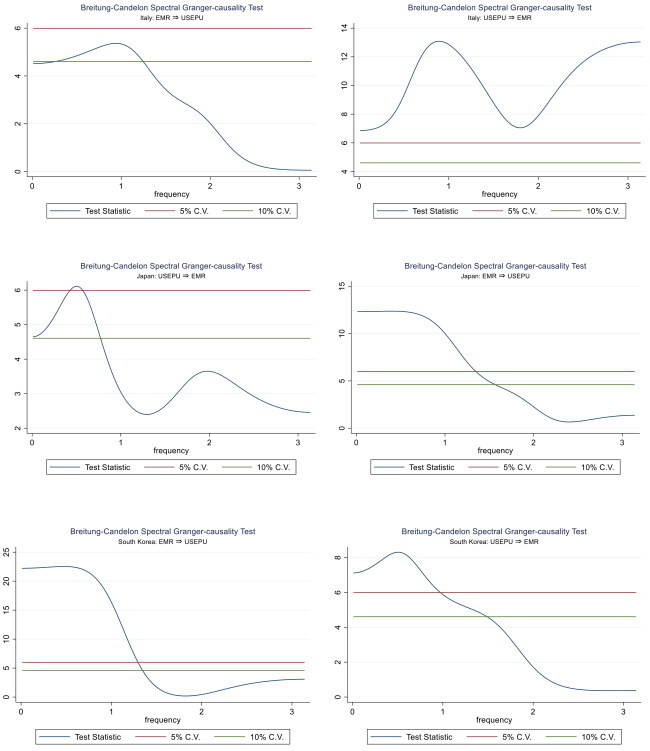

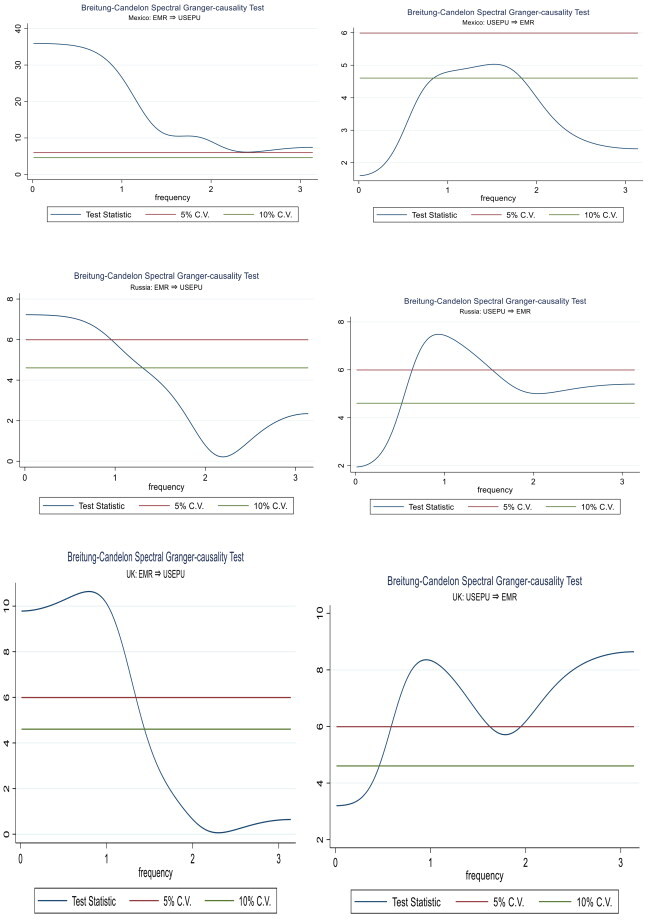

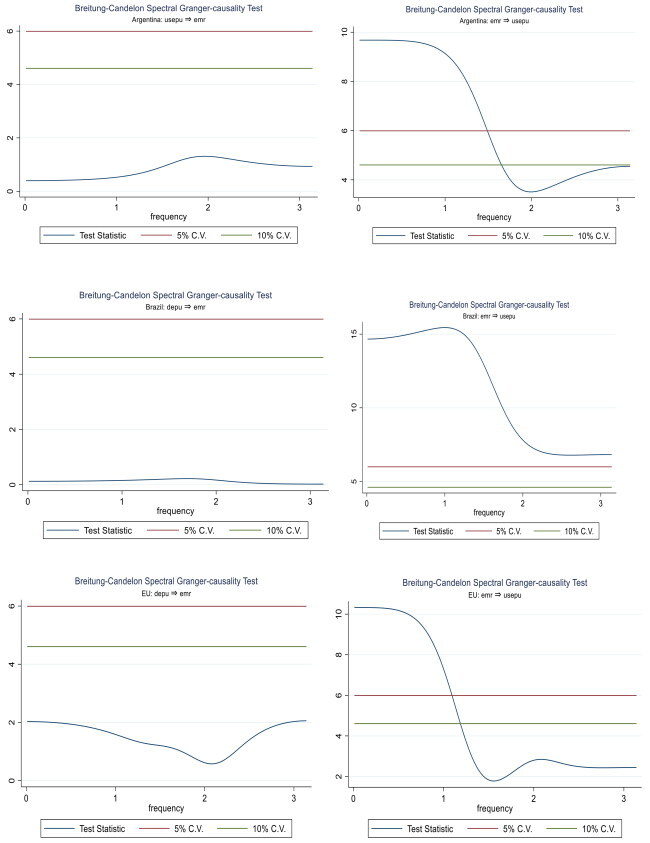

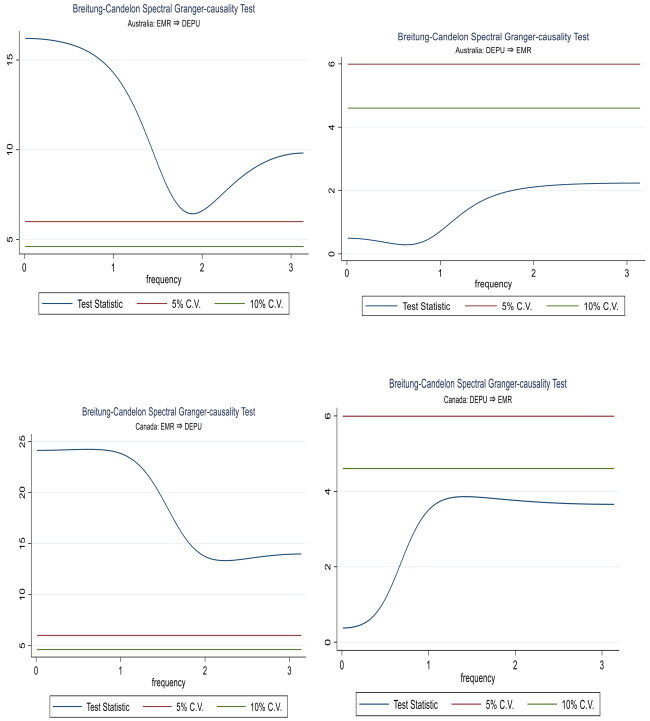

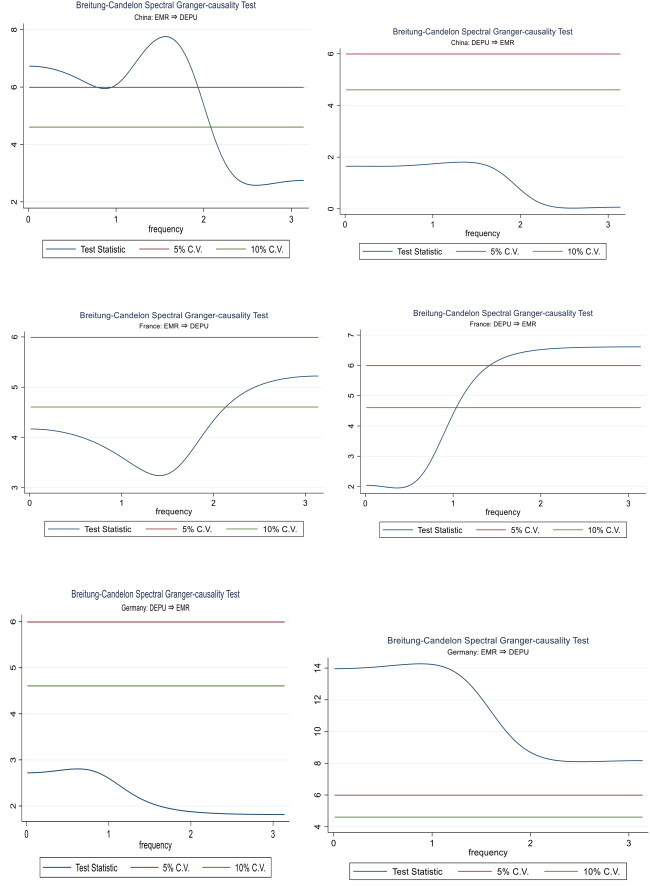

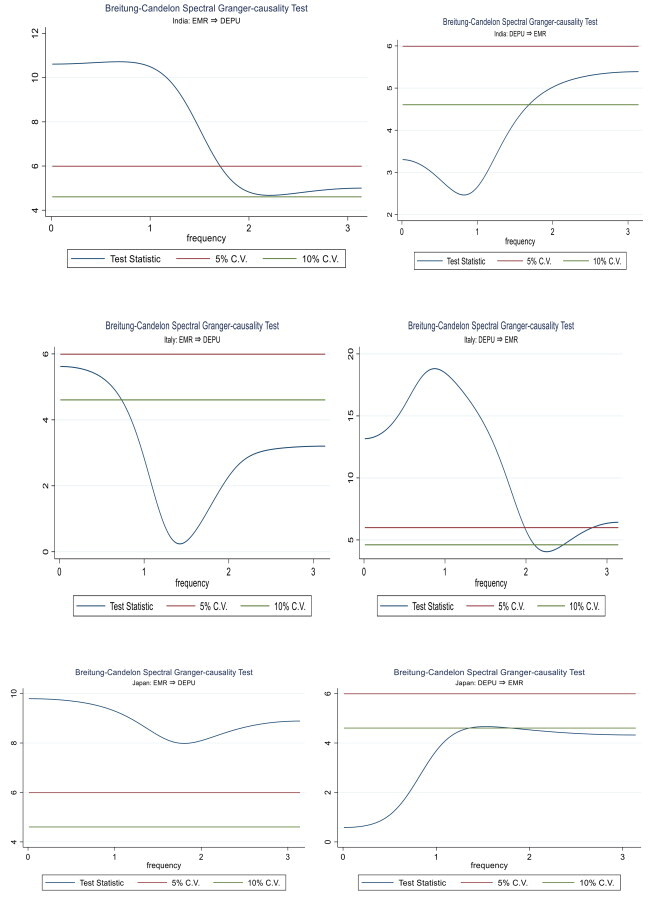

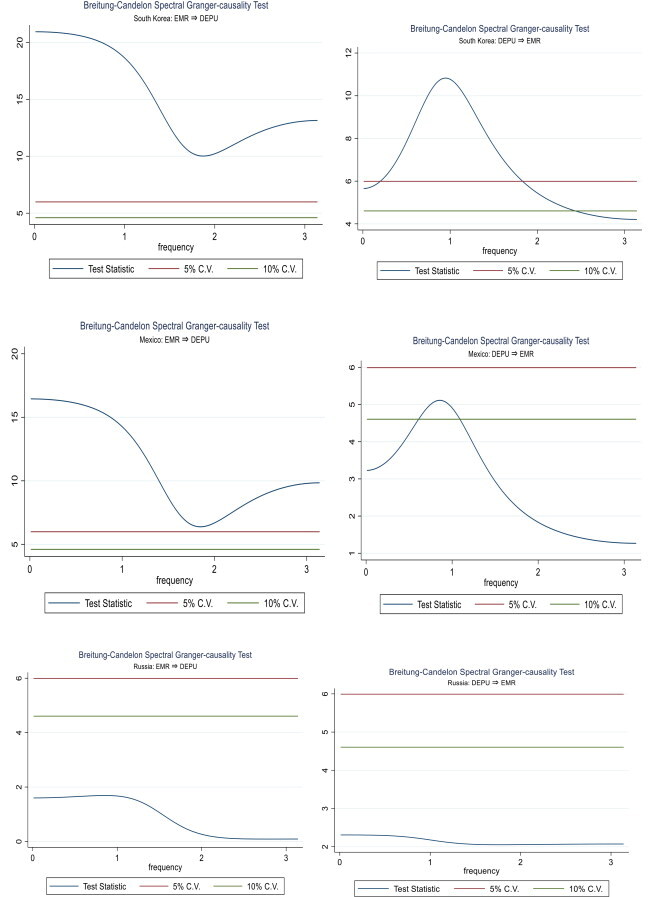

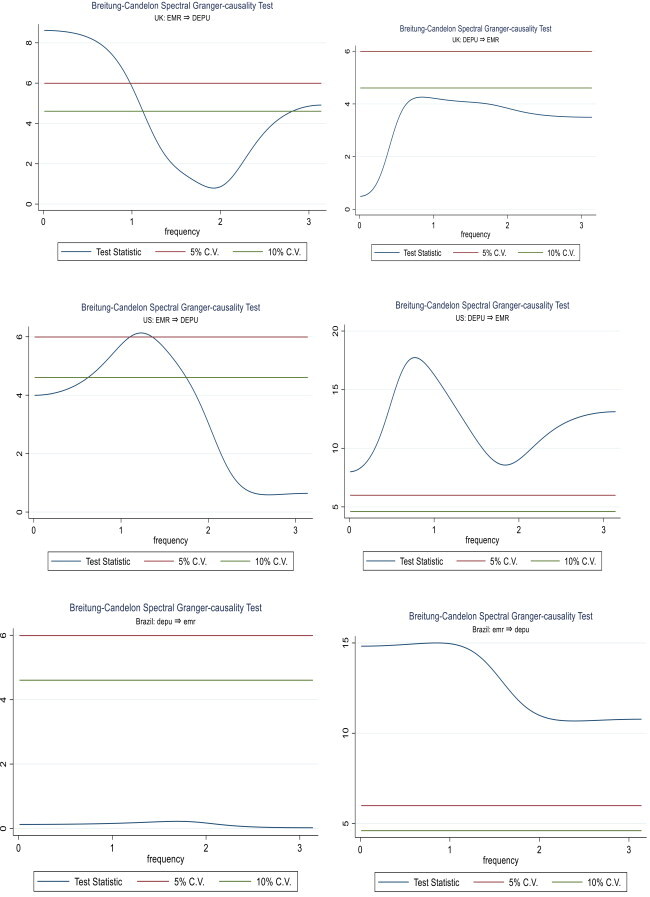

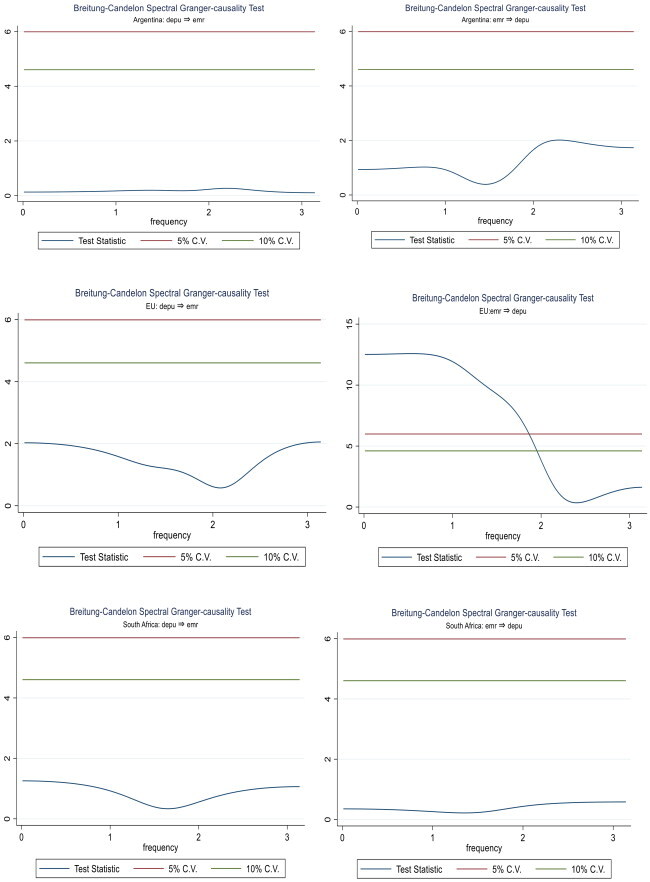

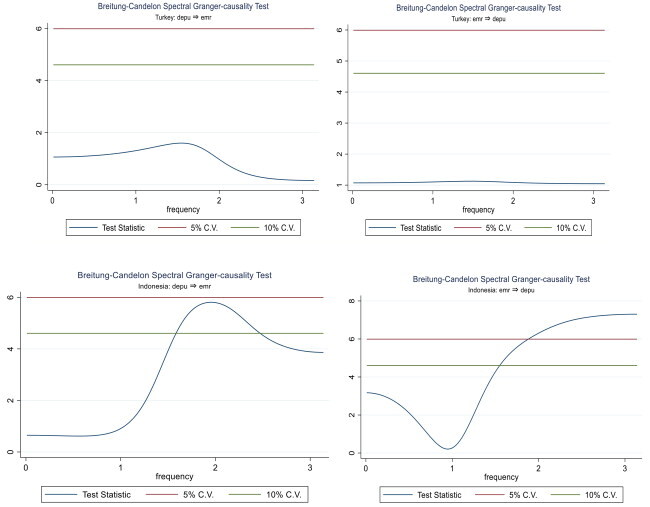

In this section, we present and discuss the results of our four hypotheses on the causality between economic policy uncertainty and the returns of the equity markets. All these analyses have been done at the three chosen frequencies. That is ω = 2.5, ω = 1.5 and ω = 0.5, representing the short-run, intermediate, and long-run periods, respectively. The results are contained in and , and their associated causality graphs are presented in Appendix A and B. For each table, the first column shows the country names, while columns 2 and 3 present the period for the analysis and the optimal lag selection. Next, we present the findings on the BC causality tests for the hypotheses: i) H0: DEPU⇒EMR, which denotes the null hypothesis of no Granger causality from domestic economic policy uncertainty (DEPU) to equity market returns and ii) H0: EMR ⇒ DEPU represents the null hypothesis of no Granger-causality from equity returns to DEPU. Finally, the last column presents the causal outcomes regarding the supported hypothesis at the different frequencies. To ensure easy comprehension of the results, we use graphs to visualise the hypotheses at the chosen frequencies (see and ).

