ABSTRACT

The crucial determinant factor for ASEAN to support the Indo-Pacific strategy is whether ASEAN can retain and exercise the centrality. This paper addresses the issue on the centrality as to whether ASEAN can retain its centrality in the Indo-Pacific region. The issue is whether ASEAN can continue to assume an important position in Indo-Pacific economic transactions, more specifically in global value chains (GVCs) in the Indo-Pacific region. As GVC is expected to reflect the economic integration and interconnectivity of the region, higher participation of ASEAN in the Indo-Pacific GVC as compared with its own GVC, or at least a similar level of participation, is considered as retention of centrality. However, the reality is not such the case, and ASEAN is losing its centrality in the Indo-Pacific region in terms of GVC participation. This is partly due to the fact that Indo-Pacific is less integrated than ASEAN. Under this situation, the paper provides some policy implications for ASEAN to retain the centrality in Indo-Pacific. One of such policies is to increase and promote foreign direct investment (FDI) as it is the key to create GVCs. FDI flows as percentage of GDP in Indo-Pacific is much smaller in Indo-Pacific than in ASEAN.

1. Introduction

The concept of the Indo-Pacific strategy is wide and distinct each other among major advocating countries such as Australia, Japan, India and the United States in terms of a geostrategic context, but their basic concept overlaps. All of them pursue a free and open Indo-Pacific, emphasizing the rule of law and securing prosperity, peace and stability. Other countries that do not necessarily belong to this region (e.g., France, Germany) also share these principles and values.

Indo-Pacific is not the form, nor the structure of a new entity, at least for now. These countries have issued their own concepts in their specific areas (e.g., United States Department of Defense’s Indo-Pacific Strategy Report: Preparedness, Partnerships, and Promoting a Networked Region (June 1 2019); and US Department of State, A Free and Open Indo-Pacific Advancing a Shared Vision (November 2019)) and expressed their support to the ideas (Box 1).

Box 1. Quotes by high-level officials on Indo-Pacific

While recent announcements and initiatives on promoting Indo-Pacific are impressive, including the ASEAN Outlook on Indo-Pacific (AOIP) in June 2019Footnote2 and the 23rd ASEAN-Japan Summit on AOIP of 12 November 2020Footnote3, the concept of Indo-Pacific is still at work. Some visualize the Indo-Pacific initiative as opposed to China’s belt and road initiative (BRI). However, for those countries that belong to not only China’s initiative but also the Indo-Pacific region, these two initiatives stand complementarily each other and are not subject to the choice of one or another. In this respect, the position of ASEAN vis-à-vis Indo-Pacific is important and a determinant factor for other small and peripheral countries in the Indo-Pacific region whether to support and be part of the construct.

The crucial determinant factor for ASEAN to support the Indo-Pacific Strategy is whether ASEAN can retain and exercise the centrality. Centrality for ASEAN is one of the purposes of ASEAN as stipulated in the ASEAN Charter: “(T)o maintain the centrality and proactive role of ASEAN as the primary driving force in its relations and cooperation with its external partners in a regional architecture that is open, transparent and inclusive”Footnote4 (Article 1. 15). Underlining this purpose and adhering to the principle of the centrality in external political, economic, social and cultural relations, ASEAN reconfirms its position vis-à-vis Indo-Pacific in the AOIP.

This Outlook consists of the following elementsFootnote5

A perspective of viewing the Asia-Pacific and Indian Ocean regions, not as contiguous territorial spaces but as a closely integrated and interconnected region, with ASEAN playing a central and strategic role;

An Indo-Pacific region of dialogue and cooperation instead of rivalry;

An Indo-Pacific region of development and prosperity for all; and

The importance of the maritime domain and perspective in the evolving regional architecture.

What is expected is that Indo-Pacific is a closely integrated and interconnected region with ASEAN. Otherwise ASEAN centrality is not guaranteed nor achievable. The Japanese Government recognizes this, saying that, as the hinge of two oceans, “Japan will further promote infrastructure development, trade and investment, and enhance business environment and human development, strengthening connectivity in ASEAN region.”Footnote6

This paper addresses the issue on the centrality whether ASEAN can retain its centrality in the Indo-Pacific region. The issue is whether ASEAN can continue to assume an important position in Indo-Pacific economic transactions. In this paper, as the region which has been integrated through production networks, retaining the position of production hub for their value chains is considered crucial. Therefore, ASEAN’s centrality as measured by their participation in global value chains (GVCs) is examined in the context of the Indo-Pacific region. ASEAN’s centrality is reflected by the integration and interconnectivity of the region.

