ABSTRACT

Higher education in countries like Ghana faces significant challenges, including financial barriers, which usually hinder students’ educational progress and graduation rates. While some students usually rely on family support and personal savings, these resources are generally insufficient for covering all educational expenses. Although student loans have emerged as a beacon of hope to address these challenges, research on this topic, particularly in developing countries, has remained underexplored. This study, grounded in the Theory of Planned Behaviour, investigates the psychological factors influencing Ghanaian students’ decisions to utilize student loans and the impact on graduation rates. Data is gathered from 114 Ghanaian students using a purposive sampling technique. The analysis reveals a positive correlation between favourable attitudes toward student loans and intentions to use them. Subjective norms significantly influence loan decisions, while perceived behavioural control has no significant impact. Also, loan decisions positively correlate with graduation rates, suggesting loans can enhance academic persistence. These findings highlight the need for responsible loan programs to improve graduation outcomes and socioeconomic development.

1. Introduction

College graduation stands as a pinnacle achievement for students globally as it reflects years of dedication and growth (Fomunyam Citation2022). However, achieving this milestone is often hindered by obstacles such as financial barriers and strike actions, particularly in regions like Ghana (Hagedorn, Wattick, and Olfert Citation2022; Niyi Jacob, Elizabeth, and Ndubuisi Citation2020). These challenges underscore the importance of exploring various funding options available to students. While family support, grants, scholarships, and personal savings provide some relief, they often fall short of covering the substantial costs associated with tertiary education (Elmira and Suryadarma Citation2020; Herbaut and Geven Citation2020; Stoddard and Urban Citation2020). Consequently, many students find themselves disappointed when they realize that fully sponsored scholarship opportunities are scarce (Zacharias and Ryan Citation2021). In addressing the issue of financing higher education, student loans have emerged as a promising solution, offering students the means to pursue their academic ambitions without immediate financial burden (Card and Solis Citation2022; Froidevaux et al. Citation2020). According to Froidevaux et al.(Citation2020), by providing access to funds that can cover tuition fees, living expenses, and other educational costs, student loans alleviate the financial stress associated with higher education, enabling students to focus on their studies and ultimately enhance their prospects of graduation. Notwithstanding its potential benefits, the drivers of student loans in developing countries have attracted less attention.

The Theory of Planned Behaviour (TPB) offers a valuable framework for understanding how individual attitudes, subjective norms, and perceived behavioral control collectively shape behavioral intentions, particularly in the context of educational financing choices(Shih et al. Citation2022; Su et al. Citation2021). Theoretically, the TPB suggests that positive attitudes toward the value of education can significantly influence an individual's inclination to consider student loans as a feasible means to fund their studies (Sims et al. Citation2020). Building on this, societal and familial expectations, or subjective norms, further contribute by either encouraging or dissuading individuals from taking on student loans, depending on the perceived social acceptability of incurring educational debt (Gubik Citation2021). Lastly, perceived behavioral control, which encompasses an individual’s assessment of their financial literacy and future employment prospects, plays a crucial role in determining their confidence in managing student loans effectively (Cloutier and Roy Citation2020). Collectively, these factors may interact to shape the intention to acquire student loans, reflecting the complex interplay between personal beliefs, social influences, and perceived ability to manage debt.

Despite the significance of these psychological determinants, existing literature often overlooks their interrelated role in shaping students’ decisions regarding student loans. Existing research has either studied the psychological factors that influence students’ graduation (Kee Citation2021; Mekonen et al. Citation2021; Raza, Qazi, and Yousufi Citation2021), or the psychological effects on students loan dynamics (Abraham et al. Citation2020; Xiao and Kim Citation2022). Despite the wealth of research on psychological factors impacting graduation rates and the psychological effects on student loan dynamics, there remains a conspicuous absence of studies that integrate all components of the TPB to investigate their effects on students’ loan decisions comprehensively. This gap represents a significant lacuna in our understanding as existing research has provided only partial insights into the factors driving students’ borrowing behaviors and repayment patterns. Closing this gap is crucial because it enables policymakers and educational institutions to effectively tailor interventions, provides insights into alleviating student debt burden, and contributes to advancing theoretical knowledge in behavioral economics and psychology by elucidating financial decision-making mechanisms among students. This study, therefore, addresses the identified gap by investigating how attitudes, norms, and perceived behavior control influence Ghanaian students’ loan decisions and how it ultimately influences graduation rates.

The contribution of the study is as follows: First, the study extends the TPB application in education literature (Sarosa Citation2022; Shih et al. Citation2022; Su et al. Citation2021) by, for the first time, investigating how individual attitudes, subjective norms, and perceived behavioral control potentially influence educational financing choices. Secondly, elucidating the link between student loan utilization and graduation rates can provide valuable insights into the effectiveness of student loan programs in fostering academic persistence and attainment and will contribute to the literature on education outcomes (Barbera et al. Citation2020; Pike and Robbins Citation2020). Finally, bridging the gap in knowledge regarding students’ attitudes, subjective norms, and their impact on student loan decisions and graduation rates holds immense significance for fostering educational advancement and socio-economic development within the Ghanaian context and advances the discussion in the literature (Addo and Adusei Citation2021; Bondzi–Simpson and Agomor Citation2021).