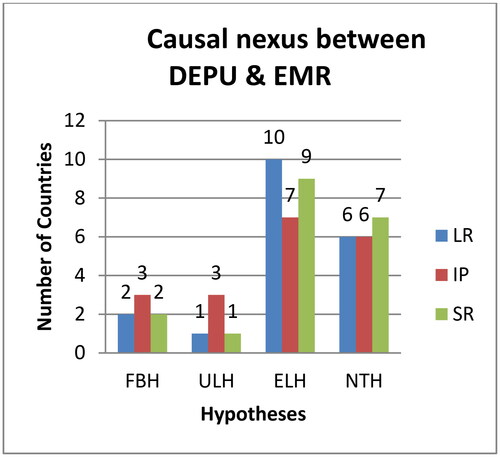

Figure 1. Causal nexus between DEPU & EMR.

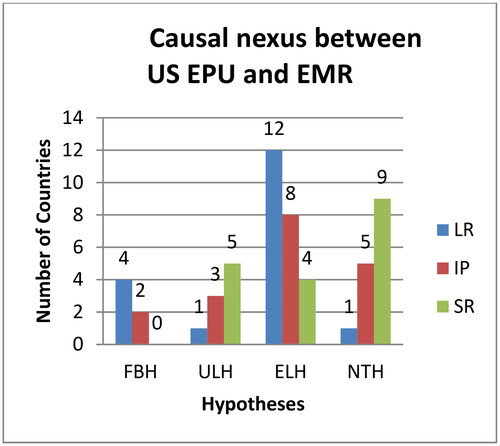

Figure 2. Causal nexus between US EPU and EMR.

Table 2. Causal nexus between domestic economic policy uncertainty and equity market returns.

shows the relationship between each country’s DEPU and equity market returns. Appendix A presents the associated causality graphs, which show the results of Granger causality at unknown frequencies. From and , in the long run, we observe that the ten countries, including Australia, Brazil, Canada, China, Germany, India, Japan, Mexico, the EU, and the UK results support the equity-leads hypothesis (ELH). In contrast, six countries, which include France, Russia, Argentina, South Africa, Turkey, and Indonesia, are associated with the neutrality hypothesis (NTH). While two countries (South Korea and Italy) follow the feedback hypothesis (FBH), only the US presents evidence of the uncertainty-leading hypothesis (ULH) in our sample of countries in the study. So, in the long run, for the majority (representing 53%) of the sample, changes in equity market returns predict changes in economic policy uncertainty. Therefore, contrary to a prior expectation, we did not find evidence supporting the uncertainty-leading hypothesis in the long run except in the US. The conventional wisdom following Pástor and Veronesi (Citation2012, Citation2013) exposition is that the expected value of stock returns should be negative at the announcement of government policy change. Intuitively, positive announcement returns tend to be small as investors mostly anticipate policy changes that cause stock price rises. Additionally, new policies can add extra uncertainty and increase the volatility of the stochastic discount factor, increasing risk premia.

In contrast with our results, Ongan and Gocer (Citation2017) find evidence of bidirectional causality. Wu et al. (Citation2016) argue that this theory does not hold in all contexts since countries are different. Most importantly, the empirical findings of Wu et al. (Citation2016) partly support our results in the case of India. Also, Saeed et al. (Citation2023) Granger causality test results confirm a unidirectional causality from stock prices to economic policy uncertainty in India. Like our results, Ulusoy (Citation2019) found strong evidence supporting the stock price leading hypothesis in most of their sample and explained that the forward-looking nature of stock prices may be a leading indicator of uncertainty. They further argued that as stock markets mature in developed and emerging countries, they can influence and even master the behaviour of market participants, including policymakers. Furthermore, in the long run, the equity or stock price leading hypothesis suggests that long-term movements in equity markets in these countries might influence future policy decisions. This outcome could be attributed to government interventions using stimulus policies to correct market downturns and restore investor confidence. Hong et al. (Citation2024) also find strong evidence in support of our findings in a time-varying context. They found strong evidence supporting the stock price leading hypothesis in most of their sample, while the uncertainty leading hypothesis was only supported in half of the sample. Contrary to our findings, Ulusoy (Citation2019) found strong evidence in support of the stock price leading hypothesis in the US, Canada, Sweden, South Korea, Brazil, India and Chile, while the EPU leading hypothesis and feedback hypothesis were detected only in Hongkong and Singapore, respectively. The neutrality hypothesis was associated with most countries, including Germany, the UK, Italy, Australia, Russia, Mexico, Spain, the Netherlands, and Ireland.

The bidirectional causality between DEPU and EMR in Italy and South Korea could imply that permanent changes in both EPU and EMR might influence each other. For example, a sustained market downturn could lead to heightened policy uncertainty, while high long-term EPU might deter investments, impacting future stock market returns. However, in the case of the US stock market, where the S&P 500 index returns are Granger caused by US EPU, it is consistent with conventional wisdom, as explained by Pástor and Veronesi (Citation2012, Citation2013). However, its relatively isolated nature suggests that the US might be the only case where long-term policy uncertainty directly impacts stock market returns. This result is surprising given the size and international influence of the US economy, making investors more sensitive to long-term policy changes in this market. At low frequency, the neutrality hypothesis evident in France, Russia, Argentina, South Africa, Turkey, and Indonesia implies that the equity markets and policy uncertainty might evolve independently over long-term horizons. However, earlier findings by Jiang et al. reveal a nonlinear interaction between EPU changes and US stock market fluctuations, with significant multifractality in cross-correlations influenced by major international events.