The term centrality has been vaguely used. There have not been attempts to measure it in numerical terms as it is more rooted in the concept. If gains or losses in centrality would be measured with concrete indicators, ASEAN would find it when and at what conditions the region would lose or gain centrality and take actions to stem further the losses or strengthen the gains. This paper proposes to measure it by increases or decreases in their participation in GVCs.

After this introduction, this paper defines the constituents of Indo-Pacific and provides a methodology and a set of terminology used in GVCs (Section 2) so that readers have a common understanding on what this paper attempts. The following section deals with the questions to be addressed to clarify what this paper answers (Section 3), followed by the analytical framework and its analysis (Section 4). With the finding of losing centrality, the question for ASEAN as well as its partners is how to increase and preserve the ASEAN centrality. Some policy recommendations are made (Section 5). The paper ends with some concluding remarks (Section 6).

2. Definition and the methodology

In order to make analysis on Indo-Pacific, if any statistical calculation is required, there is the need of clear definition on this particular region. Unfortunately, there was no clear geographical definition. While it is a common thinking not to include China as this concept is often positioned against China’s BRI, it is not certain whether the United States and other North American countries as well as South America are included in terms of geographical construct. However, United States’ definition on Indo-Pacific is to include its own country as “the United States is a Pacific nation” because of inclusion Pacific states and Pacific territoriesFootnote7

In the geographic definition this paper includes the United States. This is partly because a part of the country is geographically located in that region. China is not included. Thus, the countries covered under this region are 40 as shown in .

Table 1. List of countries of Indo-Pacific included in this paper: 40 countries

The methodology used here to assess the centrality of ASEAN is to measure the extent to which ASEAN can play a central role in shaping the economic transactions in Africa, Asia and the Pacific. ASEAN’s centrality is revealed if ASEAN’s products are proven to be essential for production by companies operating in Africa, Asia and the Pacific. The more essential their products are, the more integrated ASEAN is and thus the larger centrality. The extent of the use of ASEAN products in other countries can be estimated in the context of ASEAN’s involvement in global value chains (GVCs).

There are several approaches to analyzing GVCs. Using and analyzing company case studies that represent best to illustrate their production systems in the industries such as automobiles, electronics, textiles and clothing is one of such approaches. A recent and modern approach is to analyze GVCs by using value-added trade dataFootnote8 One of advantages of this approach provides a macroeconomic view of integration of each individual state into the value chains which are linked through trade and empowered by foreign direct investment (FDI) as well as non-equity mode of investmentFootnote9

In the GVC analysis using value-added trade, there is some common terminology. It includes foreign value added (FVA), domestic value-added (DVA) and value-added incorporated in other countries’ exports (DVX). The chain has both backward (upstream) part and forward (downstream) part. The sum of this shows the extent to which the country is involved in global value chains (GVC participation). The terminology used in this paper is as follows:

Foreign value added (FVA) indicates what part of a country’s gross exports consists of inputs that have been produced in other countries.

Domestic value added (DVA) is the part of exports created in country, i.e., the part of exports that contributes to GDP.

The sum of foreign and domestic value-added equates to gross exports.

Value-added incorporated in other countries’ exports (DVX) indicates the extent to which a country’s exports are used as inputs to exports from other countries. At the global level, the sum of this value and the sum of foreign value added is the same.

GVC participation indicates a country’s exports that is part of a multistage trade process, involved in both upstream and downstream parts of GVCs. It is the sum of FVA and DVX.

3. Questions to be addressed

ASEAN has been successfully positioning itself in the ASEAN + 1 (ASEAN and one dialogue partner country) and ASEAN + 3 (ASEAN and three dialogue partner countries – China, Japan and Republic of Korea –) framework. The question to be addressed is whether ASEAN can maintain its centrality in the wider region, namely the Indo-Pacific region. In order for ASEAN to support the Indo-Pacific concept, this criteria is important. If the centrality even increases in this region, there is no problem of promoting the concept. However, if not, and if it decreases, what will ASEAN have to do to improve its positioning vis-à-vis centrality? At this moment, there is no option to opt out the concept as the AOIP is based on the principles of strengthening ASEAN centralityFootnote10

In addressing the question on ASEAN centrality, it is important to know which countries become more important players in affecting and even shaping value chain structures in Indo-Pacific as compared with the ASEAN region. If GVCs in Indo-Pacific show the same trend as in ASEAN, China would be gaining importance in input providers to the Indo-Pacific exports, and Japan losing importanceFootnote11 If ASEAN becomes weaker as producers and input providers in the Indo-Pacific region, what ASEAN and Indo-Pacific should do to increase ASEAN production networks and enhance ASEAN benefits from such chains.

