?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

For stochastic loss reserving, we propose an individual information model (IIM) which accommodates not only individual/micro data consisting of incurring times, reporting developments, settlement developments as well as payments of individual claims but also heterogeneity among policies. We give over-dispersed Poisson assumption about the moments of reporting developments and payments of every individual claims. Model estimation is conducted under quasi-likelihood theory. Analytic expressions are derived for the expectation and variance of outstanding liabilities, given historical observations. We utilise conditional mean square error of prediction (MSEP) to measure the accuracy of loss reserving and also theoretically prove that when risk portfolio size is large enough, IIM shows a higher prediction accuracy than individual/micro data model (IDM) in predicting the outstanding liabilities, if the heterogeneity indeed influences claims developments and otherwise IIM is asymptotically equivalent to IDM. Some simulations are conducted to investigate the conditional MSEPs for IIM and IDM. A real data analysis is performed basing on real observations in health insurance.

1. Introduction

In the background of stochastic reserving, loss reserving is referred to a procedure to predict incurred outstanding liabilities in general insurance companies. It is well known that chain-ladder method proposed by Mack (Citation1993) and its related versions can be easily performed by using pencil and paper because of the simple aggregate data structure called run-off triangle and hence are popular in practice. However, as England and Verrall (Citation2002) mentioned, the advantages of aggregate data models are at the cost of prediction accuracy because of information loss caused by simply aggregating individual or micro data, which records incurring time, reporting time, settlement time as well as payment processes of individual claims. In risk management of insurance companies, with the modern computer technology, it is urgent for actuaries to explore the usage of related information to improve the accuracy in predicting the liabilities, which also attracts increasing interests of many scholars from actuarial science. Antonio and Plat (Citation2014), Pigeon et al. (Citation2013, Citation2014) demonstrated by an empirical analysis that loss reserving based on individual data had more prediction accuracy than aggregate models. Huang, Qiu, Wu, Zhou (Citation2015), Huang, Qiu, Wu (Citation2015) and Huang et al. (Citation2016) revealed that individual loss reserving had more accuracy than methods using aggregate data in sense that the former produced a smaller mean square error.

A small stream of earlier literature about IDMs, for example, Arjas (Citation1989) and Norberg (Citation1993, Citation1999) formulated a probabilistic framework for the developments of individual claims. Most recently, Yu and He (Citation2016) modelled the individual claim development process by marked Cox processes (also known as double stochastic processes). As we all know, it is challenging to acquire analytic expressions for the moments of outstanding liabilities under continuous-time IDMs. Perhaps partly for this reason, there is a great deal of work that has been done under discrete-time IDMs, see, e.g., Pigeon et al. (Citation2013, Citation2014), Verrall et al. (Citation2010), Huang, Qiu, Wu, Zhou (Citation2015), Huang, Qiu, Wu (Citation2015) and Huang et al. (Citation2016). Zhao and Zhou (Citation2010) considered the R-delays so as to predict the incurred but not settled outstanding liabilities. Unfortunately, IDMs also confront information loss caused by neglecting individual information, i.e., information from policy or policyholder. It is not clear so far how much accuracy in predicting the outstanding liabilities is sacrificed, when the individual information is neglected. In the present paper, we will explore how much improvement in the accuracy that will be measured by conditional MSEP can be achieved by incorporating the useful individual information into modelling under discrete time framework similar as Huang, Qiu, Wu, Zhou (Citation2015), Huang, Qiu, Wu (Citation2015) and Huang et al. (Citation2016). Besides, we avoid the strong Poisson distribution assumption for the number of individual claims assumed in Huang, Qiu, Wu, Zhou (Citation2015), Huang, Qiu, Wu (Citation2015) and Huang et al. (Citation2016) and instead extend to weak assumptions about the first two moments so that parameters estimation can be conducted under quasi-likelihood theory (cf. McCullagh & Nelder, Citation1989).