2. Literature review and theoretical framework

2.1. Theoretical perspective on the theory of planned behavior

The Theory of Planned Behavior is one of the most influential and popular conceptual frameworks for the study of human action (Shih et al. Citation2022; Su et al. Citation2021). The theory states that an individual's behavioral intentions, which can determine their actual behaviors, depend on three conceptually independent factors: their attitude toward the behavior, subjective norms, and perceived behavioral control. According to the TPB, favorable attitudes and subjective norms, and greater perceived control lead to increased behavioral intention and likelihood of actual behavioral performance (Ramus and Nielsen Citation2005)

The TPB has been applied to understand intentions and behaviors across a wide variety of contexts, including health, sustainability, technology use, education, and consumer choice domains (Abou Kamar et al. Citation2024; Kamble, Gunasekaran, and Arha Citation2019; Ulker-Demirel and Ciftci Citation2020). In an educational context, the TPB provides a framework for examining students’ decision-making processes regarding important choices that can impact their educational trajectories and outcomes. These choices include taking out student loans, which enable enrollment and persistence for students who could otherwise not afford higher education.

Students’ attitudes towards debt influence the decision of whether to utilize student loans, their perceptions of whether parents or peers believe they should or should not take loans, and whether they feel capable of taking on and eventually repaying debt. These factors can determine behavioral intentions regarding taking out loans, which in turn shape actual loan uptake. According to Black et al. (Citation2023), student loan debt enables persistence and degree completion by providing financial resources to students who have economic disadvantages. Therefore, the TPB presents a relevant framework for examining how psychosocial factors shape the decision to assume debt, which consequently impacts graduation outcomes.

2.2. Hypotheses development on TPB factors influencing student loan decisions

Students’ attitudes toward taking out loans to finance their education are likely to play an influential role in their decision-making process. According to the TPB, the more favorable the attitudes toward a behavior, the stronger an individual’s intention to perform it. Research indicates mixed findings regarding students’ attitudes about debt. While some studies suggest students have negative views of debt (Dickson, Mulligan, and DeVahl Citation2020; Froidevaux et al. Citation2020; Lea Citation2021), other research has found neutral attitudes or acceptance towards loans as necessary to expand educational opportunities (Black et al. Citation2023; Harper et al. Citation2021; Mezza et al. Citation2020). Contextual factors related to national and campus culture surrounding debt may shape attitudes. Given that loans enable persistence and degree completion for financially constrained students (Harper et al. Citation2021), it is expected that students who believe financing education through debt is normal and provides opportunity will hold positive attitudes toward loans. On the other hand, students who view debt as something to be avoided may hold negative attitudes. Furthermore, students who are confident in their ability to handle loans and eventually achieve returns on investment in their education will likely hold favorable attitudes.

Perceived behavioral control refers to individuals’ perceptions of their ability to perform a behavior, including the ease or challenge of actual performance. It is shaped by past experience, obstacles, and resources available to facilitate the behavior (Cloutier and Roy Citation2020). Research (Sung et al. Citation2021; Ullah Citation2020) shows that perceived behavioral control influences intentions, which shape actions. Students may feel they have control over loan uptake if they perceive themselves as competent in processes like filling out applications correctly, comparing favorable options, and budgeting finances. In contrast, perceiving the processes as confusing or the capability for repayment as uncertain could inhibit feeling in control. Having access to informational, family, or institutional resources to guide loan decisions enhances control. As found across behaviors, perceived behavioral control is expected to shape loan intentions.

Subjective norms refer to perceived social pressures to engage or not engage in a behavior (Gubik Citation2021; Raut Citation2020). The expectations and behaviors of important referent individuals such as parents, other family members, friends, teachers, or respected peers can shape perceived norms. Research evidence suggests subjective norms are an important influence on student loan decision-making. For example, young adults’ perceptions of parental norms about the riskiness of debt are associated with loan aversion (Furuta Citation2021). Additionally, first-generation students who lack guidance from parents experienced in higher education financing face challenges navigating loan decisions (Ricks and Warren Citation2021), given the evidence that social expectations and pressures from significant others can shape student loan decisions.

In conclusion, the hypotheses state:

H1: Students’ attitudes toward utilizing loans to finance education will positively predict their intentions to take out student loans.

H2: Students with higher perceived behavioral control related to taking out and managing loans will have greater intentions to utilize loans to finance their education.

H3: Subjective norms concerning the utilization of student loans will positively predict students’ intentions to take out education loans.

2.3. Student loans and graduation rates

Taking out student loans enables enrollment, persistence and completion of college degrees for students who could otherwise not afford tuition and expenses or would struggle financially (Barbera et al. Citation2020; Pike and Robbins Citation2020). Debt invested in human capital is expected to eventually yield individual and societal returns. Students without sufficient financial means must make strategic decisions about using loans to not merely access college but persist through graduation. Research on debt influences shows moderate loans positively impact retention and graduation, while excessive loans or credit constraints negatively impact persistence and completion rates (Chen and Bahr Citation2021; Hu and Ortagus Citation2023). Debt levels must be managed to enable opportunity while avoiding unaffordable repayment burdens (Brooks and Levitin Citation2020). Moderate loans allow students time for coursework instead of extensive paid employment and relieve financial stress. Small to mid-range loans also deter college dropouts more than grants alone by motivating degree completion to gain means to repay. The following therefore, is hypothesized:

Hypothesis 4: Utilization of student loans will positively predict students’ likelihood of graduating college.

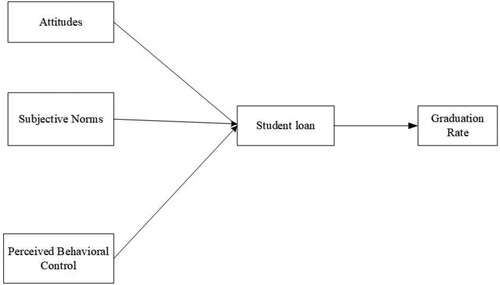

Figure 1. Conceptual framework.