Turning to the transitional period, we uncover evidence supporting the uncertainty-leading hypothesis in France, Italy, and India. The causality between DEPU and equity market returns in the intermediate period confirms the equity-leading hypothesis in 7 out of 19 countries. These include Australia, Brazil, Canada, China, Germany, Mexico, and the EU. Evidence of the feedback hypothesis is documented in Japan, South Korea, and the US, whereas the neutrality hypothesis is revealed in India, Russia, the UK, and the US. The findings of reverse causality between domestic EPU and own EMR agree with Li et al. (Citation2016), who report bidirectional causality between policy uncertainty and the returns of the equity markets in China and India. Implying that heightened economic uncertainty will reduce stock returns just as elevated equity market uncertainty would amplify economic policy uncertainty. In the short run, it turns out that the majority (9 out of 19 countries) follow the equity-leading hypothesis, while the uncertainty hypothesis is confirmed only in Italy. In the short run, we uncover evidence supporting the feedback hypothesis in only France and India. In contrast, the neutrality hypothesis is reported in Argentina, China, Russia, South Africa, the EU, and the UK. These intermediate run results portray a persistence of some of the patterns we observed in the long run and some new dynamics. This trend underscores the importance of analysing causality across heterogeneous investment horizons.

Further diagnosis of the results reveals exciting patterns, for instance, except in Australia, Canada, Germany, Russia, Mexico, Brazil, Argentina, South Africa, and Turkey, where the causal relations between domestic policy uncertainty and the returns of the domestic equity markets are homogeneous across frequencies, for the remaining countries, majority of them exhibit varying causal relations. Countries that show the most varying causal nexus between DEPU and EMR across all periods are France, India, and the US. In France, for instance, we find evidence supporting the neutrality hypothesis in the long run, the uncertainty-leading hypothesis in the medium term, and the bidirectional causality or feedback hypothesis in the short run. In the case of India, evidence exists in support of the neutrality hypothesis in the long run, the uncertainty-leading hypothesis in the intermediate period, and the feedback hypothesis in the short run. In the US, we report a unidirectional causality from uncertainty to equity market returns in the long run, bidirectional causality in the intermediate period, and unidirectional causality from equity market returns to changes in domestic policy uncertainty in the short run. For China, we document an equity-leading hypothesis in the long and intermediate terms but a neutrality hypothesis in the short run. The equity-leading hypothesis is upheld in the UK in the long run, but the neutrality hypothesis in the intermediate and short runs. South Korea follows the feedback hypothesis in the long and intermediate periods but is the equity-leading hypothesis in the short run. The EU records the equity-leading hypothesis in the long and intermediate periods but the neutrality hypothesis in the short run. Finally, Indonesia shows evidence of the neutrality hypothesis in the long and intermediate terms but the equity-leading hypothesis in the short run.

Similarly, Japan supports the equity-leading hypothesis in the lower and higher frequency but not the medium frequency. In Italy, the uncertainty-leading hypothesis prevails in the intermediate and short run, but the feedback hypothesis is in the long run. Japan documents the equity-led hypothesis in the long and short runs but not in the intermediate run. Previous studies support these results. For example, Albrecht et al. (Citation2023) show that the EPU index is a leading indicator of stock return drops at short-term investment horizons. However, at the same time, stock returns affect this uncertainty on long investment horizons in the US, Japan and Germany. The lack of consistency regarding the causal relationship between economic policy uncertainty originating from domestic sources and the returns of the domestic equity markets in most (52.6%) of our samples implies that the causal relationship is sensitive to changes in the investment horizon. These results vindicate our argument that in the presence of nonlinearity, using linear models to examine the causality between these variables could be misleading and, as the evidence shows, may not reveal the true relationship. The possible explanation for the sensitivity of our causal results across frequencies can be attributed to factors, including time-varying market dynamics, investor behaviour and market psychology, and differences in underlying economic structures and policy frameworks. First, equity markets react strongly to unexpected news and events in the short run. Equity market fluctuations in the short run may elicit domestic policy responses to stabilise the markets. Conversely, short-term policy adjustments could quickly impact market sentiment (EMR). The intermediate period may combine the influence of short-term reactions with long-term considerations. Policymakers may examine the persistence of market volatility before implementing more substantial policy changes. Also, agents may consider the likely long-term implications of policy decisions when reacting to current events.

Regarding investor behaviour and market psychology explanation, investors tend to be more risk-averse in the short term, making them overreact to bad news or policy uncertainty, resulting in rapid changes in EMR. This behaviour might have accounted for the dominance of equity or stock price leading hypothesis in our results in the short run. However, long-term investors making investment decisions based on economic fundamentals tend to be less reactive to short-term policy uncertainty. Therefore, their investment decisions tend to be primarily driven by long-term economic prospects and policy stability, which might have led to the Granger causality running from EMR to DEPU in some countries (Wang & Wang, Citation2019). Finally, differences in underlying economic structures and policy frameworks could explain the sensitivity of our results across frequencies. For example, differences in institutional frameworks, monetary policy regimes, and fiscal flexibility might result in heterogeneity in the effectiveness and speed of monetary policy transmission mechanisms across G20 countries. This diversity could explain the varied causal outcomes across frequencies. Additionally, the maturity of the markets also played a role. Developed economies with more mature financial markets might react differently to policy uncertainty than emerging economies.

The findings support the equity-leading hypothesis regardless of frequency. However, these results are not surprising, as Antonakakis et al. (Citation2013) posit that changes in stock returns can influence economic policy uncertainty, as policymakers sometimes have to change policies in response to heightened stock market uncertainty. As a result, the more volatile the stock markets, the more uncertain economic policies are expected. Moreover, our results collaborate with Ajmi et al. (Citation2015), who document a unidirectional causality from equity market uncertainty to EPU in the US. However, this result contradicts the prediction that stock prices fall at the announcement of government policy change (Pástor & Veronesi, Citation2012, Citation2013).