The conditional MSEP is broadly used to compare different models for loss reserving. It is well known that the conditional MSEP is the sum of process variance caused by the randomness of outstanding liabilities and estimation error originating from uncertainty of parameters estimators. It is theoretically feasible to estimate it by bootstrap method. There were some examples which discussed the MSEP under collective models – for instance, Mack (Citation1993), Mack (Citation2000) (comparing three methods – Benktander, Bornhuetter–Ferguson and chain-ladder under the criteria of MSEP), Alai et al. (Citation2009, Citation2010) (Bornhuetter–Ferguson method under generalised linear model) and Wüthrich and Merz (Citation2008) (comprehensive summary of the details of methods based on aggregate data). Besides, Lindholm et al. (Citation2020) introduced a semi-analytic approximation method to estimate the conditional MSEP, where the method is illustrated by loss reserving based on aggregate data. Examples that have applied the approximation method are Wahl (Citation2019), who computed explicit moments of outstanding liabilities by applying discretisation scheme under the framework of Antonio and Plat (Citation2014), and Wahl et al. (Citation2019) who modelled individual data on aggregate level. In the present paper, we also use the approximation method for the MSEP, which is derived under IIM, because of its simplification.

The paper is organised as follows. In Section 2, we describe the data structure and display the mathematical expression of outstanding liabilities caused by a risk portfolio at a given evaluation date. In Section 3, we separately model reporting developments, settlement delays and payments of claims and in each part, we formulate the model assumptions as well as estimation for the model parameters. Section 4 mainly derives the formulas of loss reserve and conditional variance of outstanding liabilities given historical observations, and studies the improvement of accuracy achieved by IIM with respect to IDM. Section 5 reports some simulation results and a real data analysis. Section 6 concludes the paper with a few remarks.

2. Data structure

Claim events incurred by some policy are usually reported to the insurer in some time periods (reporting delays) after their occurrence and the reported claims are finally settled with some time lags (settlement delays) between their reports and final settlements. Before going further, it is necessary to discuss the supports of reporting and settlement delays. In the following assumption, we assume that there exists maximum reporting delay and settlement delay

. Actually, there are basically two cases for the supports of the delays: finite and infinite. It would be a known priori (generally read from the items of the insurance contracts) if the supports are finite or infinite before any loss reserving is taken care of. Even for the case the delays take unrestricted values, if the probability to take values over certain limits is quite small, one can safely assume a capped delays by cutting off the tails with probability small enough. As a result, the assumption of capped delays is reasonable in many real insurance businesses, especially for such insurance without very much high claims payments. An example is the general health insurance. The assumption of capped delays has been extensively adopted in such traditional methods as chain-ladder algorithm. If the tails cannot be safely cut off, however, the models such as the one proposed in Crevecoeur et al. (Citation2019) or some others would be more suitable. From the statistical point of view, for their distributions to be reasonably estimated with observations over a finite number of years, at least one of the two assumptions is necessary: they take only a finite number of values with arbitrary probabilities (but subject to normalisation) or countably infinitely many values but with their distribution functions identified by finite many parameters. Whatever the case, the number of unknown parameters that need to be estimated must be finite. Here the former is taken, whereas Crevecoeur et al. (Citation2019), for example, took the latter.

Then we specify the data structure used in our model. It is in discrete time version as, e.g., Huang, Qiu, Wu (Citation2015) did. Typically, the data for modelling is organised through periods with fixed length such as 1 year, one season or 1 month depending on lines of business. Conventionally, those periods are referred to ‘(accident) years’. This is also a way widely adopted by insurers to predict the incurred outstanding liabilities in practice. Specifically, the whole observation horizon is made of n accident years and loss reserving is evaluated at the end of nth accident year. In year i, , there are

insurance policies, each of which is coded by

,

.

Every individual is associated with a random risk exposure

and d-dimensional vector of covariate

whose first entry is 1 and other entries indicating the individual information/features that influence the developments of individual claims. The developments of claims incurred by individual

are detailed as follows.

The reporting developments of claims are recorded by

,

For

Payments for each claim are assumed to be paid for only once at its final settlement. For

Then the random element associated with individual is denoted by

, which are i.i.d. from the population

which can be considered as a complete observation of a representative policy in year i.

Following conventional terms, a claim, which has been reported to the insurer but not settled, is known as RBNS claim and a claim, which has been incurred but not reported to the insurer, is known as IBNR claim. For accident year i, the individual observed data is as follows.