3. Methodology

3.1. Research design and approach

A cross-sectional survey research design is employed in the present study. Cross-sectional survey designs are suitable when the aim is to collect data from a sample of participants at a specific point in time to describe their attitudes, beliefs, or behaviors(Ampofo et al. Citation2023). In this study, data is gathered from Ghanaian students through a structured questionnaire to examine their attitudes, norms, perceived behavioral control, and intentions regarding student loan decisions. The cross-sectional survey design is appropriate for the present study as it allows for the quantitative examination of relationships between variables derived from the Theory of Planned Behavior and student loan decisions (Tuffour et al. Citation2023). Additionally, this design is useful when the research objectives involve describing the characteristics of a population, in this case, Ghanaian students, and making inferences about their behaviors related to student loan uptake and graduation rates (Agyabeng-Mensah et al. Citation2022). Furthermore, cross-sectional surveys are efficient in terms of time and cost, making them suitable for studies with limited resources (Spector Citation2019).

3.2. Sampling

To explore the influence of attitudes, subjective norms, and perceived behavioral control on student loan decisions, this study focused on students from the University of Ghana (UG) and Kwame Nkrumah University of Science and Technology (KNUST). According to Atuahene (Citation2013), these universities are known for their diverse student populations and active engagement in issues related to student loans; hence ideal for a study of this nature. Following Guarte and Barrios (Citation2006), a purposive sampling technique is employed to ensure that the selected respondents have relevant experience in student loans and can provide insightful data relevant to our investigation. A total of 120 respondents are initially targeted based on their known history of engaging with student loan schemes.

3.3. Survey instrument and data gathering

To systematically gather this data, we developed a structured questionnaire specifically designed to probe into the various components of the Theory of Planned Behavior, ensuring a direct link between our methodological approach and the theoretical underpinnings of our study. A structured questionnaire is developed based on five(5) variables derived from the Theory of Planned Behavior (attitudes, norms, perceived behavioral control, and intentions), student loan, and graduation, as indicated in . The construct items are measured on a five-point Likert scale with ‘1 = strongly disagree to 5 = strongly agree.

The questionnaire is validated by experts in the field and revised accordingly before administration. An online platform is utilized to administer the questionnaire, ensuring anonymity and confidentiality for the participants (Regmi et al. Citation2017). Participants are invited to complete the questionnaire through personalized email invitations, which include a brief explanation of the study's purpose and a link to access the online platform.

To encourage participation and allow sufficient time for thoughtful responses, reminders are sent bi-weekly over a period of one month (Saleh and Bista Citation2017). The online platform remains active throughout the data collection phase, enabling participants to complete the questionnaire at their convenience within the specified timeframe. This approach ensures a standardized data collection process and facilitates replicability of the study in similar contexts (Creswell and Creswell Citation2018). During the data collection phase, discrepancies and incomplete responses resulted in the exclusion of data from 6 participants. As a result, the final sample size comprised 114 respondents. This adjusted sample size provides a strong basis for analysis, ensuring that the data remains representative and sufficiently robust to draw valid conclusions about the influence of psychological and social factors on students’ loan-related decisions in the Ghanaian context.

3.4. Data analysis

Following the steps employed by Tuffour et al. (Citation2023), this study employs the Partial Least Squares Structural Equation Modeling (PLS-SEM) approach using SmartPLS version 4 to analyze the data collected. PLS-SEM is well-suited for this study due to its ability to model complex relationships, its exploratory theory-building capabilities, its flexibility with small sample sizes, and its alignment with the purposive sampling approach taken. Again, the analysis follows a two-step process recommended for PLS-SEM (Hair et al. Citation2017), where the measurement model is first evaluated for reliability and validity through metrics such as outer loadings, internal consistency, and discriminant validity assessments and second, the structural model's path coefficients are examined to test the hypothesized relationships derived from the TPB.

Outer loading, which measures the strength of relationships between indicators and latent constructs, is assessed, with a desirable threshold typically set at 0.7 or above (Ampofo et al. Citation2023). Variance Inflation Factor (VIF) is employed to detect multicollinearity, with an ideal threshold below 5. Additionally, Cronbach’s Alpha, rho_A, Composite Reliability, and Average Variance Extracted (AVE) will be computed to assess internal consistency and convergent validity. A Cronbach's Alpha and rho_A value exceeding 0.7, Composite Reliability above 0.7, and AVE higher than 0.5 are generally considered acceptable thresholds indicative of reliability and validity in the context of our analysis. These rigorous reliability tests ensure the accuracy and robustness of our findings, providing confidence in the conclusions drawn from the data.

4. Results

4.1. Descriptive statistics

presents the descriptive statistics and provides an overview of the demographic characteristics of the study participants. It reveals a total sample size of 114 individuals, consisting of 67 males (59.8%) and 45 females (40.2%). Regarding age distribution, the majority of participants fell within the 21–25 age range, accounting for 54.4% of the sample, followed by those aged 15-20, comprising 27.2%. A smaller proportion of participants were aged 26–30 (17.5%), while individuals aged 31–35 constituted a negligible percentage (.9%). Overall, the data reflects a diverse representation of gender and age groups among Ghanaian students, which is essential for understanding the nuanced influences of attitudes, norms, and perceived behavior control on loan decisions and subsequent graduation rates.