Similarly, given the fact that Japan is one of the most important partner countries for ASEAN, it is also interesting to know how these two regions fare in the Indo-Pacific region.

The questions to be addressed here include:

Can ASEAN retain importance in the Indo-Pacific region as input providers for the exports from the region?

Like in ASEAN exports, is China gaining importance in input providers to the Indo-Pacific exports, and Japan losing importance?

In the buyer market of region’s products, what is the extent to which their exports are utilized as inputs to other countries’ exports? Are the exports from Indo-Pacific purchased by foreign countries as inputs more than those from ASEAN, or vice versa?

If ASEAN becomes weaker as producers and input providers in the Indo-Pacific region, what ASEAN and Indo-Pacific should do to increase ASEAN production networks and enhance ASEAN benefits from such chains?

4. Analysis

4.1. ASEAN GVCs

The ASEAN-Japan Centre (AJC) has undertaken a project on GVCs in ASEAN based on the value-added trade dataFootnote12 ASEAN has already been involved in GVCs for a long time and its participation level is higher than any other regions except EU. Both the share of foreign inputs in exports (FVA) and the GVC participation share (FVA + DVX) is higher for ASEAN than for the world average.

Not only foreign companies but also ASEAN companies provide inputs to the production undertaken in ASEAN. Because of GVCs, ASEAN companies are engaged in intra-regional trade, providing inputs to their regional or global value chains. In exporting 1.6 USD trillion from ASEAN in 2019, DVA or value created by ASEAN companies in their own countries accounts for 62% of it, or nearly 1 USD trillion. Inputs to ASEAN exports from other ASEAN countries was worth 8% of the total ASEAN exports. Therefore, altogether ASEAN’s contribution to ASEAN exports emanating from directly within its own countries and indirectly by receiving inputs from other ASEAN countries would reach 70% of the total or 1,119 USD billion (DVA + inputs from other ASEAN countries integrated into ASEAN exports). This figure indicates that ASEAN as a whole creates and owns this amount of value added in its export business. The higher this level is, the higher the centrality is.

There are some stylized facts about ASEAN GVCs based on the study by AJCFootnote13

In the upstream part of GVCs (in the supplier market) of ASEAN, ASEAN is more involved in GVCs than any other regional groups except EU (FVA: 38% for ASEAN and 31% for the world in 2019).

In the downstream part of GVC (in the buyer market) of ASEAN, the volume (DVX) is 26% of gross exports, smaller than that in the supplier market. This implies that ASEAN’s products are less extensively used for other countries’ exports as compared with the volume of foreign inputs integrated into ASEAN’s exports.

Length of GVCs or GVC participation (FVA+DVX): 64% for ASEAN and 62% for the world).

ASEAN is increasingly important providers for production networks established in ASEAN (share of ASEAN inputs imported and used in total exports from ASEAN rose from 3% in 1990, 5% in 1995, 6% in 2000 and 8% in 2019). China has been also rising, but Japan has been losing importance in ASEAN exports in terms of their shares in ASEAN exports.

There is a positive relationship between GVC participation and FDI presence.

Regional integration and GVCs reinforce each other.

The more the countries are involved in GVCs, the higher the economic growth (GDP per capita) is attained for both ASEAN and the world.

4.2. GVCs in Indo-pacific

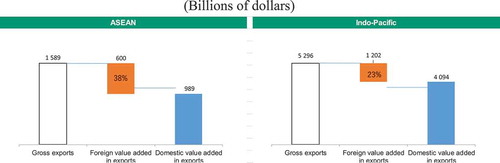

If the same analysis is extended to the Indo-Pacific region, the volume of gross exports increases from 1.6 USD trillion to 5.3 USD trillion, and the foreign content in the exports (or FVA) increases from 600 USD billion to 1,202 USD billion (). However, the FVA share decreases from 38% to 23%. As FVA is an input from abroad to the exports from the region in question, the extent of upstream part (supplier market) of GVCs in Indo-Pacific is lower than in ASEAN. Lowering of the FVA share for Indo-Pacific means that Japan and the United States, two major exporters from this region do not use much ASEAN inputs for their exports. While ASEAN uses inputs from these two countries in their exports, exports from these two countries do not use much ASEAN products. Thus, the share becomes lower. The lowering share is, however, not limited to ASEAN. Reflecting the fact that FVA is lower in Indo-Pacific, contribution as intermediate producers to Indo-Pacific exports from other major countries are also smaller.