The reporting developments of a representative policy in year i are truncated in sense that we can only observe

For

For

Then individual observation is the union of

,

,

and

, that is

and the historical observations of all policies in the portfolio, denoted by

, is just the union of policy-specified observation that is

, where

is the policy-specified realisations of

in year i that is

It is well known that RBNS and IBNR claims of the risk portfolio naturally result in outstanding liabilities to the insurer. Specifically, the total of future payments for all the RBNS and IBNR claims can be represented as

(3)

(3) where

are RBNS and IBNR liabilities incurred in year i, respectively. Thoroughly, we take the convention

if

.

3. Model specification

This section separately specifies the models for the reporting developments, settlement developments and payments of claims. In each part, we first give model assumptions and then detail the parameter estimations under both IIM and IDM. The model assumptions in this section are all given under the condition that risk exposure r and covariates are known.

3.1. Modelling reporting developments of claims

Model assumption for reporting developments of claims is given as follows. It is mainly about the first and second moments of reporting developments of claims. The assumption involves vectors of parameters , which are all d-dimensional vector.

Assumption 3.1

For an individual with assume that

are independent,

and

where

with

and

,

as well as

.

Remark 3.1

In order to make be reasonably estimated, the condition

is necessary.

By independence among policies and assumption above, one can construct the quasi-likelihood function of reported claims as follows,

(4)

(4) where

is policy-specified quantities of

that is

One can refer to McCullagh and Nelder (Citation1989) for more details about quasi-likelihood theory. Similar to maximum likelihood estimation, parameters

can be estimated by maximising

with respect to the parameters. Denote by

and stack

s as a vector

such that entry

is corresponding to

in vector

. The quasi-score function, i.e., partial derivatives of

with respect to the parameters is

(5)

(5) where

. To determine the block entries of

, one needs the unit vector

with 1 at component s (any positive integer) and

, of which dimensions can be read from context, and the following partial derivatives

where

and ⊗ is the Kronecker product.

The covariance matrix of , which is also the negative expected value of

, is

(6)

(6) The parameters

are estimated by Newton–Raphson with Fisher scoring starting with initials

and updating estimated parameters in the following way:

where

and

are obtained by replacing

with

. Write the estimated parameters as

. To estimate dispersion parameter ϕ, we adopt conventional method–moment estimation that is,

where

s are plug-in estimates of

that is

IDM considers that policy's feature information has no effect on reporting developments that is the coefficients of

are thought to be zero. Obviously, IDM is a misspecified model if the feature information indeed influence those developments. Therefore, in IDM, λ and

are thought to keep fixed among all policies and then

is same for the policies. By maximising function

in (Equation4

(4)

(4) ) with respect to

, one can obtain that

(7)

(7) where

representing total number of reported claims with reporting delay u and

meaning total exposures in the first n−u years.

3.2. Modelling settlement delays

In IIM, the settlement developments of individual claims after their reporting to the insurer have the following assumption. The assumption involves vectors of parameters , which are all d-dimensional vector.

Assumption 3.2

Assume that given

follows multinomial distribution with parameters

and

where

with

, as well as

and the tuples

are independent.

Remark 3.2

Similar to the condition in Remark 3.1, the condition is necessary to make

be reasonably estimated. Therefore, it is enough to assume

.

For (

) reported claims of representative policy in year i, one can only observe

and

(the number of RBNS claims with settlement delays no less than n−i−u), where

if

. According to the assumption above, the individual log-likelihood of settlement developments is

(8)

(8) where

is the tail probability of settlement delays no less than v. Obviously, an alternative form of term in the last term in the first line of (Equation8

(8)

(8) ) is

. Further, if we write

, which means number of settled claims with settlement delay v, (Equation8

(8)

(8) ) becomes

(9)

(9) To estimate

by Newton–Raphson with Fisher scoring, we need the identities in the following proposition.

Proposition 3.1

The gradient of with respect to

is

and conditional expectation of Hessian matrix of

given

is

(10)

(10) where

and

We estimate by maximising overall log-likelihood function

which is the summation of individual log-likelihood

, that is

is obtained as follows:

where

To obtain

, similar as previous section, we use Newton–Raphson with Fisher scoring which needs the following gradients

and its covariance matrix

, where

(11)

(11)

In IDM, similar as in the section above, probabilities

are thought to keep fixed among all policies that is

is independent of

. By MLE again, we have

(12)

(12) where

with

3.3. Modelling claim payments

We give some assumptions about payments of individual claims as follows. The assumptions involve a -dimensional vector of parameters

.