Table 1. Gender and age range of respondents.

shows the reliability test results and demonstrates robustness across various measures for the latent constructs under investigation. Outer loadings, indicative of the strength of relationships between indicators and latent variables, showcase high values ranging from 0.785–0.934, surpassing the commonly accepted threshold of 0.7. This underscores the reliability of the measurement model. Concerning multicollinearity, assessed through Variance Inflation Factor (VIF), all values are below the recommended threshold of 5, indicating no significant issues with multicollinearity among the variables. Internal consistency, as evaluated by Cronbach's alpha, rho_a, and rho_c coefficients, exceeds the desirable benchmark of 0.7 for all constructs, with values ranging from 0.811–0.884. Furthermore, Composite Reliability values range from 0.862–0.959, affirming the constructs’ reliability. Additionally, the Average Variance Extracted (AVE) values, ranging from 0.667–0.787, surpass the acceptable threshold of 0.5, indicating satisfactory convergent validity. According to Ampofo et al. (Citation2023), these findings collectively suggest that the constructs are reliable, with strong internal consistency and convergent validity, enhancing the credibility of the study's outcomes.

Table 2. Measurement reliability.

4.2. Discriminant validity

From , the HTMT values indicate the extent to which the constructs differ from one another compared to how they correlate with themselves. Notably, the HTMT values for all construct pairs are below the threshold of 0.9, suggesting satisfactory discriminant validity as recommended by previous studies(Tuffour et al. Citation2023; Voorhees et al. Citation2016). Specifically, the highest HTMT value observed is 0.650 between the constructs SN and SG, indicating that the constructs are more strongly related to themselves than to each other. Overall, these findings support the distinctiveness of the constructs under investigation, bolstering the confidence in the validity of our measurement model and the interpretation of our results.

Table 3. Heterotrait-monotrait ratio (HTMT).

From , the results from the Fornell-Larcker criterion reveal the discriminant validity of the latent constructs in our model. According to Baah, Jin, and Tang (Citation2020)criterion, the diagonal elements (representing the square roots of the AVE values) are consistently higher than the off-diagonal elements within their respective rows and columns. This indicates that each construct shares more variance with its indicators than with other constructs in the model, demonstrating satisfactory discriminant validity.

Table 4. Fornell-Larcker criterion.

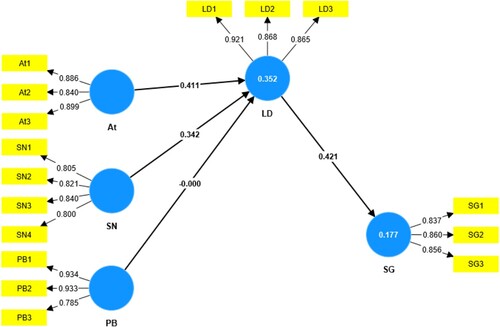

shows the PLS algorithm.

Figure 2. PLS results.

4.3. Hypotheses testing

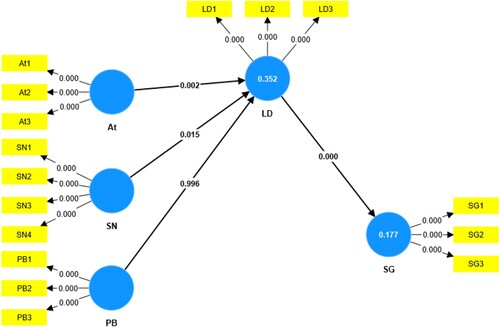

In examining the impact of attitudes towards student loans on loan decisions, our statistical analysis yielded compelling evidence in support of hypothesis H1. Specifically, with a T statistic of 3.057 and a p-value of 0.002, we found a statistically significant positive association between favorable attitudes towards student loans and the likelihood of students deciding to take out loans. This finding not only confirms our initial hypothesis but also underscores the critical role that individual attitudes play in the decision-making process regarding educational financing.

In contrast, the analysis did not yield significant results concerning the relationship between perceived behavioral control and loan decisions. Despite a low standard deviation of 0.000, the T statistic of 0.005 and the high p-value of 0.996 led to the rejection of hypothesis H2. This indicates that perceived behavioral control does not have a substantial impact on individuals’ decisions regarding student loans.

Regarding subjective norms, the analysis demonstrated a significant relationship with loan decisions. With a T statistic of 2.442 and a p-value of 0.015, hypothesis H3 was accepted. This suggests that the perceived influence of societal norms and expectations plays a role in shaping individuals’ decisions to take out student loans. The significant association we uncovered between student loan decisions and graduation rates, supported by a T statistic of 3.899 and a p-value of 0.000, underscores the pivotal role that access to loans plays in enabling students to complete their education. This finding, confirming hypothesis H4, suggests that responsible loan programs could be instrumental in improving graduation outcomes.

Overall, these findings underscore the significance of attitudes and subjective norms in influencing loan decisions, which in turn impact student graduation rates. However, perceived behavioral control was not found to be a significant factor in this context. These results provide valuable insights for policymakers and educational institutions aiming to understand and address the dynamics of student loan decisions and their consequences on academic outcomes.

The results, as illustrated in , are derived from bootstrapping techniques within PLS-SEM, providing robust and reliable estimates This methodological approach allows for the identification of the pathways through which attitudes, norms, and perceived behavioral control influence students’ loan decisions and, ultimately, their graduation rates .

Figure 3. Bootstrapping results.

Table 5. Results for the direct relationship.