Figure 1. Structure of value-added exports, 2019: comparison between ASEAN and Indo-Pacific

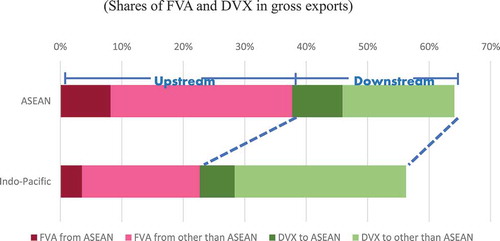

As GVC participation is defined as the sum of upstream and downstream parts of chains (total length of value chains), adding the downstream part (DVX) to the upstream part (FVA) brings the overall level of GVC participation. According to this, Indo-Pacific is again lower than that in ASEAN, but the difference narrows. This is because the length of downstream part (buyer market) of GVCs for Indo-Pacific is longer than that for ASEAN (34% vs 26%) (). It implies that exported products from Japan or the United States, major exporters from Indo-Pacific, tend to be utilized more as inputs to the exports from other countries than in ASEAN exports. Exported products from Japan and the United States as intermediary products, are being integrated into other countries’ exports. The GVC participation ratio (to exports) is 64% for ASEAN and 56% for Indo-Pacific ().

Figure 2. GVC participation ratio, 2019: comparison between ASEAN and Indo-Pacific

The question is the extent to which ASEAN is involved in FVA, DVA and DVX of Indo-Pacific. In the ASEAN region, ASEAN companies account for 8% each of FVA and DVX of total value created in the ASEAN exports (). In other words, 16% of ASEAN value chains are for ASEAN’s involvement as input provider or input receivers. In the Indo-Pacific region, ASEAN’s involvement in its value chains as input providers (4%) and input receivers (6%) is 10% (). Compared GVCs in ASEAN with GVCs in Indo-Pacific, first the length of GVCs (GVC participation) is shorter for the latter; second, ASEAN’s role in the GVCs created within these two regions is smaller also for the latter region. It is apparent that in Indo-Pacific, ASEAN loses centrality to a certain extent or cannot retain the same level of strength in involving GVCs, the cornerstone of bonding countries and industries through production.

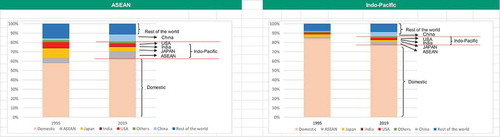

As ASEAN is losing its importance in creating value-added trade by moving from ASEAN to Indo-Pacific, other major countries are also losing ( and ). Japan as well as ASEAN lost more than half. India, which remained as a marginal contributor to value-added trade in both ASEAN and Indo-Pacific (less than 1%), this contribution is smaller in Indo-Pacific than in ASEAN. China’s loss is less than other major countries. Multinational enterprises (MNEs) including those from Japan and the United States have not extended GVCs into Africa and the Pacific. Therefore, their contribution to Indo-Pacific exports has been less than to ASEAN.

Figure 3. Value-added exports, by domestic, and ASEAN, Japan, India, United States, China and other foreign country value-added creators, 1995 and 2019

Table 2. Value-added contribution to exports from ASEAN and Indo-Pacific by contributors, 2019 (Per cent of gross exports)

Major contributors to the upstream part of production chains (supplier market) in ASEAN and Indo-Pacific have the following characteristics:

ASEAN is the largest foreign value-added contributor to exports from both the ASEAN (8% of ASEAN exports in 2018) and Indo-Pacific (4%) regions, but it is more important in ASEAN ().

Japanese importance as suppliers over two decades halved in both ASEAN (10% in 1995 to 5% of ASEAN exports in 2019) and Indo-Pacific (4% in 1995 to 2% of Indo-Pacific exports in 2019) ( and ). Like ASEAN, Japan is more important in ASEAN exports than Indo-Pacific exports.