Assumption 3.3

Claim payments

are independent, independent of

and also assume that conditional mean and variance satisfy

with

where

is a

-dimensional vector of covariates.

Arrange all settled payments of the risk portfolio into the set , where

is covariate associated with payments

and

is the total number of settled claims. Construct quasi-likelihood by independence among policies and assumption above,

(13)

(13) where

. Denote

and

. The quasi-score function–partial derivatives of

with respect to the parameters is

(14)

(14) where

.

The covariance matrix of , which is also the negative expected value of

, is

(15)

(15) The parameters

are estimated by iteratively re-weighted least square (IRLS) algorithm, which is as follows,

Initialise

Compute adjusted response

Update

To estimate dispersion parameter , we also adopt conventional method–moment estimation that is,

where

.

In IDM, the coefficients of covariates about individual features are considered to be zero, i.e., , and

s only depended on reporting and settlement delays, which means it just needs to estimate

by the similar procedure as stated above. Therefore, estimator

for

is a maximiser of the

, which is the function of

that is under

, and

in Equation (Equation13

(13)

(13) ) is independent of individual information and only takes one of the following forms:

(16)

(16) Then the estimate of

under IDM is denoted by

, which is a policy-free estimate.

4. Prediction for outstanding liabilities

In this section, the terminologies ‘loss reserve’ and ‘loss reserving’ are precisely specified, measurement of accuracy of loss reserving is then discussed and we also shows the improvement of accuracy of loss reserving basing on IIM with respect to IDM.

4.1. Loss reserve and loss reserving

Recalling the total outstanding liability R defined in (Equation3(3)

(3) ), by ‘loss reserve’, we refer to the projection

(17)

(17) of R on the observations

by the evaluation date n, where the subscript ‘

’ indicates portfolio size, since loss reserve is based on specific risk portfolio. One can see that

is a function of unknown parameters

and hence it needs to be estimated.

To derive moments about outstanding liabilities R and conditional variance of R, the following quantities are needed. For , denote by

(18)

(18) where

is conditional moment of claim payments given

, reporting delays u and settlement delays no less than v, so that corresponding policy-specified quantities are

(19)

(19) Then we derive the following theorem which provides formulas to compute not only the loss reserve

but also variance of outstanding liabilities R given observations

.

Theorem 4.1

Under the model formulated by Assumptions 3.1–3.3, the loss reserve is (20)

(20) and the variance of R given observations

is

It can be clearly seen that loss reserve depends on not only the information from observed data in terms of the number of RBNS claims and policy's feature information but also unknown parameters

, which results in the need for estimating

. Accordingly, the term ‘loss/claims reserving’ is used for certain reasonable estimate of the loss reserve. Formally, after getting certain reasonable estimates

of the unknown parameters from the observed data, as, for example, what has been done in the previous section, we have the following theorem.

Theorem 4.2

By loss reserving we refer to the (random) quantity (21)

(21) where

s and

s are obtained by substituting unknown parameters with their estimates.

According to the theorem above, it is easy to obtain loss reserving under IDM by simply replacing s and

s in (Equation21

(21)

(21) ) with policy-free estimates

s and

s, respectively. Specifically, to distinguish two different estimates for reserve, we use symbol

to indicate loss reserving under IDM, which is

(22)

(22) where

,

and

4.2. Measurement of prediction accuracy

It is essential to measure accuracy of loss reserving and especially accuracy improvement of loss reserving by considering useful individual information with respect to the one without this information. To measure the prediction accuracy of some reserve estimate , which is

measurable, a natural idea is conditional mean square error of prediction (MSEP) which is defined as

(23)

(23) For loss reserving

, which includes individual information, and

without individual information, their MSEPs are

and

, respectively. To measure the difference in prediction accuracy of

and

, we use the following ratio:

(24)

(24) It is well known that individual information model performs better in terms of prediction accuracy than individual data model, if

, but it is hard to compute

with unknown parameters. Fortunately, we can compare

and number 1 when portfolio size m is large enough. It is notable that individual data model is nested in individual information model. Then we have the following theorem under some regular conditions (see Van der Vaart, Citation2000), which illustrates the advantages of individual information model over individual data model.