5. Discussion

The analysis has uncovered a significant positive association between students’ attitudes toward educational loans and their intentions to utilize such financing. This aligns with the tenets of the TPB which posits that favorable perspectives of behavior predict one’s plans to perform it (Black et al. Citation2023; Mezza et al. Citation2020). Practically, those harboring optimistic views about the necessity and prospective benefits of loans for enabling their academic goals and careers displayed greater willingness to take on loans. This mirrors previous findings that acceptance of loans as a vehicle for opportunity drives students’ loans decisions (Harper et al. Citation2021). Therefore, in determining pathways for degree attainment, mindsets regarding the utility of borrowing apparently outweigh strictly economic calculations. Taken together, these results underscore the cognitive-attitudinal components interplaying with structural elements in students’ enrollment choices.

Despite hypothesizing a positive relationship between perceived behavioral control (PBC) and intentions to utilize loans for education financing, our results indicate an insignificant association. Several practical reasons may explain this unexpected finding. Firstly, while PBC encompasses perceptions of competence and control over loan-related processes, other factors such as socioeconomic background, cultural beliefs, and institutional support could significantly influence loan decision-making. For instance, students from disadvantaged backgrounds may face greater barriers to accessing informational resources or may perceive higher risks associated with loan uptake, thereby attenuating the impact of PBC on intentions(Mazhari and Atherton Citation2021). Additionally, the complexity of loan procedures and uncertainty regarding future repayment capabilities may overshadow individuals’ perceived control, leading to a weaker relationship with intentions (Roche Carioti Citation2020). Moreover, contextual factors such as fluctuating economic conditions or changing government policies regarding student loans could further confound this relationship. Overall, these practical considerations underscore the complex nature of loan decision-making and suggest the need for a more detailed understanding of the interplay between perceived control and other influencing factors in shaping students’ intentions to utilize loans for education financing.

The analysis also shows that subjective norms have a significant relationship with loan decisions. This aligns with previous research indicating that an individual's perception of social pressures shapes their financial choices (Raut Citation2020). Given that taking out student loans is often seen as a societally encouraged path to higher education, it logically follows that such subjective norms would factor into students’ willingness to incur education debt. Consequently, individuals may be more likely to take out loans if they believe it is an expected or encouraged choice within their social circles (Gubik Citation2021). Practically speaking, this highlights that addressing financial decisions without accounting for their social context risks ignoring key psychological motivators. Interventions targeting improved loan literacy may benefit from acknowledging these normative influences. Overall, these results conclusively demonstrate that subjective norms have a significant relationship with loan decisions, underscoring the need to consider peer and social pressures when exploring student borrowing behaviors.

Finally, the analysis has demonstrated a significant relationship between loan decisions and student graduation rates. This aligns with prior research which found that the inability to secure adequate financing threatens students’ capacity to persist through to graduation (Barbera et al. Citation2020; Pike and Robbins Citation2020). Given that loans facilitate access to tuition and living expenses, it logically follows that loan-enabled funding would be linked to improved completion rates. Consequently, as the results conclusively showed, students who take out larger education loans may be more likely to graduate college, presumably by providing the financial means to continue their studies. As highlighted by Barr, Bird, and Castleman (Citation2021), increasing enrollment in responsible loan programs could serve as an impactful intervention for improving graduation outcomes. Overall, these findings underscore that loan decisions represent a key factor tied to students’ ability to successfully earn their degree, highlighting the need for policy discussions regarding responsible financing options. By facilitating persistence to graduation, thoughtful loan access promises benefits both for individual socioeconomic mobility and wider public returns on educational investments.

6. Conclusion

This study has investigated the psychological factors shaping students’ decisions regarding taking out loans to finance their education. While prior research explored determinants of graduation rates or post-loan effects separately(Barbera et al. Citation2020; Pike and Robbins Citation2020), few studies adopted an integrated approach grounded in psychological theory to elucidate intentions behind loan uptake. This study thus made important contributions by holistically examining how attitudes, subjective norms, and perceived behavioral control influence loan decisions and relating these back to graduation outcomes.

The results demonstrated that students holding favorable perspectives of loans and perceiving social pressures to undertake debt displayed greater willingness to borrow to enable their studies. While perceived behavioral control showed no significant association, attitudes and subjective norms were impactful drivers of loan uptake intentions. Additionally, the analysis evidenced that student loans corresponded to improved graduation rates, presumably by facilitating persistence through degree completion.

7. Implications

Practically, Our findings offer actionable insights for policymakers and educational institutions aiming to enhance student access to higher education in Ghana. By recognizing the critical role of favourable attitudes and subjective norms in students’ loan decisions, policymakers can develop targeted communication strategies that positively frame student loans and address common misconceptions. Educational institutions, on the other hand, could implement financial literacy programs that empower students to make informed decisions about their financing options. In adition, policymakers need to recognize the importance of addressing not only structural barriers but also psychological determinants in promoting access to higher education. Secondly, interventions aimed at improving loan literacy and addressing social pressures surrounding loan decisions may help empower students to make informed financial choices. Thirdly, discussions regarding responsible financing options should be prioritized to ensure that students have access to the resources they need to persist through to graduation.

Theoretically, our research contributes significantly to the academic discourse by achieving three key theoretical advancements. First, we have broadened the application of the Theory of Planned Behaviour within the context of educational financing, offering new insights into student decision-making processes. Second, our findings illuminate the psychological factors that influence students’ decisions to take out loans and their subsequent impact on graduation rates, highlighting the importance of considering these factors in the design of loan programs. Lastly, by exploring the interplay between economic and psychosocial drivers of loan decisions, our study fills a crucial gap in the literature, particularly concerning students in developing countries. These advancements not only enrich the theoretical landscape but also have practical implications for policymakers and educational institutions aiming to support students’ educational aspirations effectively.