Next, and Appendix B show the causal results between International (US) economic policy uncertainty and each country’s equity market returns, while shows the hypotheses in terms of causality outcome. We did not examine the US case since it is used to proxy international economic policy uncertainty. Besides, in Germany and Brazil, where the equity leading hypothesis is maintained through all frequencies, all other countries exhibit time-varying causal relations between International (US) EPU and EMR. Japan follows the feedback hypothesis at a lower frequency (ω = 0.5), the equity-leading hypothesis at a medium frequency (ω = 1.5), and the neutrality hypothesis at a higher frequency (ω = 2.5). Australia, Canada, and India follow the uncertainty-leading hypothesis in the long run and the neutrality hypothesis in the short run. However, Australia and India found evidence supporting the neutrality hypothesis in the intermediate period, but Canada followed the equity-led hypothesis.

Table 3. Causal nexus between international (US) economic policy uncertainty and equity market returns.

The results reveal that in the short-run, US EPU Granger caused EMR in China, France, Italy, Russia, and the UK. The Stock price or equity leading hypothesis is found in Germany, Mexico, Brazil, and Turkey. The neutrality hypothesis is supported in Australia, Canada, India, Japan, South Korea, Argentina, the European Union (EU), South Africa, and Indonesia. However, no evidence of bidirectional causality was detected. The findings of the US EPU leading hypothesis, in the short-run, as supported in China, France, Italy, Russia, and the UK, imply that high-frequency fluctuations in US economic policy uncertainty can influence stock prices in these countries. This phenomenon, on the one hand, could be attributed to global risk spillover. Changes in US policy might create a ripple effect of uncertainty impacting global risk appetite and leading to capital outflows from emerging markets.

On the other hand, bad news about US policy uncertainty could cause risk aversion among international investors, leading them to sell assets in other markets, including G20 economies. The findings of Alqahtani and Taillard (Citation2019) support our results in the case of Qatar. They revealed that changes in US policy uncertainty affect Qatar’s stock market returns. Moreover, Colombo (Citation2013) revealed that the US EPU predicted European industrial production in the case of European countries relatively more than their domestic policy shocks. Therefore, we can extend the results of Colombo (Citation2013) to the stock market in the context of European countries. In the context of China, the heavy interlinkages between the Chinese and the US economy through capital flows, as noted by Lastauskas and Minh (Citation2021), make it possible for shocks to spill over between them. Specifically, the authors find that Chinese output growth is significantly more vulnerable to sudden changes in US interest rates if the shocks are transmitted through financial linkages. Interestingly, the US dollar’s status as a reserve currency and China’s massive reserve accumulation naturally make the two economies strongly interlinked. Given this solid financial connection between the two largest economies, it is unsurprising that policy uncertainty shock from the US will impact the Chinese equity market returns.

The equity-leading hypothesis revealed in Germany, Mexico, Brazil, and Turkey suggests that short-term movements in these G20 equity markets might precede changes in the US policy. This finding could be explained by market contagion and policy signalling. First, a sudden fall in G20 stock markets may raise concerns about global financial stability, triggering US authorities to respond and restore investor confidence. Strong positive performance in some G20 markets might signal robust global economic prospects, potentially influencing US policy decisions. Finally, the neutrality hypothesis was reported in Australia, Canada, India, Japan, South Korea, Argentina, the European Union (EU), South Africa, and Indonesia. This finding indicates that the equity markets of these countries might be less reactive to short-run US policy uncertainty due to strong domestic fundamentals or limited financial integration.

The intermediate run confirmed the US EPU leading hypothesis in Italy, Russia, and the UK. The equity or stock price leading hypothesis was supported in Canada, Germany, Japan, Argentina, Brazil, South Africa, Turkey, and Indonesia; Neutrality hypothesis was found in Australia, China, India, South Korea, and the EU, while evidence of bidirectional causality was reported in France and Mexico. The results show some continuation of the short-run dynamics, suggesting that the impact of US EPU and G20 EMR might persist for a moderate period. The bidirectional causality uncovered in France and Mexico indicates that changes in US EPU and subsequent market reactions in these countries might influence each other over a slightly longer time horizon.

Finally, in the long run, Granger causality from US EPU to EMR is only reported in France. The equity or stock price leading hypothesis is supported in Australia, Canada, Germany, India, Mexico, Russia, Argentina, Brazil, the EU, South Africa, Turkey, and Indonesia. The neutrality hypothesis is only detected in China, while the bidirectional causal effect is detected in Italy, Japan, South Korea, and the UK. Only France exhibits long-run causality from US EPU to its own EMR. This could be explained by France’s deeper economic ties with the US. The dominant stock price leading hypothesis detected in this time horizon indicates that most G20 economies show long-run causality running from their own equity markets to US EPU. This finding suggests that long-term trends in these markets might influence future US policy decisions. This outcome could be explained by the importance of G20 countries in the world economy and investor behaviour. Focusing on explaining the importance of the G20 in the global market, the performance of major G20 economies can significantly impact global economic growth prospects, possibly influencing long-term US policy decisions.

Moreover, long-term sustained market downturns in G20 economies might pressure US policymakers to implement measures to promote global economic stability. The feedback hypothesis revealed that Italy, Japan, South Korea, and the UK exhibit long-term feedback loops. It indicates that long-term changes in US EPU and long-term trends in their equity markets might influence each other. The neutrality hypothesis reported only in China could imply that China’s long-run relationship between US EPU and EMR remains neutral. This finding could be due to China’s large domestic market and limited future economic dependence on the US. Indeed, Bekkers et al. (Citation2021) revealed more profound structural changes projected to occur in the Chinese economy over the next two decades. These changes, among others, include the shift to focus on the domestic economy, implying raising the consumption share in GDP and a move to reduce the China-US bilateral trade surplus to nearly zero. These changes suggest a limited economic interdependence between the two largest economies in the future.

Comparing the results of the causal nexus between domestic EPU and EMR on the one hand and International (US) economic policy uncertainty and equity market returns on the other, as contained in and , we observe that in the long run, out of 19 countries, we find evidence of domestic uncertainty explaining domestic equity returns only in the US. Similarly, out of 18 countries, only France shows that international uncertainty predicts domestic equity returns. Turning to the intermediate period, France, India, and Italy have evidence supporting the domestic uncertainty Granger causing domestic equity returns, while Italy, Russia, and the UK show that international uncertainty Granger causes domestic stock market returns. In the short run, whereas only Italy supports the domestic uncertainty Granger causes stock returns hypothesis, as many as five countries, including China, France, Italy, Russia, and the UK, supported the international uncertainty Granger causes domestic stock market returns hypothesis.