Theorem 4.3

When portfolio size m tends to infinity, where

means converging in probability, if the individual data model is true, that is the coefficients of

are zero. Otherwise,

(25)

(25) where

with

(26)

(26) and if the asymptotic bias

.

The theorem above shows that IIM is asymptotically equivalent to IDM, if IDM is true and otherwise the former has higher prediction accuracy than the latter when portfolio size is large enough. One can intuitively understand that as portfolio size tends to infinity, both models can capture all the information included in observations when IDM holds true, since IIM is a generalised version of IDM. However, individual data model fails to capture the effects of policy's feature information and thus leads to greater bias when IIM holds true.

An important issue one concerns is how much prediction accuracy of loss reserving can be improved, if IIM holds true, in a fixed risk portfolio that is one cares about actual value of

under true IIM. However, there are unknown parameters

in

and

. An approximation method that comes to one's mind is substituting estimated parameters

to them, which however needs to further take estimation error of

into account. We directly use the method named semi-analytical approximation for

(One can refer to Lindholm et al. (Citation2020) for more details), which is also discussed in Wahl (Citation2019) under micro data model. Then the approximations for

and

are

(27)

(27) so that

(28)

(28) where

is the gradient of loss reserve

with respect to

computed at

and

is asymptotic covariance of

. It is easily known that

where and

are plug-in estimates and

is obtained by inserting

into

in Equation (Equation11

(11)

(11) ). One can refer to Chapter 9 in McCullagh and Nelder (Citation1989) for more details.

Proposition 4.4

The gradient of with respect to

is

the gradient of

with respect to

is

where

,

and

, and the gradient of

with respect to

is

where

5. Simulations and real data analysis

Reported in this section include the results from a few small simulations conducted to further investigate . A real data in health insurance was also analysed to show the application of IIM and the accuracy improvement by using IIM with respect to IDM in practice.

5.1. Simulation

In this simulation, the risk exposures associated with every individuals were drawn from the uniform distribution on , the covariates were produced by multivariate standard normal distribution and we simulated the random developments of claims for a fixed risk portfolio. In each run, we directly compute

according to Equation (Equation24

(24)

(24) ) so that we can know how much accuracy is improved by using IIM with respect to IDM under the fixed risk portfolio.

Because there are only assumptions about mean and variance for reporting developments and payments of claims, we need additional distributional assumptions to generate them, which arise as follows. First, for individual reporting developments s, we generated them by the additional assumption which says that

follows Poisson distribution with mean

. Second, for individual payments

, similarly, we generated them by assuming that

follows Poisson distribution with mean

. Each run in the simulation was conducted with the setting: n = 5,

,

, a risk portfolio size

i.e., 10, 000 policies in each year, and any combination of parameters which varied according to the setting in the following two examples.

Example 5.1

Dimension d = 3 and the parameters varied in an auxiliary parameter t ranging in by step 0.01 as

Parameters for reporting developments:

Parameters for settlement developments:

Parameters for payments:

Covariates were produced by bivariate standard normal distribution in this example.

Example 5.2

Dimension d = 4 and parameters varied over t ranging in by step 0.01 as

Parameters for reporting developments:

Parameters for settlement developments:

Parameters for payments:

Covariates were produced by ternary standard normal distribution in this example.

In each run, we estimated loss reserve by both IIM and IDM using the simulated data that is we computed by Equation (Equation21

(21)

(21) ) as well as

by (Equation22

(22)

(22) ) and true parameters were used to compute

and

according to Theorem 4.1. Then we computed

by inserting the computed

,

,

and

into Equation (Equation24

(24)

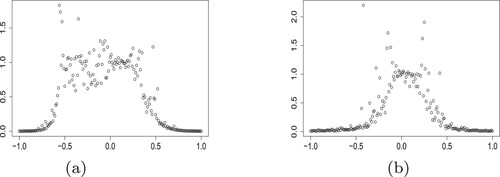

(24) ). At last, we plotted the simulated results in Figure .

Figure 1. The simulated over varying coefficients of covariates. (a) Example 5.1 and (b) Example 5.2.