8. Limitations and future studies

While our study establishes a significant relationship between loan decisions and graduation rates, it is important to acknowledge the limitations inherent in our research design. The cross-sectional nature of our study limits our ability to infer causality. Additionally, our sample, drawn exclusively from two universities in Ghana, may not fully represent the diverse experiences of students across different regions or types of institutions. Despite these challenges, the findings of our study remain robust.

Building on our findings, future research should explore the long-term impacts of student loan decisions on career outcomes and financial well-being post-graduation. Additionally, qualitative studies could provide deeper insights into the personal and cultural factors that influence students’ attitudes toward debt. Investigating these areas will further enrich our understanding of how to effectively support students in navigating the complexities of educational financing.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abou Kamar, M., A. Maher, I. E. Salem, and A. M. Elbaz. 2024. “Gamification Impact on Tourists’ pro-Sustainability Intentions: Integration of Technology Acceptance Model (TAM) and the Theory of Planned Behaviour (TPB).” Tourism Review 79 (2): 487–504. https://doi.org/10.1108/TR-04-2023-0234.

- Abraham, K. G., E. Filiz-Ozbay, E. Y. Ozbay, and L. J. Turner. 2020. “Framing Effects, Earnings Expectations, and the Design of Student Loan Repayment Schemes.” Journal of Public Economics 183:104067. https://doi.org/10.1016/j.jpubeco.2019.104067.

- Addo, P. K., and A. Adusei. 2021. “Risk Management in Higher Education: The Role of Educational Leaders in Translating Policy into Practice in the Ghanaian Context.” The IEA Classroom Environment Study 49 (2): 146–162.

- Agyabeng-Mensah, Y., E. Afum, C. Baah, and D. Essel. 2022. “Exploring the Role of External Pressure, Environmental Sustainability Commitment, Engagement, Alliance and Circular Supply Chain Capability in Circular Economy Performance.” International Journal of Physical Distribution & Logistics Management 52 (5/6): 431–455. https://doi.org/10.1108/IJPDLM-12-2021-0514.

- Ampofo, S. A., Y. Shao, E. Opoku-Mensah, D. Effah, P. Tuffour, D. Darko, and E. Asiedu-Aryeh. 2023. “Sustainable Mining: Examining the Direct and Configuration Path of Legitimacy Pressure, Dual Embeddedness Resource Dependency and Green Mining Towards Resource Management.” Resources Policy 86 (PA): 104252. https://doi.org/10.1016/j.resourpol.2023.104252.

- Atuahene, F. 2013. “Charting Higher Education Development in Ghana: Growth, Transformations, and Challenges.” International Perspectives on Education and Society 21:215–263. https://doi.org/10.1108/S1479-3679(2013)0000021011.

- Baah, C., Z. Jin, and L. Tang. 2020. “Organizational and Regulatory Stakeholder Pressures Friends or Foes to Green Logistics Practices and Financial Performance: Investigating Corporate Reputation as a Missing Link.” Journal of Cleaner Production 247:119125. https://doi.org/10.1016/j.jclepro.2019.119125.

- Barbera, S. A., S. D. Berkshire, C. B. Boronat, and M. H. Kennedy. 2020. “Review of Undergraduate Student Retention and Graduation Since 2010: Patterns, Predictions, and Recommendations for 2020.” Journal of College Student Retention: Research, Theory & Practice 22 (2): 227–250.. https://doi.org/10.1177/1521025117738233.

- Barr, A., K. A. Bird, and B. L. Castleman. 2021. “The Effect of Reduced Student Loan Borrowing on Academic Performance and Default: Evidence from a Loan Counseling Experiment.” Journal of Public Economics 202:104493. https://doi.org/10.1016/j.jpubeco.2021.104493.

- Black, S. E., J. Denning, L. J. Dettling, S. Goodman, and L. J. Turner. 2023. “Taking it to the Limit: Effects of Increased Student Loan Availability on Attainment, Earnings, and Financial Well-Being.” SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4331400.

- Bondzi–Simpson, P. E., and K. S. Agomor. 2021. “Financing Public Universities in Ghana Through Strategic Agility: Lessons from Ghana Institute of Management and Public Administration (GIMPA).” Global Journal of Flexible Systems Management 22 (1): 1–15. https://doi.org/10.1007/s40171-020-00254-6.

- Brooks, J., and A. Levitin. 2020. “Redesigning Education Finance: How Student Loans Outgrew the “Debt”, Paradigm.” Georgetown Law Journal 109 (5): 5–80.

- Card, D., and A. Solis. 2022. “Measuring the Effect of Student Loans on College Persistence.” Education Finance and Policy 17 (2): 335–366. https://doi.org/10.1162/edfp_a_00342.

- Chen, R., and P. R. Bahr. 2021. “How Does Undergraduate Debt Affect Graduate School Application and Enrollment?” Research in Higher Education 62 (4): 528–555. https://doi.org/10.1007/s11162-020-09610-y.

- Cloutier, J., and A. Roy. 2020. “Consumer Credit Use of Undergraduate, Graduate and Postgraduate Students: An Application of the Theory of Planned Behaviour.” Journal of Consumer Policy 43 (3): 565–592. https://doi.org/10.1007/s10603-019-09447-8.

- Creswell, J. W., and J. D. Creswell. 2018. Research Design: Qualitative, Quantitative, and Mixed Methods Approaches. 5th ed. Sage publications.