Based on the findings, we document that we did not find enough evidence to identify which source of uncertainty is essential in predicting changes in the returns of equity markets in the cross-section of countries in the long run and intermediate period. However, in the short term, the uncertainty of US economic policy dominates in explaining the returns of the domestic stock market. This result could be due to the high integration of these markets with the international (US) capital markets. These results are not surprising because voluminous literature (Bloom, Citation2017; Das & Kumar, Citation2018; Ko & Lee, Citation2015; Lastauskas & Minh, Citation2021) indicates that when markets are integrated, shocks to one market can have spillover effects on the others. Moreover, asset pricing models explain that integrated markets react strongly to global happenings relative to local factors and vice versa (Alagidede, Citation2009; Brogaard & Detzel, Citation2015; Hong et al., Citation2024).

5. Policy implications of the findings

Based on the results of the empirical analysis, we highlight the causal relationships between US Economic Policy Uncertainty (US EPU) and Equity Market Returns (EMR) across G20 economies in different time horizons. The findings hold significant policy implications, especially for policymakers and investors in the US and other G20 economies.

On the causal relations between domestic uncertainty and domestic equity market returns, we can infer that irrespective of the frequency, we find more evidence supporting equity market returns Granger causing domestic policy uncertainty, thus confirming the equity-leading hypothesis. The implication is that frequent changes in domestic stock market returns could trigger changes in domestic policy uncertainty. This outcome is possible if equity market returns become highly volatile, triggering policymakers to intervene frequently by changing policy, resulting in elevated policy uncertainty. For instance, Smaniotto and Zani (Citation2020) noted that Brazil, France, Italy, Japan, South Korea, and Mexico implemented circuit breakers on the daily price movements in their respective markets to dampen market volatility. Since governments shape the environment through their policy actions, sudden policy changes can increase policy uncertainty (Pástor & Veronesi, Citation2012).

However, these results are far from surprising as Antonakakis et al. (Citation2013) had earlier posited that stock market volatility contributes to increasing domestic policy uncertainty, as policymakers sometimes must adjust policies in reaction to elevated stock market volatility. Moreover, Ulusoy (Citation2019) found similar evidence supporting the stock price leading hypothesis in most of their sample and explains that the forward-looking nature of stock prices may act as a leading indicator of uncertainty. They further argued that as stock markets mature in developed and emerging countries, they can influence and even master the behaviour of market participants, including policymakers. Furthermore, in the long run, the equity or stock price leading hypothesis suggests that long-term movements in equity markets in these countries might influence future policy decisions. These results imply that agents’ behaviour elicits appropriate and timely policy action to avoid further uncertainty. However, with only a few exceptions, our results contradicted the long-held view that stock prices fall at the announcement of government policy change (Pástor & Veronesi, Citation2012, Citation2013). Specifically, our results support the predictions of Pástor and Veronesi (Citation2012, Citation2013) in the case of the US in the long run, Italy in the short and intermediate period, and India and France in the intermediate term. However, in most G20 markets, our findings disagreed with theirs. Therefore, like Wu et al. (Citation2016), this argument is not always supported since countries differ regarding market maturity, underlying market structures and policy frameworks, Investor behaviour, institutional structures, and information asymmetry.

Also, we document a modicum of evidence on bidirectional causality between domestic economic policy uncertainty and domestic stock market returns at different frequencies. For instance, we find this evidence in Italy and Korea in the long run. In addition, we document this in the intermediate period and short-run in Japan, South Korea, the US, France and India, respectively. This result means heightened policy uncertainty will reduce stock returns just as stock market uncertainty will amplify EPU.

These findings hold significant policy implications: Firstly, in the short run, the dominant short-term EMR to DEPU causality suggests that policymakers in many G20 economies, especially in the case of Australia, Canada, Germany, Japan, South Korea, Mexico, the US, Brazil, and Indonesia, might already be actively intervening in markets during periods of volatility. Indeed, Smaniotto and Zani (Citation2020) noted that Brazil, France, Italy, Japan, South Korea, and Mexico implemented circuit breakers on the daily price movements in their respective markets. These interventions can be further evaluated for effectiveness and potential unintended consequences. However, Italy’s unique pattern of short-term DEPU impacting EMR calls for more targeted policy adjustments to minimise adverse market reactions to policy uncertainty. Finally, economies with short-term bidirectional causality, particularly in the case of France and India, can benefit from improved coordination between policymakers and market regulators to create a more predictable and stable environment.

Secondly, in the long run, we suggest that in countries where long-term equity market performance influences future policy decisions, as in the case of Australia, Canada, China, Germany, India, Japan, Mexico, the UK, Brazil, and the EU, policymakers can benefit from focusing on long-term economic growth strategies that promote investor confidence and market stability. Also, the US finding of DEPU impacting long-term EMR highlights the importance of clear and consistent communication of policy decisions to mitigate uncertainty and maintain market stability. Moreover, countries where our results have revealed bidirectional causality, which include Italy and South Korea, require a more holistic approach. Policymakers should address the root causes of policy uncertainty while simultaneously implementing measures to stabilise markets during periods of high uncertainty.

Turning to whether changes in international uncertainty can predict returns on the domestic equity market and vice versa, we find more support for the equity-leading hypothesis (ELH) in the long and intermediate runs and the neutrality hypothesis in the short run. This finding implies that the causal relationship between changes in international (US) uncertainty and returns on the domestic stock market is sensitive to heterogeneous investment decisions and policy uncertainty across horizons. Given these findings, we posit that the causal relationship between international uncertainty and the performance of equity markets is not as straightforward as was earlier conceived by previous literature (Albrecht et al., Citation2023; Alqahtani & Taillard, Citation2019; Hashmi et al., Citation2021; Kannadhasan & Das, Citation2020). Albrecht et al. (Citation2023) find that the EPU index lags stock markets during global financial turmoil, particularly in the US, Japan, and Germany, with short-term effects also confirmed. Kannadhasan and Das (Citation2020) revealed that EPU holds a consistent negative relationship across all quantiles. Therefore, for policy purposes, we advocate that policymakers, especially capital market regulators, should develop strategies tailored to their economies’ specific time horizon of the DEPU-EMR relationship while crafting policy to address the adverse effects of external uncertainty shocks on the equity markets because, as noted earlier, short-term and long-term changes in uncertainty may have an entirely different impact on the equity market performance of a country (Wang & Wang, Citation2019).