We obtained the results consistent with Theorem 4.3 from the simulations above.

When the coefficients of

When those coefficients are away from zero,

5.2. Real data analysis

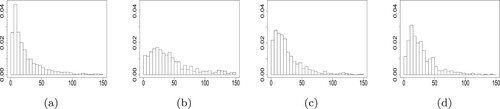

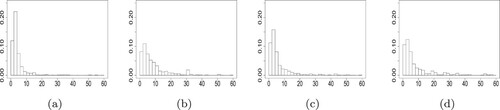

In this section, we analysed a dataset, which was collected by a commercial insurance company in China. The dataset recorded writing and expiring dates of policies, individual information, see Table , and developments of reported claims between 1/1/2019 and 8/31/2019.

Table 1. The individual information in real data analysis.

To visualise the effects of individual information on the developments of claims, for example, the histograms of reporting and settlement delays measured in days were provided under a few combinations of covariate values including gender, geographical location and age, as presented in Figures and . It was strongly proposed that the individual information had impacts on the distributions of reporting and settlement delays.In the dataset, all the reporting delays were not more than 150 days (5 months). By China Banking and Insurance Regulatory Commission, the reported claims in health insurance are generally required to be settled within 2 months if no disagreement exists. It is appropriate to take 1 month as the time unit (‘accident year’ in previous sections). Thus the maximum reporting and settlement delays were safely set to and

(the real data supported this assumption).

Figure 2. Histograms of reporting delays (in days): (a) Female, Region III, age 9–20; (b) Male, Region I, age 45–50; (c) Male, Region VI, age 20–40; (d) Male, Region III, age >55.

Figure 3. Histograms of settlement delays (in days): (a) Female, Region III, age 9–20; (b) Male, Region I, age 45–50; (c) Male, Region VI, age 20–40; (d) Male, Region III, age >55.

To illustrate the proposed model for loss reserving, evaluation date was set as 8/31/2019. That is, we worked with n = 8, and

(months). There are four factors organised into eight features

, as shown in Table . Besides, reporting and settlement delays, which were regarded as factors to model claim payments as Assumption 3.2 formulated, were respectively organised into five features

,

and three features

.

The estimated parameters for the reporting developments under IIM, their standard errors and p-values of significance test were displayed in Table , while the corresponding estimated results under IDM, i.e., ,

in (Equation7

(7)

(7) ) are

respectively. Besides, the estimated dispersion parameter

. These results in () provide obvious evidence that individual information has effects on the reporting developments of claims in sense that most covariates associated with individual information are significant at significance level 0.05.

Similar results for settlement developments and payments are listed in Tables and . These results also provide obvious evidence that individual information has effects on settlement developments and payments of claims. Besides, the estimated dispersion parameter and the estimates under IDM are

Table 2. Estimated parameters for reporting developments, their standard errors and p-values.

Table 3. Estimated parameters for settlements developments, their standard errors and p-values.

Table 4. Estimated parameters for payments, their standard errors and p-values.

In Table , the columns with names ‘IBNR’, ‘RBNS’ and ‘Loss reserving’ correspond to estimates of IBNR reserve, RBNS reserve and total loss reserve, respectively. The square roots of approximated conditional MSEPs under IIM and IDM are in the fourth column of Table . The rightmost column in this table showed the computed by (Equation28

(28)

(28) ). We can see that loss reserving by IIM provides more stable prediction of outstanding liabilities than that by IDM since the former has smaller conditional MSEP and after incorporating useful individual information into loss reserving, the prediction accuracy is greatly increased by

.

6. Conclusion

This paper explored the improvement of accuracy in predicting outstanding liabilities, which are incurred by general insurance companies, by incorporating useful individual information into modelling. The reporting developments and payments of individual claims were given weak assumptions about their first two moments and modelled under quasi-likelihood theory, while settlement delays were modelled by multinomial logistic regression. Based on the model specification, loss reserve and conditional variance of outstanding liabilities were derived, which were further used to compute loss reserving and conditional MSEP. It was theoretically proved that loss reserving incorporating useful individual information shows higher accuracy than that under IDM, where the accuracy is measured by the conditional MSEP, when portfolio size is large enough. The conclusion is also supported by the simulations and real data analysis.