United States’ importance as input providers to GVCs in Indo-Pacific is smaller than in ASEAN like other major countries, but larger than Japan’s importance for Indo-Pacific ().

China’s importance as input contributors to exports rose both for ASEAN (2% in 1995 to 8% in 2019) and Indo-Pacific (1% to 5%) ( and ).

India has remained making a small value-added contribution to exports from both ASEAN and Indo-Pacific (less than 1%).

The downstream part (buyer market) of GVCs for Indo-Pacific shows a somewhat different picture. shows a longer downstream chain for Indo-Pacific. Countries of Indo-Pacific are more engaged in the downstream part of GVCs than in the upstream part of GVCs (34% vs 23%). ASEAN and China in the region are major recipients of both ASEAN and Indo-Pacific exports for their GVCs (), while EU is larger buyers of Indo-Pacific exports than ASEAN exports. As compared with ASEAN’s DVX, Indo-Pacific’s DVX is longer driven by non-Indo Pacific countries, or “the rest of the world” (). Therefore, the downstream chains of GVCs have some different features from the upstream chains:

ASEAN as well as Japan become smaller buyers for Indo-Pacific as compared with for ASEAN.

It suggests that other countries such as China, United States and India became larger buyers, though these changes are small.

Concentration of buyer market is less than that of supplier market. In other words, there is no dominant market occupants.

China has smaller volume of buying (3% of gross exports from Indo-Pacific; ) than volume of supplying (5%; ).

Table 3. Value-added exports integrated into other countries’ exports from ASEAN and Indo-Pacific by destination, 2019 (Per cent of gross exports)

5. Policy implications

Requiring less ASEAN’s (as well as Japan’s) products as inputs to GVCs in Indo-Pacific than in ASEAN implies that ASEAN’s (as well as Japan’s) influence in production networks is smaller in Indo-Pacific. Generally speaking, Indo-Pacific is less external market-oriented than ASEAN. This region includes big economies like Japan and the United States and, compared with ASEAN, is less dependent on trade (exports and imports). Therefore, GVC participation, particularly in its upstream part (supplier market), is lower for all economies of the region (). Nevertheless, ASEAN’s presence in GVCs is even smaller than China’s, which is the opposite to the case of GVCs in ASEAN. In the downstream part (buyer market), in terms of gross exports, ASEAN buys less Indo-Pacific products in their exports than ASEAN buys products from ASEAN exports.

Under the situation where Indo-Pacific is less integrated than ASEAN, then, the question still remains the same: how to retain ASEAN centrality and increase the Japanese contribution to GVCs in Indo-Pacific? For a larger number of countries to benefit from Indo-Pacific GVCs, there are a number of policy recommendations in order. These recommendations which are mainly targeting Indo-Pacific countries, should also help ASEAN retain its centrality. They include the following.

Indo-Pacific should create conducive environment for furthering trade and investment for ASEAN companies as well as other companies in and out of the region. Indo-Pacific governments should maintain a conducive trade and investment environment and put in place infrastructural prerequisites to enable GVC growth.

As there is lack of production capacities in Indo-Pacific, building production capacities are required for Indo-Pacific companies to become partners with both other Indo-Pacific companies and extra Indo-Pacific such as EU, and other major country firms to join GVCs.

Indo-Pacific should consider to expand its production networks by revitalizing various schemes and existing free trade agreements (FTAs) as well as creating region-wide schemes to promote and facilitate trade and investment. As production networks established in ASEAN go beyond ASEAN to form a wider value chain, a systematic mechanism to facilitate trade and investment is required (e.g., creating ASEAN’s old BBC (Brand to Brand Complementation) scheme in Indo-Pacific, utilizing the existing FTAs such as ASEAN-India FTA, Japan-India FTA).

As Indo-Pacific does not have a regional structure, there is the need of institutionalizing regional integration schemes and measures through private sector initiatives. ASEAN plays a less important role in Indo-Pacific than in own region in terms of contributing to value chains created in respective regions. Because of absence of institutionalizing regional integration in the region, the private sector becomes more important in pushing toward integration through production networks. Indo-Pacific governments should at least embed GVCs in overall development strategies and industrial development policies to raise awareness toward GVCs. The private sector can play a central role in Indo-Pacific as was the case of ASEAN integration at the beginning of its process.