- Dickson, T., E. P. Mulligan, and J. DeVahl. 2020. “The Toll of Student Debt: Stress Among Health Professions Students and the Promising Role of Financial Self-Efficacy on Career Choices.” Journal of Physical Therapy Education 34 (4): 339–346. https://doi.org/10.1097/JTE.0000000000000162.

- Elmira, E., and D. Suryadarma. 2020. “Financing Tertiary Education in Indonesia: Assessing the Feasibility of an Income-Contingent Loan System.” Higher Education 79 (2): 361–375. https://doi.org/10.1007/s10734-019-00414-3.

- Fomunyam, G. K. 2022. “Female Graduation Rate in STEM Programs in Tertiary Education: The Case of the Gulf Cooperation Council Countries (GCCs).” International Journal of Applied Engineering and Technology (London) 4 (4): 21–26.

- Froidevaux, A., J. Koopmann, M. Wang, and P. Bamberger. 2020. “Is Student Loan Debt Good or bad for Full-Time Employment upon Graduation from College?” Journal of Applied Psychology 105 (11): 1246–1261. https://doi.org/10.1037/apl0000487.

- Furuta, K. 2021. “Parental Perceptions of University Cost, Fear of Debt, and Choice of High School in Japan.” British Journal of Sociology of Education 42 (5-6): 667–685. https://doi.org/10.1080/01425692.2021.1896356.

- Guarte, J. M., and E. B. Barrios. 2006. “Estimation Under Purposive Sampling.” Communications in Statistics: Simulation and Computation 35 (2): 277–284. https://doi.org/10.1080/03610910600591610.

- Gubik, A. S. 2021. “Entrepreneurial Career: Factors Influencing the Decision of Hungarian Students.” Entrepreneurial Business and Economics Review 9 (3): 43–58. https://doi.org/10.15678/EBER.2021.090303.

- Hagedorn, R. L., R. A. Wattick, and M. D. Olfert. 2022. ““My Entire World Stopped”: College Students’ Psychosocial and Academic Frustrations During the COVID-19 Pandemic.” Applied Research in Quality of Life 17 (2): 1069–1090. https://doi.org/10.1007/s11482-021-09948-0.

- Hair, J. F., L. M. Matthews, R. L. Matthews, and M. Sarstedt. 2017. “PLS-SEM or CB-SEM: Updated Guidelines on Which Method to Use.” International Journal of Multivariate Data Analysis 1 (2): 107–123.

- Harper, C. E., L. Scheese, E. Zhou, and R. Darolia. 2021. “Who do College Students Turn to for Financial Aid and Student Loan Advice, and is it Advice Worth Following?” Journal of Student Financial Aid 50 (3). https://doi.org/10.55504/0884-9153.1729.

- Herbaut, E., and K. Geven. 2020. “What Works to Reduce Inequalities in Higher Education? A Systematic Review of the (Quasi-)Experimental Literature on Outreach and Financial aid.” Research in Social Stratification and Mobility 65:100442. https://doi.org/10.1016/j.rssm.2019.100442.

- Hu, X., and J. C. Ortagus. 2023. “National Evidence of the Relationship between Dual Enrollment and Student Loan Debt.” Educational Policy 37 (5): 1241–1276. https://doi.org/10.1177/08959048221087204.

- Kamble, S., A. Gunasekaran, and H. Arha. 2019. “Understanding the Blockchain Technology Adoption in Supply Chains-Indian Context.” International Journal of Production Research 57 (7): 2009–2033.. https://doi.org/10.1080/00207543.2018.1518610.

- Kee, C. E. 2021. “The Impact of COVID-19: Graduate Students’ Emotional and Psychological Experiences.” Journal of Human Behavior in the Social Environment 31 (1-4): 476–488. https://doi.org/10.1080/10911359.2020.1855285.

- Lea, S. E. G. 2021. Debt and Overindebtedness: Psychological Evidence and its Policy Implications. Social Issues and Policy Review 15 (1): 146–179. https://doi.org/10.1111/sipr.12074.

- Mazhari, T., and G. Atherton. 2021. “Students’ Financial Concerns in Higher Education.” Higher Education Quarterly. https://doi.org/10.1111/hequ.12267.

- Mekonen, E. G., B. S. Workneh, M. S. Ali, and N. Y. Muluneh. 2021. “The Psychological Impact of COVID-19 Pandemic on Graduating Class Students at the University of Gondar, Northwest Ethiopia.” Psychology Research and Behavior Management 14:109–122. https://doi.org/10.2147/PRBM.S300262.

- Mezza, A., D. Ringo, S. Sherlund, and K. Sommer. 2020. “Student Loans and Homeownership.” Journal of Labor Economics 38 (1): 215–260. https://doi.org/10.1086/704609.

- Niyi Jacob, O., A. I. Elizabeth, and G. Ndubuisi. 2020. “Problems Faced by Students in Public Universities in Nigeria and the Way Forward.” Jurnal Sinestesia 4 (1): 230–241.

- Pike, G. R., and K. R. Robbins. 2020. “Using Panel Data to Identify the Effects of Institutional Characteristics, Cohort Characteristics, and Institutional Actions on Graduation Rates.” Research in Higher Education 61 (4): 485–509. https://doi.org/10.1007/s11162-019-09567-7.

- Ramus, K., and N. A. Nielsen. 2005. “Online Grocery Retailing: What do Consumers Think?” Internet Research 15 (3): 335–352. https://doi.org/10.1108/10662240510602726.