Based on the findings, we did not find enough evidence to identify which source of uncertainty is more important in explaining changes in domestic stock market returns in the cross-section of countries in our sample in the long run and intermediate period. However, in the short run (about 2.5 months), changes in the US economic policy uncertainty appear dominant in explaining changes in the returns of domestic equity markets, especially in countries such as China, France, Italy, Russia, and the UK. We attribute this outcome to the high integration of these markets with the international (US) capital markets. Extant literature (Ben Amar & Carlotti, Citation2021; Hashmi et al., Citation2021; Ko & Lee, Citation2015; Lastauskas & Minh, Citation2021; Tiwari et al., Citation2019: Al Nasser & Hajilee, Citation2016) indicates that when markets are integrated, shocks to one market can spillover to the others. For example, Al Nasser and Hajilee (Citation2016) find evidence of stock market integration between emerging (Brazil, China, Mexico, Russia and Turkey) and developed (US, UK, and Germany) markets, finding short-run integration of all emerging and developed markets. However, significant long-run integration of all emerging market returns is only possible with Germany. The practical implications for the international investor community are that investment in assets within the long and intermediate investment horizons (within 4.5 months to 1 year) would be insulated from changes in external shocks. However, investments in assets with a short investment horizon (about 2.5 months or less) would be susceptible to changes in US uncertainty shocks. Having said this, investors in Italy, Russia, and the UK, on the one hand, and France, on the other hand, should be mindful of equity market investment within the intermediate and long horizons, respectively, as their assets would also be affected by changes in external uncertainty shocks, especially from the US. Based on these results, we offer further policy recommendations for US policymakers and the G20 forum to consider.

On the one hand, the US policymakers should consider the following policy suggestions: First, the short-run impact of US EPU on some G20 equity markets, such as China, France, Italy, Russia, and the UK, suggests careful consideration of the potential global ramifications of policy decisions. Therefore, policymakers should strive for clear communication and transparency to minimise unintended consequences for international financial stability. Secondly, the limited evidence for long-run causality from US EPU to G20 EMR suggests that long-term US policy decisions might be more influenced by domestic factors and global economic trends rather than solely by short-term market fluctuations in other G20 economies. However, policymakers should remain mindful of the potential long-term impact of their policies on global economic stability, particularly regarding the performance of major G20 economies.

On the other hand, policymakers at the G20 forum should consider the following policy prescriptions: First, Economies where US EPU Granger causes short-term EMR fluctuations, including China, France, Italy, Russia, and the UK, might benefit from developing contingency plans or implementing measures to mitigate the impact of US policy uncertainty on their domestic markets. This strategy could involve strengthening domestic financial institutions, promoting foreign direct investment, or diversifying trade relationships. Secondly, the dominant long-run causality from G20 EMR to US EPU suggests that strong domestic economic policies and a focus on long-term growth prospects can influence US policy decisions. G20 economies should prioritise policies that promote financial stability, attract foreign investment, and foster a robust and competitive business environment. Finally, policymakers should promote international cooperation. The interconnected financial markets highlighted by our research underscores the importance of international cooperation among G20 economies. Collaborative efforts to manage policy uncertainty, promote financial stability, and foster global economic growth can benefit all G20 members.

6. Concluding remarks

We examine the causal relations between domestic and international (US) economic policy uncertainty (EPU) and equity markets of 19 G20 countries. Employing the frequency-domain causality test, with monthly data spanning January 1997 to June 2021, provides valuable insights into the complex relationship between US EPU and EMR across G20 economies in different time horizons. First, the findings support the equity-leading hypothesis regardless of the investment horizon, suggesting that frequent interventions by policymakers to dampen market volatility during periods of high policy uncertainty may exacerbate the uncertainty. This finding challenged the position that stock prices fall at the announcement of government policy change. While we find limited evidence supporting this prediction, we argue that this position is not always supported since countries differ regarding market maturity, underlying market structures and policy frameworks, investor behaviour and preferences, institutional structures, and information asymmetry. Second, the results show that the causality between policy uncertainty (whether domestic or international) and equity returns is sensitive to heterogeneous investment decisions and policy uncertainty across horizons in most of our sample. We attributed the sensitivity of the results across frequency to factors, including time-varying market dynamics, investor behaviour and market psychology, and differences in underlying economic structures and policy frameworks. For example, investors tend to be more risk-averse in the short term, making them overreact to bad news or policy uncertainty, resulting in rapid changes in EMR. This behaviour might have accounted for the dominance of equity or stock price leading hypothesis in our results in the short run. However, long-term investors making investment decisions based on economic fundamentals tend to be less reactive to short-term policy uncertainty. Therefore, long-term economic prospects and policy stability influence their investment decisions, which might have led to some countries’ Granger causality from EMR to DEPU. Finally, International (US) policy uncertainty has a domineering causal effect in predicting domestic equity returns relative to domestic policy uncertainty in the short run (about 2.5 months). Therefore, the varying results across frequencies are consistent with the prediction of the fractal market hypothesis.

Therefore, capital market regulators should develop strategies tailored to the specific time horizon of the DEPU-EMR or US EPU-EMR relationship in their economies since short-term and long-term changes in uncertainty may have an entirely different impact on the equity market performance of a country and thus should be regulated differently. Moreover, policymakers should ensure clear and consistent communication of policy decisions, even during uncertain times, to help manage investor expectations and maintain market stability. Given the potential spillover effects of EPU, international cooperation among G20 economies in managing policy uncertainty and promoting financial stability is crucial. Most importantly, investors should stay informed about global economic and political developments, particularly policy changes in the US. Monitor economic indicators like trade data, inflation rates, and consumer sentiment to assess potential shifts in US policy uncertainty. Diversify their portfolio across different G20 economies, asset classes, and sectors to mitigate risks associated with US policy uncertainty. Consider including assets with a low correlation to US markets, such as emerging market bonds or real estate.