ASEAN should utilize better the initiatives and programmes announced or implemented by the partner countries. For example, the Japanese government (Ministry of Economy, Trade and Industry) introduced a programme to diversify and multiplicate supply chains in ASEAN to deal with various risks such as the COVID-19 that disrupted the supply chains. Similarly, in its Indo-Pacific guidelines, the government of Germany is encouraging the German companies to diversify their operations into ASEANFootnote14 ASEAN should not miss out such opportunities.

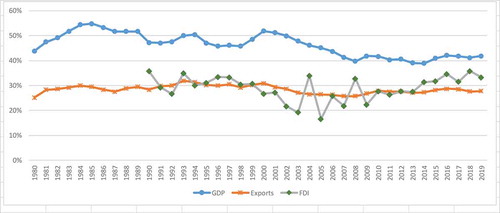

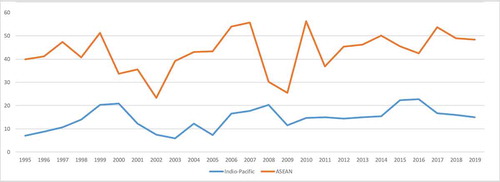

GVCs is the nexus of trade and investment. FDI had been generally smaller than trade in Indo-Pacific for the first decade of the 2000s. Since 2013 the share of Indo-Pacific in global FDI inflows has surpassed that in exports (). Countries in Indo-Pacific should continue to promote FDI. The share of Indo-Pacific in world FDI inflows is lower than that of world GDP. There is more room to increase FDI.

Figure 4. Shares of Indo-Pacific FDI, exports and GDP in the world totals, 1980–2019

Note: For exports, data are for goods and services and on BPM5 basis until 2004.

Potential for further FDI is also proven by the low volume of FDI. As compared with ASEAN, Indo-Pacific shows smaller presence of FDI. In terms of GDP, Indo-Pacific attracts only 10 USD-$20 per 1,000 USD GDP, one-fourth of what ASEAN gets (). In promoting FDI, countries should pay more attention to FDI that creates value chains. There is a positive relationship between GVC participation and FDI presence, and regional integration and GVCs reinforce each other. There is the finding that the more the countries are involved in GVCs, the higher the economic growth (GDP per capita) is attained for both ASEAN and the worldFootnote15 ASEAN and Japan together through FDI tend to create production chains in automobiles, electronics and services such as transport services.

Figure 5. FDI flows to ASEAN and Indo-Pacific as per 1000 USD GDP, 1995–2019

Africa is an important part of Indo-Pacific. While only a part of African countries are covered under the Indo-Pacific region, these African countries need to be integrated more with other countries in Indo-Pacific, particularly with important investors from the region such as Singapore, India and MalaysiaFootnote16 (China – non Indo-Pacific country – is the largest investor from Asia.) These countries are already traditional investors in Africa. FDI provides not only a means to develop, but also an important facet of economic cooperation between the two regions.

As ASEAN is the most dynamically growing in the world, Indo-Pacific should benefit from the ASEAN dynamism. One of the ways to benefit from such dynamism is to attract ASEAN FDI. Appropriate policy measures should be put in place to attract ASEAN FDI and to benefit from the dynamism of ASEAN corporate sector.

6. Conclusion

The role of ASEAN in Indo-Pacific GVC is lower than that in ASEAN GVC. Therefore, the ASEAN connectivity also becomes smaller. However, while this is partly because Indo-Pacific is less integrated than ASEAN, there are some ways for both Indo-Pacific and ASEAN to rectify the situation as mentioned above, and then ASEAN can play a central role in the region or exercise the centrality. With increasing strength of ASEAN economies and companies, opportunities are emerging for a bigger role for ASEAN to play in the Indo-Pacific region and the regional GVC.

ASEAN’s higher GVC participation in its own region is explained by its unique characteristics of ASEAN as exporters (or suppliers) of parts and components as well as raw materials. This unique characteristics does not work in Indo-Pacific as much as in ASEAN because of absence of international production networks. As ASEAN is the production hub of various manufacturing products whose elasticity of demand is relatively high (“downstreamness” as per Antràs and Chor (2013)Footnote17), the centrality question for ASEAN is whether non-ASEAN countries of Indo-Pacific demonstrate potential supplier relationships and their products are more demanded (higher demand elasticity). It is a paramount priority of ASEAN to have their products more demand-elastic in Indo-Pacific if it moves toward further integration of the regional economy beyond ASEAN.

Acknowledgements

The author wishes to thank two anonymous reviewers for their helpful comments. Errors and omissions are only those of the author and should not be attributed to his organization.