Table 5. Reserving, accuracy of prediction and accuracy improvement of IIM with respect to IDM.

While the proposed model is basically a parametric model in statistical context, some one may be concerned with the limitation that the model is subjective and thus question its robustness in practical applications. Regarding this aspect, a possible next step is to study this problem under a nonparametric framework. Especially, it is more interesting to model the dependence of claims development on individual information by machine learning (including deep learning).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Zhigao Wang

Zhigao Wang is a Ph.D. candidate in Statistics at East China Normal University.

Xianyi Wu

Xianyi Wu is a professor in School of Statistics at East China Normal University.

Chunjuan Qiu

Chunjuan Qiu is an associate professor in School of Statistics at East China Normal University.

References

- Alai, D. H., Merz, M., & Wüthrich, M. V. (2009). Mean square error of prediction in the Bornhuetter–Ferguson claims reserving method. Annals of Actuarial Science, 4(1), 7–31. https://doi.org/https://doi.org/10.1017/S1748499500000580

- Alai, D. H., Merz, M., & Wüthrich, M. V. (2010). Prediction uncertainty in the Bornhuetter–Ferguson claims reserving method: Revisited. Annals of Actuarial Science, 5(1), 7–7. https://doi.org/https://doi.org/10.1017/S1748499510000023

- Antonio, K., & Plat, R. (2014). Micro-level stochastic loss reserving for general insurance. Scandinavian Actuarial Journal, 2014(7), 649–669. https://doi.org/https://doi.org/10.1080/03461238.2012.755938

- Arjas, E. (1989). The claims reserving problem in non-life insurance: Some structural ideas. ASTIN Bulletin: The Journal of the IAA, 19(2), 139–152. https://doi.org/https://doi.org/10.2143/AST.19.2.2014905

- Crevecoeur, J., Antonio, K., & Verbelen, R. (2019). Modeling the number of hidden events subject to observation delay. European Journal of Operational Research, 277(3), 930–944. https://doi.org/https://doi.org/10.1016/j.ejor.2019.02.044

- England, P. D., & Verrall, R. J. (2002). Stochastic claims reserving in general insurance. British Actuarial Journal, 8(3), 443–544. https://doi.org/https://doi.org/10.1017/S1357321700003809

- Huang, J., Qiu, C., & Wu, X. (2015). Stochastic loss reserving in discrete time: Individual vs. aggregate data models. Communications in Statistics-Theory and Methods, 44(10), 2180–2206. https://doi.org/https://doi.org/10.1080/03610926.2014.976473

- Huang, J., Qiu, C., Wu, X., & Zhou, X. (2015). An individual loss reserving model with independent reporting and settlement. Insurance: Mathematics and Economics, 64(1), 232–245. https://doi.org/https://doi.org/10.1016/j.insmatheco.2015.05.010

- Huang, J., Wu, X., & Zhou, X. (2016). Asymptotic behaviors of stochastic reserving: Aggregate versus individual models. European Journal of Operational Research, 249(2), 657–666. https://doi.org/https://doi.org/10.1016/j.ejor.2015.09.039

- Lindholm, M., Lindskog, F., & Wahl, F. (2020). Estimation of conditional mean squared error of prediction for claims reserving. Annals of Actuarial Science, 14(1), 93–128. https://doi.org/https://doi.org/10.1017/S174849951900006X

- Mack, T. (1993). Distribution-free calculation of the standard error of chain ladder reserve estimates. ASTIN Bulletin: The Journal of the IAA, 23(2), 213–225. https://doi.org/https://doi.org/10.2143/AST.23.2.2005092

- Mack, T. (2000). Credible claims reserves: The Benktander method. ASTIN Bulletin: The Journal of the IAA, 30(2), 333–347. https://doi.org/https://doi.org/10.2143/AST.30.2.504639

- McCullagh, P., & Nelder, J. A. (1989). Generalized linear models (2nd ed). Chapman and Hall.