- Raut, R. K. 2020. “Past Behaviour, Financial Literacy and Investment Decision-Making Process of Individual Investors.” International Journal of Emerging Markets 15 (6): 1243–1263. https://doi.org/10.1108/IJOEM-07-2018-0379.

- Raza, S. A., W. Qazi, and S. Q. Yousufi. 2021. “The Influence of Psychological, Motivational, and Behavioral Factors on University Students’ Achievements: The Mediating Effect of Academic Adjustment.” Journal of Applied Research in Higher Education 13 (3): 849–870. https://doi.org/10.1108/JARHE-03-2020-0065.

- Regmi, P. R., E. Waithaka, A. Paudyal, P. Simkhada, and E. Van Teijlingen. 2017. “Guide to the Design and Application of Online Questionnaire Surveys.” Nepal Journal of Epidemiology 6 (4): 640–644. https://doi.org/10.3126/nje.v6i4.17258.

- Ricks, J. R., and J. M. Warren. 2021. “Experiences of Successful First-Generation College Students with College Access.” Journal of School Counseling 11 (1): 1–35.

- Roche Carioti, K. 2020. “Student Loan Debt: A Problem-Based Learning Activity for Introductory Economics Students.” The Journal of Economic Education 51 (2): 130–142. https://doi.org/10.1080/00220485.2020.1731388.

- Saleh, A., and K. Bista. 2017. “Examining Factors Impacting Online Survey Response Rates in Educational Research: Perceptions of Graduate Students.” Journal of Multidisciplinary Evaluation 13 (29): 63–74. https://doi.org/10.56645/jmde.v13i29.487.

- Sarosa, S. 2022. “The Effect of Perceived Risks and Perceived Cost on Using Online Learning by High School Students.” Procedia Computer Science 197:477–483. https://doi.org/10.1016/j.procs.2021.12.164

- Shih, H.-M., B. H. Chen, M.-H. Chen, C.-H. Wang, and L.-F. Wang. 2022. “A Study of the Financial Behavior Based on the Theory of Planned Behavior.” International Journal of Marketing Studies 14 (2): 1. https://doi.org/10.5539/ijms.v14n2p1.

- Sims, T., S. Raposo, J. N. Bailenson, and L. L. Carstensen. 2020. “The Future is now: Age-Progressed Images Motivate Community College Students to Prepare for Their Financial Futures.” Journal of Experimental Psychology: Applied 26 (4): 593–603. https://doi.org/10.1037/xap0000275.

- Spector, P. E. 2019. “Do Not Cross Me: Optimizing the Use of Cross-Sectional Designs.” Journal of Business and Psychology 34 (2): 125–137. https://doi.org/10.1007/s10869-018-09613-8.

- Stoddard, C., and C. Urban. 2020. “The Effects of State-Mandated Financial Education on College Financing Behaviors.” Journal of Money, Credit and Banking 52 (4): 747–776. https://doi.org/10.1111/jmcb.12624.

- Su, Y., Z. Zhu, J. Chen, Y. Jin, T. Wang, C. L. Lin, and D. Xu. 2021. “Factors Influencing Entrepreneurial Intention of University Students in China: Integrating the Perceived University Support and Theory of Planned Behavior.” Sustainability (Switzerland) 13 (8): 4519. https://doi.org/10.3390/su13084519.

- Sung, P. L., T. Y. Hsiao, L. Huang, and A. M. Morrison. 2021. “The Influence of Green Trust on Travel Agency Intentions to Promote low-Carbon Tours for the Purpose of Sustainable Development.” Corporate Social Responsibility and Environmental Management 28 (4): 1185–1199. https://doi.org/10.1002/csr.2131.

- Tuffour, P., G. Chen, R. A. Agyapong, A. Abdallah, and E. Opoku-Mensah. 2023. “To What Extent Does Organizational Learning Influence the Stakeholder Pressure–Green Procurement Nexus? Evidence from Ghana.” Creativity and Innovation Management 32 (3): 442–457. https://doi.org/10.1111/caim.12566.

- Ulker-Demirel, E., and G. Ciftci. 2020. “A Systematic Literature Review of the Theory of Planned Behavior in Tourism, Leisure and Hospitality Management Research.” Journal of Hospitality and Tourism Management 43:209–219. https://doi.org/10.1016/j.jhtm.2020.04.003.

- Ullah, N. 2020. “Integrating TAM/TRI/TPB Frameworks and Expanding their Characteristic Constructs for DLT Adoption by Service and Manufacturing Industries-Pakistan Context.” 2020 International Conference on Technology and Entrepreneurship, ICTE 2020. https://doi.org/10.1109/ICTE47868.2020.9215537.

- Voorhees, C. M., M. K. Brady, R. Calantone, and E. Ramirez. 2016. “Discriminant Validity Testing in Marketing: An Analysis, Causes for Concern, and Proposed Remedies.” Journal of the Academy of Marketing Science 44 (1): 119–134. https://doi.org/10.1007/s11747-015-0455-4.

- Xiao, J. J., and K. T. Kim. 2022. “The Able Worry More? Debt Delinquency, Financial Capability, and Financial Stress.” Journal of Family and Economic Issues 43 (1): 138–152. https://doi.org/10.1007/s10834-021-09767-3.

- Zacharias, N., and J. Ryan. 2021. “Moving Beyond ‘Acts of Faith’: Effective Scholarships for Equity Students.” Journal of Higher Education Policy and Management 43 (2): 147–165. https://doi.org/10.1080/1360080X.2020.1777499.