Additional information

Notes on contributors

Masataka Fujita

Masataka Fujitais currently the Secretary General of the ASEAN-Japan Centre, an international organization based in Tokyo. Former Head of Investment Trends and Issues Branch, United Nations Conference on Trade and Development.

Notes

1 United States Department of Defense, “Indo-Pacific Strategy Report,” 5.

2 ASEAN Secretariat, “ASEAN Outlook.”

3 “Joint Statement of the 23rd ASEAN-Japan Summit on Cooperation on ASEAN Outlook on the Indo-Pacific,” https://www.mofa.go.jp/files/100114942.pdf. Accessed January 25, 2021.

4 The ASEAN Charter, 2007, https://asean.org/asean/asean-charter/charter-of-the-association-of-southeast-asian-nations/. Accessed January 25, 2021.

5 ASEAN Secretariat, “ASEAN Outlook,” 2.:

6 Mission of Japan to ASEAN, “Free and Open Indo-Pacific Strategy,” undated, https://www.asean.emb-japan.go.jp/files/000352880.pdf. Accessed January 25, 2021.

7 United States Department of Defense, “Indo-Pacific Strategy Report.”.

8 OECD calls it “trade in value added (TiVA)”..

9 See the paper series of non-equity mode of operations in ASEAN by AJC https://www.asean.or.jp/ja/trade-info/nem_papers/..

10 ASEAN Secretariat, “ASEAN Outlook,” 2–3..

11 ASEAN-Japan Centre, “Global Value Chains.”.

12 As of December 2020 AJC has published the following papers on GVCs in ASEAN: Paper 1. A Regional Perspective; Paper 2: Brunei Darussalam; Paper 3: Cambodia; Paper 8. Philippines; Paper 9. Singapore; Paper 10: Thailand; Paper 11: Viet Nam; Paper 12: Automobiles; Paper 14: Textiles and Clothing; Paper 15: Agribusiness; and Paper 16. Tourism. Available on https://www.asean.or.jp/en/centre-wide/centrewide_en/.

13 ASEAN-Japan Centre, “Global Value Chains.” Some data are updated..

14 The German Federal Government, “Policy guidelines for the Indo-Pacific.”.

15 ASEAN-Japan Centre, “Global Value Chains.”.

16 UNCTAD and UNDP, Asian Foreign Direct Investment..

17 Antràs and Chor,“Organizing the Global Value Chain.”

Bibliography

- Antràs, P., and D. Chor. “Organizing the Global Value Chain.” Econometrica 81, no. 6 (2013): 2127–2204.

- ASEAN Secretariat. “ASEAN Outlook on the Indo-Pacific.” 2019. Accessed January 25, 2021. https://asean.org/storage/2019/06/ASEAN-Outlook-on-the-Indo-Pacific_FINAL_22062019.pdf

- ASEAN-Japan Centre (AJC). 2019. “Global Value Chains in ASEAN: A Regional Perspective.” Paper 1 (Revised), January. Accessed January 25, 2021. https://www.asean.or.jp/en/wp-content/uploads/sites/3/GVC_A-Regional-Perspective_Paper-1-Revised_2019_full_web.pdf

- The German Federal Government. “Policy Guidelines for the Indo-Pacific Region: Germany – Europe – Asia: Shaping the 21st Century Together.” September, 2020. Accessed January 25, 2021. https://www.auswaertiges-amt.de/en/aussenpolitik/regionaleschwerpunkte/asien/german-government-policy-guidelines-indo-pacific/2380510

- United Nations Conference on Trade and Development (UNCTAD) and United Nations Development Programme (UNDP). Asian Foreign Direct Investment in Africa: Towards a New Era of Cooperation among Developing Countries. Geneva and New York: United Nations publication, 2007.

- United States Department of Defense. “Indo-Pacific Strategy Report: Preparedness, Partnerships, and Promoting a Networked Region.” June 1, 2019. Accessed January 25, 2021. https://media.defense.gov/2019/Jul/01/2002152311/-1/-1/1/DEPARTMENT-OF-DEFENSE-INDO-PACIFIC-STRATEGY-REPORT-2019.PDF

- United States Department of State. “A Free and Open Indo-Pacific Advancing A Shared Vision.” November 3, 2019. Accessed January 25, 2021. https://www.state.gov/a-free-and-open-indo-pacific-advancing-a-shared-vision/