- Norberg, R. (1993). Prediction of outstanding liabilities in non-life insurance 1. ASTIN Bulletin: The Journal of the IAA, 23(1), 95–115. https://doi.org/https://doi.org/10.2143/AST.23.1.2005103

- Norberg, R. (1999). Prediction of outstanding liabilities II. Model variations and extensions. ASTIN Bulletin: The Journal of the IAA, 29(1), 5–25. https://doi.org/https://doi.org/10.2143/AST.29.1.504603

- Pigeon, M., Antonio, K., & Denuit, M. (2013). Individual loss reserving with the multivariate skew normal framework. ASTIN Bulletin: The Journal of the IAA, 43(3), 399–428. https://doi.org/https://doi.org/10.1017/asb.2013.20

- Pigeon, M., Antonio, K., & Denuit, M. (2014). Individual loss reserving using paid-incurred data. Insurance: Mathematics and Economics, 58(2), 121–131. https://doi.org/https://doi.org/10.1016/j.insmatheco.2014.06.012

- Van der Vaart, A. W. (2000). Asymptotic Statistics. Cambridge University Press.

- Verrall, R. J., Nielsen, J. P., & Jessen, A. H. (2010). Prediction of RBNS and IBNR claims using claim amounts and claim counts. Astin Bulletin, 40(2), 871–887. https://doi.org/https://doi.org/10.2143/AST.40.2.2061139

- Wahl, F. (2019). Explicit moments for a class of micro-models in non-life insurance. Insurance: Mathematics and Economics, 89(7), 140–156. https://doi.org/https://doi.org/10.1016/j.insmatheco.2019.10.001

- Wahl, F., Lindholm, M., & Verrall, R. (2019). The collective reserving model. Insurance: Mathematics and Economics, 87(7), 34–50. https://doi.org/https://doi.org/10.1016/j.insmatheco.2019.04.003

- Wüthrich, M. V., & Merz, M. (2008). Stochastic Claims Reserving Methods in Insurance. John Wiley and Sons.

- Yu, X., & He, R. (2016). Individual claims reserving models based on marked Cox processes. Chinese Journal of Applied Probability and Statistics 32(2), 201-219. http://aps.ecnu.edu.cn/EN/Y2016/V32/I2/201

- Zhao, X., & Zhou, X. (2010). Applying copula models to individual claim loss reserving methods. Insurance: Mathematics and Economics, 46(2), 290–299. https://doi.org/https://doi.org/10.1016/j.insmatheco.2009.11.001

Appendix

Proof

Proof of Proposition 3.1

To derive the following gradient and Hessian matrix, we need the identities , which gives that

Then we have the following gradient according to formulas above, which is

By some algebraic computation, it follows that

Because

is just the number of those reported claims incurred in accident year i,

Observe further that

for

and

Therefore,

(A1)

(A1)

Let v = n−i−u and note that

Then, Equation (EquationA1

(A1)

(A1) ) gives rise to the desired result.

Proof

Proof of Theorem 4.1

By (Equation3(3)

(3) ), the loss reserve can be computed as

According to Assumption 3.2, for a representative policy in year i, given

with

,

follows multinomial distribution with parameters

and

. Then by Assumption 3.3, the RBNS loss reserve is

It can be easily proved that IBNR claims are independent of historical observation

by Assumption 3.1–3.3. Hence, IBNR loss reserve is computed by

According to independence assumptions in Assumptions 3.1–3.3, the developments of RBNS claims are independent of developments of IBNR claims, which results in the independence between

and

. Then the variance of R given

is

First, for

, we compute

For

, compute

which is equal to

which can be computed as follows:

Then by independence among policies and Assumptions 3.2 and 3.3, the variance of RBNS loss reserve given

is

Because IBNR claims are independent of historical observation

, variance of IBNR loss reserve given

is computed by

Proof

Proof of Theorem 4.3

Expand about true parameters

by Taylor expansion. Then we have

One knows that

. Write

and

,

and

. To compute the partial derivative in the Taylor expansion above, we need the following partial derivatives:

By the law of large numbers, it can be proved that

, where

, where denoting

(A2)

(A2)

It is well known that under some regular conditions and hence

. Besides,

If individual data model hold true, one can similarly prove that

. Therefore,

in this case. If individual information model holds true, we can easily prove that

is asymptotically biased, which results from the following arguments. The law of large numbers readily gives

and

. Further, we have

and

. We have

where

and then

Apparently,

and by the law of large numbers and some simple algebra operations, we show that

Therefore, if asymptotic bias Δ is not zero,

. Then we complete the proof.